Lecture 6: Intermediate macroeconomics, autumn Lars Calmfors

|

|

|

- Bruce Price

- 5 years ago

- Views:

Transcription

1 Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors

2 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate Why devalue? The Baltic economies and the current crisis Speculative attacks Liquidity traps Literaure: Krugman-Obstfeld chapter 17 OECD Economic Outlook chapter 1, pp

3 2 Fixed exchange rates historically Gold standard: Failed attempts to restore the gold standard: 1920s Bretton Woods system: Current situation From 1973 floating exchange rates between most OECD currencies. But many small open economies have chosen to peg their currencies to large currencies (dollar, the British pound, euro earlier the D-mark or the French franc) or a currency basket (a weighted average of currencies). Some countries have a crawling peg (depreciation against another currency at a given rate) or a managed float (the central bank tries to influence a floating exchange rate but does not change it according to a predetermined plan). China used to have a fixed exchange rate to the dollar. Official change to a managed float against a currency basket Fixed rate to the dollar again in the current crisis.

4 3 Sweden : Fixed exchange rate within the Bretton Woods system (devaluation 1949) : Fixed exchange rate to the D-mark within the European snake (devaluation 1976) : Fixed exchange rate to a trade-weighted basket with extra weight for the dollar (repeated devaluations: 1977, 1981 and 1982) : Fixed exchange rate to the ecu (weighted average of the currencies within the EU). Abandoned after exchange rate crisis ?: Freely floating exchange rate with inflation target for the central bank? -?: EMU membership with the euro as the common currency?????

5 4 ERM (European Exchange Rate Mechanism) established Exchange rate band +/- 2.25% around central parity. Widened band after exchange rate crises 1992/93 to +/- 15 %, but Belgium, Denmark, France, Germany and the Netherlands maintained the earlier narrow bands. ERM 2 after the start of EMU: Denmark + Greece + euro area. Today Denmark, Estonia, Latvia, Lithuania + euro area. Condition for EMU entry: ERM membership for two years. Slovenia, Cyprus, Malta and Slovak Republic have been ERM members but have now entered the euro area.

6 5 The central bank balance sheet Assets Liabilities Foreign assets Deposits held by private banks Domestic assets Currency in circulation

7 6 The central bank balance sheet (cont.) Foreign assets: foreign currency bonds owned by the central bank (international reserves). Affected by the central bank s interventions in the foreign exchange market. Gold included. Domestic assets: the central bank s claims on its own citizens and domestic institutions. Typically domestic government bonds and loans to domestic private banks. Deposits by private bank: may be withdrawn from the central bank at any time Currency in circulation: notes and coins Assets = liabilities + net worth Assume that the bank s net worth in constant: changes in the central bank s assets will be mirrored in the central bank s liabilities changes in the central bank s assets affect the domestic money supply. Central bank liabilities = the monetary base The money supply is a multiple of the monetary base

8 7 How can the central bank increase the money supply? Purchase foreign assets (increase the foreign exchange reserves) Purchase domestic assets (the stock of assets held by the private sector decreases) - The money the central bank uses to pay for the purchase directly enters the money supply and causes it to expand - Repurchase (repo) transactions: if the central bank purchases government bills, it also enters an agreement to sell the bills at a given future date. - Repo transactions affect the repo rate, i.e. the short-term interest rate.

9 8 Money supply and the current crisis Normally central banks only make transactions in shortterm papers In the current economic crisis central banks have increased the money supply also through transactions in longer-term papers (quantitative easing, unconventional measures) - purchase of government and commercial bonds - lending to banks against corporate debt collateral - lending to banks on longer term Huge expansion of central bank balance sheets

10 9

11 10 A fixed exchange rate and interest rate parity Interest rate parity: R = R* + (E e E)/E Credible fixed exchange rate E e = E. This implies: R = R* Monetary policy must be pursued such that: M/P = L(R*, Y) Y L. This must be matched by M

12 11 Monetary policy and fixed exchange rates Under a fixed exchange rate the central bank buys and sells foreign assets to keep the exchange rate fixed and to maintain domestic interest rates equal to foreign interest rates Under a fixed exchange rate the central bank is not able to adjust domestic interest rates to attain other goals Monetary policy in therefore ineffective in influencing output and employment

13 121 Fixed Exchange Rates Copyright 2006 Pearson Addison-Wesley. All rights reserved

14 131 Monetary Policy and Fixed Exchange Rates (cont.) Copyright 2006 Pearson Addison-Wesley. All rights reserved

15 14 1 Fiscal policy and fixed exchange rates in the short run Temporary changes in fiscal policy are more effective in influencing output and employment in the short run. Expansionary fiscal policy increasing output and income raises demand of real monetary assets, putting upward pressure on interest rates and on the domestic currency. To prevent an appreciation of the domestic currency, the central bank buys foreign assets, thereby increasing the money supply and decreasing interest rates.

16 151 Fiscal Policy and Fixed Exchange Rates in the Short Run (cont.) A fiscal expansion increases aggregate demand To prevent the domestic currency from appreciating, the central bank buys foreign assets, increasing the money supply and decreasing interest rates. Copyright 2006 Pearson Addison-Wesley. All rights reserved

17 161 Conclusions on stabilisation policy Flexible exchange rate - Monetary policy is the primary stabilisation tool - Fiscal policy is not so effective (exchange rate offset) Fixed exchange rate - Monetary policy is ineffective (tied down by interest rate parity) - Fiscal policy is the only effective stabilisation tool

18 171 Devaluations and revaluations Depreciations and appreciations: changes in the value of a currency under a floating exchange rate. Governed by markets. Devaluations and revaluations: changes in the value of a currency under a fixed exchange rate. Governed by the central bank. Devaluation: a unit of domestic currency is made less valuable, so that more units must be exchanged for one unit of foreign currency. Revaluation: a unit of domestic currency is made more valuable, so that fewer units need to be exchanged for one unit of foreign currency.

