Regional Economic Outlook

|

|

|

- Alfred Hopkins

- 5 years ago

- Views:

Transcription

1 Regional Economic Outlook Caucasus and Central Asia Azim Sadikov International Monetary Fund Resident Representative November 6, 2013

2 Outline Global Outlook CCA: Recent Developments, Outlook, and Risks Vision: Becoming Vibrant Emerging Markets Georgia: The Economy in 2013 and the Outlook

3 The global recovery has weakened Global Manufacturing PMI (Monthly Data, Index; > 50 = expansion; SA) Merchandise Exports (Annualized Monthly Percent Change, 3mma) Latest: Aug World Advanced Emerging Advanced Emerging Latest: Aug Source: IMF, Global Data Source. Global Outlook

World U.S.")

2.9 1.6-0.4 2.0 1.5 7.6 2.3 5.")

3.6 2.6 1.0 1.2 3.0 7.")

4 The WEO forecast has been revised down, mainly on account of emerging economies WEO Real GDP Growth Projections (percent change from a year earlier) World U.S. Euro Area Japan Russia China CEE CCA 2013 (Oct. 2013) (Apr. 2013) (Oct. 2013) (Apr. 2013) Source: IMF, World Economic Outlook. Global Outlook 8

5 EM growth has declined for both cyclical and structural reasons 1.0 Decomposing the Slowdown 1/ (percentage points) Potential Cyclical Change in real growth Brazil South Africa China Russia India Source: IMF, World Economic Outlook. 1/ Cyclical component of growth calculated as the difference between real and potential growth. Potential growth estimated using multivariate filter (see Box 1.2 of the October 2013 WEO for details). 5

300 250 Food Metals Gold (right scale) 500 400 175 150 95% confidence interval 86% confidence interval 68% confidence interval Futures")

6 Metals and food prices are falling but oil prices have recently risen Global commodity price developments 1 (Index; 2005 = 100) Brent crude oil price prospects 2 (U.S. dollars per barrel) Food Metals Gold (right scale) % confidence interval 86% confidence interval 68% confidence interval Futures Dec-08 Dec-10 Dec-12 Dec Sources: IMF, Primary Commodity Price System; and IMF staff calculations. 1 Food index derived from average price of corn, wheat, rice, and soybeans. 2 Derived from prices of futures options on Sep. 12, Global Outlook

7 Financial conditions have tightened 10 Bond Yields (Percent, Aug 2, 2012 Oct 22, 2013) Chairman Bernanke's testimony to Congress Announcement by Fed not to taper 3 Aug-12 Nov-12 Feb-13 May-13 Aug-13 KAZ (Dev Bank, 20YR) ARM (7YR) TUR (10YR) GEO (10YR) Emerging markets Sources: IMF, World Economic Outlook; and Bloomberg LP. Global Outlook

8 Risks to global growth remain on the downside Global financial conditions tighten by more than expected Continued stop-gap measures and uncertainty over fiscal policy in the US Financial fragmentation in the euro area weighs on investment Insufficient fiscal consolidation and structural reforms in Japan Lower potential growth in emerging markets Lower commodity prices 8 8

9 Policy priorities Euro area United States Emerging markets Repair financial system Adopt a banking union Reduce budget deficit over the medium term Calibrate the timing of exit from unconventional monetary policy Improve resilience to shocks Accelerate structural reforms Let exchange rate adjust to capital flows Global Outlook 9

10 Caucasus and Central Asia Kazakhstan Georgia Armenia Azerbaijan Uzbekistan Turkmenistan Tajikistan Kyrgyz Republic Oil and gas exporters Oil and gas importers

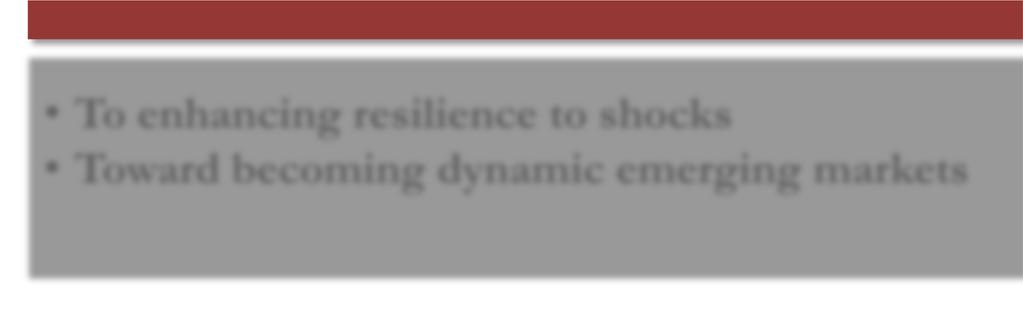

11 Overview Outlook Risks Policies Robust growth over the near term A lower-than-anticipated growth in emerging economies Tightening of external financing conditions To enhancing resilience to shocks Toward becoming dynamic emerging markets 11

12 The economic outlook remains favorable despite sluggish growth in trading partners Real GDP, 2014 (Annual growth, percent) CCA oil and gas exporters CCA oil and gas importers -6 Russia Central and Eastern Europe TKM UZB KGZ TJK AZE KAZ GEO ARM Sources: IMF, World Economic Outlook; and IMF staff calculations and projections. 12

13 Inflation stays largely within a comfort range Headline CPI Inflation (Annual percent change) 25 Oil and Gas Exporters 25 Oil and Gas Importers KGZ UZB TKM AZE KAZ TJK ARM CEE GEO -5 Jul-10 Jul-11 Jul-12 Jul-13-5 Jul-10 Jul-11 Jul-12 Jul-13 Sources: National authorities; and IMF staff calculations.

