Mike Lombardi, FCIA, FSA, MAAA, CERA

|

|

|

- Victor Walsh

- 5 years ago

- Views:

Transcription

1 Mike Lombardi, FCIA, FSA, MAAA, CERA Mike Lombardi is a managing principal of Tillinghast Towers Perrin and has been with its Toronto office since He specializes in providing actuarial advice with respect to insurance mergers and acquisitions, demutualization, and Canadian insurance company financial reporting. Mr. Lombardi is currently the appointed actuary for four Canadian branches or subsidiaries and regularly peer reviews the work of appointed actuaries for a number of other insurance companies. Mr. Lombardi is a member of the Canadian Institute of Actuaries Committee on Professional Conduct. Since 2004, his role has included reviewing all cases involving professional actuarial misconduct and recommending appropriate discipline action. Mr. Lombardi is a frequent speaker and moderator at industry seminars, and he has authored various articles in Canadian and U.S. life insurance trade publications, such as Emphasis, Marketing Options, Investment Executive, the SOA Financial Reporting Newsletter and the CIA Bulletin. He has appeared on TV in the Report on Business channel to discuss life insurance shareholder value management practices.

2 Mike Lombardi, FCIA, FSA, MAAA, CERA Mr. Lombardi has served on a variety of professional committees of the Society of Actuaries (SOA) and the Canadian Institute of Actuaries (CIA). Most recently, this included chairman of the Committee on the Role of the Appointed Actuary committee, chairman of the Appointed Actuary program committee, member of the Practice Standards Council, and member of the CIA Board of Directors. In June 2003, he became President of the Canadian Institute of Actuaries. In August, 2005 he was elected Vice-President of the Society of Actuaries. Currently, he is chair of the CIA s international committee the Committee on International Relations. Mr. Lombardi holds a B.Sc. from McGill University and a management certificate from the University of Western Ontario. He is a Fellow of the Canadian Institute of Actuaries, a Fellow of the Society of Actuaries and a Member of the American Academy of Actuaries.

3 What went wrong? Actuarial perspectives on the global financial crisis Pacific Rim Actuaries Club of Toronto Mike Lombardi February 19, 2009

4 Agenda actions by the Treasury, the Fed, the FDIC, and by Congress to keep financial system and our economy together. Causes Government policies post 9/11 era excessive liquidity rapid expansion of home ownership explosion of so-called non-traditional loans sub-prime mortgages creative payment terms 2

5 Overview Current crisis is global collapse of the housing market crisis in the global financial markets collapse of the stock markets a global recession Desperate attempts to prevent a 1930s depression lowest interest rates in decades collapse of large financial institutions billions spent by governments worldwide on bank bailouts billions more to stimulate economies via deficit spending Questions how did we get here? what has been the impact on insurance companies? what are the lessons learned? 3

6 U.S Sub-prime mortgage crisis Causes Boom in the housing market High-risk mortgage loans and lending practices Inaccurate credit ratings Government and central bank policies 4

7 Boom in the housing market Background Central banks and government policy success in fight against inflation interest rates dropping for over 10 years US government policy encouraging home ownership Economy mild recessions low unemployment end of business cycles? stock and real estate prices start rising interest rates low, spreads narrow 5

8 Boom in the housing market Background Consumer low interest rates encourage consumer spending and debt house prices constantly rising if can t pay mortgage, can sell for a gain at a higher price incentive to refinance existing mortgages speculators purchased second, third and fourth homes, condos, and apartments Home=$$$=ATM 6

