... Eye on the Economy August

|

|

|

- Katrina Cameron

- 5 years ago

- Views:

Transcription

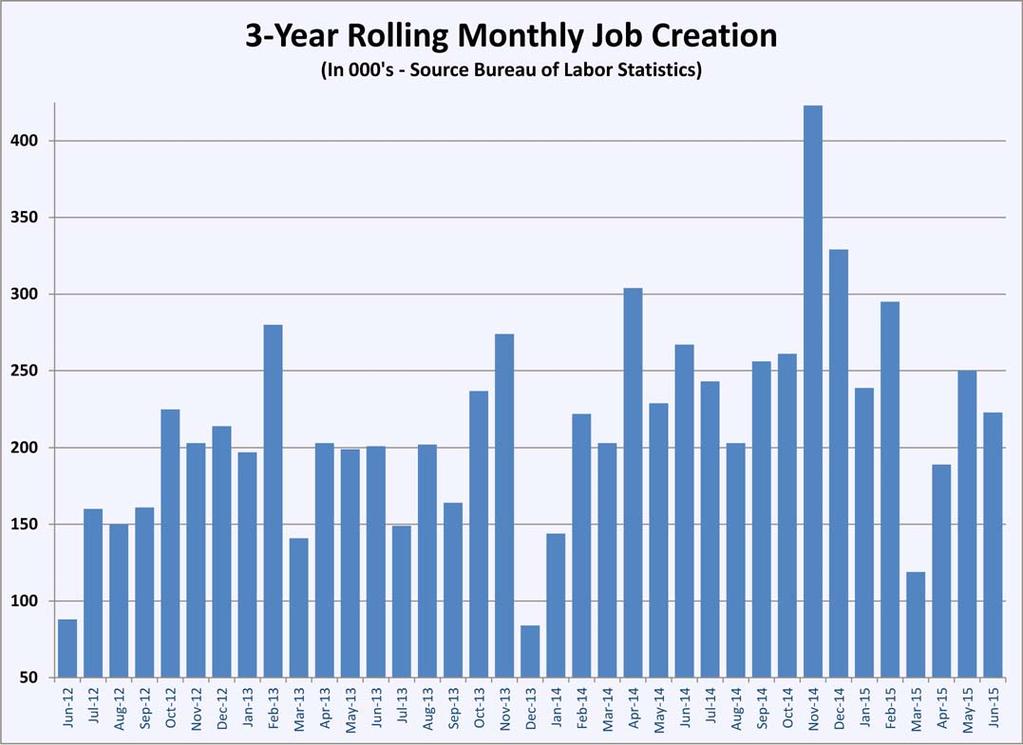

1 Eye on the Economy August At mid-year 2015, the underlying economic support for the commercial property sector is as strong as it has been since the peak of the last economic cycle in Unlike that peak, there is little of the frothiness of the housing bubble boom and room for even more upside in this business cycle. Looking forward into 2016, what clouds loom for commercial real estate are in the potential for tighter fiscal policy to disrupt the good times. The principle source of optimism and strong real estate performance has been the labor market. Employment grew by some 3.1 million jobs in 2014, reaching a new historical high for the number employed in the U.S. Coupled with construction volumes that are still some 30 percent below the pre-recession peak, the demand for office and industrial space outstripped supply by a considerable amount. That created good news for occupancy and rental rates. The July 2 jobs report showed that 1.3 million jobs had been created during the first six months of 2015, dropping unemployment to 5.3 percent. The decline in unemployment was attributed to a further decline in the workforce rather than the rise in employment. While the trend of lower workforce participation is troubling the 62.6 percent labor participation rate was the lowest since October 1977 the decline thus far in 2015 has been primarily from people who were fully employed leaving the workforce, rather than unemployed workers giving up. The job gains occur as consumers grow more confident about the outlook for the economy and their own finances. Consumer spending rose 2.9 percent in the second quarter following an increase of 1.8 percent from January through March., reflecting pent-up response to lower gas prices since mid-late Consumer confidence showed strength in how people viewed the current situation with less confidence about the future. The Conference Board said June 30 that its consumer confidence index rose to in June, up from a May reading of 94.6, but declined again in July to The survey of current conditions found consumers registering an index of Consumers are in a better position to contribute to the economy that at any time since the housing bubble in the mid-2000s. Today, however, the consumer balance sheet is much improved. Debt-to-income ratios are lower than have existed for 30 years or more. Home values are improving at a higher pace, beginning to recover the ground lost after the mortgage crisis. Home inventories are low with little more than a five-month supply available and new construction has only topped the million-unit mark within the past year. There are fewer obstacles to healthy consumer spending, a driver of 70 percent of the economy.

