UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

|

|

|

- Lester Conrad Thomas

- 6 years ago

- Views:

Transcription

1 UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY A. The pre-depression era versus the early postwar decades 1. The old facts 2. The new facts 3. Why didn t the economy become more stable? B. The early postwar decades versus The facts: the Great Moderation 2. Why did the economy become more stable? II. INFLATION AND MONETARY POLICY OVER THE POSTWAR PERIOD A. Inflation 1. The big picture: The rise and fall of inflation 2. Looking in more detail B. The role of monetary policy 1. Monetary policy and inflation 2. Issues that this raises III. THE RUN-UP TO THE GREAT RECESSION A. The 2001 recession B. The rise and fall of house prices C. Financial distress D. The first stages of the downturn E. The initial policy response IV. CRISIS IN THE FALL OF 2008 AND EARLY 2009 A. Financial crisis in September 2008 B. Comparison with the start of the Great Depression C. Real decline D. International contagion E. Policy actions in the heart of the crisis F. Rapidly rising unemployment and (slightly) falling inflation V. THE SLOW RECOVERY A. The trough B. The pace of recovery C. Possible reasons for the slow recovery VI. A LITTLE ABOUT THE EUROPEAN CRISIS

2 Economics 134 Spring 2018 David Romer LECTURE 3 Postwar Fluctuations and the Great Recession January 24, 2018

3 I. CHANGES IN MACROECONOMIC VOLATILITY

4 Traditional data series showed a dramatic stabilization of the economy.

5 Macroeconomic volatility in the early postwar decades was very similar to before the Depression (or before WWI).

6 The Rise of Stabilization Policy Keynes s General Theory (1936). The maturation of the Federal Reserve. The greater size of government (leading to automatic stabilizers and more scope for discretionary fiscal policy). Deposit insurance. Formal government commitment to stabilization: It is the responsibility of the Federal Government to promote maximum employment, production, and purchasing power (Employment Act of 1946).

7 Possible Reasons that the Rise of Stabilization Policy Did Not Cause the Economy to Quickly Become Much More Stable

8 Macroeconomic volatility fell dramatically around the mid-1980s.

9 20 Real GDP Growth 1947:2-2007:4 Real GDP Growth (Percent) II 1949-III 1951-IV 1954-I 1956-II 1958-III 1960-IV 1963-I 1965-II 1967-III 1969-IV 1972-I 1974-II 1976-III 1978-IV 1981-I 1983-II 1985-III 1987-IV 1990-I 1992-II 1994-III 1996-IV 1999-I 2001-II 2003-III 2005-IV The fall in volatility in the mid-1980s shows up clearly in real GDP growth.

10 Possible Reasons that the Economy Was Much More Stable from Roughly 1985 to Roughly 2005 (the Great Moderation )

11 II. INFLATION AND MONETARY POLICY OVER THE POSTWAR PERIOD

12 Inflation rose irregularly over the 1960s and 1970s, fell dramatically in the early 1980s, and has remained low.

13 Some Issues Raised by Postwar Inflation Behavior Why was monetary policy conducted in a way that led to a rising inflation? What changed around 1980? What is the link (if any) between the rising inflation and the failure of the real economy to become more stable? What is the link (if any) between the conquest of inflation and the Great Moderation?

14 The history of postwar monetary policy is complicated.

15 III. THE RUN-UP TO THE GREAT RECESSION

16 The recession was the smallest since 1947.

17 Interest rates didn t rise much before the 2001 recession.

18 NASDAQ Composite Index Tech bubble burst in early 2000.

19 House prices rose dramatically in the mid-2000s and then fell sharply.

20 Issues: How might the decline in house prices have affected the economy? Why was the aftermath of the bursting of housing bubble so much worse than the aftermath of the bursting of the tech bubble?

21 TED Spread Difference between the interest rates on short-term loans between banks (LIBOR) and short-term government debt (T-bills). It is a measure of credit risk.

22 TED spread spiked in August 2007.

23 Residential Construction Spending Residential construction began to fall in 2006.

24 Real GDP peaked in 2007Q4 and then fell moderately. Employment peaked in Jan and then fell, first slowly and then rapidly.

