Vietnam s s Economy in 2009

|

|

|

- Posy Richards

- 5 years ago

- Views:

Transcription

1 AmCham in Ho Chi Minh-City New World Hotel, May Vietnam s s Economy in 2009 Le Dang Doanh Member of the Board, Senior Research Fellow Institute of Development Studies (IDS) ledangdoanh@gmail.com

2 Content Vietnam s s economy in 2008 prior the global crisis. Impacts of global crisis on Vietnam s s economy and the stimulus package of the Vietnamese Government. Reforms. Prospects.

(TCTK 2009)")

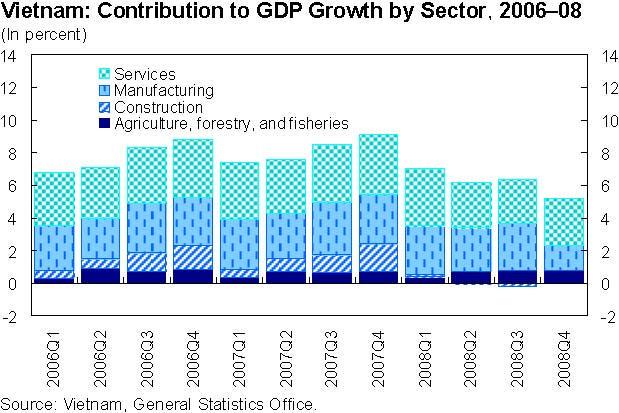

3 Growth in agricultural production in :major stabilizing factor T!c!" t"ng tr##ng GDP (%) (TCTK 2009)

4

5 Three Periods and three different Policies in 2008 The Government prepared the plan for 2008 with high expectation: growth rate percent, over-fulfillment of the Five-Years Plan in three years, surpassing the level of low-income economy in Until March 2008:Credit supply increased by 53 percent. State-owned conglomerates diversified their investment into various fields outside their main profile: financial investment, securities, real estate, hotels etc. High inflation, volatile exchange rate, high trade deficit. From March to October: Draconic but efficient measures tightening monetary policy: high interest rate, high compulsory reserve requirement, compulsory purchasing of SBV-bonds. High burden for SMEs and farmers, huge challenges for commercial banks; disputed temporary stop of rice export. October until now: Reducing interest rate from 14 to 7 %, easing reserve requirement. Stimulus package, easing monetary supply.

6 Credit growth, base rate, oil prices, and inflation % Brent Crude Oil Price (US$ per barrel) - Left-hand Axis 140 Y-o-y Inflation (%) - Right-hand Axis Y-o-y Credit Growth (%) - Right-hand Axis 60% 120 Base Rate (%) - Right-hand Axis 50% Crude Oil Price (US$ a barrel) % 30% 20% Credit Growth & Inflation (%) 20 10% 0 0% Dec-06 Jan-07 Feb-07 Mar-07 Apr-07 May-07 Jun-07 Jul-07 Aug-07 Sep-07 Oct-07 Nov-07 Dec-07 Source: GSO for inflation, SBV for credit growth and base rate, and Global Financial Data for oil prices, from Nguyen Xuan Thanh, (2009) Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08

7 Inflation in regional economies Inflation: Vietnam Inflation in the International context ADB Citigroup China Hongkong India Indonesia S.Korea Source: Malaysia ADB Singapore Update 2008, Taipei Thailand Citigroup Vietnam September, Asia ASEAN 2008 Indonesia Malaysia Singapore Thái Lan Châu Á ASEAN

8

9 Exchange rate fluctuation

10 Nominal and Real Exchange Rate of VND 130 NEER REER Jan-01 Apr-01 Jul-01 Oct-01 Jan-02 Apr-02 Jul-02 Oct-02 Jan-03 Apr-03 Jul-03 Oct-03 Jan-04 Apr-04 Jul-04 Oct-04 Jan-05 Apr-05 Jul-05 Oct-05 Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

11 Trade Balance

12 Reform of state-owned Enterprises (SOEs( SOEs) So far 3800 Small and medium sized SOEs have been equitized,, sharing ~ 17 percent of total SOEs- asset. The remaining 1824 SOEs are bigger like commercial banks or organized in state-owned corporations or conglomerates and are very difficult to equitized.. The equitization process has been slowing down significantly. State-owned conglomerates don t t have a clear legal framework, operate mainly as monopolies or have predominant market share and enjoy good connections with the Government.

13 Export expansion: Share of main VN export destination in total United States China Growth rate EU U.S. Japan ASEAN China

14 Export and import are declining Import export Import and export y.o.y growth rate (3- month moving average) Source: GSO, 2009

15

16 FDI by sector Real estate increased from 11 to 48 %. Manufacture drops from 62% to 25% 26% 11% 1% % Real estate related projects Oil and Gas Manufacture Service % 3% 48% %

17 New Issues on FDI Sharp increase on internationally non-tradable goods like real estate, golf courses with limited employment or qualified workers. Overly high demand on arable land, creating problems with landless farmers, food security. High investment on environmental sensitive industries like cement, steel mills by low spill-over effect. The Vedan- pollution caused angry public reaction. No clear regional and industrial planning: too many oil refineries, still mills in many provinces while FDI in agriculture remain modest. Huge shortage on highly qualified, trained labor forces.

18 Occurred Strikes in Vietnam s_ v ình công N_m

19 Industrial Structure by Ownership in 2005 State Non- State Foreig n Total Hanoi region 29.3% 28.2% 42.5% 100% HCMC region 24.5% 22.8% 52.7% 100% C e n t r a l Vietnam 44.3% 36.4% 19.3% 100% Other regions 54.1% 37.1% 8.9% 100%

20 Vietnamese Government Budget Deficit (% of GDP) Official Budget Balance Revenue and Grants Of Which: Oil Revenue Expenditure

21

22 Budget Constraints In 2009 Vietnam s s budget revenues face serious drops: Revenue from crude oil sale declined by - 45% in the first 4 months. Tax holidays and tax incentives contributed to further loss of budget revenues. High expectation on Government s s expenditures for assistance. The Government asks the National Assembly (NA) to increase the budget deficit from -5% GDP to 8% of GDP in the next five years with a regressive decline to -5%. The NA express concern about efficiency of budget spending and wish to accept a -7% GDP beudget deficit for 2009.

