The Brazilian boom is it happening and what will it mean for copper industry growth in this newly industrializing economy?

|

|

|

- Elfrieda Sherman

- 6 years ago

- Views:

Transcription

1 The Brazilian boom is it happening and what will it mean for copper industry growth in this newly industrializing economy? Presented by Paranapanema S.A. Brazil Mario L. Lorencatto

2 Table of Contents 1. Introduction to Paranapanema 2. Economic Scenario in Brazil 3. Brazilian Copper Industry 4. Prospects for the Copper Business in Brazil 5. Paranapanema s Investment Program & Upcoming Business Opportunities 6. Contact Details 2

3 INTRODUCTION TO PARANAPANEMA 3

Employs 3,500 people; Market maker")

4 2,512 3,192 4,098 4,026 Largest non-integrated producer of refined copper in Brazil: Production capacity: 280,000 t/yr; 98% of total domestic production; 40% of total consumption; 650,000 t/yr. of suphuric acid; Operates other 3 plants producing copper & alloys products (rolled, bars, drawn wires, tubes and fittings): Production capacity being raised from 72,000 to 130,000 t/yr.; 41% share of the domestic market; Net Revenues (R$ MLN) Employs 3,500 people; Market maker of the local copper scrap segment, controlling 65% of the local volume;

5 Compelling case of business turnaround new management and improved results; Focus on the copper business retain its leadership position; Adjusted EBITDA (R$ MLN) Sold its non-copper businesses: fertilizer, tin mining, zinc semi manufactured, mining rights; CAPEX program of $600MLN in 2011/14; Social/environmental responsability; Shares listed in the Novo Mercado of BM&FBOVESPA 53% of capital owned by Caixa, PREVI and PETROS: Shares price up by 170% since Jun/12. 5

6 6

7 7 ECONOMIC SCENARIO IN BRAZIL

8 Economic Scenario in Brazil Policy Focus: economic growth, employment and social development; Anticyclical economic measures: Expansionary monetary and fiscal policies; Public investments in infrastructure; Less market driven vs. government interventions; The country s basic infrastructure as bottlenecks to higher growth; Increased protective barriers on foreign trade; Domestic inflation projected at 5.74% - above the 4.5% target; The Brazilian Real expected to trade within vs. the US Dollar; Government holds political majority through a diverse group of parties kickoff of the 2014 elections for the Federal and States administrations. 8

9 GDP of US$ 2.5 TLN World s 7th largest GDP by sector Population: 198MLN 5.2% unemployment Sources: IBGE/IMF 9 9

10 % of GDP 50% 47% 40% 36% 34% 30% 29% 26% 26% 26% 25% 24% 22% 21% 21% 20% 10% 0% Source: International Monetary Fund 10 10

11 Billion US$ F Source: IMF, Bloomberg, IBGE, Haver and Itaú 11 11

12 PAC was introduced in 2007 to promote the planning and execution of investments linked to social and urban infrastructure, logistics and energy, contributing to rapid and sustainable development. PAC 1 Investments = US$ BLN Focus on infrastructure projects: stadiums, urban mobility, ports and airports and services such as security, IT, electric power and turism. Investments = US$ BLN PAC 2 The investments concentrate on the infrastructure projects to improve the sport facilities, urban mobility and housing. Source: Brazilian Government

13 Brazil will host two of the world s major sport events: 2014 FIFA World Cup Investments = US$ 13.1 BLN Focus on infrastructure projects: stadiums, ports and airports upgrading, urban mobility and services as security, IT, electric power and turism The Olympic and Paralympic Games Investments = US$ 6.3 BLN The investments are concentrated on the infrastructure projects, construction works to improve the sport facilities, urban mobility and accomodation. Sources: Brazilian Government 13 13

14 THE BRAZILIAN COPPER INDUSTRY 14 14

15 Mining Mineração Caraíba/Glencore Vale Yamana Gold Semi-manufactured Paranapanema Termomecânica Cecil Ibrame Refining Paranapanema Mineração Caraíba/Glencore Vale Wire-rod 11 out of the 17 established companies also manufacture wires and cables. Wires and cables: More than 100 companies several including international companies such as Commscope, Draka- Telcon, Furukawa, General Cable, Phelps Dodge, Nexans and Prysmian. Source: Sindicel and ABC 15 15

16 The Brazilian copper chain reached total production of 805 th tons (contained copper) in Thousand tons 1,139 Based on the investments for the next years, the production could reach 1,139 th tons in Wires and Cables Semi-manufactured Cathode Concentrate Source: Sindicel and ABC 16 16

17 FORECAST REGIONS (th t) Africa North America LATAM Asia Europe Middle East Oceania Total Brazil MINE PRODUCTION REFINED PRODUCTION REFINED USAGE ,031 1,205 1,355 1,447 1,713 2,005 2, ,181 1,435 1, ,952 1,695 1,643 1,740 1,863 2,022 2,080 1,710 1,496 1,405 1,280 1,370 1,451 1,466 2,188 1,764 1,897 1,957 1,929 1,917 1,904 7,240 7,271 7,290 7,305 8,194 8,745 9,123 4,064 4,197 4,135 4,178 4,367 4,430 4, ,699 2,998 3,084 2,858 3,094 3,384 3,621 7,565 7,787 8,298 8,789 10,076 11,475 12,552 9,183 10,035 11,269 11,729 12,437 13,160 13,918 1,416 1,434 1,463 1,500 1,569 1,609 1,660 3,490 3,380 3,596 3,687 3,821 3,968 4,003 4,482 3,536 3,861 3,994 3,980 4,064 4, ,012 1,061 1,034 1,012 1,021 1,060 1,113 1,121 1, ,705 15,958 16,194 16,279 17,928 19,332 20,190 18,260 18,306 19,009 19,697 21,597 23,534 24,810 17,929 17,301 19,264 19,931 20,670 21,578 22, Brazilian Copper Concentrate Production (th t) Mines Chapada Jaguari Salobo Sossego Total Brazil Chinese GDP is 3.6x the Brazilian GDP China consumes 20x more copper than Brazil Source: Brook Hunt 17 17

