Navigating the Road to BHPH Success Six Step Approach!

|

|

|

- Winfred O’Connor’

- 5 years ago

- Views:

Transcription

1 Navigating the Road to BHPH Success Six Step Approach! Presented by: Kenneth Shilson, President Subprime Analytics NABD May 25, 2016 Visit Booth #

2

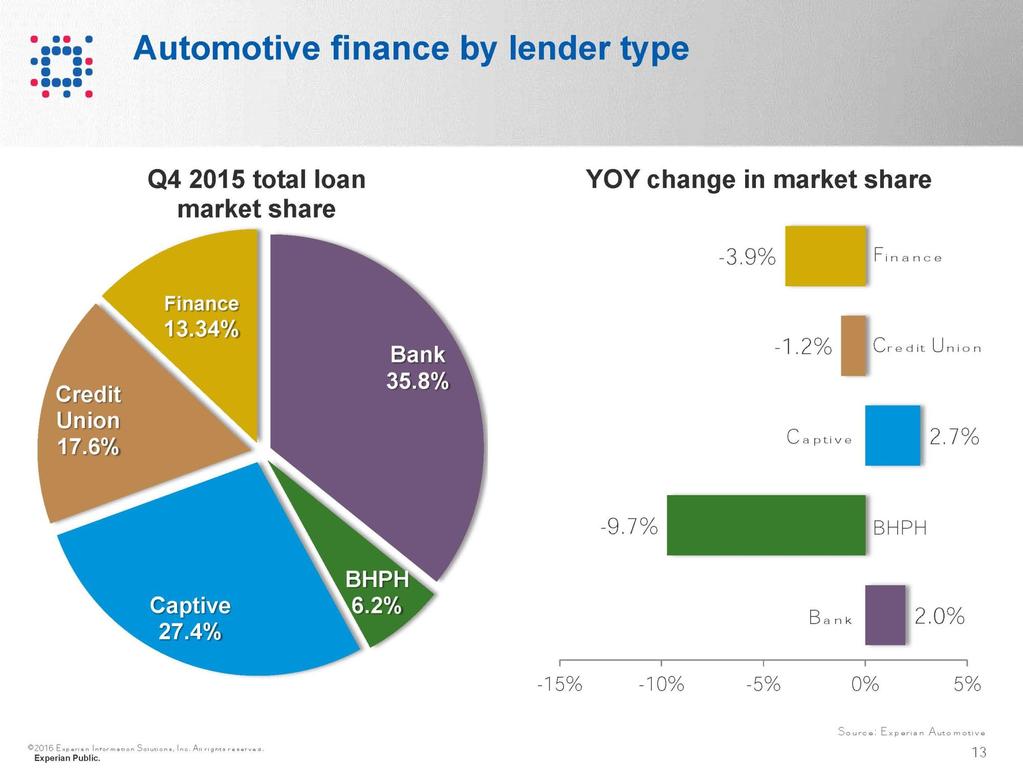

3 Source: Experian Automotive

4 Step 1 BHPH Must Regain Lost Market Share

5 Understanding The Auto Finance Marketplace! Source: Experian Automotive and Subprime Analytics

6

7

8

9

10

11 Step 2 Your Business Model Dictates Your Success!

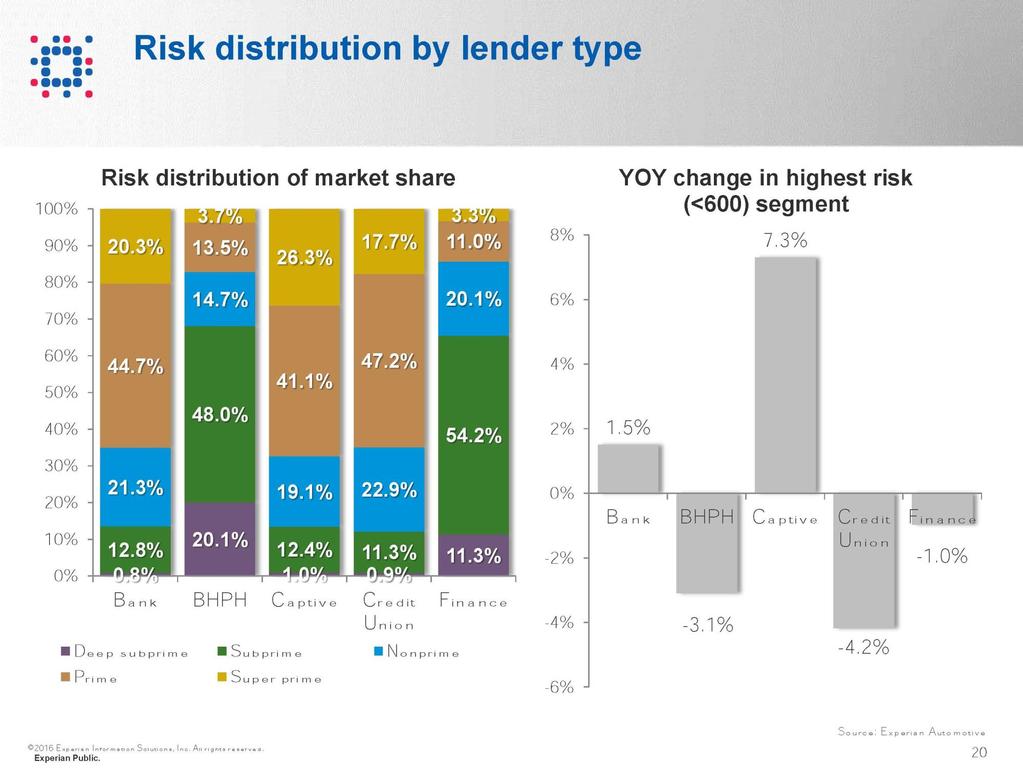

12

13 Average Amount Financed Average Amount Financed $11,500 $11,000 $10,689 $10,765 $11,090 $10,500 $10,084 $10,000 $9,667 $9,500 $9,000 $8, Average Amount Financed Source: Subprime Analytics Booth #115

14

15 Average Payment Amount $90 Average Weekly Payment Amount $89 $89 $89 $88 $87 $87 $87 $86 $86 $85 $ $89 Per Week = $386 Per Month Source: NCM, Subprime Analytics

16

17 Months Average Original Term (Months) Average Original Term (Months) Effective Duration is 2-6 Months Longer! Source: Subprime Analytics Booth #115

18 Opportunity Knocks From Auto Bond Defaults! More than 8.4% of (auto bond) borrowers with weak credit scores who took out loans in the first quarter of 2014 had missed payments by November, according to Moody s analysis of Equifax credit-reporting data. That was the highest level since David Stockman Contra Corner January 11, 2015

19 Step 3 Successful BHPH Operators Must Maintain Financial Flexibility! Average Debt to Total Assets 57% 56% 55% 54% 53% 52% 51% 50% 49% 48% 47% 56% 52% 51% 50% Debt to Total Assets Source: SGC Accounting Reduce Leverage Don t Increase It!