23 Comparison of selected macroeconomic indicators China Malaysia Thailand ViÖt Nam GDP Growth rate 2007 (%) 11,9 6,3 4,9 8,5 GDP Growth rate 2008 (%) 9,1 5,1 3,4 6,2 Stimulus package (billion USD) 586 1,9 8,7 6 Size of Stimulus Package (%GDP) 16,7 1,0 3,5 6,8 State Budget Balance (%GDP) +0,2-5,4-1,4-5 Budget Expenditure (%GDP) 20,4 26,1 19,3 27,6 Balance of Current Account (%GDP) Foreign Reserve billion USD) 10, , , ,7 23 Inflation (CPI, %) 6,2 5,7 7, Lending Interest rate (%) 6,7 6,0 7,2 16,1 Import(% GDP)

24 Corruption Perception Index (CPI) from TI

25 Performance in 2008 GDP-Growth-rate: ~ 6.23 %, target was 8.5% (Agr.:3.8%, Industries &Construction: 6.3%, Services:7.2%) ( SOE: 2.05%, Domestic Private: 8.37%, FDI: 10.78%). GDP:88billion USD. GDP/capita: 1030 USD according to current prices, but according to stable prices it is equivalent to 900 US$ only and Vietnam did not surpass the level of a low-income economy. Inflation: ~23%, CPI in the last three months were negative due to global decline of commodities prices and tight monetary policy. Investment: 43,1% % of GDP, +22.2% compared to 2007; FDI-Commitment: ~ USD 64 billion; Disbursement: ~ USD 11.5 billion. Export of merchandises: ~ 62.9 billion USD ( growth rate: 29.5%); Export of services: USD billion. Import of merchandises: ~ 80.4 billion USD ( growth rate: 28.3%), import of services: USD billion. Trade deficit: ~ 17.5 billion USD or ~ 27.8% of export. VN-index of the Securities Market dropped from 1200 in 2007 to 280. Equitization of SOEs slowing down. Real Estate market stagnated.

26 Global Warming, Pollution and Nontraditional Security Issues Vietnam is extremely vulnerable to global warming and rising sea level. Pollution, environmental damages are serious at urban and rural regions. Air pollution, ground water, solid waste processing need urgent investment and efficient measures. Nontraditional Security issues like human trafficking, drug smuggling, swine (A/H1N1) flu etc. are emerging and Vietnam needs to be better prepared.

27 Targets in 2009 GDP-Growth rate: ~ 6.5% (IMF: 4.8%, WB:5.5%, ADB: 6%, BMI: 2.6%, EIU 0.3% (!). Growth rate is expected to reach ~ 4-5 percent on annual basis. Inflation: < 15 %, could be likely ~8%. Investment: 39% of GDP Export: + 13 %, could be likely -5 or 8% due to price drop and declining export contracts. (IMF:-15.5% on annual basis). Import is expected to decline by %. Unemployment should be a serious social-economic issue. Stimulus Package of the Government implemented.

28

29 Trade balance (export-import) in million USD of agrarian products compared to total trade Cán cân th ng m_i hàng hóa chung Cán cân th ng m_i nông lâm s_n (TCTK 2008)

30

31 Agriculture: Stabilizing Factor in the stormy time Agriculture in Vietnam still shares 21 percent of the GDP, provides 50 percent of total employment, contributing to more than 20.4 percent of total export. Agriculture ensures food security for the whole population and by that way contributes to economic-social stability. Lower commodities prices and efforts of the Government (timely purchasing of rice, construction of silos etc) encourage the farmers. The profit margin for the farmer is better than Agriculture in 2009 is expected to grow at ~ 4 percent, rice export should reach 5 million ton. Coffee, black pepper, seafood generally face price drops but still have access to international market. Agriculture in various regions could serve as a flexible sack to absorb some labor forces and ease the pressure of unemployment from industries and services.

32 Some Improvement in the Second Quarter

33 Encouraging Signs in the first 4 months After severe declines in the first Quarter there are multiple encouraging signs for a gradual, difficult recovery of the economy in April: higher industrial output (5.4% compared to the same period in 2008), increasing retail trade turnover, construction and real estate market warming up, growing Vn-Index etc. FDI-implemented capital reached USD 2.2 billion, a -30% drop to Saving deposit increased 9.88% to the same period of 2008, credit supply increased sharply by 4.86% compared to March 2009, total money supply increased by 11.4 compared with 5.53% in 2008.

34 Exchange Rate of VND versus USD in March

35 Exchange Rate Fluctuation SBV has allowed a widening band from 3 to 5% on exchange rate regime but keep a stable official exchange rate for VND to USD. Commercial banks ask for an additional fee of 1% by lending in USD. Exchange rate at the free market reached VND/USD. There are two opposite opinions: devaluation by 30% could boost the declining export. Other opinion is worry about external debts services, burden for businesses. The low value-added garment, footwear and consumer electronic with small vertical intra-industrial trade doesn t t provide a high benefit from a devaluation. SNV is likely to keep the exchange rate stable within the band.

36 Macroeconomic Indicators The Government may ask the NA for various changes in macroeconomic indicators in the May-Session 2009: GDP growth rate from 6.5% to 5%, export etc. Trade deficit was high but reduced due to rapid decline of import. Balance of current account of international payment remains volatile due to reduced FDI and ODAdisbursement, remittance and declining tourism. Current- account deficit should decline from 13.7% in 2008 to 8% of GDP in 2009.Vietnam should likely sustain a balance for current-account for international payment thanks to FDI, remittance, ODA and tourism.. Inflation should be likely under control due to cautious monetary policy and low world commodities prices.

37 Transparency and Openness Monetary and financial data are hardly accessible, e.g. foreign reserve, international credit of FDI, total saving deposit etc are not available. Inconsistency of data creates obstacle for analysis. Information on land, urban regional planning is secret and hardly available. Economic Anomaly: Despite dramatic downturn of Securities Market and Real Estate, NPL of the commercial banks is < 4 percent only. The health of some small newly established commercial banks is highly questionable as these banks invested heavily on Securities and Real estate Market in 2007 and No official information is available. Merger& Acquisition of some small banks are in the discussion. Data on unemployment is hardly accurate and reliable, there is no unemployment registration system. Unemployment should reach 2 million in 2009.

38 FDI: Still an Attractive Location Foreign investors still remain confident on medium and long term potential of Vietnam s s economy. JBIC- studies confirm Vietnam as a high priority for Japanese investors. Committed FDI in first four months declined -17%, but in April declined by -87%, disbursement declined -32%. An unknown number of FDEs has closed or suspended their operations. Numerous foreign-invested entrepreneurs, mainly small South Korean one, disappear without to pay insurance, salaries, taxes. Delay of implementation of committed FDI, no clear roadmap of progress. Thousand hectares of cleared land remain unused caused angry reaction of the related farmers. Inefficient use of land for golf courses, environmental damages called public awareness.

39

40

41

42

43 High Pressure on domestic SMEs and informal sector 7000 SMEs have been bankrupt, but it could be likely 20 percent of total SMEs. 30% face tremendous difficulties or could be clinically dead.. They face declining demand, shortage of contracts, credit and liquidity constraints. From 1500 handicraft villages with 11 million employees are at least 5 million unemployed, including furniture, silk producers etc. The situation of 2.2 million household businesses is not clear but the press reported from a decline of turnover by 30-40% in the first three months. Most of the informal sector don t t provide insurance for employees.

