BRAZIL MEANS BUSINESS. Presentation by: Igly Serafim Senior Commercial Specialist São Paulo, Brazil

|

|

|

- Beverly Terry

- 5 years ago

- Views:

Transcription

1 BRAZIL MEANS BUSINESS Presentation by: Igly Serafim Senior Commercial Specialist São Paulo, Brazil

2 Brazil s future is today 1. Inflation control 2. Development of policies focused on social assistance. 3. Increase in investments 4. Informal economy reduction / Formal job positions increase 5. Wages increase 6. Credit and consumption expansion 7. Purchasing power 8. Demographics Source: Estadao Newspaper August 2010

3 BRAZIL USA

4 REGIONAL DISPARITIES - % of total GDP (2008) North 4,92 Center-West 7,28 South 19,03 Northeast 13,68 Southeast 55,09 Note: 5 cities represent almost 24% of Brazilian GDP as follows: SP 12% RJ 5,2% DF 3,8% BH 1,4% Curitiba 1,2% Source: International Monetary Fund

5 Brazil GDP Compared to rest of Latin America (US$ trillion) Source: CIA.gov the World Factbook

6 Brazil Record GDP 8 th on World ranking Country $ Ranking USA ,8 1º China 5.364,9 2º Japan 5.272,9 3º Germany 3.332,8 4º France 2.668,8 5º United Kingdom 2.222,6 6º Italy 2.121,1 7º Brazil 1.910,5 8º

7 Why Brazil? Economic Indicators 2010 Estimates GDP: US$ 1.65 Trillion (2009) Growth Rate: 7.4% Inflation Rate: 5% year Foreign Direct Investment : US$ 30 Billion Interest Rates, SELIC at % year Foreign Exchange Rate: 1 USD = 1.60 Reais Unemployment Rate: 7.3 % Credit Expansion: 21.2% Source: Central Bank Brazil, IBGE

8 HEALTHY ECONOMY: Macroeconomic Analysis Achieved investment grade status (S&P Rating Services April 2008) Strong post crisis economy relative to other countries Inflation under control Appreciating currency Interest rates low

9 PRESIDENT LUIS INÁCIO LULA DA SILVA Took office on January 1 st, Labor Party PT. First mandate with 61.27% in Second mandate with 60,83% in Elections October 2010.

10 EXCHANGE RATE

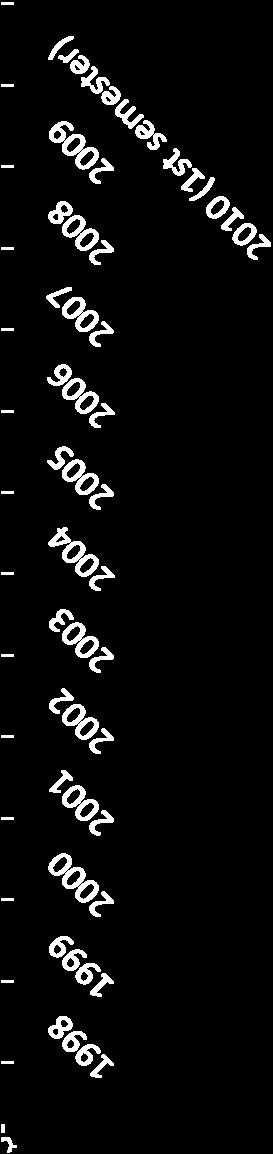

11 Growth rate Lula Government

Source: Trade Economics.")

12 Brazil Unemployment Rate (Lula Government) Source: Trade Economics.com (from IBGE)

13 Brazil Reaction to Global Financial Crisis Government measures: Tax cuts such as IPI (federal tax on domestic and imported manufactured products Interest rate reduction 10.25% per year Incentives for civil construction Infrastructure development MOST IMPORTANT: Government Banks Expanded Credit

14 UNDER LULA - ACCESS TO CREDIT More than 10 million new jobs created in formal sector. The lowest inflation rates in decades Expansion of purchasing power and credit and for millions although some contraction in 2008 Lula Administration s emphasis on lowering public debt and reducing real interest rates expands bank credit to businesses for investment. Spreads (the difference between banks cost of funds and their lending rates) is highest in the world.

15 INTEREST RATES The SELIC rate is currently 10.50% (per year). Mortgage loans range from 8% to 12% per year for up to 25 year loans plus inflation. Businesses generally pay from 2% to 4.5% (per month), depending on creditworthiness. Checking account rates are about 140 % year. Credit Card rates are 233 % per year. Source: Central Bank Brazil

16 The Favela Today (in%) Source: Copo pela Metade; Author Ricardo Neves Ibope 2003 page 224

17 Top Exports from Brazil Sugar cane Orange Juice Beef & Chicke n Oil Corn Soy Coffee Ethanol Iron ore Airplanes

18 Brazil Exports Worldwide (US$ billion) Source: Exame Magazine April 2009

19 Brazil Exports to US (US$ million)

20 Bilateral Trade (US$ Thousands) USA Exports USA Imports Office of Trade and Industry Information (OTTI), U.S. Department of Commerce

21 Brazil Compared: U.S. Exports to Latin America U$ Thousand Mexico Brazil Venezuela Colombia Chile Argentina Peru Ecuador Source: Foreign Trade Division, U.S. Census Bureau

")

22 Brazilian Imports by Economic Blocks 36,187,476,416 25,625,203,865 29,216,602,946 11,530,564,312 15,990,157,812 20,041,091,354 20,182,730,487 15,911,145,829 3,710,477, China United States (including Puerto Rico) European Union

23 Best Prospects for Sales to Brazil Agricultural Sector Aerospace (Aircraft and Parts / Airports) Electrical Power Systems Environmental Franchising ICT - Information & Communication Technologies Insurance Medical Equipment Mining Oil and Gas Pharmaceuticals Safety & Security Transportation (Ports / Railways) Travel and Tourism

24 Brazilian Barriers to Business Custo Brazil

25 Despite Economy growing, Brazil is still considered a closed market among the emerging countries

26 4 main problems affecting the Brazilian competitiveness WEF (World Economy Forum Dom Cabral Foundation Qualified labor force / education Infrastructure Bureaucracy Labor laws Customs Regulations Taxes, Fees and Duties

27 CUSTO BRAZIL: THE TAX SYSTEM Import II Export IE FEDERAL Industrialized Products IPI Credit Operations IOF Rural Property ITR Fortune STATE Heritage and Donation ITCMS Circulation of Goods and Services ICMS Property of Vehicles IPVA MUNICIPAL Urban Property IPTU Transmission of Property ITBI Services of any Nature ISS (*) Pending of regulation

28 Hypothetical Cost Buildup for an Imported Machine in US Dollars FOB price of Product 100,000 Freight 2,400 Insurance (1%) 1,000 CIF Price of Product 103,400 Import Duty Rate: 19% -- applied to CIF 19,646 IPI: 5% -- applied to CIF + import duty 6,152 ICMS: 18% -- applied to CIF + import duty + IPI 23,256 Merchant Marine Tax: 25% of ocean freight cost 600 Warehouse: 0.65% of CIF; or min. US$ 170, max US$ Terminal Handling Charges: average US$ 100 per container 100 Contribution to Custom Broker's union 2.2% CIF; or min of US$ 71, max US$ Custom Brokerage Fee: average 0.65% of CIF or min US$ 170, max US$ SISCOMEX Fee 30 Typical Cargo Transportation charge 35 Typical Bank Costs: 2% of FOB 2,000 FINAL COST 156,064

