Financial Crises and Asset Prices. Tyler Muir June 2017, MFM

|

|

|

- Christine Palmer

- 5 years ago

- Views:

Transcription

1 Financial Crises and Asset Prices Tyler Muir June 2017, MFM

2 Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What can we learn about credit cycles and models of crises / frictions? Krishnamurthy Muir 2017 Broad empirical facts Useful for calibration and sorting out models

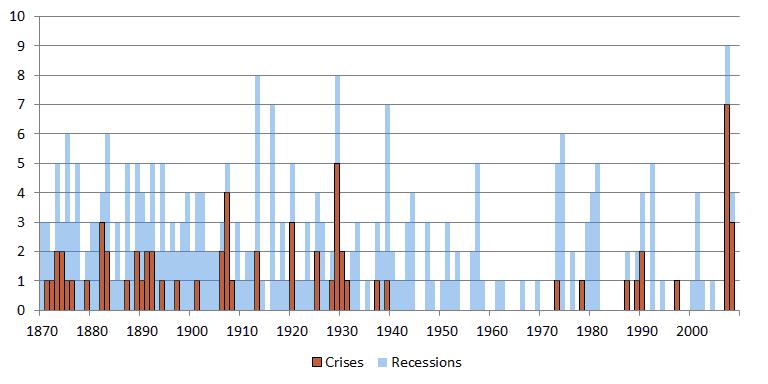

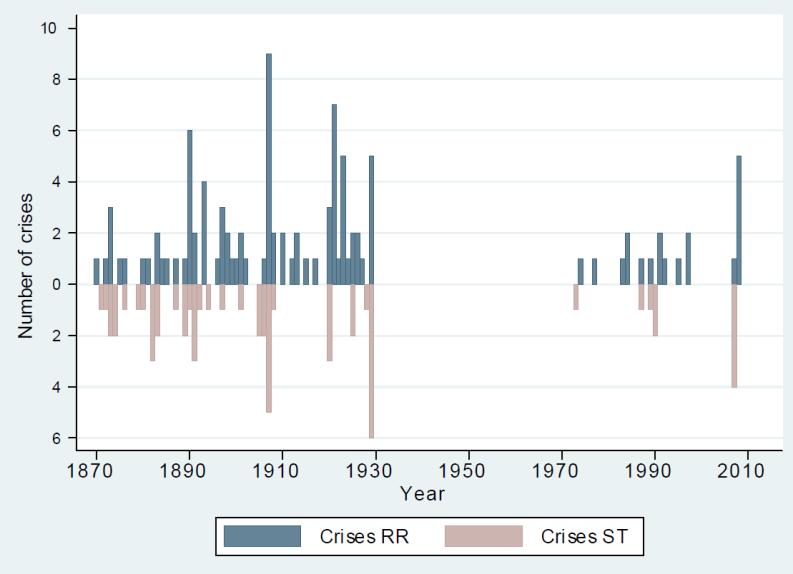

3 Data across 14 countries Asset prices: credit spreads, d/p, stock returns Many sources, discuss spreads later Macro: consumption, GDP from Barro and Ursua Financial crisis dates: Schularick and Taylor, Reinhart Rogoff we define financial crises as events during which a country's banking sector experiences bank runs, sharp increases in default rates accompanied by large losses of capital that result in public intervention, bankruptcy, or forced merger of financial institutions.

4

5 Background: Learning about asset pricing Big question, why do risk premia E[R] move so much over time? Gordon Growth d / p = r g Volatile prices Smooth cash flows Expected return, E[r], must be very volatile

6 Why? Theories: why do expected returns vary so much? Standard: rep agent (household) Habits (S=surplus consumption), LRR (S=vol(c)), Rare disaster (S=prob disaster) Behavioral: S=extrapolation, sentiment Intermediary models S = health of financial sector, risk bearing capacity

7 How can we distinguish? Look for episodes where S should have moved according to rep agent models Recessions, wars Compare to episodes where banking system and credit were adversely affected Historical data 14 countries Financial crises ( = bank runs), recessions, deep recessions, wars

8 Result Risk premia appear largest in banking crises 30% % 20% 15% 10% 5% % Financial Crises Recessions Deep Recessions Wars 0 Change in d/p Change in Credit Spread

9 Result Consumption state variables don t match variation 30% 25% 20% 15% 10% 5% % Financial Crises Recessions Deep Recessions Wars 0 Decline in Consumption Consumption Volatility

10 Result (2) Price declines during financial crises should be temporary if really about expected returns

11 Interpretation Explanation for spikes in risk premia can t only rely on macro economy doing poorly Suggestive: credit / health of banking system are important for asset prices Suggestive of intermediary theories, but can we more accurately measure S and test?

