Lessons Learned? Comparing the Federal Reserve s Response to the Crises of and

|

|

|

- Jasmine Waters

- 6 years ago

- Views:

Transcription

1 Lessons Learned? Comparing the Federal Reserve s Response to the Crises of and David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009

2 Presentation Outline Summarize the Fed s Response in Summarize the Fed s Response in Consider whether the Fed has learned the lessons of the Great Depression The views expressed in this presentation are not necessarily official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.

3 The Financial Crisis and Recession of Worst financial crisis since the Great Depression Severe recession, but not nearly as bad as the Great Depression Monetary and fiscal policy have been much more aggressive in than during The Fed was largely passive during Why?

4 The Recessions of and

5

6

7

8 Crisis of : Initial Response August 2007: Fed reduces discount rate and reassures markets that its discount window is available December 2007: Fed creates the Term Auction Facility (TAF) to lend term funds to banks without the stigma associated with discount window borrowing December 2007: Fed establishes swap lines with ECB and Swiss National Bank. Later establishes swap lines with eight more central banks (including the Bank of Mexico).

9 Section 13(3) of the Federal Reserve Act Permits lending to any individual, partnership or corporation in unusual and exigent circumstances if the borrower is unable to secure adequate credit accommodations from other banking institutions. Such loans must be secured to the satisfaction of the [lending] Federal Reserve Bank. Added to the Federal Reserve Act in July 1932, but little used before 2008 Used extensively in to provide loans to non-bank financial institutions and markets

10 Section 13(3) Actions in Loan to facilitate the acquisition of Bear Stearns by JPMorgan-Chase (March 2008) Primary Dealer Credit Facility (March 2008) Loans to AIG (September 2008) Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (Sept. 2008) Commercial Paper Funding Facility (Sept. 2008) Term Asset-Backed Securities Lending Facility (Nov. 2008)

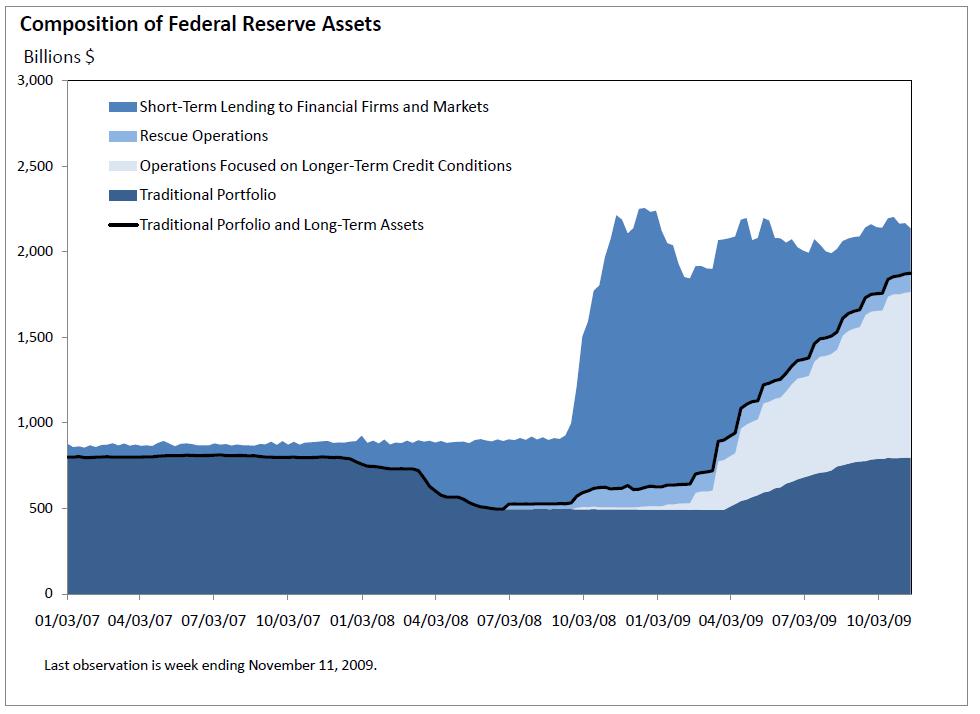

11 Other Fed Actions in Federal funds target rate reduced to 0-25 basis point range Large-scale purchases of Treasury securities, agency debt, and agency mortgage-backed securities (MBS) These actions have resulted in a massive increase in the Fed s balance sheet and the U.S. monetary base; some increase in broader money (M2) growth.

