BEYOND THE CREDIT SCORE: The Secondary Mortgage Market

|

|

|

- Thomas O’Brien’

- 5 years ago

- Views:

Transcription

1 BEYOND THE CREDIT SCORE: The Secondary Mortgage Market

2 Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout Illinois. Together we empower communities to thrive through three programs: Organizing, Policy Advocacy, and Training and Technical Assistance. Our members include housing counseling agencies, homeless service providers, developers of affordable housing and policymakers. These organizations serve low- and moderate-income households, helping to provide a place to call home, thereby strengthening the community at large. At Housing Action Illinois our supporters, participants and members agree that a stronger Illinois begins at home. HAI is a HUD Housing Counseling Intermediary with Affiliates in Illinois, Indiana and Missouri. 2

3 AGENDA Explain the purpose of the secondary mortgage market Explain the history of the market Show how secondary market rules impacted housing policy and neighborhoods Show how investor needs impact mortgages and underwriting Explain the role of the secondary market in the housing crash 3

4 The Secondary Mortgage Market 4

5 The Secondary Mortgage Market The Secondary Mortgage Market is where banks sell mortgage loans to investors, which creates liquidity for the origination of new mortgages 5

6 HISTORY OF THE MORTGAGE MARKET 6

and Loan Associations began offering")

7 Early Mortgages Mortgages offered by private companies, including insurers Required up to 50% down payment Often interest only or short-term loans with a balloon payment Limited the number of people who could buy homes Eventually, Building (Savings) and Loan Associations began offering mortgages 7

8 8 Alchetron

9 The Great Depression 9

10 Federal Home Loan Bank 10

11 THE NEW DEAL

12 Homeowners Loan Corporation 12

13 Homeowners Loan Corporation Congress created the Home Owners Loan Corporation to refinance existing home loans. Helped to prevent thousands of families from losing their homes to foreclosure. 13

