SEPTEMBER Overview

|

|

|

- Dominic Stanley

- 5 years ago

- Views:

Transcription

1 Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1). Among major emerging markets, growth in the first half of the year has been broadly steady. In Q3, industrial production continues to be more robust in developing countries, and there appears to be early signs of a recovery among high-income countries (Figure 2). A modest pickup in global growth is expected in the second half of 214 raising annual growth to around [2.8] percent in 214 and an average of [3.5] percent in In developing countries, growth is expected to remain below its long-run average in most regions (Figure 3). Recent Developments in High-Income Countries. Among high-income countries growth has diverged. Growth in the United States has been gathering momentum while the Euro Area and Japan appear to be stagnating. Supported by rising employment and investment growth, and a still accommodative monetary policy stance, U.S. growth recovered strongly in Q2 from a sharp contraction in Q1. The recovery in the US economy is expected to gather pace in H2 214 as better employment prospects support real income growth and confidence, fiscal consolidation pressures ease, and investment rises in line with strong profit and favorable financing conditions. GDP growth for 214 is projected at about 2. percent, and picking-up above trend in 215 to around 3. percent. Meanwhile, with the strength of the recovery continuing to be impaired by weak domestic demand, the Euro Area GDP was flat in Q2, following a small uptick in Q1. A slow improvement in credit and labor market conditions should provide some momentum ahead, but investment prospects remain subdued and precautionary savings still high. Exports should gradually pickup, supported by strengthening demand from the U.S. and a weakening euro. Growth is expected to resume in H2, with overall growth for 214 projected to reach about 1 percent. In Japan, a sales tax hike in April caused a more significant contraction in activity than initially expected, while exports failed to pick-up despite a weak yen. Monetary policy accommodation and reform commitments will provide ongoing support, but fiscal consolidation is expected to keep domestic demand subdued throughout 215, with exports only recovering slowly. Real GDP growth is projected to around 1 percent in 214, down from 1.5 percent in 213. Global trade. Global trade was an important engine of growth for the world economy in the precrisis period, but has remained relatively subdued since 211. Weighed down by weakness in high-income countries (accounting for some two-thirds of global imports), global trade growth in the first six months of 214 continued on its weak pre-crisis trend. The projected pick-up in high Developing Trends was prepared by the Development Economics Prospects Group (DECPG) of the World Bank. This note reflects the views of the group, but is not formally cleared by the World Bank.

2 SEPTEMBER 214 -income economic activity is expected to lift trade growth modestly. This should provide some impetus to developing countries, particularly those for whom the U.S is a major trading partner. Financial Markets. Notwithstanding a weak start to the year, equity markets have risen to alltime highs and government bond yields have fallen to record lows. U.S. and U.K. benchmark stock indices, in particular, have risen to record highs on the back of strengthening macro data, accommodative U.S. monetary policy, and credit easing by the ECB expected to begin in October. The ECB s announced policy measures contributed to the observed weakening of the euro against the dollar in recent months. This has generated capital flows into U.S. long-term bond markets but also riskier assets such as emerging market stock and bond markets. The continued accommodative monetary stance of ECB could help counteract the global impact of eventual monetary tightening in the U.S. Capital Flows. Capital flows to developing countries, which weakened in early 214 in a market sell-off but resumed strongly since March, are up 14 percent from a year earlier (Figure 4). Much of this increase reflects bond issuance by Chinese issuers, which account for an unprecedented quarter of all developing-country bond issuance. More generally, year-to-date gross capital flows have increased to developing countries in all regions, except Europe and Central Asia where bank flows have dropped sharply, partly as a result of tensions in Ukraine and sanctions on Russia (Figure 5). Commodity Markets. Despite intensification of violence in Iraq and the conflict in Ukraine, oil prices moderated further in August to $1/bbl down from $15/bbl in July. Robust supply prospects due to increased output from Iraq, Libya and the U.S., along with weak economic data for China and Europe supported the weakening of oil prices. Signs of a mostly solid crop season kept agricultural prices broadly stable. Rice has proven to be the strong exception with prices up 12 percent since June, largely due to lower inventories in India and Thailand, which are key global rice suppliers. Meanwhile, the metal price index remained unchanged in August after gaining 5 percent in July. However, a major slowdown in China's construction sector (the world s largest metal consumer) could exert further heavy downward pressure on some metal prices such as iron ore and copper, hurting such metal exporters. Risks. Developing countries face risks from monetary policy tightening in the U.S., deflation in the Euro Area, and geopolitical tensions or public health threats in a number of regions. Monetary policy in high-income countries is expected to diverge. The U.S. Federal Reserve is projected to start raising policy rates in mid-215, which carries the risk of bouts of financial market volatility. In contrast, in the Euro Area where inflation continues to drift down, deflation risks are increasing and the ECB has announced additional easing measures. In Japan, where inflation expectations are still weakly anchored, loose monetary policy is projected to continue. Developing countries are vulnerable to bouts of financial market disruptions as a result of changes in monetary policy in high-income countries or weakening investor sentiment if geopolitical tensions (e.g., in Russia or Iraq) or health concerns (e.g. from the Ebola virus in West Africa, Figure 6) escalate. In addition, investor sentiment could suffer if a rapid unwinding of Chinese debt leads to sharp deleveraging.

