Global Financial Crisis:

|

|

|

- Horace Chapman

- 5 years ago

- Views:

Transcription

1 Global Financial Crisis: Causes and Consequences Dr. Prajapati Trivedi Senior Economist The World Bank

2 Presentation Outline Meaning of Global Financial Crisis Causes Consequences Saudi Arabia India

3 Global Financial Crisis The global financial crisis of 2008 is the worst of its kind since the Great Depression Began with failures of large financial institutions in the United States Rapidly evolved into a global crisis resulting in a number of European bank failures

4 Meaning of Global Financial Crisis The term financial crisis is applied broadly to a variety of situations Usually, some financial institutions or assets suddenly lose a large part of their value Banking Panics (and recessions) Stock market crashes Bursting of financial bubles Currency crisis Sovereign defaults

5 Banking Panics (and recessions) Commercial banks suffer a sudden rush of withdrawals by depositors, this is called a bank run September 7, 2008: Two United States Government sponsored enterprises (GSEs), Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation), into conservatorship run by FHFA September 14, 2008 Lehman Brothers files for bankruptcy. Sale of Merrill Lynch to Bank of America September 16, 2008 AIG faces severe liquidity crunch Financial institutions lost a large part of their value in coming days and weeks

6

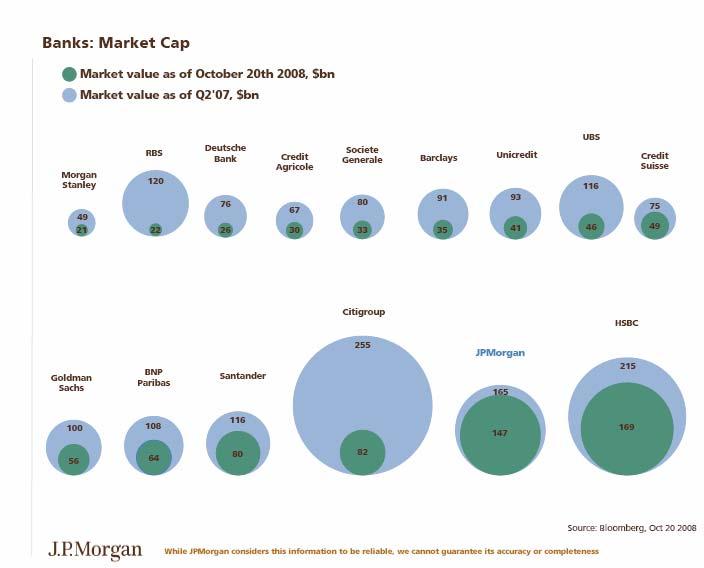

7 Banking Panics (and recessions) 1 year ago RBS paid $100 billion for ABN Amro. For this amount it could now buy: Citibank Morgan Stanley Goldman Sachs Merrill Lynch Deutsche Bank Barclays $22.5 billion $10.5 billion $21 billion $12.3 billion $13 billion $12.7 billion And still have $8 billion change...with which it would be able to pick up GM, Ford, Chrysler and the Honda F1 Team.

8 Speculative Bubbles and Crashes A bubble exists when the price of stock exceeds the value of the future income (such as interest or dividends) that would be received by owning it to maturity Dutch tulip mania Wall Street Crash of 1929 Japanese property bubble of the 1980s, Crash of the dot-com bubble in , and now the United States housing bubble.

9 Speculative Bubbles and Crashes

10 Speculative Bubbles and Crashes

11 Causes Leveraged Investment Asset-Liability Mismatch Regulatory Failures Fraud Medford Contangion Œcopathy Self-fulfilling Prophecy Sub-prime Mortgage

12 Why History is Repeated? Schumpeterian Creative Destruction Regulatory Evolution New markets Nature of competition

13 Consequences

14

15

16

17 All you need is cash The increasingly desperate search for the stuff is changing modern management?

18 Consequences for the Saudi Economy Impact on the Demand Side of Development Process Government Investment Consumer Demand Private Sector Demand

19 Consequences for the Saudi Economy Impact on the Supply Side of Development Process Capital Flows Liquidity working capital flows Skilled Labor Unskilled labor Energy Raw Materials Impact of the crisis on the reform of the Saudi economy

20 Consequences for the Saudi Economy Impact on the Demand Side of Development Process Government Investment Long pipeline of funded Government projects Funds from budget surpluses also committed for projects Hence neutral impact is expected in the medium term.

21 Consequences for the Saudi Economy Impact on the Demand Side of Development Process Consumer Demand No reason for Saudi consumption spending to change. Expatriate consumer spending may decrease as some private sector projects may be postponed Given that the Saudi economy was till recently facing an excess demand situation, on balance this may be a positive factor.

22 Relationship between Individual Consumption and GDP 1971A 1973A 1975A 1977A 1979A 1981A 1983A 1985A 1987A 1989A 1991A 1993A 1995A 1997A 1999A 2001A 2003A 1969A Years Abroad Clothes Rent Food Furniture Medical Other Entertainme Transport GDP Saudi Riyals

23 Consequences for the Saudi Economy Impact on the Demand Side of Development Process Private sector Investment Private sector investment in real estate sector likely to be affected adversely. However, this may be a good outcome given that the Saudi real estate market was over-heated and was suffering from speculative fever. Private sector investment related to other aspects of population requirements not likely to be affected as the real purchasing power of Saudi consumer is not likely to be adversely affected.

