The Global Depression: Causes and Prospects for the US and Developing Countries

|

|

|

- Stanley Bruce

- 5 years ago

- Views:

Transcription

1 The Global Depression: Causes and Prospects for the US and Developing Countries Jan Kregel Presentation for THE INTERNATIONAL WORKING GROUP ON GENDER, MACROECONOMICS AND INTERNATIONAL ECONOMICS Knowledge Networking Program on Engendering Macroeconomics and International Economics WORKSHOP: JUNE 29-JULY 10, 2009

2 US: Causes of Crisis Global savings glut global imbalances Fed left interest rates too low Fraudulent lending practices Financial innovations: Originate and Distribute Faulty Risk Management Practice Hedge Funds Private equity Derivatives credit default swaps Excessive Regulation (CRAs) Faulty Regulation single variable, micro regulation Credit Rating Agencies Off Balance Sheet entities Poor people (Housing policy CRA, FNMA) NOT ME!

3 Structural Causes International: lack of symmetric adjustment Domestic: Unequal Distribution of Income High profits low wages Real wages > productivity growth Globalisation: profits invested abroad Imports are from US owned companies Demand deficiency: Households could spend only by borrowing Finance: Housing finance Commodity speculation

4 Role of Finance Private Equity funds pressure on profits, wages Outsourcing of jobs and investment Price stability, lower import prices Mortgage finance Fannie, Freddie, subprime Provided financing for rising consumer debt/ commercial real estate Real Return Investment Funds Commodity price speculation (biofuels) Energy price speculation Rising Demand in Developing countries Rising terms of trade Rising Capital Flows Rising International Reserves Reduced US interest rates

5 US Outlook Can the egg be put back together? Deleveraging Financial Institutions lower financing Households lower demand Decoupling Deglobalisation Balance Sheet Recession vs Cyclical downturn Insolvency Liquidity crisis Demand Stimulus Currency archeology National accounting higher household saving

6 Contentious Issues Employment impact of stimulus The Deficit is too large Can t borrow any more rating downgrade Will cause higher interest rates Will cause inflation Exit strategy What is Fed Policy? What is Treasury Policy? Tarp, PPIP, Nationalisation New Regulatory Structure

7

8

9

10 30 S&P/Case-Shiller Home Price Index: Composite 10 3-month %Change-ann SA, Jan-00=100 S&P/Case-Shiller Home Price Index: Composite 10 % Change - Year to Year SA, Jan-00= Source: S&P, Fiserv, and MacroMarkets LLC /Haver Analytics

11 22.5 Retail Sales & Food Services % Change - Year to Year SA, Mil.$ Retail Sales & Food Services 6-month %Change-ann SA, Mil.$ Source: Census Bureau/Haver Analytics

12 8 Real Personal Consumption Expenditures % Change - Year to Year SAAR, Bil.Chn.2000$ University of Michigan: Consumer Expectations 3-month MovingAverage NSA, Q1-66= Sources: BEA, UMICH /Haver

13 Total Light Vehicle Retail Sales {Imported+Domestic} 3-month MovingAverage SAAR, Mil. Units Source: Autodata Corporation /Haver Analytics

14 22.5 IP: Consumer Goods % Change - Year to Year SA, 2002=100 IP: Equipment % Change - Year to Year SA, 2002= Source: Federal Reserve Board /Haver Analytics

15 Capacity Utilization: Manufacturing [SIC] SA, % of Capacity Source: Federal Reserve Board /Haver Analytics

16 22.5 NFIB: Percent Planning to Increase Employment, Net SA, % NFIB: Percent Planning Capital Expenditures next 3 to 6 Months SA, % Source: National Federation of Independent Business /Haver Analytics

17 US Corporate Profit Margin (Pre Tax, Quality Adjusted, in %) Source: Haver Analytics

18 90000 Manufacturers' New Orders: Capital Goods 3-month MovingAverage SA, Mil.$ Manufacturers' Shipments: Capital Goods 3-month MovingAverage SA, Mil.$ Source: Census Bureau /Haver Analytics

19 675 Unemployment Insurance: Initial Claims, 4-Week Moving Average SA,Thous Unemployment Insurance: Initial Claims, State Programs SA, Thous Source: Department of Labor /Haver Analytics

20 8 All Employees: Goods-Producing Industries % Change - Year to Year SA, Thous All Employees: Total Nonfarm Payrolls % Change - Year to Year SA, Thous Source: Bureau of Labor Statistics /Haver Analytics

21 Consumer Confidence: Expectations SA, 1985= Source: The Conference Board /Haver Analytics

22 120 PPI: Crude Materials 6-month %Change-ann SA, 1982=100 PPI: Crude Materials % Change - Year to Year SA, 1982= Source: Bureau of Labor Statistics /Haver Analytics

23 CPI-U: All Items % Change - Year to Year SA, = Source: Bureau of Labor Statistics /Haver Analytics

24

25 12 Export Price Index: All Exports % Change - Year to Year NSA, 2000=100 Import Price Index: Nonpetroleum Imports % Change - Year to Year NSA, 2000= Source: Bureau of Labor Statistics /Haver Analytics

26 Monthly US Trade Balance Goods and Services ($, in millions) Source: Haver Analytics

27 30 Imports of Goods and Services, Census Basis % Change - Year to Year SA, Mil.$ Exports of Goods and Services, Census Basis % Change - Year to Year SA, Mil.$ Source: Bureau of the Census /Haver Analytics

28

29

30 Balance on Current Account as a % of GDP SAAR, % Source: Haver Analytics

31 20000 Net Foreign Official Purchases: Government Agency Bonds 12-month MovingAverage NSA, Mil.$ Net Foreign Official Purchases: Treasury Bonds & Notes 12-month MovingAverage NSA, Mil.$ Source: US Treasury /Haver Analytics

32

33

34

35 Why did US Finance go Bad?

36 Evolution of US Financial Structure The Decline of Commercial Deposit Banking Financial Deregulation The Shift to Fee and Commission Income Mortgage Backed Bonds and Securitisation The Collapse of the Savings and Loan Banks The 1980s Real Estate Collapse The Private Sector Response Securitisation The Basle Committee Capital Adequacy Standards The Financial Modernisation Act The Collapse of the Dot Com Bubble The Shift to Real Estate

37 Traditional lending and product sales have seen severe margin compression US banks net interest margin Percent US mutual fund distribution fee Basis points on Avg. AUM * * * * * * * * * * * * 37

38 Banks have been changing their business models to generate higher Sub prime yields mortgage Emerging market bonds Lending to Latin American countries Emerging economies are issuing bonds to finance their rapid economic growth Banks ignored the risk that governments could default Junk bonds investment Investment in junk bonds Increasing number of LBO transactions issued a large amount of high yield junk bond Savings and Loans companies joined in speculation of high yield bonds and property and failed when interest rates rose Alternative investment financing Lending to hedge funds and private equity firms Substantial demand from hedge funds and private equity for leverage financing Banks regard these new and successful investors as lower risks and lending covered by the investment collateral Lending to homeowners with lower credit quality Securitization allows banks to lend to higher risk homeowners on one hand while offloading the risks and loans to investors on the other hand Abundant liquidity and financial deregulation have enabled the change 1980 s s s 2000 s 38

