Special Eurobarometer 418 SOCIAL CLIMATE REPORT

|

|

|

- Cameron Smith

- 5 years ago

- Views:

Transcription

1 Special Eurobarometer 418 SOCIAL CLIMATE REPORT Fieldwork: June 2014 Publication: November 2014 This survey has been requested by the European Commission, Directorate-General for Employment, Social Affairs and Inclusion and co-ordinated by Directorate-General for Communication. This document does not represent the point of view of the European Commission. The interpretations and opinions contained in it are solely those of the authors. Special Eurobarometer 418 / Wave EB81.5 TNS Opinion & Social

2 Project title Special Eurobarometer Social climate Linguistic Version Catalogue Number EN KE EN-N ISBN DOI /54999 European Union, 2014

3 Special Eurobarometer 418 Social climate Conducted by TNS opinion & social at the request of the Directorate-General for Employment, Social Affairs and Inclusion Survey co-ordinated by the Directorate-General for Communication

4 TABLE OF CONTENTS INTRODUCTION... 2 EXECUTIVE SUMMARY... 4 I. SOCIAL CLIMATE INDEX... 8 II. CURRENT SITUATION Personal situation Country Social protection and inclusion III. EXPECTATIONS FOR THE NEXT 12 MONTHS Personal situation Country Social protection and inclusion IV. CHANGES IN THE LAST 5 YEARS Personal situation Country Social protection and inclusion GENERAL CONCLUSIONS ANNEXES Technical specifications Questionnaire Tables 1

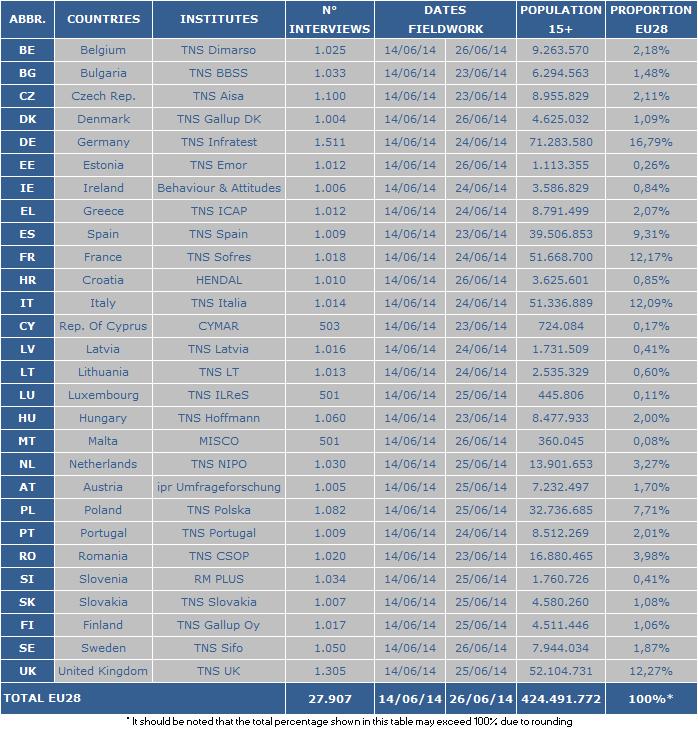

5 INTRODUCTION This report presents the results of the sixth in a series of Eurobarometer surveys undertaken with the overall objective of providing an up-to-date picture of European citizens perceptions of the current social climate. It examines their views on 15 separate aspects relating to personal circumstances, the national picture and social protection and inclusion. How do Europeans judge the present situation, how does it compare with five years ago and what are their expectations over the next 12 months will things improve, worsen or remain the same? The first in this series of surveys was conducted in June , eight months after the financial and economic crisis within Europe began. By June 2010, when the second wave of the survey was conducted 2, whilst there were signs of improvement in some Member States, the overall position was still one of economic difficulty. Twelve months later, when the third wave was conducted in June , there had been further improvement in the situation with an increase in EU27 Gross Domestic Product (GDP) and a fall in unemployment. However, by the end of 2011, the European debt crisis had worsened, with Greece, Italy, Ireland, Spain and Portugal receiving a financial bail-out. By June 2012, when the fourth wave of the survey was conducted 4, there were signs of a possible recovery, with first quarter GDP stabilizing after negative growth in the fourth quarter of Since June 2013 (when the last survey was conducted), and to set the context for this latest wave of research, signs of an economic recovery have continued although it is still modest. That said, the economic situation and the recovery within the EU remain fragile and large disparities continue across Member States underpinned by structural challenges, financing costs and public finances sustainability. The latest wave of the Social Climate survey was carried out by TNS opinion & social network in the 28 Member States of the European Union between the 14 th and 27 th June It evaluates Europeans current perceptions of their own situation and that of their country. Some respondents from different social and demographic groups were interviewed face-to-face at home on behalf of Directorate-General for Employment, Social Affairs & Inclusion. The methodology used is that of Eurobarometer surveys as carried out by the DG for Communication ( Strategy, Corporate Communication Actions and Eurobarometer Unit) 5.. A technical note on the manner in which interviews were conducted by the Institutes within the TNS opinion & social network is appended as an annex to this report. Also included are the interview methods and confidence intervals The results tables are included in the annex. 2

6 The findings of the survey have been analysed firstly at EU level and secondly by country. At an EU level the results are based on the 28 Member States. Some of the results have also been compared with the five previous waves of the survey conducted in 2013, 2012, 2011, 2010 and , and some have been compared with the previous wave of research in Where appropriate a range of socio-demographic variables respondents age, terminal education age, occupation and ability to pay household bills - have been used to provide further analysis. Note: In this report, countries are referred to by their official abbreviation. The abbreviations used in this report correspond to: ABBREVIATIONS BE Belgium LT Lithuania BG Bulgaria LU Luxembourg CZ Czech Republic HU Hungary DK Denmark MT Malta DE Germany NL The Netherlands EE Estonia AT Austria IE Ireland PL Poland EL Greece PT Portugal ES Spain RO Romania FR France SI Slovenia HR Croatia SK Slovakia IT Italy FI Finland CY Republic of Cyprus*** SE Sweden LV Latvia UK The United Kingdom EU28 EU15 NMS13 EURO AREA European Union 28 Member States BE, IT, FR, DE, LU, NL, DK, UK, IE, PT, ES, EL, AT, SE, FI* BG, CZ, EE, HR, CY, LT, LV, MT, HU, PL, RO, SI, SK** BE, FR, IT, LU, DE, AT, ES, PT, IE, NL, FI, EL, EE, SI, CY, MT, SK, LV * EU15 refers to the 15 countries forming the European Union before the enlargements of 2004, 2007 and 2013 ** The NMS13 are the 13 new Member States which joined the European Union during the 2004, 2007 and 2013 enlargements *** Cyprus as a whole is one of the 28 European Union Member States. However, the acquis communautaire has been suspended in the part of the country which is not controlled by the government of the Republic of Cyprus. For practical reasons, only the interviews carried out in the part of the country controlled by the government of the Republic of Cyprus are included in the CY category and in the EU28 average. * * * * * We wish to thank the people throughout Europe who have given their time to take part in this survey. Without their active participation, this study would not have been possible. 7 At an EU level previous waves of the survey are based on 27 Member States. Croatia joined the EU on the 1 st July 2013, after fieldwork for the 2013 survey was conducted. 3

7 EXECUTIVE SUMMARY Europeans are divided in their overall perception of the current situation. The EU social climate index, which takes into account views on personal circumstances, the national picture and social protection and inclusion, is -1 in It is slightly lower than the 2013 index (-0.9), and is the lowest index recorded in the series. At a national level the social climate index ranges from a high of 3.1 (in Malta) to a low of -5.3 (in Greece). The most positive perceptions are found in the Benelux and Nordic countries, along with Malta, Austria and Germany. The Member States with a positive index are Malta (3.1), Denmark (2.9), Luxembourg and the Netherlands (both 2.2), Austria (1.8), Sweden (1.7), Germany (1.6), Finland (1.3), Belgium (0.6), the UK and Estonia (both 0.1). With the exception of Estonia, these Member States have formed the top ten in the overall social climate index in each of the six years of the survey 8. Estonia has ranked in the top ten in three of the six surveys: 2010, 2011 and Only four of these eleven Member States show an improvement in the social climate index since 2013: Malta (up 2.1 points), Estonia (up 0.6 points), the Netherlands (up 0.3 points) and Denmark (up 0.1). The largest decline in the social climate index can be observed in Sweden (down 0.6 points) followed by Belgium (down 0.5), Luxembourg (down 0.4), Austria, Germany and the UK (all down by 0.3 points), and Finland (down 0.2). Compared with the 2009 indices, six of these eleven Member States show an improvement, with the most notable in Malta (up 3.3 points), followed by Germany (up 1.3), Estonia (up 0.5), Austria (up 0.2) and Denmark and the UK (both up 0.1 point). The largest decline in the index can be seen in Belgium and in the Netherlands (both down 0.4 points) followed by Luxembourg, Sweden and Finland (all down 0.1 point). The least positive perceptions can be seen in southern and eastern Member States. Greece is the lowest ranked Member State with an index of -5.3, followed by Bulgaria (-3.6), Romania and Cyprus (both -3.4), Croatia (-3.3), Italy (-3), Portugal (-2.6), Hungary (-2.3), Spain (-2.2) and Slovakia (-2.1). Greece has been the lowest ranked Member State on this overall measure in five of the six years, the exception being 2010, when it ranked ahead of Romania. 8 Including countries ranked equal tenth in any survey year 4