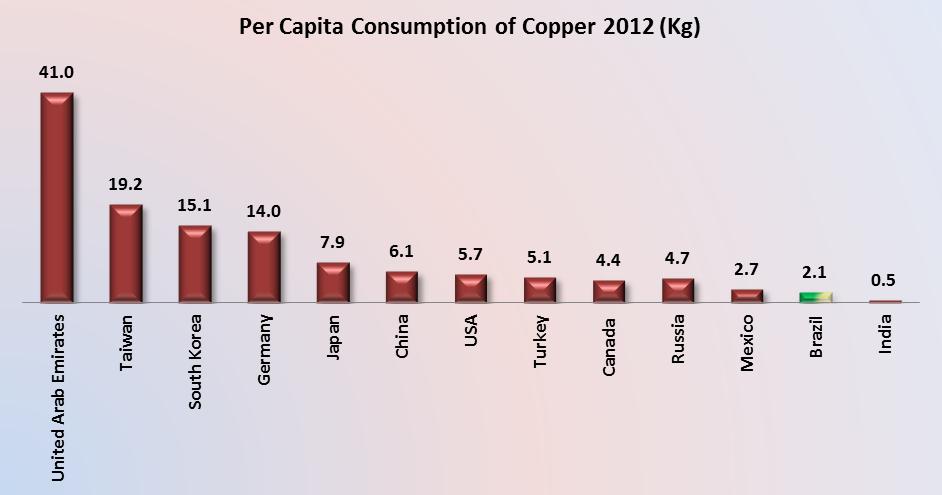

18 Refined Copper - World Consumption Copper Concentrate - World Production Saudi Arabia 1% Thailand 1% Poland 1% Mexico 1% Turkey 2% Brazil 2% Taiwan 2% India 3% Russia 4% Others 25% South Korea 4% Japan 5% USA 9% China 40% Mexico 3% Congo 3% Canada 3% Indonesia 3% Zambia 4% Kazakhstan 2% Russia 4% Poland 3% Iran 2% Brazil 1% Australia 6% Others 10% USA 7% Peru 8% Chile 33% China 8% Source: Sindicel 18 18

19 19 19

20 CAGR = 7.1 % 21 21

Tubes and Alloys (th t) Others 12.4 40% Imports 3.")

21 Complete Line Products (th t) Complete Line Products (th t) Others % Paranapanema % CAGR = 7.1 % Others % Paranapanema % Total = th t Imports % Total = th t Imports % Tubes and Alloys (th t) Tubes and Alloys (th t) Others % Imports % Paranapanema % CAGR = 3.6 % Others % Imports % Paranapanema % Total = 30.8 th t Source: Paranapanema s estimate Total = 35.5 th t 22 22

22 CAGR = 2.5 % 23 23

23 PROSPECTS FOR THE COPPER SECTOR IN BRAZIL 24 24

24 Growth in refined copper usage: Brazil Global % 4.4% % 4.9% Recovery in the domestic industrial production; Infrastructure projects and favorable momentum in civil construction; Weaker local currency; Reduction in the VAT incentives to imported products; Increased import duties on copper tubes: from 15% to 25%; Import substitution growth opportunities for the local producers; Sharp cuts in electricity prices; 25 25

25 Tax Incentive Programs: Reintegra and Desenvolve ; Reduction of payroll taxes; Attractive long term financing from public Development Banks; Growing threat of substituting copper in some applications: PVC tubes in civil construction; Aluminum in the cable & wires and auto segments; Development and expansion of new applications for copper; New Regulations for mining activities: tougher to obtain mining licenses; higher royalties; more strict environmental protection; incentives to vertical integration; Excess capacity: industry consolidation semi-manufactured segment

26 PARANAPANEMA S INVESTMENT PROGRAM 2011/

27 CAPEX Projects (Revised in Feb., 2013) Total I. Expansion and upgrade of the refined copper plant Update and expansion of refined copper plant: Cu production from 220 to 280 thousand t /yr; Production cost from $629/t to $432/t; Use of scrap from 20% to 24%; Sulphuric acid from 572 to 650 thousand t/yr. New precious metals refinery: 2,4 t/yr of gold, 33,5 t/yr of silver, platinum and selenium. $8MLN $156MLN $32MLN $ 25MLN $196MLN $ 25MLN Enviromental Improvement Projects. $14MLN $4MLN $18MLN II. Expansion and update of the plants of semielaborated products New plant of seamless copper tubes: from 18 to 36 thousand t/yr cast & roll. Expansion of rolled copper plant (cold rolling process) from 28 to 55 thousand t/yr. Expansion of rolled copper plant (hot rolling process) from 60 to 200 thousand t/yr. $11MLN $48MLN $27MLN $77MLN $85MLN $86MLN $77MLN $85MLN Total I and II $19MLN $204MLN $73MLN $191MLN $487MLN III. Other projects and maintenance $51MLN $13MLN $9MLN $40MLN $113MLN Total I, II and III $70MLN $217MLN $82MLN $231MLN $600MLN 28

28 PARANAPANEMA S UPCOMING BUSINESS OPPORTUNITIES 29 29

29 Further expand production capacity of refined copper: From 280 to 320 thousand t/yr. up to 69% of the local consumption; Required investment: $35MLN plus additional working capital; Expanding exports sales of copper tubes and laminated products: Paranapanema s production capacity will represent about 83% and 124% of the domestic consumption, respectively; New products niche opportunities in semi-manufactured; Vertical Integration: participation in the copper mining segment: Focus on opportunities within Brazil; Leverage on the company s strategic advantages: logistic/smelter; Paranapanema will not develop mining operations capability; Preference for projects in advanced stages of development; Medium and small size deposits 300 to 400 thousand t; Secure up to 30% equity ownership and 100% of the offtaking; Increase domestic sourcing of copper concentrate from 23% to 70%

30 Edson Monteiro Machado President/VP Operations Tel / Mário L. Lorencatto CFO and Investor Relations Director Tel /7904/ José Rodolfo Montemurro Investor Relations Dept. Tel /

31 THANK YOU! 32 32

Market analysis. Mines Smelters Zinc Copper. President & CEO Jan Johansson. Boliden s Capital Markets Days 7-8 June 2006 Odda, Norway

Boliden s Capital Markets Days 7-8 June 2006 Odda, Norway Market analysis President & CEO Jan Johansson Mines Smelters Zinc Copper Boliden s Capital Markets Days 7-8 June 2006 Odda, Norway 2 Continued

Boliden s Capital Markets Days 7-8 June 2006 Odda, Norway Market analysis President & CEO Jan Johansson Mines Smelters Zinc Copper Boliden s Capital Markets Days 7-8 June 2006 Odda, Norway 2 Continued

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile. 4-6 October 2017

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Peru s Fundamentals and Economic Outlook

Peru s Fundamentals and Economic Outlook Julio Velarde Governor Central Bank of Peru October 2016 Content 1. Slow Global Recovery 5. Gradual withdrawal of monetary stimulus 2. Reversal in Peru s external