14 Risks to the near-term outlook are tilted to the downside Risk Slower than expected growth in emerging markets Channel Russia/China Commodity prices and volumes Tighter global financial conditions Financial flows Funding costs CCA Impact Exports FDI Remittances Oil and gas Aluminum Cotton Non-ferrous metals Bank credit lines FDI Rollover needs

15 Oil and gas exporters: weakening fiscal balances 10 5 Oil and Gas Exporters (Percent of GDP) Oil and Gas Exporters (Fiscal breakeven oil prices, U.S. dollars per barrel) Overall fiscal balance Non-oil fiscal balance (percent of non-oil GDP) AZE KAZ TKM Sources: National authorities; and IMF staff estimates.

16 Oil and gas importers: Save for the rainy day General Government Deficit (percent of GDP) CCA Oil Importers Central and Eastern Europe Georgia General Government Debt (percent of GDP) CCA Oil Importers Central and Eastern Europe Georgia Sources: National authorities; and IMF staff estimates. 16

17 Weakening external positions underscore the need for adjustment Oil and Gas Exporters (percent of GDP) Gross external debt, left scale Current account balance Reserves, months of imports Oil and Gas Importers (percent of GDP) Central and Eastern Europe (percent of GDP) * Current account balance for CCA oil and gas exporters; current account deficit for CCA oil and gas importers and CEE. Sources: National authorities; and IMF staff estimates.

18 Continue to bolster financial sector soundness Non-performing Loans 1/ (On a 90-day basis; percent of total loans) Capital Adequacy Ratio (Percent of risk-weighted assets) (latest) (latest) ARM AZE GEO KAZ KGZ UKR TUR CEE 2/ 0 ARM AZE GEO KAZ KGZ UKR TUR CEE 2/ Sources: National authorities; and IMF staff estimates. 1/ 90-day basis. 2/ Includes BIH, BGR, HRV, HUN, LVA, LTU, MKD, POL, ROU, and TUR. 18

19 Summary of near-term priorities Oil and Gas Exporters Delink spending decisions from short-term fluctuations in oil prices, in particular save in good times Preserve oil wealth for future generation and ensure that budgets are sustainable Improve spending quality to ensure that all public investment are productive Oil and Gas Importers Create fiscal space by reining in hardto-reverse expenditures and by broadening tax bases Use part of the space to better target safety nets, and to invest in health, education, and infrastructure Increase exchange rate flexibility to lower the risk of output and price fluctuations Some countries need to restore the health of the banking system 19

20 Vision for the CCA: Become vibrant emerging markets Growth

21 Obstacles and risks to the CCA vision

22 Accelerate reforms to become dynamic emerging markets Strengthen fiscal frameworks Improve the effectiveness of monetary policy Foster financial development Transition to emerging markets Enhance structural reforms Promote trade integration

23 CCA: Key Takeaways Growth to remain reasonably rapid but risks are tilted to the downside. Oil exporters need to preserve oil wealth for future generation. Oil importers should increase fiscal buffers and introduce more exchange rate flexibility. All need ambitious reforms to become dynamic emerging markets.

24 Georgia

Georgia Azerbaijan Armenia Russia Turkey 8.0 6.0 4.0 2.0 0.")

25 Georgia s neighborhood: Growth expected to pick up in Gross Domestic Product (percent change) Georgia Azerbaijan Armenia Russia Turkey Source: IMF, World Economic Outlook.

26 Activity has been broadly flat since July Monthly GDP, Billions of GEL Actual GDP Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Seasonally adjusted GDP Sources: GEOSTAT and IMF staff estimates.

27 Investment-led slowdown, with consumption flat and external sector performing strongly Contribution to the Annual Nominal GDP Growth Jan-Jun, 2013 over Jan-Jun, 2012 (percent change) Total 2.0 Discrepancy -0.5 Imports 2.5 Exports 4.4 Investment -4.5 Public consumption -0.9 Private consumption Sources: GEOSTAT, IMF staff estimates

28 Investment- and government-dependent sectors dragging growth down Sector Contribution to the Annual Nominal GDP Growth Jan-Jun, 2013 over Jan-Jun, 2012 (percent change) Total 2.0 Industry 0.5 Agriculture Real estate & rent Trade Education and Health Other -0.1 Public administration -0.9 Construction Sources: GEOSTAT, IMF staff estimates

29 Shortfalls in government spending, especially capital Total Spending (percent of GDP) Capital Expenditure (percent of GDP) Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Sources: NBG, IMF staff estimates;

30 more than offset somewhat weaker revenue, resulting in fiscal surplus so far Total Revenue (percent of GDP) Fiscal Balance (percent of GDP) Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec -3.0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Sources: NBG, IMF staff estimates;

31 Need to continue prudent fiscal policy to safeguard debt sustainability Fiscal Deficit (percent of GDP) Government Debt (percent of GDP) Sources: MOF and Fund Staff estimates;

32 Deflationary pressures due to the strength of lari, the slowdown, and administered price cuts Consumer Price Inflation and the Policy Rate Policy rate (Rhs). Core Inflation Headline May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12 Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13 Sources: GEOSTAT and IMF staff estimates;

33 Market rates started to come down, reacting to weak credit demand and monetary loosening GEL loan rates 14.0 USD loan rates 15.0 GEL deposit rates g Policy Rate USD deposit rates Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12 Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12 Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Sources: NBG and IMF staff estimates.

34 Yet, corporate loans stagnant; household loans continue to grow slowly 9 8 Bank Loans (in billions of GEL) 7 6 Households Corporations Loans to Individuals 1 0 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Sources: GEOSTAT and IMF staff estimates;

35 Exports and Tourism performing strongly Number of Tourists thousands, (rhs) Exports, 3-month moving average, annual growth Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 0 Sources: GEOSTAT and IMF staff estimates. 35

36 partly supported by a re-opening of the Russian market Share of exports to Russia in total exports (in percent). Share of tourists from Russia in total tourists (in percent) / / Sources: National authorities; and IMF staff estimates.

