Fannie Mae and Freddie Mac. Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons

|

|

|

- Albert Lynch

- 5 years ago

- Views:

Transcription

1 Fannie Mae and Freddie Mac Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons

2

3 Origins of Fannie Mae

4 Great Depression New Deal Personal income, tax revenue, profits, and prices all drop International trade drops by more than 50% U.S. unemployment at 25% Herbert Hoover laissez-faire approach to the economy Rely on businesses to voluntarily keep the economy stable Some attempts at reform Federal Home Loan Bank Act - new home construction Emergency Relief and Construction Act (ERA) - public works programs Reforms fell short, but laid some framework for New Deal

5 New Deal Franklin Delano Roosevelt elected in 1932 Promised to bring U.S. out of Great Depression New Deal Collection of federal programs, public work projects, and financial reforms/regulations Three R s: Relief, Recovery, Reform Bank Holiday to restabilize banks with help from federal supervision Led to federal insurance of deposits - Federal Deposit Insurance Corporation (FDIC)

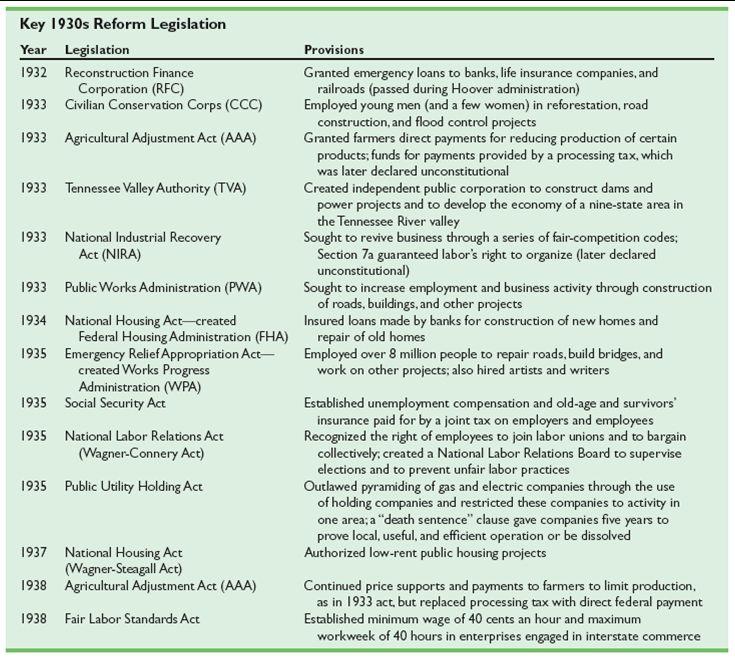

6 Famous New Deal Legislation Who knows some examples?

7

8 Fannie Mae Federal National Mortgage Association (FNMA) Part of Second New Deal - Founded in 1938 Purpose: Expand secondary mortgage market Securitize mortgages through mortgage-backed securities (MBS) Allows lenders to reinvest assets into more lending Increases the number of lenders in the mortgage market by reducing reliance on locally-based savings and loan associations/thrifts Fannie Mae would buy mortgages from lenders to free up capital that could go to borrowers

9 History Great Depression caused chaos in the housing market In 1933, 20% to 25% of U.S. s outstanding mortgage debt was in default Fannie Mae was created by amendments to the National Housing Act First chartered as National Mortgage Association of Washington Gives local banks federal money to finance home mortgages Attempted to increase amount of home ownership and the availability of affordable housing Could buy and sell mortgages

10 Monopoly over Secondary Mortgage Market Federal government wanted to facilitate home mortgages Energize residential construction industry Provide housing for citizens Rejuvenate lending institutions by stimulating cash flow for new loans Formed liquid secondary mortgage market Fannie Mae bought insured mortgages from the Federal Housing Administration (FHA) from private lenders Would either keep the mortgages in own portfolio or sell to private investors Leads to formation of liquid secondary mortgage market

11 Benefits Private lenders more confident about making FHA-insured mortgages Lenders assured that they could turn the mortgages into cash if needed Leads to more inclined to extend mortgage credit Smooth out housing market between capital-rich and capital-poor areas Buy and sell loans across the country through Fannie Mae

12 Fannie Mae s Operations

13 1949 Expansion of Fannie Mae In 1949, Fannie Mae began buying and selling loans guaranteed by the Veterans Administration (VA). Whereas the association purchased 6,734 loans in 1948, that number rose to 133,032 in Critics argued that this addition made the government too involved with the private sector.

14 Federal National Mortgage Association Charter Act The Housing and Home Finance Agency acquired Fannie Mae from the Federal Loan Agency in A 1954 amendment by Congress, the Federal National Mortgage Association Charter Act made Fannie Mae a mixed-ownership corporation. Mortgage lenders now had to own common stock to be able to sell mortgages. The enterprise became responsible for Providing special assistance to the President or Congress with certain mortgages. Managing mortgages obtained before 1954.

15 The Largest Mortgage Buyer Primary mortgage lenders were temporarily unable to to make new mortgages, because they lacked the required liquid resources in Fannie Mae became the largest mortgage buyer in the market. Fluctuating periods of high borrowing costs that caused the association s profits to fall signified the need for major change.

16 Transformation In 1968, Fannie Mae transitioned from a mixed-ownership corporation to a private one, thus separating its activity and debt from the federal budget. The Housing and Urban Development Act of 1968 split Fannie Mae in two, the new Fannie Mae and the Government National Mortgage Association (GNMA), or Ginnie Mae.

17 The New Fannie Mae and Ginnie Mae The new Fannie Mae conducted secondary mortgage market activities as was done before. Ginnie Mae assumed the government assistance and mortgage management functions and guaranteed FHA and VA mortgages. The Department of Housing and Urban Development (HUD) oversaw the new Fannie Mae.

18 Fannie Mae in 1970 Oakley Hunter became the new president of Fannie Mae in January 1970 following the removal of Raymond H. Lapin by President Richard Nixon. Fannie Mae s transition to private control was completed on May 21, 1970, and the corporation went public on the New York and Pacific Exchanges. The board of directors comprised fifteen members, ten of whom were elected by stockholders and the remaining five who were appointed by the president. The federal government authorized Fannie Mae to purchase mortgages not insured by the FHA, VA, or Farmers Home Administration (FmHA), also known as conventional mortgages. Freddie Mac was established to compete with Fannie Mae and expand the secondary mortgage market.