19 181 Devaluation The central bank buys foreign assets the money supply increases and domestic interest rates fall, causing a fall in the rate return on domestic currency deposits. Domestic products become less expensive relative to foreign products aggregate demand and output increase. Official international reserve assets, i.e. foreign bonds, increase.

20 19 Devaluation (cont.) If the central bank devalues the domestic currency so that the new fixed exchange rate is E 1, it buys foreign assets, increasing the money supply, decreasing the interest rate and increasing output Copyright 2006 Pearson Addison-Wesley. All rights reserved

21 202 Why does a country devalue? 1. Expansionary fiscal policy may be impossible because of large budget deficits and large government debt: Sweden 1992 or Argentina Under a fixed exchange rate and free capital movements an exchange rate devaluation is the only way of using monetary policy. 3. Past inflation may have deteriorated international competitiveness and priced a country out of international markets. 4. Foreign exchange reserves may be depleted, for example because of large current account deficits.

22 212 Balance of payment crisis A balance of payments crisis arises if the central bank does not have enough international reserves to maintain the fixed exchange rate. To sustain a fixed exchange rate the central bank must have enough foreign assets to sell to meet the demand for the national currency at the fixed exchange rate. If investors expect that the domestic currency will be devalued, they will demand foreign assets instead of domestic assets (whose value is expected to fall). This fear exacerbates the crisis: - Investors exchange domestic currency for foreign currency depleting the foreign exchange reserves even more. - Financial capital is moved to foreign assets: capital flight. The government can seek to keep capital in the country by raising the interest rate, i.e. by decreasing the money supply. The outcome is high interest rates, low money supply, low aggregate demand, low output and low employment.

23 22 Financial Crises and Capital Flight (cont.) Expected devaluation makes the expected return on foreign assets higher To attract investors to hold domestic assets (currency) at the original exchange rate, the interest rate must rise through a sale of foreign assets. Copyright 2006 Pearson Addison-Wesley. All rights reserved

24 Fig. 17-5: Capital Flight, the Money Supply, and the Interest Rate Expected devaluation makes the expected return on foreign assets higher 23 To attract investors to hold domestic assets (currency) at the original exchange rate, the interest rate must rise through a sale of foreign assets.

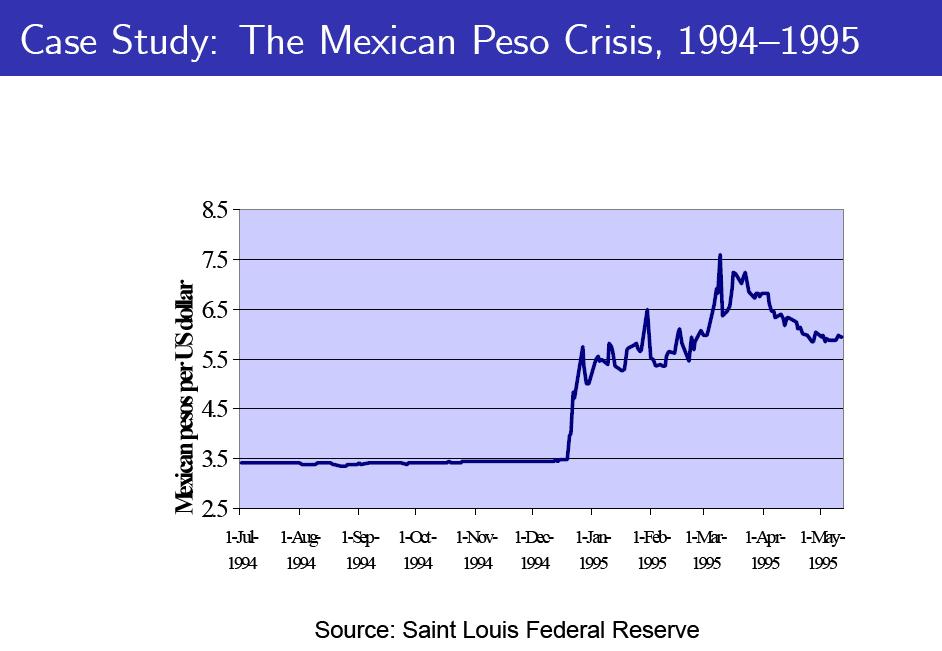

25 24 Speculative attacks 1. Response to future unavoidable development 2. Self-fulfilling expectations (multiple equilibria) It is always technically possible to defend a fixed exchange rate through selling foreign currency from foreign exchange reserves or currency obtained from borrowing: the problem is the goal conflicts caused by high interest rates Lower employment Higher interest rates on government debt and thus larger government budget deficits Private sector bankruptcies (banks and financial firms) Examples: Sweden 1992, Mexico 1994, Brazil , Argentina 2001 Dramatic increases in unemployment Huge government budget deficits Bankruptcies of banks, financial firms and real estate firms

26 25

27 26

28 27 Current crisis in the Baltic states Fixed exchange rates vis-à-vis the euro - currency boards - all outstanding central bank debt is backed by foreign currency reserves Typical emerging-market crisis - earlier large current-account deficits and capital inflows (Swedish banks) - reckless lending by Swedish banks - high inflation and lost cost competitiveness - capital flow reversals - expectations of exchange rate depreciations - interest rate hikes - deep recessions Attempts to restore competitiveness through wage and price cuts * EP P by lowering P at constant E