Peru s Fundamentals and Economic Outlook Julio Velarde Governor Central Bank of Peru October 2016 Content 1. Slow Global Recovery 5. Gradual withdrawal of monetary stimulus 2. Reversal in Peru s external

Gold demand statistics

Gold demand statistics Table 2: Gold demand (tonnes) 2014 2015 Q2 14 Q3 14 Q4 14 Q2 15 Q3 15 Q4 15 Jewellery 2,482.0 2,397.5 589.5 591.5 686.0 596.9 513.7 623.7 663.2 481.9-19 Technology 348.5 333.8 86.6

Gold demand statistics Table 2: Gold demand (tonnes) 2014 2015 Q2 14 Q3 14 Q4 14 Q2 15 Q3 15 Q4 15 Jewellery 2,482.0 2,397.5 589.5 591.5 686.0 596.9 513.7 623.7 663.2 481.9-19 Technology 348.5 333.8 86.6

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability Julio Velarde Governor Central Bank of Peru March 2016 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability Julio Velarde Governor Central Bank of Peru March 2016 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments

Copper market trends. Jorge Cantallopts. December Logo Gobierno: 160x162px. Ministerio, Subsecretaría, Organismo, etc.

Logo Gobierno: 160x162px. Ministerio, Subsecretaría, Organismo, etc.:160x145px Copper market trends Jorge Cantallopts Director of Research and Public Policies Chilean Copper Comission (Cochilco) December

Logo Gobierno: 160x162px. Ministerio, Subsecretaría, Organismo, etc.:160x145px Copper market trends Jorge Cantallopts Director of Research and Public Policies Chilean Copper Comission (Cochilco) December

Peru s fundamentals and economic outlook Julio Velarde Governor Central Bank of Peru. September 2015

Peru s fundamentals and economic outlook Julio Velarde Governor Central Bank of Peru September 2015 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments and prospects

Peru s fundamentals and economic outlook Julio Velarde Governor Central Bank of Peru September 2015 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments and prospects

Southern Africa regional superpower in the making. Dr Roelof Botha

Southern Africa regional superpower in the making Dr Roelof Botha Health sector focus Composition of Gauteng health budget FY 01 by programme (total R5. billion) R b Central Hospitals: 6.5 Facilities Management:.

Southern Africa regional superpower in the making Dr Roelof Botha Health sector focus Composition of Gauteng health budget FY 01 by programme (total R5. billion) R b Central Hospitals: 6.5 Facilities Management:.

Construction and Mining Technique

Construction and Mining Technique Atlas Copco Capital Markets Day, December 2, 2008 Björn Rosengren, Business Area President Atlas Copco Capital Markets Day, December 2, 2008 Construction and Mining Technique

Construction and Mining Technique Atlas Copco Capital Markets Day, December 2, 2008 Björn Rosengren, Business Area President Atlas Copco Capital Markets Day, December 2, 2008 Construction and Mining Technique

Report on Finnish Technology Industry Exports

Report on Finnish Technology Industry Exports Last observation October 2018, 2.1.2019 Goods Export of Technology Industry from Finland Goods Export of Technology Industry from Finland by Branches Source:

Report on Finnish Technology Industry Exports Last observation October 2018, 2.1.2019 Goods Export of Technology Industry from Finland Goods Export of Technology Industry from Finland by Branches Source:

Market Briefing: Global Markets

Market Briefing: Global Markets July 6, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box Table Of Contents Table

Market Briefing: Global Markets July 6, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box Table Of Contents Table

Economic Outlook January, 2012

Economic Outlook January, 2012 Summary Global economy Low global growth scenario, tail risks have become smaller. Risks (Debt Ceiling, elections in Italy, growth in Europe). Brazil Activity shows signs

Economic Outlook January, 2012 Summary Global economy Low global growth scenario, tail risks have become smaller. Risks (Debt Ceiling, elections in Italy, growth in Europe). Brazil Activity shows signs

Peruvian mining: A competitive and attractive investment. ING. Victor Gobitz, CEO Buenaventura

Peruvian mining: A competitive and attractive investment ING. Victor Gobitz, CEO Buenaventura INDEX Megatrend I. Location (World Context) II. Natural Resources - Mining potential of Peru - Value and structure

Peruvian mining: A competitive and attractive investment ING. Victor Gobitz, CEO Buenaventura INDEX Megatrend I. Location (World Context) II. Natural Resources - Mining potential of Peru - Value and structure

Section 232 Tariffs on Steel and Aluminum Products. Presentation to the National Association of Steel Pipe Distributors Timothy C.

Section 232 Tariffs on Steel and Aluminum Products Presentation to the National Association of Steel Pipe Distributors Timothy C. Brightbill What Is Section 232? Under Section 232 of the Trade Expansion

Section 232 Tariffs on Steel and Aluminum Products Presentation to the National Association of Steel Pipe Distributors Timothy C. Brightbill What Is Section 232? Under Section 232 of the Trade Expansion

Global Resources Fund (PSPFX)

") Global Resources Fund (PSPFX) Global Resources are the building blocks of the world we live in. As the world s population grows and emerging regions develop a more vibrant infrastructure for commerce,

Global Resources Fund (PSPFX) Global Resources are the building blocks of the world we live in. As the world s population grows and emerging regions develop a more vibrant infrastructure for commerce,

ICSG - Lisbon Long-term Copper Dynamic

AG ICSG - Lisbon Long-term Copper Dynamic April 212 Metals Research xiao.fu@db.com; (44) 2 7547 1558 AG/London All prices are those current at the end of the previous trading session unless otherwise indicated.

AG ICSG - Lisbon Long-term Copper Dynamic April 212 Metals Research xiao.fu@db.com; (44) 2 7547 1558 AG/London All prices are those current at the end of the previous trading session unless otherwise indicated.