12 Intermediary pricing kernel Asset pricing equation M captures marginal utility (V (W)), marginal value of a dollar Often try to measure V (W) from household Intermediary theory: use V (W) of intermediary

13 Intermediary pricing kernel How to measure V (W) of intermediary? Theory: Brunnermeier Pedersen (2009) Idea: bad times, constraints tighten, intermediaries delever, V (W) is high AEM (2014): log change in leverage of broker-dealers, flow of funds quarterly Large deleveraging in crisis

14 Adrian Etula Muir 2014: cross section (25 S/BM, 10 Mom, 6 Bonds)

15 Comparison to other models

16 Time-series regressions Predictive regression Source: Haddad Muir 2017

17 Identification The veil hypothesis: intermediaries just reflect marginal utility of HH but don t actually matter How can we test? Haddad and Muir 2017 Key prediction of frictionless view of these results is that all risk premia increase proportionally to risk aversion shock Alternative: relative risk premia elasticities should be larger in more intermediated asset classes if there is an intermediary risk aversion shock

18 Intermediary risk aversion shock

19 Conclusions Suggestive: credit conditions / health of banking system are important for asset prices Separated this effect from rep agent being affected by bad macroeconomic shock More work Spelling out the frictions (multiple intermediary models), calibrating models Empirical work on identification vs frictionless views Connect micro studies (Mitchell Pulvino 2010, Du Tepper Verdelhan 2017, etc) to macro

20 Part 2: Macro Krishnamurthy and Muir (2017) How Credit Cycles across a Financial Crisis

21 We describe the behavior of output, credit, and credit spreads around a financial crisis What is a financial crisis? Is a crisis just a bad TFP realization? Data through the lens of F " z " model F " is financial sector fragility ( amplifier ) z " is shock (losses) to the financial sector balance sheet ( trigger ) Main results: 1. Crises are associated with large unexpected losses to the financial sector 2. Fragility and size of losses summarize the subsequent output decline 3. Pre-crisis, the runup is driven by a credit supply expansion: spreads appear to be too low 21

22 Time 0 is the crisis 22

23 Empirical Strategy What happens around a financial crisis? Approach: Define a set of dates identified with a major financial crisis Examine the behavior of output, credit, and spreads around these dates Compare to non-crisis events 23

24 Theory: What is a financial crisis? Shock z " : recessionary shock, lower expected cash-flows on assets held by intermediaries Fragility F " : high leverage/low equity capital, short-term debt, correlated intermediary positions, interconnected exposures Trigger + Amplification Asset price feedback Credit crunch Bank runs/failures/disintermediation Credit spreads rise: Expected default + risk/illiquidity premium Kiyotaki-Moore, He-Krishnamurthy, Brunnermeier-Sannikov, Bernanke Gertler others 24

25 Quantitative Identify high fragility (F " ) Identify large losses (z " ) Define crises as events with large losses hitting fragile financial sector Side benefit: avoids we know one when see one critique of the narrative approach (e.g., Schularick Taylor, Reinhart Rogoff) 25

26 Data: Credit spreads, crisis dates, GDP across 14 countries from old newspapers 1930-present from various central banks and other data sets (Datastream, Global Financial Database) for more recent credit spreads High grade minus low grade corporate spread Corporate bond index to government bond We normalize each country s spread as: s &," = spread &," spread & Total of 900 country-year observations 26

27 Credit spreads: Individual bond prices on banks, sovereigns, railroad, etc. Over 4000 unique bonds, 200,000 bond / years We convert to yield to maturity Spread = high 10 th percentile avg yield minus low 10 th percentile avg yield 27

28 Data: Credit spreads, crisis dates, GDP We cross this data with crisis-recession dates from Schularick- Taylor (ST) and non-financial recession from ST. Robustness: Reinhart-Rogoff (RR), Bordo-Eichengreen-Klingebiel- Martinez (BE) Total of 900 country-year observations: 44 ST crises 48 RR crises 27 BE crises GDP data from Barro-Ursua 28

29 29

30 RESULT 1: LOSSES AND CRISES 30

31 Specification Panel data regressions (country i, horizon k): Interact spreads with crisis dummies ln y &,"45 = a y & + a " &:&: [b 8 s &," + b 8 => s &,"=> ] + &," s &," + => s &,"=> ] + c x " + ε &,"45 Controls: lagged GDP growth, 3 year credit growth from Schularick- Taylor Standard errors cluster by country 31

32 Spread spikes = Losses 32

33 33

34 RESULT 2: FRAGILITY (F) X LOSSES (z) 34

35 Do all spread spikes end badly? (LTCM v. 2008) 35

36 HighCredit = 1, if > median of 3-year credit growth 36

37 Impulse response in High Credit state 37

38 Impulse response ST crises: 38

39 Post-war sample 39

40 RESULT 3: PRE-CRISIS BUILD UP 40

41 Pre-crisis behavior Schularick and Taylor fact: Crises preceded by credit growth New fact: Crises also preceded by falling credit spreads Explanations: 1. (Over optimistic) income prospects drives borrowing/lending 2. Financial sector risk pricing and risk premia fall 3. Note: not predicted by existing intermediary based models / rational models of credit boom bust See also Baron Xiong (2017) 41

