European Employment and Social Policy

|

|

|

- Dorcas McCormick

- 5 years ago

- Views:

Transcription

This document does not represent the point of")

1 Special Eurobarometer European Commission European Employment and Social Policy Report Fieldwork : May 2009 June 2009 Publication: September 2009 Special Eurobarometer 316 / Wave 71.2 TNS Opinion & Social This survey was requested and coordinated by the Directorate-General for Communication ( Research and Political Analysis Unit) This document does not represent the point of view of the European Commission. The interpretations and opinions contained in it are solely those of the authors.

2 INTRODUCTION EUROPEANS CURRENT EMPLOYMENT SITUATION Sample structure Length of current/last job Frequency of changing employers PERCEIVED IMPACT OF THE ECONOMIC CRISIS ON THE JOB MARKET Job losses as a result of the economic crisis Concern about potential economic crisis impact on job market Perceived economic crisis cycle CONFIDENCE IN RETAINING EMPLOYMENT Confidence in retaining jobs Confidence in having a job in two years time CONSEQUENCES OF JOB LOSS Confidence in finding new employment Expectations about the level of unemployment insurance JOB SEEKING Job seeking strategies The importance of qualifications and professional experience TRAINING Participation in training in the past 12 months Assessment of training required to retain current employment

3 6.3 Assessment of training required to find employment Perceived obstacles to training Financing training ATTITUDES TOWARD EMPLOYMENT Europeans and Flexicurity The effectiveness of employment measures PERCEPTIONS OF EU EMPLOYMENT AND SOCIAL POLICIES Perception of the EU s role in employment and social affairs The European Social Fund Familiarity with the European Globalisation Adjustment Fund CONCLUSION ANNEXES Tecnical note Tables Questionnaire 2

4 INTRODUCTION Currently, the European Union s economy is in the midst of the deepest and most widespread recession of the post-war era. In terms of GDP growth, the European Commission forecasts a sharp contraction of the EU economy, by 4% in 2009 (compared with positive growth of 0.8% in 2008). Almost all EU countries are severely hit by the worsening of the financial crisis, the sharp global downturn and ongoing housing market corrections in some economies. 1 However, the EU's strong and coordinated policy response is providing tangible help to support and stimulate economic activity. 2 There have been some signs of improvement and it is forecast that the economy is set to stabilise in 2010 as the ambitious measures taken by governments and central banks are expected to halt the contraction in economic activity and facilitate recovery. 3 The EU has strengthened its efforts to promote employment and social inclusion, as part of its strategy to deal with the economic and financial crisis, through comprehensive initiatives such as: A 200 billion recovery package. Proposing changes to the European Social Fund (ESF) and the European Globalisation Adjustment Fund (EGF) to ensure greater access and support to the labour market. The EURES jobs portal, which provides support for jobseekers who want to take up the right to work in another European country. The new skills for new jobs initiative, improving the analysis and prediction of the economy s future skills requirements, thereby matching people to jobs more efficiently and provide an insight into training needs. The European Employment Strategy, which is one of the pillars of the EU s Strategy for Growth and Jobs, continues to provide a framework for Member States to take coordinated action to promote employment in the context of the crisis. The Commission has stepped up its monitoring of the employment and social situation, including the publication of a new series of monthly monitoring reports on the rapidly changing situation. The European Commission has adopted a "shared commitment for employment", which puts forward key priorities and actions to preserve jobs and help those facing difficulties while paving the way for recovery. The EU played a leading role in the G20 Summit in London on 2 April 2009, which agreed international action to stimulate the economy and improve regulation of the financial sector. Commissioner for Employment, Social Affairs and Equal Opportunities, Vladimír Špidla, discussed the social dimension of the crisis with his counterparts from the G8 countries at the G8 Labour Ministers meeting on 30 March Employment Summit: May 7, boosting efforts to promote employment and social inclusion in the light of the financial crisis

5 To measure the impact of the economic crisis on Europeans jobs and employment prospects, the European Commission's Directorate-General for Employment, Social Affairs and Equal Opportunities commissioned this Eurobarometer study, which was carried out by TNS Opinion & Social using a representative sample of 26,756 people aged 15 or older in the 27 European Union Member States as well as the three candidate countries (Croatia, the former Yugoslav Republic of Macedonia and Turkey). This report starts off by looking at Europeans current employment situation in terms of the proportion of people who are employed and the extent to which people remain with one employer or change employers over their career. The report then considers the extent to which there have been job losses now and over time, either for people personally, their immediate family or colleagues. It then determines that the level of concern regarding future job losses is at its highest in this current wave, most probably due to Europeans feeling that the worst of the economic crisis is yet to come. The report then turns to European citizens own vision for the future their personal confidence that they will keep or find a job and, if unemployed, the expectations about the level of social protection that will be provided. Within this context, we look at job seeking, specifically in terms of the type of assets that are important in finding a job, and the extent to which Europeans are geographically mobile with regard to employment. Training can be a large asset in retaining and finding employment and respondents participation in training is assessed. Here it is found that employers play a large part in financing training, thereby removing the largest obstacle to training (namely finance). Lastly, this report looks at the level of public approval for measures promoting the concept of 'flexicurity' a policy approach which combines more flexible labour markets with high levels of employment security and social protection. It then considers the extent of awareness of EU instruments such as the European Social Fund (ESF), whether the current 10% budget allocation is perceived to be sufficient, and the overall impact of the EU on employment and social affairs. This report presents the principal results obtained. 5 These are analysed in terms of the European average for the 27 Member States (EU27) and then reviewed on a country-by-country basis. For relevant questions, results are also compared to those observed in the previous Eurobarometer surveys on European employment and social policy 6 carried out in and Geographical mobility of citizens 8 carried out in The averages for the previous reports represent the results obtained for all the Member States of the European Union as it was composed at that time. The reader should be aware that there are two types of reports for this Eurobarometer study. This, the Full Report covers an in-depth analysis and focuses on the historical trend questions asked in a Standard Eurobarometer wave, as well as some new questions that focus specifically on the current economic crisis. It reports in detail at the overall EU level as well as at national level and provides insights into socio-demographic analysis of the results. 5 Please also note that the total percentages shown in the tables of this report may exceed 100% where the respondent is allowed to give several answers to a particular question. 6 Special Eurobarometer 261/EB65.3/2006 European employment and social policy 7 It should be noted that Special Eurobarometer 261 was carried out in the 25 Member States which then constituted the EU and, therefore, all references to this survey at EU level refer to this group of countries. 8 Special Eurobarometer 305/EB70.1/2009/ Geographical mobility of citizens 4

6 The Summary Report provides a concise snapshot of the main findings in this Eurobarometer wave, focusing specifically on the impact of the economic crisis on jobs as seen by European citizens at the overall as well as the national level. The current survey, as in 2006 and in 2008, was conducted by the TNS Opinion & Social network. The fieldwork was carried out between 29 May and 15 June The methodology used is that of Eurobarometer surveys as carried out by the Directorate General for Communication ( Research and Political Analysis Unit). A technical note on the manner in which interviews were conducted by the Institutes within the TNS Opinion & Social network is appended as an annex to this report. This note indicates the interview methods and the confidence intervals. 5

7 In this report, the countries are represented by their official abbreviations. The abbreviations used in this report correspond to: ABBREVIATIONS EU27 /NA BE BG CZ D-E DE D-W EE EL ES FR IE IT CY CY (tcc) LT LV LU HU MT NL AT PL PT RO SI SK FI SE UK HR TR MK European Union 27 Member States Don t know / No answer Belgium Bulgaria Czech Republic Denmark East Germany Germany West Germany Estonia Greece Spain France Ireland Italy Republic of Cyprus* Area not controlled by the government of the Republic of Cyprus Lithuania Latvia Luxembourg Hungary Malta The Netherlands Austria Poland Portugal Romania Slovenia Slovakia Finland Sweden The United Kingdom Croatia Turkey The Former Yugoslav Republic of Macedonia (FYROM)** * Cyprus as a whole is one of the 27 European Union Member States. However, the acquis communautaire is suspended in the part of the country that is not controlled by the government of the Republic of Cyprus. For practical reasons, only the interviews conducted in the part of the country controlled by the government of the Republic of Cyprus are recorded in the category CY and included in the EU27 average. The interviews conducted in the part of the country not controlled by the government of the Republic of Cyprus are recorded in the category CY (tcc) [tcc: Turkish Cypriot Community]. ** Provisional code which does not prejudge in any way the definitive nomenclature for this country, which will be agreed following the conclusion of negotiations currently taking place at the United Nations. 6

8 1. EUROPEANS CURRENT EMPLOYMENT SITUATION The first section of the report provides context by looking at Europeans current levels of employment, and explores which countries have relatively higher levels of unemployment. Within this context, we look at how long employees stay with one employer, and the frequency of changing employers. 1.1 Sample structure - Overall, half of Europeans are employed, with a stable result since Half of Europeans are currently not working (or inactive) (50%), whilst 42% are employed and just under a tenth (8%) are self-employed 9. Looking further into the non-working segment, a quarter of Europeans are retired or unable to work due to illness, 9% are students, 8% are house persons (responsible for ordinary shopping and looking after the home) and 8% are unemployed or temporarily not working. 10 By comparison with the data of 2008, the data shows some slight changes with 44% being employed and 7% being self-employed, while the proportion of non-working Europeans has remained almost unchanged at 49%. 9 D15a.2 What is your current occupation? (Aggregated) 10 D15a.1 What is your current occupation? (Specified) 7

9 D15a. What is your current occupation? - % EU Retired or unable to work through illness Skilled manual w orker 10% 11% Student 9% 9% Employed position, working mainly at a desk 8% 9% Unemployed or temporarily not working 8% 7% Responsible for ordinary shopping and looking after the home, or without any current occupation, not working 8% 8% Employed position, not at a desk, but in a service job (hospital, restaurant, police, fireman, etc.) Middle management, other management (department head, junior manager, teacher, technician) 6% 6% 7% 7% Other (unskilled) manual worker, servant 4% 3% Employed position, not at a desk but travelling (salesmen, driver, etc.) 3% 3% Owner of a shop, craftsmen, other self-employed person 3% 3% Employed professional (employed doctor, lawyer, accountant, architect) 2% 2% Business proprietors, ow ner (full or partner) of a company 2% 2% Professional (law yer, medical practitioner, accountant, architect, etc.) 2% 2% Supervisor General management, director or top management 1% 1% 1% 1% Farmer 1% 1% 8 25% 25%