2 The economy in Western Pennsylvania picked up steam in May and June as more people entered the labor market and employers added 15,700 and 6,700 jobs respectively. The year-over-year increase through six months has been 23,500 nonfarm jobs. The seasonally adjusted unemployment rate is generated from a separate survey of households, which showed the labor force grew by 6,400 people to 1.22 million people. There are a lot of positive things going on that are more solid than we re used to seeing in the past 15 years, notes Jack Shelley, senior vice president for real estate lending and services for Dollar Bank. When things heat up, developers tend to fall in love with every opportunity and that s how things get overbuilt. Right now that s not happening, even though we re seeing more development than in many years. We re starting to catch up with ourselves with pent-up demand. The improvements to the consumer side of the economy offset softness in business investment and government spending to drive a 2.3 percent increase in gross domestic product (GDP) during the second quarter. Growth was muted by a slight decline in equipment expenditures and a 68.2 percent decline in mining and drilling by oil and gas companies. The measure of private domestic demand which strips out trade, inventories and government spending rose 2.5 percent. The rise in GDP was somewhat below economists expectations, but that was in part due to revisions that the Bureau of Economic Analysis (BEA) made to the first quarter GDP which now shows a 0.6 percent increase and its methodology. A trend that the BEA is investigating and is expected to provide explanation and guidance about later this year is the disparity in growth between the first quarter and subsequent quarters. Real GDP growth typically declines ten percent in the first quarter of the year, without seasonal adjustments, and the second quarter then rebounds by roughly 20 percent. Since 2000, however, the seasonally-adjusted growth rates have been much lower during the first quarters and have fallen precipitously after Because most analysts forecasted a solid first quarter 2015 based on other economic data, the decline seemed to really spark questions this year. The methodology for seasonal adjustments relies on adjustments to the individual categories within GDP that are then aggregated to reach a total. This top line GDP may be affected by seasonal interactions between the components themselves that get skewed once aggregated, offers Kurt Rankin, vice president and economist for the PNC Financial Services Group. Rankin is quick to point out that this is his best guess of the reason, but notes that seasonal adjustments are arbitrary and seem to need some revisions to make the adjusted comparisons valid. This may seem like a lot of economic nit-picking but when you consider the key role that consumer and business confidence played in prolonging the recovery after 2011 and the role that GDP growth is playing in the Federal Reserve Bank s decisionmaking on interest rates, getting the rate of real growth right isn t a trivial matter. In fact the Federal Reserve Bank of San Francisco (FRBSF) studied this residual seasonality and in its May 18 Economic Letter concluded that the BEA is not adjusting out calendar impacts. After doing its own round of adjustments, the FRBSF estimates that GDP grew at a much faster rate from January through March.

3 Regardless of whether or not there is as dramatic a rebound in the second and third quarters of 2015 as in 2014, there are few domestic head winds to slow the U.S. economy. June and July brought reminders that some of the world s largest economies aren t on as firm a footing as the American economy, but thus far the ripples from the Greek debt default and the slowdown in China have barely been felt in the U.S. As had been predicted, the small size of the Greek economy and the certainty of the ultimate outcome of negotiations to restructure its debt rendered that crisis insignificant to the U.S. Few options existed for Greece except to agree to austerity measures and social changes that the European Union and mainly Germany made as provisions for extending a lifeline. While there was media discussion of Greece s problems imploding the EU, there was little likelihood of that happening. U.S. investors and businesses behaved as though there was little chance of a Greek default triggering a global financial event, and indeed, when a deal was struck the reaction to the agreement was muted. Of more potential danger is a recession in China. Concerns over a real estate bubble persist and the level of consumption and investment by Chinese companies has declined compared to the decade-long trend; however, Chinese GDP growth remained at seven percent in the second quarter, slightly higher than the 6.9 percent that was forecasted. Chinese stock exchanges have gotten headlines for the recent volatility but the Shanghai Index has risen more than 20 percent since January 1 and Hong Kong s Hang Seng Index is up roughly six percent. Investors in Chinese stocks seem to have an increasing level of anxiety over the role the Chinese government will play in supporting the markets. China has purchased blue-chip stocks through a portfolio called the China Securities Financial Corp. and has dialed back inflows into the market, either to test whether stocks can be supported without intervention or because its own liquidity is constrained. Few observers believe it is the latter and government response to significant weekly or daily selloffs seems to reinforce that opinion. These two highlights of the global economy reflect the environment in which American companies must do business. Weaker demand and weak economies in Europe coupled with the fear that the Eurozone may yet dissolve continue to create pressure to maintain loose monetary policy. Likewise, a softer Chinese economy will be an incentive for the central bank there to stimulate growth. Either of these scenarios, let alone the relative strength of U.S. businesses, makes investing in U.S. assets more inviting. For at least the balance of 2015, U.S commercial real estate assets will be among the favorite of those foreign investments. It is the favored position of U.S. real estate that might give some observers pause, as the market conditions begin to more closely resemble those in Certainly there are similarities to that period from the perspective of capital chasing assets but there are a number of metrics that indicate a difference in markets. For one, there is virtually no asset class that has been overbuilt in the way the housing market was in There is an argument to make for a bubble in apartment construction but the number of new apartments in the pipeline is not near

4 some of the historical highs of previous cycles and both occupancy levels and rents continue to climb for apartments. For the remaining commercial real estate products, regulatory constraints have kept pressure on appraisals and loan-to-value ratios that have restrained property valuations. It s difficult to make a case that any commercial asset class is artificially inflated, except to the degree that the low interest rates are factored in. Interest rates would seem to be the main risk factor looming for the real estate market. In her most recent remarks to Congress, Federal Reserve Bank Chair Janet Yellen signaled that the Fed was finally ready to raise rates. Neither the stock markets nor the Treasury debt market mustered much of a response to Yellen s remarks, creating the impression that the first increase or two is already priced into the markets. At this point, there seems to be confidence that the Fed will manage any tightening skillfully and that the increases that occur over the next 12 to 18 months will be small. For an industry that depends upon job growth, consumer confidence, economic stability and appetite for yield as its recipe for success, commercial real estate is in a very strong environment for the next 18 to 30 months. The primary risk appears to be higher interest rates, a risk that seems remote and limited in its impact. Seasonally-adjusted GDP growth rates for the first quarter have declined steadily over the past four decades. Source: Federal Reserve Bank of San Francisco.

