NABD 2014 National Conference. Benchmarks and Industry Trends

|

|

|

- Berenice Underwood

- 5 years ago

- Views:

Transcription

1 NABD 2014 National Conference Benchmarks and Industry Trends

2 About NCM Associates Pioneered the automotive 20 Group in 1947 Provide 20 Groups Education Consulting Benchmark Tools Data Management Solutions 100% employee-owned and headquartered in Overland Park, KS

3 NABD 2014 Industry Trends NCM Buy Here, Pay Here 20 Group Data Monthly data reporting Dealer client industry specific surveys Over $500 million in outstanding receivables Over 47,000 units sold

4 Sales Volume 14: -1.3% 13: -0.4% 12: +2.8% Profitability 14: -8.3% 13: -14.8% 12: +21.6% Tax Season Ups and Downs

5 Inventory Levels 14: 55 days supply 13: 51 days supply 12: 54 days supply Cost 14: +$398/unit 13: +$586/unit 12: +$198/unit Recon 14: +$1,006/unit 13: +$1,013/unit 12: +$1,304/unit Tax Season Ups and Downs

6 Collections Aging (30+) 14: 5.3% 13: 5.0% 12: 4.2% Losses 14: $4,865/account 13: $4,779/account 12: $3,482/account Tax Season Ups and Downs

7 2014 -???? Sales Collections Looking ahead

8 Questions? For more information: ncm20.com/bhph

9 Was 2013 A Bad Year For BHPH? Wednesday, May 21, 2014 The Wynn, Las Vegas, NV By: Ken Shilson, CPA President Subprime Analytics Booth #123 NABD

10 Stansberry & Associates Investment Research 1. Founded in 1999 by Porter Stansberry. Based in Baltimore, MD. They are nationally recognized financial analysts and editors. 2. Stansberry predicted the financial crisis in 2008, the problems at GM in 2008, the failures of Fannie Mae and Freddie Mac, and others! 3. Their analysis is quoted in WSJ, Barron s, Washington Post and other leading publications. They provide financial opinions to CNBC, Fox Business News, and CNN. 4. They publish a monthly newsletter with over 100,000 subscribers. March 2014 issue was on Subprime auto loans. 5. Their financial research is considered credible!

11 Special Finance vs. BHPH? Who is Winning? These guys are borrowing money for around 2% and lending to subprime borrowers for 19% - a ridiculous spread Oh, and they re adding lots of leverage. (March 2014) Source: Stansberry & Associates Investment Research

12 The Greed Factor! And so, last year (2013), after three years of soaring loan amounts, collapsing lending standards, and expanding terms (loans up to seven years in duration), subprime car loans make up more than one in four loans made. Not surprisingly, $18 billion of car loans were securitized and sold to investors, thereby moving the credit risk from the finance companies to the investors. Sound familiar? Source: Stansberry & Associates Investment Research

13 Special Finance Auto Losses Increasing! Standard & Poor s released a report on February 26, 2014, warning that subprime auto loans were beginning to go bad at an alarming rate, before any material decrease to employment or other economic activity. In our opinion, we re at a turning point with respect to subprime auto loan performance, the credit-ratings agency wrote, similar to where we were in Source: Standard & Poors 2/26/14 Report On Subprime Auto Loan Performance

14 The Subprime Auto Market! The average auto loan today is for 65 months (about 5 years). Twenty percent of all auto loans are for durations between 73 and 84 months. Plus, the average dollar amount of these loans more than $26,000 is the largest ever recorded (March 2014) Source: Stansberry & Associates Investment Research

15 More Subprime Customers Today! Finally, the percentage of subprime borrowers is now at a record high 27% of all car borrowers. That s almost double the amount of subprime borrowers that were in the car market back in (March 2014) Source: Stansberry & Associates Investment Research

16 Opportunity Knocks for BHPH! Americans currently owe more than $800 billion dollars against their cars and trucks 34% of this debt is owed by subprime credits. Another 10% is owed by deep subprime folks with credit scores below 550. (March 2014) Source: Stansberry & Associates Investment Research

17 How is the aggressive underwriting in 2013 working out for Subprime Finance Companies?

18

19

20

21

22 What happened to BHPH Market Share in 2013?

23 An overview of the automotive loan market Source: Experian Automotive

24

25 Is Subprime credit risk being priced properly in customer payments and down payments?

26

27 Are BHPH Operators Maximizing Customer Payments? Average Weekly Payment Amount: $87 Average Weekly Payment Amount $87 $87 $86 $86 $85 $85 $84 $84 $83 $ Source: NCM/Subprime Analytics Source: NCM, Subprime Analytics Up 3% Since 2009!

28 Are BHPH Operators Maximizing Down Payments? Average Customer Down Payment: Average Cash Down Payment (Excluding Trades) $1,100 $1,050 $1,039 $1,033 $1,000 $950 $900 $959 $910 $887 $850 $ Average Down Payment Source: Subprime Analytics 17% Decrease Since 2009!

29 Are BHPH Operators Financing Larger Contracts? Average Amount Financed: Average Amount Financed $11,000 $10,689 $10,500 $10,000 $9,500 $9,488 $9,412 $9,667 $10,084 $9,000 $8, Average Amount Financed Source: Subprime Analytics Up 12% Since 2009!

30 Are the Term of BHPH Contracts Getting Longer? Average Original Term (Months) Average Original Term (Months) Months Year Average Original Term (Months) Source: Subprime Analytics Note: Average effective duration is 2-6 months longer than the original term.

31 What is the trend on in Cash in Deal? Average Vehicle Cost, Down Payment, Cash in Deal: Average Vehicle Cost, Cash Down Payment, Cash in Deal $7,000 $6,000 $5,000 $4,000 $5,029 $5,150 $3,990 $4,117 $5,466 $4,507 $5,582 $4,672 $6,181 $5,294 $3,000 $2,000 $1,000 $1,039 $1,033 $959 $910 $887 $ Average Vehicle Cost Average Down Payment Average Cash in Deal Source: Subprime Analytics ACV up 22%; CID Up 32%

32 Standard & Poors Ratings Services expects Subprime auto losses to rise in Source: S&P Auto Loan Performance Report 2/26/14

33 Maximizing Recoveries Has Never Been More Important In BHPH Success!

34 Mitigating BHPH Losses Has Never Been More Important! Average Recovery Dollars Per Unit: Average Recovery Dollars Per Unit $3,000 $2,971 $2,500 $2,000 $2,152 $2,286 $2,295 $2,437 $1,500 $1,000 $500 $ Average Recovery Dollars Per Unit Source: Subprime Analytics Recoveries up 38% since 2009.

