Global Financial Crisis

|

|

|

- Debra Hudson

- 5 years ago

- Views:

Transcription

1 Global Financial Crisis Hand in the homework that is due today What caused the Global Financial Crisis? We ll focus today on Financial Innovation and Regulatory Issues Other issues have been cited, including monetary policy errors, capital inflows from abroad. Prof. Bonham has placed several short pieces about todays material online.

2 Housing boom and bust surge in home prices Why? Housing prices began to fall in 2007 Delinquencies and foreclosures surged 20% failure rate on sub-prime mortgages 650! 569! 488! 406! 325! 244! 163! 81! 0! 1980Q1! 1985Q1! 1990Q1! 1995Q1! 2000Q1! 2005Q1! San Diego! Los Angeles! Sacramento! Stockton!

3 Financial Market Fallout 2007: Crisis in markets for mortgage-related assets Large losses at hedge funds from credit default swaps» mortgage bond guaranteeing Credit rating downgrades of subprime products Prices of mortgage-backed securities fell and demand dried up Banks began to write down mortgage-related assets Some institutions were unable to raise needed funds Two key crisis events were outside the U.S.: In August 2007, French bank BNP Paribas froze redemptions saying couldn t value underlying securities UK bank Northern Rock bailed out in Sep 2007 Fed and other central banks began aggressive response

4 Financial Market Fallout 2008: Credit conditions continued to worsen March: Bear Sterns Sep: Fannie Mae and Freddie Mac Sep. 15: Lehman Bros. Sep. 16: AIG Sep. 25: WAMU Credit markets froze up US and world entered most severe recession since 1930s How did the structure and operation of financial markets and institutions cause this?

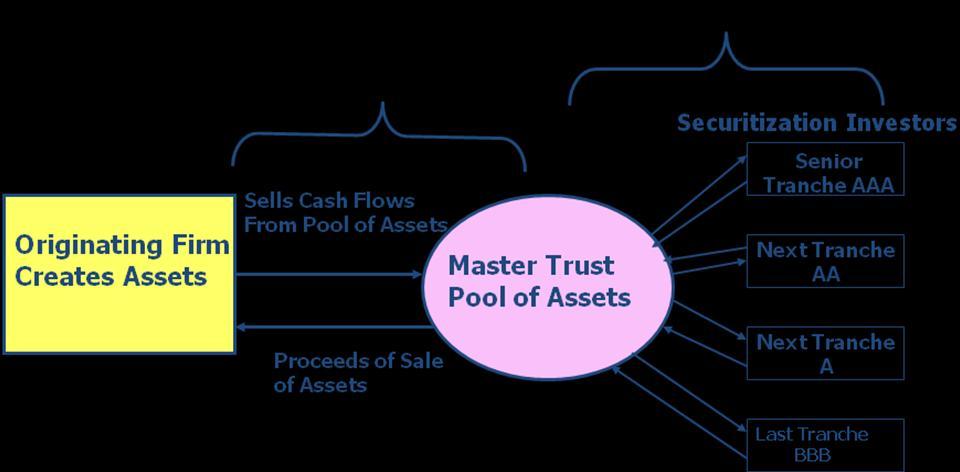

5 Mortgage lending What is the traditional model for mortgage lending? Banks make loans and hold loans as income-earning assets How is most of it done now? A bank or loan originating company (e.g. Countrywide) makes a loan and then sells it» In U.S. Fannie Mae and Freddie Mac or private financial institution They securitize the loans and sell them to investors The originate-to-distribute model

6 Originate-to-Distribute Model "

7 Creating asset backed securities

8 Collateralized Debt Obligations This is a form of collateralized debt obligation (CDO) What are the benefits of such structured finance? Pooling lowers risk through diversification Subordination allows some highly-rated securities» Credit default swaps can be used to reduce risk further» Some investors can only hold highly-rated securities Security sales can tap large pool of funds This all means lower interest rates, greater access to credit And risk is channeled to investors who are willing to bear it

9 Growth of CDO Market Why did it grow so fast? financial innovation growth of non-bank financial institutions low interest rate environment rapid home price appreciation

10 Mortgage meltdown Prices of mortgage credit default swaps ABX price AAA AA A BBB BBB- Jan07 Mar07 May07 Jul07 Sep07 Nov07 Jan08 Mar08 May08 Jan09 Nov08 Sep08 Jul08

11 What went wrong? Exposure to losses was much larger than believed Underestimation of potential home price decline Correlation of losses Some securitized asset structures magnified losses» CDO-squared MarketPlace video Lack of transparency made it harder for investors to assess risk Incentive problems in structured finance» Loan originators have no skin in the game Poor monitoring

