2013 San Diego Economic Outlook. Marney Cox Chief Economist San Diego Association of Governments November 15, 2012

|

|

|

- Noel Walsh

- 5 years ago

- Views:

Transcription

1 2013 San Diego Economic Outlook Marney Cox Chief Economist San Diego Association of Governments November 15, 2012

2 The Problem Gross Domestic Product Trillion$ Annual Gap Potential GDP Actual GDP

3 Big Picture What Caused the Problem? Jobs Consumption Expenditures Disposable Income

4 US Change in Payroll Jobs Steep Drop & Slow Rebound During Recession Recession 132% Starts December 2007 During Expansion Expansion Begins July 2009 Debt / Income Ratio 66% - 8% - 7.1M Jobs 5% - 3% 1% 26 Months 40 Months

5 Why Slow Job Growth? Did $787B (6% of GDP) Federal Stimulus Generate Jobs? Employment Multiplier is zero Job created is offset by a job lost. Employment Multiplier is one or less Each dollar of spending on idle resources adds one dollar to GDP. Employment Multiplier exceeds one Earnings from newly employed resources create jobs for other idle resources.

6 US $787 Billion Stimulus Package Less than 10% of Stimulus Funds Spent Generated Earnings Targeted Stimulus (multiplier > 1) $62B - Tax incentives for homes and cars - Education layoff prevention Discretionary Spending (multiplier << 1) $428B - Jobless benefits - Health care for needy - Medicaid costs - Job training - Affordable housing programs Tax Incentives & Breaks (multiplier = 0) $279B - Renewable energy - Home energy efficiency - Faster depreciation for capital investments - Tax credits for workers

7 US Lowering the U-Rate Will Take Time Until U Falls Expect More Stimulus Policies % Unemployed 27 Weeks or More New LF Entrants % of Unemployed Expenditures 40% 10% Requires 1.2M Jobs/Yr 20% $1.3 Trillion Deficit Years Years

8 US Change in Consumer Consumption Consumption Represents 70%+ of GDP During Recession Recession 132% Starts December 2007 Expansion Begins Expansion Begins July 2009 July 2009 Debt / Income Ratio - 8% 5% - 3% - 6% 66% 1% 8 Quarters 11 Quarters

9 US Why Slow Consumption Growth? Contributors to Slow Growth Household Credit Debt Outstanding Personal Savings Rate 132% 112% Debt / Income Ratio Debt / Income Ratio 5% 3.3% 66% 66% 1% 1% Years Years Years

10 US Change in Real Disposable Income Affects Sustainability-Gap Widening During Recession Recession 132% Starts Starts December Debt / Income Ratio - 5.7% - 8% During During Expansion Expansion Expansion Begins Expansion Begins Expansion July 2009 July Begins 2009 July % 5% - 3% -9.0% 1% 26 Months 4027 Months

11 Why Slow Income Growth? Emp/Pop Ratio Discouraged Workers Wages & Hours Worked Disposable Income Y-O-Y ( Cumulative Change Index 2005=100) Ave Wkly Hours -4ppt Real -5% Wages

12 Attempts to Fix the Problem Have They Worked? Increase Deficit Spending Increase Loanable Funds Lower Interest Rates

13 US Deficit Spending & Job Openings Attempt 1 to Fix the Problem Federal Federal Revenue Surplus & Expenditures & Deficit Expenditures Unemployed Per Per Job Opening 6.8-U / Opening 6.8-U / Opening $1.3 Trillion Deficit Revenues 4.3-U / Opening 3.8-U / Opening $1.3 Trillion Deficit Years Years

14 US Interest Rates & Housing Starts Attempt 2 to Fix the Problem Federal Reserve Interest Rates FF Rate New Housing Starts 2.3M Starts $1.3 Trillion Deficit 10 Year T- Rate $1.3 Trillion 0.872M Starts Years Years

15 US Loanable Funds & Loans Excess Bank Reserves Attempt 3 to Fix the Problem $1.3 Trillion Deficit $1.3 Trillion Years Years

16 Outlook for San Diego

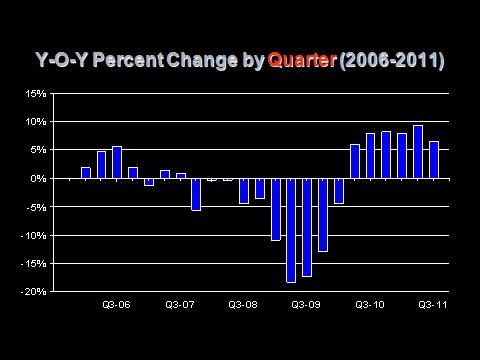

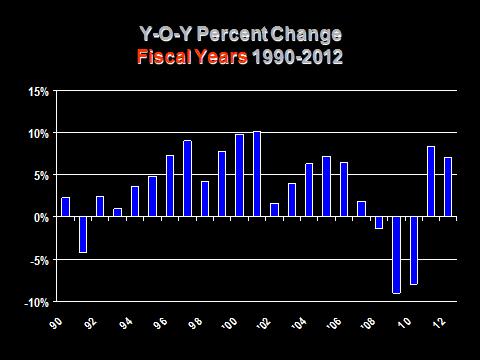

17 SD Payroll Jobs Change Y-O-Y by Quarter ,000 60,000 40,000 20, ,000-40,000-60,000-80, ,000

18 SD Payroll Jobs Change Y-O-Y by Month 40,000 20, ,000-40,000-60,000-80, ,

19 SD 2011 Jobs Actual vs Estimate (EDD Non-Agricultural Employment) 25,000 20,000 15,000 10, Est 2011 Act 5, ,000 Jan Feb Mar Apr May Jun Jul Aug Sep

20 SD Job Change Industries -40,000-20, ,000 40,000-31,800-9,700-23,300-7,300-13,500-11,700-4,900-1,200 6,000 19,600

21 Employment (in Thousands) Jobs by Industry (non-agricultural ) 1,400 1,200 1, Government Professional and Business Services Trade Leisure and Hospitality Educational and Health Services Manufacturing Natural Resources and Mining Construction Financial Activities Other Services Information Transportation, Warehousing and Utilities Agriculture

22 Monthly Unemployment Rates September 2011 to 2012 (YOY) 14.00% San Diego 9.7% to 8.4% California (SA) 11.9% to 10.2% 12.00% United States (SA) 9.0% to 7.9% 10.00% 8.00% 6.00% 4.00% 2.00% 0.00%

23 SD Per Capita Income Real 2009$, % Growth 50,000 45,000 40,000 35,000 30,000 25,000 20,000 15,000 10,000 5, (P)

24 SD Venture Capital Funds Resources for High Tech Jobs, M$ per Year $2,500 $2,000 $1,500 $1,000 23Q12 $500 $ '00 '02 '04 '06 '

