The yellow highlighted areas are bear markets with NO recession.

|

|

|

- Jodie May

- 5 years ago

- Views:

Transcription

1 Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve gone back and looked at the major causes of each recession, bear market: The yellow highlighted areas are bear markets with NO recession.

2 Major Causes of Recessions and Bear Markets The main causes of recessions and bear markets include: Restrictive monetary policies, rising rates High oil prices Rising inflation Too much debt Bad allocation of capital Late phase of cycle Derivatives have played a role in most bear markets and recessions since 1987 Below is a current reading of my model of the economics section, there are several red flags: Most economic and market cycles end because toward the end of a cycle the economy is heating up and inflation is anticipated to be a problem so the Federal Reserve starts to raise rates. This

, Federal Reserve was raising rates 3. 1991, Gulf War I and high oil prices 4.")

3 causes the economy to slow down, and then the sins of the economic cycle start to show up, for example: too much leverage in housing, mortgages sold globally as tranches, derivatives , the bursting of the tech bubble (too much capital went into technology), Federal Reserve was raising rates , Gulf War I and high oil prices , derivatives, falling dollar, Iran Iraq war, rising oil prices Age of Economic Cycle Below is a chart that shows the growth and length of each expansion, cycle of the U.S. economy going back to 1950: The average expansion since 1950 lasts about 5.5 years. The longest expansion occurred from 1991 to 2002 thanks to the technology boom of the 1990s. The shortest was the 1980 expansion, as the economy was recovering from the high inflation, oil spikes and oil supply disruptions of the 1970s.

4 Also, notice growth has slowed for each expansion since the 1980s. I wrote about the causes of the slowing of the U.S. economy in a Special Report about the new normal. Click here to read the Special Report. Below is a chart that shows the forecasts and trends for this economic cycle, expansion: This expansion started in late 2009, so this economic cycle is mature and aging. The one benefit of slower growth is we don t get the normal inflation concerns where the Fed needs to raise rates to slow the economy and inflationary pressures. Inflation, Interest Rates and the Federal Reserve This cycle is very different than most cycles due to the Great Recession. Inflation and interest rates are at historic lows, especially this late in the cycle. Normally interest rates reflect at least inflation. Inflation has averaged about 1.8% this cycle, so interest rates are abnormally low. The Fed recently raised rates for the first time in almost ten years. Its goal is to normalize interest rates. It s expected that the Fed will raise rates about three to four times in This could be very disruptive to the markets, and economy. To stimulate the economy, the Federal Reserve will normally lower rates making it an easier decision for businesses to expand and consumers to purchase big ticket items. This cycle, the Fed lowered rates to.25%.

5 If the U.S. has a financial crisis, our Federal Reserve will not be able to lower rates enough to stimulate the economy. We could have a prolonged recession because the Fed has run out of effective monetary bullets, especially lowering rates to stimulate the economy. Below is a chart that shows the Fed Funds rate and CPI (inflation): Inflation and interest rates have been falling since the early 1980s. Notice that most of the time, the Fed Funds rate is higher than inflation. Since the Great Recession, the Fed Funds rate does not reflect inflation. Investors/savers who loan their money out want to be paid at least the rate of inflation. Many savers/investors have not kept up with inflation. Also notice in the above chart, inflation has fallen below zero during this economic cycle. The Federal Reserve has lots experience and tools to deal with inflation. It has less tools and experience dealing with deflation. Deflation has been a concern here in the U.S. and globally. Below is the latest federal funds rate forecasts from the Federal Reserve.

6 Most Federal Reserve members forecast rates to be ½ to 1% higher next year. If this happens, the raises could be disruptive to the markets and economy as it has been in the past. The prospect that the Fed will continue to raise rates is a red flag. Credit Spreads and Yield Curves Credit spreads are widening and this is a red flag. Below is a current chart of credit spreads:

7 The chart shows how high yield rates are rising, and the spread between corporate and high yield rates is widening. This normally means that investors are probably selling their high yield bonds because of fear of defaults. This normally occurs as we near a recession. Analysts and economists will point out that many energy companies have issued high yield bonds, and because oil prices are below breakeven points investors are selling their energy high yield bonds due to fear of defaults. There have already been over a dozen energy company bankruptcies, most of them are very small companies. It is true that junk bonds in the energy sector is a major concern, but investors are selling their high yield bond funds and ETFs causing more high yield bonds to sell off, thus lower prices and higher yields. The yield curve is not a problem and probably won t be. When short-term yields move higher than long-term yields (aka inverted yield curve) it tells investors that short-term yields are rising because of inflation pressures. Short-term rising rates should slow down the economy easing inflationary pressures. Long-term rates don t rise as much under this scenario. Historically inverted yield curves are an indicator of a potential recession. Here is the current chart for the yield curve:

8 The current yield curve is normal, with long-term rates are higher than short-term rates. It s hard to imagine that short-term rates could move higher than long-term rates in this slow growth, low inflation environment. Oil Prices and the Middle East For the past four decades, many cycles ended caused high oil prices due to strong economic activity or oil supply disruptions due to wars, conflicts in the Middle East. This cycle is very different, oil prices are down substantially. Lower oil prices should help the consumer and many countries and industries that are dependent on oil. The oil industry is important to our economy because it provides many high paying jobs, and the oil our economy needs (we still import about 6 million barrels of oil a day). The U.S. oil industry, similar to many oil nations and international energy companies, are struggling to survive with these very low oil prices. Currently oil prices are lower than many oil company breakeven points. Most oil companies had losses this year, and is one of the reasons for the poor performance of the markets. Oil company debt is becoming a concern as written about in the section above. There are many reasons for lower oil prices that I will analyze in a future monthly issue. Most analysts believe oil prices will be higher if we don t have a recession, especially if we have oil supply disruptions from the oil rich Middle East. The Middle East is more volatile and dangerous than normal. The fall is oil prices is part of a larger problem the global economy faces.