3 Figure 1. GDP outcomes disappointed across major high-income countries GDP growth, annualized, percent USA Japan Euro Area Developing, Haver Analytics Figure 3. Developing country growth forecast below historical averages 1 Real GDP growth, percent Figure 5. Capital flows remained robust in 214., Bloomberg 213H1 213H2 214H EAP LAC ECA SAS SSA MNA $ billion 16 Equity Bond Bank * * EAP ECA LAC MENA SA SSA * For the first eight months of the year Figure 2. Industrial production in developing countries is more robust IP growth y/y percent M1 213 M3 213 M5, Haver Analytics Figure 4. Capital inflows to developing countries remain dynamic billion $ Jan-13 Mar-13 May-13, Dealogic Figure 6. Impact of 1 percentage point decline in Russian GDP on growth of neighbors % -1 Baltics Kazakhstan 213 M7 Jul-13 range mid-point Turkey 213 M9 Sep-13 World High income countries Developing countries 213 M11 Nov M1 Jan M3 Bond issuances New bank loans Equity issuance Slovak/Sloven Belarus Mar-14 Tajikistan 214 M5 May M7

4 Major Data Releases Fri, 29 August - Fri 19 Sep, 214 Upcoming releases: Mon, 22 Sep 214- Fri, 3 Oct 214 Country Date Indicator PeriodActual Forecast Previous Country Date Indicator Period Previous Indonesia 8/31/214 PMI Manufacturing AUG Mexico 9/22/214 Unemployment Rate AUG 5.19% Thailand 9/1/214 Core CPI (Y-o-Y) AUG 1.8% 1.8% 1.8% China 9/22/214 PMI Manufacturing SEP P 5.2 Turkey 9/1/214 PMI Manufacturing AUG Eurozone 9/23/214 PMI Composite SEP P 52.5 Mexico 9/1/214 PMI Manufacturing AUG Brazil 9/24/214 Current Account Balance - BoP AUG $ -6.2 B Brazil 9/2/214 Industrial Production (Y-o-Y) JUL -3.6% -3.9% -6.9% Malaysia 9/25/214 Unemployment Rate JUL 2.7% United States 9/2/214 ISM Manufacturing Survey AUG Turkey 9/25/214 Interest Rate Decision % Brazil 9/3/214 Interest Rate Decision - 11.% 11% 11.% United States 9/25/214 Durable Goods Orders (M-o-M) AUG 22.6% India 9/3/214 PMI Composite AUG Germany 9/26/214 GfK Consumer Confidence Survey OCT 8.6 Hungary 9/3/214 GDP (Q-o-Q) Q2 F.8% 1.1% United States 9/26/214 GDP (Q-o-Q) Q2-2.1% Romania 9/3/214 GDP (Q-o-Q) Q2-1.%.2% Argentina 9/26/214 Current Account Balance - BoP Q2 $ -3.3 B United States 9/5/214 Unemployment Rate AUG 6.1% 6.12% 6.2% Eurozone 9/29/214 Flash CPI - EU Harmonised (Yo-Y) SEP.3% Japan 9/7/214 GDP (Y-o-Y) Q2 F -7.1% -7.% -6.8% Eurozone 9/29/214 Unemployment Rate AUG 11.5% China 9/7/214 Exports AUG 9.4% -6.% 14.58% Japan 9/29/214 Unemployment Rate AUG 3.8% Russia 9/8/214 GDP (Y-o-Y) Q2.8%.9% Romania 9/3/214 Interest Rate Decision % Turkey 9/8/214 Industrial Production (Y-o-Y) JUL 3.6% 1.3% 1.4% Germany 9/3/214 Retail Sales (Y-o-Y) AUG.7% Turkey 9/1/214 GDP (Q-o-Q) Q2 -.5% -1.% 1.7% France 9/3/214 Consumer Spending (Y-o-Y) JUL 1.8% Philippines 9/1/214 Unemployment Rate Q2 6.7% 7.% Turkey 9/3/214 Trade Balance AUG $ B Malaysia 9/11/214 Industrial Production (Y-o-Y) JUL.5% 4.5% 7.% Thailand 9/3/214 Current Account Balance - BoP AUG $ -.86 B Mexico 9/11/214 Industrial Production (M-o-M) JUL.28%.4% -.17 (R) % South Africa 9/3/214 Trade Balance AUG ZAR B Japan 9/12/214 Industrial Production (M-o-M) JUL F.2% -3.4% Indonesia 1/1/214 Trade Balance AUG $.13 B Eurozone 9/12/214 Industrial Production (Y-o-Y) JUL 1.1%.% India 1/1/214 PMI Manufacturing SEP 52.4 India 9/12/214 Industrial Production (Y-o-Y) JUL 3.5% 3.4% Turkey 1/1/214 PMI Manufacturing SEP 5.3 Argentina 9/12/214 CPI (M-o-M) AUG 1.4% Romania 1/1/214 GDP (Q-o-Q) Q2-1.% Turkey 9/15/214 Unemployment Rate JUN 9.5% Eurozone 1/1/214 PMI Manufacturing SEP 5.7 United States 9/15/214 Industrial Production (Y-o-Y) AUG 5.% Brazil 1/1/214 PMI Manufacturing SEP 5.2 Eurozone 9/17/214 CPI (Y-o-Y) AUG.4% Brazil 1/1/214 Trade Balance SEP $.13 B United States 9/17/214 Current Account Balance - BoP Q2 $ B Japan 1/1/214 PMI Composite SEP 5.8 South Africa 9/18/214 Interest Rate Decision % Brazil 1/2/214 Industrial Production (Y-o-Y) AUG -3.6% Philippines 9/19/214 Current Account Balance - BoP Q2 $ 1.96 B Malaysia 1/3/214 Trade Balance AUG MYR 3.64 B Turkey 1/3/214 CPI (Y-o-Y) SEP 9.54% South Africa 1/3/214 PMI Manufacturing SEP 51.1