10 Looking at the results at the national level, the highest proportions of citizens not working can be found in Turkey (68%) and the former Yugoslav Republic of Macedonia (66%) in both these countries at least two-thirds of citizens are not working. However, in Turkey, there are relatively higher proportions of house persons (35%) and students (14%), with just over one in ten Turkish citizens classifying themselves as unemployed (11%). This is in contrast with former Yugoslav Republic of Macedonia, where a quarter of citizens say they are unemployed the highest of all European countries surveyed and far higher than the country with the next highest level of unemployment (Lithuania at 16%). Slovakia stands out as a country with higher levels of employment (62% working), followed by Sweden (59%), the Netherlands (58%), the Czech Republic (57%) and Finland (56%). Looking at the country groupings, lower levels of those working are apparent in NMS10 at 47% and NMS12 at 48%. Looking at the occupational levels by socio-demographics reveals that those who are most likely to be employed: Are Men Aged or aged Are educated until the age of 20 or beyond Have an internet connection at home 9

11 D15a.2 What is your current occupation? Employed Selfemployed Not working EU27 42% 8% 50% Sex Male 46% 11% 43% Female 39% 5% 56% Age % 1% 69% % 10% 25% % 13% 24% % 5% 80% Education (End of) 15-22% 5% 73% % 8% 40% % 12% 28% Still studying % Internet connection at home Yes 52% 10% 38% No 28% 5% 67% - Turkey and former Yugoslav Republic of Macedonia show the lowest levels of employment - Employees who are currently not working, were asked about their previous type of employment 11. Here, it is relevant to note that, of the respondents currently not working, 23% have never done any paid work. Taking into account that half the sample are currently not working, it means that 12% of the sample have never done any paid work. On a country level, a second interesting finding arises: Turkey and the former Yugoslav Republic of Macedonia, who have the highest proportion of respondents currently not working (68% and 66% respectively), also have the highest proportion of respondents who have never done any paid work (71% and 52% of those who are currently unemployed, respectively). Therefore, of the respondents sampled, just under half of those in Turkey (48%) have never done any paid work (34% for those in the former Yugoslav Republic of Macedonia). Greece and Italy also deserve a mention, where just under a quarter of respondents have never worked (24% for each). By contrast, countries where very few respondents have never worked include Denmark (3%), Finland (4%) and the UK (5%). The socio-demographic breakdown shows that across the EU27 those who are most likely to have never done any paid work are: Women Aged D15b.1 Did you do any paid work in the past? What was your last occupation? 10

12 Still studying Currently a student (or else, a house person) 1.2 Length of current/last job - On average, people have been with their current employer/last employer for around 12 years- The largest proportion of those surveyed have been with their current/last employer for one to five years (31%) whilst 15% say they have been with their employer for 6 to 10 years, a further 15% for 11 to 20 years and 16% of the sample have been with their employer for more than 20 years, resulting in an overall average of 11.6 years 12. This is lower than the average recorded in 2006 (12.2 years) largely due to more of the sample stating that they ve been with their employer for one to five years. QD5 For how long have you been working for your current employer or last employer if you are not currently working? - %EU to 5 years 28% 31% More than 20 years 11 to 20 years 6 to 10 years Never had any paid work 16% 17% 15% 15% 15% 14% 12% 14% Less than one year 4% 6% 7% 6% Countries that report the highest levels of employer-loyalty, in terms of staying with one employer for the greatest length of time, include Slovenia (14.9 years), Finland (13.7 years), France (13.6 years) and Luxembourg (13.5 years). By contrast, Romania (6.2 years), Turkey (7.3 years) and Latvia (7.7 years) report the lowest levels of staying with one employer, though it should be noted that 33% of those in Romania are also unsure of the answer to this question, and 51% in Turkey have never had any paid work (though the average figures excludes mentions of don t know and never had any paid work ). Those in the EU15 have also stayed with their current employer for longer (12.1 years) when compared to those countries which joined the EU since 2004 (9.9 years). 12 QD5. For how long have you been working for your current employer or last employer if you are not currently working? 11

13 QD5 For how long have you been working for your current employer or last employer if you are not currently working? - average SI FI FR LU IT EL DE BE SE PT NL MT EU27 AT CY ES SK CZ PL BG LT HU IE EE UK LV RO 6,2 7,7 14,9 14,2 13,7 13,1 13,6 12,4 13,5 14,3 13, ,2 13,9 13,1 13, ,3 12,8 12,7 12,1 13,4 11,8 10,6 11,7 12,7 11,6 12,2 11,4 12, , ,9 10,7 11,6 10, ,6 13,3 10,3 10,7 10,2 9,8 10,1 10,1 9,8 11,8 9,7 10 9,5 10 9,3 9,6 8,9 14,1 12

14 The socio-demographic analysis reveals: Men are likely to stay with one employer for longer than women. Those who are older tend to have stayed with their last employer for longer. Respondents with a household composition of one or two people have been with their current employer for longer. In-line with the age-related findings, those who are retired were with their last employer for the longest (20.2 years), followed by those who are self-employed (11.8 years) and managers (11.3 years). Those in rural villages worked with their employer for longer than those in large towns. Those who own their house/apartment have been with their employer longer. Predictably, those who haven t lost their jobs due to the economic crisis, who are not concerned about losing their jobs, and who feel a sense of job stability, tend to have been with their current/last employer for longer. 13

15 QD5 For how long have you been working for your current employer or last employer if you are not currently working? Never had any paid work Less than one year 1 to 5 years 6 to 10 years 11 to 20 years More than 20 years EU27 12% 4% 31% 15% 15% 16% 7% Sex Male 9% 3% 31% 15% 16% 19% 7% Female 15% 4% 30% 16% 15% 12% 8% Age % 8% 36% 2% - - 4% % 4% 53% 21% 10% 1% 5% % 3% 29% 20% 24% 15% 6% % 2% 12% 13% 20% 34% 11% Education (End of) 15-11% 2% 21% 15% 18% 22% 11% % 4% 36% 17% 17% 15% 7% 20+ 2% 3% 38% 19% 17% 16% 5% Still studying 81% 5% 10% 1% - - 3% Household composition 1 9% 4% 27% 15% 16% 20% 9% 2 7% 4% 28% 13% 17% 23% 8% 3 16% 4% 35% 16% 14% 9% 6% 4+ 18% 3% 34% 17% 14% 8% 6% Respondent occupation scale Self- employed 1% 4% 29% 18% 22% 15% 11% Managers - 2% 35% 22% 23% 16% 2% Other white collars - 3% 46% 22% 16% 10% 3% Manual workers - 4% 46% 20% 16% 10% 4% House persons 36% 5% 29% 11% 6% 4% 9% Unemployed 10% 7% 49% 14% 6% 4% 10% Retired 5% 2% 11% 12% 21% 35% 14% Students 81% 5% 10% 1% - - 3% Subjective urbanisation Rural village 11% 4% 29% 15% 16% 17% 8% Small/mid size town 14% 3% 29% 16% 15% 16% 7% Large town 12% 5% 35% 14% 15% 12% 7% Ownership house/ apartment Yes 11% 3% 27% 16% 17% 18% 8% No 15% 6% 39% 14% 11% 9% 6% Has lost his job Yes 3% 10% 53% 14% 9% 4% 7% No 13% 3% 29% 15% 16% 17% 7% Concerned about losing job No 6% 3% 32% 18% 19% 17% 5% A bit 6% 3% 41% 20% 17% 9% 4% Yes 7% 3% 40% 19% 16% 9% 6% Job stability Confident - 3% 39% 21% 20% 13% 4% Not confident - 4% 51% 16% 15% 8% 6% 14

16 1.3 Frequency of changing employers - Most respondents have changed their employer between one and five times- Sixty-percent of those surveyed say they have changed their employer between one and five times, with only 13% saying they have never changed employer 13. The remainder of the sample is divided between those who have changed employer 6 to 10 times (9%) and more than 10 times (2%) whilst 12% spontaneously say they have never had any paid work and the remainder are unsure. Countries with the highest average levels of changing jobs include Denmark (4.6 times), the UK (4.5 times), Sweden (4.2 times) and France (4 times), resulting in an overall higher frequency of changing employers in EU15 (3.3 times) when compared to NMS12 (2.6 times). In addition, comparing the results with the 2006 Eurobarometer shows that Spain, Cyprus and Slovakia show comparatively higher levels of changing jobs, largely due to fewer people saying they have never changed employer. 13 QD4. How many times have you changed employer in your working life so far? 15

17 QD4 How many times have you changed employer in your working life so far? (DO NOT COUNT VACATION JOBS WHILE IN FULL-TIME EDUCATION) - average UK SE FR FI EE LV ES NL IE EU27 HU LT AT SK CY EL PT DE CZ PL BG BE SI LU MT RO IT 4 3,7 3,5 3,9 3,5 3,4 3,4 3,5 3,4 2,4 3,2 3 3,2 3 3,2 2,9 3,1 2,9 3, ,9 2,9 2,3 2,9 2 2,9 2,5 2,7 2,6 2,7 2,4 2,7 2,6 2,6 2,4 2,6 2,4 2,5 2,3 2,3 2,2 2,2 1,8 2,1 1,8 2 1,7 2 1,9 4,2 4,2 4,6 4,7 4,5 4,5 16

