2008 CRISIS : COLD OR CANCER?

|

|

|

- Isabella Dixon

- 5 years ago

- Views:

Transcription

1 2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin

2 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market and State Lessons for capitalism 2

3 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market and State Lessons for capitalism 3

4 Financial crisis Banking Crises Bankruptcy I n a b i l i t y to p ay d ebts. OR Run on the Bank, Credit Crunch

5 Financial crisis Economic Crises An economic crisis can take the form of a recession or a depression. Economic Crisis will most likely experience a falling GDP, a drying up of liquidity and rising/falling prices due to inflation / deflation

6 Financial crisiss Capital Market Bubbles/Crashes Market Price of stocks are higher than present value of future Cash flows. A dramatic decline of stock prices in a market. Crashes are driven by panic as much as by underlying economic factors

7 Financial crisis Currency Crisis A currency crisis occurs when the value of a currency changes quickly, undermining its ability to serve as a Medium of exchange or a Store of value.

8 Financial crisis Stock Market Crisis 1910: Shanghai rubber stock market crisis 1929: Wall Street Crash 1980: Japanese property bubble A Short History Bank Crisis 1980: Latin American debt crisis; beginning in Mexico : United State Saving & Loan Crisis Economic Crisis : Argentine economic crisis [breakdown of banking system] Currency Crisis : Speculative attacks on currencies in the European Exchange Rate Mechanism Economic Crisis in Mexico, speculative attack and default on Mexico Debts

9 A short crisis? 9

10 Jul 25, 2009 The Recession Is Over hits for "recession is over Slate The Recession Is Over! What America's best economic forecaster is saying. By Daniel GrossPosted Tuesday, July 14, 2009 Sept. 15, 2009 Bernanke declares 'recession is very likely over' Unfortunately, unemployment will come down slowly

11 The roots of the crisis Easy access to cheap borrowing combined with: low interest rates (since the collapse of the internet bubble) null regulation (Glass-Steagall Act in 1999) Fundamentals of the US economy Low level of savings rate Unbalanced international trade Excessive private consumption Financial sector oriented economy Last transformation of the American dream capitalism Risk value: new sources of profit 11

12 Water in the dam Asset price bubbles are not rare in history (tulip speculation in Netherlands, share prices in the 1920s, «dotcom» bubble ) Low US interest rates Low Japanese interest rates Impact of China and sovereign wealth funds (state-owned investment fund composed of financial assets such as stocks, bonds, property, precious metals or other) 12

13 Why low interest rates? Economic boost? Laxist monetary policy? Stop increasing Wages? -European responses different from the US policy: - Competition race? - More cautious Euro zone? 13

14 Easy mortgage: subprimes A myriad of actors Subprime borrowing Credit score (good borrower vs. bad borrower) Adjustable-rate mortgages Expectations that house prices would rise faster than loan rates Subprime crisis once mortgages securitized RMBS (Residential Mortgage Backed Security) SPV (Special Purpose Vehicle) Things can go wrong 14

15 Explosion in mortgage assets, USA 2004: beginning of the end 15

16 Housing market 16

17 The crisis goes on 17

18 Why did banks create these securities? How banks work? Is there a risk for not getting back my money? Basel capital rules (Basel I in 1998 and Basel II in 2004) In the 1990s, they changed their core business Trading income Increasing fees from mortgage securitization A new financial capitalism is born 18

19 Explosion in mortgage assets, USA 2004: beginning of the end 19

20 Financial (De)regulation New US policies to encourage home ownership Changes to Fannie Mae and Freddie Mac rules Changes to rules on investment banks Publication of Basel II proposals 20

21 Consequences A US CREDIT CRUNCH followed by an ECONOMIC CRISIS 21

22 22

23 23

24 Bad times for the economy Macroeconomic consequences Microeconomic consequences Financial consequences Political consequences 24