19 Downturn for Fannie Mae Fannie Mae was susceptible to a rise in interest rates that began in 1979 and lost millions of dollars borrowing at high rates. New chairman David O. Maxwell instituted a number of programs to hand over some of this interest-rate risk. One of these initiatives was buying adjustable-rate mortgages, to which many primary lending institutions were shifting. In 1981, Fannie Mae began selling mortgage-backed securities (MBS) to assist with financing its mortgage purchases and to generate fee income. Institutions traded loans directly for more liquid securities with the MBS swap program.

20 Recovery and Renewal Fannie Mae was profitable once again by The enterprise started to borrow money from abroad to finance its purchases and to market real estate mortgage investment conduits (REMIC). These securities had adjustable maturity dates that attracted unconventional investors. On its fiftieth anniversary, Fannie Mae had put $400 billion into the U.S. mortgage industry. $300 billion came after It was added to the Standard and Poor s 500 stock index in 1988.

21 The 1990s The Fannie Mae Foundation for charitable contributions was established in The association began its Opening Doors to Affordable Housing, Trillion Dollar Commitment, and Partnership Office initiatives. The Housing and Community Development Act of 1992 amended Fannie Mae s charter with the provision that the corporation meet annual affordable housing goals established by HUD and approved by Congress. The corporation extended its activity into the subprime market by increasing the ratio of loan portfolios in distressed inner cities areas outlined by the 1977 Community Reinvestment Act. In 1999, Fannie Mae adjusted its mission statement to emphasize affordable rental housing and homeownership.

22

23 Introduction of Freddie Mac established by Congress as a private corporation through the Emergency Home Finance Act Founded to increase competition for the new privately held portion of Fannie Mae Authorized to create a secondary market for conventional mortgages (those that lack federal backing) Main difference = purchases mortgages from smaller thrift banks instead of commercial banks Currently regulated by the Federal Housing Finance Agency

24

25 Our statutory mission is to provide liquidity, stability and affordability to the US housing market.

26 What is a GSE? Consists of privately held corporations with public purposes Created to reduce the cost of capital for certain borrowing sectors of the economy Carry implicit backing, but no direct obligations

27 Early Mortgage-Backed Securities first MBS offering by GNMA, face value of $70M, investors bought fraction of security Pass-throughs - passed principal and interest payments on mortgages through to the investor Freddie Mac issued first MBS Fannie Mae issued first MBS Pension funds, mutual funds, insurance companies, and banks are all buyers of these securities Disadvantages: credit risk, interest rate risk, prepayment risk (option to prepay underlying loans if rates fall)

28 Introduction of CMO s Freddie Mac issued first multi-class MBS (Fannie Mae in 1985) through Salomon Brothers and First Boston Consists of a pool of mortgages organized by maturity and risk Distribute principal and interest payments based on predetermined rules and agreements Structure: Tranches: groups of mortgages organized by their risk profiles, have different principal balances, interest rates, maturity dates and repayment defaults Tranches retired in order of priority Congress created the Real Estate Mortgage Conduit (REMIC) to facilitate issuance of CMO s Disadvantages: still uncertainty as to when the early tranches will be paid off

29 Financial Institutions Reform, Recovery and Enforcement Act FIRREA was passed, response to Savings and Loans crisis Cut Freddie Mac s ties to the Federal Home Loan Bank System Made regulation of Freddie Mac and Fannie Mae consistent Formed an eighteen-member board of directors of Freddie Mac, subject to oversight by HUD Converted stock into Voting Common Stock Listed on NYSE between 1984 and 2010 July 8th, common stock exclusively traded on OTC under ticker symbol, FMCC

30 Other important dates Freddie Mac began receiving affordable housing credit for buying subprime securities HUD suggested the company was lagging behind and should do more Freddie Mac put under conservatorship of the U.S. federal government

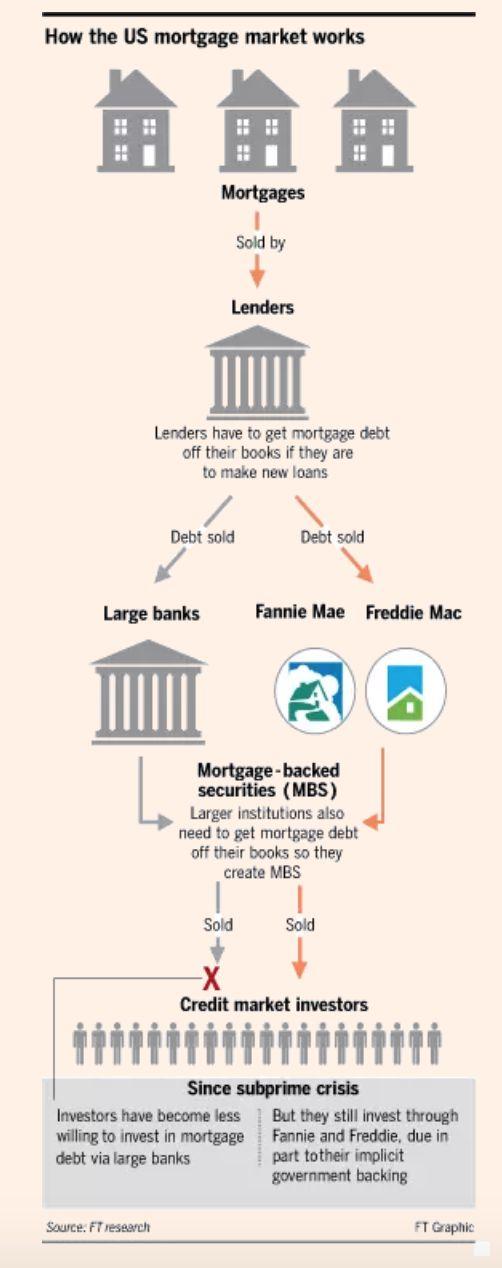

31 Linkage of Markets Conducts business in both the US residential mortgage market and the global securities market Links U.S. homebuyers with the global capital market Player of Two Markets: 1. U.S. Residential Mortgage Market finances mortgages through guaranteed mortgage securities backed by pools of mortgages and other financial instruments in the global capital market 2. Global Securities Market