39

40

41

42 Where were the Margins of Safety in Adjustable rate Sub Prime Mortgages? Cash Flows of ARMs Option ARMs 2/28, 3/27 Designed to Look like Hedge Finance in early years Income covered payments At reset the margins of safety are automatically reduced Outflow Re set Inflow

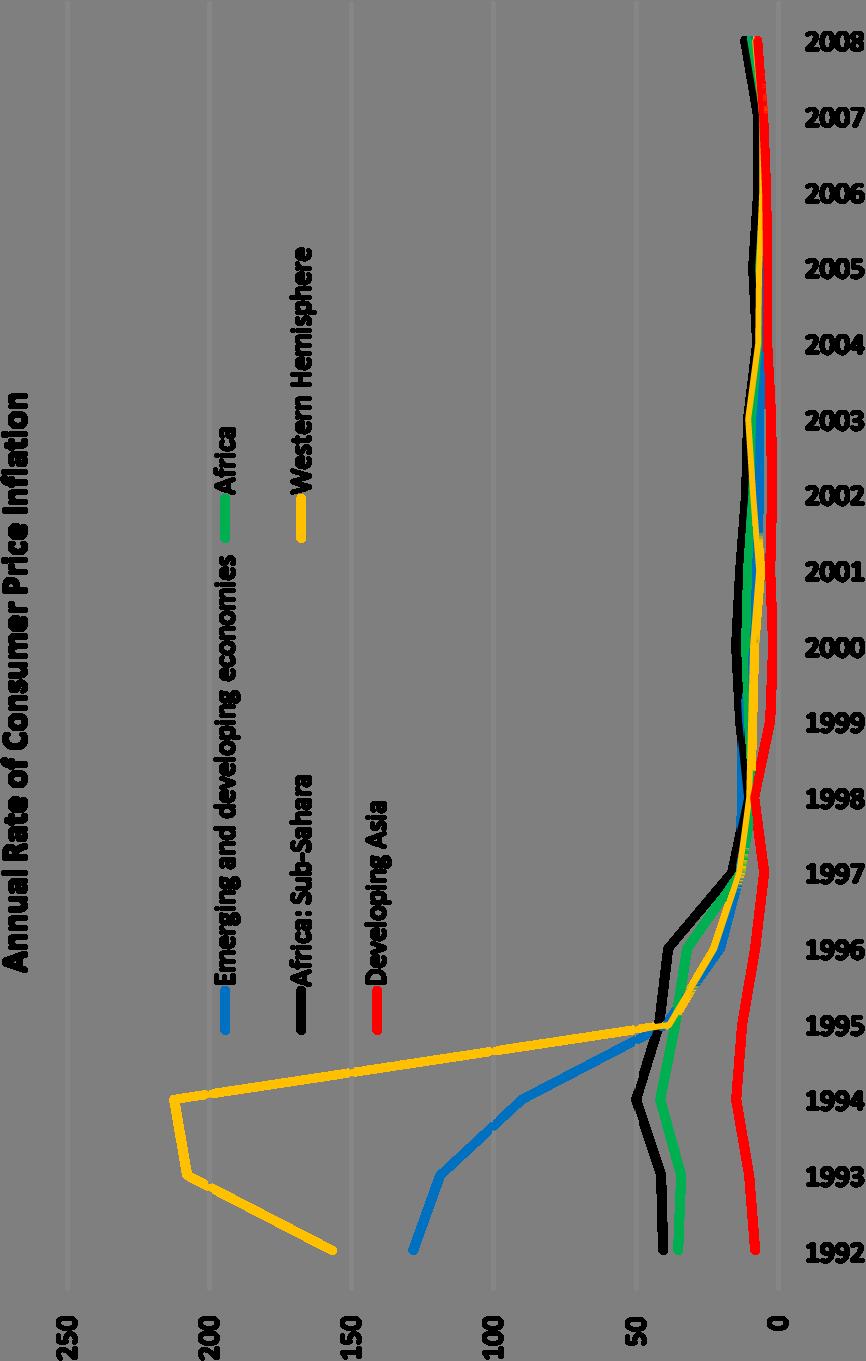

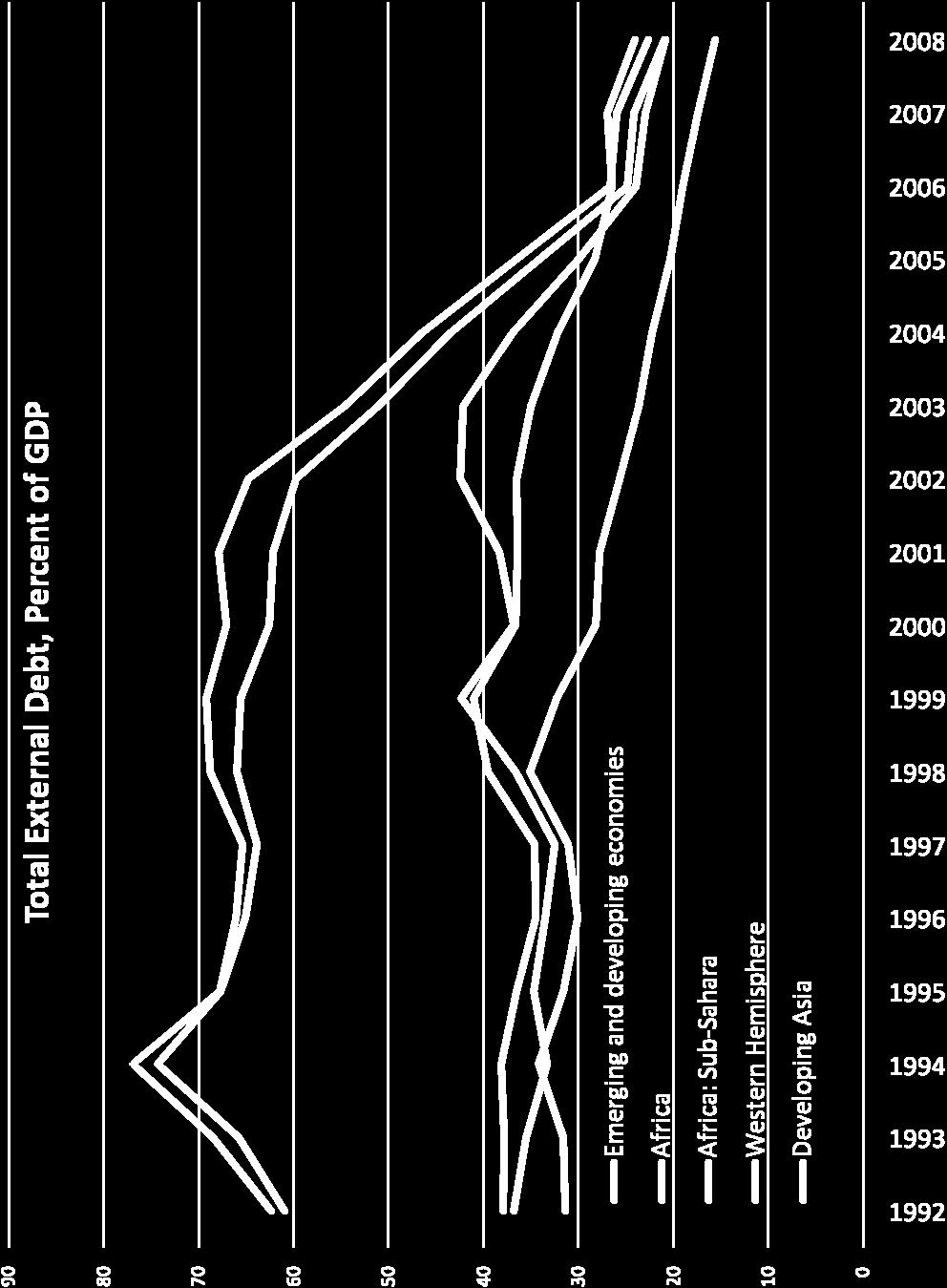

43

44 Interest Rate Spread: 10-Year Treasury Bond Less Fed Funds Rate % Source: Federal Reserve Board/Haver Analytics

45 Total Assets: All Commercial Banks SA, Bil.$ Cash Assets: All Commercial Banks SA, Bil.$ OCT NOV DEC JAN FEB MAR APR MAY JUN 08 JUL AUG SEP Source: Federal Reserve Board /Haver Analytics

46 Reserve Bank Credit Outstanding (Avg, Mil.$) Reserve Bank Credit: Primary Credit to Depository Institutions (Avg, Mil.$) Reserve Bank Credit: Primary Dealer Credit Facility (Avg, Mil.$) NOV DEC JAN FEB MAR Source: Federal Reserve Board /Haver Analytics APR MAY JUN 08 JUL AUG SEP OCT

47

48

49 Global Evolution of the Crisis Mid 2006 house prices stop rising Early 2007 Countrywide, New Century losses June 2007 SIV, and Conduits lose funding Summer 2007 Banks recapitalise, meet guarantees European holding CMOs, or financing US construction also hit covered bond market 2008 Second 9/11 Bear Stearns, Lehman Brothers AIG Liquidity crisis Hits Emerging market countries Capital flight, exchange rates, industrial production Collapse of global Trade finance China needs export financing Collapse of Global demand Hits least developed countries exports

50 Developing Country Experience during the Dot Com and Sub Prime Bubbles Exceptionally Positive Performance Rising growth rates Low, stable inflation rates Improved external (surplus) balances Improving debt burdens Rising FDI Inflows (primarily in emerging market economies) Rising employment levels 2

51 3

52

53 53

54

55

56

57 Emerging Markets BRICs were especially fortunate 57

58 58

59 59

60 60

61 What caused this good performance? Washington Consensus Policies? Or deregulated developed country financial systems? Private Equity Funds driving shareholder value Outsourcing of production and employment Rising foreign direct investment Rising US household mortgage debt Rising demand for developing country exports Commodity Index Funds + Speculation Rising Commodity Prices Improved developing country terms of trade Rising energy prices Most developing countries are now petroleum producers Investment in biofuels also improved soft commodity prices Interest Arbitrage carry trade Short term capital flows to emerging markets Lower interest rates / lower risk spreads lower debt service 61

62 Is this pattern likely to continue? The Bubble turned developing countries to export led growth dependent on primary commodity exports and semimanufactured processed goods Large external surpluses = Large global imbalances US demand made trade the engine of global growth US Financial System financed the growth of global demand 62

63 Global Response to Crisis Global stimulus packages to offset decline Need Coordinated response Surplus countries should lead to avoid aggravating global imbalances But Europe declines coordination or additional stimulus Only Japan and China have major stimulus Most developing countries do not have financial resources IMF will not approve financing for stimulus 63

