Global Financial Stability Report: Grappling with Crisis Legacies

|

|

|

- Allison Pope

- 5 years ago

- Views:

Transcription

1 Global Financial Stability Report: Grappling with Crisis Legacies Seminar for Senior Bank Supervisors from Emerging Economies Laura E. Kodres /International Monetary Fund October 17, 2011

2 Chapter 1 Overcoming Political Risks and Crisis Legacies

3 A Growing Crisis of Confidence Private debt Subprime crisis originates in US banks Banking Systemic banking crisis spreads from US to Europe Sovereign Problems in euro periphery sov. debt Medium-term debt burdens in core AE Political Difficulty in reaching political consensus on fiscal consolidation and adjustment 2

4 Stability risks have risen across all risk metrics Risks Emerging market risks Credit risks April 2009 GFSR April 2011 GFSR September 2011 GFSR Macroeconomic risks Market and liquidity risks Away from center signifies higher risks, easier monetary and financial conditions, or higher risk appetite. Monetary and financial Conditions Risk appetite 3

5 Italian Greek WE sovereign Spanish Irish Greek Italian French Spanish US Oil Commodities Vix Eurofirst 300 EM Equities S&P 500 Swiss franc 10-year bund 10-year treasury Gold prompting a flight to safe assets Asset Price Performance since April GFSR (percent, VIX in percentage points; VIX and sovereign CDS inverted) 20 Sovereign CDS Bank equities Commodities Risk assets Safe-haven assets

6 What s different from Lehman? Interbank funding stress is less, while Libor OIS Spreads (bps) Lehman Current Euro area United States partly due to sovereign strains Sovereign CDS Spreads (bps) Euro area United States risk perceptions are greater for European banks Bank CDS Spreads (bps) Euro area United States with stress rising on broad markets Broad Equity Markets (indices, 9/15/08 = 100) Euro area U.S. Volatility index index index 5

7 Sovereign strains becoming more widespread Greece Ireland 500 Portugal 0 Jan-11 Apr-11 Jul-11 Credit Default Swap Spreads (basis points) Spain Jan-11 Apr-11 Jul-11 Italy Belgium France 140 United Kingdom United States 20 Germany 0 Jan-11 Apr-11 Jul-11 6

8 ... threatening a shift towards a bad equilibrium Bad Equilibrium Inadequate Policy Response Increased Volatility Weaker Investor Base Shock to Debt Dynamics for Vulnerable Sovereign Reduced Volatility Good Equilibrium Adequate Policy Response Stronger Investor Base Higher Spreads Weaker Growth Worse Debt Dynamics Lower Spreads Stronger Growth Better Debt Dynamics 7

9 Euro area risk-free debt has shrunk by half Sovereign CDS spreads Spreads as of April 2010 (end-2009 debt) Spreads as of August 2011 (end-2010 debt) Over 200 bps Under 200 bps Netherlands 5% Greece 5% Ireland 2% Portugal 2% Netherlands 5% Greece 4% Ireland 1% Portugal 2% Germany 22% Spain 9% Germany 24% Spain 9% Finland 1% Austria 3% France 21% Belgium 5% Italy 26% Finland 1% Austria 3% France 20% Belgium 5% Italy 25% 8

10 Euro area sovereign risks have spilled over to the EU banking system... Cumulative Spillovers from High-Spread Euro Area Sovereigns to the European Banking System ( bn) Spillovers from... Greek sovereign Irish & Portuguese sovereign Belgian, Spanish & Italian sovereign High-spread euro area banking sector 9

11 but the impact has varied greatly by country Spillovers from High-Spread Euro Area Sovereigns to Country Banking Systems (percent of assets) Greece Cyprus Portugal Italy Spain Belgium Ireland Luxembourg France Germany Slovenia Netherlands Austria United Kingdom Malta Denmark Sweden Finland Poland Hungary Sovereigns Banks

12 Core Tier 1 Ratio and some banks are under substantial pressure Distribution of Spillovers from High-Spread Euro Area to European Banks High-spread euro area Other Europe Spillover greater than... (percent of capital) 9 percent of all banks 7 percent of total assets 7 percent of all banks 4 percent of total assets 50 percent 75 percent 100 percent percent of all banks 1 percent of total assets Spillover (in percent of risk-weighted assets) 11

13 Sovereign Stress Has Spilled Over to Bank Equity 13

14 But Capital Buffers Do Matter! 14

15 Impact of Economic Slowdown and Sovereign Stress European Bank Equities (7/1/2011=100) for Bank Equities Germany June IP UK 95 lower than expected 300 France Germany Spain Italy Greece GIIPS Sov Spreads Spanish PMI fell in July fell while Italian increased German Q2 GDP came in significantly lower

16 Euro Area Banks Vulnerable to Wholesale Funding Pressures Euro Area Banks Liability Profile (% of total Liabilities) 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% IE FR GR AT IT PT BE DE ES FI NL Capital Other Liabs Other Deposits LT Debt Short-Term Liabs 16