12

13

14 Summary of Fed Response in Increased lending via liquidity facilities Rescue operations to mitigate systemic risk Massive increase in Federal Reserve balance sheet and monetary base since September 2008 to prevent deflation and promote economic recovery

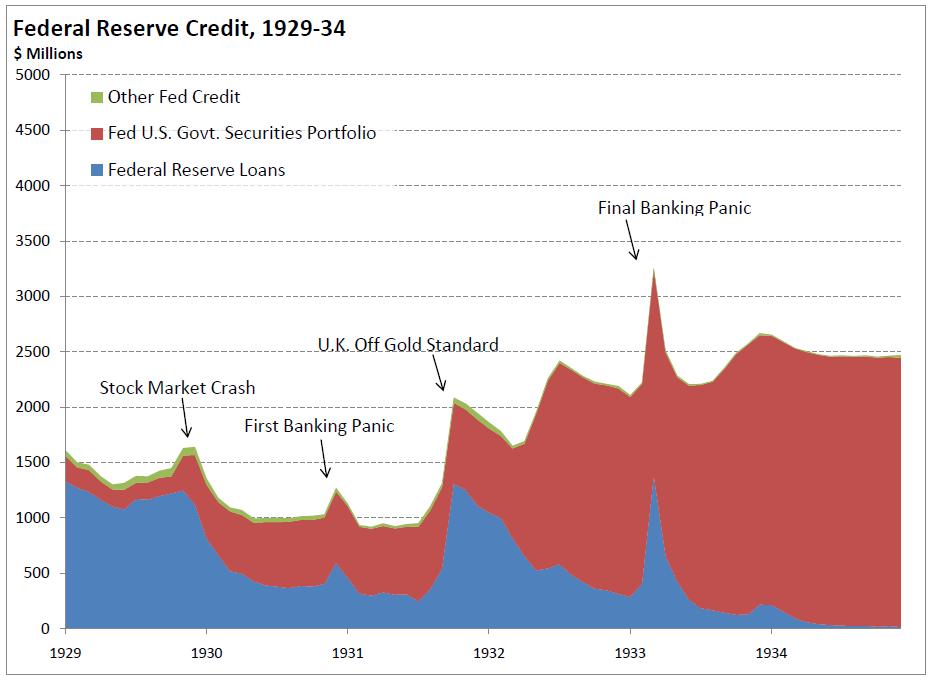

15 Federal Reserve Policy, New York Fed responded swiftly to the stock market crash in 1929 Fed largely ignored banking panics of Federal Reserve credit contracted in Increase in monetary base was not sufficient to prevent collapse of the money stock and price level

16

17

18 Why Wasn t the Fed More Responsive? Fed officials misinterpreted financial conditions Low interest rates and little discount window borrowing were seen as evidence of monetary ease.

19

20 Why Wasn t the Fed More Responsive? Fed officials misinterpreted financial conditions Low interest rates and little discount window borrowing were seen as evidence of monetary ease. Federal Reserve Act limited discount window loans only to member banks with prime collateral. Some officials wanted tighter policy to discourage financial speculation. Officials thought that they were following Bagehot s Rule, especially in response to gold outflows in 1931 and Would Benjamin Strong have done better?

21 Lessons Learned? The Fed s response to the crisis of was markedly more aggressive than its response in : New liquidity facilities Rescue operations Large expansion of monetary base beginning in Sept Deflation avoided The Fed is unlikely to raise reserve requirements in order to reduce excess reserves, as they did in

22 Lessons Learned? But, Some critics argue that the Fed was too slow to increase the monetary base Others criticize the Fed for not rescuing Lehman Brothers Still others are concerned that rescue operations promote moral hazard and threaten the Fed s political independence Will the Fed remove monetary stimulus in time to forestall higher inflation or another asset bubble?

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

Money and Banking ECON3303. Lecture 9: Financial Crises. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Money and Banking ECON3303 Lecture 9: Financial Crises William J. Crowder Ph.D. What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows

Financial Crises: The Great Depression and the Great Recession

Financial Crises: The Great Depression and the Great Recession ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 43 Readings Mishkin Ch. 12 Bernanke (2002): On Milton

Financial Crises: The Great Depression and the Great Recession ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 43 Readings Mishkin Ch. 12 Bernanke (2002): On Milton

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Monetary Policy Normalization: What s New? What s Old? How Does It Matter?

Monetary Policy Normalization: What s New? What s Old? How Does It Matter? Cletus Coughlin Senior Vice President and Policy Adviser to the President Federal Reserve Bank of St. Louis May 28, 2015 The views

Monetary Policy Normalization: What s New? What s Old? How Does It Matter? Cletus Coughlin Senior Vice President and Policy Adviser to the President Federal Reserve Bank of St. Louis May 28, 2015 The views

Economic Outlook. Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis. NLB,LLC The Lodge, Des Peres, MO.

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

Three Lessons for Monetary Policy from the Panic of 2008

Three Lessons for Monetary Policy from the Panic of 2008 James Bullard President and CEO Federal Reserve Bank of St. Louis The Philadelphia Fed Policy Forum December 4, 2009 Any opinions expressed here

Three Lessons for Monetary Policy from the Panic of 2008 James Bullard President and CEO Federal Reserve Bank of St. Louis The Philadelphia Fed Policy Forum December 4, 2009 Any opinions expressed here

THE FINANCIAL CRISIS AND THE GREAT RECESSION

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

The Great Recession. ECON 43370: Financial Crises. Eric Sims. Spring University of Notre Dame

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

I. Learning Objectives II. The Functions of Money III. The Components of the Money Supply

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

Financial Crises and the Great Recession

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Chapter 8. Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Capital structure and the financial crisis

Capital structure and the financial crisis Richard H. Fosberg William Paterson University Journal of Finance and Accountancy Abstract The financial crisis on the late 2000s had a major impact on the financial

Capital structure and the financial crisis Richard H. Fosberg William Paterson University Journal of Finance and Accountancy Abstract The financial crisis on the late 2000s had a major impact on the financial

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT?