64 US will adjust In absence of Global Coordinated Response Households will delever Higher savings rates, lower demand for imports Financial institututions will delever Reduced foreign investment Reduced outsourcing Reduced foreign financing Global trade and finance will contract Developing countries will again face external constraints IMF conditionality returns 64

65 What stimulus Response? Hydraulic Keynesian deficit spending Financial Bailouts little impact on incomes impact of balance sheets Government expenditures take time to implement are politically sensitive Are designed for cyclical downturns Designed to reduce excess capacity Not to make redundant capacity profitable 65

66 Is there an alternative stimulus policy? Roosevelt example increase incomes and employment directly TERA used by Roosevelt when Governor of NY CCC, FERA, PWA WPA Argentina example First used by Duhalde as Intendente of Lomas Zamorra 1980s Jefes de Hogares after the crisis Keynes s example Targetted sectoral demand 66

67 Federal Emergency Relief Administration Hopkins Direct grants to States (with 3:1 matching) Hired unemployed teachers to teach adults literacy to provide vocational training to provide rural schooling Jobs to students in laboratories, libraries and museums Rural rehabilitation seed fertilizer and live stock to provide self sufficiency Non farm family subsistence gardens School lunches provided by women on work relief 67

68 68

69 Keynes s concerns With unemployment over 10% We are more in need today of a rightly distributed demand than of a greater aggregate demand Facing a collapse in major export industries: unemployment was in iron, shipbuilding, coal Replacing foreign demand to support these industries would maintain excess capacity and create inflation Better use demand to make transition to new industries 69

70 For emerging market developing countries Facing loss of export led growth : New National Development Strategy Use external surplus to support domestic demand led growth This is not easy example of Japan How employment guarantee can help resolve this problem It can reduce domestic saving income security It can reduce reliance on exports sector programs example of Brazil s Medium Term Plan It can reduce reliance on investment financial stability of consumption led domestic growth Employment Guarantee can also alleviate inflation threat: Training buffer stock 70

71 For Least Developed Countries A suitably designed ELR programme to provide employment can also be designed to satisfy: MDG Goal 1: Eradicate Extreme Hunger and Poverty MDG Goal 2: Universal Primary Education MDG Goal 3: Promote Gender Equality and Empower Women MDG 4 and 5: Reduce Child Mortality and Improve Maternal Health 71

72 Employment Guarantee Crucial Component of Stimulus policy Anti inflation policy National development strategy MDG policy Emergency or Structural Policy? Antecedents precede crisis Provides structural support to labour market 72

73 Thank you

2012 As the Fundamentals Improve Stateside, They Deteriorate Abroad

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H 212 As the Fundamentals Improve Stateside, They Deteriorate Abroad December 211 Paul L. Kasriel, Chief Economist PH: 312..15 plk1@ntrs.com

