Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

|

|

|

- Paulina Stone

- 5 years ago

- Views:

Transcription

1 Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

2 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director & Vice Chair Federal Home Loan Bank of Atlanta Experience Director Federal Reserve Bank of Richmond Federal Home Loan Bank System Regulator Federal Deposit Insurance Corporation Federal Home Loan Bank Board Lender National Bank of Detroit Officer, United States Army 2

3 Bank Failure Liquidation Economic Financial Managerial 3

4 Recent US Failures AIG Bank United Bear Stearns Citibank Downey Fannie & Freddie GMAC Indy Mac Lehman Brothers WAMU Wachovia Hundreds of smaller banks Who will fail next Friday? 4

5 Bank Failure and the Economy Economic Recession High and/or Increasing Unemployment High Real Interest Rates Regional Boom to Bust Low Confidence in Banks or the Central Bank 5

6 Bank Failure and Asset/Liability Management Low Capital Losses Loan Problems Concentrated Portfolio Loss of Cost Control Quick Growth Liquidity Non Core Fund Reliance Lack of Good Collateral Bad Press & Run High-yield Assets High Sensitivity 6

7 Bank Failure and Management High number and percentage of loans to insiders Passive Board of Directors Lack of coherent business plan Quick growth funded by high cost funds offset by high yield assets High dividend payouts and stock repurchase programs Shrinkage to maintain capital ratios leads to even lower profits given fixed non-interest costs Ineffective risk management Fraud 7

8 Empirical Analysis of Recent US Bank Failure Leading Causes High problem loans to capital and ALLL Large losses High provision Losses on securities High non current loans Portfolio concentration in high risk ADC loans Low capital High non core funding Other Factors Prior quick growth High yield assets Fraud 8

Federal Reserve provides long-term loans and purchases securities (US $2")

9 Resultant Governmental Actions US Treasury invests in low-cost preferred stock (US $250 billion) FDIC raises deposit insurance limit and guarantees bank debt (US $400 billion) Federal Reserve provides long-term loans and purchases securities (US $2 trillion) 9

10 Housing Problem History Home prices rise quickly after dot.com bust and central bank reduces interest rate to very low levels Investors earn 50+% returns with 10% annual appreciation and encourage speculators to purchase more property Mortgagors need innovative loans and piggy-back loans to afford a home prior to even higher prices Wall Street encourages brokers to originate more high-yield loans for MBS MBS losses trigger dominoes to fall 10

11 Importance of Real Estate Household Sector Assets Real Estate 27% Business Sector Assets Real Estate 25% Other 73% Other 75% 11

12 US Financial Market US $52 trillion of Debt Other 73% Mortgage 27% US $14 trillion Mortgage Debt Residential 76 Commercial 17 Apartment 6 Farm Percent 12

13 US Home Prices Annual Price Change 2001: 8.9% 2002: 15.0% 2003: 13.4% 2004: 19.9% 2005: 14.8% 2006: 0.2% 2007: -9.7% 2008: -19.1% 2009: -2.5% % 13

14 Accommodative Monetary Policy Reduce Interest Rates 13 Times Reduce Cost of Short-term Borrowing Consumer Corporate Fiscal Stimulate Growth Reduce Value of US$ Stimulate Inflation Increase Rates Mid

15 Interest Rate Trends Three Month Treasury Bill Percent

; Higher Rate Loan B/C: Mediocre to Weak Credit History (10%); Much Higher Rate Loan")

16 Mortgage Risk A: Excellent Credit History (84%); Prime Borrower Alt-A: Income not Verified or Property not Appraised (6%); Higher Rate Loan B/C: Mediocre to Weak Credit History (10%); Much Higher Rate Loan 16

17 Credit Score Payment history Amount of debt owed Length of credit history New credit requested Types of credit used

18 Real Estate Loan Risk Type - Balloon loans or non-amortizing more risky than amortizing Interest Rate - Adjustable-rate more risky than fixed rate Amortization Period - Long-Term (40 years) amortization more risky than medium-term (15 years) Purpose - Equity refinance more risky than purchase Occupancy - Second home or investment home more risky than primary property 18

19 Mortgage Products Monthly Payment per $100,000 Loan Initial is First Five Years Initial Pay Later Pay 30 Fixed Fixed Interest only ARM Pay Option Fixed-rate 30 Year Fixed-rate 40 Year Interest-only (5 years) 30 Year Loan Adjustable-rate 30 Year Loan Payment Option (up to 110% LTV) 30 Year Loan 19