35 What s ahead for BHPH Vehicle Inventory Supply?

36 Total Wholesale Supply: Off-rental, Off-lease, & Repos Peak to trough swing: 2.5M units -36% Source: Manheim Consulting

37

38 Don t miss presentations by Manheim and Tom Kontos tomorrow for updated information!

39 What did successful BHPH operators do in 2013? 1) Did not match silly special finance loans. Some integrated special finance and BHPH. 2) Used portfolio liquidation to reduce debt and increase financial flexibility. 3) Trimmed inventory carrying levels and reconditioning expense. 4) Controlled operating expenses by implementing technology to increase efficiency. 5) Expanded online marketing to connect with prospective customers. 6) Maximized recoveries to mitigate repo losses. 7) Worked on getting compliant.

40 Managing Credit Risk Is The Key To Subprime Success! You Must Match The Right Customers With The Vehicles They Can Afford Through Good Underwriting! Learn From Past Losses; Don t Repeat Them!

41 My Conclusion: Maybe 2013 will not turn out to be so bad after all!

42 Questions At this time you are welcome to ask questions on anything covered during this presentation Kenneth B. Shilson, CPA Subprime Analytics 2180 North Loop W., Ste. 270 Houston, TX Booth #123

Navigating the Road to BHPH Success Six Step Approach!

Navigating the Road to BHPH Success Six Step Approach! Presented by: Kenneth Shilson, President Subprime Analytics NABD May 25, 2016 Visit Booth #115 www.bhphinfo.com www.subanalytics.com Source: Experian

Navigating the Road to BHPH Success Six Step Approach! Presented by: Kenneth Shilson, President Subprime Analytics NABD May 25, 2016 Visit Booth #115 www.bhphinfo.com www.subanalytics.com Source: Experian

National Alliance of Buy Here, Pay Here Dealers (NABD) 2180 North Loop West, Suite 260 Houston, Texas

2180 North Loop West, Suite 260 Houston, Texas") BUY HERE, PAY HERE INDUSTRY BENCHMARKS/TRENDS - 2010 - CONTRIBUTORS: www.bhphinfo.com www.sgcaccounting.com www.ncm20.com www.subanalytics.com www.subanalytics.com National Alliance of Buy Here, Pay Here

BUY HERE, PAY HERE INDUSTRY BENCHMARKS/TRENDS - 2010 - CONTRIBUTORS: www.bhphinfo.com www.sgcaccounting.com www.ncm20.com www.subanalytics.com www.subanalytics.com National Alliance of Buy Here, Pay Here

Underwriting, Metrics, and Credit Scoring That Reduce Losses

Underwriting, Metrics, and Credit Scoring That Reduce Losses Presentation to Innovate 2012 Monday, September 17, 2012 Part One Ken Shilson, CPA President, Subprime Analytics Booth # 132 2180 North Loop

Underwriting, Metrics, and Credit Scoring That Reduce Losses Presentation to Innovate 2012 Monday, September 17, 2012 Part One Ken Shilson, CPA President, Subprime Analytics Booth # 132 2180 North Loop

BUY HERE, PAY HERE INDUSTRY BENCHMARKS/TRENDS - 2017 - CONTRIBUTORS: www.sgcaccounting.com www.ncm20.com www.subanalytics.com www.niada.com Kenneth Shilson & Associates, PC dba Subprime Analytics 2180

BUY HERE, PAY HERE INDUSTRY BENCHMARKS/TRENDS - 2017 - CONTRIBUTORS: www.sgcaccounting.com www.ncm20.com www.subanalytics.com www.niada.com Kenneth Shilson & Associates, PC dba Subprime Analytics 2180

May the Auto Industry Brief is published monthly by. manheim consulting

May 2013 summary economy: moving ahead at moderate speed page 1 retail and wholesale vehicle markets page 2 Q&a with tom webb page 5 the Auto Industry Brief is published monthly by manheim consulting.

May 2013 summary economy: moving ahead at moderate speed page 1 retail and wholesale vehicle markets page 2 Q&a with tom webb page 5 the Auto Industry Brief is published monthly by manheim consulting.

Welcome! Credit Scoring and Sub-Prime Lending

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Make Tax Season Great Again

PRESENTED BY: WILLIAM J. NEYLAN III, PRESIDENT/CEO TRS TAX MAX Online: www.taxmax.com Toll Free: 866-642-4107 BREAKING NEWS! Coming later in the presentation Who is Tax Max? Nationwide Company Started

PRESENTED BY: WILLIAM J. NEYLAN III, PRESIDENT/CEO TRS TAX MAX Online: www.taxmax.com Toll Free: 866-642-4107 BREAKING NEWS! Coming later in the presentation Who is Tax Max? Nationwide Company Started

A Line of Credit Might Be the Largest Financial Commitment of Your Life, But It Can Unlock the Full Potential of Your BHPH Operation

Worth the Effort A Line of Credit Might Be the Largest Financial Commitment of Your Life, But It Can Unlock the Full Potential of Your BHPH Operation By Paxton Wright One of the keys to operating an auto

Worth the Effort A Line of Credit Might Be the Largest Financial Commitment of Your Life, But It Can Unlock the Full Potential of Your BHPH Operation By Paxton Wright One of the keys to operating an auto

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q4 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q4 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

Did you miss Risk-Based Lending Part 1?