8 The social climate index has dropped in three of these ten Member States since 2013, with the most marked decline in Bulgaria (down 0.3 points), and followed by Slovakia and Italy (both down 0.1). The index in Cyprus remains unchanged, with the largest improvement in the social climate index in Portugal (up 0.8 points) followed by Romania (up 0.6), Spain (up 0.5), Croatia (up 0.2) and Hungary and Greece (both up 0.1 points). Compared with the 2009 indices only one Member State has improved - Hungary (up 1.4). The only other Member States with a positive shift in their social climate index since 2013 are Ireland up 0.4 points (to -0.9); Lithuania up 0.2 points (to -1.4); Poland up 0.2 points (to -1.8); and Slovenia up 0.1 point (to -1.9). Respondents who say that they almost always struggle to pay their household bills have an overall social climate index of -4.1, compared with an index of -2.2 for those who struggle from time to time and a positive index of 0.2 for those who almost never have difficulty paying their household bills. The index for those who struggle to pay bills from time to time (down 0.2 points) and for those who almost never have difficulty paying their bills (down 0.1 point) has slightly worsened since The indices for these two groups are now at their lowest level in the series. Respondents who are unemployed have a lower overall social climate index (-3.3) than all other occupational groups, while those in managerial jobs have the highest index (0.6). Managers are the only occupational group with a positive score. Europeans hold more positive perceptions about their personal situation than they do about national indicators. In terms of their personal situation, they are most positive about the area in which they live (4.3) and their life in general (2.5), and somewhat less positive about their personal job situation (1.2) and the financial situation of their household (0.8). In terms of their perceptions of measures associated with social protection and inclusion, Europeans have a positive index on the healthcare system (1) and are divided in their opinions about the relations between people from different cultural and religious backgrounds or nationalities (0). They are less satisfied with unemployment benefits (-1.4) and the pension system (-1.7), and even less so about the way inequalities and poverty are addressed in their country (-3). Europeans are least positive about national indicators, notably those that most immediately affect their own economic situation: the employment situation (-4.1), the affordability of housing (-3.3), the cost of living (-2.9), their national economy (-2.6), and the affordability of energy (-2.5). They are somewhat less negative about the way in which public administration runs (-1.7). The indices for eight of the 15 measures have declined from their 2013 levels by between 0.1 and 0.6 points, with two remaining the same and five increasing by between 0.1 and 0.9 points. 5

9 The five measures where indices have improved are: the economy up 0.9 points; local area up 0.4 points; the cost of living and unemployment benefits both up 0.2 points; and the national employment situation up 0.1 point. The indices for personal job situation and energy affordability remain unchanged. On the remaining eight measures, the most notable drops in opinion can be seen for the way in which poverty and inequalities are addressed (down 0.6 points); life in general and the affordability of housing (both down 0.4 points); and relations between people from different cultural or religious backgrounds or nationalities (down 0.3). The majority of Europeans expect no change to their personal situation in the next 12 months in relation to their local area (75%), their life in general (59%), and their job situation (60%) and household finances (61%). Those who expect change are a little more likely to think things will improve than that they will get worse. In relation to the six national indicators, the only measure where a majority of Europeans expect no change in the next 12 months is in the way public administration is run (59%). Across all six indicators those who expect change are more likely to think things will become worse rather than improve: slightly more likely in relation to the national economy and employment situation, and much more likely in relation to the cost of living, housing affordability and energy affordability. On four out of the five social protection and inclusion indicators, the majority of Europeans expect the situation to remain unchanged in the next 12 months: the national healthcare system (57%), relations between people from different cultural or religious backgrounds or nationalities (56%), the way inequalities and poverty are addressed (53%) and unemployment benefits (51%). Just under half of Europeans expect no change to pension system (49%). Across all five measures those who expect change are much more likely to think things will worsen than improve. Europeans hold a more optimistic outlook than they did in 2013 with a positive shift in the net balance of opinion 9 across each of the 15 indicators, most marked in relation to their expectations with regard to the economy and national employment situation, followed by the cost of living, pension system and unemployment benefits. 9 The difference between the proportion who say things will improve and the proportion who say they will get worse 6

10 On the measures relating to respondents personal circumstances, Europeans are most likely to think that their situation is similar to five years ago in terms of the area in which they live (60%) and their personal job situation (47%). In terms of the household financial situation and life in general opinion is more evenly divided between those who think the situation is unchanged and those who think it has got worse: 42% vs. 38% on household financial situation and 40% vs. 33% on general life. Where respondents do perceive things to have changed they are more likely to say that they have got worse than that they have improved in relation to: household finances (38% vs. 17%); personal job situation (26% vs. 17%) and general life (33% vs. 26%). Opinion is evenly divided on changes in the local area (18% vs. 19%). Europeans widely perceive the national situation to have deteriorated when compared with five years ago across five of the six national indicators, with most thinking the situation is worse in terms of the cost of living (74%), the affordability of energy (63%) and of housing (62%), the national employment situation (60%) and the national economy (57%). A large minority (38%) think the way public administration is run has got worse. On the five social protection and inclusion indicators, only a minority of Europeans perceive the situation is the same as it was five years ago. The majority of Europeans think that pension system is worse (52%), just under half perceive the situation has become worse in relation to the healthcare system (46%) and the way their country addresses inequalities and poverty (46%) and a slightly smaller proportion (43%) think that unemployment benefits are worse. The only measure where Europeans are more likely to say the situation remains unchanged than it has worsened is relations between people from different cultural or religious backgrounds or nationalities (44% unchanged vs. 37% got worse). Europeans are now somewhat more positive about the current situation relative to five years ago than they were in There has been a positive shift in the net balance of opinion on each of the 15 indicators, albeit in most cases relatively small. The largest positive shifts in opinion are in relation to the economy and the national employment situation. 7

11 I. SOCIAL CLIMATE INDEX This first chapter of the report provides an overview of the current social climate in the EU and how this compares to perceptions held over the last five years. The chapter examines Europeans overall perceptions of the current situation, taking into account their views on personal circumstances, the national picture and areas relating to social protection and inclusion, and summarising these opinions into a single overall score. The overall score is based on the results of two questions. The first of these asks respondents how satisfied they are, on the whole, with the life they lead, with answers given on a four point scale from very satisfied to not at all satisfied 10. The second question asks respondents to judge the current situation in relation to fourteen different areas covering both their personal circumstances and social and economic factors within their country. Responses are invited on a four-point scale ranging from very good to very bad 11. In order to calculate the overall social climate index, each measure is allocated a score between -10 and 10, as shown below: Q1: Satisfaction with the life you lead Q2: Judgement of current situation in 14 areas Very satisfied 10 Very good 10 Fairly satisfied 3.33 Rather good 3.33 Not very satisfied Rather bad Not at all satisfied -10 Very bad -10 Don t know Not scored Don t know Not scored The overall social climate index for each respondent is then calculated as the mean of the scores for each of the 15 measures (one at Q1 and fourteen at Q2). The following table shows the social climate index for the EU as a whole, and for each of the 28 Member States for the latest wave (SP418), for each of the 27 Member States and Croatia for the previous wave (SP408), and for the 27 Member States for the first four waves: SP315 (2009), SP349 (2010), SP370 (2011) and SP391 (2012). 10 Q1 On the whole, are you very satisfied, fairly satisfied, not very satisfied or not at all satisfied with the life you lead? (READ OUT) Very satisfied, Fairly satisfied, Not very satisfied, Not at all satisfied, Don t know 11 Q2 How would you judge the current situation in each of the following? (SHOW CARD WITH SCALE ONE ANSWER PER LINE) (READ OUT) The area you live in, the healthcare system in (OUR COUNTRY), The pension system in (OUR COUNTRY), Unemployment benefits in (OUR COUNTRY), The cost of living in (OUR COUNTRY), Relations in (OUR COUNTRY) between people from different cultural or religious backgrounds or nationalities, The way inequalities and poverty are addressed in (OUR COUNTRY), How affordable energy is in (OUR COUNTRY), How affordable housing is in (OUR COUNTRY), The way public administration runs in (OUR COUNTRY), The situation of the (NATIONALITY) economy, Your personal job situation, The financial situation of your household, The employment situation in (OUR COUNTRY)? Very good, Rather good, Rather bad, Very bad, Don t know 8