42 Spread pre-crises compared to other periods 42

43 Froth and Output 43

44 Marginal probabilities of ST crisis P(Crisis) from Probit Year P(Crisis HC_HF=0) P(Crisis HC_HF=1) 44

45 HOW DID 2008 MATCH UP? 45

46 How did 2008 match up? Low spreads; fast credit growth 46

47 How did 2008 match up? 47

48 Summary Spikes in spreads + real fragility = Losses + Amplification Lead to poor GDP outcomes (Kiyotaki-Moore, He- Krishnamurthy) Crises are preceded by unusually low spreads Spreads pre-crisis do not price an increase in fragility Credit supply expansions precede crises Surprise is a key dimension of crises Aftermath of financial crises is deep recession We use variation in severity indexed by spreads Results consistent with Reinhart-Rogoff, Schularick- Taylor; We give more precise answers, useful for calibrating models 48

49 Conclusions Recent interest in macro models of intermediation, asset prices, crises Stylized empirical facts appear promising for these theories Some shortcomings as well (e.g., risk premia low before a crisis) Quantitative patterns for theories to target More to be done on understanding mechanisms of frictions, identification vs frictionless models

FINANCIAL CRISES AND RISK PREMIA

FINANCIAL CRISES AND RISK PREMIA Tyler Muir July, 2016 Abstract I analyze the behavior of risk premia in financial crises, wars, and recessions in an international panel spanning over 140 years and over

FINANCIAL CRISES AND RISK PREMIA Tyler Muir July, 2016 Abstract I analyze the behavior of risk premia in financial crises, wars, and recessions in an international panel spanning over 140 years and over

How Credit Cycles across a Financial Crisis

How Credit Cycles across a Financial Crisis Arvind Krishnamurthy Stanford GSB and NBER Tyler Muir UCLA and NBER August 2017 Abstract We study the behavior of credit and output across a financial crisis

How Credit Cycles across a Financial Crisis Arvind Krishnamurthy Stanford GSB and NBER Tyler Muir UCLA and NBER August 2017 Abstract We study the behavior of credit and output across a financial crisis

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Expansion and Neglected Crash Risk. Online Appendix

Credit Expansion and Neglected Crash Risk Online Appendix Matthew Baron and Wei Xiong A. Additional details on data construction Here we present additional information related to data sources and variable

Credit Expansion and Neglected Crash Risk Online Appendix Matthew Baron and Wei Xiong A. Additional details on data construction Here we present additional information related to data sources and variable

WP/18/23. Lending Standards and Output Growth. by Divya Kirti

WP/18/23 Lending Standards and Output Growth by Divya Kirti IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate. The views expressed

WP/18/23 Lending Standards and Output Growth by Divya Kirti IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate. The views expressed

Bubbles, Liquidity and the Macroeconomy

Bubbles, Liquidity and the Macroeconomy Markus K. Brunnermeier The recent financial crisis has shown that financial frictions such as asset bubbles and liquidity spirals have important consequences not

Bubbles, Liquidity and the Macroeconomy Markus K. Brunnermeier The recent financial crisis has shown that financial frictions such as asset bubbles and liquidity spirals have important consequences not

Do Intermediaries Matter for Aggregate Asset Prices? Discussion

Do Intermediaries Matter for Aggregate Asset Prices? by Valentin Haddad and Tyler Muir Discussion Pietro Veronesi The University of Chicago Booth School of Business Main Contribution and Outline of Discussion

Do Intermediaries Matter for Aggregate Asset Prices? by Valentin Haddad and Tyler Muir Discussion Pietro Veronesi The University of Chicago Booth School of Business Main Contribution and Outline of Discussion

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Overborrowing, Financial Crises and Macro-prudential Policy

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Do Intermediaries Matter for Aggregate Asset Prices?