Welcome! We will begin today at 1pm central. Did you miss Risk-Based Lending Part 1? Check out the archive for video + slides Risk-Based Lending Three Credit Union Perspectives Betsy Sommers, SVP Seasons

Welcome! We will begin today at 1pm central. Did you miss Risk-Based Lending Part 1? Check out the archive for video + slides Risk-Based Lending Three Credit Union Perspectives Betsy Sommers, SVP Seasons

How to be Successful With Higher-Risk Auto Lending

How to be Successful With Higher-Risk Auto Lending Heartland Credit Union Association Annual Convention Overland Park, KS October 6, 2017 By Brett Christensen, Owner CU Lending Advice, LLC brett@culendingadvice.com

How to be Successful With Higher-Risk Auto Lending Heartland Credit Union Association Annual Convention Overland Park, KS October 6, 2017 By Brett Christensen, Owner CU Lending Advice, LLC brett@culendingadvice.com

THE HOUSING BUBBLE CHAPTER 11. Thursday, December 1, 11

THE HOUSING BUBBLE CHAPTER 11 HOUSING AND THE BUBBLE 2 HOUSING AND THE BUBBLE The housing bubble is one of the main causes of the current downturn for two reasons: Decrease in wealth from housing caused

THE HOUSING BUBBLE CHAPTER 11 HOUSING AND THE BUBBLE 2 HOUSING AND THE BUBBLE The housing bubble is one of the main causes of the current downturn for two reasons: Decrease in wealth from housing caused

Lender Solutions White Paper: Not All Vehicles Depreciate Alike

Lender Solutions White Paper: Not All Vehicles Depreciate Alike The current automotive landscape has proven to be very interesting for lenders as continued pent-up demand is driving expanded growth for

Lender Solutions White Paper: Not All Vehicles Depreciate Alike The current automotive landscape has proven to be very interesting for lenders as continued pent-up demand is driving expanded growth for

Relationships. Results. COMPANY OVERVIEW COMMERCIAL REAL ESTATE DEBT, EQUITY & SERVICING

Relationships. COMPANY OVERVIEW Results. COMMERCIAL REAL ESTATE DEBT, EQUITY & SERVICING COMMERCIAL REAL ESTATE DEBT, EQUITY & SERVICING Relationships. Results. For more than 50 years, NorthMarq Capital

Relationships. COMPANY OVERVIEW Results. COMMERCIAL REAL ESTATE DEBT, EQUITY & SERVICING COMMERCIAL REAL ESTATE DEBT, EQUITY & SERVICING Relationships. Results. For more than 50 years, NorthMarq Capital

Today s Business Environment

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

Housing and Credit Markets Outlook

Housing and Credit Markets Outlook FTA Revenue Estimating Conference Springfield, IL Amy Crews Cutts, SVP Chief Economist October 7, Equifax Inc. Government Shutdown and Debt Ceiling! As of October 1 st

Housing and Credit Markets Outlook FTA Revenue Estimating Conference Springfield, IL Amy Crews Cutts, SVP Chief Economist October 7, Equifax Inc. Government Shutdown and Debt Ceiling! As of October 1 st

The Mortgage and Housing Market Outlook

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q3 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q3 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

Relationships. Results. COMPANY OVERVIEW COMMERCIAL REAL ESTATE DEBT, EQUITY & SERVICING

Relationships. COMPANY OVERVIEW Results. COMMERCIAL REAL ESTATE DEBT, EQUITY & SERVICING C O M M E R C I A L R E A L E S TAT E D E B T, E Q U I T Y & S E R V I C I N G Relationships. Results. For more

Relationships. COMPANY OVERVIEW Results. COMMERCIAL REAL ESTATE DEBT, EQUITY & SERVICING C O M M E R C I A L R E A L E S TAT E D E B T, E Q U I T Y & S E R V I C I N G Relationships. Results. For more

Understanding The Importance Of Regularly Monitoring Collateral Risk Levels

Understanding The Importance Of Regularly Monitoring Collateral Risk Levels Auto lenders have had a spike in volume since the recession because of pent-up consumer demand to replace aging vehicles and

Understanding The Importance Of Regularly Monitoring Collateral Risk Levels Auto lenders have had a spike in volume since the recession because of pent-up consumer demand to replace aging vehicles and

Housing Recovery is Underway, But Not for Everyone

Housing Recovery is Underway, But Not for Everyone Eric Belsky August 2013 Dallas, TX Housing Markets Have Corrected In Significant Ways Both price and quantity reductions have occurred Even after price

Housing Recovery is Underway, But Not for Everyone Eric Belsky August 2013 Dallas, TX Housing Markets Have Corrected In Significant Ways Both price and quantity reductions have occurred Even after price

Markets Overlooking A Clear & Present Danger?

Markets Overlooking A Clear & Present Danger? May 8, 2017 by Lance Roberts of Real Investment Advice There is in interesting dichotomy currently occurring within the economy. While consumer confidence,

Markets Overlooking A Clear & Present Danger? May 8, 2017 by Lance Roberts of Real Investment Advice There is in interesting dichotomy currently occurring within the economy. While consumer confidence,

State of the Automotive Finance Market Fourth Quarter 2015

State of the Automotive Finance Market Fourth Quarter 2015 Melinda Zabritski Sr. Director Financial Solutions 2016 2015 Experian Information Solutions, Inc. Inc. All rights All rights reserved. reserved.

State of the Automotive Finance Market Fourth Quarter 2015 Melinda Zabritski Sr. Director Financial Solutions 2016 2015 Experian Information Solutions, Inc. Inc. All rights All rights reserved. reserved.

Melinda Zabritski, Director of Automotive Credit

State of the Automotive Finance Market First Quarter 2012 Melinda Zabritski, Director of Automotive Credit Experian and the marks used herein are service marks or registered trademarks of Experian Information

State of the Automotive Finance Market First Quarter 2012 Melinda Zabritski, Director of Automotive Credit Experian and the marks used herein are service marks or registered trademarks of Experian Information

ECONOMY: DESPITE SLOW APRIL, FUNDAMENTALS ARE IMPROVING

May 2009 ECONOMY: DESPITE SLOW APRIL, FUNDAMENTALS ARE IMPROVING page 1 RETAIL AND WHOLESALE VEHICLE MARKETS page 3 Q&A WITH TOM WEBB page 5 The Auto Industry Brief is published monthly by Manheim Consulting.

May 2009 ECONOMY: DESPITE SLOW APRIL, FUNDAMENTALS ARE IMPROVING page 1 RETAIL AND WHOLESALE VEHICLE MARKETS page 3 Q&A WITH TOM WEBB page 5 The Auto Industry Brief is published monthly by Manheim Consulting.