32 Profit-Driven Company with a Public Mission How does Freddie Mac make profit? 1. Guarantee Fee Income When principal and interest is passed along to the holder of the MBS, Freddie Mac keeps a percentage of the interest as a guarantee fee for assuming credit risk Similar to an insurance policy - guarantees that the principal and interest on the underlying loan will be paid back regardless of whether the borrower actually repays 2. Retained Portfolios Invest heavily in other MBSs Because of implied Federal guarantee, able to issue a debt at yields lower than other corporations Earn spreads on their portfolios which are greater than other institutions because of this funding advantage

33

34 &

35 Freddie Mac and Fannie Mae: Similarities Both were established to promote housing market and mortgage sale Though Fannie Mae was established first, both buy mortgages from banks (anything from small individual banks to larger retail banks) After purchasing mortgages from private banks, the enterprises rebrand them as MBSs and sell them on the secondary market With regard to the financial crisis of 2008, the two organizations were treated fiscally and legally as one body

36 Freddie Mac and Fannie Mae: Differences Freddie Mac was established to compete with Fannie Mae and allowed it to buy non-fha mortgages and translate them into MBSs Fannie Mae purchases mortgages from more retail banks whereas Freddie Mac purchases from more thrift banks Freddie Mac buys mortgages that do not have government guarantees for its loans and wants to transfer the risk of default

37 Ginnie Mae vs. Freddie Mac and Fannie Mae Ginnie Mae is a government-run organization that guarantees MBSs Ginnie Mae insured bonds have the explicit government backing, whereas Freddie Mac and Fannie Mae do not Unlike a treasury bond, Ginnie Mae funds can lose value if interest rates go up All three type of securities follow similar up-down trends in the market

38 Freddie and Fannie in the Early 2000s In 2001, Freddie Mac and Fannie Mae controlled 43% of the the Housing Market In 2003, they controlled over 90% of the market Through $75 million spent on an advertisement in 2000, Freddie Mac and Fannie Mae positioned themselves as the purveyor of the American Dream of homeownership

39 Interest Rates in the Modern Era

40 What was the Subprime Mortgage Crisis? The mid 2000s were characterised by a housing boom which was correlated with a decrease in interest rates Increased housing and easily accessible loans lead lenders to offer home loans to individuals with poor credit and high risk profiles Sharp increase in high risk mortgages started in early 2007 When the real estate bubble burst, many high risk borrowers were unable to make payments on their mortgages

41 How were Freddie Mac and Fannie Mae Involved? GSE status of the two enterprises meant that they had government support while remaining more autonomous due to lack of bureaucratic oversight Investors favored the two GSEs over private bank mortgages due to the implied fiscal security The two provided MBSs that historically averaged over 35 points (.35%) higher than Triple A rated Treasury Bonds. The burst of the housing bubble led to the meltdown of liquidity in MBS, leading to a bailout on September 17, 2008 costing a total of $187 billion

42 Breakdown of the Mortgage Market

43 Freddie Mac and Fannie Mae in Recent News Biggest investor is the United States government High uncertainty due to high political impact and externalities has caused the prices of stock to drop after the subprime crisis Since 2012, the GSEs paid over $200 Billion in dividends to the U.S. Treasury Bills preventing the Treasury from collecting dividends cyclically appear before Congress

44 Freddie Mac and Fannie Mae in Recent News

45 Works Cited GRAPHIC.html ut efore-investing-in-fannie.aspx

Printable Lesson Materials

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Mortgage Backed Securities: The US Approach. 4 February 2003 Soula Proxenos International Housing Finance Services

Mortgage Backed Securities: The US Approach 4 February 2003 Soula Proxenos Today s Session... Overview of MBS in the United States Investor Considerations for MBS Fannie Mae s MBS Business Slide 2 Mortgage

Mortgage Backed Securities: The US Approach 4 February 2003 Soula Proxenos Today s Session... Overview of MBS in the United States Investor Considerations for MBS Fannie Mae s MBS Business Slide 2 Mortgage

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

FINANCIAL POLICY FORUM DERIVATIVES STUDY CENTER

FINANCIAL POLICY FORUM DERIVATIVES STUDY CENTER www.financialpolicy.org 1660 L Street, NW, Suite 1200 rdodd@financialpolicy.org Washington, D.C. 20036 PRIMER MORTGAGE-BACKED SECURITIES Ivo Kolev Research

FINANCIAL POLICY FORUM DERIVATIVES STUDY CENTER www.financialpolicy.org 1660 L Street, NW, Suite 1200 rdodd@financialpolicy.org Washington, D.C. 20036 PRIMER MORTGAGE-BACKED SECURITIES Ivo Kolev Research

Chapter 11 11/18/2014. Mortgages and Mortgage Markets. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Hearing on The Housing Decline: The Extent of the Problem and Potential Remedies December 13, 2007

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Overview of Mortgage Lending

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Summary of Senate Banking Committee Leaders Bipartisan Housing Finance Reform Draft

Summary of Senate Banking Committee Leaders Bipartisan Housing Finance Reform Draft The housing market accounts for nearly 20 percent of the American economy, so it is critical that we have a strong and

Summary of Senate Banking Committee Leaders Bipartisan Housing Finance Reform Draft The housing market accounts for nearly 20 percent of the American economy, so it is critical that we have a strong and

Federal National Mortgage Association

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

Memorandum on Federal Housing Finance Reform ECONOMY & JOBS

PRESIDENTIAL MEMORANDA Memorandum on Federal Housing Finance Reform ECONOMY & JOBS Issued on: March 27, 2019 MEMORANDUM FOR THE SECRETARY OF THE TREASURY THE SECRETARY OF AGRICULTURE THE SECRETARY OF HOUSING

PRESIDENTIAL MEMORANDA Memorandum on Federal Housing Finance Reform ECONOMY & JOBS Issued on: March 27, 2019 MEMORANDUM FOR THE SECRETARY OF THE TREASURY THE SECRETARY OF AGRICULTURE THE SECRETARY OF HOUSING

6/21/2013. Section I. Purpose of Course. History and Overview of Mortgage Law, Regulation and Requirements