5

Quarterly Economics Briefing

Quarterly Economics Briefing March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook

Quarterly Economics Briefing March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook

Third Quarter 2015 An independent economic analysis of Arkansas three largest metro areas: Central Arkansas Northwest Arkansas The Fort Smith region

Third Quarter 2015 An independent economic analysis of Arkansas three largest metro areas: Central Arkansas Northwest Arkansas The Fort Smith region About The Compass The Compass Report is managed by Talk

Third Quarter 2015 An independent economic analysis of Arkansas three largest metro areas: Central Arkansas Northwest Arkansas The Fort Smith region About The Compass The Compass Report is managed by Talk

Gauging Current Conditions:

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation Vol. 2 2005 The gauges below indicate the economic outlook for the current year and for 2006 for factors that typically

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation Vol. 2 2005 The gauges below indicate the economic outlook for the current year and for 2006 for factors that typically

Baseline U.S. Economic Outlook, Summary Table*

July 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Economy Continues to Expand in Mid-218, But Trade Remains

July 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Economy Continues to Expand in Mid-218, But Trade Remains

2012 Economic Outlook: Overview of U.S. Economy. Presented by: Mark Evans, CFA Director of Investment Strategies

2012 Economic Outlook: Overview of U.S. Economy Presented by: Mark Evans, CFA Director of Investment Strategies mevans@viningsparks.com A Recovery of Sorts Rates have fallen even further Economy is getting

2012 Economic Outlook: Overview of U.S. Economy Presented by: Mark Evans, CFA Director of Investment Strategies mevans@viningsparks.com A Recovery of Sorts Rates have fallen even further Economy is getting

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist

August 18 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Excellent Second Quarter Growth as Labor Market Continues

August 18 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Excellent Second Quarter Growth as Labor Market Continues

The Labor Force Participation Puzzle

The Labor Force Participation Puzzle May 23, 2013 by David Kelly of J.P. Morgan Funds Slow growth and mediocre job creation have been common themes used to describe the U.S. economy in recent years, as

The Labor Force Participation Puzzle May 23, 2013 by David Kelly of J.P. Morgan Funds Slow growth and mediocre job creation have been common themes used to describe the U.S. economy in recent years, as

OUTLOOK THE CHANGING STRUCTURE OF THE WA ECONOMY ABOUT OUTLOOK

OUTLOOK July 2017 I Chamber of Commerce and Industry of Western Australia (Inc) THE CHANGING STRUCTURE OF THE WA ECONOMY ABOUT OUTLOOK Outlook is CCIWA s biannual analysis of the Western Australian economy.

OUTLOOK July 2017 I Chamber of Commerce and Industry of Western Australia (Inc) THE CHANGING STRUCTURE OF THE WA ECONOMY ABOUT OUTLOOK Outlook is CCIWA s biannual analysis of the Western Australian economy.

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist.

January 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Another Fed Rate Hike in December, Inflation Remains

January 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Another Fed Rate Hike in December, Inflation Remains

Global Markets. CHINA AND GLOBAL MARKET VOLATILITY.

PRICE POINT August 015 Timely intelligence and analysis for our clients. Global Markets. CHINA AND GLOBAL MARKET VOLATILITY. EXECUTIVE SUMMARY Eric Moffett Portfolio Manager, Asia Opportunities Strategy

PRICE POINT August 015 Timely intelligence and analysis for our clients. Global Markets. CHINA AND GLOBAL MARKET VOLATILITY. EXECUTIVE SUMMARY Eric Moffett Portfolio Manager, Asia Opportunities Strategy

Observation. January 18, credit availability, credit

January 18, 11 HIGHLIGHTS Underlying the improvement in economic indicators over the last several months has been growing signs that the economy is also seeing a recovery in credit conditions. The mortgage

January 18, 11 HIGHLIGHTS Underlying the improvement in economic indicators over the last several months has been growing signs that the economy is also seeing a recovery in credit conditions. The mortgage

The UK economic and fiscal outlook

The UK economic and fiscal outlook Report for StepChange Debt Charity Centre for Economics and Business Research ltd Contents Executive summary 3 Global economic outlook 4 UK economic outlook 8 UK regional

The UK economic and fiscal outlook Report for StepChange Debt Charity Centre for Economics and Business Research ltd Contents Executive summary 3 Global economic outlook 4 UK economic outlook 8 UK regional

What's really happening to house prices. November How big is the fall (so far)?

?") November 2017 David Norman Chief Economist david.norman@aucklandcouncil.govt.nz 021 516 103 What's really happening to house prices Once we account for these seasonal effects, prices have fallen around

November 2017 David Norman Chief Economist david.norman@aucklandcouncil.govt.nz 021 516 103 What's really happening to house prices Once we account for these seasonal effects, prices have fallen around

The Equifax Economic and Credit Markets Outlook

The Equifax Economic and Credit Markets Outlook A CUNA Roundtable Amy Crews Cutts SVP- Chief Economist, Equifax May 15, 2014 Comments on the Economic Outlook General forecast is that economic growth accelerates

The Equifax Economic and Credit Markets Outlook A CUNA Roundtable Amy Crews Cutts SVP- Chief Economist, Equifax May 15, 2014 Comments on the Economic Outlook General forecast is that economic growth accelerates

Monetary Policy as the Economy Approaches the Fed s Dual Mandate

EMBARGOED UNTIL Wednesday, February 15, 2017 at 1:10 P.M., U.S. Eastern Time OR UPON DELIVERY Monetary Policy as the Economy Approaches the Fed s Dual Mandate Eric S. Rosengren President & Chief Executive

EMBARGOED UNTIL Wednesday, February 15, 2017 at 1:10 P.M., U.S. Eastern Time OR UPON DELIVERY Monetary Policy as the Economy Approaches the Fed s Dual Mandate Eric S. Rosengren President & Chief Executive

First Quarter 2016 Quarterly narrative REGIONAL SUMMARIES Fort Smith region Northwest Arkansas Central Arkansas Jonesboro

