Business cycle fluctuations Part II

|

|

|

- Jasper Mason

- 5 years ago

- Views:

Transcription

1 Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr

2 Lecture 7: Business cycle fluctuations Part II 1. Real Business Cycles vs Keynesians 2. Asset markets and business cycles 3. International Business Cycles

3 RealBusinessCycleversusKeynesians Macroeconomists mostly agree on what business cycles look like. Also a reasonable agreement on the likely candidates for the shocks which cause business cycles Disagreement over (a) The relative importance of different shocks. (b) The propagation mechanisms which cause business cycles.

4 Real Business Cycles (RBC) Real Business Cycle models emphasize change in technology (understand TFP) as the source of economic fluctuations. Solow model emphasized TFP as source of growth. Now emphasize (random) variations in TFP as source of business cycles. Propagation mechanisms: intertemporal labor substitution and capital accumulation. Intertemporal labor substitution. When productivity is high, wanttoworkmore,producemore.whenitislow,thereverse. Capital accumulation: when productivity is high, invest and produce more. Opposite when low.

5 Real Business Cycles (RBC) Empirical implications: (1) TFP fluctuations must be correlated with GDP fluctuations. (2) When a positive technology shock happens firms increase labour demand which leads to higher employment and output. They also invest more due to raising marginal productivity of capital if the shock is persistent. Thus positive co-movements between employment, investment, productivity and output. Exactly what we see in the data.

")

6 Source: Basu et al. (2006)

7 Business cycle moments U.S. business cycle moments. Quarterly data 1948Q1-2010Q4. HP filtered series Source: Eric Sims, 2011

8 RBC controversies At least three controversial implications of RBC a) business cycles caused by supply and not demand shocks b) need to assume flat labour supply curve - if supply curve not flat then wages rather than employment rises in a boom which is counterfactual. However, in reality need large changes in wages to increase employment - labour supply curve steep. c) business cycles are an optimal market response to supply shocks and so government stabilisation policy is misconceived.

9 Real Wage Productivity improvement leads to increase in labour demand Labour Supply Employment If (short run) labour supply curve is very flat then increases in labour demand due to technology improvements bring forth big increase in employment but smallincreaseinwages-asseenindata.

10 Keynesians(and Neo-Keynesians) Underlying these models is the idea that business cycles are inefficient and it is welfare improving to remove them. In its most general form Keynesian macroeconomics is based on the idea that market prices either will not adjust or will not adjust by enough to ensure full employment/full capacity output. Price/wage rigidities are of various forms and lead to socially inefficient output.

11 Remember from lecture 4. Wage rigidity : short-run equilibrium Real Wage w/p Long run Rigid Real Wage (short-run) short-run Employment With rigid wages (short run), labour is demand determined. A positive demand shock lowers unemployment (increase hours). The opposite for a negative demand shock.

12 Keynesians(and Neo-Keynesians) In the previous example, a recession is inefficient. Driven by wage rigidity which lowers employment below its potential level (as determined by the long-run supply curve). The simple remedy to this problem is for the government to increase demand in the economy - either by increasing expenditure, the money supply or lowering taxes. Provides a role for public intervention to stabilize output. Big issue is the efficiency of such stabilization policies. We will discuss this in later lectures.

13 Whatiscausingthe business cycle? Still great dispute over the propagation mechanism. Debate also marked over the causes of business cycles Consensus view is that while Real Business Cycle has forced us to re-evaluate importance of supply shocks it is incorrect in arguing that technology shocks are the main driving force behind the business cycle or that business cycle fluctuations are optimal. Technology shocks usually found to explain about 30% of business cycle.

14 Demandorsupplyshocks? Large number of studies trying to identify the respective contribution of supply (technology) and demand shocks. Basu et al. (2006) among others compute the of % of variance of output due to technology shocks in the US at different horizons Horizon (years) % of variance of output due to technology shocks Consensus leads towards demand shocks most important cause of business cycles even though at longer horizons productivity shocks much more important.

15 Demandorsupplyshocks? Business cycles comoves a lot with consumer sentiment Source: Angeletos et al. (2013)

16 Lecture 7: Business cycle fluctuations Part II 1. Real Business Cycles vs Keynesians 2. Asset markets and business cycles 3. International Business Cycles

17 Assets and liabilities Assets: forms in which wealth is held = mean to transfer consumption across periods (and states of the world). Assets: stocks, bonds, houses, money & deposits, derivatives, currencies Assets differ by their degree of liquidity and riskiness. Liabilities are also means to transfer consumption across time but implies higher consumption today than tomorrow. Note that liabilities of an agent (bank, household, ) are assets of an another

18 Asset markets and business cycles Want to show how financial markets can propagate shocks and amplify economic fluctuations. Basic message: increasing asset prices tend to increase consumption and investment if those assets are used as collateral for borrowing by consumers and firms. Illustrate this theoretically in a two period model of consumption with collateral constraints.

19 Limited commitment and collateral Borrowers need incentives not to default on their debts. These incentives typically provided by collateral requirements. This is due to limited commitment: borrowers cannot commit to repay loans. Even if they can afford repayment in future, may choose not to repay. Strategic default. Examples: House is collateral for a mortgage loan, car is collateral for a car loan. Collateral can also support borrowing for other purposes, such as home equity lines for consumption purchases. A fall in the value of the collateral can lead to a large reduction in borrowing and consumption.

20 A simple two period model of consumption The consumer s first period budget constraint: + = = consumption; = output; = taxes; = wealth (positive or negative). Second period(denoted with ): = + (1 + ) Start without financial frictions(no collateral constraint). Intertemporal budget constraint with free borrowing and lending: + /(1 + ) = ( ) + ( )/(1 + ) = Y Net present value of expenditures = net present value of income (Y).