14 Federal Housing Administration 14

15 Fannie Mae 15

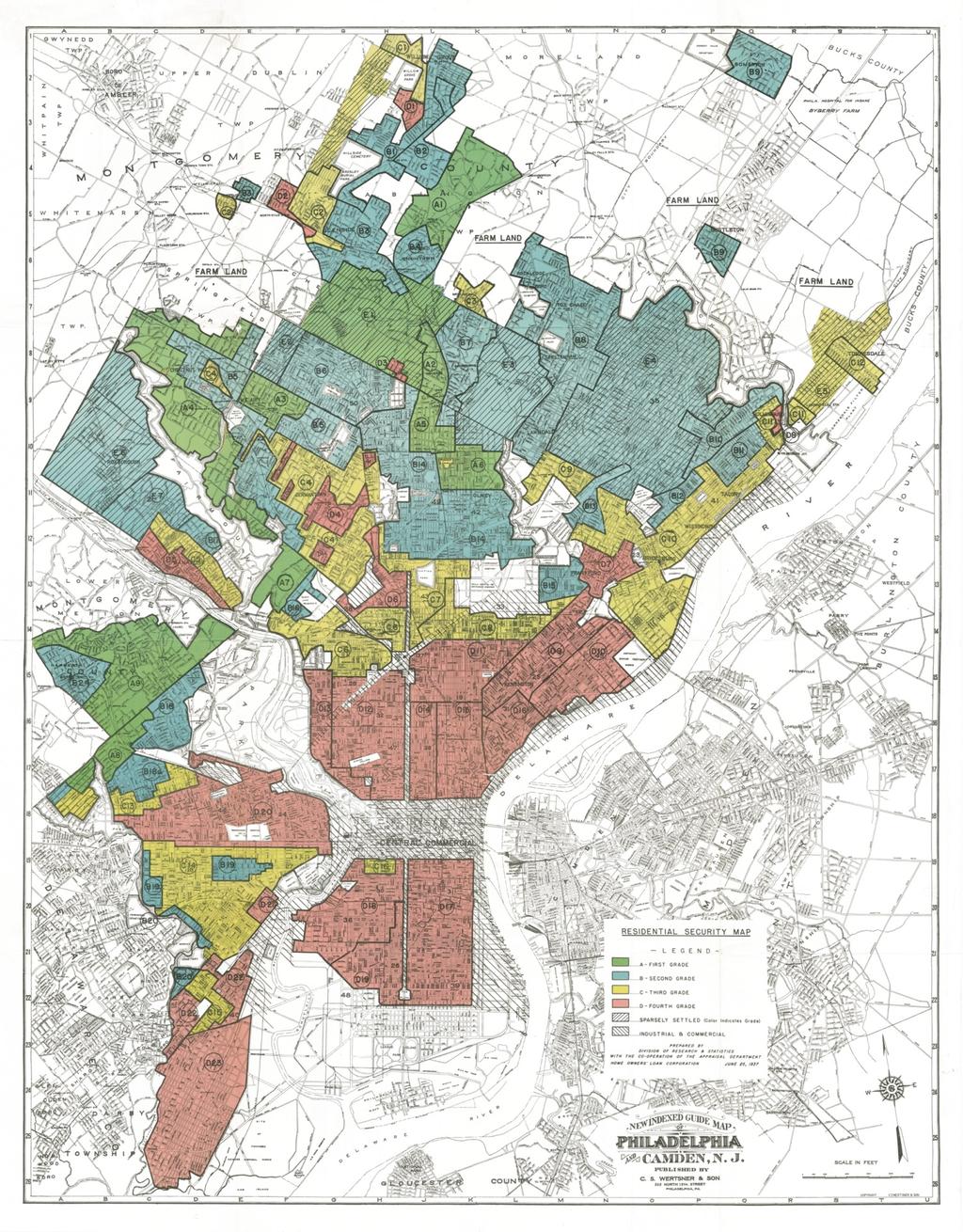

16 Residential Security Maps Home Ownership Loan Corporation hired appraisers to create maps to determine the quality of neighborhoods in 239 cities Neighborhood quality identified by color 16

17 Residential Security Maps Green = Best Blue = Still Desirable Yellow = Definitely Declining Red = Hazardous 17

18 Chicago 18

19 Chicago 19

20 Chicago Note the description for the Washington Park neighborhood. If you were a lender in that era, would you want to lend there? Eventually, the maps created by the Homeowners Loan Corporation and private firms were used by the entire mortgage industry to determine where to lend and how to price products. 20

21 Chicago In Chicago, this contributed to contract buying and other abuses that continue to impact many Chicago neighborhoods 21

22 MANHATTAN, NEW YORK 22

23 MANHATTAN, NEW YORK Credit: Mapping Inequality 23

24 New Orleans 24

25 Philadelphia 25

26 Aurora, Illinois 26

27 27

28 Ginnie Mae 28

29 The Rise of the Secondary Market 29

30 Fannie Mae Goes Private 30

31 Ginnie Mae 31

32 Freddie Mac 32

33 Conforming Mortgages 33

34 Alt-A Mortgages 34

35 Sub Prime Mortgages 35

36 Mortgage Backed Securities 36

37 37 Credit: Massachusetts Real Estate Law Blog

38 Collateralized Debt Obligations Type of security often composed of the riskier portions of mortgagebacked securities. 38

39 Credit Default Swaps A type of credit derivative allowing a purchaser of the swap to transfer loan default risk to a seller of the swap. The seller agrees to pay the purchaser if a default event occurs. The purchaser does not need to own the loan covered by the swap. 39

40 Credit Default Swaps Credit: Goldonomic 40

41 Credit Default Swaps Credit: The Cagle Post 41

42 Synthetic Credit Default Obligation A CDO that holds credit default swaps that reference assets (rather than holding cash assets), allowing investors to make bets for or against those referenced assets. 42

43 43

44 Private Label Securitization 44

45 Private Label Securitization 45

46 All this financial creativity was a lot like cheap sangria, said Michael Mayo, a managing director and financial services analyst at Calyon Securities (USA) Inc. A lot of cheap ingredients repackaged to sell at a premium, he told the Commission. It might taste good for a while, but then you get headaches later and you have no idea what s really inside. Financial Crisis Inquiry Commission Report 46

47 Foreclosure Crisis 47

48 48 Credit: Decoded Science

49 Foreclosure Crisis Starting in mid 2007, global financial markets began to experience serious liquidity challenges related mainly to rising concerns about U.S. mortgage credit quality. As home prices fell, recently originated subprime and nontraditional mortgage loans began to default at record rates. These developments led to growing concerns about the value of financial positions in mortgage-backed securities and related derivative instruments held by major financial institutions in the U.S. and around the world. The difficulty in determining the value of mortgage-related assets and, therefore, the balance-sheet strength of large banks and non-bank financial institutions ultimately led these institutions to become wary of lending to one another, even on a short-term basis. Prepared testimony of FDIC Chair Sheila Bair to FCIC, 9/2/

50 Foreclosure Crisis 50

51 The Present 51

52 The Present FHA Fannie and Freddie Fintech = Financial Technology Private Label Security Credit Box Remains Tight in Conforming Market Lenders using Portfolio Products to Serve Non-Conforming Buyers 52

53 The Present 53

54 The Present Chicago Reader Zakkiyyah Najeebah 54

55 QUESTIONS??? DAVID YOUNG P: (312) EXT. 202

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

6/21/2013. Section I. Purpose of Course. History and Overview of Mortgage Law, Regulation and Requirements

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

APPENDIX A: GLOSSARY

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

Financing Residential Real Estate. Lesson 11: FHA-Insured Loans

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

Financing Residential Real Estate Lesson 11: FHA-Insured Loans Introduction In this lesson we will cover: FHA loan programs, rules for FHA loans (including those governing maximum loan amounts, the minimum