25 Macroeconomic consequences GDP growth Public Debt Unemployment Income inequalities 25

26 GDP impact

27 More recently 27

28 GDP decrease in developped countries Table 1.1 The global outlook in summary (percentage change from previous year, except interest rates and oil price) e 2010f 2011f 2012f Real GDP growth 5 World 1,7-2,1 3,3 3,3 3,5 Memo item: World (PPP weights) 6 1,3-0,4 4,2 4,0 4,3 High income 0,4-3,3 2,3 2,4 2,7 OECD Countries 0,3-3,4 2,2 2,3 2,6 Euro Area 0,4-4,1 0,7 1,3 1,8 Japan -1,2-5,2 2,5 2,1 2,2 United States 0,4-2,4 3,3 2,9 3,0 Non-OECD countries 3,0-1,7 4,2 4,2 4,5 Developing countries 5,7 1,7 6,2 6,0 6,0 East Asia and Pacific 8,5 7,1 8,7 7,8 7,7 China 9,6 8,7 9,5 8,5 8,2 Indonesia 6,0 4,5 5,9 6,2 6,3 Thailand 2,5-2,3 6,2 4,0 5,0 Europe and Central Asia 4,2-5,3 4,1 4,2 4,5 Russia 5,6-7,9 4,5 4,8 4,7 Turkey 0,7-4,7 6,3 4,2 4,7 Poland 4,8 1,7 3,0 3,7 4,0 Latin America and Caribbean 4,1-2,3 4,5 4,1 4,2 Brazil 5,1-0,2 6,4 4,5 4,1 Mexico 1,8-6,5 4,3 4,0 4,2 Argentina 7,0-1,2 4,8 3,4 4,4 28

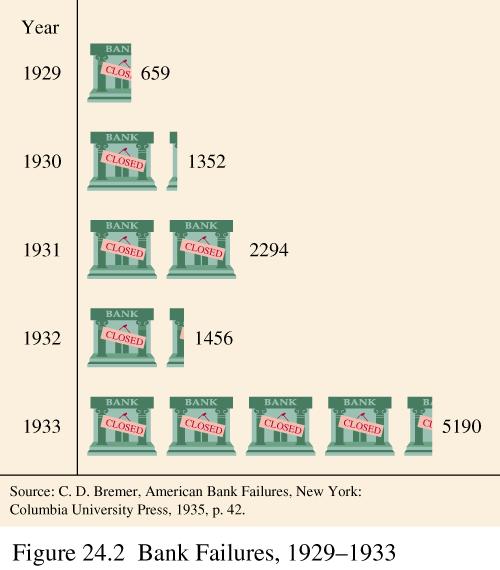

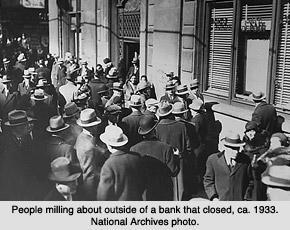

29 Public debt levels 29

30 Confidence erroded 30

31 Bank lending growth 31

32 Labor still prime affected 32

33 Crisis and unemployment 33

34 Crisis and income inequalities in the US 34

35 How the crisis affected global trade? Volume of world merchandise exports, (Annual % change) Growth in World merchandise exports trade by region (Year to year % change in dollar values) 35

36 Microeconomic consequences I Bank Failures 36

37 Microeconomic consequences II 37

38 Time-lags: Schematic comparison of stock markets, employment, public revenues and public debt Stock markets Employment Public revenues Public debt?? uncertainties??????? Oct Nov Dec Jan Feb Mar Apr May June Jul Aug Sep Oct Nov Dec Jan Feb Mar G20 G20 G20

39 To sum up Basic story of the crisis: Causes of mortgage bubble Role of the financial sector Manage risks Allocate capital Run payment mechanisms Regulators Insufficient regulations Special interests Economics as a not so credible science 39

40 Lessons for Capitalism Permanent sources of crisis: Information Confidence Corporate governance Market and States Capitalism and self-regulation Governments are strongly exposed 40

41 41

Global Economic Prospects and the Developing Countries William Shaw December 1999

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

Global Economic Prospects: Navigating strong currents

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

2016 Economic Outlook for Ireland & Eurozone IFP Launch

2016 Economic Outlook for Ireland & Eurozone IFP Launch December 3 rd 2015 Jim Power Global Background US & UK growing at reasonable pace Euro Zone growing well below potential Emerging markets in some

2016 Economic Outlook for Ireland & Eurozone IFP Launch December 3 rd 2015 Jim Power Global Background US & UK growing at reasonable pace Euro Zone growing well below potential Emerging markets in some

Financial Analysts Meeting. 4 th November 2010

Financial Analysts Meeting 4 th November EH world macro economic scenario -2011 World economy has registered a clear rebound World GDP rebounded by +5,8% between Q1- and Q2-. with a strong upturn of world

Financial Analysts Meeting 4 th November EH world macro economic scenario -2011 World economy has registered a clear rebound World GDP rebounded by +5,8% between Q1- and Q2-. with a strong upturn of world

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

Financial Crisis and Global Recession: At a Turning Point?