18 The socio-demographic groupings most likely to have changed employers are: Men. Aged Educated up to the age of 19. Living alone in the household. Currently unemployed, or manual workers. Living in large towns. Respondents who have lost their jobs due to the economic crisis. QD4 How many times have you changed employer in your working life so far? (DO NOT COUNT VACATION JOBS WHILE IN FULL-TIME EDUCATION) Never had any paid work Never changed of employer 1 to 5 times 6 times or more EU27 12% 13% 60% 11% 4% Sex Male 10% 13% 61% 13% 3% Female 15% 13% 59% 9% 4% Age % 12% 32% 4% 2% % 12% 67% 11% 4% % 12% 67% 15% 3% % 14% 63% 11% 4% Education (End of) 15-11% 12% 61% 12% 4% % 12% 67% 13% 4% 20+ 2% 17% 68% 11% 2% Still studying 81% 4% 13% 0% 2% Household composition 1 9% 12% 60% 14% 5% 2 8% 13% 64% 12% 3% 3 16% 12% 60% 9% 3% 4+ 18% 13% 57% 9% 3% Respondent occupation scale Self- employed 1% 18% 65% 10% 6% Managers 1% 20% 67% 10% 2% Other white collars 1% 15% 71% 11% 2% Manual workers - 14% 68% 15% 3% House persons 36% 6% 48% 7% 3% Unemployed 9% 5% 62% 20% 4% Retired 5% 15% 65% 10% 5% Students 81% 4% 13% 0% 2% Subjective urbanisation Rural village 11% 14% 61% 10% 4% Small/mid size town 13% 13% 60% 11% 3% Large town 12% 11% 60% 13% 4% Has lost his job Yes 3% 4% 67% 22% 4% No 13% 14% 60% 10% 3% 17

19 2. PERCEIVED IMPACT OF THE ECONOMIC CRISIS ON THE JOB MARKET In this section, we look at whether Europeans have experienced job losses, either personally, amongst their families and friends or amongst colleagues, and their level of concern regarding future job losses due to the economic crisis. Here, we find that Europeans are very concerned about future job losses, which is probably due to the fact that they feel the worst impact of the economic crisis is yet to come. 2.1 Job losses as a result of the economic crisis - Europeans have experienced job losses due to the economic crisis - Europeans were asked whether, due to the economic crisis, they themselves had lost a job, someone from their family or friendship circle had lost their job or whether one of their colleagues had lost their job 14. Overall, 9% of those polled say they had lost their job due to the economic crisis. However, further analysis of these citizens at the overall EU27 level show that 3% have since found a job (and are not currently unemployed) resulting in an overall net job loss of 6%. In addition, since the total potential active working population is 58%, this results in a total effective net job loss, due to the economic crisis, of 3.48%. Compared to personal job loss, more citizens know families or friends that have lost their jobs (36%) and around a quarter state that one of their colleagues has lost their job (24%). Looking at the individual results at the national level, it is clear that the responses to these three measures show a strong correlation countries where respondents are more likely to have personally experienced job loss also rank highly in terms of friends/family and colleagues losing their jobs. The claimed job loss rate across all three measures is highest in the following countries (with the figures indicating claimed personal job loss 15 ; friends/family job loss; and colleagues job loss): Latvia 21%; 61%; 57% Lithuania 18%; 54%; 43% Spain 17%; 55%; 36% Ireland 16%; 49%; 37% Portugal 16%; 39%; 32% Estonia 15%; 52%; 42% Hungary 15%; 48%; 38% Other countries that stand out are Slovenia and Slovakia where, though the personal and friends/family job loss measure is on par or below the EU average of 9% and 36%, the incidence of colleagues having lost their jobs is higher: Slovakia (9%; 37%; 38%), Slovenia (7%; 29%; 37%). 14 QB1. Please tell me whether or not each of the following situations has happened to you, as a result of the economic crisis? You lost your job; Someone from your family, a relative, or a close friend lost their job; One of your colleagues has lost their job 15 Please note that these figures are the actual claimed personal job loss, and not the recalculated net job loss 18

20 On the other hand are countries that have experienced comparatively lower job losses across all three measures: Luxembourg 4%; 23%; 17% Greece 4%; 28%; 12% The Netherlands 5%; 24%; 16% Malta 5%; 26%; 15% Belgium 7%; 21%; 14% Cyprus 7%; 30%; 13% We see that, for the country groupings, countries in the EU6 16 report lower levels of job losses (7%, 31%, 19%) compared to NMS10 (11%, 37%, 27%). QB1. Please tell me whether or not each of the following situations has happened to you, as a result of the economic You lost your job crisis? Someone from your family, a relative, or a close friend lost their job One of your colleagues has lost their job EU27 9% 36% 24% BE 7% 21% 14% BG 10% 31% 29% CZ 11% 38% 35% 7% 36% 26% DE 7% 30% 20% EE 15% 52% 42% IE 16% 49% 37% EL 4% 28% 12% ES 17% 55% 36% FR 7% 33% 19% IT 6% 33% 18% CY 7% 30% 13% LV 21% 61% 57% LT 18% 54% 43% LU 4% 23% 17% HU 15% 48% 38% MT 5% 26% 15% NL 5% 24% 16% AT 7% 32% 27% PL 9% 31% 17% PT 16% 39% 32% RO 9% 28% 26% SI 7% 29% 37% SK 9% 37% 38% FI 9% 32% 23% SE 7% 37% 24% UK 9% 44% 28% HR 10% 32% 31% TR 12% 44% 24% MK 10% 35% 22% Highest percentage per item Highest percentage per country Lowest percentage per item Lowest percentage per country 16 The EU6 average is made up of the following: Belgium, Denmark, West-Germany, France, Italy and the Netherlands 19

21 From a socio-demographic point of view, those who have been hardest hit by job losses due to the economic crisis are: Men. Aged or aged 40-54, though this is understandable since this is the core working population. Those who were educated up to the age of 19. Living in large towns. QB1.Please tell me whether or not each of the following situations has happened to you, as a result of the economic crisis. Someone from your family, a relative, or a close friend lost their job One of your colleagues has lost their job You lost your job EU27 36% 24% 9% Sex Male 36% 29% 11% Female 36% 19% 7% Age % 23% 10% % 32% 13% % 31% 12% % 13% 3% Education (End of) 15-37% 18% 8% % 29% 12% % 25% 7% Still studying 30% 13% 3% Respondent occupation scale Self- employed 32% 25% 5% Managers 34% 28% 3% Other white collars 39% 30% 4% Manual workers 41% 33% 7% House persons 38% 12% 7% Unemployed 54% 53% 59% Retired 27% 9% 2% Students 30% 13% 3% Subjective urbanisation Rural village 35% 22% 8% Small/mid size town 36% 24% 9% Large town 37% 27% 10% 20