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H 212 As the Fundamentals Improve Stateside, They Deteriorate Abroad December 211 Paul L. Kasriel, Chief Economist PH: 312..15 plk1@ntrs.com

The First Phase of the U.S. Recovery and Beyond

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference May 13, 2008 Janet L. Yellen President and CEO Federal Reserve Bank of San Francisco Overview Financial

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference May 13, 2008 Janet L. Yellen President and CEO Federal Reserve Bank of San Francisco Overview Financial

The World Economic & Financial System: Risks & Prospects

The World Economic & Financial System: Risks & Prospects Dr. Jacob A. Frenkel Chairman & CEO Group of Thirty (G30).Bank Indonesia 7th Annual International Seminar Global Financial Tsunami: What Can We

The World Economic & Financial System: Risks & Prospects Dr. Jacob A. Frenkel Chairman & CEO Group of Thirty (G30).Bank Indonesia 7th Annual International Seminar Global Financial Tsunami: What Can We

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Consumer Price Index, Jobless Claims, Housing Starts Each of These Reports Have Favorable Aspects to Note

Consumer Price Index, Jobless Claims, Housing Starts Each of These Reports Have Favorable Aspects to Note January 19, Asha G. Bangalore agb3@ntrs.com The Consumer Price Index (CPI) held steady in December,

Consumer Price Index, Jobless Claims, Housing Starts Each of These Reports Have Favorable Aspects to Note January 19, Asha G. Bangalore agb3@ntrs.com The Consumer Price Index (CPI) held steady in December,

Households: Net Worth Advances, Debt Outstanding Declines. Chart 1

Asha G. Bangalore agb3@ntrs.com Households: Net Worth Advances, Debt Outstanding Declines June 9, 2 Households experienced another quarter of gains in their net worth without improvements in real estate

Asha G. Bangalore agb3@ntrs.com Households: Net Worth Advances, Debt Outstanding Declines June 9, 2 Households experienced another quarter of gains in their net worth without improvements in real estate

Macroeconomic Outlook: Implications for Agriculture. It has been 26 years since we have experienced a significant recession

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Decline in Economic Activity Larger Than Advance GDP Estimate February 27, 2009

Northern Trust Global Economic Research 5 South LaSalle Chicago, Illinois 663 northerntrust.com Asha G. Bangalore agb3@ntrs.com Decline in Economic Activity Larger Than Advance GDP Estimate February 27,

Northern Trust Global Economic Research 5 South LaSalle Chicago, Illinois 663 northerntrust.com Asha G. Bangalore agb3@ntrs.com Decline in Economic Activity Larger Than Advance GDP Estimate February 27,

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Financial Markets Fall 2008 Economic Update

Financial Markets Fall 28 Economic Update October 7, 28 Jeff Rubin Chief Economist, Chief Strategist Avery Shenfeld Managing Director, Senior Economist Crash in Commodity Prices Exaggerates Growth Slowdown

Financial Markets Fall 28 Economic Update October 7, 28 Jeff Rubin Chief Economist, Chief Strategist Avery Shenfeld Managing Director, Senior Economist Crash in Commodity Prices Exaggerates Growth Slowdown

Liquidity Management: Beyond Quantitative Easing

Liquidity Management: Beyond Quantitative Easing June 2014 Agenda 1. Assessing Risk: Current Market Conditions a. Global Macroeconomics b. Monetary Policy c. Quantitative Easing (QE) d. Asset Bubbles e.

Liquidity Management: Beyond Quantitative Easing June 2014 Agenda 1. Assessing Risk: Current Market Conditions a. Global Macroeconomics b. Monetary Policy c. Quantitative Easing (QE) d. Asset Bubbles e.

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY. Paul Darby Executive Director & Deuty Chief Economist Twitter hashtag: #psforum

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

Economic Outlook in 2010

Economic Outlook in 2010 Presented to: Institute of Internal Auditors April 1, 2010 Harvey Rosenblum Executive Vice President & Director of Research Jessica Renier Senior Economic Analyst Federal Reserve

Economic Outlook in 2010 Presented to: Institute of Internal Auditors April 1, 2010 Harvey Rosenblum Executive Vice President & Director of Research Jessica Renier Senior Economic Analyst Federal Reserve

How Strong is the US Economy?

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H How Strong is the US Economy? December 2 Asha Bangalore. Senior Vice President PH: 3..16 agb3@ntrs.com 2 Northern Trust Corporation

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H How Strong is the US Economy? December 2 Asha Bangalore. Senior Vice President PH: 3..16 agb3@ntrs.com 2 Northern Trust Corporation

Economic Update: Will Tailwinds Offset Headwinds in 2012? Asha Bangalore

N O R T H E R N T R U S T Economic Update: Will Tailwinds Offset Headwinds in 2? Asha Bangalore Senior Vice President & Economist, Northern Trust (3) 444-4146, agb3@ntrs.com 1 2 Northern Trust Corporation

N O R T H E R N T R U S T Economic Update: Will Tailwinds Offset Headwinds in 2? Asha Bangalore Senior Vice President & Economist, Northern Trust (3) 444-4146, agb3@ntrs.com 1 2 Northern Trust Corporation

Transitioning From the Great Recession to Recovery to Expansion

Transitioning From the Great Recession to Recovery to Expansion AUGUSTINE FAUCHER, DIRECTOR OF MACROECONOMICS FROM MOODY S ECONOMY.COM The Great Recession Is Over Recessions since World War II Peak Trough

Transitioning From the Great Recession to Recovery to Expansion AUGUSTINE FAUCHER, DIRECTOR OF MACROECONOMICS FROM MOODY S ECONOMY.COM The Great Recession Is Over Recessions since World War II Peak Trough

Single-family home sales and construction are not expected to regain 2005 peaks

Single-family home sales and construction are not expected to regain 25 peaks Millions of units 8. 7. 6. 5. Housing starts (right axis) 4. Home sales (left axis) 3. 2. 1. 198 1985 199 1995 2 25 21 215

Single-family home sales and construction are not expected to regain 25 peaks Millions of units 8. 7. 6. 5. Housing starts (right axis) 4. Home sales (left axis) 3. 2. 1. 198 1985 199 1995 2 25 21 215

Real Estate Market. Lawrence Yun, Ph.D. Presentation to New England REALTORS Conference. February 2, 2010 NATIONAL ASSOCIATION OF REALTORS

Real Estate Market Trends & Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation to New England REALTORS Conference February 2, 2010 Housing Stimulus Impact Tax Credit

Real Estate Market Trends & Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation to New England REALTORS Conference February 2, 2010 Housing Stimulus Impact Tax Credit

2008 CRISIS : COLD OR CANCER?

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

The U.S. Economic Outlook

The U.S. Economic Outlook Gering/Scottsbluff Economic Forum August 23, 216 George A. Kahn Vice President and Economist The views expressed are those of the author and do not necessarily reflect the opinions