First Quarter 2016 Quarterly narrative An independent economic analysis of four Arkansas metro areas: Central Arkansas Northwest Arkansas The Fort Smith region Jonesboro metro REGIONAL SUMMARIES Fort Smith

First Quarter 2016 Quarterly narrative An independent economic analysis of four Arkansas metro areas: Central Arkansas Northwest Arkansas The Fort Smith region Jonesboro metro REGIONAL SUMMARIES Fort Smith

NATIONAL ECONOMIC OUTLOOK

November 2017 NATIONAL ECONOMIC OUTLOOK Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist THE PNC FINANCIAL

November 2017 NATIONAL ECONOMIC OUTLOOK Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist THE PNC FINANCIAL

HKU announces 2015 Q2 HK Macroeconomic Forecast

Press Release HKU announces 2015 Q2 HK Macroeconomic Forecast April 9, 2015 1 Overview The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong

Press Release HKU announces 2015 Q2 HK Macroeconomic Forecast April 9, 2015 1 Overview The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong

One Policymaker s Wait for Better Economic Data

EMBARGOED UNTIL June 1, 2015 at 9:00 A.M. Eastern Time OR UPON DELIVERY One Policymaker s Wait for Better Economic Data Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

EMBARGOED UNTIL June 1, 2015 at 9:00 A.M. Eastern Time OR UPON DELIVERY One Policymaker s Wait for Better Economic Data Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

The yellow highlighted areas are bear markets with NO recession.

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Q Capital Markets Review

Q1 2016 Capital Markets Review The December malaise awakened explosively to start 2016. The market correction that had been held back by managers push for returns in December let loose in January as the

Q1 2016 Capital Markets Review The December malaise awakened explosively to start 2016. The market correction that had been held back by managers push for returns in December let loose in January as the

Goal-Based Monetary Policy Report 1

Goal-Based Monetary Policy Report 1 Financial Planning Association Golden Valley, Minnesota January 16, 2015 Narayana Kocherlakota President Federal Reserve Bank of Minneapolis 1 Thanks to David Fettig,

Goal-Based Monetary Policy Report 1 Financial Planning Association Golden Valley, Minnesota January 16, 2015 Narayana Kocherlakota President Federal Reserve Bank of Minneapolis 1 Thanks to David Fettig,

Economic Outlook

2013-2014 Economic Outlook Published by: Department of Finance Province of New Brunswick P.O. Box 6000 Fredericton, New Brunswick E3B 5H1 Canada Internet: www.gnb.ca/0024/index-e.asp March 26, 2013 Cover:

2013-2014 Economic Outlook Published by: Department of Finance Province of New Brunswick P.O. Box 6000 Fredericton, New Brunswick E3B 5H1 Canada Internet: www.gnb.ca/0024/index-e.asp March 26, 2013 Cover:

2015: FINALLY, A STRONG YEAR

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated quarterly to reflect the current economic outlook for factors that typically impact

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated quarterly to reflect the current economic outlook for factors that typically impact

US Economy Update May 2014

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

US Economy Update May 2014 MACRO REPORT Key Insights Monica Defend Head of Global Asset Allocation Research Annalisa Usardi Economist, US & LATAM Global Asset Allocation Research Also contributing Riccardo

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The gauges below are updated quarterly to reflect the current economic outlook for factors that typically impact

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The gauges below are updated quarterly to reflect the current economic outlook for factors that typically impact

Economists Expect Big Jump In 2Q GDP - We'll See May 16, 2017 by Gary Halbert of Halbert Wealth Management

Economists Expect Big Jump In 2Q GDP - We'll See May 16, 2017 by Gary Halbert of Halbert Wealth Management Page 1, 2018 Advisor Perspectives, Inc. All rights reserved. IN THIS ISSUE: 1. First Trust Predicts

Economists Expect Big Jump In 2Q GDP - We'll See May 16, 2017 by Gary Halbert of Halbert Wealth Management Page 1, 2018 Advisor Perspectives, Inc. All rights reserved. IN THIS ISSUE: 1. First Trust Predicts

Joseph S Tracy: A strategy for the 2011 economic recovery

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Consolidated Investment Report

Consolidated Investment Report September 2015 As Palm Beach County s Chief Financial Officer, the Clerk & Comptroller is charged with safeguarding and investing all County funds. The Clerk s management

Consolidated Investment Report September 2015 As Palm Beach County s Chief Financial Officer, the Clerk & Comptroller is charged with safeguarding and investing all County funds. The Clerk s management

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR FURTHER DISTRIBUTION. PRICE POINT December 2015 Timely intelligence and analysis for our clients. Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR FURTHER DISTRIBUTION. PRICE POINT December 2015 Timely intelligence and analysis for our clients. Australian Equity IMPROVING OUTLOOK FOR A TRANSITIONING ECONOMY

HKU announces 2014 Q4 HK Macroeconomic Forecast

Press Release October 8, 2014 HKU announces 2014 Q4 HK Macroeconomic Forecast Hong Kong Economic Outlook The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the

Press Release October 8, 2014 HKU announces 2014 Q4 HK Macroeconomic Forecast Hong Kong Economic Outlook The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the

MISSISSIPPI S BUSINESS Monitoring the state s economy

MISSISSIPPI S BUSINESS Monitoring the state s economy A Publication of the University Research Center, Mississippi Institutions of Higher Learning MARCH 2015 VOLUME 73, NUMBER 3 ECONOMY AT A GLANCE he

MISSISSIPPI S BUSINESS Monitoring the state s economy A Publication of the University Research Center, Mississippi Institutions of Higher Learning MARCH 2015 VOLUME 73, NUMBER 3 ECONOMY AT A GLANCE he