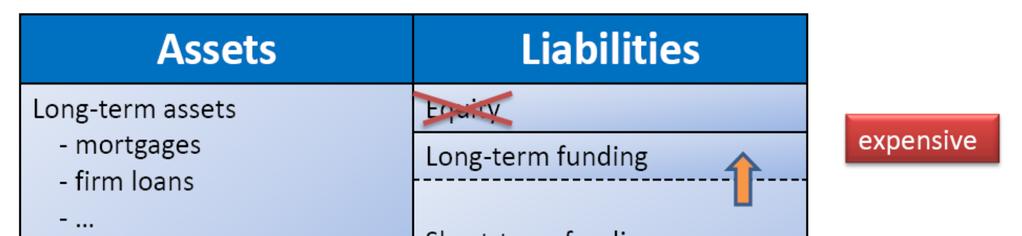

21 A simple two period model of consumption Utility to be maximized: U = log(c) +β log( )with 0 < β < 1 Budget constraint: + /(1 + ) = ( ) + ( )/(1 + ) = This implies: / = β(1+r) For simplicity, assume β(1+r) = 1 Thus: = /(1 + β) = Agents consume a constant fraction of lifetime income (permanent income hypothesis).

22 A simple two period model of consumption = = /(1 + β) Using first period budget constraint: + = = /(1 + β) = " #$% [ ( )] Lend if future income (net of taxes) lower than today s income and borrow otherwise. From now on, we consider the borrowing case: < ( ) < 0 Financial frictions in the form of borrowing constraint would limit the possibility of borrowing.

23 Financial frictions (collateral constraint) Supposenowconsumershaveahouse & ofprice '. Housing is illiquid: cannot be sold but possible to borrow against housing wealth, with a collateral constraint: ) '& 1 + Borrowing in first period restricted by the value of collateral. Where ) is negatively related to the tightness of the constraint. ) = 0: no borrowing at all ) large enough : constraint does not matter

24 Financial frictions (collateral constraint) Assume optimal debt ( ) larger than what households can borrow: > ) +, #$-. This implies that consumers are constrained: = ) '& 1 + Using first period budget constraint: + = = ( ) + ) +, #$- Higher collateral value of housing allows more borrowing and thus higher consumption.

25 Financial frictions (collateral constraint) = ( ) + ) +, #$- For constrained consumers, fall in value of collateral will lead to one-for-one reduction in consumption. So reduction in price of housing p can lead to fall in consumption through a fall in collateral value for loans. Here we take p as exogenous, but fall in p can have an amplifier effect in equilibrium. Initial fall leads to less consumption, less borrowing. Reduces demand for housing, which can further drive down house prices and consumption. The fall in consumption is thus associated to a fall in aggregate demand and output.

26 Realeffectofafallinhousingwealth Prices (of consumption) Short Run Supply Curve Fall in housing wealth Output Aggregate demand falls through falling consumption when housing wealth falls.

27 U.S. Real Home Price Index ( ) Source: Shiller website

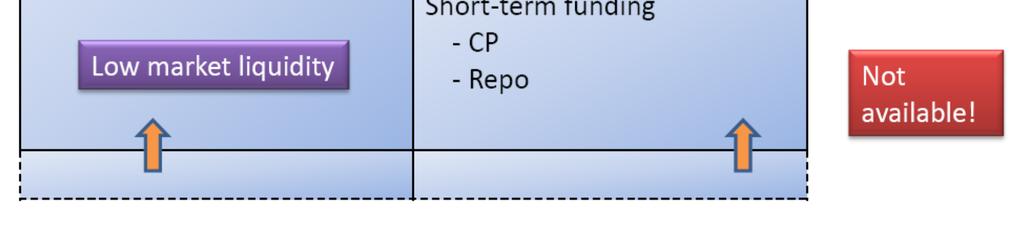

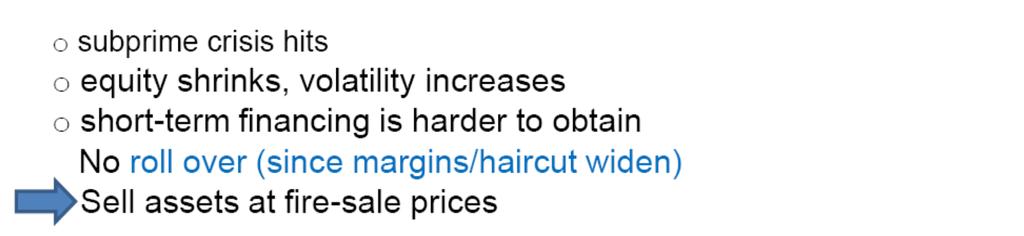

28 Financial frictions (collateral constraint) This amplification mechanism through collateral constraint illustrates how changes in the value of assets (here housing) can triggers economic fluctuations. The mechanism can be extended to banks and firms. Value of collateral of firms fall, which reduces their ability to borrow and triggers further fall in their value. Value of bank assets fall, which makes it hard for them to borrow. Need to sell assets, value banking assets drop further. Bank need to deleverage further. More fire sales of assets, etc... = Vicious spiral of deleveraging. Reminds the last financial crisis/recession. Opposite occurs in period of asset prices booms.

29 Bank balance sheets expand in good times

30 Deleveraging during the financial crisis

31 Financial accelerator The financial accelerator is a related concept. Small shocks to the economy get amplified by the financial accelerator. Decline in output and asset prices reduce the net worth of firms willing to borrow (the sum of his internal funds [liquid assets] and the collateral value of his illiquid assets) Financial distress increases risk for lenders Cost of external finance up and this reduces investment [Bernanke on the Great Depression and mechanism to understand current crisis]

32 Lecture 7: Business cycle fluctuations Part II 1. Real Business Cycles vs Keynesians 2. Asset markets and business cycles 3. International business cycles

33 International business cycles (IBC) In a globalized world, shocks (demand and supply) are transmitted across borders (through trade in goods and financial assets). International business cycles is about understanding the international propagation of shocks. A key feature of international business cycle is co-movements of the main aggregate variables across countries (consumption, investment, employment, output). Another important dimension is the understanding of international relative prices (think exchange rates) but we abstract fromitfornowandfocusonquantities.

34 Comovements Quarterlydata over Source: Ambler et al. (2004)

35 International business cycle facts Positive international propagation of shocks. Consumption, investment, employment and output positively correlated across countries. Why positive comovements of aggregate variables? Various hypothesis: - Positive spillovers of supply (think technology) shocks. To the opposite, country-specific technology shocks tend to predict negative comovements of output as inputs (labor and capital) are allocated towards their more productive use. - Positive spillovers of demand shocks through trade in particular (potentially also through financial markets).