Do Intermediaries Matter for Aggregate Asset Prices? Valentin Haddad and Tyler Muir October 1, 2017 Abstract We propose a simple framework for intermediary asset pricing. Two elements shape if and how

Do Intermediaries Matter for Aggregate Asset Prices? Valentin Haddad and Tyler Muir October 1, 2017 Abstract We propose a simple framework for intermediary asset pricing. Two elements shape if and how

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns Tobias Adrian tobias.adrian@ny.frb.org Erkko Etula etula@post.harvard.edu Tyler Muir t-muir@kellogg.northwestern.edu

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns Tobias Adrian tobias.adrian@ny.frb.org Erkko Etula etula@post.harvard.edu Tyler Muir t-muir@kellogg.northwestern.edu

Financial Intermediaries and the Cross-Section of Asset Returns. Discussion

Financial Intermediaries and the Cross-Section of Asset Returns by Adrian, Etula, Muir Discussion Pietro Veronesi The University of Chicago Booth School of Business 1 What does this paper do? 1. From Broker-Dealer

Financial Intermediaries and the Cross-Section of Asset Returns by Adrian, Etula, Muir Discussion Pietro Veronesi The University of Chicago Booth School of Business 1 What does this paper do? 1. From Broker-Dealer

A Macroeconomic Framework for Quantifying Systemic Risk. June 2012

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Credit Spreads and the Severity of Financial Crises

Credit Spreads and the Severity of Financial Crises Arvind Krishnamurthy Stanford GSB Tyler Muir Yale SOM January 2, 2015 Abstract We study the behavior of credit spreads and their link to economic growth

Credit Spreads and the Severity of Financial Crises Arvind Krishnamurthy Stanford GSB Tyler Muir Yale SOM January 2, 2015 Abstract We study the behavior of credit spreads and their link to economic growth

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Credit Booms, Financial Crises and Macroprudential Policy

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Main Points: Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable

NBER July 2018 Main Points: 2 Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable US housing bubble and the crisis of

NBER July 2018 Main Points: 2 Revival of research on credit cycles shows that financial crises follow credit expansions, are long time coming, and in part predictable US housing bubble and the crisis of

The Leverage Cycle. John Geanakoplos. Discussion by. Franklin Allen. University of Pennsylvania.

The Leverage Cycle by John Geanakoplos Discussion by Franklin Allen University of Pennsylvania allenf@wharton.upenn.edu NBER Macroeconomics Annual 2009 July 15, 2009 Over the last dozen years or so John

The Leverage Cycle by John Geanakoplos Discussion by Franklin Allen University of Pennsylvania allenf@wharton.upenn.edu NBER Macroeconomics Annual 2009 July 15, 2009 Over the last dozen years or so John

Should Unconventional Monetary Policies Become Conventional?

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Leverage Across Firms, Banks and Countries

Şebnem Kalemli-Özcan, Bent E. Sørensen and Sevcan Yeşiltaş University of Houston and NBER, University of Houston and CEPR, and Johns Hopkins University Dallas Fed Conference on Financial Frictions and

Şebnem Kalemli-Özcan, Bent E. Sørensen and Sevcan Yeşiltaş University of Houston and NBER, University of Houston and CEPR, and Johns Hopkins University Dallas Fed Conference on Financial Frictions and

Identifying Banking Crises

Identifying Banking Crises Matthew Baron (Cornell) Emil Verner (Princeton & MIT Sloan) Wei Xiong (Princeton) April 10, 2018 Consequences of banking crises Consequences are severe, according to Reinhart

Identifying Banking Crises Matthew Baron (Cornell) Emil Verner (Princeton & MIT Sloan) Wei Xiong (Princeton) April 10, 2018 Consequences of banking crises Consequences are severe, according to Reinhart

Understanding the Macro-Financial Effects of Household Debt: A Global Perspective

WP/8/76 Understanding the Macro-Financial Effects of Household Debt: A Global Perspective by Adrian Alter, Alan Xiaochen Feng, and Nico Valckx IMF Working Papers describe research in progress by the author(s)

WP/8/76 Understanding the Macro-Financial Effects of Household Debt: A Global Perspective by Adrian Alter, Alan Xiaochen Feng, and Nico Valckx IMF Working Papers describe research in progress by the author(s)

Overborrowing, Financial Crises and Macro-prudential Policy. Macro Financial Modelling Meeting, Chicago May 2-3, 2013

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Do Intermediaries Matter for Aggregate Asset Prices?

Do Intermediaries Matter for Aggregate Asset Prices? Preliminary Version Valentin Haddad and Tyler Muir January 6, 2018 Abstract Existing studies find that intermediary balance sheets are strongly correlated

Do Intermediaries Matter for Aggregate Asset Prices? Preliminary Version Valentin Haddad and Tyler Muir January 6, 2018 Abstract Existing studies find that intermediary balance sheets are strongly correlated

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

The Term Structure of Growth-at-Risk

The Term Structure of Growth-at-Risk Tobias Adrian, Federico Grinberg, Nellie Liang, Sheheryar Malik* Mar. 3, 2018 Abstract Using panels of 11 advanced and 10 emerging economies, we show that loose financial

The Term Structure of Growth-at-Risk Tobias Adrian, Federico Grinberg, Nellie Liang, Sheheryar Malik* Mar. 3, 2018 Abstract Using panels of 11 advanced and 10 emerging economies, we show that loose financial