12 Poor monitoring led to falling credit quality Total= 2,215 2,885 3,945 2,920 3,120 2,980 2,430 1,800 (annualized) FHA/VA Conforming Jumbo HEL Alt-A Subprime Q4 (annualized)

13 What went wrong? Incentive problems in structured finance (continued) The rating agencies What do the rating agencies do?» Why have the grown in importance over the years? What is their particular role in structured finance?» What are the potential problems with reliance on rating agencies? Incentives for issuing investment bank? Incentives for rating agencies?» What went wrong?» How might we fix it? See Lowenstein, Roger, Triple-A Failure: The Ratings Game, New York Times, April 27,

14 What went wrong? Little or no regulation of non-bank financial institutions Severe maturity mismatches Very high leverage ratios, facilitated by regulatory changes and regulatory arbitrage» Why is high leverage attractive? Dangerous? Banks set up structured investment vehicles (SIVs) to hold asset backed securities (also called more generally special purpose vehicles» But banks were still threatened. Why? Liquidity backstops

15 Leverage at U.S. Investment Banks

16 Why did it spread beyond mortgages? Why did a crisis in a relatively limited part of the markets turn into a full-blown financial crisis? Borrower balance sheet effects» Loss spiral asset price falls -> must sell assets to correct balance sheet -> asset sales cause further asset price declines -> etc.» Margin / haircut spiral. With increased assessments of risk, larger margins are required -> must reduce leverage -> asset sales -> as in loss spiral. Lending channel» Precautionary hoarding by banks and nonbanks. Runs on nonbank financial institutions» E.g. hedge funds pulling money out of Bear Sterns; AIG forced to post more collateral

17 Why did it spread beyond mortgages? Network effects» Counterparty risk. The argument for saving AIG. See Brunnermeier, Markus K. Deciphering the Liquidity and Credit Crunch , Journal of Economic Perspectives 23:1, Winter 2009,

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know April13, 2010 Agenda Introduction Presentation Steve Herscovici, Managing Principal, Analysis Group Bill Chambers, Finance

Credit Rating Agencies and the Credit Crisis: What Securities Attorneys Need to Know April13, 2010 Agenda Introduction Presentation Steve Herscovici, Managing Principal, Analysis Group Bill Chambers, Finance

Capital Market Trends and Forecasts

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

The Financial Crisis. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

Why is the Country Facing a Financial Crisis?

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

The Financial Crisis of 2008 and Subprime Securities. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2008 and Subprime Securities Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Paula Tkac Federal Reserve Bank of Atlanta Subprime mortgages are commonly

The Financial Crisis of 2008 and Subprime Securities Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Paula Tkac Federal Reserve Bank of Atlanta Subprime mortgages are commonly

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Leveraged Losses: Lessons from the Mortgage Market Meltdown

Leveraged Losses: Lessons from the Mortgage Market Meltdown David Greenlaw, Jan Hatzius, Anil K Kashyap, Hyun Song Shin US Monetary Policy Forum Conference Draft February 29, 2008 Outline: Characterize

Leveraged Losses: Lessons from the Mortgage Market Meltdown David Greenlaw, Jan Hatzius, Anil K Kashyap, Hyun Song Shin US Monetary Policy Forum Conference Draft February 29, 2008 Outline: Characterize

Lessons from the Failures in Risk Management during The Subprime Crisis

Lessons from the Failures in Risk Management during The Subprime Crisis Michel Crouhy Head of Research & Development NATIXIS Corporate and Investment Bank Michel.crouhy@natixis.com Conference on Quantitative

Lessons from the Failures in Risk Management during The Subprime Crisis Michel Crouhy Head of Research & Development NATIXIS Corporate and Investment Bank Michel.crouhy@natixis.com Conference on Quantitative

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Econ 330 Exam 2 Name ID Section Number

Econ 330 Exam 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When financial institutions go on a lending spree and expand

Econ 330 Exam 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When financial institutions go on a lending spree and expand

The Financial Crisis and the Bailout

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference May 13, 2008 Janet L. Yellen President and CEO Federal Reserve Bank of San Francisco Overview Financial

Credit, Housing, Commodities and the Economy Chartered Financial Analysts Institute Annual Conference May 13, 2008 Janet L. Yellen President and CEO Federal Reserve Bank of San Francisco Overview Financial