9 International Risks are Rising Most of the risks the U.S. economy and markets face are external, and are red flags, especially debt levels and poor allocation of capital. I wrote an article earlier this year about the reversal of a major global trend, the China and commodities boom. Click here to read the article. Below are excerpts from the Special Report: In the 2000s, the major economic trends were China and the global financial crisis. China s growth and global central bank money printing as a remedy to the global financial crisis caused a repeat of the 1970s inflation hedges and real assets as the preferred investments. There are many signs that these two trends are reversing. China has been a major trend for the 21 st century. The economic growth of China has been unprecedented. China has grown from near zero to about half the GDP of the U.S. China s growth has basically been driven by manufacturing, government spending in infrastructure, and real estate development. China s economic story is in transition: it s slowing and the government is trying to shift it from a manufacturing and export driven economy to a consumer driven economy like the U.S. and Japan. The U.S. s economy is about 70% consumer. Below are the current trends for China:

10 China s growth is slowing. It s going to be harder for China to grow at its past pace because of the law of large numbers. The charts show that the transition to a consumer driven economy is not going well. China does not have the safety nets that the U.S. has, so the Chinese save a lot more, and they tend to want to invest their savings into real estate. The slowdown in the Chinese economy, and also the transition to a consumption economy has caused a reversal in commodity prices. China is not buying the quantity of iron ore, copper, lumber. as it has in the past. Below is a 15-year chart of the Dow Jones Commodity Futures Index:

11 Let s review the chart: As China s voracious appetite for most commodities grew in the early part of the century, commodity prices more than tripled during the period. Prices collapsed during the financial crisis, and the long-term bullish trend line was broken. Prices did recover. As China s growth is showing signs of slowing, and as it tries to make its transition to consumption, commodity prices resumed its bearish trend. The index and many commodity prices are down about 50% from its peak. Most commodities are in bear markets. Commodity prices need to find a bottom and then consolidate, similar to what prices did in 2009, If the Chinese economy continues to decelerate, then the impact on commodities and resource economies, countries (Canada, Australia, Russia, Middle East, Africa, Latin America ) could cause more economic and market stress, especially those countries that have high debt. China is now having to deal with the massive debt (282% of GDP), and their bad capital allocation decisions by its centrally planned economy. This is what normally happens at the end of a cycle, trend: too much debt and bad capital allocation decisions. China does have about a $3 trillion foreign reserve surplus, so this could help them, but they could continue to make bad economic and capital allocation decisions. China will continue to play a major role in the global economy, but it won t be similar to its economic boom in the first decade of the 21 st century.

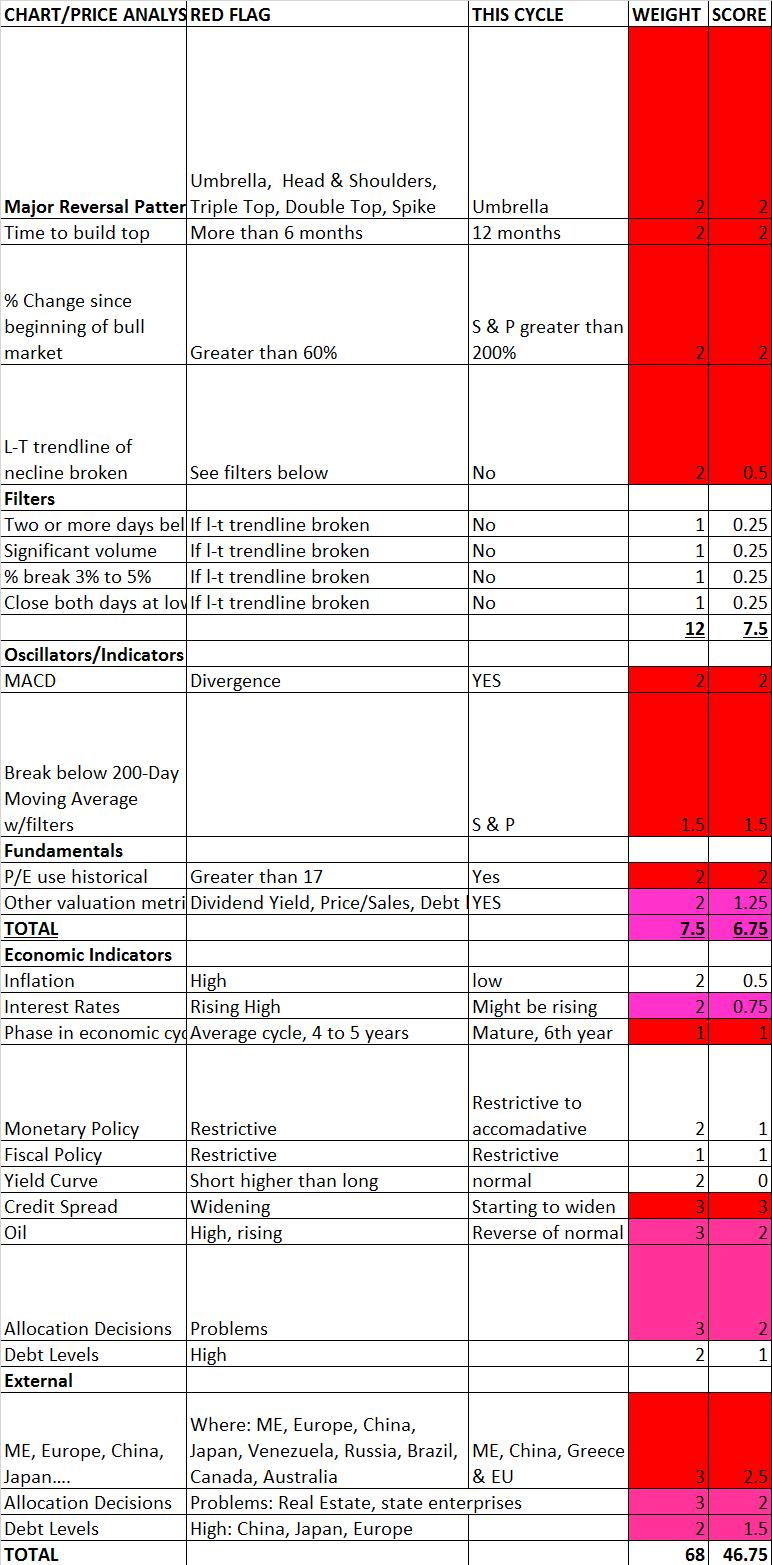

12 Again, the major trend reversal of the China and commodity boom is a major risk to the global economy including the U.S. Conclusion My model is at 69%, the potential of a major market reversal. Here is the current reading of my model:

13

14 The red flags include: A long-term topping pattern that is in its 12 th month of formation (the longer a formation takes to develop, the more serious the formation is) The topping pattern is an identifiable rounding top, umbrella pattern Breaking of the 200-day moving average, considered a long-term trend MACD diverged when the market was making new highs and confirming the right side of the umbrella long-term bearish pattern P/E has expanded from around 13 to about 17 during this cycle. A 17 P/E is high for a slower growing economy and earnings, and rising risks. Other valuation metrics also suggest the markets are fair to overvalued. This economic expansion and bull market are in the mature phase and are aging The Fed is starting to raise rates, and it could be disruptive to global markets and asset valuations Credit spreads are widening. Part of the reasons for rising high yield rates is related to the oil, energy bust. The reversal of the China and commodity boom and the economic problems this trend reversal is causing to the global economy and markets. Too much debt and bad allocation decisions made in China and some emerging market economies. Because of the late phase of this economic and market cycle investors should consider: Raising cash Lowering the beta of one s portfolio Lowering the P/E of one s portfolio Making sure the debt levels of the stocks, ETFs, and mutual funds are low. Being ready to scoop up bargains when we have an inevitable bear market I m currently working on my 2016 economic and market forecast. It should be ready in a few weeks.