24 Consequences for the Saudi Economy Impact on the Supply Side of Development Process Capital Flows There will be a slow-down of private capital flows (FDI) as the financial crisis decreases the available pool of funds. However, from this smaller pool a much larger proportion of funds may be expected to come to Saudi Arabia. This is because of the large and stable buying power of Saudi consumers and Kingdom favorable business climate. According to the World Bank Saudi Arabia is ranked number 16 and is ahead of all countries in the Middle East. Impact likely to be neutral.

25 Consequences for the Saudi Economy Impact on the Supply Side of Development Process Liquidity Working capital flows Like all other countries, Kingdom s banks were also in danger of a potential liquidity crisis resulting from losses on banks foreign investments. However, timely intervention by the Saudi government on October 16, 2008 eliminated this risk. The Supreme Economic Council asked SAMA to ensure sufficient liquidity for the Banks and guarantee the security of bank deposits. Impact likely to be neutral.

26 Consequences for the Saudi Economy Impact on the Supply Side of Development Process Skilled labor Given the global slow down and retrenchment in OECD countries, the available pool of skilled workers will increase and there would be a downward pressure on their salaries. This would benefit Kingdom. Impact likely to be positive.

27 Consequences for the Saudi Economy Impact on the Supply Side of Development Process Unskilled labor Given the global slow down and retrenchment in OECD countries, the available pool of un-skilled workers will also increase and there would be a downward pressure on their salaries. As one of the largest employers of expatriate labor force, this trend would benefit the Kingdom. Impact likely to be positive.

28 Consequences for the Saudi Economy Impact on the Supply Side of Development Process Raw Materials intermediate inputs Global slow down will reduce the price of commodities in general. Hence, the cost of construction materials (steel, copper, etc) will come down and benefit the Kingdom. Impact likely to be positive.

29 Consequences for the Saudi Economy Affect on the welfare and quality of life of citizens Inflation Globally inflation rates have started to come down and that is also the case in Saudi Arabia. This trend will be further supported by strengthening of the dollar vis a vis other currencies. Hence, on balance, the financial crisis may be good for controlling inflation.

30 Consequences for the Saudi Economy Affect on the welfare and quality of life of citizens Jobs Saudi unemployment is not demand driven. Rather, it is a structural problem. Hence, the dampening of demand is not likely to have any immediate negative impact. If Surplus projects are executed and other reform measures implemented, there may be a greater job creation for Saudis. Hence, on balance, the financial crisis may be neutral for jobs creation in the Kingdom.

31 Consequences for the Saudi Economy Affect on the welfare and quality of life of citizens Travel Abroad Stronger dollar (hence stronger Riyal) makes it easier for the Saudis to travel abroad. Hence, on balance, the financial crisis may be good for citizens who want to travel abroad.

32 Consequences for the Saudi Economy Impact of the crisis on the reform of the Saudi economy There is a global trend towards accelerating reform agendas for dealing with the financial crisis in the short run as well as in the long-run. Kingdom will benefit from the experience of other countries and be able to upgrade its regulatory environment. The recent decrease in oil prices has once again brought the focus to the much needed reforms. Kingdom will now be able to work on a post-oil economy. The massive surpluses in the recent pasts ($70.6 billion in 2006 and $47.6 billion in 2007) have made it easier to make investment in these reforms. Hence, impact f the crisis likely to be positive.

33 Please send comments to Dr. Prajapati Trivedi or

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

1. What was life like in Iceland before the financial crisis? 3. How much did Iceland s three banks borrow? What happened to the money?

E&F/Raffel Inside Job Directed by Charles Ferguson Intro: The Case of Iceland 1. What was life like in Iceland before the financial crisis? 2. What changed in 2000? 3. How much did Iceland s three banks

E&F/Raffel Inside Job Directed by Charles Ferguson Intro: The Case of Iceland 1. What was life like in Iceland before the financial crisis? 2. What changed in 2000? 3. How much did Iceland s three banks

Historical Backdrop to the 2007/08 Liquidity Crunch

/08 Liquidity Historical /08 Liquidity Christopher G. Lamoureux October 1, /08 Liquidity Long Term Capital Management August 17, Russian Government restructured debt. Relatively minor event that shook

/08 Liquidity Historical /08 Liquidity Christopher G. Lamoureux October 1, /08 Liquidity Long Term Capital Management August 17, Russian Government restructured debt. Relatively minor event that shook

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Economy In Crisis: How Global Financial Crisis Affects India & The World?