44 Expectation of SMEs in 2009? Likely to develop well Some growth but down from 2008 Tremendous difficulties but hope to overcome Temporary suspension of business 197 (13%) 259 (17%) 470 (31%) 147 (10%) Likely to go bankrupt 421 (29%)

45 Risk on employment and social impacts Declining demand from international market leaded to reduced production and employment. MOLISA announced that unemployment should reach peoples based on reports of 40/64 provinces workers should return home from abroad. Unemployment could reach 2 million in The social safety system in Vietnam is under development, unemployment insurance shall be in force from January 2010 only. Farmers in Vietnam face multiple risks. The Government of Vietnam is providing preferential credit for unemployed peoples for retraining and seeking employment.

46 Policy responses Subsidized loans: 223,000 billions VND have been disbursed (around $US12 billion): Not clear where the money gone: for roll-over loans? Employment? Tax cut for small and medium enterprises. Who benefits from this support? Implications: Fiscal deficit (8-10% of GDP this year) Limited scope of deficit financing Risks of re-merging inflation Floating government bonds on USD: not successful Trade-off in managing more flexible exchange rate Policy dilemma: where to use more effectively stimulus packages: long-term vs. short-term measures

47 Some other Issues Fuel price increase frequently, higher fuel price to regional fuel prices (China, Singapore). From March electricity price has increased by 8.93 percent. If included the peak hours prices, the de-facto price increase is 32% and is unacceptable for business. Unpredictable changes without consultation with the business communities. Inspection of state-owned conglomerates temporarily suspended.

48 Some Positive Development Social-economic stability could be sustained. Preparations for the next Party Congress intensified and some election syndromes emerged until Vietnam is officially recognized as market economy by Australia and New Zealand. Japan resumed ODA after the PCI-case. Vietnam-Japan agreed on strategic partnership. Vietnam could developed economic cooperation and foreign direct investment to the Middle East. Increasing efforts of the Government to reform administrative regulations: Project 30. The Law on the right to get access to information is under preparation.

49 Strong Expectation on Reform Domestic and foreign invested enterprises expect the Government to implement effective reforms on public administration (taxation, customs, land access, construction, environmental authorization etc.). World Bank Doing Business Ranking of Vietnam is low. Monopolies and SOEs reforms are urgent. So far Vietnam equitized 15 percent of total capital of SOEs. State-owned conglomerates continue to enjoy access to projects, mineral reserves, credits. Banking and Securities Market need to learn lessons from the global crisis and prepare for the post-crisis aera.

50 Prospects Different scenarios: V-shape curve with rapid recovery. Some signs of contending of the economic slow-down are all ready started. U-shape curve: Vietnam s s economic recovery not ahead of the world economy due to high dependence on FDI and export and slow reform. An W-shape development could be not totally excluded. L-shape curve: should be excluded if slow reform, insufficient restructuring of the economy, revitalizing of inflation.

Viet Nam GDP growth by sector Crude oil output Million metric tons 20

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

Viet Nam This economy is weathering the global economic crisis relatively well due largely to swift and strong policy responses. The GDP growth forecast for 29 is revised up from that made in March and

LAO ECONOMIC MONITOR APRIL 2017

LAO ECONOMIC MONITOR APRIL 2017 May-June 2017 1. Recent Economic Developments and Outlook 2. Health Sector Financing in Lao PDR 1. Recent Economic Developments Contents 1. Key findings 2. Growth and inflation

LAO ECONOMIC MONITOR APRIL 2017 May-June 2017 1. Recent Economic Developments and Outlook 2. Health Sector Financing in Lao PDR 1. Recent Economic Developments Contents 1. Key findings 2. Growth and inflation

Global Economic Prospects: Navigating strong currents

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Myanmar Economic Monitor May 2018 Growth Amidst Uncertainty. Hans Anand Beck Lead Economist, Myanmar

Myanmar Economic Monitor May 2018 Growth Amidst Uncertainty Hans Anand Beck Lead Economist, Myanmar May 17, 2018 Key Takeaways The economy performed better in 2017/18 amidst uncertainty. A stronger-than-expected

Myanmar Economic Monitor May 2018 Growth Amidst Uncertainty Hans Anand Beck Lead Economist, Myanmar May 17, 2018 Key Takeaways The economy performed better in 2017/18 amidst uncertainty. A stronger-than-expected

Presentation. Global Financial Crisis and the Asia-Pacific Economies: Lessons Learnt and Challenges Introduction of the Issues

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 211, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 211, Manila,

World Bank Thailand Economic Monitor November Press Launch November 4, 2009

World Bank Thailand Economic Monitor November 2009 Press Launch November 4, 2009 overview The Thai economy is rebounding from a rocky first half of 2009, but the medium-term outlook is uncertain. The Thai

World Bank Thailand Economic Monitor November 2009 Press Launch November 4, 2009 overview The Thai economy is rebounding from a rocky first half of 2009, but the medium-term outlook is uncertain. The Thai

Economic Outlook Economic Intelligence Center 27 th November 2015

Economic Outlook 2016 Economic Intelligence Center 27 th November 2015 Global outlook Domestic outlook 2 In 2016, recovery pace in most regions are expected to pick up except for China Eurozone 2.0 1.5

Economic Outlook 2016 Economic Intelligence Center 27 th November 2015 Global outlook Domestic outlook 2 In 2016, recovery pace in most regions are expected to pick up except for China Eurozone 2.0 1.5

THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) Website:

Website:") THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, 72-74 Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) 3 827 0527 Website: www.tcsc.vn MONTHLY REPORT OCTOBER 2012 Research Department research@tcsc.vn

THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, 72-74 Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) 3 827 0527 Website: www.tcsc.vn MONTHLY REPORT OCTOBER 2012 Research Department research@tcsc.vn

VIETNAM S POLICY RESPONSES TO THE FINANCIAL CRISIS

VIETNAM S POLICY RESPONSES TO THE FINANCIAL CRISIS LE Thi Thuy Van EAI Background Brief No. 447 Date of Publication: 14 April 2009 Executive Summary 1. Vietnam s economy had already entered a period of

VIETNAM S POLICY RESPONSES TO THE FINANCIAL CRISIS LE Thi Thuy Van EAI Background Brief No. 447 Date of Publication: 14 April 2009 Executive Summary 1. Vietnam s economy had already entered a period of

MACRO-ECONOMICS AND MACRO FINANCIAL CRISIS

MACRO-ECONOMICS AND MACRO FINANCIAL CRISIS Dr. Lê Xuân Ngh a 1. The world economy and perspectives. The recovery of the US economy continues to face difficulties. The CPI decreased by 0.1% in June indicating

