Unlocking Global Growth. Min Zhu International Monetary Fund

|

|

|

- Esmond Tate

- 5 years ago

- Views:

Transcription

1 Unlocking Global Growth Min Zhu International Monetary Fund 1

2 Outline I. Cyclical recovery slow II. Real and financial sectors diverging III. Macro policy space limited IV. Global structural changes emerge V. Proactive policies needed 2

3 I. Cyclical recovery slow 3

4 World GDP (Real; 2 = 1) October 27 Projections Oct 214 Actual 4

5 GDP Growth (Real; in percent) World Euro area Brazil China India Japan United States 5

6 8 7 World demand (in percent of GDP) Investment/GDP Consumption/GDP Government expenditure/gdp 6

7 5 World FDI (in percent of world GDP) FDI liabilities/gdp FDI assets/gdp 7

8 GDP vs Trade (average annual growth in percent) GDP Trade 8

9 Deleveraging revisited: government sector General Government Interest Expense (percent of GDP) 5 Yr Sovereign Credit Default Swap Spreads (annual average; basis points) Maximum since 26 Historic minimum 1/ / Maximum since 26 3/ Historic minimum 4/ 9 8 Direction of adjustment Direction of adjustment IT IE PT GR ES FR DE NL CA UK US JP AU SE -1 GR PT IT ES IE FR NL DE JP AU UK US SE Stressed EA Other EA Other AEs Stressed EA Other EA Other AEs Sources: Bloomberg L.P.; and IMF staff calculations; 1/ Calculations based on data from 199 to 213. Data for Germany starts in 1991, for Netherlands in 1995 and for the US in 21. 2/ 214 data corresponds to the January - August average. 3/ For Greece, the maximum CDS spreads level since 26 is 155bps. 4/ Calculation 9 based on data from 23 to August 214. Data for Spain and Sweden start in 24, for Ireland in 27, for Australia, Netherlands and the UK in 28, and for the US in 29.

10 Deleveraging revisited: household sector Household Leverage in AEs 1/ (debt-to-total assets; percent) Household Debt Service Burden in AEs 1/ (percent of net disposable income) or latest Maximum since 26 Historic minimum 2/ or latest Maximum since 26 4 Direction of adjustment 3 25 Direction of adjustment IE GR PT ES IT NL FR DE AU SE CA JP UK US -1 GR IE PT ES IT NL FR DE CA AU UK US SE JP Stressed EA Other EA Other AEs Stressed EA Other EA Other AEs Sources: OECD; BIS Quarterly Review (212); Bartiloro et al. (212); Bank of Ireland; Banco do Portugal; Brissims et al. (29); and IMF staff estimates: 1/ Household debt data for Sweden includes debt through housing cooperatives. 2/ Calculation based on data from 1995 to 212 or latest. For Denmark data starts in 23, for Ireland and Spain in 22, and 1 for Switzerland in 2.

11 Deleveraging revisited: corporate sector Corporate Debt-to-Assets Ratio in AEs (percent) Interest Payments to Cash Flow in AEs (percent) Maximum since 26 Historic minimum 1/ Maximum since 26 Historic minimum 1/ 4 Direction of adjustment 5 Direction of adjustment PT GR ES IT IE DE FR NL US JP CA AU SE UK -1 GR PT IT ES IE NL FR DE CA AU US UK SE JP Stressed EA Other EA Other AEs Stressed EA Other EA Other AEs Sources: Worldscope; and IMF staff calculations. 1/ Calculation based on data from 1995 to

12 Deleveraging revisited: banks Leverage Ratio in AEs 1/ (tangible assets-to-tier 1 common capital) 214 Q2 Maximum since 26 Minimum since 26 Direction of adjustment Profitability in AEs (retained earnings-to-adjusted tangible assets ratio) 214 Q2 Minimum since 26 Maximum since Direction of adjustment ES IT PT IE GR FR NL DE CA SE AU JP UK US -1 PT GR IE IT ES FR NL DE UK SE US JP CA AU Stressed EA Other EA Other AEs Stressed EA Other EA Other AEs Sources: SNL; and IMF staff calculations. 1/ Leverage ratio for Japan is defined as tangible assets-to-tangible common equity. The maximum bank leverage ratio in Germany could be overstated, as the sample does not include small banks, which are important as a group in the total. 12

13 13

14 A warning from the past: UK after World War I 14

15 Credit and investment Better here Than here Credit growth to corporates (yoy, 4Q MA) Capital expenditure (% of operating cash flows; rhs) Capex Sample Average(rhs) 2 United States Euro Area Japan Emerging Markets Bank Credit Growth from BRICS banks (median); Capex growth 15 is yoy growth for a sample of 12 Ems;

16 Saving vs Investment: United States (in percent of GDP) HH Non-Fin Fin Gov HH Non-Fin Fin Gov Saving Saving Saving Saving Investment Investment Investment Investment Sources: Haver Analytics 16

17 7 Inflation (in percent) World Japan Euro area 17

18 5-year 5-year forward inflation swaps (in percent) 18

19 II. Real and financial sectors diverging 19

20 Global financial markets Advanced Economies (in billions of U.S. dollars) Emerging Market Economies (in billions of U.S. dollars) 25, 25, 2, 2, Total Reserves Minus Gold Equity Markets Debt Securities 15, 15, Bank Assets 1, 1, 5, 5,

21 Excess financial risk taking? Sovereign Yield Compression Credit Risk Mispricing Record Low Volatility Average Sovereign Bonds (z-scores) Undervalued Top declile Overvalued Bottom decile Note: 5y5y sovereign bond yield in local currency terms minus 5y5y survey-based expectation of real GDP growth and inflation across 15 advanced economies and 9 emerging markets. Z- score computed as mean-adjusted return, scaled by the standard deviation: (y-y bar)/σ Corporate Spreads (z-scores) EU investment grade U.S. investment grade U.S. high yield EU high yield Undervalued Overvalued Note: Z-scores relative to the historical distribution of the respective option-adjusted spreads. Global Composite Volatility Index

22 Credit intermediation shifting to the shadows Asset Managers Rising in Systemic Importance in the United States Largest Holders of Private Bonds 18 Financial Assets (USD tn) 3 Ownership of Corporate and Foreign Bonds (percent) Pension Funds Banks Insurance Asset Managers Pension Funds Banks Asset Managers Insurance 11

5 45 Ownership by Single Fund Family")

Top 1 AMs: $19 tn (3% of all AUM) 4 35 3 45 4 35 25 3 $46 tn 2 15 1 5 25 2 15")

23 Asset managers: a source of contagion? Brand Risk Concentrated Holdings Liquidity Mismatch Asset Manager AUM (Total = $65 tn) 5 45 Ownership by Single Fund Family of Large Individual Corporate Issuers (Percent of total debt issuance) Number of Days for the Full Liquidation of U.S. Credit Mutual Funds and ETFs (Corporate bonds) Top 1 AMs: $19 tn (3% of all AUM) $46 tn day limit for redemption payments High Yield EM External Debt

24 Asset managers spark sovereign crises Large redemptions, portfolio reallocations, market power abused Debt Owned by a Single Fund Family (percent) Franklin Templeton s Big Bets Credit rating C High yield Country Percentage of Country's debt held by...its value, Franklin Templeton Investments and in billions CCC Ukraine Uruguay 14.2% $4.45 B Sri Lanka Ghana Serbia Fiji Congo Uganda Hungary 13.6% $14.8 BB Armenia Croatia Indonesia Hungary French Polynesia Investment grade Ukraine 1.5% $8.78 BBB Turkey Uruguay Malaysia 1.4% $18.54 Turks & Caicos A Ireland South Korea 5.6% $

25 Liquidity illusion today Liquidity trap tomorrow? Ample Monetary Liquidity But Deteriorating Structural Market Liquidity (USD tn) 1 Central Bank Balance Sheets FED ECB BOJ (USD mn) 13.5 Size of Trades (> 5mn; 6-month average; investment grade) BOE* SNB * Bank of England data unavailable before 26 due to defini the BoE s balance sheet items 12

26

27 Spillovers could be global Rising Share of EMs in AE Portfolios Advanced Economy Bond Allocations to EMs (percent of total) 1 Leading to Higher Synchronization of Asset Prices Synchronization Index AE and EM 5 And Higher Impact of U.S. Shocks Estimated Impact of Increase in Vol and U.S. Rates on EM Sovereign Yields (bps) Note: Portion of total variation explained by the 1 st principal component on levels of AE and EM bonds; 6-month moving window Volatility shock US rate shock Total 27 14

28 III. Macro policy space limited 28

29 25 Public debt (in percent of GDP) Advanced economies Japan Italy United States Canada France Germany Emerging economies India Brazil China Russia 28 Change

30 11 Public debt in advanced economies (in percent of GDP)

31 Emerging markets: consolidation postponed Revisions to Forecasts (percent of GDP; excluding China) Overall Fiscal Balance Debt-to-GDP ratio Oct Balance Sept. 212 Debt Sept. 212 Oct

32 75 5 Contributions to deleveraging (percent of GDP) Output Growth Inflation Nominal Debt Growth Leverage Growth Asia Financial Crisis Nordic Countries Global Financial Crisis Sources: BIS, Penn World Tables, Staff Calculations AE EM Hyper Inflation (rhs)

33 Advanced economies need to reduce debt but conditions are a challenge CAPB (percent of potential GDP) 1 Government Debt (percent of GDP) Real GDP Growth (percent) 5 Deflator (percent) FAD WEMD Report 9/25/214 Historical episodes Latest crisis

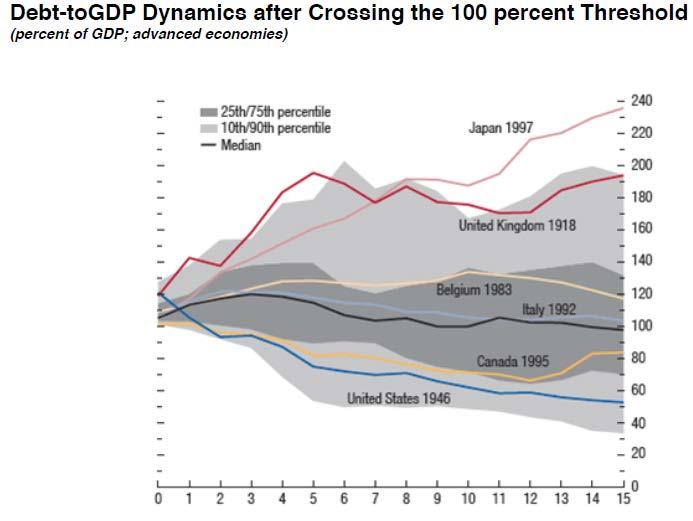

34 Debt-to-GDP Dynamics after Public Debt Reaches 1 Percent of GDP (Percent of GDP, advanced economies) 34

35 35

36 Government debt (in percent of GDP) Government interest expense (in percent of GDP) Advanced Economies Japan United Kingdom United States Euro area Emerging Market and Middle-Income Economies Brazil China India Russia

37 Central bank assets /GDP.7 US EU Japan UK.8 China India Brazil Russia Sources: Haver Analytics 37

38 Interest Rates (in percent) US Japan EU UK China India Brazil Russia Sources: Bloomberg 38

")

39 Policy rate expectations (percent; dashed lines are from April 214 WEO) 39

40 US 1-year treasury breakdown (in percent) Bund breakdown (in percent) 4

41 1.3 U.S. Dollar Euro Japanese Yen Sources: IFS 41

42 IV. Global structural changes emerge 42

43 7 GDP based on PPP (share of world GDP) 1 Investment based on PPP (share in total world investment) 6 5 Advanced economies Emerging market and developing economies 8 Advanced economies Emerging and developing economies Consumption based on PPP (share in total world consumption) 1 Exports based on PPP (share in total world exports) 8 Advanced economies Emerging and developing economies 8 Advanced economies Emerging and developing economies FDI assets based on PPP (share in total world FDI) Advanced economies Emerging and developing economies 1 8 FDI liabilities based on PPP (share in total world FDI) Advanced economies Emerging and developing economies Sources: WEO

44 44

45 7 EM GDP per capita Strong progress in last decade % 2% 25% 3% EM GDP Per Capita Relative to the U.S. (PPP, 5-yr average) Source: Penn Table 7.1, WEO, IMF staff calculation. 45

46 (in percent of GDP) Consumption Advanced Economies Investment Current account Consumption Emer.& Develop. Eco. Investment Current account

47 Working age population (in millions) Euro area Japan China India United States United Kingdom Brazil Sub-Saharan Africa 47

48 Real income growth (Percent change between 1988 and 28) Source: Branko Milanovic (212) 48

49 Total factor productivity Growth in percent Source: Antonin Bergeaud et al (214) 49

50 Interconnectivity 5

51 Interconnectivity 51

52 Interconnectivity 52

53 Interconnectivity 53

54 Interconnectivity 54

55 Interconnectivity 55

56 56

57 57

58 58

59 59

60 V. Proactive policies needed 6

61 I. Growth enhancing supply side policies a) Structural reform i. Product market competition ii. Labor market flexibility iii. Increase service sector productivity iv. Pension reform b) Smart investment i. Infrastructure investment ii. Knowledge economy a) Long term R&D b) Innovative SMEs iii. Measures to move traditional sectors to their frontier iv. Long-term human capital formation a) Education b) Healthcare c) Childcare c) Supply-side supporting monetary and fiscal policies i. Smart/quality fiscal expenditure ii. Monetary policy with targeted transmission channel iii. Monetary and fiscal policies maintain growth speed 61

62 II. Macroeconomic stability a) Be vigilant in financial market risks i. Strengthen monetary and credit transmission to the real economy ii. Use macroprudential policies b) Implement consistent regulatory reform and enhance supervision of the shadow banking system c) Monitor of global liquidity flows and currency dynamics d) Prepare for Fed s interest rate hike e) Form medium term fiscal consolidation plans III. Global cooperation a) Facilitate globalization (trade, capital flows) b) Enhance global financial safety net c) Implement global regulatory reform d) Put into practice new multilateralism 62

63 Thank you 63

Progress towards Strong, Sustainable and Balanced Growth. Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction)

") Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Progress Towards Strong, Sustainable, and Balanced Growth. Figure 1: Recovery From Financial Crisis (100 = First Quarter of Real GDP contraction)

") Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

2017 Asia and Pacific Regional Economic Outlook:

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle. Angel Gavilan, Martin Hillebrand December 2017

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle Angel Gavilan, Martin Hillebrand December 217 The last boom in capital flows was largely a global phenomenon Sum of current account

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle Angel Gavilan, Martin Hillebrand December 217 The last boom in capital flows was largely a global phenomenon Sum of current account

World Economic Outlook

World Economic Outlook Marco E. Terrones Assistant to the Director Research Department, IMF May 2012 The views expressed in this presentation are those of the author and do not necessarily represent those

World Economic Outlook Marco E. Terrones Assistant to the Director Research Department, IMF May 2012 The views expressed in this presentation are those of the author and do not necessarily represent those

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Negative Interest Rate Policies: Sources and Implications

Negative Interest Rate Policies: Sources and Implications November 4, 216 Marc Stocker Based on a recently published CEPR / World Bank Working Paper Disclaimer! The views presented here are those of the

Negative Interest Rate Policies: Sources and Implications November 4, 216 Marc Stocker Based on a recently published CEPR / World Bank Working Paper Disclaimer! The views presented here are those of the

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

ECB LTRO Dec Greece program

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows Marcel Fratzscher European Central Bank Conference Financial Globalization: Shifting Balances Banco

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows Marcel Fratzscher European Central Bank Conference Financial Globalization: Shifting Balances Banco

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager. November 2015

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager November 2015 Agenda Macro update & government bonds Emerging market corporate bonds Fund positioning Emerging markets risks today Risks Slowing

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager November 2015 Agenda Macro update & government bonds Emerging market corporate bonds Fund positioning Emerging markets risks today Risks Slowing

International Monetary Fund

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY. Villa d'este, Cernobbio - September 7, 8 and 9, 2012

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY Villa d'este, Cernobbio - September 7, 8 and 9, 1 Working paper, September 1. Kindly authorized by the Author.

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY Villa d'este, Cernobbio - September 7, 8 and 9, 1 Working paper, September 1. Kindly authorized by the Author.

Financial Crisis What do we know?

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Global risks and challenges of the world economy

FINANCE A VÝKONNOST FIRIEM VO VEDE, VYUCE A PRAXE Global risks and challenges of the world economy Univerzita Tomáše Bati ve Zline Fakulta mamagementu a ekonomiky Medzinarodní vedecká konference 23.- 24.

FINANCE A VÝKONNOST FIRIEM VO VEDE, VYUCE A PRAXE Global risks and challenges of the world economy Univerzita Tomáše Bati ve Zline Fakulta mamagementu a ekonomiky Medzinarodní vedecká konference 23.- 24.

FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED MEMBERS OF THE PRESS ONLY, NOT FOR FURTHER DISTRIBUTION.

2018 Global Market Outlook Press Briefing GLOBAL FIXED INCOME Mark Vaselkiv Portfolio Manager, CIO, Fixed Income November 14, 2017 FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED

2018 Global Market Outlook Press Briefing GLOBAL FIXED INCOME Mark Vaselkiv Portfolio Manager, CIO, Fixed Income November 14, 2017 FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED

2016 External Sector Report

216 External Sector Report Global Imbalances and Policy Challenges September, 216 o Evolution of Global Current Accounts and Exchange Rates Widening and reconfiguration of imbalances in 215 Drivers: Asymmetric

216 External Sector Report Global Imbalances and Policy Challenges September, 216 o Evolution of Global Current Accounts and Exchange Rates Widening and reconfiguration of imbalances in 215 Drivers: Asymmetric

A short history of debt

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

World Economic Outlook Central Europe and Baltic Countries

World Economic Outlook Central Europe and Baltic Countries Presentation by Susan Schadler and Christoph Rosenberg September 5 World growth returns to trend. (World real GDP growth, annual percent change)

World Economic Outlook Central Europe and Baltic Countries Presentation by Susan Schadler and Christoph Rosenberg September 5 World growth returns to trend. (World real GDP growth, annual percent change)

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates Takatoshi Kato Deputy Managing Director International Monetary Fund September 3, 27 1 9 Growth has been

Challenges to the International Monetary System: Rebalancing Currencies, Institutions, and Rates Takatoshi Kato Deputy Managing Director International Monetary Fund September 3, 27 1 9 Growth has been

Stronger growth, but risks loom large

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

Fiscal Policy and the Global Crisis

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Financial Stability Review November Press Briefing Luis de Guindos 29 November 2018

Financial Stability Review November 218 Press Briefing Luis de Guindos 29 November 218 Risk assessment The financial stability environment has become more challenging Four key risks over a two-year horizon

Financial Stability Review November 218 Press Briefing Luis de Guindos 29 November 218 Risk assessment The financial stability environment has become more challenging Four key risks over a two-year horizon

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

Turkey: Recent Developments and Future Prospects. ISBANK Economic Research Division October 2018

Turkey: Recent Developments and Future Prospects ISBANK Economic Research Division October 2018 Macroeconomic Outlook Strong Economic Growth Cycle GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

Turkey: Recent Developments and Future Prospects ISBANK Economic Research Division October 2018 Macroeconomic Outlook Strong Economic Growth Cycle GDP of 851 bn USD (2017), 10.6k USD (2017) per capita

Recent Recent Developments 0

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Trends and opportunities across regions: Europe

Trends and opportunities across regions: Europe Monday, 6 June 2011 Head of Institutional Fixed Income Europe Three themes shaping global opportunities I. Long term: Spheres of influence are shifting among

Trends and opportunities across regions: Europe Monday, 6 June 2011 Head of Institutional Fixed Income Europe Three themes shaping global opportunities I. Long term: Spheres of influence are shifting among

Potential Gains from the Reform Package

Chart 1 Potential Gains from the Reform Package GDP per capita, % 18 16 14 12 8 6 4 2 Ireland Germany Finland Portugal Spain France Greece Note: The estimated cumulative GDP impact from structural reforms

Chart 1 Potential Gains from the Reform Package GDP per capita, % 18 16 14 12 8 6 4 2 Ireland Germany Finland Portugal Spain France Greece Note: The estimated cumulative GDP impact from structural reforms

FINANCIAL FORECASTS ECONOMIC RESEARCH. January No. 1. What will be the characteristics of euro-zone financial markets in 2016?

ECONOMIC RESEARCH January - No. What will be the characteristics of euro-zone financial markets in? We believe investors will be faced with the following characteristics in euro-zone financial markets

ECONOMIC RESEARCH January - No. What will be the characteristics of euro-zone financial markets in? We believe investors will be faced with the following characteristics in euro-zone financial markets

Consequences of ageing for international finance

Consequences of ageing for international finance Hyun Song Shin* Bank for International Settlements G20 Symposium: For the Better Future: Demographic Changes and Macroeconomic Challenges Tokyo, 17 January

Consequences of ageing for international finance Hyun Song Shin* Bank for International Settlements G20 Symposium: For the Better Future: Demographic Changes and Macroeconomic Challenges Tokyo, 17 January

Internet Appendix: Government Debt and Corporate Leverage: International Evidence

Internet Appendix: Government Debt and Corporate Leverage: International Evidence Irem Demirci, Jennifer Huang, and Clemens Sialm September 3, 2018 1 Table A1: Variable Definitions This table details the

Internet Appendix: Government Debt and Corporate Leverage: International Evidence Irem Demirci, Jennifer Huang, and Clemens Sialm September 3, 2018 1 Table A1: Variable Definitions This table details the

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for August 2011 All data are as of Wednesday, August 31, 2011. The regional indices are

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for August 2011 All data are as of Wednesday, August 31, 2011. The regional indices are

UPDATE ON FISCAL STIMULUS AND FINANCIAL SECTOR MEASURES. April 26, 2009

UPDATE ON FISCAL STIMULUS AND FINANCIAL SECTOR MEASURES April 26, 2009 This note provides an update of information in the paper, The State of Public Finances: Outlook and Medium-Term Policies After the

UPDATE ON FISCAL STIMULUS AND FINANCIAL SECTOR MEASURES April 26, 2009 This note provides an update of information in the paper, The State of Public Finances: Outlook and Medium-Term Policies After the

The effects of the financial crisis on developing countries mapping out the issues. By Julian Jessop

The effects of the financial crisis on developing countries mapping out the issues By Julian Jessop 1. Plan of My Talk The outlook for advanced economies. Impact on developing countries. Some losers and

The effects of the financial crisis on developing countries mapping out the issues By Julian Jessop 1. Plan of My Talk The outlook for advanced economies. Impact on developing countries. Some losers and

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Adverse scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2018

9 April 218 ECB-PUBLIC Adverse scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 218 Introduction In accordance with its mandate, the European Insurance

9 April 218 ECB-PUBLIC Adverse scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 218 Introduction In accordance with its mandate, the European Insurance

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

International Economic Outlook

International Monetary Fund September 9, 16 International Economic Outlook Alejandro Werner Director Western Hemisphere Department 1 Global and Regional Developments Relevant Issues Global and Regional

International Monetary Fund September 9, 16 International Economic Outlook Alejandro Werner Director Western Hemisphere Department 1 Global and Regional Developments Relevant Issues Global and Regional

International Monetary Fund. World Economic Outlook. Jörg Decressin Senior Advisor Research Department, IMF

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016

17 March 2016 ECB-PUBLIC Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016 Introduction In accordance with its mandate, the European Insurance

17 March 2016 ECB-PUBLIC Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016 Introduction In accordance with its mandate, the European Insurance

Heraklis Polemarchakis The Debt of Nations

Heraklis Polemarchakis The Debt of Nations The Crisis in the Euro Area Bank of Greece, Vouliagmeni, May 23 24, 2013 Outline An overview of numbers across the world Total for advanced economies Why Does

Heraklis Polemarchakis The Debt of Nations The Crisis in the Euro Area Bank of Greece, Vouliagmeni, May 23 24, 2013 Outline An overview of numbers across the world Total for advanced economies Why Does

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for July 2011 All data are as of Friday, July 29, 2011. The regional indices are based

Capital Markets and Corporate Governance Service Line Capital Markets Practice, FPD Emerging Capital Markets Update for July 2011 All data are as of Friday, July 29, 2011. The regional indices are based

Emerging Markets Outlook

Mark Mobius, Ph.D. Executive Chairman Templeton Emerging Markets Group Emerging Markets Outlook Dealer Use Only / Not for Distribution to the Public Agenda Performance Emerging Markets Equities: Demand

Mark Mobius, Ph.D. Executive Chairman Templeton Emerging Markets Group Emerging Markets Outlook Dealer Use Only / Not for Distribution to the Public Agenda Performance Emerging Markets Equities: Demand

World Economic Outlook. Recovery Strengthens, Remains Uneven April

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

Currency Market Outlook EMPRES-7173

Currency Market Outlook 1 Currency Markets Outlook certainly one lesson is that we should get used to periods of higher volatility Mario Draghi President of the European Central Bank ECB Press Conference

Currency Market Outlook 1 Currency Markets Outlook certainly one lesson is that we should get used to periods of higher volatility Mario Draghi President of the European Central Bank ECB Press Conference

Sovereign Debt Managers Forum

Sovereign Debt Managers Forum Breakout Session 1: Market Dynamics in International Capital Markets for Sovereign Debt By C J P Siriwardena Assistant Governor Central Bank of Sri Lanka 04 December 2014

Sovereign Debt Managers Forum Breakout Session 1: Market Dynamics in International Capital Markets for Sovereign Debt By C J P Siriwardena Assistant Governor Central Bank of Sri Lanka 04 December 2014

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Economic Outlook. Macro Research Itaú Unibanco

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions JOHN W. BECK Senior Vice President Co-Director, Global Fixed Income Franklin

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions JOHN W. BECK Senior Vice President Co-Director, Global Fixed Income Franklin

Spillovers from Dollar Appreciation

June 6-7, 216 International Monetary Fund Spillovers from Dollar Appreciation Florence Jaumotte (with J. Chow, S.G. Park, and S. Zhang) Motivation Context: appreciation of US Dollar changing growth differentials,

June 6-7, 216 International Monetary Fund Spillovers from Dollar Appreciation Florence Jaumotte (with J. Chow, S.G. Park, and S. Zhang) Motivation Context: appreciation of US Dollar changing growth differentials,

Toward A Bottom-Up Approach in Assessing Sovereign Default Risk

Toward A Bottom-Up Approach in Assessing Sovereign Default Risk Dr. Edward I. Altman Stern School of Business New York University Keynote Lecture Risk Day Conference MacQuarie University Sydney, Australia

Toward A Bottom-Up Approach in Assessing Sovereign Default Risk Dr. Edward I. Altman Stern School of Business New York University Keynote Lecture Risk Day Conference MacQuarie University Sydney, Australia

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance Agus D.W. Martowardojo Governor Bank Indonesia Prepared for Mandiri Investment Forum, January 27, 2015 2 1 Global Economic

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance Agus D.W. Martowardojo Governor Bank Indonesia Prepared for Mandiri Investment Forum, January 27, 2015 2 1 Global Economic

How to measure country risk?

How to measure country risk? Produced by: Cross-country Emerging Markets Unit For the Occasion of: Second BBVA Resarch Emerging Market Seminar Madrid, July 13, 211 Road map to the presentation 1. Previous

How to measure country risk? Produced by: Cross-country Emerging Markets Unit For the Occasion of: Second BBVA Resarch Emerging Market Seminar Madrid, July 13, 211 Road map to the presentation 1. Previous

Emerging market equities

November 22, 2010 Emerging market equities Jean-Pierre Talon, FSA, FICA Introduction Focus of this presentation is to set out the rationale for a strategic bias toward emerging market equities Consider

November 22, 2010 Emerging market equities Jean-Pierre Talon, FSA, FICA Introduction Focus of this presentation is to set out the rationale for a strategic bias toward emerging market equities Consider

Macroeconomic overview SEE and Macedonia

Macroeconomic overview SEE and Macedonia Zoltan Arokszallasi Chief Analyst, Macro & FX/FI Research Erste Group Bank Erste Investors Breakfast, 29 September, Skopje 02. Oktober SEE shows mixed performance

Macroeconomic overview SEE and Macedonia Zoltan Arokszallasi Chief Analyst, Macro & FX/FI Research Erste Group Bank Erste Investors Breakfast, 29 September, Skopje 02. Oktober SEE shows mixed performance

Latin America Sovereign Ratings in a Weakening Global Economy Shelly Shetty, Head of Latin America Sovereigns

Latin America Sovereign Ratings in a Weakening Global Economy Shelly Shetty, Head of Latin America Sovereigns October 11, 211 Agenda Latin America Sovereigns: Ratings Trajectory In A Weakening Global Environment

Latin America Sovereign Ratings in a Weakening Global Economy Shelly Shetty, Head of Latin America Sovereigns October 11, 211 Agenda Latin America Sovereigns: Ratings Trajectory In A Weakening Global Environment

All-Country Equity Allocator July 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

Details of the changes to the Investment Policies and Revision of the Investment Restrictions on the underlying funds of:

Details of the changes to the Investment Policies and Revision of the Investment Restrictions on the underlying funds of: 1. J60 Templeton Emerging Markets 2. L05 Templeton Global Bond (EUR) 3. L06 Templeton

Details of the changes to the Investment Policies and Revision of the Investment Restrictions on the underlying funds of: 1. J60 Templeton Emerging Markets 2. L05 Templeton Global Bond (EUR) 3. L06 Templeton

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, 13 th September 2018.

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, th September 08. This note reports estimates of the economic impact of introducing a carbon tax of 50 per ton of CO in the Netherlands.

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, th September 08. This note reports estimates of the economic impact of introducing a carbon tax of 50 per ton of CO in the Netherlands.

OECD ECONOMIC OUTLOOK

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

Regional Economic Outlook

E U R Advanced Europe Emerging Europe Regional Economic Outlook Spring 18 Key Messages Strong economic growth but lead indicators point to a peak Much lower wage growth in most of advanced Europe than

E U R Advanced Europe Emerging Europe Regional Economic Outlook Spring 18 Key Messages Strong economic growth but lead indicators point to a peak Much lower wage growth in most of advanced Europe than

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

WORLD ECONOMIC OUTLOOK October 2017

WORLD ECONOMIC OUTLOOK October 2017 Andreas Bauer Sr Resident Representative @imf_delhi World Economic Outlook The big picture Global activity picked up further in 2017H1 the outlook is now for higher

WORLD ECONOMIC OUTLOOK October 2017 Andreas Bauer Sr Resident Representative @imf_delhi World Economic Outlook The big picture Global activity picked up further in 2017H1 the outlook is now for higher

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

All-Country Equity Allocator February 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Charles Waters cwaters@dcmadvisors.com 917-386-6264 All-Country Equity Allocator February

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Charles Waters cwaters@dcmadvisors.com 917-386-6264 All-Country Equity Allocator February

World real GDP growth in 2010 Annual percent change

World real GDP growth in 20 Annual percent change % or more 6-% 3-6% 0-3% Less than 0% No data Source: International Monetary Fund. World real GDP growth in 2011 Annual percent change % or more 6-% 3-6%

World real GDP growth in 20 Annual percent change % or more 6-% 3-6% 0-3% Less than 0% No data Source: International Monetary Fund. World real GDP growth in 2011 Annual percent change % or more 6-% 3-6%

Financial Globalization, governance, and the home bias. Bong-Chan Kho, René M. Stulz and Frank Warnock

Financial Globalization, governance, and the home bias Bong-Chan Kho, René M. Stulz and Frank Warnock Financial globalization Since end of World War II, dramatic reduction in barriers to international

Financial Globalization, governance, and the home bias Bong-Chan Kho, René M. Stulz and Frank Warnock Financial globalization Since end of World War II, dramatic reduction in barriers to international

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Why Invest In Emerging Markets? Why Now?

Why Invest In Emerging Markets? Why Now? 2018 Over the long term, Emerging Markets (EM) have been a winning alternative compared to traditional Developed Markets (DM)... 350 300 250 200 150 100 50 1998

Why Invest In Emerging Markets? Why Now? 2018 Over the long term, Emerging Markets (EM) have been a winning alternative compared to traditional Developed Markets (DM)... 350 300 250 200 150 100 50 1998

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

Gold demand statistics

Gold demand statistics Table 2: Gold demand (tonnes) 2014 2015 Q2 14 Q3 14 Q4 14 Q2 15 Q3 15 Q4 15 Jewellery 2,482.0 2,397.5 589.5 591.5 686.0 596.9 513.7 623.7 663.2 481.9-19 Technology 348.5 333.8 86.6

Gold demand statistics Table 2: Gold demand (tonnes) 2014 2015 Q2 14 Q3 14 Q4 14 Q2 15 Q3 15 Q4 15 Jewellery 2,482.0 2,397.5 589.5 591.5 686.0 596.9 513.7 623.7 663.2 481.9-19 Technology 348.5 333.8 86.6

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016 Page 1 Themes Oil s Not Well A world of cheap petroleum Eastern Anxiety China attempts a difficult transition Growing Prospects Central

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016 Page 1 Themes Oil s Not Well A world of cheap petroleum Eastern Anxiety China attempts a difficult transition Growing Prospects Central

STOXX BROAD, SIZE AND BLUE-CHIP INDICES EMERGING AND DEVELOPED MARKETS, EAST ASIA, AFRICA. August 2012

STOXX BROAD, SIZE AND BLUE-CHIP INDICES EMERGING AND DEVELOPED MARKETS, EAST ASIA, AFRICA August 2012 1 Agenda 1. Definitions Page 03 2. Design Page 10 3. Composition Page 13 4. Performance Page 24 2 1.

STOXX BROAD, SIZE AND BLUE-CHIP INDICES EMERGING AND DEVELOPED MARKETS, EAST ASIA, AFRICA August 2012 1 Agenda 1. Definitions Page 03 2. Design Page 10 3. Composition Page 13 4. Performance Page 24 2 1.

Why Invest In Emerging Markets? Why Now?

Why Invest In Emerging Markets? Why Now? 2017 Over the long term, Emerging Markets (EM) have been a winning alternative compared to traditional Developed Markets (DM)... 350 300 250 200 150 100 50 1997

Why Invest In Emerging Markets? Why Now? 2017 Over the long term, Emerging Markets (EM) have been a winning alternative compared to traditional Developed Markets (DM)... 350 300 250 200 150 100 50 1997

GLOBAL ECONOMY AND IMPLICATIONS FOR ISRAEL

GLOBAL ECONOMY AND IMPLICATIONS FOR ISRAEL Aaron Institute for Economic Policy Annual Conference May 4, 217 Craig Beaumont, European Department, IMF Outline World economic outlook (WEO) Broader trends

GLOBAL ECONOMY AND IMPLICATIONS FOR ISRAEL Aaron Institute for Economic Policy Annual Conference May 4, 217 Craig Beaumont, European Department, IMF Outline World economic outlook (WEO) Broader trends

RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO OCTOBER 2003

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

Global Sovereign Conference Singapore 6 September

Global Sovereign Conference Singapore September 1 --- --- Politics, Populism and the Global Economy Brian Coulton Chief Economist --- --- Key Messages World economy muddling along but global macro risks

Global Sovereign Conference Singapore September 1 --- --- Politics, Populism and the Global Economy Brian Coulton Chief Economist --- --- Key Messages World economy muddling along but global macro risks

Public Debt Sustainability Analysis for Market Access Countries (MACs): The IMF s Framework. S. Ali Abbas International Monetary Fund

: The IMF s Framework. S. Ali Abbas International Monetary Fund") Public Debt Sustainability Analysis for Market Access Countries (MACs): The IMF s Framework S. Ali Abbas International Monetary Fund September 215 1 Outline Motivation for 213 MAC DSA reform Risk - Based

Public Debt Sustainability Analysis for Market Access Countries (MACs): The IMF s Framework S. Ali Abbas International Monetary Fund September 215 1 Outline Motivation for 213 MAC DSA reform Risk - Based

Global Financial Stability Report: Grappling with Crisis Legacies

Global Financial Stability Report: Grappling with Crisis Legacies Seminar for Senior Bank Supervisors from Emerging Economies Laura E. Kodres /International Monetary Fund October 17, 2011 Chapter 1 Overcoming

Global Financial Stability Report: Grappling with Crisis Legacies Seminar for Senior Bank Supervisors from Emerging Economies Laura E. Kodres /International Monetary Fund October 17, 2011 Chapter 1 Overcoming

Global Economic Prospects: Navigating strong currents

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

RESILIENCE IN A TIME OF HIGH DEBT

RESILIENCE IN A TIME OF HIGH DEBT PRE-RELEASE OF THE SPECIAL CHAPTER OF THE OECD ECONOMIC OUTLOOK (To Be Released on 28th November at 11.00am CET) Paris, 23th November 2017 www.oecd.org/economy/economicoutlook.htm

RESILIENCE IN A TIME OF HIGH DEBT PRE-RELEASE OF THE SPECIAL CHAPTER OF THE OECD ECONOMIC OUTLOOK (To Be Released on 28th November at 11.00am CET) Paris, 23th November 2017 www.oecd.org/economy/economicoutlook.htm

China: Beyond the headlines. Bill Maldonado HSBC Global Asset Management

China: Beyond the headlines Bill Maldonado HSBC Global Asset Management Are you a China Bull or a Bear? Source: Various news publications 2 Bear myth #1: Hard landing? GDP: Growth is slowing, but it s

China: Beyond the headlines Bill Maldonado HSBC Global Asset Management Are you a China Bull or a Bear? Source: Various news publications 2 Bear myth #1: Hard landing? GDP: Growth is slowing, but it s

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving. Alen Kovac, Chief Economist EBC May 2016 Ljubljana

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving Alen Kovac, Chief Economist EBC May 216 Ljubljana Real economy highlights Recent GDP track record reveals more favorable footprint

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving Alen Kovac, Chief Economist EBC May 216 Ljubljana Real economy highlights Recent GDP track record reveals more favorable footprint

Sovereign Risk, Debt Management and Financial Stability

Monetary and Capital Markets Department Sovereign Assets and Liabilities Management Division Sovereign Risk, Debt Management and Financial Stability Udaibir S. Das Tunis, March 30, 2010 Outline Sovereign

Monetary and Capital Markets Department Sovereign Assets and Liabilities Management Division Sovereign Risk, Debt Management and Financial Stability Udaibir S. Das Tunis, March 30, 2010 Outline Sovereign

Date of Latest Changes

Emerging Capital Markets Update for May 2011 All data are as of Tuesday, May 31, 2011. The regional indices are based on an average of major EM countries in each region where the data are available. Summary

Emerging Capital Markets Update for May 2011 All data are as of Tuesday, May 31, 2011. The regional indices are based on an average of major EM countries in each region where the data are available. Summary

Money, Finance and the Real Economy: what went wrong?

Money, Finance and the Real Economy: what went wrong? Anton Brender Rotterdam, December 1, 15 December 15 FIRMS SPENDING BEHAVIOUR RESPONDS LESS TO INTEREST RATES CHANGES Non-financial firms borrowing

Money, Finance and the Real Economy: what went wrong? Anton Brender Rotterdam, December 1, 15 December 15 FIRMS SPENDING BEHAVIOUR RESPONDS LESS TO INTEREST RATES CHANGES Non-financial firms borrowing

GLOBAL FIXED INCOME OVERVIEW

2016 Global Market Outlook Press Briefing GLOBAL FIXED INCOME OVERVIEW Edward A. Wiese, CFA, Head of Fixed Income November 18, 2015 Global Fixed Income Outlook: Summary Environment Developed market yields

2016 Global Market Outlook Press Briefing GLOBAL FIXED INCOME OVERVIEW Edward A. Wiese, CFA, Head of Fixed Income November 18, 2015 Global Fixed Income Outlook: Summary Environment Developed market yields

Recent developments and challenges for the Portuguese economy

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Does One Law Fit All? Cross-Country Evidence on Okun s Law

Does One Law Fit All? Cross-Country Evidence on Okun s Law Laurence Ball Johns Hopkins University Global Labor Markets Workshop Paris, September 1-2, 2016 1 What the paper does and why Provides estimates

Does One Law Fit All? Cross-Country Evidence on Okun s Law Laurence Ball Johns Hopkins University Global Labor Markets Workshop Paris, September 1-2, 2016 1 What the paper does and why Provides estimates

Global Economic Prospects: A Fragile Recovery. June M. Ayhan Kose Four Questions

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

Economic Outlook. Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012.

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

Session 16. Review Session

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?