Economy In Crisis: How Global Financial Crisis Affects India & The World? US Economy is in worst recession since the Great Depression and the Federal Government of the United States has already announced

Economy In Crisis: How Global Financial Crisis Affects India & The World? US Economy is in worst recession since the Great Depression and the Federal Government of the United States has already announced

Money and Banking ECON3303. Lecture 9: Financial Crises. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Chapter 8. Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

History of Recession. The Last Recession

Financial Instability is it a curse or a boom? Is it like that reality check which we need to bring us back to the path of inclusive growth and development or is it a result of Greed and No fear, is it

Financial Instability is it a curse or a boom? Is it like that reality check which we need to bring us back to the path of inclusive growth and development or is it a result of Greed and No fear, is it

Black Monday Exploring Current Financial Crisis

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

Capital Markets Update

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

Group 14 Dallas Hall, Chuck Dobson, Guy Tahye, Tunde Olabiyi

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

U.S. Global Investors Searching for Opportunities, Managing Risk

1 U.S. Global Investors Searching for Opportunities, Managing Risk Gold and Commodities Trends Sustainable or Speculative? Frank E. Holmes CEO and Chief Investment Officer September 2008 08-580 Cycles

1 U.S. Global Investors Searching for Opportunities, Managing Risk Gold and Commodities Trends Sustainable or Speculative? Frank E. Holmes CEO and Chief Investment Officer September 2008 08-580 Cycles

Introduction. Learning Objectives. Chapter 15. Money, Banking, and Central Banking

Chapter 15 Money, Banking, and Central Banking Introduction Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley have been big names on Wall Street for years. Known as investment

Chapter 15 Money, Banking, and Central Banking Introduction Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley have been big names on Wall Street for years. Known as investment

Comments on Toward a 3-Tiered Market for US Home Mortgages

Comments on Toward a 3-Tiered Market for US Home Mortgages Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation at the Brookings Conference on Restructuring

Comments on Toward a 3-Tiered Market for US Home Mortgages Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation at the Brookings Conference on Restructuring

GLOBAL SLOWDOWN AND INDIAN ECONOMY

GLOBAL SLOWDOWN AND INDIAN ECONOMY Principal Kasturis College of Arts, Commerce & science Shikhrapur, Pune (MS) INDIA India s financial sector is not deeply integrated with the global financial system,

GLOBAL SLOWDOWN AND INDIAN ECONOMY Principal Kasturis College of Arts, Commerce & science Shikhrapur, Pune (MS) INDIA India s financial sector is not deeply integrated with the global financial system,

Introduction. Why study Financial Markets and Institutions? Primary versus Secondary Markets. Financial Markets

Why study Financial Markets and Institutions? Introduction Markets and institutions are primary channels to allocate capital in our society Proper capital allocation leads to growth in: Societal Wealth

Why study Financial Markets and Institutions? Introduction Markets and institutions are primary channels to allocate capital in our society Proper capital allocation leads to growth in: Societal Wealth

Rating the Raters Rating agencies role in financial crises; lessons learned; the way forward

agencies role in financial crises; lessons learned; the way forward May 2014 Abstract: Agencies (CRAs) give opinion as to relative strength of any entity to meet financial obligations. Like any business

agencies role in financial crises; lessons learned; the way forward May 2014 Abstract: Agencies (CRAs) give opinion as to relative strength of any entity to meet financial obligations. Like any business

Economic Bubbles: Then & Now. By Hamilton Boudreaux

Economic Bubbles: Then & Now By Hamilton Boudreaux Economic Bubbles Historical perspective Economic theory What really happened Current examples & appraisal issues What is an economic bubble? An economic

Economic Bubbles: Then & Now By Hamilton Boudreaux Economic Bubbles Historical perspective Economic theory What really happened Current examples & appraisal issues What is an economic bubble? An economic

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates Ming-sen Wang Department of Economics University of Arizona June 20, 2013 Overview The ideas of economists and political philosophers, both

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates Ming-sen Wang Department of Economics University of Arizona June 20, 2013 Overview The ideas of economists and political philosophers, both

SUB PRIME CRISIS & EUROZONE CRISIS. Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts)

") SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

2008 STOCK MARKET COLLAPSE

2008 STOCK MARKET COLLAPSE Will Pickerign A FINACIAL INSTITUTION PERSECTIVE QUOTE In one way, I m Sympathetic to the institutional reluctance to face the music - Warren Buffet (Fortune 8/16/2007) RECAP

2008 STOCK MARKET COLLAPSE Will Pickerign A FINACIAL INSTITUTION PERSECTIVE QUOTE In one way, I m Sympathetic to the institutional reluctance to face the music - Warren Buffet (Fortune 8/16/2007) RECAP

Financial Markets, Lessors and Impacts on Aerospace Finance

Financial Markets, Lessors and Impacts on Aerospace Finance Presentation to ITA Conference 2010 Nick Pastushan Chief Investment Officer CIT Transportation Finance October 5, 2010 CIT Commercial Segments

Financial Markets, Lessors and Impacts on Aerospace Finance Presentation to ITA Conference 2010 Nick Pastushan Chief Investment Officer CIT Transportation Finance October 5, 2010 CIT Commercial Segments

Global Securities Lending Business and Market Update

NORTHERN TRUST 2009 INSTITUTIONAL CLIENT CONFERENCE GLOBAL REACH, LOCAL EXPERTISE Global Securities Lending Business and Market Update Michael A. Vardas, CFA Managing Director Quantitative Management and

NORTHERN TRUST 2009 INSTITUTIONAL CLIENT CONFERENCE GLOBAL REACH, LOCAL EXPERTISE Global Securities Lending Business and Market Update Michael A. Vardas, CFA Managing Director Quantitative Management and

The 2008 crisis and the future: Have the important lessons been learned?