36 Business cycle synchronization Crucial issue are the sources of business cycle synchronization. Obvious candidates: - Technological transfers. - Similar sectoral specialization. - Trade globalization(trade in goods). - Financial globalization(trade in financial assets).

37 Business cycle synchronization Typically run the following regression for country pairs (., 0): 1 23,4 = " , ,4 7;# 1 23,4 =measureofsynchronizationbetweencountry. and (0)atdate () 5 2 and 5 3 arecountryspecificfactors 8 23,4 are determinants of synchronization between country. and 0 at date (distance,tradeingoodsbetween. and 0.). Ideally, control for country bilateral fixed factors and estimate effects in the time-dimension: : 1 23,4 = " , ,4 7;# :

38 1 Trade intensity and business cycle synchronization (France vis-à-vis OECD countries) Business cycle synchronization with France 0,8 0,6 0,4 0,2 0-2,5 USA GER BEL PER NOR -0,2 Indicator of Trade Intensity with France controlling for size of trading partner Health warning: correlation is not causality

39 Empiricalfindings Identification of causality difficult but quite a consensus that: - Trade globalization (trade in goods) between countries increase their synchronization. - So does the similarity in sectoral specialization. - Geographical distance is also a strong predictor: countries further apart exhibit less synchronization. Holds controlling for trade and specialization similarity. Technological transfers? - The impact of financial integration between countries is found to be more ambiguous. Why?

40 Trade, Finance, Specialization and Synchronization Trade Integration + Financial Integration + + (but small)? Business cycle synchronization + Sectoral Specialization - This figure from Imbs (2004) summarizes the effects of variable x on y (with x and y being trade integration, financial integration, specialization and cycle synchronization). Source: Imbs (2004)

41 Financial integration and the transmission of shocks On going debate regarding the impact of financial integration between countries on business cycle synchronization and international transmission of last financial crisis. Kalemli-Ozcan, Papaioannou and Peydro (2011) revisits the question. 1. Identifytheeffectinthetimeseries. 2. Use legal harmonization of financial harmonization within the EU to identify properly the causality. Countries within the EU adopted European directives at different dates. Find that financial integration within EU lowers business cycle synchronization in normal times. But opposite in times of financial crisis.

42 Banking Integration and Synchronization Source: Kalemli-Ozcan, Papaioannou and Peydro(2011)

43 Banking Integration and Synchronization Source: Kalemli-Ozcan, Papaioannou and Peydro(2011)

44 Financial crisis, recessions and recoveries Recessions Output loss (percent from peak) Duration (quarters) All recessions Recoveries Time until recovery to previous peak (quarters) Output gain after four quarters (percent from trough) All recessions Financial crises Financial crises Highly synchronized recessions Financial crises which are highly synchronized Highly synchronized recessions Financial crises which are highly synchronized Source: IMF WEO April 2009

45 Financial integration and the transmission of the financial crisis Application: emerging markets lending during the crisis Emerging markets are prone to sudden stop in capital flows. Large fall of capital inflows towards these markets during the last financial crisis. True across all asset classes but especially relevant for international bank lending. = The international lending channel See Goldberg and Cetorelli(2009)

46 Source: Goldberg and Cetorelli (2009)

47 Financial integration and the transmission of shocks Application: emerging markets lending during the crisis Goldberg and Cetorelli(2009) emphasize how global banks played a significant role in the transmission of the 2007 to 2009 crisis to emerging market economies. Loan supply in emerging markets was significantly reduced through three different channels (i) a contraction in direct, cross-border lending by foreign banks (ii) a contraction in local lending by foreign banks affiliates in emerging markets (iii) a contraction in loan supply by domestic banks resulting from the funding shock to their balance sheet induced by the decline in lending through interbank markets Banks relying on distressed global banks for funding were more heavily hit.

48 International Lending Channel Large Global Bank (in the US) Asset Liabilities Liquid assets Deposit Foreign Loans Internal borrowing Domestic Loans Foreign Affiliate (in Argentina) Asset Liabilities Liquid assets Deposit Internal Lending Loans Small stand-alone bank (in Argentina) Asset Liquid assets Loans Liabilities Deposit Foreign borrowing

49 Summary Two views of the business cycle: 1) driven by demand shocks that are propagated through price rigidities; 2) driven by supply shocks (technology) propagated through investment and employment. Consensus that demand shocks tend to dominate at least at shorter horizons. Financial frictions (collateral or borrowing constraints) amplify business cycles. Shocks propagate internationally, generating international comovements. Trade globalization amplify such international comovements while the role of financial globalization is more ambiguous. During the last financial crisis though, financial globalization spread the crisis globally.

Understanding the World Economy Final Exam Indicative answers

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

1 Business-Cycle Facts Around the World 1

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

The Real Business Cycle Model

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

Financial Regulation, Banking Integration, and Business Cycle Synchronization

Financial Regulation, Banking Integration, and Business Cycle Synchronization Elias Papaioannou (London Business School, CEPR, and NBER) European Investment Bank Luxembourg February 2014 1 Introduction

Financial Regulation, Banking Integration, and Business Cycle Synchronization Elias Papaioannou (London Business School, CEPR, and NBER) European Investment Bank Luxembourg February 2014 1 Introduction

A Real Intertemporal Model with Investment Copyright 2014 Pearson Education, Inc.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Intermediate Macroeconomics

Intermediate Macroeconomics Lecture 5 - An Equilibrium Business Cycle Model Zsófia L. Bárány Sciences Po 2011 October 5 What is a business cycle? business cycles are the deviation of real GDP from its

Intermediate Macroeconomics Lecture 5 - An Equilibrium Business Cycle Model Zsófia L. Bárány Sciences Po 2011 October 5 What is a business cycle? business cycles are the deviation of real GDP from its

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri Name (print): Name (signature): Section Registered (circle one): T 1:30 T 6:00 W 1:30 As always, the honor code rules are in effect. You know