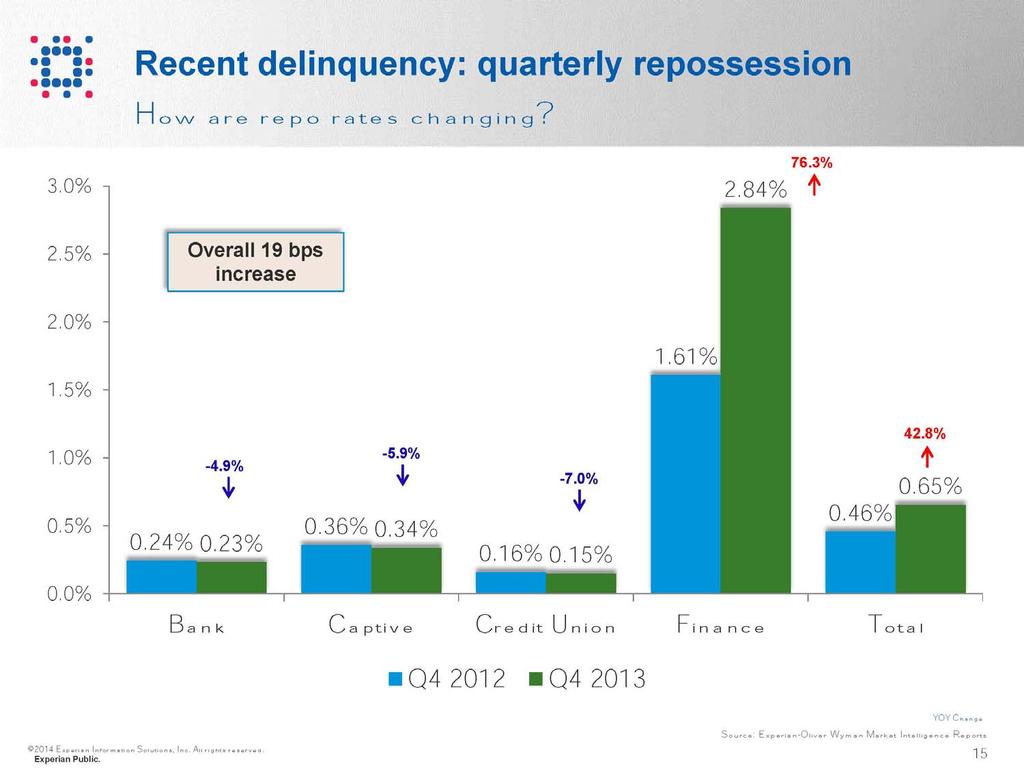

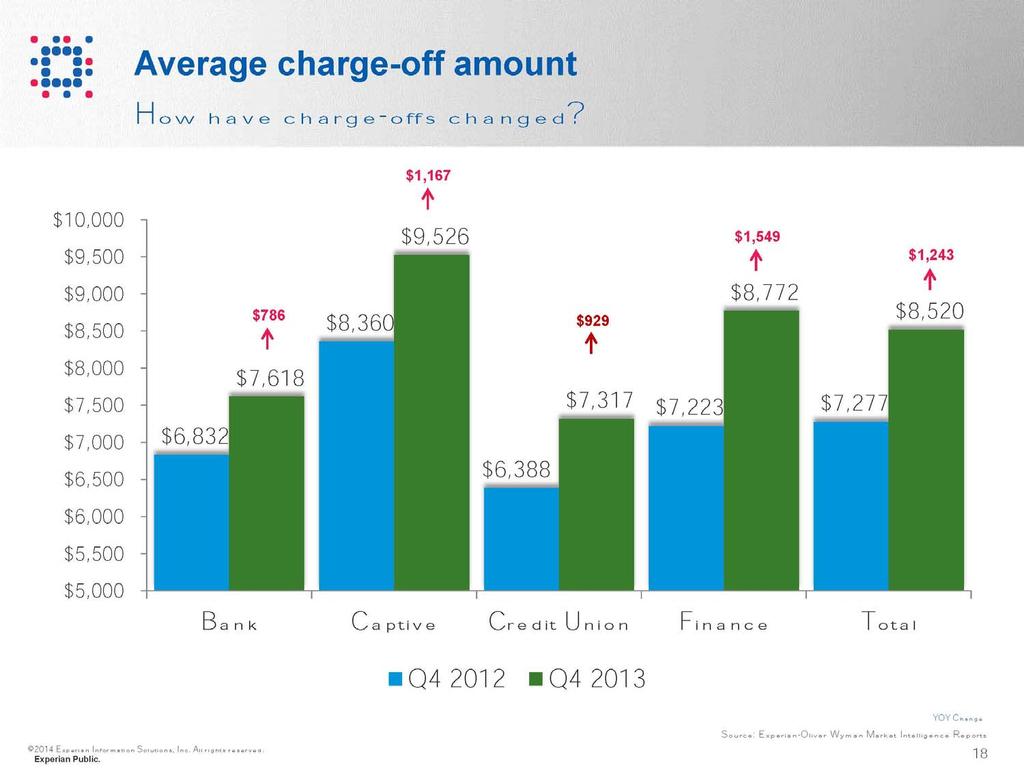

State of the Automotive Finance Market Fourth Quarter 2013

State of the Automotive Finance Market Fourth Quarter 2013 Melinda Zabritski Sr. Director, Experian Automotive Experian and the marks used herein are service marks or registered trademarks of Experian

State of the Automotive Finance Market Fourth Quarter 2013 Melinda Zabritski Sr. Director, Experian Automotive Experian and the marks used herein are service marks or registered trademarks of Experian

Financing Residential Real Estate. Qualifying the Buyer

Financing Residential Real Estate Lesson 8: Qualifying the Buyer Introduction In this lesson we will cover: the underwriting process, qualifying the buyer, and factors taken into account when a buyer s

Financing Residential Real Estate Lesson 8: Qualifying the Buyer Introduction In this lesson we will cover: the underwriting process, qualifying the buyer, and factors taken into account when a buyer s

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity The National Council of State Housing Agencies (NCSHA) and the state Housing Finance Agencies

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity The National Council of State Housing Agencies (NCSHA) and the state Housing Finance Agencies

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

The Equifax Economic and Credit Markets Outlook

The Equifax Economic and Credit Markets Outlook A CUNA Roundtable Amy Crews Cutts SVP- Chief Economist, Equifax May 15, 2014 Comments on the Economic Outlook General forecast is that economic growth accelerates