MACRO-ECONOMICS AND MACRO FINANCIAL CRISIS Dr. Lê Xuân Ngh a 1. The world economy and perspectives. The recovery of the US economy continues to face difficulties. The CPI decreased by 0.1% in June indicating

Sustaining Resilience, Expanding Opportunities for Inclusive Growth

1 Sustaining Resilience, Expanding Opportunities for Inclusive Growth Deputy Governor Diwa C. Guinigundo Bangko Sentral ng Pilipinas Source: Google images 2 PH emerges as growth leader in the ASEAN pack

1 Sustaining Resilience, Expanding Opportunities for Inclusive Growth Deputy Governor Diwa C. Guinigundo Bangko Sentral ng Pilipinas Source: Google images 2 PH emerges as growth leader in the ASEAN pack

Vietnam: Economic Context

Vietnam: Economic Context Parliamentary Network Visit to Vietnam March 5 8, 218 Hanoi, Vietnam Jonathan Dunn IMF Resident Representative International Monetary Fund Outline 2 IMF activities Economic achievements

Vietnam: Economic Context Parliamentary Network Visit to Vietnam March 5 8, 218 Hanoi, Vietnam Jonathan Dunn IMF Resident Representative International Monetary Fund Outline 2 IMF activities Economic achievements

The Outlook for Asian & Australian Economies

The Outlook for Asian & Australian Economies Asian economies maintain stable growth led by domestic demand although growth pace slows down slightly AKI FUKUCHI, YOKO HAGIWARA ECONOMIC RESEARCH OFFICE TOKYO

The Outlook for Asian & Australian Economies Asian economies maintain stable growth led by domestic demand although growth pace slows down slightly AKI FUKUCHI, YOKO HAGIWARA ECONOMIC RESEARCH OFFICE TOKYO

KBank Capital Markets Perspectives 29 February 2016

KBank Capital Markets Perspectives 29 February 2016 Thailand Economic Monitor and BoT Forecast : March 2016 Thailand s economy steadied in February, though domestic demand decelerated slightly from January

KBank Capital Markets Perspectives 29 February 2016 Thailand Economic Monitor and BoT Forecast : March 2016 Thailand s economy steadied in February, though domestic demand decelerated slightly from January

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

L-1 Part 2 Introduction to Indonesia Case Study

L-1 Part 2 Introduction to Indonesia Case Study IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Stephan Danninger This training material

L-1 Part 2 Introduction to Indonesia Case Study IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Stephan Danninger This training material

China Economic Outlook 2013

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

AFC VIETNAM FUND UPDATE

Fund Category Vietnam Public Equities Country Focus Subscriptions Redemptions Benchmark Fund Manager Investment Manager Investment Advisor Fund Base Currency Vietnam Monthly at NAV (five business days

Fund Category Vietnam Public Equities Country Focus Subscriptions Redemptions Benchmark Fund Manager Investment Manager Investment Advisor Fund Base Currency Vietnam Monthly at NAV (five business days

RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO OCTOBER 2003

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

Economic Outlook: Global and India. Ajit Ranade IEEMA T & D Conclave December 12, 2014

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Cambodia. Impacts of Global Financial Crisis

Cambodia Impacts of Global Financial Crisis Cambodia s economy has significant vulnerabilities to the global economic crisis. Cambodia is a small open economy with a dynamism based on a non-diversified

Cambodia Impacts of Global Financial Crisis Cambodia s economy has significant vulnerabilities to the global economic crisis. Cambodia is a small open economy with a dynamism based on a non-diversified

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

INVESTMENT environments IN VIETNAM

VIETNAM The Economic and Cultural Office in Taipei INVESTMENT environments IN VIETNAM Mr. Bui Trong Dinh Assistant to the Head Office / in charge of investment Taipei - October 2010 1 VIETNAM investment

VIETNAM The Economic and Cultural Office in Taipei INVESTMENT environments IN VIETNAM Mr. Bui Trong Dinh Assistant to the Head Office / in charge of investment Taipei - October 2010 1 VIETNAM investment

RIETI Special Seminar. The New Landscape of World Trade with Mega-FTAs and Japan's Strategy. Handout. URATA Shujiro

RIETI Special Seminar The New Landscape of World Trade with Mega-FTAs and Japan's Strategy Handout URATA Shujiro Faculty Fellow, RIETI / Professor of Economics, Graduate School of Asia-Pacific Studies,

RIETI Special Seminar The New Landscape of World Trade with Mega-FTAs and Japan's Strategy Handout URATA Shujiro Faculty Fellow, RIETI / Professor of Economics, Graduate School of Asia-Pacific Studies,

Global Economic Prospects and the Developing Countries William Shaw December 1999

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Part. Situation and Economic Indicators of SMEs in 2012 and 2013

Part 01 Situation and Economic Indicators of SMEs in 2012 and 2013 Chapter 1 + Gross Domestic Product of SMEs 1 Gross Domestic Product of SMEs The overall gross domestic product (GDP) of 2012 expanded

Part 01 Situation and Economic Indicators of SMEs in 2012 and 2013 Chapter 1 + Gross Domestic Product of SMEs 1 Gross Domestic Product of SMEs The overall gross domestic product (GDP) of 2012 expanded

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Vietnam Economy: Prospects, Integration & Footwear Industry. Vo Tri Thanh (CIEM)

") Vietnam Economy: Prospects, Integration & Footwear Industry Vo Tri Thanh (CIEM) Presentation at the Vietnam Footwear Summit Ho Chi Minh City, 15-16 March 2017 12/03/2017 1 Outline of presentation 30 years

Vietnam Economy: Prospects, Integration & Footwear Industry Vo Tri Thanh (CIEM) Presentation at the Vietnam Footwear Summit Ho Chi Minh City, 15-16 March 2017 12/03/2017 1 Outline of presentation 30 years

Mongolia Selected Macroeconomic Indicators December 18, 2013

Mongolia Selected Macroeconomic Indicators December 18, 213 For further information, please contact: SSelenge@imf.org 2 2 27 28 29 21 211 212 213 212 213 Q1 Q2 Q3 Oct. Nov. First 11 months Total US$-value

Mongolia Selected Macroeconomic Indicators December 18, 213 For further information, please contact: SSelenge@imf.org 2 2 27 28 29 21 211 212 213 212 213 Q1 Q2 Q3 Oct. Nov. First 11 months Total US$-value

The Long Journey to Recovery. Russia Economic Report April 2016 Edition No. 35

The Long Journey to Recovery Russia Economic Report April 216 Edition No. 35 1 2 3 The anticipated recovery was delayed and the economy adjusted through a sharp income drop. The government s policy response

The Long Journey to Recovery Russia Economic Report April 216 Edition No. 35 1 2 3 The anticipated recovery was delayed and the economy adjusted through a sharp income drop. The government s policy response

