Session 12. The New Normal. Deflation and Zero Lower Bound.

|

|

|

- Sibyl Beasley

- 5 years ago

- Views:

Transcription

1 Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession

2 Deflation and the Zero Lower Bound Trap Deflation is defined as a decline in the aggregate price level. Hence deflation is simply negative inflation. Deflation can be seen as a natural adjustment to weak economic conditions (this is how equilibrium can be restored). In a scenario where nominal interest rates get to zero and because nominal interest rates cannot become negative, additional deflation will make real interest rates increase and reduce growth rates. Traditional monetary policy (lowering interest rates) cannot help and the economy enters a trap of decreased demand, lower GDP growth and even more deflation that further increases real interest rates.

3 Deflation and the Zero Lower Bound Trap In a deep recession the low level of spending relative to income (the excess of saving relative to investment) might require a negative (real) interest rate. (real) Interest Rate Investment Saving

4 Deflation and Default Inflation (positive or negative) can produce a redistribution of wealth across borrowers and lenders. Negative inflation (deflation) raises the real value of debt so it redistributes wealth from borrowers to savers. Higher (real) debt will deter consumption and it can also lead to default (as borrowers are hurt) Default can spread over to the financial system as the number of bad loans increases (and possibly banks face the same real increase in their value of their debt).

5 Financial Crisis: Liquidity, Flight to Quality and Banking Crises In times of uncertainty there is an increase in the demand for liquid assets (currency, government debt). Banks operate in a fractional-reserve system (their liquidity or reserves do not cover all deposits). Their business is to transform short-term liabilities (deposits) into long-term assets (loans, mortgages). An increase in the demand for liquidity can lead a healthy financial institution to become illiquid. Only the central bank can provide the necessary liquidity. An illiquid bank can lead to a bank run: in particular in the absence of insurance on bank deposits, customers will withdraw their deposits as they worry about insolvency. A bank run increases the demand for liquidity and can lead to a collapse of of the banking system.

6 Banking Crisis: The Unstable Balance Sheet of Banks Commercial Bank Balance Sheet Assets Deposits at Central Bank & Cash Securities (Short & Long Term) Loans to Customers (Short & Long Term) Liabilities Deposits of Customers (Short Term) Loans from Central Bank (Short Term) Debt (Short and Long Term) Equity

7 Banking Crisis: Balance Sheet of Lehman Brothers February 29, 2008 (Billions of USD) Assets Liabilities Cash Accounts payable Receivables ST debt Long Term Investments Other current liabilities Other LT assets Long term debt Equity Total Total

8 The Great Depression: Background The Gold Standard. The gold standard was adopted in most countries around the world in the years between 1870 and This adoption ended a long period of bi-metallic standard in which both gold and silver were used to back the money in circulation. During WWI several countries suspended the gold standard but later it was resumed again (e.g. Britain resumed the gold standard in 1925). The Gold Standard imposes constraints on the way central banks can run their monetary policy and provide liquidity in times when needed. The Great Depression was a world-wide phenomenon every industrialized country underwent some decline in economic activity. For many of these countries the Great Depression led to a sharp increase in unemployment, decline in output and in the abandonment of the Gold Standard (1933 in the US). Usually we consider the years as the period that we call The Great Depression.

9 The Great Depression (US)

10 The Great Depression (US)

11 The Great Depression: Role of the Central Bank Monetary Base (Currency + Reserves) Money Supply (M1) Jan-28 Jan-29 Jan-30 Jan-31 Jan-32 Jan-33 Jan-34 Jan-35 Jan Jan-28 Jan-29 Jan-30 Jan-31 Jan-32 Jan-33 Jan-34 Jan-35 Jan Price level 1000 Real money balances (M1/P) Jan-28 Jan-29 Jan-30 Jan-31 Jan-32 Jan-33 Jan-34 Jan-35 Jan Jan-28 Jan-29 Jan-30 Jan-31 Jan-32 Jan-33 Jan-34 Jan-35 Jan-36

12 The Great Depression: Role of the Central Bank Money Multiplier (C/D + 1)/(C/D+ R/D) Jan-28 Jan-29 Jan-30 Jan-31 Jan-32 Jan-33 Jan-34 Jan-35 Jan-36

13 The Great Depression: Role of the Central Bank Ratios Currency-to-deposit ratio (C/D) 10 Reserves-to-deposit ratio (R/D) 6 Jan-28 Jan-29 Jan-30 Jan-31 Jan-32 Jan-33 Jan-34 Jan-35 Jan-36

14 The Great Recession Monetary Base (C+R) and Money Supply M1 (C+D) M Monetary Base

15 The Great Recession Money Multiplier = Money Supply / Monetary Base= = (C/D + 1)/(C/D+ R/D)

16 The Great Recession Ratios Currency-to-deposit ratio (C/D) Reserves-to-deposit ratio (R/D)

17 The Great Depression versus the Great Recession The absence of a deposit insurance mechanism combined with the reluctance of the central bank to serve as the lender of last resort was a key reason for the dramatic output collapse during the Great Depression. In the 2008 crisis the central bank acted in a very different manner. It provided as much liquidity as necessary through several Quantitative Easing rounds. While the US and Europe still faced a deep crisis, they managed to avoid a much worse outcome.