Economic Outlook. Macro Research Itaú Unibanco

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Jörg Decressin Deputy Director

World Economic Outlook October 13 Jörg Decressin Deputy Director Research Department, IMF 1 Outline Prospects for Advanced Economies Recent Developments and Implications for Emerging Economies Medium-term

World Economic Outlook October 13 Jörg Decressin Deputy Director Research Department, IMF 1 Outline Prospects for Advanced Economies Recent Developments and Implications for Emerging Economies Medium-term

Economic Stimulus Packages and Steel: A Summary

Economic Stimulus Packages and Steel: A Summary Steel Committee Meeting 8-9 June 2009 Sources of information on stimulus packages Questionnaire to Steel Committee members, full participants and observers

Economic Stimulus Packages and Steel: A Summary Steel Committee Meeting 8-9 June 2009 Sources of information on stimulus packages Questionnaire to Steel Committee members, full participants and observers

Global Aluminum FRP Industry

28 th International Aluminum Conference, Geneva, Switzerland Global Aluminum FRP Industry Sustainability Economic & Environmental Erwin Mayr, President Novelis Europe 9/19/2013 Topic today: Industry Sustainability

28 th International Aluminum Conference, Geneva, Switzerland Global Aluminum FRP Industry Sustainability Economic & Environmental Erwin Mayr, President Novelis Europe 9/19/2013 Topic today: Industry Sustainability

Market Briefing: Gold

Market Briefing: Gold January 3, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table

Market Briefing: Gold January 3, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table

CLSA Copper Access Day 4 JUNE MICHAEL NOSSAL Executive General Manager Business Development HKEx: 1208

CLSA Copper Access Day 4 JUNE 2014 MICHAEL NOSSAL Executive General Manager Business Development HKEx: 1208 Important information This presentation and the information contained herein are given for general

CLSA Copper Access Day 4 JUNE 2014 MICHAEL NOSSAL Executive General Manager Business Development HKEx: 1208 Important information This presentation and the information contained herein are given for general

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

STATISTICS Last update: 03/07/2017

STATISTICS 2012-2016 Last update: 03/07/2017 BU NEWS BUSINESS [USD, BILLIONS] New business by year, vs. total world exports 3,000 2,500 2,000 1,500 1,000 500 12,131 1,138 40 127 971 14,023 1,323 53 143

STATISTICS 2012-2016 Last update: 03/07/2017 BU NEWS BUSINESS [USD, BILLIONS] New business by year, vs. total world exports 3,000 2,500 2,000 1,500 1,000 500 12,131 1,138 40 127 971 14,023 1,323 53 143

U.S. Global Investors Searching for Opportunities, Managing Risk

U.S. Global Investors Searching for Opportunities, Managing Risk On On the the Ground in in Emerging Markets: Our First-Hand Look at at Opportunities Frank E. Holmes CEO and Chief Investment Officer John

U.S. Global Investors Searching for Opportunities, Managing Risk On On the the Ground in in Emerging Markets: Our First-Hand Look at at Opportunities Frank E. Holmes CEO and Chief Investment Officer John

MONGOLIA is OPEN. for BUSINESS. Invest Mongolia Agency

MONGOLIA is OPEN for BUSINESS Invest Mongolia Agency WHY INVEST IN MONGOLIA 1. Large mineral resource base that can be leveraged for value added processing 2. Situated between two giant economies, China

MONGOLIA is OPEN for BUSINESS Invest Mongolia Agency WHY INVEST IN MONGOLIA 1. Large mineral resource base that can be leveraged for value added processing 2. Situated between two giant economies, China

Investor Presentation. Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG)

") Investor Presentation Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG) Agenda Outlook Gerdau Highlights 2 Economic outlook GDP Growth 2014 2015f 2016f World 3.4% 3.1% 3.2%

Investor Presentation Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG) Agenda Outlook Gerdau Highlights 2 Economic outlook GDP Growth 2014 2015f 2016f World 3.4% 3.1% 3.2%

The Evolving Role of Trade in Asia: Opening a New Chapter. Fall 2018 REO Background Paper

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

BUSINESS YEAR 2009 RESULTS

BUSINESS YEAR 2009 RESULTS Madrid, 26 February 2010 WORLD PRODUCTION OF STAINLESS STEEL Thousand Mt. 30,000 28,000 26,000 24,000 22,000 20,000 18,000 16,000 14,000 12,000 10,000 8,000 6,000 4,000 2,000

BUSINESS YEAR 2009 RESULTS Madrid, 26 February 2010 WORLD PRODUCTION OF STAINLESS STEEL Thousand Mt. 30,000 28,000 26,000 24,000 22,000 20,000 18,000 16,000 14,000 12,000 10,000 8,000 6,000 4,000 2,000

Hindalco. Investor Presentation Q4 FY17 Mumbai, May 30, Excellence by Design

Hindalco Investor Presentation Q4 FY17 Mumbai, May 30, 2017 Forward Looking & Cautionary Statement Certain statements in this report may be forward looking statements within the meaning of applicable securities

Hindalco Investor Presentation Q4 FY17 Mumbai, May 30, 2017 Forward Looking & Cautionary Statement Certain statements in this report may be forward looking statements within the meaning of applicable securities

Global Economy is Expected to Grow by 3.4 % in 2016 GDP growth in 2016, %

Russia Brazil Mexico Rest of Latin America Rest of Eastern Europe Middle East and Africa Global Economy is Expected to Grow by 3.4 % in 216 GDP growth in 216, % 9 8 7 6 5 4 3 2 1-1 -2-3 -4 North America

Russia Brazil Mexico Rest of Latin America Rest of Eastern Europe Middle East and Africa Global Economy is Expected to Grow by 3.4 % in 216 GDP growth in 216, % 9 8 7 6 5 4 3 2 1-1 -2-3 -4 North America

Investor Presentation. Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG)

") Investor Presentation Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG) Agenda Outlook Gerdau Highlights 2 Economic Outlook GDP Growth 2014 2015f 2016f World 3.4% 3.1% 3.4%

Investor Presentation Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG) Agenda Outlook Gerdau Highlights 2 Economic Outlook GDP Growth 2014 2015f 2016f World 3.4% 3.1% 3.4%

Investor Presentation

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Region / Country (in Mt and %) 2017f 17/16 World 1,622 7.0% European Union 162 2.5% Better outlook for steel consumption NAFTA 139

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Region / Country (in Mt and %) 2017f 17/16 World 1,622 7.0% European Union 162 2.5% Better outlook for steel consumption NAFTA 139

Global Styrene Butadiene Rubber (SBR) Market Study ( )

Market Study ( )") Global Styrene Butadiene Rubber (SBR) Market Study (2014 2025) Table of Contents 1. INTRODUCTION 1.1. Introduction to SBR Market Product Description Properties Industry Structure Value Chain Market Dynamics

Global Styrene Butadiene Rubber (SBR) Market Study (2014 2025) Table of Contents 1. INTRODUCTION 1.1. Introduction to SBR Market Product Description Properties Industry Structure Value Chain Market Dynamics

Southern Copper Corporation Highlights

Southern Copper Corporation Highlights ht Southern Copper Corporation Highlights March 2009 January 2009 0 Safe Harbor Statement This presentation contains forward-looking statements, as defined by federal

Southern Copper Corporation Highlights ht Southern Copper Corporation Highlights March 2009 January 2009 0 Safe Harbor Statement This presentation contains forward-looking statements, as defined by federal