Mongolia Selected Macroeconomic Indicators January 24, 2014

Mongolia Selected Macroeconomic Indicators January 2, 21 For further information, please contact: SSelenge@imf.org 2 2 27 2 29 21 211 212 213 213 Q1 Q2 Q3 Oct. Nov. Dec. Q Total US$-value 1,3 1,97 2,3

Mongolia Selected Macroeconomic Indicators January 2, 21 For further information, please contact: SSelenge@imf.org 2 2 27 2 29 21 211 212 213 213 Q1 Q2 Q3 Oct. Nov. Dec. Q Total US$-value 1,3 1,97 2,3

The Global Economy and Viet Nam: Current Situation and Perspectives

2017/SOM1/EC/006 Agenda Item: 7c The Global Economy and Viet Nam: Current Situation and Perspectives Purpose: Information Submitted by: Central Institute for Economic Management First Economic Committee

2017/SOM1/EC/006 Agenda Item: 7c The Global Economy and Viet Nam: Current Situation and Perspectives Purpose: Information Submitted by: Central Institute for Economic Management First Economic Committee

VIETNAM COUNTRY REPORT

VIETNAM COUNTRY REPORT GIANG TRINH Vice chairman of the Vietnam Bond Market Association Asian Securities Forum Bangkok, November 214 ECONOMY 2 STABILIZATION PRIMES GROWTH Vietnam s economy has been fully

VIETNAM COUNTRY REPORT GIANG TRINH Vice chairman of the Vietnam Bond Market Association Asian Securities Forum Bangkok, November 214 ECONOMY 2 STABILIZATION PRIMES GROWTH Vietnam s economy has been fully

Emerging Global Challenges and implications for Indonesia

Emerging Global Challenges and implications for Indonesia Muhammad Chatib Basri Harvard Kennedy School and University of Indonesia Short term problems: macroeconomic stability 2 The macroeconomic impact

Emerging Global Challenges and implications for Indonesia Muhammad Chatib Basri Harvard Kennedy School and University of Indonesia Short term problems: macroeconomic stability 2 The macroeconomic impact

Mongolia Selected Macroeconomic Indicators September 19, 2013

Mongolia Selected Macroeconomic Indicators September 19, 13 For further information, please contact: SSelenge@imf.org Jan-8 May-8 Sep-8 Jan-9 May-9 Sep-9 Jan-1 May-1 Sep-1 May-11 Sep-11 May-1 Sep-1 May-13

Mongolia Selected Macroeconomic Indicators September 19, 13 For further information, please contact: SSelenge@imf.org Jan-8 May-8 Sep-8 Jan-9 May-9 Sep-9 Jan-1 May-1 Sep-1 May-11 Sep-11 May-1 Sep-1 May-13

B-GUIDE: Market Outlook

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

INDONESIA. The Real Economy

INDONESIA Macroeconomic stability is strengthening in Indonesia. The external environment is likely to be supportive for the economy. This positive trend is reflected in the recent upgrade of Indonesia

INDONESIA Macroeconomic stability is strengthening in Indonesia. The external environment is likely to be supportive for the economy. This positive trend is reflected in the recent upgrade of Indonesia

Asia Bond Monitor March 2015

June 1 asianbondsonline.adb.org Key Developments in Asian Local Currency Markets Consumer price inflation in Malaysia accelerated to.1% year-on-year (y-o-y) in May from 1.8% y-o-y in April, mainly due

June 1 asianbondsonline.adb.org Key Developments in Asian Local Currency Markets Consumer price inflation in Malaysia accelerated to.1% year-on-year (y-o-y) in May from 1.8% y-o-y in April, mainly due

Economic Monthly ASEAN & India

Economic Monthly ASEAN & India AKI FUKUCHI ECONOMIC RESEARCH OFFICE TOKYO YUMA TSUCHIYA ECONOMIC RESEARCH OFFICE SINGAPORE APRIL 8 (ORIGINAL JAPANESE VERSION RELEASED ON APRIL 8) MUFG Bank, Ltd. A member

Economic Monthly ASEAN & India AKI FUKUCHI ECONOMIC RESEARCH OFFICE TOKYO YUMA TSUCHIYA ECONOMIC RESEARCH OFFICE SINGAPORE APRIL 8 (ORIGINAL JAPANESE VERSION RELEASED ON APRIL 8) MUFG Bank, Ltd. A member

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

VIETNAM BRIEF ABOUT THE COUNTRY AND OPPORTUNITIES IN DOING BUSINESS

VIETNAM BRIEF ABOUT THE COUNTRY AND OPPORTUNITIES IN DOING BUSINESS 1 CONTENTS: I. OVERVIEW OF ECONOMY IN VIETNAM II. III. IV. OVERVIEW OF FDI IN VIETNAM PROCEDURES FOR INVESTMENT TIPS FOR DOING BUSINESS

VIETNAM BRIEF ABOUT THE COUNTRY AND OPPORTUNITIES IN DOING BUSINESS 1 CONTENTS: I. OVERVIEW OF ECONOMY IN VIETNAM II. III. IV. OVERVIEW OF FDI IN VIETNAM PROCEDURES FOR INVESTMENT TIPS FOR DOING BUSINESS

From Stability to Prosperity for All

From Stability to Prosperity for All March 2012 PQU Press Presentation Rogier van den Brink, Lead Economist Karl Kendrick Chua, Country Economist Poverty Reduction and Economic Management (PREM) Unit World

From Stability to Prosperity for All March 2012 PQU Press Presentation Rogier van den Brink, Lead Economist Karl Kendrick Chua, Country Economist Poverty Reduction and Economic Management (PREM) Unit World

An Informal Economic Report of the World Bank Vietnam Consultative Group Informal Mid-Year Review

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized VIETNAM : EXPORT PERFORMANCE IN 1999 AND BEYOND An Informal Economic Report of the World

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized VIETNAM : EXPORT PERFORMANCE IN 1999 AND BEYOND An Informal Economic Report of the World

Russian Federation. Recent Economic Developments and Challenges. October 2015 IMF MOSCOW OFFICE

Russian Federation Recent Economic Developments and Challenges IMF MOSCOW OFFICE October 215 1 Outline Shocks affecting Russia s economy Policy Reaction: Monetary and Fiscal Policy Responses Current economic

Russian Federation Recent Economic Developments and Challenges IMF MOSCOW OFFICE October 215 1 Outline Shocks affecting Russia s economy Policy Reaction: Monetary and Fiscal Policy Responses Current economic

Indonesia Economics Update

Indonesia Economics Update THEE Kian Wie and Siwage Dharma Negara Economic Research Centre Indonesian Institute of Sciences (P2E LIPI) Jakarta 24 September 2010 Macroeconomic Developments Growth Balance