An Overview of the Housing Finance System in the United States

An Overview of the Housing Finance System in the United States Sean M. Hoskins Analyst in Financial Economics Katie Jones Analyst in Housing Policy N. Eric Weiss Specialist in Financial Economics March

An Overview of the Housing Finance System in the United States Sean M. Hoskins Analyst in Financial Economics Katie Jones Analyst in Housing Policy N. Eric Weiss Specialist in Financial Economics March

Homeowner Affordability and Stability Plan Fact Sheet

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

The Mortgage Industry

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Printable Lesson Materials

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

M E M O R A N D U M Financial Crisis Inquiry Commission

M E M O R A N D U M Financial Crisis Inquiry Commission To: From: Commissioners Ron Borzekowski Wendy Edelberg Date: July 7, 2010 Re: Analysis of housing data As is well known, the rate of serious delinquency

M E M O R A N D U M Financial Crisis Inquiry Commission To: From: Commissioners Ron Borzekowski Wendy Edelberg Date: July 7, 2010 Re: Analysis of housing data As is well known, the rate of serious delinquency

The US Housing Market Crisis and Its Aftermath

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

The Current Real Estate Finance Climate

The Current Real Estate Finance Climate Elizabeth J. Zook, Esq. Carruthers & Roth, P.A. (336) 478-1110 December 10, 2008 Residenti tial Housing Market Subprime Mortgage Crisis i Ongoing financial crisis

The Current Real Estate Finance Climate Elizabeth J. Zook, Esq. Carruthers & Roth, P.A. (336) 478-1110 December 10, 2008 Residenti tial Housing Market Subprime Mortgage Crisis i Ongoing financial crisis

1 Anthony B. Sanders, Ph.D. is Professor of Finance at the School of Management at George Mason University

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

FORECLOSURES, FHA, VA AND PURCHASE MONEY MORTGAGES

Chapter 2 we will take a quick look at foreclosures before moving on to various forms of financing. CHAPTER 2 FORECLOSURES, FHA, VA AND PURCHASE MONEY MORTGAGES CHAPTER LEARNING OBJECTIVES Upon completion

Chapter 2 we will take a quick look at foreclosures before moving on to various forms of financing. CHAPTER 2 FORECLOSURES, FHA, VA AND PURCHASE MONEY MORTGAGES CHAPTER LEARNING OBJECTIVES Upon completion

Hearing on The Housing Decline: The Extent of the Problem and Potential Remedies December 13, 2007

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

More on Mortgages. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES ACUIA Region 3 Meeting Presented by: Bob Parks, CPA Director, Financial Institutions Group Overview Mortgage market and credit union trends

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES ACUIA Region 3 Meeting Presented by: Bob Parks, CPA Director, Financial Institutions Group Overview Mortgage market and credit union trends

Mortgage Market Statistical Annual 2017 Yearbook. Table of Contents

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Overview of Mortgage Lending

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Testimony of Keith Johnson. Former President of Clayton Holdings, Inc. and. Former President of Washington Mutual s Long Beach Mortgage

Testimony of Keith Johnson Former President of Clayton Holdings, Inc. and Former President of Washington Mutual s Long Beach Mortgage Before the Financial Crisis Inquiry Commission September 23, 2010 Chairman

Testimony of Keith Johnson Former President of Clayton Holdings, Inc. and Former President of Washington Mutual s Long Beach Mortgage Before the Financial Crisis Inquiry Commission September 23, 2010 Chairman

6/18/2015. Residential Mortgage Types and Borrower Decisions. Role of the secondary market Mortgage types:

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Why is the Country Facing a Financial Crisis?

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Testimony of Michael D. Calhoun President, Center for Responsible Lending. Before the House Committee on Financial Services

Testimony of Michael D. Calhoun President, Center for Responsible Lending Before the House Committee on Financial Services Hearing: A Legislative Proposal to Protect American Taxpayers and Homeowners by

Testimony of Michael D. Calhoun President, Center for Responsible Lending Before the House Committee on Financial Services Hearing: A Legislative Proposal to Protect American Taxpayers and Homeowners by

homeownership rental housing business finance colorado housing and finance authority annual financial report

homeownership rental housing business finance colorado housing and finance authority annual financial report December 31, 2017 and 2016 COLORADO HOUSING AND FINANCE AUTHORITY Annual Financial Report Table

homeownership rental housing business finance colorado housing and finance authority annual financial report December 31, 2017 and 2016 COLORADO HOUSING AND FINANCE AUTHORITY Annual Financial Report Table

Small Multifamily Building Risk Share Initiative Request for Comment [Docket No FR 5728 N 01]

![Small Multifamily Building Risk Share Initiative Request for Comment [Docket No FR 5728 N 01]](/thumbs/94/122321777.jpg "Small Multifamily Building Risk Share Initiative Request for Comment [Docket No FR 5728 N 01]") January 3, 2014 To: Re: Regulations Division, Office of General Counsel Department of Housing and Urban Development 451 7th Street SW, Room 10276 Washington, DC 20410 0500 Small Multifamily Building Risk