37 1.0 Exports growth and imports contraction reducing the trade deficit Georgia: Trade Balance (billions of USD) Imports Exports Balance Q1 2011Q2 2011Q3 2011Q4 2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2 2013Q3 Sources: GEOSTAT and IMF staff estimates.

38 Current account deficit narrowing: structural or temporary? CA deficit (USD bln) % of GDP Sources: NBG, IMF staff estimates;

39 With external inflows proving resilient 1.4 Electronic Transfers (remittances) Jan-Sep 2012 Jan-Sep Billions of USD Jan-Jun 2012 FDI Jan-Jun Sources: NBG, IMF staff estimates;

40 the NBG used the opportunity to accumulate reserves 3.2 Foreign assets Foreign assets (excluding IMF ) 1.6 Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Sources: NBG and IMF staff estimates.

41 Georgia: Key Takeaways Near Term 1. Slowdown in 2013 due to: weak investor confidence reflecting political and policy uncertainty shortfalls in government spending 2. Growth should pick up in 2014 but requires restoring investor confidence overcoming spending shortfalls while avoiding waste 3. Strong performance of the external sector likely to continue, supported by a gradual re-opening of the Russian market progress toward deeper integration with the EU (I)

42 Georgia: Medium Term Policy Challenges 1. Generate sustained job-creating growth pursue structural reforms to improve competitiveness invest in education and job training improve business environment 2. Reduce external sector vulnerabilities (I) lock-in some of the recent gains in the current account allow greater exchange rate flexibility remain vigilant and manage carefully short-term capital flows 3. Build fiscal buffers adopt a prudent 2014 budget use fiscal policy to contain domestic demand

43 Thank You! To access the full report online or to provide comments, please visit: and click the link for Regional Economic Outlook (I)

Caucasus and Central Asia Regional Economic Outlook October 2011

Regional Economic Outlook October 211 Oil and gas exporters Oil and gas importers Kazakhstan Georgia Uzbekistan Kyrgyz Republic Armenia Azerbaijan Turkmenistan Tajikistan Overview Global outlook (CCA)

Regional Economic Outlook October 211 Oil and gas exporters Oil and gas importers Kazakhstan Georgia Uzbekistan Kyrgyz Republic Armenia Azerbaijan Turkmenistan Tajikistan Overview Global outlook (CCA)

Caucasus and Central Asia Regional Economic Outlook

Juha Kähkönen International Monetary Fund November 212 Overview Global outlook (CCA) outlook and risks CCA macroeconomic policies CCA structural challenges 2 The global recovery has weakened 6 Global Manufacturing

Juha Kähkönen International Monetary Fund November 212 Overview Global outlook (CCA) outlook and risks CCA macroeconomic policies CCA structural challenges 2 The global recovery has weakened 6 Global Manufacturing

Regional Economic Outlook. May 2015

Regional Economic Outlook Caucasus and Central Asia May 215 Outline Global Environment CCA Outlook, Risks, and Policies 2 Global growth remains moderate and uneven World U.S. Euro Area Emerging markets

Regional Economic Outlook Caucasus and Central Asia May 215 Outline Global Environment CCA Outlook, Risks, and Policies 2 Global growth remains moderate and uneven World U.S. Euro Area Emerging markets

Regional Economic Outlook. November 2014

Regional Economic Outlook Caucasus and Central Asia November 214 Outline Global Outlook CCA Outlook, Risks, and Policies 2 An uneven global recovery continues Real GDP Growth Projections (Percent change

Regional Economic Outlook Caucasus and Central Asia November 214 Outline Global Outlook CCA Outlook, Risks, and Policies 2 An uneven global recovery continues Real GDP Growth Projections (Percent change

Caucasus and Central Asia Regional Economic Outlook. November, 2017

1 Caucasus and Central Asia Regional Economic Outlook November, 217 2 Roadmap Outlook, Opportunities, and Challenges Maintaining Macroeconomic Stability Securing Higher and More Inclusive Growth Key Takeaways

1 Caucasus and Central Asia Regional Economic Outlook November, 217 2 Roadmap Outlook, Opportunities, and Challenges Maintaining Macroeconomic Stability Securing Higher and More Inclusive Growth Key Takeaways

Russian Federation. Recent Economic Developments and Challenges. October 2015 IMF MOSCOW OFFICE

Russian Federation Recent Economic Developments and Challenges IMF MOSCOW OFFICE October 215 1 Outline Shocks affecting Russia s economy Policy Reaction: Monetary and Fiscal Policy Responses Current economic

Russian Federation Recent Economic Developments and Challenges IMF MOSCOW OFFICE October 215 1 Outline Shocks affecting Russia s economy Policy Reaction: Monetary and Fiscal Policy Responses Current economic

World Economic Outlook. Recovery Strengthens, Remains Uneven April

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

Central, Eastern, and Southeastern Europe: The Past and Future of Convergence

Central, Eastern, and Southeastern Europe: The Past and Future of Convergence LSE SU Emerging Markets Forum London, March 1, 218 Bas B. Bakker Senior Regional Resident Representative for Central, Eastern

Central, Eastern, and Southeastern Europe: The Past and Future of Convergence LSE SU Emerging Markets Forum London, March 1, 218 Bas B. Bakker Senior Regional Resident Representative for Central, Eastern

Prospects for the Region

Prospects for the Region OECD South Caucasus and Ukraine Initiative Workshop on Financial Market Development Warsaw, November 17, 29 Mark Allen Senior IMF Resident Representative for Central and Eastern

Prospects for the Region OECD South Caucasus and Ukraine Initiative Workshop on Financial Market Development Warsaw, November 17, 29 Mark Allen Senior IMF Resident Representative for Central and Eastern

SEPTEMBER Overview

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Recovery at risk? Central and Eastern Europe remains vulnerable to external funding threats.