18 When Interest Rates Reach Zero: Quantitative Easing US Federal Reserve Balance Sheet Assets Loans to Commercial Banks Securities Liabilities Currency Deposits of Commercial Banks Commercial Banks Balance sheet Assets Deposits at Central Bank Loans to Customers Securities Liabilities Deposits from Customers Loans from Central Bank

19 When Interest Rates Reach Zero: Quantitative Easing Balance sheet of a Central Bank Assets Liabilities Loans to banks Securities 755 1,846 2,159 Govt ,010 Agency+MBS 0 1,069 1,149 Currency Reserves 43 1,139 1,078 Balance sheet of commercial banks Assets Liabilities Securities Loans Reserves 43 1,139 1,078 Deposits Loans from Central Bank All figures from US Federal Reserve. End of the year. Billions of USD.

20 When Interest Rates Reach Zero: Quantitative Easing

21 Bailout or Profit-Making Provision of Liquidity?

22 Reminder of the Cost of Banking Crisis Governments (not central banks) step in during banking crises and bail out banks by providing capital or taking ownership of private banks. Some examples: US Savings and Loans crisis (80s/90s) $124 billion (about 1% of GDP) Sweden early 90 s: spent 4% of GDP with a final cost of 2% Ireland : Guarantees of Euro 70 billion (25% of GDP) England : Loan/Share Purchases Billion Pounds (8.5% GDP) + Guarantees of 332 billion Pounds. Spain 2012: Billion (3%-7% of GDP)

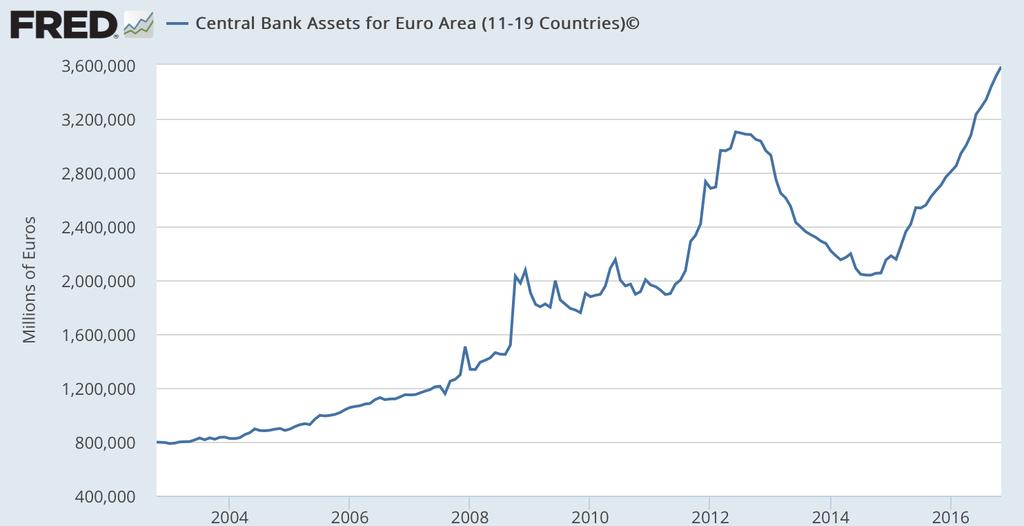

23 The Slow-Acting ECB Unlike the US Federal Reserve, the ECB did not engage in Quantitative Easing. It raised interest rates in 2011 under the assumption that the crisis was over. It then engage in giving loans to commercial loans with three-year maturity but banks quickly returned the loans and sent the balance sheet of the ECB towards normal levels. It only engaged in Quantitative Easing after the Euro area had already fallen into a second recession.