China & Commodities - the First Major Trend Reversal of the 21st Century

China & Commodities - the First Major Trend Reversal of the 21 st Century There are major economic and investment trends that happen about every 10 years. In 2013, I wrote the reversal of a major trend,

China & Commodities - the First Major Trend Reversal of the 21 st Century There are major economic and investment trends that happen about every 10 years. In 2013, I wrote the reversal of a major trend,

Job creation continues, and the unemployment rate has dropped to 5% Earnings are expected to grow about 5% to 8% for 2016

2016 Market Outlook Many analysts and investors have low expectations for 2016 Bullish Case U.S. economy continues in expansion mode. Job creation continues, and the unemployment rate has dropped to 5%

2016 Market Outlook Many analysts and investors have low expectations for 2016 Bullish Case U.S. economy continues in expansion mode. Job creation continues, and the unemployment rate has dropped to 5%

May Market Outlook. Bullish Case. The fear of a U.S. recession has been reduced by analysts and investors.

May Market Outlook Bullish Case Earnings forecasts for 2017 are higher. The fear of a U.S. recession has been reduced by analysts and investors. Interest rates, inflation and oil prices remain low, and

May Market Outlook Bullish Case Earnings forecasts for 2017 are higher. The fear of a U.S. recession has been reduced by analysts and investors. Interest rates, inflation and oil prices remain low, and

Quarterly Chartbook. September 30, Which way is up? Copyright , All rights reserved. investwithcornerstone.com

Quarterly Chartbook September 30, 2009 Which way is up? Which way is up? Given the huge amount of Fiscal and Monetary stimulus, it is not surprising that the market has gotten up off the mat. Which way

Quarterly Chartbook September 30, 2009 Which way is up? Which way is up? Given the huge amount of Fiscal and Monetary stimulus, it is not surprising that the market has gotten up off the mat. Which way

June Market Outlook. Bullish Case. Interest rates, inflation and oil prices remain low, and are good for the economy and asset prices.

June Market Outlook Bullish Case Earnings forecasts for 2017 are higher for now. For much of the year, earnings forecasts were constantly being lowered. Now they look like they re stabilizing for now.

June Market Outlook Bullish Case Earnings forecasts for 2017 are higher for now. For much of the year, earnings forecasts were constantly being lowered. Now they look like they re stabilizing for now.

The Global Recession of 2016

INTERVIEW BARRON S The Global Recession of 2016 Forecaster David Levy sees a spreading global recession intensifying and ultimately engulfing the world s economies By LAWRENCE C. STRAUSS December 19, 2015

INTERVIEW BARRON S The Global Recession of 2016 Forecaster David Levy sees a spreading global recession intensifying and ultimately engulfing the world s economies By LAWRENCE C. STRAUSS December 19, 2015

On Our Radar September 2015

On Our Radar September 2015 The Dow Jones Industrial Average (DJIA), S&P 500 and NASDAQ Composite fell 6.56 percent, 6.25 percent, and 6.85 percent, respectively, in August, which was highlighted by a

On Our Radar September 2015 The Dow Jones Industrial Average (DJIA), S&P 500 and NASDAQ Composite fell 6.56 percent, 6.25 percent, and 6.85 percent, respectively, in August, which was highlighted by a

Since 4Q16, the Fed has just held one meeting without a rate increase skipping only Sept Their challenges are numerous.

Monetary Policy All of the central banks face major challenges. Too high, too low, avoiding inversion and in the case of the Bank of Japan, how to conduct policy at all. US Federal Reserve ECONOMIC & MARKET

Monetary Policy All of the central banks face major challenges. Too high, too low, avoiding inversion and in the case of the Bank of Japan, how to conduct policy at all. US Federal Reserve ECONOMIC & MARKET

Jeremy Siegel on Dow 15,000 By Robert Huebscher December 18, 2012

Jeremy Siegel on Dow 15,000 By Robert Huebscher December 18, 2012 Jeremy Siegel is the Russell E. Palmer Professor of Finance at the Wharton School of the University of Pennsylvania and a Senior Investment

Jeremy Siegel on Dow 15,000 By Robert Huebscher December 18, 2012 Jeremy Siegel is the Russell E. Palmer Professor of Finance at the Wharton School of the University of Pennsylvania and a Senior Investment

Gundlach s Forecast for 2016

Gundlach s Forecast for 2016 January 19, 2016 by Robert Huebscher Jeffrey Gundlach is a prescient and accurate forecaster. Last week, as he does each January, he offered his market outlook. But unlike

Gundlach s Forecast for 2016 January 19, 2016 by Robert Huebscher Jeffrey Gundlach is a prescient and accurate forecaster. Last week, as he does each January, he offered his market outlook. But unlike

Game-Changers in the Era of Dissonance

Game-Changers in the Era of Dissonance The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation

Game-Changers in the Era of Dissonance The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation

PINECONE MACRO RESEARCH SPECIAL REPORT JANUARY Could Oil End the Global Super Cycle?

