U.S. Steel Market Outlook. Amy Ebben ArcelorMittal USA November 30, 2018

|

|

|

- Grace Mathews

- 5 years ago

- Views:

Transcription

1 U.S. Steel Market Outlook Amy Ebben ArcelorMittal USA November 30, 2018

2 Agenda ArcelorMittal introduction U.S. steel industry performance and trade Global steel industry Review of steel markets 1

3 About ArcelorMittal World's leading steel and mining company with about 199,000 employees in 60 countries Recognized leader in all major global steel markets, including automotive, construction, household appliances and packaging, with leading R&D and technology, as well as sizeable captive supplies of raw materials and outstanding distribution networks An industrial presence in 19 countries exposes the company to all major markets, from emerging to mature Values geographical breadth, product diversity and raw material security 2017 Crude Steel Production ACIS 16% 25% NAFTA Europe 47% 12% Brazil 2

4 ArcelorMittal in the United States ArcelorMittal has facilities, offices and joint venture partnerships in 14 states and the District of Columbia

5 Steel demand in the U.S. continues to improve but remains below pre-recession levels M tons U.S. Apparent Steel Consumption: Steel Consumption Avg % E Source: AISI, AMUSA Marketing; 18E based on YTD September annualized 4

6 Varying levels of demand performance among the major steel products has led to prolonged recovery Flat Roll Products Long Products Pipe & Tube All Charts in M tons Flat Avg -6% Long Avg -18% P&T Avg +11% E E E 63% 26% 11% 5 Source: AISI, Images from WorldSteel, AMUSA Marketing, 2018E based on YTD Sep annualized; % represents percentage of 2017 US steel consumption

7 Section 232 steel tariffs April 19, 2017: Commerce initiates 232 investigation Jan 11, 2018: Report given to President affirming that steel is important to national security and hurt by imports March 8, 2018: Presidential Proclamation of 25% tariff on all imports effective March 23 Canada, Mexico, EU to be exempt temporarily while negotiations continue Country-level exemptions: Korea, Argentina and Brazil agree to quotas in place of tariffs; Australia given full exemption with no quota Product exemptions: process put in place for U.S. manufacturers to apply for one year waiver June 1, 2018: 25% tariff put in place for Canada, Mexico, and EU Retaliatory tariffs announced on domestic steel exports and other goods August 10, 2018: President announces Turkey s tariff rate will be doubled to 50% Sources: Dept of Commerce, Customs & Border Protection, AMUSA Marketing 6

8 The Why Behind Section % 90% 85% 80% 75% 70% 65% 60% 55% 50% 45% 40% U.S. Monthly Raw Steel Capacity Utilization Jan 2005-Mar % Source: AISI, AMUSA Marketing M tons U.S. Quarterly Flat Roll Imports & Market Share Jan 2011-Mar 2017 Import Share (RHS) Imports % 25% 24% 23% 22% 21% 20% 19% 18% 17% 16% 15% 14% 13% 12% 11% 10% 9% 8% 7

9 Section 232 Scope 2017 Carbon Flat Roll Imports (M tons) Section 232 Current Status Canada % Tariff Mexico EU Turkey South Korea % Tariff 25% Tariff 50% Tariff Absolute Quota: 70% of Avg Australia Brazil Argentina Full Exemption Absolute Quota: Avg imports of 70% for finished and 100% for semi s Absolute Quota: 135% of Avg Others % Tariff Source: CBP, AISI, AMUSA Marketing

10 Industry utilization approaches 80%; Flat Roll mills at higher utilization 95% 90% 85% 80% 75% 70% 65% 60% 55% 50% 45% 40% U.S. Monthly Raw Steel Capacity Utilization Jan 2005-Sep % Source: AISI 9

11 Imports have been volatile since S232 investigation was announced M tons U.S. Quarterly Flat Roll Imports & Market Share Jan 2011-Sep Import Share (RHS) Imports % 25% 24% 23% 22% 21% 20% 19% 18% 17% 16% 15% 14% 13% 12% 11% 10% 9% 8% Source: AISI, AMUSA Marketing 10

12 Exports are cooling on high domestic prices and retaliatory tariffs Other Impacts: Steel prices increased significantly post-232 but have weakened since Summer. Carbon Flat Roll Exports Jan 2013-Sep M tons Mexico Others 7% 45% % Canada Idled domestic capacity has been restarted. Domestic mills have announced new investments to increase future capacity. Source: AISI, AMUSA Marketing

13 The Global Steel Industry is Performing Well in Crude Steel Production by Month: Y/Y % Change 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% -1% World U.S. China EU -2% Jan Feb Mar Apr May Jun Jul Aug Sep YTD All major steel producing regions have increased production YTD Global steel production is up 5% y/y. Source: World Steel Association 12

14 What does 5% growth look like? M metric tons Annual 5% Change in Raw Steel Production Just 5% growth in China is equivalent to adding ½ of the entire U.S. industry USA China 0 USA 2018E Source: World Steel Association, AMUSA Marketing 13

15 The impact of China on the global industry M metric tons Crude Steel Production: China USA Source: World Steel Association 14

16 US industry s position among world s top steel-producing countries has declined 2000 Crude Steel Production 2017 Crude Steel Production All Others 35% 3% Brazil 2% Turkey 5% 5% Germany South Korea China 15% 13% Japan 3% India 12% USA 7% Russia All Others 18% Brazil Turkey 2% 2% Germany 3% South Korea 4% 4% Russia 5% USA 6% India 6% Japan 49% China Source: World Steel Association 15