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT? L. Randall Wray Levy Economics Institute and University of Missouri - Kansas City www.levy.org; www.cfeps.org; wrayr@umkc.edu *Report of a Research Project

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT? L. Randall Wray Levy Economics Institute and University of Missouri - Kansas City www.levy.org; www.cfeps.org; wrayr@umkc.edu *Report of a Research Project

Financial Turmoil: Federal Reserve Policy Responses

Order Code RL34427 Financial Turmoil: Federal Reserve Policy Responses Updated October 23, 2008 Marc Labonte Specialist in Macroeconomic Policy Government and Finance Division Financial Turmoil: Federal

Order Code RL34427 Financial Turmoil: Federal Reserve Policy Responses Updated October 23, 2008 Marc Labonte Specialist in Macroeconomic Policy Government and Finance Division Financial Turmoil: Federal

4) The dark side of financial liberalization is. A) market allocations B) credit booms C) currency appreciation D) financial innovation

The dark side of financial liberalization is. A) market allocations B) credit booms C) currency appreciation D) financial innovation") Chapter 9 Financial Crises 1) A major disruption in financial markets characterized by sharp declines in asset prices and firm failures is called a A) financial crisis B) fiscal imbalance C) free-rider

Chapter 9 Financial Crises 1) A major disruption in financial markets characterized by sharp declines in asset prices and firm failures is called a A) financial crisis B) fiscal imbalance C) free-rider

Ben S Bernanke: Federal Reserve policies in the financial crisis

Ben S Bernanke: Federal Reserve policies in the financial crisis Speech by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Greater Austin Chamber of Commerce,

Ben S Bernanke: Federal Reserve policies in the financial crisis Speech by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Greater Austin Chamber of Commerce,

Understanding the Policy Response to the Financial Crisis. Macroeconomic Theory Honors EC 204

Understanding the Policy Response to the Financial Crisis Macroeconomic Theory Honors EC 204 Key Problems in the Crisis Bank Solvency Declining home prices and rising mortgage defaults put banks in danger

Understanding the Policy Response to the Financial Crisis Macroeconomic Theory Honors EC 204 Key Problems in the Crisis Bank Solvency Declining home prices and rising mortgage defaults put banks in danger

Financial Bubbling: from the Asian Crisis to the Subprime Mess

Financial Bubbling: from the Asian Crisis to the Subprime Mess University of Bari by Giovanni Ferri (University of Bari) Workshop The complexity of financial crisis in a long-period perspective: facts,

Financial Bubbling: from the Asian Crisis to the Subprime Mess University of Bari by Giovanni Ferri (University of Bari) Workshop The complexity of financial crisis in a long-period perspective: facts,

Monetary Policy and Financial Stability

Monetary Policy and Financial Stability Charles I. Plosser President and Chief Executive Officer Federal Reserve Bank of Philadelphia The 26 th Annual Monetary and Trade Conference Presented by: The Global

Monetary Policy and Financial Stability Charles I. Plosser President and Chief Executive Officer Federal Reserve Bank of Philadelphia The 26 th Annual Monetary and Trade Conference Presented by: The Global

History May Not Repeat, But It Does Rhyme*

History May Not Repeat, But It Does Rhyme* Looking at the 2000s through a 1930s Lens *Mark Twain Mark D. Vaughan American University / Economics 639 Disclaimer The views expressed in this presentation

History May Not Repeat, But It Does Rhyme* Looking at the 2000s through a 1930s Lens *Mark Twain Mark D. Vaughan American University / Economics 639 Disclaimer The views expressed in this presentation

Swimming Upstream: Monetary Policy Following the Financial Crisis

Presentation at the Central Bank of Chile, Fourth Summit Meeting of Central Banks on Inflation Targeting Santiago, Chile By John C. Williams, President and CEO Federal Reserve Bank of San Francisco For

Presentation at the Central Bank of Chile, Fourth Summit Meeting of Central Banks on Inflation Targeting Santiago, Chile By John C. Williams, President and CEO Federal Reserve Bank of San Francisco For

The Federal Reserve as a Lender of Last Resort: an Historical Perspective

The Federal Reserve as a Lender of Last Resort: an Historical Perspective Michael Bordo Rutgers University and the Hoover Institution Federal Reserve Bank of Atlanta May 20 2014 1. The LLR: Definition

The Federal Reserve as a Lender of Last Resort: an Historical Perspective Michael Bordo Rutgers University and the Hoover Institution Federal Reserve Bank of Atlanta May 20 2014 1. The LLR: Definition

Chapter 10. Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics. Chapter Preview