Final Exam Macroeconomics Winter 2011 Prof. Veronica Guerrieri Name (print): Name (signature): Section Registered (circle one): T 1:30 T 6:00 W 1:30 As always, the honor code rules are in effect. You know

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Bubbles, Liquidity and the Macroeconomy

Bubbles, Liquidity and the Macroeconomy Markus K. Brunnermeier The recent financial crisis has shown that financial frictions such as asset bubbles and liquidity spirals have important consequences not

Bubbles, Liquidity and the Macroeconomy Markus K. Brunnermeier The recent financial crisis has shown that financial frictions such as asset bubbles and liquidity spirals have important consequences not

VII. Short-Run Economic Fluctuations

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Business Cycles II: Theories

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

ECS 3701 Monetary Economics

ECS 3701 Monetary Economics Boston UNISA 2015 26: Transmission Mechanisms of Monetary Policy Errol Goetsch 078 573 5046 errol@xe4.org Lorraine 082 770 4569 lg@xe4.org www.facebook.com/groups/ecs3701 Page

ECS 3701 Monetary Economics Boston UNISA 2015 26: Transmission Mechanisms of Monetary Policy Errol Goetsch 078 573 5046 errol@xe4.org Lorraine 082 770 4569 lg@xe4.org www.facebook.com/groups/ecs3701 Page

1 Asset Pricing: Bonds vs Stocks

Asset Pricing: Bonds vs Stocks The historical data on financial asset returns show that one dollar invested in the Dow- Jones yields 6 times more than one dollar invested in U.S. Treasury bonds. The return

Asset Pricing: Bonds vs Stocks The historical data on financial asset returns show that one dollar invested in the Dow- Jones yields 6 times more than one dollar invested in U.S. Treasury bonds. The return

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Fall University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Notes VI - Models of Economic Fluctuations

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

MACROECONOMICS II - CONSUMPTION

MACROECONOMICS II - CONSUMPTION Stefania MARCASSA stefania.marcassa@u-cergy.fr http://stefaniamarcassa.webstarts.com/teaching.html 2016-2017 Plan An introduction to the most prominent work on consumption,

MACROECONOMICS II - CONSUMPTION Stefania MARCASSA stefania.marcassa@u-cergy.fr http://stefaniamarcassa.webstarts.com/teaching.html 2016-2017 Plan An introduction to the most prominent work on consumption,

Please choose the most correct answer. You can choose only ONE answer for every question.

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Cost Shocks in the AD/ AS Model

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Intertemporal choice: Consumption and Savings

Econ 20200 - Elements of Economics Analysis 3 (Honors Macroeconomics) Lecturer: Chanont (Big) Banternghansa TA: Jonathan J. Adams Spring 2013 Introduction Intertemporal choice: Consumption and Savings

Econ 20200 - Elements of Economics Analysis 3 (Honors Macroeconomics) Lecturer: Chanont (Big) Banternghansa TA: Jonathan J. Adams Spring 2013 Introduction Intertemporal choice: Consumption and Savings

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Spring University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 27 Readings GLS Ch. 8 2 / 27 Microeconomics of Macro We now move from the long run (decades

Real Business Cycle (RBC) Theory

Theory") Real Business Cycle (RBC) Theory ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 17 Readings GLS Ch. 17 GLS Ch. 19 2 / 17 The Neoclassical Model and RBC

Real Business Cycle (RBC) Theory ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 17 Readings GLS Ch. 17 GLS Ch. 19 2 / 17 The Neoclassical Model and RBC

Risk Shocks and Economic Fluctuations. Summary of work by Christiano, Motto and Rostagno

Risk Shocks and Economic Fluctuations Summary of work by Christiano, Motto and Rostagno Outline Simple summary of standard New Keynesian DSGE model (CEE, JPE 2005 model). Modifications to introduce CSV

Risk Shocks and Economic Fluctuations Summary of work by Christiano, Motto and Rostagno Outline Simple summary of standard New Keynesian DSGE model (CEE, JPE 2005 model). Modifications to introduce CSV

Road Map. Does consumption theory accurately match the data? What theories of consumption seem to match the data?

TOPIC 3 The Demand Side of the Economy Road Map What drives business investment decisions? What drives household consumption? What is the link between consumption and savings? Does consumption theory accurately

TOPIC 3 The Demand Side of the Economy Road Map What drives business investment decisions? What drives household consumption? What is the link between consumption and savings? Does consumption theory accurately

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

IN THIS LECTURE, YOU WILL LEARN:

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

Financial Factors in Business Cycles

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Quantitative Significance of Collateral Constraints as an Amplification Mechanism

RIETI Discussion Paper Series 09-E-05 Quantitative Significance of Collateral Constraints as an Amplification Mechanism INABA Masaru The Canon Institute for Global Studies KOBAYASHI Keiichiro RIETI The

RIETI Discussion Paper Series 09-E-05 Quantitative Significance of Collateral Constraints as an Amplification Mechanism INABA Masaru The Canon Institute for Global Studies KOBAYASHI Keiichiro RIETI The

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Chapter 11. Market-Clearing Models of the Business Cycle. Copyright 2008 Pearson Addison-Wesley. All rights reserved.

Chapter 11 Market-Clearing Models of the Business Cycle Study Two Market-Clearing Business Cycle Models Real Business Cycle Model Keynesian Coordination Failure Model 11-2 Applying Bank Run Model to Financial

Chapter 11 Market-Clearing Models of the Business Cycle Study Two Market-Clearing Business Cycle Models Real Business Cycle Model Keynesian Coordination Failure Model 11-2 Applying Bank Run Model to Financial

Channels of Monetary Policy Transmission. Konstantinos Drakos, MacroFinance, Monetary Policy Transmission 1

Channels of Monetary Policy Transmission Konstantinos Drakos, MacroFinance, Monetary Policy Transmission 1 Discusses the transmission mechanism of monetary policy, i.e. how changes in the central bank

Channels of Monetary Policy Transmission Konstantinos Drakos, MacroFinance, Monetary Policy Transmission 1 Discusses the transmission mechanism of monetary policy, i.e. how changes in the central bank