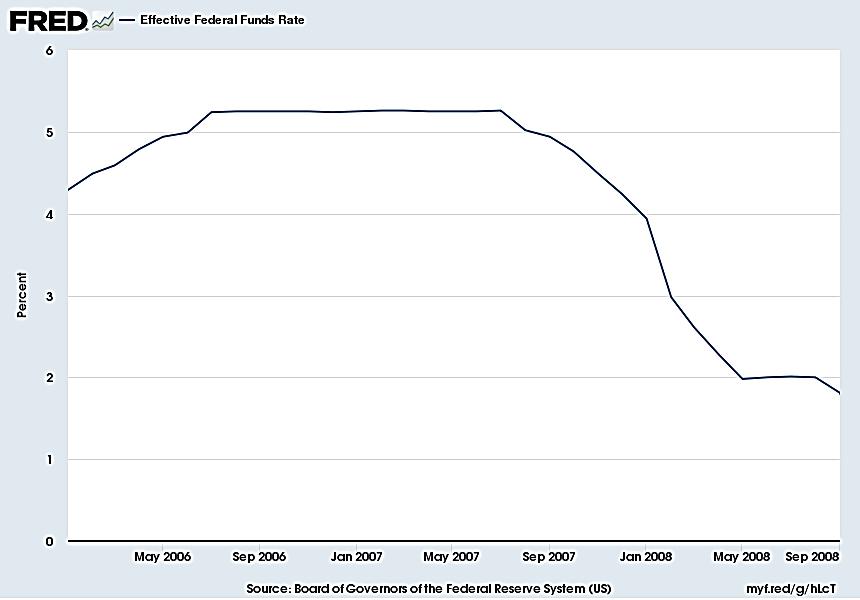

25 Major Policy Actions before September 2008 Fiscal policy: Economic Stimulus Act of 2008 (February) Monetary policy: Lower interest rates; various Fed special programs, and interventions to help troubled financial firms

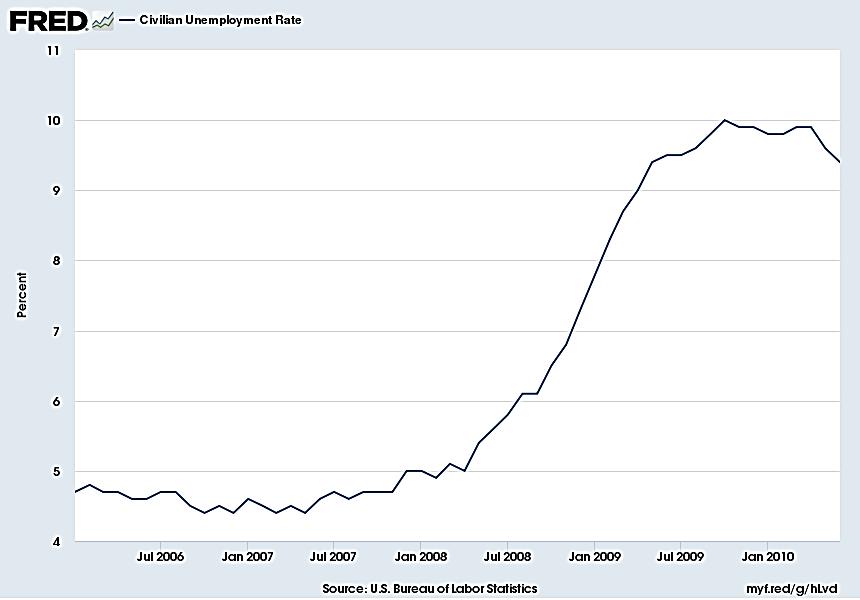

26

27 IV. CRISIS IN THE FALL OF 2008 AND EARLY 2009

28 Delinquency Rate on Single-Family Mortgages Percent /1/02 7/1/02 1/1/03 7/1/03 1/1/04 7/1/04 1/1/05 7/1/05 1/1/06 7/1/06 1/1/07 7/1/07 1/1/08 7/1/08 1/1/09 7/1/09 1/1/10 7/1/10 1/1/11 7/1/11 1/1/12 7/1/12

29

30 World Stock Prices, 1929 and 2008 Initial fall in stock prices was larger in than in

31 Initial rise in interest rate spreads was much larger in than in

32 World Industrial Output, 1929 and 2008 Initial fall in output in was similar to

33 GDP and employment plummeted in the second half of 2008 and early 2009.

34 IP fell early in US; rest of the world followed quickly.

35 The Policy Response Monetary policy: Federal funds rate lowered to almost zero (December 2008); quantitative easing (December 2008 and March 2009); more Fed special programs Financial rescue: AIG rescue and Fannie and Freddie takeover (September 2008); Troubled Asset Relief Program (TARP) (October 2008); stress test (May 2009) Fiscal policy: American Recovery and Reinvestment Act of 2009 (February 2009)

36

37 Unemployment

38 Okun s Law A shortfall of GDP growth from normal of 1 percentage point is usually associated with a rise in the unemployment rate of about ½ percentage point.

39 Okun s Law, Δu = -0.5*(GDP Growth 2.2) The rise in unemployment in 2009 was unusually large given the behavior of real GDP.

40 Core inflation fell during the recession, but not by as much as one might have expected given high unemployment.

41 V. THE SLOW RECOVERY

42 Real GDP reached its low in 2009Q2; employment in Feb

43 GDP never had a period of rapid growth, and never returned toward its previous path.

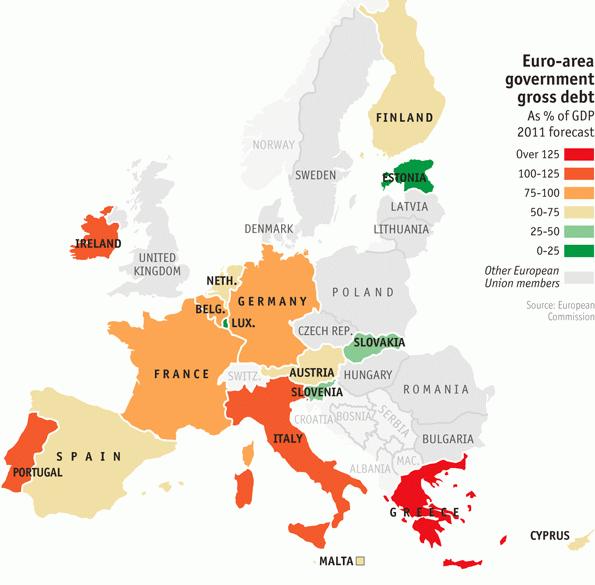

44 The unemployment rate stayed above 6% until Sept

The fall in unemployment in 2011 and 2012 was unusually large given")

45 Okun s Law, Δu = -0.5*(GDP Growth 2.2) The fall in unemployment in 2011 and 2012 was unusually large given the behavior of real GDP.

46 Possible Reasons for the Slow Recovery

47 Home Vacancy Rate

48 Does high debt depress consumer spending?

49 VI. A LITTLE ABOUT THE EUROPEAN CRISIS

50 Euro area GDP turned down again in 2011, and did not return to its pre-crisis peak until 2015.

51 Unemployment in Greece and Spain reached Depressionlike levels.

52 Unit Labor Costs across the Eurozone Labor costs rose rapidly in many European countries but not Germany.

53

54 30 10-Year Government Bond Yields Percent Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Germany Ireland Greece Spain France Italy Portugal United Kingdom The crisis spread from Greece to many other countries in late 2010.

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Economic Shocks: the Great Depression and Great Recession. Andy Bauer Senior Regional Economist October 19, 2017

Economic Shocks: the Great Depression and Great Recession Andy Bauer Senior Regional Economist October 19, 2017 Economic Shocks: the Great Depression and Great Recession Andy Bauer Senior Regional Economist

Economic Shocks: the Great Depression and Great Recession Andy Bauer Senior Regional Economist October 19, 2017 Economic Shocks: the Great Depression and Great Recession Andy Bauer Senior Regional Economist

Perspectives on the U.S. Economy

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Introduction and Economic Landscape. Vance Ginn Spring 2013

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

Introduction and Economic Landscape Vance Ginn Spring 2013 Introduction CV (underlined words typically are links or videos) Syllabus We will use Blackboard, which is where you will find the syllabus, important

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 11

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 11 THE ZERO LOWER BOUND IN PRACTICE FEBRUARY 26, 2018 I. INTRODUCTION II. TWO EPISODES AT THE ZERO

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 11 THE ZERO LOWER BOUND IN PRACTICE FEBRUARY 26, 2018 I. INTRODUCTION II. TWO EPISODES AT THE ZERO

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS. Economics 134 Spring 2018 Professor David Romer LECTURE 19

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

Economic and Housing Outlook 1. William Strauss, Senior Economist and Economic Advisor Federal Reserve Bank of Chicago. Economic and Housing Outlook

Economic and Housing Outlook Builder Chicago, IL May, William Strauss Senior Economist and Economic Advisor The Great Recession ended in June, but the economy expanded by just.% over the past year Real

Economic and Housing Outlook Builder Chicago, IL May, William Strauss Senior Economist and Economic Advisor The Great Recession ended in June, but the economy expanded by just.% over the past year Real

Globalization. International Financial (Chap. 8) and Monetary (Chap. 9) Relations

and Monetary (Chap. 9) Relations") Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

15 th. edition Gwartney Stroup Sobel Macpherson. First page. edition Gwartney Stroup Sobel Macpherson

Alternative Views of Fiscal Policy An Overview GWARTNEY STROUP SOBEL MACPHERSON Fiscal Policy, Incentives, and Secondary Effects Full Length Text Part: 3 Macro Only Text Part: 3 Chapter: 12 Chapter: 12

Alternative Views of Fiscal Policy An Overview GWARTNEY STROUP SOBEL MACPHERSON Fiscal Policy, Incentives, and Secondary Effects Full Length Text Part: 3 Macro Only Text Part: 3 Chapter: 12 Chapter: 12

Emerging from the Crisis

Emerging from the Crisis i Franklin Allen University of Pennsylvania Elena Carletti European University Institute Louvain-La-Neuve May 6, 2010 What caused the crisis? The conventional wisdom used to be

Emerging from the Crisis i Franklin Allen University of Pennsylvania Elena Carletti European University Institute Louvain-La-Neuve May 6, 2010 What caused the crisis? The conventional wisdom used to be

The sharp accumulation in government debt can t go on forever

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

To understand where the U.S. Economy is going, we need to understand where we have been

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Professor Christina Romer. LECTURE 22 FISCAL POLICY April 14, 2016

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 22 FISCAL POLICY April 14, 2016 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 22 FISCAL POLICY April 14, 2016 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Professor Christina Romer. LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018 I. OVERVIEW II. THE MONEY MARKET, THE FEDERAL RESERVE, AND INTEREST

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018 I. OVERVIEW II. THE MONEY MARKET, THE FEDERAL RESERVE, AND INTEREST

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

Professor Christina Romer. LECTURE 21 FISCAL POLICY April 10, 2018

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 21 FISCAL POLICY April 10, 2018 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 21 FISCAL POLICY April 10, 2018 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Twin Problems: Employment and Consumer Spending

Twin Problems: Employment and Consumer Spending September 1, 11 Asha G. Bangalore agb3@ntrs.com The elevated unemployment rate remains at the top of the Fed s worry list. Nearly as important is the recent

Twin Problems: Employment and Consumer Spending September 1, 11 Asha G. Bangalore agb3@ntrs.com The elevated unemployment rate remains at the top of the Fed s worry list. Nearly as important is the recent

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

Professor Christina Romer. LECTURE 22 FISCAL POLICY April 14, 2016

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 22 FISCAL POLICY April 14, 2016 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer LECTURE 22 FISCAL POLICY April 14, 2016 I. REVIEW OF THE KEYNESIAN CROSS DIAGRAM A. Determination of output in the short run B. What

Q Economic Outlook

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Q1 Economic Outlook Presented by: Craig Dismuke Chief Economic Strategist cdismuke@viningsparks.com 1/24/ Page 1 Q1 ECONOMIC OUTLOOK A. European Drama, Weak U.S. Growth, and Central Bank Intervention B.

Transitioning From the Great Recession to Recovery to Expansion

Transitioning From the Great Recession to Recovery to Expansion AUGUSTINE FAUCHER, DIRECTOR OF MACROECONOMICS FROM MOODY S ECONOMY.COM The Great Recession Is Over Recessions since World War II Peak Trough

Transitioning From the Great Recession to Recovery to Expansion AUGUSTINE FAUCHER, DIRECTOR OF MACROECONOMICS FROM MOODY S ECONOMY.COM The Great Recession Is Over Recessions since World War II Peak Trough

Economic and Residential Outlook 1. William Strauss, Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic and Residential Outlook Rockford Area Realtors Rockford, IL July, William Strauss Senior Economist and Economic Advisor The Great Recession ended in June, but the economy expanded by.% over the

Economic and Residential Outlook Rockford Area Realtors Rockford, IL July, William Strauss Senior Economist and Economic Advisor The Great Recession ended in June, but the economy expanded by.% over the

Coping with the Zero Nominal Bound

Economics 196 Spring 2012 David Romer Coping with the Zero Nominal Bound April 3, 2012 A Couple of Ground Rules No electronic devices. I expect you to participate. I. INTRODUCTION Unemployment has been

Economics 196 Spring 2012 David Romer Coping with the Zero Nominal Bound April 3, 2012 A Couple of Ground Rules No electronic devices. I expect you to participate. I. INTRODUCTION Unemployment has been

Great Recession. Prof. Eric Sims. Fall University of Notre Dame

Great Recession Prof. Eric Sims University of Notre Dame Fall 25 / 28 Overview Worst economic contraction since Great Depression (by most measures) Could do entire course on the subject We will do a very

Great Recession Prof. Eric Sims University of Notre Dame Fall 25 / 28 Overview Worst economic contraction since Great Depression (by most measures) Could do entire course on the subject We will do a very

The Global Economy Heightened Risks

The Global Economy Heightened Risks RISI Latin American Conference 16 August, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. Latin America Some Improvement

The Global Economy Heightened Risks RISI Latin American Conference 16 August, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. Latin America Some Improvement

What could debt restructuring imply for the Eurozone? Adrian Cooper

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

Empirically Evaluating Economic Policy in Real Time. The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, John B.

Empirically Evaluating Economic Policy in Real Time The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, 2009 John B. Taylor To honor Martin Feldstein s distinguished leadership

Empirically Evaluating Economic Policy in Real Time The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, 2009 John B. Taylor To honor Martin Feldstein s distinguished leadership

Capital Markets Update

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Will The Recovery Hold? By Doug Duncan Vice President and Chief Economist Fannie Mae June 17, 2010

Will The Recovery Hold? By Doug Duncan Vice President and Chief Economist Fannie Mae June 17, 2010 1 Disclaimer Opinions, analyses, estimates, forecasts, and other views of Fannie Mae's Economics & Mortgage

Will The Recovery Hold? By Doug Duncan Vice President and Chief Economist Fannie Mae June 17, 2010 1 Disclaimer Opinions, analyses, estimates, forecasts, and other views of Fannie Mae's Economics & Mortgage

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

The Big Picture. Macro Principles. Lecture 1

What is Macroeconomics? GDP Other Measures The Big Picture Macro Principles Lecture 1 Growth Fluctuations Today s Topics The main ideas in this lecture What do we mean by macroeconomics? What are the major

What is Macroeconomics? GDP Other Measures The Big Picture Macro Principles Lecture 1 Growth Fluctuations Today s Topics The main ideas in this lecture What do we mean by macroeconomics? What are the major

Financial Highlights

November 16, 2011 Financial Highlights Federal Reserve Balance Sheet 1 Europe European Bond Spreads 2 Mortgage Markets Mortgage Rates 3 Mortgage Applications Consumer Credit Revolving and Nonrevolving

November 16, 2011 Financial Highlights Federal Reserve Balance Sheet 1 Europe European Bond Spreads 2 Mortgage Markets Mortgage Rates 3 Mortgage Applications Consumer Credit Revolving and Nonrevolving

The Financial Sector. Scott Mertens, Kristen Hecht, Chris Letcher, Chris Weber, Joseph Brendel, Jun Mei. Cougar Investment Fund

The Financial Sector Scott Mertens, Kristen Hecht, Chris Letcher, Chris Weber, Joseph Brendel, Jun Mei Cougar Investment Fund Introduction- Financial Sector - The financial sector consists of investment

The Financial Sector Scott Mertens, Kristen Hecht, Chris Letcher, Chris Weber, Joseph Brendel, Jun Mei Cougar Investment Fund Introduction- Financial Sector - The financial sector consists of investment

9/10/2014 Printable format for Business Cycles: The Concise Encyclopedia of Economics Library of Economics and Liberty

Printable Format for http://www.econlib.org/library/enc/businesscycles.html Business Cycles by Christina D. Romer About the Author FAQ: Print Hints T he United States and all other modern industrial economies

Printable Format for http://www.econlib.org/library/enc/businesscycles.html Business Cycles by Christina D. Romer About the Author FAQ: Print Hints T he United States and all other modern industrial economies

Macro Lecture 14: Late 2000 s Revisited. Fannie Mae Eases Credit To Aid Mortgage Lending

Macro Lecture 14: Late 2000 s Revisited Review gage-backed Securities (MBS) Figure 14.1 summarizes mortgage backed securities (MBS): A financial organization such as Fannie Mae, Bear Stearns, etc. o Buys

Macro Lecture 14: Late 2000 s Revisited Review gage-backed Securities (MBS) Figure 14.1 summarizes mortgage backed securities (MBS): A financial organization such as Fannie Mae, Bear Stearns, etc. o Buys

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY. Paul Darby Executive Director & Deuty Chief Economist Twitter hashtag: #psforum

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

Sample Exam 1: QEII Labor Market Rescue?

Sample Exam 1: QEII Labor Market Rescue? It seems the people who most need an economic recovery are the last to benefit. Currently the U.S. is experiencing a slow recovery, and like the last two, a jobless

Sample Exam 1: QEII Labor Market Rescue? It seems the people who most need an economic recovery are the last to benefit. Currently the U.S. is experiencing a slow recovery, and like the last two, a jobless

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

1 World Economy. Value of Finnish Forest Industry Exports Fell by Almost a Quarter in 2009

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies?

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

AUGUST 2012 An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 Provided as a convenience, this screen-friendly version is identic

AUGUST 2012 An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 Provided as a convenience, this screen-friendly version is identical in content to the principal, printer-friendly version

AUGUST 2012 An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 Provided as a convenience, this screen-friendly version is identical in content to the principal, printer-friendly version

The Global Economy Modest Improvement

Title line 1 Title line 2 The Global Economy Modest Improvement Name David Katsnelson, Director Title, date RISI Macroeconomic Service 3 June, 2015 1 Agenda 1. Global Snapshot 2. China 3. External Environment

Title line 1 Title line 2 The Global Economy Modest Improvement Name David Katsnelson, Director Title, date RISI Macroeconomic Service 3 June, 2015 1 Agenda 1. Global Snapshot 2. China 3. External Environment

BUDGET. Budget Plan. November 1, 2001

2002-2003 BUDGET Budget Plan November 1, 2001 2002-2003 Budget The Budget Plan 2002-2003 Section 1 Economic Situation Since the Beginning of 2001 and Revised Outlook for 2001 and 2002 Section 2 The Government

2002-2003 BUDGET Budget Plan November 1, 2001 2002-2003 Budget The Budget Plan 2002-2003 Section 1 Economic Situation Since the Beginning of 2001 and Revised Outlook for 2001 and 2002 Section 2 The Government

Notes Numbers in the text and tables may not add up to totals because of rounding. Unless otherwise indicated, years referred to in describing the bud

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 4 to 4 Percentage of GDP 4 Surpluses Actual Projected - -4-6 Average Deficit, 974 to Deficits -8-974 979 984 989

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 4 to 4 Percentage of GDP 4 Surpluses Actual Projected - -4-6 Average Deficit, 974 to Deficits -8-974 979 984 989

International Summer Program June 26 th to July 17 th, 2006

International Summer Program June 26 th to July 17 th, 2006 ECB & Fed A comparison By Christine Brandt Introduction Economic areas and datas Member states/districts, population, GDP, unemployment rate...

International Summer Program June 26 th to July 17 th, 2006 ECB & Fed A comparison By Christine Brandt Introduction Economic areas and datas Member states/districts, population, GDP, unemployment rate...

WHAT THE REALLY HAPPENED...

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

March 2008 Third District Housing Market Conditions Nathan Brownback

March 28 Third District Housing Market Conditions Nathan Brownback By many measures, the economy of the Third District closely tracks the national economy. Thus far in the current housing cycle, this appears

March 28 Third District Housing Market Conditions Nathan Brownback By many measures, the economy of the Third District closely tracks the national economy. Thus far in the current housing cycle, this appears

What is the global economic outlook?

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

Intermediate Macroeconomics: Great Recession

Intermediate Macroeconomics: Great Recession Eric Sims University of Notre Dame Fall 2013 1 Introduction The Great Recession is the name now commonly given to the economic contraction that occurred in

Intermediate Macroeconomics: Great Recession Eric Sims University of Notre Dame Fall 2013 1 Introduction The Great Recession is the name now commonly given to the economic contraction that occurred in

Macro Lecture 14: Late 2000 s Revisited

Macro Lecture 14: Late 0 s Revisited Review gage-backed Securities (MBS) Figure 14.1 summarizes mortgage backed securities (MBS) A financial organization such as Fannie Mae or Bear Stearns or o buys a

Macro Lecture 14: Late 0 s Revisited Review gage-backed Securities (MBS) Figure 14.1 summarizes mortgage backed securities (MBS) A financial organization such as Fannie Mae or Bear Stearns or o buys a

The Global Financial Crisis and the double recession in Spain

The Global Financial Crisis and the double recession in Spain Background Much of the western world experienced a slowdown of economic activity sometime between the latter part of 2007 and the beginning

The Global Financial Crisis and the double recession in Spain Background Much of the western world experienced a slowdown of economic activity sometime between the latter part of 2007 and the beginning

Eurozone Economic Watch. November 2017

Eurozone Economic Watch November 2017 Eurozone: improved outlook, still subdued inflation Our MICA-BBVA model for growth estimates for the moment a quarterly GDP figure of around -0.7% in, after % QoQ

Eurozone Economic Watch November 2017 Eurozone: improved outlook, still subdued inflation Our MICA-BBVA model for growth estimates for the moment a quarterly GDP figure of around -0.7% in, after % QoQ

Policy Reforms after the Crisis

367 Policy Reforms after the Crisis Norman Chan The title of this session is supposed to be policy reforms after the 28 9 financial crisis. I think there s a big question about the title because I m not

367 Policy Reforms after the Crisis Norman Chan The title of this session is supposed to be policy reforms after the 28 9 financial crisis. I think there s a big question about the title because I m not

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

The Outlook for the European and the German Economy

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The First Phase of the U.S. Recovery and Beyond

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

Session 12. The New Normal. Deflation and Zero Lower Bound.

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

1.1. Low yield environment

1. Key developments Overall, the macroeconomic outlook has deteriorated since June 215. Although many European countries continue to recover, economic growth still remains fragile reflecting high public

1. Key developments Overall, the macroeconomic outlook has deteriorated since June 215. Although many European countries continue to recover, economic growth still remains fragile reflecting high public

Economy Check-In: Post 2008 Crisis Market Update Special Report

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Eurozone Economic Watch. February 2018

Eurozone Economic Watch February 2018 Eurozone: Strong growth continues in 1Q18, but confidence seems to peak GDP growth moderated slightly in, but there was an upward revision to previous quarters. Available

Eurozone Economic Watch February 2018 Eurozone: Strong growth continues in 1Q18, but confidence seems to peak GDP growth moderated slightly in, but there was an upward revision to previous quarters. Available

The Global Economy Heightened Risks

The Global Economy Heightened Risks RISI North American Conference 5 October, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot 2. USA Steady Growth 3. Europe Growing Slowly 4. China

The Global Economy Heightened Risks RISI North American Conference 5 October, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot 2. USA Steady Growth 3. Europe Growing Slowly 4. China

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis Masahiro Kawai, ADBI Macro Economy Research Conference Fiscal Policy in the Post-Crisis World Nomura Foundation for Global Studies

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis Masahiro Kawai, ADBI Macro Economy Research Conference Fiscal Policy in the Post-Crisis World Nomura Foundation for Global Studies

Mandatory Spending Since 1962

D. Andrew Austin Analyst in Economic Policy Mindy R. Levit Analyst in Public Finance February 16, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress

D. Andrew Austin Analyst in Economic Policy Mindy R. Levit Analyst in Public Finance February 16, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress

Spring Forecast: slowly recovering from a protracted recession

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

Chad Wilkerson. Vice President, Economist, and Oklahoma City Branch Executive Federal Reserve Bank of Kansas City

Chad Wilkerson Vice President, Economist, and Oklahoma City Branch Executive Federal Reserve Bank of Kansas City www.kansascityfed.org History and Structure of the Federal Reserve System The Federal Reserve

Chad Wilkerson Vice President, Economist, and Oklahoma City Branch Executive Federal Reserve Bank of Kansas City www.kansascityfed.org History and Structure of the Federal Reserve System The Federal Reserve

Lessons from previous US recessions and recoveries

Lessons from previous US recessions and recoveries Satish Ranchhod The US economy is emerging from a period of significant weakness. This article examines how US economic activity evolved during previous

Lessons from previous US recessions and recoveries Satish Ranchhod The US economy is emerging from a period of significant weakness. This article examines how US economic activity evolved during previous

No 02. Chapter 1. Chapter Outline. What Macroeconomics Is About. Introduction to Macroeconomics

No 02. Chapter 1 Introduction to Macroeconomics Chapter Outline What Macroeconomists Do Why Macroeconomists Disagree Macroeconomics: the study of structure and performance of national economies and government

No 02. Chapter 1 Introduction to Macroeconomics Chapter Outline What Macroeconomists Do Why Macroeconomists Disagree Macroeconomics: the study of structure and performance of national economies and government

The U.S. Economic Outlook, Fiscal Issues and European Crisis

The U.S. Economic Outlook, Fiscal Issues and European Crisis October 1 Troy Davig Director of Research Outlook themes The US remains in a moderate growth environment The unemployment rate is 8.1%, close

The U.S. Economic Outlook, Fiscal Issues and European Crisis October 1 Troy Davig Director of Research Outlook themes The US remains in a moderate growth environment The unemployment rate is 8.1%, close

LECTURES 7-9: POLICY INSTRUMENTS, including MONEY. L7: Goals and Instruments Policy goals: Internal balance & External balance Policy instruments

LECTURES 7-9: POLICY INSTRUMENTS, including MONEY L7: Goals and Instruments Policy goals: Internal balance & External balance Policy instruments The Swan Diagram The principle of goals & instruments L8:

LECTURES 7-9: POLICY INSTRUMENTS, including MONEY L7: Goals and Instruments Policy goals: Internal balance & External balance Policy instruments The Swan Diagram The principle of goals & instruments L8:

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 7

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 7 MONETARY FACTORS IN THE GREAT DEPRESSION? FEBRUARY 7, 2018 I. MONETARY ARRANGEMENTS IN THE 1920S

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 7 MONETARY FACTORS IN THE GREAT DEPRESSION? FEBRUARY 7, 2018 I. MONETARY ARRANGEMENTS IN THE 1920S

The U.S. Economy: An Optimistic Outlook, But With Some Important Risks

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

What Happens During Recessions, Crunches and Busts?

What Happens During Recessions, Crunches and Busts? Stijn Claessens, M. Ayhan Kose and Marco E. Terrones Financial Studies Division, Research Department International Monetary Fund Presentation at the

What Happens During Recessions, Crunches and Busts? Stijn Claessens, M. Ayhan Kose and Marco E. Terrones Financial Studies Division, Research Department International Monetary Fund Presentation at the

Florida: An Economic Overview

Florida: An Economic Overview March 24, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview March 24, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

Joseph S Tracy: A strategy for the 2011 economic recovery

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

June 24th, Rate Reversal. Author: Benjamin Struck President

June 24th, 2013 Rate Reversal Author: Benjamin Struck President 1 Economic Summary 3 Strategic Allocation 5 Tactical Allocation 6 2 Last week s selloff was broad based and applied to nearly all asset classes.

June 24th, 2013 Rate Reversal Author: Benjamin Struck President 1 Economic Summary 3 Strategic Allocation 5 Tactical Allocation 6 2 Last week s selloff was broad based and applied to nearly all asset classes.

Economic and Housing Outlook

Economic and Housing Outlook Macdonald Realty Monday, January 23, 212 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: European developments U.S. economy and forecasts Canadian economic

Economic and Housing Outlook Macdonald Realty Monday, January 23, 212 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: European developments U.S. economy and forecasts Canadian economic

Discussion on The Great Recession: What Recovery?

Discussion on The Great Recession: What Recovery? Robert E. Hall Hoover Institution and Department of Economics Stanford Universtiy rehall@stanford.edu Twelfth BIS Annual Conference June 13 September 17,

Discussion on The Great Recession: What Recovery? Robert E. Hall Hoover Institution and Department of Economics Stanford Universtiy rehall@stanford.edu Twelfth BIS Annual Conference June 13 September 17,

The Financial Sector

Brad Smith January 30, 2009 The Financial Sector Yield Curve The yield curve has maintained its steepness over the past sixth months and has continued to be depressed on both short and long ends. With

Brad Smith January 30, 2009 The Financial Sector Yield Curve The yield curve has maintained its steepness over the past sixth months and has continued to be depressed on both short and long ends. With

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM?

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM? Jean-Pierre Aubry, Associate Fellow, CIRANO Annual conference of the Canadian Economic Association HEC, Montréal, May 30th

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM? Jean-Pierre Aubry, Associate Fellow, CIRANO Annual conference of the Canadian Economic Association HEC, Montréal, May 30th

October 29, Can the Fed Successfully Exit from Its Recent Policy?

October 29, 2014 Can the Fed Successfully Exit from Its Recent Policy? Stephen M. Miller, PhD The U.S. economic recovery continues with many pundits predicting an improving trajectory over the next two

October 29, 2014 Can the Fed Successfully Exit from Its Recent Policy? Stephen M. Miller, PhD The U.S. economic recovery continues with many pundits predicting an improving trajectory over the next two

Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

The Great Escape? Douglas Porter, CFA. Deputy Chief Economist & Managing Director, BMO Capital Markets

The Great Escape? Douglas Porter, CFA Deputy Chief Economist & Managing Director, BMO Capital Markets Financial Markets Revive (as of May 3, 21) 16 Stocks 16 15 Canadian Dollar ( ) 15 Commodities 4.5 14

The Great Escape? Douglas Porter, CFA Deputy Chief Economist & Managing Director, BMO Capital Markets Financial Markets Revive (as of May 3, 21) 16 Stocks 16 15 Canadian Dollar ( ) 15 Commodities 4.5 14

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16 FISCAL POLICY IN THE GREAT RECESSION MARCH 19, 2018 I. OVERVIEW II. ECONOMIC STIMULUS ACT

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16 FISCAL POLICY IN THE GREAT RECESSION MARCH 19, 2018 I. OVERVIEW II. ECONOMIC STIMULUS ACT

MAKING SENSE OF ECONOMIC INDICATORS

WELCOME TO THE WEBINAR FRB MIAMI & FRB NASHVILLE TEACHERS! 1 WEBINAR LINK HTTP://FRBATL.ADOBECONNECT.COM/ECONINDICATORS/ DIAL-IN NUMBER (MUST USE FOR AUDIO) 855-377-2663 ACCESS CODE: 71032685 REMINDER:

WELCOME TO THE WEBINAR FRB MIAMI & FRB NASHVILLE TEACHERS! 1 WEBINAR LINK HTTP://FRBATL.ADOBECONNECT.COM/ECONINDICATORS/ DIAL-IN NUMBER (MUST USE FOR AUDIO) 855-377-2663 ACCESS CODE: 71032685 REMINDER:

Fiscal Policy & Colored Animals

Fiscal Policy & Colored Animals Eric M. Leeper Department of Economics, Indiana University September 2010 College of Arts & Sciences Alumni Event The Message If we allow the The Message to distract us

Fiscal Policy & Colored Animals Eric M. Leeper Department of Economics, Indiana University September 2010 College of Arts & Sciences Alumni Event The Message If we allow the The Message to distract us