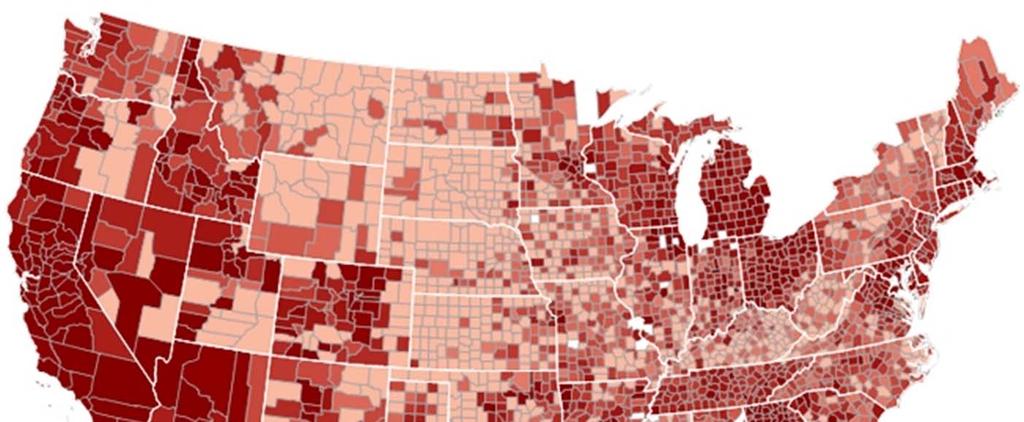

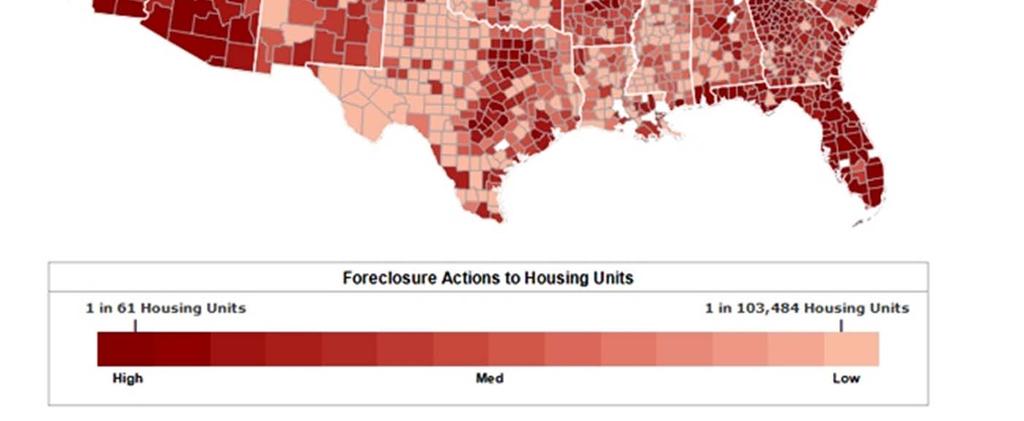

20 U.S. Foreclosure Market Report Heat Map 2010

21 Mortgage Problems Remain About 67% of homes are funded by mortgage loans About 13% of home loans are 30+ days slow or in foreclosure About 27% of borrowers have negative equity Loan workouts are performing badly with about 15% of loans 90+ days slow again current 21

22 Supply Factors Investment Banks Sell Highly-Rated Securities backed by High-Yield Loans Mortgage Brokers Originate High-Yield Loans then Sold to Banks Mortgagors Require Credit to Afford Homes Prior to Higher Prices Investors and Speculators Seek Credit to Purchase Real Estate and Enhance Returns 22

23 Securitization Pool of Residential Mortgages Mortgage Payments Mortgage Backed Security Packager/ Servicer Senior Tranche (AAA) Mezzanine Tranche () Junior Tranche (Low-grade) 23

24 CDO s (Collateralized Debt Obligations) RMBS From Loans CDO Collateral MEZZANINE CDO of ABS AAA AA A Unrated 81% 11% 4% 3% 1% Loan Losses CDO CDO Other CDO s Super Senior AAA AA A Equity 62% 14% 8% 6% 6% 24 4%

25 Financial Market Flight-to-quality Unexpected losses on highly-rated mortgage-backed securities lead to: Wall Street unable to sell new MBS and stop buying loans from mortgage brokers Mortgage brokers incur liquidity problems and fail when unable to sell loans and correspondent banks cut lines of credit Sub-prime, Alternative-A and investment mortgagors unable to obtain credit Prime mortgagor loans underwritten more carefully Stock of unsold homes increase, absorption periods lengthen and prices fall 25

26 Acquisition, Development and Construction (ADC) Loans Excess housing inventory eliminates demand for new home lots by builders Expectations of falling home prices stem demand for new homes Strict underwriting limits potential buyers As a result, land sells for 20% of cost; banks also incur substantial losses on ADC loans 26