Juan Carlos Castro-Fernández * Working Paper This version: 19 November 2017

BIG RECESSIONS AND SLOW RECOVERIES Juan Carlos Castro-Fernández * Working Paper This version: 19 November 17 ABSTRACT It has been frequently claimed that financial crises are more painful and lead to slower

BIG RECESSIONS AND SLOW RECOVERIES Juan Carlos Castro-Fernández * Working Paper This version: 19 November 17 ABSTRACT It has been frequently claimed that financial crises are more painful and lead to slower

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER March 215 He and Krishnamurthy (Chicago, Stanford) Systemic

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER March 215 He and Krishnamurthy (Chicago, Stanford) Systemic

LECTURE 9 The Effects of Credit Contraction: Credit Market Disruptions. October 19, 2016

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 9 The Effects of Credit Contraction: Credit Market Disruptions October 19, 2016 I. OVERVIEW AND GENERAL ISSUES Effects of Credit Balance-sheet

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 9 The Effects of Credit Contraction: Credit Market Disruptions October 19, 2016 I. OVERVIEW AND GENERAL ISSUES Effects of Credit Balance-sheet

On the Scale of Financial Intermediaries

Federal Reserve Bank of New York Staff Reports On the Scale of Financial Intermediaries Tobias Adrian Nina Boyarchenko Hyun Song Shin Staff Report No. 743 October 215 Revised December 216 This paper presents

Federal Reserve Bank of New York Staff Reports On the Scale of Financial Intermediaries Tobias Adrian Nina Boyarchenko Hyun Song Shin Staff Report No. 743 October 215 Revised December 216 This paper presents

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

A Policy Model for Analyzing Macroprudential and Monetary Policies

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

1 Business-Cycle Facts Around the World 1

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

The Labor Market Consequences of Adverse Financial Shocks

The Labor Market Consequences of Adverse Financial Shocks November 2012 Unemployment rate on the two sides of the Atlantic Credit to the private sector over GDP Credit to private sector as a percentage

The Labor Market Consequences of Adverse Financial Shocks November 2012 Unemployment rate on the two sides of the Atlantic Credit to the private sector over GDP Credit to private sector as a percentage

What is Cyclical in Credit Cycles?

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

Credit Booms Gone Bust

Credit Booms Gone Bust Monetary Policy, Leverage Cycles and Financial Crises, 1870 2008 Moritz Schularick (Free University of Berlin) Alan M. Taylor (UC Davis & Morgan Stanley) Federal Reserve Bank of

Credit Booms Gone Bust Monetary Policy, Leverage Cycles and Financial Crises, 1870 2008 Moritz Schularick (Free University of Berlin) Alan M. Taylor (UC Davis & Morgan Stanley) Federal Reserve Bank of

An Introduction to Macroeconomics

An Introduction to Macroeconomics Economics 4353 - Intermediate Macroeconomics Aaron Hedlund University of Missouri Fall 2015 Econ 4353 (University of Missouri) Introduction Fall 2015 1 / 19 What is Macroeconomics?

An Introduction to Macroeconomics Economics 4353 - Intermediate Macroeconomics Aaron Hedlund University of Missouri Fall 2015 Econ 4353 (University of Missouri) Introduction Fall 2015 1 / 19 What is Macroeconomics?

Financial Intermediaries and Monetary Economics

Financial Intermediaries and Monetary Economics By T. Adrian and H. Shin Based on a series of papers by Adrian, Shin, and coauthors and forthcoming in Handbook of Monetary Economics Motivation This paper

Financial Intermediaries and Monetary Economics By T. Adrian and H. Shin Based on a series of papers by Adrian, Shin, and coauthors and forthcoming in Handbook of Monetary Economics Motivation This paper

Integrating Banking and Banking Crises in Macroeconomic Analysis. Mark Gertler NYU May 2018 Nobel/Riksbank Symposium

Integrating Banking and Banking Crises in Macroeconomic Analysis Mark Gertler NYU May 2018 Nobel/Riksbank Symposium Overview Adapt macro models to account for financial crises (like recent one) Emphasis

Integrating Banking and Banking Crises in Macroeconomic Analysis Mark Gertler NYU May 2018 Nobel/Riksbank Symposium Overview Adapt macro models to account for financial crises (like recent one) Emphasis

MACROECONOMICS AND FINANCIAL MARKETS

MACROECONOMICS AND FINANCIAL MARKETS Veronica Guerrieri and Harald Uhlig Discussion by Luigi Bocola Northwestern University and FRB Minneapolis The views expressed herein are those of the author and not

MACROECONOMICS AND FINANCIAL MARKETS Veronica Guerrieri and Harald Uhlig Discussion by Luigi Bocola Northwestern University and FRB Minneapolis The views expressed herein are those of the author and not

Do Intermediaries Matter for Aggregate Asset Prices?