29 28 Why don t the Baltic economies devalue? Violation of EMU entry criterion Fixed exchange rate seen as anchor for low inflation Most of private-sector debt is in euros (foreign currency) Devaluation would increase the domestic-currency value of debt denominated in euros - D = ED * But what matters is the real burden of debt - D P = ED P * The real burden of debt increases also if P Main difference: it takes longer time to achieve real exchange rate depreciation through wage/price cuts than through exchange rate devaluation - hence more time for Swedish banks to compensate credit losses through operating profits on their other activities

30 29

31 30

32 31

33 32 China s exchange rate policy Undervalued exchange rate has been maintained through central bank purchases of dollar: accumulation of dollar assets by the central bank - Current account surplus in 2008: 10 percent of GDP - The largest foreign currency reserves in the world: 20 percent of world reserves Explanations - High private savings because of underdeveloped social security and pension system - Undervalued exchange rate helps industrialisation through strategy of export-led growth - Precautionary motive for accumulating assets: ability to meet capital outflows (cf Asian crisis) Problems: - Distorted relative prices: imports are too expensive - Overinvestment in export sector - Low purchasing power for domestic consumers Problems associated with appreciation - Exchange rate losses on accumulated dollar reserves - Many export firms that are profitable today would become unprofitable - Risks of financial crisis

34 33 Fig Growth Rates of International Reserves Source: Economic Report of the President.

35 34 More on interest rates and exchange rates: liquidity traps Liquidity trap: occurs when nominal interest rate, R, falls to zero. The central bank cannot encourage people to hold more money. Nominal interest rates cannot fall below zero agents would then have to pay to deposit their money in banks. R = 0 people are indifferent between holding money and interest-bearing assets.

36 35 Liquidity trap (cont.) Interest rate parity: R R E * = + = e E E Set R = 0 and solve for E: 0 E = e E 1 R * Then nominal exchange rate is now determined by * R and A temporary change in the money supply does not affect output as in the standard AA-DD framework. When the foreign interest rate is given, the only way for the central bank to influence the exchange rate is by affecting e E. expectations, e E. A permanent monetary expansion will raise expectations of inflation and cause markets to expect a depreciation of the currency. This will depreciate the currency and raise output.

37 36 The historical gold standard During the gold standard central banks guaranteed that currencies could be converted into gold at a fixed price The gold standard thus implied a fixed price of different currencies in gold: this locked all cross exchange rates between different currencies The gold standard tied changes in money supply to changes in the gold stock: this ensured that inflation would not run away The gold standard was abandoned only during deep crises (usually wars): implicit commitment to return to earlier parities afterwards Long-run price movements tied to changes in the gold stock associated with swings in gold production Monetary policy could not be used for stabilisation of the business cycle

38 37 Gold-dollar exchange standard in the Bretton Woods system The dollar functioned as a reserve currency N 1-problem: With N currencies only N 1 countries need to maintain fixed exchange rates (because there are only N 1 exchange rates) The reserve currency country (the US) can choose any rate of change of money supply: the others must adjust their money supply increases and interest rates so that they maintain fixed exchange rates vis-à-vis the dollar. The system worked until the US started printing money and create inflation in the 1960s (financing of the Vietnam war and domestic social reforms) Other countries (Germany, France, Japan) were not prepared to maintain fixed exchange rates, as this implied that they would import inflation The Bretton-Woods system broke down after a series of serious exchange rate crises

39 38 ERM-system in the 1980s and 1990s Germany functioned as reserve currency country Germany determined the inflation rate in the ERM area (other countries could import price stability from Germany) But German monetary policy aimed at stabilising the German business cycle In the early 1990s after German unification there was a strong boom in Germany at the same time as Europe went into recession. German high interest rates to keep down domestic inflation aggravated the recession in the rest of Europe. EMU was seen by many (France in particular) as a way of replacing German control of European monetary policy with common European decision making in a common European Central Bank.

40 Convergence of Inflation Rates Among EMS Members,

41 40

Lecture 7: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 7: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 EMU Economic and Monetary Union An old idea in the European Union 1989: Delors report 1991: Maastricht treaty 1997: Stability pact Eleven

Lecture 7: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 EMU Economic and Monetary Union An old idea in the European Union 1989: Delors report 1991: Maastricht treaty 1997: Stability pact Eleven

Chapter 18. The International Financial System

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 9 Essential macroeconomic tools. Baldwin&Wyplosz 2009 The Economics of European Integration, 3 rd Edition

Chapter 9 Essential macroeconomic tools 2 Background theory A quick refresher on basic macroeconomic principles Application of these principles to the question of exchange rate regimes 3 Output and prices

Chapter 9 Essential macroeconomic tools 2 Background theory A quick refresher on basic macroeconomic principles Application of these principles to the question of exchange rate regimes 3 Output and prices

The International Monetary System

INTERNATIONAL FINANCIAL MANAGEMENT Fourth Edition EUN / RESNICK The International Monetary System 2 Chapter Two INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter serves to introduce the

INTERNATIONAL FINANCIAL MANAGEMENT Fourth Edition EUN / RESNICK The International Monetary System 2 Chapter Two INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter serves to introduce the

Chapter 18: Output and the Exchange Rate in the Short Run

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention

Fixed Exchange Rates and Foreign Exchange Intervention") Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Intermediate Macroeconomics, 7.5 ECTS

STOCKHOLMS UNIVERSITET Intermediate Macroeconomics, 7.5 ECTS SEMINAR EXERCISES STOCKHOLMS UNIVERSITET page 1 SEMINAR 1. Mankiw-Taylor: chapters 3, 5 and 7. (Lectures 1-2). Question 1. Assume that the production