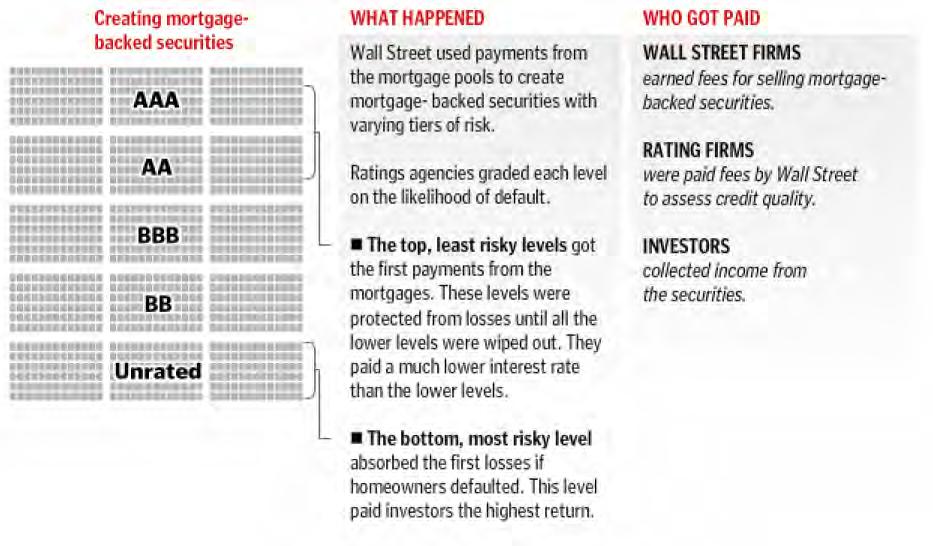

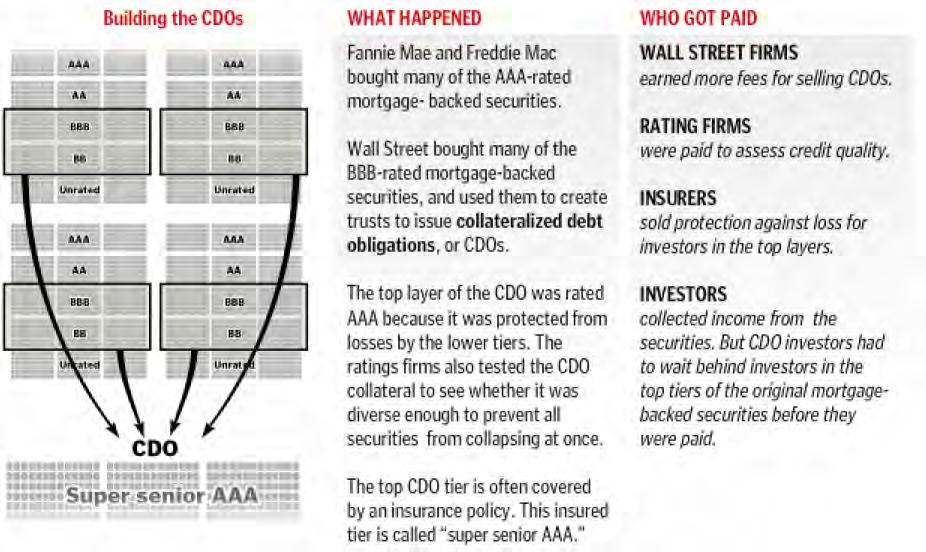

9 Boom in the housing market (cont d) Investors hungry for ways to achieve higher yields very attracted to highly rated instruments with superior spreads securitization mortgage backed securities (MBS) derivatives.collateralized debt obligations (CDO) Investment bankers (MS, GS, Merrill Lynch, Bear Stearns) slice, dice individual mortgages into pools of MBS and CDO transfer risk by selling units to investors, pension funds, insurance companies, hedge funds, and other investment bankers different layers (or tranches ) had different risks Highest rated Lower rated Last tranche (unrated) Low, safe return Higher return, moderate risk Highest return, highest risk 7

10 Agenda 8

11 Agenda 9

12 Boom in the housing market Bank can t issue mortgages fast enough to keep up with demand investment banker ready to buy any and all mortgages low underwriting standards since risk is being passed on easy money>>>no need to wait 30 years for profits to mature Investment banker not worried about risk expect to quickly flip to hedge fund, pension funds, insurance companies, other investment bankers AIG, AMBAC, MBIA facilitate securitization provide guarantees to enhance ratings provide default insurance (via credit default swap) on financial instruments 10

13 High-risk mortgage loans and lending practices Business model has changed!!!! Originate and hold becomes originate and distribute Brokers>>>mortgage banks>>>investment banks>>>investors Decline in underwriting standards growth in sub-prime low or no documentation stated income will suffice NINJA mortgages : No Income, No Job, no Assets no money down interest only mortgage teaser rates and Adjustable Rate Mortgages (ARM) negative amortization mortgages 11

14 Inaccurate credit ratings Model assumptions based on historic studies investment bankers not experienced at looking at individual mortgages but instead look at overall pools originate and hold data used to forecast very different originate and distribute underwriting experience based on historic default experience nobody worried because even if mortgage buyers default, prices are higher little or no loss of principal for investor high ratings encouraged investors to buy securities backed by subprime mortgages investors were unable or unwilling to perform own due diligence relied on ratings rating agencies and conflicts of interest paid by investment banks 12

15 Government and central bank policies Government policies only added fuel to fire Social policy belief that home ownership was way to wealth for all banks not permitted to discriminate in lending practices (Community Reinvestment Act ) needed to meet quotas on loans to minorities investment bankers were ready buyers for sub prime mortgages Deregulation policy discouraged government interference in market practices no action taken against fraud, misleading sales, and weakening underwriting standards Monetary policy interest rates kept low for too long after dot-com and 9/11 low interest rates and easy money multiplied the money supply bubble got bigger and out of control when interest rates finally raised, housing market crashed 13

16 Agenda 14

17 MBS and CDO risks Credit risk Asset price risk Liquidity risk Counterparty risk the risk that the homeowner or borrower will be unable or unwilling to pay back the loan the risk that assets (MBS in this case) will depreciate in value, resulting in financial losses, markdowns and possibly margin calls the risk that a business entity will be unable to obtain financing the risk that a party to a contract will be unable or unwilling to uphold their obligations. The aggregate effect of these and other risks has recently been called systemic risk which refers to when formerly uncorrelated risks shift and become highly correlated, damaging the entire financial system 15

18 Boom and bust in the housing market Causes 16

19 Agenda 17

20 Agenda 18

21 Deleveraging pressures Effect of a 75% write-down 10 to 1 leverage Assets Liabilities Assets Liabilities Surplus 4 10 Surplus % asset value write-down means surplus drops by 30% 19

22 Deleveraging pressures Effect of a 75% write-down 33 to 1 leverage Assets Liabilities Assets Liabilities Surplus Surplus % asset value write-down means surplus is wiped out! 20

23 Agenda actions by the Treasury, the Fed, the FDIC, and by Congress to keep financial system and our economy together. Causes Government policies post 9/11 era excessive liquidity rapid expansion of home ownership explosion of so-called non-traditional loans sub-prime mortgages creative payment terms 21

24 BBB tranche price movements 22

25 AA tranche price movements 23

26 AAA tranche price movements 24

27 Financial crisis arrives Vicious credit cycle Market withdrawal High credit losses Rating instability Tighter underwriting Global credit crunch Liquidity crisis Financial institution problems Government intervention Investment losses in bank and hedge funds portfolios globally Deleveraging Lack of confidence Intensifying deleveraging Collapse of Bear Stearns Government takeover of GSEs (Fannie Mae and Freddie Mac) Lehman, Merrill,WAMU, Wachovia TARP-toxic asset purchase plan FDIC Liquidity guarantees Capital purchase programs TARP focus shifts to preferred share capital 25