Indonesia Economics Update THEE Kian Wie and Siwage Dharma Negara Economic Research Centre Indonesian Institute of Sciences (P2E LIPI) Jakarta 24 September 2010 Macroeconomic Developments Growth Balance

Global/Regional Economic and Financial Outlook. Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June

Global/Regional Economic and Financial Outlook Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June 11-12 2015 2015/SFOM13/002 Session: 1 Global/Regional Economic and Financial

Global/Regional Economic and Financial Outlook Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June 11-12 2015 2015/SFOM13/002 Session: 1 Global/Regional Economic and Financial

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

Introduction to VIETNAM

Introduction to VIETNAM Vietnam is a densely populated, emerging economy that has implemented market-oriented reforms since 1986 and benefited from large foreign direct investment inflows since its accession

Introduction to VIETNAM Vietnam is a densely populated, emerging economy that has implemented market-oriented reforms since 1986 and benefited from large foreign direct investment inflows since its accession

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya August 6, 2015 Outline 1. The Information basis for the MPC meeting 2.

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya August 6, 2015 Outline 1. The Information basis for the MPC meeting 2.

Asia Bond Monitor November 2018

January 9 asianbondsonline.adb.org Key Developments in Asian Local Currency Markets L ast week, the Philippines raised USD. billion from the sale of -year global bonds priced at basis points above benchmark

January 9 asianbondsonline.adb.org Key Developments in Asian Local Currency Markets L ast week, the Philippines raised USD. billion from the sale of -year global bonds priced at basis points above benchmark

PART 1. recent trends and developments

PART 1 recent trends and developments 1 REGIONAL OVERVIEW OF MERCHANDISE TRADE A. A RETURN TO TRADE CONTRACTION The sluggish growth in developed economies and uncertainty linked to the European economic

PART 1 recent trends and developments 1 REGIONAL OVERVIEW OF MERCHANDISE TRADE A. A RETURN TO TRADE CONTRACTION The sluggish growth in developed economies and uncertainty linked to the European economic

Managing Global Shocks: The Case of Indonesia

Managing Global Shocks: The Case of Indonesia Dr. Hartadi A. Sarwono Deputy Governor IIF Asian Regional Economic Forum Singapore, March 5, 2009 Outline 2 1. Crisis highlights 2. Macroconomic Condition

Managing Global Shocks: The Case of Indonesia Dr. Hartadi A. Sarwono Deputy Governor IIF Asian Regional Economic Forum Singapore, March 5, 2009 Outline 2 1. Crisis highlights 2. Macroconomic Condition

THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) Website:

Website:") THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, 72-74 Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) 3 827 0527 Website: www.tcsc.vn MONTHLY REPORT JULY 2012 Research Department research@tcsc.vn

THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, 72-74 Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) 3 827 0527 Website: www.tcsc.vn MONTHLY REPORT JULY 2012 Research Department research@tcsc.vn

Development of Economy and Financial Markets of Kazakhstan

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

AsianBondsOnline WEEKLY DEBT HIGHLIGHTS

AsianBondsOnline WEEKLY 9 January 7 asianbondsonline.adb.org Key Developments in Asian Local Currency Markets Consumer price inflation in Indonesia eased to.% year-on-year (y-o-y) in December from.6% y-o-y

AsianBondsOnline WEEKLY 9 January 7 asianbondsonline.adb.org Key Developments in Asian Local Currency Markets Consumer price inflation in Indonesia eased to.% year-on-year (y-o-y) in December from.6% y-o-y

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms One of the commonalities between most Asian governments is the dedicated commitment they have in using policies and initiatives

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms One of the commonalities between most Asian governments is the dedicated commitment they have in using policies and initiatives

AFC VIETNAM FUND UPDATE

Fund Category Country Focus Subscriptions Redemptions Benchmark Fund Manager Investment Manager Investment Advisor Vietnam Public Equities Vietnam Monthly at NAV (five business days before month end) Monthly

Fund Category Country Focus Subscriptions Redemptions Benchmark Fund Manager Investment Manager Investment Advisor Vietnam Public Equities Vietnam Monthly at NAV (five business days before month end) Monthly

Valentyn Povroznyuk, Radu Mihai Balan, Edilberto L. Segura

September 214 GDP grew by 1.2% yoy in Q2 214. Industrial output growth was equal to 1.4% yoy in June 214. The consolidated budget deficit narrowed to.2% of GDP in January-July 214. Consumer inflation slightly

September 214 GDP grew by 1.2% yoy in Q2 214. Industrial output growth was equal to 1.4% yoy in June 214. The consolidated budget deficit narrowed to.2% of GDP in January-July 214. Consumer inflation slightly

GLOBAL MACROECONOMIC AND CURRENCY ANALYSIS 2015 REVIEW AND 2016 OUTLOOK

A REPORT OF MACROECONOMICS GLOBAL MACROECONOMIC AND CURRENCY ANALYSIS 2015 REVIEW AND 2016 OUTLOOK A FORECAST ON VND/USD WITH REGARD TO FUNDAMENTAL ANALYSIS November 5, 2015 YEN TRAN [E] haiyentran.t@gmail.com

A REPORT OF MACROECONOMICS GLOBAL MACROECONOMIC AND CURRENCY ANALYSIS 2015 REVIEW AND 2016 OUTLOOK A FORECAST ON VND/USD WITH REGARD TO FUNDAMENTAL ANALYSIS November 5, 2015 YEN TRAN [E] haiyentran.t@gmail.com

Macroeconomic Perspectives for Thailand

1 Macroeconomic Perspectives for Thailand Pattama Teanravisitsagool Macroeconomic Strategy and Planning, Director Office of the National Economic and Social Development Board 27 April 2009 WWW.NESDB.GO.TH

1 Macroeconomic Perspectives for Thailand Pattama Teanravisitsagool Macroeconomic Strategy and Planning, Director Office of the National Economic and Social Development Board 27 April 2009 WWW.NESDB.GO.TH

Ukraine: Breaking Through the Perfect Storm

Ukraine: Breaking Through the Perfect Storm 34th Meeting of the Central Bank Governors' Club of Central Asia, Black Sea Region and Balkan Countries 26 Sep 2015, Tbilisi 2 Ukraine went through the perfect

Ukraine: Breaking Through the Perfect Storm 34th Meeting of the Central Bank Governors' Club of Central Asia, Black Sea Region and Balkan Countries 26 Sep 2015, Tbilisi 2 Ukraine went through the perfect

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Asia Bond Monitor June 2018

September 8 asianbondsonline.adb.org Key Developments in Asian Local Currency Markets Japan s industrial production fell.% on a month-on-month (m-o-m) basis but rose.% on a year-on-year (y-o-y) basis in