STOCKHOLMS UNIVERSITET Intermediate Macroeconomics, 7.5 ECTS SEMINAR EXERCISES STOCKHOLMS UNIVERSITET page 1 SEMINAR 1. Mankiw-Taylor: chapters 3, 5 and 7. (Lectures 1-2). Question 1. Assume that the production

Chapter 18. The International Financial System Intervention in the Foreign Exchange Market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention

Fixed Exchange Rates and Foreign Exchange Intervention") Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 19 International Monetary Systems: An Historical Overview

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

Monetary Integration

Monetary Integration By Michael Möhnle Table of Contents 1. 6-Stages of Economic Integration 2. International Monetary Integration - Bretton Woods 3. European Monetary Integration 4. European (Economic

Monetary Integration By Michael Möhnle Table of Contents 1. 6-Stages of Economic Integration 2. International Monetary Integration - Bretton Woods 3. European Monetary Integration 4. European (Economic

Chapter 19 (8) International Monetary Systems: An Historical Overview

International Monetary Systems: An Historical Overview") Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld

International Environment Economics for Business (IEEB)

") International Environment Economics for Business (IEEB) Sergio Vergalli sergio.vergalli@unibs.it Vergalli - Lezione 1 The European Currency Crisis (1992-1993) Presented By: Garvey Ngo Nancy Ramirez Background

International Environment Economics for Business (IEEB) Sergio Vergalli sergio.vergalli@unibs.it Vergalli - Lezione 1 The European Currency Crisis (1992-1993) Presented By: Garvey Ngo Nancy Ramirez Background

Lecture 1: Intermediate macroeconomics, autumn 2012

Lecture 1: Intermediate macroeconomics, autumn 2012 Lars Calmfors Literature: Mankiw, Chapters 3 and 5. 1 Topics 1. The relationship between saving, investment and the interest rate in a closed economy

Lecture 1: Intermediate macroeconomics, autumn 2012 Lars Calmfors Literature: Mankiw, Chapters 3 and 5. 1 Topics 1. The relationship between saving, investment and the interest rate in a closed economy

Figure: EUR-USD Exchange Rate

Figure: EUR-USD Exchange Rate SuSe 2013 1 Monetary Policy and EMU: Open Economy Setting Figure: EUR-USD Exchange Rate SuSe 2013 2 Monetary Policy and EMU: Open Economy Setting Figure: Indirect Quotation

Figure: EUR-USD Exchange Rate SuSe 2013 1 Monetary Policy and EMU: Open Economy Setting Figure: EUR-USD Exchange Rate SuSe 2013 2 Monetary Policy and EMU: Open Economy Setting Figure: Indirect Quotation

International Finance

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

Fragility of Incomplete Monetary Unions

Fragility of Incomplete Monetary Unions Incomplete monetary unions Fixed exchange-rate regimes that fall short of a full monetary union but they substantially constrain the ability of the national government

Fragility of Incomplete Monetary Unions Incomplete monetary unions Fixed exchange-rate regimes that fall short of a full monetary union but they substantially constrain the ability of the national government

Chapter 7 Fixed Exchange Rate Regimes and Short Run Macroeconomic Policy

George Alogoskoufis, International Macroeconomics and Finance Chapter 7 Fixed Exchange Rate Regimes and Short Run Macroeconomic Policy Up to now we have been assuming that the exchange rate is determined

George Alogoskoufis, International Macroeconomics and Finance Chapter 7 Fixed Exchange Rate Regimes and Short Run Macroeconomic Policy Up to now we have been assuming that the exchange rate is determined

Welcome to: International Finance

Welcome to: International Finance Introduction & International Monetary System Reading: Chapter 1 (p1-3) & Chapter 2 Why is International Finance Important? ٣ Why is International Finance Important? In

Welcome to: International Finance Introduction & International Monetary System Reading: Chapter 1 (p1-3) & Chapter 2 Why is International Finance Important? ٣ Why is International Finance Important? In

Lecture 1: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 1: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics 1. The relationship between savings, investment and real interest rates in a closed economy (the world economy) 2. The relationship

Lecture 1: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics 1. The relationship between savings, investment and real interest rates in a closed economy (the world economy) 2. The relationship

Study Questions (with Answers) Lecture 17 European Monetary Unification and the Euro

Lecture 17 European Monetary Unification and the Euro") Study Questions (with Answers) Page 1 of 4(5) Study Questions (with Answers) Lecture 17 pean Monetary Unification and the Part 1: Multiple Choice Select the best answer of those given. 1. The is a. The

Study Questions (with Answers) Page 1 of 4(5) Study Questions (with Answers) Lecture 17 pean Monetary Unification and the Part 1: Multiple Choice Select the best answer of those given. 1. The is a. The

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

To Fix or Not to Fix?

To Fix or Not to Fix? Linda Tesar, Department of Economics Notes at: http://www.econ.lsa.umich.edu/~ltesar April 5, 2000 Fixed vs. Flexible Exchange rates The Theory: Money demand: M/P = L(Y,I) Interest

To Fix or Not to Fix? Linda Tesar, Department of Economics Notes at: http://www.econ.lsa.umich.edu/~ltesar April 5, 2000 Fixed vs. Flexible Exchange rates The Theory: Money demand: M/P = L(Y,I) Interest

Chapter Eleven. The International Monetary System

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

POLI 12D: International Relations Sections 1, 6

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

The Mundell-Fleming model

The Mundell-Fleming model 2013 General short run macroeconomic equilibrium Income influences demand for money Goods Market Money Market Interest rates affect aggregate demand in the open the economy Income

The Mundell-Fleming model 2013 General short run macroeconomic equilibrium Income influences demand for money Goods Market Money Market Interest rates affect aggregate demand in the open the economy Income