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

DECIPHERING THE ? LIQUIDITY AND CREDIT CRUNCH. Markus K. Brunnermeier

1 DECIPHERING THE 2007-0? LIQUIDITY AND CREDIT CRUNCH Markus K. Brunnermeier http://www.princeton.edu/~markus Overview of Talk 2 1. Run-up Originate and distribute banking model Shadow banking system (SIVs,

1 DECIPHERING THE 2007-0? LIQUIDITY AND CREDIT CRUNCH Markus K. Brunnermeier http://www.princeton.edu/~markus Overview of Talk 2 1. Run-up Originate and distribute banking model Shadow banking system (SIVs,

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Sub-prime mortgages are just a niche within the US residential mortgage

4 The sub-prime mortgage crisis: a synopsis Karen Weaver Sub-prime mortgages are just a niche within the US residential mortgage lending market, yet in 2007 they took centre stage in the global financial

4 The sub-prime mortgage crisis: a synopsis Karen Weaver Sub-prime mortgages are just a niche within the US residential mortgage lending market, yet in 2007 they took centre stage in the global financial

1. What was life like in Iceland before the financial crisis? 3. How much did Iceland s three banks borrow? What happened to the money?

E&F/Raffel Inside Job Directed by Charles Ferguson Intro: The Case of Iceland 1. What was life like in Iceland before the financial crisis? 2. What changed in 2000? 3. How much did Iceland s three banks

E&F/Raffel Inside Job Directed by Charles Ferguson Intro: The Case of Iceland 1. What was life like in Iceland before the financial crisis? 2. What changed in 2000? 3. How much did Iceland s three banks

The Sub Prime Debacle and Financial Turmoil

The Sub Prime Debacle and Financial Turmoil Presented at the 13th Finsia and Melbourne Centre for Financial Studies Banking and Finance Conference Monday 29th and Tuesday 30th September, 2008 The University

The Sub Prime Debacle and Financial Turmoil Presented at the 13th Finsia and Melbourne Centre for Financial Studies Banking and Finance Conference Monday 29th and Tuesday 30th September, 2008 The University

Chapter 11 11/18/2014. Mortgages and Mortgage Markets. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Investor Presentation. February 11, 2014

Investor Presentation February 11, 2014 Information Related to Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform

Investor Presentation February 11, 2014 Information Related to Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP NOTE-TAKING COLUMN: Complete this section during the video. Include definitions and

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP NOTE-TAKING COLUMN: Complete this section during the video. Include definitions and

The Future of the Mortgage Market: Where Do We Go From Here?

The Future of the Mortgage Market: Where Do We Go From Here? Stuart Gabriel, Director of the Ziman Center for Real Estate, Arden Realty Chair and Professor of Finance, Anderson School of Management, University

The Future of the Mortgage Market: Where Do We Go From Here? Stuart Gabriel, Director of the Ziman Center for Real Estate, Arden Realty Chair and Professor of Finance, Anderson School of Management, University

Subprime: Tentacles. How could a modest increase in. of a Crisis

Run on the United Kingdom s Northern Rock bank, a fallout from the U.S. subprime crisis. Subprime: Tentacles of a Crisis Randall Dodd How could a modest increase in seriously delinquent subprime mortgages,

Run on the United Kingdom s Northern Rock bank, a fallout from the U.S. subprime crisis. Subprime: Tentacles of a Crisis Randall Dodd How could a modest increase in seriously delinquent subprime mortgages,

Money and Banking ECON3303. Lecture 9: Financial Crises. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Notice regarding Revisions of Earnings Forecasts

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

Capital Markets Update

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Residential Lending "Changing Directions"

Residential Lending "Changing Directions" Community Banker Conference Andrew Olszowy Manager - Consumer Compliance Team October 25, 2007 Federal Reserve Bank of Boston 1 Residential Lending Then, Circa

Residential Lending "Changing Directions" Community Banker Conference Andrew Olszowy Manager - Consumer Compliance Team October 25, 2007 Federal Reserve Bank of Boston 1 Residential Lending Then, Circa

Beryl Credit Pulse on Structured Finance

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

Chapter 8. Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

The Rise and Fall of Securitization

Wisconsin School of Business October 31, 2012 The rise and fall of home values 210 800 190 700 170 600 150 500 130 400 110 300 90 200 70 100 50 1985 1990 1995 2000 2005 2010 Home values 0 Source: Case

Wisconsin School of Business October 31, 2012 The rise and fall of home values 210 800 190 700 170 600 150 500 130 400 110 300 90 200 70 100 50 1985 1990 1995 2000 2005 2010 Home values 0 Source: Case

Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation

Harvard University From the SelectedWorks of William Werkmeister Spring April, 2010 Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation William Werkmeister,

Harvard University From the SelectedWorks of William Werkmeister Spring April, 2010 Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation William Werkmeister,

Group 14 Dallas Hall, Chuck Dobson, Guy Tahye, Tunde Olabiyi

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

The Subprime Crisis. Literature: Blanchard, O. (2009), The Crisis: Basic Mechanisms, and Appropriate Policies, IMF, WP 09/80.