September 8 asianbondsonline.adb.org Key Developments in Asian Local Currency Markets Japan s industrial production fell.% on a month-on-month (m-o-m) basis but rose.% on a year-on-year (y-o-y) basis in

THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) Website:

Website:") THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, 72-74 Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) 3 827 0527 Website: www.tcsc.vn MONTHLY REPORT AUGUST 2012 Research Department research@tcsc.vn

THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, 72-74 Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) 3 827 0527 Website: www.tcsc.vn MONTHLY REPORT AUGUST 2012 Research Department research@tcsc.vn

Monthly Economic Insight

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Asia Bond Monitor November 2018

7 December 8 Key Developments in Asian Local Currency Markets T he monetary board of the Bangko Sentral ng Pilipinas decided to keep its key policy rates steady during its final meeting for the year on

7 December 8 Key Developments in Asian Local Currency Markets T he monetary board of the Bangko Sentral ng Pilipinas decided to keep its key policy rates steady during its final meeting for the year on

THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) Website:

Website:") THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, 72-74 Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) 3 827 0527 Website: www.tcsc.vn MONTHLY REPORT MARCH 2012 Research Department research@tcsc.vn

THANH CONG SECURITIES COMPANY Floor 3&5, Centec Tower, 72-74 Nguyen Thi Minh Khai, Dis.3, HCMC Phone : + 84 (08) 3 827 0527 Website: www.tcsc.vn MONTHLY REPORT MARCH 2012 Research Department research@tcsc.vn

Trade Balance (LHS) Exports (RHS) Imports (RHS)

Exports (RHS) Imports (RHS)") 14,000 RM Million % change y-o-y 50.0 12,000 40.0 10,000 30.0 8,000 20.0 6,000 10.0 4,000 0.0 2,000 (10.0) 0 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16

14,000 RM Million % change y-o-y 50.0 12,000 40.0 10,000 30.0 8,000 20.0 6,000 10.0 4,000 0.0 2,000 (10.0) 0 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16

MALAYSIA Summary Exports grew by 6% in 2002 A broad based recovery gained momentum in 2002.

MALAYSIA Summary A broad-based economic recovery gained momentum in 2002, despite a more challenging external environment. Macroeconomic fundamentals have continued to strengthen. Financial and corporate

MALAYSIA Summary A broad-based economic recovery gained momentum in 2002, despite a more challenging external environment. Macroeconomic fundamentals have continued to strengthen. Financial and corporate

Key developments and outlook

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

1. Macroeconomic Highlights

1. Macroeconomic Highlights ht Macroeconomic Highlights Resilient growth over the last 2 years, despite the global economic slowdown Banking industry robust with high level of CAR and low NPLN. In 2008

1. Macroeconomic Highlights ht Macroeconomic Highlights Resilient growth over the last 2 years, despite the global economic slowdown Banking industry robust with high level of CAR and low NPLN. In 2008

Reviewing Macro-economic Developments and Understanding Macro-Economic Policy

MINISTRY OF FINANCE GOVERNMENT OF INDIA Reviewing Macro-economic Developments and Understanding Macro-Economic Policy Module 5 Contemporary Themes in India s Economic Development and the Economic Survey

MINISTRY OF FINANCE GOVERNMENT OF INDIA Reviewing Macro-economic Developments and Understanding Macro-Economic Policy Module 5 Contemporary Themes in India s Economic Development and the Economic Survey

Outlook for Central Vietnam, including Tax Incentives

Outlook for Central Vietnam, including Tax Incentives Presentation by Nguyen Quang Phuc, Director, Tax and Advisory Services ECV Business Forum, 24 November 2017 Outlook for Central Vietnam, including

Outlook for Central Vietnam, including Tax Incentives Presentation by Nguyen Quang Phuc, Director, Tax and Advisory Services ECV Business Forum, 24 November 2017 Outlook for Central Vietnam, including

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

The Korean Economy: Resilience amid Turbulence

The Korean Economy: Resilience amid Turbulence Dr. Il SaKong Special Economic Advisor Adviser to the President Republic of Korea November 17, 17, 2008 November 17, 2008 1. Recent Macroeconomic Developments

The Korean Economy: Resilience amid Turbulence Dr. Il SaKong Special Economic Advisor Adviser to the President Republic of Korea November 17, 17, 2008 November 17, 2008 1. Recent Macroeconomic Developments

Institue of Strategic and International Studies (ISIS) Malaysia.

Malaysia.") Institue of Strategic and International Studies (ISIS) Malaysia www.isis.org.my MALAYSIAN RESPONSES TO THE GLOBAL ECONOMIC AND FINANCIAL CRISIS Mahani Zainal Abidin ISIS Malaysia 6 February 2009 Institue

Institue of Strategic and International Studies (ISIS) Malaysia www.isis.org.my MALAYSIAN RESPONSES TO THE GLOBAL ECONOMIC AND FINANCIAL CRISIS Mahani Zainal Abidin ISIS Malaysia 6 February 2009 Institue

INDONESIA ECONOMIC QUARTERLY CLOSING THE GAP. Frederico Gil Sander Lead Economist October 3, 2017

INDONESIA ECONOMIC QUARTERLY CLOSING THE GAP Frederico Gil Sander Lead Economist October 3, 2017 How is the economy doing? What to expect in 2018? Closing the gap Growth steady amid mostly favorable conditions

INDONESIA ECONOMIC QUARTERLY CLOSING THE GAP Frederico Gil Sander Lead Economist October 3, 2017 How is the economy doing? What to expect in 2018? Closing the gap Growth steady amid mostly favorable conditions

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

What questions would you like answered?

What questions would you like answered? Define the following: Globalisation an expansion of world trade leading to increased international interdependence GDP The value of goods and services produced in

What questions would you like answered? Define the following: Globalisation an expansion of world trade leading to increased international interdependence GDP The value of goods and services produced in

APPENDIX: A SNAPSHOT OF INDONESIAN ECONOMIC INDICATORS

APPENDIX: A SNAPSHOT OF INDONESIAN ECONOMIC INDICATORS Appendix Figure : Quarterly and annual GDP growth (percent growth) Appendix Figure : Contributions to GDP expenditures (quarter-on-quarter, seasonally

APPENDIX: A SNAPSHOT OF INDONESIAN ECONOMIC INDICATORS Appendix Figure : Quarterly and annual GDP growth (percent growth) Appendix Figure : Contributions to GDP expenditures (quarter-on-quarter, seasonally

Vietnam Economy - IMF Article IV Consultation Report Summary (Summer 2017)

") Vietnam Economy - IMF Article IV Consultation Report Summary (Summer 2017) Inwa Advisers Pte Ltd. Incorporated in the Republic of Singapore. Co Reg No. 198601745D. Summary of Main Points (I)* POSITIVES