The International Monetary System

The International Monetary System Eiteman et al., Chapter 2 Winter 2004 Outline of the Chapter Currency Terminology History of the International Monetary System Contemporary Currency Regimes Emerging Markets

The International Monetary System Eiteman et al., Chapter 2 Winter 2004 Outline of the Chapter Currency Terminology History of the International Monetary System Contemporary Currency Regimes Emerging Markets

Study Questions. Lecture 17 European Monetary Unification and the Euro

Study Questions Page 1 of 4 Study Questions Lecture 17 pean Monetary Unification and the Part 1: Multiple Choice Select the best answer of those given. 1. The is a. The common currency that the members

Study Questions Page 1 of 4 Study Questions Lecture 17 pean Monetary Unification and the Part 1: Multiple Choice Select the best answer of those given. 1. The is a. The common currency that the members

Governments and Exchange Rates

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Week 1. Currency Systems and Crises

Week 1 Currency Systems and Crises Definition An exchange rate is the amount of currency that one needs in order to buy one unit of another currency, or the amount of currency that one receive when selling

Week 1 Currency Systems and Crises Definition An exchange rate is the amount of currency that one needs in order to buy one unit of another currency, or the amount of currency that one receive when selling

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform

Developing Countries: Growth, Crisis, and Reform") Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

LECTURE XIV. 31 July Tuesday, July 31, 12

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

Slides for International Finance Pegged Exchange Rates (KOM Chapter 18)

") Pegged Exchange Rates (KOM Chapter 18) American University 2012-11-15 Preview Managed Exchange Rates Monetary authority balance sheets monetary base vs. money supply foreign exchange market interventions

Pegged Exchange Rates (KOM Chapter 18) American University 2012-11-15 Preview Managed Exchange Rates Monetary authority balance sheets monetary base vs. money supply foreign exchange market interventions

Study Questions. Lecture 15 International Macroeconomics

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

3. If the price of a British pound increases from $1.50 per pound to $1.80 per pound, we say that:

STUDY GUIDE FINAL ECO41 FALL 2013 UDAYAN ROY Ch 13 National Income Accounting See the questions in Homework 7 and Homework 8. CHAPTER 14 Exchange Rates and Interest Parity 1. How many dollars would it

STUDY GUIDE FINAL ECO41 FALL 2013 UDAYAN ROY Ch 13 National Income Accounting See the questions in Homework 7 and Homework 8. CHAPTER 14 Exchange Rates and Interest Parity 1. How many dollars would it

Fixed Exchange Rates and Currency Unions

Trade and International Finance SciencesPo Second Year Fall 2018 Fixed Exchange Rates and Currency Unions Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Fixed exchange rates and currency

Trade and International Finance SciencesPo Second Year Fall 2018 Fixed Exchange Rates and Currency Unions Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Fixed exchange rates and currency

THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 14 THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter introduces

Chapter 14 THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter introduces

M.Sc. in Economic Policy Studies

M.Sc. in Economic Policy Studies John FitzGerald, room 3012, jofitzge@tcd.ie 30/10/2015 1 Outline of lectures 5: October 30 th Exchange rates monetary policy and the real economy Exchange rates What drives

M.Sc. in Economic Policy Studies John FitzGerald, room 3012, jofitzge@tcd.ie 30/10/2015 1 Outline of lectures 5: October 30 th Exchange rates monetary policy and the real economy Exchange rates What drives

3/9/2010. Topics PP542. Macroeconomic Goals (cont.) Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History

Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History") Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

UC Berkeley Fall Final examination SOLUTION SHEET

Pierre-Olivier Gourinchas Econ182 Department of Economics International Monetary Economics UC Berkeley Fall 2004 Final examination SOLUTION SHEET WRITE YOUR ANSWERS TO QUESTION 1 ON PAGES 2-5. 1. [30 points,

Pierre-Olivier Gourinchas Econ182 Department of Economics International Monetary Economics UC Berkeley Fall 2004 Final examination SOLUTION SHEET WRITE YOUR ANSWERS TO QUESTION 1 ON PAGES 2-5. 1. [30 points,

Chapter 13 Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy

Chapter 13 Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy 1 Goals of Chapter 13 Two primary aspects of interdependence between economies of different nations International

Chapter 13 Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy 1 Goals of Chapter 13 Two primary aspects of interdependence between economies of different nations International

Goals of Topic 8. NX back!! What is the link between the exchange rate and net exports? How do different policies affect the trade deficit?

TOPIC 8 International Economics Goals of Topic 8 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

TOPIC 8 International Economics Goals of Topic 8 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

Economics of European Integration Lecture # 9 Monetary Integration I

Economics of European Integration Lecture # 9 Monetary Integration I Spring Semester 2009 Gerald Willmann Gerald Willmann, Department of Economics, KU Leuven Why Studying History? Monetary union is the

Economics of European Integration Lecture # 9 Monetary Integration I Spring Semester 2009 Gerald Willmann Gerald Willmann, Department of Economics, KU Leuven Why Studying History? Monetary union is the

Ch. 2 International Monetary System. Motives for Int l Financial Markets. Motives for Int l Financial Markets

Ch. 2 International Monetary System Topics Motives for International Financial Markets History of FX Market Exchange Rate Systems Euro Eurocurrency Market Motives for Int l Financial Markets The markets

Ch. 2 International Monetary System Topics Motives for International Financial Markets History of FX Market Exchange Rate Systems Euro Eurocurrency Market Motives for Int l Financial Markets The markets

EconS 327 Review for Test 2

Test 2 is on Friday, April 24 Test 2 has 30 multiple choice questions. Test 2 will cover the material assigned during weeks 1-14. This includes o Material covered on Test 1 o Material from weeks 8-14 o