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

More on Mortgages. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

Federal National Mortgage Association

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

October 9, Federal Housing Finance Agency Office of Strategic Initiatives th St, S.W. Washington, D.C To Whom it May Concern:

Federal Housing Finance Agency Office of Strategic Initiatives 400 7 th St, S.W. Washington, D.C. 20024 To Whom it May Concern: On August 12 th, 2014 the Federal Housing Finance Agency (FHFA) released

Federal Housing Finance Agency Office of Strategic Initiatives 400 7 th St, S.W. Washington, D.C. 20024 To Whom it May Concern: On August 12 th, 2014 the Federal Housing Finance Agency (FHFA) released

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

The US Housing Market Crisis and Its Aftermath

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

February 5, Dear Secretary Geithner:

The Honorable Timothy F. Geithner Secretary of the Treasury U.S. Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Dear Secretary Geithner: The Mortgage Bankers Association 1

The Honorable Timothy F. Geithner Secretary of the Treasury U.S. Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Dear Secretary Geithner: The Mortgage Bankers Association 1

An Overview of the Housing Finance System in the United States

An Overview of the Housing Finance System in the United States Sean M. Hoskins Analyst in Financial Economics Katie Jones Analyst in Housing Policy N. Eric Weiss Specialist in Financial Economics March

An Overview of the Housing Finance System in the United States Sean M. Hoskins Analyst in Financial Economics Katie Jones Analyst in Housing Policy N. Eric Weiss Specialist in Financial Economics March

Chap. 15. Government Securities

Reading: Chapter 15 Chap. 15. Government Securities 1. The variety of federal government debt 2. Federal agency debt 3. State and local government debt 4. Authority bonds and Build America bonds 5. Foreign

Reading: Chapter 15 Chap. 15. Government Securities 1. The variety of federal government debt 2. Federal agency debt 3. State and local government debt 4. Authority bonds and Build America bonds 5. Foreign

Fannie, Freddie, and Housing Finance: What s It All About?

Fannie, Freddie, and Housing Finance: What s It All About? Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation to the Central Banking Seminar, Federal Reserve

Fannie, Freddie, and Housing Finance: What s It All About? Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation to the Central Banking Seminar, Federal Reserve

With all the borrowing that we do today, it is hard to believe that prior to the 1930s,

Hit the Books Instructions: As you read, trace over the words that are shaded and underlined. This will help you to understand and retain important information. With all the borrowing that we do today,

Hit the Books Instructions: As you read, trace over the words that are shaded and underlined. This will help you to understand and retain important information. With all the borrowing that we do today,

GOVERNMENT-SPONSORED ENTERPRISES

GOVERNMENT-SPONSORED ENTERPRISES This chapter contains descriptions of and data on the Government-sponsored enterprises listed below. These enterprises were established and chartered by the Federal Government.

GOVERNMENT-SPONSORED ENTERPRISES This chapter contains descriptions of and data on the Government-sponsored enterprises listed below. These enterprises were established and chartered by the Federal Government.

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

Common Stock. 82,000,000 Shares. Citi OFFERING CIRCULAR

OFFERING CIRCULAR 82,000,000 Shares Common Stock We are offering 82,000,000 shares of our common stock, no par value, in this offering. We are also concurrently offering 45,000,000 shares of our 8.75%

OFFERING CIRCULAR 82,000,000 Shares Common Stock We are offering 82,000,000 shares of our common stock, no par value, in this offering. We are also concurrently offering 45,000,000 shares of our 8.75%

A Citizen s Guide to the 2008 Financial Report of the U.S. Government

A citizens guide to the report of the united states government The federal government s financial health OVERVIEW Fiscal Year (FY) 2008 was a year of unprecedented change in the financial position and

A citizens guide to the report of the united states government The federal government s financial health OVERVIEW Fiscal Year (FY) 2008 was a year of unprecedented change in the financial position and

Mortgage Market Statistical Annual 2017 Yearbook. Table of Contents

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

homeownership rental housing business finance colorado housing and finance authority annual financial report

homeownership rental housing business finance colorado housing and finance authority annual financial report December 31, 2017 and 2016 COLORADO HOUSING AND FINANCE AUTHORITY Annual Financial Report Table

homeownership rental housing business finance colorado housing and finance authority annual financial report December 31, 2017 and 2016 COLORADO HOUSING AND FINANCE AUTHORITY Annual Financial Report Table

11/9/2017. Chapter 11. Mortgages and Mortgage Markets. Traditional and Modern Housing Finance: From S&Ls to Securities. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

ISSUE BRIEF JUNE An Analysis of the Corker-Warner GSE Reform Bill and Its Implications for Affordable Housing Finance

ISSUE BRIEF JUNE 2013 An Analysis of the Corker-Warner GSE Reform Bill and Its Implications for Affordable Housing Finance ISSUE BRIEF An Analysis of the Corker-Warner GSE Reform Bill and Its Implications

ISSUE BRIEF JUNE 2013 An Analysis of the Corker-Warner GSE Reform Bill and Its Implications for Affordable Housing Finance ISSUE BRIEF An Analysis of the Corker-Warner GSE Reform Bill and Its Implications

APPENDIX A: GLOSSARY

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

Subprime Crisis Update on Federal Government Response

Subprime Crisis Update on Federal Government Response With Congress in a brief recess, now is an opportune time to provide a brief update on federal activities surrounding the continuing subprime mortgage

Subprime Crisis Update on Federal Government Response With Congress in a brief recess, now is an opportune time to provide a brief update on federal activities surrounding the continuing subprime mortgage

Mortgage REITs. March 20, Calvin Schnure Senior Vice President, Research & Economic Analysis

Mortgage REITs March 20, 2018 Calvin Schnure Senior Vice President, Research & Economic Analysis cschnure@nareit.com, 202-739-9434 Executive Summary Mortgage REITs (mreits) are companies that finance residential

Mortgage REITs March 20, 2018 Calvin Schnure Senior Vice President, Research & Economic Analysis cschnure@nareit.com, 202-739-9434 Executive Summary Mortgage REITs (mreits) are companies that finance residential

GSE Reform: Consumer Costs in a Reformed System

ONE VOICE. ONE VISION. ONE RESOURCE. GSE Reform: Consumer Costs in a Reformed System In evaluating any proposal for GSE reform, three major objectives must be balanced: protecting taxpayers, attracting