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

2015 Highlights. 6% growth in Sales Volume vs. 2014, despite slowdown in Domestic Market;

Conference Call 2015 Highlights Date: 02/12/2016 Call in Portuguese with simultaneously translation to English 7:00 a.m. (EST) / 10:00 a.m. (Brasilia) Dial in USA: +1 786 924-6977 Dial in Brazil: +55 11

Conference Call 2015 Highlights Date: 02/12/2016 Call in Portuguese with simultaneously translation to English 7:00 a.m. (EST) / 10:00 a.m. (Brasilia) Dial in USA: +1 786 924-6977 Dial in Brazil: +55 11

CEO s review. Annual General Meeting on March 30, 2017

CEO s review Annual General Meeting on March 30, 2017 Contents 1. Safety 2. Outotec today 3. 2016 in a nutshell 4. Market situation 5. Assessment of the company s situation and focus areas 6. Outlook for

CEO s review Annual General Meeting on March 30, 2017 Contents 1. Safety 2. Outotec today 3. 2016 in a nutshell 4. Market situation 5. Assessment of the company s situation and focus areas 6. Outlook for

Tariffs, NAFTA, and the Administration

Tariffs, NAFTA, and the Administration Presented by The Franklin Partnership, LLP Policy Resolution Group at Bracewell LLP March 2018 Your Team in Washington, D.C. Lobbying Firm The Franklin Partnership,

Tariffs, NAFTA, and the Administration Presented by The Franklin Partnership, LLP Policy Resolution Group at Bracewell LLP March 2018 Your Team in Washington, D.C. Lobbying Firm The Franklin Partnership,

Vale: focus on capital allocation and costs

Vale: focus on capital allocation and costs Fabio Schvartsman Itaú 9th Annual Itaú BBA LatAm Commodities Conference 1 São Paulo, September 27th, 2017 This presentation may include statements that present

Vale: focus on capital allocation and costs Fabio Schvartsman Itaú 9th Annual Itaú BBA LatAm Commodities Conference 1 São Paulo, September 27th, 2017 This presentation may include statements that present

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing November 17, 2 Dr. Edward Yardeni 16-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 13 13 Figure

Chart Collection for Morning Briefing November 17, 2 Dr. Edward Yardeni 16-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 13 13 Figure

The mining sector in Africa

HIF, Freiberg 11.08.2015 The mining sector in Africa and the conflict minerals issue Table of contents Mining sector in Africa Artisanal and smallscale mining Conflict minerals Mining sector in Africa

HIF, Freiberg 11.08.2015 The mining sector in Africa and the conflict minerals issue Table of contents Mining sector in Africa Artisanal and smallscale mining Conflict minerals Mining sector in Africa

African Mining Time for a reality check?

African Mining Time for a reality check? LSE: RRS NASDAQ: GOLD Mine Africa Forum, March 218 The World in CRISIS? or ON THE MEND? Trump mania and nationalism illegal immigration BREXIT and European populism

African Mining Time for a reality check? LSE: RRS NASDAQ: GOLD Mine Africa Forum, March 218 The World in CRISIS? or ON THE MEND? Trump mania and nationalism illegal immigration BREXIT and European populism

Investor Presentation 2017

Investor Presentation 2017 Gerdau steel in the world www.gerdau.com 1 Outlook Gerdau Highlights 2 Economic outlook GDP Growth 2016 2017f 2018f World 3.1% 3.5% 3.6% US 1.6% 2.3% 2.5% Brazil -3.6% 0.5% 2.5%

Investor Presentation 2017 Gerdau steel in the world www.gerdau.com 1 Outlook Gerdau Highlights 2 Economic outlook GDP Growth 2016 2017f 2018f World 3.1% 3.5% 3.6% US 1.6% 2.3% 2.5% Brazil -3.6% 0.5% 2.5%

MONTHLY COPPER BULLETIN

MONTHLY COPPER BULLETIN Aug-2012 05 th September 2012 LME COPPER PRICES, STOCKS & VOLUMES (Jan 2011-Sept 2012) S&P 500 INDEX & LME COPPER PRICE (Aug-Sept 2012) OFFICIAL MARKET DATA & PRICE INDICATORS DATE

MONTHLY COPPER BULLETIN Aug-2012 05 th September 2012 LME COPPER PRICES, STOCKS & VOLUMES (Jan 2011-Sept 2012) S&P 500 INDEX & LME COPPER PRICE (Aug-Sept 2012) OFFICIAL MARKET DATA & PRICE INDICATORS DATE

Latin America Equities

Latin America Equities March 2013 Stephen Burrows, Senior Investment Manager Emerging Markets - Pictet Asset Management Dec-10 Feb-11 Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12

Latin America Equities March 2013 Stephen Burrows, Senior Investment Manager Emerging Markets - Pictet Asset Management Dec-10 Feb-11 Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12

Conference Call Second Quarter 2008 Earnings

Conference Call Second Quarter 2008 Earnings Paulo Penido Pinto Marques CFO and Investor Relations Director August 14, 2008 1 Disclaimer Declarations relative to business perspectives of the Company, operating

Conference Call Second Quarter 2008 Earnings Paulo Penido Pinto Marques CFO and Investor Relations Director August 14, 2008 1 Disclaimer Declarations relative to business perspectives of the Company, operating

The Copper Journal Weekly Report Index Of Charts

Weekly Report Index Of Charts 1 Price & Inventory Report 2 Base Metals Barometer 3 Year To Date % Price Change 4 LME Nonferrous Metals YTD % Change 5 Precious Metals YTD % Price Change 6 Energy YTD % Price

Weekly Report Index Of Charts 1 Price & Inventory Report 2 Base Metals Barometer 3 Year To Date % Price Change 4 LME Nonferrous Metals YTD % Change 5 Precious Metals YTD % Price Change 6 Energy YTD % Price

FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged -

REVISED to reflect the 2 nd QE for the Oct-Dec Qtr of 2017 FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged - March 8, 2018 Copyright

REVISED to reflect the 2 nd QE for the Oct-Dec Qtr of 2017 FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged - March 8, 2018 Copyright

China s Overseas Direct Investment (ODI): Current situation and future outlook

: Current situation and future outlook") China s Overseas Direct Investment (ODI): Current situation and future outlook New York Stock Exchange (NYSE) Dr. Qin Xiao Chairman, the Boyuan Foundation January 7, 2015 Agenda A. China s ODI: High Growth

China s Overseas Direct Investment (ODI): Current situation and future outlook New York Stock Exchange (NYSE) Dr. Qin Xiao Chairman, the Boyuan Foundation January 7, 2015 Agenda A. China s ODI: High Growth