28 Agenda actions by the Treasury, the Fed, the FDIC, and by Congress to keep financial system and our economy together. Causes Government policies post 9/11 era excessive liquidity rapid expansion of home ownership explosion of so-called non-traditional loans sub-prime mortgages creative payment terms 26

29 Stock market movements since last year 27

30 Volatility index is dramatically higher 28

31 Global decline in interest rates 29

32 Agenda 30

33 Corporate A bonds spreads exceed 500 bps! 31

34 Currencies: US dollar and Japanese yen are in high demand 32

35 Credit default swaps represent trillions of dollars 33

36 Insurance company issues Consequences of current environment Increase in unrealized capital losses Low yields = higher liability values More policyholder options in-the-money Segregated funds UL minimum interest rate guarantees Lower asset values = lower fees Deteriorating capital ratios Difficulty in raising debt or additional capital 34

37 Insurance company issues Risk management priorities Managing balance sheet volatility Exposure to defaults ALM programs Hedging programs Re-pricing products Regulatory solvency Rating agency downgrades Analyst and investor confidence Reputation risk 35

38 Values of insurance companies have collapsed 36

39 Values of insurance companies have collapsed 37

40 Outlook for insurance industry Depends on future scenario Recovery to pre-crisis Reserves release (CALM and seg fund guarantees) Improvement in fee based income Default charges reversed Market value of equities increase Narrower credit spreads negative for bond reinvestments but positive for market value of bond assets Improved MCCSR ratios Current level continues Stable reserves and MCCSR Lower fee income Deepening crisis Further reserve strengthening Further deterioration in fee based income More defaults Market value of equities decrease Deteriorating MCCSR ratios 38

41 Actuarial Perspectives: Regulation and risk management Financial accounting and regulation consistent accounting, regulation and capital requirements banks and insurers different countries avoidance of regulatory and accounting arbitrage capital requirements need to be dynamic and responsive to changing risk (example: no capital charge for subprime mortgage) counter cyclical regulations Risk management models important but need to be validated VaR measures minimum tail risk, unlike CTE which measures expected tail risk Risk culture remuneration incentives need to be aligned with risk risk management should be more than compliance Independence of chief risk officer subject to professional standards CERA designation 39

42 Lessons learned (or relearned) Default assumptions Asset growth assumptions Model complexity Stress testing ignored Lack of due diligence Conflict of interest Anti-selection Counter-party risk Not enough capital Assumption that riskier mortgages would behave no different from past Assumption that house prices would never fall Customized by bankers, difficult to validate Models showed impact of higher defaults but it was dismissed as unlikely to ever happen Investors did not do own scrutiny Investment bankers did not check quality of mortgages Rating agencies paid by investment banker to make deal possible Unaffordable product Intermediaries profited from sale Intermediaries not at risk Will AIG and other writers of default insurers honour their obligations? Highly leveraged, unregulated investment bankers (30 to 1) 40

43 Lessons learned (or relearned) Tail risks Liquidity risk Duration mismatch Off balance sheet risks Non regulated entities (Shadow banking system) Self-regulation Risk management Black swan events do happen Markets can evaporate, even for highly rated investments Don t use short term funds to invest long term Just because a risk is not on your balance sheet doesn t mean it s gone Hedge funds, private equity, sovereign funds, etc. operate outside the banking system Can frustrate analysis and policy solutions Sometimes becomes no regulation Did anybody know what was going on? Was anyone listening? 41

44 Open questions for debate Should we regulate the shadow banking system (hedge funds, investment banks, non-regulated entities).. Should the government buy up bad assets Are incentive bonuses necessary to encourage excellent performance. Was this a failure in risk management Will current fiscal and monetary policy avoid a prolonged recession.. Is mark-to-market accounting to blame. Should accounting standards be designed to be counter-cyclical... Would actuaries have made a difference. why and how? or should it inject more capital and/or nationalize banks?..or do they encourage reckless risktaking? or was it proof that we need it more than ever?.or will they only create a different problem of high debt and high inflation? or is it a necessary tool to reveal the truth?.or should this be the role of capital standards? why or why not? 42

45 Questions? 43

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Money and Banking ECON3303. Lecture 9: Financial Crises. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP NOTE-TAKING COLUMN: Complete this section during the video. Include definitions and

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP NOTE-TAKING COLUMN: Complete this section during the video. Include definitions and

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

The Causes of the 2008 Financial Crisis

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

The Mortgage Debt Market: A Tragedy

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Chapter 8. Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Global Financial Crisis

Global Financial Crisis Hand in the homework that is due today What caused the Global Financial Crisis? We ll focus today on Financial Innovation and Regulatory Issues Other issues have been cited, including

Global Financial Crisis Hand in the homework that is due today What caused the Global Financial Crisis? We ll focus today on Financial Innovation and Regulatory Issues Other issues have been cited, including

SUB PRIME CRISIS & EUROZONE CRISIS. Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts)

") SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

2008 STOCK MARKET COLLAPSE

2008 STOCK MARKET COLLAPSE Will Pickerign A FINACIAL INSTITUTION PERSECTIVE QUOTE In one way, I m Sympathetic to the institutional reluctance to face the music - Warren Buffet (Fortune 8/16/2007) RECAP