12 315 (2009) OVERALL SOCIAL CLIMATE INDEX (Evaluation of the current situation) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU MT DK LU NL AT SE DE FI BE UK EE CZ IE FR LT LV PL SI SK ES HU PT IT HR CY RO BG EL The overall social climate index for the EU28 is stands at -1 in 2014 which indicates that Europeans are divided in their assessments of the current situation. This represents a small decline from a score of -0.9 in 2013, and is the lowest index recorded in the series. 9

13 That said, the 2014 index is only somewhat lower than the highest index (-0.6) recorded in As in previous years the index varies considerably between countries. The highest indices are found in the Nordic and Benelux countries, along with Malta, Austria and Germany. Malta has the highest index (3.1), followed Denmark (2.9), Luxembourg and the Netherlands (both 2.2), Austria (1.8), Sweden (1.7), Germany (1.6), Finland (1.3) and Belgium (0.6). The UK and Estonia are the only other Member States with a positive index, although it is only marginally so in both: UK (0.1); and Estonia (0.1). With the exception of Estonia, these Member States have formed the top ten in the overall social climate index in each of the six years of the survey 12. Estonia has ranked in the top ten in three of the six surveys: 2010, 2011 and The overall social climate index has declined in seven of these Member States since 2013, and improved in four (Malta, Denmark, the Netherlands and Estonia). The biggest improvement can be observed in Malta (up 2.1 points) and the shift is notably greater than positive shifts in any other Member States. It is the most significant improvement for Malta in the series, with smaller positive shifts between 2009 and 2010, and 2011 and 2012 (up 0.4 points in each case), and between 2012 and 2013 (up 0.9 points). In the 2010 to 2011 period the index in Malta declined by 0.5 points. As a result of this large positive shift in 2014 Malta now holds its highest index to date, and has risen from ranking ninth in 2013 to ranking first in Estonia shows the second biggest improvement (up 0.6 points). Like Malta, it is also its most significant improvement in the series, with a somewhat smaller positive shift between 2009 and 2010 (up 0.4 points), and declines in the following periods, most notable between 2010 and 2011 (down 0.3 points). The improvement in 2014 has resulted in Estonia rising from eleventh in the rankings in 2013 to tenth in the rankings, a position it shares jointly with the UK. This is its highest ranking in the series, and a position it also held in 2010 (jointly with the UK) and in The most notable decline in these eleven Member States since 2013 is witnessed in Sweden (down 0.6 points). It is its most significant decline in the series, with smaller negative shifts between 2010 and 2011 (down 0.1 point) and 2012 and 2013 (down 0.3 points). In the periods between 2009 and 2010, and 2011 and 2012 the index in Sweden improved (up 0.5 points and 0.4 points respectively). The decline since 2013 sees Sweden drop from third in the rankings in 2013 to sixth in 2014, with its worst index (albeit marginally lower than that in 2009) and lowest ranking in the series. 12 Including countries ranked equal tenth in any survey year 10

14 In addition to Sweden, four other top ten Member States have an overall social climate index in 2014 lower than that in The greatest declines can be seen in the Netherlands which, in spite of a small improvement since 2013 (up 0.3 points), shows a drop (down 0.4 points) from 2.6 in 2009 to 2.2 in 2014; and in Belgium, with a decline (down 0.4 points) from 1 to 0.6 respectively. Luxembourg and Finland, like Sweden, show marginal declines (down 0.1 point in each case), with a drop from 2.3 to 2.2 in Luxembourg and 1.4 to 1.3 in Finland. The largest improvement in the top ten Member States since 2009 can be seen in Malta (up 3.3 points), with a notably greater positive shift than in any other Member State, followed by Germany (up 1.3 points) and Estonia (up 0.5 points). The bottom ten i.e. lowest ranked countries on this measure are southern and eastern European countries. Greece is the lowest ranked country with an index of -5.3, followed by Bulgaria (-3.6), Romania and Cyprus (both -3.4), Croatia (-3.3), Italy (-3), Portugal (-2.6), Hungary (-2.3), Spain (-2.2) and Slovakia (-2.1). The overall social climate index has declined in three of these Member States since 2013, improved in six (Spain, Hungary, Portugal, Croatia, Romania and Greece), and remains unchanged in Cyprus. Greece has been the lowest ranked Member State on this overall measure in five of the six survey years, the exception being in 2010, when it was ranked ahead of Romania. The index in Greece has improved marginally since 2013 (up 0.1 point), after a greater increase in 2013 (up 0.4 points) and declines in each of the previous survey years since 2009, with the most marked decline between 2012 and 2011 (down 1.2 points). The recent improvements in the last two survey periods are a reflection perhaps of cautious optimism now about the economy s prospects, although the 2014 index is still lower than the indices between 2009 and Among these lowest ranked countries, Portugal and Spain are the only other southern European countries experiencing particularly difficult economic circumstances 13 which show an improvement in the social climate index since In Portugal it has increased by 0.8 points, from -3.4 in 2013 to -2.6 in 2014, following declines in all but one of the survey periods (2011) since Nevertheless, in ranking terms the improvement has only seen Portugal move up from twenty-fourth position in 2013 (shared jointly with Cyprus) to twenty-second position in 2014, lower than its highest ranking of twenty-first in 2011 and similar to its ranking in In Spain the social climate index has increased by 0.5 points, from -2.7 in 2013 to -2.2 in 2014, following one of the largest declines of any Member State between 2013 and 2012 (down 0.6 points) 14 ; broadly similar declines between 2011 and 2012 (down 0.5 points) and 2010 and 2011 (down 0.7); and a marginal increase between 2009 and 2010 (up 0.1). 13 The countries included here are Spain, Portugal, Italy, Cyprus and Greece 14 The Netherlands showed the largest decline, down 0.9 points and Slovenia showed a similar level of decline to Spain down 0.6 points 11

15 In ranking terms, the recent improvement has only seen Spain move up one position, from twenty-first in 2013 to twentieth in 2014, lower than its sixteenth position in the first three waves of the series 15 and eighteenth position in None of the southern European countries in the bottom ten show an improvement in the social climate index since With the exception of Portugal, all show a deterioration of at least one point, with the greatest decline in Cyprus (down 2.7 points) from -0.7 in 2009 to -3.4 in 2014, followed by Greece (down 1.5 points) from -3.8 to -5.3; Spain, (down 1.2 points) from -1 to -2.2; and Italy (down 1.1 point) from -1.9 to -3. Portugal shows only a small decline (down 0.3 points) from -2.3 in 2009 to -2.6 in Among the eastern and central European Member States in these lowest ranked countries 16, the biggest decline since 2013 is observed in Bulgaria (down 0.3 points) from an index of -3.3 to -3.6 in 2014, following a broadly similar drop between 2012 and 2013 (down 0.4 points), after a consistent pattern of improvement since 2009, albeit marginal since Bulgaria s 2014 index is similar to its baseline index of -3.6, both being the lowest in the series. The largest improvement since 2013 can be seen in Romania (up 0.6 points) from -4 to - 3.4, following a small decline in its index between 2012 and 2013 (down 0.2 points), increases between the 2010 and 2011, and 2011 and 2012 periods (up 0.1 point and 0.6 points respectively), and a decline between the baseline survey and 2010 (down 2.1 points). In ranking terms, Romania has moved up from twenty-seventh position in 2013 to equal twenty-fifth in , lower than its baseline ranking of twenty-third, when it was at its highest position in the series. In addition to Romania, Slovakia is the only other eastern European country in this group showing a deterioration in the social climate index since 2009 (down 0.5 points) from -1.6 to Bulgaria s index, as already noted, shows no change since 2009, with Hungary the only country in the group showing an improvement since 2009, (up 1.4 points) from -3.7 to This is driven by a marked improvement in the social climate index between 2012 and 2013 (up 1.4 points), with only a marginal improvement (up 0.1 points) between 2013 and 2014, a slightly greater improvement between 2009 and 2010 (up 0.3 points), and small declines between the 2010 and 2011, and 2011 and 2012 survey periods (down 0.2 points in each). In ranking terms, Hungary has moved up from a baseline ranking of twenty-sixth to twenty-first position in 2014, lower than its twentieth ranking in 2013, the highest in the series. Among the remaining seven Member States (those not ranked in the top ten or bottom ten ) there has been an improvement in the overall social climate index since 2013 in Ireland, Lithuania, Poland and Slovenia. Most increases are small, with the most notable in Ireland, (up 0.4 points) from -1.3 in 2013 to -0.9 in Ireland and Lithuania show the most notable improvement in their social climate indices since 2009 (Lithuania up 1.1 points and Ireland up 0.9). 15 In 2010 jointly shared with Slovenia, and in 2011 jointly shared with Ireland 16 The countries included here are Slovakia, Hungary, Romania and Bulgaria 17 A position it shares with Cyprus 12