April 26, Q11 Earnings Release. April 27, 2011

April 26, 2011 1Q11 Earnings Release Share Price (03/31/2011) ROMI3 R$ 11.25/share Market Capitalization (03/31/2011) R$ 841 million US$ 516 million Number of shares (03/31/2011) Common: 74,757,547 Total:

April 26, 2011 1Q11 Earnings Release Share Price (03/31/2011) ROMI3 R$ 11.25/share Market Capitalization (03/31/2011) R$ 841 million US$ 516 million Number of shares (03/31/2011) Common: 74,757,547 Total:

Southern Copper Corporation

Southern Copper Corporation March 2010 0 I. Introduction 1 Management Presenters Presenters Raúl Jacob Title Manager of Financial Planning & IR 2 Corporate Structure 80.0% (*) Public Float 20.0% (*) 99.29

Southern Copper Corporation March 2010 0 I. Introduction 1 Management Presenters Presenters Raúl Jacob Title Manager of Financial Planning & IR 2 Corporate Structure 80.0% (*) Public Float 20.0% (*) 99.29

Sandra Crowl, CAIA. Member of the Investment Committee

Sandra Crowl, CAIA Member of the Investment Committee 1 Macro Backdrop and Investment Ideas for 2018 2 Emerging Markets Tailwinds Overall consumption growth, annual change Global trade growth, in volume

Sandra Crowl, CAIA Member of the Investment Committee 1 Macro Backdrop and Investment Ideas for 2018 2 Emerging Markets Tailwinds Overall consumption growth, annual change Global trade growth, in volume

MONTHLY FINANCE REVIEW

ISSN 0388-0605 MONTHLY FINANCE REVIEW ch 2018 No. 536 Policy Research Institute MINISTRY OF FINANCE JAPAN MONTHLY FINANCE REVIEW ch. 2018 (No.536) CONTENTS STATISTICS(Released by Ministry of Finance) A.

ISSN 0388-0605 MONTHLY FINANCE REVIEW ch 2018 No. 536 Policy Research Institute MINISTRY OF FINANCE JAPAN MONTHLY FINANCE REVIEW ch. 2018 (No.536) CONTENTS STATISTICS(Released by Ministry of Finance) A.

Stock Market Briefing: S&P 500 Revenues & the Economy

Stock Market Briefing: S&P Revenues & the Economy December 21, 217 Dr. Edward Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-36 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at

Stock Market Briefing: S&P Revenues & the Economy December 21, 217 Dr. Edward Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-36 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

Delivering growth in the new steel horizon

Delivering growth in the new steel horizon Michel Wurth Member of Group Management Board 24 September 2008 Disclaimer Forward-Looking Statements This document may contain forward-looking information and

Delivering growth in the new steel horizon Michel Wurth Member of Group Management Board 24 September 2008 Disclaimer Forward-Looking Statements This document may contain forward-looking information and

Disclaimer FORWARD LOOKING STATEMETNS. This text includes forward looking statements.

May 2017 Disclaimer This presentation has been prepared by Halcor S.A. (the «Company») for use during the Hellenic Fund and Asset Management Association. This text is provided under confidentiality for

May 2017 Disclaimer This presentation has been prepared by Halcor S.A. (the «Company») for use during the Hellenic Fund and Asset Management Association. This text is provided under confidentiality for

TURNING VISION INTO REALITY FEBRUARY 2015 TSX: FM; LSE: FQM

TURNING VISION INTO REALITY FEBRUARY 2015 TSX: FM; LSE: FQM CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENT Some of the statements contained in the following material are forward-looking statements

TURNING VISION INTO REALITY FEBRUARY 2015 TSX: FM; LSE: FQM CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENT Some of the statements contained in the following material are forward-looking statements

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing November 14, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 16 Figure

Chart Collection for Morning Briefing November 14, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 16 Figure

Investor Relations Jay Bachmann Danièle Daouphars

Investor Document Investor Relations Jay Bachmann jay.bachmann@lafarge.com +33 1 44 34 93 71 Granulats et Béton - Afrique du Sud, stade Moses Mabhida Danièle Daouphars daniele.daouphars@lafarge.com +33

Investor Document Investor Relations Jay Bachmann jay.bachmann@lafarge.com +33 1 44 34 93 71 Granulats et Béton - Afrique du Sud, stade Moses Mabhida Danièle Daouphars daniele.daouphars@lafarge.com +33

Business performance compared with the first nine months of the prior year was mainly influenced by the following factors:

Despite the weak economic environment Aurubis AG breaks even in the first nine months of fiscal year 2008/09 and records a significantly higher net cash flow than in the prior year Hamburg, 12 August 2009

Despite the weak economic environment Aurubis AG breaks even in the first nine months of fiscal year 2008/09 and records a significantly higher net cash flow than in the prior year Hamburg, 12 August 2009

A short history of debt

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

Consolidated Business Results for the First Quarter of the Fiscal Year Ending March 31, 2014 (U.S. GAAP)

") Komatsu Ltd. Corporate Communications Dept. Tel: +81-(0)3-5561-2616 Date: July 29, 2013 URL: http://www.komatsu.com/ Consolidated Business Results for the First Quarter of the Fiscal Year Ending March

Komatsu Ltd. Corporate Communications Dept. Tel: +81-(0)3-5561-2616 Date: July 29, 2013 URL: http://www.komatsu.com/ Consolidated Business Results for the First Quarter of the Fiscal Year Ending March

Alcoa s Perspective on Global Aluminum Platts Aluminium Symposium January Greg Wittbecker, Vice President, Alcoa Materials Management

Alcoa s Perspective on Global Aluminum Platts Aluminium Symposium 2012 16 January 2012 Greg Wittbecker, Vice President, Alcoa Materials Management Cautionary Statement Forward-Looking Statements This presentation

Alcoa s Perspective on Global Aluminum Platts Aluminium Symposium 2012 16 January 2012 Greg Wittbecker, Vice President, Alcoa Materials Management Cautionary Statement Forward-Looking Statements This presentation

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR. Data through May Issued: July 2018

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR Data through May 218 Issued: July 218 OVERVIEW OF SECTION 232 Section 232 of the Trade Expansion Act of 1962, as amended, authorizes the President to adjust

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR Data through May 218 Issued: July 218 OVERVIEW OF SECTION 232 Section 232 of the Trade Expansion Act of 1962, as amended, authorizes the President to adjust

Southern Copper Corporation Highlights. September 2008

Southern Copper Corporation Highlights September 2008 0 Safe Harbor Statement This presentation contains forward-looking statements, as defined by federal securities laws, with respect to our financial