2008 STOCK MARKET COLLAPSE Will Pickerign A FINACIAL INSTITUTION PERSECTIVE QUOTE In one way, I m Sympathetic to the institutional reluctance to face the music - Warren Buffet (Fortune 8/16/2007) RECAP

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Capital Market Trends and Forecasts

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

The Recession

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

The Role of Ethics in the Current Financial Crisis: The Ethics of Securitization. John R. Boatright Loyola University Chicago

The Role of Ethics in the Current Financial Crisis: The Ethics of Securitization John R. Boatright Loyola University Chicago The Crisis is a Failure of... Market actors (mortgage companies, commercial/

The Role of Ethics in the Current Financial Crisis: The Ethics of Securitization John R. Boatright Loyola University Chicago The Crisis is a Failure of... Market actors (mortgage companies, commercial/

THE FINANCIAL CRISIS AND THE GREAT RECESSION

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

WHAT THE REALLY HAPPENED...

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

Making Securitization Work for Financial Stability and Economic Growth

Shadow Financial Regulatory Committees of Asia, Australia-New Zealand, Europe, Japan, Latin America, and the United States Making Securitization Work for Financial Stability and Economic Growth Joint Statement

Shadow Financial Regulatory Committees of Asia, Australia-New Zealand, Europe, Japan, Latin America, and the United States Making Securitization Work for Financial Stability and Economic Growth Joint Statement

Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation

Harvard University From the SelectedWorks of William Werkmeister Spring April, 2010 Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation William Werkmeister,

Harvard University From the SelectedWorks of William Werkmeister Spring April, 2010 Financial Crisis 101: A Beginner's Guide to Structured Finance, Financial Crisis, and Market Regulation William Werkmeister,

Historical Backdrop to the 2007/08 Liquidity Crunch

/08 Liquidity Historical /08 Liquidity Christopher G. Lamoureux October 1, /08 Liquidity Long Term Capital Management August 17, Russian Government restructured debt. Relatively minor event that shook

/08 Liquidity Historical /08 Liquidity Christopher G. Lamoureux October 1, /08 Liquidity Long Term Capital Management August 17, Russian Government restructured debt. Relatively minor event that shook

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS22932 Credit Default Swaps: Frequently Asked Questions Edward Vincent Murphy, Government and Finance Division September

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS22932 Credit Default Swaps: Frequently Asked Questions Edward Vincent Murphy, Government and Finance Division September

The Mortgage Industry

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?

Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Introduction and Economic Landscape. Vance Ginn Spring 2013

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

The Financial Crisis. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

Group 14 Dallas Hall, Chuck Dobson, Guy Tahye, Tunde Olabiyi

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

1. What was life like in Iceland before the financial crisis? 3. How much did Iceland s three banks borrow? What happened to the money?

E&F/Raffel Inside Job Directed by Charles Ferguson Intro: The Case of Iceland 1. What was life like in Iceland before the financial crisis? 2. What changed in 2000? 3. How much did Iceland s three banks

E&F/Raffel Inside Job Directed by Charles Ferguson Intro: The Case of Iceland 1. What was life like in Iceland before the financial crisis? 2. What changed in 2000? 3. How much did Iceland s three banks

Econ 330 Exam 2 Name ID Section Number

Econ 330 Exam 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When financial institutions go on a lending spree and expand

Econ 330 Exam 2 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When financial institutions go on a lending spree and expand

The Financial Systems Complexity

The Financial Systems Complexity Some Data on the Financial System The Role of the Financial System Information Challenges & the Financial System Government Regulation and Supervision Financial Panics:

The Financial Systems Complexity Some Data on the Financial System The Role of the Financial System Information Challenges & the Financial System Government Regulation and Supervision Financial Panics:

I. Learning Objectives II. The Functions of Money III. The Components of the Money Supply

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

Lecture 25 Unemployment Financial Crisis. Noah Williams

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

A Multi-Agent Model of Financial Stability and Credit Risk Transfers of Banks Presentation for Bank of Italy Workshop on ABM in Banking and Finance: Turin Feb 9-11 Sheri Markose,, Yang Dong, Bewaji Oluwasegun

Don t Blame the Messenger or Ignore the Message. Ray Ball. The message? Highly leveraged institutions gambling heavily on risky, low-transparency

Don t Blame the Messenger or Ignore the Message Ray Ball The message? Highly leveraged institutions gambling heavily on risky, low-transparency securities are simply asking for trouble. To avoid future

Don t Blame the Messenger or Ignore the Message Ray Ball The message? Highly leveraged institutions gambling heavily on risky, low-transparency securities are simply asking for trouble. To avoid future

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Lecture 26 Exchange Rates The Financial Crisis. Noah Williams

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

Keefe, Bruyette & Woods Insurance Conference. September 7, 2005

Keefe, Bruyette & Woods Insurance Conference September 7, 2005 What We Will Cover Radian: A legacy of innovation and success Facing new challenges and opportunities Focusing on creating value Well positioned

Keefe, Bruyette & Woods Insurance Conference September 7, 2005 What We Will Cover Radian: A legacy of innovation and success Facing new challenges and opportunities Focusing on creating value Well positioned

Reflections on the Financial Crisis Allan H. Meltzer

Reflections on the Financial Crisis Allan H. Meltzer I am going to make several unrelated points, and then I am going to discuss how we got into this financial crisis and some needed changes to reduce

Reflections on the Financial Crisis Allan H. Meltzer I am going to make several unrelated points, and then I am going to discuss how we got into this financial crisis and some needed changes to reduce

The Financial Crisis and the Bailout

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

4) The dark side of financial liberalization is. A) market allocations B) credit booms C) currency appreciation D) financial innovation