The U.S. Economic Outlook Gering/Scottsbluff Economic Forum August 23, 216 George A. Kahn Vice President and Economist The views expressed are those of the author and do not necessarily reflect the opinions

The Stimulus Didn t Work An Overlooked Fact that Needs Mention September 18, 2009

Northern Trust Global Economic Research 0 South LaSalle Chicago, Illinois northerntrust.com Asha G. Bangalore agb@ntrs.com The Stimulus Didn t Work An Overlooked Fact that Needs Mention September 18, 9

Northern Trust Global Economic Research 0 South LaSalle Chicago, Illinois northerntrust.com Asha G. Bangalore agb@ntrs.com The Stimulus Didn t Work An Overlooked Fact that Needs Mention September 18, 9

ECONOMIC AND FINANCIAL HIGHLIGHTS

ECONOMIC AND FINANCIAL HIGHLIGHTS DURABLE GOODS Orders and Shipments for Core Capital Goods 2 REAL ESTATE Pending Home Sales Index 3 S&P Case-Shiller Home Price Index 4 FHFA Home Price Index 5 Sales and

ECONOMIC AND FINANCIAL HIGHLIGHTS DURABLE GOODS Orders and Shipments for Core Capital Goods 2 REAL ESTATE Pending Home Sales Index 3 S&P Case-Shiller Home Price Index 4 FHFA Home Price Index 5 Sales and

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Capital Market Trends and Forecasts

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Q Economic Outlook

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Economic Outlook. Cathy E. Minehan President and CEO Federal Reserve Bank of Boston. Presented to Regional and Community Bankers June 7, 2005

Economic Outlook Cathy E. Minehan President and CEO Federal Reserve Bank of Boston Presented to Regional and Community Bankers June 7, 5 Overview of the US Economy Over the near-term, the expansion appears

Economic Outlook Cathy E. Minehan President and CEO Federal Reserve Bank of Boston Presented to Regional and Community Bankers June 7, 5 Overview of the US Economy Over the near-term, the expansion appears

North American Economic Outlook: Gradual Though Sustained Recovery

ECONOMICS I RESEARCH North American Economic Outlook: Gradual Though Sustained Recovery Presentation to the Canadian Association of Movers Paul Ferley (416) 974-7231 Assistant Chief Economist paul.ferley@rbc.com

ECONOMICS I RESEARCH North American Economic Outlook: Gradual Though Sustained Recovery Presentation to the Canadian Association of Movers Paul Ferley (416) 974-7231 Assistant Chief Economist paul.ferley@rbc.com

Capital Markets and M&A in Latin America

Capital Markets and M&A in Latin America 10th Annual LABA Conference Latin America: Growth Perspectives in a Shifting Political Landscape Bernardo Parnes Chief Executive Officer - Banco Bradesco BBI S.A.

Capital Markets and M&A in Latin America 10th Annual LABA Conference Latin America: Growth Perspectives in a Shifting Political Landscape Bernardo Parnes Chief Executive Officer - Banco Bradesco BBI S.A.

Recession Now Putting Our Forecast Where Our Mouth Has Been February 4, 2008

Northern Trust Global Economic Research 5 South LaSalle Chicago, Illinois 663 northerntrust.com Paul L. Kasriel Director of Economic Research 312..15 312.557.2675 fax plk1@ntrs.com Asha Bangalore Economist

Northern Trust Global Economic Research 5 South LaSalle Chicago, Illinois 663 northerntrust.com Paul L. Kasriel Director of Economic Research 312..15 312.557.2675 fax plk1@ntrs.com Asha Bangalore Economist

U.S. Economic Update and Outlook. Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 2013

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS Yiping Huang Seminar at the Crawford School of Economics and Government, ANU, March 1, 29 GLOBAL FINANCIAL CRISIS Three unique factors contributed to the current

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS Yiping Huang Seminar at the Crawford School of Economics and Government, ANU, March 1, 29 GLOBAL FINANCIAL CRISIS Three unique factors contributed to the current

Moving On Up Today s Economic Environment

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Housing and Credit Markets Outlook

Housing and Credit Markets Outlook FTA Revenue Estimating Conference Springfield, IL Amy Crews Cutts, SVP Chief Economist October 7, Equifax Inc. Government Shutdown and Debt Ceiling! As of October 1 st

Housing and Credit Markets Outlook FTA Revenue Estimating Conference Springfield, IL Amy Crews Cutts, SVP Chief Economist October 7, Equifax Inc. Government Shutdown and Debt Ceiling! As of October 1 st

Housing and Mortgage Market Update

Housing and Mortgage Market Update VCU Real Estate Trends Conference October 14, 29 Amy Crews Cutts, PhD Deputy Chief Economist Recession Risks Still Elevated, Housing Contraction Ongoing Recession risks

Housing and Mortgage Market Update VCU Real Estate Trends Conference October 14, 29 Amy Crews Cutts, PhD Deputy Chief Economist Recession Risks Still Elevated, Housing Contraction Ongoing Recession risks

Rising Risks for the Housing Outlook

Rising Risks for the Housing Outlook Master Builders Association of Pierce County October 17, 2018 Robert Dietz, Ph.D. NAHB Chief Economist Population Growth Pierce County population growing faster than

Rising Risks for the Housing Outlook Master Builders Association of Pierce County October 17, 2018 Robert Dietz, Ph.D. NAHB Chief Economist Population Growth Pierce County population growing faster than

Global Outlook and Policy Challenges. Olivier Blanchard Economic Counsellor Research Department

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Will The Recovery Hold? By Doug Duncan Vice President and Chief Economist Fannie Mae June 17, 2010

Will The Recovery Hold? By Doug Duncan Vice President and Chief Economist Fannie Mae June 17, 2010 1 Disclaimer Opinions, analyses, estimates, forecasts, and other views of Fannie Mae's Economics & Mortgage

Will The Recovery Hold? By Doug Duncan Vice President and Chief Economist Fannie Mae June 17, 2010 1 Disclaimer Opinions, analyses, estimates, forecasts, and other views of Fannie Mae's Economics & Mortgage

An Update on Economic Conditions. January 5, 2010

An Update on Economic Conditions Raymond Owens January 5, 21 Real Gross Domestic Product 8 7 6 5 4 Percent change from previous quarter at annual rate 3 Q3 2.2% 2 1-1 -2-3 -4-5 -6-7 21 22 23 24 25 26 27

An Update on Economic Conditions Raymond Owens January 5, 21 Real Gross Domestic Product 8 7 6 5 4 Percent change from previous quarter at annual rate 3 Q3 2.2% 2 1-1 -2-3 -4-5 -6-7 21 22 23 24 25 26 27

Capital Markets Update

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

- US LEI & CEI - Yardeni Research, Inc.