3.")

12")

5 SEPTEMBER 214 High-income Real Economy Industrial Production Financial Markets G-3 stock markets Manufacturing PMIs U.S. and German bond yields Yield (percent) 3.5 US 3 German Mar 13 Jun 13 Sep 13 Dec 13 Mar 14 Jun 14 Sep 14 Source: Markit Economics, World Bank Inflation Yields on 1-year government bonds Yield (percent) Portugal Spain 4 3 Italy 2 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14

")

and Markit")

")

6 SEPTEMBER 214 Industrial Activity Industrial Production Global IP growth Business Sentiment Manufacturing Purchasing Managers Index (PMI) Regional IP growth: EAP, ECA, LAC and Markit. PMI Indexes in selected countries (1) and Markit Regional IP growth: MENA, SAS, SSA PMI Indexes in selected countries (2) and Markit

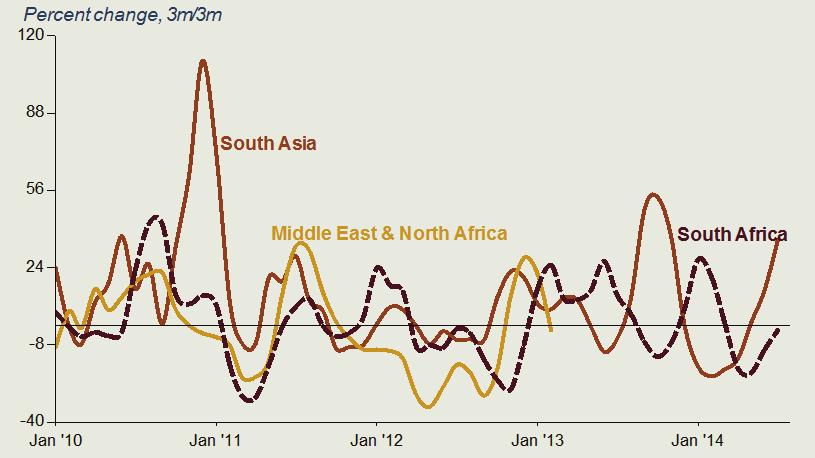

7 SEPTEMBER 214 International Trade Imports Global Import Volumes Exports Global Export Volumes Regional Import Volumes: EAP, ECA, LAC Regional Export Volumes: EAP, ECA, LAC Regional Import Volumes: MENA, SAS, SSA Export volumes for selected economies

Maize")

8 SEPTEMBER 214 Commodities Oil and Metals Crude Oil Prices Agriculture Stock-to-use ratios Metals Prices Source: US Department of Agriculture (July 214) Maize and wheat prices Precious Metals Prices Coffee prices

5 6 5 45")

9 SEPTEMBER 214 Finance Credit and Equity Markets 5-year sovereign CDS spreads for developing countries Capital Flows Developing-country sovereign bond spreads since 211 basis points 7 (JP Morgan EMBIG spreads, basis points ) Average Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14. MSCI stock market indices 25 EM sovereign bond spreads 2 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 and JPMorgan. Foreign portfolio inflows to developing countries $ billions EM Fixed Income Funds EM Equity Funds 5 Jan Jul Jan Jul Jan Jul Jan Jul. MSCI stock market indices developing regions and EPFR. Gross capital flows to developing countries. and Dealogic.