Vietnam Economy - IMF Article IV Consultation Report Summary (Summer 2017) Inwa Advisers Pte Ltd. Incorporated in the Republic of Singapore. Co Reg No. 198601745D. Summary of Main Points (I)* POSITIVES

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

AFC VIETNAM FUND UPDATE

Fund Category Vietnam Public Equities Country Focus Subscriptions Redemptions Benchmark Fund Manager Investment Manager Investment Advisor Fund Base Currency Vietnam Monthly at NAV (five business days

Fund Category Vietnam Public Equities Country Focus Subscriptions Redemptions Benchmark Fund Manager Investment Manager Investment Advisor Fund Base Currency Vietnam Monthly at NAV (five business days

FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged -

REVISED to reflect the 2 nd QE for the Oct-Dec Qtr of 2017 FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged - March 8, 2018 Copyright

REVISED to reflect the 2 nd QE for the Oct-Dec Qtr of 2017 FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged - March 8, 2018 Copyright

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia Hernando Vargas Banco de la República Colombia March, 2009 Contents I. The state of the Colombian economy

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia Hernando Vargas Banco de la República Colombia March, 2009 Contents I. The state of the Colombian economy

Introduction to the UK Economy

Introduction to the UK Economy What are the key objectives of macroeconomic policy? Price Stability (CPI Inflation of 2%) Growth of Real GDP (National Output) Falling Unemployment / Raising Employment

Introduction to the UK Economy What are the key objectives of macroeconomic policy? Price Stability (CPI Inflation of 2%) Growth of Real GDP (National Output) Falling Unemployment / Raising Employment

ASIAN ECONOMIES. Economics, interest rates and currencies chart pack

ASIAN ECONOMIES Economics, interest rates and currencies chart pack Amy Auster Senior Economist Melbourne 2 May 25 E-mail: austera@anz.com Internet: http://www.anz.com/go/economics 1 Major revisions to

ASIAN ECONOMIES Economics, interest rates and currencies chart pack Amy Auster Senior Economist Melbourne 2 May 25 E-mail: austera@anz.com Internet: http://www.anz.com/go/economics 1 Major revisions to

Advanced and Emerging Economies Two speed Recovery

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Regional Economic Outlook

Regional Economic Outlook Caucasus and Central Asia Azim Sadikov International Monetary Fund Resident Representative November 6, 2013 Outline Global Outlook CCA: Recent Developments, Outlook, and Risks

Regional Economic Outlook Caucasus and Central Asia Azim Sadikov International Monetary Fund Resident Representative November 6, 2013 Outline Global Outlook CCA: Recent Developments, Outlook, and Risks

Macroeconomic policies conducive to job-rich and inclusive growth

Macroeconomic policies conducive to job-rich and inclusive growth Enrique Blanco Armas Senior Economist World Bank April 14, 2011 Launch of Labour and Social Trends Report for Indonesia Inter-Continental

Macroeconomic policies conducive to job-rich and inclusive growth Enrique Blanco Armas Senior Economist World Bank April 14, 2011 Launch of Labour and Social Trends Report for Indonesia Inter-Continental

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Japan s New Trade Policy in Asia-Pacific

Japan s New Trade Policy in Asia-Pacific August 22, 2013 Shujiro URATA Waseda University 1 Contents I. Japan s Economic Situation II. High Economic Growth and Regional Economic Integration in Asia-Pacific

Japan s New Trade Policy in Asia-Pacific August 22, 2013 Shujiro URATA Waseda University 1 Contents I. Japan s Economic Situation II. High Economic Growth and Regional Economic Integration in Asia-Pacific

Inflation Remains Tepid in November at 0.2% as Transport Cost Trending Downward

19 December 2018 ECONOMIC REVIEW November 2018 Consumer Price Index Inflation Remains Tepid in November at 0.2% as Transport Cost Trending Downward Headline inflation back to near 4-year low. Consumer

19 December 2018 ECONOMIC REVIEW November 2018 Consumer Price Index Inflation Remains Tepid in November at 0.2% as Transport Cost Trending Downward Headline inflation back to near 4-year low. Consumer

The Outlook for Asian & Australian Economies

The Outlook for Asian & Australian Economies Stable growth to continue led by domestic demand, impact of US-China trade conflict will bear watching AKI FUKUCHI, YOKO HAGIWARA, SHOHEI TAKASE ECONOMIC RESEARCH

The Outlook for Asian & Australian Economies Stable growth to continue led by domestic demand, impact of US-China trade conflict will bear watching AKI FUKUCHI, YOKO HAGIWARA, SHOHEI TAKASE ECONOMIC RESEARCH

6-8 September 2011, Manila, Philippines. Jointly organized by UNESCAP and BANGKO SENTRAL NG PILIPINAS. Country Experiences 3: Net Energy Exporters

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

Japan s Economy: Monthly Review

Japan's Economy 18 July 214 (No. of pages: 8) Japanese report: 18 Jul 214 Japan s Economy: Monthly Review China s shadow banking problem requires continued monitoring Economic Intelligence Team Mitsumaru

Japan's Economy 18 July 214 (No. of pages: 8) Japanese report: 18 Jul 214 Japan s Economy: Monthly Review China s shadow banking problem requires continued monitoring Economic Intelligence Team Mitsumaru

Viet Nam. Economic performance

Viet Nam Rising foreign direct investment helped to accelerate economic growth to 6. in 1. Inflation abated, and robust external accounts enabled the rebuilding of foreign reserves. Growth is forecast

Viet Nam Rising foreign direct investment helped to accelerate economic growth to 6. in 1. Inflation abated, and robust external accounts enabled the rebuilding of foreign reserves. Growth is forecast

Economic Monthly ASEAN & India

Economic Monthly ASEAN & India AKI FUKUCHI ECONOMIC RESEARCH OFFICE TOKYO YUMA TSUCHIYA ECONOMIC RESEARCH OFFICE SINGAPORE 8 FEBRUARY 218 (ORIGINAL JAPANESE VERSION RELEASED ON 1 FEBRUARY 218) The Bank

Economic Monthly ASEAN & India AKI FUKUCHI ECONOMIC RESEARCH OFFICE TOKYO YUMA TSUCHIYA ECONOMIC RESEARCH OFFICE SINGAPORE 8 FEBRUARY 218 (ORIGINAL JAPANESE VERSION RELEASED ON 1 FEBRUARY 218) The Bank

The Outlook for Asian & Australian Economies

The Outlook for Asian & Australian Economies Stable growth will continue backed by solid domestic demand and an expansion of export to advanced countries 16 MARCH 18 (ORIGINAL JAPANESE VERSION RELEASED

The Outlook for Asian & Australian Economies Stable growth will continue backed by solid domestic demand and an expansion of export to advanced countries 16 MARCH 18 (ORIGINAL JAPANESE VERSION RELEASED