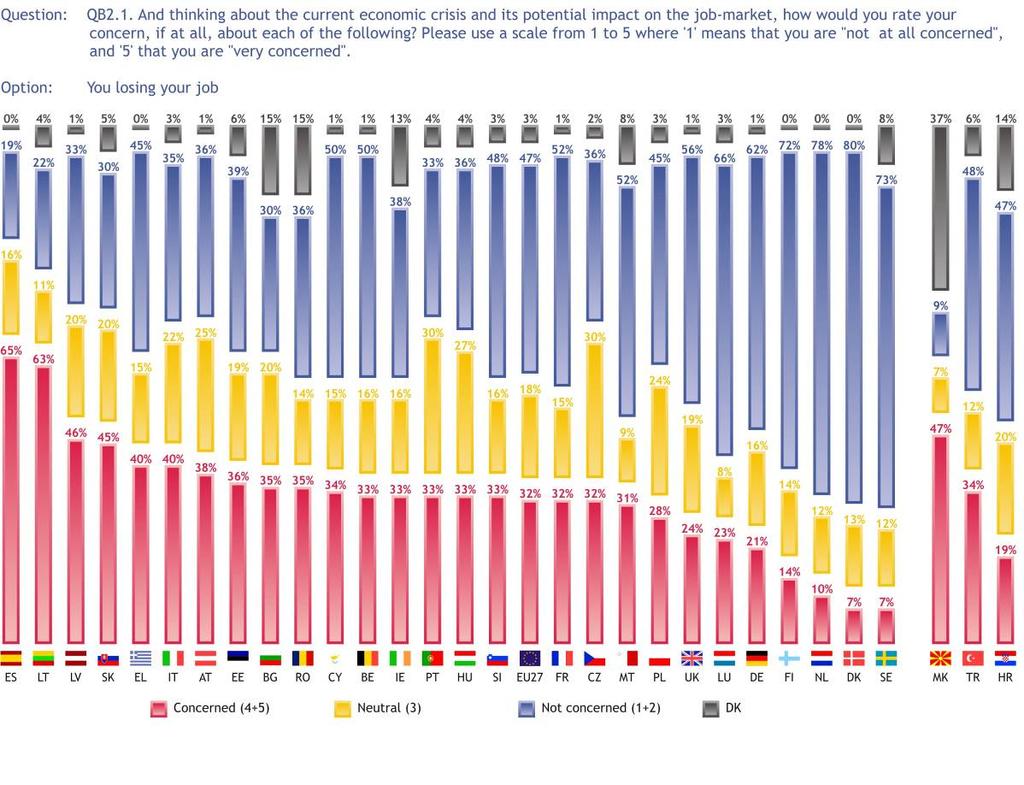

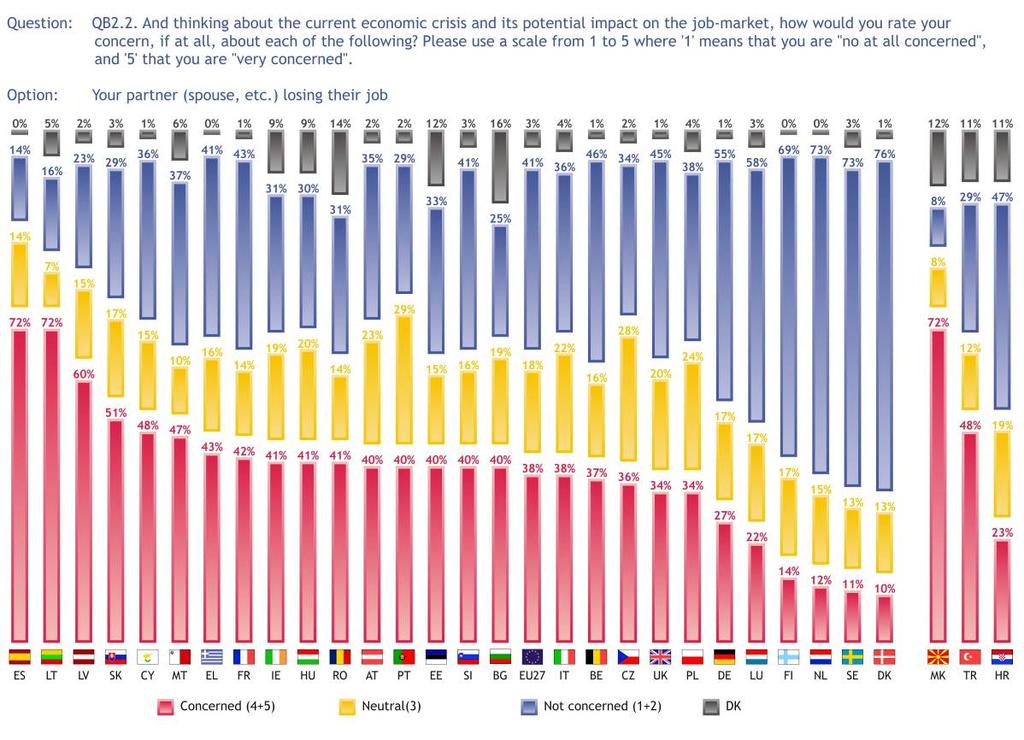

22 2.2 Concern about potential economic crisis impact on job market - Although there have been job losses due to the economic crisis, the level of concern regarding job losses to come is high - Europeans were asked to consider the current economic crisis and its impact on the job market, and to indicate their level of concern regarding job losses for themselves, their partners and their children. 17 For each of these statements there were high spontaneous mentions of Not applicable, largely from those not working, the unmarried or those who do not have children. It would therefore be prudent to exclude these respondents from the analysis. This provides the following results: QB2. And thinking about the current economic crisis and its potential impact on the job-market, how would you rate your concern, if at all, about each of the following? Answer 'concerned' -%EU Your children losing their job 47% Your partner (spouse, etc.) losing their job 38% You losing your job 32% The first key finding in the above data is that Europeans concern for their children s job losses is the highest. Later in this report, we will see that Europeans believe that the level of one s qualifications and professional experience are the two most important assets required for finding a job easily. It could therefore be hypothesised that parents concerns stem from the fact that children/young people, as entrants into the job market, are likely to have fewer years of work experience, and are therefore more vulnerable in these economic times, coupled with parents natural concern over the wellbeing of their children. 17 QB2. And thinking about the current economic crisis and its potential impact on the job-market, how would you rate your concern, if at all, about each of the following? Please use a scale from 1 to 5 where '1' means that you are "no at all concerned", and '5' that you are "very concerned". You losing your job; Your partner (spouse, etc.) losing their job; Your children losing their job 21

23 It is also important to note that close to a third of working Europeans (32%) are very concerned about losing their jobs, with even higher levels of concern over their spouses losing their jobs. Turning now to the national data, the second key finding emerges: the employed population in countries where the level of concern for personal job loss is high also rank the highest for concern regarding their spouses or children losing their jobs. Countries with high levels of concern for all three measures include: Spain 65% personal; 72% partner; 77% children Lithuania 63% personal; 72% partner; 69% children Latvia 46% personal; 60% partner; 72% children Here it is noted that, in terms of the actual job loss analysis provided above, citizens from Spain, Latvia and Lithuania also reported higher incidences of job losses, thus justifying their higher level of concern for future job losses. At the opposite end of the spectrum are countries with low levels of concern about job loss for themselves, their partners or their children, namely Denmark (80% not concerned about personal job loss; 76% not concerned for partner; 62% not concerned for children), the Netherlands (78%; 73%; 60%), Sweden (73%; 73%; 56%), Finland (72%; 69%; 51%) and Luxembourg (66%; 58%; 56%). In addition, when reporting on actual job losses above, citizens in the Netherlands and Luxembourg reported a lower incidence of job loss, hence their lower level of concern. In terms of the country groupings, it is noted that the group consisting of the Nordic countries and The Netherlands shows less concern regarding job losses across all three measures; in contrast, respondents in NMS12 are less likely to be not concerned only 38% (for personal), 33% (for partner) and 27% (for children) say they are not concerned about future job losses. 22

24 23

25 Analysis by socio-demographic variables shows: Women are more concerned about future job losses, for themselves, their partners and their children. Those aged are most likely to be concerned about job losses for themselves and their partners, whereas those aged 55+ are most concerned about their children s potential job losses. This makes sense in light of these respondents children most likely being old enough to be employed. Respondents who ended their education earlier (age 15 or before, are most concerned about job losses on all three measures). Those who have personally lost their jobs, are more worried that the same will happen to their partners and children. As would be expected, those who are not confident about their job stability, are also more worried that the economic crisis will result in them, their spouses or children losing their jobs. 24

26 QB2. And thinking about the current economic crisis and its potential impact on the job-market, how would you rate your concern, if at all, about each of the following? Please use a scale from 1 to 5 where '1' means that you are "no at all concerned", and '5' that you are "very concerned". You losing your job Your partner (spouse, etc.) losing their job Your children losing their job Concerned (4+5) Not concerned (1+2) Concerned (4+5) Not concerned (1+2) Concerned (4+5) Not concerned (1+2) EU27 32% 47% 3% 38% 41% 3% 47% 31% 4% Sex Male 30% 48% 3% 34% 44% 3% 43% 34% 4% Female 34% 46% 3% 42% 38% 3% 51% 28% 4% Age % 45% 4% 40% 36% 5% 28% 44% 18% % 45% 2% 41% 37% 2% 34% 41% 10% % 44% 2% 40% 39% 2% 48% 30% 3% % 57% 4% 29% 54% 4% 51% 28% 2% Education (End of) 15-38% 42% 4% 44% 38% 3% 57% 23% 2% % 43% 2% 42% 37% 2% 46% 31% 4% % 56% 2% 30% 49% 2% 36% 41% 4% Still studying 26% 48% 7% 29% 44% 9% 23% 47% 21% Has lost his job Yes % 18% 2% 65% 18% 5% No 32% 47% 3% 34% 44% 3% 46% 32% 4% Job stability Confident 25% 54% 1% 30% 48% 1% 36% 41% 4% Not confident 77% 9% 2% 62% 18% 3% 60% 16% 6% 25

27 2.3 Perceived economic crisis cycle - When considering the impact of the economic crisis on the job market, more than six in ten Europeans feel the worst is yet to come - Europeans high levels of concern about job losses are explained when one considers that 61% of Europeans feel that the worst is still to come. 18 Just over a quarter of Europeans (28%) feel more optimistically that the impact of the crisis on jobs has already reached its peak, while around one in ten (11%) have no opinion. The highest proportions of respondents believing the worst is still to come can be found in Latvia (82%), Estonia (76%), Lithuania (74%), Cyprus (73%), Luxembourg (73%) and Croatia (73%). As seen above, Latvia and Lithuania are very concerned about job losses, most likely due to also feeling that the worst is yet to come. Estonia and Cyprus follow the same trend of being concerned about job losses and feeling the worst is yet to come. Luxembourg and Croatia show somewhat different results: though both countries feel the worst of the crisis is yet to come, both also show lower than average levels of concern about job losses. The trend at the other end of the spectrum also holds true: Sweden, a country that showed the lowest levels of concern over job losses, is also now most likely to say that the impact of the economic crisis on jobs has already reached its peak (45%), followed by Turkey (39%) and Denmark (36%; another country that posted low levels of job loss concern). 18 QB3 Some analysts say that the impact of the economic crisis on the job market has already reached its peak and things will recover little by little; others, on the contrary, say that the worst is still to come. Which of the two statements is closer to your opinion? 26

28 However, it should be noted that the absolute majority of citizens in all three of these countries still feel that the worst is still to come. Finally, it is worth noting the comparatively high levels of citizens in Bulgaria who are unable to give an opinion (34% don t know), together with Romania (23% don t know) and Portugal (21% don t know). Looking at the results on a socio-demographic level, and discarding relatively higher mentions of don t know (where relevant), reveals that some groups are slightly more likely to feel the worst is yet to come including: Aged 40+. Those who ended their education before the age of 20. Living in a household with two people. Currently unemployed. Living in a rural village. Not the owners of their house or apartment. Those who do not have an internet connection at home (though the same group are also more likely to say don t know). Pessimistic in general about the national situation of employment, the national economy and the financial situation in their household. Those who have lost their jobs due to the economic crisis (though those who haven t lost their jobs are also more likely to have no opinion). Those who are concerned about losing their jobs and not confident in their job stability. 27

29 QB3 Some analysts say that the impact of the economic crisis on the job market has already reached its peak and things will recover little by little; others, on the contrary, say that the worst is still to come. Which of the two statements is closer to your opinion? The worst is still to come The impact of the crisis on jobs has already reached its peak EU27 61% 28% 11% Sex Male 61% 30% 9% Female 61% 27% 12% Age % 33% 13% % 32% 9% % 27% 8% % 25% 13% Education (End of) 15-62% 24% 14% % 28% 10% % 32% 8% Still studying 52% 34% 14% Household composition 1 61% 25% 14% 2 64% 26% 10% 3 59% 31% 10% 4+ 59% 31% 10% Respondent occupation scale Self- employed 61% 29% 10% Managers 61% 32% 7% Other white collars 57% 33% 10% Manual workers 62% 29% 9% House persons 59% 28% 13% Unemployed 70% 22% 8% Retired 62% 24% 14% Students 52% 34% 14% Subjective urbanisation Rural village 63% 26% 11% Small/mid size town 60% 29% 11% Large town 59% 31% 10% Ownership house/ apartment Yes 60% 29% 11% No 63% 26% 11% Internet connection at home Yes 60% 31% 9% No 62% 24% 14% Nat. situation of employment Good 50% 40% 10% Bad 64% 26% 10% Situation of national economy Good 49% 40% 11% Bad 64% 26% 10% Financial situation household Good 57% 33% 10% Bad 68% 20% 12% Has lost his job Yes 69% 24% 7% No 60% 29% 11% Concerned about losing job No 57% 34% 9% A bit 57% 32% 11% Yes 65% 27% 8% Job stability Confident 59% 33% 8% Not confident 70% 22% 8% 28