Financial Crisis and Global Recession: At a Turning Point? Richard Newfarmer Special Representative to UN and WTO World Bank Cairo June 15, 2009 Main messages Recession in the US now appears to be bottoming

Financial Crisis and Global Recession: At a Turning Point? Richard Newfarmer Special Representative to UN and WTO World Bank Cairo June 15, 2009 Main messages Recession in the US now appears to be bottoming

GLOBAL MARKET OUTLOOK

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

The Forecast for Emerging Markets

The Forecast for Emerging Markets Monday, April 27, 2009 09:30 AM - 10:45 AM Moderator Komal Sri-Kumar, Managing Director, Chief Global Strategist, TCW Group Inc.; Senior Fellow, Milken Institute Speakers

The Forecast for Emerging Markets Monday, April 27, 2009 09:30 AM - 10:45 AM Moderator Komal Sri-Kumar, Managing Director, Chief Global Strategist, TCW Group Inc.; Senior Fellow, Milken Institute Speakers

The Mexican Economy: Now and in the Future

Manuel Sánchez BBVA Investor conference "LATAM: Growth at your fingertips" Milan, Italy, May 10 2012 Index 1 Structural strengths 2 Recent developments and outlook 3 Long term opportunities 4 Consolidation

Manuel Sánchez BBVA Investor conference "LATAM: Growth at your fingertips" Milan, Italy, May 10 2012 Index 1 Structural strengths 2 Recent developments and outlook 3 Long term opportunities 4 Consolidation

The World Economic & Financial System: Risks & Prospects

The World Economic & Financial System: Risks & Prospects Dr. Jacob A. Frenkel Chairman & CEO Group of Thirty (G30).Bank Indonesia 7th Annual International Seminar Global Financial Tsunami: What Can We

The World Economic & Financial System: Risks & Prospects Dr. Jacob A. Frenkel Chairman & CEO Group of Thirty (G30).Bank Indonesia 7th Annual International Seminar Global Financial Tsunami: What Can We

Global Outlook and Policy Challenges. Olivier Blanchard Economic Counsellor Research Department

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Economic Status and Policies

China International Sulphur & Sulphuric Acid Conference (212) Economic Status and Policies Zhao Jinping Dept. of Foreign Economic Relations The Development Research Center of the State Council of China

China International Sulphur & Sulphuric Acid Conference (212) Economic Status and Policies Zhao Jinping Dept. of Foreign Economic Relations The Development Research Center of the State Council of China

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

ECONOMIC BULLETIN - No. 41, NOVEMBER Statistical tables

ECONOMIC BULLETIN - No. 41, NOVEMBER 2005 APPENDIX Appendix Statistical tables The world economy Table a1 GDP at constant prices a2 Industrial production a3 Consumer prices a4 External current account

ECONOMIC BULLETIN - No. 41, NOVEMBER 2005 APPENDIX Appendix Statistical tables The world economy Table a1 GDP at constant prices a2 Industrial production a3 Consumer prices a4 External current account

Capital Markets Update

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Asia s strongest brand in banking, banking the world s strongest economies

Credit Suisse Investor Conference Peter Wong, Chief Executive, HSBC Asia-Pacific Asia s strongest brand in banking, banking the world s strongest economies 21 March 2011 www.hsbc.com Forward-looking statements

Credit Suisse Investor Conference Peter Wong, Chief Executive, HSBC Asia-Pacific Asia s strongest brand in banking, banking the world s strongest economies 21 March 2011 www.hsbc.com Forward-looking statements

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY. Paul Darby Executive Director & Deuty Chief Economist Twitter hashtag: #psforum

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

A Global Economic and Market Outlook

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

The Argentine economy in the new political and international environment. MIGUEL A. KIGUEL econviews