16 The next table shows how the overall social climate index varies by socio-demographic characteristics at the overall EU level, again showing the results for each of the six survey years. 13

17 As has been found in previous surveys in the series, the most notable socio-demographic differences are related to employment status and economic circumstances as measured by people s perceptions of their difficulty in paying bills. There is a strong relationship between how difficult people say they are finding it to pay their household bills and their overall social climate index. Thus those who say that they almost never find it difficult to pay their bills have a positive index in 2014 of 0.2, compared with an index of -2.2 for those who struggle some of the time, and -4.1 for those who almost always have difficulty paying household bills. Perceptions among each of the three groups remain very similar to the views held in There has been a marginal improvement in perceptions among those who struggle most of the time, up 0.1 point from -4.2, its lowest level in the series, but the index remains at its second lowest level, down 1.1 points on the index of -3 in There has been a small deterioration between 2013 and 2014 in perceptions among those who almost never struggle to pay household bills (down 0.1 point), and the index is now at its lowest level in the series, down 0.3 points on the highest score recorded in There has also been a small deterioration between 2013 and 2014 in perceptions among those who struggle to pay household bills from time to time (down 0.2 points). The index for this group is also at its lowest level in the series, down 0.6 points from the highest score of -1.6 recorded in In terms of employment status, the most marked difference is between the perceptions of the unemployed and all other occupational groups. Those who are unemployed have an overall social climate index of -3.3 in 2014, compared with the EU average of -1. There has been a small deterioration between 2013 and 2014 (down 0.2 points), and the index is now at its lowest level in the series, down 0.4 points on the baseline index of -2.9 in House persons have a somewhat lower index (-2.1) than all other groups with the exception of the unemployed. The index for house persons shows a small deterioration on the 2013 index (down 0.2 points) and is the lowest score in the series, 1.2 points below the highest index of -0.9 recorded in Managers have the highest index (0.6, down from 0.8 in 2013). They are the only occupational group with a positive score. Perceptions are broadly similar across the four age groups, although those aged and those aged 55+, both of whom have an index of -0.8 in 2014, are slightly more positive than year olds (-1) and year olds (-1.2). This reflects the findings in earlier surveys where younger people have been the most positive group and those aged 55+ have tended to be slightly more positive than the middle age groups. Among year olds, perceptions are more negative than in 2013, with the social climate index declining from -0.4 to This follows an increase between 2012 and 2013, but otherwise reflects a generally downward trend among young people from the benchmark index of -0.1 in The current index of -0.8 is at its lowest level in the series. There has been a smaller decline in the index for year olds, from -1 in 2013 to -1.2 in Again, the index for this group is now at its lowest level in the series, down 0.4 points from the index of -0.8 in recorded in each of the first three surveys. 14

18 The index of -1 for year olds is unchanged since 2013 and remains at a similar level to the 2009 baseline (-0.9). The slight increase in the index among those aged 55+, from -0.9 in 2013 to -0.8 in 2014, brings it into line with the index for those aged However, the index is still somewhat lower than in 2009 (-0.5). In terms of gender, men (-0.7) have a higher index than women (-1.3), a consistent pattern since The index for men has improved slightly since 2013 (up 0.1 point), although it remains at a somewhat lower level than the highest index of -0.5 recorded in each of the first three surveys. The index for women has declined since 2013 (down 0.3 points) and is now at its lowest level in the series, down 0.5 points on the highest index (also recorded in the first three surveys). In terms of age of leaving full-time education, those still studying have the highest index (-0.1), closely followed by those who left education at the age of 20 or older (-0.2); those who left aged 15 or younger have the lowest index (-2). The index has declined since 2013 among those leaving education aged (down 0.3 points) and, albeit marginally, among those leaving at the age of 20 or older (down 0.1 point). It has also declined among those who are still studying (down 0.3 points), but has improved among those leaving aged 15 or under (up 0.3 points). These shifts in the indices mean that the only groups with a 2014 index that is not its lowest in the series are students and people who left education aged 15 or under. 15

19 II. CURRENT SITUATION Having explored Europeans overall perceptions of the social climate, this chapter of the report looks at the different measures that feed into their overall perception. These are examined in three sections; the first examines four factors related to people s personal situation, the second six (primarily economic) factors related to the national situation in their country and the third five factors related to social protection and social inclusion. 1. PERSONAL SITUATION This section focuses on people s current perceptions of their personal situation in four areas: their life in general; the area in which they live; their personal job situation; and the financial situation of their household. The results are reported as indices following the method outlined in Chapter I. Each of the four aspects of people s personal situation is examined in turn for the EU as a whole, and for each of the 28 Member States for the latest wave, for the EU27 as a whole and for each of the Member States and Croatia for the previous wave, and for the EU27 overall and the 27 Member States across the first four waves. 16

20 The table below summarises people s satisfaction with their life in general. 315 (2009) Your life in general (Evaluation of the current situation) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU DK NL SE MT LU FI UK IE AT DE BE SI CY CZ FR PL ES EE SK LT HR LV HU IT RO PT BG EL

21 Europeans overall evaluation of their life in general is positive, although not overwhelmingly so. This has been the pattern in each of the six survey waves. The index of 2.5 in 2014 has decreased by 0.4 points from It is the lowest in the series, and shows a decline of 1 point from the high of 3.5 in The score of 2.5 is, however, the second highest EU level index across the 15 survey measures. As in previous years the index varies considerably between countries. The highest indices are found in the Nordic countries and Benelux states (with the exception of Belgium 18 ), along with Malta, the UK, Ireland, Austria and Germany. Denmark continues to have the highest index (7.9), as it has done for the five previous years, followed by the Netherlands (6.2), Sweden (6), Malta (5.3), and Luxembourg and Finland (both 5). There are only five Member States where the net perception is negative, with Greece recording the lowest index (-2.7), followed by Bulgaria (-2.1), Portugal (-1), Romania (-0.3) and Italy (-0.2). Comparing the results at a national level with those from 2013, nine Member States 19 show a year-on-year improvement in terms of people s satisfaction with their life as a whole, the index remains unchanged in Denmark, the Netherlands and Cyprus, and the remaining sixteen Member States show a decline. The largest increase is noted in Hungary (up 1.1 point), followed by Malta (up 1), Austria and Ireland (both up 0.8) and Romania and Portugal (both up 0.7 points). In ranking terms, Malta shows the greatest improvement of any Member State rising from ninth position in 2013 to fourth position in Hungary and Malta have seen the largest increases of all EU Member States over the whole survey period, both up 1.4 points from 3.9 in 2009 to 5.3 in 2014 in Malta, and from -0.8 to 0.6 respectively in Hungary. The largest declines since 2013 can be seen in Italy (down 1 point), France (down 0.9), Germany (down 0.8), Luxembourg (down 0.7) and Belgium (down 0.6). Across the period, the largest overall declines can be observed in Cyprus and Greece (both down 2.1 points from 4.6 to 2.5 in Cyprus and from -0.6 to -2.7 in Greece), followed by Italy (from 1.6 to -0.2), Portugal (from 0.5 to -1), France (from 3.4 to 2.2) and Belgium (from 4.9 to 3.8). 18 Belgium sits just outside the top ten countries (ranked eleventh) with an index of Malta, Austria, Ireland, Estonia, Slovakia, Hungary, Romania, Portugal and Bulgaria 18

22 The graph below illustrates long term trends in the overall EU index score for satisfaction with life in general. Whilst the results in 2013 suggested possible signs of recovery with a small uplift after the slump in 2012, which saw the index drop from its highest level (3.5) in June to its second lowest level in the series (2.7) 21, this has not continued in The index now stands at 2.5, down 0.4 points on 2013, and at its lowest level in the series, also recorded in January-February 2009 in the depths of the economic crisis. 20 Also recorded in Autumn 2001 and Autumn Also recorded in Autumn 2008 and Spring