The dark side of financial liberalization is. A) market allocations B) credit booms C) currency appreciation D) financial innovation") Chapter 9 Financial Crises 1) A major disruption in financial markets characterized by sharp declines in asset prices and firm failures is called a A) financial crisis B) fiscal imbalance C) free-rider

Chapter 9 Financial Crises 1) A major disruption in financial markets characterized by sharp declines in asset prices and firm failures is called a A) financial crisis B) fiscal imbalance C) free-rider

Martha Leiper Senior Vice President & Deputy Chief Investment Officer

Investment Strategies Corporate Level Martha Leiper Senior Vice President & Deputy Chief Investment Officer Southeastern Actuaries Conference November 21, 2008 Table of Contents Current Environment The

Investment Strategies Corporate Level Martha Leiper Senior Vice President & Deputy Chief Investment Officer Southeastern Actuaries Conference November 21, 2008 Table of Contents Current Environment The

Printable Lesson Materials

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Black Monday Exploring Current Financial Crisis

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

Comments on Hoshi and Kashyap,

Comments on Hoshi and Kashyap, Will US Bank Recapitalization Plan Succeed? Lessons from Japan Takatoshi Ito University of Tokyo AEA January 5, 2009 San Francisco Takatoshi Ito AEA 2009 1 Memorable Quotes,

Comments on Hoshi and Kashyap, Will US Bank Recapitalization Plan Succeed? Lessons from Japan Takatoshi Ito University of Tokyo AEA January 5, 2009 San Francisco Takatoshi Ito AEA 2009 1 Memorable Quotes,

FINANCIAL CRISES AGENDA

FINANCIAL CRISES A.Y. 2015/2016 Prof. Alberto Dreassi adreassi@units.it DEAMS University of Trieste AGENDA Recap on the role of financial institutions Why are there financial crises? Are they similar?

FINANCIAL CRISES A.Y. 2015/2016 Prof. Alberto Dreassi adreassi@units.it DEAMS University of Trieste AGENDA Recap on the role of financial institutions Why are there financial crises? Are they similar?

The Great Recession. ECON 43370: Financial Crises. Eric Sims. Spring University of Notre Dame

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

The Macro-economy and the Global Financial Crisis

The Macro-economy and the Global Financial Crisis Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Global economic

The Macro-economy and the Global Financial Crisis Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Global economic

Hearing on The Housing Decline: The Extent of the Problem and Potential Remedies December 13, 2007

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Why Regulate Shadow Banking? Ian Sheldon

Why Regulate Shadow Banking? Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Bank

Why Regulate Shadow Banking? Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Bank

Causes Of The Actual Global Financial Crisis. While many argue that this is the main cause of the global savings glut, the opposite is the

YourLastName 1 YourFirstName YourLastName Instructor's Name Course Title 1 August 2015 Causes Of The Actual Global Financial Crisis Introduction The US is one of the countries that have demonstrated their

YourLastName 1 YourFirstName YourLastName Instructor's Name Course Title 1 August 2015 Causes Of The Actual Global Financial Crisis Introduction The US is one of the countries that have demonstrated their

The Search for the Real Causes of the Current Global Financial Crisis: Role of Financial Innovations

The Search for the Real Causes of the Current Global Financial Crisis: Role of Financial Innovations Presentation at The Korea Institute for International Economic Policy Seoul, Korea Yoon-shik Park Professor

The Search for the Real Causes of the Current Global Financial Crisis: Role of Financial Innovations Presentation at The Korea Institute for International Economic Policy Seoul, Korea Yoon-shik Park Professor

Risk Management A Perspective on the Financial Crisis

Risk Management A Perspective on the Financial Crisis Ruairi O Healai June 2009 For Broker/Dealer Use Only at the European Capabilities Forum 24-26 June 2009 and Not to be Distributed to the Public Agenda

Risk Management A Perspective on the Financial Crisis Ruairi O Healai June 2009 For Broker/Dealer Use Only at the European Capabilities Forum 24-26 June 2009 and Not to be Distributed to the Public Agenda

OUTLINE November 1, Review: PPF & AD. How close an output gap? Output Gap & Multiplier 10/31/2017 1:25 PM. Overview of Policy

OUTLINE November 1, 2017 Overview of Policy Contractionary and Expansionary Policy Fiscal and Monetary Policy The Financial Crisis of 2007-09 Great Recession Midterm tonight (if that s news, we should

OUTLINE November 1, 2017 Overview of Policy Contractionary and Expansionary Policy Fiscal and Monetary Policy The Financial Crisis of 2007-09 Great Recession Midterm tonight (if that s news, we should

Protecting Financial Stability in the Era of Too Big to Fail

Page 1 Protecting Financial Stability in the Era of Too Big to Fail SPEAKING NOTES MICHÈLE BOURQUE, CDIC PRESIDENT AND CEO ECONOMIC CLUB OF CANADA 23 OCT. 2013, OTTAWA Introduction Good morning, I am pleased

Page 1 Protecting Financial Stability in the Era of Too Big to Fail SPEAKING NOTES MICHÈLE BOURQUE, CDIC PRESIDENT AND CEO ECONOMIC CLUB OF CANADA 23 OCT. 2013, OTTAWA Introduction Good morning, I am pleased

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Channeling Growth Capital to Small and Medium-Size Businesses. Global Conference 2010

Channeling Growth Capital to Small and Medium-Size Businesses Global Conference 2010 Channeling Growth Capital to Small and Medium-Size Businesses Wednesday, April 28, 2010; 6:30-7:45 AM Moderator: Betsy