Test 2 is on Friday, April 24 Test 2 has 30 multiple choice questions. Test 2 will cover the material assigned during weeks 1-14. This includes o Material covered on Test 1 o Material from weeks 8-14 o

Chapter 14: Essential facts of monetary integration

Chapter 14: Essential facts of monetary integration It was the 1992 EMS crisis that provided the immediate impetus for monetary unification. Barry Eichengreen (2002) Prehistory: before paper money Until

Chapter 14: Essential facts of monetary integration It was the 1992 EMS crisis that provided the immediate impetus for monetary unification. Barry Eichengreen (2002) Prehistory: before paper money Until

Suggested Solutions to Problem Set 4

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al)

") Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter

Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter

Study Questions (with Answers) Lecture 15 International Macroeconomics

Lecture 15 International Macroeconomics") Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Lecture 4: Intermediate macroeconomics, autumn 2012

Lecture 4: Intermediate macroeconomics, autumn 2012 Lars Calmfors Literature: Krugman Obstfeld Melitz, Chapters 14 and 15. 1 What have we done so far? Where are we going? Lecture 1: National income, saving

Lecture 4: Intermediate macroeconomics, autumn 2012 Lars Calmfors Literature: Krugman Obstfeld Melitz, Chapters 14 and 15. 1 What have we done so far? Where are we going? Lecture 1: National income, saving

Balance of Payments Analysis (BOP)

") Topic2 Balance of Payments Analysis (BOP) 1 BOP Statement A statistic measurement of all transactions between domestic and foreign residents over a specified period of time. 2 Business Transactions which

Topic2 Balance of Payments Analysis (BOP) 1 BOP Statement A statistic measurement of all transactions between domestic and foreign residents over a specified period of time. 2 Business Transactions which

26/10/2016. The Euro. By 2016 there are 19 member countries and about 334 million people use the. Lithuania entered 1 January 2015

The Euro 1 The Economics of the Euro 2 The History and Politics of the Euro Prepared by: Fernando Quijano Dickinson State University 1of 88 In 1961 the economist Robert Mundell wrote a paper discussing

The Euro 1 The Economics of the Euro 2 The History and Politics of the Euro Prepared by: Fernando Quijano Dickinson State University 1of 88 In 1961 the economist Robert Mundell wrote a paper discussing

EconS 327 Test 2 Spring 2010

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

Module 44. Exchange Rates and Macroeconomic Policy. What you will learn in this Module:

Module 44 Exchange Rates and Macroeconomic Policy What you will learn in this Module: The meaning and purpose of devaluation and revaluation of a currency under a fixed exchange rate regime Why open -economy

Module 44 Exchange Rates and Macroeconomic Policy What you will learn in this Module: The meaning and purpose of devaluation and revaluation of a currency under a fixed exchange rate regime Why open -economy

TOPIC 9. International Economics

TOPIC 9 International Economics 2 Goals of Topic 9 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

TOPIC 9 International Economics 2 Goals of Topic 9 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

Lecture 5: Intermediate macroeconomics, autumn 2014

Lecture 5: Intermediate macroeconomics, autumn 2014 Lars Calmfors Literature: Krugman Obstfeld Melitz, chapters 16 and 17. 1 1 Topics Absolute and relative purchasing power parity (PPP) The Balassa-Samuelson

Lecture 5: Intermediate macroeconomics, autumn 2014 Lars Calmfors Literature: Krugman Obstfeld Melitz, chapters 16 and 17. 1 1 Topics Absolute and relative purchasing power parity (PPP) The Balassa-Samuelson

Chapter 13 (2) National Income Accounting and the Balance of Payments

National Income Accounting and the Balance of Payments") Chapter 13 (2) National Income Accounting and the Balance of Payments Preview National income accounts measures of national income measures of value of production measures of value of expenditure National

Chapter 13 (2) National Income Accounting and the Balance of Payments Preview National income accounts measures of national income measures of value of production measures of value of expenditure National

OECD III: EMU. Gavin Cameron Lady Margaret Hall. Michaelmas Term 2004

OECD III: EMU Gavin Cameron Lady Margaret Hall Michaelmas Term 2004 the Trinity Free Capital Mobility USA, Japan ERM, NICs, EMU Independent domestic monetary policy Stable (Fixed) Exchange Rate Bretton

OECD III: EMU Gavin Cameron Lady Margaret Hall Michaelmas Term 2004 the Trinity Free Capital Mobility USA, Japan ERM, NICs, EMU Independent domestic monetary policy Stable (Fixed) Exchange Rate Bretton

Fiscal Policy, Budget Deficits and the Economic Crisis. Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010

Fiscal Policy, Budget Deficits and the Economic Crisis Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010 Three lines of defence against the economic crisis 1. Measures to deal with the

Fiscal Policy, Budget Deficits and the Economic Crisis Lars Calmfors Intermediate macroeconomics Stockholm, 30 March 2010 Three lines of defence against the economic crisis 1. Measures to deal with the

The Impact of an Increase In The Money Supply and Government Spending In The UK Economy

The Impact of an Increase In The Money Supply and Government Spending In The UK Economy 1/11/2016 Abstract The international economic medium has evolved in the direction of financial integration. In the

The Impact of an Increase In The Money Supply and Government Spending In The UK Economy 1/11/2016 Abstract The international economic medium has evolved in the direction of financial integration. In the

Chapter 17. Exchange Rates and International Economic Policy

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

The Brussels Economic Forum

The Brussels Economic Forum What kind of policies should the new Member States apply to optimise their speed of convergence? Banco de Portugal VÍTOR CONSTÂNCIO Brussels, 23d of April 24 I. INTRODUCTION