The Argentine economy in the new political and international environment MIGUEL A. KIGUEL econviews October 2009 1 Outline The international environment is helping Argentina once again The domestic financial

The Argentine economy in the new political and international environment MIGUEL A. KIGUEL econviews October 2009 1 Outline The international environment is helping Argentina once again The domestic financial

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno eparker@unr.edu DJIA / CPI 15,000 10,000 5,000 0 1949 1951 1953 A Look at the DJIA Adjusting

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno eparker@unr.edu DJIA / CPI 15,000 10,000 5,000 0 1949 1951 1953 A Look at the DJIA Adjusting

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference May 13, 2008 Janet L. Yellen President and CEO Federal Reserve Bank of San Francisco Overview Financial

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference May 13, 2008 Janet L. Yellen President and CEO Federal Reserve Bank of San Francisco Overview Financial

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking Institutional Money Kongress Frankfurt, 21 February 2017 300 Park Avenue South - 5

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking Institutional Money Kongress Frankfurt, 21 February 2017 300 Park Avenue South - 5

The First Phase of the U.S. Recovery and Beyond

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

The 2008 crisis and the future: Have the important lessons been learned?

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

Emerging Global Challenges and implications for Indonesia

Emerging Global Challenges and implications for Indonesia Muhammad Chatib Basri Harvard Kennedy School and University of Indonesia Short term problems: macroeconomic stability 2 The macroeconomic impact

Emerging Global Challenges and implications for Indonesia Muhammad Chatib Basri Harvard Kennedy School and University of Indonesia Short term problems: macroeconomic stability 2 The macroeconomic impact

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

The economic crisis, the health sector, & why you should be worried

Workshop 11 Public procurement from the private sector: Austerity, PPP & health service innoavtion Gastein, 6 th October 2012 The economic crisis, the health sector, & why you should be worried Steve Wright

Workshop 11 Public procurement from the private sector: Austerity, PPP & health service innoavtion Gastein, 6 th October 2012 The economic crisis, the health sector, & why you should be worried Steve Wright

The Korean Economy: Resilience amid Turbulence

The Korean Economy: Resilience amid Turbulence Dr. Il SaKong Special Economic Advisor Adviser to the President Republic of Korea November 17, 17, 2008 November 17, 2008 1. Recent Macroeconomic Developments

The Korean Economy: Resilience amid Turbulence Dr. Il SaKong Special Economic Advisor Adviser to the President Republic of Korea November 17, 17, 2008 November 17, 2008 1. Recent Macroeconomic Developments

Transitioning From the Great Recession to Recovery to Expansion

Transitioning From the Great Recession to Recovery to Expansion AUGUSTINE FAUCHER, DIRECTOR OF MACROECONOMICS FROM MOODY S ECONOMY.COM The Great Recession Is Over Recessions since World War II Peak Trough

Transitioning From the Great Recession to Recovery to Expansion AUGUSTINE FAUCHER, DIRECTOR OF MACROECONOMICS FROM MOODY S ECONOMY.COM The Great Recession Is Over Recessions since World War II Peak Trough

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability Julio Velarde Governor Central Bank of Peru March 2016 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments

Monetary Policy: A Key Driver for Long Term Macroeconomic Stability Julio Velarde Governor Central Bank of Peru March 2016 Agenda 1. Peru s growth is based on strong fundamentals 2. Recent economic developments

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Mexican Q1 economic data: a reality shock, or there is still a brighter outlook?

Mexican Q1 economic data: a reality shock, or there is still a brighter outlook? Rafael Amiel, Director Latin America Economics IHS Global Insight Julio 2013 Mexico becomes fashionable again Mexico Makes

Mexican Q1 economic data: a reality shock, or there is still a brighter outlook? Rafael Amiel, Director Latin America Economics IHS Global Insight Julio 2013 Mexico becomes fashionable again Mexico Makes

Macroeconomic Outlook: Implications for Agriculture. It has been 26 years since we have experienced a significant recession

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

BRICs: actual growth and cooperation perspectives. International Advisory Council 3 rd Metting August 15, Luciano Coutinho President

BRICs: actual growth and cooperation perspectives International Advisory Council 3 rd Metting August 15, 2011 Luciano Coutinho President Emerging countries remain ahead in worldwide growth Annual Growth