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

2008 CRISIS : COLD OR CANCER?

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

Introduction and Economic Landscape. Vance Ginn Spring 2013

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

Reflections on the Financial Crisis Allan H. Meltzer

Reflections on the Financial Crisis Allan H. Meltzer I am going to make several unrelated points, and then I am going to discuss how we got into this financial crisis and some needed changes to reduce

Reflections on the Financial Crisis Allan H. Meltzer I am going to make several unrelated points, and then I am going to discuss how we got into this financial crisis and some needed changes to reduce

off their risks, and a market may rise to meet the trading demand.

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) Only small companies can go through financial markets to obtain financing. 2) The reinvestment of cash back into the

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) Only small companies can go through financial markets to obtain financing. 2) The reinvestment of cash back into the

Causes Of The Actual Global Financial Crisis. While many argue that this is the main cause of the global savings glut, the opposite is the

YourLastName 1 YourFirstName YourLastName Instructor's Name Course Title 1 August 2015 Causes Of The Actual Global Financial Crisis Introduction The US is one of the countries that have demonstrated their

YourLastName 1 YourFirstName YourLastName Instructor's Name Course Title 1 August 2015 Causes Of The Actual Global Financial Crisis Introduction The US is one of the countries that have demonstrated their

10 Years After the Financial Crisis: Where Do Shareholder Rights Stand?

NEW YORK PUERTO RICO / TEXAS / ILLINOIS / 845 THIRD AVENUE NEW YORK, NY 10022 (212) 759-4600 WOLFPOPPER.COM 10 Years After the Financial Crisis: Where Do Shareholder Rights Stand? Chet B. Waldman Wolf

NEW YORK PUERTO RICO / TEXAS / ILLINOIS / 845 THIRD AVENUE NEW YORK, NY 10022 (212) 759-4600 WOLFPOPPER.COM 10 Years After the Financial Crisis: Where Do Shareholder Rights Stand? Chet B. Waldman Wolf

New Risk Management Strategies

Moderator: Jon Najarian, Co-Founder, optionmonster.com New Risk Management Strategies Wednesday, May 4, 2011; 2:30 PM - 3:45 PM Speakers: Jim Lenz, Chief Credit and Risk Officer, Wells Fargo Advisors John

Moderator: Jon Najarian, Co-Founder, optionmonster.com New Risk Management Strategies Wednesday, May 4, 2011; 2:30 PM - 3:45 PM Speakers: Jim Lenz, Chief Credit and Risk Officer, Wells Fargo Advisors John

Ewart S Williams: Implications of the current financial crisis for Trinidad and Tobago

Ewart S Williams: Implications of the current financial crisis for Trinidad and Tobago Address by Mr Ewart S Williams, Governor of the Central Bank of Trinidad and Tobago, at a TTMA Seminar Crisis in global

Ewart S Williams: Implications of the current financial crisis for Trinidad and Tobago Address by Mr Ewart S Williams, Governor of the Central Bank of Trinidad and Tobago, at a TTMA Seminar Crisis in global

Chapter 02 Test Bank - Static

Chapter 02 Test Bank - Static Student: 1. Only small companies can go through financial markets to obtain financing. 2. The reinvestment of cash back into the firm's operations is an example of a flow

Chapter 02 Test Bank - Static Student: 1. Only small companies can go through financial markets to obtain financing. 2. The reinvestment of cash back into the firm's operations is an example of a flow

2009 San Diego Apartment Perspective

2009 San Diego Apartment Perspective Graham Bryan, CRB, CCIM, SIOR President, CCIM San Diego Chapter Linda Morris, ARM President, San Diego County Apartment Association National and Local Economic Overview

2009 San Diego Apartment Perspective Graham Bryan, CRB, CCIM, SIOR President, CCIM San Diego Chapter Linda Morris, ARM President, San Diego County Apartment Association National and Local Economic Overview

AQA Economics A-level

AQA Economics A-level Macroeconomics Topic 3: Economic Performance 3.1 Economic growth and economic cycle Notes The difference between short run and long run growth Short run growth is the percentage increase

AQA Economics A-level Macroeconomics Topic 3: Economic Performance 3.1 Economic growth and economic cycle Notes The difference between short run and long run growth Short run growth is the percentage increase

Globalization. International Financial (Chap. 8) and Monetary (Chap. 9) Relations

and Monetary (Chap. 9) Relations") Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Implications of the Dodd-Frank Act on Too Big to Fail A presentation for Washington University s Life-Long Learning Institute

Implications of the Dodd-Frank Act on Too Big to Fail A presentation for Washington University s Life-Long Learning Institute Julie L. Stackhouse Executive Vice President May 4, 2016 Remember these headlines?

Implications of the Dodd-Frank Act on Too Big to Fail A presentation for Washington University s Life-Long Learning Institute Julie L. Stackhouse Executive Vice President May 4, 2016 Remember these headlines?

1 Anthony B. Sanders, Ph.D. is Professor of Finance at the School of Management at George Mason University

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of and

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of 1929-33 and 2007-09 David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009 Presentation

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of 1929-33 and 2007-09 David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009 Presentation

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

Bell Ringer. How do we know if the economy is healthy?