Central, Eastern and Southeastern Europe (CESEE) Recovery at risk? Central and Eastern Europe remains vulnerable to external funding threats. May 5, 214 James Roaf Senior Resident Representative IMF Regional

Central, Eastern and Southeastern Europe (CESEE) Recovery at risk? Central and Eastern Europe remains vulnerable to external funding threats. May 5, 214 James Roaf Senior Resident Representative IMF Regional

The Long Journey to Recovery. Russia Economic Report April 2016 Edition No. 35

The Long Journey to Recovery Russia Economic Report April 216 Edition No. 35 1 2 3 The anticipated recovery was delayed and the economy adjusted through a sharp income drop. The government s policy response

The Long Journey to Recovery Russia Economic Report April 216 Edition No. 35 1 2 3 The anticipated recovery was delayed and the economy adjusted through a sharp income drop. The government s policy response

Global Economic Prospects: Navigating strong currents

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Middle East and North Africa Regional Economic Outlook

Regional Economic Outlook Morocco Algeria Tunisia Libya Lebanon Egypt Syria Iraq Iran Jordan Saudi Kuwait Arabia Bahrain Afghanistan Pakistan Mauritania Sudan Djibouti Qatar Yemen Oman United Arab Emirates

Regional Economic Outlook Morocco Algeria Tunisia Libya Lebanon Egypt Syria Iraq Iran Jordan Saudi Kuwait Arabia Bahrain Afghanistan Pakistan Mauritania Sudan Djibouti Qatar Yemen Oman United Arab Emirates

UPDATE ON GLOBAL PROSPECTS AND POLICY CHALLENGES

G R O U P O F T W E N T Y UPDATE ON GLOBAL PROSPECTS AND POLICY CHALLENGES G-20 Leaders Summit September 5 6, 2013 St. Petersburg Prepared by Staff of the I N T E R N A T I O N A L M O N E T A R Y F U

G R O U P O F T W E N T Y UPDATE ON GLOBAL PROSPECTS AND POLICY CHALLENGES G-20 Leaders Summit September 5 6, 2013 St. Petersburg Prepared by Staff of the I N T E R N A T I O N A L M O N E T A R Y F U

БОЛЬШЕ, ЧЕМ НЕФТЬ. ПУТЬ КАЗАХСТАНА к росту благосостояния через диверсификацию

БОЛЬШЕ, ЧЕМ НЕФТЬ ПУТЬ КАЗАХСТАНА к росту благосостояния через диверсификацию What this Report is About: Diversification and Development Resource dependence is not a curse Shared Prosperity Kazakhstan

БОЛЬШЕ, ЧЕМ НЕФТЬ ПУТЬ КАЗАХСТАНА к росту благосостояния через диверсификацию What this Report is About: Diversification and Development Resource dependence is not a curse Shared Prosperity Kazakhstan

WORLD ECONOMIC OUTLOOK October 2017

WORLD ECONOMIC OUTLOOK October 2017 Andreas Bauer Sr Resident Representative @imf_delhi World Economic Outlook The big picture Global activity picked up further in 2017H1 the outlook is now for higher

WORLD ECONOMIC OUTLOOK October 2017 Andreas Bauer Sr Resident Representative @imf_delhi World Economic Outlook The big picture Global activity picked up further in 2017H1 the outlook is now for higher

Recovery at risk? - CEE external vulnerability and Poland Article IV preliminary conclusions

Central, Eastern and Southeastern Europe (CESEE) Recovery at risk? - CEE external vulnerability and Poland Article IV preliminary conclusions CASE, Warsaw - May 27, 214 James Roaf Senior Resident Representative

Central, Eastern and Southeastern Europe (CESEE) Recovery at risk? - CEE external vulnerability and Poland Article IV preliminary conclusions CASE, Warsaw - May 27, 214 James Roaf Senior Resident Representative

U.S. Monetary Policy and Emerging Markets Challenges

U.S. Monetary Policy and Emerging Markets Challenges Jose Viñals Financial Counselor and Director, IMF CEMLA, October, 213 Recovery of the global economy continues 6. GDP Growth Projections (In percent)

U.S. Monetary Policy and Emerging Markets Challenges Jose Viñals Financial Counselor and Director, IMF CEMLA, October, 213 Recovery of the global economy continues 6. GDP Growth Projections (In percent)

Recent developments. Note: The author of this section is Yoki Okawa. Research assistance was provided by Ishita Dugar. 1

Growth in the Europe and Central Asia region is anticipated to ease to 3.2 percent in 2018, down from 4.0 percent in 2017, as one-off supporting factors wane in some of the region s largest economies.

Growth in the Europe and Central Asia region is anticipated to ease to 3.2 percent in 2018, down from 4.0 percent in 2017, as one-off supporting factors wane in some of the region s largest economies.

MIND THE CREDIT GAP. Spring 2015 Regional Economic Issues Report on Central, Eastern and Southeastern Europe (CESEE) recovery. repair.

recovery. repair.") Spring 215 Regional Economic Issues Report on Central, Eastern and Southeastern Europe (CESEE) repair recovery MIND THE CREDIT GAP downturn expansion May, 215 Growth Divergence in 214 Quarterly GDP Growth,

Spring 215 Regional Economic Issues Report on Central, Eastern and Southeastern Europe (CESEE) repair recovery MIND THE CREDIT GAP downturn expansion May, 215 Growth Divergence in 214 Quarterly GDP Growth,

Asian Development Outlook 2016: Asia s Potential Growth

Asian Development Outlook 2016: Asia s Potential Growth Juzhong Zhuang Deputy Chief Economist Asian Development Bank Presentation at The views expressed in this document are those of the author and do

Asian Development Outlook 2016: Asia s Potential Growth Juzhong Zhuang Deputy Chief Economist Asian Development Bank Presentation at The views expressed in this document are those of the author and do

Poland s Economic Prospects

Poland s Economic Prospects Unicredit Conference Warsaw, June 8, 11 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe Recovery is driven by domestic demand Contributions to Real

Poland s Economic Prospects Unicredit Conference Warsaw, June 8, 11 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe Recovery is driven by domestic demand Contributions to Real

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty 2016 Article IV Consultation Report on Indonesia John G. Nelmes IMF Senior Resident Representative for Indonesia Academic

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty 2016 Article IV Consultation Report on Indonesia John G. Nelmes IMF Senior Resident Representative for Indonesia Academic

World Economic Outlook Is the Tide Rising?

