Integrating Real Estate Market-Based Indicators into Fundamental Home Price Forecasting Systems

|

|

|

- Clifton Lindsey

- 5 years ago

- Views:

Transcription

1 Integrating Real Estate Market-Based Indicators into Fundamental Home Price Forecasting Systems Western Economics Association 86 th Annual Conference 8:15 am 10:00 am, Saturday, July 2, 2011 Forecasting Short and Medium-Run Trends in Home Prices Chair: Jesse Weiher, Federal Housing Finance Agency by Norm Miller, PhD, Professor, University of San Diego Contact: Michael Sklarz, PhD, CEO and President, Collateral Analytics Contact:

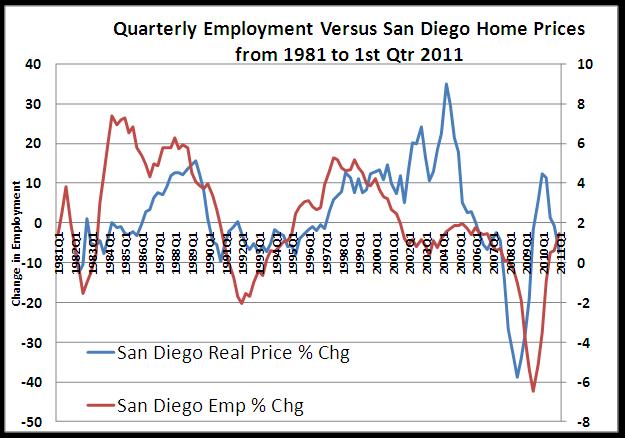

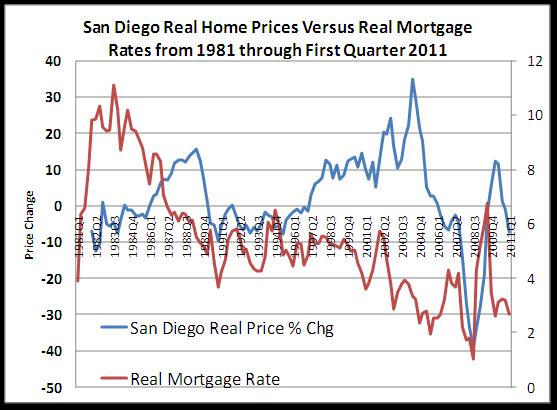

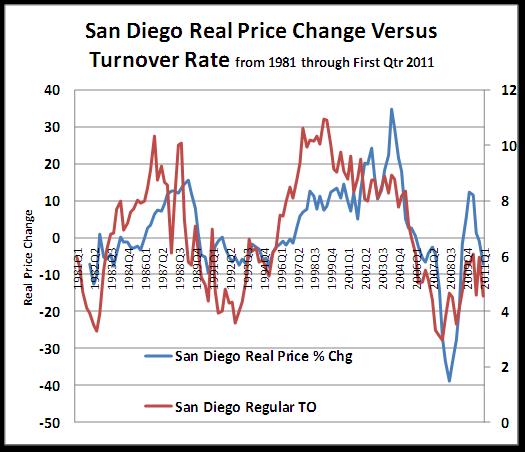

2 Our Results We can predict housing market prices fairly well in the long run using economic fundamentals representing demand, supply and the capital markets. To predict shorter term price trends and turning points we need to add a variety of market-based technical indicators, along with factors that may be unique to recent market conditions or unique to local markets. Variable selection is both and art and a science and one should remain skeptical of purely statistical curve fitting exercises. Local submarket and micro-market trends can vary significantly from broader metro trends, but we can forecast at fairly small geographic and intra-market (e.g. price range, property type, home age) levels using the nearly real-time data now available.

3 Fundamental Demand Drivers Household growth rates per year Employment in absolute numbers and in relative growth rates Past home price trends Mortgage Interest Rates and or Affordability Ratios that include Income, LTV and median prices and interest rates Hypothesized Relationship On Housing Prices Positive Positive Positive Inverse for mortgage rates, positive for affordability indexes Rent (multifamily market) to Price (median home) ratios Positive Credit Access (LTV trends, % of Mortgages at 90% plus LTV, % of loan applications approved, average credit score) Seasonal pattern of demand for localized market Positive except for credit score which is negative. Positive for % of LTVs above 90% temporarily and then negative with a substantial lead time. Positive and negative based on month of transaction

4 Examples of Other Unique Factors Affecting Local Demand Currency Exchange Rates (Stronger foreign currency may affect local prices if a significant portion of the market is international) Hypothesized Relationship On Housing Prices Positive with strength of foreign currency, inverse with US Dollar Oil Prices (Affects transportation-dependent submarkets more so than central mixed-use locations or those with a oil sensitive economy like Houston Inverse in general but positive in markets like Houston Hurricanes, tornadoes, floods, nuclear power accidents, natural disasters Positive on remaining stock

5 Supply Drivers and Constraints Housing permits to total stock issued Wharton Residential Land Use Regulatory Index Population density (another proxy for high land costs) or land prices to median home prices Government Interference Examples Home tax credit programs Hypothesized Relationship On Housing Prices Inverse as more elastic supply puts less pressure on price Positive as the higher the hurdle to develop property the more upward pressure on prices when trends are positive. When price trends are negative, there will be less effect. Positive Positive and temporary Below-market financing subsidies Positive and temporary Changes in tax laws on capital gains Varies with the direction of the ruling; will affect behavior most just prior to the change.

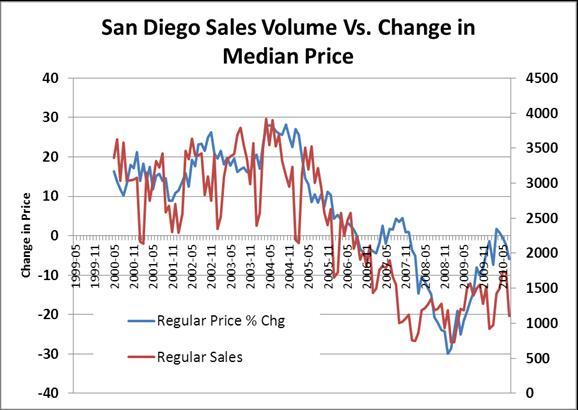

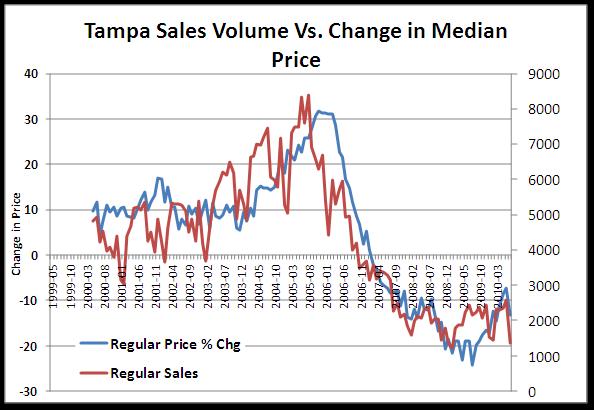

6 Market-Based Technical Examples Hypothesized Relationship On Housing Prices Sales Transaction Volume, Volume % Trend, By Price Range, By Size, By Age Positive Turnover Rate as % of Stock using Regular (non-distress) sales only Distressed Sales as Percent of Total Sales and % Trend Average New Listing Price Over Past Period Listing Price Trend and the same in terms of Average New Listing Price Per Square Feet Expired, Withdrawn, (Off-Market) Listings that did not sell as a percent of the total number of listings or sales, or the Number of Listings Pulled Off Market (by price range and size as well) Sold Price-to-Listing Price Ratio and Percent Change Trend Time on the Market to Sell (DOM) and the Percent Change Trend in DOM Positive Inverse Positive Inverse Positive Inverse

7

8

9

10 Seasonality in Prices

11 Seasonality in LA and Chicago

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28 Los Angeles Median Single Family Price and Buy/Sell Indicator

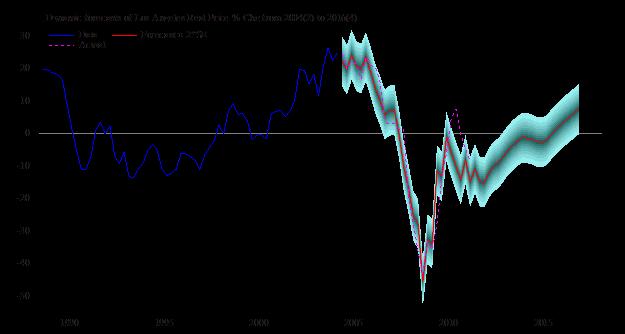

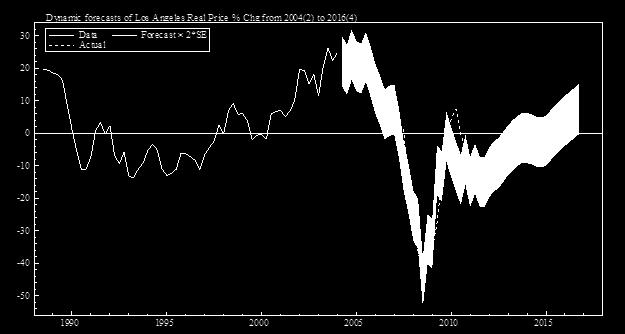

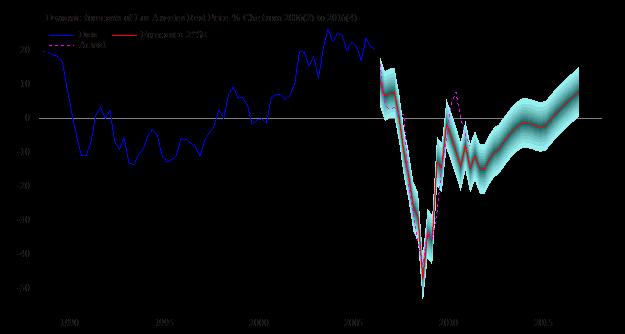

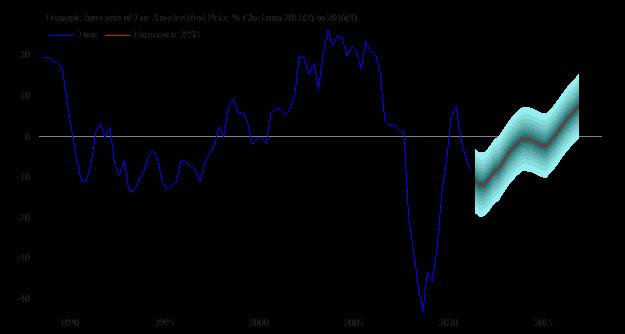

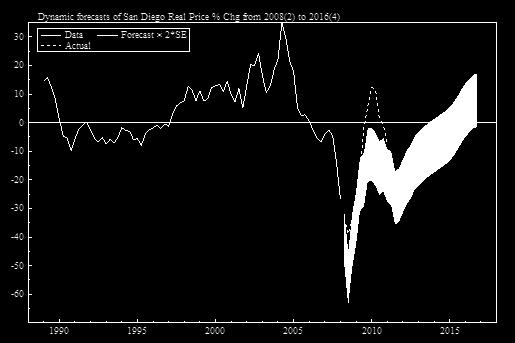

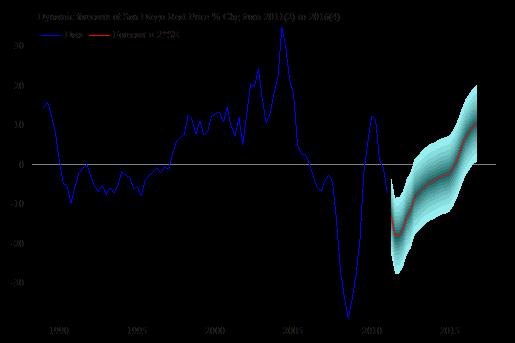

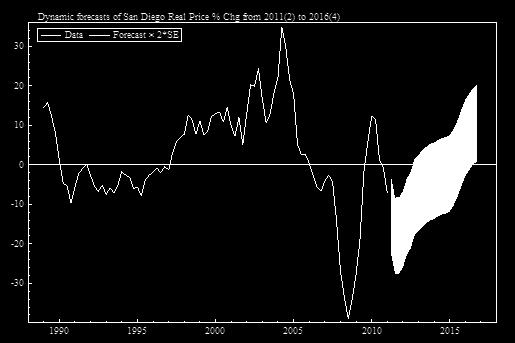

29 Forecasts

30

31

32

33

34

35

36

37 Red dots show greater price declines than blue dots in San Diego Mapped at Zip code plus 2 level Source: Collateral Analytics

38 San Diego Home Prices Mapped at Zip Plus 4

39 San Diego Mapped at Zip Plus 4 level second view

40 Conclusions We can now predict home prices reasonably well in the short and intermediate term for micro-markets around the United States. By adding market-based technical indicators of the housing market we can capture behavioral aspects and predict turning points much better than when using fundamentals alone. Metro market averages can be misleading, just as Case-Shiller indices are a poor representation of the typical owner in any given metro. Note that just because we can forecast home prices does not mean that we can capitalize on speculation in housing. Transactions costs are too high to buy and sell direct assets unless we expect shortterm price swings that exceed 20% which are very rare. Someday indices may work to allow short selling and hedging.

From a Micro Market Metric Perspective

And Current State of HousingandMortgage Markets: From a Micro Market Metric Perspective By Norm Miller Ph.D. Burnham Moores Center for Real Estate, University of San Diego and Michael Sklarz Ph.D. Co Founders

And Current State of HousingandMortgage Markets: From a Micro Market Metric Perspective By Norm Miller Ph.D. Burnham Moores Center for Real Estate, University of San Diego and Michael Sklarz Ph.D. Co Founders

Residential Mortgage Default Forecasting: How Much Do Price Trends Matter?

Residential Mortgage Default Forecasting: How Much Do Price Trends Matter? by Dr. Michael Sklarz*, Dr. Norman Miller** and Anthony Pennington-Cross*** December 4, 2018 Introduction Default rates on mortgage

Residential Mortgage Default Forecasting: How Much Do Price Trends Matter? by Dr. Michael Sklarz*, Dr. Norman Miller** and Anthony Pennington-Cross*** December 4, 2018 Introduction Default rates on mortgage

Las Vegas Housing-Market Conditions

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Volume 40, 3rd Please note: the numbers at the end of the figure and table titles correspond to sources of data, which

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Volume 40, 3rd Please note: the numbers at the end of the figure and table titles correspond to sources of data, which

Las Vegas Housing-Market Conditions

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Las Vegas Housing Market Searching for Bottom Volume 56, 3rd The national housing market was beset with problems in third

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Las Vegas Housing Market Searching for Bottom Volume 56, 3rd The national housing market was beset with problems in third

Las Vegas Housing-Market Conditions

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Facing Difficulties Volume 44, 3rd Residential construction remains depressed. The supply of empty housing units (new homes,

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Facing Difficulties Volume 44, 3rd Residential construction remains depressed. The supply of empty housing units (new homes,

Las Vegas Housing Market Conditions Volume 34, 1st Quarter, 2005

Las Vegas Housing Market Conditions The Center for Business and Economic Research Volume 34, 1st Quarter, 25 The Las Vegas Housing Market Conditions has a new look, with several new statistical additions.

Las Vegas Housing Market Conditions The Center for Business and Economic Research Volume 34, 1st Quarter, 25 The Las Vegas Housing Market Conditions has a new look, with several new statistical additions.

The State of the Nation s Housing Report 2017

The State of the Nation s Housing Report 217 Tennessee Governor s Housing Conference Nashville, Tennessee September 2, 217 The Report s Major Themes National home prices have regained their previous peak,

The State of the Nation s Housing Report 217 Tennessee Governor s Housing Conference Nashville, Tennessee September 2, 217 The Report s Major Themes National home prices have regained their previous peak,

TEMPORARY SELLING REQUIREMENTS FOR PROPERTIES IMPACTED BY THE CALIFORNIA WILDFIRES

TO: Freddie Mac Sellers December 6, 2018 2018-25 SUBJECT: TEMPORARY SELLING REQUIREMENTS RELATED TO CALIFORNIA WILDFIRES AND UPDATES TO ELIGIBILITY FOR PROPERTIES IMPACTED BY HURRICANE IRMA Freddie Mac

TO: Freddie Mac Sellers December 6, 2018 2018-25 SUBJECT: TEMPORARY SELLING REQUIREMENTS RELATED TO CALIFORNIA WILDFIRES AND UPDATES TO ELIGIBILITY FOR PROPERTIES IMPACTED BY HURRICANE IRMA Freddie Mac

CBER-LIED Report on Housing-Market Conditions

CBER-LIED Report on Housing-Market Conditions CBER and Lied Institute Report Volume 59, 2nd, Housing Markets Remained Downbeat in Second United States: Growth of the U.S. economy picked up to a slow pace

CBER-LIED Report on Housing-Market Conditions CBER and Lied Institute Report Volume 59, 2nd, Housing Markets Remained Downbeat in Second United States: Growth of the U.S. economy picked up to a slow pace

Las Vegas Housing-Market Conditions

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Not So Much of a Recovery Volume 53, 4th Sales of existing US homes registered another drop in December. The 17 percent

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Not So Much of a Recovery Volume 53, 4th Sales of existing US homes registered another drop in December. The 17 percent

COMPOSITE PRICE INDICES FOR COMMERCIAL REAL ESTATE SOARED IN 2015

CCRSI RELEASE JANUARY 216 (With data through December 215) COMPOSITE PRICE INDICES FOR COMMERCIAL REAL ESTATE SOARED IN 215 DOUBLE-DIGIT PRICE GROWTH ACROSS ALL REGIONAL AND PROPERTY-TYPE INDICES IN 215

CCRSI RELEASE JANUARY 216 (With data through December 215) COMPOSITE PRICE INDICES FOR COMMERCIAL REAL ESTATE SOARED IN 215 DOUBLE-DIGIT PRICE GROWTH ACROSS ALL REGIONAL AND PROPERTY-TYPE INDICES IN 215

Comments on Forecasts

Comments on Forecasts Kenneth T. Rosen The Sky s The Limit Conference and Expo November 3, 2017 Risks to Economic Outlook Tax cuts in a full employment economy and a global synchronized expansion leads

Comments on Forecasts Kenneth T. Rosen The Sky s The Limit Conference and Expo November 3, 2017 Risks to Economic Outlook Tax cuts in a full employment economy and a global synchronized expansion leads

CHART 2 - N. Kona Residential Median Price vs Number Sold Since 1997

GRIGGS REPORT #123 - OCTOBER 15, 212 A BIMONTHLY REAL ESTATE MARKET PERSPECTIVE FOR NORTH KONA AND THE BIG ISLAND PAGE 1 NORTH KONA RESIDENTIAL DATA ABOUT THE PENDING RATIO: The Pending Ratio is used throughout

GRIGGS REPORT #123 - OCTOBER 15, 212 A BIMONTHLY REAL ESTATE MARKET PERSPECTIVE FOR NORTH KONA AND THE BIG ISLAND PAGE 1 NORTH KONA RESIDENTIAL DATA ABOUT THE PENDING RATIO: The Pending Ratio is used throughout

SEPTEMBER S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX UP 6.2% IN LAST 12 MONTHS

SEPTEMBER S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX UP 6.2% IN LAST 12 MONTHS NEW YORK, NOVEMBER 28, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller

SEPTEMBER S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX UP 6.2% IN LAST 12 MONTHS NEW YORK, NOVEMBER 28, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller

What s Available, What s Reliable?

What s Available, What s Reliable? June 2, 2011 William R. Emmons, Daigo K. Gubo, and Julia S. Maués Federal Reserve Bank of St. Louis The views expressed are those of the presenters, not necessarily those

What s Available, What s Reliable? June 2, 2011 William R. Emmons, Daigo K. Gubo, and Julia S. Maués Federal Reserve Bank of St. Louis The views expressed are those of the presenters, not necessarily those

Office-Using Jobs and Net Migration Point to Continued Strength

October 20, 2017 Office-Using Jobs and Net Migration Point to Continued Strength Key Takeaways Secondary Sunbelt office markets are priced to offer attractive, risk-adjusted returns relative to the Gateway²

October 20, 2017 Office-Using Jobs and Net Migration Point to Continued Strength Key Takeaways Secondary Sunbelt office markets are priced to offer attractive, risk-adjusted returns relative to the Gateway²

2019 Outlook. January

2019 Outlook January 2019 0 Performance in the multifamily market remained healthy during 2018 and is expected to continue into 2019, but with more modest growth in comparison to recent years. The multifamily

2019 Outlook January 2019 0 Performance in the multifamily market remained healthy during 2018 and is expected to continue into 2019, but with more modest growth in comparison to recent years. The multifamily

A Divided Real Estate Nation

Real Estate Reality Check Explanation of "What Happened" from the 26 Leadership Conference Boom ended August 2 Mortgage rates rose almost one point Affordability conditions deteriorated Speculative investors

Real Estate Reality Check Explanation of "What Happened" from the 26 Leadership Conference Boom ended August 2 Mortgage rates rose almost one point Affordability conditions deteriorated Speculative investors

COMMERCIAL REAL ESTATE PRICING LEAPS FORWARD IN AUGUST BOOSTED BY STRONG NET ABSORPTION IN FIRST HALF OF YEAR

CCRSI RELEASE OCTOBER 2012 (With data through AUGUST 2012) COMMERCIAL REAL ESTATE PRICING LEAPS FORWARD IN AUGUST BOOSTED BY STRONG NET ABSORPTION IN FIRST HALF OF YEAR CCRSI INDICES POST STRONGEST GAINS

CCRSI RELEASE OCTOBER 2012 (With data through AUGUST 2012) COMMERCIAL REAL ESTATE PRICING LEAPS FORWARD IN AUGUST BOOSTED BY STRONG NET ABSORPTION IN FIRST HALF OF YEAR CCRSI INDICES POST STRONGEST GAINS

Subprime Bond Case Study Two Harbors Investment Corp. August 6, 2014

Two Harbors Investment Corp. Two Harbors Investment Corp. is proud to present:. The company believes periodic webinars will provide an opportunity to share more in-depth insights on various topics which

Two Harbors Investment Corp. Two Harbors Investment Corp. is proud to present:. The company believes periodic webinars will provide an opportunity to share more in-depth insights on various topics which

Las Vegas Housing Market Conditions

Las Vegas Housing Market Conditions The Center for Business and Economic Research Las Vegas Housing Market Conditions, Volume 35, 2nd 2005 Volume 35, 2nd 2005 Please note: the numbers at the end of the

Las Vegas Housing Market Conditions The Center for Business and Economic Research Las Vegas Housing Market Conditions, Volume 35, 2nd 2005 Volume 35, 2nd 2005 Please note: the numbers at the end of the

CHART 2 - N. Kona Residential Median Price vs Number Sold Since 1997

GRIGGS REPORT #152 - DECEMBER 31, 13 A TWICE MONTHLY REAL ESTATE MARKET PERSPECTIVE FOR NORTH KONA AND THE BIG ISLAND PAGE 1 NORTH KONA RESIDENTIAL DATA ABOUT THE PENDING RATIO: The Pending Ratio is used

GRIGGS REPORT #152 - DECEMBER 31, 13 A TWICE MONTHLY REAL ESTATE MARKET PERSPECTIVE FOR NORTH KONA AND THE BIG ISLAND PAGE 1 NORTH KONA RESIDENTIAL DATA ABOUT THE PENDING RATIO: The Pending Ratio is used

CECL Workshop Vintage Method

CECL Workshop Vintage Method John J. Doherty, CPA MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2017 Wolf & Company, P.C. Introduction John J. Doherty Member of the Firm jdoherty@wolfandco.com

CECL Workshop Vintage Method John J. Doherty, CPA MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2017 Wolf & Company, P.C. Introduction John J. Doherty Member of the Firm jdoherty@wolfandco.com

About Landmark. Investment. Acquisitions. Joint Ventures. Property Development. Value Enhancement

About Landmark Landmark Realty Capital (LRC) is a private real estate operating, investment and development company, as well as a direct source of debt & equity capital. Our principals have over 60 years

About Landmark Landmark Realty Capital (LRC) is a private real estate operating, investment and development company, as well as a direct source of debt & equity capital. Our principals have over 60 years

CCRSI RELEASE APRIL 2014 (With data through FEBRUARY 2014)

") CCRSI RELEASE APRIL 2014 (With data through FEBRUARY 2014) PRICE MOMENTUM FOR COMMERCIAL REAL ESTATE CONTINUED TO BUILD IN FEBRUARY REFLECTING BROAD RECOVERY IN MARKET FUNDAMENTALS AND PRICING, EQUAL-WEIGHTED

CCRSI RELEASE APRIL 2014 (With data through FEBRUARY 2014) PRICE MOMENTUM FOR COMMERCIAL REAL ESTATE CONTINUED TO BUILD IN FEBRUARY REFLECTING BROAD RECOVERY IN MARKET FUNDAMENTALS AND PRICING, EQUAL-WEIGHTED

Las Vegas Housing-Market Conditions

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Still, a Ways to Go Volume 45, 4th The oversupply of single-family units that was created in the speculative-housing euphoria

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Still, a Ways to Go Volume 45, 4th The oversupply of single-family units that was created in the speculative-housing euphoria

COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY

CCRSI RELEASE JULY 2013 (With data through May 2013) COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY STRONG ABSORPTION ACROSS ALLL SIZE AND QUALITY DIMENSIONS OF REAL ESTATEE SECTOR REFLECTED

CCRSI RELEASE JULY 2013 (With data through May 2013) COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY STRONG ABSORPTION ACROSS ALLL SIZE AND QUALITY DIMENSIONS OF REAL ESTATEE SECTOR REFLECTED

Housing & Mortgage Outlook. Frank Nothaft Chief Economist May 22, 2018

Housing & Mortgage Outlook Frank Nothaft Chief Economist May 22, 2018 Economic & Housing Outlook Effect of higher mortgage rates Inventory-for-sale remains low Less refinance, more purchase & home-improvement

Housing & Mortgage Outlook Frank Nothaft Chief Economist May 22, 2018 Economic & Housing Outlook Effect of higher mortgage rates Inventory-for-sale remains low Less refinance, more purchase & home-improvement

Mortgage Rates, Household Balance Sheets, and Real Economy

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

Mortgage Rates, Household Balance Sheets, and Real Economy May 2015 Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao

PRESS RELEASE. Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices

Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices New York, August 27, 2013 Data through June 2013, released today by for its S&P/Case-Shiller 1 Home Price

Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices New York, August 27, 2013 Data through June 2013, released today by for its S&P/Case-Shiller 1 Home Price

Are You as Diversified as You Think?

Are You as Diversified as You Think? A BERKSHIRE RESEARCH VIEWPOINT August 2017 Are You as Diversified as You Think? A BERKSHIRE RESEARCH VIEWPOINT August 2017 2 EXECUTIVE SUMMARY As the U.S. business

Are You as Diversified as You Think? A BERKSHIRE RESEARCH VIEWPOINT August 2017 Are You as Diversified as You Think? A BERKSHIRE RESEARCH VIEWPOINT August 2017 2 EXECUTIVE SUMMARY As the U.S. business

Home Prices Extend Gains According to the S&P/Case-Shiller Home Price Indices

PRESS RELEASE Home Prices Extend Gains According to the S&P/Case-Shiller Home Price Indices New York, January 29, 2013 Data through November 2012, released today by S&P Dow Jones Indices for its S&P/Case-Shiller

PRESS RELEASE Home Prices Extend Gains According to the S&P/Case-Shiller Home Price Indices New York, January 29, 2013 Data through November 2012, released today by S&P Dow Jones Indices for its S&P/Case-Shiller

COMMERCIAL REAL ESTATE PRICES MIXED: GENERAL COMMERCIAL SECTOR GAINS MOMENTUM WHILE INVESTMENT GRADE SEES SEASONAL DIP

APRIL 2012 CCRSI RELEASE (With data through February 2012) COMMERCIAL REAL ESTATE PRICES MIXED: GENERAL COMMERCIAL SECTOR GAINS MOMENTUM WHILE INVESTMENT GRADE SEES SEASONAL DIP SLOW BUT STABLE PRICING

APRIL 2012 CCRSI RELEASE (With data through February 2012) COMMERCIAL REAL ESTATE PRICES MIXED: GENERAL COMMERCIAL SECTOR GAINS MOMENTUM WHILE INVESTMENT GRADE SEES SEASONAL DIP SLOW BUT STABLE PRICING

Real Estate Investment and Capital Market Perspectives An evolving and different recovery continues

Real Estate Investment and Capital Market Perspectives An evolving and different recovery continues presented to: NCREIF Valuation Committee Jim Clayton, Ph.D. Vice President Research Cornerstone Real

Real Estate Investment and Capital Market Perspectives An evolving and different recovery continues presented to: NCREIF Valuation Committee Jim Clayton, Ph.D. Vice President Research Cornerstone Real

S&P CORELOGIC CASE-SHILLER NATIONAL INDEX SETS 30-MONTH ANNUAL RETURN HIGH

S&P CORELOGIC CASE-SHILLER NATIONAL INDEX SETS 30-MONTH ANNUAL RETURN HIGH NEW YORK, FEBRUARY 28, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller Indices,

S&P CORELOGIC CASE-SHILLER NATIONAL INDEX SETS 30-MONTH ANNUAL RETURN HIGH NEW YORK, FEBRUARY 28, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller Indices,

COMMERCIAL PRICING SURGE

CCRSI RELEASE MARCH 2013 (With data through JANUARY 2013) COMMERCIAL REAL ESTATE PRICING LEVELS OFF FOLLOWING YEAR-END SURGE IN JANUARY INCREASING LIQUIDITY AND DECLINING DISTRESSED IMPROVING INVESTOR

CCRSI RELEASE MARCH 2013 (With data through JANUARY 2013) COMMERCIAL REAL ESTATE PRICING LEVELS OFF FOLLOWING YEAR-END SURGE IN JANUARY INCREASING LIQUIDITY AND DECLINING DISTRESSED IMPROVING INVESTOR

Nationally, Home Prices Went Up in the Second Quarter of 2011 According to the S&P/Case-Shiller Home Price Indices

Nationally, Home Prices Went Up in the Second Quarter of 2011 According to the S&P/Case-Shiller Home Price Indices New York, August 30, 2011 Data through June 2011, released today by S&P Indices for its

Nationally, Home Prices Went Up in the Second Quarter of 2011 According to the S&P/Case-Shiller Home Price Indices New York, August 30, 2011 Data through June 2011, released today by S&P Indices for its

Housing Recovery is Underway, But Not for Everyone

Housing Recovery is Underway, But Not for Everyone Eric Belsky August 2013 Dallas, TX Housing Markets Have Corrected In Significant Ways Both price and quantity reductions have occurred Even after price

Housing Recovery is Underway, But Not for Everyone Eric Belsky August 2013 Dallas, TX Housing Markets Have Corrected In Significant Ways Both price and quantity reductions have occurred Even after price

LAS VEGAS LEADS PRICE GAINS IN JUNE ACCORDING TO S&P CORELOGIC CASE-SHILLER INDEX

LAS VEGAS LEADS PRICE GAINS IN JUNE ACCORDING TO S&P CORELOGIC CASE-SHILLER INDEX NEW YORK, AUGUST 28, 2018 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller Indices,

LAS VEGAS LEADS PRICE GAINS IN JUNE ACCORDING TO S&P CORELOGIC CASE-SHILLER INDEX NEW YORK, AUGUST 28, 2018 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller Indices,

ECONOMIC CURRENTS THE SOUTH FLORIDA ECONOMIC QUARTERLY

THE SOUTH FLORIDA ECONOMIC QUARTERLY Volume I, Issue 1 Introduction Economic Currents provides a comprehensive overview of the South Florida regional economy. The report combines current employment, economic

THE SOUTH FLORIDA ECONOMIC QUARTERLY Volume I, Issue 1 Introduction Economic Currents provides a comprehensive overview of the South Florida regional economy. The report combines current employment, economic

HOUSING AND LABOR MARKET TRENDS: CALIFORNIA

HOUSING AND LABOR MARKET TRENDS: CALIFORNIA July 2014 Community Development Research Federal Reserve Bank of San Francisco National Trends Composition of distressed sales by geography Percent of Buy-Side

HOUSING AND LABOR MARKET TRENDS: CALIFORNIA July 2014 Community Development Research Federal Reserve Bank of San Francisco National Trends Composition of distressed sales by geography Percent of Buy-Side

Pace of Decline in Home Prices Moderates as the First Quarter of 2012 Ends, According to the S&P/Case-Shiller Home Price Indices

PRESS RELEASE Pace of Decline in Home Prices Moderates as the First Quarter of 2012 Ends, According to the S&P/Case-Shiller Home Price Indices New York, May 29, 2012 Data through March 2012, released today

PRESS RELEASE Pace of Decline in Home Prices Moderates as the First Quarter of 2012 Ends, According to the S&P/Case-Shiller Home Price Indices New York, May 29, 2012 Data through March 2012, released today

S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX CONTINUES STEADY GAINS IN OCTOBER

S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX CONTINUES STEADY GAINS IN OCTOBER NEW YORK, DECEMBER 26, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller

S&P CORELOGIC CASE-SHILLER NATIONAL HOME PRICE NSA INDEX CONTINUES STEADY GAINS IN OCTOBER NEW YORK, DECEMBER 26, 2017 S&P Dow Jones Indices today released the latest results for the S&P CoreLogic Case-Shiller

Backtesting and Optimizing Commodity Hedging Strategies

Backtesting and Optimizing Commodity Hedging Strategies How does a firm design an effective commodity hedging programme? The key to answering this question lies in one s definition of the term effective,

Backtesting and Optimizing Commodity Hedging Strategies How does a firm design an effective commodity hedging programme? The key to answering this question lies in one s definition of the term effective,

Investor Presentation. May 13, 2013

Investor Presentation May 13, 2013 Information Related to Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform

Investor Presentation May 13, 2013 Information Related to Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform

S&P/Case-Shiller Home Price Indices

Annual Rates of Change Continue to Improve According to the S&P/Case-Shiller Home Price Indices New York, October 25, 2011 Data through August 2011, released today by S&P Indices for its S&P/Case-Shiller

Annual Rates of Change Continue to Improve According to the S&P/Case-Shiller Home Price Indices New York, October 25, 2011 Data through August 2011, released today by S&P Indices for its S&P/Case-Shiller

PRESS RELEASE. Home Price Gains Continue to Moderate According to the S&P/Case-Shiller Home Price Indices

Home Price Gains Continue to Moderate According to the S&P/Case-Shiller Home Price Indices New York, July 29, 2014 Data through May 2014, released today by for its S&P/Case-Shiller 1 Home Price Indices,

Home Price Gains Continue to Moderate According to the S&P/Case-Shiller Home Price Indices New York, July 29, 2014 Data through May 2014, released today by for its S&P/Case-Shiller 1 Home Price Indices,

All Three Home Price Composites End 2011 at New Lows According to the S&P/Case-Shiller Home Price Indices

PRESS RELEASE All Three Home Price Composites End 2011 at New Lows According to the S&P/Case-Shiller Home Price Indices New York, February 28, 2012 Data through December 2011, released today by S&P Indices

PRESS RELEASE All Three Home Price Composites End 2011 at New Lows According to the S&P/Case-Shiller Home Price Indices New York, February 28, 2012 Data through December 2011, released today by S&P Indices

Metropolitan Area Statistics (4Q 2012)

") Metropolitan Area Statistics (4Q 2012) Apartment Completions 4Q 2011 4Q 2012 % Chg. Atlanta 490 288-41% Boston 678 995 47% Chicago 506 711 41% Cleveland 4 13 225% Columbus 255 322 26% Dallas-Ft. Worth

Metropolitan Area Statistics (4Q 2012) Apartment Completions 4Q 2011 4Q 2012 % Chg. Atlanta 490 288-41% Boston 678 995 47% Chicago 506 711 41% Cleveland 4 13 225% Columbus 255 322 26% Dallas-Ft. Worth

Fannie Mae 2011 Third-Quarter Credit Supplement. November 8, 2011

Fannie Mae 2011 Third-Quarter Credit Supplement November 8, 2011 This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for

Fannie Mae 2011 Third-Quarter Credit Supplement November 8, 2011 This presentation includes information about Fannie Mae, including information contained in Fannie Mae s Quarterly Report on Form 10-Q for

VOLUME FINANCE HOUSING COMMERCIAL REAL ESTATE EMPLOYMENT TRANSIT & TOURISM

VOLUME 3 2018 EMPLOYMENT FINANCE HOUSING COMMERCIAL REAL ESTATE TRANSIT & TOURISM Published March 2018 VOLUME 3 2018 HIGHLIGHTS Unemployment in New York City fell to a record low in February 2018 NYC-based

VOLUME 3 2018 EMPLOYMENT FINANCE HOUSING COMMERCIAL REAL ESTATE TRANSIT & TOURISM Published March 2018 VOLUME 3 2018 HIGHLIGHTS Unemployment in New York City fell to a record low in February 2018 NYC-based

APARTMENT TRENDS. U.S. Economic and Multi-Family Outlook. Special Client Webcast May 31, 2006

APARTMENT TRENDS U.S. Economic and Multi-Family Outlook Special Client Webcast May 31, 2006 U.S. Apartment Market Economic and Apartment Supply-Demand Overview and Outlook U.S. Economic Conditions Ideal

APARTMENT TRENDS U.S. Economic and Multi-Family Outlook Special Client Webcast May 31, 2006 U.S. Apartment Market Economic and Apartment Supply-Demand Overview and Outlook U.S. Economic Conditions Ideal

An Empirical Model of Subprime Mortgage Default from 2000 to 2007

An Empirical Model of Subprime Mortgage Default from 2000 to 2007 Patrick Bajari, Sean Chu, and Minjung Park MEA 3/22/2009 1 Introduction In 2005 Q3 10.76% subprime mortgages delinquent 3.31% subprime

An Empirical Model of Subprime Mortgage Default from 2000 to 2007 Patrick Bajari, Sean Chu, and Minjung Park MEA 3/22/2009 1 Introduction In 2005 Q3 10.76% subprime mortgages delinquent 3.31% subprime

Searching For Values (and Yield) Among Distressed Debt Issuers

Among Distressed Debt Issuers") June 21, 2012 Thank you for reading Green Thought$. It is our privilege to provide you with our insight on current financial market events and our outlook on topics relevant to you. Searching For Values

June 21, 2012 Thank you for reading Green Thought$. It is our privilege to provide you with our insight on current financial market events and our outlook on topics relevant to you. Searching For Values

PRESS RELEASE. Widespread Slowdown in Home Price Gains According to the S&P/Case-Shiller Home Price Indices

Widespread Slowdown in Home Price Gains According to the S&P/Case-Shiller Home Price Indices New York, August 26, 2014 Data through June 2014, released today by for its S&P/Case-Shiller 1 Home Price Indices,

Widespread Slowdown in Home Price Gains According to the S&P/Case-Shiller Home Price Indices New York, August 26, 2014 Data through June 2014, released today by for its S&P/Case-Shiller 1 Home Price Indices,

Forward-Looking Statements

January 2018 Forward-Looking Statements The Company's assumptions and financial projections in this presentation are based upon "forward-looking" information and are being made pursuant to the safe harbor

January 2018 Forward-Looking Statements The Company's assumptions and financial projections in this presentation are based upon "forward-looking" information and are being made pursuant to the safe harbor

DFAST Modeling and Solution

Regulatory Environment Summary Fallout from the 2008-2009 financial crisis included the emergence of a new regulatory landscape intended to safeguard the U.S. banking system from a systemic collapse. In

Regulatory Environment Summary Fallout from the 2008-2009 financial crisis included the emergence of a new regulatory landscape intended to safeguard the U.S. banking system from a systemic collapse. In

STRONG MARKET FUNDAMENTALS SUPPORT BROAD PRICE GAINS IN MAY

CCRSI RELEASE JULY 2014 (With data through MAY 2014) STRONG MARKET FUNDAMENTALS SUPPORT BROAD PRICE GAINS IN MAY VALUE-WEIGHTED U.S. COMPOSITE PRICE INDEX APPROACHES PRERECESSION PEAK LEVELS This month's

CCRSI RELEASE JULY 2014 (With data through MAY 2014) STRONG MARKET FUNDAMENTALS SUPPORT BROAD PRICE GAINS IN MAY VALUE-WEIGHTED U.S. COMPOSITE PRICE INDEX APPROACHES PRERECESSION PEAK LEVELS This month's

Las Vegas Housing-Market Conditions

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Space Available Volume 50, 1st Quarter, 2009 A windshield survey, the simplest one to take, shows that Las Vegas offers

Las Vegas Housing-Market Conditions The Center for Business and Economic Research Space Available Volume 50, 1st Quarter, 2009 A windshield survey, the simplest one to take, shows that Las Vegas offers

The Single-Family Outlook and its Impact on Multifamily

The Single-Family Outlook and its Impact on Multifamily 2016 NMHC Research Forum April 6-7, 2016 Svenja Gudell, Ph.D. Zillow Chief Economist svenjag@zillow.com @SvenjaGudell HOME VALUES, INVENTORY AND

The Single-Family Outlook and its Impact on Multifamily 2016 NMHC Research Forum April 6-7, 2016 Svenja Gudell, Ph.D. Zillow Chief Economist svenjag@zillow.com @SvenjaGudell HOME VALUES, INVENTORY AND

MEGATREND 1: WAGE GROWTH IS FLAT, BUT DISCRETIONARY INCOME IS UP

MEGATRENDS MegaTrends 1. Wage growth is flat, but discretionary income is up 2. The regional economy is recovering but not yet recovered 3. Consumer behavior is changing 4. Tenant behavior is changing

MEGATRENDS MegaTrends 1. Wage growth is flat, but discretionary income is up 2. The regional economy is recovering but not yet recovered 3. Consumer behavior is changing 4. Tenant behavior is changing

Rethinking Tax Benefits for Home Owners

Marquette University e-publications@marquette Economics Faculty Research and Publications Economics, Department of 4-1-2014 Rethinking Tax Benefits for Home Owners Andrew Hanson Marquette University, andrew.r.hanson@marquette.edu

Marquette University e-publications@marquette Economics Faculty Research and Publications Economics, Department of 4-1-2014 Rethinking Tax Benefits for Home Owners Andrew Hanson Marquette University, andrew.r.hanson@marquette.edu

Office of the Chief Economist National Credit Union Administration. Economic Overview. California State Examiner School.

Office of the Chief Economist National Credit Union Administration California State Examiner School May 30, 2017 Credit Union Performance Trends Recent Data About Credit Union Performance in California,

Office of the Chief Economist National Credit Union Administration California State Examiner School May 30, 2017 Credit Union Performance Trends Recent Data About Credit Union Performance in California,

Community Banking in the 21st Century

Community Banking in the 21st Century Findings from the 2013 Federal Reserve / CSBS Survey of Community Bankers Jim Fuchs Assistant Vice President Federal Reserve Bank of St. Louis Charles Vice Commissioner

Community Banking in the 21st Century Findings from the 2013 Federal Reserve / CSBS Survey of Community Bankers Jim Fuchs Assistant Vice President Federal Reserve Bank of St. Louis Charles Vice Commissioner

Humboldt Economic Index

skip navigation Current Issue Archive Projects Sponsors Real Estate Links Home Acknowledgments Contact Information Humboldt Economic Index April 2008 Professor Erick Eschker, Director Casey O'Neill, Assistant

skip navigation Current Issue Archive Projects Sponsors Real Estate Links Home Acknowledgments Contact Information Humboldt Economic Index April 2008 Professor Erick Eschker, Director Casey O'Neill, Assistant

Real Estate Investment Guidelines Overview Buy and Hold rules. David Wright

Real Estate Investment Guidelines Overview Buy and Hold rules Financing Fannie Mae Residential (traditional fixed Rate mortgages terms can be from 8-30 years) Commercial (terms vary) Bank Portfolio Residential

Real Estate Investment Guidelines Overview Buy and Hold rules Financing Fannie Mae Residential (traditional fixed Rate mortgages terms can be from 8-30 years) Commercial (terms vary) Bank Portfolio Residential

Capital Market Update. February 10, 2011 Marc Louargand, Ph.D., CRE, FRICS Principal SALTASH PARTNERS LLC investing in American ingenuity

Capital Market Update February 10, 2011 Marc Louargand, Ph.D., CRE, FRICS Principal SALTASH PARTNERS LLC investing in American ingenuity A Brief Tour of the Capital Market What s happened in the past year?

Capital Market Update February 10, 2011 Marc Louargand, Ph.D., CRE, FRICS Principal SALTASH PARTNERS LLC investing in American ingenuity A Brief Tour of the Capital Market What s happened in the past year?

Strong Investor Demand but Policy Concerns Persist. The Nature of Health Insurance is Shifting.

U.S. Research Report 18 HEALTHCARE MARKETPLACE Strong Investor Demand but Policy Concerns Persist. The Nature of Health Insurance is Shifting. Overview The U.S. healthcare real estate sector remains on

U.S. Research Report 18 HEALTHCARE MARKETPLACE Strong Investor Demand but Policy Concerns Persist. The Nature of Health Insurance is Shifting. Overview The U.S. healthcare real estate sector remains on

NAHB Priced-Out Estimates for 2019

NAHB Priced-Out Estimates for 2019 January 2, 2019 Special Study for HousignEconomics.com By Na Zhao, Ph.D. This article announces NAHB s priced out estimates for 2019, showing how higher home prices and

NAHB Priced-Out Estimates for 2019 January 2, 2019 Special Study for HousignEconomics.com By Na Zhao, Ph.D. This article announces NAHB s priced out estimates for 2019, showing how higher home prices and

Regional Snapshot: The Cost of Living in Metro Atlanta

Regional Snapshot: The Cost of Living in Metro Atlanta Photo by rawpixel.com on Unsplash Atlanta Regional Commission, February 2018 For more information, contact: cdegiulio@atlantaregional.org In Summary

Regional Snapshot: The Cost of Living in Metro Atlanta Photo by rawpixel.com on Unsplash Atlanta Regional Commission, February 2018 For more information, contact: cdegiulio@atlantaregional.org In Summary

Defining Daily Value in a Non-Commodity Market

Defining Daily Value in a Non-Commodity Market Enabling Property Derivatives: The Radar Logic Approach Presented by Michael A. Feder, President and CEO at Real Estate Derivatives World 2007, New York,

Defining Daily Value in a Non-Commodity Market Enabling Property Derivatives: The Radar Logic Approach Presented by Michael A. Feder, President and CEO at Real Estate Derivatives World 2007, New York,

THE ECONOMIC IMPACT OF THE 2013 GENERAL OBLIGATION BONDS FOR AFFORDABLE HOUSING IN AUSTIN NOVEMBER 2016

THE ECONOMIC IMPACT OF THE 2013 GENERAL OBLIGATION BONDS FOR AFFORDABLE HOUSING IN AUSTIN NOVEMBER 2016 INTRODUCTION Civic Economics and HousingWorks are pleased to present this analysis of the economic

THE ECONOMIC IMPACT OF THE 2013 GENERAL OBLIGATION BONDS FOR AFFORDABLE HOUSING IN AUSTIN NOVEMBER 2016 INTRODUCTION Civic Economics and HousingWorks are pleased to present this analysis of the economic

JPMorgan Insurance Trust Class 1 Shares

Prospectus JPMorgan Insurance Trust Class 1 Shares May 1, 2017 JPMorgan Insurance Trust Core Bond Portfolio* * The Portfolio does not have an exchange ticker symbol. The Securities and Exchange Commission

Prospectus JPMorgan Insurance Trust Class 1 Shares May 1, 2017 JPMorgan Insurance Trust Core Bond Portfolio* * The Portfolio does not have an exchange ticker symbol. The Securities and Exchange Commission

2015 REAL ESTATE ECONOMIC FORECAST The National Economy and What It Means For Real Estate

2015 REAL ESTATE ECONOMIC FORECAST The National Economy and What It Means For Real Estate February 5, 2015 Jeanette I. Rice Kentucky Chapter National economy in great shape for 2015 Creating excellent

2015 REAL ESTATE ECONOMIC FORECAST The National Economy and What It Means For Real Estate February 5, 2015 Jeanette I. Rice Kentucky Chapter National economy in great shape for 2015 Creating excellent

Flexible Choice Bridge (ARM 7-4 )

") Flexible Choice Bridge (ARM 7-4 ) Fannie Mae Multifamily offers a 7-year variable-rate financing option with a low embedded interest rate cap, and a fixed-rate conversion option for Multifamily Affordable

Flexible Choice Bridge (ARM 7-4 ) Fannie Mae Multifamily offers a 7-year variable-rate financing option with a low embedded interest rate cap, and a fixed-rate conversion option for Multifamily Affordable

CITIES IN THE WEST: SEATTLE, LAS VEGAS AND SAN FRANCISCO LEAD GAINS IN S&P CORELOGIC CASE-SHILLER HOME PRICE INDICES

CITIES IN THE WEST: SEATTLE, LAS VEGAS AND SAN FRANCISCO LEAD GAINS IN S&P CORELOGIC CASE-SHILLER HOME PRICE INDICES NEW YORK, JANUARY 30, 2018 S&P Dow Jones Indices today released the latest results for

CITIES IN THE WEST: SEATTLE, LAS VEGAS AND SAN FRANCISCO LEAD GAINS IN S&P CORELOGIC CASE-SHILLER HOME PRICE INDICES NEW YORK, JANUARY 30, 2018 S&P Dow Jones Indices today released the latest results for

Reprinted with permission from Mortgage Banking magazine (February 2007, pages 48-56) published by the Mortgage Bankers Association (MBA).

published by the Mortgage Bankers Association (MBA).") Reprinted with permission from Mortgage Banking magazine (February 2007, pages 48-56) published by the Mortgage Bankers Association (MBA). Cover Report: Servicing Trends REFI BUSINESS 101 Steve Michaels*

Reprinted with permission from Mortgage Banking magazine (February 2007, pages 48-56) published by the Mortgage Bankers Association (MBA). Cover Report: Servicing Trends REFI BUSINESS 101 Steve Michaels*

The state of the nation s Housing 2013

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

Raising the minimum wage: What do we know? What should cities do?

Raising the minimum wage: What do we know? What should cities do? Chris Tilly Director, UCLA Institute for Research on Labor and Employment League of California Cities, Los Angeles County Division University

Raising the minimum wage: What do we know? What should cities do? Chris Tilly Director, UCLA Institute for Research on Labor and Employment League of California Cities, Los Angeles County Division University

HOUSING REPORT SOUTHEAST MICHIGAN SEPTEMBER 2018

SOUTHEAST MICHIGAN SEPTEMBER 2018 Southeast Michigan Recovery Run How Much Longer? This month marks the 10-year anniversary of the market peak prior to the bursting of the housing bubble. The nationwide

SOUTHEAST MICHIGAN SEPTEMBER 2018 Southeast Michigan Recovery Run How Much Longer? This month marks the 10-year anniversary of the market peak prior to the bursting of the housing bubble. The nationwide

Identifying, Assessing and Mitigating Potential Redlining Risk

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

State of the U.S. Multifamily Market. Q Review and Forecast

State of the U.S. Multifamily Market Q1 2015 Review and Forecast Agenda Economy Leasing Fundamentals Rent and NOI Trends Single-Family Market Capital Markets Economy page 3 GDP Growth Contributions To

State of the U.S. Multifamily Market Q1 2015 Review and Forecast Agenda Economy Leasing Fundamentals Rent and NOI Trends Single-Family Market Capital Markets Economy page 3 GDP Growth Contributions To

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class Manuel Adelino Antoinette Schoar Felipe Severino Duke, MIT and NBER, Dartmouth Discussion: Nancy Wallace, UC Berkeley

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class Manuel Adelino Antoinette Schoar Felipe Severino Duke, MIT and NBER, Dartmouth Discussion: Nancy Wallace, UC Berkeley

CCRSI RELEASE JANUARY 2014 (With data through NOVEMBER 2013)

") CCRSI RELEASE JANUARY 2014 (With data through NOVEMBER 2013) COMMERCIAL REAL ESTATE PRICES POST STEADY GAINS IN NOVEMBER STRONG ABSORPTION ACROSS PROPERTY TYPES SUPPORT BROAD GAINS IN PRICING This month's

CCRSI RELEASE JANUARY 2014 (With data through NOVEMBER 2013) COMMERCIAL REAL ESTATE PRICES POST STEADY GAINS IN NOVEMBER STRONG ABSORPTION ACROSS PROPERTY TYPES SUPPORT BROAD GAINS IN PRICING This month's

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Identifying Issues in the Subprime Mortgage Market: The Bay Area

Identifying Issues in the Subprime Mortgage Market: The Bay Area Presentation prepared by Carolina Reid, Ph.D. Community Development Department Federal Reserve Bank of San Francisco March 7, 2008 Analysis

Identifying Issues in the Subprime Mortgage Market: The Bay Area Presentation prepared by Carolina Reid, Ph.D. Community Development Department Federal Reserve Bank of San Francisco March 7, 2008 Analysis

Shorts and Derivatives in Portfolio Statistics

Shorts and Derivatives in Portfolio Statistics Morningstar Methodology Paper April 17, 2007 2007 Morningstar, Inc. All rights reserved. The information in this document is the property of Morningstar,

Shorts and Derivatives in Portfolio Statistics Morningstar Methodology Paper April 17, 2007 2007 Morningstar, Inc. All rights reserved. The information in this document is the property of Morningstar,

Understanding The Importance Of Regularly Monitoring Collateral Risk Levels

Understanding The Importance Of Regularly Monitoring Collateral Risk Levels Auto lenders have had a spike in volume since the recession because of pent-up consumer demand to replace aging vehicles and

Understanding The Importance Of Regularly Monitoring Collateral Risk Levels Auto lenders have had a spike in volume since the recession because of pent-up consumer demand to replace aging vehicles and

Economic and Fiscal Update. Ben Rosenfield, Controller Ted Egan, Ph.D., Chief Economist City and County of San Francisco January 23, 2018

Economic and Fiscal Update Ben Rosenfield, Controller Ted Egan, Ph.D., Chief Economist City and County of San Francisco January 23, 2018 San Francisco Unemployment Rate Continues to Find New Lows Now Down

Economic and Fiscal Update Ben Rosenfield, Controller Ted Egan, Ph.D., Chief Economist City and County of San Francisco January 23, 2018 San Francisco Unemployment Rate Continues to Find New Lows Now Down

AIA / COMPENSATION REPORT Compensation Report 2015 SAMPLE CHAPTER

NATIONAL REPORT Compensation Report 2015 4 Like employers in the broader construction industry, U.S. architecture firms are still recovering from the economic effects of the Great Recession. In recent

NATIONAL REPORT Compensation Report 2015 4 Like employers in the broader construction industry, U.S. architecture firms are still recovering from the economic effects of the Great Recession. In recent

2016 State of the City Mayor Mike Rawlings. December 2016

2016 State of the City Mayor Mike Rawlings December 2016 Police & Fire Pension: Assets Projected to Expire Between 2027 & 2030, Depending on Rate of Withdrawal $3.0B $2.5B $2.0B $1.5B $1.0B $0.5B $0.0B

2016 State of the City Mayor Mike Rawlings December 2016 Police & Fire Pension: Assets Projected to Expire Between 2027 & 2030, Depending on Rate of Withdrawal $3.0B $2.5B $2.0B $1.5B $1.0B $0.5B $0.0B

Supplemental Financial Information Q4 2018

A P O L L O C O M M E R C I A L R E A L E S T A T E F I N A N C E, I N C. Supplemental Financial Information Q4 2018 February 13, 2019 Information is as of December 31, 2018, except as otherwise noted.

A P O L L O C O M M E R C I A L R E A L E S T A T E F I N A N C E, I N C. Supplemental Financial Information Q4 2018 February 13, 2019 Information is as of December 31, 2018, except as otherwise noted.

Will Rising Interest Rates Pummel Your Portfolio?

Will Rising Interest Rates Pummel Your Portfolio? ULI Fall Meeting Chicago - November 2013 Dr. Richard Barkham, MRICS Global Research Director, Grosvenor Group Eileen Marrinan, CRE Director of Research,

Will Rising Interest Rates Pummel Your Portfolio? ULI Fall Meeting Chicago - November 2013 Dr. Richard Barkham, MRICS Global Research Director, Grosvenor Group Eileen Marrinan, CRE Director of Research,

HOUSING AND LABOR MARKET TRENDS: CALIFORNIA

HOUSING AND LABOR MARKET TRENDS: CALIFORNIA January 2013 Community Development Research Federal Reserve Bank of San Francisco National Trends Composition of distressed sales by geography 60% Proportion

HOUSING AND LABOR MARKET TRENDS: CALIFORNIA January 2013 Community Development Research Federal Reserve Bank of San Francisco National Trends Composition of distressed sales by geography 60% Proportion

Financial Strength and Operational Excellence

Financial Strength and Operational Excellence 425 Mass Washington, D.C. RiverTower New York, NY Longacre House New York, NY 1401 Joyce on Pentagon Row Arlington, VA JUNE 2010 Trump Place New York, NY 180

Financial Strength and Operational Excellence 425 Mass Washington, D.C. RiverTower New York, NY Longacre House New York, NY 1401 Joyce on Pentagon Row Arlington, VA JUNE 2010 Trump Place New York, NY 180

INTRODUCTION AND SUMMARY

1 INTRODUCTION AND SUMMARY Rising house prices and incomes, an aging housing stock, and a pickup in household growth are all contributing to today s strong home improvement market. Demand is robust in

1 INTRODUCTION AND SUMMARY Rising house prices and incomes, an aging housing stock, and a pickup in household growth are all contributing to today s strong home improvement market. Demand is robust in

COMMERCIAL. first look

CCRSI RELEASE AUGUST 213 (With data through June 213) COMMERCIAL REAL ESTATE PRICES SEE MIDYEAR SURGE WITH STRONGEST QUARTER RLY INCREASE SINCE 211 RECOVERY BROADENS AS GENERAL COMMERCIAL SEGMENT EDGES

CCRSI RELEASE AUGUST 213 (With data through June 213) COMMERCIAL REAL ESTATE PRICES SEE MIDYEAR SURGE WITH STRONGEST QUARTER RLY INCREASE SINCE 211 RECOVERY BROADENS AS GENERAL COMMERCIAL SEGMENT EDGES

Demand for social and affordable housing in WSCD area FINAL. Prepared for

Demand for social and affordable housing in WSCD area FINAL SEPTEMBER 2018 Prepared for NSW FHA SGS Economics and Planning Pty Ltd 2018 This report has been prepared for NSW FHA. SGS Economics and Planning

Demand for social and affordable housing in WSCD area FINAL SEPTEMBER 2018 Prepared for NSW FHA SGS Economics and Planning Pty Ltd 2018 This report has been prepared for NSW FHA. SGS Economics and Planning

Progress and Postulates: Seeds of Opportunity in Tehama County and the North State Corning, CA April 23, 2013

Progress and Postulates: Seeds of Opportunity in Tehama County and the North State Corning, CA April 23, 2013 Robert Eyler, PhD Frank Howard Allen Research Scholar and Professor, Economics Director, Executive

Progress and Postulates: Seeds of Opportunity in Tehama County and the North State Corning, CA April 23, 2013 Robert Eyler, PhD Frank Howard Allen Research Scholar and Professor, Economics Director, Executive