Do Intermediaries Matter for Aggregate Asset Prices? Valentin Haddad and Tyler Muir April 16, 2018 Abstract Existing studies find that intermediary balance sheets are strongly correlated with asset returns,

Do Intermediaries Matter for Aggregate Asset Prices? Valentin Haddad and Tyler Muir April 16, 2018 Abstract Existing studies find that intermediary balance sheets are strongly correlated with asset returns,

HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE

DISCUSSION OF: HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE BY MIAN, SUFI AND VERNER Emi Nakamura Columbia University December 2015 Nakamura Inflation Expectations December 2015 1 / 24 Could a credit boom

DISCUSSION OF: HOUSEHOLD DEBT AND BUSINESS CYCLES WORLDWIDE BY MIAN, SUFI AND VERNER Emi Nakamura Columbia University December 2015 Nakamura Inflation Expectations December 2015 1 / 24 Could a credit boom

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

Márcio G. P. Garcia PUC-Rio Brazil Visiting Scholar, Sloan School, MIT and NBER. This paper aims at quantitatively evaluating two questions:

Discussion of Unconventional Monetary Policy and the Great Recession: Estimating the Macroeconomic Effects of a Spread Compression at the Zero Lower Bound Márcio G. P. Garcia PUC-Rio Brazil Visiting Scholar,

Discussion of Unconventional Monetary Policy and the Great Recession: Estimating the Macroeconomic Effects of a Spread Compression at the Zero Lower Bound Márcio G. P. Garcia PUC-Rio Brazil Visiting Scholar,

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Monetary Economics July 2014

ECON40013 ECON90011 Monetary Economics July 2014 Chris Edmond Office hours: by appointment Office: Business & Economics 423 Phone: 8344 9733 Email: cedmond@unimelb.edu.au Course description This year I

ECON40013 ECON90011 Monetary Economics July 2014 Chris Edmond Office hours: by appointment Office: Business & Economics 423 Phone: 8344 9733 Email: cedmond@unimelb.edu.au Course description This year I

Credit Booms Gone Bust: Monetary Policy, Leverage Cycles and Financial Crises,

Credit Booms Gone Bust: Monetary Policy, Leverage Cycles and Financial Crises, 1870 2008 Moritz Schularick (Free University, Berlin) Alan M. Taylor (University of California, Davis, and NBER) Taylor &

Credit Booms Gone Bust: Monetary Policy, Leverage Cycles and Financial Crises, 1870 2008 Moritz Schularick (Free University, Berlin) Alan M. Taylor (University of California, Davis, and NBER) Taylor &

Risk, Uncertainty and Monetary Policy

Risk, Uncertainty and Monetary Policy Geert Bekaert Marie Hoerova Marco Lo Duca Columbia GSB ECB ECB The views expressed are solely those of the authors. The fear index and MP 2 Research questions / Related

Risk, Uncertainty and Monetary Policy Geert Bekaert Marie Hoerova Marco Lo Duca Columbia GSB ECB ECB The views expressed are solely those of the authors. The fear index and MP 2 Research questions / Related

When Credit Bites Back: Leverage, Business Cycles, and Crises

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

Market Quality, Financial Crises, and TFP Growth in the US:

Market Quality, Financial Crises, and TFP Growth in the US: 1840 2014 Kevin R. James Systemic Risk Centre London School of Economics k.james1@lse.ac.uk Akshay Kotak Said School Oxford University akshay.kotak@sbs.ox.ac.uk

Market Quality, Financial Crises, and TFP Growth in the US: 1840 2014 Kevin R. James Systemic Risk Centre London School of Economics k.james1@lse.ac.uk Akshay Kotak Said School Oxford University akshay.kotak@sbs.ox.ac.uk

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Discussion of "The Value of Trading Relationships in Turbulent Times"

Discussion of "The Value of Trading Relationships in Turbulent Times" by Di Maggio, Kermani & Song Bank of England LSE, Third Economic Networks and Finance Conference 11 December 2015 Mandatory disclosure

Discussion of "The Value of Trading Relationships in Turbulent Times" by Di Maggio, Kermani & Song Bank of England LSE, Third Economic Networks and Finance Conference 11 December 2015 Mandatory disclosure

Financial Cycles and Credit Growth Across Countries

Financial Cycles and Credit Growth Across Countries By Nuno Coimbra and Helene Rey Credit growth is an ubiquitous variable in the literature on crises and financial stability. Crises tend to be credit

Financial Cycles and Credit Growth Across Countries By Nuno Coimbra and Helene Rey Credit growth is an ubiquitous variable in the literature on crises and financial stability. Crises tend to be credit

Penitence after accusations of error,...