Bell Ringer How do we know if the economy is healthy? Objectives 1. Explain what gross domestic product (GDP) is and what it measures. 2. Compare the GDP of the United States with other countries. Gross

Bell Ringer How do we know if the economy is healthy? Objectives 1. Explain what gross domestic product (GDP) is and what it measures. 2. Compare the GDP of the United States with other countries. Gross

Lecture 7. Unemployment and Fiscal Policy

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Systemic Risk and Sentiment

Systemic Risk and Sentiment May 24 2012 X JORNADA DE RIESGOS FINANCIEROS RISKLAB-MADRID Giovanni Barone-Adesi Swiss Finance Institute and University of Lugano Loriano Mancini Swiss Finance Institute and

Systemic Risk and Sentiment May 24 2012 X JORNADA DE RIESGOS FINANCIEROS RISKLAB-MADRID Giovanni Barone-Adesi Swiss Finance Institute and University of Lugano Loriano Mancini Swiss Finance Institute and

Mike Lombardi, FCIA, FSA, MAAA, CERA

Mike Lombardi, FCIA, FSA, MAAA, CERA Mike Lombardi is a managing principal of Tillinghast Towers Perrin and has been with its Toronto office since 1991. He specializes in providing actuarial advice with

Mike Lombardi, FCIA, FSA, MAAA, CERA Mike Lombardi is a managing principal of Tillinghast Towers Perrin and has been with its Toronto office since 1991. He specializes in providing actuarial advice with

The Financial Crisis: Origins, Causes And Conclusions

The Financial Crisis: Origins, Causes And Conclusions Abstract Eneida Permeti University of Tirana Blerta Mjeda University of Tirana The crisis in recent years took start in response to a crisis of the

The Financial Crisis: Origins, Causes And Conclusions Abstract Eneida Permeti University of Tirana Blerta Mjeda University of Tirana The crisis in recent years took start in response to a crisis of the

September 30, These government programs have helped stabilize the economy over the last year.

September 30, 2009 Macro Economic Update The International Monetary Fund has recently projected that global writedowns on loans and investments will total $3.4 trillion between 2007 and 2010. The banking

September 30, 2009 Macro Economic Update The International Monetary Fund has recently projected that global writedowns on loans and investments will total $3.4 trillion between 2007 and 2010. The banking

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP NOTE-TAKING COLUMN: Complete this section during the video. Include definitions and

STUDY GUIDE SHOULD GOVERNMENT BAIL OUT BIG BANKS? KEY TERMS: bankruptcy de-regulation credit bailout depression TARP NOTE-TAKING COLUMN: Complete this section during the video. Include definitions and

Fannie Mae and Freddie Mac in Conservatorship

Order Code RS22950 September 15, 2008 Fannie Mae and Freddie Mac in Conservatorship Mark Jickling Specialist in Financial Economics Government and Finance Division Summary On September 7, 2008, the Federal

Order Code RS22950 September 15, 2008 Fannie Mae and Freddie Mac in Conservatorship Mark Jickling Specialist in Financial Economics Government and Finance Division Summary On September 7, 2008, the Federal

Economic Outlook. Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012.

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

Massachusetts Tax Revenue Forecasts for FY 2009 and FY 2010

Massachusetts Tax Revenue Forecasts for FY 2009 and FY 2010 Beacon Hill Institute at Suffolk University 8 Ashburton Place, Boston, MA 02108 www.beaconhill.org 617 573 8750 bhi@beaconhill.org December 15,

Massachusetts Tax Revenue Forecasts for FY 2009 and FY 2010 Beacon Hill Institute at Suffolk University 8 Ashburton Place, Boston, MA 02108 www.beaconhill.org 617 573 8750 bhi@beaconhill.org December 15,

Chapter 15: Monetary Policy

Chapter 15: Monetary Policy Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne monetary policy and describe the Federal Reserve s monetary policy goals. 2. Describe the Federal Reserve s

Chapter 15: Monetary Policy Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne monetary policy and describe the Federal Reserve s monetary policy goals. 2. Describe the Federal Reserve s

The NEW Triad. Max P. Michaels

The NEW Triad Max P. Michaels With $2.3 trillion in foreign trade and $12 trillion in cross-border investments, globalization is progressing just the way the architects of modern America envisaged it.

The NEW Triad Max P. Michaels With $2.3 trillion in foreign trade and $12 trillion in cross-border investments, globalization is progressing just the way the architects of modern America envisaged it.

In this alert we want to address some very specific questions for our clients:

EMAIL ALERT DATE: September 18, 2008 Subject: The Current Market Turmoil: Questions and Answers Dear BOS Clients and Colleagues: Email Alert In this email alert we want to address some very specific questions

EMAIL ALERT DATE: September 18, 2008 Subject: The Current Market Turmoil: Questions and Answers Dear BOS Clients and Colleagues: Email Alert In this email alert we want to address some very specific questions

Keynesian excess: Easy policy and slower economic growth

Keynesian excess: Easy policy and slower economic growth Warren Matthews Belhaven University Robert Driver DeVry University ABSTRACT Since the recession of 2007-2009, US fiscal and monetary policies have

Keynesian excess: Easy policy and slower economic growth Warren Matthews Belhaven University Robert Driver DeVry University ABSTRACT Since the recession of 2007-2009, US fiscal and monetary policies have

FINANCE, SAVING, AND INVESTMENT

24 FINANCE, SAVING, AND INVESTMENT During September 2008: The U.S. government took over the risky debts of Fannie Mae and Freddie Mac. The New York Fed, the U.S. Treasury, and Bank of America tried to