Could Oil End the Global Super Cycle? Super cycles are made up of multiple business cycles or short term debt cycles the kind we as investors have to deal with once or twice per decade. Super cycles, or

Could Oil End the Global Super Cycle? Super cycles are made up of multiple business cycles or short term debt cycles the kind we as investors have to deal with once or twice per decade. Super cycles, or

Ira Epstein s Gold Report

Ira Epstein s Gold Report 3-12-2015 Will the Federal Reserve leave in or take out the word patient at this Wednesday s FOMC Meeting? 10-Year Notes are a proxy for Gold Prices Currency War in full swing

Ira Epstein s Gold Report 3-12-2015 Will the Federal Reserve leave in or take out the word patient at this Wednesday s FOMC Meeting? 10-Year Notes are a proxy for Gold Prices Currency War in full swing

March 16, Dear Investors:

March 16, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: At Crescat we remain positioned to capitalize on a downturn in the economic

March 16, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: At Crescat we remain positioned to capitalize on a downturn in the economic

The Economy: Growth Has Been Weak But Long-Lasting

The Economy: Growth Has Been Weak But Long-Lasting October 19, 2016 by Gary Halbert of Halbert Wealth Management 1. Why This Economic Recovery Has Been So Disappointing 2. The Fourth Longest Economic Expansion

The Economy: Growth Has Been Weak But Long-Lasting October 19, 2016 by Gary Halbert of Halbert Wealth Management 1. Why This Economic Recovery Has Been So Disappointing 2. The Fourth Longest Economic Expansion

A Guide to 2016 s Market Volatility. CONGRESS WEALTH MANAGEMENT, LLC 250 Northern Ave, Suite 310, Boston, MA

CONGRESS WEALTH MANAGEMENT, LLC 250 Northern Ave, Suite 310, Boston, MA 02210 www.congresswealth.com Contents What will it take to calm the markets? Will the correction in U.S. stocks turn into a bear

CONGRESS WEALTH MANAGEMENT, LLC 250 Northern Ave, Suite 310, Boston, MA 02210 www.congresswealth.com Contents What will it take to calm the markets? Will the correction in U.S. stocks turn into a bear

Gundlach s Forecast for 2017

Gundlach s Forecast for 2017 January 11, 2017 by Robert Huebscher Investors will confront excessive debt, high P/E levels and political uncertainty as they enter the Trump presidential era. In response,

Gundlach s Forecast for 2017 January 11, 2017 by Robert Huebscher Investors will confront excessive debt, high P/E levels and political uncertainty as they enter the Trump presidential era. In response,

April Economic Outlook GDP Employment

April Economic Outlook This month I will focus on this economic cycle, U.S. interest rates here, and the global trend of negative interest rates. First let s review some of the primary U.S. economic indicators.

April Economic Outlook This month I will focus on this economic cycle, U.S. interest rates here, and the global trend of negative interest rates. First let s review some of the primary U.S. economic indicators.

HOPE FOR ROTATION. So, let me talk a little about each of these. Tariffs. Tariffs are restrictions to trade; they are a tax and they cause inflation.

HOPE FOR ROTATION We ve said repeatedly that we believe the current bull market will continue until there is either a recession or a restrictive monetary policy. So far, that position has been accurate

HOPE FOR ROTATION We ve said repeatedly that we believe the current bull market will continue until there is either a recession or a restrictive monetary policy. So far, that position has been accurate

To fully understand the dramatic turns in the financial markets that

01_chap_murphy.qxd 10/24/03 2:06 PM Page 1 CHAPTER 1 A Review of the 1980s To fully understand the dramatic turns in the financial markets that started in 1980, it s necessary to know something about the

01_chap_murphy.qxd 10/24/03 2:06 PM Page 1 CHAPTER 1 A Review of the 1980s To fully understand the dramatic turns in the financial markets that started in 1980, it s necessary to know something about the

Global economy in charts

Global economy in charts Ian Stewart, Debapratim De, Tom Simmons & Peter Ireson Economics & Markets Research, Deloitte, London Summary 1. Global activity easing 2. Slowdown most apparent in euro area 3.

Global economy in charts Ian Stewart, Debapratim De, Tom Simmons & Peter Ireson Economics & Markets Research, Deloitte, London Summary 1. Global activity easing 2. Slowdown most apparent in euro area 3.

Gary Shilling - Why You Should Own Bonds

Gary Shilling - Why You Should Own Bonds February 17, 2015 by Robert Huebscher If you followed Gary Shilling s advice for the last 30 years, you would be very wealthy. Shilling runs the New Jersey-based

Gary Shilling - Why You Should Own Bonds February 17, 2015 by Robert Huebscher If you followed Gary Shilling s advice for the last 30 years, you would be very wealthy. Shilling runs the New Jersey-based

The U.S. Economy After the Great Recession: America s Deleveraging and Recovery Experience

The U.S. Economy After the Great Recession: America s Deleveraging and Recovery Experience Sherle R. Schwenninger and Samuel Sherraden Economic Growth Program March 2014 Introduction The bursting of the

The U.S. Economy After the Great Recession: America s Deleveraging and Recovery Experience Sherle R. Schwenninger and Samuel Sherraden Economic Growth Program March 2014 Introduction The bursting of the

Lesson 3 - Measuring Economic Performance

Lesson 3 - Measuring Economic Performance Economic Activity: All of the actions that involve the production, distribution, and consumption of goods and services within a society. Economic Fluctuations:

Lesson 3 - Measuring Economic Performance Economic Activity: All of the actions that involve the production, distribution, and consumption of goods and services within a society. Economic Fluctuations:

THE SPECIALIST IN TRADING AND INVESTMENT

WCU: US jobs shocker kicks gold back to life By Ole Hansen Commodities continue to recover with the Bloomberg Commodity Index reaching a seven-month high. During this process the index, which reflects

WCU: US jobs shocker kicks gold back to life By Ole Hansen Commodities continue to recover with the Bloomberg Commodity Index reaching a seven-month high. During this process the index, which reflects

th Quarter Economic Outlook

2018 4 th Quarter Economic Outlook This year economic and earnings growth, employment gains, and consumer and business confidence have all been positive, but looking forward to next year investors, analysts

2018 4 th Quarter Economic Outlook This year economic and earnings growth, employment gains, and consumer and business confidence have all been positive, but looking forward to next year investors, analysts

Data Brief. Dangerous Trends: The Growth of Debt in the U.S. Economy

cepr Center for Economic and Policy Research Data Brief Dangerous Trends: The Growth of Debt in the U.S. Economy Dean Baker 1 September 7, 2004 CENTER FOR ECONOMIC AND POLICY RESEARCH 1611 CONNECTICUT

cepr Center for Economic and Policy Research Data Brief Dangerous Trends: The Growth of Debt in the U.S. Economy Dean Baker 1 September 7, 2004 CENTER FOR ECONOMIC AND POLICY RESEARCH 1611 CONNECTICUT

Third Quarter Market Review

Third Quarter Market Review The S&P 500 continued its winning streak, with the index appreciating in value by 3.96% for the quarter (see chart below). This market barometer was up all three months of the

Third Quarter Market Review The S&P 500 continued its winning streak, with the index appreciating in value by 3.96% for the quarter (see chart below). This market barometer was up all three months of the

Accelerating Deflation and Monetary Policy

Accelerating Deflation and Monetary Policy Summary Deflation is proceeding at an accelerated pace due to the widening deflationary GDP gap. Eliminating deflation through economic stimulus by increasing

Accelerating Deflation and Monetary Policy Summary Deflation is proceeding at an accelerated pace due to the widening deflationary GDP gap. Eliminating deflation through economic stimulus by increasing

Global Macroeconomic Outlook March 2016

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Market Insight: Turn Down the News Volume, Listen to the Market

August 9, 2018 Market Insight: Turn Down the News Volume, Listen to the Market If you just listened to the news headlines, it would be hard to find reasons to like this market. Trade Wars ; Tariff Threats

August 9, 2018 Market Insight: Turn Down the News Volume, Listen to the Market If you just listened to the news headlines, it would be hard to find reasons to like this market. Trade Wars ; Tariff Threats

The Basics of Economic Growth. Real GDP per person in Canada tripled in the 50 years between 1958 and 2008.