20 How Some BHPH Operators Are Portfolio Number Competing Successfully! Annual ROI (A) Life of Loan ROI Interest Method Net Loss Rates (B) State Percent Portfolio Liquidated % 114.8% Simple 19.83% WI 67.2% % 123.7% Simple 27.16% IL 56.3% % 113.3% Simple 34.83% OH 57.3% % 124.8% Simple 9.58% TN 60.7% % 115.9% Simple 33.45% TX 62.6% % 124.7% Simple 25.03% PA 64.3% Median 45.6% 119.8% 26.1% 61.6% Average 44.1% 119.5% 25.0% 61.4% (A) ROI calculated before operating costs, debt expense & collection costs. (B) Loss/Liquidation Rate net of Recoveries. Source: Subprime Analytics Booth #115

21 Business Models Which Generated The Highest ROIs! Portfolio Number Annual ROI (A) Average ACV Average Down Payment Average Term (Months) Average Amount Financed APR Average Weekly Payment % $4,523 $ $8, % $ % $3,844 $ $8, % $ % $4,371 $1, $9, % $ % $5,460 $1, $9, % $ % $5,041 $ $11, % $ % $4,887 $ $10, % $89 Median 45.6% $4,705 $ $9, % $90 Average 44.1% $4,688 $ $9, % $93 (A) Cash ROI calculated before operating costs, debt expense & collection costs. Source: Subprime Analytics Booth #115

22

23 What Can You Do To Protect Your Operation? 1. Appoint a Chief Compliance Officer. 2. Implement a complaint resolution protocol. 3. Review and document your underwriting and collection procedures. 4. Learn from your competitors mistakes. 5. Implement the take aways from NABD 2016 on compliance best practices. 5/19/2016

24 Step 5 Develop Efficient Systems And Implement Technology Visit our exhibit hall to see the latest products and services. The technology has never been better! 5/19/2016

25 Step 6 Keeping Them Sold Is About Customer Relationships Not Transactions! 5/19/2016

26 Now Here Is Brent Carmichael, Executive Moderator For NCM Q & A Will Follow Brent s Presentation! Ken Shilson, CPA Booth #

27 NABD 2016 INDUSTRY TRENDS & BENCHMARKS Presented May 25, 2016 by Brent Carmichael

28 INDUSTRY TRENDS & BENCHMARKS + NCM Buy Here Pay Here (BHPH) 20 Group Data Monthly data reporting $850 million+ in outstanding receivables More than 65,000 units sold 76

29 WHAT TO DO ABOUT SUBPRIME + Take it on + Get into it + Dip down + Ride it out 77

30 TAKE IT ON

31 TAKE IT ON + Pros Sell more vehicles Inventory availability Cash flow Step up for repeats 79

32 TAKE IT ON + Cons: Lining up financing Inventory cost Sales process Shrinking customer base 80

33 GET INTO IT

34 GET INTO IT + Pros: Keep all the money No hoops Inventory availability Keep the repeats 82

35 GET INTO IT + Cons: Cash flow Inventory cost Competition Risk 83

36 DIP DOWN 84

37 DIP DOWN + Pros: Sell more vehicles Grow customer base Inventory availability 85

38 DIP DOWN + Cons: Increased delinquencies Increased losses Reconditioning Morale 86

39 RIDE IT OUT 87

40 RIDE IT OUT + Pros: No effort Cash flow House clean 88

41 RIDE IT OUT + Cons: Shrinking customer base Cash flow Downsizing 89

42 ABOUT US

43 ABOUT NCM ASSOCIATES Pioneered the automotive 20 Group in Groups + Education + Benchmark tools + Business intelligence + Consulting + Travel support 91 ncmassociates.com/bhph

44 VISIT US AT BOOTH #223

45

NABD 2014 National Conference. Benchmarks and Industry Trends

NABD 2014 National Conference Benchmarks and Industry Trends About NCM Associates Pioneered the automotive 20 Group in 1947 Provide 20 Groups Education Consulting Benchmark Tools Data Management Solutions

NABD 2014 National Conference Benchmarks and Industry Trends About NCM Associates Pioneered the automotive 20 Group in 1947 Provide 20 Groups Education Consulting Benchmark Tools Data Management Solutions

National Alliance of Buy Here, Pay Here Dealers (NABD) 2180 North Loop West, Suite 260 Houston, Texas

2180 North Loop West, Suite 260 Houston, Texas") BUY HERE, PAY HERE INDUSTRY BENCHMARKS/TRENDS - 2010 - CONTRIBUTORS: www.bhphinfo.com www.sgcaccounting.com www.ncm20.com www.subanalytics.com www.subanalytics.com National Alliance of Buy Here, Pay Here

BUY HERE, PAY HERE INDUSTRY BENCHMARKS/TRENDS - 2010 - CONTRIBUTORS: www.bhphinfo.com www.sgcaccounting.com www.ncm20.com www.subanalytics.com www.subanalytics.com National Alliance of Buy Here, Pay Here

BUY HERE, PAY HERE INDUSTRY BENCHMARKS/TRENDS - 2017 - CONTRIBUTORS: www.sgcaccounting.com www.ncm20.com www.subanalytics.com www.niada.com Kenneth Shilson & Associates, PC dba Subprime Analytics 2180

BUY HERE, PAY HERE INDUSTRY BENCHMARKS/TRENDS - 2017 - CONTRIBUTORS: www.sgcaccounting.com www.ncm20.com www.subanalytics.com www.niada.com Kenneth Shilson & Associates, PC dba Subprime Analytics 2180