30 3. CONFIDENCE IN RETAINING EMPLOYMENT This section explores whether Europeans feel confident of retaining their jobs or, for those who are currently unemployed, their confidence that they will have a job in two year s time. 3.1 Confidence in retaining jobs -Europeans confidence in keeping their current job has declined- Respondents who are currently working were asked the confidence in their ability to keep their job in the coming months 19. Although Europeans are fairly confident (80% are confident in their ability to keep their job in the coming months), this figure has declined from 84% confidence in the 2006 Eurobarometer survey. This is largely due to fewer people being very confident about keeping their job (50% in 2006 vs. 40% in 2009). Countries where respondents are the most confident that they will keep their job in the coming months include Luxembourg (93%), Denmark and Finland (both 92%) and Sweden (90%). On the other hand are the countries where at least a third of respondents do not feel confident about their ability to keep a job: Slovakia (42%), Hungary (41%), Lithuania (40%), Turkey (39%) and Greece (35%). Overall, those in the EU15 are more confident in their ability to keep their jobs (82%) when compared to the NMS12 (70%). 19 QD7 How confident would you say you are in your ability to keep your job in the coming months? Are you? Very confident; Fairly confident; Not very confident; Not at all confident; Don't know 29

31 Comparing the results from the 2006 Eurobarometer shows the largest decrease in confidence occurred in the following countries: Latvia (87% to 71%), Spain (86% to 72%), Ireland (89% to 75%), Lithuania (73% to 57%) and Greece (78% to 63%). On the other hand, confidence levels increased in seven countries. Item was not previously asked for MK EB71.2 May-Jun 2009 / EB65.3 Apr-May

32 The socio-demographic analysis shows that those who are most confident in their ability to keep their jobs in the coming months are: Aged (those aged and working are more likely to be not confident while a larger proportion of those aged 55+ are unsure of their answer). Educated for longer (age 20 and older). Living in a larger household (4 or more people). Managers (manual workers are the least confident). Owners of their house/apartment. Optimistic in general about the national situation of employment, the national economy and the financial situation in their household. Not concerned about losing their job due to the economic crisis impact on the job market. 31

33 QD7 How confident would you say you are in your ability to keep your job in the coming months? Are you? Confident Not confident EU27 80% 16% 4% Sex Male 81% 16% 3% Female 80% 16% 4% Age % 19% 3% % 16% 3% % 16% 3% % 16% 9% Education (End of) 15-71% 21% 8% % 18% 4% % 11% 2% Still studying - Household composition 1 77% 17% 6% 2 78% 17% 5% 3 80% 17% 3% 4+ 83% 15% 2% Respondent occupation scale Self- employed 81% 14% 5% Managers 90% 8% 2% Other white collars 81% 16% 3% Manual workers 74% 22% 4% House persons Unemployed Retired Students Ownership house/ apartment Yes 81% 16% 3% No 77% 18% 5% Nat. situation of employment Good 89% 9% 2% Bad 78% 18% 4% Situation of national economy Good 87% 10% 3% Bad 78% 18% 4% Financial situation household Good 88% 9% 3% Bad 60% 34% 6% Concerned about losing job No 96% 3% 1% A bit 87% 10% 3% Yes 62% 35% 3% 32

34 3.2 Confidence in having a job in two years time - Two thirds of Europeans who want to be working in two years time feel confident they will have a job - All respondents were asked how confident they were of having a job in two years time. 20 However, it should be borne in mind that 35% of respondents spontaneously said they were not looking for a job in two years time. It would therefore be prudent to exclude these respondents from the analysis. This results in an overall confidence of 66% in this survey (of the sub-base), which is stable as compared with the confidence level reported in The data at national level shows a great correlation between countries where the workers are confident in their ability to keep their jobs, and all potentially active respondents confidence in having a job in two years time. The countries with the highest confidence levels are again Finland (90%), Denmark (87%), the Netherlands (85%), Luxembourg (83%) and the UK (81%). In addition, there s similarity in the countries that are not confident: Slovakia (57%), former Yugoslav Republic of Macedonia (55%), Lithuania, Latvia and Greece (all three at 52%). Again, confidence is higher amongst the 15 original European Union Member States (70%), driven especially by high levels of confidence in Finland, Austria and Sweden (78%) when compared to the 12 New Member States (54%). 20 QD8 Would you say that you are very confident, fairly confident, not very confident or not at all confident in having a job in 2 years time? 33

, Lithuania (51% to 39%), the Czech Republic (80% to 71%) and Bulgaria (47% to 39%).")

35 Item was not previously asked for HR, MK, TR EB71.2 May-Jun 2009 / EB70.1 Oct-Nov 2008 Comparing the results with the 2008 Eurobarometer shows decreased confidence in Latvia (61% to 46%), Lithuania (51% to 39%), the Czech Republic (80% to 71%) and Bulgaria (47% to 39%). However, there have been increases in the confidence about having a job in two years time for those in Luxembourg (75% to 83%), Romania (49% to 56%) and Germany (68% to 74%). Overall, around half of Member States have seen a rise in confidence by this measure, and half have seen a fall. Analysis of the socio-demographic variables reveals the following: Men are more likely than women to be confident by this measure. The highest confidence level is found in the age group, with the lowest confidence in the potentially active 55+ age group (bearing in mind that respondents who spontaneously say they won t be looking for a job in 2 years time have been excluded from the analysis). The confidence level increases proportionately with education, with those who have been educated at least to the age of 20 being the most confident. 34

36 The further demographic trends follow the same trends as noticed amongst workers confidence levels, in that those who are the most confident are optimistic about the national economy and employment, and haven t been hit by the economic crisis impact on the job market. QD8 Would you say that you are very confident, fairly confident, not very confident or not at all confident in having a job in 2 years time? Very confident + Fairly confident Not very confident + Not at all confident EU27 66% 28% 6% Sex Male 69% 26% 5% Female 63% 30% 6% Age % 27% 5% % 25% 4% % 29% 4% % 33% 14% Education (End of) 15-50% 41% 9% % 30% 5% % 18% 3% Still studying 65% 28% 7% Nat. situation of employment Good 84% 13% 3% Bad 63% 31% 6% Situation of national economy Good 79% 17% 4% Bad 63% 31% 6% Has lost his job Yes 47% 49% 4% No 69% 25% 6% 35

37 4. CONSEQUENCES OF JOB LOSS This section explores respondents perceived confidence in finding new employment, in the event of being laid off, and what proportion of their income they feel would be covered by their country s unemployment insurance. 4.1 Confidence in finding new employment - Finding a new job is perceived to be harder than before - Working respondents were asked their perceived likelihood of finding a job in the next six months if they were laid off. 21 Thirty-nine percent of Europeans feel they are very likely, 21% feel they are likely and 33% feel they are unlikely to find a new job in the next six months. A decline in confidence levels is evident for this measure as well: very likely declined from 44% in 2008 (to 39% in 2009) while those feeling it unlikely that they would find a new job increased from 28% in 2008 to 33% currently, showing one of the most significant shifts when these results are compared with The following countries post the lowest likelihood levels on this measure, with the figure in brackets indicating the proportion of respondents who felt it was not likely that they would find a job: Hungary (47%), Italy (46%), the former Yugoslav Republic of Macedonia (45%) and Lithuania (44%). Here, the reader is reminded that the former Yugoslav Republic of Macedonia and Lithuania also ranked lowest with regard to confidence levels in having a job in two years time. 21 QD14 If you were to be laid-off, how would you rate on a scale of 1 to 10, the likelihood of you finding a job in the next six months? '1' means that it "would be not at all likely" and '10' means that it "would be very likely". 36

38 On the other side of the spectrum are countries that believe the chance of finding a new job is very likely : Denmark (71%), the Netherlands (65%), Sweden (63%) and Finland (59%). Predictably, these countries were also prominent in people s confidence levels to retain their jobs. It therefore fits that countries in the EU15 states are more likely to feel they ll find a job (38% very likely), compared to NMS 12 (43% very likely). There are also higher levels of optimism in the non-euro zone (47% very likely) when compared to the Euro zone (35% very likely). Item was not previously asked for HR, MK, TR EB71.2 May-Jun 2009 / EB70.1 Oct-Nov 2008 Lithuania, one of the countries with the lowest optimism about finding a new job, also shows the highest increase in respondents believing they are not likely to find a job: from 23% in 2008 to 44% currently. Other countries showing major shifts, with more respondents feeling they re not likely to find a job include Ireland (26% to 42%), Spain (28% to 40%), Estonia (17% to 29%, although Estonians are still more optimistic than the EU average on this measure) and Hungary (35% to 47%, resulting in Hungary being the most pessimistic of all countries surveyed). 37

39 Analysis on socio-demographic variables shows the following groups are more likely to feel they won t be able to find a job: Women. Older respondents (aged 55+). Those who are lesser educated (ended their education at or before the age of 15). Manual workers (with managers showing the most optimism). People in rural villages and small towns (people in large towns show more optimism). Do not have an internet connection at home. Are not satisfied with the life they lead. Are generally pessimistic about the national employment situation, national economy and financial situation in their household. Have lost their job due to the economic crisis. Are concerned about losing their jobs, and not confident in their job stability. 38