23 The next table below shows how people rate the area in which they live. 315 (2009) The area you live in (Evaluation of the current situation) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU SE AT LU NL IE MT FI DE DK BE UK FR LT EE ES CZ SI CY PL LV PT SK RO HU HR EL IT BG

24 Europeans overall evaluation of the area in which they live is positive, more so than their satisfaction with life in general, and is the highest EU level index across all of the 15 survey measures. The index of 4.3 has increased by 0.4 points since It is marginally higher than the indices in and just below (by 0.1 point) the high of 4.4 in The highest indices are again found in the Nordic countries and, on this measure, all the Benelux states, along with Austria, Ireland, Malta, Germany and the UK. Respondents in Sweden, as in each of the five earlier waves, have the most positive perceptions of the area they live in, with an index in 2014 of 7.4, followed by Austria (6.7), Luxembourg (6.6), the Netherlands (6.5), Ireland (6.3), Malta (6.2), Finland (5.7), Germany and Denmark (both 5.3), Belgium (5.2) and the UK (5.1). No country has a net negative perception of the area in which people live. Respondents in Bulgaria are the most divided with an index of 0.9. After Bulgaria, the countries that have the least positive perceptions are Italy (2), Greece (2.4), Croatia (2.5), and Hungary and Romania (both 2.9). Comparing the results at a national level with those from previous waves, twenty-three Member States show a year-on-year improvement between 2013 and 2014 in terms of people s perception of the area in which they live; the UK shows no change; and the remaining four 22 show a decline. The biggest improvements are noted in Malta, up 1.9 points, after a smaller increase of 0.6 points in 2013, to a six-year high index of 6.2; in Greece, up 1.8 points, after a smaller increase of 0.6 points in 2013, to a six-year high of 2.4; Austria, up 1.6 points, after a small decline of 0.1 points in 2013, to a six-year high of 6.7; Spain, also up 1.6 points, following a decline of 0.5 points in 2013, to an index of 4.3, again its highest in the series; and Portugal, up 1 point, after a small increase of 0.2 points in 2013, also now holding its highest index in the series standing at 3.6. Austria and Malta show the greatest improvements of all 28 Member States in the 2014 rankings relative to those in 2013, both rising seven places, Austria from ninth to second position and Malta from thirteenth to sixth. Malta and Austria have also seen the largest increases of all EU Member States since 2009 (both up 1.9 points), followed by Lithuania (up 1.1 point), and Latvia and Hungary (both up 1 point). The largest decline since 2013 in people s perceptions of the area they live in is seen in Bulgaria (down 0.7 points), followed by Germany (down 0.4). Across the period, the largest overall declines are observed in Cyprus (from 5 to 3.8) followed by Belgium (from 6.1 to 5.2). 22 Sweden, Germany, Belgium and Bulgaria 21

25 The next table summarises Europeans perceptions of their personal job situation. 315 (2009) Your personal job situation (Evaluation of the current situation) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU DK SE FI LU MT AT DE NL UK BE FR EE CZ LV SK IE SI PL LT ES IT PT CY BG HR HU RO EL

26 At the EU level, the overall index of 1.2 for people s personal job situation in 2014 is positive, and remains unchanged from However, both indices are the second lowest in the series, ahead of only the 2012 index of 0.9, and there is a decline of 0.5 points from the high of 1.7 in That said, the EU level index for personal job situation is the third highest among the 15 survey measures. The highest indices are found in the Nordic and Benelux countries, along with Malta, Austria, Germany, and the UK broadly reflecting the pattern seen to date in this section. However, Ireland ranks sixteenth out of the twenty-eight countries on personal job situation, compared with rankings of fifth on local area and equal eighth (along with Austria) on life in general. Respondents in Denmark have the most positive perception of their job situation, with an index of 5.8, followed by Sweden (5.6), Finland (5.3), Luxembourg (4.3), Malta (3.9), Austria (3.8), Germany (3.2), the Netherlands (3), the UK (2.8) and Belgium (2.6). The most negative perceptions of the respondent s personal job situation are seen in southern and eastern European Member States. Greece (-3.6) has the lowest index, followed by Romania (-2.7), Hungary (-2.2), Croatia (-1.5), Bulgaria (-1.3), Cyprus (-1.2), Portugal and Italy (both -1.1) and Spain (-0.4). Comparing the results at a national level with those from previous waves, thirteen Member States 23 show a year-on-year decline between 2013 and 2014 in terms of people s evaluation of their personal job situation; Austria, Latvia and Slovenia show no change; and the remaining twelve show an improvement. The biggest improvements between 2013 and 2014 can be observed in Ireland and Spain (both up 1.4 points) to indices of 0.8 in Ireland (its highest index in the series) and -0.4 in Spain. They are followed by Malta (up 1.1 point), Cyprus (up 0.9), Croatia (up 0.7) and Finland (up 0.6 points). Malta shows the largest improvement in index between 2009 and 2014 (up by 2.1 points), followed by Lithuania (up 1.5), Latvia (up 1.3) and Sweden (up 0.9 points). Malta is now ranked fifth on this measure, up from ninth in 2013 and fourteenth in The largest declines since 2013 in people s perceptions of their job situation can be seen in Estonia (down 1 point), Belgium and the Czech Republic (both down 0.7) and Romania and Luxembourg (both down 0.6 points). Across the period, the largest overall declines in people s evaluation of their personal job situation are seen in Cyprus (down 3.1 points), Greece (down 2.6), Romania (down 2.2), the Netherlands and Portugal (both down 1.3), and Italy (down 0.8 points). In spite of its inclusion in this group, the Netherlands still has the eighth highest index of all 28 countries on this measure. Cyprus shows the greatest drop in ranking, from equal eleventh in 2009 to twenty-third in Sweden, Luxembourg, Germany, the Netherlands, Belgium, France, Estonia, the Czech Republic, Lithuania, Italy, Portugal, Hungary and Romania 23

27 The last of the four measures relating to Europeans personal situation concerns people s perceptions of the current financial situation of their household. 315 (2009) The financial situation of your household (Evaluation of the current situation) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU DK SE NL LU FI MT AT DE UK BE EE FR SI IE CZ LT PL LV SK ES IT HR CY HU RO PT BG EL

28 With an EU level index of 0.8, Europeans overall assessment of their household s current financial situation broadly reflects their view of their personal job situation (1.2), and is the fifth highest index among the 15 survey measures. The index has declined by 0.1 point since 2013 and has returned to its lowest level in the series, last recorded in The 2014 index is 0.7 points behind the high observed in The similarity between people s evaluation of their household finances and personal job situation are largely reflected at the individual country level, with the highest indices again found in the Nordic countries and Benelux states, Malta, Austria, Germany and the UK. Respondents in Denmark have the most positive perception of their household s current financial situation, with an index of 5.2, followed by Sweden (4.5), the Netherlands (3.8), Luxembourg (3.7), Finland (3.5), Malta (3.3), Austria (2.8), Germany and the UK (both 2.3) and Belgium (1.9). Nine of these ten Member States have been ranked in the top ten on this measure in each of the six survey years, the exception being Malta, which has risen from fifteenth position in 2009 to sixth in 2014, replacing France, which has dropped to twelfth position. The most negative perceptions of household finances are again seen in southern and eastern European countries. Greece (-3.9) has the lowest index in 2014, followed by Bulgaria (-2.2), Portugal (-1.8), Romania (-1.7), Hungary (-1.5), Cyprus (-1.4) and Croatia (-1.3). Fourteen Member States 24 show a year-on-year improvement between 2013 and 2014 in terms of people s evaluation of their household s financial situation. In most cases the movements tend to be small, with the most notable improvements in Malta (up 1.4 points), Ireland and Cyprus (both up 0.8 points) and Slovenia, Spain and Bulgaria (all up 0.5 points). Malta has seen the largest improvement of any Member State on this measure since 2009, from a baseline of 0.6 in 2009 to 3.3 in 2014 (up 2.7 points). Other notable improvements since 2009 can be observed in Hungary, from -3.2 to -1.5 (up 1.7 points); in Austria, from 1.8 to 2.8 (up 1 point); and in Lithuania, from -0.7 to 0.3 (also up 1 point). The index for the household financial situation has remained the same since 2013 in four Member States: the Netherlands, Lithuania, Latvia and Greece. In the remaining ten countries declines in the index tend to be small, with Belgium showing the greatest drop (down 0.9 points), followed by Sweden (down 0.8). In spite of their inclusion in this group, both countries remain in the top ten Member States with the highest indices on this measure, Sweden dropping in ranking from first in 2013 to second in 2014, and Belgium dropping from sixth to tenth position respectively. 24 Denmark, Finland, Malta, Austria, Estonia, Slovenia, Ireland, Slovakia, Spain, Croatia, Cyprus, Hungary, Romania and Bulgaria 25