10 SEPTEMBER 214 Exchange Rate & Inflation Exchange Rates Euro, US dollar and Yen Source: Haver, IFS Inflation Developing and high income inflation Prospects Group; IMF IFS. NERs of selected developing country currencies Inflation in EAP, ECA and LAC Source: Haver, IFS Prospects Group; IMF IFS. NEERs of selected developing country currencies Inflation in MENA, SAS and SSA Source: Haver, IFS Source: Prospects Group; IMF IFS.

Global Economic Prospects. South Asia. June 2014 Andrew Burns

Global Economic Prospects South Asia June 214 Andrew Burns Main Messages 214 Global forecast has been downgraded, mainly reflecting one-off factors Financing conditions have eased temporarily, but are

Global Economic Prospects South Asia June 214 Andrew Burns Main Messages 214 Global forecast has been downgraded, mainly reflecting one-off factors Financing conditions have eased temporarily, but are

Global Monthly April 2018

Global Monthly April 2018 US$, billions 500 400 300 200 100 Total Potentially impacted by new tariffs 0 China exports to U.S. U.S. exports to China Monthly Highlights Global economy: maturing upturn, gradual

Global Monthly April 2018 US$, billions 500 400 300 200 100 Total Potentially impacted by new tariffs 0 China exports to U.S. U.S. exports to China Monthly Highlights Global economy: maturing upturn, gradual

Global Outlook. October 22, M. Marc Stocker DEC-Development Prospects Group

Global Outlook October 22, 214 M. Marc Stocker DEC-Development Prospects Group mstocker1@worldbank.org 1 About Growth Forecasts Public release of growth forecasts in the Global Economic Prospects in June

Global Outlook October 22, 214 M. Marc Stocker DEC-Development Prospects Group mstocker1@worldbank.org 1 About Growth Forecasts Public release of growth forecasts in the Global Economic Prospects in June

The External Environment for Developing Countries

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries July 2009 The World Bank Development Economics Prospects Group

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries July 2009 The World Bank Development Economics Prospects Group

World Economic Outlook. Recovery Strengthens, Remains Uneven April

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

National Monetary Policy Forum. Chris Loewald, Head: Policy Development and Research 10 April 2016 Pretoria

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Global Economic Prospects: Update Global Recovery in Transition

Global Economic Prospects: Update Global Recovery in Transition April 2015 M. Ayhan Kose 1 Global Prospects: Three Questions 1. How have global economic conditions changed since December? Broadly as expected;

Global Economic Prospects: Update Global Recovery in Transition April 2015 M. Ayhan Kose 1 Global Prospects: Three Questions 1. How have global economic conditions changed since December? Broadly as expected;

World Economic outlook

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Caucasus and Central Asia Regional Economic Outlook October 2011

Regional Economic Outlook October 211 Oil and gas exporters Oil and gas importers Kazakhstan Georgia Uzbekistan Kyrgyz Republic Armenia Azerbaijan Turkmenistan Tajikistan Overview Global outlook (CCA)

Regional Economic Outlook October 211 Oil and gas exporters Oil and gas importers Kazakhstan Georgia Uzbekistan Kyrgyz Republic Armenia Azerbaijan Turkmenistan Tajikistan Overview Global outlook (CCA)

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Eurozone Economic Watch

BBVA Research - Global Economic Watch December 2018 / 1 Eurozone Economic Watch December 2018 Eurozone GDP growth still slows gradually, but high uncertainty could take its toll GDP growth could grow by

BBVA Research - Global Economic Watch December 2018 / 1 Eurozone Economic Watch December 2018 Eurozone GDP growth still slows gradually, but high uncertainty could take its toll GDP growth could grow by

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing Divergence in emergers monetary policy This year economic activity across the emergers has been subdued but inflation has generally remained moderate, allowing

Emerging Markets Weekly Economic Briefing Divergence in emergers monetary policy This year economic activity across the emergers has been subdued but inflation has generally remained moderate, allowing

The External Environment for Developing Countries

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries January 2009 The World Bank Development Economics Prospects Group

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries January 2009 The World Bank Development Economics Prospects Group

Eurozone Economic Watch

BBVA Research Eurozone Economic Watch November 2018 / 1 Eurozone Economic Watch November 2018 Eurozone: Growth to recover in 4Q18, but concerns about the slowdown next year are growing Eurozone GDP growth

BBVA Research Eurozone Economic Watch November 2018 / 1 Eurozone Economic Watch November 2018 Eurozone: Growth to recover in 4Q18, but concerns about the slowdown next year are growing Eurozone GDP growth

HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES

Key Points HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES Global growth has moderated, and it is expected to slow from 3 percent in 18 to.9 percent in. International trade and manufacturing

Key Points HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES Global growth has moderated, and it is expected to slow from 3 percent in 18 to.9 percent in. International trade and manufacturing

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

WTO lowers forecast after sub-par trade growth in first half of 2014

PRESS RELEASE PRESS/722 26 September 214 (-) WTO lowers forecast after sub-par trade growth in first half of 214 TRADE STATISTICS WTO economists have reduced their forecast for world trade growth in 214

PRESS RELEASE PRESS/722 26 September 214 (-) WTO lowers forecast after sub-par trade growth in first half of 214 TRADE STATISTICS WTO economists have reduced their forecast for world trade growth in 214

Global Economic Watch

BBVA Research Global Economic Watch July 2018 / 1 Global Economic Watch July 2018 Steady global growth, but risks intensify Our BBVA-GAIN model projects that global growth could remain slightly above 1%

BBVA Research Global Economic Watch July 2018 / 1 Global Economic Watch July 2018 Steady global growth, but risks intensify Our BBVA-GAIN model projects that global growth could remain slightly above 1%

The External Environment for Developing Countries

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries March 2008 The World Bank Development Economics Prospects Group

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries March 2008 The World Bank Development Economics Prospects Group

Global MT outlook: Will the crisis in emerging markets derail the recovery?

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

JUNE 2014 Developing Trends This note reflects the views of the team, but is not formally cleared by the World Bank Group.

Overview Developing Trends was prepared by the Development Economics Prospects Group (DECPG) of the World Bank. The team is coordinated by Allen Dennis (Overview), and is comprised of Tehmina Khan (High-income),

Overview Developing Trends was prepared by the Development Economics Prospects Group (DECPG) of the World Bank. The team is coordinated by Allen Dennis (Overview), and is comprised of Tehmina Khan (High-income),

The External Environment for Developing Countries

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries June 2009 The World Bank Development Economics Prospects Group

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries June 2009 The World Bank Development Economics Prospects Group

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for August 2011 All data are as of Wednesday, August 31, 2011. The regional indices are

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for August 2011 All data are as of Wednesday, August 31, 2011. The regional indices are

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

International Monetary Fund

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

Global Economic Prospects: Navigating strong currents

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Date of Latest Changes

Emerging Capital Markets Update for May 2011 All data are as of Tuesday, May 31, 2011. The regional indices are based on an average of major EM countries in each region where the data are available. Summary

Emerging Capital Markets Update for May 2011 All data are as of Tuesday, May 31, 2011. The regional indices are based on an average of major EM countries in each region where the data are available. Summary

Developing Trends: May 2013

Developing Trends: May 213 Overview Quarterly GDP trends diverge among major economies. Supported by a pick-up in consumption expenditures (3.2 percent, q/q saar) and gross private domestic investment

Developing Trends: May 213 Overview Quarterly GDP trends diverge among major economies. Supported by a pick-up in consumption expenditures (3.2 percent, q/q saar) and gross private domestic investment

Global Economic Outlook

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Recent developments. Note: The author of this section is Yoki Okawa. Research assistance was provided by Ishita Dugar. 1

Growth in the Europe and Central Asia region is anticipated to ease to 3.2 percent in 2018, down from 4.0 percent in 2017, as one-off supporting factors wane in some of the region s largest economies.

Growth in the Europe and Central Asia region is anticipated to ease to 3.2 percent in 2018, down from 4.0 percent in 2017, as one-off supporting factors wane in some of the region s largest economies.

Eurozone Economic Watch. November 2017

Eurozone Economic Watch November 2017 Eurozone: improved outlook, still subdued inflation Our MICA-BBVA model for growth estimates for the moment a quarterly GDP figure of around -0.7% in, after % QoQ

Eurozone Economic Watch November 2017 Eurozone: improved outlook, still subdued inflation Our MICA-BBVA model for growth estimates for the moment a quarterly GDP figure of around -0.7% in, after % QoQ

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO)

") Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for July 2011 All data are as of Friday, July 29, 2011. The regional indices are based

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for July 2011 All data are as of Friday, July 29, 2011. The regional indices are based

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

Global Economic Prospects

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

GLOBAL OUTLOOK ECONOMIC WATCH. July 2017

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

Eurozone Economic Watch. May 2018

Eurozone Economic Watch May 2018 BBVA Research - Eurozone Economic Watch / 2 Eurozone: more moderate growth with higher uncertainty The eurozone GDP growth slowed in more than expected. Beyond temporary

Eurozone Economic Watch May 2018 BBVA Research - Eurozone Economic Watch / 2 Eurozone: more moderate growth with higher uncertainty The eurozone GDP growth slowed in more than expected. Beyond temporary

OUTLOOK 2014/2015. BMO Asset Management Inc.