BRICs: actual growth and cooperation perspectives International Advisory Council 3 rd Metting August 15, 2011 Luciano Coutinho President Emerging countries remain ahead in worldwide growth Annual Growth

Boosting Sustainable Economic Growth in Mexico. Manuel Sánchez

Manuel Sánchez World Affairs Council of Houston Federal Reserve Bank of Dallas, Houston, Texas, November 1, 2012 Contents 1 Current economic rebound 2 Outlook 3 Inflation and monetary policy 4 Concluding

Manuel Sánchez World Affairs Council of Houston Federal Reserve Bank of Dallas, Houston, Texas, November 1, 2012 Contents 1 Current economic rebound 2 Outlook 3 Inflation and monetary policy 4 Concluding

Capital Flows and Monetary Coordination. Rakesh Mohan Executive Director International Monetary Fund

Capital Flows and Monetary Coordination Rakesh Mohan Executive Director International Monetary Fund June 9, 214 Capital Flows: Historical Overview Pre-WW I Debt flows, mostly long-term Gold standard stable

Capital Flows and Monetary Coordination Rakesh Mohan Executive Director International Monetary Fund June 9, 214 Capital Flows: Historical Overview Pre-WW I Debt flows, mostly long-term Gold standard stable

Presentation. Global Financial Crisis and the Asia-Pacific Economies: Lessons Learnt and Challenges Introduction of the Issues

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 211, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 211, Manila,

Snapshot of SA Economy

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

World Economic Outlook. Recovery Strengthens, Remains Uneven April

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

International Monetary Fund

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee June 8-9, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee June 8-9, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

THE IMPACT OF FINANCIAL TURMOIL ON THE WORLD COTTON AND TEXTILE MARKET

THE IMPACT OF FINANCIAL TURMOIL ON THE WORLD COTTON AND TEXTILE MARKET Presented by Paul Morris Chairman of the Standing Committee INTERNATIONAL COTTON ADVISORY COMMITTEE 1999 China International Cotton

THE IMPACT OF FINANCIAL TURMOIL ON THE WORLD COTTON AND TEXTILE MARKET Presented by Paul Morris Chairman of the Standing Committee INTERNATIONAL COTTON ADVISORY COMMITTEE 1999 China International Cotton

Outlook for the World Economy: Implications for the Caribbean. Saul Lizondo. Western Hemisphere Department International Monetary Fund

Outlook for the World Economy: Implications for the Caribbean Saul Lizondo Associate Director Western Hemisphere Department International Monetary Fund Trinidad id d and Tobago, September, 1 Presentation

Outlook for the World Economy: Implications for the Caribbean Saul Lizondo Associate Director Western Hemisphere Department International Monetary Fund Trinidad id d and Tobago, September, 1 Presentation

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Recent Economic Developments and Monetary Policy in Mexico

Recent Economic Developments and Monetary Policy in Mexico Javier Guzmán Calafell, Deputy Governor, Banco de México* United States-Mexico Chamber of Commerce, Northeast Chapter New York City, 2 June 2017

Recent Economic Developments and Monetary Policy in Mexico Javier Guzmán Calafell, Deputy Governor, Banco de México* United States-Mexico Chamber of Commerce, Northeast Chapter New York City, 2 June 2017

Macroeconomic Impact of the Subprime Crisis

Franco German Council of Economic Advisors Paris, 5 February 2008 Dr. Stefan Kooths DIW Berlin, Macro Analysis and Forecasting Approach Assuming a strictly macroeconomic point of view - Thinking in aggregates

Franco German Council of Economic Advisors Paris, 5 February 2008 Dr. Stefan Kooths DIW Berlin, Macro Analysis and Forecasting Approach Assuming a strictly macroeconomic point of view - Thinking in aggregates

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Short-term momentum: Will it be sustained?