, The Crisis: Basic Mechanisms, and Appropriate Policies, IMF, WP 09/80.") The Subprime Crisis Literature: Blanchard, O. (2009), The Crisis: Basic Mechanisms, and Appropriate Policies, IMF, WP 09/80. Hellwig, Martin (2008), The Causes of the Financial Crisis, CESifo Forum 9 (4),

The Subprime Crisis Literature: Blanchard, O. (2009), The Crisis: Basic Mechanisms, and Appropriate Policies, IMF, WP 09/80. Hellwig, Martin (2008), The Causes of the Financial Crisis, CESifo Forum 9 (4),

Too Big to Fail Causes, Consequences and Policy Responses. Philip E. Strahan. Annual Review of Financial Economics Conference.

Too Big to Fail Causes, Consequences and Policy Responses Philip E. Strahan Annual Review of Financial Economics Conference October, 13 Too Big to Fail is a credibility problem Markets expect creditors

Too Big to Fail Causes, Consequences and Policy Responses Philip E. Strahan Annual Review of Financial Economics Conference October, 13 Too Big to Fail is a credibility problem Markets expect creditors

Safe Harbor Statement

Third Quarter 2009 Safe Harbor Statement All statements made during today s investor presentation and in these webcast slides that address events, developments or results that we expect or anticipate may

Third Quarter 2009 Safe Harbor Statement All statements made during today s investor presentation and in these webcast slides that address events, developments or results that we expect or anticipate may

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

The Mortgage and Housing Market Outlook

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Mike Lombardi, FCIA, FSA, MAAA, CERA

Mike Lombardi, FCIA, FSA, MAAA, CERA Mike Lombardi is a managing principal of Tillinghast Towers Perrin and has been with its Toronto office since 1991. He specializes in providing actuarial advice with

Mike Lombardi, FCIA, FSA, MAAA, CERA Mike Lombardi is a managing principal of Tillinghast Towers Perrin and has been with its Toronto office since 1991. He specializes in providing actuarial advice with

Capital structure and the financial crisis

Capital structure and the financial crisis Richard H. Fosberg William Paterson University Journal of Finance and Accountancy Abstract The financial crisis on the late 2000s had a major impact on the financial

Capital structure and the financial crisis Richard H. Fosberg William Paterson University Journal of Finance and Accountancy Abstract The financial crisis on the late 2000s had a major impact on the financial

The Financial Crisis of ? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

Making Securitization Work for Financial Stability and Economic Growth

Shadow Financial Regulatory Committees of Asia, Australia-New Zealand, Europe, Japan, Latin America, and the United States Making Securitization Work for Financial Stability and Economic Growth Joint Statement

Shadow Financial Regulatory Committees of Asia, Australia-New Zealand, Europe, Japan, Latin America, and the United States Making Securitization Work for Financial Stability and Economic Growth Joint Statement

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Complexities of the Financial Turmoil of 2007 and 2008

The Complexities of the Financial Turmoil of 2007 and 2008 Gregory A. Krohn Bucknell University William R. Gruver Bucknell University Sparked by rising defaults on subprime mortgages, the financial turmoil

The Complexities of the Financial Turmoil of 2007 and 2008 Gregory A. Krohn Bucknell University William R. Gruver Bucknell University Sparked by rising defaults on subprime mortgages, the financial turmoil

OUTLINE November 1, Review: PPF & AD. How close an output gap? Output Gap & Multiplier 10/31/2017 1:25 PM. Overview of Policy

OUTLINE November 1, 2017 Overview of Policy Contractionary and Expansionary Policy Fiscal and Monetary Policy The Financial Crisis of 2007-09 Great Recession Midterm tonight (if that s news, we should

OUTLINE November 1, 2017 Overview of Policy Contractionary and Expansionary Policy Fiscal and Monetary Policy The Financial Crisis of 2007-09 Great Recession Midterm tonight (if that s news, we should

WHAT THE REALLY HAPPENED...