Real GDP per person in Canada tripled in the 50 years between 1958 and 2008. What has brought about this growth in production, incomes, and living standards? We see even greater economic growth in modern

Real GDP per person in Canada tripled in the 50 years between 1958 and 2008. What has brought about this growth in production, incomes, and living standards? We see even greater economic growth in modern

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

The Nutcracker and the Bond King

The Nutcracker and the Bond King 10-year bond yields have just experienced one of the sharpest 100-day percentage drops in over 50 years Interest rates are now below their closing level of the 666 March

The Nutcracker and the Bond King 10-year bond yields have just experienced one of the sharpest 100-day percentage drops in over 50 years Interest rates are now below their closing level of the 666 March

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Gundlach: U.S. Economy and Stocks Could Be Burnt Out

Gundlach: U.S. Economy and Stocks Could Be Burnt Out September 12, 2018 by Robert Huebscher Stimulative measures drive growth, and the U.S. economy and stock market have benefited from quantitative easing,

Gundlach: U.S. Economy and Stocks Could Be Burnt Out September 12, 2018 by Robert Huebscher Stimulative measures drive growth, and the U.S. economy and stock market have benefited from quantitative easing,

... Eye on the Economy August

............................................................................................. Eye on the Economy August 2015.............................................................................................

............................................................................................. Eye on the Economy August 2015.............................................................................................

Policy Reforms after the Crisis

367 Policy Reforms after the Crisis Norman Chan The title of this session is supposed to be policy reforms after the 28 9 financial crisis. I think there s a big question about the title because I m not

367 Policy Reforms after the Crisis Norman Chan The title of this session is supposed to be policy reforms after the 28 9 financial crisis. I think there s a big question about the title because I m not

I don't understand the argument that even though inflation is not accelerating, the world nevertheless suffers from "global excess liquidity":

August 17, 2005 Global Excess Liquidity? I don't understand the argument that even though inflation is not accelerating, the world nevertheless suffers from "global excess liquidity": Economics focus A

August 17, 2005 Global Excess Liquidity? I don't understand the argument that even though inflation is not accelerating, the world nevertheless suffers from "global excess liquidity": Economics focus A

Chapter 4: A First Look at Macroeconomics

Chapter 4: A First Look at Macroeconomics Principles of Macroeconomics I. Economics as a Social Science A. Economics is the social science that studies the choices that individuals, businesses, governments,

Chapter 4: A First Look at Macroeconomics Principles of Macroeconomics I. Economics as a Social Science A. Economics is the social science that studies the choices that individuals, businesses, governments,

The Everything Bust. Causes, Consequences, and Profit Opportunities. Mike Larson Senior Analyst

The Everything Bust Causes, Consequences, and Profit Opportunities Mike Larson Senior Analyst The extremely favorable (and arguably artificial ) market environment that lasted from March 2009 through January

The Everything Bust Causes, Consequences, and Profit Opportunities Mike Larson Senior Analyst The extremely favorable (and arguably artificial ) market environment that lasted from March 2009 through January

The Grand Illusion November 4, 2016

The Grand Illusion November 4, 2016 Many know that the economy is not good. Fact is, the economic issues actually began in 2000 and have only been made worse. The world economy is in a systemic crisis

The Grand Illusion November 4, 2016 Many know that the economy is not good. Fact is, the economic issues actually began in 2000 and have only been made worse. The world economy is in a systemic crisis

The Long View Rates, GDP & Challenges

The Long View Rates, GDP & Challenges May 3, 2017 by Lance Roberts of Real Investment Advice There has been much debate about the current low levels of interest rates in the economy today. The primary

The Long View Rates, GDP & Challenges May 3, 2017 by Lance Roberts of Real Investment Advice There has been much debate about the current low levels of interest rates in the economy today. The primary

3.14. The Link between Bonds and Stocks.

3.14. The Link between Bonds and Stocks. This chapter covers the important link between the bond and stock markets. It shows how the positive link between bond yields and stocks has existed over the last

3.14. The Link between Bonds and Stocks. This chapter covers the important link between the bond and stock markets. It shows how the positive link between bond yields and stocks has existed over the last

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Hurricanes End 83-Month Employment Expansion

Hurricanes End 83-Month Employment Expansion October 6, 2017 by Urban Carmel of The Fat Pitch The bond market agrees with the macro data. The yield curve has 'inverted' (10 year yields less than 2- year

Hurricanes End 83-Month Employment Expansion October 6, 2017 by Urban Carmel of The Fat Pitch The bond market agrees with the macro data. The yield curve has 'inverted' (10 year yields less than 2- year

How Successful is China s Economic Rebalancing?*

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

The Saturday Economist UK Economic Outlook Q1 2015

The Saturday Economist The Saturday Economist UK Economic Outlook Q1 2015 Leisure and Construction driving recovery UK Economic Outlook March 2015 Page 1 The UK recovery continues. We expect growth of

The Saturday Economist The Saturday Economist UK Economic Outlook Q1 2015 Leisure and Construction driving recovery UK Economic Outlook March 2015 Page 1 The UK recovery continues. We expect growth of

Wrestling with Something Else : Why this Gold Bear Market Is Different

Wrestling with Something Else : Why this Gold Bear Market Is Different May 15, 2015 by Frank Holmes of U.S. Global Investors Earlier this week, I had the pleasure to appear on Jim Puplava s Financial Sense

Wrestling with Something Else : Why this Gold Bear Market Is Different May 15, 2015 by Frank Holmes of U.S. Global Investors Earlier this week, I had the pleasure to appear on Jim Puplava s Financial Sense

On My Radar: Recession Watch Keep an Eye on This Chart

On My Radar: Recession Watch Keep an Eye on This Chart April 27, 2015 by Steve Blumenthal of CMG Capital Management Group The most difficult thing is the decision to act, the rest is merely tenacity. -

On My Radar: Recession Watch Keep an Eye on This Chart April 27, 2015 by Steve Blumenthal of CMG Capital Management Group The most difficult thing is the decision to act, the rest is merely tenacity. -

What questions would you like answered?