27 Implications of Home Loan Problems Lower tax base Higher homelessness Bank failures and GSE problems Lost real estate wealth and MBS investment value Inability to refinance or obtain home equity loan Lost employment and retail spending Very weak economy 27

28 Central bank Governmental efforts to support affordable housing Wall Street and credit rating agencies Unregulated mortgage brokers Other bank regulators Bank management, risk managers and board of directors Crisis Culprits 28

29 Regulatory Implications Strict loan underwriting Higher FDIC insurance premiums Higher capital requirements More attention to liquidity and concentration The Federal Reserve and Department of Treasury invested in bank capital and served as a lender of first resort The stimulus added to an already large fiscal deficit and debt 29

30 Brasil s Real Estate Sector? 2 Biggest Reasons for Rapidly Rising Home Prices: Biggest Threats from High Home Prices:

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

William C. Handorf, Ph. D.

Risk Management and Value Creation 2011 1 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Expert Witness Director and Vice Chair

Risk Management and Value Creation 2011 1 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Expert Witness Director and Vice Chair

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Money and Banking ECON3303. Lecture 9: Financial Crises. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Announcement March 5, Updates and Clarifications for Streamlined Refinance Products

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Diana Hancock Ψ Wayne Passmore Ψ Federal Reserve Board

Diana Hancock Ψ Wayne Passmore Ψ Federal Reserve Board Ψ The results in this presentation are preliminary materials circulated to stimulate discussion and critical comment. The analysis and conclusions

Diana Hancock Ψ Wayne Passmore Ψ Federal Reserve Board Ψ The results in this presentation are preliminary materials circulated to stimulate discussion and critical comment. The analysis and conclusions

The Financial Crisis. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Capital Market Trends and Forecasts

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

MGIC Investment Corporation Bear Stearns Mortgage Finance & Housing Markets Conference May 18, 2006

MGIC Investment Corporation Bear Stearns Mortgage Finance & Housing Markets Conference May 18, 2006 Patrick Sinks President and Chief Operating Officer Safe Harbor Statement During the course of this presentation,

MGIC Investment Corporation Bear Stearns Mortgage Finance & Housing Markets Conference May 18, 2006 Patrick Sinks President and Chief Operating Officer Safe Harbor Statement During the course of this presentation,

Testimony of Keith Johnson. Former President of Clayton Holdings, Inc. and. Former President of Washington Mutual s Long Beach Mortgage

Testimony of Keith Johnson Former President of Clayton Holdings, Inc. and Former President of Washington Mutual s Long Beach Mortgage Before the Financial Crisis Inquiry Commission September 23, 2010 Chairman

Testimony of Keith Johnson Former President of Clayton Holdings, Inc. and Former President of Washington Mutual s Long Beach Mortgage Before the Financial Crisis Inquiry Commission September 23, 2010 Chairman

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know April13, 2010 Agenda Introduction Presentation Steve Herscovici, Managing Principal, Analysis Group Bill Chambers, Finance

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know April13, 2010 Agenda Introduction Presentation Steve Herscovici, Managing Principal, Analysis Group Bill Chambers, Finance

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C FORM 10-K

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 x o (MARK ONE) FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended: December

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 x o (MARK ONE) FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended: December

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions. Ingrid Gould Ellen

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

Securitized Products An Overlooked Source of Income

Securitized Products An Overlooked Source of Income March 26, 2014 Michael S. Nguyen, Managing Director, Liquidity Management Scott Cabalka, Vice President, Institutional Portfolio Manager RBC Global Asset

Securitized Products An Overlooked Source of Income March 26, 2014 Michael S. Nguyen, Managing Director, Liquidity Management Scott Cabalka, Vice President, Institutional Portfolio Manager RBC Global Asset

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

The Causes of the 2008 Financial Crisis

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

Subprime: Tentacles. How could a modest increase in. of a Crisis

Run on the United Kingdom s Northern Rock bank, a fallout from the U.S. subprime crisis. Subprime: Tentacles of a Crisis Randall Dodd How could a modest increase in seriously delinquent subprime mortgages,

Run on the United Kingdom s Northern Rock bank, a fallout from the U.S. subprime crisis. Subprime: Tentacles of a Crisis Randall Dodd How could a modest increase in seriously delinquent subprime mortgages,

The Recession

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

SUB PRIME CRISIS & EUROZONE CRISIS. Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts)

") SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

July 28, Elizabeth M. Murphy Secretary Securities and Exchange Commission 100 F Street, NE Washington, DC 20549

Jennifer J. Johnson Secretary Board of Governors of the Federal Reserve 20 th Street and Constitution Avenue, NW Washington, DC 20549 Robert E. Feldman Executive Secretary Federal Deposit Insurance Corporation