Review: objectives. CHAPTER 2 The Data of Macroeconomics slide 0

Review: objectives Remind you of the main theories. Overview of how parts of the course all fit together. Draw the most important and general lessons to remember from the course. CHAPTER 2 The Data of

Review: objectives Remind you of the main theories. Overview of how parts of the course all fit together. Draw the most important and general lessons to remember from the course. CHAPTER 2 The Data of

Monetary Business Cycles. Introduction: The New Keynesian Model in the context of Macro Theory

Monetary Business Cycles Introduction: The New Keynesian Model in the context of Macro Theory Monetary business cycles Continuation of Real Business cycles (A. Pommeret) 2 problem sets Common exam Martina.Insam@unil.ch,

Monetary Business Cycles Introduction: The New Keynesian Model in the context of Macro Theory Monetary business cycles Continuation of Real Business cycles (A. Pommeret) 2 problem sets Common exam Martina.Insam@unil.ch,

11/6/2013. Chapter 17: Consumption. Early empirical successes: Results from early studies. Keynes s conjectures. The Keynesian consumption function

Keynes s conjectures Chapter 7:. 0 < MPC < 2. Average propensity to consume (APC) falls as income rises. (APC = C/ ) 3. Income is the main determinant of consumption. 0 The Keynesian consumption function

Keynes s conjectures Chapter 7:. 0 < MPC < 2. Average propensity to consume (APC) falls as income rises. (APC = C/ ) 3. Income is the main determinant of consumption. 0 The Keynesian consumption function

Business Cycles II: Theories

International Economics and Business Dynamics Class Notes Business Cycles II: Theories Revised: November 23, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm In the previous lecture

International Economics and Business Dynamics Class Notes Business Cycles II: Theories Revised: November 23, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm In the previous lecture

Micro-foundations: Consumption. Instructor: Dmytro Hryshko

Micro-foundations: Consumption Instructor: Dmytro Hryshko 1 / 74 Why Study Consumption? Consumption is the largest component of GDP (e.g., about 2/3 of GDP in the U.S.) 2 / 74 J. M. Keynes s Conjectures

Micro-foundations: Consumption Instructor: Dmytro Hryshko 1 / 74 Why Study Consumption? Consumption is the largest component of GDP (e.g., about 2/3 of GDP in the U.S.) 2 / 74 J. M. Keynes s Conjectures

New Keynesian Model. Prof. Eric Sims. Fall University of Notre Dame. Sims (ND) New Keynesian Model Fall / 20

New Keynesian Model Fall / 20") New Keynesian Model Prof. Eric Sims University of Notre Dame Fall 2012 Sims (ND) New Keynesian Model Fall 2012 1 / 20 New Keynesian Economics New Keynesian (NK) model: leading alternative to RBC model

New Keynesian Model Prof. Eric Sims University of Notre Dame Fall 2012 Sims (ND) New Keynesian Model Fall 2012 1 / 20 New Keynesian Economics New Keynesian (NK) model: leading alternative to RBC model

Macro Notes: Introduction to the Short Run

Macro Notes: Introduction to the Short Run Alan G. Isaac American University But this long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy,

Macro Notes: Introduction to the Short Run Alan G. Isaac American University But this long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy,

Macroeconomic Cycle and Economic Policy

Macroeconomic Cycle and Economic Policy Lecture 1 Nicola Viegi University of Pretoria 2016 Introduction Macroeconomics as the study of uctuations in economic aggregate Questions: What do economic uctuations

Macroeconomic Cycle and Economic Policy Lecture 1 Nicola Viegi University of Pretoria 2016 Introduction Macroeconomics as the study of uctuations in economic aggregate Questions: What do economic uctuations

A Real Intertemporal Model with Investment

Test Thursday, 16 th of February starting at 18:00 (ca. an hour), B34 There will be a session (solving last year s test) Tuesday 14 th of February at 18:00 Copyright 2005 Pearson Education and Dr Yunus

Test Thursday, 16 th of February starting at 18:00 (ca. an hour), B34 There will be a session (solving last year s test) Tuesday 14 th of February at 18:00 Copyright 2005 Pearson Education and Dr Yunus

Chapter 16 Consumption. 8 th and 9 th editions 4/29/2017. This chapter presents: Keynes s Conjectures

2 0 1 0 U P D A T E 4/29/2017 Chapter 16 Consumption 8 th and 9 th editions This chapter presents: An introduction to the most prominent work on consumption, including: John Maynard Keynes: consumption

2 0 1 0 U P D A T E 4/29/2017 Chapter 16 Consumption 8 th and 9 th editions This chapter presents: An introduction to the most prominent work on consumption, including: John Maynard Keynes: consumption

MACROECONOMICS FOR ECONOMIC POLICY

COURSE SYLLABUS MACROECONOMICS FOR ECONOMIC POLICY Instructors: Adam Reiff (lecturer), Rita Peto (TA) Department: Department of Economics, Central European University Semester and year: Fall, 2014/2015

COURSE SYLLABUS MACROECONOMICS FOR ECONOMIC POLICY Instructors: Adam Reiff (lecturer), Rita Peto (TA) Department: Department of Economics, Central European University Semester and year: Fall, 2014/2015

A Theory of Macroprudential Policies in the Presence of Nominal Rigidities by Farhi and Werning

A Theory of Macroprudential Policies in the Presence of Nominal Rigidities by Farhi and Werning Discussion by Anton Korinek Johns Hopkins University SF Fed Conference March 2014 Anton Korinek (JHU) Macroprudential

A Theory of Macroprudential Policies in the Presence of Nominal Rigidities by Farhi and Werning Discussion by Anton Korinek Johns Hopkins University SF Fed Conference March 2014 Anton Korinek (JHU) Macroprudential

Long-term uncertainty and social security systems

Long-term uncertainty and social security systems Jesús Ferreiro and Felipe Serrano University of the Basque Country (Spain) The New Economics as Mainstream Economics Cambridge, January 28 29, 2010 1 Introduction

Long-term uncertainty and social security systems Jesús Ferreiro and Felipe Serrano University of the Basque Country (Spain) The New Economics as Mainstream Economics Cambridge, January 28 29, 2010 1 Introduction