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

The Credit Crisis in Commercial Real Estate

The Credit Crisis in Commercial Real Estate 1 Summary Commercial real estate accounts for a meaningful 6.5% of GDP Commercial real estate entered the recession in reasonable balance The credit crisis creates

The Credit Crisis in Commercial Real Estate 1 Summary Commercial real estate accounts for a meaningful 6.5% of GDP Commercial real estate entered the recession in reasonable balance The credit crisis creates

The Rise and Fall of the U.S. Mortgage and Credit Markets

The Rise and Fall of the U.S. Mortgage and Credit Markets Wednesday, April 29, 2009 11:00 AM - 12:15 PM Moderator: Rick Newman Chief Business Correspondent, U.S. News & World Report Speakers: James Barth,

The Rise and Fall of the U.S. Mortgage and Credit Markets Wednesday, April 29, 2009 11:00 AM - 12:15 PM Moderator: Rick Newman Chief Business Correspondent, U.S. News & World Report Speakers: James Barth,

Lecture 26 Exchange Rates The Financial Crisis. Noah Williams

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

Selected Financial Information <under Japanese GAAP> For the first quarter ended June 30, Mitsubishi UFJ Financial Group, Inc.

Selected Financial Information ended June 30, 2008 Mitsubishi UFJ Financial Group, Inc. [Contents] Starting in this fiscal year, MUFG has adopted the Accounting Standards for Quarterly

Selected Financial Information ended June 30, 2008 Mitsubishi UFJ Financial Group, Inc. [Contents] Starting in this fiscal year, MUFG has adopted the Accounting Standards for Quarterly

NAR Research on the Impact of Jumbo Mortgage Credit Crunch

NAR Research on the Impact of Jumbo Mortgage Credit Crunch Introduction Mortgage rates are at 50 year lows, thereby raising housing affordability conditions to all-time high levels. However, the historically

NAR Research on the Impact of Jumbo Mortgage Credit Crunch Introduction Mortgage rates are at 50 year lows, thereby raising housing affordability conditions to all-time high levels. However, the historically

Housing and Mortgage Market Update

Housing and Mortgage Market Update VCU Real Estate Trends Conference October 14, 29 Amy Crews Cutts, PhD Deputy Chief Economist Recession Risks Still Elevated, Housing Contraction Ongoing Recession risks

Housing and Mortgage Market Update VCU Real Estate Trends Conference October 14, 29 Amy Crews Cutts, PhD Deputy Chief Economist Recession Risks Still Elevated, Housing Contraction Ongoing Recession risks

Financial Crises: The Great Depression and the Great Recession

Financial Crises: The Great Depression and the Great Recession ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 43 Readings Mishkin Ch. 12 Bernanke (2002): On Milton

Financial Crises: The Great Depression and the Great Recession ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 43 Readings Mishkin Ch. 12 Bernanke (2002): On Milton

Mortgage REITs. March 20, Calvin Schnure Senior Vice President, Research & Economic Analysis

Mortgage REITs March 20, 2018 Calvin Schnure Senior Vice President, Research & Economic Analysis cschnure@nareit.com, 202-739-9434 Executive Summary Mortgage REITs (mreits) are companies that finance residential

Mortgage REITs March 20, 2018 Calvin Schnure Senior Vice President, Research & Economic Analysis cschnure@nareit.com, 202-739-9434 Executive Summary Mortgage REITs (mreits) are companies that finance residential

Two Harbors Investment Corp.

Two Harbors Investment Corp. Webinar Series October 2013 Fundamental Concepts in Hedging Welcoming Remarks William Roth Chief Investment Officer July Hugen Director of Investor Relations 2 Safe Harbor

Two Harbors Investment Corp. Webinar Series October 2013 Fundamental Concepts in Hedging Welcoming Remarks William Roth Chief Investment Officer July Hugen Director of Investor Relations 2 Safe Harbor

Would Islamic Finance have prevented the global financial crisis?

La Trobe University Islamic Banking and Finance Symposium Would Islamic Finance have prevented the global financial crisis? Mohammed Amin PwC Overview Preamble Global financial crisis - effects Global

La Trobe University Islamic Banking and Finance Symposium Would Islamic Finance have prevented the global financial crisis? Mohammed Amin PwC Overview Preamble Global financial crisis - effects Global

SUB PRIME CRISIS & EUROZONE CRISIS. Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts)

") SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

The Financial Turmoil in 2007 and 2008 Events

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

Financial Bubbling: from the Asian Crisis to the Subprime Mess

Financial Bubbling: from the Asian Crisis to the Subprime Mess University of Bari by Giovanni Ferri (University of Bari) Workshop The complexity of financial crisis in a long-period perspective: facts,

Financial Bubbling: from the Asian Crisis to the Subprime Mess University of Bari by Giovanni Ferri (University of Bari) Workshop The complexity of financial crisis in a long-period perspective: facts,

The Subprime Market Meltdown: Crisis or Opportunity?