24 The Slow-Acting ECB ECB Balance Sheet (First Round of Monetary Expansion) Assets Loans to Commercial Banks Securities Liabilities Currency Deposits of Commercial Banks Commercial Banks Balance sheet Assets Deposits at Central Bank Loans to Customers Securities Liabilities Deposits from Customers Loans from Central Bank

25 The Slow-Acting ECB

26 Bank of Japan

27 Deflation in Japan Real GDP Growth Inflation

28 The Exit Strategy How will Central Banks control monetary policy when the economy goes back to normal? It can undo all purchases of securities. But wouldn t this put upward pressure on interest rate? Yes, but that s what monetary policy does during an expansion, it follows with higher interest rates. It can also keep the securities and simply raise interest rates on reserves to control inflation.

29 The Exit Strategy Central Bank Balance Sheet Assets Loans to Commercial Banks Securities Liabilities Currency Deposits of Commercial Banks Commercial Banks Balance sheet Assets Deposits at Central Bank Loans to Customers Securities Liabilities Deposits from Customers Loans from Central Bank

30 Session 12: Summary Interest rates adjust to the state of the business cycle. When inflation is low nominal interest rates should be low. If inflation gets close to zero or becomes negative, interest rates reach the zero lower bound and this might become a trap.

ECN 106 Macroeconomics 1. Lecture 10

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Coping with the Zero Nominal Bound

Economics 196 Spring 2012 David Romer Coping with the Zero Nominal Bound April 3, 2012 A Couple of Ground Rules No electronic devices. I expect you to participate. I. INTRODUCTION Unemployment has been

Economics 196 Spring 2012 David Romer Coping with the Zero Nominal Bound April 3, 2012 A Couple of Ground Rules No electronic devices. I expect you to participate. I. INTRODUCTION Unemployment has been

OCR Economics A-level

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.5 Approaches to policy and macroeconomic context Notes Explain why approaches to macroeconomic policy change in accordance

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.5 Approaches to policy and macroeconomic context Notes Explain why approaches to macroeconomic policy change in accordance

The Federal Reserve System and Open Market Operations

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

Session 8. Business Cycles in a Closed Economy.

Session 8. Business Cycles in a Closed Economy. Building a Model of Aggregate Demand Money Market: The LM Curve Goods Market: The IS Curve A Graphical Representation of the Equilibrium: The IS/LM Model

Session 8. Business Cycles in a Closed Economy. Building a Model of Aggregate Demand Money Market: The LM Curve Goods Market: The IS Curve A Graphical Representation of the Equilibrium: The IS/LM Model

Answers to Questions: Chapter 8

Answers to Questions in Textbook 1 Answers to Questions: Chapter 8 1. In microeconomics, the demand curve shows the various quantities of a specific product that a consumer wants at various prices for

Answers to Questions in Textbook 1 Answers to Questions: Chapter 8 1. In microeconomics, the demand curve shows the various quantities of a specific product that a consumer wants at various prices for

In January 2017 UK Public sector net debt is 1,682.8 billion equivalent to 85.3% of GDP

UK National Debt Budget deficit annual borrowing... 2 UK net borrowing... 3 UK net borrowing as % of GDP... 3 Deficit down but debt up?... 4 Debt as % of GDP... 4 Recent history of UK National Debt...

UK National Debt Budget deficit annual borrowing... 2 UK net borrowing... 3 UK net borrowing as % of GDP... 3 Deficit down but debt up?... 4 Debt as % of GDP... 4 Recent history of UK National Debt...

Economic state of the union, EuroMemo Engelbert Stockhammer Kingston University

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

The Outlook for the European and the German Economy

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Great Recession. Prof. Eric Sims. Fall University of Notre Dame

Great Recession Prof. Eric Sims University of Notre Dame Fall 25 / 28 Overview Worst economic contraction since Great Depression (by most measures) Could do entire course on the subject We will do a very

Great Recession Prof. Eric Sims University of Notre Dame Fall 25 / 28 Overview Worst economic contraction since Great Depression (by most measures) Could do entire course on the subject We will do a very

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri Name (print): Name (signature): Section Registered (circle one): T 1:30 T 6:00 W 1:30 As always, the honor code rules are in effect. You know

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri Name (print): Name (signature): Section Registered (circle one): T 1:30 T 6:00 W 1:30 As always, the honor code rules are in effect. You know

The Monetary System: What It Is and How It Works

4 The Monetary System: What It Is and How It Works CHAPTER 5 Inflation Modified by Ming Yi 2016 Worth Publishers, all rights reserved 3 IN THIS CHAPTER, YOU WILL LEARN: The definition, functions, and types

4 The Monetary System: What It Is and How It Works CHAPTER 5 Inflation Modified by Ming Yi 2016 Worth Publishers, all rights reserved 3 IN THIS CHAPTER, YOU WILL LEARN: The definition, functions, and types

Introduction. ECON204 Notes. Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

The Great Depression, golden age, and global financial crisis

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.