The Brussels Economic Forum What kind of policies should the new Member States apply to optimise their speed of convergence? Banco de Portugal VÍTOR CONSTÂNCIO Brussels, 23d of April 24 I. INTRODUCTION

The Euro and the New Member States

The Euro and the New Member States Natalia Tamirisa International Monetary Fund Warsaw, October 29, 2007 Focus Macroeconomic challenges NMS face as they prepare to join EMU Policies that can help overcome

The Euro and the New Member States Natalia Tamirisa International Monetary Fund Warsaw, October 29, 2007 Focus Macroeconomic challenges NMS face as they prepare to join EMU Policies that can help overcome

International Currency Experiences: National and Global Choices. International currency experiences in the 20th C. Choices for an exchange rate system

International Currency Experiences: National and Global Choices International currency experiences in the 20th C.» The Gold Standard period» The interwar 1920-1930 period» The Bretton Woods period» Post

International Currency Experiences: National and Global Choices International currency experiences in the 20th C.» The Gold Standard period» The interwar 1920-1930 period» The Bretton Woods period» Post

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 18 The International Monetary System, 1870-19731973 Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 18 The International Monetary System, 1870-19731973 Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Discussion of Jeffrey Frankel s Systematic Managed Floating. by Assaf Razin. The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017

Discussion of Jeffrey Frankel s Systematic Managed Floating by Assaf Razin The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017 Scope Jeff s paper proposes to define an intermediate arrangement,

Discussion of Jeffrey Frankel s Systematic Managed Floating by Assaf Razin The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017 Scope Jeff s paper proposes to define an intermediate arrangement,

EMPLOYMENT RATE IN EU-COUNTRIES 2000 Employed/Working age population (15-64 years)

") EMPLOYMENT RATE IN EU-COUNTRIES 2 Employed/Working age population (15-64 years EU-15 Denmark Netherlands Great Britain Sweden Portugal Finland Austria Germany Ireland Luxembourg France Belgium Greece Spain

EMPLOYMENT RATE IN EU-COUNTRIES 2 Employed/Working age population (15-64 years EU-15 Denmark Netherlands Great Britain Sweden Portugal Finland Austria Germany Ireland Luxembourg France Belgium Greece Spain

Botswana s exchange rate policy

BIS Botswana s exchange rate policy Kealeboga Masalila and Oduetse Motshidisi 1. Introduction In the construction of a market-based development strategy, a key policy consideration is the selection of

BIS Botswana s exchange rate policy Kealeboga Masalila and Oduetse Motshidisi 1. Introduction In the construction of a market-based development strategy, a key policy consideration is the selection of

Economic Policy in the Crisis. Lars Calmfors Jönköping International Business School, 2 November 2009

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Monetary Policy under Fixed Exchange Rates

Monetary Policy under Fixed Exchange Rates 1. CB attempts to stimulate economy (buys domestic assets) 2. E 0 E 2 ; AA 1 AA 2 3. But CB is pegging! Can t allow depreciation to happen 4. So the CB sells

Monetary Policy under Fixed Exchange Rates 1. CB attempts to stimulate economy (buys domestic assets) 2. E 0 E 2 ; AA 1 AA 2 3. But CB is pegging! Can t allow depreciation to happen 4. So the CB sells

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Social Development in Estonia: Choices

Social Development in Estonia: Choices European Economic and Social Committee The Social Situation in the Baltic States// Economic Governance, Wages and Collective Agreements Brussels, 27 November 2012

Social Development in Estonia: Choices European Economic and Social Committee The Social Situation in the Baltic States// Economic Governance, Wages and Collective Agreements Brussels, 27 November 2012

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016

Currency Crises: Theory and Evidence

Currency Crises: Theory and Evidence Lecture 3 IME LIUC 2008 1 The most dramatic form of exchange rate volatility is a currency crisis when an exchange rate depreciates substantially in a short period.

Currency Crises: Theory and Evidence Lecture 3 IME LIUC 2008 1 The most dramatic form of exchange rate volatility is a currency crisis when an exchange rate depreciates substantially in a short period.

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 5. Deadline: April 30th

Rutgers University Spring 2012 Name: Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 5. Deadline: April 30th 1. If the marginal propensity to consume for a nation is 0.8,

Rutgers University Spring 2012 Name: Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 5. Deadline: April 30th 1. If the marginal propensity to consume for a nation is 0.8,

Intermediate Macroeconomics

Intermediate Macroeconomics L1: National Income in Closed and Open Economies Anna Seim Department of Economics, Stockholm University Spring 2015 Topics The relationship between Saving and investment in

Intermediate Macroeconomics L1: National Income in Closed and Open Economies Anna Seim Department of Economics, Stockholm University Spring 2015 Topics The relationship between Saving and investment in

Growth, competitiveness and jobs: priorities for the European Semester 2013 Presentation of J.M. Barroso,

Growth, competitiveness and jobs: priorities for the European Semester 213 Presentation of J.M. Barroso, President of the European Commission, to the European Council of 14-1 March 213 Economic recovery

Growth, competitiveness and jobs: priorities for the European Semester 213 Presentation of J.M. Barroso, President of the European Commission, to the European Council of 14-1 March 213 Economic recovery

The Open Economy Revisited: the Exchange-Rate Regime

C H A P T E R 12 : the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS SIXTH EDITION N. GREGORY MANKIW PowerPoint Slides by Ron Cronovich 2008 Worth Publishers, all rights reserved In

C H A P T E R 12 : the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS SIXTH EDITION N. GREGORY MANKIW PowerPoint Slides by Ron Cronovich 2008 Worth Publishers, all rights reserved In