The Equifax Economic and Credit Markets Outlook A CUNA Roundtable Amy Crews Cutts SVP- Chief Economist, Equifax May 15, 2014 Comments on the Economic Outlook General forecast is that economic growth accelerates

The Mortgage Debt Market: A Tragedy

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

KAR Auction Services, Inc. Corporate Update. Second Quarter 2018

KAR Auction Services, Inc. Corporate Update Second Quarter 2018 Forward-Looking Statements This presentation includes forward-looking statements as that term is defined in the Private Securities Litigation

KAR Auction Services, Inc. Corporate Update Second Quarter 2018 Forward-Looking Statements This presentation includes forward-looking statements as that term is defined in the Private Securities Litigation

FINANCIAL POLICY FORUM. Washington, D.C PRIMER REPO OR REPURCHASE AGREEMENTS MARKET

FINANCIAL POLICY FORUM DERIVATIVES STUDY CENTER www.financialpolicy.org 1333 H Street, NW, 3 rd Floor rdodd@financialpolicy.org Washington, D.C. 20005 PRIMER REPO OR REPURCHASE AGREEMENTS MARKET Randall

FINANCIAL POLICY FORUM DERIVATIVES STUDY CENTER www.financialpolicy.org 1333 H Street, NW, 3 rd Floor rdodd@financialpolicy.org Washington, D.C. 20005 PRIMER REPO OR REPURCHASE AGREEMENTS MARKET Randall

The Current Real Estate Finance Climate

The Current Real Estate Finance Climate Elizabeth J. Zook, Esq. Carruthers & Roth, P.A. (336) 478-1110 December 10, 2008 Residenti tial Housing Market Subprime Mortgage Crisis i Ongoing financial crisis

The Current Real Estate Finance Climate Elizabeth J. Zook, Esq. Carruthers & Roth, P.A. (336) 478-1110 December 10, 2008 Residenti tial Housing Market Subprime Mortgage Crisis i Ongoing financial crisis

KAR Auction Services, Inc. Corporate Update. Third Quarter 2017

KAR Auction Services, Inc. Corporate Update Third Quarter 2017 Forward-Looking Statements This presentation includes forward-looking statements as that term is defined in the Private Securities Litigation

KAR Auction Services, Inc. Corporate Update Third Quarter 2017 Forward-Looking Statements This presentation includes forward-looking statements as that term is defined in the Private Securities Litigation

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q4 2016 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q4 2016 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2016 Experian Information Solutions,

The Office of Economic Policy HOUSING DASHBOARD. March 16, 2016

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

ALI-ABA Course of Study The Subprime Mortgage Crisis: From A to Z September 18-19, 2008 Washington, D.C.

507 ALI-ABA Course of Study The Subprime Mortgage Crisis: From A to Z September 18-19, 2008 Washington, D.C. U.S. Treasury Department Releases on Fannie Mae and Freddie Macsupplemental material Submitted

507 ALI-ABA Course of Study The Subprime Mortgage Crisis: From A to Z September 18-19, 2008 Washington, D.C. U.S. Treasury Department Releases on Fannie Mae and Freddie Macsupplemental material Submitted

Total Loss Accidents Up 20% How Does this Impact your Lending Portfolio?

Total Loss Accidents Up 20% How Does this Impact your Lending Portfolio? Presented by: Anne Holtzman, Senior Vice President of Claims and Recovery at Allied Solutions Market Conditions Increased percentage

Total Loss Accidents Up 20% How Does this Impact your Lending Portfolio? Presented by: Anne Holtzman, Senior Vice President of Claims and Recovery at Allied Solutions Market Conditions Increased percentage

HARP Refinance Guide. How You can Benefit from the HARP Program

HARP Refinance Guide How You can Benefit from the HARP Program Contents How HARP Can Help You You Might Qualify for HARP but Not Know It HARP Qualification Basics HARP History HARP 1.0 HARP 2.0 HARP 3.0

HARP Refinance Guide How You can Benefit from the HARP Program Contents How HARP Can Help You You Might Qualify for HARP but Not Know It HARP Qualification Basics HARP History HARP 1.0 HARP 2.0 HARP 3.0

How the Trump administration can continue progress in U.S. housing

How the Trump administration can continue progress in U.S. housing By Mark Zandi January 5, 2017 While housing has come a long way since the financial crisis, it has yet to fully recover. First-time home

How the Trump administration can continue progress in U.S. housing By Mark Zandi January 5, 2017 While housing has come a long way since the financial crisis, it has yet to fully recover. First-time home

Sharing the Pain and Gain in the Housing Market

THE ASSOCIATED PRESS /David Zalubowski Sharing the Pain and Gain in the Housing Market How Fannie Mae and Freddie Mac Can Prevent Foreclosures and Protect Taxpayers by Combining Principal Reductions with

THE ASSOCIATED PRESS /David Zalubowski Sharing the Pain and Gain in the Housing Market How Fannie Mae and Freddie Mac Can Prevent Foreclosures and Protect Taxpayers by Combining Principal Reductions with

Investor Presentation As of March 31, 2018

Investor Presentation As of March 31, 2018 Consumer finance company focused on sub-prime auto market Established in 1991. IPO in 1992 Through March 31, 2018, approximately $14.6 billion in contracts originated

Investor Presentation As of March 31, 2018 Consumer finance company focused on sub-prime auto market Established in 1991. IPO in 1992 Through March 31, 2018, approximately $14.6 billion in contracts originated

Fannie Mae 2012 Second-Quarter Credit Supplement. August 8, 2012

Fannie Mae 2012 Second-Quarter Credit Supplement August 8, 2012 This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for

Fannie Mae 2012 Second-Quarter Credit Supplement August 8, 2012 This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for

First Quarter 2017 Financial Results Supplement. May 2, 2017

First Quarter 2017 Financial Results Supplement May 2, 2017 Table of contents Financial Results 3 Quarterly Financial Results 4 Market-Related Items 5 Segment Financial Results 6 Portfolio Balances 7 Treasury

First Quarter 2017 Financial Results Supplement May 2, 2017 Table of contents Financial Results 3 Quarterly Financial Results 4 Market-Related Items 5 Segment Financial Results 6 Portfolio Balances 7 Treasury

Homeowner Benefits and Responsibilities

Homeowner Benefits and Responsibilities Introduction Homeowner Benefits and Responsibilities Benefits of Homeownership Responsibilities of Homeownership Refinancing and Home Equity Preventing Foreclosure

Homeowner Benefits and Responsibilities Introduction Homeowner Benefits and Responsibilities Benefits of Homeownership Responsibilities of Homeownership Refinancing and Home Equity Preventing Foreclosure

The Post-Crisis World: Where Will Agency MBSs Trade?