THE 2018 ECONOMY: A BIT BETTER THAN IN 2017

THE 2018 ECONOMY: A BIT BETTER THAN IN 2017 Presented by: Elliot F. Eisenberg, Ph.D. President: GraphsandLaughs, LLC November 9, 2017 Detroit, MI The Economy is Solid! GDP = C+I+G+(X-M) The Stock Market

THE 2018 ECONOMY: A BIT BETTER THAN IN 2017 Presented by: Elliot F. Eisenberg, Ph.D. President: GraphsandLaughs, LLC November 9, 2017 Detroit, MI The Economy is Solid! GDP = C+I+G+(X-M) The Stock Market

Interest Rate Forecast

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Quarterly Economics Briefing

Quarterly Economics Briefing September March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic

Quarterly Economics Briefing September March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic

2017 FIRST QUARTER RESULTS

2017 FIRST QUARTER RESULTS Dr. Steven N. Weisbart, CLU June 28, 2017 Highlights For the property/casualty (P/C) insurance industry in the first quarter of 2017, the financial weather report (compared with

2017 FIRST QUARTER RESULTS Dr. Steven N. Weisbart, CLU June 28, 2017 Highlights For the property/casualty (P/C) insurance industry in the first quarter of 2017, the financial weather report (compared with

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Fed Delivers Another December Rate Hike

Fed Delivers Another December Rate Hike December 14, 2017 by Chris Molumphy of Franklin Templeton Investments The US Federal Reserve delivered another interest-rate hike at its December monetary policy

Fed Delivers Another December Rate Hike December 14, 2017 by Chris Molumphy of Franklin Templeton Investments The US Federal Reserve delivered another interest-rate hike at its December monetary policy

file:///c:/users/cathy/appdata/local/microsoft/windows/temporary Int...

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

2013 Economic and Financial Market Outlook

2013 Economic and Financial Market Outlook Reflections on the economic recovery to date The economic recovery that began in the third quarter of 2009 is now three and a half years old. During this period,

2013 Economic and Financial Market Outlook Reflections on the economic recovery to date The economic recovery that began in the third quarter of 2009 is now three and a half years old. During this period,

Outlook and Market Review Fourth Quarter 2013

Outlook and Market Review Fourth Quarter 2013 Economic growth remains sluggish and inflation is not on the radar screen. The Bureau of Economic Analysis revised fourth quarter GDP growth to a 2.4% rate

Outlook and Market Review Fourth Quarter 2013 Economic growth remains sluggish and inflation is not on the radar screen. The Bureau of Economic Analysis revised fourth quarter GDP growth to a 2.4% rate

Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017

ISSN 1718-836 Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017 Re: Québec Excerpts from The Quebec Economic Plan November 2017 Update, Québec Public Accounts 2016-2017

ISSN 1718-836 Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017 Re: Québec Excerpts from The Quebec Economic Plan November 2017 Update, Québec Public Accounts 2016-2017

The Economic Outlook

The Economic Outlook Pennsylvania Association of Community Bankers 137th Annual Convention Amelia Island, FL September 6, 2014 Charles I. Plosser President and CEO Federal Reserve Bank of Philadelphia

The Economic Outlook Pennsylvania Association of Community Bankers 137th Annual Convention Amelia Island, FL September 6, 2014 Charles I. Plosser President and CEO Federal Reserve Bank of Philadelphia

Monthly Economic Indicators And Charts

Monthly Economic Indicators And Charts June Richard F. Moody- Chief Economist Steve Pfitzer Investor Relations Information contained herein is based on data obtained from recognized sources believed to

Monthly Economic Indicators And Charts June Richard F. Moody- Chief Economist Steve Pfitzer Investor Relations Information contained herein is based on data obtained from recognized sources believed to

Economic Barometer. Mixed Signals. Labor Market Improvement Household Demand Household Demand Continued Business Demand

www.csb.uncw.edu/cbes Economic Barometer CAMERON SCHOOL OF BUSINESS H. DAVID AND DIANE SWAIN CENTER FOR BUSINESS AND ECONOMIC SERVICES Volume IV, Issue 2 April 2012 Inside this issue: Labor Market Improvement

www.csb.uncw.edu/cbes Economic Barometer CAMERON SCHOOL OF BUSINESS H. DAVID AND DIANE SWAIN CENTER FOR BUSINESS AND ECONOMIC SERVICES Volume IV, Issue 2 April 2012 Inside this issue: Labor Market Improvement

THE 2018 ECONOMY: BETTER THAN IN 2017

THE 2018 ECONOMY: BETTER THAN IN 2017 Presented by: Elliot F. Eisenberg, Ph.D. President: GraphsandLaughs, LLC March 5, 2018 Boise, ID The Economy is Solid! GDP = C+I+G+(X-M) The Stock Market Is Doing

THE 2018 ECONOMY: BETTER THAN IN 2017 Presented by: Elliot F. Eisenberg, Ph.D. President: GraphsandLaughs, LLC March 5, 2018 Boise, ID The Economy is Solid! GDP = C+I+G+(X-M) The Stock Market Is Doing

The Index Leading Indicators

Our Sponsors: Housing Sales Up, Wide Growth Professor Erick Eschker, Director Jonathan Ashbach, Assistant Editor Catherine Carter, Assistant Analyst While no especially dramatic records were broken in

Our Sponsors: Housing Sales Up, Wide Growth Professor Erick Eschker, Director Jonathan Ashbach, Assistant Editor Catherine Carter, Assistant Analyst While no especially dramatic records were broken in

GENERAL FUND REVENUE REPORT & ECONOMIC OUTLOOK. September 2011 Barry Boardman, Ph.D. Fiscal Research Division North Carolina General Assembly

GENERAL FUND REVENUE REPORT & ECONOMIC OUTLOOK September 2011 Barry Boardman, Ph.D. Fiscal Research Division North Carolina General Assembly 0 Overview Growth trends established earlier this year continued