Underwriting, Metrics, and Credit Scoring That Reduce Losses

Underwriting, Metrics, and Credit Scoring That Reduce Losses Presentation to Innovate 2012 Monday, September 17, 2012 Part One Ken Shilson, CPA President, Subprime Analytics Booth # 132 2180 North Loop

Underwriting, Metrics, and Credit Scoring That Reduce Losses Presentation to Innovate 2012 Monday, September 17, 2012 Part One Ken Shilson, CPA President, Subprime Analytics Booth # 132 2180 North Loop

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q4 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q4 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q1 2018 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q1 2018 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q4 2016 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q4 2016 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q1 2016

State of the Automotive Finance Market A look at loans and leases in Q1 2016 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q1 2016 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

State of the Automotive Finance Market

State of the Automotive Finance Market Presented by: Melinda Zabritski Q3 2018 1 Experian Session overview Market Overview Outstanding balances Total risk distributions Delinquency Originations New and

State of the Automotive Finance Market Presented by: Melinda Zabritski Q3 2018 1 Experian Session overview Market Overview Outstanding balances Total risk distributions Delinquency Originations New and

A Line of Credit Might Be the Largest Financial Commitment of Your Life, But It Can Unlock the Full Potential of Your BHPH Operation

Worth the Effort A Line of Credit Might Be the Largest Financial Commitment of Your Life, But It Can Unlock the Full Potential of Your BHPH Operation By Paxton Wright One of the keys to operating an auto

Worth the Effort A Line of Credit Might Be the Largest Financial Commitment of Your Life, But It Can Unlock the Full Potential of Your BHPH Operation By Paxton Wright One of the keys to operating an auto

Melinda Zabritski, Director of Automotive Credit

State of the Automotive Finance Market Third Quarter 2010 Melinda Zabritski, Director of Automotive Credit 2010 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein

State of the Automotive Finance Market Third Quarter 2010 Melinda Zabritski, Director of Automotive Credit 2010 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q3 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q3 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

State of the Automotive Finance Market Fourth Quarter 2015

State of the Automotive Finance Market Fourth Quarter 2015 Melinda Zabritski Sr. Director Financial Solutions 2016 2015 Experian Information Solutions, Inc. Inc. All rights All rights reserved. reserved.

State of the Automotive Finance Market Fourth Quarter 2015 Melinda Zabritski Sr. Director Financial Solutions 2016 2015 Experian Information Solutions, Inc. Inc. All rights All rights reserved. reserved.

Melinda Zabritski, Director of Automotive Credit

State of the Automotive Finance Market First Quarter 2012 Melinda Zabritski, Director of Automotive Credit Experian and the marks used herein are service marks or registered trademarks of Experian Information

State of the Automotive Finance Market First Quarter 2012 Melinda Zabritski, Director of Automotive Credit Experian and the marks used herein are service marks or registered trademarks of Experian Information

Make Tax Season Great Again

PRESENTED BY: WILLIAM J. NEYLAN III, PRESIDENT/CEO TRS TAX MAX Online: www.taxmax.com Toll Free: 866-642-4107 BREAKING NEWS! Coming later in the presentation Who is Tax Max? Nationwide Company Started

PRESENTED BY: WILLIAM J. NEYLAN III, PRESIDENT/CEO TRS TAX MAX Online: www.taxmax.com Toll Free: 866-642-4107 BREAKING NEWS! Coming later in the presentation Who is Tax Max? Nationwide Company Started

State of the Automotive Finance Market

State of the Automotive Finance Market Presented by: Melinda Zabritski Q4 2018 1 Experian Session overview Market Overview Outstanding balances Total risk distributions Delinquency Originations New and

State of the Automotive Finance Market Presented by: Melinda Zabritski Q4 2018 1 Experian Session overview Market Overview Outstanding balances Total risk distributions Delinquency Originations New and

State of the Automotive Finance Market Fourth Quarter 2013

State of the Automotive Finance Market Fourth Quarter 2013 Melinda Zabritski Sr. Director, Experian Automotive Experian and the marks used herein are service marks or registered trademarks of Experian

State of the Automotive Finance Market Fourth Quarter 2013 Melinda Zabritski Sr. Director, Experian Automotive Experian and the marks used herein are service marks or registered trademarks of Experian

State of the Automotive Finance Market Third Quarter 2015

State of the Automotive Finance Market Third Quarter 2015 Melinda Zabritski Sr. Director Financial Solutions 2015 2015 Experian Information Solutions, Inc. Inc. All rights All rights reserved. reserved.

State of the Automotive Finance Market Third Quarter 2015 Melinda Zabritski Sr. Director Financial Solutions 2015 2015 Experian Information Solutions, Inc. Inc. All rights All rights reserved. reserved.

Investing for Small Governments

Tuesday MAY, 23 2017 10:20AM 12PM Investing for Small Governments MODERATOR SPEAKERS Al Rolek Finance Director, River Falls, WI John Grady Managing Director, Public Trust Advisors Darrel Thomas Assistant

Tuesday MAY, 23 2017 10:20AM 12PM Investing for Small Governments MODERATOR SPEAKERS Al Rolek Finance Director, River Falls, WI John Grady Managing Director, Public Trust Advisors Darrel Thomas Assistant

Unemployment Insurance Financing

Unemployment Insurance Financing Presentation to Employment Security Council August 3, 2010 2 Discussion Topics Program Objectives Status of Nevada s Trust Fund Federal Loan Process Costs of Borrowing

Unemployment Insurance Financing Presentation to Employment Security Council August 3, 2010 2 Discussion Topics Program Objectives Status of Nevada s Trust Fund Federal Loan Process Costs of Borrowing

LendIt Michele Raneri April 2016

LendIt 2016 Michele Raneri April 2016 Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein

LendIt 2016 Michele Raneri April 2016 Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein

Staying out of Trouble - How to Improve Your Capacity Assessment Reports A Presentation for CCO Members David F. McCarroll, CPA, CA

Staying out of Trouble - How to Improve Your Capacity Assessment Reports A Presentation for CCO Members David F. McCarroll, CPA, CA It looked like the right thing to do: Staying out of Trouble Presentation

Staying out of Trouble - How to Improve Your Capacity Assessment Reports A Presentation for CCO Members David F. McCarroll, CPA, CA It looked like the right thing to do: Staying out of Trouble Presentation

Unique insights on the consumer credit market

Unique insights on the consumer credit market Highlights from the 2015 Experian Oliver Wyman Market Intelligence Report Experian and the marks used herein are service marks or registered trademarks of