What questions would you like answered? Define the following: Globalisation an expansion of world trade leading to increased international interdependence GDP The value of goods and services produced in

What questions would you like answered? Define the following: Globalisation an expansion of world trade leading to increased international interdependence GDP The value of goods and services produced in

Interest rates: How we got here and where we re going

Interest rates: How we got here and where we re going Prepared July 5, 2013 Summary Investors are understandably concerned about the state of the bond market today given that interest rates began moving

Interest rates: How we got here and where we re going Prepared July 5, 2013 Summary Investors are understandably concerned about the state of the bond market today given that interest rates began moving

INTRODUCTION TO YIELD CURVES. Amanda Goldman

INTRODUCTION TO YIELD CURVES Amanda Goldman Agenda 1. Bond Market and Interest Rate Overview 1. What is the Yield Curve? 1. Shape and Forces that Change the Yield Curve 1. Real-World Examples 1. TIPS Important

INTRODUCTION TO YIELD CURVES Amanda Goldman Agenda 1. Bond Market and Interest Rate Overview 1. What is the Yield Curve? 1. Shape and Forces that Change the Yield Curve 1. Real-World Examples 1. TIPS Important

Interest rates: How we got here and where we re going

SITUATION ANALYSIS Interest rates: How we got here and where we re going Summary Investors are understandably concerned about the state of the bond market today given that interest rates began moving sharply

SITUATION ANALYSIS Interest rates: How we got here and where we re going Summary Investors are understandably concerned about the state of the bond market today given that interest rates began moving sharply

Jake Bernstein Trading Webinar

Jake Bernstein Trading Webinar http:// 2017 Mid Year FORECAST Expectations being Confirmed What s Next? 10 and 11 June 2017 2017 by Jake Bernstein www.2chimps.net www.seasonaltrader.com www.jakestradingstrategies.com

Jake Bernstein Trading Webinar http:// 2017 Mid Year FORECAST Expectations being Confirmed What s Next? 10 and 11 June 2017 2017 by Jake Bernstein www.2chimps.net www.seasonaltrader.com www.jakestradingstrategies.com

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation. Richard C Marston Wharton School, University of Pennsylvania

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation Richard C Marston Wharton School, University of Pennsylvania Outline 1. Is there a New Normal ahead for stocks? 2. Is the

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation Richard C Marston Wharton School, University of Pennsylvania Outline 1. Is there a New Normal ahead for stocks? 2. Is the

INTRODUCTION TO YIELD CURVES. Amanda Goldman

INTRODUCTION TO YIELD CURVES Amanda Goldman Agenda 1. Bond Market and Interest Rate Overview 1. What is the Yield Curve? 1. Shape and Forces that Change the Yield Curve 1. Real-World Examples 1. TIPS Important

INTRODUCTION TO YIELD CURVES Amanda Goldman Agenda 1. Bond Market and Interest Rate Overview 1. What is the Yield Curve? 1. Shape and Forces that Change the Yield Curve 1. Real-World Examples 1. TIPS Important

Chapter 6 ECONOMIC GROWTH. World Economic Growth. In this chapter-

Chapter 6 ECONOMIC GROWTH In this chapter- Define and calculate the growth rate and explain the implications of sustained growth in economic activity Briefly describe the economic growth trends in the

Chapter 6 ECONOMIC GROWTH In this chapter- Define and calculate the growth rate and explain the implications of sustained growth in economic activity Briefly describe the economic growth trends in the

Economic & Capital Market Outlook Third Quarter, 2018

Economic & Capital Market Outlook Third Quarter, 2018 Economic Outlook The domestic economy is functioning as well as any period since 2007, however we expect economic growth to slow next year. Measured

Economic & Capital Market Outlook Third Quarter, 2018 Economic Outlook The domestic economy is functioning as well as any period since 2007, however we expect economic growth to slow next year. Measured

Market Pullback A Q&A with our Investment Team

Market Pullback A Q&A with our Investment Team The Morningstar Investment Management group August 2015 Last week, stock markets fell globally in the toughest week of 2015 to date. Investors weighed concerns

Market Pullback A Q&A with our Investment Team The Morningstar Investment Management group August 2015 Last week, stock markets fell globally in the toughest week of 2015 to date. Investors weighed concerns

Weekly Economic Commentary

LPL FINANCIAL RESEARCH Weekly Economic Commentary May 28, 2013 Gauging Global Growth in 2013: An Update John Canally, CFA Economist LPL Financial Highlights Our long-held forecast for real GDP growth for

LPL FINANCIAL RESEARCH Weekly Economic Commentary May 28, 2013 Gauging Global Growth in 2013: An Update John Canally, CFA Economist LPL Financial Highlights Our long-held forecast for real GDP growth for

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001 By Dean Baker December 20, 2001 Now that it is officially acknowledged that a recession has begun, most economists are predicting that it will soon be

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001 By Dean Baker December 20, 2001 Now that it is officially acknowledged that a recession has begun, most economists are predicting that it will soon be

Edward D. Goard, CFA Chief Investment Officer, Fixed Income

Edward D. Goard, CFA Chief Investment Officer, Fixed Income What s Different This Time? Last recession not supply side driven, inventory correction Demand side recession caused by deleveraging: Consumers

Edward D. Goard, CFA Chief Investment Officer, Fixed Income What s Different This Time? Last recession not supply side driven, inventory correction Demand side recession caused by deleveraging: Consumers

Elstree. Welcome to planet Japan.

Elstree Welcome to planet Japan. 1 Japan is another planet for gaijin credit analysts: defaults are about half the rest of the world and credit margins are much lower than global equivalents. We ve always

Elstree Welcome to planet Japan. 1 Japan is another planet for gaijin credit analysts: defaults are about half the rest of the world and credit margins are much lower than global equivalents. We ve always

A PIVOTAL OCTOBER. Issue #14. October 2018

A PIVOTAL OCTOBER Issue #14 October 2018 Stock markets tend to post their best returns from October to April but October itself can be the most volatile month of the year. The tug of war between good news

A PIVOTAL OCTOBER Issue #14 October 2018 Stock markets tend to post their best returns from October to April but October itself can be the most volatile month of the year. The tug of war between good news

Fourth Quarter Market Outlook. Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

Introduction. ECON204 Notes. Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

Has US Debt Reached A Tipping Point?