40 QD14 If you were to be laid-off, how would you rate on a scale of 1 to 10, the likelihood of you finding a job in the next six months? '1' means that it "would be not at all likely" and '10' means that it "would be very likely". Not likely Likely Very likely EU27 33% 21% 39% 7% Sex Male 31% 21% 41% 6% Female 35% 21% 36% 7% Age % 24% 45% 5% % 22% 46% 5% % 22% 36% 6% % 14% 24% 15% Education (End of) 15-46% 20% 23% 11% % 23% 36% 7% % 20% 49% 5% Still studying Respondent occupation scale Self- employed 33% 15% 38% 14% Managers 26% 17% 53% 5% Other white collars 32% 25% 37% 5% Manual workers 36% 24% 35% 5% House persons Unemployed Retired Students Subjective urbanisation Rural village 33% 22% 37% 8% Small/mid size town 35% 22% 37% 7% Large town 29% 20% 46% 5% Internet connection at home Yes 30% 21% 43% 6% No 40% 23% 29% 9% Satis. life you lead Satisfied 30% 22% 42% 6% Not satisfied 46% 21% 25% 8% Nat. situation of employment Good 20% 17% 58% 6% Bad 36% 22% 35% 7% Situation of national economy Good 25% 18% 52% 5% Bad 35% 22% 36% 7% Financial situation household Good 29% 21% 44% 6% Bad 44% 23% 26% 7% Has lost his job Yes 40% 24% 33% 3% No 32% 21% 40% 7% Concerned about losing job No 26% 15% 53% 7% A bit 32% 30% 33% 5% Yes 43% 26% 27% 4% Job stability Confident 29% 21% 44% 6% Not confident 51% 24% 21% 4% 39

41 4.2 Expectations about the level of unemployment insurance - Unemployment is expected to lead to a cut of around 30% of current income - Just over a quarter of Europeans (28%) believe that, if they were laid off, their country s unemployment insurance would compensate them for between 51% and 70% of their current income 22. Around a fifth believe that their welfare system would pay out a sum higher than this band (though only 4% believe it to be as high as 91% to 100% of current income) while a further 28% believe it to be lower than 51% of current income. Although this question was only asked of working Europeans, 24% stated that they did not know the level of protection against loss of income offered by their country. The results show little change over time. QD16 If you were to be laid-off, how much do you think the unemployment insurance and the welfare system in (OUR COUNTRY) will compensate you for the loss of income during the first six months as a percentage of your current income? - %EU % or less of your current income 17% 17% 31 to 50% of your current income 11% 12% 51 to 70% of your current income 27% 28% 71 to 90% of your current income 16% 17% 91 to 100% of your current income 4% 4% 23% 24% 22 QD16 If you were to be laid-off, how much do you think the unemployment insurance and the welfare system in (OUR COUNTRY) will compensate you for the loss of income during the first six months as a percentage of your current income? 40

, the Netherlands (43%) and Sweden (43%).")

42 Close to two-thirds of working citizens in Luxembourg believe their country s welfare system will pay out at least 71% of their current income. This is far above the countries with the second highest perceived level of income protection: Spain (44% perceived payment of 71%+ to apply), the Netherlands (43%) and Sweden (43%). By contrast, those in the UK, Greece and Croatia do not expect a large payment, and in fact 56% of those in the UK expect a payment of 30% or less of current income (40% in Greece and 36% in Croatia state the same). Citizens in the Former Yugoslav Republic of Macedonia, Malta and Turkey show high levels of ambivalence, with more than half of working citizens not knowing what level of income protection is offered in their country. Comparing the results with 2008 shows that, overall, the perceived levels of unemployment insurance compensation have remained stable. However, some shifts at national level are evident; more British citizens believe that the insurance benefit will be 30% or less of current income (49% in 2008 to 56% currently) rather than being higher. In Malta, mentions for this band have also increased (19% to 25%) though more respondents also don t know what level of compensation is provided (43% to 51%). Similar increases over time in the level of uncertainty can also be seen in Portugal (26% to 45%) and Latvia (28% to 36%). In contrast, more of those polled in Romania now believe that the unemployment insurance will be 91% to 100% of income (4% to 12%), and more Slovenians believe their insurance will be 71% to 90% of income (14% to 30%). 41

43 Item was not previously asked for HR, MK, TR EB71.2 May-Jun 2009 / EB70.1 Oct-Nov 2008 The socio-demographic analysis shows the following groups are more likely to state the level of unemployment insurance will be at least 71% of income: Men (though it is also noted that more women are unsure of the level of insurance). Aged (25-39). Here also, it is clear that many older respondents (55+) do not know the level of unemployment insurance. Higher educated (age 20 and beyond). Close to a third of those who ended their education before the age of 16 don t know the level of insurance. White-collar workers (those who are self-employed are more likely to be unsure.) Live in rural villages. 42

44 Have an internet connection at home. Positive about the financial situation in their household. Confident in their job stability. QD16 If you were to be laid-off, how much do you think the unemployment insurance and the welfare system in (OUR COUNTRY) will compensate you for the loss of income during the first six months as a percentage of your current income? 71% or more of your current income 51 to 70% of your current income 50% or less of your current income EU27 20% 28% 28% 24% Sex Male 22% 28% 28% 22% Female 19% 27% 28% 26% Age % 28% 29% 26% % 26% 28% 23% % 30% 28% 21% % 25% 26% 34% Education (End of) 15-16% 29% 23% 32% % 28% 29% 23% % 27% 28% 21% Still studying Respondent occupation scale Self- employed 11% 16% 35% 38% Managers 21% 31% 29% 19% Other white collars 24% 28% 28% 20% Manual workers 22% 30% 25% 23% House persons Unemployed Retired Students Subjective urbanisation Rural village 24% 28% 23% 25% Small/mid size town 20% 29% 28% 23% Large town 17% 25% 34% 24% Internet connection at home Yes 22% 28% 28% 22% No 17% 25% 28% 30% Financial situation household Good 22% 28% 27% 23% Bad 17% 27% 30% 26% Job stability Confident 21% 28% 28% 23% Not confident 18% 26% 32% 24% 43

45 5. JOB SEEKING In this section, we look at whether respondents feel job mobility (changing job or sector) or geographic mobility (changing location) will assist the most in finding a job and the qualifications and experience required to find a job more easily. 5.1 Job seeking strategies - Most would first apply for a job in a different location, rather than change jobs - Citizens who are currently working were asked how, in the event of being laid off, they would find a job by applying for the same or a different job, in the same or a different location. 23 Most European working citizens feel they would find a job by applying for the same kind of job, in the same location but for a different employer (47%). Alternatively, just under a third say they would opt for the same kind of job, but in a different location (32%). Around one in ten feel they would apply for a different kind of job in another location (9%) while 13% would start their own business. QD15 If you were to be laid-off, how would you find a job? (MAX. 2 ANSWERS) -%EU By applying for the same kind of job, in the same location, but for another employer By applying for the same kind of job but in a different location By applying for a completely different kind of job in the same location By starting your own business By applying for a completely different kind of job in another location Other (SPONTANEOUS) 19% 18% 13% 14% 9% 10% 4% 5% 9% 8% 32% 32% 47% 46% Those not working were asked a similar question, 24 examining what they believe would be the easiest way of finding a job. Here it should be noted that 29% of those not working spontaneously said that they were not looking for a job. They have therefore been excluded from the analysis. 23 QD15 If you were to be laid-off, how would you find a job? (MAX. 2 ANSWERS) 24 QD17 In your opinion, what would be the easiest way to find a job? (MAX. 2 ANSWERS) 44

46 A relatively large proportion of those not working and looking for a job say they would take up any job (38%). This response has barely changed since the previous reading (37% in 2006 up to 38% now). Around a quarter of those not working further say they would apply for the same kind of job, either in the same location (27%) or a different location (21%). QD17 In your opinion, what would be the easiest way to find a job? (MAX. 2 ANSWERS) -%EU By taking up any job By applying for the same kind of job as your last one, in the same location, but for another employer By applying for the same kind of job as your last one, but in a different location By starting your own business By applying for a completely different kind of job than your last one, but still in the same location By applying for a completely different kind of job than your last one, and in a different location Other (SPONTANEOUS) 3% 4% 13% 14% 12% 12% 8% 8% 10% 9% 21% 22% 27% 27% 38% 37% Turning now to the analysis by country for 2009, and for those working, the following countries working citizens have a much higher preference for staying in the same job and same location, when compared to the other options: Turkey, Romania, Cyprus, Greece, Poland, the Czech Republic and the UK. Only four countries provide higher mentions for applying for the same job but in a different location when compared to keeping the same job and location: the former Yugoslav Republic of Macedonia, Slovenia, France, Luxembourg and The Netherlands. 45

47 QD15. If you were to be laid-off, how would you find a job? (MAX. 2 ANSWERS) By applying for the same kind of job, in the same location, but for another employer By applying for the same kind of job but in a different location By applying for a completely different kind of job in the same location By starting your own business By applying for a completely different kind of job in another location Other (SPONTANEOUS) EU27 47% 32% 19% 13% 9% 4% 9% BE 52% 27% 23% 12% 8% 4% 3% BG 55% 16% 28% 10% 6% 2% 11% CZ 54% 27% 23% 9% 6% 2% 7% 59% 35% 30% 8% 11% 3% 2% DE 51% 44% 15% 10% 11% 5% 7% EE 34% 30% 26% 11% 20% 4% 6% IE 50% 37% 16% 11% 9% 3% 14% EL 48% 26% 12% 29% 4% 0% 8% ES 45% 36% 23% 14% 13% 3% 6% FR 40% 43% 16% 15% 14% 2% 6% IT 37% 21% 18% 14% 8% 4% 16% CY 55% 27% 23% 7% 8% 2% 7% LV 43% 25% 20% 11% 12% 9% 7% LT 42% 27% 22% 9% 16% 9% 6% LU 36% 38% 10% 9% 12% 8% 9% HU 42% 32% 15% 3% 10% 2% 9% MT 36% 35% 11% 8% 17% 3% 15% NL 40% 42% 12% 14% 12% 6% 4% AT 51% 39% 24% 8% 8% 5% 5% PL 48% 17% 19% 12% 7% 2% 12% PT 50% 34% 12% 10% 6% 2% 16% RO 51% 16% 16% 14% 4% 3% 17% SI 30% 35% 15% 14% 16% 9% 4% SK 55% 25% 29% 11% 6% 2% 11% FI 41% 32% 25% 13% 9% 3% 3% SE 51% 32% 26% 14% 5% 5% 5% UK 55% 29% 23% 13% 8% 3% 6% HR 50% 26% 22% 9% 8% 4% 7% TR 46% 13% 4% 16% 5% 8% 14% MK 20% 26% 10% 28% 11% 8% 13% Highest percentage per item Highest percentage per country Lowest percentage per item Lowest percentage per country 46