During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity.") Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Thoughts and Concerns: 1) During the July to September quarter the financial turmoil surrounding Greece and Europe increased in its intensity. In an effort to support the European banking system (and indirectly

Aggregate Expenditure and Equilibrium Output. The Core of Macroeconomic Theory. Aggregate Output and Aggregate Income (Y)

") C H A P T E R 8 Aggregate Expenditure and Equilibrium Output Prepared by: Fernando Quijano and Yvonn Quijano The Core of Macroeconomic Theory 2of 31 Aggregate Output and Aggregate Income (Y) Aggregate

C H A P T E R 8 Aggregate Expenditure and Equilibrium Output Prepared by: Fernando Quijano and Yvonn Quijano The Core of Macroeconomic Theory 2of 31 Aggregate Output and Aggregate Income (Y) Aggregate

Chapter 21: Study Questions Key, Version A

Chapter 21: Study Questions Key, Version A Name: Class (day & time): Discussing the concepts and working examples with others is allowable. However, receiving answers from someone else, and turning these

Chapter 21: Study Questions Key, Version A Name: Class (day & time): Discussing the concepts and working examples with others is allowable. However, receiving answers from someone else, and turning these

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks September 26, 2013 by Andrew Balls of PIMCO In the following interview, Andrew Balls, managing director and head of European portfolio

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks September 26, 2013 by Andrew Balls of PIMCO In the following interview, Andrew Balls, managing director and head of European portfolio

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Econ 330 Spring 2017: FINAL EXAM Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Tobin's q theory suggests that monetary

Econ 330 Spring 2017: FINAL EXAM Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Tobin's q theory suggests that monetary

III. 9. IS LM: the basic framework to understand macro policy continued Text, ch 11

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Economic Outlook. Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis. NLB,LLC The Lodge, Des Peres, MO.

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

Economic Outlook Christopher J. Neely Assistant Vice President, Federal Reserve Bank of St. Louis NLB,LLC The Lodge, Des Peres, MO April 8, 2010 The opinions expressed are my own and not necessarily those

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM. April 10, Prof. Bill Even FORM 1. Directions

Name ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM April 10, 2008 Prof. Bill Even FORM 1 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth

Name ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM April 10, 2008 Prof. Bill Even FORM 1 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth

Econ 102 Exam 2 Name ID Section Number

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

The Government Deficit and the Financial Crisis

The Government Deficit and the Financial Crisis The 2008 financial crisis has resulted in a huge increase in the federal government deficit. Government spending has increased significantly, and tax revenue

The Government Deficit and the Financial Crisis The 2008 financial crisis has resulted in a huge increase in the federal government deficit. Government spending has increased significantly, and tax revenue

ECON 3010 Intermediate Macroeconomics. Chapter 4 The Monetary System: What It Is and How It Works

ECON 3010 Intermediate Macroeconomics Chapter 4 The Monetary System: What It Is and How It Works Money: Definition Money is the stock of assets that can be readily used to make transactions. Money: Functions

ECON 3010 Intermediate Macroeconomics Chapter 4 The Monetary System: What It Is and How It Works Money: Definition Money is the stock of assets that can be readily used to make transactions. Money: Functions

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Macroeconomic projections for Assumptions from the external surrounding. Baseline macroeconomic scenario for

Dimitar Bogov Governor November, Macroeconomic projections for -4 Assumptions from the external surrounding Baseline macroeconomic scenario for -4 Comparison with the previous projection In the period

Dimitar Bogov Governor November, Macroeconomic projections for -4 Assumptions from the external surrounding Baseline macroeconomic scenario for -4 Comparison with the previous projection In the period

International Money and Banking: 13. Default Risk and Collateral

International Money and Banking: 13. Default Risk and Collateral Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Default Risk and Collateral Spring 2018 1 / 13 Moving Beyond Risk-Free

International Money and Banking: 13. Default Risk and Collateral Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Default Risk and Collateral Spring 2018 1 / 13 Moving Beyond Risk-Free

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

chapter: >> Income and Expenditure WHAT YOU WILL LEARN IN THIS CHAPTER Krugman/Wells The Multiplier: An Informal Introduction

chapter: 11 >> Income and Expenditure Krugman/Wells WHAT YOU WILL LEARN IN THIS CHAPTER The nature of the multiplier, which shows how initial changes in spending lead to further changes. The meaning of

chapter: 11 >> Income and Expenditure Krugman/Wells WHAT YOU WILL LEARN IN THIS CHAPTER The nature of the multiplier, which shows how initial changes in spending lead to further changes. The meaning of

The main lessons to be drawn from the European financial crisis

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

Answers to Questions: Chapter 5

Answers to Questions: Chapter 5 1. Figure 5-1 on page 123 shows that the output gaps fell by about the same amounts in Japan and Europe as it did in the United States from 2007-09. This is evidence that

Answers to Questions: Chapter 5 1. Figure 5-1 on page 123 shows that the output gaps fell by about the same amounts in Japan and Europe as it did in the United States from 2007-09. This is evidence that

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

I. Learning Objectives II. The Income-Consumption and Income-Saving Relationships

I. Learning Objectives In this chapter students will learn: A. How changes in income affect consumption (and saving). B. About factors other than income that can affect consumption. C. How changes in real

I. Learning Objectives In this chapter students will learn: A. How changes in income affect consumption (and saving). B. About factors other than income that can affect consumption. C. How changes in real

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING Prof. Bill Even FORM 3. Directions

1 ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING 2013 Prof. Bill Even FORM 3 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth the equivalent

1 ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING 2013 Prof. Bill Even FORM 3 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth the equivalent

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 11

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 11 THE ZERO LOWER BOUND IN PRACTICE FEBRUARY 26, 2018 I. INTRODUCTION II. TWO EPISODES AT THE ZERO

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 11 THE ZERO LOWER BOUND IN PRACTICE FEBRUARY 26, 2018 I. INTRODUCTION II. TWO EPISODES AT THE ZERO

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Advanced Macroeconomics 4. The Zero Lower Bound and the Liquidity Trap

Advanced Macroeconomics 4. The Zero Lower Bound and the Liquidity Trap Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) The Zero Lower Bound Spring 2015 1 / 26 Can Interest Rates Be Negative?

Advanced Macroeconomics 4. The Zero Lower Bound and the Liquidity Trap Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) The Zero Lower Bound Spring 2015 1 / 26 Can Interest Rates Be Negative?

Joseph S Tracy: A strategy for the 2011 economic recovery

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Financial Crises and the Great Recession

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Professor Christina Romer. LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018 I. OVERVIEW II. THE MONEY MARKET, THE FEDERAL RESERVE, AND INTEREST

Economics 2 Spring 2018 Professor Christina Romer Professor David Romer LECTURE 22 FINANCIAL MARKETS AND MONETARY POLICY April 12, 2018 I. OVERVIEW II. THE MONEY MARKET, THE FEDERAL RESERVE, AND INTEREST

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Session 16. Review Session

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Game-Changers in the Era of Dissonance

Game-Changers in the Era of Dissonance The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation

Game-Changers in the Era of Dissonance The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation

The Recession

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

The 2007-2009 Recession 1. Originins in the Housing Market 2. Financial Crisis 3. Recession and Liquidity Trap 4. Policy Responses and the Zero Lower Bound Housing Market A sharp decline in house prices

Bank as a supplier of liquidity

Fall 2008 International Corporate Finance I LECTURE 10 Banking Crisis and Regulatory Responses Tokuo Iwaisako HITOTSUBASHI UNIVERSITY 1 Bank as a supplier of liquidity Diamond and Dybvig (1983), Journal

Fall 2008 International Corporate Finance I LECTURE 10 Banking Crisis and Regulatory Responses Tokuo Iwaisako HITOTSUBASHI UNIVERSITY 1 Bank as a supplier of liquidity Diamond and Dybvig (1983), Journal

Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

QUANTITATIVE EASING: WHAT MIGHT MILTON FRIEDMAN HAVE SAID?

QUANTITATIVE EASING: WHAT MIGHT MILTON FRIEDMAN HAVE SAID? COMMENTS TO THE ECONOMIC CLUB OF SHEBOYGAN APRIL 20, 2016 Paul L. Kasriel econtrarian@gmail.com Econtrarian, LLC 920-818-0236 The Econtrarian

QUANTITATIVE EASING: WHAT MIGHT MILTON FRIEDMAN HAVE SAID? COMMENTS TO THE ECONOMIC CLUB OF SHEBOYGAN APRIL 20, 2016 Paul L. Kasriel econtrarian@gmail.com Econtrarian, LLC 920-818-0236 The Econtrarian

To understand where the U.S. Economy is going, we need to understand where we have been

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Y669 International Political Economy. September 21, 2010

Y669 International Political Economy September 21, 2010 What is an exchange rate? The price of a currency expressed in terms of other currencies or gold. What the International Monetary System Has to Do

Y669 International Political Economy September 21, 2010 What is an exchange rate? The price of a currency expressed in terms of other currencies or gold. What the International Monetary System Has to Do

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Which of the following is not an accurate statement of core capital goods? A) proxy for business investments B) does not include transportation equipment C)

Econ 102 Final Exam Name ID Section Number 1. Which of the following is not an accurate statement of core capital goods? A) proxy for business investments B) does not include transportation equipment C)

In addition, the sample portfolio ended the quarter with 100% invested in cash equivalent and fixed income investments.

Review: Sample Income Portfolio In the past quarter, the portfolio s value was impacted by the following changes in market values Bonds and preferred shares increased by $472.47 Deposits of interest and

Review: Sample Income Portfolio In the past quarter, the portfolio s value was impacted by the following changes in market values Bonds and preferred shares increased by $472.47 Deposits of interest and

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM?

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM? Jean-Pierre Aubry, Associate Fellow, CIRANO Annual conference of the Canadian Economic Association HEC, Montréal, May 30th

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM? Jean-Pierre Aubry, Associate Fellow, CIRANO Annual conference of the Canadian Economic Association HEC, Montréal, May 30th

Money, Banking, and Finance PLATO Global Government and Economics Mastery Test

Money, Banking, and Finance PLATO Global Government and Economics Mastery Test 1. Money is useful to people because it is: a. a medium of exchange b. prestigious c. nice to look at d. something that makes

Money, Banking, and Finance PLATO Global Government and Economics Mastery Test 1. Money is useful to people because it is: a. a medium of exchange b. prestigious c. nice to look at d. something that makes

Warm ups *What are two examples of people not included in the unemployment rate?

Warm ups 8.31.2017 *What are two examples of people not included in the unemployment rate? *What are the four major types of spending used to calculate GDP? Lesson Objective: *describe four phases of business

Warm ups 8.31.2017 *What are two examples of people not included in the unemployment rate? *What are the four major types of spending used to calculate GDP? Lesson Objective: *describe four phases of business

No. 3 BANK OF RUSSIA FOREIGN EXCHANGE ASSET MANAGEMENT REPORT. Moscow

No. 3 2015 FOREIGN EXCHANGE ASSET MANAGEMENT REPORT Moscow Bank of Russia Foreign Exchange Asset Management Report 2015 Reference to the Central Bank of the Russian Federation is mandatory in case of reproduction.

No. 3 2015 FOREIGN EXCHANGE ASSET MANAGEMENT REPORT Moscow Bank of Russia Foreign Exchange Asset Management Report 2015 Reference to the Central Bank of the Russian Federation is mandatory in case of reproduction.

MACROECONOMICS IN THE GLOBAL ECONOMY

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Professor Antonio Fatás Final Exam February 23, 2015 Instructions: (PLEASE READ) Space to answer the questions is limited. DO NOT WRITE IN THE BACK

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Professor Antonio Fatás Final Exam February 23, 2015 Instructions: (PLEASE READ) Space to answer the questions is limited. DO NOT WRITE IN THE BACK

Lecture 6: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Exemplar for Internal Assessment Resource Economics Level 2

Exemplar for internal assessment resource Economics 2.6A for Achievement Standard 91227 Exemplar for Internal Assessment Resource Economics Level 2 Resource title: Government policies that could lift the

Exemplar for internal assessment resource Economics 2.6A for Achievement Standard 91227 Exemplar for Internal Assessment Resource Economics Level 2 Resource title: Government policies that could lift the

Chapter 10. Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics. Chapter Preview

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of and

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of 1929-33 and 2007-09 David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009 Presentation

Lessons Learned? Comparing the Federal Reserve s Response to the Crises of 1929-33 and 2007-09 David C. Wheelock Vice President and Economist Federal Reserve Bank of St. Louis November 23, 2009 Presentation

Unconventional Monetary Policy during the Great Recession: Theory, Empirical Evidence and Limitations. Kilian Rieder 1.

Unconventional Monetary Policy during the Great Recession: Theory, Empirical Evidence and Limitations Kilian Rieder 1 1 University of Oxford, kilian.rieder@univ.ox.ac.uk Paris Dauphine, London Campus Guest

Unconventional Monetary Policy during the Great Recession: Theory, Empirical Evidence and Limitations Kilian Rieder 1 1 University of Oxford, kilian.rieder@univ.ox.ac.uk Paris Dauphine, London Campus Guest

Discussion on The Great Recession: What Recovery?