The Subprime Market Meltdown: Crisis or Opportunity? Jonathan Beinner CIO and Co-Head, US and Global Fixed Income, GSM Tom Teles Head, Mortgage Backed Securities, GSM July 10, 2007 Discussion outline.

The Subprime Market Meltdown: Crisis or Opportunity? Jonathan Beinner CIO and Co-Head, US and Global Fixed Income, GSM Tom Teles Head, Mortgage Backed Securities, GSM July 10, 2007 Discussion outline.

Lecture 25 Unemployment Financial Crisis. Noah Williams

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

OCTOBER 1, 2007 RECORDED CALL TRANSCRIPT

ART TILDESLEY Good morning. This is Art Tildesley, Director of Investor Relations at Citigroup. I am here with Chuck Prince, our Chairman and Chief Executive Officer, and Gary Crittenden, our Chief Financial

ART TILDESLEY Good morning. This is Art Tildesley, Director of Investor Relations at Citigroup. I am here with Chuck Prince, our Chairman and Chief Executive Officer, and Gary Crittenden, our Chief Financial

THE FINANCIAL CRISIS: WHAT CAUSED IT?

THE FINANCIAL CRISIS: WHAT CAUSED IT? Martin Neil Baily With the assistance of Matt Johnson Long version. Draft of April 1, 2008 Prepared for the American-European Conference, Brookings, Institut Montaigne,

THE FINANCIAL CRISIS: WHAT CAUSED IT? Martin Neil Baily With the assistance of Matt Johnson Long version. Draft of April 1, 2008 Prepared for the American-European Conference, Brookings, Institut Montaigne,

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions. Ingrid Gould Ellen

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

Deposit Insurance or Lender of Last Resort

Deposit Insurance or Lender of Last Resort Cecchetti compares deposit insurance and lender of last resort as means to prevent banking crises Deposit Insurance could actually increase the probability of

Deposit Insurance or Lender of Last Resort Cecchetti compares deposit insurance and lender of last resort as means to prevent banking crises Deposit Insurance could actually increase the probability of

11/9/2017. Chapter 11. Mortgages and Mortgage Markets. Traditional and Modern Housing Finance: From S&Ls to Securities. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

The Great Recession. ECON 43370: Financial Crises. Eric Sims. Spring University of Notre Dame

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

Keefe, Bruyette & Woods Insurance Conference. September 7, 2005

Keefe, Bruyette & Woods Insurance Conference September 7, 2005 What We Will Cover Radian: A legacy of innovation and success Facing new challenges and opportunities Focusing on creating value Well positioned

Keefe, Bruyette & Woods Insurance Conference September 7, 2005 What We Will Cover Radian: A legacy of innovation and success Facing new challenges and opportunities Focusing on creating value Well positioned

SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure

No achievement without commitment SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure Conference Call Tuesday March 27, 27 Jacques Guerber Vice-Chairman of the Management

No achievement without commitment SUB-PRIME US RESIDENTIAL MORTGAGES Analysis and Overview of Dexia Group s Exposure Conference Call Tuesday March 27, 27 Jacques Guerber Vice-Chairman of the Management

P1: a/b P2: c/d QC: e/f T1: g c01 JWBT092-Acharya February 19, :48 Printer: Courier Westford

PART One Causes of the Financial Crisis of 2007 2009 Matthew Richardson There is almost universal agreement that the fundamental cause of the financial crisis was the combination of a credit boom and a

PART One Causes of the Financial Crisis of 2007 2009 Matthew Richardson There is almost universal agreement that the fundamental cause of the financial crisis was the combination of a credit boom and a

LOOKING BEHIND THE AGGREGATES: A REPLY TO FACTS AND MYTHS ABOUT THE FINANCIAL CRISIS OF 2008

LOOKING BEHIND THE AGGREGATES: A REPLY TO FACTS AND MYTHS ABOUT THE FINANCIAL CRISIS OF 28 Working Paper No. QAU8-5 Ethan Cohen-Cole Burcu Duygan-Bump Jose Fillat Judit Montoriol-Garriga Federal Reserve

LOOKING BEHIND THE AGGREGATES: A REPLY TO FACTS AND MYTHS ABOUT THE FINANCIAL CRISIS OF 28 Working Paper No. QAU8-5 Ethan Cohen-Cole Burcu Duygan-Bump Jose Fillat Judit Montoriol-Garriga Federal Reserve

Chapter 14. The Mortgage Markets. Chapter Preview

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

Chapter 14 The Mortgage Markets Chapter Preview The average price of a U.S. home is well over $208,000. For most of us, home ownership would be impossible without borrowing most of the cost of a home.