January 3, 2014 To: Re: Regulations Division, Office of General Counsel Department of Housing and Urban Development 451 7th Street SW, Room 10276 Washington, DC 20410 0500 Small Multifamily Building Risk

Chapter 11 11/18/2014. Mortgages and Mortgage Markets. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

11/9/2017. Chapter 11. Mortgages and Mortgage Markets. Traditional and Modern Housing Finance: From S&Ls to Securities. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Exhibit 3 with corrections through Memorandum

Exhibit 3 with corrections through 4.21.10 Memorandum High LTV, Subprime and Alt-A Originations Over the Period 1992-2007 and Fannie, Freddie, FHA and VA s Role Edward Pinto Consultant to mortgage-finance

Exhibit 3 with corrections through 4.21.10 Memorandum High LTV, Subprime and Alt-A Originations Over the Period 1992-2007 and Fannie, Freddie, FHA and VA s Role Edward Pinto Consultant to mortgage-finance

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

NATIONAL ASSOCIATION OF REALTORS

NATIONAL ASSOCIATION OF REALTORS The Voice for Real Estate 430 North Michigan Avenue Chicago, Illinois 60611-4087 312.329.8411 Fax 312.329.5962 Visit us at www.realtor.org. 222 St Joseph Avenue Long Beach,

NATIONAL ASSOCIATION OF REALTORS The Voice for Real Estate 430 North Michigan Avenue Chicago, Illinois 60611-4087 312.329.8411 Fax 312.329.5962 Visit us at www.realtor.org. 222 St Joseph Avenue Long Beach,

Executive Summary Chapter 1. Conceptual Overview and Study Design

Executive Summary Chapter 1. Conceptual Overview and Study Design The benefits of homeownership to both individuals and society are well known. It is not surprising, then, that policymakers have adopted

Executive Summary Chapter 1. Conceptual Overview and Study Design The benefits of homeownership to both individuals and society are well known. It is not surprising, then, that policymakers have adopted

The Current Foreclosure Crisis Trends and Roadblocks to Recovery

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

Fannie, Freddie, and Housing Finance: What s It All About?

Fannie, Freddie, and Housing Finance: What s It All About? Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation to the Central Banking Seminar, Federal Reserve

Fannie, Freddie, and Housing Finance: What s It All About? Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation to the Central Banking Seminar, Federal Reserve

TESTIMONY OF BRUCE MARKS. Chief Executive Officer. Neighborhood Assistance Corporation of America (NACA)

") TESTIMONY OF BRUCE MARKS Chief Executive Officer Neighborhood Assistance Corporation of America (NACA) My name is Bruce Marks. I am Chief Executive Officer of the Neighborhood Assistance Corporation of

TESTIMONY OF BRUCE MARKS Chief Executive Officer Neighborhood Assistance Corporation of America (NACA) My name is Bruce Marks. I am Chief Executive Officer of the Neighborhood Assistance Corporation of

Federal Reserve System Primary Market Secondary Market

Chapter 14: Real Estate Financing: Practices Introduction to the Real Estate Financing Market Federal Reserve System Primary Market Secondary Market Federal Reserve System Role Maintain sound credit conditions

Chapter 14: Real Estate Financing: Practices Introduction to the Real Estate Financing Market Federal Reserve System Primary Market Secondary Market Federal Reserve System Role Maintain sound credit conditions

Exhibit 2 with corrections through Memorandum

Exhibit 2 with corrections through 10.11.10 Memorandum Sizing Total Federal Government and Federal Agency Contributions to Subprime and Alt- A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto

Exhibit 2 with corrections through 10.11.10 Memorandum Sizing Total Federal Government and Federal Agency Contributions to Subprime and Alt- A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto

Oral Testimony of Ann Fulmer. V.P. Business Relations, Interthinx, Inc., a Verisk Analytics Company. Before the Financial Crisis Inquiry Commission

Oral Testimony of Ann Fulmer V.P. Business Relations, Interthinx, Inc., a Verisk Analytics Company Before the Financial Crisis Inquiry Commission September 21, 2010 Miami Mr. Chairman, Mr. Vice Chairman,

Oral Testimony of Ann Fulmer V.P. Business Relations, Interthinx, Inc., a Verisk Analytics Company Before the Financial Crisis Inquiry Commission September 21, 2010 Miami Mr. Chairman, Mr. Vice Chairman,

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

The Financial Crisis and the Bailout

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity The National Council of State Housing Agencies (NCSHA) and the state Housing Finance Agencies

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity The National Council of State Housing Agencies (NCSHA) and the state Housing Finance Agencies

Econ 330 Exam 2 Name ID Section Number

Econ 330 Exam 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When financial institutions go on a lending spree and expand

Econ 330 Exam 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When financial institutions go on a lending spree and expand

RE: The Federal Housing Finance Agency s proposed housing goals for Fannie Mae and Freddie Mac for

CENTER FOR COMMUNITY CAPITAL UNIVERSITY OF NORTH CAROLINA AT CHAPEL HILL Dr. Roberto G. Quercia, Director 1700 Martin Luther King Blvd Janneke H. Ratcliffe, Executive Director CB 3452 Ste 129 Room 128

CENTER FOR COMMUNITY CAPITAL UNIVERSITY OF NORTH CAROLINA AT CHAPEL HILL Dr. Roberto G. Quercia, Director 1700 Martin Luther King Blvd Janneke H. Ratcliffe, Executive Director CB 3452 Ste 129 Room 128

AUDITED FINANCIAL STATEMENTS

AUDITED FINANCIAL STATEMENTS For the years ended June 30, 2010 and 2009 Audited Financial Statements WEST VIRGINIA HOUSING DEVELOPMENT FUND For the Years Ended June 30, 2010 and 2009 Audited Financial

AUDITED FINANCIAL STATEMENTS For the years ended June 30, 2010 and 2009 Audited Financial Statements WEST VIRGINIA HOUSING DEVELOPMENT FUND For the Years Ended June 30, 2010 and 2009 Audited Financial

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission About the Housing Commission Created by the Bipartisan Policy Center, a non-profit

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission About the Housing Commission Created by the Bipartisan Policy Center, a non-profit

Table of Contents. Book 1. Book 4. Book 2. Book 5. Book 3. The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs

1 Table of Contents Book 1 The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs Book 2 Taking the Loan Application Book 3 Processing the Loan Automated Underwriting Uniform

1 Table of Contents Book 1 The Mortgage Cycle & Its Key Players Regulatory Compliance Loan Types & Programs Book 2 Taking the Loan Application Book 3 Processing the Loan Automated Underwriting Uniform

1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application.

GLOSSARY 1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application. Acceptance A verbal or written acceptance of an offer to buy

GLOSSARY 1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application. Acceptance A verbal or written acceptance of an offer to buy

REAL ESTATE TERMS Acceleration: Adjustable-Rate Mortgage (ARM): Adjusted Basis: Adjustment Date: Adjustment Interval: Adjustment Period:

: Adjusted Basis: Adjustment Date: Adjustment Interval: Adjustment Period:") REAL ESTATE TERMS A Acceleration: The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgager (borrower), or by using the right

REAL ESTATE TERMS A Acceleration: The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgager (borrower), or by using the right

Basics in Mortgage Lending Test for Loan Officers

Basics in Mortgage Lending Test for Loan Officers Name: Date: Company Name: 1. The purpose of the Equal Credit Opportunity Act is: To discourage predatory lending To create new avenues and programs for

Basics in Mortgage Lending Test for Loan Officers Name: Date: Company Name: 1. The purpose of the Equal Credit Opportunity Act is: To discourage predatory lending To create new avenues and programs for

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

Broker. Financing Real Estate. Chapter 12. Copyright Gold Coast Schools 1

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

THE POLICY RESPONSE TO FORECLOSURES:

THE POLICY RESPONSE TO FORECLOSURES: WHAT CAN STATE AND LOCAL ACTORS DO? PRESENTATION TO THE MISSOURI HOMEOWNERSHIP PRESERVATION SUMMIT JANUARY 14, 2010 JEFFERSON CITY, MISSOURI Spillover Effects of Foreclosures

THE POLICY RESPONSE TO FORECLOSURES: WHAT CAN STATE AND LOCAL ACTORS DO? PRESENTATION TO THE MISSOURI HOMEOWNERSHIP PRESERVATION SUMMIT JANUARY 14, 2010 JEFFERSON CITY, MISSOURI Spillover Effects of Foreclosures

Craig Nickerson, National Community Stabilization Trust (NCST) Rob Grossinger, Enterprise Community Partners (Enterprise)

Rob Grossinger, Enterprise Community Partners (Enterprise)") Presenters Host: National Development Council Moderator: TBD Presenters: Craig Nickerson, National Community Stabilization Trust (NCST) Rob Grossinger, Enterprise Community Partners (Enterprise) 2 NSP

Presenters Host: National Development Council Moderator: TBD Presenters: Craig Nickerson, National Community Stabilization Trust (NCST) Rob Grossinger, Enterprise Community Partners (Enterprise) 2 NSP

Fannie Mae Reports Third-Quarter 2011 Results

Contact: Number: Katherine Constantinou 202-752-5403 5552a Resource Center: 1-800-732-6643 Date: November 8, 2011 Fannie Mae Reports Third-Quarter 2011 Results Company Focused on Providing Liquidity to

Contact: Number: Katherine Constantinou 202-752-5403 5552a Resource Center: 1-800-732-6643 Date: November 8, 2011 Fannie Mae Reports Third-Quarter 2011 Results Company Focused on Providing Liquidity to

Fannie Mae and Freddie Mac. Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons

Fannie Mae and Freddie Mac Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons Origins of Fannie Mae Great Depression New Deal Personal income, tax revenue, profits, and prices all drop

Fannie Mae and Freddie Mac Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons Origins of Fannie Mae Great Depression New Deal Personal income, tax revenue, profits, and prices all drop

Fannie Mae and Freddie Mac the two federally

Fannie Mae, Freddie Mac, and Housing Finance Reform By Sarah Mickelson, Director, Public Policy and Elayne Weiss, Senior Policy Analyst, National Low Income Housing Coalition See also: National Housing

Fannie Mae, Freddie Mac, and Housing Finance Reform By Sarah Mickelson, Director, Public Policy and Elayne Weiss, Senior Policy Analyst, National Low Income Housing Coalition See also: National Housing

Table of Contents. Sample

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 5 2.1 INTERNAL CONTROLS... 5

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 5 2.1 INTERNAL CONTROLS... 5

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer August 2016 Community Reinvestment Act (CRA) a Brief History 2 Community Reinvestment Act (CRA) The Community Reinvestment Act (CRA) Brief

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer August 2016 Community Reinvestment Act (CRA) a Brief History 2 Community Reinvestment Act (CRA) The Community Reinvestment Act (CRA) Brief

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions. Ingrid Gould Ellen

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

The Mortgage and Housing Market Outlook

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

Your Guide to Home Financing

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

S&P/Case Shiller index

S&P/Case Shiller index Home price index Index Jan. 2000=100, 3 month ending 240 220 200 180 160 10-metro composite 140 120 20-metro composite 100 80 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

S&P/Case Shiller index Home price index Index Jan. 2000=100, 3 month ending 240 220 200 180 160 10-metro composite 140 120 20-metro composite 100 80 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE. SUBJECT: Home Loan Program 2012 Mid-Year Report CONSENT: X ATTACHMENT(S): 1

: 1") TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE SUBJECT: Home Loan Program 2012 Mid-Year Report ITEM NUMBER: 4c CONSENT: X ATTACHMENT(S): 1 ACTION: DATE OF MEETING: September 7, 2012 INFORMATION: X PRESENTER(S):

TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE SUBJECT: Home Loan Program 2012 Mid-Year Report ITEM NUMBER: 4c CONSENT: X ATTACHMENT(S): 1 ACTION: DATE OF MEETING: September 7, 2012 INFORMATION: X PRESENTER(S):

New Lending Rules. Copyright 2014 The CE Shop. All rights reserved. 1

New Lending Rules In this session we re going to be talking about some new lending guidelines and some new forms that will impact your clients, said Mike. We ll see how that fits in with the title of the

New Lending Rules In this session we re going to be talking about some new lending guidelines and some new forms that will impact your clients, said Mike. We ll see how that fits in with the title of the

Financing Residential Real Estate. Conventional Financing

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of a conventional loan, qualifying standards

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of a conventional loan, qualifying standards

NAR Research on the Impact of Jumbo Mortgage Credit Crunch

NAR Research on the Impact of Jumbo Mortgage Credit Crunch Introduction Mortgage rates are at 50 year lows, thereby raising housing affordability conditions to all-time high levels. However, the historically

NAR Research on the Impact of Jumbo Mortgage Credit Crunch Introduction Mortgage rates are at 50 year lows, thereby raising housing affordability conditions to all-time high levels. However, the historically

Comments on Forecasts

Comments on Forecasts Kenneth T. Rosen The Sky s The Limit Conference and Expo November 3, 2017 Risks to Economic Outlook Tax cuts in a full employment economy and a global synchronized expansion leads

Comments on Forecasts Kenneth T. Rosen The Sky s The Limit Conference and Expo November 3, 2017 Risks to Economic Outlook Tax cuts in a full employment economy and a global synchronized expansion leads

Government-Sponsored Enterprises and Financial Stability

Government-Sponsored Enterprises and Financial Stability Wayne Passmore Federal Reserve Board GSE Workshop April 27, 2017 The views expressed are the author s and should not be interpreted as representing

Government-Sponsored Enterprises and Financial Stability Wayne Passmore Federal Reserve Board GSE Workshop April 27, 2017 The views expressed are the author s and should not be interpreted as representing

The Federal Reserve s HOEPA Proposal and Subprime Related Legislation by. Locke Lord Bissell & Liddell LLP Barnett Sivon & Natter P.C.