29 Across the period, the largest overall declines in people s evaluation of their household s financial situation can be seen in Greece (down 3.1 points), Cyprus (down 1.9), Italy and Portugal (both down 1.4) and Belgium (down 0.9). Cyprus, along with Spain, show the largest drop of all 28 Member States in their rankings now compared with those held in 2009: Spain dropping from equal thirteenth 25 in 2009 to twentieth in 2014; and Cyprus dropping from seventeenth to twenty-third position respectively. This section concludes by providing an overview of the most notable socio-demographic differences on the four measures relating to people s personal situation. As was the case in relation to the overall social climate index, the key factors that differentiate how people feel about their personal situation are their perception of how difficult it is to pay their household bills, their occupational status and, to a somewhat lesser extent, the age at which they left education. As seen in relation to the overall social climate index, there is a strong relationship between how difficult people are finding it to pay their household bills and their perceptions of their personal situation. Those who struggle to pay their bills most of the time have much lower indices than those who almost never struggle to do so on all four measures, with particularly large differences between these two groups in relation to both their household financial and personal job situations. 418 (2014) Your life in general The area you live in Your personal job situation The financial situation of your household EU Difficulties paying bills Most of the time From time to time Almost never Since 2013, there have been some improvements in perceptions, most notably among those who have difficulty paying bills most of the time in relation to the area they live in (up 1.1 point), with smaller improvements among those who struggle with bills from time to time (up 0.3 points) and those who almost never struggle with bills (up 0.4 points). Across the three remaining measures there are no notable improvements in perceptions. The most notable worsening of opinion is among those who struggle to pay their bills from time to time in relation to life in general (down 0.8 points), with a less marked deterioration among those who struggle most of the time (down 0.5 points). Change in index 2014 vs Your life in general The area you live in Your personal job situation The financial situation of your household Difficulties paying bills Most of the time = From time to time Almost never Along with Ireland 26

30 Comparing the 2014 results with those from 2009 shows a deterioration in the perceptions of those who routinely struggle to pay their household bills on all but one measure (local area), with the most notable worsening of opinions in relation to life in general (down 1.8 points), and with perceptions of the local area showing only a small improvement (up 0.2 points). It also shows that those who almost never struggle to pay bills are starting to find things more difficult, with small deteriorations across three indicators and only a small improvement in the fourth - local area (up 0.2 points) - among this group as well. Change in index 2014 vs Your life in general The area you live in Your personal job situation The financial situation of your household Difficulties paying bills Most of the time From time to time -1.1 = Almost never In terms of the respondent s occupational status, the largest differences in the 2014 indices are between the unemployed, who score lowest on all four measures, and managers, who score highest on each measure (with the exception of life in general where students have a slightly higher index of 4.6). Not surprisingly, the difference in perceptions between the two groups is particularly marked in relation to personal job situation and the household financial situation: 418 (2014) Your life in general The area you live in Your personal job situation The financial situation of your household EU Respondent occupation scale Managers Unemployed Since 2013 there has been a worsening in managers perceptions of life in general (down 0.5 points), marginal positive shifts in their opinions on the local area and household financial situation (both up 0.1 point) and no change in perceptions of their job situation. Compared with 2009, managers are slightly more positive about the area in which they live (up 0.2 points) but somewhat more pessimistic about other aspects of their personal situation, most notably their general life (down 0.4 points). The unemployed also show an improvement since 2013 in their opinions about the local area (up 0.3 points). They are marginally more negative about their job situation (down 0.1 point), somewhat more negative about household finances (down 0.3 points) and notably more pessimistic about their life in general (down 1.3 points). Compared with 2009, the unemployed, like managers, hold more positive opinions on their local area (up 0.3 points) and less positive views on each of the other measures. The largest negative shift in opinion since 2009 is on life in general (down 1.4 points) and it is more marked than that seen for managers in relation to this measure. 27

31 In terms of age of leaving education, those who left-time education at 15 or younger, or aged 16-19, are less satisfied with their personal situation than those who continued their education to age 20 or older and students: 418 (2014) Your life in general The area you live in Your personal job situation The financial situation of your household EU Education (End of) Still studying

32 2. COUNTRY Having explored Europeans perceptions of their personal situation, this next section of the chapter looks at their views on the national picture, with a particular focus on economic indicators. Respondents were asked to judge the current situation in relation to six aspects of life in their own country: the cost of living; the affordability of energy; the affordability of housing; the way public administration runs; the economic situation; and the employment situation. As before, the results are reported as indices. Each of the six aspects is examined in turn for the EU as a whole, and for each country, for the latest wave and for the last five waves. 29

33 The table below summarises people s satisfaction with the cost of living in their country. The cost of living in (OUR COUNTRY) (Evaluation of the current situation) 315 (2009) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU SE NL DK DE AT MT LU BE UK FI FR ES IE CZ SK LT EE PL HU IT PT SI LV CY RO EL BG HR

34 Europeans net evaluation of the cost of living in their country is somewhat negative, with an index of -2.9 at the EU level. This is the fourth lowest overall index across the 15 survey measures. The 2014 index represents a small improvement on the overall score of -3.1 recorded in 2013, but remains slightly below the highest point in the whole series of -2.7 in There is national variation, with the highest indices again found in the Nordic and Benelux countries, Germany, Austria, Malta and the UK. Having said this, only four countries have a positive index on this measure, and only two Sweden (1.6) and the Netherlands (1.5) have an index of one or higher. Four countries have an index of -6 or lower, with Croatia having the lowest score (-7.1), followed by Bulgaria (-6.6), Greece (-6.5) and Romania (-6.1). Comparing the results at a national level with those from 2013, seventeen Member States 26 show an improvement in terms of people s satisfaction with the cost of living; Slovenia shows no change; and the remainder show a year-on-year decline. The largest improvements are observed in Malta (up 2.6 points), Estonia (up 1.6), Portugal (up 1.3), Spain (up 1.2) and Ireland (up 1.1), followed by Slovakia and Cyprus (both up 0.8 points). Malta also shows the largest improvement of any Member State on this measure since the first wave, from a baseline of -5.6 in 2009 to -1.2 in 2014 (up 4.4 points), followed by Ireland, from -5.6 to -3.8 respectively (up 1.8). The only other Member State showing an improvement in 2014 of at least one point on the baseline index is Hungary - from -6.1 to -4.7 respectively (up 1.4). Where indices on the cost of living have declined since 2013, these declines tend to be relatively small, with the highest in Austria (down 1.1 point), followed by Luxembourg (down 0.9) and Sweden, Belgium and Bulgaria (each down 0.8 points). Across the period, the largest deteriorations on this measure can be seen in Luxembourg (down 2.1 points), Cyprus (down 1.4) and Austria, Finland and Estonia (each down 1.2 points). There have been some notable changes in the relative positions of countries on this measure since 2009: Malta has risen sixteen places from twenty-second equal position in 2009 to sixth in 2014, whilst Ireland (also twenty-second equal in 2009) has risen nine places to thirteenth. In contrast, Slovenia has dropped eight places from fourteenth in 2009 to twenty-second in 2014 and Cyprus, seven places from seventeenth equal positon to twenty-fourth. 26 The Netherlands, Malta, the UK, France, Spain, Ireland, the Czech Republic, Slovakia, Lithuania, Estonia, Poland, Hungary, Portugal, Italy, Cyprus, Romania and Greece 31

35 The next table summarises Europeans perceptions of how affordable energy is in their country. How affordable energy is in (OUR COUNTRY) (Evaluation of the current situation) 315 (2009) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU CZ EE LV NL SE AT DK MT LU BG SI FI PL HU SK ES DE FR BE HR IT LT IE UK PT RO EL CY

36 People s perceptions of how affordable energy currently is in their country are slightly better than their views of the overall cost of living, with an index of -2.5 at the EU level, the sixth lowest EU level index among the 15 survey measures. The index remains unchanged on 2013, and is somewhat lower than the baseline index (-2.2) and the highest index in the series recorded in 2010 (-2). There is again a large amount of variation between individual countries, although this variation follows a somewhat different pattern from those seen earlier in the report. This is not unexpected, since energy prices in individual countries will reflect a range of different supply and demand conditions in each country that are not necessarily related to a country s overall economic situation 27. The most positive perceptions of the affordability of energy can be observed in the Czech Republic (4.2), Estonia (3.6) and Latvia (1.9). These Member States have occupied the first three positions on this measure in each of the six survey years. Six other countries have positive indices on this measure in 2014: the Netherlands (1.3), Sweden (0.9), Austria (0.7), Denmark and Malta (both 0.5) and Luxembourg (0.2). It is worth noting in this context that the cost to consumers of gas and electricity in Sweden, Denmark and Austria is high relative to other EU countries 28. There is more similarity with earlier findings in terms of the countries with the most negative perceptions of the affordability of energy. Five countries have an index of -4 or lower on this measure: Cyprus (-6.9), Greece (-6.6), Romania (-5.7) and Portugal (-5.3), joined in this instance by the UK (-4.1). Most Member States show an improvement in terms of people s judgements of the affordability of energy relative to the position in 2013, opinion in Estonia remains unchanged, and six countries 29 show a year-on-year decline. The largest improvements since 2013 are observed in Malta (up 4.1 points), Hungary (up 2 points), Poland and Slovakia (both up 1.1 point), and Austria, Bulgaria and Lithuania (each up 0.9 points). The large positive shifts in Malta and Hungary have resulted in notable improvements in their rankings: Malta rising from nineteenth position in 2013 to equal seventh in 2014; and Hungary rising from equal twentieth to equal twelfth. The largest improvements between 2009 and 2014 on this measure are seen in Bulgaria, Hungary and Malta. The largest increase (5.8 points) can be observed in Bulgaria, although this is largely accounted for by a huge shift in perceptions between 2009 and 2010, when the index moved from -5.9 to , with slight declines in the following years before the increase noted above in In Malta the net increase is 5.4 points, from -4.9 in 2009 to 0.5 in 2014; with the index in Hungary increasing by 4.1 points over the same period, from -5.9 to including the geopolitical situation, import diversification, network costs, environmental protection costs, severe weather conditions and levels of excise and taxation _%28EUR_per_kWh%29_YB14.png 29 Latvia, Denmark, Spain, Germany, Belgium and the UK 30 This may reflect the economic recovery in Bulgaria in 2010, following a rapid economic decline in

37 The shifts in Malta, Bulgaria and Hungary have resulted in big improvements in their rankings, with Malta rising from twenty-fourth position in 2009 to equal seventh in 2014, and Bulgaria and Hungary from twenty-sixth equal in 2009 to tenth and equal twelfth respectively in The largest declines in people s judgements of the affordability of energy relative to the position in 2013 can be observed in Spain (down 2.1 points) from -0.2 to -2.3, and Latvia and the UK (each down 0.8 points) from 2.7 to 1.9 and from -3.3 to -4.1 respectively. The shifts in Spain and the UK have affected their rankings, with Spain dropping from equal eighth position in 2013 to sixteenth in 2014, and the UK dropping from eighteenth to twenty-fourth position. The Member States with the largest deterioration in perceptions of the affordability of energy since 2009 are Spain (down 4 points), followed by Cyprus (down 2.5), Romania (down 1.7), Greece (down 1.6), and Latvia (down 1.3). The shift in Spain has seen it drop twelve places in the rankings, from fourth position in 2009 to sixteenth now. 34

38 The next table below shows respondents perceptions of the affordability of housing in their country. How affordable housing is in (OUR COUNTRY) (Evaluation of the current situation) 315 (2009) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU DK EE CZ LV NL SE AT DE BG HU IE FI MT BE HR FR SK IT UK PL PT EL SI ES LT RO LU CY

39 Europeans evaluation of the affordability of housing in their country is somewhat negative, with an index of -3.3 at the EU level. This index has declined since 2013 (down 0.4 points from an index of -2.9), and has returned to its lowest level in the series, also recorded in 2011 and It is the second lowest EU level index among the 15 survey measures. The index varies nationally. As was the case in relation to perceptions of energy costs, there is a less discernible pattern than on previous measures in terms of the countries with the highest and lowest indices on this measure. Only three Member States have a positive index on this measure, with the highest in Denmark (1), followed by Estonia (0.7) and the Czech Republic (0.5). The remainder have a negative index, with two having an index of -5 or lower: Cyprus (-6.5) and Luxembourg (-5.1). A further nine countries have an index of at least -4: Spain, Lithuania and Romania (-4.8 in each), Slovenia (-4.7), Greece (-4.6), Portugal (-4.5), the UK and Poland (both -4.3) and Italy (-4.1). Thirteen of the 28 Member States 31 have seen an improvement since 2013 in perceptions of the affordability of housing, opinion in the Netherlands remains the same, and the remaining countries show a year-on-year decline. The largest improvements since 2013 can be observed in Malta (up 1.1 point), Hungary (up 1) and the Czech Republic, Slovakia and Romania (each up 0.6 points). Between 2009 and 2014 the index on this measure has improved by one point or more in six Member States. The greatest improvement is observed in Bulgaria, with a net increase of 4.7 points, from an index of -6.4 in 2009 to -1.7 in As was the case in relation to the affordability of energy, this relates to a shift in perceptions between 2009 and 2010, when the index moved from -6.4 to The other Member States showing the most marked improvements are: Hungary (up 2.5 points), Malta (up 2), the Czech Republic (up 1.8), Ireland (up 1.5) and Cyprus (up 1 point). Bulgaria and Hungary have risen notably in the country rankings on this measure since 2009, Bulgaria from twentysixth position to equal eighth and Hungary from twenty-second position to tenth. Only five Member States show a decline in satisfaction with housing costs since 2014 of one point or more, with the largest in Germany and Belgium (both down 1.4 points), followed by the UK (down 1.3), and Sweden and Ireland (both down 1.1 point). The largest shifts towards more negative perceptions between 2009 and 2014 are again in Germany (down 2.4 points) and Sweden (down 1.7 points), along with Austria (down 1 point), although all of these countries remain in the top ten in terms of ranking. The most notable drops in ranking on this measure can be observed in Slovenia (from twelfth equal in 2009 to twenty-third in 2014) and Luxembourg (from fifteenth equal to twentyseventh). 31 The Czech Republic, Hungary, Malta, Croatia, Slovakia, Poland, Portugal, Greece, Slovenia, Spain, Lithuania, Romania and Cyprus 36

40 The fourth measure in this section concerns people s views of the way that public administration runs in their country. The way public administration runs in (OUR COUNTRY) (Evaluation of the current situation) 315 (2009) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU DE DK MT LU EE FI SE NL AT BE UK CZ LT FR HU SK PL IE LV BG PT ES SI CY RO IT HR EL

41 Europeans overall judgement of the way that public administration runs in their country is slightly negative, but less so than for the five other measures covered in this section, with an index of -1.7 at the EU level. There has been a slight but consistent deterioration in perceptions on this measure over the series, with the index falling by 0.1 each year from a high of -1.2 in As with other measures, there are large differences nationally in perceptions. The pattern tends to follow that seen for most of the measures, with the highest indices found in the Nordic and Benelux countries, Germany, Malta and Austria, with Estonia also having relatively positive views on public administration. Germany, Denmark and Malta have the highest indices (2 in each), followed by Luxembourg (1.9), Estonia (1.7), Finland (1.4), Sweden (1.2), the Netherlands (0.5), Austria (0.2) and Belgium (-0.3). The UK has the next highest index (-1.3) and has lost a position in the top ten which it held for the previous four surveys. Similarly, the most negative perceptions are again found in southern and eastern European countries, reflecting the pattern seen on most measures. Nine countries have an index of -3 or worse on this measure. Greece has the lowest index (-6.3), followed by Croatia (-5.6), Italy (-4.8), Romania (-4), Cyprus and Slovenia (both -3.6), Spain (-3.4), and Portugal and Bulgaria (both -3.3). Twelve Member States 32 show an improvement since 2013 in terms of people s satisfaction with the way that public administration runs in their country, Poland and Latvia show no change, and the remainder show a year-on-year decline. The largest improvement on this measure between 2013 and 2014 is seen in the Netherlands (up 1.7 points), followed by Spain (up 1.1), Malta (up 0.9) and Estonia (up 0.8), whilst the largest improvements between 2009 and 2013 can be noted in Malta (up 3 points), Latvia (up 2.1) and Ireland (up 1.2). Malta s equal first ranking in 2014 compares with rankings of eighth in 2013 and eleventh in Perceptions of the way that public administration runs have worsened since 2013 in fourteen Member States, with the largest declines in Belgium and Austria (both down 1.5 points), Bulgaria (down 1.2), Hungary (down 1) and Romania and Slovakia (both down 0.8 points). Over the six survey years the largest decline can be observed in Slovenia, down 3.9 points from 0.3 in 2009 to -3.6 in 2014, with its ranking declining from ninth to twentythird equal over this period. The indices in Cyprus and Spain have also dropped by two points or more between 2009 and 2014 (both down 2.2 points). 32 Denmark, Malta, Estonia, Finland, the Netherlands, the UK, Lithuania, Portugal, Spain, Cyprus, Slovenia and Greece 38