17 Jan-08 May-08 Aug-08 Nov-08 Feb-09 May-09 Aug-09 Nov-09 Feb-10 May-10 Aug-10 Nov-10 Feb-11 May-11 Aug-11 Nov-11 Feb-12 May-12 Real Economy Impact From Deleveraging? Bank Credit to the Nonfinancial Private Sector Under a Deleveraging Scenario (In percent year-on-year) Belgium Greece Ireland Italy Portugal Spain 17

18 EU Banks Capital: Current Situation European Bank Core Tier 1 Ratios (percent of risk-weighted assets) 63% of banks 70% of total assets Individual Banks 18% of banks 19% of total assets 0% of banks 0% of total assets 10% 8% 6% 18

19 Advanced economies are stuck between repair and expansion phase of the credit cycle Phases of the Credit Cycle REPAIR RECOVERY Households Banking sector Valuation Asset quality Credit conditions Corporate fundamentals DOWNTURN EXPANSION 18

20 U.S. Household Balance Sheets and Housing Still Weak U.S. Housing Inventories and Foreclosures (millions of units) Delinquencies and Foreclosures Underwater Mortgages 1/ Actual Inventories Q

21 Low policy rates encourage a search for yield : mispricing credit? Fed Funds Rates, BBB-rated Corporate Credit Spreads, and U.S. Real GDP Cumulative Growth U.S. Fed Funds Rates (percent) Past Current Past cycles U.S. BBB-rated Corporate Spreads (100 = beginning of each cycle) Past Current Current cycles U.S. Real GDP Cumulative Growth (100 = beginning of each cycle) Past Current

22 Emerging economies are further along in the credit cycle Phases of the Credit Cycle REPAIR Latam RECOVERY Households Banking sector Valuation Asset quality Credit conditions Corporate fundamentals DOWNTURN EXPANSION 21

23 Emerging markets are in the expansion phase (standard deviations from mean, z-scores) Total Credit 1/ (RHS) Real equity prices Portfolio Flows / In percent of GDP 22

24 Credit growth Rapid Credit Growth Can Lead to Rising Nonperforming Loans in EMs 0 Credit and GDP Growth (cumulative percent change; ) Turkey Brazil Poland Colombia Peru Morocco Mexico Russia Hungary Philippines Malaysia Thailand South Africa Chile India China Argentina Indonesia Nominal GDP growth Predicted NPL Ratios in 2011 and 2012 (percent, no shock) 2010 (Actual) Emerging Asia EMEA Latin America 24

0-1 -2-3 Latin America EMEA Emerging Asia -4-5 2011 2012")

25 An external shock would test the resilience of emerging market banks 1 Absolute Change in Capital Adequacy Ratios Under Combined Macro Shocks (percentage points) Latin America EMEA Emerging Asia

26 Consequences of the Political Phase of the Crisis Economically Viable Feasible Set is Shrinking Over Time Economically Viable Politically Feasible Politically Feasible 26

27 New, dangerous, political, phase of the crisis The risks to global financial stability and growth have increased. With limited room to deploy further monetary and fiscal stimulus, easy policy responses have been largely exhausted. Policymakers face hard choices, but markets confidence in their ability to resolve problems has weakened. The need is now for coordinated, timely, bold, action. 26

28 Advanced Economies avoid near-term crisis Sovereign risks Public (US, EU, Japan) medium-term credible fiscal consolidation Balance sheet repair Private (Households, US) mortgage debt - banks Banks Banks (EU) more capital (private, public, EFSF) funding structures Complete financial reform agenda 27

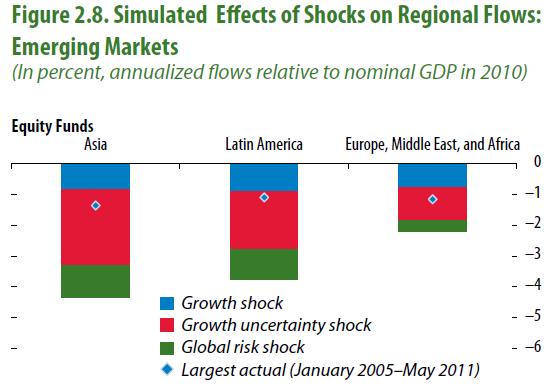

29 Emerging Economies avoid future crisis Contain buildup of macrofinancial vulnerabilities macro (monetary, fiscal) macro-prudential and CFM Enhance macro-financial resilience to cope with external shocks structural financial reform 28

30 Chapter 2 Long-Term Investors and Their Asset Allocation: Where Are They Now?

31 Focus of chapter: Institutional investors Real-money investors, unleveraged, long-term horizon. Mainly pension funds and insurance companies. $70 trillion in assets; mostly equities and bonds (> 80 percent) 31

32

33 We use detailed data on mutual fund flows into equity and bond funds by destination country to run regressions Complementary data also from IMF Survey on Global Asset Allocation 33

34 Asset allocation driven by (i) Growth prospects (ii) Country risk (iii)macroeconomic stability (inflation, exchange rates) (iv)global risk NOT driven by (i) Interest rate differentials BUT the latter may still matter for leveraged investors 34

35 Asset allocation behavior affected by (i) Crisis Greater risk consciousness: liquidity, credit risks (including sovereign) Can be seen in data: break in regressions (ii) Low-interest-rate environment Pension funds, insurance co s are hurting Pressure to increase yields, but biding time; interest rate differentials may matter in future (iii)regulation Aims to make financial institutions safer, but shifts them away from longer-term risky assets 35