Discussion on The Great Recession: What Recovery? Robert E. Hall Hoover Institution and Department of Economics Stanford Universtiy rehall@stanford.edu Twelfth BIS Annual Conference June 13 September 17,

Discussion on The Great Recession: What Recovery? Robert E. Hall Hoover Institution and Department of Economics Stanford Universtiy rehall@stanford.edu Twelfth BIS Annual Conference June 13 September 17,

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

Review: Income Portfolio

Review: Income Portfolio In the most recent quarter we only made one change to the portfolio s investments. Namely, we re-invested the proceeds of the maturing Bell Canada Bond, plus a portion of the portfolio

Review: Income Portfolio In the most recent quarter we only made one change to the portfolio s investments. Namely, we re-invested the proceeds of the maturing Bell Canada Bond, plus a portion of the portfolio

Yves Mersch: Monetary policy and economic inequality

Yves Mersch: Monetary policy and economic inequality Keynote speech by Mr Yves Mersch, Member of the Executive Board of the European Central Bank, at the Corporate Credit Conference, hosted by Muzinich,

Yves Mersch: Monetary policy and economic inequality Keynote speech by Mr Yves Mersch, Member of the Executive Board of the European Central Bank, at the Corporate Credit Conference, hosted by Muzinich,

Short run prospects in Europe and the United States

Short run prospects in Europe and the United States Olivier Blanchard September 2003 Strong hope in Europe that the US expansion is gaining strength, and will take Europe out of its slump. Half right,

Short run prospects in Europe and the United States Olivier Blanchard September 2003 Strong hope in Europe that the US expansion is gaining strength, and will take Europe out of its slump. Half right,

ECON 10020/20020 Principles of Macroeconomics Problem Set 5

ECON 10020/20020 Principles of Macroeconomics Problem Set 5 Dennis C. Plott University of Notre Dame Department of Economics March 25, 2015 Email: dennis.plott@gmail.com 1 Name: 1. Due: Thursday 2 nd April

ECON 10020/20020 Principles of Macroeconomics Problem Set 5 Dennis C. Plott University of Notre Dame Department of Economics March 25, 2015 Email: dennis.plott@gmail.com 1 Name: 1. Due: Thursday 2 nd April

Andersons Professor of International Trade Department of Agricultural, Environmental & Development Economics Ohio State University

Macroeconomic Outlook Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Global economic

Macroeconomic Outlook Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Global economic

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

GLOBAL FINANCIAL SYSTEM. Lecturer Oleg Deev

GLOBAL FINANCIAL SYSTEM Lecturer Oleg Deev oleg@mail.muni.cz Contents Concept of the global financial system Evolution of the global financial system International reserve currency Post-Bretton Woods global

GLOBAL FINANCIAL SYSTEM Lecturer Oleg Deev oleg@mail.muni.cz Contents Concept of the global financial system Evolution of the global financial system International reserve currency Post-Bretton Woods global

The sharp accumulation in government debt can t go on forever

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014)

") Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

ECON Intermediate Macroeconomics (Professor Gordon) First Midterm Examination: Fall 2011 Answer sheet

First Midterm Examination: Fall 2011 Answer sheet") ECON 311 - Intermediate Macroeconomics (Professor Gordon) First Midterm Examination: Fall 2011 Answer sheet YOUR NAME: Circle the TA session you attend: Ofer 9AM 4PM Nuri 4PM Juan 9AM INSTRUCTIONS: 1.

ECON 311 - Intermediate Macroeconomics (Professor Gordon) First Midterm Examination: Fall 2011 Answer sheet YOUR NAME: Circle the TA session you attend: Ofer 9AM 4PM Nuri 4PM Juan 9AM INSTRUCTIONS: 1.

From Debt Money to Public Money System

From Money to Public Money System Modeling A Transition Process Simplified (A Revised Version) Kaoru Yamaguchi, Ph.D. Japan Futures Research Center Awaji Island, Japan E-mail: director@muratopia.net Abstract

From Money to Public Money System Modeling A Transition Process Simplified (A Revised Version) Kaoru Yamaguchi, Ph.D. Japan Futures Research Center Awaji Island, Japan E-mail: director@muratopia.net Abstract

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates Ming-sen Wang Department of Economics University of Arizona June 20, 2013 Overview The ideas of economists and political philosophers, both

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates Ming-sen Wang Department of Economics University of Arizona June 20, 2013 Overview The ideas of economists and political philosophers, both

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING Prof. Bill Even FORM 1. Directions

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING 2011 Prof. Bill Even FORM 1 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth the equivalent