GENERAL FUND REVENUE REPORT & ECONOMIC OUTLOOK September 2011 Barry Boardman, Ph.D. Fiscal Research Division North Carolina General Assembly 0 Overview Growth trends established earlier this year continued

Banks at a Glance: Economic and Banking Highlights by State 4Q 2017

Economic and Banking Highlights by State 4Q 2017 These semi-annual reports highlight key indicators of economic and banking conditions within each of the nine states comprising the 12th Federal Reserve

Economic and Banking Highlights by State 4Q 2017 These semi-annual reports highlight key indicators of economic and banking conditions within each of the nine states comprising the 12th Federal Reserve

Economic Review - Third Quarter 2015

Economic Review - Third Quarter 2015 The state of the general economy can help or hinder a business prospects and therefore has a direct impact on the value of a business. The economic recovery following

Economic Review - Third Quarter 2015 The state of the general economy can help or hinder a business prospects and therefore has a direct impact on the value of a business. The economic recovery following

Market Month: April 2017

Market Month: April 2017 The Markets (as of market close April 28, 2017) Equities continued their positive trend in April, spurred by favorable corporate earnings reports, proposed federal tax cuts, and

Market Month: April 2017 The Markets (as of market close April 28, 2017) Equities continued their positive trend in April, spurred by favorable corporate earnings reports, proposed federal tax cuts, and

HKU announces 2015 Q3 HK Macroeconomic Forecast

Press Release HKU announces 2015 Q3 HK Macroeconomic Forecast July 7, 2015 1 Overview The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong

Press Release HKU announces 2015 Q3 HK Macroeconomic Forecast July 7, 2015 1 Overview The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong

2012 6 http://www.bochk.com 2 3 4 ECONOMIC REVIEW(A Monthly Issue) June, 2012 Economics & Strategic Planning Department http://www.bochk.com An Analysis on the Plunge in Hong Kong s GDP Growth and Prospects

2012 6 http://www.bochk.com 2 3 4 ECONOMIC REVIEW(A Monthly Issue) June, 2012 Economics & Strategic Planning Department http://www.bochk.com An Analysis on the Plunge in Hong Kong s GDP Growth and Prospects

The real change in private inventories added 0.15 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy rebounded in the second quarter of 2007, growing at an annual rate of 3.4% Q/Q (+1.8% Y/Y), according to the GDP advance estimates

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy rebounded in the second quarter of 2007, growing at an annual rate of 3.4% Q/Q (+1.8% Y/Y), according to the GDP advance estimates

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

July 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Job Growth Picked Back Up Again

growth but still remains at approximately 1.5% of potential GDP.

THE UK ECONOMY IN FOCUS/APPLICATIONS Reminder of key objectives: Low and positive inflation (inflation rate target of 2%/- 1%) Sustainable growth of real GDP (no target) falling unemployment (no target)

THE UK ECONOMY IN FOCUS/APPLICATIONS Reminder of key objectives: Low and positive inflation (inflation rate target of 2%/- 1%) Sustainable growth of real GDP (no target) falling unemployment (no target)

Ireland. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 2015 rebalancing recovery Outlook for Rising domestic demand improves prospects for 2015 Published in collaboration with Highlights The Irish economy grew by 4.8% last year, which was

EY Forecast June 2015 rebalancing recovery Outlook for Rising domestic demand improves prospects for 2015 Published in collaboration with Highlights The Irish economy grew by 4.8% last year, which was

The U.S. and Regional Economic Outlook. A. It s always a pleasure to meet with the Portland Rotary Club.

Presentation to the Portland Rotary Governor Hotel, Portland, Oregon By Robert T. Parry, President and CEO of the Federal Reserve Bank of San Francisco For delivery November 25, 2003, 12:45 PM Pacific

Presentation to the Portland Rotary Governor Hotel, Portland, Oregon By Robert T. Parry, President and CEO of the Federal Reserve Bank of San Francisco For delivery November 25, 2003, 12:45 PM Pacific

Economy Check-In: Post 2008 Crisis Market Update Special Report

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Keeping the Economy on Track

San Francisco Rotary Club Marines Memorial Club For delivery December 5, 2000 at approx. 12:55 PM PST By Robert T. Parry, President, Federal Reserve Bank of San Francisco I. Good afternoon. Keeping the

San Francisco Rotary Club Marines Memorial Club For delivery December 5, 2000 at approx. 12:55 PM PST By Robert T. Parry, President, Federal Reserve Bank of San Francisco I. Good afternoon. Keeping the

Macro Monthly UBS Asset Management June 2018

Macro Monthly UBS Asset Management June 18 Investing in a mature cycle Erin Browne Head of Asset Allocation Evan Brown, CFA Director, Asset Allocation Roland Czerniawski, CFA Associate Director, Asset

Macro Monthly UBS Asset Management June 18 Investing in a mature cycle Erin Browne Head of Asset Allocation Evan Brown, CFA Director, Asset Allocation Roland Czerniawski, CFA Associate Director, Asset

VIEW FROM A. VIEW FROM A MILE HIGH: Tapering the Era of Cap Rate Compression. NOVEMBER 2013 July 2013

THE QUESTION OF HOW RISING TREASURY YIELDS WILL IMPACT CAP RATES has been a major topic of discussion over the past six months. Although many investors are concerned by the increase in Treasury yields,

THE QUESTION OF HOW RISING TREASURY YIELDS WILL IMPACT CAP RATES has been a major topic of discussion over the past six months. Although many investors are concerned by the increase in Treasury yields,

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist

May 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary With Job Market in Good Shape,

May 217 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Mekael Teshome Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary With Job Market in Good Shape,