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT The lending industry is overdue for disruption Potential for Disruption Low High Mortgage SMB Loans International

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT The lending industry is overdue for disruption Potential for Disruption Low High Mortgage SMB Loans International

The US Housing Market Crisis and Its Aftermath

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

Financial Crisis Impact on Long Term Ag Forecast

1 Financial Crisis Impact on Long Term Ag Forecast Paul N. Ellinger University of Illinois pellinge@illinois.edu www.farmdoc.uiuc.edu/ellinger 217-333-5503 Economic Conditions Surging commodity prices

1 Financial Crisis Impact on Long Term Ag Forecast Paul N. Ellinger University of Illinois pellinge@illinois.edu www.farmdoc.uiuc.edu/ellinger 217-333-5503 Economic Conditions Surging commodity prices

GLOBAL FINANCIAL CRISIS 2008

GLOBAL FINANCIAL CRISIS 2008 Background Information Credit Crunch Comes Full Cycle Implications on Services Sector / Main Street and Information Services NOVEMBER 21, 2008 Joachim C. Bartels Founder and

GLOBAL FINANCIAL CRISIS 2008 Background Information Credit Crunch Comes Full Cycle Implications on Services Sector / Main Street and Information Services NOVEMBER 21, 2008 Joachim C. Bartels Founder and

Ivan Gjaja (212) Natalia Nekipelova (212)

Natalia Nekipelova (212)") Ivan Gjaja (212) 816-8320 ivan.m.gjaja@ssmb.com Natalia Nekipelova (212) 816-8075 natalia.nekipelova@ssmb.com In a departure from seasonal patterns, January speeds were 1% CPR higher than December speeds.

Ivan Gjaja (212) 816-8320 ivan.m.gjaja@ssmb.com Natalia Nekipelova (212) 816-8075 natalia.nekipelova@ssmb.com In a departure from seasonal patterns, January speeds were 1% CPR higher than December speeds.

Black Monday Exploring Current Financial Crisis

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

The Financial Turmoil in 2007 and 2008

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

1. Asymmetric Information and Financial Crises (45 points, 40 minutes)

") Final Exam, Fall 2008 Answer the following essay questions in two to three blue book pages each. Be sure to fully explain your answers using economic reasoning and any equations and/or graphs needed to

Final Exam, Fall 2008 Answer the following essay questions in two to three blue book pages each. Be sure to fully explain your answers using economic reasoning and any equations and/or graphs needed to

4) The dark side of financial liberalization is. A) market allocations B) credit booms C) currency appreciation D) financial innovation

The dark side of financial liberalization is. A) market allocations B) credit booms C) currency appreciation D) financial innovation") Chapter 9 Financial Crises 1) A major disruption in financial markets characterized by sharp declines in asset prices and firm failures is called a A) financial crisis B) fiscal imbalance C) free-rider

Chapter 9 Financial Crises 1) A major disruption in financial markets characterized by sharp declines in asset prices and firm failures is called a A) financial crisis B) fiscal imbalance C) free-rider

The year 2008 marked a watershed for

Financial Turmoil and the Economy Economic Research Economic Research, the other areas contributing to this report, and the Legal department are part of an interdepartmental committee the Federal Reserve

Financial Turmoil and the Economy Economic Research Economic Research, the other areas contributing to this report, and the Legal department are part of an interdepartmental committee the Federal Reserve

R cession Economics NBER says U.S. recession began December 2007

Recession Economics Christopher Thornberg Founding Principal, Beacon Economics NBER says U.S. recession began December 2007 MonDec1, 12:20pmET WASHINGTON (Reuters) The U.S. economy slipped into recession

Recession Economics Christopher Thornberg Founding Principal, Beacon Economics NBER says U.S. recession began December 2007 MonDec1, 12:20pmET WASHINGTON (Reuters) The U.S. economy slipped into recession

II. What went wrong in risk modeling. IV. Appendix: Need for second generation pricing models for credit derivatives

Risk Models and Model Risk Michel Crouhy NATIXIS Corporate and Investment Bank Federal Reserve Bank of Chicago European Central Bank Eleventh Annual International Banking Conference: : Implications for

Risk Models and Model Risk Michel Crouhy NATIXIS Corporate and Investment Bank Federal Reserve Bank of Chicago European Central Bank Eleventh Annual International Banking Conference: : Implications for

The Mortgage Debt Market: A Tragedy

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

The Post-Crisis World: Where Will Agency MBSs Trade?