48 Comparing the results with 2006, for those working, at the national level, it emerges that citizens who are now more likely to remain in the same location, with the same job, are Lithuanians, Maltese, Austrians and the Spanish. The increase in Malta for this statement can be attributed to fewer mentions of starting your own business. Austrians are more likely to stay within the same location (whether in the same or a different job) and less likely to choose a different location. Item was not previously asked for MK EB71.2 May-Jun 2009 / EB65.3 Apr-May 2006 The Spanish record increases on all statements, largely due to fewer Spaniards answering don t know to this question than in In contrast, countries that are now more inclined to apply for the same kind of job, but in a different location, include the Czech Republic, Hungary, Latvia, Ireland and Portugal. 47

49 Analysing the working respondents socio-demographic groupings show: Women tend to prefer to stay in the same job, in the same location, while men are more likely to start their own business. Those in the youngest age group (age 15-24) post higher scores on all measures with the exception of starting their own business. Respondents who have been educated for longer (age 20 or above) are more geographically mobile (applying for the same type of job, but in a different location) and more likely to start their own business. Those with lower education levels are more likely to say they ll explore other options or are unsure of what they would do. Self-employed workers are most likely to say they ll start their own business, explore other options or are unsure of what they would do. Managers show greater geographic mobility (applying for the same kind of job, but in a different location) while other white-collar workers and manual workers show greater job mobility (being open to applying for a different kind of job). Those in large towns are more likely to want to remain in the same location, whilst those in rural villages are comparatively more open to exploring other locations, suggesting an acceptance that larger towns may offer better employment prospects. Interestingly, home ownership does not seem to impact on geographic mobility, as those who own their house or apartment are as willing to change location (whilst applying for the same kind of job) as those who don t own their accommodations. 48

50 QD15 If you were to be laid-off, how would you find a job? (MAX. 2 ANSWERS) By applying for the same kind of job, in the same location, but for another employer By applying for the same kind of job but in a different location By applying for a completely different kind of job in the same location By starting your own business By applying for a completely different kind of job in another location Other (SPONTANEOUS) EU27 47% 32% 19% 13% 9% 4% 9% Sex Male 44% 33% 18% 15% 10% 3% 9% Female 51% 31% 20% 10% 8% 4% 8% Age % 37% 23% 9% 12% 2% 5% % 34% 19% 13% 10% 2% 7% % 34% 19% 13% 9% 3% 8% % 18% 17% 14% 7% 10% 18% Education (End of) 15-45% 27% 17% 10% 9% 6% 14% % 30% 21% 12% 10% 4% 8% % 37% 17% 15% 8% 3% 7% Still studying Respondent occupation scale Self- employed 28% 18% 11% 30% 7% 7% 19% Managers 50% 40% 15% 13% 7% 4% 6% Other white collars 51% 32% 21% 8% 10% 2% 7% Manual workers 51% 33% 22% 9% 11% 3% 7% House persons Unemployed Retired Students Subjective urbanisation Rural village 39% 36% 17% 13% 12% 4% 11% Small/mid size town 48% 31% 20% 13% 9% 4% 8% Large town 57% 28% 20% 12% 6% 3% 7% Ownership house/ apartment Yes 46% 32% 18% 14% 9% 3% 9% No 50% 33% 20% 10% 11% 4% 7% 49

51 Turning now to results for those not working by country, non-working citizens of the following countries are most likely to take up any job, rather than staying in the same job and same location: Slovenia, the former Yugoslav Republic of Macedonia, Italy and Latvia. In addition, Slovenia and Latvia record large increases for this statement when compared to 2006 (Slovenia: 28% to 51% for any job; Latvia: 32% to 52%) with Estonia and Spain also showing increased openness to taking up any job. By contrast, those who prefer to stay within the same job and same location, rather than taking up any job, come from the Netherlands, Cyprus, Denmark and Sweden. It should nevertheless be noted that Denmark records a decrease in willingness to stay in the same job and location and take up any job and increases in willingness to take up a different type of job (whether in the same or a different location). The Swedish are also less likely to take up any job (when compared to 2006), and show more interest in starting their own business. QD17 In your opinion, what would be the easiest way to find a job? (MAX. 2 ANSWERS) By taking up any job By applying for the same kind of job as your last one, in the same location, but for another employer By applying for the same kind of job as your last one, but in a different location By starting your own business By applying for a completely different kind of job than your last one, but still in the same location By applying for a completely different kind of job than your last one, and in a different location EU27 38% 27% 21% 13% 12% 8% 3% 10% Other (SPONTANEOUS) BE 44% 32% 27% 12% 15% 6% 2% 3% BG 40% 22% 12% 3% 10% 7% 3% 23% CZ 41% 29% 13% 10% 23% 0% 1% 6% 27% 34% 24% 9% 22% 15% 7% 7% DE 28% 31% 29% 6% 15% 9% 4% 13% EE 28% 33% 22% 20% 14% 11% 2% 8% IE 31% 31% 20% 6% 11% 6% 5% 28% EL 38% 39% 22% 17% 4% 6% 1% 2% ES 51% 29% 15% 13% 16% 8% 1% 4% FR 33% 30% 34% 19% 14% 7% 5% 5% IT 44% 11% 15% 20% 6% 7% 3% 14% CY 25% 32% 9% 10% 16% 12% 8% 13% LV 52% 20% 12% 8% 14% 8% 3% 7% LT 47% 24% 16% 10% 8% 7% 5% 7% LU 35% 20% 30% 9% 8% 8% 5% 16% HU 41% 24% 12% 8% 10% 7% 6% 6% MT 39% 18% 18% 15% 6% 4% 2% 22% NL 31% 42% 27% 10% 10% 6% 3% 3% AT 37% 36% 25% 9% 19% 9% 7% 0% PL 29% 27% 17% 22% 12% 7% 3% 4% PT 42% 19% 17% 6% 14% 4% 3% 12% RO 27% 16% 5% 12% 7% 1% 1% 43% SI 51% 12% 16% 20% 6% 12% 7% 3% SK 45% 27% 10% 25% 18% 8% 3% 8% FI 29% 29% 19% 4% 19% 9% 4% 15% SE 31% 37% 24% 12% 7% 5% 2% 17% UK 40% 39% 26% 9% 15% 12% 1% 4% HR 42% 24% 13% 16% 8% 6% 2% 12% TR 24% 23% 8% 11% 5% 4% 5% 28% MK 45% 9% 8% 30% 3% 7% 3% 9% Highest percentage per item Lowest percentage per item Highest percentage per country Lowest percentage per country 50

52 The socio-demographic analysis of those who are not working (and still excluding those who spontaneously said they were not looking for a job) shows: Men are more likely than women to apply for the same type of job (whether in the same or a different location) or to start their own business. Women, on the other hand, are more likely to say they ll take up any job. Those in the middle age groups (age 25-54) tend to prefer staying in the same job and same location. Here, younger respondents are more likely to believe they would start their own business. Better educated respondents prefer applying for the same kind of job, while lesser educated respondents would take on any kind of job. People in rural villages are also more likely to be willing to take on any kind of job. 51

53 QD17 In your opinion, what would be the easiest way to find a job? (MAX. 2 ANSWERS) By taking up any job By applying for the same kind of job as your last one, in the same location, but for another employer By applying for the same kind of job as your last one, but in a different location By starting your own business By applying for a completely different kind of job than your last one, but still in the same location By applying for a completely different kind of job than your last one, and in a different location Other (SPONTANEOUS) EU27 38% 27% 21% 13% 12% 8% 3% 10% Sex Male 35% 29% 23% 15% 13% 8% 3% 9% Female 40% 26% 19% 11% 12% 7% 2% 11% Age % 26% 21% 16% 9% 7% 2% 13% % 30% 21% 12% 14% 10% 4% 4% % 30% 23% 10% 15% 7% 2% 6% % 19% 11% 14% 13% 7% 2% 19% Education (End of) 15-44% 24% 15% 10% 14% 8% 2% 11% % 30% 21% 11% 13% 8% 3% 6% % 31% 27% 13% 17% 10% 4% 5% Still studying 33% 26% 21% 18% 9% 6% 3% 15% Subjective urbanisation Rural village 42% 25% 21% 12% 10% 9% 2% 9% Small/mid size town 39% 26% 20% 14% 14% 6% 3% 10% Large town 32% 31% 21% 13% 12% 8% 3% 11% 52

54 5.2 The importance of qualifications and professional experience - Europeans continue to place high importance on professional experience and qualifications as key assets for employability - More than half of Europeans feel that the level of professional experience (54%) and one s qualifications (52%) are the two most important assets to emphasise in order to find a job easily today. 25 These two assets stand apart from the other options measured, and professional experience has increased from 51% in 2006 to 54% currently. QD6 In your opinion, which two assets should one emphasize in order to easily find a job today? (MAX. 2 ANSWERS) - %EU Professional experience Level of one s qualifications 54% 51% 52% 51% Ability to adapt Computer skills Language skills Willingness to work abroad None of these (SPONTANEOUS) Other (SPONTANEOUS) 6% 5% 1% 1% 2% 2% 2% 2% 19% 19% 17% 21% 34% 35% The 2009 national analysis reveals some interesting trends. The French place less importance on the level of one s qualifications (37%) and opt rather to emphasise professional experience (70%) as well as the ability to adapt (55%). Citizens in Malta and Cyprus follow a similar trend: both place considerable emphasis on the level of one s qualification (70% for both Cyprus and Malta), whilst just under half choose professional experience (46% and 45% for Malta and Cyprus respectively) but then post results higher than the EU average for computer skills (32% for Malta and 30% for Cyprus compared to the EU average of 19%). 25 QD6 In your opinion, which two assets should one emphasize in order to easily find a job today? (MAX. 2 ANSWERS) 53