The Post-Crisis World: Where Will Agency MBSs Trade? Financial Engineering Practitioners Seminar DEPT. OF INDUSTRIAL ENGINEERING AND OPERATIONS RESEARCH SCHOOL OF ENGINEERING AND APPLIED SCIENCE COLUMBIA

The Post-Crisis World: Where Will Agency MBSs Trade? Financial Engineering Practitioners Seminar DEPT. OF INDUSTRIAL ENGINEERING AND OPERATIONS RESEARCH SCHOOL OF ENGINEERING AND APPLIED SCIENCE COLUMBIA

The United States Economy: Economic Terms and the Global Economy. Mr. Mattingly U.S. History

The United States Economy: Economic Terms and the Global Economy Mr. Mattingly U.S. History Measuring an Economy: GDP Gross Domestic Product (GDP) = total dollar value of all final goods and services produced

The United States Economy: Economic Terms and the Global Economy Mr. Mattingly U.S. History Measuring an Economy: GDP Gross Domestic Product (GDP) = total dollar value of all final goods and services produced

Trends Report Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers

Trends Report 2018 Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers 2018 Alternative Financial Services Lending Trends Overview How subprime borrower behavior

Trends Report 2018 Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers 2018 Alternative Financial Services Lending Trends Overview How subprime borrower behavior

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage Buying your first home is both exhilarating and overwhelming. Stay on top of it all with this step-by-step guide on what to expect

First-time Homebuyer s Guide: Follow These Steps to Get Your First Mortgage Buying your first home is both exhilarating and overwhelming. Stay on top of it all with this step-by-step guide on what to expect

Homeowner Affordability and Stability Plan Fact Sheet

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

How to Stay Relevant in a Disruptive Lending Environment

How to Stay Relevant in a Disruptive Lending Environment Don Arkell CU Lending Advice Friday, June 10, 2016 2:15 p.m. Lending Attitude Check The best lenders learn that lending is both an attitude and

How to Stay Relevant in a Disruptive Lending Environment Don Arkell CU Lending Advice Friday, June 10, 2016 2:15 p.m. Lending Attitude Check The best lenders learn that lending is both an attitude and

Comments on Forecasts

Comments on Forecasts Kenneth T. Rosen The Sky s The Limit Conference and Expo November 3, 2017 Risks to Economic Outlook Tax cuts in a full employment economy and a global synchronized expansion leads

Comments on Forecasts Kenneth T. Rosen The Sky s The Limit Conference and Expo November 3, 2017 Risks to Economic Outlook Tax cuts in a full employment economy and a global synchronized expansion leads

National Debt No Problem - We Owe It To Ourselves - WRONG!

National Debt No Problem - We Owe It To Ourselves - WRONG! June 20, 2018 by Gary Halbert of Halbert Wealth Management 1. Over 40 Years of Writing This Newsletter 2. National Debt Not a Problem We Owe It

National Debt No Problem - We Owe It To Ourselves - WRONG! June 20, 2018 by Gary Halbert of Halbert Wealth Management 1. Over 40 Years of Writing This Newsletter 2. National Debt Not a Problem We Owe It

THC Asset-Liability Management (ALM) Insight Issue 5

Insight Issue 5") , WHOLE LOAN SALE TO AGENCIES: A Strategy key words: risk capacity, G-spread, LLPA, yield attribution, fixed rate 1-4 family mortgage, whole loan pricing THC Asset-Liability Management (ALM) Insight Issue

, WHOLE LOAN SALE TO AGENCIES: A Strategy key words: risk capacity, G-spread, LLPA, yield attribution, fixed rate 1-4 family mortgage, whole loan pricing THC Asset-Liability Management (ALM) Insight Issue

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

1. It s All About Income

1. It s All About Income Loan modification programs are based on one thing, income. The biggest misconception out there is that the bank cares about the type of hardship you have. This myth couldn t be

1. It s All About Income Loan modification programs are based on one thing, income. The biggest misconception out there is that the bank cares about the type of hardship you have. This myth couldn t be

1. Allocates scarce capital among competing uses 2. Spreads/shares risk 3. Facilitates inter-temporal trade

Chapter 2: The Financial System What it is: What it does: A network of financial intermediaries (banks, S&Ls, credit unions, etc.), facilitators (credit rating agencies, appraisers, etc.), and markets

Chapter 2: The Financial System What it is: What it does: A network of financial intermediaries (banks, S&Ls, credit unions, etc.), facilitators (credit rating agencies, appraisers, etc.), and markets

Fannie Mae 2010 First Quarter Credit Supplement. May 10, 2010

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Fannie Mae 2010 First Quarter Credit Supplement May 10, 2010 1 These materials present tables and other information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on

Metro D.C. Monitor. The 20 strongest-performing metro areas

Metro D.C. Monitor Tracking Economic Recession and Recovery in the Greater Washington Region December 2009 Most economists report that the recession is technically over. Gross domestic product returned

Metro D.C. Monitor Tracking Economic Recession and Recovery in the Greater Washington Region December 2009 Most economists report that the recession is technically over. Gross domestic product returned

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q1 2018 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q1 2018 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

Trio is the best solution

Trio is the best solution Why trio exists W H Y T R I O E X I S T S : Here s the reality Approximately 30% of mortgage applicants are denied. The US housing market has high demand for an alternative to

Trio is the best solution Why trio exists W H Y T R I O E X I S T S : Here s the reality Approximately 30% of mortgage applicants are denied. The US housing market has high demand for an alternative to

Non-QM. Qualified Mortgages General QMs. GSE QMs. Agency QMs. Points & Fees 5%

Subprime 2006 No down payment required (80/20) or 100% LTV Average 580 credit score Income stated No reserves Negative Amortization and balloon payments No appraisal requirements Prepayment penalties Exceptions