World Economic Outlook Is the Tide Rising? January 214 1 Global activity has strengthened. Further improvements expected. WEO Update in a nutshell Advanced economy growth has picked up Robust private demand

World Economic Outlook Is the Tide Rising? January 214 1 Global activity has strengthened. Further improvements expected. WEO Update in a nutshell Advanced economy growth has picked up Robust private demand

Regional Economic Issues in CESEE

Regional Economic Issues in CESEE JVI Lecture, Vienna, February 8, 2017 Bas B. Bakker Senior Regional Resident Representative for Central and Eastern Europe Outlook for CESEE 2 Within CESEE dichotomy:

Regional Economic Issues in CESEE JVI Lecture, Vienna, February 8, 2017 Bas B. Bakker Senior Regional Resident Representative for Central and Eastern Europe Outlook for CESEE 2 Within CESEE dichotomy:

Recent Economic Developments and Monetary Policy in Mexico

Recent Economic Developments and Monetary Policy in Mexico Javier Guzmán Calafell, Deputy Governor, Banco de México* United States-Mexico Chamber of Commerce, Northeast Chapter New York City, 2 June 2017

Recent Economic Developments and Monetary Policy in Mexico Javier Guzmán Calafell, Deputy Governor, Banco de México* United States-Mexico Chamber of Commerce, Northeast Chapter New York City, 2 June 2017

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Global Economic Prospects. South Asia. June 2014 Andrew Burns

Global Economic Prospects South Asia June 214 Andrew Burns Main Messages 214 Global forecast has been downgraded, mainly reflecting one-off factors Financing conditions have eased temporarily, but are

Global Economic Prospects South Asia June 214 Andrew Burns Main Messages 214 Global forecast has been downgraded, mainly reflecting one-off factors Financing conditions have eased temporarily, but are

Snapshot of SA Economy

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

Jörg Decressin Deputy Director

World Economic Outlook October 13 Jörg Decressin Deputy Director Research Department, IMF 1 Outline Prospects for Advanced Economies Recent Developments and Implications for Emerging Economies Medium-term

World Economic Outlook October 13 Jörg Decressin Deputy Director Research Department, IMF 1 Outline Prospects for Advanced Economies Recent Developments and Implications for Emerging Economies Medium-term

Middle East and North Africa Regional Economic Outlook. November 12, 2013

Middle East and North Africa Regional Economic Outlook November 12, 213 Outline Global Outlook MENAP: Recent Developments, Outlook, and Risks Oil Exporters Oil Importers Key Takeaways 2 Global Outlook

Middle East and North Africa Regional Economic Outlook November 12, 213 Outline Global Outlook MENAP: Recent Developments, Outlook, and Risks Oil Exporters Oil Importers Key Takeaways 2 Global Outlook

ECONOMIC MONITOR GEORGIA Issue 8 [updated] June 2018

![ECONOMIC MONITOR GEORGIA Issue 8 [updated] June 2018](/thumbs/85/92879534.jpg "ECONOMIC MONITOR GEORGIA Issue 8 [updated] June 2018") ECONOMIC MONITOR GEORGIA Issue 8 [updated] June 218 Overview High economic growth of 5.% in 217 and 5.5% in Jan-Apr 218 Demand side: balanced growth based on consumption, investment and net exports Positive

ECONOMIC MONITOR GEORGIA Issue 8 [updated] June 218 Overview High economic growth of 5.% in 217 and 5.5% in Jan-Apr 218 Demand side: balanced growth based on consumption, investment and net exports Positive

Outlook for the Mexican Economy Alejandro Díaz de León Carrillo, Governor, Banco de México. April, 2018

Alejandro Díaz de León Carrillo, Governor, Banco de México April, Outline 1 External Conditions Current Outlook.1. Monetary Policy and Inflation Determinants in Mexico Evolution of Economic Activity Recent

Alejandro Díaz de León Carrillo, Governor, Banco de México April, Outline 1 External Conditions Current Outlook.1. Monetary Policy and Inflation Determinants in Mexico Evolution of Economic Activity Recent

The Future of Mexican Monetary Policy

The Future of Mexican Monetary Policy Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Mexico Summit Mexico City, 2 March 2017 */ The views expressed herein are strictly personal.

The Future of Mexican Monetary Policy Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Mexico Summit Mexico City, 2 March 2017 */ The views expressed herein are strictly personal.

How Do the Challenges Facing Emerging Europe Compare?

How Do the Challenges Facing Emerging Europe Compare? 12 th CEI Summit Economic Forum Mark Allen Senior IMF Resident Representative for Central and Eastern Europe First Shock: collapse in trade 6 4 World

How Do the Challenges Facing Emerging Europe Compare? 12 th CEI Summit Economic Forum Mark Allen Senior IMF Resident Representative for Central and Eastern Europe First Shock: collapse in trade 6 4 World

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

The impact of global market volatility on the EBRD region. CSE and OCE September 02, 2015

The impact of global market volatility on the EBRD region CSE and OCE September 02, 2015 KEY RECENT DEVELOPMENTS IN CHINA AND COMMODITY MARKETS Emerging markets growth has been decelerating since 2009

The impact of global market volatility on the EBRD region CSE and OCE September 02, 2015 KEY RECENT DEVELOPMENTS IN CHINA AND COMMODITY MARKETS Emerging markets growth has been decelerating since 2009