55 Germany and the Netherlands also place the main emphasis on the level of one s qualifications, with more than two-thirds of citizens in these countries choosing this attribute. Although the Danish emphasise the level of one s qualification (56%), the ability to adapt is also important in this country, ranking second (53%). Looking at the country groupings, it is noted that, when comparing EU15 with NMS12, those in EU15 are more likely to emphasise professional experience (54%), the ability to adapt (36%) and computer skills (19%), whereas those in NMS12 are more likely to emphasise the level of one s qualifications (55%) and language skills (24%). 54

56 QD6 In your opinion, which two assets should one emphasize in order to easily find a job today? (MAX. 2 ANSWERS) Professional experience Level of one s qualifications Ability to adapt Computer skills Language skills Willingness to work abroad None of these (SPONTANEOUS) Other (SPONTANEOUS) EU27 54% 52% 34% 19% 17% 6% 1% 2% 2% BE 56% 57% 30% 16% 28% 4% 0% 1% 0% BG 53% 54% 17% 22% 25% 5% 1% 0% 5% CZ 58% 54% 35% 18% 21% 1% 1% 1% 1% 42% 56% 53% 21% 16% 4% 0% 1% 1% DE 42% 67% 34% 22% 17% 5% 0% 2% 1% EE 47% 50% 25% 18% 41% 4% 0% 3% 2% IE 44% 64% 37% 21% 10% 8% 1% 2% 2% EL 58% 54% 15% 29% 21% 4% 1% 5% 0% ES 67% 53% 26% 7% 13% 5% 1% 4% 2% FR 70% 37% 55% 9% 8% 11% 0% 1% 1% IT 51% 45% 27% 19% 22% 10% 2% 3% 1% CY 45% 70% 20% 30% 18% 2% 0% 7% 0% LV 48% 36% 34% 12% 33% 8% 3% 6% 1% LT 68% 61% 22% 13% 15% 2% 1% 2% 2% LU 44% 61% 31% 13% 33% 7% 0% 1% 1% HU 58% 48% 28% 15% 25% 4% 1% 4% 2% MT 46% 70% 22% 32% 7% 5% 1% 2% 1% NL 53% 67% 41% 15% 11% 2% 0% 3% 1% AT 58% 48% 31% 28% 16% 10% 1% 1% 1% PL 44% 55% 23% 15% 34% 5% 1% 2% 3% PT 64% 52% 23% 12% 7% 6% 2% 2% 3% RO 61% 64% 21% 14% 7% 3% 0% 2% 5% SI 53% 45% 30% 17% 26% 6% 3% 4% 1% SK 48% 42% 28% 24% 40% 7% 1% 1% 2% FI 56% 51% 46% 11% 22% 3% 0% 2% 2% SE 42% 54% 51% 20% 14% 4% 1% 5% 1% UK 50% 42% 41% 34% 10% 4% 1% 2% 2% HR 47% 45% 30% 26% 25% 5% 2% 2% 2% TR 42% 35% 15% 25% 32% 2% 4% 4% 10% MK 33% 36% 16% 35% 36% 8% 3% 6% 3% Highest percentage per item Highest percentage per country Lowest percentage per item Lowest percentage per country 55

57 Comparing the results at national level from 2006 to 2009 shows: The rise in overall mentions for professional experience is largely due to citizens in Malta, the Czech Republic, Cyprus and Romania who increased mentions of this asset by at least 10 percentage points QD6 In your opinion, which two assets should one emphasize in order to easily find a job today? (MAX. 2 ANSWERS) Answer 'professional experience' FR LT ES PT RO AT HU EL CZ FI BE EU27 SI NL BG IT UK SK LV EE MT CY PL LU IE SE DE % 71% 68% 65% 67% 61% 64% 62% 61% 51% 58% 55% 58% 54% 58% 58% 58% 47% 56% 59% 56% 49% 54% 51% 53% 48% 53% 55% 53% 53% 51% 50% 50% 49% 48% 47% 48% 50% 47% 46% 46% 34% 45% 35% 44% 41% 44% 39% 44% 47% 42% 40% 42% 39% 42% 37% 56

58 Belgians now place greater emphasis on the level of one s qualifications and professional experience at the expense of language skills and computer skills The British have increased their mentions of computer skills and decreased mentions of language skills Latvians have higher mentions particularly for the ability to adapt and to some extent the willingness to work abroad and record fewer mentions of level of one s qualifications On a socio-demographic level, we find: Men are more likely to emphasise professional experience compared to women. Women, on the other hand, are more likely to mention computer skills. The youngest age group is more likely to mention level of one s qualifications and language skills while those in the middle age groups (aged 25-54) place greater emphasis on professional experience and ability to adapt than their younger and older counterparts. Better educated people, and those who are still studying, emphasise the level of one s qualifications more. Better educated respondents also mention the ability to adapt more. Students see greater value in language skills. Managers place greater emphasis on the level of one s qualifications and the ability to adapt. Other white-collar workers and house persons are more likely to mention computer skills. Manual workers place greater emphasis on professional experience and the ability to adapt. Finally, students place emphasis on the level of one s qualifications and language skills. QD6 In your opinion, which two assets should one emphasize in order to easily find a job today? (MAX. 2 ANSWERS) Professional experience Level of one s qualifications Ability to adapt Computer skills Language skills Willingness to work abroad None of these (SPONTANEOUS ) Other (SPONTANEOUS ) EU27 54% 52% 34% 19% 17% 6% 1% 2% 2% Sex Male 58% 51% 35% 17% 16% 6% 1% 3% 1% Female 51% 53% 33% 20% 18% 6% 1% 2% 2% Age % 56% 30% 20% 24% 7% 1% 2% 1% % 50% 36% 17% 15% 5% 1% 3% 1% % 50% 38% 19% 14% 5% 1% 3% 1% % 53% 30% 19% 17% 7% 1% 2% 4% Education (End of) 15-53% 49% 31% 20% 14% 6% 2% 2% 4% % 49% 36% 20% 15% 5% 1% 2% 1% % 58% 38% 15% 17% 6% 0% 3% 1% Still studying 42% 60% 26% 21% 31% 8% 1% 2% 1% Respondent occupation scale Self- employed 57% 50% 36% 15% 16% 6% 2% 3% 1% Managers 54% 60% 42% 15% 16% 4% 0% 2% 0% Other white collars 59% 48% 35% 23% 16% 4% 1% 2% 0% Manual workers 62% 48% 40% 16% 13% 6% 1% 2% 1% House persons 49% 54% 26% 23% 18% 7% 1% 3% 3% Unemployed 58% 44% 31% 18% 14% 7% 2% 4% 2% Retired 49% 54% 30% 19% 17% 6% 1% 2% 4% Students 42% 60% 26% 21% 31% 8% 1% 2% 1% 57

59 6. TRAINING In this section, respondents were asked whether they had participated in training in the past 12 months. Workers then self-assess their level of education and training; whether it is sufficient in order to keep their job, and non-workers are asked a similar question in the context of them finding a job soon. Analysis then turns to the perceived obstacles among those who would like to have training, but feel they can t access it, and find that most people feel affordability is the main barrier to further education or training. This is placed in context when assessing, amongst those who have received training, how the training was funded. 6.1 Participation in training in the past 12 months - Around one in five of those sampled have recently participated in training courses - Just over one in five respondents (22%) have participated in training course in the past 12 months 26, a figure that has declined from 24% in On this measure, Sweden stands out as more than half of the respondents from the country had participated in training recently (55%). This is followed by Finland (42%), the Netherlands (38%), Denmark (33%) and the UK (30%). Countries where fewer respondents have recently received training include Greece (6%), Bulgaria (8%), and Italy (11%). Looking at the country groupings, the highest levels of training can therefore be found in Finland, Austria and Sweden (41%), and a higher incidence in the EU15 (24%) when compared to NMS12 (17%). 26 QD9. During the last 12 months, have you participated in any training courses? 58

60 Comparing the results with the 2006 Eurobarometer, on a country level, shows that the following countries indicate higher levels of training: Luxembourg (22% to 28%), Spain (16% to 20%), Germany (23% to 26%) and Romania (10% to 13%). However, in most countries, fewer respondents have received training particularly in Belgium (30% to 21%), Cyprus (18% to 12%), the UK (34% to 30%), Greece (10% to 6%) and the Netherlands (42% to 38%). Item was not previously asked for MK EB71.2 May-Jun 2009 / EB65.3 Apr-May

61 The socio-demographic analysis shows: Men are more likely to have received training than women. Those in the middle age groups (age 25-54) are more likely to have received training. People who are better educated are more likely to have received training. Managers are most likely to have received training, and in fact, more managers have received training than not. As expected, pensioners and house persons are the least likely to have received training. In general, people who are optimistic about the national situation of employment, the national economy and their household s financial situation are more likely to have received training. Interestingly, there is no difference in the incidence of training amongst those who have lost their jobs due to the economic crisis, and those who haven t, though those who are concerned about losing their jobs, and are not confident about their job stability, are less likely to have received training. 60

62 QD9 During the last 12 months, have you participated in any training courses? Yes No EU27 22% 77% 1% Sex Male 24% 75% 1% Female 20% 78% 2% Age % 73% 2% % 67% 1% % 69% 1% % 91% 2% Education (End of) 15-6% 93% 1% % 77% 1% % 61% 1% Still studying 21% 76% 3% Respondent occupation scale Self- employed 26% 73% 1% Managers 58% 42% - Other white collars 35% 64% 1% Manual workers 29% 70% 1% House persons 6% 92% 2% Unemployed 18% 82% - Retired 3% 95% 2% Students 21% 76% 3% Nat. situation of employment Good 30% 68% 2% Bad 21% 78% 1% Situation of national economy Good 29% 69% 2% Bad 21% 78% 1% Financial situation household Good 27% 72% 1% Bad 14% 84% 2% Has lost his job Yes 23% 77% - No 22% 76% 2% Concerned about losing job No 38% 61% 1% A bit 28% 71% 1% Yes 24% 75% 1% Job stability Confident 40% 60% - Not confident 19% 79% 2% 61