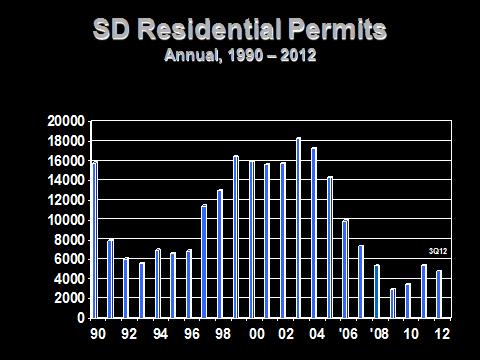

25 SD Housing Permits & Prices

26 SD Population Growth-Slow & Changing Annual Change Population, Dom & Intl Migration, Employment ,000 70,000 50,000 30,000 10,000-10,000-30,000-50,000-70, '00 '05 10 Population Domestic Migration International Migration Employment

27 SD Taxable Sales (Percent Change)

28 Trade Value M$ Trade with Mexico thru Otay Mesa $35,000 $30,000 $25,000 $20,000 $15,000 $10,000 $5,000 $0

29 2013 Outlook Summary Continued Slow-Below Trend-Growth in 2013 National / International No Recession, Not Out of Woods Large Output Gap-Slow Growth Recent Data-third time a charm? Uncertainties-Cliff, Europe Problem is speed not direction San Diego Job Growth 1%; U-rate 8.0% Home Price +5%; Trade with Mexico +6% Fiscal Cliff threat to San Diego

30 2013 San Diego Economic Outlook Marney Cox Chief Economist San Diego Association of Governments November 15, 2012

2012 Economic Outlook. Marney Cox Chief Economist San Diego Association of Governments April 11, 2012

2012 Economic Outlook Marney Cox Chief Economist San Diego Association of Governments April 11, 2012 Big Picture State of the Recovery Three Key Growth Trends Jobs Disposable Income Consumption Expenditures

2012 Economic Outlook Marney Cox Chief Economist San Diego Association of Governments April 11, 2012 Big Picture State of the Recovery Three Key Growth Trends Jobs Disposable Income Consumption Expenditures

2012 Economic Outlook. Marney Cox Chief Economist San Diego Association of Governments December 15, 2011

2012 Economic Outlook Marney Cox Chief Economist San Diego Association of Governments December 15, 2011 Three Trends to Watch Job Growth Consumption Expenditures Disposable Income Growth US Payroll Jobs

2012 Economic Outlook Marney Cox Chief Economist San Diego Association of Governments December 15, 2011 Three Trends to Watch Job Growth Consumption Expenditures Disposable Income Growth US Payroll Jobs

Economic Outlook 2013 Impact on California

The Fermanian Business & Economic Institute business & economics in action FBEI 2013 Economic Outlook 2013 Impact on California 29 th Annual San Diego Economic Roundtable January 25, 2013 Lynn Reaser,

The Fermanian Business & Economic Institute business & economics in action FBEI 2013 Economic Outlook 2013 Impact on California 29 th Annual San Diego Economic Roundtable January 25, 2013 Lynn Reaser,

2010 Economic Forecast: U.S. and State Conditions

2010 Economic Forecast: U.S. and State Conditions Russell R. Evans Director and Research Economist Center for Applied Economic Research Oklahoma State University Stillwater russell.evans@okstate.edu http://www.spears.okstate.edu/caer

2010 Economic Forecast: U.S. and State Conditions Russell R. Evans Director and Research Economist Center for Applied Economic Research Oklahoma State University Stillwater russell.evans@okstate.edu http://www.spears.okstate.edu/caer

Robert D. Cruz, PhD, Chief Economist

Robert D. Cruz, PhD, Chief Economist Office of Economic Development and International Trade Miami-Dade County cruzr1@miamidade.gov / www.miamidade.gov/oedit Office of Economic Development and International

Robert D. Cruz, PhD, Chief Economist Office of Economic Development and International Trade Miami-Dade County cruzr1@miamidade.gov / www.miamidade.gov/oedit Office of Economic Development and International

The next recession will not be. The Great Recession. Damon Runberg, Economist Oregon Employment Department

The next recession will not be The Great Recession Damon Runberg, Economist Oregon Employment Department Why the fears? Simplified Business Cycle Peak 2 consecutive quarters of GDP declines Wages Rise

The next recession will not be The Great Recession Damon Runberg, Economist Oregon Employment Department Why the fears? Simplified Business Cycle Peak 2 consecutive quarters of GDP declines Wages Rise

Economic Data and Interest Rate Forecast

Economic Data and Interest Rate Forecast February 2018 (Data through February 14, 2018) Monthly highlights Nonfarm Payroll off to solid start in 2018 Year over year wage growth jumps Manufacturing sector

Economic Data and Interest Rate Forecast February 2018 (Data through February 14, 2018) Monthly highlights Nonfarm Payroll off to solid start in 2018 Year over year wage growth jumps Manufacturing sector

Outlook 2018: IE and Southern California So Cal Economic Summit Corona Chamber of Commerce March 29, 2018

Outlook 2018: IE and Southern California 2018 So Cal Economic Summit Corona Chamber of Commerce March 29, 2018 Robert A. Kleinhenz, Ph.D. Economist/Exec Director of Research UCR Business Forecast Outline

Outlook 2018: IE and Southern California 2018 So Cal Economic Summit Corona Chamber of Commerce March 29, 2018 Robert A. Kleinhenz, Ph.D. Economist/Exec Director of Research UCR Business Forecast Outline

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16 FISCAL POLICY IN THE GREAT RECESSION MARCH 19, 2018 I. OVERVIEW II. ECONOMIC STIMULUS ACT

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16 FISCAL POLICY IN THE GREAT RECESSION MARCH 19, 2018 I. OVERVIEW II. ECONOMIC STIMULUS ACT

National Economic Conditions. Cheyenne AIA Meeting February 25th, 2011 Rob Godby

National Economic Conditions Cheyenne AIA Meeting February 25th, 2011 Rob Godby Percent Change Recovery is Technically Underway 8 Quarter-Quarter Growth in Real GDP 6 4 2 0-2 -4-6 -8 I II III IV I II III

National Economic Conditions Cheyenne AIA Meeting February 25th, 2011 Rob Godby Percent Change Recovery is Technically Underway 8 Quarter-Quarter Growth in Real GDP 6 4 2 0-2 -4-6 -8 I II III IV I II III

The Transitioning Massachusetts Economy

The Transitioning Massachusetts Economy Alan Clayton-Matthews School of Public Policy and Urban Affairs Northeastern University February 4, 2011 MassEcon Members Meeting Quarterly Growth at Annual Rates

The Transitioning Massachusetts Economy Alan Clayton-Matthews School of Public Policy and Urban Affairs Northeastern University February 4, 2011 MassEcon Members Meeting Quarterly Growth at Annual Rates