Penitence after accusations of error,... Comments Martin Eichenbaum NBER, July 2013 Background Economists have long argued about the role that policy played in major macro episodes and the way policy institutions

Penitence after accusations of error,... Comments Martin Eichenbaum NBER, July 2013 Background Economists have long argued about the role that policy played in major macro episodes and the way policy institutions

flow-based borrowing constraints and macroeconomic fluctuations

flow-based borrowing constraints and macroeconomic fluctuations Thomas Drechsel (LSE) Annual Congress of the EEA University of Cologne 27 August 2018 in a nutshell I What do the dynamics of firm borrowing

flow-based borrowing constraints and macroeconomic fluctuations Thomas Drechsel (LSE) Annual Congress of the EEA University of Cologne 27 August 2018 in a nutshell I What do the dynamics of firm borrowing

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk

Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk") Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

Comparing Different Regulatory Measures to Control Stock Market Volatility: A General Equilibrium Analysis

Comparing Different Regulatory Measures to Control Stock Market Volatility: A General Equilibrium Analysis A. Buss B. Dumas R. Uppal G. Vilkov INSEAD INSEAD, CEPR, NBER Edhec, CEPR Goethe U. Frankfurt

Comparing Different Regulatory Measures to Control Stock Market Volatility: A General Equilibrium Analysis A. Buss B. Dumas R. Uppal G. Vilkov INSEAD INSEAD, CEPR, NBER Edhec, CEPR Goethe U. Frankfurt

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY C. Detken, K. Masuch and F. Smets 1 On 11-12 December 2003, the Directorate Monetary Policy of the Directorate General Economics in

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY C. Detken, K. Masuch and F. Smets 1 On 11-12 December 2003, the Directorate Monetary Policy of the Directorate General Economics in

Financial Intermediation and Capital Reallocation

Financial Intermediation and Capital Reallocation Hengjie Ai, Kai Li, and Fang Yang NBER Summer Institute, Asset Pricing July 09, 2015 1 / 19 Financial Intermediation and Capital Reallocation Motivation

Financial Intermediation and Capital Reallocation Hengjie Ai, Kai Li, and Fang Yang NBER Summer Institute, Asset Pricing July 09, 2015 1 / 19 Financial Intermediation and Capital Reallocation Motivation

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Macro Notes: Introduction to the Short Run

Macro Notes: Introduction to the Short Run Alan G. Isaac American University But this long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy,

Macro Notes: Introduction to the Short Run Alan G. Isaac American University But this long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy,

Currency Risk Premia and Macro Fundamentals

Discussion of Currency Risk Premia and Macro Fundamentals by Lukas Menkhoff, Lucio Sarno, Maik Schmeling, and Andreas Schrimpf Christiane Baumeister Bank of Canada ECB-BoC workshop on Exchange rates: A

Discussion of Currency Risk Premia and Macro Fundamentals by Lukas Menkhoff, Lucio Sarno, Maik Schmeling, and Andreas Schrimpf Christiane Baumeister Bank of Canada ECB-BoC workshop on Exchange rates: A

Financial Amplification, Regulation and Long-term Lending

Financial Amplification, Regulation and Long-term Lending Michael Reiter 1 Leopold Zessner 2 1 Instiute for Advances Studies, Vienna 2 Vienna Graduate School of Economics Barcelona GSE Summer Forum ADEMU,

Financial Amplification, Regulation and Long-term Lending Michael Reiter 1 Leopold Zessner 2 1 Instiute for Advances Studies, Vienna 2 Vienna Graduate School of Economics Barcelona GSE Summer Forum ADEMU,

The Labor Market Consequences of Adverse Financial Shocks

13TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 8 9, 2012 The Labor Market Consequences of Adverse Financial Shocks Tito Boeri Bocconi University and frdb Pietro Garibaldi University of Torino and

13TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 8 9, 2012 The Labor Market Consequences of Adverse Financial Shocks Tito Boeri Bocconi University and frdb Pietro Garibaldi University of Torino and

Discussion of - Leverage-induced Fire Sales & Crashes - Leverage Network & Market Contagion

Discussion of - Leverage-induced Fire Sales & Crashes - Leverage Network & Market Contagion Brunnermeier by Markus Brunnermeier MFM Conference 2018 New York, Jan 25 th, 2018 2 papers with different focus

Discussion of - Leverage-induced Fire Sales & Crashes - Leverage Network & Market Contagion Brunnermeier by Markus Brunnermeier MFM Conference 2018 New York, Jan 25 th, 2018 2 papers with different focus

Which Financial Frictions? Parsing the Evidence from the Financial Crisis of

Which Financial Frictions? Parsing the Evidence from the Financial Crisis of 2007-9 Tobias Adrian Paolo Colla Hyun Song Shin February 2013 Adrian, Colla and Shin: Which Financial Frictions? 1 An Old Debate