Southern Copper Corporation Highlights September 2008 0 Safe Harbor Statement This presentation contains forward-looking statements, as defined by federal securities laws, with respect to our financial

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 12, 2014 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 12, 2014 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

Investor Presentation

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Better outlook for steel consumption Region / Country (in mt and %) 2017f 17/16 World 1,535 1.3% European Union 158 0.5% NAFTA 135

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Better outlook for steel consumption Region / Country (in mt and %) 2017f 17/16 World 1,535 1.3% European Union 158 0.5% NAFTA 135

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR. March Issued: May 2018

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR March 218 Issued: May 218 OVERVIEW OF SECTION 232 Section 232 of the Trade Expansion Act of 1962, as amended, authorizes the President to adjust the imports

SPECIAL REPORT: U.S. ALUMINUM IMPORT MONITOR March 218 Issued: May 218 OVERVIEW OF SECTION 232 Section 232 of the Trade Expansion Act of 1962, as amended, authorizes the President to adjust the imports

NORTH AMERICAN UPDATE

NORTH AMERICAN UPDATE December 6 th, 2018 INNOVATION INSIGHT GROWTH SINCE 1968 TOUGH YEAR FOR RETURNS AROUND THE WORLD Index Year-to-date Performance MSCI World -1.2% MSCI USA 3.9% MSCI Canada -3.9% MSCI

NORTH AMERICAN UPDATE December 6 th, 2018 INNOVATION INSIGHT GROWTH SINCE 1968 TOUGH YEAR FOR RETURNS AROUND THE WORLD Index Year-to-date Performance MSCI World -1.2% MSCI USA 3.9% MSCI Canada -3.9% MSCI

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES. Bank of Russia.

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

Global Top 500 Report of Mining and Metal,

Global Top 500 Report of Mining and Metal, 2008-2009 This top 500 report is based over 1,000 mining companies (excluding coal, petroleum and natural gas) and metal companies (excluding metalworks) are

Global Top 500 Report of Mining and Metal, 2008-2009 This top 500 report is based over 1,000 mining companies (excluding coal, petroleum and natural gas) and metal companies (excluding metalworks) are

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Vantage Investment Partners. Quarterly Market Review

Vantage Investment Partners Quarterly Market Review First Quarter 2016 Quarterly Market Review First Quarter 2016 This report features world capital market performance and a timeline of events for the

Vantage Investment Partners Quarterly Market Review First Quarter 2016 Quarterly Market Review First Quarter 2016 This report features world capital market performance and a timeline of events for the

Investor Presentation

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Better outlook for steel consumption Region / Country (in mt and %) 2017f 17/16 World 1,535 1.3% European Union 158 0.5% NAFTA 135

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Better outlook for steel consumption Region / Country (in mt and %) 2017f 17/16 World 1,535 1.3% European Union 158 0.5% NAFTA 135

Opportunities For Growth In New Markets

Page 1 / 22 Opportunities For Growth In New Markets Redefining Emerging Markets by Introduction of Iran March 2017 Page 2 / 22 CONTENTS What Makes us the Next BRICS Growth Sectors and Opportunities Page

Page 1 / 22 Opportunities For Growth In New Markets Redefining Emerging Markets by Introduction of Iran March 2017 Page 2 / 22 CONTENTS What Makes us the Next BRICS Growth Sectors and Opportunities Page

Peru s fundamentals and economic outlook Julio Velarde Governor Central Bank of Peru. March 2015

Peru s fundamentals and economic outlook Julio Velarde Governor Central Bank of Peru March 2015 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments and prospects 3.

Peru s fundamentals and economic outlook Julio Velarde Governor Central Bank of Peru March 2015 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments and prospects 3.

Outline of Consolidated Results for Second Quarter of FY2018

Outline of Consolidated Results for Second Quarter of (Year Ending March 31, 2019) October 31, 2018 Contents 1. Outline of Consolidated Results for Second Quarter of 2. Supplementary Materials on Financial

Outline of Consolidated Results for Second Quarter of (Year Ending March 31, 2019) October 31, 2018 Contents 1. Outline of Consolidated Results for Second Quarter of 2. Supplementary Materials on Financial

Aurubis AG Annual General Meeting. Hamburg, Februar 26, 2014

Aurubis AG Annual General Meeting Hamburg, Februar 26, 2014 Agenda 1. Fiscal year 2012/13 2. Events in fiscal year 2012/13 3. Current fiscal year 2013/14 4. Outlook ANNUAL GENERAL MEETING 2014 2/26/2014

Aurubis AG Annual General Meeting Hamburg, Februar 26, 2014 Agenda 1. Fiscal year 2012/13 2. Events in fiscal year 2012/13 3. Current fiscal year 2013/14 4. Outlook ANNUAL GENERAL MEETING 2014 2/26/2014

Investor Presentation

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Region / Country (in Mt and %) 2017f 17/16 18/17 World 1,622 7.0% 1.6% European Union 162 2.5% 1.4% Better outlook for steel consumption

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Region / Country (in Mt and %) 2017f 17/16 18/17 World 1,622 7.0% 1.6% European Union 162 2.5% 1.4% Better outlook for steel consumption

Market Correlations: Brent Crude Oil

Market Correlations: Brent Crude Oil March 6, 2018 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at blog.

Market Correlations: Brent Crude Oil March 6, 2018 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at blog.

SEPTEMBER Overview

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Positive trend in earnings and strong cash flow

Positive trend in earnings and strong cash flow Presentation of the Q3/2017 result Martin Lindqvist, President & CEO Håkan Folin, CFO October 25, 2017 Agenda Q3/2017 and performance by division Financials

Positive trend in earnings and strong cash flow Presentation of the Q3/2017 result Martin Lindqvist, President & CEO Håkan Folin, CFO October 25, 2017 Agenda Q3/2017 and performance by division Financials

New Trends and Challenges in Government Debt Management

New Trends and Challenges in Government Debt Management Phillip Anderson The World Bank Treasury 1818 H Street, N.W. Washington, DC, 2433, USA treasury.worldbank.org 1 Recent Trends 2 Progress and Challenges

New Trends and Challenges in Government Debt Management Phillip Anderson The World Bank Treasury 1818 H Street, N.W. Washington, DC, 2433, USA treasury.worldbank.org 1 Recent Trends 2 Progress and Challenges

Mongolia s economy and competitiveness.