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

The Federal Reserve as a Lender of Last Resort: an Historical Perspective. Michael Bordo Rutgers University and the Hoover Institution

The Federal Reserve as a Lender of Last Resort: an Historical Perspective Michael Bordo Rutgers University and the Hoover Institution Overview 1. Definition of LLR 2. Origins in England 3. Financial Crises

The Federal Reserve as a Lender of Last Resort: an Historical Perspective Michael Bordo Rutgers University and the Hoover Institution Overview 1. Definition of LLR 2. Origins in England 3. Financial Crises

Chapter Fourteen. Chapter 10 Regulating the Financial System 5/6/2018. Financial Crisis

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

U.S. Monetary Policy Objectives in the Short and Long Run 1

Presentation to the Andrew Brimmer Policy Forum IBEFA/ASSA Meeting San Francisco, CA By Janet L. Yellen, President and CEO, Federal Reserve Bank of San Francisco For delivery on January 4, 2009, 2:30 PM

Presentation to the Andrew Brimmer Policy Forum IBEFA/ASSA Meeting San Francisco, CA By Janet L. Yellen, President and CEO, Federal Reserve Bank of San Francisco For delivery on January 4, 2009, 2:30 PM

Black Monday Exploring Current Financial Crisis

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

AD-AS Analysis of Financial Crises, the ZLB, and Unconventional Policy

AD-AS Analysis of Financial Crises, the ZLB, and Unconventional Policy ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2018 1 / 38 Readings Text: Mishkin Ch. 15 pg. 355-361;

AD-AS Analysis of Financial Crises, the ZLB, and Unconventional Policy ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2018 1 / 38 Readings Text: Mishkin Ch. 15 pg. 355-361;

Globalization and Economic Crises in the Asia-Pacific: Imperatives on Statistics Management

Globalization and Economic Crises in the Asia-Pacific: Imperatives on Statistics Management Fourth Regional Course/Workshop on Statistical Quality Management UN SIAP 21-25 Sep 2009, Daejeon By George Manzano

Globalization and Economic Crises in the Asia-Pacific: Imperatives on Statistics Management Fourth Regional Course/Workshop on Statistical Quality Management UN SIAP 21-25 Sep 2009, Daejeon By George Manzano

How did Monetary Policy Implementation Change with the Financial Crisis?

How did Monetary Policy Implementation Change with the Financial Crisis? John McGowan Assistant Vice President Money Markets, Markets Group, FRBNY September 28, 2015 Internal FR I. FRS Mandate and Pre-

How did Monetary Policy Implementation Change with the Financial Crisis? John McGowan Assistant Vice President Money Markets, Markets Group, FRBNY September 28, 2015 Internal FR I. FRS Mandate and Pre-

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

The year 2008 marked a watershed for

Financial Turmoil and the Economy Economic Research Economic Research, the other areas contributing to this report, and the Legal department are part of an interdepartmental committee the Federal Reserve

Financial Turmoil and the Economy Economic Research Economic Research, the other areas contributing to this report, and the Legal department are part of an interdepartmental committee the Federal Reserve

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Julie Stackhouse Senior Vice President Federal Reserve Bank of St. Louis May 22, 2009 The views expressed are those of Julie Stackhouse and may not represent the official views of the Federal Reserve Bank

Topics. Origins of the Financial Crisis The Economy. Managing the Bailouts Impact on Exchange Rate System Conclusions

International Scenarios of the Financial Markets in 2009: Forecasts and Strategies." Robert Mundell December 3, 2008 Rome Topics Origins of the Financial Crisis The Economy Lessons from the Crisis Managing

International Scenarios of the Financial Markets in 2009: Forecasts and Strategies." Robert Mundell December 3, 2008 Rome Topics Origins of the Financial Crisis The Economy Lessons from the Crisis Managing

EconomicLetter. Insights from the. The Term Auction Facility s Effectiveness in the Financial Crisis of

Vol. 5, No. MAY EconomicLetter Insights from the F e d e r a l R e s e r v e B a n k o f D a l l a s The Term Auction Facility s Effectiveness in the Financial Crisis of 7 9 by Tao Wu The TAF and other

Vol. 5, No. MAY EconomicLetter Insights from the F e d e r a l R e s e r v e B a n k o f D a l l a s The Term Auction Facility s Effectiveness in the Financial Crisis of 7 9 by Tao Wu The TAF and other

Joseph S Tracy: A strategy for the 2011 economic recovery

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Chapter 15: Monetary Policy

Chapter 15: Monetary Policy Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne monetary policy and describe the Federal Reserve s monetary policy goals. 2. Describe the Federal Reserve s

Chapter 15: Monetary Policy Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne monetary policy and describe the Federal Reserve s monetary policy goals. 2. Describe the Federal Reserve s

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

Great Recession. Prof. Eric Sims. Fall University of Notre Dame

Great Recession Prof. Eric Sims University of Notre Dame Fall 25 / 28 Overview Worst economic contraction since Great Depression (by most measures) Could do entire course on the subject We will do a very

Great Recession Prof. Eric Sims University of Notre Dame Fall 25 / 28 Overview Worst economic contraction since Great Depression (by most measures) Could do entire course on the subject We will do a very

The 2008 crisis and the future: Have the important lessons been learned?