U.S. Economic Update and Outlook. Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 2013

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

Monthly Labour Force Survey Statistics December 2018

800 Monthly Labour Force Survey Statistics CALGARY CMA Table 282-0135 Labour force survey estimates (LFS), by census metropolitan area based on 2011 census boundaries, 3-month moving average, seasonally

800 Monthly Labour Force Survey Statistics CALGARY CMA Table 282-0135 Labour force survey estimates (LFS), by census metropolitan area based on 2011 census boundaries, 3-month moving average, seasonally

Monthly Labour Force Survey Statistics November 2018

800 Monthly Labour Force Survey Statistics CALGARY CMA Table 282-0135 Labour force survey estimates (LFS), by census metropolitan area based on 2011 census boundaries, 3-month moving average, seasonally

800 Monthly Labour Force Survey Statistics CALGARY CMA Table 282-0135 Labour force survey estimates (LFS), by census metropolitan area based on 2011 census boundaries, 3-month moving average, seasonally

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee June 8-9, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee June 8-9, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

VECTRA BANK 23 RD ANNUAL ECONOMIC FORECAST BREAKFAST START SMART IN 2016! Member FDIC VectraBank.com

VECTRA BANK 23 RD ANNUAL ECONOMIC FORECAST BREAKFAST START SMART IN 2016! Member FDIC VectraBank.com Colorado s Economy and State Budget Office of State Planning and Budgeting April 26, 2016 Jason Schrock,

VECTRA BANK 23 RD ANNUAL ECONOMIC FORECAST BREAKFAST START SMART IN 2016! Member FDIC VectraBank.com Colorado s Economy and State Budget Office of State Planning and Budgeting April 26, 2016 Jason Schrock,

ECONOMIC OUTLOOK GROWING BUT SLOWING. Chris Akers State Demography Office November 4, 2016

z ECONOMIC OUTLOOK GROWING BUT SLOWING Chris Akers State Demography Office November 4, 2016 OVERVIEW Global Economic Outlook Better in 2017 U.S. Economic Overview Slowing Job Growth Colorado 2015 Economic

z ECONOMIC OUTLOOK GROWING BUT SLOWING Chris Akers State Demography Office November 4, 2016 OVERVIEW Global Economic Outlook Better in 2017 U.S. Economic Overview Slowing Job Growth Colorado 2015 Economic

Illinois Job Index Note: BLS revised its estimates for the number of jobs and seasonal adjustment method at the beginning of 2010.

Illinois Job Index Release Data Issue 4/21/2010 Jan 1990 / Mar 2010 Note: BLS revised its estimates for the number of jobs and seasonal adjustment method at the beginning of 2010. For April Illinois Job

Illinois Job Index Release Data Issue 4/21/2010 Jan 1990 / Mar 2010 Note: BLS revised its estimates for the number of jobs and seasonal adjustment method at the beginning of 2010. For April Illinois Job

Illinois Job Index. Growth Rate %

Illinois Job Index Release Data Issue 03/14/2011 Jan 1990 / Jan 2011 2011.02 www.real.illinois.edu For January Illinois Job Index, the Nation, RMW and the state all had positive job growth. The monthly

Illinois Job Index Release Data Issue 03/14/2011 Jan 1990 / Jan 2011 2011.02 www.real.illinois.edu For January Illinois Job Index, the Nation, RMW and the state all had positive job growth. The monthly

The Outlook for the U.S. Economy: Sunny Skies But Developing Storm Clouds? The Financial Executives Networking Group Des Peres, MO

The Outlook for the U.S. Economy: Sunny Skies But Developing Storm Clouds? The Financial Executives Networking Group Des Peres, MO Kevin L. Kliesen Business Economist and Research Officer March 28, 2018

The Outlook for the U.S. Economy: Sunny Skies But Developing Storm Clouds? The Financial Executives Networking Group Des Peres, MO Kevin L. Kliesen Business Economist and Research Officer March 28, 2018

The Great Recession 1-2 Punch of Credit Crisis and Consumer Retrenchment

Economic Recovery: Wherefore Art Thou? Jon Haveman Chief Economist, BAC Economic Institute November 8, 1 The Great Recession 1- Punch of Credit Crisis and Consumer Retrenchment 6 GDP Growth (SAAR) and

Economic Recovery: Wherefore Art Thou? Jon Haveman Chief Economist, BAC Economic Institute November 8, 1 The Great Recession 1- Punch of Credit Crisis and Consumer Retrenchment 6 GDP Growth (SAAR) and

The U.S. and California Is The Recovery Here at Last? UCLA Anderson School of

The U.S. and California Is The Recovery Here at Last? Jerry Nickelsburg Senior Economist UCLA Anderson Forecast State of the County January 20, 2010 SEPTEMBER 2008 In September 2008 Financial Markets Stopped

The U.S. and California Is The Recovery Here at Last? Jerry Nickelsburg Senior Economist UCLA Anderson Forecast State of the County January 20, 2010 SEPTEMBER 2008 In September 2008 Financial Markets Stopped

Economic and Fiscal Update. Ben Rosenfield, Controller Ted Egan, Ph.D., Chief Economist City and County of San Francisco January 23, 2018

Economic and Fiscal Update Ben Rosenfield, Controller Ted Egan, Ph.D., Chief Economist City and County of San Francisco January 23, 2018 San Francisco Unemployment Rate Continues to Find New Lows Now Down

Economic and Fiscal Update Ben Rosenfield, Controller Ted Egan, Ph.D., Chief Economist City and County of San Francisco January 23, 2018 San Francisco Unemployment Rate Continues to Find New Lows Now Down

December Employment Report: Further Deterioration of Labor Market Conditions January 9, 2009

Northern Trust Global Economic Research 50 South LaSalle Chicago, Illinois 60603 northerntrust.com Asha G. Bangalore agb3@ntrs.com December Employment Report: Further Deterioration of Labor Market Conditions

Northern Trust Global Economic Research 50 South LaSalle Chicago, Illinois 60603 northerntrust.com Asha G. Bangalore agb3@ntrs.com December Employment Report: Further Deterioration of Labor Market Conditions

Review of Membership Developments

RIPE Network Coordination Centre Review of Membership Developments 7 October 2009/ GM / Lisbon http://www.ripe.net 1 Applications development RIPE Network Coordination Centre 140 120 100 80 60 2007 2008

RIPE Network Coordination Centre Review of Membership Developments 7 October 2009/ GM / Lisbon http://www.ripe.net 1 Applications development RIPE Network Coordination Centre 140 120 100 80 60 2007 2008

Economic Indicators For Manufacturing Executives

Economic Indicators For Manufacturing Executives Valuable Data for a Complex World Presented by: Cliff Waldman Chief Economist, MAPI Foundation cwaldman@mapi.net Today s Presentation The Value of Economic