42 The next table shows Europeans judgement of the economic situation in their country in 2014, and in the five previous survey years. The economic situation in (OUR COUNTRY) (Evaluation of the current situation) 315 (2009) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU DE DK MT SE LU AT NL EE BE UK FI LT PL HU CZ LV IE SK FR RO PT IT SI ES BG CY HR EL

43 Europeans perceptions of the current economic situation in their country are somewhat negative overall, but less so than their views on the cost of living. The index of -2.6 at the EU level makes it the fifth lowest rated aspect of life among the 15 measured in the survey. Having said this, perceptions have improved since 2013 (up 0.9 points), and show the greatest improvement of any of the 15 measures since The index of -2.6 is the highest recorded in the series and up 1.5 points from the baseline index of -4.1, and again shows the greatest improvement of all 15 measures between 2009 and The index varies between countries, with the difference between the most positive and most negative ratings (11.5 points) the third highest of the 15 survey measures 33. The highest indices are again found in the Nordic and Benelux countries (with the exception on this measure of Finland), Germany, Malta, Austria, Estonia and the UK. Finland sits just outside the top ten countries, ranked eleventh. Seven countries have a positive index on this measure, with the highest index being found in Germany (3.6), followed by Denmark and Malta (both 2.7), Sweden (2.6), Luxembourg (2.2), Austria (0.6) and the Netherlands (0.1). Nine countries have an index of -5 or lower, with Greece having the most negative perception of their country s current economic situation (-7.9), followed by Croatia (-7.6), Cyprus (-7.4), Bulgaria (-6.8), Spain and Slovenia (both -6.7), Italy (-6), and Portugal and Romania (both -5.4). Comparing the results at a national level with those from 2013, twenty-three Member States show a year-on-year improvement in terms of people s satisfaction with the current economic situation in their country. The largest improvement can be seen in the UK (up 2.7 points), followed by Ireland (up 2.6 points) and Malta (up 2.5 points). A further ten countries have seen their index increase by more than one point between 2013 and 2014: Portugal, the Netherlands, the Czech Republic, Cyprus, Lithuania, Denmark, Estonia, Romania, Hungary and Spain, with the most notable shifts in Portugal (up 1.8 points), the Netherlands and the Czech Republic (up 1.6) and Cyprus (up 1.5). There are some notable improvements in perceptions of the national economic situation at country level across the six years of the survey, with net increases of at least four points recorded in six Member States: Germany has seen a particularly strong improvement in perceptions, with large year-on-year increases in 2010 and 2011 followed by a slight improvement in 2012, a slight worsening in 2013 and a small improvement in The overall net improvement between 2009 and 2014 is 6.8 points. This improvement has seen Germany rise in the ranking on this measure from tenth of the 27 Member States in 2009 to first in 2013 and again in Malta has also seen a large increase between 2009 and 2014 of 6.5 points, with particularly notable improvements between 2012 and This improvement has seen Malta rise in the ranking on this measure from thirteenth position in 2009 to equal second in

44 Like Germany, Latvia has seen a year-on-year improvement, from a low of -8.3 in 2009 (when it was ranked lowest of the 27 Member States) to a high of -3.7 in 2014 (and a ranking of sixteenth), a net gain of 4.6 points. The UK also shows improvement across the series, notably stronger between 2013 and The overall result is a 4.5 point net gain, from an index of -5.5 in 2009 to -1 in 2014, and a rise from twenty-first position to tenth. Estonia has also seen a positive trend each year up until 2012, with a small decline in 2013 (down 0.5 points) followed by a positive shift in The overall result is a 4.2 point net gain, from an index of -4.7 in 2009 to -0.5 in 2014, seeing it move from sixteenth position to eighth. Hungary has seen an increase between 2009 and 2014 of 4 points, improving from -7.3 in 2009 to -3.3 in 2014, with a rise in the ranking on this measure from twenty-sixth to fourteenth position. Only five Member States show a decline in perceptions of the current economic situation between 2013 and 2014, with the largest in Finland (down 2.1 points), followed by Sweden (down 0.7), Croatia and Austria (both down by 0.6 points) and Luxembourg (down 0.5). The declines in Finland, Sweden and Austria are surprising in the context of the other results reported to date. In Finland it reflects the actual economic situation with the country in recession and negative growth in the third and fourth quarters last year and the first quarter in It sees Finland drop in ranking from seventh position in 2013 to eleventh in 2014, moving outside the top ten most positive Member States for the first time in the series. By far the largest deterioration in satisfaction with the current national economic situation between 2009 and 2014 is to be seen in Cyprus where there has been a yearon-year decline in the index up until 2014 (when it increased 1.5 points on 2013). This has resulted in a net drop of 7.8 points, from an index of 0.4 in 2009 to -7.4 in Cyprus, whose banks have a large exposure to Greek debt, has plummeted dramatically in the rankings on this measure from third of 27 Member States in 2009 to become the lowest ranked of any Member State in 2013, before improving slightly to twenty-sixth in Only two other Member States have seen their index drop by more than two points between 2009 and 2014: Slovenia dropping 3.9 points from an index of -2.8 in 2009 to -6.7 in 2014 (with a fall in its ranking from ninth to twenty-third equal); and Finland down 2.1 points from an index of -0.2 in 2009 to -2.3 in 2014 (with a fall in its ranking from fifth to eleventh equal). A further five countries have seen their index drop by at least one point: Greece (down 1.7); Spain (down 1.4); Italy (down 1.2); Bulgaria (down 1.1); and Poland (down 1). 33 The highest difference is in relation to the pension system, followed by the healthcare system 41

45 The last measure examined in this section concerns people s level of satisfaction with the employment situation in their country. The employment situation in (OUR COUNTRY) (Evaluation of the current situation) 315 (2009) 349 (2010) 370 (2011) 391 (2012) 408 (2013) 418 (2014) EU DE MT DK LU AT SE UK EE LT BE NL FI LV PL HU CZ IE PT FR SK IT RO CY BG SI ES EL HR

46 Europeans assess the employment situation in their country more negatively than they do any of the other dimensions they are asked about in the survey, with an index of -4.1 at the EU level. The 2014 index shows a very small increase on the overall score of -4.2 in 2013 (up 0.1 point), and remains only slightly higher than the lowest score of -4.4 recorded in National variation in the index broadly reflects the pattern seen on most measures, with the highest indices found in the Nordic and Benelux countries (with the exception of Finland), Germany, Malta, Austria, the UK and Estonia, joined on this indicator by Lithuania. Finland sits just outside the top ten on this measure, ranked twelfth. The lowest indices are again found in southern and eastern European states, joined on this measure by France. Only three countries have a positive index on this measure, with Germany having the highest index (1.1), followed by Malta (0.8) and Denmark (0.2). Nine countries have an index of lower than -6. Croatia, Greece and Spain have the most negative perceptions of their countries current employment situation, with indices of -8.3, -8.1 and -8 respectively, followed by Slovenia (-7.6); Bulgaria (-7.4); Cyprus (-7); Romania (-6.9); Italy (-6.7) and Slovakia (-6.2). Not surprisingly, there is a relationship between the perceptions of individual countries of the employment situation in their country and the level of unemployment in the country concerned, with higher indices generally found in countries with relatively low levels of unemployment, and vice versa. For example, Germany, Malta and Denmark, which score highest on this measure, have some of the lowest current unemployment rates in the EU28 (although not the lowest); and Croatia, Greece and Spain, which score lowest on this measure, have the highest unemployment rates in the EU There are some exceptions to this rule, most notably in Romania, which has the eighth lowest unemployment rate in the EU28, but ranks twenty-second in terms of its perceptions of the employment situation in the country; and in Slovenia, which has the thirteenth lowest unemployment rate in the EU28, but ranks twenty-fifth on this indicator. Of course, people s perceptions of the employment situation in their country may be influenced by a wider range of factors than simply the rate of unemployment. People s judgements of the employment situation in their country have improved in sixteen Member States 35 since 2014; France and the Czech Republic show no change; and the remainder show a worsening of perceptions. The largest improvements are observed in Ireland (up 1.6 points), Portugal (up 1.5) and the UK (up 1.4). These improvements reflect recent reductions in the unemployment rate 36 in each of these Member States. 34 Based on an analysis of the most recently published Eurostat unemployment statistics: 35 Malta, Denmark, the UK, Estonia, Lithuania, the Netherlands, Latvia, Poland, Hungary, Ireland, Portugal, Romania, Cyprus, Slovenia, Spain and Greece 36 This is based on comparisons of seasonally adjusted unemployment rates in April 2013 versus April In the UK, April 2014 data is not available and comparisons are based on April 2013 versus February