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

Conference on European Financial Systems: In and Out of the Crisis Siena The 2008 crisis and the future: Have the important lessons been learned? Paulo Soares de Pinho Nova School of Business and Economics

SUB PRIME CRISIS & EUROZONE CRISIS. Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts)

") SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

SUB PRIME CRISIS & EUROZONE CRISIS Presented by Amitesh Kumar Sinha, Dir. Fin (Accounts) Prof Khaled Soufani ESCP/LONDON ESCP London London Business School courtyard in snow Housing Bubble - MORTGAGE LENDING

Economies are constantly buffeted by shocks to aggregate

Ball2e_CH18_Ball2e_CH18 12/8/10 2:48 AM Page 551 chapter eighteen Financial Crises 18.1 THE MECHANICS OF FINANCIAL CRISES 18.2 FINANCIAL RESCUES 18.3 THE U.S. FINANCIAL CRISIS OF 2007 2009 18.4 THE FUTURE

Ball2e_CH18_Ball2e_CH18 12/8/10 2:48 AM Page 551 chapter eighteen Financial Crises 18.1 THE MECHANICS OF FINANCIAL CRISES 18.2 FINANCIAL RESCUES 18.3 THE U.S. FINANCIAL CRISIS OF 2007 2009 18.4 THE FUTURE

Session 12. The New Normal. Deflation and Zero Lower Bound.

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Intermediate Macroeconomics: Great Recession

Intermediate Macroeconomics: Great Recession Eric Sims University of Notre Dame Fall 2013 1 Introduction The Great Recession is the name now commonly given to the economic contraction that occurred in

Intermediate Macroeconomics: Great Recession Eric Sims University of Notre Dame Fall 2013 1 Introduction The Great Recession is the name now commonly given to the economic contraction that occurred in

The Causes of the 2008 Financial Crisis

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

UK Summary The Causes of the 2008 Financial Crisis The text discusses the background history of the financial crash through focusing on prime and sub-prime mortgage lending. It then explores the key reasons

Financial Turmoil: Federal Reserve Policy Responses

Order Code RL34427 Financial Turmoil: Federal Reserve Policy Responses Updated April 7, 2008 Marc Labonte Specialist in Macroeconomic Policy Government and Finance Division Financial Turmoil: Federal Reserve

Order Code RL34427 Financial Turmoil: Federal Reserve Policy Responses Updated April 7, 2008 Marc Labonte Specialist in Macroeconomic Policy Government and Finance Division Financial Turmoil: Federal Reserve

William C Dudley: The Federal Reserve's liquidity facilities

William C Dudley: The Federal Reserve's liquidity facilities Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal Reserve Bank of New York, at the Vanderbilt University

William C Dudley: The Federal Reserve's liquidity facilities Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal Reserve Bank of New York, at the Vanderbilt University

The Need to Return to a Monetary Framework. John B. Taylor 1 January 2009

The Need to Return to a Monetary Framework John B. Taylor 1 January 2009 Sometime in mid September 2008, the Federal Reserve began creating money at an amazingly rapid pace. For the week ending September

The Need to Return to a Monetary Framework John B. Taylor 1 January 2009 Sometime in mid September 2008, the Federal Reserve began creating money at an amazingly rapid pace. For the week ending September

Answer Key: False Question 3 of / 1.0 Points Asymmetric information problems are more severe during a financial panic.

Question 1 of 33 Lenders of last resort intend to A.add liquidity to financial markets. B.restore confidence in financial markets. C.lower interest rates. Question 2 of 33 By allowing Lehman to fail, the

Question 1 of 33 Lenders of last resort intend to A.add liquidity to financial markets. B.restore confidence in financial markets. C.lower interest rates. Question 2 of 33 By allowing Lehman to fail, the

ECN 106 Macroeconomics 1. Lecture 10

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

The Failure of US Neoliberalism: Financial Panic, Economic Stagnation and What We Can Do About It

The Failure of US Neoliberalism: Financial Panic, Economic Stagnation and What We Can Do About It Bill Barclay, Chicago Political Economy Group and Democratic Socialists of America Three Sections What

The Failure of US Neoliberalism: Financial Panic, Economic Stagnation and What We Can Do About It Bill Barclay, Chicago Political Economy Group and Democratic Socialists of America Three Sections What

The Great Depression: An Overview by David C. Wheelock

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

Topic 8 : The Interwar Globalization Backlash

Topic 8 : The Interwar Globalization Backlash Department of Economics University of Warwick March, 2014 We focus on the monetarist view : It was the Fed s policy mistake ignoring the importance of money

Topic 8 : The Interwar Globalization Backlash Department of Economics University of Warwick March, 2014 We focus on the monetarist view : It was the Fed s policy mistake ignoring the importance of money

Has the Federal Reserve Learned to be an Effective Lender of Last Resort in its First One Hundred Years?