36

37 Emerging market flows are resumption/ acceleration from trend before the crisis In line with empirical results: flows respond to good growth prospects and lower country risk But risk of reversal; seen in August, mostly as a result of increased global risk; in line with our simulations 37

38 38

39 Sovereign asset management becoming more important: SWFs $4.7 trillion International reserves $10 trillion, in some cases more than necessary: some reserve managers are establishing investment tranche 39

40 40

41 Chapter 3 Towards Operationalizing Macroprudential Policies: When to Act? 41

42 Road Map Good shocks: healthy fluctuations Bad shocks: rise in systemic risks Dampen effects of bad shocks. Structural analysis: Macroeconomicfinancial model Econometric analysis: Slow-moving indicators Fast-moving indicators Operationalize macroprudential tools Identify systemic risk Distinguish healthy fluctuations from rise in systemic risk Determine robust systemic risk indicators

43 Deviations of credit-to-gdp ratio from baseline Credit Growth: Rapid in many scenarios Ratio of Credit to GDP (In percentage points) Bad Shock: Asset Bubble Good Shock: Healthy Productivity Increases Quarters

44 Banking Soundness Indicators Differentiate

45 Event Study: 3 years before to 2 years after financial crisis Contd

46 Event Study: 3 years before to 2 years after financial crisis

47 Sounding the alarm: policymakers preferences? Noise-to-Signal Ratios for Different Credit Indicators

48 Sounding the alarm: Other indicators? Receiver Operating Characteristics for other indicators

49 Credit and Asset Prices: Powerful together Crisis probability >5 pp 20-25% >15%

50 Short-term alarm for imminent crisis Comparison of various market-price based near-coincident indicators for the U.S.

51 Indicators and policies A stitch in time

52 Policies costly if source of shocks mistaken (ex: Squashing healthy growth with time-varying capital requirements)

53 Practical Guidelines Know sources of shocks Credit growth central, but cannot be used to distinguish good from bad shocks Combine credit growth with other indicators: asset prices, foreign liabilities, direct cross-border lending to private sector Thresholds reflect policymakers preferences Near-coincident indicators: LIBOR-OIS and yield curve Policies universal in use, country-specific in design Case for coordination among policy makers especially: To understand the source of shocks In managed exchange rate regimes with fx-denominated loans (the effects of any shock get amplified). 53

54 International Monetary Fund October 17, 2011 GFSR Challenges to Global Financial Stability

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

International Monetary Fund

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

Global Economic Outlook

Global Economic Outlook The Institute of Strategic and International Studies Kuala Lumpur, November 2012 Mangal Goswami Mangal Goswami Deputy Director IMF Singapore Regional Training Institute Action Needed

Global Economic Outlook The Institute of Strategic and International Studies Kuala Lumpur, November 2012 Mangal Goswami Mangal Goswami Deputy Director IMF Singapore Regional Training Institute Action Needed

Mexico: 2016 IMF ARTICLE IV CONSULTATION

Mexico: 2016 IMF ARTICLE IV CONSULTATION Wilson Center, January 9, 2017 Western Hemisphere Department International Monetary Fund BACKGROUND Growth in Economic Activity and Employment Have Remained Stable

Mexico: 2016 IMF ARTICLE IV CONSULTATION Wilson Center, January 9, 2017 Western Hemisphere Department International Monetary Fund BACKGROUND Growth in Economic Activity and Employment Have Remained Stable

ECB LTRO Dec Greece program

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016

17 March 2016 ECB-PUBLIC Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016 Introduction In accordance with its mandate, the European Insurance

17 March 2016 ECB-PUBLIC Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016 Introduction In accordance with its mandate, the European Insurance

PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

How to measure country risk?

How to measure country risk? Produced by: Cross-country Emerging Markets Unit For the Occasion of: Second BBVA Resarch Emerging Market Seminar Madrid, July 13, 211 Road map to the presentation 1. Previous

How to measure country risk? Produced by: Cross-country Emerging Markets Unit For the Occasion of: Second BBVA Resarch Emerging Market Seminar Madrid, July 13, 211 Road map to the presentation 1. Previous

CENTRAL BANK OF THE REPUBLIC OF TURKEY

CENTRAL BANK OF THE REPUBLIC OF TURKEY Growth and Financial System Durmuş YILMAZ Governor February, 211 1 Presentation Outline I. Recent Developments in the Turkish Economy II. III. Monetary Policy Policy

CENTRAL BANK OF THE REPUBLIC OF TURKEY Growth and Financial System Durmuş YILMAZ Governor February, 211 1 Presentation Outline I. Recent Developments in the Turkish Economy II. III. Monetary Policy Policy

Challenges and Opportunities in Recent Financial Market Developments

Challenges and Opportunities in Recent Financial Market Developments Mario Marcel Central Bank of Chile OMFIF 2018 Global Public Investor Conference, May 23, 2018 London International context Economic

Challenges and Opportunities in Recent Financial Market Developments Mario Marcel Central Bank of Chile OMFIF 2018 Global Public Investor Conference, May 23, 2018 London International context Economic

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Macroeconomic overview SEE and Macedonia

Macroeconomic overview SEE and Macedonia Zoltan Arokszallasi Chief Analyst, Macro & FX/FI Research Erste Group Bank Erste Investors Breakfast, 29 September, Skopje 02. Oktober SEE shows mixed performance

Macroeconomic overview SEE and Macedonia Zoltan Arokszallasi Chief Analyst, Macro & FX/FI Research Erste Group Bank Erste Investors Breakfast, 29 September, Skopje 02. Oktober SEE shows mixed performance

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

International Monetary Fund. World Economic Outlook. Jörg Decressin Senior Advisor Research Department, IMF

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES. Bank of Russia.