Subprime 2006 No down payment required (80/20) or 100% LTV Average 580 credit score Income stated No reserves Negative Amortization and balloon payments No appraisal requirements Prepayment penalties Exceptions

Payday and Small-Dollar, High-Cost Installment Loans

Payday and Small-Dollar, High-Cost Installment Loans NCSL August 4, 2015 Seattle, WA Nick Bourke www.pewtrusts.org/small-loans Pew Resources for Understanding the CFPB s Proposal www.pewtrusts.org/small-loans

Payday and Small-Dollar, High-Cost Installment Loans NCSL August 4, 2015 Seattle, WA Nick Bourke www.pewtrusts.org/small-loans Pew Resources for Understanding the CFPB s Proposal www.pewtrusts.org/small-loans

Refinance Report August 2012

This report contains data on refinance program activity of Fannie Mae and Freddie Mac (the Enterprises) through. Report Highlights Refinance volume continued to be strong in August as 30-year mortgage

This report contains data on refinance program activity of Fannie Mae and Freddie Mac (the Enterprises) through. Report Highlights Refinance volume continued to be strong in August as 30-year mortgage

Financial Overview. Discussion Overview 2015 INVESTOR AND ANALYST CONFERENCE. Carol Tomé. Fiscal 2015 Financial Guidance

2015 INVESTOR AND ANALYST CONFERENCE Financial Overview Carol Tomé CFO & Executive Vice President Corporate Services Discussion Overview Fiscal 2015 Financial Guidance Our View of the U.S. Economy and

2015 INVESTOR AND ANALYST CONFERENCE Financial Overview Carol Tomé CFO & Executive Vice President Corporate Services Discussion Overview Fiscal 2015 Financial Guidance Our View of the U.S. Economy and

State of the Automotive Finance Market Third Quarter 2015

State of the Automotive Finance Market Third Quarter 2015 Melinda Zabritski Sr. Director Financial Solutions 2015 2015 Experian Information Solutions, Inc. Inc. All rights All rights reserved. reserved.

State of the Automotive Finance Market Third Quarter 2015 Melinda Zabritski Sr. Director Financial Solutions 2015 2015 Experian Information Solutions, Inc. Inc. All rights All rights reserved. reserved.

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout

Gmac auto loan rate for 72 months

As one of the world's leading and largest graduate business schools, INSEAD brings together people, cultures and ideas to change lives and to transform organisations. Loan Program FY2006 FY2007; Stafford

As one of the world's leading and largest graduate business schools, INSEAD brings together people, cultures and ideas to change lives and to transform organisations. Loan Program FY2006 FY2007; Stafford

WHERE IS THE ECONOMIC RECOVERY?

WHERE IS THE ECONOMIC RECOVERY? June marks the 23 rd month of the United States economic recovery, so the big question is: How is it working for you? If you are in real estate (and many other industries)

WHERE IS THE ECONOMIC RECOVERY? June marks the 23 rd month of the United States economic recovery, so the big question is: How is it working for you? If you are in real estate (and many other industries)

Fourth Quarter 2014 Financial Results Supplement

Fourth Quarter 20 Financial Results Supplement February 19, 2015 Table of contents Financial Results Segment Business Information 2 - Annual Financial Results 12 - Single-Family New Funding Volume 3 -

Fourth Quarter 20 Financial Results Supplement February 19, 2015 Table of contents Financial Results Segment Business Information 2 - Annual Financial Results 12 - Single-Family New Funding Volume 3 -

ABS InduStry MAkeS SenSe OF. LOAn LeveL data

ABS InduStry MAkeS SenSe OF LOAn LeveL data As the market adds data on current borrower behavior to its study of loan performance, traditional tools and models are fast becoming obsolete. 10 Asset Securitization

ABS InduStry MAkeS SenSe OF LOAn LeveL data As the market adds data on current borrower behavior to its study of loan performance, traditional tools and models are fast becoming obsolete. 10 Asset Securitization

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Session Overview. Budgeting Skills Training - Instructor Notes. Thank you for teaching the Budgeting Skills Training Class :D

Session Overview Budgeting Skills Training - Instructor Notes Thank you for teaching the Budgeting Skills Training Class :D The instructor notes contain suggestions for you on how to teach this class.

Session Overview Budgeting Skills Training - Instructor Notes Thank you for teaching the Budgeting Skills Training Class :D The instructor notes contain suggestions for you on how to teach this class.

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

Overview of Types of Mortgages Available

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

State of the Automotive Finance Market

State of the Automotive Finance Market Presented by: Melinda Zabritski Q3 2018 1 Experian Session overview Market Overview Outstanding balances Total risk distributions Delinquency Originations New and

State of the Automotive Finance Market Presented by: Melinda Zabritski Q3 2018 1 Experian Session overview Market Overview Outstanding balances Total risk distributions Delinquency Originations New and

A Closer Look: Credit-risk Transfer to Private Investors

A Closer Look: Credit-risk Transfer to Private Investors Freddie Mac Multifamily s strategy of transferring as much of our credit risk as possible to private investors enables us to fulfill our mission

A Closer Look: Credit-risk Transfer to Private Investors Freddie Mac Multifamily s strategy of transferring as much of our credit risk as possible to private investors enables us to fulfill our mission

Investor Presentation As of June 30, 2018

Investor Presentation As of June 30, 2018 Consumer finance company focused on sub-prime auto market Established in 1991. IPO in 1992 Through June 30, 2018, approximately $14.8 billion in contracts originated

Investor Presentation As of June 30, 2018 Consumer finance company focused on sub-prime auto market Established in 1991. IPO in 1992 Through June 30, 2018, approximately $14.8 billion in contracts originated

Melinda Zabritski, Director of Automotive Credit

State of the Automotive Finance Market Third Quarter 2010 Melinda Zabritski, Director of Automotive Credit 2010 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein

State of the Automotive Finance Market Third Quarter 2010 Melinda Zabritski, Director of Automotive Credit 2010 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein

State of the Automotive Finance Market. Melinda Zabritski Sr. Director Experian Automotive

State of the Automotive Finance Market Melinda Zabritski Sr. Director Experian Automotive Discussion Points What s on the road? Return of the US automotive market Shifting consumer dynamic Overall consumer

State of the Automotive Finance Market Melinda Zabritski Sr. Director Experian Automotive Discussion Points What s on the road? Return of the US automotive market Shifting consumer dynamic Overall consumer