29 IPOD INDEX ipod prices around the world Here is the CommSec ipod Index, based on January 2007 prices for 2GB ipod Nanos. 1 Brazil $ India $ Sweden $ Denmark $ United Kingdom $ United States $ Japan $147.63

30 Energy

31

32 Infrastructure Matters in Brazil BR US Difference Soy production costs dollars cheaper in Brazil Transportation costs dollars cheaper in U.S. Port costs dollars cheaper in U.S. Total dollars in favor of USA Conclusion: To produce soy in Brazil is 51 dollars cheaper than in the US. But the logistics costs not only eliminate this advantage but inverts the equation. At the end, it is 24 dollars cheaper export from the US than Brazil. Source: Veja Magazine Aug/07

33 Transportation Logistics costs Transportation costs In dollars per ton BRAZIL USA ARGENTINA Estadao Newspaper, Aug. 2010

34 Infrastructure problems

35 Expansion to 2013 US$ 735 billion will be invested: 477 infrastructure 258 civil construction 100 Worldcup and Olympics Expansion to 2020 US$ 400 billion in: goods and services oil Estadao Newspaper, July 2010

36 Great opportunities to attract investments Pre Salt PAC* World Cup 2014 Olympic Games 2016 *PAC Plan to Accelerate Growth in Portuguese

37 KEY PAC PROJECTS (in USD) Infrastructure SECTOR MINISTRY FUNDING Civil Cabinet, Ministry of Transportation and Ministry of Finance USD 240 billion Sanitation Ministry of Cities USD 19 billion Science and Technology Ministry of Science and Technology USD 16 billion Education Ministry of Education USD 3.8 billion Security Ministry of Justice USD 3 billion Youth Programs Ministry of Labor USD 2.5 billion Heath Care National Health Foundation USD 1.9 billion Transportation Ministry of Cities USD 214 million TOTAL PLANNED PAC EXPENDITURES USD 287 billion

38 Pre-Salt Reserves The New Frontier: 100 Billion Barrels?

39 The Brazilian Oil and Gas Sector (November 2009) Over 60 oil companies with oil exploration and appraisal areas in Brazil Petrobras investment: US$174 B (US$ 92 in Brazil s E&P). Other oil co s: Est. US$34.5 B Opportunity: 819 oil blocks auctioned; Petrobras plans to contract about 300 new vessels (e.g. oil drilling and production platforms, ships, platform support boats, and very large crude oil carriers.) Pre salt oil fields: Petrobras plans to invest USD$ billion from 2009 to 2020 to produce 5.7 million bpd plus 1,815 million bpd from pre salt fields. This figure includes Petrobras and its partners pre salt production. Challenge: Heavy emphasis on local equipment content. Complex suppliers registration process with Petrobras

40 POWER GENERATION - renewables Prospects for Wind Power Generation

41 RIO DE JANEIRO HOSTS World Military Games 2012 World Cup 2014 Olympic Games 2016

42 Estimated investments Construction - US $50billion from Transportation Public security Education and training

43 Investments in Sport Facilities Half of Rio 2016 venues are ready 20 new facilities are to be built: Aquatic sports stadium with 18,000 seats (US$40 million) Olympic Park: gymnastics, cycling, etc. (US$200 mil.) Olympic Village of 32 buildings 12 floors each with 17,000 beds (US$450 million). Tennis Center with 16 courts (US$45 million). Renovated rowing stadium $2 million. Beach volley arena (US$7 million). Renovation of Maracanã Stadium (Opening and closing Olympic ceremonies as well as soccer games) US$400 million (completion for 2014 Soccer World Cup).

44 Investments in Hotel/Hospital Facilities In 2010, the number of visitors to the city is expected to grow in 10% in comparison to 2008, when 1.68 million tourists came to Rio. By the time of the 2014 Soccer World Cup and the 2016 Olympic Games this number will increase even more. Several hotels are being refurbished. The municipality of Rio may reduce taxes to attract new investment in hotels; thereby creating opportunities for U.S. hotel chains in refurbishment, architectural projects and building or acquiring existing hotels. As for hospitals, a clinic will be built within the Olympic Village.

45 Investments in City Infrastructure Upgrades at seaports and airports ($5 Billion) Modernization and enlargement of two International Airport terminals (increase capacity from 15 million to 25 million passengers), Highway widening, Construction of Olympic lanes, Port of Rio revitalization to include new 300,000 sq. ft. area featuring bars, restaurants, an amphitheater, multi-use space and parking, Port dredging, Construction of two new subway lines, Creation of a Bus Rapid Transit (BRT) system, Housing projects (including low income housing) and Water sanitation.

46 Challenges for new President: Taxes, fees and duties Collection tax system in Brazil is voracious, tricky and unfair US$ 663 billion US$ 2.2 of each US$ 5.88 collected became taxes in Brazil in duties Are now in progress 26.5% effective taxes on consumption of income of $600/month 7.5 % effective tax rate on consumption of $9000 monthly income

47 Challenges for new President: PAC behind schedule Macapa Airport Fortaleza Subway and dredging Recife Subway, BR-101 NorthEast, Refinaria Dredging Suape Transnordestina Railway North-South Railway BR365 - duplication Dredging São Francisco do Sul Port Dredging Itajai Salvador Subway, Despoluicao Bahia Brasilia Airport Vitoria Airport, Dredging Vitoria, Sanitation Manguinhos Complex Highway BR 493 Dredging Santos Guarulhos Airport Reform P53 Platform

48 Thank you! Igly Serafim Senior Commercial Specialist São Paulo, Brazil

Brazil s economic growth and use of the BNDES financing for strategic infrastructure projects. Tokyo June 21, Luciano Coutinho President

Brazil s economic growth and use of the BNDES financing for strategic infrastructure projects Tokyo June 21, 2011 Luciano Coutinho President Brazil begins a new development cycle The Brazilian economy

Brazil s economic growth and use of the BNDES financing for strategic infrastructure projects Tokyo June 21, 2011 Luciano Coutinho President Brazil begins a new development cycle The Brazilian economy

DOING BUSINESS IN BRAZIL. CESAR CUNHA CAMPOS DIRECTOR, FGV PROJETOS

DOING BUSINESS IN BRAZIL CESAR CUNHA CAMPOS DIRECTOR, FGV PROJETOS diretoria.fgvprojetos@fgv.br Greece, September 2014 1 ABOUT FGV AND FGV PROJETOS Fundação Getulio Vargas (FGV) was founded in 1944 FGV

DOING BUSINESS IN BRAZIL CESAR CUNHA CAMPOS DIRECTOR, FGV PROJETOS diretoria.fgvprojetos@fgv.br Greece, September 2014 1 ABOUT FGV AND FGV PROJETOS Fundação Getulio Vargas (FGV) was founded in 1944 FGV

$100bn forecast in new investment following privatization of infrastructure assets for highways, railways, ports and airports

Everywhere you do business $100bn forecast in new investment following privatization of infrastructure assets for highways, railways, ports and airports For information on doing business in Brazil, please

Everywhere you do business $100bn forecast in new investment following privatization of infrastructure assets for highways, railways, ports and airports For information on doing business in Brazil, please

Wagner Ferreira Cardoso Executive Secretary of Infrastructure National Confederation of Industry

1 Infrastructure Overview and Ports Regulatory Framework 1st CNI DIPLOMATIC BRIEFING Wagner Ferreira Cardoso Executive Secretary of Infrastructure National Confederation of Industry Brasília, June 9, 2014

1 Infrastructure Overview and Ports Regulatory Framework 1st CNI DIPLOMATIC BRIEFING Wagner Ferreira Cardoso Executive Secretary of Infrastructure National Confederation of Industry Brasília, June 9, 2014

BUSINESS MEETING BRAZIL - CHINA. Brazilian Association of Infrastructure and Basic Industries. São Paulo May 13, 2011

Brazilian Association of Infrastructure and Basic Industries BUSINESS MEETING BRAZIL - CHINA São Paulo May 13, 2011 Ralph Lima Terra Executive Vice-President 1 ABDIB AND INFRASTRUCTURE 2 ABDIB AND INFRASTRUCTURE

Brazilian Association of Infrastructure and Basic Industries BUSINESS MEETING BRAZIL - CHINA São Paulo May 13, 2011 Ralph Lima Terra Executive Vice-President 1 ABDIB AND INFRASTRUCTURE 2 ABDIB AND INFRASTRUCTURE

Investing in Brazil Trade and Promotion Department. Consulate General of Brazil in Chicago

Investing in Brazil Trade and Promotion Department. Consulate General of Brazil in Chicago Country Facts and Key Data Census 2010 IBGE Country Facts and Key Data Population: 200 million of people (2010Census)

Investing in Brazil Trade and Promotion Department. Consulate General of Brazil in Chicago Country Facts and Key Data Census 2010 IBGE Country Facts and Key Data Population: 200 million of people (2010Census)

International Taxation of Cross- Border Trade and Investments in BRICS: the Brazilian Experience. Prof. Dr. Luís Eduardo Schoueri

International Taxation of Cross- Border Trade and Investments in BRICS: the Brazilian Experience Prof. Dr. Luís Eduardo Schoueri Consumption Taxation Common Domestic Problems Diversity within the territory

International Taxation of Cross- Border Trade and Investments in BRICS: the Brazilian Experience Prof. Dr. Luís Eduardo Schoueri Consumption Taxation Common Domestic Problems Diversity within the territory

Economic Outlook January, 2012

Economic Outlook January, 2012 Summary Global economy Low global growth scenario, tail risks have become smaller. Risks (Debt Ceiling, elections in Italy, growth in Europe). Brazil Activity shows signs

Economic Outlook January, 2012 Summary Global economy Low global growth scenario, tail risks have become smaller. Risks (Debt Ceiling, elections in Italy, growth in Europe). Brazil Activity shows signs

Investor Presentation 2017

Investor Presentation 2017 Gerdau steel in the world www.gerdau.com 1 Outlook Gerdau Highlights 2 Economic outlook GDP Growth 2016 2017f 2018f World 3.1% 3.5% 3.6% US 1.6% 2.3% 2.5% Brazil -3.6% 0.5% 2.5%

Investor Presentation 2017 Gerdau steel in the world www.gerdau.com 1 Outlook Gerdau Highlights 2 Economic outlook GDP Growth 2016 2017f 2018f World 3.1% 3.5% 3.6% US 1.6% 2.3% 2.5% Brazil -3.6% 0.5% 2.5%

Presentation of 1Q13 Results

Presentation of 1Q13 Results Disclaimer This presentation may include declarations about Mills expectations regarding future events or results. All declarations based upon future expectations, rather than

Presentation of 1Q13 Results Disclaimer This presentation may include declarations about Mills expectations regarding future events or results. All declarations based upon future expectations, rather than

Brazil A COUNTRY OF CONTRASTS. May 19th, Sunrise in Amazon / Amazônia

Brazil A COUNTRY OF CONTRASTS 1 Sunrise in Amazon / Amazônia OBJECTIVE Brief presentation and discussion to put Brazil's market reality in perspective 2 Rio-Niteroi Bridge / Rio de Janeiro THREE ASPECTS

Brazil A COUNTRY OF CONTRASTS 1 Sunrise in Amazon / Amazônia OBJECTIVE Brief presentation and discussion to put Brazil's market reality in perspective 2 Rio-Niteroi Bridge / Rio de Janeiro THREE ASPECTS

Panel on Brazilian Economy

Panel on Brazilian Economy International Consultative Council FUNDAÇÃO DOM CABRAL - FDC October 2012 Luciano Coutinho Luciano Coutinho President 1 Uncertainties in the International scenery: Developed

Panel on Brazilian Economy International Consultative Council FUNDAÇÃO DOM CABRAL - FDC October 2012 Luciano Coutinho Luciano Coutinho President 1 Uncertainties in the International scenery: Developed

Corporate Presentation and 3Q17 Results

Corporate Presentation and 3Q17 Results 1 Company Overview 2 Market Outlook 3 Financial Profile 2 Overview of Mills Complete in engineering products and services, in Brazil for more than 65 years. Company

Corporate Presentation and 3Q17 Results 1 Company Overview 2 Market Outlook 3 Financial Profile 2 Overview of Mills Complete in engineering products and services, in Brazil for more than 65 years. Company

INSTITUTIONAL PRESENTATION

INSTITUTIONAL PRESENTATION DISCLAIMER This presentation contains estimates and forward-looking statements regarding our strategy and opportunities for future growth. Such information is mainly based on

INSTITUTIONAL PRESENTATION DISCLAIMER This presentation contains estimates and forward-looking statements regarding our strategy and opportunities for future growth. Such information is mainly based on

The Global Summit of Women 2009 Santiago, Chile May 14-16

The Global Summit of Women 2009 Santiago, Chile May 14-16 Presentation on Doing Business in Chile By Bruno Philippi, President, SOFOFA (Federacion Gremial de la Industria), Chile Global Summit of Women

The Global Summit of Women 2009 Santiago, Chile May 14-16 Presentation on Doing Business in Chile By Bruno Philippi, President, SOFOFA (Federacion Gremial de la Industria), Chile Global Summit of Women

Food Processing and Meat Technology to Brazil

Food Processing and Meat Technology to Brazil São Paulo, 28-31 March 2011 Invitation to join the Danish business delegation on the occasion of the official visit to Brazil of H.E. Ms. Lene Espersen, Minister

Food Processing and Meat Technology to Brazil São Paulo, 28-31 March 2011 Invitation to join the Danish business delegation on the occasion of the official visit to Brazil of H.E. Ms. Lene Espersen, Minister

April 26, Q11 Earnings Release. April 27, 2011

April 26, 2011 1Q11 Earnings Release Share Price (03/31/2011) ROMI3 R$ 11.25/share Market Capitalization (03/31/2011) R$ 841 million US$ 516 million Number of shares (03/31/2011) Common: 74,757,547 Total:

April 26, 2011 1Q11 Earnings Release Share Price (03/31/2011) ROMI3 R$ 11.25/share Market Capitalization (03/31/2011) R$ 841 million US$ 516 million Number of shares (03/31/2011) Common: 74,757,547 Total:

Brazil s Moment in the Sun

Brazil s Moment in the Sun Panel Detail: Wednesday, April 28, 2010 11:00 AM - 12:15 PM Speakers: Jose Alfredo Graca Lima, Consulate General of Brazil Everaldo Franca, CEO, PPS Portfolio Performance Inc.

Brazil s Moment in the Sun Panel Detail: Wednesday, April 28, 2010 11:00 AM - 12:15 PM Speakers: Jose Alfredo Graca Lima, Consulate General of Brazil Everaldo Franca, CEO, PPS Portfolio Performance Inc.

Economic Outlook. Macro Research Itaú Unibanco

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Swiss Global Finance. Facts and Figures

Swiss Global Finance Facts and Figures Latin America Bilateral Economic Relations Switzerland s Main Trading Partners in Latin America Share of Total Goods Exports (in % of total Swiss exports to Latin

Swiss Global Finance Facts and Figures Latin America Bilateral Economic Relations Switzerland s Main Trading Partners in Latin America Share of Total Goods Exports (in % of total Swiss exports to Latin

DAVID STUBBS ECONOMIC & BUSINESS UPDATE

DAVID STUBBS ECONOMIC & BUSINESS UPDATE Panama July 2012 Why should I care? Economic health of a country impacts everyone living or investing there. Infrastructure investment Job creation Future real estate

DAVID STUBBS ECONOMIC & BUSINESS UPDATE Panama July 2012 Why should I care? Economic health of a country impacts everyone living or investing there. Infrastructure investment Job creation Future real estate

BRAZIL. 1. General trends

Economic Survey of Latin America and the Caribbean 2014 1 BRAZIL 1. General trends In 2013, the Brazilian economy grew by 2.5%, an improvement over the 1% growth recorded in 2012. That low growth continued

Economic Survey of Latin America and the Caribbean 2014 1 BRAZIL 1. General trends In 2013, the Brazilian economy grew by 2.5%, an improvement over the 1% growth recorded in 2012. That low growth continued

Eng. José Carlos de Oliveira Lima. FIESP Vice-President CONSIC President (Superior Council of the Construction Industry)

") Eng. José Carlos de Oliveira Lima FIESP Vice-President CONSIC President (Superior Council of the Construction Industry) 2 The Production Chain from the construction industry, coordinated by the Department

Eng. José Carlos de Oliveira Lima FIESP Vice-President CONSIC President (Superior Council of the Construction Industry) 2 The Production Chain from the construction industry, coordinated by the Department

BRAGGING RIGHTS: WHAT OTHERS ARE SAYING ABOUT TEXAS

THE TEXAS ADVANTAGE BRAGGING RIGHTS: WHAT OTHERS ARE SAYING ABOUT TEXAS 2015 Gold Shovel: 2015, 2014, 2013, 2012, 2008 Silver Shovel: 2011, 2010, 2009, 2007 CEOs Name Texas Best State for Business for

THE TEXAS ADVANTAGE BRAGGING RIGHTS: WHAT OTHERS ARE SAYING ABOUT TEXAS 2015 Gold Shovel: 2015, 2014, 2013, 2012, 2008 Silver Shovel: 2011, 2010, 2009, 2007 CEOs Name Texas Best State for Business for

A-level ECONOMICS 7136/3

SPECIMEN MATERIAL A-level ECONOMICS 7136/3 Paper 3 Economic principles and issues Insert Brazil: The hot BRIC Extract A: Who are the BRICs? Extract B: Brazilian economy Extract C: How does Brazil compare

SPECIMEN MATERIAL A-level ECONOMICS 7136/3 Paper 3 Economic principles and issues Insert Brazil: The hot BRIC Extract A: Who are the BRICs? Extract B: Brazilian economy Extract C: How does Brazil compare

Presentation of 2Q13 Results

Presentation of 2Q13 Results Disclaimer This presentation may include declarations about Mills expectations regarding future events or results. All declarations based upon future expectations, rather than

Presentation of 2Q13 Results Disclaimer This presentation may include declarations about Mills expectations regarding future events or results. All declarations based upon future expectations, rather than

Y qué está pasando en Brasil?

Y qué está pasando en Brasil? Ilan Goldfajn Chief Economist and Partner, Itaú Unibanco August, 2013 Summary Why has the Brazilian economy decelerated? The low growth and full employment paradox (new middle

Y qué está pasando en Brasil? Ilan Goldfajn Chief Economist and Partner, Itaú Unibanco August, 2013 Summary Why has the Brazilian economy decelerated? The low growth and full employment paradox (new middle

GBTA BTI Outlook: Brasil

GBTA BTI Outlook: Brasil 2 nd Half - 2016 Agenda GBTA BTI Outlook Brazil: Overview Methodology GBTA BTI : Global Context Brazil Business Travel Spending Details 2 Overview In 2017, completed 8 th Global

GBTA BTI Outlook: Brasil 2 nd Half - 2016 Agenda GBTA BTI Outlook Brazil: Overview Methodology GBTA BTI : Global Context Brazil Business Travel Spending Details 2 Overview In 2017, completed 8 th Global

Global Resources Fund (PSPFX)

") Global Resources Fund (PSPFX) Global Resources are the building blocks of the world we live in. As the world s population grows and emerging regions develop a more vibrant infrastructure for commerce,

Global Resources Fund (PSPFX) Global Resources are the building blocks of the world we live in. As the world s population grows and emerging regions develop a more vibrant infrastructure for commerce,

PPPs in Brazil: a brief overview

THE PPP X-CHANGE, The GOI-ADB PPP Workshop, January 2010 PPPs in Brazil: a brief overview Isaac Pinto Averbuch Program Director Mumbai - Jan/2010 About Brazil Map of Brazil Brazil is located in Eastern

THE PPP X-CHANGE, The GOI-ADB PPP Workshop, January 2010 PPPs in Brazil: a brief overview Isaac Pinto Averbuch Program Director Mumbai - Jan/2010 About Brazil Map of Brazil Brazil is located in Eastern

MACROECONOMIC OUTLOOK

BRADESCO-APIMEC MACROECONOMIC OUTLOOK DECEMBER, 2015 FABIANA D ATRI Economic Research Departament- DEPEC 2 International outlook INTERNATIONAL SCENARIO Comingtotheendofcommoditiescycle Chinese economy

BRADESCO-APIMEC MACROECONOMIC OUTLOOK DECEMBER, 2015 FABIANA D ATRI Economic Research Departament- DEPEC 2 International outlook INTERNATIONAL SCENARIO Comingtotheendofcommoditiescycle Chinese economy

Presentation of 4Q12 Results

Presentation of 4Q12 Results Disclaimer This presentation may include declarations about Mills expectations regarding future events or results. All declarations based upon future expectations, rather than

Presentation of 4Q12 Results Disclaimer This presentation may include declarations about Mills expectations regarding future events or results. All declarations based upon future expectations, rather than

The International Executive Development Programme in Development Finance BRAZIL STUDY TOUR GUIDE Country Profile

The International Executive Development Programme in Development Finance BRAZIL STUDY TOUR GUIDE Country Profile 1. Brazil overview Brazil is the largest country in Latin America in terms of land area,

The International Executive Development Programme in Development Finance BRAZIL STUDY TOUR GUIDE Country Profile 1. Brazil overview Brazil is the largest country in Latin America in terms of land area,

APPENDIX 2 TO ANNEX VIII ICELAND SCHEDULE OF SPECIFIC COMMITMENTS

APPENDIX 2 TO ANNEX VIII ICELAND SCHEDULE OF SPECIFIC COMMITMENTS I. HORIZONTAL COMMITMENTS ALL SECTORS INCLUDED IN THIS SCHEDULE 3) All foreign investment and currency transfers must be reported to the

APPENDIX 2 TO ANNEX VIII ICELAND SCHEDULE OF SPECIFIC COMMITMENTS I. HORIZONTAL COMMITMENTS ALL SECTORS INCLUDED IN THIS SCHEDULE 3) All foreign investment and currency transfers must be reported to the

BRASIL ENERGIA PETRÓLEO Magazine

BRASIL ENERGIA PETRÓLEO Magazine Brasil Energia Petróleo is the most important and influential publication of the Brazilian oil & gas sector. It brings wide and deep monthly coverage of the key issues

BRASIL ENERGIA PETRÓLEO Magazine Brasil Energia Petróleo is the most important and influential publication of the Brazilian oil & gas sector. It brings wide and deep monthly coverage of the key issues

How Alaska's Economy Benefits from International Trade & Investment

How Alaska's Economy Benefits from International Trade & Investment With more than 95 percent of the world s population and 80 percent of the world s purchasing power outside the United States, future

How Alaska's Economy Benefits from International Trade & Investment With more than 95 percent of the world s population and 80 percent of the world s purchasing power outside the United States, future

Contents. HSBC Group in the world. HSBC in Brazil. New Economic Scenario / Macroeconomic Forecasts

HSBC GLOBAL & LOCAL STRATEGY IN A NEW ECONOMIC SCENARIO Conrado Engel CEO & President of HSBC Bank Brasil 26 March 2010 The British Chamber of Commerce and Industry in Brazil - São Paulo 0 Contents HSBC

HSBC GLOBAL & LOCAL STRATEGY IN A NEW ECONOMIC SCENARIO Conrado Engel CEO & President of HSBC Bank Brasil 26 March 2010 The British Chamber of Commerce and Industry in Brazil - São Paulo 0 Contents HSBC

Institutional Presentation Caixa para descrição.

Institutional Presentation 2016 Caixa para descrição. Disclaimer This presentation contains estimates and forward-looking statements regarding our strategy and opportunities for future growth. Such information

Institutional Presentation 2016 Caixa para descrição. Disclaimer This presentation contains estimates and forward-looking statements regarding our strategy and opportunities for future growth. Such information

Japan's Balance of Payments Statistics and International Investment Position for 2016

Japan's Balance of Payments Statistics and International Investment Position for 16 July 17 International Department Bank of Japan Japan's balance of payments statistics for 16 -- the annually revised

Japan's Balance of Payments Statistics and International Investment Position for 16 July 17 International Department Bank of Japan Japan's balance of payments statistics for 16 -- the annually revised

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS The following discussion contains an analysis of our financial condition and results of operations for the nine months

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS The following discussion contains an analysis of our financial condition and results of operations for the nine months

The Political Economy of Brazilian Local Government Taxation: changing the rules without changing the law for efficiency

The Political Economy of Brazilian Local Government Taxation: changing the rules without changing the law for efficiency Monica Pinhanez Institute on Municipal Finance and Governance Munk School of Global

The Political Economy of Brazilian Local Government Taxation: changing the rules without changing the law for efficiency Monica Pinhanez Institute on Municipal Finance and Governance Munk School of Global

Second Quarter and Six Months Ended June 30, 2008 Results Presentation. August 7, 2008

Second Quarter and Six Months Ended June 30, 2008 Results Presentation August 7, 2008 Forward Looking Statements This presentation contains forward-looking statements made pursuant to the safe harbor provisions

Second Quarter and Six Months Ended June 30, 2008 Results Presentation August 7, 2008 Forward Looking Statements This presentation contains forward-looking statements made pursuant to the safe harbor provisions

JBS 3Q14 Results Presentation November 13 th, 2014

JBS 3Q4 Results Presentation November 3 th, 04 Disclaimer This release contains forward-looking statements relating to the prospects of the business, estimates for operating and financial results, and

JBS 3Q4 Results Presentation November 3 th, 04 Disclaimer This release contains forward-looking statements relating to the prospects of the business, estimates for operating and financial results, and

How Nevada's Economy Benefits from International Trade & Investment

How Nevada's Economy Benefits from International Trade & Investment With more than 95 percent of the world s population and 80 percent of the world s purchasing power outside the United States, future

How Nevada's Economy Benefits from International Trade & Investment With more than 95 percent of the world s population and 80 percent of the world s purchasing power outside the United States, future

Investor Presentation

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Better outlook for steel consumption Region / Country (in mt and %) 2017f 17/16 World 1,535 1.3% European Union 158 0.5% NAFTA 135

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Better outlook for steel consumption Region / Country (in mt and %) 2017f 17/16 World 1,535 1.3% European Union 158 0.5% NAFTA 135

Investor Presentation

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Better outlook for steel consumption Region / Country (in mt and %) 2017f 17/16 World 1,535 1.3% European Union 158 0.5% NAFTA 135

Investor Presentation 2017 www.gerdau.com 1 Outlook Gerdau Highlights 2 Better outlook for steel consumption Region / Country (in mt and %) 2017f 17/16 World 1,535 1.3% European Union 158 0.5% NAFTA 135

Foreign Investment in Uruguay. Recent Legal Developments

Recent Legal Developments Uruguay has demonstrated a committed attitude towards investors, making the respect for the rule of law a golden rule. Basic Legal Framework Recent Legal Developments Foreign

Recent Legal Developments Uruguay has demonstrated a committed attitude towards investors, making the respect for the rule of law a golden rule. Basic Legal Framework Recent Legal Developments Foreign

The Americas. Port of the Americas. Executive Director, Port of the Americas Authority

Port the Americas Rhonda M. Castillo Gammill, Esq., P.E. Executive Director, Port the Americas Authority Port the Americas Authority - Public Corporation created by Law 171 August 11, 2002 Objective: promote,

Port the Americas Rhonda M. Castillo Gammill, Esq., P.E. Executive Director, Port the Americas Authority Port the Americas Authority - Public Corporation created by Law 171 August 11, 2002 Objective: promote,

Corporate Presentation March 2013

Corporate Presentation March 2013 Disclaimer This presentation may include declarations about Mills expectations regarding future events or results. All declarations based upon future expectations, rather

Corporate Presentation March 2013 Disclaimer This presentation may include declarations about Mills expectations regarding future events or results. All declarations based upon future expectations, rather

Investing in Mozambique UK MOZAMBIQUE INVESTMENT FORUM 2010

Investing in Mozambique UK MOZAMBIQUE INVESTMENT FORUM 2010 Structure of Presentation 1. Location 2. Reasons for Good Performance 3. Investment Policies Tax System Guarantees Tax incentives Bilateral Agreement

Investing in Mozambique UK MOZAMBIQUE INVESTMENT FORUM 2010 Structure of Presentation 1. Location 2. Reasons for Good Performance 3. Investment Policies Tax System Guarantees Tax incentives Bilateral Agreement

THE RECOVERY OF THE BRAZILIAN ECONOMY WALTER BAÈRE FILHO

THE RECOVERY OF THE BRAZILIAN ECONOMY WALTER BAÈRE FILHO Deputy Executive Secretary of Planning, Development and Management THE ECONOMY REFLECTS THE ADJUSTED POLICIES BOOMING CAPITAL MARKET 85,032 pts

THE RECOVERY OF THE BRAZILIAN ECONOMY WALTER BAÈRE FILHO Deputy Executive Secretary of Planning, Development and Management THE ECONOMY REFLECTS THE ADJUSTED POLICIES BOOMING CAPITAL MARKET 85,032 pts

How to Manage New Port Developments in what happened to 20% growth rates and readily available finance?

AAPA XVIII Latin American Congress of Ports 09 July 2009 David Taylor How to Manage New Port Developments in 2009 or what happened to 20% growth rates and readily available finance? Typical pattern in

AAPA XVIII Latin American Congress of Ports 09 July 2009 David Taylor How to Manage New Port Developments in 2009 or what happened to 20% growth rates and readily available finance? Typical pattern in

BRAZIL AND DUBAI 2018 FAMILY BANK PROPOSED BUSINESS EXPOSURE TRIP TO BRAZIL AND DUBAI

FAMILY BANK PROPOSED BUSINESS EXPOSURE TRIP TO BRAZIL AND DUBAI 7 th April 19 th April 2018 A F R I C A N T O U C H S A F A R I S L T D ( A T S T R A V E L ) Page 1 BRIEF ABOUT BRAZIL Brazil is the fifth

FAMILY BANK PROPOSED BUSINESS EXPOSURE TRIP TO BRAZIL AND DUBAI 7 th April 19 th April 2018 A F R I C A N T O U C H S A F A R I S L T D ( A T S T R A V E L ) Page 1 BRIEF ABOUT BRAZIL Brazil is the fifth

Japan's Balance of Payments Statistics and International Investment Position for 2017

Japan's Balance of Payments Statistics and International Investment Position for 217 July 218 International Department Bank of Japan Japan's balance of payments statistics for 217 -- the annually revised

Japan's Balance of Payments Statistics and International Investment Position for 217 July 218 International Department Bank of Japan Japan's balance of payments statistics for 217 -- the annually revised

The Brazilian Economy and the Pharmaceutical Market

The Brazilian Economy and the Pharmaceutical Market São Paulo, April 9th, 2010 The Brazilian Economy 2 GDP- Annual Growth Rate % per year Source: IBGE and Ministry of Economy 3 IMF Projected GDP growth

The Brazilian Economy and the Pharmaceutical Market São Paulo, April 9th, 2010 The Brazilian Economy 2 GDP- Annual Growth Rate % per year Source: IBGE and Ministry of Economy 3 IMF Projected GDP growth

$3.56 trillion. $2.216 trillion

ECONOMY SUMMARY INTRODUCTION The main goal of this macro-study is to investigate Brazil and to get a global view of its economy. This chapter will focus on Brazil s economy by giving an answer to the following

ECONOMY SUMMARY INTRODUCTION The main goal of this macro-study is to investigate Brazil and to get a global view of its economy. This chapter will focus on Brazil s economy by giving an answer to the following

Brazil: A New Major Player Emerges on the World Stage

Brazil: A New Major Player Emerges on the World Stage Brazil in Context Strengthening Economic Stability Inflation Under Control: 1984 - Present Inflation Rates (IPCA), Percent 2500 2000 1500 1000 500

Brazil: A New Major Player Emerges on the World Stage Brazil in Context Strengthening Economic Stability Inflation Under Control: 1984 - Present Inflation Rates (IPCA), Percent 2500 2000 1500 1000 500

Saudi Arabia at a Glance

Invest Saudi Table of Contents Saudi Arabia at a Glance Saudi Arabia Economy Why Invest in Saudi? Key Incentives Available for Investors Strategic Sectors & Opportunities Investments We Value the Most

Invest Saudi Table of Contents Saudi Arabia at a Glance Saudi Arabia Economy Why Invest in Saudi? Key Incentives Available for Investors Strategic Sectors & Opportunities Investments We Value the Most

B E N E F I T S O F T H E T F A I M P L E M E N T A T I O N T H E B R A Z I L I A N P R I V A T E S E C T O R P E R S P E C T I V E

B E N E F I T S O F T H E T F A I M P L E M E N T A T I O N T H E B R A Z I L I A N P R I V A T E S E C T O R P E R S P E C T I V E G E N E R A L B E N E F I T S Transparency, certainty, coordination,

B E N E F I T S O F T H E T F A I M P L E M E N T A T I O N T H E B R A Z I L I A N P R I V A T E S E C T O R P E R S P E C T I V E G E N E R A L B E N E F I T S Transparency, certainty, coordination,

OFFERING MEMORANDUM. Perimeter Road Development Site Miami, Florida

OFFERING MEMORANDUM Perimeter Road Development Site Miami, Florida A rare opportunity to acquire +/- 3.93 acres of land with unparalleled frontage onto the Dolphin Expressway and Miami International Airport

OFFERING MEMORANDUM Perimeter Road Development Site Miami, Florida A rare opportunity to acquire +/- 3.93 acres of land with unparalleled frontage onto the Dolphin Expressway and Miami International Airport

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing November 17, 2 Dr. Edward Yardeni 16-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 13 13 Figure

Chart Collection for Morning Briefing November 17, 2 Dr. Edward Yardeni 16-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 13 13 Figure

Investor Presentation. February 2008

Investor Presentation February 2008 1 1 Highlights Among the most competitive steel companies in the world Strong low cost structure as a result of diversified production processes and multiple raw material

Investor Presentation February 2008 1 1 Highlights Among the most competitive steel companies in the world Strong low cost structure as a result of diversified production processes and multiple raw material

Brazil. November, 2015 kpmg.com

Brazil November, 2015 kpmg.com Brazil by the numbers LARGEST COUNTRY IN SOUTH AMERICA IN TERMS OF GDP (BRL 4.4 TRILLION IN 2014) CHALLENGING MACROECONOMIC ENVIRONMENT A CONVOLUTION OF ECONOMIC, POLITICAL

Brazil November, 2015 kpmg.com Brazil by the numbers LARGEST COUNTRY IN SOUTH AMERICA IN TERMS OF GDP (BRL 4.4 TRILLION IN 2014) CHALLENGING MACROECONOMIC ENVIRONMENT A CONVOLUTION OF ECONOMIC, POLITICAL

Exchange rate in Brazil: a macroeconomic assessment on the first ten years of free floating policy during the Plano Real

Exchange rate in Brazil: a macroeconomic assessment on the first ten years of free floating policy during the Plano Real Alexandre da Silva de Oliveira Catholic University of São Paulo PUC-SP DEPE Research

Exchange rate in Brazil: a macroeconomic assessment on the first ten years of free floating policy during the Plano Real Alexandre da Silva de Oliveira Catholic University of São Paulo PUC-SP DEPE Research

Missouri Tourism Forecast FY

Current River Missouri Tourism Forecast FY2014-2018 St. Charles Fete de Glace St. Louis Missouri History Museum February 2014 Summary of key points Missouri s tourism economy will continue to expand over

Current River Missouri Tourism Forecast FY2014-2018 St. Charles Fete de Glace St. Louis Missouri History Museum February 2014 Summary of key points Missouri s tourism economy will continue to expand over

From HMO to IPO the Brazilian Experience. Luiz Kaufmann. IFC INTERNATIONAL HEALTH CONFERENCE 2007 April 2007

From HMO to IPO the Brazilian Experience Luiz Kaufmann IFC INTERNATIONAL HEALTH CONFERENCE 2007 April 2007 IFC INTERNATIONAL HEALTH CONFERENCE 2007 April 2007 From HMO to IPO The Brazilian Experience Luiz

From HMO to IPO the Brazilian Experience Luiz Kaufmann IFC INTERNATIONAL HEALTH CONFERENCE 2007 April 2007 IFC INTERNATIONAL HEALTH CONFERENCE 2007 April 2007 From HMO to IPO The Brazilian Experience Luiz

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile. 4-6 October 2017

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Institutional Presentation

Institutional Presentation October 2016 Caixa para descrição. Disclaimer This presentation contains estimates and forward-looking statements regarding our strategy and opportunities for future growth.

Institutional Presentation October 2016 Caixa para descrição. Disclaimer This presentation contains estimates and forward-looking statements regarding our strategy and opportunities for future growth.

LOG-IN LOGÍSTICA INTERMODAL S.A.

Rio de Janeiro, November 13, 2018 LOG-IN LOGÍSTICA INTERMODAL S.A. Content Financial and Operating Summary... 02 Consolidated Result... 02 Coastal Shipping... 05 Vila Velha Terminal (TVV)... 09 Intermodal

Rio de Janeiro, November 13, 2018 LOG-IN LOGÍSTICA INTERMODAL S.A. Content Financial and Operating Summary... 02 Consolidated Result... 02 Coastal Shipping... 05 Vila Velha Terminal (TVV)... 09 Intermodal

IFC S EXPERIENCE IN THE TRANSPORT SECTOR

APPENDIX D: IFC S EXPERIENCE IN THE TRANSPORT SECTOR The International Finance Corporation s (IFC s) IEG reviewed IFC s investments in the transport sector between 1990 and 2005. IEG found several things:

APPENDIX D: IFC S EXPERIENCE IN THE TRANSPORT SECTOR The International Finance Corporation s (IFC s) IEG reviewed IFC s investments in the transport sector between 1990 and 2005. IEG found several things:

Economic Stimulus Packages and Steel: A Summary

Economic Stimulus Packages and Steel: A Summary Steel Committee Meeting 8-9 June 2009 Sources of information on stimulus packages Questionnaire to Steel Committee members, full participants and observers

Economic Stimulus Packages and Steel: A Summary Steel Committee Meeting 8-9 June 2009 Sources of information on stimulus packages Questionnaire to Steel Committee members, full participants and observers

BRAZILIAN ECONOMIC OUTLOOK

BRAZILIAN ECONOMIC OUTLOOK BRAZILIAN ECONOMIC OUTLOOK Henrique Meirelles Henrique Meirelles February 8th, 2016 February 08th, 2016 INTRODUCTION 80 s Hyper inflation and volatility. 1994 Monetary stabilization

BRAZILIAN ECONOMIC OUTLOOK BRAZILIAN ECONOMIC OUTLOOK Henrique Meirelles Henrique Meirelles February 8th, 2016 February 08th, 2016 INTRODUCTION 80 s Hyper inflation and volatility. 1994 Monetary stabilization

M&A and Private Equity in Brazil An overview

www.pwc.com.br M&A and Private Equity in Brazil An overview Introduction Brazil has developed into the largest market for private equity in Latin America, accounting for more than Mexico and Argentina

www.pwc.com.br M&A and Private Equity in Brazil An overview Introduction Brazil has developed into the largest market for private equity in Latin America, accounting for more than Mexico and Argentina

Capital Account Management in Brazil

RETHINKING MACRO POLICY II: FIRST STEPS AND EARLY LESSONS APRIL 16 17, 2013 Capital Account Management in Brazil Marcio Holland Secretary of Economic Policy Ministry of Finance, Brazil Paper presented

RETHINKING MACRO POLICY II: FIRST STEPS AND EARLY LESSONS APRIL 16 17, 2013 Capital Account Management in Brazil Marcio Holland Secretary of Economic Policy Ministry of Finance, Brazil Paper presented

Japan's Balance of Payments for 2010 July 2011 International Department Bank of Japan

Japan's Balance of Payments for 21 July 211 International Department Bank of Japan This is an English translation of the Japanese original released on March 18, 211. Please contact below in advance to

Japan's Balance of Payments for 21 July 211 International Department Bank of Japan This is an English translation of the Japanese original released on March 18, 211. Please contact below in advance to

The Brazilian boom is it happening and what will it mean for copper industry growth in this newly industrializing economy?

The Brazilian boom is it happening and what will it mean for copper industry growth in this newly industrializing economy? Presented by Paranapanema S.A. Brazil Mario L. Lorencatto Table of Contents 1.

The Brazilian boom is it happening and what will it mean for copper industry growth in this newly industrializing economy? Presented by Paranapanema S.A. Brazil Mario L. Lorencatto Table of Contents 1.

Global Market Selection. John Senese. Global Reach 2008 Cleveland State University May 27, 2008

Global Market Selection Making the choices that are right for your Company John Senese Global Reach 2008 Cleveland State University May 27, 2008 World Population North America Population: 337M Europe Population:

Global Market Selection Making the choices that are right for your Company John Senese Global Reach 2008 Cleveland State University May 27, 2008 World Population North America Population: 337M Europe Population:

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS Summary Spain has significantly increased its trade openness in the last two decades Despite the global crisis and increased competition from

SPANISH EXTERNAL SECTOR AND COMPETITIVENESS: SOME HIGHLIGHTS Summary Spain has significantly increased its trade openness in the last two decades Despite the global crisis and increased competition from

Doing Business in Brazil: 2012 Country Commercial Guide for U.S. Companies

Doing Business in Brazil: 2012 Country Commercial Guide for U.S. Companies INTERNATIONAL COPYRIGHT, U.S. & FOREIGN COMMERCIAL SERVICE AND U.S. DEPARTMENT OF STATE, 2012. ALL RIGHTS RESERVED OUTSIDE OF

Doing Business in Brazil: 2012 Country Commercial Guide for U.S. Companies INTERNATIONAL COPYRIGHT, U.S. & FOREIGN COMMERCIAL SERVICE AND U.S. DEPARTMENT OF STATE, 2012. ALL RIGHTS RESERVED OUTSIDE OF

Two tales of development

Two tales of development BRAZIL-INDIA 17 Liliana Lavoratti, Rio de Janeiro India is still almost unknown to Brazilians in general. Given the distance not only geographically as well as quite different

Two tales of development BRAZIL-INDIA 17 Liliana Lavoratti, Rio de Janeiro India is still almost unknown to Brazilians in general. Given the distance not only geographically as well as quite different

Situation Analysis Macroeconomic situation and outlook for 2015 LATAM Mexico, Chile and Brazil. By Miguel Valdivieso

Situation Analysis Macroeconomic situation and outlook for 2015 LATAM Mexico, Chile and Brazil www.fitchbenne*partners.com - Execu6ve Search & Human Capital Current Situation Macroeconomic situation in

Situation Analysis Macroeconomic situation and outlook for 2015 LATAM Mexico, Chile and Brazil www.fitchbenne*partners.com - Execu6ve Search & Human Capital Current Situation Macroeconomic situation in

1Q12 Results Page 9 of 29 ALL RAIL OPERATIONS BUSINESS DESCRIPTION

Results Page 9 of 29 ALL RAIL OPERATIONS BUSINESS DESCRIPTION ALL Rail operations are composed of 6 rail concessions in Brazil and Argentina, totaling 21.3 thousand km of rail tracks, 1,095 locomotives

Results Page 9 of 29 ALL RAIL OPERATIONS BUSINESS DESCRIPTION ALL Rail operations are composed of 6 rail concessions in Brazil and Argentina, totaling 21.3 thousand km of rail tracks, 1,095 locomotives

OVERVIEW. Doing Business in Brazil Practical Business and Legal Considerations. Fabiano Gallo September, 2016

OVERVIEW Doing Business in Brazil Practical Business and Legal Considerations Fabiano Gallo September, 2016 Impeachment of President Dilma Roussef I m p e a c h m e n t of P r e s i d e n t D i l m a R

OVERVIEW Doing Business in Brazil Practical Business and Legal Considerations Fabiano Gallo September, 2016 Impeachment of President Dilma Roussef I m p e a c h m e n t of P r e s i d e n t D i l m a R

ISA s investments in Brazil January 30, 2017

ISA s investments in Brazil January 30, 2017 AGENDA 2 ISA s Corporate Strategy VISION In 2020, ISA s 2012 profits will be tripled, by capturing the most profitable growth opportunities in its existing

ISA s investments in Brazil January 30, 2017 AGENDA 2 ISA s Corporate Strategy VISION In 2020, ISA s 2012 profits will be tripled, by capturing the most profitable growth opportunities in its existing

Franchise Agreement - Latam

Franchise Agreement - Latam Brazilian Franchise Law and Disclosure Requirements Article 2 of the Brazilian Franchise Law (Law No. 8.955 of December 15, 1994) defines a commercial franchise as a system

Franchise Agreement - Latam Brazilian Franchise Law and Disclosure Requirements Article 2 of the Brazilian Franchise Law (Law No. 8.955 of December 15, 1994) defines a commercial franchise as a system

Peruvian mining: A competitive and attractive investment. ING. Victor Gobitz, CEO Buenaventura

Peruvian mining: A competitive and attractive investment ING. Victor Gobitz, CEO Buenaventura INDEX Megatrend I. Location (World Context) II. Natural Resources - Mining potential of Peru - Value and structure

Peruvian mining: A competitive and attractive investment ING. Victor Gobitz, CEO Buenaventura INDEX Megatrend I. Location (World Context) II. Natural Resources - Mining potential of Peru - Value and structure

U.S. Department of Commerce U.S. Commercial Service. Resources for U.S. Exporters. March 27, 2015

U.S. Department of Commerce U.S. Commercial Service Resources for U.S. Exporters March 27, 2015 Who Are We? Federal government agency created in 1980 Part of the U.S. Department of Commerce Mission: Promote

U.S. Department of Commerce U.S. Commercial Service Resources for U.S. Exporters March 27, 2015 Who Are We? Federal government agency created in 1980 Part of the U.S. Department of Commerce Mission: Promote

BRICs: actual growth and cooperation perspectives. International Advisory Council 3 rd Metting August 15, Luciano Coutinho President

BRICs: actual growth and cooperation perspectives International Advisory Council 3 rd Metting August 15, 2011 Luciano Coutinho President Emerging countries remain ahead in worldwide growth Annual Growth

BRICs: actual growth and cooperation perspectives International Advisory Council 3 rd Metting August 15, 2011 Luciano Coutinho President Emerging countries remain ahead in worldwide growth Annual Growth

As close as you need, as far as you go

As close as you need, as far as you go BBVA, a global group For more than 150 years our clients have been the centre of our business. Now as a highly solvent international financial group we offer clients

As close as you need, as far as you go BBVA, a global group For more than 150 years our clients have been the centre of our business. Now as a highly solvent international financial group we offer clients

Economic Performance. Lessons from the past and a guide for the future Björn Rúnar Guðmundson, Director

Economic Performance Lessons from the past and a guide for the future Björn Rúnar Guðmundson, Director Analysis of economic performance Capital and labour: The raw ingredients in economic development However,

Economic Performance Lessons from the past and a guide for the future Björn Rúnar Guðmundson, Director Analysis of economic performance Capital and labour: The raw ingredients in economic development However,

Interesting times for Brazil:

Interesting times for Brazil: Political and macro-economic developments and opportunities Jan Eichbaum Consul General of Luxembourg in Brazil Luxembourg, 3 rd October 2014 Jan Eichbaum Interesting times

Interesting times for Brazil: Political and macro-economic developments and opportunities Jan Eichbaum Consul General of Luxembourg in Brazil Luxembourg, 3 rd October 2014 Jan Eichbaum Interesting times

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Stronger growth, but risks loom large

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

VEDP QUARTERLY ECONOMIC UPDATE

VEDP QUARTERLY ECONOMIC UPDATE September 2016 VIRGINIA ECONOMIC DEVELOPMENT PARTNERSHIP YESVIRGINIA.ORG 1 US ECONOMIC OUTLOOK 1 8% - Source: Consensus Forecasts, September 2016 2 US WEEKLY INDICATORS 5%

VEDP QUARTERLY ECONOMIC UPDATE September 2016 VIRGINIA ECONOMIC DEVELOPMENT PARTNERSHIP YESVIRGINIA.ORG 1 US ECONOMIC OUTLOOK 1 8% - Source: Consensus Forecasts, September 2016 2 US WEEKLY INDICATORS 5%

Japan's Balance of Payments for August 2009 International Department Bank of Japan

Japan's Balance of Payments for 28 August 29 International Department Bank of Japan This is an English translation of the Japanese original released on March 24, 29 Balance of Payments 28 Please contact

Japan's Balance of Payments for 28 August 29 International Department Bank of Japan This is an English translation of the Japanese original released on March 24, 29 Balance of Payments 28 Please contact

Highlights of Ecuador A wrap-up of 2010 and a forecast for 2011

Highlights of Ecuador A wrap-up of 2010 and a forecast for 2011 1. Synopsis Ecuador s economic growth, as measured in terms of the variation in GDP went from 0.98% in 2009 to 3.3% in 2010, according to

Highlights of Ecuador A wrap-up of 2010 and a forecast for 2011 1. Synopsis Ecuador s economic growth, as measured in terms of the variation in GDP went from 0.98% in 2009 to 3.3% in 2010, according to

I. INTRODUCTION TO THE US ECONOMY

I. INTRODUCTION TO THE US ECONOMY The US has the largest and most technologically powerful economy in the world, with a per capita GDP of $49,800. In this market-oriented economy, private individuals and

I. INTRODUCTION TO THE US ECONOMY The US has the largest and most technologically powerful economy in the world, with a per capita GDP of $49,800. In this market-oriented economy, private individuals and

TBS International Limited. Jefferies 5 th Annual Shipping, Logistics & Offshore Services Conference Presentation September 17, 2008

TBS International Limited Jefferies 5 th Annual Shipping, Logistics & Offshore Services Conference Presentation September 17, 2008 Forward Looking Statements This presentation contains forward-looking

TBS International Limited Jefferies 5 th Annual Shipping, Logistics & Offshore Services Conference Presentation September 17, 2008 Forward Looking Statements This presentation contains forward-looking

Kentaro Tsuboi, Director General

JBIC Finance for Maritime Offshore Projects November 2012 Kentaro Tsuboi, Director General Marine and Aerospace Finance/Financial Products Department Industry Finance Group Agenda 1. JBIC Overview 2. JBIC

JBIC Finance for Maritime Offshore Projects November 2012 Kentaro Tsuboi, Director General Marine and Aerospace Finance/Financial Products Department Industry Finance Group Agenda 1. JBIC Overview 2. JBIC

International Economic Outlook

International Monetary Fund September 9, 16 International Economic Outlook Alejandro Werner Director Western Hemisphere Department 1 Global and Regional Developments Relevant Issues Global and Regional

International Monetary Fund September 9, 16 International Economic Outlook Alejandro Werner Director Western Hemisphere Department 1 Global and Regional Developments Relevant Issues Global and Regional