Central and Eastern Europe: Global spillovers and external vulnerabilities

Central and Eastern Europe: Central and Eastern Europe: Global spillovers and external vulnerabilities ICEG Annual Conference Brussels, May 28 Christoph Rosenberg International Monetary Fund Overview The

Central and Eastern Europe: Central and Eastern Europe: Global spillovers and external vulnerabilities ICEG Annual Conference Brussels, May 28 Christoph Rosenberg International Monetary Fund Overview The

Quarterly Report. April June 2015

April June August 12, 1 1 Outline 1 2 Monetary Policy External Conditions 3 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks April-June 2 Monetary Policy Conduction in

April June August 12, 1 1 Outline 1 2 Monetary Policy External Conditions 3 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks April-June 2 Monetary Policy Conduction in

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Global Outlook and Policy Challenges. Olivier Blanchard Economic Counsellor Research Department

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Monetary Policy Outlook for Mexico

Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar Washington, DC, 8 October 2016 Outline 1 2 3 4 5 Monetary Policy in Mexico Evolution of the Mexican Economy Inflation

Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar Washington, DC, 8 October 2016 Outline 1 2 3 4 5 Monetary Policy in Mexico Evolution of the Mexican Economy Inflation

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Developing Asia s Short-Run Economic Outlook and Main Risks

Developing Asia s Short-Run Economic Outlook and Main Risks Dr. Donghyun Park, Asian Development Bank Workshop on Bond Market Development in Emerging East Asia Raffles Hotel Le Royal Phnom Penh, Cambodia,

Developing Asia s Short-Run Economic Outlook and Main Risks Dr. Donghyun Park, Asian Development Bank Workshop on Bond Market Development in Emerging East Asia Raffles Hotel Le Royal Phnom Penh, Cambodia,

HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES

Key Points HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES Global growth has moderated, and it is expected to slow from 3 percent in 18 to.9 percent in. International trade and manufacturing

Key Points HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES Global growth has moderated, and it is expected to slow from 3 percent in 18 to.9 percent in. International trade and manufacturing

Monetary Policy under Fed Normalization and Other Challenges

Javier Guzmán Calafell, Deputy Governor, Banco de México* Santander Latin America Day London, June 28 th, 2018 */ The opinions and views expressed in this document are the sole responsibility of the author

Javier Guzmán Calafell, Deputy Governor, Banco de México* Santander Latin America Day London, June 28 th, 2018 */ The opinions and views expressed in this document are the sole responsibility of the author

US$m mn

Jamaica and the Global Financial Crisis Outline Pre-Stand By Jamaica Jamaica Debt Exchange pre-condition to the IMF-SBA Post-Stand By Jamaica Key Issues 2 3 PRE-STAND BY JAMAICA Persistent national savings

Jamaica and the Global Financial Crisis Outline Pre-Stand By Jamaica Jamaica Debt Exchange pre-condition to the IMF-SBA Post-Stand By Jamaica Key Issues 2 3 PRE-STAND BY JAMAICA Persistent national savings

CBRT Policy Mix. Devrim Yavuz Central Bank of the Republic of Turkey. April Jakarta

CBRT Policy Mix Devrim Yavuz Central Bank of the Republic of Turkey April 2018 Jakarta Outline Global Financial Crises: The lessons taken, the challenges faced and the need for policy mix How the trade-offs

CBRT Policy Mix Devrim Yavuz Central Bank of the Republic of Turkey April 2018 Jakarta Outline Global Financial Crises: The lessons taken, the challenges faced and the need for policy mix How the trade-offs

Global Outlook. October 22, M. Marc Stocker DEC-Development Prospects Group

Global Outlook October 22, 214 M. Marc Stocker DEC-Development Prospects Group mstocker1@worldbank.org 1 About Growth Forecasts Public release of growth forecasts in the Global Economic Prospects in June

Global Outlook October 22, 214 M. Marc Stocker DEC-Development Prospects Group mstocker1@worldbank.org 1 About Growth Forecasts Public release of growth forecasts in the Global Economic Prospects in June

Global Economic Prospects: Update Global Recovery in Transition

Global Economic Prospects: Update Global Recovery in Transition April 2015 M. Ayhan Kose 1 Global Prospects: Three Questions 1. How have global economic conditions changed since December? Broadly as expected;

Global Economic Prospects: Update Global Recovery in Transition April 2015 M. Ayhan Kose 1 Global Prospects: Three Questions 1. How have global economic conditions changed since December? Broadly as expected;

GLOBAL OUTLOOK ECONOMIC WATCH. July 2017

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

Mexico s Macroeconomic Outlook and Monetary Policy

Mexico s Macroeconomic Outlook and Monetary Policy Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Washington, DC, 13 October 2017 */ The opinions and views expressed in this document

Mexico s Macroeconomic Outlook and Monetary Policy Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Washington, DC, 13 October 2017 */ The opinions and views expressed in this document

MonitorING Turkey ING BANK A.Ş. Further fiscal support in the Medium Term Plan. Emerging Markets 4 October 2017

q ING BANK A.Ş. ECONOMIC RESEARCH GROUP MonitorING Turkey October 17 Emerging Markets October 17 USD/TRY MonitorING Turkey Further fiscal support in the Medium Term Plan In 17, accelerated spending and

q ING BANK A.Ş. ECONOMIC RESEARCH GROUP MonitorING Turkey October 17 Emerging Markets October 17 USD/TRY MonitorING Turkey Further fiscal support in the Medium Term Plan In 17, accelerated spending and

Seminar Series on Regional Economic Integration

Seminar Series on Regional Economic Integration IMF Outreach Presentation on the IMF 214 Spillover Report Sweta Saxena Senior Economist IMF Research Department 26 September 214 9: 11: Manila time ADB Headquarters,

Seminar Series on Regional Economic Integration IMF Outreach Presentation on the IMF 214 Spillover Report Sweta Saxena Senior Economist IMF Research Department 26 September 214 9: 11: Manila time ADB Headquarters,

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya August 6, 2015 Outline 1. The Information basis for the MPC meeting 2.

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya August 6, 2015 Outline 1. The Information basis for the MPC meeting 2.

How to Get Back on the Fast Track?

REGIONAL ECONOMIC ISSUES REPORT ON CENTRAL, EASTERN AND SOUTHEASTERN EUROPE How to Get Back on the Fast Track? MAY, 216 EUROPEAN DEPARTMENT Map of Central, Eastern, and South-Eastern Europe Baltics CEE

REGIONAL ECONOMIC ISSUES REPORT ON CENTRAL, EASTERN AND SOUTHEASTERN EUROPE How to Get Back on the Fast Track? MAY, 216 EUROPEAN DEPARTMENT Map of Central, Eastern, and South-Eastern Europe Baltics CEE

Inflation projection of Narodowy Bank Polski based on the NECMOD model

Economic Institute Inflation projection of Narodowy Bank Polski based on the NECMOD model Warsaw / 9 March Inflation projection of the NBP based on the NECMOD model Outline: Introduction Changes between

Economic Institute Inflation projection of Narodowy Bank Polski based on the NECMOD model Warsaw / 9 March Inflation projection of the NBP based on the NECMOD model Outline: Introduction Changes between

О КЛЮЧЕВОЙ СТАВКЕ RUSSIAN ECONOMIC OUTLOOK AND CHALLENGES TO MONETARY POLICY. December Bank of Russia Presentation for Investors

О КЛЮЧЕВОЙ СТАВКЕ RUSSIAN ECONOMIC OUTLOOK AND CHALLENGES TO MONETARY POLICY Bank of Russia Presentation for Investors December 16 USD per barrel RUB / USD 2 Oil Eхporters Production-cut Agreements Support

О КЛЮЧЕВОЙ СТАВКЕ RUSSIAN ECONOMIC OUTLOOK AND CHALLENGES TO MONETARY POLICY Bank of Russia Presentation for Investors December 16 USD per barrel RUB / USD 2 Oil Eхporters Production-cut Agreements Support

MONETARY POLICY COMMITTEE STATEMENT FOR THIRD QUARTER Governor s Presentation to the Media. 16 th November, 2016

1 MONETARY POLICY COMMITTEE STATEMENT FOR THIRD QUARTER 2016 Governor s Presentation to the Media 16 th November, 2016 INTRODUCTION 2 This presentation is structured as follows: 1. Decision of the Monetary

1 MONETARY POLICY COMMITTEE STATEMENT FOR THIRD QUARTER 2016 Governor s Presentation to the Media 16 th November, 2016 INTRODUCTION 2 This presentation is structured as follows: 1. Decision of the Monetary

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Presentation. Global Financial Crisis and the Asia-Pacific Economies: Lessons Learnt and Challenges Introduction of the Issues

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 211, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 211, Manila,

ECONOMIC OUTLOOK. September, 2017 MINISTRY OF ECONOMY AND SUSTAINABLE DEVELOPMENT

ECONOMIC OUTLOOK September, 2017 MINISTRY OF ECONOMY AND SUSTAINABLE DEVELOPMENT CONTENTS GDP growth... 3 Potential Level of Economic Growth and GDP Gap... 3 Macroeconomic Environment in the Region...

ECONOMIC OUTLOOK September, 2017 MINISTRY OF ECONOMY AND SUSTAINABLE DEVELOPMENT CONTENTS GDP growth... 3 Potential Level of Economic Growth and GDP Gap... 3 Macroeconomic Environment in the Region...

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES

16 QUARTERLY INVESTMENT STRATEGY APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers Index EMERGING ECONOMIES Purchasing Managers Index US Eurozone Japan Brazil Russia India China Industrial

16 QUARTERLY INVESTMENT STRATEGY APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers Index EMERGING ECONOMIES Purchasing Managers Index US Eurozone Japan Brazil Russia India China Industrial

Emerging Markets Weekly Economic Briefing

21 Emerging Markets Emerging Markets Weekly Economic Briefing Recession looms for some emerging economies Several major emerging economies struggling with domestically-induced problems are now in, or flirting

21 Emerging Markets Emerging Markets Weekly Economic Briefing Recession looms for some emerging economies Several major emerging economies struggling with domestically-induced problems are now in, or flirting

Sovereign Credit Outlook. Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 2018

Sovereign Credit Outlook Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 218 Agenda Global Perspective Regional Overview Sovereign Ratings and Recent Actions Colombia

Sovereign Credit Outlook Richard Francis Director, Latin America Sovereigns Corficolombiana Conference December 5, 218 Agenda Global Perspective Regional Overview Sovereign Ratings and Recent Actions Colombia

Reflections on the Global Economic Outlook

Reflections on the Global Economic Outlook A presentation to the ACI-ICA World Congress October 2018 Mahmoud Mohieldin Senior Vice President World Bank Group @wbg2030 worldbank.org/sdgs Global Megatrends

Reflections on the Global Economic Outlook A presentation to the ACI-ICA World Congress October 2018 Mahmoud Mohieldin Senior Vice President World Bank Group @wbg2030 worldbank.org/sdgs Global Megatrends

Chapter 1 International economy

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

China Economic Outlook 2013

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

Asia and the Pacific: Economic Outlook and Drivers

2018/FDM1/004 Session 2.1 Asia and the Pacific: Economic Outlook and Drivers Purpose: Information Submitted by: International Monetary Fund Finance and Central Bank Deputies Meeting Port Moresby, Papua

2018/FDM1/004 Session 2.1 Asia and the Pacific: Economic Outlook and Drivers Purpose: Information Submitted by: International Monetary Fund Finance and Central Bank Deputies Meeting Port Moresby, Papua

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing Global scenarios Slower growth in emerging markets is a key risk to our central forecast for the global economy. While more positive signs have recently appeared

Emerging Markets Weekly Economic Briefing Global scenarios Slower growth in emerging markets is a key risk to our central forecast for the global economy. While more positive signs have recently appeared

Global Economic Prospects

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO)

") Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

2015 Market Review & Outlook. January 29, 2015

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES. Bank of Russia.

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

Macro Research Economic outlook

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

Ministry of Finance of Georgia. Georgia The Outlook. January 2018

Ministry of Finance of Georgia Georgia The Outlook January 2018 Axes of Georgia s Long-Term Growth Strategy The Government of Georgia s long-term strategy seeks sustained and inclusive growth that is based

Ministry of Finance of Georgia Georgia The Outlook January 2018 Axes of Georgia s Long-Term Growth Strategy The Government of Georgia s long-term strategy seeks sustained and inclusive growth that is based

Key developments and outlook

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

Japan Chart Book. 5 February 2014

Japan Chart Book 5 February Japan: Economic Forecast Dashboard Forecast highlights Real GDP growth forecast at. in and. in 5 Slower consumption in -5 but offset by improved exports and investment Gradual

Japan Chart Book 5 February Japan: Economic Forecast Dashboard Forecast highlights Real GDP growth forecast at. in and. in 5 Slower consumption in -5 but offset by improved exports and investment Gradual

National Monetary Policy Forum. Chris Loewald, Head: Policy Development and Research 10 April 2016 Pretoria

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

The External Environment for Developing Countries

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries March 2008 The World Bank Development Economics Prospects Group

d Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized The External Environment for Developing Countries March 2008 The World Bank Development Economics Prospects Group

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

INDONESIA ECONOMIC QUARTERLY CLOSING THE GAP. Frederico Gil Sander Lead Economist October 3, 2017

INDONESIA ECONOMIC QUARTERLY CLOSING THE GAP Frederico Gil Sander Lead Economist October 3, 2017 How is the economy doing? What to expect in 2018? Closing the gap Growth steady amid mostly favorable conditions

INDONESIA ECONOMIC QUARTERLY CLOSING THE GAP Frederico Gil Sander Lead Economist October 3, 2017 How is the economy doing? What to expect in 2018? Closing the gap Growth steady amid mostly favorable conditions

The World Economic & Financial System: Risks & Prospects

The World Economic & Financial System: Risks & Prospects Dr. Jacob A. Frenkel Chairman & CEO Group of Thirty (G30).Bank Indonesia 7th Annual International Seminar Global Financial Tsunami: What Can We

The World Economic & Financial System: Risks & Prospects Dr. Jacob A. Frenkel Chairman & CEO Group of Thirty (G30).Bank Indonesia 7th Annual International Seminar Global Financial Tsunami: What Can We

Myanmar Economic Monitor May 2018 Growth Amidst Uncertainty. Hans Anand Beck Lead Economist, Myanmar

Myanmar Economic Monitor May 2018 Growth Amidst Uncertainty Hans Anand Beck Lead Economist, Myanmar May 17, 2018 Key Takeaways The economy performed better in 2017/18 amidst uncertainty. A stronger-than-expected

Myanmar Economic Monitor May 2018 Growth Amidst Uncertainty Hans Anand Beck Lead Economist, Myanmar May 17, 2018 Key Takeaways The economy performed better in 2017/18 amidst uncertainty. A stronger-than-expected

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

International Monetary Fund. World Economic Outlook. Jörg Decressin Senior Advisor Research Department, IMF

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

Indonesia Economic Quarterly: October 2012 Maintaining resilience

Indonesia Economic Quarterly: October 1 Maintaining resilience Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank October 15, 1 Paramadina Public Policy Institute www.worldbank.org/id

Indonesia Economic Quarterly: October 1 Maintaining resilience Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank October 15, 1 Paramadina Public Policy Institute www.worldbank.org/id

Recovery and Challenges in Eastern Europe

Recovery and Challenges in Eastern Europe OECD - 7th annual meeting of Senior Budget Officials from Central, Eastern and South-Eastern European countries (CESEE) Zagreb, Croatia, 3 June - 1 July 211 Franziska

Recovery and Challenges in Eastern Europe OECD - 7th annual meeting of Senior Budget Officials from Central, Eastern and South-Eastern European countries (CESEE) Zagreb, Croatia, 3 June - 1 July 211 Franziska

Mexico: Dealing with international financial uncertainty. Manuel Sánchez

Manuel Sánchez United States Mexico Chamber of Commerce, Chicago, IL, August 6, 2015 Contents 1 Moderate economic growth 2 Waiting for the liftoff 3 Taming inflation 2 Since 2014, Mexico s economic recovery

Manuel Sánchez United States Mexico Chamber of Commerce, Chicago, IL, August 6, 2015 Contents 1 Moderate economic growth 2 Waiting for the liftoff 3 Taming inflation 2 Since 2014, Mexico s economic recovery

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Inflation Report. July September 2012

July September 1 November 7, 1 1 Outline 1 External Conditions Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks External Conditions The growth rate

July September 1 November 7, 1 1 Outline 1 External Conditions Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks External Conditions The growth rate

Prospects and Challenges for the Global Economy and the MENA Region

Prospects and Challenges for the Global Economy and the MENA Region Ministry of Finance Cairo October 25, 2011 Andreas Bauer Division i i Chief, t International Monetary Fund Key points: The global outlook

Prospects and Challenges for the Global Economy and the MENA Region Ministry of Finance Cairo October 25, 2011 Andreas Bauer Division i i Chief, t International Monetary Fund Key points: The global outlook

The real change in private inventories added 0.22 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

Inflation Report. April June 2013

April June 2013 August 7, 2013 1 Outline 1 External Conditions 2 Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks 2 External Conditions Global Environment

April June 2013 August 7, 2013 1 Outline 1 External Conditions 2 Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks 2 External Conditions Global Environment