Business Cycles. (c) Copyright 1998 by Douglas H. Joines 1

Copyright 1998 by Douglas H. Joines 1") Business Cycles (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the causes of business cycles Know how interest rates are determined Know how various economic indicators behave over the

Business Cycles (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the causes of business cycles Know how interest rates are determined Know how various economic indicators behave over the

Chapter 19/Epilogue: Advances in the Theory of Macroeconomic Fluctuations. Instructor: Dmytro Hryshko

Chapter 19/Epilogue: Advances in the Theory of Macroeconomic Fluctuations Instructor: Dmytro Hryshko Two Approaches We can summarize theories of business cycles by their view of functioning of the economy's

Chapter 19/Epilogue: Advances in the Theory of Macroeconomic Fluctuations Instructor: Dmytro Hryshko Two Approaches We can summarize theories of business cycles by their view of functioning of the economy's

Macroeconomics. Based on the textbook by Karlin and Soskice: Macroeconomics: Institutions, Instability, and the Financial System

Based on the textbook by Karlin and Soskice: : Institutions, Instability, and the Financial System Robert M Kunst robertkunst@univieacat University of Vienna and Institute for Advanced Studies Vienna October

Based on the textbook by Karlin and Soskice: : Institutions, Instability, and the Financial System Robert M Kunst robertkunst@univieacat University of Vienna and Institute for Advanced Studies Vienna October

Intermediate Macroeconomics

Intermediate Macroeconomics Lecture 10 - Consumption 2 Zsófia L. Bárány Sciences Po 2014 April Last week Keynesian consumption function Kuznets puzzle permanent income hypothesis life-cycle theory of consumption

Intermediate Macroeconomics Lecture 10 - Consumption 2 Zsófia L. Bárány Sciences Po 2014 April Last week Keynesian consumption function Kuznets puzzle permanent income hypothesis life-cycle theory of consumption

The Goods Market and the Aggregate Expenditures Model

The Goods Market and the Aggregate Expenditures Model Chapter 8 The Historical Development of Modern Macroeconomics The Great Depression of the 1930s led to the development of macroeconomics and aggregate

The Goods Market and the Aggregate Expenditures Model Chapter 8 The Historical Development of Modern Macroeconomics The Great Depression of the 1930s led to the development of macroeconomics and aggregate

Real Business Cycle Theory

Real Business Cycle Theory Paul Scanlon November 29, 2010 1 Introduction The emphasis here is on technology/tfp shocks, and the associated supply-side responses. As the term suggests, all the shocks are

Real Business Cycle Theory Paul Scanlon November 29, 2010 1 Introduction The emphasis here is on technology/tfp shocks, and the associated supply-side responses. As the term suggests, all the shocks are

Financial Institutions, Markets and Regulation: A Survey

Financial Institutions, Markets and Regulation: A Survey Thorsten Beck, Elena Carletti and Itay Goldstein COEURE workshop on financial markets, 6 June 2015 Starting point The recent crisis has led to intense

Financial Institutions, Markets and Regulation: A Survey Thorsten Beck, Elena Carletti and Itay Goldstein COEURE workshop on financial markets, 6 June 2015 Starting point The recent crisis has led to intense

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction

Chapter 1 Introduction") Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Chapter 2. Literature Review

Chapter 2 Literature Review There is a wide agreement that monetary policy is a tool in promoting economic growth and stabilizing inflation. However, there is less agreement about how monetary policy exactly

Chapter 2 Literature Review There is a wide agreement that monetary policy is a tool in promoting economic growth and stabilizing inflation. However, there is less agreement about how monetary policy exactly

Consumption. Basic Determinants. the stream of income

Consumption Consumption commands nearly twothirds of total output in the United States. Most of what the people of a country produce, they consume. What is left over after twothirds of output is consumed

Consumption Consumption commands nearly twothirds of total output in the United States. Most of what the people of a country produce, they consume. What is left over after twothirds of output is consumed

Why are some countries richer than others? Part 2

Understanding the World Economy Why are some countries richer than others? Part 2 Lecture 2 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 2 : Why are some countries richer than others?

Understanding the World Economy Why are some countries richer than others? Part 2 Lecture 2 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 2 : Why are some countries richer than others?

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Advanced Macroeconomics 6. Rational Expectations and Consumption

Advanced Macroeconomics 6. Rational Expectations and Consumption Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Consumption Spring 2015 1 / 22 A Model of Optimising Consumers We will

Advanced Macroeconomics 6. Rational Expectations and Consumption Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Consumption Spring 2015 1 / 22 A Model of Optimising Consumers We will

MODERN PRINCIPLES: MACROECONOMICS. Tyler Cowen George Mason University. Alex Tabarrok George Mason University. Worth Publishers

MODERN PRINCIPLES: MACROECONOMICS Tyler Cowen George Mason University Alex Tabarrok George Mason University Worth Publishers CONTENTS Preface xv CHAPTER 1 The Big Ideas 1 Big Idea One: Incentives Matter

MODERN PRINCIPLES: MACROECONOMICS Tyler Cowen George Mason University Alex Tabarrok George Mason University Worth Publishers CONTENTS Preface xv CHAPTER 1 The Big Ideas 1 Big Idea One: Incentives Matter

Understanding the World Economy Master in Economics and Business. Fiscal policy. Nicolas Coeurdacier

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

Financial Crises and Asset Prices. Tyler Muir June 2017, MFM

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Equilibrium with Production and Endogenous Labor Supply

Equilibrium with Production and Endogenous Labor Supply ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 21 Readings GLS Chapter 11 2 / 21 Production and

Equilibrium with Production and Endogenous Labor Supply ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 21 Readings GLS Chapter 11 2 / 21 Production and

Keynesian Business Cycles & Policy

Keynesian Business Cycles & Policy 1. Keynesian Business Cycles 2. Role for Monetary and Fiscal Policies 3. Government Budget De cits and Debt 1 Keynesian Business Cycles 1.1 Demand Shocks Stock market

Keynesian Business Cycles & Policy 1. Keynesian Business Cycles 2. Role for Monetary and Fiscal Policies 3. Government Budget De cits and Debt 1 Keynesian Business Cycles 1.1 Demand Shocks Stock market

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM Preface: This is not an answer sheet! Rather, each of the GSIs has written up some

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM Preface: This is not an answer sheet! Rather, each of the GSIs has written up some

Macroeconomic Models with Financial Frictions

Macroeconomic Models with Financial Frictions Jesús Fernández-Villaverde University of Pennsylvania December 2, 2012 Jesús Fernández-Villaverde (PENN) Macro-Finance December 2, 2012 1 / 26 Motivation I

Macroeconomic Models with Financial Frictions Jesús Fernández-Villaverde University of Pennsylvania December 2, 2012 Jesús Fernández-Villaverde (PENN) Macro-Finance December 2, 2012 1 / 26 Motivation I

If a model were to predict that prices and money are inversely related, that prediction would be evidence against that model.