Channeling Growth Capital to Small and Medium-Size Businesses Global Conference 2010 Channeling Growth Capital to Small and Medium-Size Businesses Wednesday, April 28, 2010; 6:30-7:45 AM Moderator: Betsy

The Financial Turmoil in 2007 and 2008 Events

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

Global Financial Crisis:

Global Financial Crisis: Causes and Consequences Dr. Prajapati Trivedi Senior Economist The World Bank Presentation Outline Meaning of Global Financial Crisis Causes Consequences Saudi Arabia India Global

Global Financial Crisis: Causes and Consequences Dr. Prajapati Trivedi Senior Economist The World Bank Presentation Outline Meaning of Global Financial Crisis Causes Consequences Saudi Arabia India Global

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of and

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of 1929-33 and 2007-09 David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009 Presentation

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of 1929-33 and 2007-09 David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009 Presentation

Manulife Financial Corporation Management s Discussion & Analysis. For the year ended December 31, 2017

Manulife Financial Corporation Management s Discussion & Analysis For the year ended December 31, 2017 Caution regarding forward-looking statements From time to time, Manulife Financial Corporation ( MFC

Manulife Financial Corporation Management s Discussion & Analysis For the year ended December 31, 2017 Caution regarding forward-looking statements From time to time, Manulife Financial Corporation ( MFC

Why Regulate Shadow Banking? Ian Sheldon

Why Regulate Shadow Banking? Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Bank

Why Regulate Shadow Banking? Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Bank

Ira G. PEPPERCORN. The Tragedy of the Mortgage Commons. President IRA PEPPERCORN INTERNATIONAL, LLC

The Tragedy of the Mortgage g Commons Ira G. PEPPERCORN President IRA PEPPERCORN INTERNATIONAL, LLC WORLD BANK-IFC WORKSHOP ON HOUSING FINANCE IN SOUTH ASIA JAKARTA INDONESIA MAY 28, 2009 U.S. Mortgage

The Tragedy of the Mortgage g Commons Ira G. PEPPERCORN President IRA PEPPERCORN INTERNATIONAL, LLC WORLD BANK-IFC WORKSHOP ON HOUSING FINANCE IN SOUTH ASIA JAKARTA INDONESIA MAY 28, 2009 U.S. Mortgage

Standardized Approach for Calculating the Solvency Buffer for Market Risk. Joint Committee of OSFI, AMF, and Assuris.

Standardized Approach for Calculating the Solvency Buffer for Market Risk Joint Committee of OSFI, AMF, and Assuris November 2008 DRAFT FOR COMMENT TABLE OF CONTENTS Introduction...3 Approach to Market

Standardized Approach for Calculating the Solvency Buffer for Market Risk Joint Committee of OSFI, AMF, and Assuris November 2008 DRAFT FOR COMMENT TABLE OF CONTENTS Introduction...3 Approach to Market

YIELD SPREAD PREMIUM and CREDIT DEFAULT SWAPS IN SECURITIZED RESIDENTIAL MORTGAGE LOANS by Neil F. Garfield, Esq. ALL RIGHTS RESERVED

5 10 YIELD SPREAD PREMIUM and CREDIT DEFAULT SWAPS IN SECURITIZED RESIDENTIAL MORTGAGE LOANS by Neil F. Garfield, Esq. ALL RIGHTS RESERVED In discussing yield spread premiums we have to define the three

5 10 YIELD SPREAD PREMIUM and CREDIT DEFAULT SWAPS IN SECURITIZED RESIDENTIAL MORTGAGE LOANS by Neil F. Garfield, Esq. ALL RIGHTS RESERVED In discussing yield spread premiums we have to define the three

off their risks, and a market may rise to meet the trading demand.

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) Only small companies can go through financial markets to obtain financing. 2) The reinvestment of cash back into the

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) Only small companies can go through financial markets to obtain financing. 2) The reinvestment of cash back into the

Notice regarding Revisions of Earnings Forecasts

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

To Whom It May Concern October 31, 2008 Listed Company: Mitsubishi UFJ Financial Group, Inc. Representative: Nobuo Kuroyanagi, President (Code:8306) Notice regarding Revisions of Earnings Forecasts Mitsubishi

Regulatory Proposals for Money Market Funds and Current Topics Affecting the Short-Term Investment Marketplace

Regulatory Proposals for Money Market Funds and Current Topics Affecting the Short-Term Investment Marketplace Presentation To: Presentation By: Joe Ulrey Chief Executive Officer Today s Topics Regulatory

Regulatory Proposals for Money Market Funds and Current Topics Affecting the Short-Term Investment Marketplace Presentation To: Presentation By: Joe Ulrey Chief Executive Officer Today s Topics Regulatory

March 2017 For intermediaries and professional investors only. Not for further distribution.

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

The Rise and Fall of the U.S. Mortgage and Credit Markets

The Rise and Fall of the U.S. Mortgage and Credit Markets Wednesday, April 29, 2009 11:00 AM - 12:15 PM Moderator: Rick Newman Chief Business Correspondent, U.S. News & World Report Speakers: James Barth,

The Rise and Fall of the U.S. Mortgage and Credit Markets Wednesday, April 29, 2009 11:00 AM - 12:15 PM Moderator: Rick Newman Chief Business Correspondent, U.S. News & World Report Speakers: James Barth,

Testimony of Keith Johnson. Former President of Clayton Holdings, Inc. and. Former President of Washington Mutual s Long Beach Mortgage

Testimony of Keith Johnson Former President of Clayton Holdings, Inc. and Former President of Washington Mutual s Long Beach Mortgage Before the Financial Crisis Inquiry Commission September 23, 2010 Chairman

Testimony of Keith Johnson Former President of Clayton Holdings, Inc. and Former President of Washington Mutual s Long Beach Mortgage Before the Financial Crisis Inquiry Commission September 23, 2010 Chairman

The 2008 crisis and the future: Have the important lessons been learned?