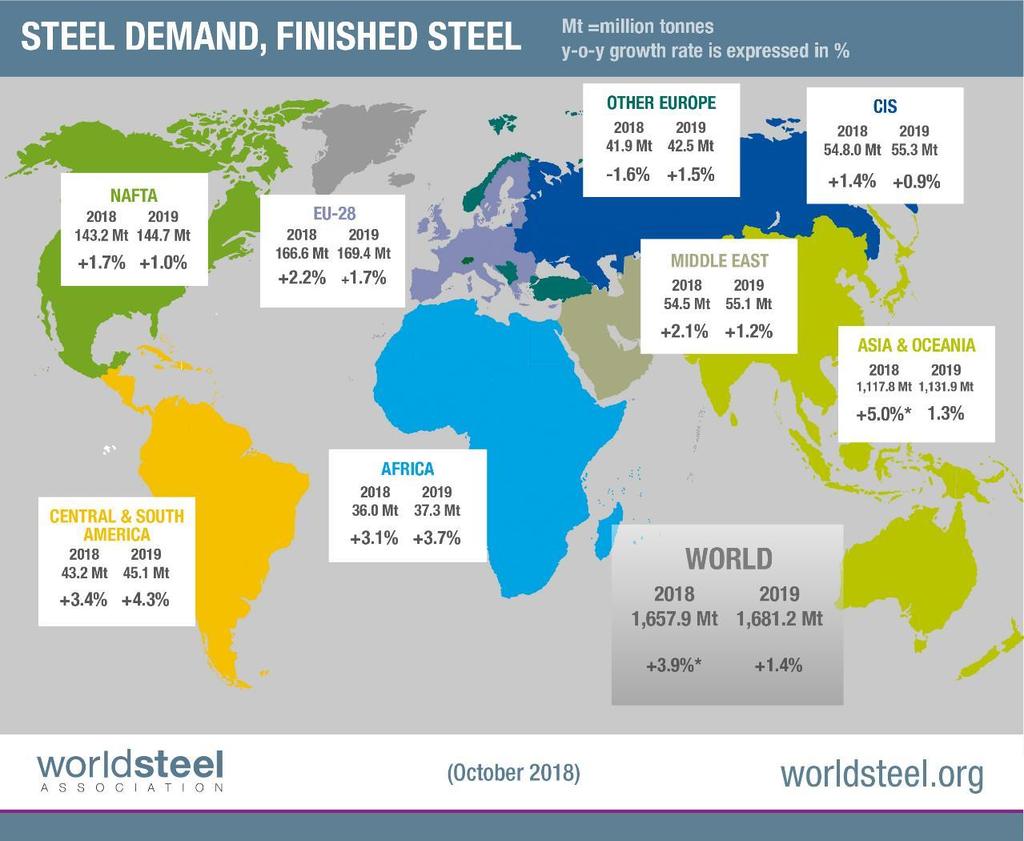

17 Global steel demand accelerated in following slowdown in Apparent Steel Consumption (Finished Steel) Y/Y % Chg 14% ASC y/y change 14% ASC (M mt) 1,700 12% 1,600 10% 8% 6% 4% 2% 0% 8% 2% 7% 8% 10% 7% 9% 7% 0% 8% 2% 7% 0% 1% 5% 4% 1% 1,500 1,400 1,300 1,200 1,100 1,000-2% 900-4% -3% 800-6% -8% % F 19F Source: World Steel Association, Oct 2018 Short Range Outlook 16

18 17

19 Review of steel markets 18

20 Steel Consuming Markets Estimated 2017 Steel Consumption by End-use Market Containers All Other Defense Appliance 3% 3% 5% 2% Energy 7% Machinery 10% 43% Construction Automotive 27% Construction and Automotive industries are the top consumers of steel in the US. About 35% of purchase flow through distribution before reaching final customer. Source: AISI Profile 2018, AMUSA Marketing 19

21 Construction likely near peak; Infrastructure spending could help future steel demand Construction Spending Billion $, SAAR Dodge index points to drop by end 2019 Nonresidential Residential $800 $700 $600 Pre-Recession Peak - Nonres. Pre-Recession Peak - Res. +7% -18% $500 $400 $300 $110 $100 $90 $80 Highway & Street Spending Billion $, SAAR $200 $ Source: FRED, Dodge, AMUSA Marketing 20

22 Auto demand remains at strong levels U.S. Motor Vehicle- Industrial Production Index Jan 2004-Oct Things to Watch USMCA changes to domestic content requirements 232 report due in February Fuel economy standards Source: FRED, AMUSA Marketing 21

23 Recovery in machinery demand has boosted Plate and Hot Roll shipments US Machinery - Industrial Production Index Jan Oct 2018 Agricultural Construction Mining & Oil/Gas Y/Y % Change in Apparent Steel Consumption -10% -15% -2% Hot Roll Plate -19% 1% 0% 1% 17 13% 18 YTD Source: FRED, AISI, AMUSA Marketing 22

24 Energy pipe & tube demand grows with pipeline investment; US pipe mills looking to gain share U.S. Oil & Gas Rig Count and Oil Price Forecast Jan 2014-Dec 2019 WTI price ($/bbl) WTI Crude Oil & Gas Rig Count Series Rig Count 2,000 1,800 1,600 1,400 1,200 1, Reduction in import share would have big impact for domestic pipe & tube producers 4.0 U.S. Energy Pipe & Tube Imports (Millions of Tons) % of imports from S. Korea in 2014 vs 25% in 2018 LP OCTG E* Source: Baker Hughes, EIA Short Term Outlook (Nov 18), AISI, AMUSA Marketing *18E = Jan-Sep annualized 23

25 Positive manufacturing sentiment providing healthy backdrop for distribution demand IP Index Steel Service Center Shipments vs. IP Durable Manufacturing Jan Oct IP Durable Manuf Service Center Flat Roll Ship (SA) Service Center shipments up 5% YTD Service Center, M tons Annual Change in Service Center Flat Roll Inventories (Millions of Tons) YTD Source: FRED, MSCI, AMUSA Marketing 24

26 2019 Outlook U.S. steel demand anticipated to post growth of 1-2% in 2018 and Underpinning growth in steel consumption is the healthy US economy which should continue to expand in Trade tensions, inflation and rising interest rates top downside risks for the year given potential impact on manufacturing output and consumer demand U.S. Apparent Steel Consumption: F M tons Steel Consumption Avg Most major steel markets are projecting flat or higher growth in Construction, the biggest market for steel, is likely nearing its cyclical peak F Although not approved by Congress, USMCA brings more certainty to North America economies, particularly as related to automotive production. Steel tariffs imposed by Section 232 remain in effect for Canada and Mexico but could be eliminated or replaced by quotas in the short term. Steel imports have trended lower following Section 232 tariffs but remain above historical market share levels. Imports will evolve based on trade remedies and global pricing dynamics. Global steel demand is expected to increase in Supply by US steel mills is increasing with restart of idled capacity and new investments. Source: AISI, World Steel Association, AMUSA Marketing 25