ECO202: PRINCIPLES OF MACROECONOMICS SECOND MIDTERM EXAM SPRING 2011 Prof. Bill Even FORM 1 Directions 1. Fill in your scantron with your unique id and form number. Doing this properly is worth the equivalent

Rebuilding of the European and US Economy and Japan. Richard C. Koo Chief Economist Nomura Research Institute Tokyo January 2012

Rebuilding of the European and US Economy and Japan Richard C. Koo Chief Economist Nomura Research Institute Tokyo January 212 Exhibit 1. US Housing Prices Are Moving along the Japanese Experience 26 24

Rebuilding of the European and US Economy and Japan Richard C. Koo Chief Economist Nomura Research Institute Tokyo January 212 Exhibit 1. US Housing Prices Are Moving along the Japanese Experience 26 24

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Economic puzzles: the world, Europe, Brexit and renminbi Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times FT-ANZ RMB Growth Strategy Series 24 th June Sydney Economic puzzles

Chapter 18: Output and the Exchange Rate in the Short Run

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

How does the government stabilize the economy?

How does the government stabilize the economy? The government has two different tool boxes it can use: 1. Fiscal Policy- Actions by Congress and the president to adjust to the G in aggregate demand. 2.

How does the government stabilize the economy? The government has two different tool boxes it can use: 1. Fiscal Policy- Actions by Congress and the president to adjust to the G in aggregate demand. 2.

Black Monday Exploring Current Financial Crisis

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

AQA Economics A-level

AQA Economics A-level Macroeconomics Topic 4: Financial Markets and Monetary Policy 4.3 Central banks and monetary policy Notes Monetary policy is used to control the money flow of the economy. This is

AQA Economics A-level Macroeconomics Topic 4: Financial Markets and Monetary Policy 4.3 Central banks and monetary policy Notes Monetary policy is used to control the money flow of the economy. This is

POLI 12D: International Relations Sections 1, 6

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

Economics of Money, Banking, and Financial Markets 6e (Mishkin) Chapter 1 Why Study Money, Banking, and Financial Markets?

Chapter 1 Why Study Money, Banking, and Financial Markets?") Economics of Money, Banking, and Financial Markets 6e (Mishkin) Chapter 1 Why Study Money, Banking, and Financial Markets? Download full Test Bank for Economics of Money, Banking and Financial Markets

Economics of Money, Banking, and Financial Markets 6e (Mishkin) Chapter 1 Why Study Money, Banking, and Financial Markets? Download full Test Bank for Economics of Money, Banking and Financial Markets

Greece Facing an Uncertain Future

Greece Facing an Uncertain Future Professor of Finance & Economics, Un. of Piraeus Chief Economist, Eurobank Group November 9, 2012 ECONOMIST CONFERENCE ON CREDIT RISK MANAGEMENT FOR BANKING AND BUSINESS:

Greece Facing an Uncertain Future Professor of Finance & Economics, Un. of Piraeus Chief Economist, Eurobank Group November 9, 2012 ECONOMIST CONFERENCE ON CREDIT RISK MANAGEMENT FOR BANKING AND BUSINESS:

Topic 8 : The Interwar Globalization Backlash

Topic 8 : The Interwar Globalization Backlash Department of Economics University of Warwick March, 2014 We focus on the monetarist view : It was the Fed s policy mistake ignoring the importance of money

Topic 8 : The Interwar Globalization Backlash Department of Economics University of Warwick March, 2014 We focus on the monetarist view : It was the Fed s policy mistake ignoring the importance of money

Solutions to Chapter 2. Financial Markets and Institutions

Solutions to Chapter 2 Financial Markets and Institutions 1. The story of Apple Computer provides three examples of financing sources: equity investments by the founders of the company, trade credit from

Solutions to Chapter 2 Financial Markets and Institutions 1. The story of Apple Computer provides three examples of financing sources: equity investments by the founders of the company, trade credit from

Monthly Economic and Financial Developments September 2004

Monthly Economic and Financial Developments September In an effort to provide the public with more frequent information on its economic surveillance activities, the Central Bank has decided to release

Monthly Economic and Financial Developments September In an effort to provide the public with more frequent information on its economic surveillance activities, the Central Bank has decided to release

Modelling the sovereign debt crisis in Europe

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

MACROECONOMICS. Section I Time 70 minutes 60 Questions

MACROECONOMICS Section I Time 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MACROECONOMICS Section I Time 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

Svein Gjedrem: The economic outlook for Norway

Svein Gjedrem: The economic outlook for Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), for Norges Bank s regional network, Region East, 19 November 2008. Please note

Svein Gjedrem: The economic outlook for Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), for Norges Bank s regional network, Region East, 19 November 2008. Please note