Economic Indicators For Manufacturing Executives Valuable Data for a Complex World Presented by: Cliff Waldman Chief Economist, MAPI Foundation cwaldman@mapi.net Today s Presentation The Value of Economic

The Great Recession 1-2 Punch of Credit Crisis and Consumer Retrenchment

Economic Recovery: Wherefore Art Thou? Jon Haveman Chief Economist, BAC Economic Institute October, 211 The Great Recession 1-2 Punch of Credit Crisis and Consumer Retrenchment 6 GDP Growth (SAAR) and

Economic Recovery: Wherefore Art Thou? Jon Haveman Chief Economist, BAC Economic Institute October, 211 The Great Recession 1-2 Punch of Credit Crisis and Consumer Retrenchment 6 GDP Growth (SAAR) and

Paul Sommers Seattle University February 2009

The Economy and the Regional Construction Market Paul Sommers Seattle University February 2009 Employment falling, financial market chaos continues Extraordinary policy measures taken by both the Fed and

The Economy and the Regional Construction Market Paul Sommers Seattle University February 2009 Employment falling, financial market chaos continues Extraordinary policy measures taken by both the Fed and

C H A P T E R 1 T H E I L L I N O I S R E P O R T

C H A P T E R 1 8 T H E I L L I N O I S R E P O R T 2 0 1 3 C H A P T E R 1 Giertz After the Great Recession, Where is the Great Recovery? By J. Fred Giertz This chapter provides a broad overview of trends

C H A P T E R 1 8 T H E I L L I N O I S R E P O R T 2 0 1 3 C H A P T E R 1 Giertz After the Great Recession, Where is the Great Recovery? By J. Fred Giertz This chapter provides a broad overview of trends

An abnormally-slow December caps off the year with a range of bright spots as well as challenges. U.S. employment situation: September 2013

An abnormally-slow December caps off the year with a range of bright spots as well as challenges U.S. employment situation: September 2013 U.S. Release employment date: October situation: 22, December

An abnormally-slow December caps off the year with a range of bright spots as well as challenges U.S. employment situation: September 2013 U.S. Release employment date: October situation: 22, December

U.S. and New England Economic Conditions and Outlook

U.S. and New England Economic Conditions and Outlook Yolanda Kodrzycki Senior Economist and Policy Advisor charts prepared by Ana Patricia Muñoz presented to New England Board of Higher Education conference

U.S. and New England Economic Conditions and Outlook Yolanda Kodrzycki Senior Economist and Policy Advisor charts prepared by Ana Patricia Muñoz presented to New England Board of Higher Education conference

Vermont Tax Seminar. Comments on the 2017 Economic Outlook Presentation to the. December 8, 2016

Comments on the 2017 Economic Outlook Presentation to the Vermont Tax Seminar December 8, 2016 Jeffrey B. Carr President and Senior Economist Economic & Policy Resources, Inc. Now the 4 th Longest Up-Cycle

Comments on the 2017 Economic Outlook Presentation to the Vermont Tax Seminar December 8, 2016 Jeffrey B. Carr President and Senior Economist Economic & Policy Resources, Inc. Now the 4 th Longest Up-Cycle

Research & Policy Brief Number 4 December 2009

Institute for Research on Labor and Employment Research & Policy Brief Number 4 December 2009 California Crisis: A Portrait of Unemployed Workers By Lauren D. Appelbaum, Ph.D. Research Director The United

Institute for Research on Labor and Employment Research & Policy Brief Number 4 December 2009 California Crisis: A Portrait of Unemployed Workers By Lauren D. Appelbaum, Ph.D. Research Director The United

Poland s Economic Prospects

Poland s Economic Prospects Unicredit Conference Warsaw, June 8, 11 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe Recovery is driven by domestic demand Contributions to Real

Poland s Economic Prospects Unicredit Conference Warsaw, June 8, 11 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe Recovery is driven by domestic demand Contributions to Real

The Economic & Financial Outlook

The Economic & Financial Outlook James Marple Director & Senior Economist TD Economics May 3, 2018 Global Economies Break Pattern Of Serial Disappointment 4.0 World GDP, Year/Year % Change 3.9 3.8 3.7

The Economic & Financial Outlook James Marple Director & Senior Economist TD Economics May 3, 2018 Global Economies Break Pattern Of Serial Disappointment 4.0 World GDP, Year/Year % Change 3.9 3.8 3.7

HOUSTON-THE WOODLANDS-SUGAR LAND METROPOLITAN STATISTICAL AREA (H-W-S MSA) Visit our website at

Visit our website at") Labor Market Information DECEMBER 2015 Employment Data HOUSTON-THE WOODLANDS-SUGAR LAND METROPOLITAN STATISTICAL AREA () Visit our website at www.wrksolutions.com The Houston-The Woodlands-Sugar Land Metropolitan

Labor Market Information DECEMBER 2015 Employment Data HOUSTON-THE WOODLANDS-SUGAR LAND METROPOLITAN STATISTICAL AREA () Visit our website at www.wrksolutions.com The Houston-The Woodlands-Sugar Land Metropolitan

Dealing with a Difficult Economy

Dealing with a Difficult Economy CATTC Jack Kyser Sr. VP & Chief Economist, LAEDC June 12, 2008 The R Word or Not? LOTS OF HURDLES FOR THE U.S. ECONOMY Housing -- when will it recover? Credit problems

Dealing with a Difficult Economy CATTC Jack Kyser Sr. VP & Chief Economist, LAEDC June 12, 2008 The R Word or Not? LOTS OF HURDLES FOR THE U.S. ECONOMY Housing -- when will it recover? Credit problems

Will the Recovery Ever End? Certified Financial Planners

Will the Recovery Ever End? Certified Financial Planners Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 25, 219 Attention: This

Will the Recovery Ever End? Certified Financial Planners Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 25, 219 Attention: This

Radu Mihai Balan, Edilberto L. Segura

April 15 GDP expanded by.9% yoy in 1, reaching EUR 15.7 billion. Industrial output expanded 1.% yoy in January, slowing down from 3.1% yoy in December. The consolidated budget deficit posted a.33% of GDP

April 15 GDP expanded by.9% yoy in 1, reaching EUR 15.7 billion. Industrial output expanded 1.% yoy in January, slowing down from 3.1% yoy in December. The consolidated budget deficit posted a.33% of GDP

Chapter 16: FISCAL POLICY

Chapter 16: FISCAL POLICY FISCAL POLICY AND ITS EFFECT ON AGGREGATE DEMAND & AGGREGATE SUPPLY What is GOVERNMENT BUDGET? The government budget is an annual statement of the revenues, the outlays, and surplus

Chapter 16: FISCAL POLICY FISCAL POLICY AND ITS EFFECT ON AGGREGATE DEMAND & AGGREGATE SUPPLY What is GOVERNMENT BUDGET? The government budget is an annual statement of the revenues, the outlays, and surplus

The Arkansas Economic Outlook

The Arkansas Economic Outlook Dr. Michael Pakko Chief Economist and State Economic Forecaster Institute for Economic Advancement, UALR November 16, 2016 The views expressed are my own, and do not necessarily

The Arkansas Economic Outlook Dr. Michael Pakko Chief Economist and State Economic Forecaster Institute for Economic Advancement, UALR November 16, 2016 The views expressed are my own, and do not necessarily

SUMMARY OF SELECTED ECONOMIC INDICATORS

SUMMARY OF SELECTED ECONOMIC INDICATORS RECENT DATA GRAPHS HISTORICAL DATA GRAPHS P.E.I. CONSUMER PRICE INDEX P.E.I. LABOUR FORCE STATISTICS CANADA/P.E.I. GROSS DOMESTIC PRODUCT, INCOME-BASED CANADA /

SUMMARY OF SELECTED ECONOMIC INDICATORS RECENT DATA GRAPHS HISTORICAL DATA GRAPHS P.E.I. CONSUMER PRICE INDEX P.E.I. LABOUR FORCE STATISTICS CANADA/P.E.I. GROSS DOMESTIC PRODUCT, INCOME-BASED CANADA /

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

The Arkansas Economic Outlook

The Arkansas Economic Outlook Dr. Michael Pakko Chief Economist and State Economic Forecaster Arkansas Economic Development Institute, UALR December 1, 2017 Overview Review of Economic Conditions: Output

The Arkansas Economic Outlook Dr. Michael Pakko Chief Economist and State Economic Forecaster Arkansas Economic Development Institute, UALR December 1, 2017 Overview Review of Economic Conditions: Output

SHAMBLING FORWARD. 02/13/2014 WORLD POPULATION 2 WALL STREET, MAIN STREET, AND CAPITOL HILL: AN ECONOMIC UPDATE

SHAMBLING FORWARD. WALL STREET, MAIN STREET, AND CAPITOL HILL: AN ECONOMIC UPDATE Shamble: To walk in an awkward, lazy, or unsteady manner, shuffling the feet FEBRUARY 12, 2014 David B. Hanson, CPA, CFA

SHAMBLING FORWARD. WALL STREET, MAIN STREET, AND CAPITOL HILL: AN ECONOMIC UPDATE Shamble: To walk in an awkward, lazy, or unsteady manner, shuffling the feet FEBRUARY 12, 2014 David B. Hanson, CPA, CFA

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS Yiping Huang Seminar at the Crawford School of Economics and Government, ANU, March 1, 29 GLOBAL FINANCIAL CRISIS Three unique factors contributed to the current

CHINA S RESPONSES TO GLOBAL FINANCIAL CRISIS Yiping Huang Seminar at the Crawford School of Economics and Government, ANU, March 1, 29 GLOBAL FINANCIAL CRISIS Three unique factors contributed to the current

Key Labor Market and Economic Metrics

Key Labor Market and Economic Metrics May Update Incorporates Data Available on May 27 th, 2016 This reference is the result of a collaboration between the Bureau of Labor Market Information and Strategic

Key Labor Market and Economic Metrics May Update Incorporates Data Available on May 27 th, 2016 This reference is the result of a collaboration between the Bureau of Labor Market Information and Strategic

Economic Outlook In the Shoes of an FOMC Member

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Babson Capital/UNC Charlotte Economic Forecast March 11, 2014

Babson Capital/UNC Charlotte Economic Forecast March 11, 2014 The data used in this report comes from the websites for the U.S. Department of Commerce's Bureau of Economic Analysis (www.bea.gov) and the

Babson Capital/UNC Charlotte Economic Forecast March 11, 2014 The data used in this report comes from the websites for the U.S. Department of Commerce's Bureau of Economic Analysis (www.bea.gov) and the

Economic Outlook. Presented to IPMA Executive Seminar. Steve Lerch Chief Economist & Executive Director. September 25, 2012 Chelan, Washington

Presented to IPMA Executive Seminar Steve Lerch Chief Economist & Executive Director Chelan, Washington WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL Summary The updated economic forecast is very

Presented to IPMA Executive Seminar Steve Lerch Chief Economist & Executive Director Chelan, Washington WASHINGTON STATE ECONOMIC AND REVENUE FORECAST COUNCIL Summary The updated economic forecast is very

Nonfarm jobs climb 6,700 in May; unemployment rate steady at 4.9%

Lincoln.dyer@ct.gov appears Office of Research Scott D. Jackson, Commissioner FOR IMMEDIATE RELEASE May 2017 Data CT Unemployment Rate = 4.9% US Unemployment Rate = 4.3% Nonfarm jobs climb 6,700 in May;

Lincoln.dyer@ct.gov appears Office of Research Scott D. Jackson, Commissioner FOR IMMEDIATE RELEASE May 2017 Data CT Unemployment Rate = 4.9% US Unemployment Rate = 4.3% Nonfarm jobs climb 6,700 in May;

Will the Recovery Ever End? Boulder Economic Forecast

Will the Recovery Ever End? Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 219 #COBizOutlook Real

Will the Recovery Ever End? Boulder Economic Forecast Place cover image here Richard Wobbekind Senior Economist and Associate Dean for Business and Government Relations January 17, 219 #COBizOutlook Real

Households: Net Worth Advances, Debt Outstanding Declines. Chart 1

Asha G. Bangalore agb3@ntrs.com Households: Net Worth Advances, Debt Outstanding Declines June 9, 2 Households experienced another quarter of gains in their net worth without improvements in real estate

Asha G. Bangalore agb3@ntrs.com Households: Net Worth Advances, Debt Outstanding Declines June 9, 2 Households experienced another quarter of gains in their net worth without improvements in real estate

Economic Outlook 2011: Non-profits at the nexus of changing private and public markets

Economic Outlook 2011: Non-profits at the nexus of changing private and public markets Santa Rosa, CA June 8, 2011 Robert Eyler, Ph.D. Chair, Economics Department Frank Howard Allen Research Fellow Director,

Economic Outlook 2011: Non-profits at the nexus of changing private and public markets Santa Rosa, CA June 8, 2011 Robert Eyler, Ph.D. Chair, Economics Department Frank Howard Allen Research Fellow Director,

Consumer Price Index, Jobless Claims, Housing Starts Each of These Reports Have Favorable Aspects to Note

Consumer Price Index, Jobless Claims, Housing Starts Each of These Reports Have Favorable Aspects to Note January 19, Asha G. Bangalore agb3@ntrs.com The Consumer Price Index (CPI) held steady in December,

Consumer Price Index, Jobless Claims, Housing Starts Each of These Reports Have Favorable Aspects to Note January 19, Asha G. Bangalore agb3@ntrs.com The Consumer Price Index (CPI) held steady in December,

Outlook for the Texas Economy. Luis Bernardo Torres Ruiz, Ph.D. August 26, 2016

Outlook for the Texas Economy Luis Bernardo Torres Ruiz, Ph.D. August 26, 2016 Research Economist Texas Society of Architects Contents 1. U.S. Economic Outlook 2. Texas Economic Outlook 3. Challenges and

Outlook for the Texas Economy Luis Bernardo Torres Ruiz, Ph.D. August 26, 2016 Research Economist Texas Society of Architects Contents 1. U.S. Economic Outlook 2. Texas Economic Outlook 3. Challenges and

Figure 1: Change in LEI-N August 2018

Nebraska Monthly Economic Indicators: September 26, 2018 Prepared by the UNL College of Business, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident Economic

Nebraska Monthly Economic Indicators: September 26, 2018 Prepared by the UNL College of Business, Bureau of Business Research Author: Dr. Eric Thompson Leading Economic Indicator...1 Coincident Economic

Modest Economic Growth and Falling GDP Gap

Modest Economic Growth and Falling GDP Gap -. -. U.S. Economic Output (Real GDP - Quarterly Growth Rate).................................... : : : : : : : : : : -. -. -. -. -. -. -. -. -. -. -. -. -. -.

Modest Economic Growth and Falling GDP Gap -. -. U.S. Economic Output (Real GDP - Quarterly Growth Rate).................................... : : : : : : : : : : -. -. -. -. -. -. -. -. -. -. -. -. -. -.

World Bank Thailand Economic Monitor November Press Launch November 4, 2009

World Bank Thailand Economic Monitor November 2009 Press Launch November 4, 2009 overview The Thai economy is rebounding from a rocky first half of 2009, but the medium-term outlook is uncertain. The Thai

World Bank Thailand Economic Monitor November 2009 Press Launch November 4, 2009 overview The Thai economy is rebounding from a rocky first half of 2009, but the medium-term outlook is uncertain. The Thai

Arkansas Economic Outlook

Arkansas Economic Forecast Conference 2011 Arkansas Economic Outlook Dr. Michael Pakko Chief Economist and State Economic Forecaster Institute for Economic Advancement, UALR November 2, 2011 Arkansas Experience

Arkansas Economic Forecast Conference 2011 Arkansas Economic Outlook Dr. Michael Pakko Chief Economist and State Economic Forecaster Institute for Economic Advancement, UALR November 2, 2011 Arkansas Experience

Introduction to the UK Economy

Introduction to the UK Economy What are the key objectives of macroeconomic policy? Price Stability (CPI Inflation of 2%) Growth of Real GDP (National Output) Falling Unemployment / Raising Employment

Introduction to the UK Economy What are the key objectives of macroeconomic policy? Price Stability (CPI Inflation of 2%) Growth of Real GDP (National Output) Falling Unemployment / Raising Employment

Economic Conditions and Outlook for the U.S., Kansas, and the Midwest

Economic Conditions and Outlook for the U.S., Kansas, and the Midwest Midwest Regional Public Finance Conference Wichita, KS April 25, 2014 Kelly D. Edmiston Federal Reserve Bank of Kansas City Overview

Economic Conditions and Outlook for the U.S., Kansas, and the Midwest Midwest Regional Public Finance Conference Wichita, KS April 25, 2014 Kelly D. Edmiston Federal Reserve Bank of Kansas City Overview

Dr. Jeffrey Michael. Director, Center for Business and Policy Research University of the Pacific

2016 San Joaquin County Economic Outlook Dr. Jeffrey Michael Director, Center for Business and Policy Research University of the Pacific U.S. and California Economic Outlook: Themes Strengths U.S. consumption

2016 San Joaquin County Economic Outlook Dr. Jeffrey Michael Director, Center for Business and Policy Research University of the Pacific U.S. and California Economic Outlook: Themes Strengths U.S. consumption

FHCF Investment Update

FHCF Investment Update Financial Market Recap Historical Yield Curves Benchmark Standings Investment Summaries by Maturity & Sector Monthly Return Comparisons Summary & Forecast Richard Smith, Portfolio

FHCF Investment Update Financial Market Recap Historical Yield Curves Benchmark Standings Investment Summaries by Maturity & Sector Monthly Return Comparisons Summary & Forecast Richard Smith, Portfolio

The Economic Outlook

The Economic Outlook 5th Annual Meyers Research: Housing Market Outlook April 18, 2018 Robert A. Kleinhenz, Ph.D. Economist/Executive Director of Research LLC Outline U.S. Economy State Economy So Cal/Local

The Economic Outlook 5th Annual Meyers Research: Housing Market Outlook April 18, 2018 Robert A. Kleinhenz, Ph.D. Economist/Executive Director of Research LLC Outline U.S. Economy State Economy So Cal/Local

ECONOMIC AND FINANCIAL HIGHLIGHTS

ECONOMIC AND FINANCIAL HIGHLIGHTS LABOR MARKET Contributions to Change in Nonfarm Payrolls 2 Unemployment and Labor Force Participation Rate 3 MANUFACTURING ISM Manufacturing Index 4 CONSUMERS Light Vehicle

ECONOMIC AND FINANCIAL HIGHLIGHTS LABOR MARKET Contributions to Change in Nonfarm Payrolls 2 Unemployment and Labor Force Participation Rate 3 MANUFACTURING ISM Manufacturing Index 4 CONSUMERS Light Vehicle

The State of Working Florida 2011

The State of Working Florida 2011 Labor Day, September 5, 2011 By Emily Eisenhauer and Carlos A. Sanchez Contact: Emily Eisenhauer Center for Labor Research and Studies Florida International University

The State of Working Florida 2011 Labor Day, September 5, 2011 By Emily Eisenhauer and Carlos A. Sanchez Contact: Emily Eisenhauer Center for Labor Research and Studies Florida International University

2015: A rosy outlook. Vlad Muscalu Chief Economist

215: A rosy outlook Vlad Muscalu Chief Economist GDP forecasting a funny rollercoaster Talking about GDP Y = C + I + G + X - M GDP = Private Consumption + Investment + +Government Consumption + Exports

215: A rosy outlook Vlad Muscalu Chief Economist GDP forecasting a funny rollercoaster Talking about GDP Y = C + I + G + X - M GDP = Private Consumption + Investment + +Government Consumption + Exports

Nonfarm jobs decline 2,000 in September; unemployment rate falls to 4.6%

Lincoln.dyer@ct.gov appears Office of Research Scott D. Jackson, Commissioner FOR IMMEDIATE RELEASE September 2017 Data CT Unemployment Rate = 4.6% US Unemployment Rate = 4.2% Nonfarm jobs decline 2,000

Lincoln.dyer@ct.gov appears Office of Research Scott D. Jackson, Commissioner FOR IMMEDIATE RELEASE September 2017 Data CT Unemployment Rate = 4.6% US Unemployment Rate = 4.2% Nonfarm jobs decline 2,000

Emerging Trends in the Regional Economy

Emerging Trends in the Regional Economy Alison Felix Economist & Branch Executive Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

Emerging Trends in the Regional Economy Alison Felix Economist & Branch Executive Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

State of Ohio Workforce. 2 nd Quarter

To Strengthen Ohio s Families through the Delivery of Integrated Solutions to Temporary Challenges State of Ohio Workforce 2 nd Quarter 2 0 1 2 Quarterly Report on the State of Ohio s Workforce Reference

To Strengthen Ohio s Families through the Delivery of Integrated Solutions to Temporary Challenges State of Ohio Workforce 2 nd Quarter 2 0 1 2 Quarterly Report on the State of Ohio s Workforce Reference

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY. Paul Darby Executive Director & Deuty Chief Economist Twitter hashtag: #psforum

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

IT STARTS HERE. Daniel R. DiMicco, Executive Chairman Nucor Corporation October 16, 2013

IT STARTS HERE Daniel R. DiMicco, Executive Chairman Nucor Corporation October 16, 2013 1 Nucor in Ohio Nucor is the largest steel producer in U.S. Headquartered in Charlotte, NC NS-Marion Bar Mill David

IT STARTS HERE Daniel R. DiMicco, Executive Chairman Nucor Corporation October 16, 2013 1 Nucor in Ohio Nucor is the largest steel producer in U.S. Headquartered in Charlotte, NC NS-Marion Bar Mill David

Keith Phillips, Sr. Economist and Advisor

The Outlook for the Texas Economy Keith Phillips, Sr. Economist and Advisor National Economic Overview Growth in US Economy Positive But Sluggish Market working to heal itself asset prices falling, inflation

The Outlook for the Texas Economy Keith Phillips, Sr. Economist and Advisor National Economic Overview Growth in US Economy Positive But Sluggish Market working to heal itself asset prices falling, inflation

Economic and Fiscal Update

Economic and Fiscal Update OCTOBER 2012 Donald J. Bruce, Professor Center for Business and Economic Research The University of Tennessee, Knoxville 88Q2 89Q2 90Q2 91Q2 92Q2 93Q2 94Q2 95Q2 96Q2 97Q2 98Q2

Economic and Fiscal Update OCTOBER 2012 Donald J. Bruce, Professor Center for Business and Economic Research The University of Tennessee, Knoxville 88Q2 89Q2 90Q2 91Q2 92Q2 93Q2 94Q2 95Q2 96Q2 97Q2 98Q2

THE STATE S REVENUE & BUDGET OUTLOOK. February 2009 Barry Boardman, Ph.D. Evan Rodewald Fiscal Research Division North Carolina General Assembly

THE STATE S REVENUE & BUDGET OUTLOOK February 2009 Barry Boardman, Ph.D. Evan Rodewald Fiscal Research Division North Carolina General Assembly State General Fund, FY 2007-08 Franchise, 2.9% Corporate

THE STATE S REVENUE & BUDGET OUTLOOK February 2009 Barry Boardman, Ph.D. Evan Rodewald Fiscal Research Division North Carolina General Assembly State General Fund, FY 2007-08 Franchise, 2.9% Corporate

May brings largest nonfarm job gain in 2014 (+5,800); unemployment rate unchanged

; unemployment rate unchanged") Office of Research Sharon M. Palmer, Commissioner FOR IMMEDIATE RELEASE May 2014 Data CT Unemployment Rate = 6.9% US Unemployment Rate = 6.3% May brings largest nonfarm job gain in 2014 (+5,800); unemployment

Office of Research Sharon M. Palmer, Commissioner FOR IMMEDIATE RELEASE May 2014 Data CT Unemployment Rate = 6.9% US Unemployment Rate = 6.3% May brings largest nonfarm job gain in 2014 (+5,800); unemployment

ECONversations. Economic and Policy Briefing Webcast Dave Altig, Research Director November 19, :00 p.m. ET

ECONversations Economic and Policy Briefing Webcast Dave Altig, Research Director November 9, 4 : p.m. ET Questions for Dave: events@atl.frb.org Technical issues: james.dooley@atl.frb.org Information received

ECONversations Economic and Policy Briefing Webcast Dave Altig, Research Director November 9, 4 : p.m. ET Questions for Dave: events@atl.frb.org Technical issues: james.dooley@atl.frb.org Information received

The Outlook for the U.S. Economy National Association of Credit Union Supervisory and Auditing Committees Annual Conference and Expo Louisville, KY

The Outlook for the U.S. Economy National Association of Credit Union Supervisory and Auditing Committees Annual Conference and Expo Louisville, KY Kevin L. Kliesen Business Economist and Research Officer

The Outlook for the U.S. Economy National Association of Credit Union Supervisory and Auditing Committees Annual Conference and Expo Louisville, KY Kevin L. Kliesen Business Economist and Research Officer

The Fate of the US Recovery: Economic Outlook and Analysis. Dr. Mira Farka

The Fate of the US Recovery: Economic Outlook and Analysis Dr. Mira Farka California State University, Fullerton Richey Advisors Inc. Coyote Hills Country Club, Fullerton, CA Nov 8, 2011 The Humpty Dumpty

The Fate of the US Recovery: Economic Outlook and Analysis Dr. Mira Farka California State University, Fullerton Richey Advisors Inc. Coyote Hills Country Club, Fullerton, CA Nov 8, 2011 The Humpty Dumpty

June 2015 Lutgert College Of Business FGCU Blvd. South Fort Myers, FL Phone

Southwest Florida Regional Economic Indicators June 215 Lutgert College Of Business 151 FGCU Blvd. South Fort Myers, FL 33965 Phone 239-59-79 www.fgcu.edu/cob/reri Table of Contents Introduction: Regional

Southwest Florida Regional Economic Indicators June 215 Lutgert College Of Business 151 FGCU Blvd. South Fort Myers, FL 33965 Phone 239-59-79 www.fgcu.edu/cob/reri Table of Contents Introduction: Regional

Analysis of CBO s Budget Outlook: Fiscal Years

Analysis of CBO s Budget Outlook: Fiscal Years 2012-2022 Feb 01, 2012 INTRODUCTION The Congressional Budget Office's (CBO) latest Budget and Economic Outlook provides sobering new evidence that our nation's

Analysis of CBO s Budget Outlook: Fiscal Years 2012-2022 Feb 01, 2012 INTRODUCTION The Congressional Budget Office's (CBO) latest Budget and Economic Outlook provides sobering new evidence that our nation's

The Urgent Need for Job Creation

The Urgent Need for Job Creation John Schmitt and Tessa Conroy July 21 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 4 Washington, D.C. 29 22-29338 www.cepr.net CEPR The Urgent

The Urgent Need for Job Creation John Schmitt and Tessa Conroy July 21 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 4 Washington, D.C. 29 22-29338 www.cepr.net CEPR The Urgent

Emerging Trends in the U.S. and Colorado Economies

Emerging Trends in the U.S. and Colorado Economies Sam Chapman Associate Economist Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

Emerging Trends in the U.S. and Colorado Economies Sam Chapman Associate Economist Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

Nonfarm jobs grow by 1,500 in October; unemployment rate unchanged at 4.2%

Lincoln.dyer@ct.gov appears Office of Research Kurt Westby, Commissioner FOR IMMEDIATE RELEASE October 2018 Data CT Unemployment Rate = 4.2% US Unemployment Rate = 3.7% Nonfarm jobs grow by 1,500 in October;

Lincoln.dyer@ct.gov appears Office of Research Kurt Westby, Commissioner FOR IMMEDIATE RELEASE October 2018 Data CT Unemployment Rate = 4.2% US Unemployment Rate = 3.7% Nonfarm jobs grow by 1,500 in October;

City of Modesto Economic Indicators December 2014 Edition

City of Modesto Economic Indicators December 2014 Edition Steve Christensen City of Modesto Economic Outlook: City of Modesto The City of Modesto continues to slowly recover from the Great Recession. Some

City of Modesto Economic Indicators December 2014 Edition Steve Christensen City of Modesto Economic Outlook: City of Modesto The City of Modesto continues to slowly recover from the Great Recession. Some

Leading Economic Indicator Nebraska

Nebraska Monthly Economic Indicators: August 19, 2016 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Nebraska Monthly Economic Indicators: August 19, 2016 Prepared by the UNL College of Business Administration, Department of Economics Authors: Dr. Eric Thompson, Dr. William Walstad Leading Economic Indicator...1

Nonfarm jobs increase by 6,100 in June; unemployment rate at 4.4%

Lincoln.dyer@ct.gov appears Office of Research Kurt Westby, Commissioner FOR IMMEDIATE RELEASE June 2018 Data CT Unemployment Rate = 4.4% US Unemployment Rate = 4.0% Nonfarm jobs increase by 6,100 in June;

Lincoln.dyer@ct.gov appears Office of Research Kurt Westby, Commissioner FOR IMMEDIATE RELEASE June 2018 Data CT Unemployment Rate = 4.4% US Unemployment Rate = 4.0% Nonfarm jobs increase by 6,100 in June;

Central Oregon Employment Situation for December 2014

January 26, 2015 Contact: Damon M. Runberg Regional Economist (541) 388-6442 Central Oregon Employment Situation for December 2014 Central Oregon closed out 2014 with mixed results. This past year Deschutes

January 26, 2015 Contact: Damon M. Runberg Regional Economist (541) 388-6442 Central Oregon Employment Situation for December 2014 Central Oregon closed out 2014 with mixed results. This past year Deschutes

PRELIMINARY IMPACT OF GLOBAL CRISIS IN INDONESIA

PRELIMINARY IMPACT OF GLOBAL CRISIS IN INDONESIA 1 Preliminary Impacts Up to January 2009, some economic indicators still showed strong results while others started to reflect impact at early stage GDP

PRELIMINARY IMPACT OF GLOBAL CRISIS IN INDONESIA 1 Preliminary Impacts Up to January 2009, some economic indicators still showed strong results while others started to reflect impact at early stage GDP

Nonfarm jobs fall by 500 in September; unemployment rate falls to 4.2%

Lincoln.dyer@ct.gov appears Office of Research Kurt Westby, Commissioner FOR IMMEDIATE RELEASE September 2018 Data CT Unemployment Rate = 4.2% US Unemployment Rate = 3.7% Nonfarm jobs fall by 500 in September;

Lincoln.dyer@ct.gov appears Office of Research Kurt Westby, Commissioner FOR IMMEDIATE RELEASE September 2018 Data CT Unemployment Rate = 4.2% US Unemployment Rate = 3.7% Nonfarm jobs fall by 500 in September;

Econ 102 Exam 2 Name ID Section Number

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

Nonfarm jobs slip 1,700 in December; unemployment rate declines to 4.4%

Lincoln.dyer@ct.gov appears Office of Research Scott D. Jackson, Commissioner FOR IMMEDIATE RELEASE December 2016 Data CT Unemployment Rate = 4.4% US Unemployment Rate = 4.7% Nonfarm jobs slip 1,700 in

Lincoln.dyer@ct.gov appears Office of Research Scott D. Jackson, Commissioner FOR IMMEDIATE RELEASE December 2016 Data CT Unemployment Rate = 4.4% US Unemployment Rate = 4.7% Nonfarm jobs slip 1,700 in

Feel No Pain: Why a Deficit In Times of High Unemployment Is Not a Burden

Issue Brief September 2010 Feel No Pain: Why a Deficit In Times of High Unemployment Is Not a Burden BY DEAN BAKER* With the economy suffering from near double-digit unemployment, public debate is dominated

Issue Brief September 2010 Feel No Pain: Why a Deficit In Times of High Unemployment Is Not a Burden BY DEAN BAKER* With the economy suffering from near double-digit unemployment, public debate is dominated

Employment in Central Oregon: January, 2015

FOR IMMEDIATE RELEASE: March 10, 2015 CONTACT INFORMATION: Damon Runberg, Regional Economist Damon.M.Runberg@oregon.gov (541) 388-6442 Employment in Central Oregon: January, 2015 Central Oregon finished

FOR IMMEDIATE RELEASE: March 10, 2015 CONTACT INFORMATION: Damon Runberg, Regional Economist Damon.M.Runberg@oregon.gov (541) 388-6442 Employment in Central Oregon: January, 2015 Central Oregon finished

Is the bounce for real? Christopher Thornberg Principal, Beacon Economics

Is the bounce for real? Christopher Thornberg Principal, Beacon Economics Will the real economy stand up? Where are we now? The good news: The recession is over The bad news: we haven t completely fixed

Is the bounce for real? Christopher Thornberg Principal, Beacon Economics Will the real economy stand up? Where are we now? The good news: The recession is over The bad news: we haven t completely fixed

Nonfarm jobs fall by 400 in February; unemployment rate unchanged at 3.8%

Lincoln.dyer@ct.gov appears Office of Research Kurt Westby, Commissioner FOR IMMEDIATE RELEASE February 2019 Data CT Unemployment Rate = 3.8% US Unemployment Rate = 3.8% Nonfarm jobs fall by 400 in February;

Lincoln.dyer@ct.gov appears Office of Research Kurt Westby, Commissioner FOR IMMEDIATE RELEASE February 2019 Data CT Unemployment Rate = 3.8% US Unemployment Rate = 3.8% Nonfarm jobs fall by 400 in February;

Finally, A Global Tailwind for U.S. Manufacturing Growth

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening