LECTURE 9 The Effects of Credit Contraction: Credit Market Disruptions. October 19, 2016

|

|

|

- Anthony Stafford

- 6 years ago

- Views:

Transcription

1 Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 9 The Effects of Credit Contraction: Credit Market Disruptions October 19, 2016

2 I. OVERVIEW AND GENERAL ISSUES

3 Effects of Credit Balance-sheet and cash-flow effects. The effects of financial crises (using mainly aggregate time-series evidence). The effects of credit disruptions (using mainly micro cross-section evidence).

4 II. PEEK AND ROSENGREN, COLLATERAL DAMAGE: EFFECTS OF THE JAPANESE BANK CRISIS ON REAL ACTIVITY IN THE UNITED STATES

5 Peek and Rosengren s Natural Experiment Financial crisis in Japan causes trouble for banks in U.S. related to Japanese banks (such as U.S. branches of Japanese banks). Decline in loans by U.S. branches of Japanese banks are almost surely caused by a decline in loan supply not loan demand.

6 Evaluation of the Natural Experiment What is their key assumption? Japan s troubles didn t affect loan supply of American banks. What is the importance of the fact that there is large regional variation in the commercial real estate market? Other things going on in the U.S. at the same time. Could this cause problems?

7 Coefficient on nonperforming loan ratio is negative and significant in two of three states with many Japanese banks, and in the three states combined.

8 Transmission of Japanese Shocks to U.S. Commercial Real Estate Lending Panel data on all domestically-owned commercial banks headquartered in one of the three states and Japanese bank branches. Data are semiannual. Dependent variable is change in total commercial real estate loans/beginning period assets held by bank in that state.

9 Testing Whether Conditions at a Japanese Parent Bank Affect Lending

10

11 Real Effects of Declines in Japanese Commercial Real Estate Lending Data are now state level (but have expanded to 25 states). Data are still semiannual. Dependent variable is semiannual change in construction in the state.

12 Testing Whether Lending Shocks Affect Real Construction Activity Bank includes two variables: Contemporaneous change in CRE loans held by branches of Japanese banks NPL for all banks in the state

13 Methodology TSLS Instrument for change in commercial real estate loans by Japanese banks with state-level measure of health of parent banks. Also use change in land prices in Japan as instrument.

14

15

16 Interpreting the coefficient: The in column (3) implies that a decline in loans by Japanese banks in a state of $100 lowers the real value of construction projects in that state by $

17 Evaluation

18 III. CHODOROW-REICH, THE EFFECT OF CREDIT MARKET DISRUPTIONS: FIRM-LEVEL EVIDENCE FROM THE FINANCIAL CRISIS

19 Big Picture Measuring the impact of credit disruption on employment financial crisis is used (somewhat) as a natural experiment. What sets the paper apart is firm-level data on credit and employment. Finds substantial effects of credit disruption on both lending and employment.

20 Relation to Literature Similar in spirit to Peek and Rosengren, but looking at firm-level outcomes (not state employment outcomes). Ivashina and Scharfstein look at lending outcomes by banks (so only about 40 observations), not firms. Nothing on employment effects. Greenstone and Mas look at employment and small business lending at the county level.

21 Relationship Lending Important starting point is that firms tend to be attached to particular financial institutions. Syndicated loan market. Testing for a relationship:

22 From: Chodorow-Reich, The Employment Effects of Credit Market Disruptions

23 Data Individual loan data from Dealscan. Bank characteristics from Federal Reserve reports, Bankscope (for foreign lenders), and CRSP (stock prices). Individual firm employment data from BLS Longitudinal Database (LBD). Merge loan and employment data (hard!).

24 From: Chodorow-Reich, The Employment Effects of Credit Market Disruptions

25 Identification is employment growth at firm i, related to bank s is an indicator for whether firm i receives a loan from bank s are observable firm characteristics are unobservable firm characteristics is the internal cost of funds at bank s If we knew we could regress employment growth on whether the firm got a loan, instrumenting with. For this to work, it is essential that be uncorrelated with.

26 Don t observe R S. Problems with this Approach Other characteristics of loans besides whether firm got one matter (for example, the interest rate and other terms). So Chodorow-Reich considers the reduced form: where M S is a measure of loan supply.

27 How does the idea of the financial crisis as a natural experiment enter the analysis? In that period, it is likely that M S and U i are relatively uncorrelated. Problems leading to the crisis did not involve the corporate loan portfolio.

28 What is Chodorow-Reich s measure of M S? Percent change in the number of loans to other firms between the periods October 2005 to June 2007 and October 2008 and June Is this a good measure? Other options?

29 M S is not a perfect measure of loan supply, so C-R instruments with: Exposure to Lehman Brothers ABX Exposure Bank statement items ( trading revenue/assets; real estate charge-offs flag, etc.)

30 From: Chodorow-Reich, The Employment Effects of Credit Market Disruptions

31 Industry State Also include firm characteristics: Employment change in county Interest rate spread over Libor charged on last precrisis loan Nonpublic; public w/o access to bond market; public with access to bond market

32 Testing Whether Measure of Lender Health is Uncorrelated with Unobserved Firm Characteristics: Khwaja and Mian (2008) Limit sample to firms that got a loan during the crisis and had multiple lenders before crisis. Regress change in lending in each borrower-lender pair during the crisis on the bank health measure and a full set of borrower fixed effects. See if results are different from same regression leaving out the borrower fixed effects.

33 From: Chodorow-Reich, The Employment Effects of Credit Market Disruptions

34 Specification: Loan Market Outcomes Can think of this as a 1 st stage (but it s not).

35 Loan Market Outcomes Sample Period: October 2008-June 2009 Uses full Dealscan sample (4000+ observations)

36 From: Chodorow-Reich, The Employment Effects of Credit Market Disruptions

37 Specification: Employment Outcomes Estimating the reduced form. Now using just the matched sample (so that he knows what bank the firm is attached to).

38 Many More Firm-level Controls: Dependent variable for 2 yrs. before the crisis. Average change in employment in the county where the firm operates. Fixed effect for 3 size bins. Fixed effect for 3 bond access bins. Firm age.

39 From: Chodorow-Reich, The Employment Effects of Credit Market Disruptions

40 Heterogeneous Treatment Effects: Interact loan supply variable with size and bondmarket access.

41 From: Chodorow-Reich, The Employment Effects of Credit Market Disruptions

42 From: Chodorow-Reich, The Employment Effects of Credit Market Disruptions

43 2007Q4 2008Q3 2008Q3 2010Q3 Other Time Periods:

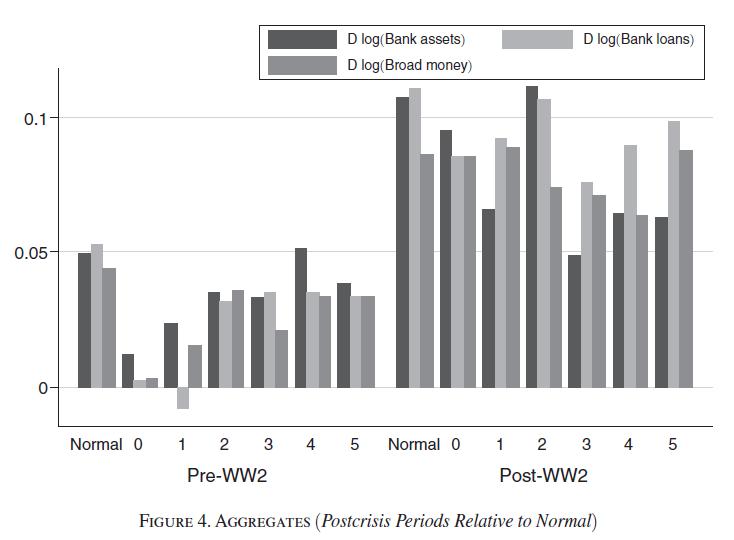

44

45 What happens when C-R does 2SLS? (FN 46) That is, regress employment growth on whether a firm got a loan, instrumenting for loan outcome with a measure of bank health? Enormous effect. Possible explanations? Does this make you nervous?

46 Placebo Tests Use the same loan supply measure (that is from ) But change sample of dependent variable. Consider 2005Q2 2007Q2 and 2001Q3 2002Q3.

47

48 Aggregating the Effects First, consider within sample. Assume every firm faced the bank health of the lender in the τ th percentile.

49 Aggregating the Effects (Continued) To move to the population, need to consider that only 2/3 of employment decline came from firms with fewer than 1000 employees. So that decreases contribution of credit disruption. Also need to consider general equilibrium effects. Chodorow-Reich has a model to spell out the issues in an appendix.

50 Evaluation

51 IV. SCHULARICK AND TAYLOR, CREDIT BOOMS GONE BUST: MONETARY POLICY, LEVERAGE CYCLES, AND FINANCIAL CRISES,

52 Three Questions Are there long-run trends in money and credit? How have the responses of money and credit to financial crises changed over time? What role do credit and money play as a cause of financial crises?

53 Data 14 advanced countries, , annual data. Series: Aggregate bank loans Total balance sheet size of the banking sector (assets) Narrow money (M0 or M1); broad money (M2 or M3) Macro variables: real GDP, stock prices, I Sources?

54 From: Jordà-Schularick-Taylor Macrohistory Database, Documentation

55 Stylized Bank Balance Sheet Assets Loans Securities Cash Reserves Liabilities and Owners Equity Deposits Bank Debt Capital

56 Question 1: What are long-run trends in money and credit?

57

58 How do Schularick and Taylor calculate trends?

59

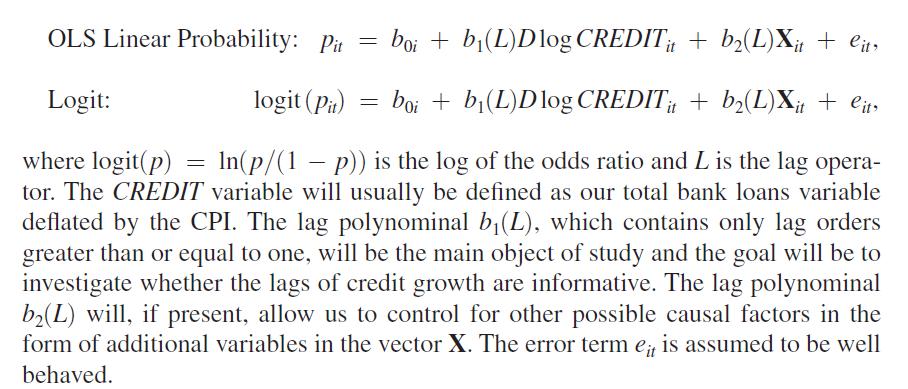

60 Stylized Bank Balance Sheet Assets Loans Securities Cash Reserves Liabilities and Owners Equity Deposits Bank Debt Capital

61 Stylized Facts Credit rose faster than money (deposits) post-world War II. Driven by an increase in funding through bank debt. Implications? Evaluation?

62 Question 2: What happens to money, credit, and output after financial crises?

63 How do they choose dates? Questions or qualms?

64

65

66 Discussion

67 Question 3: Do credit booms lead to financial crises?

68 Specification

69 Is this a convincing test of the importance of credit in causing crises? Calling this a forecasting exercise doesn t get around issues of OVB.

70 Possible Omitted Variable Bias Stories Rapid money growth leads to inflation which leads to monetary contraction and crises. House price rises lead to credit expansion and bursting bubbles. Bursting bubbles could cause crises directly. Financial innovation leads to both credit expansion and irresponsible behavior. Perhaps it is the irresponsible behavior that causes crises.

71

72

73

74

75

76 Evaluation There is a correlation between crises and credit expansion. It doesn t go away when obvious controls are included. We are a long way still from proving credit expansion causes crises.

77 Concluding Comments

LECTURE 11 The Effects of Credit Contraction and Financial Crises: Credit Market Disruptions. November 28, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 11 The Effects of Credit Contraction and Financial Crises: Credit Market Disruptions November 28, 2018 I. OVERVIEW AND GENERAL ISSUES Effects

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 11 The Effects of Credit Contraction and Financial Crises: Credit Market Disruptions November 28, 2018 I. OVERVIEW AND GENERAL ISSUES Effects

Discussion of The Employment Effects of Credit Market Disruptions: Firm-level Evidence from the Financial Crisis by Gabriel Chodorow-Reich

Discussion of The Employment Effects of Credit Market Disruptions: Firm-level Evidence from the 2008-09 Financial Crisis by Gabriel Chodorow-Reich Discussion by Bob Hall NBER ME Program Meeting Finance

Discussion of The Employment Effects of Credit Market Disruptions: Firm-level Evidence from the 2008-09 Financial Crisis by Gabriel Chodorow-Reich Discussion by Bob Hall NBER ME Program Meeting Finance

LECTURE 5 The Effects of Fiscal Changes: Cross-Section Evidence. September 21, 2016

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 5 The Effects of Fiscal Changes: Cross-Section Evidence September 21, 2016 I. OVERVIEW OF STATE-BASED STUDIES OF THE IMPACT OF FISCAL CHANGES

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 5 The Effects of Fiscal Changes: Cross-Section Evidence September 21, 2016 I. OVERVIEW OF STATE-BASED STUDIES OF THE IMPACT OF FISCAL CHANGES

LECTURE 6 The Effects of Fiscal Changes: Cross-Section Evidence. September 26, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 6 The Effects of Fiscal Changes: Cross-Section Evidence September 26, 2018 Office Hours No office hours this Thursday (9/27). Office hours

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 6 The Effects of Fiscal Changes: Cross-Section Evidence September 26, 2018 Office Hours No office hours this Thursday (9/27). Office hours

HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE

DISCUSSION OF: HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE BY MIAN, SUFI AND VERNER Emi Nakamura Columbia University December 2015 Nakamura Inflation Expectations December 2015 1 / 24 Could a credit boom

DISCUSSION OF: HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE BY MIAN, SUFI AND VERNER Emi Nakamura Columbia University December 2015 Nakamura Inflation Expectations December 2015 1 / 24 Could a credit boom

LECTURE 9 The Effects of Credit Contraction and Financial Crises: Balance Sheet and Cash Flow Effects. October 24, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 9 The Effects of Credit Contraction and Financial Crises: Balance Sheet and Cash Flow Effects October 24, 2018 I. OVERVIEW AND GENERAL

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 9 The Effects of Credit Contraction and Financial Crises: Balance Sheet and Cash Flow Effects October 24, 2018 I. OVERVIEW AND GENERAL

Professor Christina Romer. LECTURE 21 FISCAL POLICY April 10, 2018

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 21 FISCAL POLICY April 10, 2018 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 21 FISCAL POLICY April 10, 2018 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Professor Christina Romer. LECTURE 22 FISCAL POLICY April 14, 2016

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 22 FISCAL POLICY April 14, 2016 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 22 FISCAL POLICY April 14, 2016 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16 FISCAL POLICY IN THE GREAT RECESSION MARCH 19, 2018 I. OVERVIEW II. ECONOMIC STIMULUS ACT

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16 FISCAL POLICY IN THE GREAT RECESSION MARCH 19, 2018 I. OVERVIEW II. ECONOMIC STIMULUS ACT

Dollar Funding and the Lending Behavior of Global Banks

Dollar Funding and the Lending Behavior of Global Banks Victoria Ivashina (with David Scharfstein and Jeremy Stein) Facts US dollar assets of foreign banks are very large - Foreign banks play a major role

Dollar Funding and the Lending Behavior of Global Banks Victoria Ivashina (with David Scharfstein and Jeremy Stein) Facts US dollar assets of foreign banks are very large - Foreign banks play a major role

When Credit Bites Back: Leverage, Business Cycles, and Crises

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

Professor Christina Romer. LECTURE 22 FISCAL POLICY April 14, 2016

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 22 FISCAL POLICY April 14, 2016 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 22 FISCAL POLICY April 14, 2016 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Financial Crises and Asset Prices. Tyler Muir June 2017, MFM

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

LECTURE 4 The Effects of Fiscal Changes: Government Spending. September 21, 2011

Economics 210c/236a Fall 2011 Christina Romer David Romer LECTURE 4 The Effects of Fiscal Changes: Government Spending September 21, 2011 I. INTRODUCTION Theoretical Considerations (I) A traditional Keynesian

Economics 210c/236a Fall 2011 Christina Romer David Romer LECTURE 4 The Effects of Fiscal Changes: Government Spending September 21, 2011 I. INTRODUCTION Theoretical Considerations (I) A traditional Keynesian

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

Credit-Induced Boom and Bust

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

Credit-Induced Boom and Bust Marco Di Maggio (Columbia) and Amir Kermani (UC Berkeley) 10th CSEF-IGIER Symposium on Economics and Institutions June 25, 2014 Prof. Marco Di Maggio 1 Motivation The Great

Firm Debt Outcomes in Crises: The Role of Lending and. Underwriting Relationships

Firm Debt Outcomes in Crises: The Role of Lending and Underwriting Relationships Manisha Goel Michelle Zemel Pomona College Very Preliminary See https://research.pomona.edu/michelle-zemel/research/ for

Firm Debt Outcomes in Crises: The Role of Lending and Underwriting Relationships Manisha Goel Michelle Zemel Pomona College Very Preliminary See https://research.pomona.edu/michelle-zemel/research/ for

What determines the international transmission of monetary policy through the syndicated loan market? 1

What determines the international transmission of monetary policy through the syndicated loan market? 1 Asli Demirgüç-Kunt World Bank Bálint L. Horváth University of Bristol Harry Huizinga Tilburg University

What determines the international transmission of monetary policy through the syndicated loan market? 1 Asli Demirgüç-Kunt World Bank Bálint L. Horváth University of Bristol Harry Huizinga Tilburg University

Effects of Bank Lending Shocks on Real Activity: Evidence from a Financial Crisis

Effects of Bank Lending Shocks on Real Activity: Evidence from a Financial Crisis Emanuela Giacomini a *, Xiaohong (Sara) Wang a a Graduate School of Business, University of Florida, Gainesville, FL 32611-7168,

Effects of Bank Lending Shocks on Real Activity: Evidence from a Financial Crisis Emanuela Giacomini a *, Xiaohong (Sara) Wang a a Graduate School of Business, University of Florida, Gainesville, FL 32611-7168,

Syndicated loan spreads and the composition of the syndicate

Banking and Corporate Governance Lab Seminar, January 16, 2014 Syndicated loan spreads and the composition of the syndicate by Lim, Minton, Weisbach (JFE, 2014) Presented by Hyun-Dong (Andy) Kim Section

Banking and Corporate Governance Lab Seminar, January 16, 2014 Syndicated loan spreads and the composition of the syndicate by Lim, Minton, Weisbach (JFE, 2014) Presented by Hyun-Dong (Andy) Kim Section

The Samurai Bond: Credit Supply and Economic Growth in Pre-War Japan

The Samurai Bond: Credit Supply and Economic Growth in Pre-War Japan Sergi Basco Universitat Autonoma Barcelona John Tang Australian National University Bank of Spain Economic History Seminar 5 October

The Samurai Bond: Credit Supply and Economic Growth in Pre-War Japan Sergi Basco Universitat Autonoma Barcelona John Tang Australian National University Bank of Spain Economic History Seminar 5 October

Financial Cycles and Credit Growth Across Countries

Financial Cycles and Credit Growth Across Countries By Nuno Coimbra and Helene Rey Credit growth is an ubiquitous variable in the literature on crises and financial stability. Crises tend to be credit

Financial Cycles and Credit Growth Across Countries By Nuno Coimbra and Helene Rey Credit growth is an ubiquitous variable in the literature on crises and financial stability. Crises tend to be credit

Bank Capital and Lending: Evidence from Syndicated Loans

Bank Capital and Lending: Evidence from Syndicated Loans Yongqiang Chu, Donghang Zhang, and Yijia Zhao This Version: June, 2014 Abstract Using a large sample of bank-loan-borrower matched dataset of individual

Bank Capital and Lending: Evidence from Syndicated Loans Yongqiang Chu, Donghang Zhang, and Yijia Zhao This Version: June, 2014 Abstract Using a large sample of bank-loan-borrower matched dataset of individual

Professor Christina Romer. LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018 I. OVERVIEW II. THE MONEY MARKET, THE FEDERAL RESERVE, AND INTEREST

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018 I. OVERVIEW II. THE MONEY MARKET, THE FEDERAL RESERVE, AND INTEREST

Economic Watch Deleveraging after the burst of a credit-bubble Alfonso Ugarte / Akshaya Sharma / Rodolfo Méndez

Economic Watch Deleveraging after the burst of a credit-bubble Alfonso Ugarte / Akshaya Sharma / Rodolfo Méndez (Global Modeling & Long-term Analysis Unit) Madrid, December 5, 2017 Index 1. Introduction

Economic Watch Deleveraging after the burst of a credit-bubble Alfonso Ugarte / Akshaya Sharma / Rodolfo Méndez (Global Modeling & Long-term Analysis Unit) Madrid, December 5, 2017 Index 1. Introduction

Short-term debt and financial crises: What we can learn from U.S. Treasury supply

Short-term debt and financial crises: What we can learn from U.S. Treasury supply Arvind Krishnamurthy Northwestern-Kellogg and NBER Annette Vissing-Jorgensen Berkeley-Haas, NBER and CEPR 1. Motivation

Short-term debt and financial crises: What we can learn from U.S. Treasury supply Arvind Krishnamurthy Northwestern-Kellogg and NBER Annette Vissing-Jorgensen Berkeley-Haas, NBER and CEPR 1. Motivation

How did the Financial Crisis affect Bank Credit Supply and the Real Economy? Bank-Firm-level evidence from Austria

How did the 2008-9 Financial Crisis affect Bank Credit Supply and the Real Economy? Bank-Firm-level evidence from Austria Paul Pelzl a and María Teresa Valderrama b a Tinbergen Institute (TI), Vrije Universiteit

How did the 2008-9 Financial Crisis affect Bank Credit Supply and the Real Economy? Bank-Firm-level evidence from Austria Paul Pelzl a and María Teresa Valderrama b a Tinbergen Institute (TI), Vrije Universiteit

Comments on Foreign Effects of Higher U.S. Interest Rates. James D. Hamilton. University of California at San Diego.

1 Comments on Foreign Effects of Higher U.S. Interest Rates James D. Hamilton University of California at San Diego December 15, 2017 This is a very interesting and ambitious paper. The authors are trying

1 Comments on Foreign Effects of Higher U.S. Interest Rates James D. Hamilton University of California at San Diego December 15, 2017 This is a very interesting and ambitious paper. The authors are trying

Discussion of Relationship and Transaction Lending in a Crisis

Discussion of Relationship and Transaction Lending in a Crisis Philipp Schnabl NYU Stern, CEPR, and NBER USC Conference December 14, 2013 Summary 1 Research Question How does relationship lending vary

Discussion of Relationship and Transaction Lending in a Crisis Philipp Schnabl NYU Stern, CEPR, and NBER USC Conference December 14, 2013 Summary 1 Research Question How does relationship lending vary

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS. Economics 134 Spring 2018 Professor David Romer LECTURE 19

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects Manju Puri (Duke) Jörg Rocholl (ESMT) Sascha Steffen (Mannheim) 3rd Unicredit Group Conference

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects Manju Puri (Duke) Jörg Rocholl (ESMT) Sascha Steffen (Mannheim) 3rd Unicredit Group Conference

LECTURE 3 The Effects of Monetary Changes: Vector Autoregressions. September 7, 2016

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 3 The Effects of Monetary Changes: Vector Autoregressions September 7, 2016 I. SOME BACKGROUND ON VARS A Two-Variable VAR Suppose the true

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 3 The Effects of Monetary Changes: Vector Autoregressions September 7, 2016 I. SOME BACKGROUND ON VARS A Two-Variable VAR Suppose the true

Lecture 4A: Empirical Literature on Banking Capital Shocks

Lecture 4A: Empirical Literature on Banking Capital Shocks Zhiguo He University of Chicago Booth School of Business September 2017, Gerzensee ntroduction Do shocks to bank capital matter for real economy?

Lecture 4A: Empirical Literature on Banking Capital Shocks Zhiguo He University of Chicago Booth School of Business September 2017, Gerzensee ntroduction Do shocks to bank capital matter for real economy?

Unconventional Monetary Policy and Bank Lending Relationships

Unconventional Monetary Policy and Bank Lending Relationships Christophe Cahn 1 Anne Duquerroy 1 William Mullins 2 1 Banque de France 2 University of Maryland BdF-BdI Workshop - June 9, 2017 1 / 43 Motivation

Unconventional Monetary Policy and Bank Lending Relationships Christophe Cahn 1 Anne Duquerroy 1 William Mullins 2 1 Banque de France 2 University of Maryland BdF-BdI Workshop - June 9, 2017 1 / 43 Motivation

The Employment Eects of Credit Market Disruptions: Firm-level Evidence from the Financial Crisis

The Employment Eects of Credit Market Disruptions: Firm-level Evidence from the 2008-09 Financial Crisis Gabriel Chodorow-Reich October 2012 Abstract This paper investigates the eect of bank lending frictions

The Employment Eects of Credit Market Disruptions: Firm-level Evidence from the 2008-09 Financial Crisis Gabriel Chodorow-Reich October 2012 Abstract This paper investigates the eect of bank lending frictions

Debt Overhang, Rollover Risk, and Investment in Europe

Debt Overhang, Rollover Risk, and Investment in Europe Ṣebnem Kalemli-Özcan, University of Maryland, CEPR and NBER Luc Laeven, ECB and CEPR David Moreno, University of Maryland September 2015, EC Post

Debt Overhang, Rollover Risk, and Investment in Europe Ṣebnem Kalemli-Özcan, University of Maryland, CEPR and NBER Luc Laeven, ECB and CEPR David Moreno, University of Maryland September 2015, EC Post

Financial Vulnerabilities, Macroeconomic Dynamics, and Monetary Policy

Financial Vulnerabilities, Macroeconomic Dynamics, and Monetary Policy DAVID AIKMAN, ANDREAS LEHNERT, NELLIE LIANG, MICHELE MODUGNO 19 MAY, 2017 T H E V I E W S E X P R E S S E D A R E O U R O W N A N

Financial Vulnerabilities, Macroeconomic Dynamics, and Monetary Policy DAVID AIKMAN, ANDREAS LEHNERT, NELLIE LIANG, MICHELE MODUGNO 19 MAY, 2017 T H E V I E W S E X P R E S S E D A R E O U R O W N A N

Large Banks and the Transmission of Financial Shocks

Large Banks and the Transmission of Financial Shocks Vitaly M. Bord Harvard University Victoria Ivashina Harvard University and NBER Ryan D. Taliaferro Acadian Asset Management December 15, 2014 (Preliminary

Large Banks and the Transmission of Financial Shocks Vitaly M. Bord Harvard University Victoria Ivashina Harvard University and NBER Ryan D. Taliaferro Acadian Asset Management December 15, 2014 (Preliminary

Asset Price Bubbles and Systemic Risk

Asset Price Bubbles and Systemic Risk Markus Brunnermeier, Simon Rother, Isabel Schnabel AFA 2018 Annual Meeting Philadelphia; January 7, 2018 Simon Rother (University of Bonn) Asset Price Bubbles and

Asset Price Bubbles and Systemic Risk Markus Brunnermeier, Simon Rother, Isabel Schnabel AFA 2018 Annual Meeting Philadelphia; January 7, 2018 Simon Rother (University of Bonn) Asset Price Bubbles and

SUGGESTED ANSWERS TO PROBLEM SET

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 1 1. a. The conditions indicate that we should consider the IS-MP model,

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 1 1. a. The conditions indicate that we should consider the IS-MP model,

The Underwriter Relationship and Corporate Debt Maturity

The Underwriter Relationship and Corporate Debt Maturity Indraneel Chakraborty Andrew MacKinlay May 11, 2018 Abstract Supply-side frictions impact corporate debt maturity choices. Similar to bank loan

The Underwriter Relationship and Corporate Debt Maturity Indraneel Chakraborty Andrew MacKinlay May 11, 2018 Abstract Supply-side frictions impact corporate debt maturity choices. Similar to bank loan

International Shock Transmission after the Lehman Brothers Collapse. Evidence from Syndicated Lending

MPRA Munich Personal RePEc Archive International Shock Transmission after the Lehman Brothers Collapse. Evidence from Syndicated Lending Ralph de Haas and Neeltje van Horen European Bank for Reconstruction

MPRA Munich Personal RePEc Archive International Shock Transmission after the Lehman Brothers Collapse. Evidence from Syndicated Lending Ralph de Haas and Neeltje van Horen European Bank for Reconstruction

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Labour Reallocation and Productivity Dynamics: Financial Causes, Real Consequences*

Labour Reallocation and Productivity Dynamics: Financial Causes, Real Consequences* Enisse Kharroubi 6th joint Conference by the Bank of Canada and the European Central Bank. The underwhelming global post-crisis

Labour Reallocation and Productivity Dynamics: Financial Causes, Real Consequences* Enisse Kharroubi 6th joint Conference by the Bank of Canada and the European Central Bank. The underwhelming global post-crisis

Discussion of A. Loeffler E. Segalla, G. Valitova & U. Vogel

Discussion of A. Loeffler E. Segalla, G. Valitova & U. Vogel Charles Banque de France Global Financial Linkages And Monetary Policy Transmission Conference Banque de France 30 June 2017 The views are those

Discussion of A. Loeffler E. Segalla, G. Valitova & U. Vogel Charles Banque de France Global Financial Linkages And Monetary Policy Transmission Conference Banque de France 30 June 2017 The views are those

Justin Wolfers University of Michigan and Brookings, CEPR, CESifo, IZA, NBER & PIIE

The Fiscal Multiplier in Japan Decomposing Local Fiscal Multipliers: Evidence from Japan by Taisuke Kameda, Ryoichi Nanba and Takayuki Tsuruga The expert survey on the size of Japan s fiscal multiplier

The Fiscal Multiplier in Japan Decomposing Local Fiscal Multipliers: Evidence from Japan by Taisuke Kameda, Ryoichi Nanba and Takayuki Tsuruga The expert survey on the size of Japan s fiscal multiplier

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

HOUSEHOLD DEBT, CORPORATE DEBT, AND THE REAL ECONOMY: SOME EMPIRICAL EVIDENCE

HOUSEHOLD DEBT, CORPORATE DEBT, AND THE REAL ECONOMY: SOME EMPIRICAL EVIDENCE Donghyun Park, Kwanho Shin, and Shu Tian NO. 567 December 2018 adb economics working paper series ASIAN DEVELOPMENT BANK ADB

HOUSEHOLD DEBT, CORPORATE DEBT, AND THE REAL ECONOMY: SOME EMPIRICAL EVIDENCE Donghyun Park, Kwanho Shin, and Shu Tian NO. 567 December 2018 adb economics working paper series ASIAN DEVELOPMENT BANK ADB

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

Credit Booms Gone Bust

Credit Booms Gone Bust Monetary Policy, Leverage Cycles and Financial Crises, 1870 2008 Moritz Schularick (Free University of Berlin) Alan M. Taylor (UC Davis & Morgan Stanley) Federal Reserve Bank of

Credit Booms Gone Bust Monetary Policy, Leverage Cycles and Financial Crises, 1870 2008 Moritz Schularick (Free University of Berlin) Alan M. Taylor (UC Davis & Morgan Stanley) Federal Reserve Bank of

Multinational Banks and the Global Financial Crisis

Weathering the Perfect Storm? Ralph De Haas 1 Iman Van Lelyveld 2 1 European Bank for Reconstruction and Development 2 De Nederlandsche Bank EBRD/G20/RBWC Conference on Cross-Border Banking in Emerging

Weathering the Perfect Storm? Ralph De Haas 1 Iman Van Lelyveld 2 1 European Bank for Reconstruction and Development 2 De Nederlandsche Bank EBRD/G20/RBWC Conference on Cross-Border Banking in Emerging

China s macroeconomic imbalances: causes and consequences. John Knight and Wang Wei

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence. September 19, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence September 19, 2018 I. INTRODUCTION Theoretical Considerations (I) A traditional Keynesian

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence September 19, 2018 I. INTRODUCTION Theoretical Considerations (I) A traditional Keynesian

REIT and Commercial Real Estate Returns: A Postmortem of the Financial Crisis

2015 V43 1: pp. 8 36 DOI: 10.1111/1540-6229.12055 REAL ESTATE ECONOMICS REIT and Commercial Real Estate Returns: A Postmortem of the Financial Crisis Libo Sun,* Sheridan D. Titman** and Garry J. Twite***

2015 V43 1: pp. 8 36 DOI: 10.1111/1540-6229.12055 REAL ESTATE ECONOMICS REIT and Commercial Real Estate Returns: A Postmortem of the Financial Crisis Libo Sun,* Sheridan D. Titman** and Garry J. Twite***

Main Points: Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable

NBER July 2018 Main Points: 2 Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable US housing bubble and the crisis of

NBER July 2018 Main Points: 2 Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable US housing bubble and the crisis of

Market Quality, Financial Crises, and TFP Growth in the US:

Market Quality, Financial Crises, and TFP Growth in the US: 1840 2014 Kevin R. James Systemic Risk Centre London School of Economics k.james1@lse.ac.uk Akshay Kotak Said School Oxford University akshay.kotak@sbs.ox.ac.uk

Market Quality, Financial Crises, and TFP Growth in the US: 1840 2014 Kevin R. James Systemic Risk Centre London School of Economics k.james1@lse.ac.uk Akshay Kotak Said School Oxford University akshay.kotak@sbs.ox.ac.uk

The Effects of Housing Price on the Banking Sector Performance* Evidence from MSA data in the US

196 2017 The Effects of Housing Price on the Banking Sector Performance* Evidence from MSA data in the US Sung Wook JOH** and Seongjun JEONG** Abstract This paper examines the factors affecting bank activities

196 2017 The Effects of Housing Price on the Banking Sector Performance* Evidence from MSA data in the US Sung Wook JOH** and Seongjun JEONG** Abstract This paper examines the factors affecting bank activities

Real Effects of the Sovereign Debt Crisis in Europe: Evidence from Syndicated Loans

Real Effects of the Sovereign Debt Crisis in Europe: Evidence from Syndicated Loans Viral V. Acharya a, Tim Eisert b, Christian Eufinger b, Christian Hirsch c a New York University, CEPR, and NBER b Goethe

Real Effects of the Sovereign Debt Crisis in Europe: Evidence from Syndicated Loans Viral V. Acharya a, Tim Eisert b, Christian Eufinger b, Christian Hirsch c a New York University, CEPR, and NBER b Goethe

LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing. October 10, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Macroeconomic Effects from Government Purchases and Taxes. Robert J. Barro and Charles J. Redlick Harvard University

Macroeconomic Effects from Government Purchases and Taxes Robert J. Barro and Charles J. Redlick Harvard University Empirical evidence on response of real GDP and other economic aggregates to added government

Macroeconomic Effects from Government Purchases and Taxes Robert J. Barro and Charles J. Redlick Harvard University Empirical evidence on response of real GDP and other economic aggregates to added government

Financial Integration, Housing and Economic Volatility

Financial Integration, Housing and Economic Volatility by Elena Loutskina and Philip Strahan 48th Annual Conference on Bank Structure and Competition May 9th, 2012 We Care About Housing Market Roots of

Financial Integration, Housing and Economic Volatility by Elena Loutskina and Philip Strahan 48th Annual Conference on Bank Structure and Competition May 9th, 2012 We Care About Housing Market Roots of

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Discussion: Bank lending during the financial crisis of 2008

Discussion: Bank lending during the financial crisis of 2008 Emilia Bonaccorsi di Patti Banca d Italia 3rd UNICREDIT GROUP CONFERENCE ON BANKING AND FINANCE The opinions expressed do not necessarily reflect

Discussion: Bank lending during the financial crisis of 2008 Emilia Bonaccorsi di Patti Banca d Italia 3rd UNICREDIT GROUP CONFERENCE ON BANKING AND FINANCE The opinions expressed do not necessarily reflect

Quantitative Easing and Bank Lending: Evidence from Japan

Quantitative Easing and Bank Lending: Evidence from Japan David Bowman Fang Cai Sally Davies Steven Kamin Federal Reserve Board October 6, 2014 The views in this paper are solely the responsibility of

Quantitative Easing and Bank Lending: Evidence from Japan David Bowman Fang Cai Sally Davies Steven Kamin Federal Reserve Board October 6, 2014 The views in this paper are solely the responsibility of

The Domestic Credit Supply Response to International Bank Deleveraging: Is Asia Different?

WP/12/258 The Domestic Credit Supply Response to International Bank Deleveraging: Is Asia Different? Shekhar Aiyar and Sonali Jain-Chandra 2012 International Monetary Fund WP/12/258 IMF Working Paper Asia

WP/12/258 The Domestic Credit Supply Response to International Bank Deleveraging: Is Asia Different? Shekhar Aiyar and Sonali Jain-Chandra 2012 International Monetary Fund WP/12/258 IMF Working Paper Asia

Discussion of The Cost of Macroprudential Policy by Bjorn Richter, Moritz Schularick, Ilhyock Shim

Discussion of The Cost of Macroprudential Policy by Bjorn Richter, Moritz Schularick, Ilhyock Shim Ozge Akinci Federal Reserve Bank of New York International Symposium on Macroeconomics The views expressed

Discussion of The Cost of Macroprudential Policy by Bjorn Richter, Moritz Schularick, Ilhyock Shim Ozge Akinci Federal Reserve Bank of New York International Symposium on Macroeconomics The views expressed

Speculative Asset Bubbles: The Primary Drivers of Systemic Banking Crises in Post-war Advanced Economies

Speculative Asset Bubbles: The Primary Drivers of Systemic Banking Crises in Post-war Advanced Economies Presentation at the 2019 ASSA Meetings January 4th, 2019 Saktinil Roy Athabasca University Motivation

Speculative Asset Bubbles: The Primary Drivers of Systemic Banking Crises in Post-war Advanced Economies Presentation at the 2019 ASSA Meetings January 4th, 2019 Saktinil Roy Athabasca University Motivation

Cyclicality of Credit Supply: Firm Level Evidence

Cyclicality of Credit Supply: Firm Level Evidence The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Becker, Bo, and Victoria

Cyclicality of Credit Supply: Firm Level Evidence The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Becker, Bo, and Victoria

The Real Effects of Credit Line Drawdowns

The Real Effects of Credit Line Drawdowns Jose M. Berrospide Federal Reserve Board Ralf R. Meisenzahl Federal Reserve Board January 31, 2013 Abstract Do firms use credit line drawdowns to finance investment?

The Real Effects of Credit Line Drawdowns Jose M. Berrospide Federal Reserve Board Ralf R. Meisenzahl Federal Reserve Board January 31, 2013 Abstract Do firms use credit line drawdowns to finance investment?

Volume Author/Editor: Kenneth Singleton, editor. Volume URL:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Japanese Monetary Policy Volume Author/Editor: Kenneth Singleton, editor Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Japanese Monetary Policy Volume Author/Editor: Kenneth Singleton, editor Volume Publisher:

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market Seung Jung Lee FRB Lucy Qian Liu IMF Viktors Stebunovs FRB BIS CCA Research Conference on "Low interest rates,

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market Seung Jung Lee FRB Lucy Qian Liu IMF Viktors Stebunovs FRB BIS CCA Research Conference on "Low interest rates,

ECON Intermediate Macroeconomic Theory

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

Professor Christina Romer. LECTURE 24 INFLATION AND THE RETURN OF OUTPUT TO POTENTIAL April 21, 2016

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 24 INFLATION AND THE RETURN OF OUTPUT TO POTENTIAL April 21, 2016 I. KEY IDEAS II. THE BEHAVIOR OF INFLATION A. Nominal rigidities

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 24 INFLATION AND THE RETURN OF OUTPUT TO POTENTIAL April 21, 2016 I. KEY IDEAS II. THE BEHAVIOR OF INFLATION A. Nominal rigidities

Class Notes. Chapter 5 Saving and Investment in the Open Economy Learning Objectives

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

Liquidity Insurance in Macro. Heitor Almeida University of Illinois at Urbana- Champaign

Liquidity Insurance in Macro Heitor Almeida University of Illinois at Urbana- Champaign Motivation Renewed attention to financial frictions in general and role of banks in particular Existing models model

Liquidity Insurance in Macro Heitor Almeida University of Illinois at Urbana- Champaign Motivation Renewed attention to financial frictions in general and role of banks in particular Existing models model

Battle Over Japan's Mortgage Market Raises Default Risks

Battle Over Japan's Mortgage Market Raises Default Risks Global Fixed Income Research Naoko Nemoto Managing Director Tokyo (81) 3 4550 8720 naoko_nemoto@ standardandpoors.com Standard & Poor's 55 Water

Battle Over Japan's Mortgage Market Raises Default Risks Global Fixed Income Research Naoko Nemoto Managing Director Tokyo (81) 3 4550 8720 naoko_nemoto@ standardandpoors.com Standard & Poor's 55 Water

MACROECONOMICS AND FINANCIAL MARKETS

MACROECONOMICS AND FINANCIAL MARKETS Veronica Guerrieri and Harald Uhlig Discussion by Luigi Bocola Northwestern University and FRB Minneapolis The views expressed herein are those of the author and not

MACROECONOMICS AND FINANCIAL MARKETS Veronica Guerrieri and Harald Uhlig Discussion by Luigi Bocola Northwestern University and FRB Minneapolis The views expressed herein are those of the author and not

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

Bank Ratings and Lending Supply: Evidence from Sovereign Downgrades

Bank Ratings and Lending Supply: Evidence from Sovereign Downgrades Manuel Adelino Duke University Miguel A. Ferreira Nova School of Business and Economics, CEPR, and ECGI We study the causal effect of

Bank Ratings and Lending Supply: Evidence from Sovereign Downgrades Manuel Adelino Duke University Miguel A. Ferreira Nova School of Business and Economics, CEPR, and ECGI We study the causal effect of

Do firms benefit from their relationships with. credit unions during dire times?

Do firms benefit from their relationships with credit unions during dire times? Leila Aghabarari Andre Guettler Mahvish Naeem Bernardus Van Doornik ** Credit unions (CUs) are unique financial intermediaries

Do firms benefit from their relationships with credit unions during dire times? Leila Aghabarari Andre Guettler Mahvish Naeem Bernardus Van Doornik ** Credit unions (CUs) are unique financial intermediaries

The impact of CDS trading on the bond market: Evidence from Asia

Capital Market Research Forum 9/2554 By Dr. Ilhyock Shim Senior Economist Representative Office for Asia and the Pacific Bank for International Settlements 7 September 2011 The impact of CDS trading on

Capital Market Research Forum 9/2554 By Dr. Ilhyock Shim Senior Economist Representative Office for Asia and the Pacific Bank for International Settlements 7 September 2011 The impact of CDS trading on

The Loan Covenant Channel: How Bank Health Transmits to the Real Economy

The Loan Covenant Channel: How Bank Health Transmits to the Real Economy Gabriel Chodorow-Reich Harvard University and NBER Antonio Falato Federal Reserve Board April 2017 Abstract We document the importance

The Loan Covenant Channel: How Bank Health Transmits to the Real Economy Gabriel Chodorow-Reich Harvard University and NBER Antonio Falato Federal Reserve Board April 2017 Abstract We document the importance

ASSET PRICES IN ECONOMIC THEORY 1

26 1 Ing. Silvia Gantnerová, National Bank of Slovakia Asset prices, though not a goal or instrument of monetary policy, are nonetheless important for its realization, since they are a component of its

26 1 Ing. Silvia Gantnerová, National Bank of Slovakia Asset prices, though not a goal or instrument of monetary policy, are nonetheless important for its realization, since they are a component of its

MA Advanced Macroeconomics 3. Examples of VAR Studies

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

What s Driving Deleveraging? Evidence from the Survey of Consumer Finances

What s Driving Deleveraging? Evidence from the 2007-2009 Survey of Consumer Finances Karen Dynan Brookings Institution Wendy Edelberg Congressional Budget Office These slides were prepared for a presentation

What s Driving Deleveraging? Evidence from the 2007-2009 Survey of Consumer Finances Karen Dynan Brookings Institution Wendy Edelberg Congressional Budget Office These slides were prepared for a presentation

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking?

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

When Credit Bites Back: Leverage, Business Cycles, and Crises

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

Financial Crises and the Great Recession

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

flow-based borrowing constraints and macroeconomic fluctuations

flow-based borrowing constraints and macroeconomic fluctuations Thomas Drechsel (LSE) Annual Congress of the EEA University of Cologne 27 August 2018 in a nutshell I What do the dynamics of firm borrowing

flow-based borrowing constraints and macroeconomic fluctuations Thomas Drechsel (LSE) Annual Congress of the EEA University of Cologne 27 August 2018 in a nutshell I What do the dynamics of firm borrowing

The Lure of Alternative Credit Opportunities in Global Credit Investing

The Lure of Alternative Credit Opportunities in Global Credit Investing David Snow, Privcap: Today we re joined by Glenn August of Oak Hill Advisors. Glenn, welcome to PrivCap. Thanks for being here. Glenn

The Lure of Alternative Credit Opportunities in Global Credit Investing David Snow, Privcap: Today we re joined by Glenn August of Oak Hill Advisors. Glenn, welcome to PrivCap. Thanks for being here. Glenn

NBER WORKING PAPER SERIES HOW MUCH DO IDIOSYNCRATIC BANK SHOCKS AFFECT INVESTMENT? EVIDENCE FROM MATCHED BANK-FIRM LOAN DATA

NBER WORKING PAPER SERIES HOW MUCH DO IDIOSYNCRATIC BANK SHOCKS AFFECT INVESTMENT? EVIDENCE FROM MATCHED BANK-FIRM LOAN DATA Mary Amiti David E. Weinstein Working Paper 18890 http://www.nber.org/papers/w18890

NBER WORKING PAPER SERIES HOW MUCH DO IDIOSYNCRATIC BANK SHOCKS AFFECT INVESTMENT? EVIDENCE FROM MATCHED BANK-FIRM LOAN DATA Mary Amiti David E. Weinstein Working Paper 18890 http://www.nber.org/papers/w18890

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Macroeconomics of Finance

Macroeconomics of Finance Joanna Mackiewicz-Łyziak Lecture 12 Literature Borio C., 2012, The financial cycle and macroeconomics: What have we learnt?, BIS Working Papers No. 395. Business cycles Business

Macroeconomics of Finance Joanna Mackiewicz-Łyziak Lecture 12 Literature Borio C., 2012, The financial cycle and macroeconomics: What have we learnt?, BIS Working Papers No. 395. Business cycles Business

Module 31. Monetary Policy and the Interest Rate. What you will learn in this Module:

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

The yellow highlighted areas are bear markets with NO recession.

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Housing Price Booms and Crowding-Out Effects in Bank Lending

Housing Price Booms and Crowding-Out Effects in Bank Lending Indraneel Chakraborty Itay Goldstein Andrew MacKinlay November 26, 2017 Abstract Analyzing the period between 1988 and 2006, we document that

Housing Price Booms and Crowding-Out Effects in Bank Lending Indraneel Chakraborty Itay Goldstein Andrew MacKinlay November 26, 2017 Abstract Analyzing the period between 1988 and 2006, we document that