Jennifer J. Johnson Secretary Board of Governors of the Federal Reserve 20 th Street and Constitution Avenue, NW Washington, DC 20549 Robert E. Feldman Executive Secretary Federal Deposit Insurance Corporation

Fannie Mae Reports Third-Quarter 2011 Results

Contact: Number: Katherine Constantinou 202-752-5403 5552a Resource Center: 1-800-732-6643 Date: November 8, 2011 Fannie Mae Reports Third-Quarter 2011 Results Company Focused on Providing Liquidity to

Contact: Number: Katherine Constantinou 202-752-5403 5552a Resource Center: 1-800-732-6643 Date: November 8, 2011 Fannie Mae Reports Third-Quarter 2011 Results Company Focused on Providing Liquidity to

Today s Business Environment

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

Why is the Country Facing a Financial Crisis?

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

The Rise and Fall of Securitization

Wisconsin School of Business October 31, 2012 The rise and fall of home values 210 800 190 700 170 600 150 500 130 400 110 300 90 200 70 100 50 1985 1990 1995 2000 2005 2010 Home values 0 Source: Case

Wisconsin School of Business October 31, 2012 The rise and fall of home values 210 800 190 700 170 600 150 500 130 400 110 300 90 200 70 100 50 1985 1990 1995 2000 2005 2010 Home values 0 Source: Case

1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application.

GLOSSARY 1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application. Acceptance A verbal or written acceptance of an offer to buy

GLOSSARY 1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application. Acceptance A verbal or written acceptance of an offer to buy

Bulletin NUMBER: TO: Freddie Mac Sellers November 15, 2011

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

Hearing on The Housing Decline: The Extent of the Problem and Potential Remedies December 13, 2007

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure

No achievement without commitment SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure Conference Call Tuesday March 27, 27 Jacques Guerber Vice-Chairman of the Management

No achievement without commitment SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure Conference Call Tuesday March 27, 27 Jacques Guerber Vice-Chairman of the Management

CHIMERA INVESTMENT CORPORATION DIVIDEND REINVESTMENT PLAN. 25,000,000 Shares of Common Stock

PROSPECTUS CHIMERA INVESTMENT CORPORATION DIVIDEND REINVESTMENT PLAN 25,000,000 Shares of Common Stock The Dividend Reinvestment Plan, or the Plan, is designed to provide current holders of our common

PROSPECTUS CHIMERA INVESTMENT CORPORATION DIVIDEND REINVESTMENT PLAN 25,000,000 Shares of Common Stock The Dividend Reinvestment Plan, or the Plan, is designed to provide current holders of our common

Notice regarding Revisions of Earnings Forecasts

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

After-tax APRPlus The APRPlus taking into account the effect of income taxes.

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

MORTGAGE GLOSSARY Adjustable Rate Mortgage Known as an ARM, is a Mortgage that has a fixed rate of interest for only a set period of time, typically one, three or five years. During the initial period

Fannie Mae Reports Net Income of $4.6 Billion and Comprehensive Income of $4.4 Billion for Second Quarter 2015

Resource Center: 1-800-732-6643 Contact: Date: Pete Bakel 202-752-2034 August 6, 2015 Fannie Mae Reports Net Income of 4.6 Billion and Comprehensive Income of 4.4 Billion for Second Quarter 2015 Fannie

Resource Center: 1-800-732-6643 Contact: Date: Pete Bakel 202-752-2034 August 6, 2015 Fannie Mae Reports Net Income of 4.6 Billion and Comprehensive Income of 4.4 Billion for Second Quarter 2015 Fannie

2009 San Diego Apartment Perspective

2009 San Diego Apartment Perspective Graham Bryan, CRB, CCIM, SIOR President, CCIM San Diego Chapter Linda Morris, ARM President, San Diego County Apartment Association National and Local Economic Overview

2009 San Diego Apartment Perspective Graham Bryan, CRB, CCIM, SIOR President, CCIM San Diego Chapter Linda Morris, ARM President, San Diego County Apartment Association National and Local Economic Overview

Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation

Harvard University From the SelectedWorks of William Werkmeister Spring April, 2010 Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation William Werkmeister,

Harvard University From the SelectedWorks of William Werkmeister Spring April, 2010 Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation William Werkmeister,

WHAT THE REALLY HAPPENED...

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

Causes Of The Actual Global Financial Crisis. While many argue that this is the main cause of the global savings glut, the opposite is the

YourLastName 1 YourFirstName YourLastName Instructor's Name Course Title 1 August 2015 Causes Of The Actual Global Financial Crisis Introduction The US is one of the countries that have demonstrated their

YourLastName 1 YourFirstName YourLastName Instructor's Name Course Title 1 August 2015 Causes Of The Actual Global Financial Crisis Introduction The US is one of the countries that have demonstrated their

APPENDIX A: GLOSSARY

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

APPENDIX A: GLOSSARY Italicized terms within definitions are defined separately. ABCP see asset-backed commercial paper. ABS see asset-backed security. ABX.HE A series of derivatives indices constructed

Memorandum. Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Beryl Credit Pulse on Structured Finance

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

Chapter 11 11/18/2014. Mortgages and Mortgage Markets. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

New York Mortgage Trust Reports First Quarter 2018 Results

New York Mortgage Trust Reports First Quarter 2018 Results May 3, 2018 NEW YORK, May 03, 2018 (GLOBE NEWSWIRE) -- New York Mortgage Trust, Inc. (Nasdaq:NYMT) ( NYMT, the Company, we, our or us ) today

New York Mortgage Trust Reports First Quarter 2018 Results May 3, 2018 NEW YORK, May 03, 2018 (GLOBE NEWSWIRE) -- New York Mortgage Trust, Inc. (Nasdaq:NYMT) ( NYMT, the Company, we, our or us ) today

WaMu CASE STUDY (Executive Summary) (1) High Risk Lending: Case Study of Washington Mutual Bank

(1) High Risk Lending: Case Study of Washington Mutual Bank") WaMu CASE STUDY (Executive Summary) (1) High Risk Lending: Case Study of Washington Mutual Bank The first chapter focuses on how high risk mortgage lending contributed to the financial crisis, using as

WaMu CASE STUDY (Executive Summary) (1) High Risk Lending: Case Study of Washington Mutual Bank The first chapter focuses on how high risk mortgage lending contributed to the financial crisis, using as

Keefe, Bruyette & Woods Insurance Conference. S.A. Ibrahim, CEO NYSE: RDN September 7, 2010

Keefe, Bruyette & Woods Insurance Conference S.A. Ibrahim, CEO NYSE: RDN September 7, 2010 1 Safe Harbor Statements All statements made during today s investor presentation and in these webcast slides

Keefe, Bruyette & Woods Insurance Conference S.A. Ibrahim, CEO NYSE: RDN September 7, 2010 1 Safe Harbor Statements All statements made during today s investor presentation and in these webcast slides

Financing Residential Real Estate. Conventional Financing

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of a conventional loan, qualifying standards

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of a conventional loan, qualifying standards

Federated Adjustable Rate Securities Fund

Prospectus October 31, 2017 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Prospectus October 31, 2017 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

The US Housing Market Crisis and Its Aftermath

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

The PMI Group, Inc. Lehman Brothers Financial Services Conference September 10, 2007

Lehman Brothers Financial Services Conference September 10, 2007 Forward-Looking Statement FORWARD-LOOKING STATEMENTS: Statements in this presentation and oral statements made at this conference that are

Lehman Brothers Financial Services Conference September 10, 2007 Forward-Looking Statement FORWARD-LOOKING STATEMENTS: Statements in this presentation and oral statements made at this conference that are

Keefe, Bruyette & Woods Insurance Conference. September 7, 2005

Keefe, Bruyette & Woods Insurance Conference September 7, 2005 What We Will Cover Radian: A legacy of innovation and success Facing new challenges and opportunities Focusing on creating value Well positioned

Keefe, Bruyette & Woods Insurance Conference September 7, 2005 What We Will Cover Radian: A legacy of innovation and success Facing new challenges and opportunities Focusing on creating value Well positioned

Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem

Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem Juan Ospina 1 Harald Uhlig 1 1 Department of Economics University of Chicago July 20, 2016 Outline Post Mortem post mortem: an

Mortgage-Backed Securities and the Financial Crisis of 2008: a Post Mortem Juan Ospina 1 Harald Uhlig 1 1 Department of Economics University of Chicago July 20, 2016 Outline Post Mortem post mortem: an

Global Financial Crisis

Global Financial Crisis Hand in the homework that is due today What caused the Global Financial Crisis? We ll focus today on Financial Innovation and Regulatory Issues Other issues have been cited, including

Global Financial Crisis Hand in the homework that is due today What caused the Global Financial Crisis? We ll focus today on Financial Innovation and Regulatory Issues Other issues have been cited, including

Fannie Mae Reports Net Income of $2.0 Billion and Comprehensive Income of $2.2 Billion for Third Quarter 2015

Resource Center: 1-800-732-6643 Contact: Date: Pete Bakel 202-752-2034 November 5, 2015 Fannie Mae Reports Net Income of 2.0 Billion and Comprehensive Income of 2.2 Billion for Third Quarter 2015 Fannie

Resource Center: 1-800-732-6643 Contact: Date: Pete Bakel 202-752-2034 November 5, 2015 Fannie Mae Reports Net Income of 2.0 Billion and Comprehensive Income of 2.2 Billion for Third Quarter 2015 Fannie

Fannie Mae Reports Third-Quarter 2010 Results

Resource Center: 1-800-732-6643 Contacts: Number: Todd Davenport 202-752-5115 5214a Date: November 5, 2010 Fannie Mae Reports Third-Quarter 2010 Results Net Loss of $1.3 Billion Reflects Stabilizing Credit-Related

Resource Center: 1-800-732-6643 Contacts: Number: Todd Davenport 202-752-5115 5214a Date: November 5, 2010 Fannie Mae Reports Third-Quarter 2010 Results Net Loss of $1.3 Billion Reflects Stabilizing Credit-Related

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You?

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You? 1 2 2 3 3 4 Commercial real

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You? 1 2 2 3 3 4 Commercial real

Federated Adjustable Rate Securities Fund

Prospectus October 31, 2018 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Prospectus October 31, 2018 The information contained herein relates to all classes of the Fund s Shares, as listed below, unless otherwise noted. Share Class Ticker Institutional FEUGX Service FASSX Federated

Home Affordable Refinance Program

Home Affordable Refinance Program This paper is about HARP. We will explain what the program is about and how it can help many people get their mortgage payments into an affordable range. About HARP Home

Home Affordable Refinance Program This paper is about HARP. We will explain what the program is about and how it can help many people get their mortgage payments into an affordable range. About HARP Home

Lesson 13: Applying for a Mortgage Loan

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 1 of 64 341 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit

February 5, Dear Secretary Geithner:

The Honorable Timothy F. Geithner Secretary of the Treasury U.S. Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Dear Secretary Geithner: The Mortgage Bankers Association 1

The Honorable Timothy F. Geithner Secretary of the Treasury U.S. Department of the Treasury 1500 Pennsylvania Avenue, NW Washington, DC 20220 Dear Secretary Geithner: The Mortgage Bankers Association 1

Econ 330 Exam 2 Name ID Section Number

Econ 330 Exam 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When financial institutions go on a lending spree and expand

Econ 330 Exam 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When financial institutions go on a lending spree and expand

The Financial Crisis of 2008 and Subprime Securities. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2008 and Subprime Securities Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Paula Tkac Federal Reserve Bank of Atlanta Subprime mortgages are commonly

The Financial Crisis of 2008 and Subprime Securities Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Paula Tkac Federal Reserve Bank of Atlanta Subprime mortgages are commonly

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

Safe Harbor Statement

Third Quarter 2009 Safe Harbor Statement All statements made during today s investor presentation and in these webcast slides that address events, developments or results that we expect or anticipate may

Third Quarter 2009 Safe Harbor Statement All statements made during today s investor presentation and in these webcast slides that address events, developments or results that we expect or anticipate may

STRUCTURED ASSET SECURITIES CORPORATION

PROSPECTUS SUPPLEMENT (To Prospectus dated January 25, 2005) $706,107,000 (Approximate) STRUCTURED ASSET SECURITIES CORPORATION Pass-Through Certificates, Series 2005-NC1 Aurora Loan Services LLC Master

PROSPECTUS SUPPLEMENT (To Prospectus dated January 25, 2005) $706,107,000 (Approximate) STRUCTURED ASSET SECURITIES CORPORATION Pass-Through Certificates, Series 2005-NC1 Aurora Loan Services LLC Master

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

From Wall Street to Main Street: The Financial Crisis in the US

From Wall Street to Main Street: The Financial Crisis in the US Douglas J. Young Professor of Economics, Montana State University Indian Institute of Technology - Bombay Sabbatical Other Activities Extension-type

From Wall Street to Main Street: The Financial Crisis in the US Douglas J. Young Professor of Economics, Montana State University Indian Institute of Technology - Bombay Sabbatical Other Activities Extension-type

September 30, These government programs have helped stabilize the economy over the last year.

September 30, 2009 Macro Economic Update The International Monetary Fund has recently projected that global writedowns on loans and investments will total $3.4 trillion between 2007 and 2010. The banking

September 30, 2009 Macro Economic Update The International Monetary Fund has recently projected that global writedowns on loans and investments will total $3.4 trillion between 2007 and 2010. The banking

The Current Real Estate Finance Climate

The Current Real Estate Finance Climate Elizabeth J. Zook, Esq. Carruthers & Roth, P.A. (336) 478-1110 December 10, 2008 Residenti tial Housing Market Subprime Mortgage Crisis i Ongoing financial crisis

The Current Real Estate Finance Climate Elizabeth J. Zook, Esq. Carruthers & Roth, P.A. (336) 478-1110 December 10, 2008 Residenti tial Housing Market Subprime Mortgage Crisis i Ongoing financial crisis

Prospectus Supplement dated September 12, 2006 (To Prospectus dated June 29, 2006)

") Prospectus Supplement dated September 12, 2006 (To Prospectus dated June 29, 2006) $768,119,000 (Approximate) Citigroup Loan Trust 2006-NC2 Issuing Entity Asset-Backed Pass-Through Certificates, Series

Prospectus Supplement dated September 12, 2006 (To Prospectus dated June 29, 2006) $768,119,000 (Approximate) Citigroup Loan Trust 2006-NC2 Issuing Entity Asset-Backed Pass-Through Certificates, Series

Wall Street and Commercial Real Estate

Wall Street and Commercial Real Estate Everett Allen Greer March 16, 2011 Los Angeles Los Angeles 213.985.3800 New York 646.867.1600 San Francisco 415.233.6300 Dallas 214.347.7500 Greer Miami Advisors,

Wall Street and Commercial Real Estate Everett Allen Greer March 16, 2011 Los Angeles Los Angeles 213.985.3800 New York 646.867.1600 San Francisco 415.233.6300 Dallas 214.347.7500 Greer Miami Advisors,

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?

Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

OUTLINE November 1, Review: PPF & AD. How close an output gap? Output Gap & Multiplier 10/31/2017 1:25 PM. Overview of Policy

OUTLINE November 1, 2017 Overview of Policy Contractionary and Expansionary Policy Fiscal and Monetary Policy The Financial Crisis of 2007-09 Great Recession Midterm tonight (if that s news, we should

OUTLINE November 1, 2017 Overview of Policy Contractionary and Expansionary Policy Fiscal and Monetary Policy The Financial Crisis of 2007-09 Great Recession Midterm tonight (if that s news, we should

e-brief Not Here? Housing Market Policy and the Risk of a Housing Bust

e-brief August 31, 2010 FINANCIAL SERVICES Not Here? Housing Market Policy and the Risk of a Housing Bust By Jim MacGee Can a US-style housing bust happen in Canada? Recent swings in Canadian house prices

e-brief August 31, 2010 FINANCIAL SERVICES Not Here? Housing Market Policy and the Risk of a Housing Bust By Jim MacGee Can a US-style housing bust happen in Canada? Recent swings in Canadian house prices

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

GLOBAL FINANCIAL CRISIS 2008

GLOBAL FINANCIAL CRISIS 2008 Background Information Credit Crunch Comes Full Cycle Implications on Services Sector / Main Street and Information Services NOVEMBER 21, 2008 Joachim C. Bartels Founder and

GLOBAL FINANCIAL CRISIS 2008 Background Information Credit Crunch Comes Full Cycle Implications on Services Sector / Main Street and Information Services NOVEMBER 21, 2008 Joachim C. Bartels Founder and

The Financial Turmoil in 2007 and 2008

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

Mortgage Market Statistical Annual 2017 Yearbook. Table of Contents

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

CREDIT RISK MANAGEMENT GUIDANCE FOR HOME EQUITY LENDING

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision National Credit Union Administration CREDIT

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of Thrift Supervision National Credit Union Administration CREDIT

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom?

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

Did Affordable Housing Legislation Contribute to the Subprime Securities Boom? Andra C. Ghent (Arizona State University) Rubén Hernández-Murillo (FRB St. Louis) and Michael T. Owyang (FRB St. Louis) Government

2008 STOCK MARKET COLLAPSE

2008 STOCK MARKET COLLAPSE Will Pickerign A FINACIAL INSTITUTION PERSECTIVE QUOTE In one way, I m Sympathetic to the institutional reluctance to face the music - Warren Buffet (Fortune 8/16/2007) RECAP

2008 STOCK MARKET COLLAPSE Will Pickerign A FINACIAL INSTITUTION PERSECTIVE QUOTE In one way, I m Sympathetic to the institutional reluctance to face the music - Warren Buffet (Fortune 8/16/2007) RECAP

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance Prof. Stijn Van Nieuwerburgh New York University Stern School of Business March 1, 2011 Published by Princeton University

Guaranteed to Fail Fannie Mae, Freddie Mac and the Debacle of US Housing Finance Prof. Stijn Van Nieuwerburgh New York University Stern School of Business March 1, 2011 Published by Princeton University

New York Mortgage Trust Reports Fourth Quarter 2017 Results

February 20, 2018 New York Mortgage Trust Reports Fourth Quarter Results NEW YORK, Feb. 20, 2018 (GLOBE NEWSWIRE) -- New York Mortgage Trust, Inc. (Nasdaq:NYMT) ("NYMT," the "Company," "we," "our" or "us")

February 20, 2018 New York Mortgage Trust Reports Fourth Quarter Results NEW YORK, Feb. 20, 2018 (GLOBE NEWSWIRE) -- New York Mortgage Trust, Inc. (Nasdaq:NYMT) ("NYMT," the "Company," "we," "our" or "us")

Federated Adjustable Rate Securities Fund

Prospectus October 31, 2012 Share Class Institutional Service Ticker FEUGX FASSX The information contained herein relates to all classes of the Fund s Shares, as listed above, unless otherwise noted. Federated

Prospectus October 31, 2012 Share Class Institutional Service Ticker FEUGX FASSX The information contained herein relates to all classes of the Fund s Shares, as listed above, unless otherwise noted. Federated

1 Anthony B. Sanders, Ph.D. is Professor of Finance at the School of Management at George Mason University

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Sub-prime mortgages are just a niche within the US residential mortgage

4 The sub-prime mortgage crisis: a synopsis Karen Weaver Sub-prime mortgages are just a niche within the US residential mortgage lending market, yet in 2007 they took centre stage in the global financial

4 The sub-prime mortgage crisis: a synopsis Karen Weaver Sub-prime mortgages are just a niche within the US residential mortgage lending market, yet in 2007 they took centre stage in the global financial

Economic and Banking Outlook. Major issues

/1/9 Economic and Banking Outlook May 9 Major issues Consumer spending recovering? Investment t spending lagging? Housing inventories will take years to clear Bank credit losses will remain high through

/1/9 Economic and Banking Outlook May 9 Major issues Consumer spending recovering? Investment t spending lagging? Housing inventories will take years to clear Bank credit losses will remain high through

An Overview of WMMSC, WAAC, and WCC

Permanent Subcommittee on Investigations Page 1 of 6 Chairman Levin, Doctor Coburn, and members of the Permanent Subcommittee, my name is David Beck. From April 2003 through September 2008 I worked at

Permanent Subcommittee on Investigations Page 1 of 6 Chairman Levin, Doctor Coburn, and members of the Permanent Subcommittee, my name is David Beck. From April 2003 through September 2008 I worked at

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

UFS. Fixed Income. John Rosenthal Senior Managing Director MetLife

UFS Fixed Income John Rosenthal Senior Managing Director MetLife Safe Harbor Statement These materials contain statements which constitute forward-looking statements within the meaning of the Private Securities

UFS Fixed Income John Rosenthal Senior Managing Director MetLife Safe Harbor Statement These materials contain statements which constitute forward-looking statements within the meaning of the Private Securities

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 10-K. For the transition period from to.

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

Basics in Mortgage Lending Test for Loan Officers

Basics in Mortgage Lending Test for Loan Officers Name: Date: Company Name: 1. The purpose of the Equal Credit Opportunity Act is: To discourage predatory lending To create new avenues and programs for

Basics in Mortgage Lending Test for Loan Officers Name: Date: Company Name: 1. The purpose of the Equal Credit Opportunity Act is: To discourage predatory lending To create new avenues and programs for

Exhibit 3 with corrections through Memorandum

Exhibit 3 with corrections through 4.21.10 Memorandum High LTV, Subprime and Alt-A Originations Over the Period 1992-2007 and Fannie, Freddie, FHA and VA s Role Edward Pinto Consultant to mortgage-finance

Exhibit 3 with corrections through 4.21.10 Memorandum High LTV, Subprime and Alt-A Originations Over the Period 1992-2007 and Fannie, Freddie, FHA and VA s Role Edward Pinto Consultant to mortgage-finance

The level of demand for our mortgage loans may decrease as a result of rising interest rates, which could adversely impact our earnings.

RISK F A C T O RS T H A T M A Y A F F E C T F U T UR E R ESU L TS RISKS R E L A T E D T O O UR BUSIN ESS G E N E R A L L Y The level of demand for our mortgage loans may decrease as a result of rising

RISK F A C T O RS T H A T M A Y A F F E C T F U T UR E R ESU L TS RISKS R E L A T E D T O O UR BUSIN ESS G E N E R A L L Y The level of demand for our mortgage loans may decrease as a result of rising

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Conventional Financing

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of conventional loans, qualifying standards

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of conventional loans, qualifying standards

Mike Lombardi, FCIA, FSA, MAAA, CERA

Mike Lombardi, FCIA, FSA, MAAA, CERA Mike Lombardi is a managing principal of Tillinghast Towers Perrin and has been with its Toronto office since 1991. He specializes in providing actuarial advice with

Mike Lombardi, FCIA, FSA, MAAA, CERA Mike Lombardi is a managing principal of Tillinghast Towers Perrin and has been with its Toronto office since 1991. He specializes in providing actuarial advice with