24 FINANCE, SAVING, AND INVESTMENT During September 2008: The U.S. government took over the risky debts of Fannie Mae and Freddie Mac. The New York Fed, the U.S. Treasury, and Bank of America tried to

A Change in Fortune and the Reasons Why

January 16, 2009 By William W. Priest, CEO A Change in Fortune and the Reasons Why When the stock market crashed in October 1929, America s government waited three years before launching a series of dramatic

January 16, 2009 By William W. Priest, CEO A Change in Fortune and the Reasons Why When the stock market crashed in October 1929, America s government waited three years before launching a series of dramatic

The Great Depression: An Overview by David C. Wheelock

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

THE FINANCIAL CRISIS OF A PRESENTATION FOR THE TRUCKEE MEADOWS DEMOCRATIC ALLIANCE Elliott Parker, Ph.D.

MAKING SENSE OF THE FINANCIAL CRISIS OF 2008 A PRESENTATION FOR THE TRUCKEE MEADOWS DEMOCRATIC ALLIANCE Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno http://www.coba.unr.edu/faculty/parker

MAKING SENSE OF THE FINANCIAL CRISIS OF 2008 A PRESENTATION FOR THE TRUCKEE MEADOWS DEMOCRATIC ALLIANCE Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno http://www.coba.unr.edu/faculty/parker

Week Eight. Tools of the Federal Reserve

Week Eight Linus Yamane Tools of the Federal Reserve 1. Reserve Requirement (re) Determines the ratio of required reserves to deposits Actual reserves = Required reserves + Excess reserves 2. Discount

Week Eight Linus Yamane Tools of the Federal Reserve 1. Reserve Requirement (re) Determines the ratio of required reserves to deposits Actual reserves = Required reserves + Excess reserves 2. Discount

1. Only small companies can go through financial markets to obtain financing.

Fundamentals of Corporate Finance 8th Edition Brealey Test Bank Full Download: http://testbanklive.com/download/fundamentals-of-corporate-finance-8th-edition-brealey-test-bank/ Chapter 02 Financial Markets

Fundamentals of Corporate Finance 8th Edition Brealey Test Bank Full Download: http://testbanklive.com/download/fundamentals-of-corporate-finance-8th-edition-brealey-test-bank/ Chapter 02 Financial Markets

COPYRIGHTED MATERIAL.

Contents Preface CHAPTER 1 Introduction 1 What You Will Learn in This Chapter 1 Overview 1 Where We Are Going in This Book 2 Contributions Made by the Financial System 4 Transfers of Resources from Surplus

Contents Preface CHAPTER 1 Introduction 1 What You Will Learn in This Chapter 1 Overview 1 Where We Are Going in This Book 2 Contributions Made by the Financial System 4 Transfers of Resources from Surplus

Why Are Financial Intermediaries Special?

Economics of Financial Intermediation February 24, 2017 Outline Explain the special role of FIs in the financial system and the functions they provide Explain why the various FIs receive special regulatory

Economics of Financial Intermediation February 24, 2017 Outline Explain the special role of FIs in the financial system and the functions they provide Explain why the various FIs receive special regulatory

The Financial Systems Complexity

The Financial Systems Complexity Some Data on the Financial System The Role of the Financial System Information Challenges & the Financial System Government Regulation and Supervision Financial Panics:

The Financial Systems Complexity Some Data on the Financial System The Role of the Financial System Information Challenges & the Financial System Government Regulation and Supervision Financial Panics:

IT Can Happen Again: A Global Financial Crisis This time a Gringo Pathology?

IT Can Happen Again: A Global Financial Crisis This time a Gringo Pathology? Why is the financial system important? "Financial systems are crucial to the alloca2on of resources in a modern economy. They

IT Can Happen Again: A Global Financial Crisis This time a Gringo Pathology? Why is the financial system important? "Financial systems are crucial to the alloca2on of resources in a modern economy. They

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Great Depression Economic history Timing and severity

1 Great Depression Worldwide economic downturn that began in 1929 and lasted until about 1939. It was the longest and most severe depression ever experienced by the industrialized Western world. Although

1 Great Depression Worldwide economic downturn that began in 1929 and lasted until about 1939. It was the longest and most severe depression ever experienced by the industrialized Western world. Although

Thoughts on bubbles and the macroeconomy. Gylfi Zoega

Thoughts on bubbles and the macroeconomy Gylfi Zoega The bursting of the stock-market bubble in Iceland and the fall of house prices and the collapse of the currency market caused the biggest financial

Thoughts on bubbles and the macroeconomy Gylfi Zoega The bursting of the stock-market bubble in Iceland and the fall of house prices and the collapse of the currency market caused the biggest financial

Q. Are any of your money market funds at risk of breaking the buck?

Q&A Regarding Fidelity s Money Market Holdings October 23, 2008 (All fund specific holdings information included in below Q&A as of close of business on October 22, 2008) Q. Are any of your money market

Q&A Regarding Fidelity s Money Market Holdings October 23, 2008 (All fund specific holdings information included in below Q&A as of close of business on October 22, 2008) Q. Are any of your money market

The Battle Against Deflation:

The Battle Against Deflation: The Evolution of Monetary Policy and Japan's Experience April 13, 2016 The Italian Academy, Columbia University Governor, Bank of Japan On April 13, 2016, the Center on Japanese

The Battle Against Deflation: The Evolution of Monetary Policy and Japan's Experience April 13, 2016 The Italian Academy, Columbia University Governor, Bank of Japan On April 13, 2016, the Center on Japanese

A Citizen s Guide to the 2008 Financial Report of the U.S. Government

A citizens guide to the report of the united states government The federal government s financial health OVERVIEW Fiscal Year (FY) 2008 was a year of unprecedented change in the financial position and

A citizens guide to the report of the united states government The federal government s financial health OVERVIEW Fiscal Year (FY) 2008 was a year of unprecedented change in the financial position and

THE FINANCIAL CRISIS AND THE GREAT RECESSION

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?

Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Introduction... 3 Definitions... 3 Subprime loan... 3 Mortgage loan... 3

Table of Contents Introduction... 3 Definitions... 3 Subprime loan... 3 Mortgage loan... 3 Real estate and subprime lending in the US... 4 Politics... 4 The rise of subprime mortgages... 4 Risks with Subprime

Table of Contents Introduction... 3 Definitions... 3 Subprime loan... 3 Mortgage loan... 3 Real estate and subprime lending in the US... 4 Politics... 4 The rise of subprime mortgages... 4 Risks with Subprime

October 20, Benefits of FRMs

Testimony of Dr. Anthony B. Sanders Before the U.S. Senate Banking Committee Topic: entitled Housing Finance Reform: Continuation of the 30-year Fixed-Rate Mortgage. October 20, 2011 Mr. Chairman, and

Testimony of Dr. Anthony B. Sanders Before the U.S. Senate Banking Committee Topic: entitled Housing Finance Reform: Continuation of the 30-year Fixed-Rate Mortgage. October 20, 2011 Mr. Chairman, and

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 74

The Financial System 1 / 74") The Sherif Khalifa Sherif Khalifa () The 1 / 74 The financial system consists of those institutions that match saving with investment. The financial system channels funds from those who save to those with

The Sherif Khalifa Sherif Khalifa () The 1 / 74 The financial system consists of those institutions that match saving with investment. The financial system channels funds from those who save to those with

COMPARING FINANCIAL SYSTEMS. Lesson 23 Financial Crises

COMPARING FINANCIAL SYSTEMS Lesson 23 Financial Crises Financial Systems and Risk Financial markets are excessively volatile and expose investors to market risk, especially when investors are subject to

COMPARING FINANCIAL SYSTEMS Lesson 23 Financial Crises Financial Systems and Risk Financial markets are excessively volatile and expose investors to market risk, especially when investors are subject to

The Securities Industry in New York City

The Securities Industry in New York City Thomas P. DiNapoli New York State Comptroller Kenneth B. Bleiwas Deputy Comptroller Report 7-29 November 28 Highlights Before the current crisis, the securities

The Securities Industry in New York City Thomas P. DiNapoli New York State Comptroller Kenneth B. Bleiwas Deputy Comptroller Report 7-29 November 28 Highlights Before the current crisis, the securities

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno eparker@unr.edu DJIA / CPI 15,000 10,000 5,000 0 1949 1951 1953 A Look at the DJIA Adjusting

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno eparker@unr.edu DJIA / CPI 15,000 10,000 5,000 0 1949 1951 1953 A Look at the DJIA Adjusting

The Causes of the 2008 Financial Crisis

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

From Wall Street to Main Street: The Financial Crisis in the US

From Wall Street to Main Street: The Financial Crisis in the US Douglas J. Young Professor of Economics, Montana State University Indian Institute of Technology - Bombay Sabbatical Other Activities Extension-type

From Wall Street to Main Street: The Financial Crisis in the US Douglas J. Young Professor of Economics, Montana State University Indian Institute of Technology - Bombay Sabbatical Other Activities Extension-type

The 2008 Financial Crisis Background Guide By: Alexander Sakellis

The 2008 Financial Crisis Background Guide By: Alexander Sakellis Introduction Welcome Delegates to the King s in House Model United Nations and the 2008 Financial Crisis Committee. The purpose of this

The 2008 Financial Crisis Background Guide By: Alexander Sakellis Introduction Welcome Delegates to the King s in House Model United Nations and the 2008 Financial Crisis Committee. The purpose of this

Global Financial Crisis: An Indian Context.

International Journal of Management, IT & Engineering Vol. 7 Issue 11, November 2017, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

International Journal of Management, IT & Engineering Vol. 7 Issue 11, November 2017, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

FINANCIAL INSTITUTIONS, MARKETS, AND MONEY

E L E V E N T H E D I T I O N FINANCIAL INSTITUTIONS, MARKETS, AND MONEY International Student Version David S. Kidwell University of Minnesota David W. Blackwell Texas A&M University David A. Whidbee

E L E V E N T H E D I T I O N FINANCIAL INSTITUTIONS, MARKETS, AND MONEY International Student Version David S. Kidwell University of Minnesota David W. Blackwell Texas A&M University David A. Whidbee

$4,000,000,000. Freddie Mac. GLOBAL DEBT FACILITY 3.50% Fixed Rate Notes Due September 15, 2007

PRICING SUPPLEMENT DATED September 12, 2002 (to the Offering Circular Dated April 5, 2002) $4,000,000,000 Freddie Mac GLOBAL DEBT FACILITY 3.50% Fixed Rate Notes Due September 15, 2007 Reference Notes