OECD INTERIM ECONOMIC OUTLOOK Projections published:20 Sept Short-term momentum: Will it be sustained? David TURNER Project LINK Meeting, UNCTAD in Geneva Oct 3-5, 2017 www.oecd.org/economy/economicoutlook.htm

OECD INTERIM ECONOMIC OUTLOOK Projections published:20 Sept Short-term momentum: Will it be sustained? David TURNER Project LINK Meeting, UNCTAD in Geneva Oct 3-5, 2017 www.oecd.org/economy/economicoutlook.htm

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

The Financial Crisis in Emerging Markets: Lessons for Global and Not-So-Global Financial Architecture

The Financial Crisis in Emerging Markets: Lessons for Global and Not-So-Global Financial Architecture Conference Preventing the Next Financial Crisis Columbia University, December 11, 2008 Erik Berglof

The Financial Crisis in Emerging Markets: Lessons for Global and Not-So-Global Financial Architecture Conference Preventing the Next Financial Crisis Columbia University, December 11, 2008 Erik Berglof

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

THE GLOBAL FINANCIAL CRISIS LESSONS FOR FINANCIAL SECTOR REFORM

THE GLOBAL FINANCIAL CRISIS LESSONS FOR FINANCIAL SECTOR REFORM Ulrich Volz, German Development Institute (DIE) ICRIER-InWEnt Workshop on Current Developments in the Indian Financial System New Delhi,

THE GLOBAL FINANCIAL CRISIS LESSONS FOR FINANCIAL SECTOR REFORM Ulrich Volz, German Development Institute (DIE) ICRIER-InWEnt Workshop on Current Developments in the Indian Financial System New Delhi,

Business Cycle Index July 2010

Business Cycle Index July 2010 Bureau of Trade and Economic Indices, Ministry of Commerce, Tel. 0 2507 5805, Fax. 0 2507 5806, www.price.moc.go.th Thailand economic still expansion. Medium-run Leading

Business Cycle Index July 2010 Bureau of Trade and Economic Indices, Ministry of Commerce, Tel. 0 2507 5805, Fax. 0 2507 5806, www.price.moc.go.th Thailand economic still expansion. Medium-run Leading

The Hong Kong Economy in Contraction Mode

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com 22 December 08 The Hong Kong Economy in Contraction Mode Hong Kong is in recession and leading economic

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com 22 December 08 The Hong Kong Economy in Contraction Mode Hong Kong is in recession and leading economic

June Todd Hale James Russo Jonathan Banks Jean-Jacques Vandenheede

June 20 Todd Hale James Russo Jonathan Banks JeanJacques Vandenheede Nielsen Global Scorecard Shopping measures appear to be trending upward, driven by gains in China, India, Canada and the U.S., with

June 20 Todd Hale James Russo Jonathan Banks JeanJacques Vandenheede Nielsen Global Scorecard Shopping measures appear to be trending upward, driven by gains in China, India, Canada and the U.S., with

International Conference on The Impacts of and Lessons Learned from the Global Economic Crisis

International Conference on The Impacts of and Lessons Learned from the Global Economic Crisis Jiann-Chyuan Wang 2009.5.15 Outline Ⅰ.Policy measures to respond to the recent financial storm Ⅱ.Policy discussion

International Conference on The Impacts of and Lessons Learned from the Global Economic Crisis Jiann-Chyuan Wang 2009.5.15 Outline Ⅰ.Policy measures to respond to the recent financial storm Ⅱ.Policy discussion

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 12, 2014 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 12, 2014 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

Japan s Economy: Monthly Review

Japan's Economy 18 July 214 (No. of pages: 8) Japanese report: 18 Jul 214 Japan s Economy: Monthly Review China s shadow banking problem requires continued monitoring Economic Intelligence Team Mitsumaru

Japan's Economy 18 July 214 (No. of pages: 8) Japanese report: 18 Jul 214 Japan s Economy: Monthly Review China s shadow banking problem requires continued monitoring Economic Intelligence Team Mitsumaru

Advanced and Emerging Economies Two speed Recovery

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Financial Crisis and Global Recession: At a Turning Point?

Financial Crisis and Global Recession: At a Turning Point? Richard Newfarmer Special Representative to UN and WTO World Bank Geneva June 29,, 2009 Main messages Recession in the US now appears to be bottoming

Financial Crisis and Global Recession: At a Turning Point? Richard Newfarmer Special Representative to UN and WTO World Bank Geneva June 29,, 2009 Main messages Recession in the US now appears to be bottoming

Currency Crises: Theory and Evidence

Currency Crises: Theory and Evidence Lecture 3 IME LIUC 2008 1 The most dramatic form of exchange rate volatility is a currency crisis when an exchange rate depreciates substantially in a short period.