OUTLOOK 2014/2015 BMO Asset Management Inc. We would like to take this opportunity to provide our capital markets outlook for the remainder of 2014 and the first half of 2015 and our recommended asset

OUTLOOK 2014/2015 BMO Asset Management Inc. We would like to take this opportunity to provide our capital markets outlook for the remainder of 2014 and the first half of 2015 and our recommended asset

Regional Economic Outlook

Regional Economic Outlook Caucasus and Central Asia Azim Sadikov International Monetary Fund Resident Representative November 6, 2013 Outline Global Outlook CCA: Recent Developments, Outlook, and Risks

Regional Economic Outlook Caucasus and Central Asia Azim Sadikov International Monetary Fund Resident Representative November 6, 2013 Outline Global Outlook CCA: Recent Developments, Outlook, and Risks

The real change in private inventories added 0.22 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute November 2018 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute November 2018 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

eregionaloutlooksincharts

eregionaloutlooksincharts (clickonregion) EastAsiaandPaci c EuropeandCentralAsia LatinAmericaandtheCaribbean MiddleEastandNorthAfrica SouthAsia Sub-SaharanAfrica The Economic Outlook for East Asia and

eregionaloutlooksincharts (clickonregion) EastAsiaandPaci c EuropeandCentralAsia LatinAmericaandtheCaribbean MiddleEastandNorthAfrica SouthAsia Sub-SaharanAfrica The Economic Outlook for East Asia and

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

Snapshot of SA Economy

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

GLOBAL FIXED INCOME OVERVIEW

2016 Global Market Outlook Press Briefing GLOBAL FIXED INCOME OVERVIEW Edward A. Wiese, CFA, Head of Fixed Income November 18, 2015 Global Fixed Income Outlook: Summary Environment Developed market yields

2016 Global Market Outlook Press Briefing GLOBAL FIXED INCOME OVERVIEW Edward A. Wiese, CFA, Head of Fixed Income November 18, 2015 Global Fixed Income Outlook: Summary Environment Developed market yields

Short-term indicators and Updated Forecasts. Eurozone NOVEMBER 2016

Short-term indicators and Updated Forecasts Eurozone NOVEMBER 2016 EUROZONE WATCH NOVEMBER 2016 Key messages: resilience and unchanged projections The moderate pace of economic growth continued in the

Short-term indicators and Updated Forecasts Eurozone NOVEMBER 2016 EUROZONE WATCH NOVEMBER 2016 Key messages: resilience and unchanged projections The moderate pace of economic growth continued in the

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Macroeconomic and financial market developments. March 2014

Macroeconomic and financial market developments March 2014 Background material to the abridged minutes of the Monetary Council meeting 25 March 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013 on

Macroeconomic and financial market developments March 2014 Background material to the abridged minutes of the Monetary Council meeting 25 March 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013 on

Developing Countries to Remain Resilient - Risks Considerable

Developing Countries to Remain Resilient - Risks Considerable Financial turmoil a serious threat that has proven manageable so far Developing country dynamism cushions the effect on growth while inflationary

Developing Countries to Remain Resilient - Risks Considerable Financial turmoil a serious threat that has proven manageable so far Developing country dynamism cushions the effect on growth while inflationary

Developing Trends: February 2014

Developing Trends: February 2014 Overview The recent episode of market volatility had differentiated impacts on developing countries. Following a string of weaker than expected economic news in January

Developing Trends: February 2014 Overview The recent episode of market volatility had differentiated impacts on developing countries. Following a string of weaker than expected economic news in January

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

The Global Economy. RISI Asian Forest Products Summit 22 June, David Katsnelson Director, Macroeconomics

The Global Economy Heightened drisks RISI Asian Forest Products Summit 22 June, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. China Slowing, Not Crashing

The Global Economy Heightened drisks RISI Asian Forest Products Summit 22 June, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. China Slowing, Not Crashing

Mexico: Dealing with international financial uncertainty. Manuel Sánchez

Manuel Sánchez United States Mexico Chamber of Commerce, Chicago, IL, August 6, 2015 Contents 1 Moderate economic growth 2 Waiting for the liftoff 3 Taming inflation 2 Since 2014, Mexico s economic recovery

Manuel Sánchez United States Mexico Chamber of Commerce, Chicago, IL, August 6, 2015 Contents 1 Moderate economic growth 2 Waiting for the liftoff 3 Taming inflation 2 Since 2014, Mexico s economic recovery

Global Monthly July 2017

Global Monthly July 2017 Overview High-frequency data continue to suggest an ongoing recovery in global activity. Global inflation has abated, reflecting subdued energy prices and low core inflation in