Economic Barometer. Recent Developments on the National Economy

Economic Barometer CAMERON SCHOOL OF BUSINESS H. DAVID AND DIANE SWAIN CENTER FOR BUSINESS AND ECONOMIC SERVICES Volume V, Issue 4 January 2014 Inside this issue: The US Economy 1 Growth in GDP 1 Labor

Economic Barometer CAMERON SCHOOL OF BUSINESS H. DAVID AND DIANE SWAIN CENTER FOR BUSINESS AND ECONOMIC SERVICES Volume V, Issue 4 January 2014 Inside this issue: The US Economy 1 Growth in GDP 1 Labor

Economic Perspectives 3 rd Quarter Executive Summary. TRICIA NEWCOMB CIMA Associate, Senior Strategy Analyst

Economic Perspectives 3 rd Quarter 2017 Executive Summary The final estimate of Q2 GDP indicated that the economy grew at a 3.1% rate, the highest quarterly growth rate since Q1 of 2015. Consumer spending

Economic Perspectives 3 rd Quarter 2017 Executive Summary The final estimate of Q2 GDP indicated that the economy grew at a 3.1% rate, the highest quarterly growth rate since Q1 of 2015. Consumer spending

Eurozone. EY Eurozone Forecast December 2014

Eurozone EY Eurozone Forecast December 2014 Outlook for Road to recovery remains strewn with obstacles Published in collaboration with Highlights GDP growth With the Finnish economy still struggling to

Eurozone EY Eurozone Forecast December 2014 Outlook for Road to recovery remains strewn with obstacles Published in collaboration with Highlights GDP growth With the Finnish economy still struggling to

Are We There Yet? The U.S. Economy and Monetary Policy. Remarks by

Are We There Yet? The U.S. Economy and Monetary Policy Remarks by Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City January 15, 2019 Central Exchange Kansas City,

Are We There Yet? The U.S. Economy and Monetary Policy Remarks by Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City January 15, 2019 Central Exchange Kansas City,

SUBJECT: PRELIMINARY NOVEMBER 2011 ECONOMIC FORECAST

October 26, 2011 STATE OF WASHINGTON ECONOMIC AND REVENUE FORECAST COUNCIL - 34-1560 TO: FROM: Governor s Council of Economic Advisors Arun Raha, Executive Director Economic and Revenue Forecast Council

October 26, 2011 STATE OF WASHINGTON ECONOMIC AND REVENUE FORECAST COUNCIL - 34-1560 TO: FROM: Governor s Council of Economic Advisors Arun Raha, Executive Director Economic and Revenue Forecast Council

Baseline U.S. Economic Outlook, Summary Table*

March 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Weak February Job Growth, and

March 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Weak February Job Growth, and

Pacific Northwest Economic Development Council Conference Mt. Hood, Oregon June 20, 2005

Pacific Northwest Economic Development Council Conference Mt. Hood, Oregon June 20, 2005 Gary C. Zimmerman, Senior Economist Federal Reserve Bank of San Francisco Gary.Zimmerman@sf.frb.org Overview National

Pacific Northwest Economic Development Council Conference Mt. Hood, Oregon June 20, 2005 Gary C. Zimmerman, Senior Economist Federal Reserve Bank of San Francisco Gary.Zimmerman@sf.frb.org Overview National

Weekly Economic Commentary

LPL FINANCIAL RESEARCH Weekly Economic Commentary August 13, 212 China Has Already Landed Softly John Canally, CFA Economist LPL Financial Please see the LPL Financial Research Weekly Calendar on page

LPL FINANCIAL RESEARCH Weekly Economic Commentary August 13, 212 China Has Already Landed Softly John Canally, CFA Economist LPL Financial Please see the LPL Financial Research Weekly Calendar on page

Economic influences on the Australian mortgage market

Economic influences on the Australian mortgage market Presentation to Choice Aggregation Services Saul Eslake Chief Economist ANZ Burswood Resort Perth 3 rd October 7 www.anz/com/go/economics Capital city

Economic influences on the Australian mortgage market Presentation to Choice Aggregation Services Saul Eslake Chief Economist ANZ Burswood Resort Perth 3 rd October 7 www.anz/com/go/economics Capital city

The Fed and The U.S. Economic Outlook

The Fed and The U.S. Economic Outlook Maria Luengo-Prado Senior Economist and Policy Advisor Federal Reserve Bank of Boston May 13, 2016 Presentation prepared for the Telergee Alliance CFO & Controllers

The Fed and The U.S. Economic Outlook Maria Luengo-Prado Senior Economist and Policy Advisor Federal Reserve Bank of Boston May 13, 2016 Presentation prepared for the Telergee Alliance CFO & Controllers

Keith Phillips, Sr. Economist and Advisor

The Outlook for the Texas Economy Keith Phillips, Sr. Economist and Advisor National Economic Overview Growth in US Economy Positive But Sluggish Market working to heal itself asset prices falling, inflation

The Outlook for the Texas Economy Keith Phillips, Sr. Economist and Advisor National Economic Overview Growth in US Economy Positive But Sluggish Market working to heal itself asset prices falling, inflation

The U.S. Current Account Balance and the Business Cycle

The U.S. Current Account Balance and the Business Cycle Prepared for: Macroeconomic Theory American University Prof. R. Blecker Author: Brian Dew brianwdew@gmail.com November 19, 2015 November 19, 2015

The U.S. Current Account Balance and the Business Cycle Prepared for: Macroeconomic Theory American University Prof. R. Blecker Author: Brian Dew brianwdew@gmail.com November 19, 2015 November 19, 2015