Unique insights on the consumer credit market Highlights from the 2015 Experian Oliver Wyman Market Intelligence Report Experian and the marks used herein are service marks or registered trademarks of

State of the Automotive Finance Market. Melinda Zabritski Sr. Director Experian Automotive

State of the Automotive Finance Market Melinda Zabritski Sr. Director Experian Automotive Discussion Points What s on the road? Return of the US automotive market Shifting consumer dynamic Overall consumer

State of the Automotive Finance Market Melinda Zabritski Sr. Director Experian Automotive Discussion Points What s on the road? Return of the US automotive market Shifting consumer dynamic Overall consumer

Trends Report Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers

Trends Report 2018 Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers 2018 Alternative Financial Services Lending Trends Overview How subprime borrower behavior

Trends Report 2018 Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers 2018 Alternative Financial Services Lending Trends Overview How subprime borrower behavior

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Copyright Texas Education Agency, All rights reserved.

Copyright Texas Education Agency, 2012. These Materials are copyrighted and trademarked as the property of the Texas Education Agency (TEA) and may not be reproduced without the express written permission

Copyright Texas Education Agency, 2012. These Materials are copyrighted and trademarked as the property of the Texas Education Agency (TEA) and may not be reproduced without the express written permission

Welcome! Credit Scoring and Sub-Prime Lending

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Recap of 2017: The Best Year in a Decade

NOVEMBER 217 Recap of 217: The Best Year in a Decade Macroeconomic conditions remained favorable for housing and mortgage markets in 217. Despite challenges, the housing markets remain on track for their

NOVEMBER 217 Recap of 217: The Best Year in a Decade Macroeconomic conditions remained favorable for housing and mortgage markets in 217. Despite challenges, the housing markets remain on track for their

How to Stay Relevant in a Disruptive Lending Environment

How to Stay Relevant in a Disruptive Lending Environment Don Arkell CU Lending Advice Friday, June 10, 2016 2:15 p.m. Lending Attitude Check The best lenders learn that lending is both an attitude and

How to Stay Relevant in a Disruptive Lending Environment Don Arkell CU Lending Advice Friday, June 10, 2016 2:15 p.m. Lending Attitude Check The best lenders learn that lending is both an attitude and

Secrets to Success: Personal Finance Management

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Quarterly Economic Update Key Trends

Quarterly Economic Update Key Trends Linda Haran Senior Director June 2011 Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product

Quarterly Economic Update Key Trends Linda Haran Senior Director June 2011 Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product

STATE OF THE LINE REPORT

ANNUAL ISSUES SYMPOSIUM STATE OF THE LINE REPORT T H E SYSTEM @WORK KATHY ANTONELLO, FCAS, FSA, MAAA CHIEF ACTUARY NCCI Copyright NCCI Holdings, Inc. All Rights Reserved. ANNUAL ISSUES SYMPOSIUM PROPERTY/CASUALTY

ANNUAL ISSUES SYMPOSIUM STATE OF THE LINE REPORT T H E SYSTEM @WORK KATHY ANTONELLO, FCAS, FSA, MAAA CHIEF ACTUARY NCCI Copyright NCCI Holdings, Inc. All Rights Reserved. ANNUAL ISSUES SYMPOSIUM PROPERTY/CASUALTY

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Housing and Credit Markets Outlook

Housing and Credit Markets Outlook FTA Revenue Estimating Conference Springfield, IL Amy Crews Cutts, SVP Chief Economist October 7, Equifax Inc. Government Shutdown and Debt Ceiling! As of October 1 st

Housing and Credit Markets Outlook FTA Revenue Estimating Conference Springfield, IL Amy Crews Cutts, SVP Chief Economist October 7, Equifax Inc. Government Shutdown and Debt Ceiling! As of October 1 st

Driving Growth with a New Measure of Credit Capacity

Driving Growth with a New Measure of Credit Capacity Driving Innovation FICO and Equifax Open Avenues to Growth with a More Comprehensive Approach to Risk Assessment August 2012 For more than five years,

Driving Growth with a New Measure of Credit Capacity Driving Innovation FICO and Equifax Open Avenues to Growth with a More Comprehensive Approach to Risk Assessment August 2012 For more than five years,

Did you miss Risk-Based Lending Part 1?

Welcome! We will begin today at 1pm central. Did you miss Risk-Based Lending Part 1? Check out the archive for video + slides Risk-Based Lending Three Credit Union Perspectives Betsy Sommers, SVP Seasons

Welcome! We will begin today at 1pm central. Did you miss Risk-Based Lending Part 1? Check out the archive for video + slides Risk-Based Lending Three Credit Union Perspectives Betsy Sommers, SVP Seasons

Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial?

SM MARCH 2014 Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial? Contents In summary 1 Who is typically unscoreable by conventional models? 2 How do these currently

SM MARCH 2014 Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial? Contents In summary 1 Who is typically unscoreable by conventional models? 2 How do these currently

Investor Presentation

Investor Presentation March 2017 Investor Presentation Forward-Looking Statements Certain information included in this presentation and other statements or materials published or to be published by Marlin

Investor Presentation March 2017 Investor Presentation Forward-Looking Statements Certain information included in this presentation and other statements or materials published or to be published by Marlin

COMMUNITY CREDIT CHART BOOK

2016 COMMUNITY CREDIT CHART BOOK FEDERAL RESERVE B ANK of NEW YORK Editors Kausar Hamdani, Ph.D. SVP and Senior Advisor Claire Kramer Mills, Ph.D. AVP and Community Affairs Officer Data Support Jessica

2016 COMMUNITY CREDIT CHART BOOK FEDERAL RESERVE B ANK of NEW YORK Editors Kausar Hamdani, Ph.D. SVP and Senior Advisor Claire Kramer Mills, Ph.D. AVP and Community Affairs Officer Data Support Jessica

Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial?