Global Monthly July 2017 Overview High-frequency data continue to suggest an ongoing recovery in global activity. Global inflation has abated, reflecting subdued energy prices and low core inflation in

MAY Overview. Q1 GDP growth in selected high-income countries (%change, q/q saar) 10

10") Developing Trends was prepared by the Development Economics Prospects Group (DECPG) of the World Bank. The team is coordinated by Allen Dennis (Overview), and is comprised of Tehmina Khan (High-income),

Developing Trends was prepared by the Development Economics Prospects Group (DECPG) of the World Bank. The team is coordinated by Allen Dennis (Overview), and is comprised of Tehmina Khan (High-income),

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing Global scenarios Slower growth in emerging markets is a key risk to our central forecast for the global economy. While more positive signs have recently appeared

Emerging Markets Weekly Economic Briefing Global scenarios Slower growth in emerging markets is a key risk to our central forecast for the global economy. While more positive signs have recently appeared

Emerging Markets Weekly Economic Briefing

21 Emerging Markets Emerging Markets Weekly Economic Briefing Recession looms for some emerging economies Several major emerging economies struggling with domestically-induced problems are now in, or flirting

21 Emerging Markets Emerging Markets Weekly Economic Briefing Recession looms for some emerging economies Several major emerging economies struggling with domestically-induced problems are now in, or flirting

The international environment

The international environment This article (1) discusses developments in the global economy since the August 1999 Quarterly Bulletin. Domestic demand growth remained strong in the United States, and with

The international environment This article (1) discusses developments in the global economy since the August 1999 Quarterly Bulletin. Domestic demand growth remained strong in the United States, and with

Global growth fragile: The global economy is projected to grow at 3.5% in 2019 and 3.6% in 2020, 0.2% and 0.1% below October 2018 projections.

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Quarterly Report. April June 2014

April June August 1, 1 Outline 1 Monetary Policy External Conditions 5 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks Monetary Policy Conduction Monetary policy has focused

April June August 1, 1 Outline 1 Monetary Policy External Conditions 5 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks Monetary Policy Conduction Monetary policy has focused

Quarterly Report. April June 2015

April June August 12, 1 1 Outline 1 2 Monetary Policy External Conditions 3 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks April-June 2 Monetary Policy Conduction in

April June August 12, 1 1 Outline 1 2 Monetary Policy External Conditions 3 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks April-June 2 Monetary Policy Conduction in

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Macro Research Economic outlook

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

Global Economic Prospects and the Developing Countries William Shaw December 1999

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Recent Recent Developments 0

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Industrial Production Annex

Frequency Global Economic Prospects January 2012 Recent economic developments Unique exogenous shocks have affected industrial output throughout the year. The recovery in industrial output growth from

Frequency Global Economic Prospects January 2012 Recent economic developments Unique exogenous shocks have affected industrial output throughout the year. The recovery in industrial output growth from

Inflation projection of Narodowy Bank Polski based on the NECMOD model

Economic Institute Inflation projection of Narodowy Bank Polski based on the NECMOD model Warsaw / 9 March Inflation projection of the NBP based on the NECMOD model Outline: Introduction Changes between

Economic Institute Inflation projection of Narodowy Bank Polski based on the NECMOD model Warsaw / 9 March Inflation projection of the NBP based on the NECMOD model Outline: Introduction Changes between

Mexico s Macroeconomic Outlook and Monetary Policy

Mexico s Macroeconomic Outlook and Monetary Policy Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Washington, DC, 13 October 2017 */ The opinions and views expressed in this document

Mexico s Macroeconomic Outlook and Monetary Policy Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Washington, DC, 13 October 2017 */ The opinions and views expressed in this document

The Global Economy Heightened Risks

The Global Economy Heightened Risks RISI Latin American Conference 16 August, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. Latin America Some Improvement

The Global Economy Heightened Risks RISI Latin American Conference 16 August, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. Latin America Some Improvement

Special Focus: Recent Oil Price Developments in Perspective

Jan- Mar- May- Jul- Sep- Nov- Jan-5 Mar-5 May-5 For more information, visit http://www.worldbank.org/prospects Overview Table of Contents Global growth hit a soft patch in 5Q, driven by slowing activity

Jan- Mar- May- Jul- Sep- Nov- Jan-5 Mar-5 May-5 For more information, visit http://www.worldbank.org/prospects Overview Table of Contents Global growth hit a soft patch in 5Q, driven by slowing activity

Recent Economic Developments and Monetary Policy in Mexico

Recent Economic Developments and Monetary Policy in Mexico Javier Guzmán Calafell, Deputy Governor, Banco de México* United States-Mexico Chamber of Commerce, Northeast Chapter New York City, 2 June 2017