The Classical Model This lecture will begin by discussing macroeconomic models in general. This material is not covered in Froyen. We will then develop and discuss the Classical Model. Students should

The Classical Model This lecture will begin by discussing macroeconomic models in general. This material is not covered in Froyen. We will then develop and discuss the Classical Model. Students should

ADVANCED MODERN MACROECONOMICS

ADVANCED MODERN MACROECONOMICS ANALYSIS AND APPLICATION Max Gillman Cardiff Business School, Cardiff University Financial Times Prentice Halt is an imprint of Harlow, England London New York Boston San

ADVANCED MODERN MACROECONOMICS ANALYSIS AND APPLICATION Max Gillman Cardiff Business School, Cardiff University Financial Times Prentice Halt is an imprint of Harlow, England London New York Boston San

The Effects of Dollarization on Macroeconomic Stability

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

International Macroeconomics

Slides for Chapter 3: Theory of Current Account Determination International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 Motivation Build a model of an open economy to

Slides for Chapter 3: Theory of Current Account Determination International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University May 1, 2016 1 Motivation Build a model of an open economy to

A MODEL OF SECULAR STAGNATION

A MODEL OF SECULAR STAGNATION Gauti B. Eggertsson and Neil R. Mehrotra Brown University BIS Research Meetings March 11, 2015 1 / 38 SECULAR STAGNATION HYPOTHESIS I wonder if a set of older ideas... under

A MODEL OF SECULAR STAGNATION Gauti B. Eggertsson and Neil R. Mehrotra Brown University BIS Research Meetings March 11, 2015 1 / 38 SECULAR STAGNATION HYPOTHESIS I wonder if a set of older ideas... under

ECONOMICS. of Macroeconomic. Paper 4: Basic Macroeconomics Module 1: Introduction: Issues studied in Macroeconomics, Schools of Macroeconomic

Subject Paper No and Title Module No and Title Module Tag 4: Basic s 1: Introduction: Issues studied in s, Schools of ECO_P4_M1 Paper 4: Basic s Module 1: Introduction: Issues studied in s, Schools of

Subject Paper No and Title Module No and Title Module Tag 4: Basic s 1: Introduction: Issues studied in s, Schools of ECO_P4_M1 Paper 4: Basic s Module 1: Introduction: Issues studied in s, Schools of

Discussion of The International Transmission Channels of Monetary Policy Claudia Buch, Matthieu Bussiere, Linda Goldberg, and Robert Hills

Discussion of The International Transmission Channels of Monetary Policy Claudia Buch, Matthieu Bussiere, Linda Goldberg, and Robert Hills Jean Imbs June 2017 Imbs (2017) Banque de France - 30 June 2017

Discussion of The International Transmission Channels of Monetary Policy Claudia Buch, Matthieu Bussiere, Linda Goldberg, and Robert Hills Jean Imbs June 2017 Imbs (2017) Banque de France - 30 June 2017

EC307 ECONOMIC POLICY IN THE UK MACROECONOMIC POLICY THE TRANSMISSION OF MONETARY POLICY

EC307 ECONOMIC POLICY IN THE UK MACROECONOMIC POLICY THE TRANSMISSION OF MONETARY POLICY Summary This lecture gets inside the black box, discussing the transmission mechanism of monetary policy, outlining

EC307 ECONOMIC POLICY IN THE UK MACROECONOMIC POLICY THE TRANSMISSION OF MONETARY POLICY Summary This lecture gets inside the black box, discussing the transmission mechanism of monetary policy, outlining

Deflation, Credit Collapse and Great Depressions. Enrique G. Mendoza

Deflation, Credit Collapse and Great Depressions Enrique G. Mendoza Main points In economies where agents are highly leveraged, deflation amplifies the real effects of credit crunches Credit frictions

Deflation, Credit Collapse and Great Depressions Enrique G. Mendoza Main points In economies where agents are highly leveraged, deflation amplifies the real effects of credit crunches Credit frictions

Incorporate Financial Frictions into a

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Basic macroeconomic concepts

Basic macroeconomic concepts in preparation for API-120 Prof. Jeffrey Frankel MPA/ID program August 2015 Lecture (i) -- GDP definitions Reading on growth accounting: Krugman, 1994, The Myth of the Asian

Basic macroeconomic concepts in preparation for API-120 Prof. Jeffrey Frankel MPA/ID program August 2015 Lecture (i) -- GDP definitions Reading on growth accounting: Krugman, 1994, The Myth of the Asian

Macroeconomics II Consumption

Macroeconomics II Consumption Vahagn Jerbashian Ch. 17 from Mankiw (2010); 16 from Mankiw (2003) Spring 2018 Setting up the agenda and course Our classes start on 14.02 and end on 31.05 Lectures and practical

Macroeconomics II Consumption Vahagn Jerbashian Ch. 17 from Mankiw (2010); 16 from Mankiw (2003) Spring 2018 Setting up the agenda and course Our classes start on 14.02 and end on 31.05 Lectures and practical

Objectives THE BUSINESS CYCLE CHAPTER

14 THE BUSINESS CYCLE CHAPTER Objectives After studying this chapter, you will able to Distinguish among the different theories of the business cycle Explain the Keynesian and monetarist theories of the

14 THE BUSINESS CYCLE CHAPTER Objectives After studying this chapter, you will able to Distinguish among the different theories of the business cycle Explain the Keynesian and monetarist theories of the

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Default Risk and Credit Rationing Spring 2016 1 / 39 Moving

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Default Risk and Credit Rationing Spring 2016 1 / 39 Moving

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan The US recession that began in late 2007 had significant spillover effects to the rest

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan The US recession that began in late 2007 had significant spillover effects to the rest

D OES A L OW-I NTEREST-R ATE R EGIME P UNISH S AVERS?