ONE VOICE. ONE VISION. ONE RESOURCE. GSE Reform: Consumer Costs in a Reformed System In evaluating any proposal for GSE reform, three major objectives must be balanced: protecting taxpayers, attracting

Homeowner Affordability and Stability Plan Fact Sheet

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Capitalism - Pros and Cons

Capitalism - Pros and Cons Pros of Capitalism Market gives incentives to produce Incentivizes acquisition of useful skills Variety of goods available Incentive to use resources efficiently Competition

Capitalism - Pros and Cons Pros of Capitalism Market gives incentives to produce Incentivizes acquisition of useful skills Variety of goods available Incentive to use resources efficiently Competition

Summary As households and taxpayers, Americans have a large stake in the future of Fannie Mae and Freddie Mac. Homeowners and potential homeowners ind

Proposals to Reform Fannie Mae and Freddie Mac in the 112 th Congress N. Eric Weiss Specialist in Financial Economics May 18, 2011 Congressional Research Service CRS Report for Congress Prepared for Members

Proposals to Reform Fannie Mae and Freddie Mac in the 112 th Congress N. Eric Weiss Specialist in Financial Economics May 18, 2011 Congressional Research Service CRS Report for Congress Prepared for Members

The Mortgage Industry

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Exhibit 2 with corrections through Memorandum

Exhibit 2 with corrections through 10.11.10 Memorandum Sizing Total Federal Government and Federal Agency Contributions to Subprime and Alt- A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto

Exhibit 2 with corrections through 10.11.10 Memorandum Sizing Total Federal Government and Federal Agency Contributions to Subprime and Alt- A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto

The Loan Limits for Government-Backed Mortgages

The Loan Limits for Government-Backed Mortgages N. Eric Weiss Specialist in Financial Economics Katie Jones Analyst in Housing Policy Libby Perl Specialist in Housing Policy Tadlock Cowan Analyst in Natural

The Loan Limits for Government-Backed Mortgages N. Eric Weiss Specialist in Financial Economics Katie Jones Analyst in Housing Policy Libby Perl Specialist in Housing Policy Tadlock Cowan Analyst in Natural

The Effect of GSEs, CRA, and Institutional. Characteristics on Home Mortgage Lending to. Underserved Markets

The Effect of GSEs, CRA, and Institutional Characteristics on Home Mortgage Lending to Underserved Markets HUD Final Report Richard Williams, University of Notre Dame December 1999 Direct all inquiries

The Effect of GSEs, CRA, and Institutional Characteristics on Home Mortgage Lending to Underserved Markets HUD Final Report Richard Williams, University of Notre Dame December 1999 Direct all inquiries

Chapter 12. The Bond Market

Chapter 12 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Chapter 12 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Federal National Mortgage Association (Exact name of registrant as specified in its charter) Fannie Mae

Fannie Mae") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 0-Q QUARTERLY REPORT PURSUANT TO SECTION 3 OR 5(d) OF THE SECURITIES EXCHANGE ACT OF 934 For the quarterly period ended June

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 0-Q QUARTERLY REPORT PURSUANT TO SECTION 3 OR 5(d) OF THE SECURITIES EXCHANGE ACT OF 934 For the quarterly period ended June

The Perils of Privatizing the U.S. Mortgage Finance System. David Min March

AP Photo/Robert F. Bukaty The Perils of Privatizing the U.S. Mortgage Finance System David Min March 2011 www.americanprogress.org Introduction and summary The U.S. Congress and the Obama administration

AP Photo/Robert F. Bukaty The Perils of Privatizing the U.S. Mortgage Finance System David Min March 2011 www.americanprogress.org Introduction and summary The U.S. Congress and the Obama administration

Sanford C. Bernstein Investor Presentation

NMI Holdings, Inc. (NMIH) Sanford C. Bernstein Investor Presentation May 14, 2014 2014 Copyright. National MI Cautionary Note Regarding Forward- Looking Statements This presentation contains forward-looking

NMI Holdings, Inc. (NMIH) Sanford C. Bernstein Investor Presentation May 14, 2014 2014 Copyright. National MI Cautionary Note Regarding Forward- Looking Statements This presentation contains forward-looking

National Association of Home Builders. Why Housing Matters. A Comprehensive Framework for Housing Finance System Reform

Why Housing Matters A Comprehensive Framework for Housing Finance System Reform SEPTEMBER 2015 WHY HOUSING MATTERS A COMPREHENSIVE FRAMEWORK FOR HOUSING FINANCE SYSTEM REFORM SEPTEMBER 2015 Table of Contents:

Why Housing Matters A Comprehensive Framework for Housing Finance System Reform SEPTEMBER 2015 WHY HOUSING MATTERS A COMPREHENSIVE FRAMEWORK FOR HOUSING FINANCE SYSTEM REFORM SEPTEMBER 2015 Table of Contents:

Federal National Mortgage Association (Exact name of registrant as specified in its charter) Fannie Mae

Fannie Mae") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 0-Q QUARTERLY REPORT PURSUANT TO SECTION 3 OR 5(d) OF THE SECURITIES EXCHANGE ACT OF 934 For the quarterly period ended March

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 0-Q QUARTERLY REPORT PURSUANT TO SECTION 3 OR 5(d) OF THE SECURITIES EXCHANGE ACT OF 934 For the quarterly period ended March

Fannie Mae and Freddie Mac the two federally

Fannie Mae, Freddie Mac, and Housing Finance Reform By Sarah Mickelson, Director, Public Policy and Elayne Weiss, Senior Policy Analyst, National Low Income Housing Coalition See also: National Housing

Fannie Mae, Freddie Mac, and Housing Finance Reform By Sarah Mickelson, Director, Public Policy and Elayne Weiss, Senior Policy Analyst, National Low Income Housing Coalition See also: National Housing

6/18/2015. Residential Mortgage Types and Borrower Decisions. Role of the secondary market Mortgage types:

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

S&P/Case Shiller index

S&P/Case Shiller index Home price index Index Jan. 2000=100, 3 month ending 240 220 200 180 160 10-metro composite 140 120 20-metro composite 100 80 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