Recent Economic Developments and Monetary Policy in Mexico Javier Guzmán Calafell, Deputy Governor, Banco de México* United States-Mexico Chamber of Commerce, Northeast Chapter New York City, 2 June 2017

Economic Outlook January, 2012

Economic Outlook January, 2012 Summary Global economy Low global growth scenario, tail risks have become smaller. Risks (Debt Ceiling, elections in Italy, growth in Europe). Brazil Activity shows signs

Economic Outlook January, 2012 Summary Global economy Low global growth scenario, tail risks have become smaller. Risks (Debt Ceiling, elections in Italy, growth in Europe). Brazil Activity shows signs

Divergent Monetary Policy Implication for sub-saharan African Economies. By Sarah O. Alade Deputy Governor, Economic Policy Central Bank of Nigeria

Divergent Monetary Policy Implication for sub-saharan African Economies By Sarah O. Alade Deputy Governor, Economic Policy Central Bank of Nigeria Crisis background The recent financial crisis is one of

Divergent Monetary Policy Implication for sub-saharan African Economies By Sarah O. Alade Deputy Governor, Economic Policy Central Bank of Nigeria Crisis background The recent financial crisis is one of

Global Monthly October 2018

Global Monthly October 2018 Overview Global activity appears to be decelerating amid tightening financial conditions and ongoing trade tensions. Global trade remains weak despite an increase in global

Global Monthly October 2018 Overview Global activity appears to be decelerating amid tightening financial conditions and ongoing trade tensions. Global trade remains weak despite an increase in global

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Economic Outlook: Global and India. Ajit Ranade IEEMA T & D Conclave December 12, 2014

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Eurozone Economic Watch. February 2018

Eurozone Economic Watch February 2018 Eurozone: Strong growth continues in 1Q18, but confidence seems to peak GDP growth moderated slightly in, but there was an upward revision to previous quarters. Available

Eurozone Economic Watch February 2018 Eurozone: Strong growth continues in 1Q18, but confidence seems to peak GDP growth moderated slightly in, but there was an upward revision to previous quarters. Available

NOVEMBER 2018 Summary global growth is above average but slowing

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

Prospects and Challenges for the Global Economy and the MENA Region

Prospects and Challenges for the Global Economy and the MENA Region Ministry of Finance Cairo October 25, 2011 Andreas Bauer Division i i Chief, t International Monetary Fund Key points: The global outlook

Prospects and Challenges for the Global Economy and the MENA Region Ministry of Finance Cairo October 25, 2011 Andreas Bauer Division i i Chief, t International Monetary Fund Key points: The global outlook

EUROZONE ECONOMIC WATCH JANUARY 2017

EUROZONE ECONOMIC WATCH JANUARY 2017 Key messages: some changes for the better Improving confidence in across the board shows the resilience of the eurozone to the various potentially disturbing political

EUROZONE ECONOMIC WATCH JANUARY 2017 Key messages: some changes for the better Improving confidence in across the board shows the resilience of the eurozone to the various potentially disturbing political

Jörg Decressin Deputy Director

World Economic Outlook October 13 Jörg Decressin Deputy Director Research Department, IMF 1 Outline Prospects for Advanced Economies Recent Developments and Implications for Emerging Economies Medium-term

World Economic Outlook October 13 Jörg Decressin Deputy Director Research Department, IMF 1 Outline Prospects for Advanced Economies Recent Developments and Implications for Emerging Economies Medium-term

Special Focus: How important are China and India in the global demand for commodities?

For more information, visit http://www.worldbank.org/prospects Overview As in the first quarter, global growth of about 2.3 percent (saar) disappointed in the second quarter of 215. In August, equity markets

For more information, visit http://www.worldbank.org/prospects Overview As in the first quarter, global growth of about 2.3 percent (saar) disappointed in the second quarter of 215. In August, equity markets

The Thai economy is viewed to moderate from last assessment from the intensified impact of the euro area s crisis on merchandise exports, which, in

1 I. Economic and inflation outlook II. Monetary policy stances going forward 2 I. Economic and inflation outlook II. Monetary policy stances going forward 3 The Thai economy is viewed to moderate from

1 I. Economic and inflation outlook II. Monetary policy stances going forward 2 I. Economic and inflation outlook II. Monetary policy stances going forward 3 The Thai economy is viewed to moderate from

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Economic Outlook. Macro Research Itaú Unibanco

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track -

REVISED to reflect the 2 nd QE for the Apr-Jun Qtr of 2018 FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track - September 10, 2018 Copyright Mizuho Research

REVISED to reflect the 2 nd QE for the Apr-Jun Qtr of 2018 FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track - September 10, 2018 Copyright Mizuho Research

OECD Interim Economic Projections Real GDP 1 Percentage change September 2015 Interim Projections. Outlook

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,