Has the Federal Reserve Learned to be an Effective Lender of Last Resort in its First One Hundred Years? Michael D Bordo Rutgers University, Hoover Institution and NBER Shadow Open Market Committee Symposium

Has the Federal Reserve Learned to be an Effective Lender of Last Resort in its First One Hundred Years? Michael D Bordo Rutgers University, Hoover Institution and NBER Shadow Open Market Committee Symposium

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015

Instructor: Prof. Menzie Chinn UW Madison Fall 2015") Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

Thoughts on the Federal Reserve System s Exit Strategy

Economic Policy Paper 10-1 Federal Reserve Bank of Minneapolis Thoughts on the Federal Reserve System s Exit Strategy March 2010 V. V. Chari Professor, University of Minnesota Research Consultant, Federal

Economic Policy Paper 10-1 Federal Reserve Bank of Minneapolis Thoughts on the Federal Reserve System s Exit Strategy March 2010 V. V. Chari Professor, University of Minnesota Research Consultant, Federal

Comments on Hoshi and Kashyap,

Comments on Hoshi and Kashyap, Will US Bank Recapitalization Plan Succeed? Lessons from Japan Takatoshi Ito University of Tokyo AEA January 5, 2009 San Francisco Takatoshi Ito AEA 2009 1 Memorable Quotes,

Comments on Hoshi and Kashyap, Will US Bank Recapitalization Plan Succeed? Lessons from Japan Takatoshi Ito University of Tokyo AEA January 5, 2009 San Francisco Takatoshi Ito AEA 2009 1 Memorable Quotes,

Capital Market Trends and Forecasts

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Written Testimony of Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Field hearing of the Committee on Financial Services of the U.S. House of Representatives: Seeking

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?

Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

10/30/2018. Chapter 17. The Money Supply Process. Preview. Learning Objectives

Chapter 17 The Money Supply Process Preview This chapter provides an overview of how the banking system create and describes the basic principles of the money supply creation process Learning Objectives

Chapter 17 The Money Supply Process Preview This chapter provides an overview of how the banking system create and describes the basic principles of the money supply creation process Learning Objectives

LOCAL UNION NO. 952 GENERAL TRUCK DRIVERS, OFFICE, FOOD & WAREHOUSE UNION ORANGE COUNTY AND VICINITY, CALIFORNIA

LOCAL UNION NO. 952 GENERAL TRUCK DRIVERS, OFFICE, FOOD & WAREHOUSE UNION ORANGE COUNTY AND VICINITY, CALIFORNIA 140 S. Marks Way Orange, CA 92868-2698 (714) 740-6200 FAX (714) 978-0576 www.teamsters952.org

LOCAL UNION NO. 952 GENERAL TRUCK DRIVERS, OFFICE, FOOD & WAREHOUSE UNION ORANGE COUNTY AND VICINITY, CALIFORNIA 140 S. Marks Way Orange, CA 92868-2698 (714) 740-6200 FAX (714) 978-0576 www.teamsters952.org

Chapter Seventeen. Understand 10/24/2017. The Central Bank Balance Sheet and the Money Supply Process Chapter 17

Chapter Seventeen The Central Bank Balance Sheet and the Money Supply Process Chapter 17 Understand 1. The central bank s balance sheet. 2. Changing the size and the mix of the balance sheet. 3. The deposit

Chapter Seventeen The Central Bank Balance Sheet and the Money Supply Process Chapter 17 Understand 1. The central bank s balance sheet. 2. Changing the size and the mix of the balance sheet. 3. The deposit

The International Economy: Challenge and Opportunity

The International Economy: Challenge and Opportunity The Origins of the Financial Crisis Christopher J. Neely Assistant Vice President Federal Reserve Bank of St. Louis United Nations Association of St.

The International Economy: Challenge and Opportunity The Origins of the Financial Crisis Christopher J. Neely Assistant Vice President Federal Reserve Bank of St. Louis United Nations Association of St.

Will Regulatory Reform Prevent Future Crises?

Will Regulatory Reform Prevent Future Crises? James Bullard President and CEO CFA Virginia Society February 23, 2010 Richmond, Virginia. Any opinions expressed here are my own and do not necessarily reflect

Will Regulatory Reform Prevent Future Crises? James Bullard President and CEO CFA Virginia Society February 23, 2010 Richmond, Virginia. Any opinions expressed here are my own and do not necessarily reflect

The First Phase of the U.S. Recovery and Beyond

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

The Financial Crisis of 2008

Some Recent Financial Crises The Financial Crisis of 2008 Bradley University s s Economics Department Presented by Dr. Joshua J. Lewer & Dr. Robert C. Scott Theme: Bad Loans U.S. Savings and Loans - 1985

Some Recent Financial Crises The Financial Crisis of 2008 Bradley University s s Economics Department Presented by Dr. Joshua J. Lewer & Dr. Robert C. Scott Theme: Bad Loans U.S. Savings and Loans - 1985

OCR Economics A-level

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.5 Approaches to policy and macroeconomic context Notes Explain why approaches to macroeconomic policy change in accordance