- US LEI & CEI - 11 1 Figure. LEADING & COINCIDENT ECONOMIC INDICATORS (=, ratio scale) 11 1 Leading Economic Indicators recovering rapidly. Coincident Economic Indicators recovering slowly. 9 9 9 9 7

- US LEI & CEI - 11 1 Figure. LEADING & COINCIDENT ECONOMIC INDICATORS (=, ratio scale) 11 1 Leading Economic Indicators recovering rapidly. Coincident Economic Indicators recovering slowly. 9 9 9 9 7

The Causes of the 2008 Financial Crisis

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

Economic Highlights. ISM Purchasing Managers Index 1. Sixth District Payroll Employment by Industry 2. Contributions to Real GDP Growth 3

December 1, 2010 Economic Highlights Manufacturing ISM Purchasing Managers Index 1 Employment Sixth District Payroll Employment by Industry 2 Economic Activity Contributions to Real GDP Growth 3 Prices

December 1, 2010 Economic Highlights Manufacturing ISM Purchasing Managers Index 1 Employment Sixth District Payroll Employment by Industry 2 Economic Activity Contributions to Real GDP Growth 3 Prices

The Asian Face of the Global Recession

The Asian Face of the Global Recession C.P. Chandrasekhar & Jayati Ghosh Delegates to the World Economic Forum at Davos this year came despondent and left in despair. Both the discussions and the new evidence

The Asian Face of the Global Recession C.P. Chandrasekhar & Jayati Ghosh Delegates to the World Economic Forum at Davos this year came despondent and left in despair. Both the discussions and the new evidence

House prices in the United States were 14.1 percent

NationalEconomicTrends August How Much Have US House Prices Fallen? House prices in the United States were 11 percent lower in the first quarter of than they were a year earlier, according to a widely

NationalEconomicTrends August How Much Have US House Prices Fallen? House prices in the United States were 11 percent lower in the first quarter of than they were a year earlier, according to a widely

Introduction and Economic Landscape. Vance Ginn Spring 2013

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

Economic Outlook June Economic Policy Division

Economic Outlook June 215 Economic Policy Division U.S. GDP Actual and Potential Quarterly, Q1 198 to Q4 215 Real GDP Trillion 29 Dollars Log Scale $18. Forecast $15. $12.5 Actual Potential $9. $6.5 198

Economic Outlook June 215 Economic Policy Division U.S. GDP Actual and Potential Quarterly, Q1 198 to Q4 215 Real GDP Trillion 29 Dollars Log Scale $18. Forecast $15. $12.5 Actual Potential $9. $6.5 198

Index of the articles in the Monthly Report

Index of the articles in the Monthly Report 2 Deutsche Bundesbank Wilhelm-Epstein-Strasse 14 60431 Frankfurt am Main Postfach 10 06 02 60006 Frankfurt am Main Germany In the form of catchwords, this index

Index of the articles in the Monthly Report 2 Deutsche Bundesbank Wilhelm-Epstein-Strasse 14 60431 Frankfurt am Main Postfach 10 06 02 60006 Frankfurt am Main Germany In the form of catchwords, this index

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

ELR as an Alternative Development Strategy

ELR as an Alternative Development Strategy Employment Guarantee Policies: Theory and Practice: A Conference of The Levy Economics Institute of Bard College Jan Kregel October 13-14, 14, 2006 Traditional

ELR as an Alternative Development Strategy Employment Guarantee Policies: Theory and Practice: A Conference of The Levy Economics Institute of Bard College Jan Kregel October 13-14, 14, 2006 Traditional

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Shanghai Market Turning the Corner

Shanghai Market Turning the Corner C. H. Kwan Senior Fellow, Nomura Institute of Capital Markets Research When the Lehman Shock hit major global stock markets in mid-september 2008, the Shanghai Composite

Shanghai Market Turning the Corner C. H. Kwan Senior Fellow, Nomura Institute of Capital Markets Research When the Lehman Shock hit major global stock markets in mid-september 2008, the Shanghai Composite

Emerging Trends in the U.S. and Colorado Economies

Emerging Trends in the U.S. and Colorado Economies Sam Chapman Associate Economist Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

Emerging Trends in the U.S. and Colorado Economies Sam Chapman Associate Economist Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

NationalEconomicTrends

NationalEconomicTrends January 00 Stag-nations Economic growth in the United States has slowed substantially since the days of rapid expansion during the mid to late 1990s. According to preliminary estimates,

NationalEconomicTrends January 00 Stag-nations Economic growth in the United States has slowed substantially since the days of rapid expansion during the mid to late 1990s. According to preliminary estimates,

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Economic & Financial Outlook

The Economic & Financial Outlook James Marple Director & Senior Economist TD Economics May 3, 2018 Global Economies Break Pattern Of Serial Disappointment 4.0 World GDP, Year/Year % Change 3.9 3.8 3.7

The Economic & Financial Outlook James Marple Director & Senior Economist TD Economics May 3, 2018 Global Economies Break Pattern Of Serial Disappointment 4.0 World GDP, Year/Year % Change 3.9 3.8 3.7

Vermont Tax Seminar. Comments on the 2017 Economic Outlook Presentation to the. December 8, 2016

Comments on the 2017 Economic Outlook Presentation to the Vermont Tax Seminar December 8, 2016 Jeffrey B. Carr President and Senior Economist Economic & Policy Resources, Inc. Now the 4 th Longest Up-Cycle

Comments on the 2017 Economic Outlook Presentation to the Vermont Tax Seminar December 8, 2016 Jeffrey B. Carr President and Senior Economist Economic & Policy Resources, Inc. Now the 4 th Longest Up-Cycle

Modest Economic Growth and Falling GDP Gap

Modest Economic Growth and Falling GDP Gap -. -. U.S. Economic Output (Real GDP - Quarterly Growth Rate).................................... : : : : : : : : : : -. -. -. -. -. -. -. -. -. -. -. -. -. -.

Modest Economic Growth and Falling GDP Gap -. -. U.S. Economic Output (Real GDP - Quarterly Growth Rate).................................... : : : : : : : : : : -. -. -. -. -. -. -. -. -. -. -. -. -. -.

ECONOMIC & REVENUE UPDATE

January 11, 2018 Summary summary The U.S. labor market gained 148,000 net new jobs in December. U.S. housing starts in November 2017 were 12.9% above their year-ago level. Consumer confidence declined

January 11, 2018 Summary summary The U.S. labor market gained 148,000 net new jobs in December. U.S. housing starts in November 2017 were 12.9% above their year-ago level. Consumer confidence declined

Poland s Economic Prospects

Poland s Economic Prospects Unicredit Conference Warsaw, June 8, 11 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe Recovery is driven by domestic demand Contributions to Real

Poland s Economic Prospects Unicredit Conference Warsaw, June 8, 11 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe Recovery is driven by domestic demand Contributions to Real

Economic Outlook. Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis. NLB,LLC The Lodge, Des Peres, MO.