Mongolia s economy and competitiveness www.ecrc.mn Economic Policy and Competitiveness Research Center OUR VISION The Economic Policy and Competitiveness Research Center (ECPRC) established in 2010. Formed

Mongolia s economy and competitiveness www.ecrc.mn Economic Policy and Competitiveness Research Center OUR VISION The Economic Policy and Competitiveness Research Center (ECPRC) established in 2010. Formed

Mongolia Selected Macroeconomic Indicators December 18, 2013

Mongolia Selected Macroeconomic Indicators December 18, 213 For further information, please contact: SSelenge@imf.org 2 2 27 28 29 21 211 212 213 212 213 Q1 Q2 Q3 Oct. Nov. First 11 months Total US$-value

Mongolia Selected Macroeconomic Indicators December 18, 213 For further information, please contact: SSelenge@imf.org 2 2 27 28 29 21 211 212 213 212 213 Q1 Q2 Q3 Oct. Nov. First 11 months Total US$-value

Ricardo Teles / Vale. Vale s Performance in 2017

Ricardo Teles / Vale Vale s Performance in 2017 Rio 1 de Janeiro, February 28 th, 2018 Agenda 2 This presentation may include statements that present Vale's expectations about future events or results.

Ricardo Teles / Vale Vale s Performance in 2017 Rio 1 de Janeiro, February 28 th, 2018 Agenda 2 This presentation may include statements that present Vale's expectations about future events or results.

Agenda. JOÃO MIRANDA CEO Votorantim S.A. Portfolio Management. LORIVAL LUZ CFO and IRO Votorantim Cimentos. MARIO BERTONCINI CFO Votorantim Metais

Agenda JOÃO MIRANDA CEO Votorantim S.A. Portfolio Management LORIVAL LUZ CFO and IRO Votorantim Cimentos MARIO BERTONCINI CFO Votorantim Metais SERGIO MALACRIDA Corporate Treasurer Officer and IRO Votorantim

Agenda JOÃO MIRANDA CEO Votorantim S.A. Portfolio Management LORIVAL LUZ CFO and IRO Votorantim Cimentos MARIO BERTONCINI CFO Votorantim Metais SERGIO MALACRIDA Corporate Treasurer Officer and IRO Votorantim

Y qué está pasando en Brasil?

Y qué está pasando en Brasil? Ilan Goldfajn Chief Economist and Partner, Itaú Unibanco August, 2013 Summary Why has the Brazilian economy decelerated? The low growth and full employment paradox (new middle

Y qué está pasando en Brasil? Ilan Goldfajn Chief Economist and Partner, Itaú Unibanco August, 2013 Summary Why has the Brazilian economy decelerated? The low growth and full employment paradox (new middle

Market Briefing: S&P 500 Forward Earnings & the Economy

Market Briefing: S&P Forward Earnings & the Economy January, 18 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-56 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

Market Briefing: S&P Forward Earnings & the Economy January, 18 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-56 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

WORLD ENERGY INVESTMENT OUTLOOK. Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency / OECD

WORLD ENERGY INVESTMENT OUTLOOK Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency / OECD Global Strategic Challenges Security of energy supplies Threat of environmental

WORLD ENERGY INVESTMENT OUTLOOK Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency / OECD Global Strategic Challenges Security of energy supplies Threat of environmental

2010 Results. Paris - March 2, 2011

2010 Results Paris - March 2, 2011 > Highlights of 2010 > Financial results > Strategy and outlook 2010 Results 2 2010: A Year of Acceleration Highlights of 2010 Revenue of 3,892m, up 19.1% Operating profit

2010 Results Paris - March 2, 2011 > Highlights of 2010 > Financial results > Strategy and outlook 2010 Results 2 2010: A Year of Acceleration Highlights of 2010 Revenue of 3,892m, up 19.1% Operating profit

Latin America Down Under. Marcelo Bastos, Chief Operating Officer

Latin America Down Under Marcelo Bastos, Chief Operating Officer May 2016 Our values: We mine for progress Safety Performance 5 4 4.8 4.1 Safety our first value - TRIF 1 of 2.1 per million hours worked

Latin America Down Under Marcelo Bastos, Chief Operating Officer May 2016 Our values: We mine for progress Safety Performance 5 4 4.8 4.1 Safety our first value - TRIF 1 of 2.1 per million hours worked

MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2

10 2 3 6 8 9 13 14 MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2 Alpha Current Previous Alpha Current Previous Alpha Current Previous weight weight weight weight weight

10 2 3 6 8 9 13 14 MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2 Alpha Current Previous Alpha Current Previous Alpha Current Previous weight weight weight weight weight

TUBOS REUNIDOS GROUP. Special Products & Integral Services Worldwide. Tubos Reunidos. November 2014

Special Products & Integral Services Worldwide Tubos Reunidos 1 Content Tubos Reunidos Group 1. Market and Trends 2. Company Overview 3. 2014 2017 Strategic Plan 4. Financials 2 Tubos Reunidos Group Seamless

Special Products & Integral Services Worldwide Tubos Reunidos 1 Content Tubos Reunidos Group 1. Market and Trends 2. Company Overview 3. 2014 2017 Strategic Plan 4. Financials 2 Tubos Reunidos Group Seamless

Highveld Steel and Vanadium. Annual Results 31 December 2009

Highveld Steel and Vanadium Corporation Limited Annual Results 31 December 2009 Disclaimer 2 Forward looking statements This document may contain forward looking information and statements about Highveld

Highveld Steel and Vanadium Corporation Limited Annual Results 31 December 2009 Disclaimer 2 Forward looking statements This document may contain forward looking information and statements about Highveld

Company Release Fiscal Year 2014/15

Company Release Fiscal Year October 1, 2014 to September 30, 2015 At a Glance Key Aurubis Group figures 4th quarter Fiscal year Change Change Revenues m 2,528 2,944-14 % 10,995 11,241-2 % Gross profit

Company Release Fiscal Year October 1, 2014 to September 30, 2015 At a Glance Key Aurubis Group figures 4th quarter Fiscal year Change Change Revenues m 2,528 2,944-14 % 10,995 11,241-2 % Gross profit

Moderate but continued growth expected for global steel demand

PRESS RELEASE Moderate but continued growth expected for global steel demand worldsteel Short Range Outlook October 2017 Brussels, 16 October 2017 - The World Steel Association (worldsteel) today released

PRESS RELEASE Moderate but continued growth expected for global steel demand worldsteel Short Range Outlook October 2017 Brussels, 16 October 2017 - The World Steel Association (worldsteel) today released

Global Economic Briefing: Global Liquidity

Global Economic Briefing: Global Liquidity December 21, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at

Global Economic Briefing: Global Liquidity December 21, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at