S&P/Case Shiller index Home price index Index Jan. 2000=100, 3 month ending 240 220 200 180 160 10-metro composite 140 120 20-metro composite 100 80 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Sales Associate Course

Sales Associate Course Chapter Thirteen Types of Mortgages & Sources of Finance Copyright Gold Coast Schools 1 Types of Mortgages FHA - Federal Housing Administration VA - Veterans Administration Conventional

Sales Associate Course Chapter Thirteen Types of Mortgages & Sources of Finance Copyright Gold Coast Schools 1 Types of Mortgages FHA - Federal Housing Administration VA - Veterans Administration Conventional

Ninth Annual LARIBA Symposium

Ninth Annual LARIBA Symposium Freddie Mac s Role in the U.S. Housing Finance System James F. Carey, Director Freddie Mac We Open Doors Every Step of the Way Freddie Mac s Role Background Chartered by congress

Ninth Annual LARIBA Symposium Freddie Mac s Role in the U.S. Housing Finance System James F. Carey, Director Freddie Mac We Open Doors Every Step of the Way Freddie Mac s Role Background Chartered by congress

THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES

DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES") THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R. 3221 (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES Subtitle A Improvement of Safety and Soundness Supervision. Establishes

THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R. 3221 (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES Subtitle A Improvement of Safety and Soundness Supervision. Establishes

Government-Sponsored Enterprises and Financial Stability

Government-Sponsored Enterprises and Financial Stability Wayne Passmore Federal Reserve Board GSE Workshop April 27, 2017 The views expressed are the author s and should not be interpreted as representing

Government-Sponsored Enterprises and Financial Stability Wayne Passmore Federal Reserve Board GSE Workshop April 27, 2017 The views expressed are the author s and should not be interpreted as representing

SAN FRANCISCO COUNTY TRANSPORTATION AUTHORITY INVESTMENT POLICY

I. INTRODUCTION II. III. IV. The purpose of this document is to set out policies and procedures that enhance opportunities for a prudent and systematic investment policy and to organize and formalize investment-related

I. INTRODUCTION II. III. IV. The purpose of this document is to set out policies and procedures that enhance opportunities for a prudent and systematic investment policy and to organize and formalize investment-related

Federated U.S. Government Securities Fund: 2-5 Years

Prospectus March 31, 2013 Share Class R Institutional Service Ticker FIGKX FIGTX FIGIX Federated U.S. Government Securities Fund: 2-5 Years The information contained herein relates to all classes of the

Prospectus March 31, 2013 Share Class R Institutional Service Ticker FIGKX FIGTX FIGIX Federated U.S. Government Securities Fund: 2-5 Years The information contained herein relates to all classes of the

NAHB Resolution. Comprehensive Framework for Housing Finance System Reform Housing Finance Committee

Resolution No. 5 Date: City: Las Vegas, NV NAHB Resolution Title: Sponsor: Submitted by: Housing Finance Committee Michael Fink WHEREAS, the Housing Act of 1949 established a national over-arching policy

Resolution No. 5 Date: City: Las Vegas, NV NAHB Resolution Title: Sponsor: Submitted by: Housing Finance Committee Michael Fink WHEREAS, the Housing Act of 1949 established a national over-arching policy

Federal National Mortgage Association

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

1 Anthony B. Sanders, Ph.D. is Professor of Finance at the School of Management at George Mason University

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

The Post-Crisis World: Where Will Agency MBSs Trade?

The Post-Crisis World: Where Will Agency MBSs Trade? Financial Engineering Practitioners Seminar DEPT. OF INDUSTRIAL ENGINEERING AND OPERATIONS RESEARCH SCHOOL OF ENGINEERING AND APPLIED SCIENCE COLUMBIA

The Post-Crisis World: Where Will Agency MBSs Trade? Financial Engineering Practitioners Seminar DEPT. OF INDUSTRIAL ENGINEERING AND OPERATIONS RESEARCH SCHOOL OF ENGINEERING AND APPLIED SCIENCE COLUMBIA

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES ACUIA Region 3 Meeting Presented by: Bob Parks, CPA Director, Financial Institutions Group Overview Mortgage market and credit union trends

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES ACUIA Region 3 Meeting Presented by: Bob Parks, CPA Director, Financial Institutions Group Overview Mortgage market and credit union trends

Making Securitization Work for Financial Stability and Economic Growth

Shadow Financial Regulatory Committees of Asia, Australia-New Zealand, Europe, Japan, Latin America, and the United States Making Securitization Work for Financial Stability and Economic Growth Joint Statement

Shadow Financial Regulatory Committees of Asia, Australia-New Zealand, Europe, Japan, Latin America, and the United States Making Securitization Work for Financial Stability and Economic Growth Joint Statement

Ira G. PEPPERCORN. The Tragedy of the Mortgage Commons. President IRA PEPPERCORN INTERNATIONAL, LLC

The Tragedy of the Mortgage g Commons Ira G. PEPPERCORN President IRA PEPPERCORN INTERNATIONAL, LLC WORLD BANK-IFC WORKSHOP ON HOUSING FINANCE IN SOUTH ASIA JAKARTA INDONESIA MAY 28, 2009 U.S. Mortgage

The Tragedy of the Mortgage g Commons Ira G. PEPPERCORN President IRA PEPPERCORN INTERNATIONAL, LLC WORLD BANK-IFC WORKSHOP ON HOUSING FINANCE IN SOUTH ASIA JAKARTA INDONESIA MAY 28, 2009 U.S. Mortgage

S&P/Case Shiller index

S&P/Case Shiller index Home price index Index Jan. 2000=100, 3 month ending 240 220 200 180 160 10-metro composite 140 20-metro composite 120 100 80 2000 2001 2002 2003 2004 Sources: Standard & Poor's

S&P/Case Shiller index Home price index Index Jan. 2000=100, 3 month ending 240 220 200 180 160 10-metro composite 140 20-metro composite 120 100 80 2000 2001 2002 2003 2004 Sources: Standard & Poor's

Polk County Wisconsin. Policy 913 Effective Date: Revision Date: , ,

Polk County Wisconsin INVESTMENT POLICY Policy 913 Effective Date: 06-19-2000 Revision Date: 5-20-2003, 7-18-2006, 01-16-07 POLK COUNTY INVESTMENT POLICY 1.0 Policy: The County Board Chairperson, Polk

Polk County Wisconsin INVESTMENT POLICY Policy 913 Effective Date: 06-19-2000 Revision Date: 5-20-2003, 7-18-2006, 01-16-07 POLK COUNTY INVESTMENT POLICY 1.0 Policy: The County Board Chairperson, Polk

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance Prof. Stijn Van Nieuwerburgh New York University Stern School of Business March 1, 2011 Published by Princeton University

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance Prof. Stijn Van Nieuwerburgh New York University Stern School of Business March 1, 2011 Published by Princeton University

Securitization. Spring Stephen Sapp

Securitization Spring 2014 Stephen Sapp What is Securitization? Grouping together a set of assets which generate cashflows, selling this portfolio to another entity to manage (i.e., collect the cashflows),

Securitization Spring 2014 Stephen Sapp What is Securitization? Grouping together a set of assets which generate cashflows, selling this portfolio to another entity to manage (i.e., collect the cashflows),

Brenda Hughes. American Bankers Association. Committee on Banking, Housing, and Urban Affairs United States Senate

Testimony of Brenda Hughes On behalf of the American Bankers Association before the Committee on Banking, Housing, and Urban Affairs United States Senate Testimony of Brenda Hughes On behalf of the American

Testimony of Brenda Hughes On behalf of the American Bankers Association before the Committee on Banking, Housing, and Urban Affairs United States Senate Testimony of Brenda Hughes On behalf of the American

Money and Banking ECON3303. Lecture 9: Financial Crises. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You?

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You? 1 2 2 3 3 4 Commercial real

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You? 1 2 2 3 3 4 Commercial real

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout

Introduction. Master Programmes INTERNATIONAL FINANCE. Szabolcs Sebestyén

Introduction Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master Programmes INTERNATIONAL FINANCE Sebestyén (ISCTE-IUL) Introduction International Finance 1 / 43 Outline 1 Why Study Money, Banking, and

Introduction Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master Programmes INTERNATIONAL FINANCE Sebestyén (ISCTE-IUL) Introduction International Finance 1 / 43 Outline 1 Why Study Money, Banking, and

Macro Lecture 13: Mortgages and Fannie Mae

Macro Lecture 13: gages and Fannie Mae Home gages We shall study three types of mortgages which are used today: Fixed rate Variable (adjusted) rate Graduated payment These mortgages differ in how they

Macro Lecture 13: gages and Fannie Mae Home gages We shall study three types of mortgages which are used today: Fixed rate Variable (adjusted) rate Graduated payment These mortgages differ in how they

Introduction and Economic Landscape. Vance Ginn Spring 2013

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission About the Housing Commission Created by the Bipartisan Policy Center, a non-profit

Housing America s Future: New Directions for National Policy Report of the Bipartisan Policy Center Housing Commission About the Housing Commission Created by the Bipartisan Policy Center, a non-profit

Selected Legislative Proposals to Reform the Housing Finance System

Selected Legislative Proposals to Reform the Housing Finance System Sean M. Hoskins Analyst in Financial Economics N. Eric Weiss Specialist in Financial Economics Katie Jones Analyst in Housing Policy

Selected Legislative Proposals to Reform the Housing Finance System Sean M. Hoskins Analyst in Financial Economics N. Eric Weiss Specialist in Financial Economics Katie Jones Analyst in Housing Policy

The Return of Private Capital

The Return of Private Capital October 14, 2014 Private investor share of the U.S. mortgage market has declined since the financial crisis; however, private investors hold market risk on more than 75 percent

The Return of Private Capital October 14, 2014 Private investor share of the U.S. mortgage market has declined since the financial crisis; however, private investors hold market risk on more than 75 percent

Government-Sponsored Enterprises (GSEs): An Institutional Overview

: An Institutional Overview") Order Code RS21663 Updated September 9, 2008 Government-Sponsored Enterprises (GSEs): An Institutional Overview Kevin R. Kosar Analyst in American National Government Government and Finance Division Summary

Order Code RS21663 Updated September 9, 2008 Government-Sponsored Enterprises (GSEs): An Institutional Overview Kevin R. Kosar Analyst in American National Government Government and Finance Division Summary

Federal Reserve System Primary Market Secondary Market

Chapter 14: Real Estate Financing: Practices Introduction to the Real Estate Financing Market Federal Reserve System Primary Market Secondary Market Federal Reserve System Role Maintain sound credit conditions

Chapter 14: Real Estate Financing: Practices Introduction to the Real Estate Financing Market Federal Reserve System Primary Market Secondary Market Federal Reserve System Role Maintain sound credit conditions

Chapter 15 Real Estate Financing: Practice

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

I. Learning Objectives II. The Functions of Money III. The Components of the Money Supply

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

Federal National Mortgage Association (Exact name of registrant as specified in its charter) Fannie Mae

Fannie Mae") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 0-Q QUARTERLY REPORT PURSUANT TO SECTION 3 OR 5(d) OF THE SECURITIES EXCHANGE ACT OF 934 For the quarterly period ended September

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 0-Q QUARTERLY REPORT PURSUANT TO SECTION 3 OR 5(d) OF THE SECURITIES EXCHANGE ACT OF 934 For the quarterly period ended September

GAO FARM CREDIT ADMINISTRATION. Analysis of Administrative Expenses and Funding Through Assessments

GAO United States General Accounting Office Report to the Ranking Minority Member, Committee on Agriculture, Nutrition, and Forestry, U.S. Senate August 2001 FARM CREDIT ADMINISTRATION Analysis of Administrative

GAO United States General Accounting Office Report to the Ranking Minority Member, Committee on Agriculture, Nutrition, and Forestry, U.S. Senate August 2001 FARM CREDIT ADMINISTRATION Analysis of Administrative

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

Simplifying GSE Reform A Roundtable Discussion

Simplifying GSE Reform A Roundtable Discussion Andrew Davidson & Co., Inc. (AD&Co) held a roundtable discussion on housing finance reform at the Willard Hotel in Washington, DC on April 8, 2015. Andrew