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

The Recession

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

Confronting the Global Crisis in Latin America: What is the Outlook? Coordinators

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

National Economic Indicators. May 7, 2018

National Economic Indicators May 7, 18 Table of Contents GDP Release Date Latest Period Page Table: Real Gross Domestic Product Apr-7-18 8:31 Q1-18 Real Gross Domestic Product Apr-7-18 8:31 Q1-18 5 Decomposition

National Economic Indicators May 7, 18 Table of Contents GDP Release Date Latest Period Page Table: Real Gross Domestic Product Apr-7-18 8:31 Q1-18 Real Gross Domestic Product Apr-7-18 8:31 Q1-18 5 Decomposition

Economic and Market Outlook

Economic and Market Outlook Third Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Economic and Market Outlook Third Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Midwest Perspectives. Bill Testa Vice President Federal Reserve Bank of Chicago

Midwest Perspectives Community Banking Conference University of Wisconsin--Whitewater April 27, 2018 Bill Testa Vice President Federal Reserve Bank of Chicago Topics Today U.S. Economy (doing well) Midwest

Midwest Perspectives Community Banking Conference University of Wisconsin--Whitewater April 27, 2018 Bill Testa Vice President Federal Reserve Bank of Chicago Topics Today U.S. Economy (doing well) Midwest

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Economic Conditions and Outlook and Consumer Credit Conditions

Economic Conditions and Outlook and Consumer Credit Conditions NACM-CFDD Kansas City Kansas City, MO Kelly D. Edmiston Senior Economist Disclaimer This presentation reflects the views of the speaker and

Economic Conditions and Outlook and Consumer Credit Conditions NACM-CFDD Kansas City Kansas City, MO Kelly D. Edmiston Senior Economist Disclaimer This presentation reflects the views of the speaker and

Old Dominion University 2013 National Economic Outlook

Old Dominion University 2013 National Economic Outlook January 30, 2013 Professor Vinod Agarwal Professor Mohammad Najand Professor Gary A. Wagner www.odu.edu/forecasting 1 Presentation Outline 2012 Scorecard

Old Dominion University 2013 National Economic Outlook January 30, 2013 Professor Vinod Agarwal Professor Mohammad Najand Professor Gary A. Wagner www.odu.edu/forecasting 1 Presentation Outline 2012 Scorecard

U.S. Economy and Financial Markets

U.S. Economy and Financial Markets Economic Growth and Output Business Income and Finance Business Inventory Business Investment Consumption Housing Investment Income and Savings U.S. Aggregate Demand

U.S. Economy and Financial Markets Economic Growth and Output Business Income and Finance Business Inventory Business Investment Consumption Housing Investment Income and Savings U.S. Aggregate Demand

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

BOMA National Advisory Council Meeting Seaport Hotel, Boston MA

BOMA National Advisory Council Meeting Seaport Hotel, Boston MA May 5, 2017 Jeff Fuhrer, EVP and Senior Policy Advisor Federal Reserve Bank of Boston 1 Raising rates? Raising rates more this year? Next?

BOMA National Advisory Council Meeting Seaport Hotel, Boston MA May 5, 2017 Jeff Fuhrer, EVP and Senior Policy Advisor Federal Reserve Bank of Boston 1 Raising rates? Raising rates more this year? Next?

Economic Update and Outlook

Economic Update and Outlook NAIOP Vancouver Chapter Breakfast Seminar Thursday, November 18, 2010 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global and U.S. economies Canadian economy

Economic Update and Outlook NAIOP Vancouver Chapter Breakfast Seminar Thursday, November 18, 2010 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: Global and U.S. economies Canadian economy

Nonfarm Payroll Employment

PRESIDENT'S REPORT TO THE BOARD OF DIRECTORS, FEDERAL RESERVE BANK OF BOSTON Current Economic Developments - June 10, 2004 Data released since your last Directors' meeting show the economy continues to

PRESIDENT'S REPORT TO THE BOARD OF DIRECTORS, FEDERAL RESERVE BANK OF BOSTON Current Economic Developments - June 10, 2004 Data released since your last Directors' meeting show the economy continues to

Globalization. International Financial (Chap. 8) and Monetary (Chap. 9) Relations

and Monetary (Chap. 9) Relations") Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Economic Outlook June Economic Policy Division

Economic Outlook June 215 Economic Policy Division U.S. GDP Actual and Potential Quarterly, Q1 198 to Q4 215 Real GDP Trillion 29 Dollars Log Scale $18. Forecast $15. $12.5 Actual Potential $9. $6.5 198

Economic Outlook June 215 Economic Policy Division U.S. GDP Actual and Potential Quarterly, Q1 198 to Q4 215 Real GDP Trillion 29 Dollars Log Scale $18. Forecast $15. $12.5 Actual Potential $9. $6.5 198

Worcester Business Journal Economic Forecast Breakfast February 13, Jeff Fuhrer, EVP and Senior Policy Advisor Federal Reserve Bank of Boston

Worcester Business Journal Economic Forecast Breakfast February 3, 25 Jeff Fuhrer, EVP and Senior Policy Advisor Federal Reserve Bank of Boston X Not this lady X Not this guy 2 26:Jan 26:Sep 27: 28:Jan

Worcester Business Journal Economic Forecast Breakfast February 3, 25 Jeff Fuhrer, EVP and Senior Policy Advisor Federal Reserve Bank of Boston X Not this lady X Not this guy 2 26:Jan 26:Sep 27: 28:Jan

Key Commodity Themes. Maxwell Gold Director of Investment Strategy. Gradient Investments Elite Advisor Forum October 5 th, 2017

Key Commodity Themes Maxwell Gold Director of Investment Strategy Gradient Investments Elite Advisor Forum October 5 th, 2017 2001 2002 2002 2003 2004 2005 2006 2007 2007 2008 2009 2010 2011 2012 2012

Key Commodity Themes Maxwell Gold Director of Investment Strategy Gradient Investments Elite Advisor Forum October 5 th, 2017 2001 2002 2002 2003 2004 2005 2006 2007 2007 2008 2009 2010 2011 2012 2012

Global Economic Prospects: Update Global Recovery in Transition

Global Economic Prospects: Update Global Recovery in Transition April 2015 M. Ayhan Kose 1 Global Prospects: Three Questions 1. How have global economic conditions changed since December? Broadly as expected;

Global Economic Prospects: Update Global Recovery in Transition April 2015 M. Ayhan Kose 1 Global Prospects: Three Questions 1. How have global economic conditions changed since December? Broadly as expected;

How to Fix The Canadian Recession

How to Fix The Canadian Recession CFA Québec January 22, 2009 Glen Hodgson Senior Vice-President and Chief Economist hodgson@conferenceboard.ca Global Economic Highlights The world economy expanded by

How to Fix The Canadian Recession CFA Québec January 22, 2009 Glen Hodgson Senior Vice-President and Chief Economist hodgson@conferenceboard.ca Global Economic Highlights The world economy expanded by