The Post-Crisis World: Where Will Agency MBSs Trade? Financial Engineering Practitioners Seminar DEPT. OF INDUSTRIAL ENGINEERING AND OPERATIONS RESEARCH SCHOOL OF ENGINEERING AND APPLIED SCIENCE COLUMBIA

The Post-Crisis World: Where Will Agency MBSs Trade? Financial Engineering Practitioners Seminar DEPT. OF INDUSTRIAL ENGINEERING AND OPERATIONS RESEARCH SCHOOL OF ENGINEERING AND APPLIED SCIENCE COLUMBIA

Stylized Financial System

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

Global Financial Crisis and Regulatory Reforms

Global Financial Crisis and Regulatory Reforms NERO meeting at the OECD in Paris September 21, 2009 Mitsuhiro Fukao Japan Center for Economic Research fukao@jcer.or.jp 1 1. Similarity of Japanese and the

Global Financial Crisis and Regulatory Reforms NERO meeting at the OECD in Paris September 21, 2009 Mitsuhiro Fukao Japan Center for Economic Research fukao@jcer.or.jp 1 1. Similarity of Japanese and the

March 2017 For intermediaries and professional investors only. Not for further distribution.

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

1.2 Product nature of credit derivatives

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

Ten years after: Implications of the current financial market turmoil. Dr. Atchana Waiquamdee Deputy Governor Bank of Thailand

Ten years after: Implications of the current financial market turmoil Dr. Atchana Waiquamdee Deputy Governor Bank of Thailand I. The 1997 East Asia Crisis II. Latest Episode Causes of the 1997 Crisis 3

Ten years after: Implications of the current financial market turmoil Dr. Atchana Waiquamdee Deputy Governor Bank of Thailand I. The 1997 East Asia Crisis II. Latest Episode Causes of the 1997 Crisis 3

Investor Presentation. May 13, 2013

Investor Presentation May 13, 2013 Information Related to Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform

Investor Presentation May 13, 2013 Information Related to Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform

The Financial Crisis. Yale. Marinus van Reymerswaele, 1567

The Financial Crisis Gary Gorton Yale Marinus van Reymerswaele, 1567 What is the crisis? What you saw: firms fail, get acquired, or get bailed out (Lehman Brothers, Bear Stearns, Merrill Lynch, AIG); people

The Financial Crisis Gary Gorton Yale Marinus van Reymerswaele, 1567 What is the crisis? What you saw: firms fail, get acquired, or get bailed out (Lehman Brothers, Bear Stearns, Merrill Lynch, AIG); people

The Causes of the 2008 Financial Crisis

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

MORTGAGE MARKETS AND THE ENTERPRISES IN July 2008

MORTGAGE MARKETS AND THE ENTERPRISES IN 2007 July 2008 Preface This Office of Federal Housing Enterprise Oversight (OFHEO) research paper reviews developments in the housing sector and the primary and

MORTGAGE MARKETS AND THE ENTERPRISES IN 2007 July 2008 Preface This Office of Federal Housing Enterprise Oversight (OFHEO) research paper reviews developments in the housing sector and the primary and

e-brief Not Here? Housing Market Policy and the Risk of a Housing Bust

e-brief August 31, 2010 FINANCIAL SERVICES Not Here? Housing Market Policy and the Risk of a Housing Bust By Jim MacGee Can a US-style housing bust happen in Canada? Recent swings in Canadian house prices

e-brief August 31, 2010 FINANCIAL SERVICES Not Here? Housing Market Policy and the Risk of a Housing Bust By Jim MacGee Can a US-style housing bust happen in Canada? Recent swings in Canadian house prices

Interim earnings update 15 October 2008

Interim earnings update 15 October 2008 Publication scheme for 15 October 2008 8.00 a.m. CEST - Press release and Powerpoint presentation available on www.kbc.com 9.30 a.m. CEST - Teleconference for financial

Interim earnings update 15 October 2008 Publication scheme for 15 October 2008 8.00 a.m. CEST - Press release and Powerpoint presentation available on www.kbc.com 9.30 a.m. CEST - Teleconference for financial