Governor of the Bank of Latvia

Lessons from Latvia s internal adjustment strategy Ilmārs Rimšēvičs Governor of the Bank of Latvia September 4, 2012 Presentation outline Overheating of Latvia s economy Expansionary consolidation Lessons

Lessons from Latvia s internal adjustment strategy Ilmārs Rimšēvičs Governor of the Bank of Latvia September 4, 2012 Presentation outline Overheating of Latvia s economy Expansionary consolidation Lessons

Progress towards Strong, Sustainable and Balanced Growth. Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction)

") Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

European Monetary Union

European Monetary Union Chapter 20 1 Macroeconomic Performance of Europe in the 1980 s Average Annual Growth Rates, 1979-1987 W. Europe US Japan Jobs 0.1 1.6 0.9 Output 1.8 2.4 3.9 2 3 Chapter 20 1 Comparison

European Monetary Union Chapter 20 1 Macroeconomic Performance of Europe in the 1980 s Average Annual Growth Rates, 1979-1987 W. Europe US Japan Jobs 0.1 1.6 0.9 Output 1.8 2.4 3.9 2 3 Chapter 20 1 Comparison

Review Questions (with Answers) Lecture 14 Pegging the Exchange Rate

Lecture 14 Pegging the Exchange Rate") Review Questions (with Answers) Page 1 of 6(7) Review Questions (with Answers) Lecture 14 the Exchange Rate Part 1: Multiple Choice Select the best answer of those given. 1. If the central bank of Mexico

Review Questions (with Answers) Page 1 of 6(7) Review Questions (with Answers) Lecture 14 the Exchange Rate Part 1: Multiple Choice Select the best answer of those given. 1. If the central bank of Mexico

China s Currency: A Summary of the Economic Issues

Order Code RS21625 Updated July 11, 2007 China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and Trade Division Marc Labonte Government and Finance Division

Order Code RS21625 Updated July 11, 2007 China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and Trade Division Marc Labonte Government and Finance Division

Global Business Economics. Mark Crosby SEMBA International Economics

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

14.05 Intermediate Applied Macroeconomics Problem Set 5

14.05 Intermediate Applied Macroeconomics Problem Set 5 Distributed: November 15, 2005 Due: November 22, 2005 TA: Jose Tessada Frantisek Ricka 1. Rational exchange rate expectations and overshooting The

14.05 Intermediate Applied Macroeconomics Problem Set 5 Distributed: November 15, 2005 Due: November 22, 2005 TA: Jose Tessada Frantisek Ricka 1. Rational exchange rate expectations and overshooting The

Macro for SCS Nov. 29, International Trade & Finance

Macro for SCS Nov. 29, 2017 International Trade & Finance The Gains from Trade Do you believe in magic The Gains from Trade Leave the England-Portugal rivalry for the soccer field Criticism of the free

Macro for SCS Nov. 29, 2017 International Trade & Finance The Gains from Trade Do you believe in magic The Gains from Trade Leave the England-Portugal rivalry for the soccer field Criticism of the free

MACROECONOMICS. The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MANKIW N. GREGORY

C H A P T E R 12 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint

C H A P T E R 12 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 21 The International Monetary System: Past, Present, and Future

Chapter 21 The International Monetary System: Past, Present, and Future "...for the international economy the existence of a well-functioning financial system assuring efficient exchange is as important

Chapter 21 The International Monetary System: Past, Present, and Future "...for the international economy the existence of a well-functioning financial system assuring efficient exchange is as important

Chapter 12 National Income Accounting and the Balance of Payments. Chapter 13 Exchange Rates and the Foreign Exchange Market: an Asset Approach

Macroeconomics 2 for ECO International Economics: Theory & Policy Krugman and Obstfeld Chapter 12 National Income Accounting and the Balance of Payments GNP = national income depreciation + net unilateral

Macroeconomics 2 for ECO International Economics: Theory & Policy Krugman and Obstfeld Chapter 12 National Income Accounting and the Balance of Payments GNP = national income depreciation + net unilateral

Study Questions (with Answers) Lecture 15 International Macroeconomics

Lecture 15 International Macroeconomics") Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

ECN 160B SSI Final Exam August 1 st, 2012 VERSION B

ECN 160B SSI Final Exam August 1 st, 2012 VERSION B Name: ID#: Instruction: Write your name and student ID number on this exam and your blue book and your scantron. Be sure to answer all multiple choice

ECN 160B SSI Final Exam August 1 st, 2012 VERSION B Name: ID#: Instruction: Write your name and student ID number on this exam and your blue book and your scantron. Be sure to answer all multiple choice

The Trend Reversal of the Private Credit Market in the EU

The Trend Reversal of the Private Credit Market in the EU Key Findings of the ECRI Statistical Package 2016 Roberto Musmeci*, September 2016 The ECRI Statistical Package 2016, Lending to Households and

The Trend Reversal of the Private Credit Market in the EU Key Findings of the ECRI Statistical Package 2016 Roberto Musmeci*, September 2016 The ECRI Statistical Package 2016, Lending to Households and

Developing Countries Chapter 22

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

4/14/2011. Exchange Rate Policy and Devaluation. The Central Bank Balance Sheet. Central Bank Policy Options in a Crisis

Exchange Rate Policy and Devaluation BOP Surpluses: excess supply of Forex CB buys BOP Deficits: excess demand for Forex CB sells OSB must offset BOP ISLM-FX with an unexpected devaluation ISLM-FX with

Exchange Rate Policy and Devaluation BOP Surpluses: excess supply of Forex CB buys BOP Deficits: excess demand for Forex CB sells OSB must offset BOP ISLM-FX with an unexpected devaluation ISLM-FX with