D OES A L OW-I NTEREST-R ATE R EGIME P UNISH S AVERS? James Bullard President and CEO Applications of Behavioural Economics and Multiple Equilibrium Models to Macroeconomic Policy Conference July 3, 2017

D OES A L OW-I NTEREST-R ATE R EGIME P UNISH S AVERS? James Bullard President and CEO Applications of Behavioural Economics and Multiple Equilibrium Models to Macroeconomic Policy Conference July 3, 2017

An Introduction to Macroeconomics

An Introduction to Macroeconomics Economics 4353 - Intermediate Macroeconomics Aaron Hedlund University of Missouri Fall 2015 Econ 4353 (University of Missouri) Introduction Fall 2015 1 / 19 What is Macroeconomics?

An Introduction to Macroeconomics Economics 4353 - Intermediate Macroeconomics Aaron Hedlund University of Missouri Fall 2015 Econ 4353 (University of Missouri) Introduction Fall 2015 1 / 19 What is Macroeconomics?

Macroeconomics. Lecture 5: Consumption. Hernán D. Seoane. Spring, 2016 MEDEG, UC3M UC3M

Macroeconomics MEDEG, UC3M Lecture 5: Consumption Hernán D. Seoane UC3M Spring, 2016 Introduction A key component in NIPA accounts and the households budget constraint is the consumption It represents

Macroeconomics MEDEG, UC3M Lecture 5: Consumption Hernán D. Seoane UC3M Spring, 2016 Introduction A key component in NIPA accounts and the households budget constraint is the consumption It represents

Part III. Cycles and Growth:

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Exploding Bubbles In a Macroeconomic Model. Narayana Kocherlakota

Bubbles Exploding Bubbles In a Macroeconomic Model Narayana Kocherlakota presented by Kaiji Chen Macro Reading Group, Jan 16, 2009 1 Bubbles Question How do bubbles emerge in an economy when collateral

Bubbles Exploding Bubbles In a Macroeconomic Model Narayana Kocherlakota presented by Kaiji Chen Macro Reading Group, Jan 16, 2009 1 Bubbles Question How do bubbles emerge in an economy when collateral

Lecture 25 Unemployment Financial Crisis. Noah Williams

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

ECNS 303 Ch. 16: Consumption

ECNS 303 Ch. 16: Consumption Micro foundations of Macro: Consumption Q. How do households decide how much of their income to consume today and how much to save for the future? Micro question with macro

ECNS 303 Ch. 16: Consumption Micro foundations of Macro: Consumption Q. How do households decide how much of their income to consume today and how much to save for the future? Micro question with macro

Aggregate Effects of Collateral Constraints

Thomas Chaney, Zongbo Huang, David Sraer, David Thesmar discussion by Toni Whited 2016 WFA The goal of the paper is to quantify the welfare effects of collateral constraints. Reduced form regressions of

Thomas Chaney, Zongbo Huang, David Sraer, David Thesmar discussion by Toni Whited 2016 WFA The goal of the paper is to quantify the welfare effects of collateral constraints. Reduced form regressions of

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Understanding the World Economy. Fiscal policy. Nicolas Coeurdacier Lecture 9

Understanding the World Economy Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3. Debt and deficits 4. Fiscal policy

Understanding the World Economy Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3. Debt and deficits 4. Fiscal policy

7.3 The Household s Intertemporal Budget Constraint

Summary Chapter 7 Borrowing, Lending, and Budget Constraints 7.1 Overview - Borrowing and lending is a fundamental act of economic life - Expectations about future exert the greatest influence on firms

Summary Chapter 7 Borrowing, Lending, and Budget Constraints 7.1 Overview - Borrowing and lending is a fundamental act of economic life - Expectations about future exert the greatest influence on firms

III. 9. IS LM: the basic framework to understand macro policy continued Text, ch 11

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Consumption, Saving, and Investment. Chapter 4. Copyright 2009 Pearson Education Canada

Consumption, Saving, and Investment Chapter 4 Copyright 2009 Pearson Education Canada This Chapter In Chapter 3 we saw how the supply of goods is determined. In this chapter we will turn to factors that

Consumption, Saving, and Investment Chapter 4 Copyright 2009 Pearson Education Canada This Chapter In Chapter 3 we saw how the supply of goods is determined. In this chapter we will turn to factors that

Comments by: Sebnem Kalemli-Ozcan Associate Professor of Economics University of Houston and NBER. August 2007

Capital Flows and Asset Prices by Kosuke Aoki, Gianluca Benigno, and Nobuhiro Kiyotaki Comments by: Sebnem Kalemli-Ozcan Associate Professor of Economics University of Houston and NBER August 2007 This

Capital Flows and Asset Prices by Kosuke Aoki, Gianluca Benigno, and Nobuhiro Kiyotaki Comments by: Sebnem Kalemli-Ozcan Associate Professor of Economics University of Houston and NBER August 2007 This

Should Unconventional Monetary Policies Become Conventional?

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Understanding the World Economy Master in Economics and Business. Monetary policy. Nicolas Coeurdacier

Understanding the World Economy Master in Economics and Business Monetary policy Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 8 : Monetary policy 1. What is monetary policy?

Understanding the World Economy Master in Economics and Business Monetary policy Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 8 : Monetary policy 1. What is monetary policy?

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

ECONOMIC GROWTH 1. THE ACCUMULATION OF CAPITAL

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy. Martin Blomhoff Holm

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy Martin Blomhoff Holm Outline 1. Recap from lecture 10 (it was a lot of channels!) 2. The Zero Lower Bound and the

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy Martin Blomhoff Holm Outline 1. Recap from lecture 10 (it was a lot of channels!) 2. The Zero Lower Bound and the