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.5 Approaches to policy and macroeconomic context Notes Explain why approaches to macroeconomic policy change in accordance

Financial Fragility and the Lender of Last Resort

READING 11 Financial Fragility and the Lender of Last Resort Desiree Schaan & Timothy Cogley Financial crises, such as banking panics and stock market crashes, were a common occurrence in the U.S. economy

READING 11 Financial Fragility and the Lender of Last Resort Desiree Schaan & Timothy Cogley Financial crises, such as banking panics and stock market crashes, were a common occurrence in the U.S. economy

Some Thoughts on the Economy and Financial Regulatory Reform

Some Thoughts on the Economy and Financial Regulatory Reform Presented to The Economics Club of Pittsburgh Pittsburgh, PA November 13, 2008 Charles I. Plosser President and CEO Federal Reserve Bank of

Some Thoughts on the Economy and Financial Regulatory Reform Presented to The Economics Club of Pittsburgh Pittsburgh, PA November 13, 2008 Charles I. Plosser President and CEO Federal Reserve Bank of

June 24th, Rate Reversal. Author: Benjamin Struck President

June 24th, 2013 Rate Reversal Author: Benjamin Struck President 1 Economic Summary 3 Strategic Allocation 5 Tactical Allocation 6 2 Last week s selloff was broad based and applied to nearly all asset classes.

June 24th, 2013 Rate Reversal Author: Benjamin Struck President 1 Economic Summary 3 Strategic Allocation 5 Tactical Allocation 6 2 Last week s selloff was broad based and applied to nearly all asset classes.

2008 CRISIS : COLD OR CANCER?

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2011 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

The Great Depression, golden age, and global financial crisis

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

Central Bank collateral frameworks before and during the crisis

Central Bank collateral frameworks before and during the crisis The case of the Federal Reserve Central banking, liquidity crises and financial stability lecture Mai 20 th, 2011 Presentation by 1 Goals

Central Bank collateral frameworks before and during the crisis The case of the Federal Reserve Central banking, liquidity crises and financial stability lecture Mai 20 th, 2011 Presentation by 1 Goals

December 14, 2007 As of December 14, 2007 Index YTD % Change* Market Value

As of December 14, 2007 Index YTD % Change* Market Value Dow Jones Industrials 9.35% 13,339.85 S&P 500 5.35% 1,467.95 Nasdaq Composite 9.13% 2,635.74 *YTD % Changes use the index with dividends December

As of December 14, 2007 Index YTD % Change* Market Value Dow Jones Industrials 9.35% 13,339.85 S&P 500 5.35% 1,467.95 Nasdaq Composite 9.13% 2,635.74 *YTD % Changes use the index with dividends December

BEHIND THE NUMBERS. Money, Bank Capital and Zero Interest Rates. With Central Bank Rates Approaching Zero, Can Economic Policy Be Effective?

BEHIND THE NUMBERS economic facts, figures and analysis Volume 10, Number 1 February 2009 Money, Bank Capital and Zero Interest Rates With Central Bank Rates Approaching Zero, Can Economic Policy Be Effective?

BEHIND THE NUMBERS economic facts, figures and analysis Volume 10, Number 1 February 2009 Money, Bank Capital and Zero Interest Rates With Central Bank Rates Approaching Zero, Can Economic Policy Be Effective?

Main Points: Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable

NBER July 2018 Main Points: 2 Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable US housing bubble and the crisis of

NBER July 2018 Main Points: 2 Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable US housing bubble and the crisis of

Macroeconomic Policy during a Credit Crunch

ECONOMIC POLICY PAPER 15-2 FEBRUARY 2015 Macroeconomic Policy during a Credit Crunch EXECUTIVE SUMMARY Most economic models used by central banks prior to the recent financial crisis omitted two fundamental

ECONOMIC POLICY PAPER 15-2 FEBRUARY 2015 Macroeconomic Policy during a Credit Crunch EXECUTIVE SUMMARY Most economic models used by central banks prior to the recent financial crisis omitted two fundamental

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Lecture 5. Notes on the Current Crisis

Lecture 5 Notes on the Current Crisis Mark Gertler NYU June 29 .4 Real GDP growth.3.2.1.1.2.3 1975 198 1985 199 1995 2 25 18 16 core inflation federal funds rate 14 12 1 8 6 4 2 1975 198 1985 199 1995

Lecture 5 Notes on the Current Crisis Mark Gertler NYU June 29 .4 Real GDP growth.3.2.1.1.2.3 1975 198 1985 199 1995 2 25 18 16 core inflation federal funds rate 14 12 1 8 6 4 2 1975 198 1985 199 1995

Bubbles and Central Banks: Historical Perspectives

Bubbles and Central Banks: Historical Perspectives Markus K. Brunnermeier Princeton University Isabel Schnabel Johannes Gutenberg University Mainz and German Council of Economic Experts SUERF/OeNB/BWG

Bubbles and Central Banks: Historical Perspectives Markus K. Brunnermeier Princeton University Isabel Schnabel Johannes Gutenberg University Mainz and German Council of Economic Experts SUERF/OeNB/BWG