The Federal Reserve s HOEPA Proposal and Subprime Related Legislation by Charlotte M. Bahin Raymond Natter Locke Lord Bissell & Liddell LLP Barnett Sivon & Natter P.C. After receiving significant pressure

The Federal Reserve s HOEPA Proposal and Subprime Related Legislation by Charlotte M. Bahin Raymond Natter Locke Lord Bissell & Liddell LLP Barnett Sivon & Natter P.C. After receiving significant pressure

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

The Mortgage Debt Market: A Tragedy

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Lesson 13: Applying for a Mortgage Loan

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

NAHB Resolution. Comprehensive Framework for Housing Finance System Reform Housing Finance Committee

Resolution No. 5 Date: City: Las Vegas, NV NAHB Resolution Title: Sponsor: Submitted by: Housing Finance Committee Michael Fink WHEREAS, the Housing Act of 1949 established a national over-arching policy

Resolution No. 5 Date: City: Las Vegas, NV NAHB Resolution Title: Sponsor: Submitted by: Housing Finance Committee Michael Fink WHEREAS, the Housing Act of 1949 established a national over-arching policy

Memorandum. Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS. Economics 134 Spring 2018 Professor David Romer LECTURE 19

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES

DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES") THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R. 3221 (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES Subtitle A Improvement of Safety and Soundness Supervision. Establishes

THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R. 3221 (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES Subtitle A Improvement of Safety and Soundness Supervision. Establishes

Homeownership Preservation in Maryland

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crisis Inquiry Commission Hearing on

January 27, 2010 Vi. FcdEx Phil Angclides C/Jairmnll Mr. Michael C. Mayo US Banking and Financial Analyst Calyon Securities (USA) Inc 1301 Avenue of the Americas New York, NY 10019 Hon. Bill Thomas Vice

January 27, 2010 Vi. FcdEx Phil Angclides C/Jairmnll Mr. Michael C. Mayo US Banking and Financial Analyst Calyon Securities (USA) Inc 1301 Avenue of the Americas New York, NY 10019 Hon. Bill Thomas Vice

Economic and Banking Outlook. Major issues

/1/9 Economic and Banking Outlook May 9 Major issues Consumer spending recovering? Investment t spending lagging? Housing inventories will take years to clear Bank credit losses will remain high through

/1/9 Economic and Banking Outlook May 9 Major issues Consumer spending recovering? Investment t spending lagging? Housing inventories will take years to clear Bank credit losses will remain high through

February 5, Dear Secretary Geithner:

The Honorable Timothy F. Geithner Secretary of the Treasury U.S. Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Dear Secretary Geithner: The Mortgage Bankers Association 1

The Honorable Timothy F. Geithner Secretary of the Treasury U.S. Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Dear Secretary Geithner: The Mortgage Bankers Association 1

U.S. Residential. Mortgage Default. Performance Update. & Market Analysis

2016 U.S. U.S. RESIDENTIAL MORTGAGE DEFAULT PERFORMANCE UPDATE & MARKET ANALYSIS The residential mortgage servicing industry is worlds away from where it was six years ago at the peak of the housing crisis,

2016 U.S. U.S. RESIDENTIAL MORTGAGE DEFAULT PERFORMANCE UPDATE & MARKET ANALYSIS The residential mortgage servicing industry is worlds away from where it was six years ago at the peak of the housing crisis,

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom?

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

FINANCING THE LOAN/MORTGAGE SEQUENCE

THE LOAN/MORTGAGE SEQUENCE FINANCING 1. Buyer applies to lender - Savings Associations, Mutual Savings Banks, Cooperative Banks, Commercial Banks (the Thrifts); Mortgage Companies, Credit Unions, Life

THE LOAN/MORTGAGE SEQUENCE FINANCING 1. Buyer applies to lender - Savings Associations, Mutual Savings Banks, Cooperative Banks, Commercial Banks (the Thrifts); Mortgage Companies, Credit Unions, Life

Loan Comparison Report. Sample

Loan Comparison Report Prepared for: Jonny Williams Date: Prepared by: April 14, 2008 Taylor Abegg Phone: 801-225-4120 E-mail: TJAbegg@EverySingleHome.com Dear Jonny Williams Attached is the Loan Comparison

Loan Comparison Report Prepared for: Jonny Williams Date: Prepared by: April 14, 2008 Taylor Abegg Phone: 801-225-4120 E-mail: TJAbegg@EverySingleHome.com Dear Jonny Williams Attached is the Loan Comparison

Jan. 8, 2009 Page 1 of 6. C.A.R. Mortgage Update

C.A.R. Mortgage Update This week s C.A.R. Mortgage Update contains information about FHA loans, falling mortgage rates, downpayment assistance programs (DAPs), jumbo loans, mortgage securities, and IndyMac

C.A.R. Mortgage Update This week s C.A.R. Mortgage Update contains information about FHA loans, falling mortgage rates, downpayment assistance programs (DAPs), jumbo loans, mortgage securities, and IndyMac

For Immediate Release Tuesday, December 16, 2003 Jack Gillis,

For Immediate Release Contact Tuesday, December 16, 2003 Jack Gillis, 202-737-0766 STUDY CONCLUDES THAT HOMEOWNERSHIP IS THE MAIN PATH TO WEALTH FOR LOWER INCOME AND MINORITY AMERICANS America Saves Campaign