SM MAY 2015 Is the Way You Score Customers State of the Art or State of Denial? Contents In summary 1 Who is typically unscoreable by conventional models? 2 How do these currently unscored consumers score

SM MAY 2015 Is the Way You Score Customers State of the Art or State of Denial? Contents In summary 1 Who is typically unscoreable by conventional models? 2 How do these currently unscored consumers score

Quick Credit Repair Guide

1 Quick Credit Repair Guide Beacon score? You will most likely have heard of this bizarre term at some point during your home buying process and wondered what they meant and how they affect the mortgage

1 Quick Credit Repair Guide Beacon score? You will most likely have heard of this bizarre term at some point during your home buying process and wondered what they meant and how they affect the mortgage

Today s Business Environment

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

How to be Successful With Higher-Risk Auto Lending

How to be Successful With Higher-Risk Auto Lending Heartland Credit Union Association Annual Convention Overland Park, KS October 6, 2017 By Brett Christensen, Owner CU Lending Advice, LLC brett@culendingadvice.com

How to be Successful With Higher-Risk Auto Lending Heartland Credit Union Association Annual Convention Overland Park, KS October 6, 2017 By Brett Christensen, Owner CU Lending Advice, LLC brett@culendingadvice.com

Rerouting the Regulation of Insurance: The Actuaries Perspective

Rerouting the Regulation of Insurance: The Actuaries Perspective An Capitol Hill Briefing June 1, 2004 1 Rerouting the Regulation of Insurance 1 Panel Moderator: Henry W. Siegel, FSA, MAAA Vice Chairperson,

Rerouting the Regulation of Insurance: The Actuaries Perspective An Capitol Hill Briefing June 1, 2004 1 Rerouting the Regulation of Insurance 1 Panel Moderator: Henry W. Siegel, FSA, MAAA Vice Chairperson,

VANTAGESCORE SOLUTIONS INTRODUCES VANTAGESCORE 3.0 MODEL

FOR IMMEDIATE RELEASE Contact: Jeff Richardson VantageScore Solutions 203-363-2170 jeffrichardson@vantagescore.com VANTAGESCORE SOLUTIONS INTRODUCES VANTAGESCORE 3.0 MODEL New Model Sets the Standard for

FOR IMMEDIATE RELEASE Contact: Jeff Richardson VantageScore Solutions 203-363-2170 jeffrichardson@vantagescore.com VANTAGESCORE SOLUTIONS INTRODUCES VANTAGESCORE 3.0 MODEL New Model Sets the Standard for

Loss Prevention Strategy & Framework for Manitoba Public Insurance

Loss Prevention Strategy & Framework for Manitoba Public Insurance May Version:. Date Revised: May, Document Name: MAIN_MPI Loss Prevention Strategy and Framework.docx Page 0 Executive Summary Manitoba

Loss Prevention Strategy & Framework for Manitoba Public Insurance May Version:. Date Revised: May, Document Name: MAIN_MPI Loss Prevention Strategy and Framework.docx Page 0 Executive Summary Manitoba

Housing Recovery is Underway, But Not for Everyone

Housing Recovery is Underway, But Not for Everyone Eric Belsky August 2013 Dallas, TX Housing Markets Have Corrected In Significant Ways Both price and quantity reductions have occurred Even after price

Housing Recovery is Underway, But Not for Everyone Eric Belsky August 2013 Dallas, TX Housing Markets Have Corrected In Significant Ways Both price and quantity reductions have occurred Even after price

Q Industry Insights Report

Q3 2015 Industry Insights Report U.S. Financial Services Nidhi Verma Director, Financial Services Research and Consulting TransUnion TransUnion s Industry Insights Report is a quarterly overview summarizing

Q3 2015 Industry Insights Report U.S. Financial Services Nidhi Verma Director, Financial Services Research and Consulting TransUnion TransUnion s Industry Insights Report is a quarterly overview summarizing

Small Business Credit Outlook

2016 Q1 Small Business Credit Outlook Risk-Off Keeps the Expansion Intact March confirms the current wait and see mood of private companies. On a macro level, private companies are maintaining current

2016 Q1 Small Business Credit Outlook Risk-Off Keeps the Expansion Intact March confirms the current wait and see mood of private companies. On a macro level, private companies are maintaining current

Investor Presentation As of March 31, 2018

Investor Presentation As of March 31, 2018 Consumer finance company focused on sub-prime auto market Established in 1991. IPO in 1992 Through March 31, 2018, approximately $14.6 billion in contracts originated

Investor Presentation As of March 31, 2018 Consumer finance company focused on sub-prime auto market Established in 1991. IPO in 1992 Through March 31, 2018, approximately $14.6 billion in contracts originated

Assessing the Affordability of State Debt

Assessing the Affordability of State Debt January 29, 2014 Jennifer Weiner, Senior Policy Analyst New England Public Policy Center Federal Reserve Bank of Boston Views expressed are the author s and are

Assessing the Affordability of State Debt January 29, 2014 Jennifer Weiner, Senior Policy Analyst New England Public Policy Center Federal Reserve Bank of Boston Views expressed are the author s and are

Premium Savings Program Broker Training

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Premium Savings Program Broker Training April 2013 We are responding to ACA changes Pricing volatility Rate shock

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Premium Savings Program Broker Training April 2013 We are responding to ACA changes Pricing volatility Rate shock

Module 4: Debt Lesson Part 2

Module 4: Debt Lesson Part 2 Module 4: Debt Lesson Part 2 Getting Rid of Your Debt Forever The Lesson Blueprint Where do I Start First? What Tools Can I Use? Rookie Mistakes Where Do I Start? Debt Snowball

Module 4: Debt Lesson Part 2 Module 4: Debt Lesson Part 2 Getting Rid of Your Debt Forever The Lesson Blueprint Where do I Start First? What Tools Can I Use? Rookie Mistakes Where Do I Start? Debt Snowball

2006 BALANCE FINANCIAL FITNESS PROGRAM

2006 BALANCE FINANCIAL FITNESS PROGRAM Tools for Financial Independence Manage money Prepare for future bills Open / maintain checking and savings accounts Use credit wisely Invest money Attend seminars

2006 BALANCE FINANCIAL FITNESS PROGRAM Tools for Financial Independence Manage money Prepare for future bills Open / maintain checking and savings accounts Use credit wisely Invest money Attend seminars

Older consumers and student loan debt by state

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

A new highly predictive FICO Score for an uncertain world

A new highly predictive FICO Score for an uncertain world Lenders gain a 5% 15% predictive boost to manage business and control losses Number 12 January 2009 As delinquency levels increase and consumer

A new highly predictive FICO Score for an uncertain world Lenders gain a 5% 15% predictive boost to manage business and control losses Number 12 January 2009 As delinquency levels increase and consumer