Dear Delegates, Your Chairs, Aparna Sivanandam and Aarti Rangarajan

Dear Delegates, Welcome to The Federal Open Market Committee, this is Aparna Sivanandam and Aarti Rangarajan, your chairs for ChrisMUN 2017. We are extremely excited to chair this council which we hope

Dear Delegates, Welcome to The Federal Open Market Committee, this is Aparna Sivanandam and Aarti Rangarajan, your chairs for ChrisMUN 2017. We are extremely excited to chair this council which we hope

MONETARY POLICY ON THE WAY OUT OF THE CRISIS

ISSUE 29/15 DECEMBER 29 MONETARY ON THE WAY OUT OF THE CRISIS JÜRGEN VON HAGEN Highlights Telephone +32 2 227 421 info@bruegel.org www.bruegel.org The European economy and the economy of the euro area

ISSUE 29/15 DECEMBER 29 MONETARY ON THE WAY OUT OF THE CRISIS JÜRGEN VON HAGEN Highlights Telephone +32 2 227 421 info@bruegel.org www.bruegel.org The European economy and the economy of the euro area

Discussion of Sargent s Where to draw lines: monetary and fiscal uncertainties

Discussion of Sargent s Where to draw lines: monetary and fiscal uncertainties Nancy L. Stokey University of Chicago April 23, 2010 Stokey - Discussion (University of Chicago) April 23, 2010 04/2010 1

Discussion of Sargent s Where to draw lines: monetary and fiscal uncertainties Nancy L. Stokey University of Chicago April 23, 2010 Stokey - Discussion (University of Chicago) April 23, 2010 04/2010 1

COPYRIGHTED MATERIAL.

Contents Preface CHAPTER 1 Introduction 1 What You Will Learn in This Chapter 1 Overview 1 Where We Are Going in This Book 2 Contributions Made by the Financial System 4 Transfers of Resources from Surplus

Contents Preface CHAPTER 1 Introduction 1 What You Will Learn in This Chapter 1 Overview 1 Where We Are Going in This Book 2 Contributions Made by the Financial System 4 Transfers of Resources from Surplus

Monetary Policy on the Way out of the Crisis

Monetary Policy on the Way out of the Crisis Professor Juergen von Hagen - Bruegel and University of Bonn 1. THE END OF THE CRISIS IS AT HANDS More than two years after the beginning, in August 2007, of

Monetary Policy on the Way out of the Crisis Professor Juergen von Hagen - Bruegel and University of Bonn 1. THE END OF THE CRISIS IS AT HANDS More than two years after the beginning, in August 2007, of

Yves Mersch: Monetary policy and economic inequality

Yves Mersch: Monetary policy and economic inequality Keynote speech by Mr Yves Mersch, Member of the Executive Board of the European Central Bank, at the Corporate Credit Conference, hosted by Muzinich,

Yves Mersch: Monetary policy and economic inequality Keynote speech by Mr Yves Mersch, Member of the Executive Board of the European Central Bank, at the Corporate Credit Conference, hosted by Muzinich,

WHAT THE REALLY HAPPENED...

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

Chapter 24 CRISES IN EMERGING MARKETS

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

IT Can Happen Again: A Global Financial Crisis This time a Gringo Pathology?

IT Can Happen Again: A Global Financial Crisis This time a Gringo Pathology? Why is the financial system important? "Financial systems are crucial to the alloca2on of resources in a modern economy. They

IT Can Happen Again: A Global Financial Crisis This time a Gringo Pathology? Why is the financial system important? "Financial systems are crucial to the alloca2on of resources in a modern economy. They

Historical Backdrop to the 2007/08 Liquidity Crunch

/08 Liquidity Historical /08 Liquidity Christopher G. Lamoureux October 1, /08 Liquidity Long Term Capital Management August 17, Russian Government restructured debt. Relatively minor event that shook

/08 Liquidity Historical /08 Liquidity Christopher G. Lamoureux October 1, /08 Liquidity Long Term Capital Management August 17, Russian Government restructured debt. Relatively minor event that shook

CCSB Bail-Out Bulletin No. 2

CCSB Bail-Out Bulletin No. 2 If at first you don t succeed.... The Emergency Economic Stabilization Act of 2008 finally passed Congress on the second try, and the President wasted nary a second before

CCSB Bail-Out Bulletin No. 2 If at first you don t succeed.... The Emergency Economic Stabilization Act of 2008 finally passed Congress on the second try, and the President wasted nary a second before

Known and Unknown Unknowns: The Ongoing Monetary Policy Response to the Financial Crisis

Known and Unknown Unknowns: The Ongoing Monetary Policy Response to the Financial Crisis Thomas H. Root Drake University Subjects: Economics, Finance Article Type: Viewpoint In February 2002 Donald Rumsfeld,

Known and Unknown Unknowns: The Ongoing Monetary Policy Response to the Financial Crisis Thomas H. Root Drake University Subjects: Economics, Finance Article Type: Viewpoint In February 2002 Donald Rumsfeld,