For Immediate Release Contact Tuesday, December 16, 2003 Jack Gillis, 202-737-0766 STUDY CONCLUDES THAT HOMEOWNERSHIP IS THE MAIN PATH TO WEALTH FOR LOWER INCOME AND MINORITY AMERICANS America Saves Campaign

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

Welcome! Credit Scoring and Sub-Prime Lending

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

20 Hour SAFE Comprehensive: Financing Residential Real Estate

20 Hour SAFE Comprehensive: Financing Residential Real Estate COURSE MANUAL Days 1-4 Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director 9/16 NMLS Rules of Conduct for Students (ROC) Day 1 Real

20 Hour SAFE Comprehensive: Financing Residential Real Estate COURSE MANUAL Days 1-4 Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director 9/16 NMLS Rules of Conduct for Students (ROC) Day 1 Real

Subprime: Tentacles. How could a modest increase in. of a Crisis

Run on the United Kingdom s Northern Rock bank, a fallout from the U.S. subprime crisis. Subprime: Tentacles of a Crisis Randall Dodd How could a modest increase in seriously delinquent subprime mortgages,

Run on the United Kingdom s Northern Rock bank, a fallout from the U.S. subprime crisis. Subprime: Tentacles of a Crisis Randall Dodd How could a modest increase in seriously delinquent subprime mortgages,

solid, established, reliable - since 1959 All appraisals must be ordered through Nationwide Property & Appraisal Services

Conforming Overlays solid, established, reliable - since 1959 1/5/17 All appraisals must be ordered through Nationwide Property & Appraisal Services All loans must be DU underwritten and receive an Approve

Conforming Overlays solid, established, reliable - since 1959 1/5/17 All appraisals must be ordered through Nationwide Property & Appraisal Services All loans must be DU underwritten and receive an Approve

Reducing Foreclosures & Blight Restoring Community Wealth A Local Solution

Reducing Foreclosures & Blight Restoring Community Wealth A Local Solution The Damage Done 4.5 Million Homes Lost Since Sept 08 (CoreLogic Report) Latino household wealth decreased by 66%* * Pew Institute

Reducing Foreclosures & Blight Restoring Community Wealth A Local Solution The Damage Done 4.5 Million Homes Lost Since Sept 08 (CoreLogic Report) Latino household wealth decreased by 66%* * Pew Institute

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance Prof. Stijn Van Nieuwerburgh New York University Stern School of Business March 1, 2011 Published by Princeton University

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance Prof. Stijn Van Nieuwerburgh New York University Stern School of Business March 1, 2011 Published by Princeton University

2014 Freddie Mac and Fannie Mae. All Rights Reserved. MISMO is a registered trademark of the Mortgage Industry Standards Maintenance Organization.

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Closing Disclosure with Numbers Non-Seller Transaction Document Version 1.1 July 15, 2014 In support of the

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Closing Disclosure with Numbers Non-Seller Transaction Document Version 1.1 July 15, 2014 In support of the

Chapter 13 Multiple Choice Questions

Chapter 13 Multiple Choice Questions / Page 1 Chapter 13 Multiple Choice Questions 1. The primary difference between a secured and unsecured loan is a. whether or not the lender charges interest on the

Chapter 13 Multiple Choice Questions / Page 1 Chapter 13 Multiple Choice Questions 1. The primary difference between a secured and unsecured loan is a. whether or not the lender charges interest on the

Lending and Collateral Q&A

November 14, 2017 Note - Each answer in this document is written as if it were a stand-alone response. Therefore, some information may be repeated. What is an advance and how do advances work? The FHLBanks

November 14, 2017 Note - Each answer in this document is written as if it were a stand-alone response. Therefore, some information may be repeated. What is an advance and how do advances work? The FHLBanks

Mortgage Insurance What Have We Learned? (Part 2)

") Mortgage Insurance What Have We Learned? (Part 2) Prepared for: Prepared by: Date: CAS Special Interest Seminar Chicago, IL Michael A. Henk, FCAS, MAAA Consulting Actuary October 1, 2013 Anti-Trust Notice

Mortgage Insurance What Have We Learned? (Part 2) Prepared for: Prepared by: Date: CAS Special Interest Seminar Chicago, IL Michael A. Henk, FCAS, MAAA Consulting Actuary October 1, 2013 Anti-Trust Notice

e-brief Not Here? Housing Market Policy and the Risk of a Housing Bust

e-brief August 31, 2010 FINANCIAL SERVICES Not Here? Housing Market Policy and the Risk of a Housing Bust By Jim MacGee Can a US-style housing bust happen in Canada? Recent swings in Canadian house prices

e-brief August 31, 2010 FINANCIAL SERVICES Not Here? Housing Market Policy and the Risk of a Housing Bust By Jim MacGee Can a US-style housing bust happen in Canada? Recent swings in Canadian house prices