Currency Crises: Theory and Evidence Lecture 3 IME LIUC 2008 1 The most dramatic form of exchange rate volatility is a currency crisis when an exchange rate depreciates substantially in a short period.

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES. Bank of Russia.

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

January 2018 Data Release

January 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the

January 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the

To understand where the U.S. Economy is going, we need to understand where we have been

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Contents. HSBC Group in the world. HSBC in Brazil. New Economic Scenario / Macroeconomic Forecasts

HSBC GLOBAL & LOCAL STRATEGY IN A NEW ECONOMIC SCENARIO Conrado Engel CEO & President of HSBC Bank Brasil 26 March 2010 The British Chamber of Commerce and Industry in Brazil - São Paulo 0 Contents HSBC

HSBC GLOBAL & LOCAL STRATEGY IN A NEW ECONOMIC SCENARIO Conrado Engel CEO & President of HSBC Bank Brasil 26 March 2010 The British Chamber of Commerce and Industry in Brazil - São Paulo 0 Contents HSBC

Who is Eating Whose Lunch?

Who is Eating Whose Lunch? Familiar Stories Source: Jefferies LLC / April 2013. Who is Eating Whose Lunch? Emerging Stories Source: Jefferies LLC / April 2013. And Leading Tech Companies Are Also Vulnerable

Who is Eating Whose Lunch? Familiar Stories Source: Jefferies LLC / April 2013. Who is Eating Whose Lunch? Emerging Stories Source: Jefferies LLC / April 2013. And Leading Tech Companies Are Also Vulnerable

Euler Hermes 2009 H1 financial results. 28 July 2009

Euler Hermes 2009 H1 financial results Contents 1 Economic environment 2 Euler Hermes actions and achievements 3 Q2 2009 consolidated results 4 S1 2009 consolidated results 2 Contents 1 Economic environment

Euler Hermes 2009 H1 financial results Contents 1 Economic environment 2 Euler Hermes actions and achievements 3 Q2 2009 consolidated results 4 S1 2009 consolidated results 2 Contents 1 Economic environment

International Monetary Fund. World Economic Outlook. Jörg Decressin Senior Advisor Research Department, IMF

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

Asset Securitisation in East Asia

East Asian Finance-Road to Robust Markets Asset Securitisation in East Asia Ismail Dalla Hong Kong June 22-23, 06 Views expressed in this presentation do not represent official views of the World Bank

East Asian Finance-Road to Robust Markets Asset Securitisation in East Asia Ismail Dalla Hong Kong June 22-23, 06 Views expressed in this presentation do not represent official views of the World Bank

Economic recovery and employment in the EU. Raymond Torres, Director, ILO Research Department

Economic recovery and employment in the EU Raymond Torres, Director, ILO Research Department Outline of presentation I. Situation in the EU versus Japan and the US II. Role of macroeconomic policies and

Economic recovery and employment in the EU Raymond Torres, Director, ILO Research Department Outline of presentation I. Situation in the EU versus Japan and the US II. Role of macroeconomic policies and

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates Takatoshi Kato Deputy Managing Director International Monetary Fund September 3, 27 1 9 Growth has been

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates Takatoshi Kato Deputy Managing Director International Monetary Fund September 3, 27 1 9 Growth has been

GLOBAL EQUITY MARKET OUTLOOK: FAVOR U.S.; STICK WITH EM

LPL RESEARCH WEEKLY MARKET COMMENTARY KEY TAKEAWAYS U.S. economic and earnings growth continue to stand out globally and support our positive view of U.S. equities. We continue to see upside potential

LPL RESEARCH WEEKLY MARKET COMMENTARY KEY TAKEAWAYS U.S. economic and earnings growth continue to stand out globally and support our positive view of U.S. equities. We continue to see upside potential

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda Technical Appendix Methodology In our analysis, we employ a statistical procedure called Principal Component Analysis

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda Technical Appendix Methodology In our analysis, we employ a statistical procedure called Principal Component Analysis