Has US Debt Reached A Tipping Point? October 28, 2016 by Urban Carmel of The Fat Pitch Summary: Investors have become very concerned about excessive debt in the US. The worry is that current leverage has

Has US Debt Reached A Tipping Point? October 28, 2016 by Urban Carmel of The Fat Pitch Summary: Investors have become very concerned about excessive debt in the US. The worry is that current leverage has

DK EQUITY GROWTH FUND. Quarterly Report September 30, Rates of Return

DK EQUITY GROWTH FUND Quarterly Report September 30, 2001 Rates of Return 3 Mths YTD 1 Yr 2 Yrs 3 Yrs 4 Yrs 5 Yrs 6Yrs 7 Yrs 8 Yrs DK Equity Growth Fund -16.8% 5.3% 1.9% 0.4% 9.4% -8.7% -2.7% 5.4% 8.6%

DK EQUITY GROWTH FUND Quarterly Report September 30, 2001 Rates of Return 3 Mths YTD 1 Yr 2 Yrs 3 Yrs 4 Yrs 5 Yrs 6Yrs 7 Yrs 8 Yrs DK Equity Growth Fund -16.8% 5.3% 1.9% 0.4% 9.4% -8.7% -2.7% 5.4% 8.6%

General Economic Outlook Recession! Will it be Short and Shallow?

General Economic Outlook Recession! Will it be Short and Shallow? Larry DeBoer January 2002 We re in a recession. The National Bureau of Economic Research (NBER), the quasiofficial arbiter of business

General Economic Outlook Recession! Will it be Short and Shallow? Larry DeBoer January 2002 We re in a recession. The National Bureau of Economic Research (NBER), the quasiofficial arbiter of business

Market Insight: A Sea Change is Underway

February 26, 2016 Market Insight: A Sea Change is Underway The price action of the financial markets since the start of the year has been nothing short of chaotic, and many would classify it as the beginning

February 26, 2016 Market Insight: A Sea Change is Underway The price action of the financial markets since the start of the year has been nothing short of chaotic, and many would classify it as the beginning

2015 Oil Outlook. january 21, 2015

Epoch Investment Partners, Inc. january 21, 2015 2015 Oil Outlook john p. reddan, cfa, managing director & senior research analyst After trading in a range from $90-$110 per barrel from late 2010 through

Epoch Investment Partners, Inc. january 21, 2015 2015 Oil Outlook john p. reddan, cfa, managing director & senior research analyst After trading in a range from $90-$110 per barrel from late 2010 through

Prospects for the National and Local Economies: A Monetary Policymaker s View. I. Good afternoon. I m very pleased to be here with you today.

Presentation to Chapman University Annual Economic Forum Hyatt Regency, Huntington Beach, CA By Robert T. Parry, President and CEO of the Federal Reserve Bank of San Francisco For delivery May 29, 2003,

Presentation to Chapman University Annual Economic Forum Hyatt Regency, Huntington Beach, CA By Robert T. Parry, President and CEO of the Federal Reserve Bank of San Francisco For delivery May 29, 2003,

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO. Summary Outlook

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO Summary Outlook January 15, 2019 Markets in 2019 will be choppy with volatility more like this past year than the placid trading of 2017. The Fed is

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO Summary Outlook January 15, 2019 Markets in 2019 will be choppy with volatility more like this past year than the placid trading of 2017. The Fed is

The Dow Theory in Technical Analysis

The Dow Theory in Technical Analysis INTRODUCTION Today Foreign Exchange Market is one of the popular segments of the global financial market. FOREX is the largest and the most liquid financial market

The Dow Theory in Technical Analysis INTRODUCTION Today Foreign Exchange Market is one of the popular segments of the global financial market. FOREX is the largest and the most liquid financial market

As of July 10, Quarter in Review

As of July 10, 2015 Quarter in Review The following are the total returns for many of the major asset classes in the second quarter of 2015 (note that as a client you do not have exposure to all of these

As of July 10, 2015 Quarter in Review The following are the total returns for many of the major asset classes in the second quarter of 2015 (note that as a client you do not have exposure to all of these

GAUGING GLOBAL GROWTH: AN UPDATE FOR 2015 & 2016 John J. Canally, Jr., CFA Chief Economic Strategist, LPL Financial

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY October 1 15 GAUGING GLOBAL GROWTH: AN UPDATE FOR 15 & 16 John J. Canally, Jr., CFA Chief Economic Strategist, LPL Financial KEY TAKEAWAYS As companies report third

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY October 1 15 GAUGING GLOBAL GROWTH: AN UPDATE FOR 15 & 16 John J. Canally, Jr., CFA Chief Economic Strategist, LPL Financial KEY TAKEAWAYS As companies report third

The Hottest M&A Market Ever:

The Hottest M&A Market Ever: What You Should Do About It Keynote at the World Angel Investment Summit September 27, 2018 Toronto, Canada Basil Peters Early Exits 10 Years On Ten years ago when I wrote

The Hottest M&A Market Ever: What You Should Do About It Keynote at the World Angel Investment Summit September 27, 2018 Toronto, Canada Basil Peters Early Exits 10 Years On Ten years ago when I wrote

THE FED AND ECONOMY. Fixed Income Commentary

Fixed Income Commentary Portfolio Strategies & Analytics Group June 15, 2009 Tom Wammack Institutional Fixed Income Director Portfolio Strategies & Analytics Group (615) 341-6020 twammack@rwbaird.com In

Fixed Income Commentary Portfolio Strategies & Analytics Group June 15, 2009 Tom Wammack Institutional Fixed Income Director Portfolio Strategies & Analytics Group (615) 341-6020 twammack@rwbaird.com In

Global Markets. CHINA AND GLOBAL MARKET VOLATILITY.

PRICE POINT August 015 Timely intelligence and analysis for our clients. Global Markets. CHINA AND GLOBAL MARKET VOLATILITY. EXECUTIVE SUMMARY Eric Moffett Portfolio Manager, Asia Opportunities Strategy

PRICE POINT August 015 Timely intelligence and analysis for our clients. Global Markets. CHINA AND GLOBAL MARKET VOLATILITY. EXECUTIVE SUMMARY Eric Moffett Portfolio Manager, Asia Opportunities Strategy

Better Sales And Profit Growth Are Behind Good 1Q17 Results, Not Financial Engineering

Better Sales And Profit Growth Are Behind Good 1Q17 Results, Not Financial Engineering May 5, 2017 by Urban Carmel of The Fat Pitch Summary: S&P profits are up 22% yoy. Sales are 7.2% higher. By some measures,

Better Sales And Profit Growth Are Behind Good 1Q17 Results, Not Financial Engineering May 5, 2017 by Urban Carmel of The Fat Pitch Summary: S&P profits are up 22% yoy. Sales are 7.2% higher. By some measures,

It s Not As It Appears!