October 2014 Strong Dollar Effects to Investors Dollar Trend Forecast

October 2014 Strong Dollar Effects to Investors In last month investment report, we have discussed our view for the dollar trend in the next 1 to 2 years (We said that following the changing monetary policy,

October 2014 Strong Dollar Effects to Investors In last month investment report, we have discussed our view for the dollar trend in the next 1 to 2 years (We said that following the changing monetary policy,

The U.S. Economy: An Optimistic Outlook, But With Some Important Risks

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

Outlook 2013: China. Growth expected to accelerate again

Outlook 13: China Growth expected to accelerate again Weakened external demand and only limited growth supporting policies from the Chinese government were the main factors explaining China s slowing growth

Outlook 13: China Growth expected to accelerate again Weakened external demand and only limited growth supporting policies from the Chinese government were the main factors explaining China s slowing growth

The real change in private inventories added 0.22 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

LETTER. economic COULD INTEREST RATES HEAD UP IN 2015? JANUARY Canada. United States. Interest rates. Oil price. Canadian dollar.

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Australian Dollar Outlook

Tuesday, 31 March 015 Australian Dollar Outlook Still Under Pressure We have revised our AUD forecasts for this year down slightly to reflect developments over recent months. We now expect the AUD to end

Tuesday, 31 March 015 Australian Dollar Outlook Still Under Pressure We have revised our AUD forecasts for this year down slightly to reflect developments over recent months. We now expect the AUD to end

1 World Economy. Value of Finnish Forest Industry Exports Fell by Almost a Quarter in 2009

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

Economic Growth Expected to Slow and Housing to Stabilize in 2019

Consumer Confidence Expectations in the Next Six Months (%) Economic Developments December 218 Economic Growth Expected to Slow and Housing to Stabilize in 219 The U.S. economy is expected to grow 2.6

Consumer Confidence Expectations in the Next Six Months (%) Economic Developments December 218 Economic Growth Expected to Slow and Housing to Stabilize in 219 The U.S. economy is expected to grow 2.6

Investment Matters: Non- Residential Structures. Introduction. Volume 1 Number 5 May Thanks again for subscribing! By CR

Volume 1 Number 5 May 2008 Introduction Thanks again for subscribing! This month CR is going to shift gears and start with non-residential investment and commercial real estate (CRE). It appears the CRE

Volume 1 Number 5 May 2008 Introduction Thanks again for subscribing! This month CR is going to shift gears and start with non-residential investment and commercial real estate (CRE). It appears the CRE

An interim assessment

What is the economic outlook for OECD countries? An interim assessment Paris, 8 September 2011 11h00 Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General Activity has come close

What is the economic outlook for OECD countries? An interim assessment Paris, 8 September 2011 11h00 Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General Activity has come close

Monthly Bulletin of Economic Trends: Review of the Australian Economy

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

FRONT BARNETT ASSOCIATES LLC

FRONT BARNETT ASSOCIATES LLC I N V E S T M E N T C O U N S E L August 1, 2000 THE BUSINESS OUTLOOK: SLOWING CONSUMER SPENDING With the overall economy growing at an astounding 5% annual rate in the first

FRONT BARNETT ASSOCIATES LLC I N V E S T M E N T C O U N S E L August 1, 2000 THE BUSINESS OUTLOOK: SLOWING CONSUMER SPENDING With the overall economy growing at an astounding 5% annual rate in the first

To understand where the U.S. Economy is going, we need to understand where we have been

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

U.S. Economic Update and Outlook. Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 2013

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

The Hong Kong Economy in Contraction Mode

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com 22 December 08 The Hong Kong Economy in Contraction Mode Hong Kong is in recession and leading economic

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com 22 December 08 The Hong Kong Economy in Contraction Mode Hong Kong is in recession and leading economic

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011 Anthony B. Sanders Distinguished Professor of Real Estate Finance, George Mason University, and Senior Scholar, Mercatus

WHAT THE EURO CRISIS MEANS FOR TAXPAYERS AND THE U.S. ECONOMY, PART 1 DECEMBER 15, 2011 Anthony B. Sanders Distinguished Professor of Real Estate Finance, George Mason University, and Senior Scholar, Mercatus

The commercial real estate investment cycle

August 2013 The commercial real estate investment cycle Market indicators suggest upside potential Martha Peyton, Ph.D. Managing Director and Head of Real Estate Strategy and Research, TIAA-CREF Executive

August 2013 The commercial real estate investment cycle Market indicators suggest upside potential Martha Peyton, Ph.D. Managing Director and Head of Real Estate Strategy and Research, TIAA-CREF Executive

Structure and Function of the Federal Reserve System

1/17/17 Economic Outlook Cortney Cowley Economist Federal Reserve Bank of Kansas City Omaha Branch October, 17 The views expressed are those of the author and do not necessarily reflect the opinions of

1/17/17 Economic Outlook Cortney Cowley Economist Federal Reserve Bank of Kansas City Omaha Branch October, 17 The views expressed are those of the author and do not necessarily reflect the opinions of

The Outlook for the U.S. Economy March Summary View. The Current State of the Economy

The Outlook for the U.S. Economy March 2010 Summary View The Current State of the Economy 8% 6% Quarterly Change (SAAR) Chart 1. The Economic Outlook History Forecast The December 2007-2009 recession is

The Outlook for the U.S. Economy March 2010 Summary View The Current State of the Economy 8% 6% Quarterly Change (SAAR) Chart 1. The Economic Outlook History Forecast The December 2007-2009 recession is

Global FX 3 Jan 2012

Global FX Jan The euro area s sovereign debt crisis has been dominating trading in financial markets over the past year and the currency market was no exception. The region s debt problems spread from

Global FX Jan The euro area s sovereign debt crisis has been dominating trading in financial markets over the past year and the currency market was no exception. The region s debt problems spread from