PRICING SUPPLEMENT DATED September 12, 2002 (to the Offering Circular Dated April 5, 2002) $4,000,000,000 Freddie Mac GLOBAL DEBT FACILITY 3.50% Fixed Rate Notes Due September 15, 2007 Reference Notes

I. Learning Objectives II. The Functions of Money III. The Components of the Money Supply

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

Impact of Global Meltdown on GDP, Growth and Foreign Trade of Indian Economy

Impact of Global Meltdown on GDP, Growth and Foreign Trade of Indian Economy Towseef Mohi-ud-din 1, Dr Sangram Bhushan 2 Abstract: In the era of globalization financial crisis seems to have been occurring

Impact of Global Meltdown on GDP, Growth and Foreign Trade of Indian Economy Towseef Mohi-ud-din 1, Dr Sangram Bhushan 2 Abstract: In the era of globalization financial crisis seems to have been occurring

Session 28 Systemic Risk of Banks & Insurance. Richard Nesbitt, CEO Global Risk Institute in Financial Services

Session 28 Systemic Risk of Banks & Insurance Richard Nesbitt, CEO Global Risk Institute in Financial Services Our Mission GRI is the premier risk management institute, that defines thought leadership

Session 28 Systemic Risk of Banks & Insurance Richard Nesbitt, CEO Global Risk Institute in Financial Services Our Mission GRI is the premier risk management institute, that defines thought leadership

BOOM, BUST, BOOM (VIDEO) 1

1") BOOM, BUST, BOOM (VIDEO) 1 Name: 1. Compare the 1928 Calvin Coolidge and the 2006 George W. Bush State of the Union Addresses. What do you notice? 2. The 2008 Crisis is often referred to as the Mortgage

BOOM, BUST, BOOM (VIDEO) 1 Name: 1. Compare the 1928 Calvin Coolidge and the 2006 George W. Bush State of the Union Addresses. What do you notice? 2. The 2008 Crisis is often referred to as the Mortgage

UNESCAP WORKING PAPER

WP/09/04 UNESCAP WORKING PAPER Cross-Border Investment and the Global Financial Crisis in the Asia-Pacific Region Sayuri Shirai Cross-Border Investment and the Global Financial Crisis in the Asia-Pacific

WP/09/04 UNESCAP WORKING PAPER Cross-Border Investment and the Global Financial Crisis in the Asia-Pacific Region Sayuri Shirai Cross-Border Investment and the Global Financial Crisis in the Asia-Pacific

Liquidity and Leverage

Tobias Adrian Federal Reserve Bank of New York Hyun Song Shin Princeton University European Central Bank, November 29, 2007 The views expressed in this presentation are those of the authors and do not

Tobias Adrian Federal Reserve Bank of New York Hyun Song Shin Princeton University European Central Bank, November 29, 2007 The views expressed in this presentation are those of the authors and do not

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 3,

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 3, 2014 http://ijecm.co.uk/ ISSN 2348 0386 THE CAUSES OF THE 2008 ECONOMIC CRISIS Karamitrou, Maria Technological

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 3, 2014 http://ijecm.co.uk/ ISSN 2348 0386 THE CAUSES OF THE 2008 ECONOMIC CRISIS Karamitrou, Maria Technological

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

Saudi Budget 2010 FALCOM ECONOMIC RESEARCH. Snehdeep Fulzele Head of Research

FALCOM ECONOMIC RESEARCH Snehdeep Fulzele Head of Research +966 1 211 8455 Snehdeep.fulzele@falcom.com.sa FALCOM Financial Services P. O. Box 884 Riyadh 11421 Kingdom of Saudi Arabia Saudi Budget 2010

FALCOM ECONOMIC RESEARCH Snehdeep Fulzele Head of Research +966 1 211 8455 Snehdeep.fulzele@falcom.com.sa FALCOM Financial Services P. O. Box 884 Riyadh 11421 Kingdom of Saudi Arabia Saudi Budget 2010

The Financial Crisis. Yale. Marinus van Reymerswaele, 1567

The Financial Crisis Gary Gorton Yale Marinus van Reymerswaele, 1567 What is the crisis? What you saw: firms fail, get acquired, or get bailed out (Lehman Brothers, Bear Stearns, Merrill Lynch, AIG); people

The Financial Crisis Gary Gorton Yale Marinus van Reymerswaele, 1567 What is the crisis? What you saw: firms fail, get acquired, or get bailed out (Lehman Brothers, Bear Stearns, Merrill Lynch, AIG); people

Macroeconomic Theory. Economics 104 Spring 2018 Linus Yamane

Macroeconomic Theory Economics 104 Spring 2018 Linus Yamane Classical Long Run Model Level of output is determined by the Production Function Y = F(K,L) Level of K, L exogenous Who gets the output? Y =

Macroeconomic Theory Economics 104 Spring 2018 Linus Yamane Classical Long Run Model Level of output is determined by the Production Function Y = F(K,L) Level of K, L exogenous Who gets the output? Y =

Section 5 - The Financial Sector

Section 5 - The Financial Sector Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following assets is the MOST liquid? A. checkable bank deposits

Section 5 - The Financial Sector Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following assets is the MOST liquid? A. checkable bank deposits