Kenneth Temkin and Neil Mayer September 19, 2013

Kenneth Temkin and Neil Mayer September 19, 2013 Methodology Results Interpreting the Results Neil Mayer and Associates 2 We used information on clients who received pre-purchase counseling from NeighborWorks

Kenneth Temkin and Neil Mayer September 19, 2013 Methodology Results Interpreting the Results Neil Mayer and Associates 2 We used information on clients who received pre-purchase counseling from NeighborWorks

Surviving The Market NECA National Convention. Seattle, Washington September 2009

Surviving The Market NECA National Convention Seattle, Washington September 2009 1 INTRODUCTION Weber O Brien Ltd. Toledo, Ohio Certified Public Accountants 5580 Monroe Street Sylvania, OH 43560 Telephone:

Surviving The Market NECA National Convention Seattle, Washington September 2009 1 INTRODUCTION Weber O Brien Ltd. Toledo, Ohio Certified Public Accountants 5580 Monroe Street Sylvania, OH 43560 Telephone:

Small business funding options

Small business funding options 60 minutes of straight talk! Donna J. Davis Former Regional Administrator U.S. Small Business Administration 11/16/17 WiFi: QBConnect Password not required About today s

Small business funding options 60 minutes of straight talk! Donna J. Davis Former Regional Administrator U.S. Small Business Administration 11/16/17 WiFi: QBConnect Password not required About today s

The Equifax Economic and Credit Markets Outlook

The Equifax Economic and Credit Markets Outlook A CUNA Roundtable Amy Crews Cutts SVP- Chief Economist, Equifax May 15, 2014 Comments on the Economic Outlook General forecast is that economic growth accelerates

The Equifax Economic and Credit Markets Outlook A CUNA Roundtable Amy Crews Cutts SVP- Chief Economist, Equifax May 15, 2014 Comments on the Economic Outlook General forecast is that economic growth accelerates

13.1. Reading a Credit Report EXERCISE. THEME 4 Lesson 13: Applying for Credit NAME: CLASS PERIOD:

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

Black Knight Mortgage Monitor

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of May, 2014 Month-end Black Knight First Look May 2014 Total U.S. loan delinquency rate (loans 30 or more days past due,

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of May, 2014 Month-end Black Knight First Look May 2014 Total U.S. loan delinquency rate (loans 30 or more days past due,

It can be achieved... Built by Predictive Modelers for Predictive Modelers TM

Built by Predictive Modelers for Predictive Modelers TM Attaining growth in a concentrated market Finding and capitalizing on opportunity Creating competitive advantage It can be achieved... FIGHTING FOR

Built by Predictive Modelers for Predictive Modelers TM Attaining growth in a concentrated market Finding and capitalizing on opportunity Creating competitive advantage It can be achieved... FIGHTING FOR

4Q 2017 Investor Presentation

4Q 2017 Investor Presentation Forward-Looking Statements This presentation, including the accompanying oral presentation (collectively, this presentation ), does not constitute an offer to sell or the

4Q 2017 Investor Presentation Forward-Looking Statements This presentation, including the accompanying oral presentation (collectively, this presentation ), does not constitute an offer to sell or the

HOW TO USE CREDIT. Latino Community Credit Union & the Latino Community Development Center.

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

Inaugural VantageScore 4.0 Trended Data Model Validation

SM JUNE 2018 VantageScore 4.0 2015-2017 Validation: Inaugural VantageScore 4.0 Trended Data Model Validation Contents SCORE PERFORMANCE MAINSTREAM CONSUMERS 1 Trended Data Results 1 INDUSTRY RESULTS 3

SM JUNE 2018 VantageScore 4.0 2015-2017 Validation: Inaugural VantageScore 4.0 Trended Data Model Validation Contents SCORE PERFORMANCE MAINSTREAM CONSUMERS 1 Trended Data Results 1 INDUSTRY RESULTS 3

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

2016 Workers compensation premium index rates

2016 Workers compensation premium index rates NH WA OR NV CA AK ID AZ UT MT WY CO NM MI VT ND MN SD WI NY NE IA PA IL IN OH WV VA KS MO KY NC TN OK AR SC MS AL GA TX LA FL ME MA RI CT NJ DE MD DC = Under

2016 Workers compensation premium index rates NH WA OR NV CA AK ID AZ UT MT WY CO NM MI VT ND MN SD WI NY NE IA PA IL IN OH WV VA KS MO KY NC TN OK AR SC MS AL GA TX LA FL ME MA RI CT NJ DE MD DC = Under

Portfolio Supplement Q NYSE: MTG

Portfolio Supplement Q2 NYSE: MTG Summary of Loan Modification and HARP Activity Risk in Force Primary Book Risk in Force Primary Book Risk in Force 2007 Primary Book HARP/RTM: 9% HAMP & Other Mods: 8%

Portfolio Supplement Q2 NYSE: MTG Summary of Loan Modification and HARP Activity Risk in Force Primary Book Risk in Force Primary Book Risk in Force 2007 Primary Book HARP/RTM: 9% HAMP & Other Mods: 8%

Portfolio Supplement Q NYSE: MTG

Portfolio Supplement Q1 NYSE: MTG Summary of Loan Modification and HARP Activity Risk in Force Primary Book Risk in Force Primary Book Risk in Force 2007 Primary Book HARP/RTM: 10% HAMP & Other Mods: 9%

Portfolio Supplement Q1 NYSE: MTG Summary of Loan Modification and HARP Activity Risk in Force Primary Book Risk in Force Primary Book Risk in Force 2007 Primary Book HARP/RTM: 10% HAMP & Other Mods: 9%

Portfolio Supplement Q NYSE: MTG

Portfolio Supplement Q4 NYSE: MTG Summary of Loan Modification and HARP Activity Risk in Force Primary Book Risk in Force Primary Book Risk in Force 2007 Primary Book HARP/RTM: 10% HAMP & Other Mods: 9%

Portfolio Supplement Q4 NYSE: MTG Summary of Loan Modification and HARP Activity Risk in Force Primary Book Risk in Force Primary Book Risk in Force 2007 Primary Book HARP/RTM: 10% HAMP & Other Mods: 9%

2017 Experian State of Lending. Who s Winning? Community Banks vs. Credit Unions

2017 Experian State of Lending Who s Winning? Community Banks vs. Credit Unions Community Banks & Credit Unions: By the Numbers Who s Winning the Lending Game? A look at Key Performance Health Metrics:

2017 Experian State of Lending Who s Winning? Community Banks vs. Credit Unions Community Banks & Credit Unions: By the Numbers Who s Winning the Lending Game? A look at Key Performance Health Metrics:

Trending Now in Insurance and Reinsurance

Trending Now in Insurance and Reinsurance Moderator: Leonard Schulte, Director of Legal Analysis and Risk Evaluation, FHF Panelists: Kevin ampion, Executive Managing Director, Aon enfield Lynne Mchristian,

Trending Now in Insurance and Reinsurance Moderator: Leonard Schulte, Director of Legal Analysis and Risk Evaluation, FHF Panelists: Kevin ampion, Executive Managing Director, Aon enfield Lynne Mchristian,

1Q 2018 Investor Presentation. May 2018

1Q 2018 Investor Presentation May 2018 Forward-Looking Statements This presentation, including the accompanying oral presentation (collectively, this presentation ), does not constitute an offer to sell

1Q 2018 Investor Presentation May 2018 Forward-Looking Statements This presentation, including the accompanying oral presentation (collectively, this presentation ), does not constitute an offer to sell

EXHIBIT C. The Effect of Proposed MY Corporate Average Fuel Economy (CAFE) Standards on the New Vehicle Market Population

Standards on the New Vehicle Market Population") NADA COMMENTS TO NHTSA/EPA RE: MY 2017-2025 PROPOSED STANDARDS EXHIBIT C The Effect of Proposed MY 2017-2025 Corporate Average Fuel Economy (CAFE) Standards on the New Vehicle Market Population Wagner,

NADA COMMENTS TO NHTSA/EPA RE: MY 2017-2025 PROPOSED STANDARDS EXHIBIT C The Effect of Proposed MY 2017-2025 Corporate Average Fuel Economy (CAFE) Standards on the New Vehicle Market Population Wagner,

Benefits: Retirement. BLR 2015 Survey Series MARCH. Sponsor 2 Participant summary 3 Executive summary 4 Survey questions/data 10

BLR 2015 Survey Series MARCH Benefits: Retirement Each month BLR conducts a nationwide survey to learn about current HR policies and practices throughout the country. On average, more than 1,800 individuals

BLR 2015 Survey Series MARCH Benefits: Retirement Each month BLR conducts a nationwide survey to learn about current HR policies and practices throughout the country. On average, more than 1,800 individuals

Credit score ratings chart 2017

Credit score ratings chart 2017 By 2009 the worldwide bond market (total debt outstanding) reached an estimated $82.2 trillion, in 2009 dollars. [26]. As the influence and profitability of CRAs expanded,

Credit score ratings chart 2017 By 2009 the worldwide bond market (total debt outstanding) reached an estimated $82.2 trillion, in 2009 dollars. [26]. As the influence and profitability of CRAs expanded,

Question of the Day. What percent of year olds have a credit card?

Chapter 6.1 Credit Objectives Explain the advantages and disadvantages of using credit Identify the different types of consumer credit Describe secured and unsecured loans Describe how to establish a sound

Chapter 6.1 Credit Objectives Explain the advantages and disadvantages of using credit Identify the different types of consumer credit Describe secured and unsecured loans Describe how to establish a sound

The Mortgage and Housing Market Outlook

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

State Universities Retirement System of Illinois

State Universities Retirement System of Illinois Serving Illinois Community Colleges and Universities 1901 Fox Drive Champaign, IL 61820-7333 (217) 378-8800 (217) 378-9802 (FAX) Investment Department To:

State Universities Retirement System of Illinois Serving Illinois Community Colleges and Universities 1901 Fox Drive Champaign, IL 61820-7333 (217) 378-8800 (217) 378-9802 (FAX) Investment Department To:

IRS audits & RFC setup. Steven Goldberg, CPA Steven Carstens, CPA SGC Accounting

IRS audits & RFC setup Steven Goldberg, CPA Steven Carstens, CPA SGC Accounting IRS audit issues IRS audit hot topics: Expanding the audits to include all entities Bad debts Issuing 1099 forms Inventory

IRS audits & RFC setup Steven Goldberg, CPA Steven Carstens, CPA SGC Accounting IRS audit issues IRS audit hot topics: Expanding the audits to include all entities Bad debts Issuing 1099 forms Inventory

AutoCount for lenders. Dynamic market reporting and analysis with our exclusive credit and NADA vehicle valuation data

AutoCount for lenders Dynamic market reporting and analysis with our exclusive credit and NADA vehicle valuation data 2 AutoCount for lenders AutoCount for lenders provides the only combination of state

AutoCount for lenders Dynamic market reporting and analysis with our exclusive credit and NADA vehicle valuation data 2 AutoCount for lenders AutoCount for lenders provides the only combination of state

Building a strong credit history. A public education campaign brought to you by MasterCard

Building a strong credit history A public education campaign brought to you by MasterCard Buying your first car, renting your first apartment, starting college, beginning your first real job master your

Building a strong credit history A public education campaign brought to you by MasterCard Buying your first car, renting your first apartment, starting college, beginning your first real job master your

Selective Insurance Group, Inc. Bank of America Merrill Lynch Insurance Conference. February 24, Forward Looking Statement

Selective Insurance Group, Inc. Bank of America Merrill Lynch Insurance Conference February 24, 2010 Forward Looking Statement Certain statements in this report, including information incorporated by reference,

Selective Insurance Group, Inc. Bank of America Merrill Lynch Insurance Conference February 24, 2010 Forward Looking Statement Certain statements in this report, including information incorporated by reference,

The Pros, Cons & IRS Gotchas of an RFC

The Pros, Cons & IRS Gotchas of an RFC CLAconnect.com 2016 TIADA Annual Conference & Expo July 26, 2016 Today s Objectives Is A Related Finance Company (RFC) Right For You? Tax Reasons Dealers Form RFC

The Pros, Cons & IRS Gotchas of an RFC CLAconnect.com 2016 TIADA Annual Conference & Expo July 26, 2016 Today s Objectives Is A Related Finance Company (RFC) Right For You? Tax Reasons Dealers Form RFC

Measuring the Value of Rate Segmentation

Measuring the Value of Rate Segmentation ti David Cummings ISO Innovative Analytics Our Challenge Enhanced rate segmentation can add significant value BUT Increased segmentation has a cost How do we evaluate

Measuring the Value of Rate Segmentation ti David Cummings ISO Innovative Analytics Our Challenge Enhanced rate segmentation can add significant value BUT Increased segmentation has a cost How do we evaluate

Market Insight Snapshot

Market Insight Snapshot Strategic defaults off from peak but still high Problem won t really vanish until home prices climb (and stay there) June 23, 2011 Terry Stockman (not his real name) earns a handsome

Market Insight Snapshot Strategic defaults off from peak but still high Problem won t really vanish until home prices climb (and stay there) June 23, 2011 Terry Stockman (not his real name) earns a handsome

FOR IMMEDIATE RELEASE February 8, 2012

Contact Information Below CoreLogic Reports 830,000 Completed s Nationally in 2011, a Decrease of 24 Percent from One Year Ago 1.4 Million Homes in the Inventory at the End of 2011 SANTA ANA, Calif., CoreLogic

Contact Information Below CoreLogic Reports 830,000 Completed s Nationally in 2011, a Decrease of 24 Percent from One Year Ago 1.4 Million Homes in the Inventory at the End of 2011 SANTA ANA, Calif., CoreLogic

Fannie Mae 2010 First Quarter Credit Supplement. May 10, 2010

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

HOW TO PRIORITIZE PROJECTS WHEN EACH ONE IS CRITICAL. Neil Stolovitsky Senior Solution Consultant

HOW TO PRIORITIZE PROJECTS WHEN EACH ONE IS CRITICAL Neil Stolovitsky Senior Solution Consultant ATTENDING HIMSS 2017? Booth # 5147 2 AGENDA + Introductions + About Upland + Webinar + Questions 3 WHAT

HOW TO PRIORITIZE PROJECTS WHEN EACH ONE IS CRITICAL Neil Stolovitsky Senior Solution Consultant ATTENDING HIMSS 2017? Booth # 5147 2 AGENDA + Introductions + About Upland + Webinar + Questions 3 WHAT

TECHNOLOGY & SOFTWARE TAX BENEFITS & BURDENS

TECHNOLOGY & SOFTWARE TAX BENEFITS & BURDENS R&D Tax Credit & State & Local Tax Issues September 20, 2016 Ashley Thompson Director athompson@bkd.com JoAnna Simek, CPA Director jsimek@bkd.com 1 TO RECEIVE

TECHNOLOGY & SOFTWARE TAX BENEFITS & BURDENS R&D Tax Credit & State & Local Tax Issues September 20, 2016 Ashley Thompson Director athompson@bkd.com JoAnna Simek, CPA Director jsimek@bkd.com 1 TO RECEIVE

Overview of the U.S. Payments Industry

0 Overview of the U.S. Payments Industry Southern Financial Exchange Conference May 3, 2017 Today s Discussion Trends in payments volume and value Five forces impacting payments 1 US PAYMENTS INDUSTRY:

0 Overview of the U.S. Payments Industry Southern Financial Exchange Conference May 3, 2017 Today s Discussion Trends in payments volume and value Five forces impacting payments 1 US PAYMENTS INDUSTRY:

Count Balance $0.00 $0.00 $0.00 Current Delinquent Other 0 0 0

COLLECTION ACCOUNTS: Count 0 0 0 Balance $0.00 $0.00 $0.00 Current 0 0 0 Delinquent 0 0 0 Other 0 0 0 TOTAL ACCOUNTS: Count 5 5 5 Balance $0.00 $0.00 $0.00 Current 5 5 5 Delinquent 0 0 0 Other 0 0 0 ACCOUNTS

COLLECTION ACCOUNTS: Count 0 0 0 Balance $0.00 $0.00 $0.00 Current 0 0 0 Delinquent 0 0 0 Other 0 0 0 TOTAL ACCOUNTS: Count 5 5 5 Balance $0.00 $0.00 $0.00 Current 5 5 5 Delinquent 0 0 0 Other 0 0 0 ACCOUNTS

CHAPTER 8. Personal Finance. Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 1

CHAPTER 8 Personal Finance Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 1 8.8 Credit Cards Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 2 Objectives 1.

CHAPTER 8 Personal Finance Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 1 8.8 Credit Cards Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 2 Objectives 1.

Your Money, Your Goals Spotlight Series. Dealing with debt: A closer look

Your Money, Your Goals Spotlight Series Dealing with debt: A closer look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It

Your Money, Your Goals Spotlight Series Dealing with debt: A closer look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It

Eye on the South Carolina Housing Market presented at 2008 HBA of South Carolina State Convention August 1, 2008

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

GET SOCIAL WITH US. #vision2016. Tweet, follow, share throughout the session.

GET SOCIAL WITH US Tweet, follow, share throughout the session. 2015 Experian Information Solutions, Inc. All rights reserved. 1 Alternative methods to validate with low portfolio volumes Experian and

GET SOCIAL WITH US Tweet, follow, share throughout the session. 2015 Experian Information Solutions, Inc. All rights reserved. 1 Alternative methods to validate with low portfolio volumes Experian and

PENSION STRESS TESTING FOR STATE FISCAL DIRECTORS

PENSION STRESS TESTING FOR STATE FISCAL DIRECTORS NCSL LEGISLATIVE FISCAL DIRECTORS PRE-CONFERENCE LOS ANGELES, CALIFORNIA JULY 29, 2018 GREG MENNIS, DIRECTOR STRENGTHENING PUBLIC SECTOR RETIREMENT SYSTEMS

PENSION STRESS TESTING FOR STATE FISCAL DIRECTORS NCSL LEGISLATIVE FISCAL DIRECTORS PRE-CONFERENCE LOS ANGELES, CALIFORNIA JULY 29, 2018 GREG MENNIS, DIRECTOR STRENGTHENING PUBLIC SECTOR RETIREMENT SYSTEMS

NAHB Priced-Out Estimates for 2019

NAHB Priced-Out Estimates for 2019 January 2, 2019 Special Study for HousignEconomics.com By Na Zhao, Ph.D. This article announces NAHB s priced out estimates for 2019, showing how higher home prices and

NAHB Priced-Out Estimates for 2019 January 2, 2019 Special Study for HousignEconomics.com By Na Zhao, Ph.D. This article announces NAHB s priced out estimates for 2019, showing how higher home prices and