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

Capital Flows, Cross-Border Banking and Global Liquidity. May 2012

Capital Flows, Cross-Border Banking and Global Liquidity Valentina Bruno Hyun Song Shin May 2012 Bruno and Shin: Capital Flows, Cross-Border Banking and Global Liquidity 1 Gross Capital Flows Capital flows

Capital Flows, Cross-Border Banking and Global Liquidity Valentina Bruno Hyun Song Shin May 2012 Bruno and Shin: Capital Flows, Cross-Border Banking and Global Liquidity 1 Gross Capital Flows Capital flows

International Monetary Fund Global Financial Stability Outlook

International Monetary Fund Global Financial Stability Outlook Fabio Natalucci Deputy Director Monetary and Capital Markets Department 1 Financial Stability Risks Could Rise Sharply Since the April 218

International Monetary Fund Global Financial Stability Outlook Fabio Natalucci Deputy Director Monetary and Capital Markets Department 1 Financial Stability Risks Could Rise Sharply Since the April 218

Adverse macro-financial scenario for the 2018 EU-wide banking sector stress test

16 January 2018 ECB-PUBLIC Adverse macro-financial scenario for the 2018 EU-wide banking sector stress test This document sets out the adverse macro-financial scenario that banks are required to use in

16 January 2018 ECB-PUBLIC Adverse macro-financial scenario for the 2018 EU-wide banking sector stress test This document sets out the adverse macro-financial scenario that banks are required to use in

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates Takatoshi Kato Deputy Managing Director International Monetary Fund September 3, 27 1 9 Growth has been

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates Takatoshi Kato Deputy Managing Director International Monetary Fund September 3, 27 1 9 Growth has been

Chart pack to council for cooperation on macroprudential policy

Chart pack to council for cooperation on macroprudential policy Contents List of charts... 3 Macro and macro-financial setting... 5 Swedish macroeconomic setting... 5 Foreign macroeconomic setting... Macro-financial

Chart pack to council for cooperation on macroprudential policy Contents List of charts... 3 Macro and macro-financial setting... 5 Swedish macroeconomic setting... 5 Foreign macroeconomic setting... Macro-financial

Some Historical Examples of Yield Curves

3 months 6 months 1 year 2 years 5 years 10 years 30 years Some Historical Examples of Yield Curves Nominal interest rate, % 16 14 12 10 8 6 4 2 January 1981 June1999 December2009 0 Time to maturity This

3 months 6 months 1 year 2 years 5 years 10 years 30 years Some Historical Examples of Yield Curves Nominal interest rate, % 16 14 12 10 8 6 4 2 January 1981 June1999 December2009 0 Time to maturity This

Quarterly Investment Update First Quarter 2017

Quarterly Investment Update First Quarter 2017 Market Update: A Quarter in Review March 31, 2017 CANADIAN STOCKS INTERNATIONAL STOCKS Large Cap Small Cap Growth Value Large Cap Small Cap Growth Value Emerging

Quarterly Investment Update First Quarter 2017 Market Update: A Quarter in Review March 31, 2017 CANADIAN STOCKS INTERNATIONAL STOCKS Large Cap Small Cap Growth Value Large Cap Small Cap Growth Value Emerging

RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO OCTOBER 2003

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY. Villa d'este, Cernobbio - September 7, 8 and 9, 2012

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY Villa d'este, Cernobbio - September 7, 8 and 9, 1 Working paper, September 1. Kindly authorized by the Author.

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY Villa d'este, Cernobbio - September 7, 8 and 9, 1 Working paper, September 1. Kindly authorized by the Author.

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Falling Short of Expectations? Stress-Testing the European Banking System

Falling Short of Expectations? Stress-Testing the European Banking System Viral V. Acharya (NYU Stern, CEPR and NBER) and Sascha Steffen (ESMT) January 2014 1 Falling Short of Expectations? Stress-Testing

Falling Short of Expectations? Stress-Testing the European Banking System Viral V. Acharya (NYU Stern, CEPR and NBER) and Sascha Steffen (ESMT) January 2014 1 Falling Short of Expectations? Stress-Testing

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving. Alen Kovac, Chief Economist EBC May 2016 Ljubljana

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving Alen Kovac, Chief Economist EBC May 216 Ljubljana Real economy highlights Recent GDP track record reveals more favorable footprint

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving Alen Kovac, Chief Economist EBC May 216 Ljubljana Real economy highlights Recent GDP track record reveals more favorable footprint

Developing Housing Finance Systems

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

ECONOMIC AND MONETARY DEVELOPMENTS

Box 2 RECENT WIDENING IN EURO AREA SOVEREIGN BOND YIELD SPREADS This box looks at recent in euro area countries sovereign bond yield spreads and the potential roles played by credit and liquidity risk.

Box 2 RECENT WIDENING IN EURO AREA SOVEREIGN BOND YIELD SPREADS This box looks at recent in euro area countries sovereign bond yield spreads and the potential roles played by credit and liquidity risk.

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for August 2011 All data are as of Wednesday, August 31, 2011. The regional indices are

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for August 2011 All data are as of Wednesday, August 31, 2011. The regional indices are

Recent Recent Developments 0

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

GLOBAL MARKET OUTLOOK

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

World Economic Outlook Central Europe and Baltic Countries

World Economic Outlook Central Europe and Baltic Countries Presentation by Susan Schadler and Christoph Rosenberg September 5 World growth returns to trend. (World real GDP growth, annual percent change)

World Economic Outlook Central Europe and Baltic Countries Presentation by Susan Schadler and Christoph Rosenberg September 5 World growth returns to trend. (World real GDP growth, annual percent change)

August 2008 Euro area external trade deficit 9.3 bn euro 27.2 bn euro deficit for EU27

STAT/08/143 17 October 2008 August 2008 Euro area external trade deficit 9.3 27.2 deficit for EU27 The first estimate for the euro area 1 (EA15) trade balance with the rest of the world in August 2008

STAT/08/143 17 October 2008 August 2008 Euro area external trade deficit 9.3 27.2 deficit for EU27 The first estimate for the euro area 1 (EA15) trade balance with the rest of the world in August 2008

Kryzys fiskalny w Europie Strategie wyjścia. Mark Allen stały y przedstawiciel MFW na Europę Centralną i Wschodnią. 110 seminarium 2010

Kryzys fiskalny w Europie Strategie wyjścia Mark Allen stały y przedstawiciel MFW na Europę Centralną i Wschodnią 110 seminarium BRE-CASE Warszaw awa, 30 września 2010 1 Presentation based on: Fiscal Space

Kryzys fiskalny w Europie Strategie wyjścia Mark Allen stały y przedstawiciel MFW na Europę Centralną i Wschodnią 110 seminarium BRE-CASE Warszaw awa, 30 września 2010 1 Presentation based on: Fiscal Space

Report on financial stability

Report on financial stability Márton Nagy MNB Club 26 April 212 Key risks Deteriorating lending capacity stemming particularly from liquidity side raises the risk of a credit crunch, mainly in the corporate

Report on financial stability Márton Nagy MNB Club 26 April 212 Key risks Deteriorating lending capacity stemming particularly from liquidity side raises the risk of a credit crunch, mainly in the corporate

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

May 2009 Euro area external trade surplus 1.9 bn euro 6.8 bn euro deficit for EU27

STAT/09/106 17 July 2009 May 2009 Euro area external trade surplus 1.9 6.8 deficit for EU27 The first estimate for the euro area 1 (EA16) trade balance with the rest of the world in May 2009 gave a 1.9

STAT/09/106 17 July 2009 May 2009 Euro area external trade surplus 1.9 6.8 deficit for EU27 The first estimate for the euro area 1 (EA16) trade balance with the rest of the world in May 2009 gave a 1.9

Emerging Market Debt attractive yield with solid fundamentals

For professional use only Not for Public distribution Emerging Market Debt attractive yield with solid fundamentals November 2012 Kevin Daly, Senior Portfolio Manager EMD Aberdeen Asset Management Table

For professional use only Not for Public distribution Emerging Market Debt attractive yield with solid fundamentals November 2012 Kevin Daly, Senior Portfolio Manager EMD Aberdeen Asset Management Table

The Cyprus Economy: from Recovery to Sustainable Growth. Vincenzo Guzzo Resident Representative in Cyprus

The Economy: from Recovery to Sustainable Growth Vincenzo Guzzo Resident Representative in Growth momentum remains strong 18 : Real GDP ( billion) 1 Deviation from Pre-Crisis Level and Trend (Percent)

The Economy: from Recovery to Sustainable Growth Vincenzo Guzzo Resident Representative in Growth momentum remains strong 18 : Real GDP ( billion) 1 Deviation from Pre-Crisis Level and Trend (Percent)

Adverse scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2018

9 April 218 ECB-PUBLIC Adverse scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 218 Introduction In accordance with its mandate, the European Insurance

9 April 218 ECB-PUBLIC Adverse scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 218 Introduction In accordance with its mandate, the European Insurance

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Latin America Sovereign Ratings in a Weakening Global Economy Shelly Shetty, Head of Latin America Sovereigns

Latin America Sovereign Ratings in a Weakening Global Economy Shelly Shetty, Head of Latin America Sovereigns October 11, 211 Agenda Latin America Sovereigns: Ratings Trajectory In A Weakening Global Environment

Latin America Sovereign Ratings in a Weakening Global Economy Shelly Shetty, Head of Latin America Sovereigns October 11, 211 Agenda Latin America Sovereigns: Ratings Trajectory In A Weakening Global Environment

GUIDANCE FOR CALCULATION OF LOSSES DUE TO APPLICATION OF MARKET RISK PARAMETERS AND SOVEREIGN HAIRCUTS

Annex 4 18 March 2011 GUIDANCE FOR CALCULATION OF LOSSES DUE TO APPLICATION OF MARKET RISK PARAMETERS AND SOVEREIGN HAIRCUTS This annex introduces the reference risk parameters for the market risk component

Annex 4 18 March 2011 GUIDANCE FOR CALCULATION OF LOSSES DUE TO APPLICATION OF MARKET RISK PARAMETERS AND SOVEREIGN HAIRCUTS This annex introduces the reference risk parameters for the market risk component

Global Outlook and Policy Challenges. Olivier Blanchard Economic Counsellor Research Department

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

2017 Asia and Pacific Regional Economic Outlook:

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager. November 2015

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager November 2015 Agenda Macro update & government bonds Emerging market corporate bonds Fund positioning Emerging markets risks today Risks Slowing

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager November 2015 Agenda Macro update & government bonds Emerging market corporate bonds Fund positioning Emerging markets risks today Risks Slowing

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

Summary. Economic Update 1 / 7 May Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018.

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle. Angel Gavilan, Martin Hillebrand December 2017

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle Angel Gavilan, Martin Hillebrand December 217 The last boom in capital flows was largely a global phenomenon Sum of current account

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle Angel Gavilan, Martin Hillebrand December 217 The last boom in capital flows was largely a global phenomenon Sum of current account

Cosa ci riserva il 2008?

Cosa ci riserva il 28? Scenari e previsioni per l anno in corso Keith Wade Capo Economista The US economy today A re-assessment of risk De-leveraging Financial sector Real economy Historical precedents

Cosa ci riserva il 28? Scenari e previsioni per l anno in corso Keith Wade Capo Economista The US economy today A re-assessment of risk De-leveraging Financial sector Real economy Historical precedents

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 12, 2014 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 12, 2014 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

Economic Trends and Challenges

Economic Trends and Challenges in Central and Eastern Europe Christoph Rosenberg International Monetary Fund Warsaw Regional Office April 2007 Note: These are the author s s own views, not necessarily

Economic Trends and Challenges in Central and Eastern Europe Christoph Rosenberg International Monetary Fund Warsaw Regional Office April 2007 Note: These are the author s s own views, not necessarily

Financial Stability Review November Press Briefing Luis de Guindos 29 November 2018

Financial Stability Review November 218 Press Briefing Luis de Guindos 29 November 218 Risk assessment The financial stability environment has become more challenging Four key risks over a two-year horizon

Financial Stability Review November 218 Press Briefing Luis de Guindos 29 November 218 Risk assessment The financial stability environment has become more challenging Four key risks over a two-year horizon

Confronting the Global Crisis in Latin America: What is the Outlook? Coordinators

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

January 2009 Euro area external trade deficit 10.5 bn euro 26.3 bn euro deficit for EU27

STAT/09/40 23 March 2009 January 2009 Euro area external trade deficit 10.5 26.3 deficit for EU27 The first estimate for the euro area 1 (EA16) trade balance with the rest of the world in January 2009

STAT/09/40 23 March 2009 January 2009 Euro area external trade deficit 10.5 26.3 deficit for EU27 The first estimate for the euro area 1 (EA16) trade balance with the rest of the world in January 2009

Global Macro Outlook Subdued Growth, Tail Risks Diminishing ANNE VAN PRAAGH, MANAGING DIRECTOR, SOVEREIGN RATINGS

Global Macro Outlook 2014-15 Subdued Growth, Tail Risks Diminishing ANNE VAN PRAAGH, MANAGING DIRECTOR, SOVEREIGN RATINGS OCTOBER, 2014 Agenda 1. Economic Strength: o Global Growth Lower, But EMs Approaching

Global Macro Outlook 2014-15 Subdued Growth, Tail Risks Diminishing ANNE VAN PRAAGH, MANAGING DIRECTOR, SOVEREIGN RATINGS OCTOBER, 2014 Agenda 1. Economic Strength: o Global Growth Lower, But EMs Approaching

August 2012 Euro area international trade in goods surplus of 6.6 bn euro 12.6 bn euro deficit for EU27

146/2012-16 October 2012 August 2012 Euro area international trade in goods surplus of 6.6 12.6 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the

146/2012-16 October 2012 August 2012 Euro area international trade in goods surplus of 6.6 12.6 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Balanced Plus Select Portfolio Pn

Factsheet as at : August 25, 2018 Balanced Plus Select Portfolio Pn Fund objective This portfolio aims to provide long-term capital growth while keeping risk in a target volatility range of 10-12% over

Factsheet as at : August 25, 2018 Balanced Plus Select Portfolio Pn Fund objective This portfolio aims to provide long-term capital growth while keeping risk in a target volatility range of 10-12% over

Unlocking Global Growth. Min Zhu International Monetary Fund

Unlocking Global Growth Min Zhu International Monetary Fund 1 Outline I. Cyclical recovery slow II. Real and financial sectors diverging III. Macro policy space limited IV. Global structural changes emerge

Unlocking Global Growth Min Zhu International Monetary Fund 1 Outline I. Cyclical recovery slow II. Real and financial sectors diverging III. Macro policy space limited IV. Global structural changes emerge

What is driving US Treasury yields higher?

What is driving Treasury yields higher? " our programme for reducing our [Fed's] balance sheet, which began in October, is proceeding smoothly. Barring a very significant and unexpected weakening in the

What is driving Treasury yields higher? " our programme for reducing our [Fed's] balance sheet, which began in October, is proceeding smoothly. Barring a very significant and unexpected weakening in the

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico 1 Current situation Eurozone (im)balances: a Small World Rising imbalances since the creation of the euro Eurozone current

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico 1 Current situation Eurozone (im)balances: a Small World Rising imbalances since the creation of the euro Eurozone current

Federal Reserve System/IMF/World Bank. Seminar for Senior Bank Supervisors October 19 30, David S. Hoelscher

Federal Reserve System/IMF/World Bank Seminar for Senior Bank Supervisors October 19 30, 2009 David S. Hoelscher Money and Capital Markets Department International Monetary Fund Typology of Crises Type

Federal Reserve System/IMF/World Bank Seminar for Senior Bank Supervisors October 19 30, 2009 David S. Hoelscher Money and Capital Markets Department International Monetary Fund Typology of Crises Type

UPDATE ON FISCAL STIMULUS AND FINANCIAL SECTOR MEASURES. April 26, 2009

UPDATE ON FISCAL STIMULUS AND FINANCIAL SECTOR MEASURES April 26, 2009 This note provides an update of information in the paper, The State of Public Finances: Outlook and Medium-Term Policies After the

UPDATE ON FISCAL STIMULUS AND FINANCIAL SECTOR MEASURES April 26, 2009 This note provides an update of information in the paper, The State of Public Finances: Outlook and Medium-Term Policies After the

MONTHLY BANKING MONITOR

TURKEY MONTHLY BANKING MONITOR NOVEMBER DECEMBER 7TH Global Developments Financial stress for EM rose in November, due to US elections and increase in the probability of a Fed rate hike in December BBVA

TURKEY MONTHLY BANKING MONITOR NOVEMBER DECEMBER 7TH Global Developments Financial stress for EM rose in November, due to US elections and increase in the probability of a Fed rate hike in December BBVA

Schwerpunkt Außenwirtschaft 2016/17 Austrian economic activity, Austria's price competitiveness and a summary on external trade

Schwerpunkt Außenwirtschaft /7 Austrian economic activity, Austria's price competitiveness and a summary on external trade Christian Ragacs, Klaus Vondra Abteilung für volkswirtschaftliche Analysen, OeNB

Schwerpunkt Außenwirtschaft /7 Austrian economic activity, Austria's price competitiveness and a summary on external trade Christian Ragacs, Klaus Vondra Abteilung für volkswirtschaftliche Analysen, OeNB

PORTUGUESE BANKING SECTOR OVERVIEW

PORTUGUESE BANKING SECTOR OVERVIEW AGENDA I. Importance of the banking sector for the economy II. III. Credit activity Funding IV. Solvency V. State guarantee and recapitalisation schemes for credit institutions

PORTUGUESE BANKING SECTOR OVERVIEW AGENDA I. Importance of the banking sector for the economy II. III. Credit activity Funding IV. Solvency V. State guarantee and recapitalisation schemes for credit institutions

Spillovers from Dollar Appreciation

June 6-7, 216 International Monetary Fund Spillovers from Dollar Appreciation Florence Jaumotte (with J. Chow, S.G. Park, and S. Zhang) Motivation Context: appreciation of US Dollar changing growth differentials,

June 6-7, 216 International Monetary Fund Spillovers from Dollar Appreciation Florence Jaumotte (with J. Chow, S.G. Park, and S. Zhang) Motivation Context: appreciation of US Dollar changing growth differentials,

May 2012 Euro area international trade in goods surplus of 6.9 bn euro 3.8 bn euro deficit for EU27

108/2012-16 July 2012 May 2012 Euro area international trade in goods surplus of 6.9 3.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

108/2012-16 July 2012 May 2012 Euro area international trade in goods surplus of 6.9 3.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

ECONOMIC OUTLOOK. World Economy Autumn No. 33 (2017 Q3) KIEL INSTITUTE NO. 33 (2017 Q3)

KIEL INSTITUTE NO. 33 (2017 Q3)") KIEL INSTITUTE ECONOMIC OUTLOOK World Economy Autumn 7 Finalized September 6, 7 No. 33 (7 Q3) Klaus-Jürgen Gern, Philipp Hauber, Stefan Kooths, Galina Potjagailo, and Ulrich Stolzenburg Forecasting Center

KIEL INSTITUTE ECONOMIC OUTLOOK World Economy Autumn 7 Finalized September 6, 7 No. 33 (7 Q3) Klaus-Jürgen Gern, Philipp Hauber, Stefan Kooths, Galina Potjagailo, and Ulrich Stolzenburg Forecasting Center

First estimate for 2011 Euro area external trade deficit 7.7 bn euro bn euro deficit for EU27

27/2012-15 February 2012 First estimate for 2011 Euro area external trade deficit 7.7 152.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

27/2012-15 February 2012 First estimate for 2011 Euro area external trade deficit 7.7 152.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

Economic recovery and employment in the EU. Raymond Torres, Director, ILO Research Department

Economic recovery and employment in the EU Raymond Torres, Director, ILO Research Department Outline of presentation I. Situation in the EU versus Japan and the US II. Role of macroeconomic policies and

Economic recovery and employment in the EU Raymond Torres, Director, ILO Research Department Outline of presentation I. Situation in the EU versus Japan and the US II. Role of macroeconomic policies and

Determinants of intra-euro area government bond spreads during the financial crisis

Determinants of intra-euro area government bond spreads during the financial crisis by Salvador Barrios, Per Iversen, Magdalena Lewandowska, Ralph Setzer DG ECFIN, European Commission - This paper does

Determinants of intra-euro area government bond spreads during the financial crisis by Salvador Barrios, Per Iversen, Magdalena Lewandowska, Ralph Setzer DG ECFIN, European Commission - This paper does

The Macro-Economic Outlook and the Challenges for the World

The Macro-Economic Outlook and the Challenges for the World Invest Save and Impact Seminar Singapore February 27, 2013 Brian Fabbri President Fabbri Global Economics Visiting Research Fellow, CAMRI, NUS

The Macro-Economic Outlook and the Challenges for the World Invest Save and Impact Seminar Singapore February 27, 2013 Brian Fabbri President Fabbri Global Economics Visiting Research Fellow, CAMRI, NUS

World Economic Outlook

World Economic Outlook Marco E. Terrones Assistant to the Director Research Department, IMF May 2012 The views expressed in this presentation are those of the author and do not necessarily represent those

World Economic Outlook Marco E. Terrones Assistant to the Director Research Department, IMF May 2012 The views expressed in this presentation are those of the author and do not necessarily represent those

Global Economic Prospects: Spillovers amid Weak Growth. Select Publications from DECPG

// Global Economic Prospects: Spillovers amid Weak Growth February M. Ayhan Kose Disclaimer! The views presented here are those of the authors and do NOT necessarily reflect the views and policies of the

// Global Economic Prospects: Spillovers amid Weak Growth February M. Ayhan Kose Disclaimer! The views presented here are those of the authors and do NOT necessarily reflect the views and policies of the

June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28

127/2014-18 August 2014 June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

127/2014-18 August 2014 June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment Erdem Başçı Governor 28-29 April 214, Skopje Overview: Inflation and Monetary Policy Retail loan growth

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment Erdem Başçı Governor 28-29 April 214, Skopje Overview: Inflation and Monetary Policy Retail loan growth

June 2012 Euro area international trade in goods surplus of 14.9 bn euro 0.4 bn euro surplus for EU27

121/2012-17 August 2012 June 2012 Euro area international trade in goods surplus of 14.9 0.4 surplus for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

121/2012-17 August 2012 June 2012 Euro area international trade in goods surplus of 14.9 0.4 surplus for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Swedish portfolio holdings. Foreign equity securities and debt securities

Swedish portfolio holdings Foreign equity securities and debt securities 2007 Swedish portfolio holdings Foreign equity securities and debt securities 2007 Statistiska centralbyrån 2008 Swedish portfolio

Swedish portfolio holdings Foreign equity securities and debt securities 2007 Swedish portfolio holdings Foreign equity securities and debt securities 2007 Statistiska centralbyrån 2008 Swedish portfolio

January 2012 Market Update: Deeply into the Danger Zone

January 2012 Market Update: Deeply into the Danger Zone January 2012 Since the last Global Financial Stability Report (GFSR), risks to stability have increased, despite various policy steps to contain

January 2012 Market Update: Deeply into the Danger Zone January 2012 Since the last Global Financial Stability Report (GFSR), risks to stability have increased, despite various policy steps to contain

The Financial Crisis of ? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

Quarterly Investment Update First Quarter 2018

Quarterly Investment Update First Quarter 2018 Dimensional Fund Advisors Canada ULC ( DFA Canada ) is not affiliated with [insert name of Advisor]. DFA Canada is a separate and distinct company. Market

Quarterly Investment Update First Quarter 2018 Dimensional Fund Advisors Canada ULC ( DFA Canada ) is not affiliated with [insert name of Advisor]. DFA Canada is a separate and distinct company. Market

EUROZONE ECONOMIC WATCH JANUARY 2017

EUROZONE ECONOMIC WATCH JANUARY 2017 Key messages: some changes for the better Improving confidence in across the board shows the resilience of the eurozone to the various potentially disturbing political

EUROZONE ECONOMIC WATCH JANUARY 2017 Key messages: some changes for the better Improving confidence in across the board shows the resilience of the eurozone to the various potentially disturbing political

Modelling the sovereign debt crisis in Europe

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, 13 th September 2018.

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, th September 08. This note reports estimates of the economic impact of introducing a carbon tax of 50 per ton of CO in the Netherlands.

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, th September 08. This note reports estimates of the economic impact of introducing a carbon tax of 50 per ton of CO in the Netherlands.