27 Thank you 26

28 Connect with Company: ArcelorMittal USA Company page: ArcelorMittal USA Channel: ArcelorMittal USA usa.arcelormittal.com

Steel Market Outlook. AM/NS Calvert

Steel Market Outlook AM/NS Calvert Agenda ArcelorMittal at a glance USA Steel Market Outlook Global Steel Outlook and Raw Materials Trade Questions 1 The world s leading steel and mining company ArcelorMittal

Steel Market Outlook AM/NS Calvert Agenda ArcelorMittal at a glance USA Steel Market Outlook Global Steel Outlook and Raw Materials Trade Questions 1 The world s leading steel and mining company ArcelorMittal

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

Chad Utermark Executive Vice President of Beam and Plate Products Nucor Corporation March 2017

Chad Utermark Executive Vice President of Beam and Plate Products Nucor Corporation March 2017 Home Insurance Building William LeBaron Jenney The Rise of the Skyscraper Steel Cage Buildings Still Climbing

Chad Utermark Executive Vice President of Beam and Plate Products Nucor Corporation March 2017 Home Insurance Building William LeBaron Jenney The Rise of the Skyscraper Steel Cage Buildings Still Climbing

Text. improvement in earnings. Textdemand drove continued

Good Textdemand drove continued improvement in earnings Text Presentation of the Q2/2018 results Martin Lindqvist, President & CEO Håkan Folin, CFO July 20, 2018 Agenda Market and demand trends Performance

Good Textdemand drove continued improvement in earnings Text Presentation of the Q2/2018 results Martin Lindqvist, President & CEO Håkan Folin, CFO July 20, 2018 Agenda Market and demand trends Performance

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee June 8-9, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee June 8-9, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

Positive trend in earnings and strong cash flow

Positive trend in earnings and strong cash flow Presentation of the Q3/2017 result Martin Lindqvist, President & CEO Håkan Folin, CFO October 25, 2017 Agenda Q3/2017 and performance by division Financials

Positive trend in earnings and strong cash flow Presentation of the Q3/2017 result Martin Lindqvist, President & CEO Håkan Folin, CFO October 25, 2017 Agenda Q3/2017 and performance by division Financials

1 F b e 3 ruary, 2010

February 3, 2010 1 Forward-looking Statement This presentation contains certain forward-looking statements. The Company has tried, whenever possible, to identify these forward-looking statements using

February 3, 2010 1 Forward-looking Statement This presentation contains certain forward-looking statements. The Company has tried, whenever possible, to identify these forward-looking statements using

Months Consolidated Results. 28 April 2015

1 28.04.2015 2015 3 Months Consolidated Results 28 April 2015 2 28.04.2015 DISCLAMIER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about forward-looking

1 28.04.2015 2015 3 Months Consolidated Results 28 April 2015 2 28.04.2015 DISCLAMIER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about forward-looking

Investor Presentation

March, 2010 1 Disclaimer This document can contain statements which constitute forward-looking statements. Such forward-looking statements are dependent on estimates, data or methods that may be incorrect

March, 2010 1 Disclaimer This document can contain statements which constitute forward-looking statements. Such forward-looking statements are dependent on estimates, data or methods that may be incorrect

Investor Presentation

March, 2010 1 Disclaimer This document can contain statements which constitute forward-looking statements. Such forward-looking statements are dependent on estimates, data or methods that may be incorrect

March, 2010 1 Disclaimer This document can contain statements which constitute forward-looking statements. Such forward-looking statements are dependent on estimates, data or methods that may be incorrect

Third Quarter 2018 Earnings Presentation & Remarks

Third Quarter 2018 Earnings Presentation & Remarks November 1, 2018 1 Forward-looking Statements These slides and remarks are being provided to assist readers in understanding the results of operations,

Third Quarter 2018 Earnings Presentation & Remarks November 1, 2018 1 Forward-looking Statements These slides and remarks are being provided to assist readers in understanding the results of operations,

First Quarter Questions and Answers

First Quarter 2015 Questions and Answers Forward-Looking Statements This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements include

First Quarter 2015 Questions and Answers Forward-Looking Statements This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements include

Months Consolidated Results. 25 April 2016

1 25.04.2016 2016 3 Months Consolidated Results 25 April 2016 2 25.04.2016 DISCLAMIER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about forward-looking

1 25.04.2016 2016 3 Months Consolidated Results 25 April 2016 2 25.04.2016 DISCLAMIER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about forward-looking

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

Aug-12. Oct-13. Dec-14. Feb-16

Feb-2 Apr-3 Jun-4 Aug-5 Oct-6 Feb-9 Apr-1 Jun-11 Aug-12 Feb-16 Dec-1 Dec-2 Dec-3 Dec-4 Dec-5 Dec-6 Richard Farr Jim McGovern U.S. Trading European Trading Chief Market Strategist Market Strategist Tourmaline

Feb-2 Apr-3 Jun-4 Aug-5 Oct-6 Feb-9 Apr-1 Jun-11 Aug-12 Feb-16 Dec-1 Dec-2 Dec-3 Dec-4 Dec-5 Dec-6 Richard Farr Jim McGovern U.S. Trading European Trading Chief Market Strategist Market Strategist Tourmaline

Erdemir Group 2009 Consolidated Financial Results

Erdemir Group 2009 Consolidated Financial Results 22 February 2010 1 /28 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about forward-looking

Erdemir Group 2009 Consolidated Financial Results 22 February 2010 1 /28 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about forward-looking

Erdemir Group Months Consolidated Financial Results

1 / 35 Erdemir Group 2014 9 Months Consolidated Financial Results 28 October 2014 2 / 35 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements

1 / 35 Erdemir Group 2014 9 Months Consolidated Financial Results 28 October 2014 2 / 35 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements

Erdemir Group Months Consolidated Financial Results

1 / 35 Erdemir Group 2014 6 Months Consolidated Financial Results 12 August 2014 2 / 35 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements

1 / 35 Erdemir Group 2014 6 Months Consolidated Financial Results 12 August 2014 2 / 35 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements

Erdemir Group 2011 First Quarter Consolidated Financial Results. 06 May 2011

Erdemir Group 2011 First Quarter Consolidated Financial Results 06 May 2011 2 / 26 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about

Erdemir Group 2011 First Quarter Consolidated Financial Results 06 May 2011 2 / 26 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about

Decline in Economic Activity Larger Than Advance GDP Estimate February 27, 2009

Northern Trust Global Economic Research 5 South LaSalle Chicago, Illinois 663 northerntrust.com Asha G. Bangalore agb3@ntrs.com Decline in Economic Activity Larger Than Advance GDP Estimate February 27,

Northern Trust Global Economic Research 5 South LaSalle Chicago, Illinois 663 northerntrust.com Asha G. Bangalore agb3@ntrs.com Decline in Economic Activity Larger Than Advance GDP Estimate February 27,

Economic Outlook: Global and India. Ajit Ranade IEEMA T & D Conclave December 12, 2014

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Moving On Up Today s Economic Environment

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Section 232 Tariffs on Steel and Aluminum Products. Presentation to the National Association of Steel Pipe Distributors Timothy C.

Section 232 Tariffs on Steel and Aluminum Products Presentation to the National Association of Steel Pipe Distributors Timothy C. Brightbill What Is Section 232? Under Section 232 of the Trade Expansion

Section 232 Tariffs on Steel and Aluminum Products Presentation to the National Association of Steel Pipe Distributors Timothy C. Brightbill What Is Section 232? Under Section 232 of the Trade Expansion

2018 Half Year Results

A GLOBAL LEADER IN METAL FLOW ENGINEERING 2018 Half Year Results 26 July 2018 Patrick André Chief Executive 1 Disclaimer This presentation, which has been prepared by Vesuvius plc (the Company ), includes

A GLOBAL LEADER IN METAL FLOW ENGINEERING 2018 Half Year Results 26 July 2018 Patrick André Chief Executive 1 Disclaimer This presentation, which has been prepared by Vesuvius plc (the Company ), includes

Webcast Third Quarter 2005 Results. Presentation:11/10/05 Paulo Penido Pinto Marques Director of Finance and Investor Relations

Webcast Third Quarter 2005 Results Presentation:11/10/05 Paulo Penido Pinto Marques Director of Finance and Investor Relations Disclaimer Declarations relative to business perspectives of the Company,

Webcast Third Quarter 2005 Results Presentation:11/10/05 Paulo Penido Pinto Marques Director of Finance and Investor Relations Disclaimer Declarations relative to business perspectives of the Company,

Domestic progress overwhelmed by global difficulties

Domestic progress overwhelmed by global difficulties Presentation to The Association of Women in the Metal Industries 2015 Annual Conference Tucson, AZ November 13, 2015 Domestic progress overwhelmed by

Domestic progress overwhelmed by global difficulties Presentation to The Association of Women in the Metal Industries 2015 Annual Conference Tucson, AZ November 13, 2015 Domestic progress overwhelmed by

FY10/3Q Consolidated Results Highlights

February 4, 2011 1 Forward-looking Statement This presentation contains certain forward-looking statements. The Company has tried, whenever possible, to identify these forwardlooking statements using words

February 4, 2011 1 Forward-looking Statement This presentation contains certain forward-looking statements. The Company has tried, whenever possible, to identify these forwardlooking statements using words

United States Steel Corporation

Second Quarter 2016 Earnings Presentation July 26, 2016 2011 Forward-looking Statements These slides and remarks are being provided to assist readers in understanding the results of operations, financial

Second Quarter 2016 Earnings Presentation July 26, 2016 2011 Forward-looking Statements These slides and remarks are being provided to assist readers in understanding the results of operations, financial

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

2008 Economic and Market Outlook

Economic and Market Outlook Presented by: Gareth Watson Warren Jestin Vincent Delisle December 7 Economic Outlook Warren Jestin The Global Economic Landscape is Changing Rapidly Gears Down Emerging Powerhouses

Economic and Market Outlook Presented by: Gareth Watson Warren Jestin Vincent Delisle December 7 Economic Outlook Warren Jestin The Global Economic Landscape is Changing Rapidly Gears Down Emerging Powerhouses

Investor presentation. May 2015

Investor presentation May 2015 Disclaimer Forward-Looking Statements This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements include

Investor presentation May 2015 Disclaimer Forward-Looking Statements This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements include

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR. March Issued: May 2018

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR March 218 Issued: May 218 OVERVIEW OF SECTION 232 Section 232 of the Trade Expansion Act of 1962, as amended, authorizes the President to adjust the imports

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR March 218 Issued: May 218 OVERVIEW OF SECTION 232 Section 232 of the Trade Expansion Act of 1962, as amended, authorizes the President to adjust the imports

FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track -

REVISED to reflect the 2 nd QE for the Apr-Jun Qtr of 2018 FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track - September 10, 2018 Copyright Mizuho Research

REVISED to reflect the 2 nd QE for the Apr-Jun Qtr of 2018 FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track - September 10, 2018 Copyright Mizuho Research

Economic and Market Outlook

Economic and Market Outlook Third Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Economic and Market Outlook Third Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

The External Environment for Developing Countries

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries July 2009 The World Bank Development Economics Prospects Group

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries July 2009 The World Bank Development Economics Prospects Group

Moderate but continued growth expected for global steel demand

PRESS RELEASE Moderate but continued growth expected for global steel demand worldsteel Short Range Outlook October 2017 Brussels, 16 October 2017 - The World Steel Association (worldsteel) today released

PRESS RELEASE Moderate but continued growth expected for global steel demand worldsteel Short Range Outlook October 2017 Brussels, 16 October 2017 - The World Steel Association (worldsteel) today released

JSW Steel Limited Q2 FY Results Presentation October 31, 2017

JSW Steel Limited Q2 FY 2017-18 Results Presentation October 31, 2017 Key highlights Q2 FY18 Standalone performance Crude Steel production: 3.94 million tonnes Saleable Steel sales: 3.92 million tonnes

JSW Steel Limited Q2 FY 2017-18 Results Presentation October 31, 2017 Key highlights Q2 FY18 Standalone performance Crude Steel production: 3.94 million tonnes Saleable Steel sales: 3.92 million tonnes

Financial Presentation 4Q / FY 2017 IFRS Results

Financial Presentation 4Q / FY 217 IFRS Results March 1, 218 Disclaimer No representation or warranty (express or implied) is made as to, and no reliance should be placed on, the fairness, accuracy or

Financial Presentation 4Q / FY 217 IFRS Results March 1, 218 Disclaimer No representation or warranty (express or implied) is made as to, and no reliance should be placed on, the fairness, accuracy or

Core strength, sustainable growth. Lakshmi Mittal, Chairman and CEO Investor Day - 23 September 2011

Core strength, sustainable growth Lakshmi Mittal, Chairman and CEO Investor Day - 23 September 2011 Disclaimer Forward-Looking Statements This document may contain forward-looking information and statements

Core strength, sustainable growth Lakshmi Mittal, Chairman and CEO Investor Day - 23 September 2011 Disclaimer Forward-Looking Statements This document may contain forward-looking information and statements

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013 Overview of recent economic developments Framing the policy choices for the current account and growth in 2014

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013 Overview of recent economic developments Framing the policy choices for the current account and growth in 2014

AFTERSHOCKS. Benjamin Tal, Managing Director, Deputy-Chief Economist CIBC World Markets Inc. Will Investment in Renewable Energy Follow Oil Prices?

, Managing Director, Deputy-Chief Economist CIBC World Markets Inc 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2 Will Investment in Renewable Energy Follow Oil Prices? Source: UNEB, CIBC

, Managing Director, Deputy-Chief Economist CIBC World Markets Inc 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2 Will Investment in Renewable Energy Follow Oil Prices? Source: UNEB, CIBC

Erdemir Group Months Consolidated Financial Results. 11 November 2013

Erdemir Group 2013 9 Months Consolidated Financial Results 11 November 2013 2 / 32 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about

Erdemir Group 2013 9 Months Consolidated Financial Results 11 November 2013 2 / 32 DISCLAIMER Ereğli Demir Çelik Fabrikaları T.A.Ş. (Erdemir) may, when necessary, make written or verbal announcements about

Supply Chain Disruptions

Currencies Supply Chain Disruptions Political Inputs Trade Actions/Dumping Suits Anadarko Drilling Activity Eagle Ford Permian DPR Regions Drilled Completed DUC Drilled Completed DUC Drilled Completed

Currencies Supply Chain Disruptions Political Inputs Trade Actions/Dumping Suits Anadarko Drilling Activity Eagle Ford Permian DPR Regions Drilled Completed DUC Drilled Completed DUC Drilled Completed

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

Summit Strategies Group 8182 Maryland Avenue, 6th Floor St. Louis, Missouri

Summit Strategies Group 8182 Maryland Avenue, 6th Floor St. Louis, Missouri 63105 314.727.7211 Quarterly Review Global Equity Market Update GLOBAL EQUITY MARKETS CALENDAR YEAR RETURNS 2002 2003 2004 2005

Summit Strategies Group 8182 Maryland Avenue, 6th Floor St. Louis, Missouri 63105 314.727.7211 Quarterly Review Global Equity Market Update GLOBAL EQUITY MARKETS CALENDAR YEAR RETURNS 2002 2003 2004 2005

Finally, A Global Tailwind for U.S. Manufacturing Growth

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

TransGraph Research Consulting Technology

Research Consulting Technology Agriculture Metals Energy Dairy Currency Economy Brands Medium term outlook on Lead July 217 2 Market Recap LME Lead remained weak last month but recovered towards the end

Research Consulting Technology Agriculture Metals Energy Dairy Currency Economy Brands Medium term outlook on Lead July 217 2 Market Recap LME Lead remained weak last month but recovered towards the end

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

Financial Presentation 1Q 2017 IFRS Results

Financial Presentation 1Q 217 IFRS Results May 18, 217 Disclaimer No representation or warranty (express or implied) is made as to, and no reliance should be placed on, the fairness, accuracy or completeness

Financial Presentation 1Q 217 IFRS Results May 18, 217 Disclaimer No representation or warranty (express or implied) is made as to, and no reliance should be placed on, the fairness, accuracy or completeness

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR. Data through May Issued: July 2018

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR Data through May 218 Issued: July 218 OVERVIEW OF SECTION 232 Section 232 of the Trade Expansion Act of 1962, as amended, authorizes the President to adjust

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR Data through May 218 Issued: July 218 OVERVIEW OF SECTION 232 Section 232 of the Trade Expansion Act of 1962, as amended, authorizes the President to adjust

FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged -

REVISED to reflect the 2 nd QE for the Oct-Dec Qtr of 2017 FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged - March 8, 2018 Copyright

REVISED to reflect the 2 nd QE for the Oct-Dec Qtr of 2017 FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged - March 8, 2018 Copyright

ThyssenKrupp Steel, London, August ThyssenKrupp Steel

, London, August 2008 0 , London, August 2008 28 Disclaimer The information set forth and included in this presentation is not provided in connection with an offer or solicitation for the purchase or sale

, London, August 2008 0 , London, August 2008 28 Disclaimer The information set forth and included in this presentation is not provided in connection with an offer or solicitation for the purchase or sale

2017 Full Year Results

A GLOBAL LEADER IN METAL FLOW ENGINEERING 2017 Full Year Results 1 March 2018 Patrick André Chief Executive 1 Disclaimer This presentation, which has been prepared by Vesuvius plc (the Company ), includes

A GLOBAL LEADER IN METAL FLOW ENGINEERING 2017 Full Year Results 1 March 2018 Patrick André Chief Executive 1 Disclaimer This presentation, which has been prepared by Vesuvius plc (the Company ), includes

1. Executive Summary Chairman s Message Steel Industry Overview Steel Industry Outlook Standalone Financial Performance 7

Table of Contents 1. Executive Summary 3 2. Chairman s Message 4 3. Steel Industry Overview 5 4. Steel Industry Outlook 6 5. Standalone Financial Performance 7 6. Quarterly Performance Trends 12 7. Graphite

Table of Contents 1. Executive Summary 3 2. Chairman s Message 4 3. Steel Industry Overview 5 4. Steel Industry Outlook 6 5. Standalone Financial Performance 7 6. Quarterly Performance Trends 12 7. Graphite

Power of Travel Promotion Evolution

Power of Travel Promotion Evolution Promotion More Important than Ever Power of Promotion $7 million Median state = marketing budget FY 2014-15 OR 45 seconds worth of Super Bowl ads $100 million = Presidential

Power of Travel Promotion Evolution Promotion More Important than Ever Power of Promotion $7 million Median state = marketing budget FY 2014-15 OR 45 seconds worth of Super Bowl ads $100 million = Presidential

Tariffs, NAFTA, and the Administration

Tariffs, NAFTA, and the Administration Presented by The Franklin Partnership, LLP Policy Resolution Group at Bracewell LLP March 2018 Your Team in Washington, D.C. Lobbying Firm The Franklin Partnership,

Tariffs, NAFTA, and the Administration Presented by The Franklin Partnership, LLP Policy Resolution Group at Bracewell LLP March 2018 Your Team in Washington, D.C. Lobbying Firm The Franklin Partnership,

Interim results briefing. Jyri Luomakoski President and CEO Riitta Palomäki CFO 1 9 / 2016

Interim results briefing Jyri Luomakoski President and CEO Riitta Palomäki CFO 1 9 / 2016 Q3/2016: Performance in Europe improved, supply issues impacted North American business July - September, M Net

Interim results briefing Jyri Luomakoski President and CEO Riitta Palomäki CFO 1 9 / 2016 Q3/2016: Performance in Europe improved, supply issues impacted North American business July - September, M Net

EU steel market situation and outlook. Key challenges

70th Session of the OECD Steel Committee Paris, 12 13 May 2011 EU steel market situation and outlook http://www.eurofer.org/index.php/eng/issues-positions/economic-development-steel-market Key challenges

70th Session of the OECD Steel Committee Paris, 12 13 May 2011 EU steel market situation and outlook http://www.eurofer.org/index.php/eng/issues-positions/economic-development-steel-market Key challenges

Iron Ore & Steel Derivatives Let the Battle Begin

Iron Ore & Steel Derivatives Let the Battle Begin Topics Raw Material Price Volatility Financial Hedging Attributes Iron Ore World Steel Exchange Scrap Presented by: DATE: Tuesday November 30, 2010 Patrick

Iron Ore & Steel Derivatives Let the Battle Begin Topics Raw Material Price Volatility Financial Hedging Attributes Iron Ore World Steel Exchange Scrap Presented by: DATE: Tuesday November 30, 2010 Patrick

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION NOVEMBER 2018 RIYADH, SAUDI ARABIA NOVEMBER 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION NOVEMBER 2018 RIYADH, SAUDI ARABIA NOVEMBER 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

NationalEconomicTrends

NationalEconomicTrends January 00 Stag-nations Economic growth in the United States has slowed substantially since the days of rapid expansion during the mid to late 1990s. According to preliminary estimates,

NationalEconomicTrends January 00 Stag-nations Economic growth in the United States has slowed substantially since the days of rapid expansion during the mid to late 1990s. According to preliminary estimates,

Resilience and potential in emerging markets - Africa & CIS (ACIS) case study

case study") Resilience and potential in emerging markets - & CIS (ACIS) case study Christophe Cornier - Member of the Group Management Board 16 September 2009 Investor day London & New York Disclaimer Forward-Looking

Resilience and potential in emerging markets - & CIS (ACIS) case study Christophe Cornier - Member of the Group Management Board 16 September 2009 Investor day London & New York Disclaimer Forward-Looking

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION AUGUST 2018 RIYADH, SAUDI ARABIA AUGUST 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

COMPARATIVE ANALYSIS OF MONTHLY REPORTS ON THE OIL MARKET AN INTERNATIONAL ENERGY FORUM PUBLICATION AUGUST 2018 RIYADH, SAUDI ARABIA AUGUST 2018 SUMMARY FINDINGS FROM A COMPARISON OF DATA AND FORECASTS

We Distribute Products That Deliver Energy to the World. NOW Inc., Fourth Quarter and Full-Year 2017 Review & Key Takeaways

We Distribute Products That Deliver Energy to the World NOW Inc., Fourth Quarter and Full-Year 2017 Review & Key Takeaways Forward Looking Statements Statements made in the course of this presentation

We Distribute Products That Deliver Energy to the World NOW Inc., Fourth Quarter and Full-Year 2017 Review & Key Takeaways Forward Looking Statements Statements made in the course of this presentation

Eurozone Economic Watch. February 2018

Eurozone Economic Watch February 2018 Eurozone: Strong growth continues in 1Q18, but confidence seems to peak GDP growth moderated slightly in, but there was an upward revision to previous quarters. Available

Eurozone Economic Watch February 2018 Eurozone: Strong growth continues in 1Q18, but confidence seems to peak GDP growth moderated slightly in, but there was an upward revision to previous quarters. Available

Demand, supply, prices and geography

Deutsche Bank Markets Research Asia China Energy Industry Date 6 August 2014 Industry Update Demand, supply, prices and geography Getting our head around China's market for fertilizers We source this data

Deutsche Bank Markets Research Asia China Energy Industry Date 6 August 2014 Industry Update Demand, supply, prices and geography Getting our head around China's market for fertilizers We source this data

2QFY14 Results Presentation

2QFY14 Results Presentation 1 Key highlights 3QFY14 Standalone performance Consolidated performance Key update Highest ever Crude Steel production: 3.19 million tonnes Gross Turnover: `12,651 crores Net

2QFY14 Results Presentation 1 Key highlights 3QFY14 Standalone performance Consolidated performance Key update Highest ever Crude Steel production: 3.19 million tonnes Gross Turnover: `12,651 crores Net

RECESSION AND RECOVERY IN MISSOURI AND THE U.S.

RECESSION AND RECOVERY IN MISSOURI AND THE U.S. Alison Felix Senior Economist Federal Reserve Bank of Kansas City The views expressed are those of the presenter and do not necessarily reflect the positions

RECESSION AND RECOVERY IN MISSOURI AND THE U.S. Alison Felix Senior Economist Federal Reserve Bank of Kansas City The views expressed are those of the presenter and do not necessarily reflect the positions

Auscap Long Short Australian Equities Fund Newsletter August 2015

Auscap Asset Management Limited Disclaimer: This newsletter contains performance figures and information in relation to the from inception of the Fund. The actual performance for your account will be provided

Auscap Asset Management Limited Disclaimer: This newsletter contains performance figures and information in relation to the from inception of the Fund. The actual performance for your account will be provided

Monetary Policy under Fed Normalization and Other Challenges

Javier Guzmán Calafell, Deputy Governor, Banco de México* Santander Latin America Day London, June 28 th, 2018 */ The opinions and views expressed in this document are the sole responsibility of the author

Javier Guzmán Calafell, Deputy Governor, Banco de México* Santander Latin America Day London, June 28 th, 2018 */ The opinions and views expressed in this document are the sole responsibility of the author

Transforming tomorrow

Transforming tomorrow Bank of America Merrill Lynch Global Metals and Mining Conference May 2010 Disclaimer Forward-Looking Statements This document may contain forward-looking information and statements

Transforming tomorrow Bank of America Merrill Lynch Global Metals and Mining Conference May 2010 Disclaimer Forward-Looking Statements This document may contain forward-looking information and statements

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY. RUSSIA S ECONOMIC OUTLOOK AND MONETARY POLICY December 2018

4% RUSSIA S ECONOMIC OUTLOOK AND December 1 2 Consumer prices (1) At the end of 1, inflation is expected to be close to 4%, which corresponds to the Bank of Russia s target 2 Inflation indicators, % YoY

4% RUSSIA S ECONOMIC OUTLOOK AND December 1 2 Consumer prices (1) At the end of 1, inflation is expected to be close to 4%, which corresponds to the Bank of Russia s target 2 Inflation indicators, % YoY

1QFY14 Results Presentation

1QFY14 Results Presentation 1 Key highlights 1QFY14 Standalone performance Consolidated performance JSW Steel JSW Ispat merger update Highest ever Crude Steel production: 2.86 million tonnes Saleable Steel

1QFY14 Results Presentation 1 Key highlights 1QFY14 Standalone performance Consolidated performance JSW Steel JSW Ispat merger update Highest ever Crude Steel production: 2.86 million tonnes Saleable Steel

Global Markets Group. Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist. Economic Research. Trade Outlook Monthly Report

Global Markets Group Trade Outlook Monthly Report Economic Research August 2016 Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist Trade Highlights Exports in June 2016 rose

Global Markets Group Trade Outlook Monthly Report Economic Research August 2016 Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist Trade Highlights Exports in June 2016 rose

Single-family home sales and construction are not expected to regain 2005 peaks

Single-family home sales and construction are not expected to regain 25 peaks Millions of units 8. 7. 6. 5. Housing starts (right axis) 4. Home sales (left axis) 3. 2. 1. 198 1985 199 1995 2 25 21 215

Single-family home sales and construction are not expected to regain 25 peaks Millions of units 8. 7. 6. 5. Housing starts (right axis) 4. Home sales (left axis) 3. 2. 1. 198 1985 199 1995 2 25 21 215

June Todd Hale James Russo Jonathan Banks Jean-Jacques Vandenheede

June 20 Todd Hale James Russo Jonathan Banks JeanJacques Vandenheede Nielsen Global Scorecard Shopping measures appear to be trending upward, driven by gains in China, India, Canada and the U.S., with

June 20 Todd Hale James Russo Jonathan Banks JeanJacques Vandenheede Nielsen Global Scorecard Shopping measures appear to be trending upward, driven by gains in China, India, Canada and the U.S., with

Financial Markets Fall 2008 Economic Update

Financial Markets Fall 28 Economic Update October 7, 28 Jeff Rubin Chief Economist, Chief Strategist Avery Shenfeld Managing Director, Senior Economist Crash in Commodity Prices Exaggerates Growth Slowdown

Financial Markets Fall 28 Economic Update October 7, 28 Jeff Rubin Chief Economist, Chief Strategist Avery Shenfeld Managing Director, Senior Economist Crash in Commodity Prices Exaggerates Growth Slowdown

BUSINESS YEAR 2009 RESULTS

BUSINESS YEAR 2009 RESULTS Madrid, 26 February 2010 WORLD PRODUCTION OF STAINLESS STEEL Thousand Mt. 30,000 28,000 26,000 24,000 22,000 20,000 18,000 16,000 14,000 12,000 10,000 8,000 6,000 4,000 2,000

BUSINESS YEAR 2009 RESULTS Madrid, 26 February 2010 WORLD PRODUCTION OF STAINLESS STEEL Thousand Mt. 30,000 28,000 26,000 24,000 22,000 20,000 18,000 16,000 14,000 12,000 10,000 8,000 6,000 4,000 2,000

Investor Presentation. Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG)

") Investor Presentation Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG) Agenda Outlook Gerdau Highlights 2 Economic Outlook GDP Growth 2014 2015f 2016f World 3.4% 3.1% 3.4%

Investor Presentation Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG) Agenda Outlook Gerdau Highlights 2 Economic Outlook GDP Growth 2014 2015f 2016f World 3.4% 3.1% 3.4%

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

Q2 FY2014 Earnings Presentation November 8, 2013

Q2 FY2014 Earnings Presentation November 8, 2013 Important Notice Forward Looking Statements This presentation contains statements that contain forward looking statements including, but without limitation,

Q2 FY2014 Earnings Presentation November 8, 2013 Important Notice Forward Looking Statements This presentation contains statements that contain forward looking statements including, but without limitation,

Second Quarter 2018 Questions and Answers

Second Quarter 2018 Questions and Answers Page 1 Forward-Looking Statements This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements

Second Quarter 2018 Questions and Answers Page 1 Forward-Looking Statements This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements

The External Environment for Developing Countries

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries January 2009 The World Bank Development Economics Prospects Group

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries January 2009 The World Bank Development Economics Prospects Group

Forecasting Emerging Markets Equities the Role of Commodity Beta

Forecasting Emerging Markets Equities the Role of Commodity Beta Huiyu(Evelyn) Huang Grantham, Mayo, Van Otterloo& Co., LLC June 23, 215 For presentation at ISF 215. The opinions expressed here are solely

Forecasting Emerging Markets Equities the Role of Commodity Beta Huiyu(Evelyn) Huang Grantham, Mayo, Van Otterloo& Co., LLC June 23, 215 For presentation at ISF 215. The opinions expressed here are solely

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

FY2018, FY2019 Economic Outlook - Despite slower growth in 2019, the economy should remain firm. Keep a close eye upon the rise of uncertainties -

Summary FY2018, FY2019 Economic Outlook - Despite slower growth in 2019, the economy should remain firm. Keep a close eye upon the rise of uncertainties - November 15, 2018 Copyright Mizuho Research Institute

Summary FY2018, FY2019 Economic Outlook - Despite slower growth in 2019, the economy should remain firm. Keep a close eye upon the rise of uncertainties - November 15, 2018 Copyright Mizuho Research Institute

Chapter 1 International economy

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

TUBOS REUNIDOS GROUP. Special Products & Integral Services Worldwide. Tubos Reunidos. November 2014

Special Products & Integral Services Worldwide Tubos Reunidos 1 Content Tubos Reunidos Group 1. Market and Trends 2. Company Overview 3. 2014 2017 Strategic Plan 4. Financials 2 Tubos Reunidos Group Seamless

Special Products & Integral Services Worldwide Tubos Reunidos 1 Content Tubos Reunidos Group 1. Market and Trends 2. Company Overview 3. 2014 2017 Strategic Plan 4. Financials 2 Tubos Reunidos Group Seamless

The Long Journey to Recovery. Russia Economic Report April 2016 Edition No. 35

The Long Journey to Recovery Russia Economic Report April 216 Edition No. 35 1 2 3 The anticipated recovery was delayed and the economy adjusted through a sharp income drop. The government s policy response

The Long Journey to Recovery Russia Economic Report April 216 Edition No. 35 1 2 3 The anticipated recovery was delayed and the economy adjusted through a sharp income drop. The government s policy response

Mexico Economic Outlook 3Q18. August 2018

Mexico Economic Outlook 3Q18 August 2018 Key messages Global growth continues, but risks are intensifying. The economy grew 2.1% in the first half of the year. Downward bias in our growth forecast for

Mexico Economic Outlook 3Q18 August 2018 Key messages Global growth continues, but risks are intensifying. The economy grew 2.1% in the first half of the year. Downward bias in our growth forecast for

Trade and Economic Trends Evolving Patterns and Attitudes

Trade and Economic Trends Evolving Patterns and Attitudes Paul Bingham AAPA Marine Terminal Management Training Program Long Beach California October 1, 2018 World Economic Growth Increasing Emerging Markets

Trade and Economic Trends Evolving Patterns and Attitudes Paul Bingham AAPA Marine Terminal Management Training Program Long Beach California October 1, 2018 World Economic Growth Increasing Emerging Markets

Monthly Rolling Economic Electronic Presentation August 2017

CHILE AT A GLANCE Monthly Rolling Economic Electronic Presentation August 2017 CURRENT ECONOMIC PERFORMANCE GDP GROWTH (% over same quarter previous year) 3 2,5 2 1,5 1 0,5 0 QIV 2014 QI 2015 QII 2015

CHILE AT A GLANCE Monthly Rolling Economic Electronic Presentation August 2017 CURRENT ECONOMIC PERFORMANCE GDP GROWTH (% over same quarter previous year) 3 2,5 2 1,5 1 0,5 0 QIV 2014 QI 2015 QII 2015

Ferrochrome Market Overview 2017

Ferrochrome Market Overview 217 Presented by: Mark Beveridge Principal Consultant CRU Nickel, Chrome, Stainless Steel Group Key Themes Which factors define the chrome market? 1. Chinese demand and the

Ferrochrome Market Overview 217 Presented by: Mark Beveridge Principal Consultant CRU Nickel, Chrome, Stainless Steel Group Key Themes Which factors define the chrome market? 1. Chinese demand and the

Global Markets Group. Trade Performance: Narrowing Surplus Author: Juniman Chief Economist. Economic Research. Trade Outlook Monthly Report

Global Markets Group Trade Outlook Monthly Report Economic Research November 2016 Trade Performance: Narrowing Surplus Author: Juniman Chief Economist Trade Highlights Exports in September 2016 fell to

Global Markets Group Trade Outlook Monthly Report Economic Research November 2016 Trade Performance: Narrowing Surplus Author: Juniman Chief Economist Trade Highlights Exports in September 2016 fell to

Third Quarter 2018 Financial Results

Third Quarter 2018 Financial Results October 26, 2018 C r e a t i n g I n n o v a t i v e S t e e l S o l u t i o n s AK Steel Executive Management Team Roger Newport Kirk Reich Jaime Vasquez Chief Executive

Third Quarter 2018 Financial Results October 26, 2018 C r e a t i n g I n n o v a t i v e S t e e l S o l u t i o n s AK Steel Executive Management Team Roger Newport Kirk Reich Jaime Vasquez Chief Executive

SEPTEMBER Overview

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

JSW Steel Limited 2QFY16 Results Presentation October 21, 2015

JSW Steel Limited 2QFY16 Results Presentation October 21, 2015 Key highlights 2QFY16 Standalone performance Highest ever quarterly Saleable Steel sales: 3.19 million tonnes Crude Steel production: 3.25

JSW Steel Limited 2QFY16 Results Presentation October 21, 2015 Key highlights 2QFY16 Standalone performance Highest ever quarterly Saleable Steel sales: 3.19 million tonnes Crude Steel production: 3.25

Moderating External Trade Caused IPI to Hit 3-Month Low at 3%

12 July 2018 ECONOMIC REVIEW May 2018 Industrial Production Index Moderating External Trade Caused IPI to Hit 3-Month Low at 3% IPI meets market estimates. Malaysia s industrial production expands by 3%yoy

12 July 2018 ECONOMIC REVIEW May 2018 Industrial Production Index Moderating External Trade Caused IPI to Hit 3-Month Low at 3% IPI meets market estimates. Malaysia s industrial production expands by 3%yoy

First Quarter 2018 Earnings Presentation & Remarks

First Quarter 2018 Earnings Presentation & Remarks April 26, 2018 1 Forward-looking Statements These slides and remarks are being provided to assist readers in understanding the results of operations,

First Quarter 2018 Earnings Presentation & Remarks April 26, 2018 1 Forward-looking Statements These slides and remarks are being provided to assist readers in understanding the results of operations,