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

Chapter 11 11/18/2014. Mortgages and Mortgage Markets. Thrifts (continued)

") Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Mortgages and Mortgage Markets Chapter 11 Sources of Funds for Residential Mortgages McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Traditional and Modern

Lessons from the Failures in Risk Management during The Subprime Crisis

Lessons from the Failures in Risk Management during The Subprime Crisis Michel Crouhy Head of Research & Development NATIXIS Corporate and Investment Bank Michel.crouhy@natixis.com Conference on Quantitative

Lessons from the Failures in Risk Management during The Subprime Crisis Michel Crouhy Head of Research & Development NATIXIS Corporate and Investment Bank Michel.crouhy@natixis.com Conference on Quantitative

Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II

Derivatives Markets, Part II") November 2011 Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II A Review of Monoline Exposures Introduction This past August, ISDA published a short paper

November 2011 Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II A Review of Monoline Exposures Introduction This past August, ISDA published a short paper

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Did Poor Incentives Cause the Financial Crisis? Should Incentives and Pay Be Regulated?

Did Poor Incentives Cause the Financial Crisis? Should Incentives and Pay Be Regulated? Steven N. Kaplan University of Chicago Booth School of Business 1 2009 by S. Kaplan Two Questions: Did poorly designed

Did Poor Incentives Cause the Financial Crisis? Should Incentives and Pay Be Regulated? Steven N. Kaplan University of Chicago Booth School of Business 1 2009 by S. Kaplan Two Questions: Did poorly designed

Fannie Mae and Freddie Mac. Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons

Fannie Mae and Freddie Mac Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons Origins of Fannie Mae Great Depression New Deal Personal income, tax revenue, profits, and prices all drop

Fannie Mae and Freddie Mac Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons Origins of Fannie Mae Great Depression New Deal Personal income, tax revenue, profits, and prices all drop

Saving, Investment, and the Financial System

Chapter 9 MODERN PRINCIPLES OF ECONOMICS Third Edition Saving, Investment, and the Financial System Outline The Supply of Savings The Demand to Borrow Equilibrium in the Market for Loanable Funds The Role

Chapter 9 MODERN PRINCIPLES OF ECONOMICS Third Edition Saving, Investment, and the Financial System Outline The Supply of Savings The Demand to Borrow Equilibrium in the Market for Loanable Funds The Role

Financial Institutions and Markets 9TH EDITION

Financial Institutions and Markets 9TH EDITION JEFF MADURA Florida Atlantic University, SOUTH-WESTERN 1 CENGAGE Learning- Australia Brazil Japan Korea Mexico Singapore Spain United Kingdom United State

Financial Institutions and Markets 9TH EDITION JEFF MADURA Florida Atlantic University, SOUTH-WESTERN 1 CENGAGE Learning- Australia Brazil Japan Korea Mexico Singapore Spain United Kingdom United State

10 Years After the Financial Crisis: Where Do Shareholder Rights Stand?

NEW YORK PUERTO RICO / TEXAS / ILLINOIS / 845 THIRD AVENUE NEW YORK, NY 10022 (212) 759-4600 WOLFPOPPER.COM 10 Years After the Financial Crisis: Where Do Shareholder Rights Stand? Chet B. Waldman Wolf

NEW YORK PUERTO RICO / TEXAS / ILLINOIS / 845 THIRD AVENUE NEW YORK, NY 10022 (212) 759-4600 WOLFPOPPER.COM 10 Years After the Financial Crisis: Where Do Shareholder Rights Stand? Chet B. Waldman Wolf

Financial Reform. Jeremy Stein, Harvard University. A Conference in Honor of Elias M. Stein May 19, 2011

Financial Crisis and Financial Reform Jeremy Stein, Harvard University Analysis and Applications: A Conference in Honor of Elias M. Stein May 19, 2011 Overview How did we get into this mess? Short-run

Financial Crisis and Financial Reform Jeremy Stein, Harvard University Analysis and Applications: A Conference in Honor of Elias M. Stein May 19, 2011 Overview How did we get into this mess? Short-run

MORTGAGE INSURANCE: WHAT HAVE WE LEARNED? (PART 1)

") MORTGAGE INSURANCE: WHAT HAVE WE LEARNED? (PART 1) David McLaughry, FCAS, MAAA CAS Special Interest Seminar, Chicago, IL October 1, 2013 ANTI-TRUST NOTICE The Casualty Actuarial Society is committed to

MORTGAGE INSURANCE: WHAT HAVE WE LEARNED? (PART 1) David McLaughry, FCAS, MAAA CAS Special Interest Seminar, Chicago, IL October 1, 2013 ANTI-TRUST NOTICE The Casualty Actuarial Society is committed to

Securities Lending Outlook

WORLDWIDE SECURITIES SERVICES Outlook Managing Value Generation and Risk Securities lending and its risk/reward profile have been in the headlines as the credit and liquidity crisis has continued to unfold.

WORLDWIDE SECURITIES SERVICES Outlook Managing Value Generation and Risk Securities lending and its risk/reward profile have been in the headlines as the credit and liquidity crisis has continued to unfold.

September 30, These government programs have helped stabilize the economy over the last year.