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Understanding the Policy Response to the Financial Crisis. Macroeconomic Theory Honors EC 204

Understanding the Policy Response to the Financial Crisis Macroeconomic Theory Honors EC 204 Key Problems in the Crisis Bank Solvency Declining home prices and rising mortgage defaults put banks in danger

Understanding the Policy Response to the Financial Crisis Macroeconomic Theory Honors EC 204 Key Problems in the Crisis Bank Solvency Declining home prices and rising mortgage defaults put banks in danger

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

North American Economic Outlook: Climbing Out of Recession

North American Economic Outlook: Climbing Out of Recession Presentation to the Canadian Association of Movers Paul Ferley (1) 97-731 Assistant Chief Economist paul.ferley@rbc.com November 17, 9 U.S. Economic

North American Economic Outlook: Climbing Out of Recession Presentation to the Canadian Association of Movers Paul Ferley (1) 97-731 Assistant Chief Economist paul.ferley@rbc.com November 17, 9 U.S. Economic

ECONOMIC AND FINANCIAL HIGHLIGHTS

ECONOMIC AND FINANCIAL HIGHLIGHTS LABOR MARKET Contributions to Change in Nonfarm Payrolls 2 Unemployment and Labor Force Participation Rate 3 MANUFACTURING ISM Manufacturing Index 4 CONSUMERS Light Vehicle

ECONOMIC AND FINANCIAL HIGHLIGHTS LABOR MARKET Contributions to Change in Nonfarm Payrolls 2 Unemployment and Labor Force Participation Rate 3 MANUFACTURING ISM Manufacturing Index 4 CONSUMERS Light Vehicle

United States. GDP Growth Annualized Percentage Change. Industrial Production Annualized Percentage Change

Output Indicators GDP Growth Annualized Percentage Change Industrial Production Annualized Percentage Change 0 2 4 6 2.3-5 0 5 4.5 GDP Growth Industrial Production 1.0 1.5 2.0 2.5 3.0 3.5 4.0 2.9-4 -2

Output Indicators GDP Growth Annualized Percentage Change Industrial Production Annualized Percentage Change 0 2 4 6 2.3-5 0 5 4.5 GDP Growth Industrial Production 1.0 1.5 2.0 2.5 3.0 3.5 4.0 2.9-4 -2

December 2014 FINANCIAL MARKET REVIEW

December 2014 FINANCIAL MARKET REVIEW Buena Vista Investment Management LLC 241 Third Street South Wisconsin Rapids, WI 54494 715-422-0700 http://buenavistainv.com December 2014 Why Portfolios Remain Diversified

December 2014 FINANCIAL MARKET REVIEW Buena Vista Investment Management LLC 241 Third Street South Wisconsin Rapids, WI 54494 715-422-0700 http://buenavistainv.com December 2014 Why Portfolios Remain Diversified

National Monetary Policy Forum. Chris Loewald, Head: Policy Development and Research 10 April 2016 Pretoria

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

United States. Gross Domestic Product Percent change over year-ago level. Industrial Production Index, 2010=100. Unemployment Rate Percent

United States Summary Indicators Gross Domestic Product Percent change over year-ago level Industrial Production Index, 2010=100 1.0 1.5 2.0 2.5 3.0 3.5 4.0 2.5 108 110 112 114 114.9 4.0 4.5 5.0 5.5 6.0

United States Summary Indicators Gross Domestic Product Percent change over year-ago level Industrial Production Index, 2010=100 1.0 1.5 2.0 2.5 3.0 3.5 4.0 2.5 108 110 112 114 114.9 4.0 4.5 5.0 5.5 6.0

Economic Outlook. Presented to IPMA Executive Seminar. Steve Lerch Chief Economist & Executive Director. September 25, 2012 Chelan, Washington

Presented to IPMA Executive Seminar Steve Lerch Chief Economist & Executive Director Chelan, Washington WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL Summary The updated economic forecast is very

Presented to IPMA Executive Seminar Steve Lerch Chief Economist & Executive Director Chelan, Washington WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL Summary The updated economic forecast is very

There has been considerable discussion of the possibility

NationalEconomicTrends February Housing and the R Word There has been considerable discussion of the possibility that ongoing troubles in the housing market could push the economy into recession 1 But

NationalEconomicTrends February Housing and the R Word There has been considerable discussion of the possibility that ongoing troubles in the housing market could push the economy into recession 1 But

Macroeconomic Uncertainty

Macroeconomic Uncertainty Importance of Financial Planning There is, in fact, a direct relationship between household financial stability and the stability of the U.S. economy. Thus, the Federal Reserve

Macroeconomic Uncertainty Importance of Financial Planning There is, in fact, a direct relationship between household financial stability and the stability of the U.S. economy. Thus, the Federal Reserve

LAO ECONOMIC MONITOR APRIL 2017

LAO ECONOMIC MONITOR APRIL 2017 May-June 2017 1. Recent Economic Developments and Outlook 2. Health Sector Financing in Lao PDR 1. Recent Economic Developments Contents 1. Key findings 2. Growth and inflation

LAO ECONOMIC MONITOR APRIL 2017 May-June 2017 1. Recent Economic Developments and Outlook 2. Health Sector Financing in Lao PDR 1. Recent Economic Developments Contents 1. Key findings 2. Growth and inflation

National Economic Conditions. Cheyenne AIA Meeting February 25th, 2011 Rob Godby

National Economic Conditions Cheyenne AIA Meeting February 25th, 2011 Rob Godby Percent Change Recovery is Technically Underway 8 Quarter-Quarter Growth in Real GDP 6 4 2 0-2 -4-6 -8 I II III IV I II III

National Economic Conditions Cheyenne AIA Meeting February 25th, 2011 Rob Godby Percent Change Recovery is Technically Underway 8 Quarter-Quarter Growth in Real GDP 6 4 2 0-2 -4-6 -8 I II III IV I II III

The Financial Crisis of ? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

ECONOMIC AND FINANCIAL HIGHLIGHTS

ECONOMIC AND FINANCIAL HIGHLIGHTS FEDERAL RESERVE BALANCE SHEET Assets and Liabilities 2-3 REAL ESTATE Construction Spending 4 CoreLogic Home Price Index 5 Mortgage Rates and Applications 6-7 CONSUMER

ECONOMIC AND FINANCIAL HIGHLIGHTS FEDERAL RESERVE BALANCE SHEET Assets and Liabilities 2-3 REAL ESTATE Construction Spending 4 CoreLogic Home Price Index 5 Mortgage Rates and Applications 6-7 CONSUMER

Global Economic Prospects

Global Economic Prospects Slow and halting progress Andrew Burns DEC Prospects Group October, 22, 2012 1 Despite better financial conditions, stronger growth remains elusive May/June financial turmoil

Global Economic Prospects Slow and halting progress Andrew Burns DEC Prospects Group October, 22, 2012 1 Despite better financial conditions, stronger growth remains elusive May/June financial turmoil