Simplifying GSE Reform A Roundtable Discussion Andrew Davidson & Co., Inc. (AD&Co) held a roundtable discussion on housing finance reform at the Willard Hotel in Washington, DC on April 8, 2015. Andrew

Quiz The lender of mortgage money is known as the: A) trustee. B) mortgagor. C) mortgagee. D) trustor.

trustee. B) mortgagor. C) mortgagee. D) trustor.") Quiz 7 1. On a debt secured by property, the reduction of debt through regular periodic payments is known as: A) principal. B) amortization. C) reduction loan. D) retirement. 2. The lender of mortgage

Quiz 7 1. On a debt secured by property, the reduction of debt through regular periodic payments is known as: A) principal. B) amortization. C) reduction loan. D) retirement. 2. The lender of mortgage

An Introduction to the CDFI Fund

An Introduction to the CDFI Fund Making the New Markets Tax Credit Work in Native Communities PRESENTED ON MAY 24, 2018 COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND www.cdfifund.gov About the CDFI

An Introduction to the CDFI Fund Making the New Markets Tax Credit Work in Native Communities PRESENTED ON MAY 24, 2018 COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS FUND www.cdfifund.gov About the CDFI

Why is the Country Facing a Financial Crisis?

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Government and Private Initiatives to Address the Foreclosure Crisis

Government and Private Initiatives to Address the Foreclosure Crisis David Moskowitz Deputy General Counsel Berkeley Business Law Journal Berkeley Center for Law, Business and the Economy 2012 Symposium

Government and Private Initiatives to Address the Foreclosure Crisis David Moskowitz Deputy General Counsel Berkeley Business Law Journal Berkeley Center for Law, Business and the Economy 2012 Symposium

TESTIMONY OF BRUCE MARKS. Chief Executive Officer. Neighborhood Assistance Corporation of America (NACA)

") TESTIMONY OF BRUCE MARKS Chief Executive Officer Neighborhood Assistance Corporation of America (NACA) My name is Bruce Marks. I am Chief Executive Officer of the Neighborhood Assistance Corporation of

TESTIMONY OF BRUCE MARKS Chief Executive Officer Neighborhood Assistance Corporation of America (NACA) My name is Bruce Marks. I am Chief Executive Officer of the Neighborhood Assistance Corporation of

Federated Adjustable Rate Securities Fund

Prospectus October 31, 2017 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Prospectus October 31, 2017 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Principles of Mortgage Lending Secondary Marketing

Principles of Mortgage Lending Secondary Marketing DAN MCKENNEY PRESIDENT/CEO, MERRIMACK MORTGAGE COMPANY MARIO A. GOMEZ VP SECONDARY OFFICER, HARBORONE BANK Agenda History of Secondary Marketing Key Participants

Principles of Mortgage Lending Secondary Marketing DAN MCKENNEY PRESIDENT/CEO, MERRIMACK MORTGAGE COMPANY MARIO A. GOMEZ VP SECONDARY OFFICER, HARBORONE BANK Agenda History of Secondary Marketing Key Participants

May 17, Housing Sector Overview

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

Jack E. Hopkins President and CEO of CorTrust Bank Sioux Falls, SD

Testimony of Jack E. Hopkins President and CEO of CorTrust Bank Sioux Falls, SD On behalf of the Independent Community Bankers of America Before the United States Senate Committee on Banking, Housing and

Testimony of Jack E. Hopkins President and CEO of CorTrust Bank Sioux Falls, SD On behalf of the Independent Community Bankers of America Before the United States Senate Committee on Banking, Housing and

2008 STOCK MARKET COLLAPSE

2008 STOCK MARKET COLLAPSE Will Pickerign A FINACIAL INSTITUTION PERSECTIVE QUOTE In one way, I m Sympathetic to the institutional reluctance to face the music - Warren Buffet (Fortune 8/16/2007) RECAP

2008 STOCK MARKET COLLAPSE Will Pickerign A FINACIAL INSTITUTION PERSECTIVE QUOTE In one way, I m Sympathetic to the institutional reluctance to face the music - Warren Buffet (Fortune 8/16/2007) RECAP

Fannie Mae and Freddie Mac in Conservatorship

Order Code RS22950 September 15, 2008 Fannie Mae and Freddie Mac in Conservatorship Mark Jickling Specialist in Financial Economics Government and Finance Division Summary On September 7, 2008, the Federal

Order Code RS22950 September 15, 2008 Fannie Mae and Freddie Mac in Conservatorship Mark Jickling Specialist in Financial Economics Government and Finance Division Summary On September 7, 2008, the Federal

Principles of Mortgage Lending Secondary Marketing MICHAEL WILBERTON VP CAPITAL MARKETS OFFICER, HARBORONE BANK

Principles of Mortgage Lending Secondary Marketing MICHAEL WILBERTON VP CAPITAL MARKETS OFFICER, HARBORONE BANK Executive Summary History of Secondary Marketing Key Participants in the Secondary Market

Principles of Mortgage Lending Secondary Marketing MICHAEL WILBERTON VP CAPITAL MARKETS OFFICER, HARBORONE BANK Executive Summary History of Secondary Marketing Key Participants in the Secondary Market

HOUSING FINANCE REFORM PRINCIPLES

HOUSING FINANCE REFORM PRINCIPLES National Association of Federally-Insured Credit Unions NATIONAL ASSOCIATION OF FEDERALLY-INSURED CREDIT UNIONS NAFCU.ORG 1 The National Association of Federally-Insured

HOUSING FINANCE REFORM PRINCIPLES National Association of Federally-Insured Credit Unions NATIONAL ASSOCIATION OF FEDERALLY-INSURED CREDIT UNIONS NAFCU.ORG 1 The National Association of Federally-Insured

Federated Adjustable Rate Securities Fund

Prospectus October 31, 2018 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Prospectus October 31, 2018 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

The FHA Single-Family Mortgage Insurance Program: Financial Status and Related Current Issues

The FHA Single-Family Mortgage Insurance Program: Financial Status and Related Current Issues Katie Jones Analyst in Housing Policy December 21, 2012 CRS Report for Congress Prepared for Members and Committees

The FHA Single-Family Mortgage Insurance Program: Financial Status and Related Current Issues Katie Jones Analyst in Housing Policy December 21, 2012 CRS Report for Congress Prepared for Members and Committees