Financial Statements For the year ended June 30, 2017 (Unaudited)

") SHORT-TERM INVESTMENT POOL STATE OF MONTANA BOARD OF INVESTMENTS Financial Statements For the year ended June 30, 2017 (Unaudited) Montana Board of Investment FY17 STIP Unaudited Financial Statements -

SHORT-TERM INVESTMENT POOL STATE OF MONTANA BOARD OF INVESTMENTS Financial Statements For the year ended June 30, 2017 (Unaudited) Montana Board of Investment FY17 STIP Unaudited Financial Statements -

Lesson 13: Applying for a Mortgage Loan

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

GE Capital, CLL Americas

GE Capital, CLL Americas Dan Henson June 9, 2010 This document contains forward-looking statements - that is, statements related to future, not past, events. In this context, forward-looking statements

GE Capital, CLL Americas Dan Henson June 9, 2010 This document contains forward-looking statements - that is, statements related to future, not past, events. In this context, forward-looking statements

The Business of an Investment Bank

APPENDIX I The Business of an Investment Bank Most investment banks have similar functions, though they differ in their exposures to different lines of business. This appendix describes the investment

APPENDIX I The Business of an Investment Bank Most investment banks have similar functions, though they differ in their exposures to different lines of business. This appendix describes the investment

Loan Policy. Including Loan Program Parameters & Underwriting Guidelines. Last Updated 11/30/18

Loan Policy Including Loan Program Parameters & Underwriting Guidelines Last Updated 11/30/18 Commercial Lending X ( CLX ) is a national commercial financing consulting firm. CLX specializes in helping

Loan Policy Including Loan Program Parameters & Underwriting Guidelines Last Updated 11/30/18 Commercial Lending X ( CLX ) is a national commercial financing consulting firm. CLX specializes in helping

Credit Unions: Turning Strong Member Relationships into Market Share

Whitepaper Credit Unions: Turning Strong Member Relationships into Market Share Contents 1 Introduction 2 Getting Started 2 The Top 10 LOS Must-Haves for Credit Unions Built-in Compliance Tools Flexibility

Whitepaper Credit Unions: Turning Strong Member Relationships into Market Share Contents 1 Introduction 2 Getting Started 2 The Top 10 LOS Must-Haves for Credit Unions Built-in Compliance Tools Flexibility

A Publication of Paramount Capital Corporation. Strategy and Insight for the Commercial Real Estate Industry

Volume V Issue 1 A Publication of Paramount Capital Corporation Jan 15, 2013 Strategy and Insight for the Commercial Real Estate Industry A REVIEW AND UPDATE OF OUR PREDICTIONS FOR 2012 AND A DISCUSSION

Volume V Issue 1 A Publication of Paramount Capital Corporation Jan 15, 2013 Strategy and Insight for the Commercial Real Estate Industry A REVIEW AND UPDATE OF OUR PREDICTIONS FOR 2012 AND A DISCUSSION

Statement by. National Association of Local Housing Finance Agencies. to the. Tax Reform Debt, Equity and Capital and Real Estate Working Groups

Officers President Ernestine Garey Atlanta, Georgia Development Authority Vice President Marc Jahr New York, New York Housing Development Corporation Treasurer Ron Williams Houston, Texas Southeast Texas

Officers President Ernestine Garey Atlanta, Georgia Development Authority Vice President Marc Jahr New York, New York Housing Development Corporation Treasurer Ron Williams Houston, Texas Southeast Texas

Lending and Collateral Q&A

November 14, 2017 Note - Each answer in this document is written as if it were a stand-alone response. Therefore, some information may be repeated. What is an advance and how do advances work? The FHLBanks

November 14, 2017 Note - Each answer in this document is written as if it were a stand-alone response. Therefore, some information may be repeated. What is an advance and how do advances work? The FHLBanks

Deutsche Bank 2008 Leveraged Finance Conference September 24, 2008

Deutsche Bank 2008 Leveraged Finance Conference September 24, 2008 Forward-Looking Statements This presentation includes forward-looking statements within the meaning of the Private Securities Litigation

Deutsche Bank 2008 Leveraged Finance Conference September 24, 2008 Forward-Looking Statements This presentation includes forward-looking statements within the meaning of the Private Securities Litigation

Agenda Challenging Year, Great Learnings A Glimpse into 2009 Global Auto Industry GM -- What s s Next

Agenda 2008 -- Challenging Year, Great Learnings A Glimpse into 2009 Global Auto Industry GM -- What s s Next U.S. Housing Statistics Source: Census Bureau / Haver Analytics Source: National Association

Agenda 2008 -- Challenging Year, Great Learnings A Glimpse into 2009 Global Auto Industry GM -- What s s Next U.S. Housing Statistics Source: Census Bureau / Haver Analytics Source: National Association

Bank of America Merrill Lynch 2013 New York Auto Summit March 27, 2013

Bank of America Merrill Lynch 2013 New York Auto Summit March 27, 2013 Forward-Looking Statements This presentation includes forward-looking statements as that term is defined in the Private Securities

Bank of America Merrill Lynch 2013 New York Auto Summit March 27, 2013 Forward-Looking Statements This presentation includes forward-looking statements as that term is defined in the Private Securities

APPENDIX A: GLOSSARY

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

A CFO S GUIDE TO THE STRATEGIC APPLICATIONS OF ACCOUNTS RECEIVABLE INSURANCE. July Sponsored by

A CFO S GUIDE TO THE STRATEGIC APPLICATIONS OF ACCOUNTS RECEIVABLE INSURANCE July 2016 Sponsored by EXECUTIVE SUMMARY Insurance that pays for itself without having to file a claim. That may sound too good

A CFO S GUIDE TO THE STRATEGIC APPLICATIONS OF ACCOUNTS RECEIVABLE INSURANCE July 2016 Sponsored by EXECUTIVE SUMMARY Insurance that pays for itself without having to file a claim. That may sound too good

The Recession

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

Deposit Pricing in Rising Rates Session 1. Three Part Series

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Deposit Pricing in Rising Rates Session 1 Thomas Farin Chairman of the Board tfarin@farin.com 1 Three Part Series Session 1 The Deposit Toolkit Are we already in a rising rate environment? Effective Process

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance