WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM?

|

|

|

- Antony Lindsey

- 6 years ago

- Views:

Transcription

1 WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM? Jean-Pierre Aubry, Associate Fellow, CIRANO Annual conference of the Canadian Economic Association HEC, Montréal, May 30th to June 2nd 2013 CD Howe Session (June 1, 16:30-18:00) Long-Term Investment Returns: Expectations and Policy Implications

2 WHAT I WILL DISCUSS Major adjustments are still required in developed countries Implications of these adjustments for economic growth and rates of return Need for research on the nature of these adjustments and on best policies to follow to bring about these adjustments

3 WHY MAJOR ADJUSTMENTS ARE NECESSARY IN DEVELOPED COUNTRIES Very strong competition from emerging economies (no more private club of developed countries) Large savings/investments disequilibrium Large reduction in net assets held by households

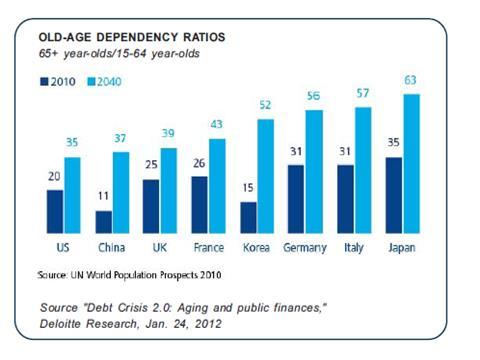

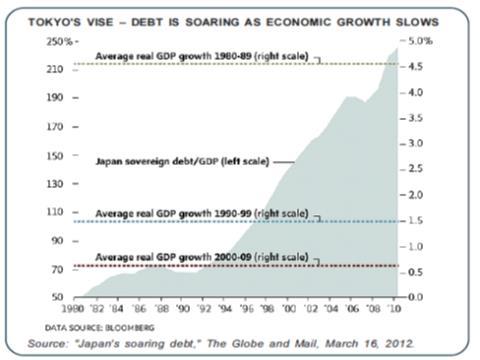

4 WHY MAJOR ADJUSTMENTS ARE NECESSARY IN DEVELOPED COUNTRIES (2) Financial crisis followed by a very slow return to full employment Sustained government deficits and high levels of government debt Aging population (we are just starting to understand the implications)

5

6 OECD LONG TERM PROJECTIONS FOR ITS MEMBERS Very high levels of government debt Relatively low GDP growth Difficulty in recognizing reduction in potential and in growth of potential in many countries Projections for many countries seriously affected by the debt crisis look very optimistic, especially as the OECD is assuming no debt writedowns.

7 OECD PROJECTIONS with no accidents Report : Medium and long-term scenarios for global growth and imbalances, 2012

8 OECD PROJECTIONS with no accidents Report : Medium and long-term scenarios for global growth and imbalances, 2012

9 FRANCE AND ITALY Rates of growth of real GDP France Italy Average rate % 0.4 % OECD Projections % 0.2% % 0.7 % Natixis : GDP Potential % 0.1%

10

11

12

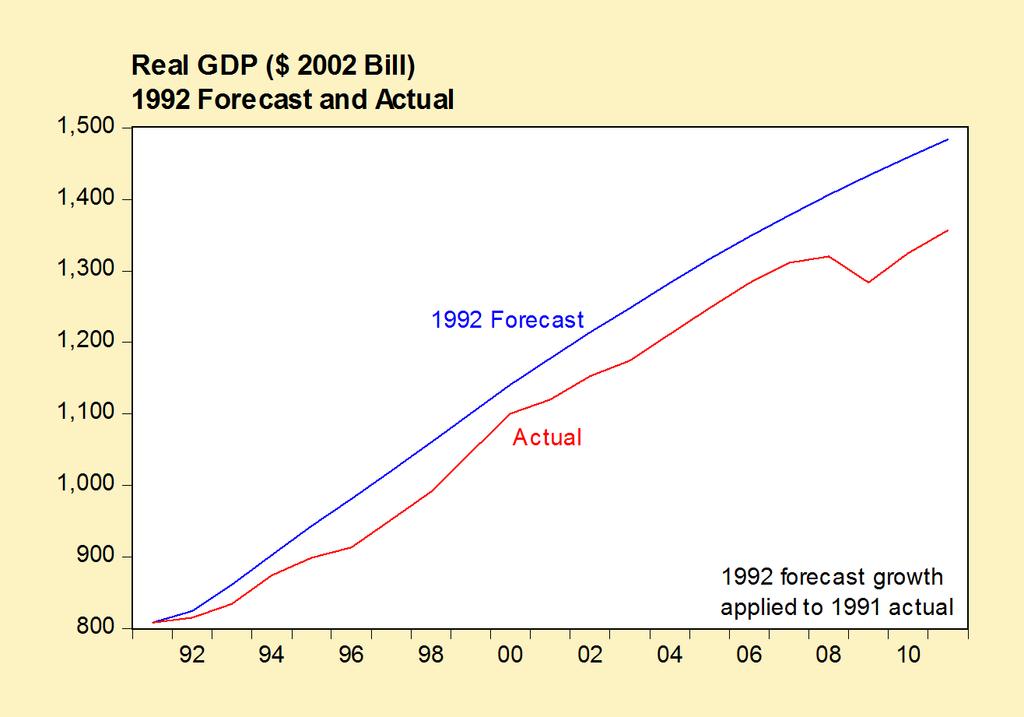

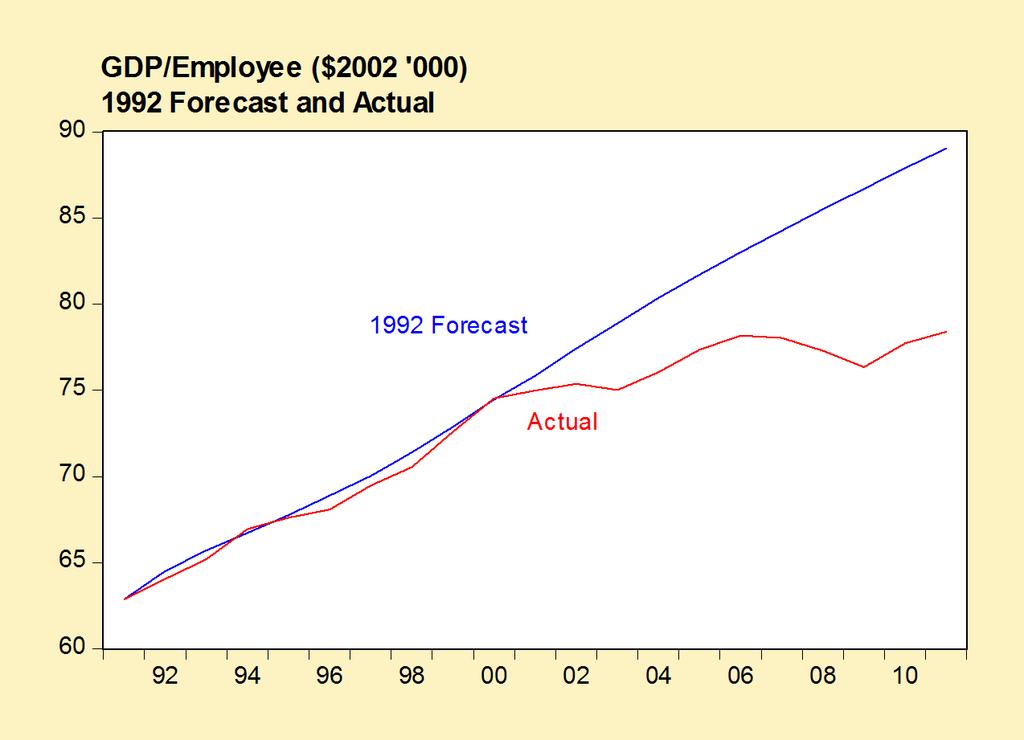

13 CANADA (rates of growth) Real GDP Labour Productivity % 2.2% 3.0% % 2.3% 1.7% % 1.7% 1.1% % 1.1% 1.8% % 1.1% 0.8% % 0.6% 1.2% Office of the Parliamentary Budget Officer, Fiscal Sustainability Report, September 2011 See in the Annex the slides extracted from a presentation made by Peter Dungan

14 OECD projections for 2014 (Dec. 2012) Output gap (%GDP) Direction of the Government cyclically-adj. output gap Balances (%GDP) France -4.6% Growing -0.4% Greece -18.4% Growing 3.9% Ireland -6.6% Growing -4.3% Italy -6.3% Growing 0.5% Japan -2.2% At best stable -7.0% Portugal -8.5% Growing 0.9% Spain -11.2% Growing -0.4% United States -2.9% Déclining from -4.6% -4.1% Euro area -4.8% At best stable -0.1% Total OECD -2.9% Stable (down from -4%) -2.6%

15 VERY SLOW RETURN TO BALANCED BUDGETS Despite extremely expansionary monetary policies for many years. Slow pace not mainly a result of low aggregate demand. Primarily a result of supply side problems and the fact that many countries are living beyond their means. Problems will take many years to resolve (especially in those countries that cannot devalue their real exchange rates).

16

17 ARE WE FACING A DISCONNECT BETWEEN THE REAL SECTOR AND THE FINANCIAL SECTOR? Significant reduction in GDP potential (in part generated by the lack of competitiveness) Lower growth of GDP resulting from lower growth in productivity and the labour force (related to the aging of the populations) Not enough production to match the commitments made to citizens and debt holders

18 ASSUMPTIONS REGARDING LONG-TERM REAL RATE OF RETURN ON RISK-FREE FINANCIAL ASSETS In the long term, the real rate of return is more likely to be high when the growth rate of the economy is high. The converse is also true. The rate of return on risk-free assets in developed countries can be expected to be lower in coming decades, as their growth rates are affected by aging populations, difficulty competing with emerging countries and problems of excessive debts. 18

19 THE DISCONNECT AND THE VALUE OF THE DEBT CERTIFICATES Without a credible plan to reduce the relative size of the government debt, countries will find it increasingly difficult to borrow. Debt certificates will lose some of their market value (=> lower return ex-post) We must think beyond the debt reduction process (Wealth effect in the life cycle model) Lower permanent income for households => a need to save more and to work for a longer period of time

20 US : SLOW RECOVERY OF HOUSEHOLD WEALTH

21 OECD PROJECTIONS LONG TERM REAL RATE OF INTEREST

22 THREE COMMENTS ON THESE PROJECTIONS Interest rates must go up from the current abnormally low level. But over the long term, real rates will continue the downward trend observed before the crisis In the high debt scenario, the OECD has included a risk premium in its real rate projection ( see in the chart the difference between the blue line and the dotted blue line)

23 THE LONG-TERM REAL RATE OF RETURN IN THE OECD COUNTRIES VERSUS THAT IN THE GLOBAL MARKET? Limits to capital mobility. Diminishing returns. Constraints on allocation of investment portfolios. Exchange rate risks. Examples (China, Japan, Southeast Asia ). 23

24 CONCLUSION «In the longer term, real interest rates are determined primarily by nonmonetary factors, such as the expected return to capital investments, which in turn is closely related to the underlying strength of the economy.» Ben S. Bernanke, March 1, 2013 Lower growth for developed countries will imply lower real long term interest rate More research is needed on this subject and on the public policies that would be the most appropriate

25 ANNEX Substantial unconventional monetary easing Aging population and rates of return 6 slides presenting abstracts from the chapter 4 of an OECD Report Canada example, projection errors on the rate of growth of productivity and the real interest rates, 4 slides from a presentation made by Peter Dungan

26 Substantial unconventional monetary easing Monetary Policy Report, April 2013, BoC

27 AGING POPULATION AND RATES OF RETURN Jean Boivin, Deputy governor, Bank of Canada, April 4,2012 the aging population in advanced economies may in time have implications for the level of global interest rates. Taken in isolation, the scarcity of labour relative to capital would lead to higher wages and lower returns on capital, which could eventually contribute to persistently lower interest rates

28 The next 6 slides present abstracts from the chapter 4 of an OECD Report : Medium and long-term scenarios for global growth and imbalances, pdf

29 «Further ahead, demographic changes, including ageing, and fundamental forces of economic convergence will bring about massive shifts in the composition of global GDP. Many countries face a long period of adjustment to erase the legacies of the crisis, particularly high unemployment, excess capacity and large fiscal imbalances. Further ahead, demographic changes, including ageing, and fundamental forces of economic convergence will bring about massive shifts in the composition of global GDP.»

30 «The scenarios presented in this chapter thus provide a benign, even optimistic, medium-term outlook for the world economy. There are large risks around this central path that could derail the recovery in one or more countries, including: further crises of confidence around the debt of one or more governments; disorderly debt defaults; the collapse of one or more systemically important financial institutions or renewed concerns around bank solvency that would further impair private credit necessary to fuel the recovery; worse-than-anticipated growth impacts from private sector deleveraging; worse-than-anticipated drag from sustained and concurrent fiscal consolidation; a spike in energy prices from already elevated levels; and more generally risks from political turmoil, conflict or natural disaster. Any or a combination of these factors could tip countries back into recession or lead to stagnation»

31 «In addition, in many OECD countries government indebtedness will exceed thresholds at which there is evidence of adverse effects on interest rates, growth and the ability to stabilise the economy. In addition, for a typical OECD country, additional offsets of 3 to 4% of GDP (in their primary balance ) will have to be found over the coming 20 years to meet spending pressures due to increasing pension and health care costs.»

32 «Over a horizon to 2030 the baseline scenario shows a build-up of a number of major macroeconomic imbalances including: high and widespread government indebtedness; rising global current account imbalances; and upward pressures on interest rates... These imbalances should be viewed as identifying future tensions which will need to be addressed by policy rather than most likely outcomes»

33 «Ageing populations are then projected to be the dominant force driving down saving rates over the long term. Demographic developments (combining the effect of changes in old-age and youth dependency ratios as well as life expectancy) are estimated to reduce the private saving rate for the median OECD country by about 3-4 percentage points by 2030, with much heterogeneity around this median.»

34 «Another optimistic assumption that underlies the scenarios presented here is that the crisis has only reduced the level of potential output and has had no permanent adverse effect on its growth rate. Compared with precrisis projections, the level of aggregate OECD potential output, both currently and over the next few years, has been revised downwards by about 2½ per cent Because even very large output gaps are assumed to close fairly quickly, the possibility of large negative output gaps persisting for several years, with hysteresis-type effects continuing to drag down the level of potential output, is thus a downside risk to the scenarios presented here.»

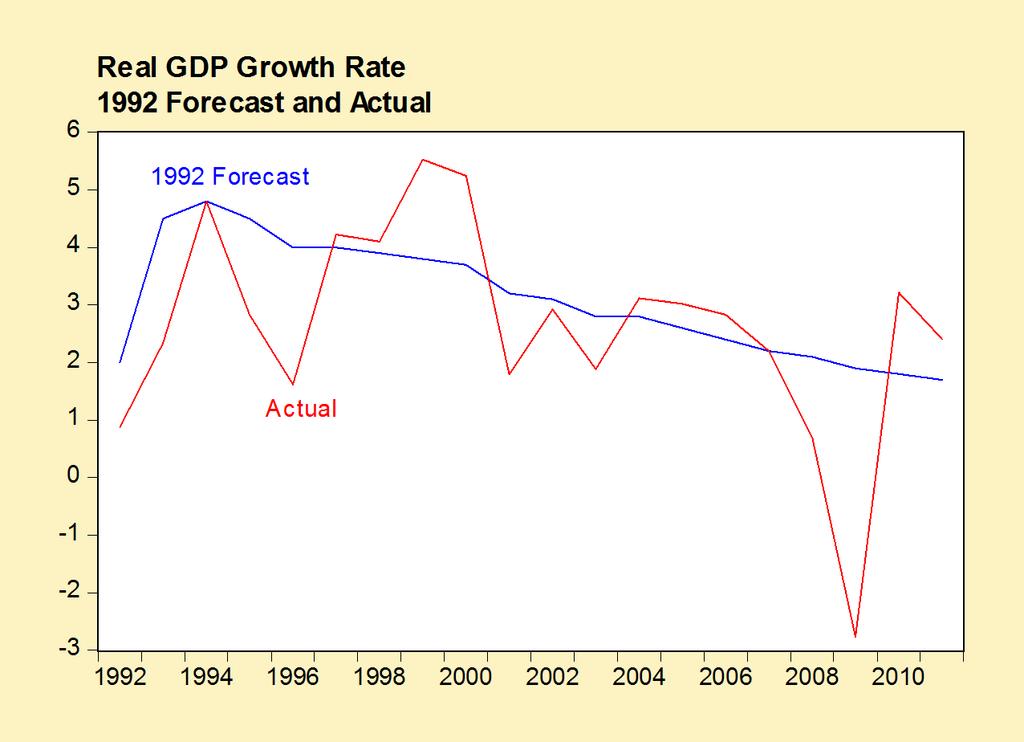

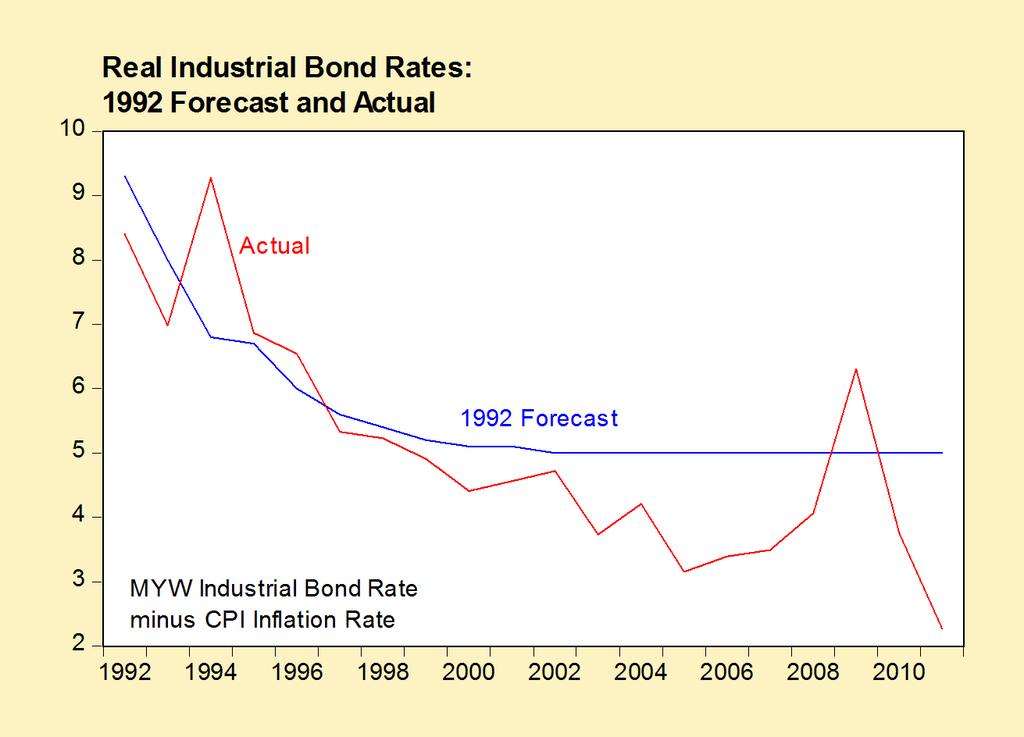

35 PROJECTION ERRORS ON ECONOMIC GROWTH AND REAL INTEREST RATES Peter Dungan, Adjunct Associate Professor of Business Economics, University of Toronto, Rotman School, Toronto, Ontario Seminar on Demographic, Economic and Investment Perspectives for Canada to 2050, Office of the Chief Actuary, Sept. 2012, One of the main error made in the economic projection made in 1992 : too high GDP growth, productivity growth, and real interest rates

36

37

38

39

The economic and fiscal outlook for OECD countries

The economic and fiscal outlook for OECD countries Presentation to the Economics and Security Committee of the NATO Parliamentary Assembly 17 February 2010 Sveinbjorn Blondal Head of Macroeconomic Policy

The economic and fiscal outlook for OECD countries Presentation to the Economics and Security Committee of the NATO Parliamentary Assembly 17 February 2010 Sveinbjorn Blondal Head of Macroeconomic Policy

What is the global economic outlook?

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

Panel Discussion: Coordinated Policies for Global Liquidity and Robust Growth

Panel Discussion: Coordinated Policies for Global Liquidity and Robust Growth Remarks to The Bank of Korea International Conference 2013 4 June 2013 Seoul, Korea Timothy Lane Deputy Governor Bank of Canada

Panel Discussion: Coordinated Policies for Global Liquidity and Robust Growth Remarks to The Bank of Korea International Conference 2013 4 June 2013 Seoul, Korea Timothy Lane Deputy Governor Bank of Canada

Global Economic Prospects

Global Economic Prospects Slow and halting progress Andrew Burns DEC Prospects Group October, 22, 2012 1 Despite better financial conditions, stronger growth remains elusive May/June financial turmoil

Global Economic Prospects Slow and halting progress Andrew Burns DEC Prospects Group October, 22, 2012 1 Despite better financial conditions, stronger growth remains elusive May/June financial turmoil

Hamburg Accountability Assessment G20 Framework Working Group

Hamburg Accountability Assessment G20 Framework Working Group 1. Introduction Strong, sustainable and balanced growth has been the overarching objective of the G20 since 2009. At their last summit in Hangzhou,

Hamburg Accountability Assessment G20 Framework Working Group 1. Introduction Strong, sustainable and balanced growth has been the overarching objective of the G20 since 2009. At their last summit in Hangzhou,

Inflation Report. January March 2013

January March 2013 May 8, 2013 Outline 1 External Conditions 2 Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants 4 Forecasts and Balance of Risks 2 External Conditions Global Environment

January March 2013 May 8, 2013 Outline 1 External Conditions 2 Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants 4 Forecasts and Balance of Risks 2 External Conditions Global Environment

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

PBO Economic and Fiscal Outlook. Ottawa, Canada November 1,

PBO Economic and Fiscal Outlook Ottawa, Canada November 1, 11 www.parl.gc.ca/pbo-dpb PBO Economic and Fiscal Outlook The mandate of the Parliamentary Budget Officer (PBO) is to provide independent analysis

PBO Economic and Fiscal Outlook Ottawa, Canada November 1, 11 www.parl.gc.ca/pbo-dpb PBO Economic and Fiscal Outlook The mandate of the Parliamentary Budget Officer (PBO) is to provide independent analysis

Modelling the sovereign debt crisis in Europe

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

GLOBAL EMPLOYMENT TRENDS 2014

Executive summary GLOBAL EMPLOYMENT TRENDS 2014 006.65 0.887983 +1.922523006.62-0.657987 +1.987523006.82-006.65 +1.987523006.60 +1.0075230.887984 +1.987523006.64 0.887985 0.327987 +1.987523006.59-0.807987

Executive summary GLOBAL EMPLOYMENT TRENDS 2014 006.65 0.887983 +1.922523006.62-0.657987 +1.987523006.82-006.65 +1.987523006.60 +1.0075230.887984 +1.987523006.64 0.887985 0.327987 +1.987523006.59-0.807987

Economic Outlook. Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012.

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

The sharp accumulation in government debt can t go on forever

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

Annex 4. The St. Petersburg Accountability Assessment

Annex 4 The St. Petersburg Accountability Assessment The G-20 s Accountability Assessment framework was established to monitor progress against past commitments and identify areas where further policy

Annex 4 The St. Petersburg Accountability Assessment The G-20 s Accountability Assessment framework was established to monitor progress against past commitments and identify areas where further policy

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

The U.S. Economic Outlook, Fiscal Issues and European Crisis

The U.S. Economic Outlook, Fiscal Issues and European Crisis October 1 Troy Davig Director of Research Outlook themes The US remains in a moderate growth environment The unemployment rate is 8.1%, close

The U.S. Economic Outlook, Fiscal Issues and European Crisis October 1 Troy Davig Director of Research Outlook themes The US remains in a moderate growth environment The unemployment rate is 8.1%, close

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Schwerpunkt Außenwirtschaft 2016/17 Austrian economic activity, Austria's price competitiveness and a summary on external trade

Schwerpunkt Außenwirtschaft /7 Austrian economic activity, Austria's price competitiveness and a summary on external trade Christian Ragacs, Klaus Vondra Abteilung für volkswirtschaftliche Analysen, OeNB

Schwerpunkt Außenwirtschaft /7 Austrian economic activity, Austria's price competitiveness and a summary on external trade Christian Ragacs, Klaus Vondra Abteilung für volkswirtschaftliche Analysen, OeNB

Daniel Mminele: Thoughts on South Africa s monetary policy

Daniel Mminele: Thoughts on South Africa s monetary policy Address by Mr Daniel Mminele, Deputy Governor of the South African Reserve Bank, at the JP Morgan Investor Conference, Washington DC, 16 April

Daniel Mminele: Thoughts on South Africa s monetary policy Address by Mr Daniel Mminele, Deputy Governor of the South African Reserve Bank, at the JP Morgan Investor Conference, Washington DC, 16 April

What could debt restructuring imply for the Eurozone? Adrian Cooper

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis Masahiro Kawai, ADBI Macro Economy Research Conference Fiscal Policy in the Post-Crisis World Nomura Foundation for Global Studies

Comment on David Vines Fiscal Policy in the Eurozone after the Crisis Masahiro Kawai, ADBI Macro Economy Research Conference Fiscal Policy in the Post-Crisis World Nomura Foundation for Global Studies

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE. 9 May 2012 Vicky Pryce

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE 9 May 2012 Vicky Pryce Contents Global and European economy UK economy Prospects for individuals and businesses Concluding remarks what next? Global and European

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE 9 May 2012 Vicky Pryce Contents Global and European economy UK economy Prospects for individuals and businesses Concluding remarks what next? Global and European

Project Link Meeting, New York

Project Link Meeting, New York October 22-24, 2012 Country Report: Italy from Rapporto di Previsione Ottobre 2012 (Economic Outlook, October 2012); Prometeia Associazione per le Previsioni Econometriche

Project Link Meeting, New York October 22-24, 2012 Country Report: Italy from Rapporto di Previsione Ottobre 2012 (Economic Outlook, October 2012); Prometeia Associazione per le Previsioni Econometriche

Insolvency forecasts. Economic Research August 2017

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

ECB LTRO Dec Greece program

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

OECD ECONOMIC OUTLOOK

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

Philipp Hildebrand: Overview of the Swiss and global economy

Philipp Hildebrand: Overview of the Swiss and global economy Introductory remarks by Mr Philipp Hildebrand, Chairman of the Governing Board of the Swiss National Bank, at the half-yearly media news conference,

Philipp Hildebrand: Overview of the Swiss and global economy Introductory remarks by Mr Philipp Hildebrand, Chairman of the Governing Board of the Swiss National Bank, at the half-yearly media news conference,

Household Balance Sheets and Debt an International Country Study

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

Economic and Housing Outlook

Economic and Housing Outlook Macdonald Realty Monday, January 23, 212 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: European developments U.S. economy and forecasts Canadian economic

Economic and Housing Outlook Macdonald Realty Monday, January 23, 212 Helmut Pastrick Chief Economist Central 1 Credit Union Outline: European developments U.S. economy and forecasts Canadian economic

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Global secular stagnation and monetary policy

Global secular stagnation and monetary policy Professor Martin Eichenbaum CLICK TO EDIT MASTER SUBTITLE STYLE Key facts Fact 1 The growth rate of the world economy has been declining since 2008. Slow growth

Global secular stagnation and monetary policy Professor Martin Eichenbaum CLICK TO EDIT MASTER SUBTITLE STYLE Key facts Fact 1 The growth rate of the world economy has been declining since 2008. Slow growth

Her Majesty the Queen in Right of Canada (2017) All rights reserved

All rights reserved") Her Majesty the Queen in Right of Canada (2017) All rights reserved All requests for permission to reproduce this document or any part thereof shall be addressed to the Department of Finance Canada. Cette

Her Majesty the Queen in Right of Canada (2017) All rights reserved All requests for permission to reproduce this document or any part thereof shall be addressed to the Department of Finance Canada. Cette

Fiscal Consolidation

Fiscal Consolidation Sam Beckett, Director, Fiscal Policy, HM Treasury 27 May 2011 Overview of presentation 1. Origin of the UK fiscal deficit 2. Fiscal policy response and framework reform 3. Latest forecasts

Fiscal Consolidation Sam Beckett, Director, Fiscal Policy, HM Treasury 27 May 2011 Overview of presentation 1. Origin of the UK fiscal deficit 2. Fiscal policy response and framework reform 3. Latest forecasts

PBO Economic and Fiscal Outlook. Ottawa, Canada June 1, dpb

PBO Economic and Fiscal Outlook Ottawa, Canada June 1, 211 www.parl.gc.ca/pbo dpb PBO Economic and Fiscal Outlook The Parliament of Canada Act mandates the Parliamentary Budget Officer (PBO) to provide

PBO Economic and Fiscal Outlook Ottawa, Canada June 1, 211 www.parl.gc.ca/pbo dpb PBO Economic and Fiscal Outlook The Parliament of Canada Act mandates the Parliamentary Budget Officer (PBO) to provide

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Imbalances in the Euro Area

Monetary Review, 2nd Quarter 213 - Part 1 89 Imbalances in the Euro Area Jacob Isaksen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY The global economic crisis and the ensuing sovereign

Monetary Review, 2nd Quarter 213 - Part 1 89 Imbalances in the Euro Area Jacob Isaksen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY The global economic crisis and the ensuing sovereign

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

An interim assessment

What is the economic outlook for OECD countries? An interim assessment Paris, 5 April 2011 11h Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General 1. The news has of course been

What is the economic outlook for OECD countries? An interim assessment Paris, 5 April 2011 11h Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General 1. The news has of course been

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Ottawa, Ontario 28 September 2012 CHECK AGAINST DELIVERY. For additional information contact:

Opening Remarks by Chief Actuary Jean-Claude Ménard Office of the Chief Actuary Office of the Superintendent of Financial Institutions Canada (OSFI) to the Canada Pension Plan (CPP) Seminar on Demographic,

Opening Remarks by Chief Actuary Jean-Claude Ménard Office of the Chief Actuary Office of the Superintendent of Financial Institutions Canada (OSFI) to the Canada Pension Plan (CPP) Seminar on Demographic,

Economic and Fiscal Assessment Update

Economic and Fiscal Assessment Update Standing Committee on Finance (FINA) 15 February 11 Kevin Page Parliamentary Budget Officer billions of chained () dollars 1,395 Real and Potential GDP 1,395 1,37

Economic and Fiscal Assessment Update Standing Committee on Finance (FINA) 15 February 11 Kevin Page Parliamentary Budget Officer billions of chained () dollars 1,395 Real and Potential GDP 1,395 1,37

Macroeconomic projections for Assumptions from the external surrounding. Baseline macroeconomic scenario for

Dimitar Bogov Governor November, Macroeconomic projections for -4 Assumptions from the external surrounding Baseline macroeconomic scenario for -4 Comparison with the previous projection In the period

Dimitar Bogov Governor November, Macroeconomic projections for -4 Assumptions from the external surrounding Baseline macroeconomic scenario for -4 Comparison with the previous projection In the period

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Spring 2013 forecast: The EU economy slowly recovering from a protracted recession

EUROPEAN COMMISSION PRESS RELEASE Brussels, 3 May 2013 Spring 2013 forecast: The EU economy slowly recovering from a protracted recession Following the recession that marked 2012, the EU economy is expected

EUROPEAN COMMISSION PRESS RELEASE Brussels, 3 May 2013 Spring 2013 forecast: The EU economy slowly recovering from a protracted recession Following the recession that marked 2012, the EU economy is expected

Economic and Fiscal Assessment Update. Ottawa, Canada November 2,

Economic and Fiscal Assessment Update Ottawa, Canada November 2, 29 www.parl.gc.ca/pbo-dpb The Federal Accountability Act mandates the Parliamentary Budget Officer (PBO) to provide independent analysis

Economic and Fiscal Assessment Update Ottawa, Canada November 2, 29 www.parl.gc.ca/pbo-dpb The Federal Accountability Act mandates the Parliamentary Budget Officer (PBO) to provide independent analysis

Spring Forecast: slowly recovering from a protracted recession

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

Session 11. Fiscal Policy

Session 11. Fiscal Policy Government size Budget balances Fiscal Policy over the business cycle Debt and sustainability Understanding Fiscal Policy: Government size Government size varies across countries.

Session 11. Fiscal Policy Government size Budget balances Fiscal Policy over the business cycle Debt and sustainability Understanding Fiscal Policy: Government size Government size varies across countries.

Short-term indicators and Updated Forecasts. Eurozone NOVEMBER 2016

Short-term indicators and Updated Forecasts Eurozone NOVEMBER 2016 EUROZONE WATCH NOVEMBER 2016 Key messages: resilience and unchanged projections The moderate pace of economic growth continued in the

Short-term indicators and Updated Forecasts Eurozone NOVEMBER 2016 EUROZONE WATCH NOVEMBER 2016 Key messages: resilience and unchanged projections The moderate pace of economic growth continued in the

Macroeconomic Outlook November 2015

Macroeconomic Outlook November 2015 Philippe WAECHTER Head of Economic Research My twitter account @phil_waechter or http://twitter.com/phil_waechter My blog http://philippewaechter.en.nam.natixis.com

Macroeconomic Outlook November 2015 Philippe WAECHTER Head of Economic Research My twitter account @phil_waechter or http://twitter.com/phil_waechter My blog http://philippewaechter.en.nam.natixis.com

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Global Economy & the Machine Tool Outlook. Jan 2010 Rhys Herbert

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

FISCAL MONITOR SELECTED TOPICS

FISCAL MONITOR Fiscal Monitor Archives Navigating the Fiscal Challenges Ahead May 2010 Fiscal Exit: From Strategy to Implementation November 2010 Shifting Gears April 2011 Addressing Fiscal Challenges

FISCAL MONITOR Fiscal Monitor Archives Navigating the Fiscal Challenges Ahead May 2010 Fiscal Exit: From Strategy to Implementation November 2010 Shifting Gears April 2011 Addressing Fiscal Challenges

Progress towards Strong, Sustainable and Balanced Growth. Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction)

") Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

December 2018 Eurosystem staff macroeconomic projections for the euro area 1

December 2018 Eurosystem staff macroeconomic projections for the euro area 1 Real GDP growth weakened unexpectedly in the third quarter of 2018, partly reflecting temporary production bottlenecks experienced

December 2018 Eurosystem staff macroeconomic projections for the euro area 1 Real GDP growth weakened unexpectedly in the third quarter of 2018, partly reflecting temporary production bottlenecks experienced

PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions JOHN W. BECK Senior Vice President Co-Director, Global Fixed Income Franklin

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions JOHN W. BECK Senior Vice President Co-Director, Global Fixed Income Franklin

The ECB Survey of Professional Forecasters. First quarter of 2017

The ECB Survey of Professional Forecasters First quarter of 217 January 217 Contents 1 Near-term inflation expectations a little higher, due to oil price rises 3 2 Longer-term inflation expectations unchanged

The ECB Survey of Professional Forecasters First quarter of 217 January 217 Contents 1 Near-term inflation expectations a little higher, due to oil price rises 3 2 Longer-term inflation expectations unchanged

The role of central banks and governments in the crisis

The role of central banks and governments in the crisis 87 th Kieler Konjunkturgespräch Kiel, March 18/19 2013 Joachim Scheide, Kiel Institute for the World Economy After the synchronous downturn we now

The role of central banks and governments in the crisis 87 th Kieler Konjunkturgespräch Kiel, March 18/19 2013 Joachim Scheide, Kiel Institute for the World Economy After the synchronous downturn we now

Maintaining Price Stability with Unconventional Monetary Policy

Peter Praet Member of the Executive Board of the European Central Bank Maintaining Price Stability with Unconventional Monetary Policy Council of the European Union Brussels, 29 January 218 Global PMI

Peter Praet Member of the Executive Board of the European Central Bank Maintaining Price Stability with Unconventional Monetary Policy Council of the European Union Brussels, 29 January 218 Global PMI

46 ECB FISCAL CHALLENGES FROM POPULATION AGEING: NEW EVIDENCE FOR THE EURO AREA

Box 4 FISCAL CHALLENGES FROM POPULATION AGEING: NEW EVIDENCE FOR THE EURO AREA Ensuring the long-term sustainability of public finances in the euro area and its member countries is a prerequisite for the

Box 4 FISCAL CHALLENGES FROM POPULATION AGEING: NEW EVIDENCE FOR THE EURO AREA Ensuring the long-term sustainability of public finances in the euro area and its member countries is a prerequisite for the

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

North American Economic Outlook: Will the Recovery Be Sustained? U.S. Economic Outlook:

ECONOMICS I RESEARCH North American Economic Outlook: Will the Recovery Be Sustained? Presentation to the Canadian Association of Movers 11 Annual Conference Paul Ferley(1) 97-71 Assistant Chief Economist

ECONOMICS I RESEARCH North American Economic Outlook: Will the Recovery Be Sustained? Presentation to the Canadian Association of Movers 11 Annual Conference Paul Ferley(1) 97-71 Assistant Chief Economist

Demographics, Structural Reform and the Growth Outlook for Europe

Demographics, Structural Reform and the Growth Outlook for Europe Karl Whelan University College Dublin Kieran McQuinn ESRI Presentation at UCD October 30, 2014 Debt Crisis or Growth Crisis? Highly indebted

Demographics, Structural Reform and the Growth Outlook for Europe Karl Whelan University College Dublin Kieran McQuinn ESRI Presentation at UCD October 30, 2014 Debt Crisis or Growth Crisis? Highly indebted

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Eurozone. EY Eurozone Forecast December 2013

Eurozone EY Eurozone Forecast December 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Cyprus Severe

Eurozone EY Eurozone Forecast December 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Cyprus Severe

Outlook for the Irish Economy

Outlook for the Irish Economy Reamonn Lydon Irish Institute of Pensions Management October 2014 A caveat these are my views only Not mine Overview Latest projections, 2014 Bulletin 4 Short- / Medium-term

Outlook for the Irish Economy Reamonn Lydon Irish Institute of Pensions Management October 2014 A caveat these are my views only Not mine Overview Latest projections, 2014 Bulletin 4 Short- / Medium-term

Economic recovery and employment in the EU. Raymond Torres, Director, ILO Research Department

Economic recovery and employment in the EU Raymond Torres, Director, ILO Research Department Outline of presentation I. Situation in the EU versus Japan and the US II. Role of macroeconomic policies and

Economic recovery and employment in the EU Raymond Torres, Director, ILO Research Department Outline of presentation I. Situation in the EU versus Japan and the US II. Role of macroeconomic policies and

Projections for the Portuguese Economy:

Projections for the Portuguese Economy: 2018-2020 March 2018 BANCO DE PORTUGAL E U R O S Y S T E M BANCO DE EUROSYSTEM PORTUGAL Projections for the portuguese economy: 2018-20 Continued expansion of economic

Projections for the Portuguese Economy: 2018-2020 March 2018 BANCO DE PORTUGAL E U R O S Y S T E M BANCO DE EUROSYSTEM PORTUGAL Projections for the portuguese economy: 2018-20 Continued expansion of economic

Macro Focus. From austerity to growth? 30 May Group Economics Macro Research

Macro Focus From austerity to growth? Group Economics Macro Research Nick Kounis Tel: +31 20 343 5616 Aline Schuiling Tel: +31 20 343 5606 30 May 2013 Europe has changed its approach. The European Commission

Macro Focus From austerity to growth? Group Economics Macro Research Nick Kounis Tel: +31 20 343 5616 Aline Schuiling Tel: +31 20 343 5606 30 May 2013 Europe has changed its approach. The European Commission

FORECAST OF OREGON S ECONOMY IN 2013: DISAPPOINTING BUT NOT DISASTROUS

FORECAST OF OREGON S ECONOMY IN 2013: DISAPPOINTING BUT NOT DISASTROUS ERIC FRUITS Editor and Adjunct Professor, Portland State University During a recent presentation that I made to the Roseburg Chamber

FORECAST OF OREGON S ECONOMY IN 2013: DISAPPOINTING BUT NOT DISASTROUS ERIC FRUITS Editor and Adjunct Professor, Portland State University During a recent presentation that I made to the Roseburg Chamber

Session 12. The New Normal. Deflation and Zero Lower Bound.

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

CHAPTER 4 PROSPECTS FOR GROWTH AND IMBALANCES BEYOND THE SHORT TERM. Introduction and summary

CHAPTER 4 PROSPECTS FOR GROWTH AND IMBALANCES BEYOND THE SHORT TERM Introduction and summary Balanced growth must be restored after the crisis Policy options are illustrated by means of variant scenarios

CHAPTER 4 PROSPECTS FOR GROWTH AND IMBALANCES BEYOND THE SHORT TERM Introduction and summary Balanced growth must be restored after the crisis Policy options are illustrated by means of variant scenarios

Fund Management Diary

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

Fund Management Diary Meeting held on 16 th October 2018 Euro-zone competitiveness imbalances In the run up to the global financial crisis differing competitiveness levels across the euro-zone contributed

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

RECENT ECONOMIC DEVELOPMENTS IN SOUTH AFRICA

RECENT ECONOMIC DEVELOPMENTS IN SOUTH AFRICA Remarks by Mr AD Mminele, Deputy Governor of the South African Reserve Bank, at the Citigroup Global Issues Seminar, held at the Ritz Carlton Hotel in Istanbul,

RECENT ECONOMIC DEVELOPMENTS IN SOUTH AFRICA Remarks by Mr AD Mminele, Deputy Governor of the South African Reserve Bank, at the Citigroup Global Issues Seminar, held at the Ritz Carlton Hotel in Istanbul,

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Study Questions. Lecture 15 International Macroeconomics

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Stability, Cohesion and Growth

Stability, Cohesion and Growth April 23, 2012 Swedish Minister for Finance Anders Borg Agenda Sweden has weathered the current crisis relatively well Lessons from the crisis in the early 1990s Further

Stability, Cohesion and Growth April 23, 2012 Swedish Minister for Finance Anders Borg Agenda Sweden has weathered the current crisis relatively well Lessons from the crisis in the early 1990s Further

Commission takes steps under the excessive deficit procedure for France, Greece, Ireland, Spain and UK; assesses Stability Programme of Cyprus

IP/09/458 Brussels, 24 March 2009 Commission takes steps under the excessive deficit procedure for France, Greece, Ireland, Spain and UK; assesses Stability Programme of Cyprus Following the assessment,

IP/09/458 Brussels, 24 March 2009 Commission takes steps under the excessive deficit procedure for France, Greece, Ireland, Spain and UK; assesses Stability Programme of Cyprus Following the assessment,

The main assumptions underlying the scenario are as follows (see the table):

:") . PROJECTIONS The projections for the Italian economy presented in this Economic Bulletin update those prepared as part of the Eurosystem staff macroeconomic projections, which were based on information

. PROJECTIONS The projections for the Italian economy presented in this Economic Bulletin update those prepared as part of the Eurosystem staff macroeconomic projections, which were based on information

2.10 PROJECTIONS. Macroeconomic scenario for Italy (percentage changes on previous year, unless otherwise indicated)

") . PROJECTIONS The projections for growth and inflation presented in this Economic Bulletin point to a strengthening of the economic recovery in Italy (Table ), based on the assumption that the weaker stimulus

. PROJECTIONS The projections for growth and inflation presented in this Economic Bulletin point to a strengthening of the economic recovery in Italy (Table ), based on the assumption that the weaker stimulus

Spanish economic outlook. June 2017

Spanish economic outlook June 2017 1 2 3 Spanish economy a pleasant surprise Growth drivers Forecasts once again bright One of the most dynamic economies in Europe Spain growing at a faster rate than EMU

Spanish economic outlook June 2017 1 2 3 Spanish economy a pleasant surprise Growth drivers Forecasts once again bright One of the most dynamic economies in Europe Spain growing at a faster rate than EMU

Eurozone Economic Watch. November 2017

Eurozone Economic Watch November 2017 Eurozone: improved outlook, still subdued inflation Our MICA-BBVA model for growth estimates for the moment a quarterly GDP figure of around -0.7% in, after % QoQ

Eurozone Economic Watch November 2017 Eurozone: improved outlook, still subdued inflation Our MICA-BBVA model for growth estimates for the moment a quarterly GDP figure of around -0.7% in, after % QoQ

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE GLOBAL TRENDS Accelerating growth in advanced economies (US, UK, Eurozone) vs. Slowdown in almost all emerging markets Downward revisions

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE GLOBAL TRENDS Accelerating growth in advanced economies (US, UK, Eurozone) vs. Slowdown in almost all emerging markets Downward revisions

LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

The ECB Survey of Professional Forecasters. Second quarter of 2017

The ECB Survey of Professional Forecasters Second quarter of 17 April 17 Contents 1 Near-term headline inflation expectations revised up, expectations for HICP inflation excluding food and energy broadly

The ECB Survey of Professional Forecasters Second quarter of 17 April 17 Contents 1 Near-term headline inflation expectations revised up, expectations for HICP inflation excluding food and energy broadly

Erdem Başçi: Recent economic and financial developments in Turkey

Erdem Başçi: Recent economic and financial developments in Turkey Speech by Mr Erdem Başçi, Governor of the Central Bank of the Republic of Turkey, at the press conference for the presentation of the April

Erdem Başçi: Recent economic and financial developments in Turkey Speech by Mr Erdem Başçi, Governor of the Central Bank of the Republic of Turkey, at the press conference for the presentation of the April

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Monetary Policy Statement: March 2010

Central Bank of the Solomon Islands Monetary Policy Statement: March 2010 Central Bank of the Solomon Islands PO Box 634, Honiara, Solomon Islands Tel: (677) 21791 Fax: (677) 23513 www.cbsi.com.sb 1.Money

Central Bank of the Solomon Islands Monetary Policy Statement: March 2010 Central Bank of the Solomon Islands PO Box 634, Honiara, Solomon Islands Tel: (677) 21791 Fax: (677) 23513 www.cbsi.com.sb 1.Money

Recent developments and challenges for the Portuguese economy

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Research US The outlook for US government debt

Investment Research General Market Conditions 3 September Research US The outlook for US government debt US net debt has risen fast during the recent recession, to more than from 36% in 7. Compared with

Investment Research General Market Conditions 3 September Research US The outlook for US government debt US net debt has risen fast during the recent recession, to more than from 36% in 7. Compared with

Welcome to Canada. I welcome the opportunity to share with you the journey our national pension plan has been on over the past 15 years.

Welcome to Canada. I welcome the opportunity to share with you the journey our national pension plan has been on over the past 15 years. I have a short presentation, and then will be happy to answer any

Welcome to Canada. I welcome the opportunity to share with you the journey our national pension plan has been on over the past 15 years. I have a short presentation, and then will be happy to answer any

FISCAL MONITOR SELECTED TOPICS

FISCAL MONITOR SELECTED TOPICS Fiscal Monitor Archives Navigating the Fiscal Challenges Ahead May 2010 Fiscal Exit: From Strategy to Implementation November 2010 Shifting Gears April 2011 Addressing Fiscal

FISCAL MONITOR SELECTED TOPICS Fiscal Monitor Archives Navigating the Fiscal Challenges Ahead May 2010 Fiscal Exit: From Strategy to Implementation November 2010 Shifting Gears April 2011 Addressing Fiscal

ff~ ~J~#~r~~.Q(n\. 05-i/y,5. Rome, May 2017 ear Pierre, ~ (/ om,:;s

a ff J#r.Q(n\. 05i/y,5. Rome, 30 111 May 2017 ear Pierre, (/ om,:;s I welcome the thrust of the 2017 European Semester package issued on May 22nd, notably the key objectives to deliver more jobs and faster

a ff J#r.Q(n\. 05i/y,5. Rome, 30 111 May 2017 ear Pierre, (/ om,:;s I welcome the thrust of the 2017 European Semester package issued on May 22nd, notably the key objectives to deliver more jobs and faster

Jean-Pierre Roth: Recent economic and financial developments in Switzerland

Jean-Pierre Roth: Recent economic and financial developments in Switzerland Introductory remarks by Mr Jean-Pierre Roth, Chairman of the Governing Board of the Swiss National Bank and Chairman of the Board

Jean-Pierre Roth: Recent economic and financial developments in Switzerland Introductory remarks by Mr Jean-Pierre Roth, Chairman of the Governing Board of the Swiss National Bank and Chairman of the Board

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an