September 30, 2009 Macro Economic Update The International Monetary Fund has recently projected that global writedowns on loans and investments will total $3.4 trillion between 2007 and 2010. The banking

September 30, 2009 Macro Economic Update The International Monetary Fund has recently projected that global writedowns on loans and investments will total $3.4 trillion between 2007 and 2010. The banking

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Financial Services A Crisis of Confidence

Moderated by: David Potterton, Global Head of Research Financial Services A Crisis of Confidence Webcast October 23, 2008 www.financial-insights.com Webcast Logistics Audio lines are muted until Q&A session

Moderated by: David Potterton, Global Head of Research Financial Services A Crisis of Confidence Webcast October 23, 2008 www.financial-insights.com Webcast Logistics Audio lines are muted until Q&A session

Beryl Credit Pulse on Structured Finance

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

Beryl Credit Pulse on Structured Finance This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the structured finance sector in light of the events of the past

Leveraged Losses: Lessons from the Mortgage Market Meltdown

Leveraged Losses: Lessons from the Mortgage Market Meltdown David Greenlaw, Jan Hatzius, Anil K Kashyap, Hyun Song Shin US Monetary Policy Forum Conference Draft February 29, 2008 Outline: Characterize

Leveraged Losses: Lessons from the Mortgage Market Meltdown David Greenlaw, Jan Hatzius, Anil K Kashyap, Hyun Song Shin US Monetary Policy Forum Conference Draft February 29, 2008 Outline: Characterize

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE FINANCIAL CRISIS INQUIRY COMMISSION.

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE FINANCIAL CRISIS INQUIRY COMMISSION July 1, 2010 Good afternoon Chairman Angelides, Vice Chairman Thomas and members

STATEMENT OF GARY GENSLER CHAIRMAN, COMMODITY FUTURES TRADING COMMISSION BEFORE THE FINANCIAL CRISIS INQUIRY COMMISSION July 1, 2010 Good afternoon Chairman Angelides, Vice Chairman Thomas and members

The Rise and Fall of Securitization

Wisconsin School of Business October 31, 2012 The rise and fall of home values 210 800 190 700 170 600 150 500 130 400 110 300 90 200 70 100 50 1985 1990 1995 2000 2005 2010 Home values 0 Source: Case

Wisconsin School of Business October 31, 2012 The rise and fall of home values 210 800 190 700 170 600 150 500 130 400 110 300 90 200 70 100 50 1985 1990 1995 2000 2005 2010 Home values 0 Source: Case

GLOBAL FINANCIAL CRISIS 2008

GLOBAL FINANCIAL CRISIS 2008 Background Information Credit Crunch Comes Full Cycle Implications on Services Sector / Main Street and Information Services NOVEMBER 21, 2008 Joachim C. Bartels Founder and

GLOBAL FINANCIAL CRISIS 2008 Background Information Credit Crunch Comes Full Cycle Implications on Services Sector / Main Street and Information Services NOVEMBER 21, 2008 Joachim C. Bartels Founder and

Testimony Concerning Regulation of Systemic Risk in the Financial Services Industry

Testimony Concerning Regulation of Systemic Risk in the Financial Services Industry Submitted for the Record By James Rech, Vice President, Risk Management and Financial Reporting Council of the American

Testimony Concerning Regulation of Systemic Risk in the Financial Services Industry Submitted for the Record By James Rech, Vice President, Risk Management and Financial Reporting Council of the American

2008 CRISIS : COLD OR CANCER?

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

The Sub Prime Debacle and Financial Turmoil

The Sub Prime Debacle and Financial Turmoil Presented at the 13th Finsia and Melbourne Centre for Financial Studies Banking and Finance Conference Monday 29th and Tuesday 30th September, 2008 The University

The Sub Prime Debacle and Financial Turmoil Presented at the 13th Finsia and Melbourne Centre for Financial Studies Banking and Finance Conference Monday 29th and Tuesday 30th September, 2008 The University

Strategic Allocaiton to High Yield Corporate Bonds Why Now?

Strategic Allocaiton to High Yield Corporate Bonds Why Now? May 11, 2015 by Matthew Kennedy of Rainier Investment Management HIGH YIELD CORPORATE BONDS - WHY NOW? The demand for higher yielding fixed income

Strategic Allocaiton to High Yield Corporate Bonds Why Now? May 11, 2015 by Matthew Kennedy of Rainier Investment Management HIGH YIELD CORPORATE BONDS - WHY NOW? The demand for higher yielding fixed income

Introduction... 3 Definitions... 3 Subprime loan... 3 Mortgage loan... 3

Table of Contents Introduction... 3 Definitions... 3 Subprime loan... 3 Mortgage loan... 3 Real estate and subprime lending in the US... 4 Politics... 4 The rise of subprime mortgages... 4 Risks with Subprime

Table of Contents Introduction... 3 Definitions... 3 Subprime loan... 3 Mortgage loan... 3 Real estate and subprime lending in the US... 4 Politics... 4 The rise of subprime mortgages... 4 Risks with Subprime

Financial Highlights

Financial Highlights 2001 2002 2003 Net income ($ millions) 639.1 629.2 493.9 Diluted earnings per share ($) 5.93 6.04 4.99 Return on equity (%) 22.7 19.3 13.7 Shareholders Equity ($ millions) 3,020 3,395

Financial Highlights 2001 2002 2003 Net income ($ millions) 639.1 629.2 493.9 Diluted earnings per share ($) 5.93 6.04 4.99 Return on equity (%) 22.7 19.3 13.7 Shareholders Equity ($ millions) 3,020 3,395