It s Not As It Appears! As equities continued to rise during the advance into the 2007 top, I screamed from the roof tops that it was a bear market advance and that the efforts to prop the markets up only

It s Not As It Appears! As equities continued to rise during the advance into the 2007 top, I screamed from the roof tops that it was a bear market advance and that the efforts to prop the markets up only

Global Financial Crisis and China s Countermeasures

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Outlook & Perspective

Outlook & Perspective All data and information as of June 30, 2016 Approved for current clients. May be presented to prospective clients in a one-on-one setting only. Morningstar Investment Services LLC

Outlook & Perspective All data and information as of June 30, 2016 Approved for current clients. May be presented to prospective clients in a one-on-one setting only. Morningstar Investment Services LLC

CURRENCY CURRENTS A free global-macro & market newsletter

CURRENCY CURRENTS A free global-macro & market newsletter 2 July 2013 Quotable For a generation, when forced to choose between Middle America and corporate America, on NAFTA, most-favored nation for China,

CURRENCY CURRENTS A free global-macro & market newsletter 2 July 2013 Quotable For a generation, when forced to choose between Middle America and corporate America, on NAFTA, most-favored nation for China,

On the Long Bond and Why the Widow Maker is Alive and Well

On the Long Bond and Why the Widow Maker is Alive and Well February 27, 2015 by Team of Knowledge Leaders Capital Perhaps one of the most important questions investors need to answer today is whether we've

On the Long Bond and Why the Widow Maker is Alive and Well February 27, 2015 by Team of Knowledge Leaders Capital Perhaps one of the most important questions investors need to answer today is whether we've

What s the Yield Curve? A Powerful Signal of Recessions Has Wall Street s Attention

BUSINESS DAY What s the Yield Curve? A Powerful Signal of Recessions Has Wall Street s Attention By Matt Phillips June 25, 2018 You can try to play down a trade war with China. You can brush off the impact

BUSINESS DAY What s the Yield Curve? A Powerful Signal of Recessions Has Wall Street s Attention By Matt Phillips June 25, 2018 You can try to play down a trade war with China. You can brush off the impact

PCA INVESTMENT MARKET RISK METRICS. Monthly Report

PCA INVESTMENT MARKET RISK METRICS Monthly Report June 2017 Takeaways Equity volatility measure (VIX) ended the month at extremely low levels, lowest since the global financial crisis, after a brief inter-month

PCA INVESTMENT MARKET RISK METRICS Monthly Report June 2017 Takeaways Equity volatility measure (VIX) ended the month at extremely low levels, lowest since the global financial crisis, after a brief inter-month

The Great Depression & New Deal ( ) Part 1: Basic Economics + Causes of GD

Part 1: Basic Economics + Causes of GD") The Great Depression & New Deal (1929-1941) Part 1: Basic Economics + Causes of GD Introduction The nation, like all capitalist nations, had suffered economic downturns many times, including longterm depressions

The Great Depression & New Deal (1929-1941) Part 1: Basic Economics + Causes of GD Introduction The nation, like all capitalist nations, had suffered economic downturns many times, including longterm depressions

Code Red How to Protect Your Savings from the Coming Crisis. By John Mauldin & Jonathan Tepper

Code Red How to Protect Your Savings from the Coming Crisis Chapter 1 The Great Experiment Before the Great Recession, central bankers used conventional monetary policy. Now they experiment with non-conventional

Code Red How to Protect Your Savings from the Coming Crisis Chapter 1 The Great Experiment Before the Great Recession, central bankers used conventional monetary policy. Now they experiment with non-conventional

Market Outlook Considerations Week Beginning November 13, 2017

Market Outlook Considerations Week Beginning November 13, 2017 DISCLAIMER-FOR-EDUCATIONAL-PURPOSES-ONLY Bobby Coats, Ph.D. Professor Economics Department of Agricultural Economics and Agribusiness University

Market Outlook Considerations Week Beginning November 13, 2017 DISCLAIMER-FOR-EDUCATIONAL-PURPOSES-ONLY Bobby Coats, Ph.D. Professor Economics Department of Agricultural Economics and Agribusiness University

China s macroeconomic imbalances: causes and consequences. John Knight and Wang Wei

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

The $VIX, the Dow, and China. 3/15/2008

The $VIX, the Dow, and China. 3/15/2008 In the past few days, I have received some questions from a few members. These questions cannot be answered in a few words, and because other members may be interested,

The $VIX, the Dow, and China. 3/15/2008 In the past few days, I have received some questions from a few members. These questions cannot be answered in a few words, and because other members may be interested,

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017 1 2017 FORECAST OVERVIEW For the 2017 housing market, the outlook is generally positive. The long recovery from the elevated delinquency

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017 1 2017 FORECAST OVERVIEW For the 2017 housing market, the outlook is generally positive. The long recovery from the elevated delinquency

Global Overview of Containerboard ICCA/WCO May 23, 2011

Global Overview of Containerboard ICCA/WCO May 23, 2011 Dr. Lynn O. Michaelis Executive Adviser, RISI President, Strategic Economic Analysis Today s Agenda Global Economic outlook the major issues/concerns

Global Overview of Containerboard ICCA/WCO May 23, 2011 Dr. Lynn O. Michaelis Executive Adviser, RISI President, Strategic Economic Analysis Today s Agenda Global Economic outlook the major issues/concerns

Playing Ball in the Later Innings Dr. Mark G. Dotzour College Station, Texas.

Playing Ball in the Later Innings Dr. Mark G. Dotzour College Station, Texas mdotzour@gmail.com www.markdotzour.com Since 1945, there have been 11 economic cycles The average recession has been 11.1 months

Playing Ball in the Later Innings Dr. Mark G. Dotzour College Station, Texas mdotzour@gmail.com www.markdotzour.com Since 1945, there have been 11 economic cycles The average recession has been 11.1 months

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

Strengths (+) and weaknesses ( )

and weaknesses ( )") Country Report Australia Country Report Marcel Weernink Economic growth in Australia decelerates due to lower mining investments. The outlook depends heavily on demand from China for its commodities and

Country Report Australia Country Report Marcel Weernink Economic growth in Australia decelerates due to lower mining investments. The outlook depends heavily on demand from China for its commodities and

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key