GLOBAL FINANCIAL CRISIS 2008

GLOBAL FINANCIAL CRISIS 2008 Background Information Credit Crunch Comes Full Cycle Implications on Services Sector / Main Street and Information Services NOVEMBER 21, 2008 Joachim C. Bartels Founder and

GLOBAL FINANCIAL CRISIS 2008 Background Information Credit Crunch Comes Full Cycle Implications on Services Sector / Main Street and Information Services NOVEMBER 21, 2008 Joachim C. Bartels Founder and

Globalization and Economic Crises in the Asia-Pacific: Imperatives on Statistics Management

Globalization and Economic Crises in the Asia-Pacific: Imperatives on Statistics Management Fourth Regional Course/Workshop on Statistical Quality Management UN SIAP 21-25 Sep 2009, Daejeon By George Manzano

Globalization and Economic Crises in the Asia-Pacific: Imperatives on Statistics Management Fourth Regional Course/Workshop on Statistical Quality Management UN SIAP 21-25 Sep 2009, Daejeon By George Manzano

The Outlook for the Housing Industry in Western Australia

The Outlook for the Housing Industry in Western Australia Dr Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Perth March 2012 Europe muddles while China rebalances China is looking to rebalance

The Outlook for the Housing Industry in Western Australia Dr Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Perth March 2012 Europe muddles while China rebalances China is looking to rebalance

Globalization. International Financial (Chap. 8) and Monetary (Chap. 9) Relations

and Monetary (Chap. 9) Relations") Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013 Overview of recent economic developments Framing the policy choices for the current account and growth in 2014

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013 Overview of recent economic developments Framing the policy choices for the current account and growth in 2014

Understanding the Macroeconomic Scenario: Global Demand, Global Supply Chains

Understanding the Macroeconomic Scenario: Global Demand, Global Supply Chains 12 June 2014 Fabio Sdogati, fabio.sdogati@polimi.it Table of Contents 1. Economic Scenario after the Great Recession 2. Structural

Understanding the Macroeconomic Scenario: Global Demand, Global Supply Chains 12 June 2014 Fabio Sdogati, fabio.sdogati@polimi.it Table of Contents 1. Economic Scenario after the Great Recession 2. Structural

FINANCIAL FORECASTS ECONOMIC RESEARCH. January No. 1. What will be the characteristics of euro-zone financial markets in 2016?

ECONOMIC RESEARCH January - No. What will be the characteristics of euro-zone financial markets in? We believe investors will be faced with the following characteristics in euro-zone financial markets

ECONOMIC RESEARCH January - No. What will be the characteristics of euro-zone financial markets in? We believe investors will be faced with the following characteristics in euro-zone financial markets

HOPE NOW. Snapshot Industry Extrapolations and HAMP Metrics

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q2-215 Q3-215 Q4-215 Q1-216 Q2-216 Jun-16 Jul-16 Aug-16 Total Completed Modifications 119,658 97,773 84,798 86,167 1,198 41,872 34,815 36,6

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q2-215 Q3-215 Q4-215 Q1-216 Q2-216 Jun-16 Jul-16 Aug-16 Total Completed Modifications 119,658 97,773 84,798 86,167 1,198 41,872 34,815 36,6

Global Economic Prospects

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Financial Reform. Jeremy Stein, Harvard University. A Conference in Honor of Elias M. Stein May 19, 2011

Financial Crisis and Financial Reform Jeremy Stein, Harvard University Analysis and Applications: A Conference in Honor of Elias M. Stein May 19, 2011 Overview How did we get into this mess? Short-run

Financial Crisis and Financial Reform Jeremy Stein, Harvard University Analysis and Applications: A Conference in Honor of Elias M. Stein May 19, 2011 Overview How did we get into this mess? Short-run

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

MEXICO S ECONOMIC OUTLOOK

Information Analytics Expertise AUGUST 2014 MEXICO S ECONOMIC OUTLOOK Rafael Amiel Director, Latin America -IHS Economics +1 215 789 7405 rafael.amiel@ihs.com Why has growth in emerging markets slowed?

Information Analytics Expertise AUGUST 2014 MEXICO S ECONOMIC OUTLOOK Rafael Amiel Director, Latin America -IHS Economics +1 215 789 7405 rafael.amiel@ihs.com Why has growth in emerging markets slowed?