Which Financial Frictions? Parsing the Evidence from the Financial Crisis of 2007-9 Tobias Adrian Paolo Colla Hyun Song Shin February 2013 Adrian, Colla and Shin: Which Financial Frictions? 1 An Old Debate

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 2 nd CEBRA International Finance and Macroeconomics Meeting Risk, Volatility and Central Bank s Policies Madrid November 2018 1 The

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 2 nd CEBRA International Finance and Macroeconomics Meeting Risk, Volatility and Central Bank s Policies Madrid November 2018 1 The

Booms and Busts in Latin America: The Role of External Factors

Economic and Financial Linkages in the Western Hemisphere Seminar organized by the Western Hemisphere Department International Monetary Fund November 26, 2007 Booms and Busts in Latin America: The Role

Economic and Financial Linkages in the Western Hemisphere Seminar organized by the Western Hemisphere Department International Monetary Fund November 26, 2007 Booms and Busts in Latin America: The Role

Asset Price Bubbles and Systemic Risk

Asset Price Bubbles and Systemic Risk Markus Brunnermeier, Simon Rother, Isabel Schnabel AFA 2018 Annual Meeting Philadelphia; January 7, 2018 Simon Rother (University of Bonn) Asset Price Bubbles and

Asset Price Bubbles and Systemic Risk Markus Brunnermeier, Simon Rother, Isabel Schnabel AFA 2018 Annual Meeting Philadelphia; January 7, 2018 Simon Rother (University of Bonn) Asset Price Bubbles and

Overview: Financial Stability and Systemic Risk

Overview: Financial Stability and Systemic Risk Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views

Overview: Financial Stability and Systemic Risk Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views

The Term Structure of Growth-at-Risk

The Term Structure of Growth-at-Risk Tobias Adrian, Federico Grinberg, Nellie Liang, Sheheryar Malik* May 16, 2018 Abstract Using panels of 11 advanced and 10 emerging economies, we show that loose financial

The Term Structure of Growth-at-Risk Tobias Adrian, Federico Grinberg, Nellie Liang, Sheheryar Malik* May 16, 2018 Abstract Using panels of 11 advanced and 10 emerging economies, we show that loose financial

Crises and Growth: A Re-Evaluation

Crises and Growth: A Re-Evaluation Romain Rancière Aaron Tornell Frank Westermann Dubrovnik, July 2005 "The regular development of wealth does not occur without pain and resistance. In crises everything

Crises and Growth: A Re-Evaluation Romain Rancière Aaron Tornell Frank Westermann Dubrovnik, July 2005 "The regular development of wealth does not occur without pain and resistance. In crises everything

A Real Intertemporal Model with Investment Copyright 2014 Pearson Education, Inc.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Chapter 11 A Real Intertemporal Model with Investment Copyright Chapter 11 Topics Construct a real intertemporal model that will serve as a basis for studying money and business cycles in Chapters 12-14.

Asset pricing in the frequency domain: theory and empirics

Asset pricing in the frequency domain: theory and empirics Ian Dew-Becker and Stefano Giglio Duke Fuqua and Chicago Booth 11/27/13 Dew-Becker and Giglio (Duke and Chicago) Frequency-domain asset pricing

Asset pricing in the frequency domain: theory and empirics Ian Dew-Becker and Stefano Giglio Duke Fuqua and Chicago Booth 11/27/13 Dew-Becker and Giglio (Duke and Chicago) Frequency-domain asset pricing

LECTURE 3 The Effects of Monetary Changes: Vector Autoregressions. September 7, 2016

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 3 The Effects of Monetary Changes: Vector Autoregressions September 7, 2016 I. SOME BACKGROUND ON VARS A Two-Variable VAR Suppose the true

Economics 210c/236a Fall 2016 Christina Romer David Romer LECTURE 3 The Effects of Monetary Changes: Vector Autoregressions September 7, 2016 I. SOME BACKGROUND ON VARS A Two-Variable VAR Suppose the true

Nobel Symposium 2018: Money and Banking

Nobel Symposium 2018: Money and Banking Markus K. Brunnermeier Princeton University Stockholm, May 27 th 2018 Types of Distortions Belief distortions Match belief surveys (BGS) Incomplete markets natural

Nobel Symposium 2018: Money and Banking Markus K. Brunnermeier Princeton University Stockholm, May 27 th 2018 Types of Distortions Belief distortions Match belief surveys (BGS) Incomplete markets natural

Quantitative Significance of Collateral Constraints as an Amplification Mechanism

RIETI Discussion Paper Series 09-E-05 Quantitative Significance of Collateral Constraints as an Amplification Mechanism INABA Masaru The Canon Institute for Global Studies KOBAYASHI Keiichiro RIETI The

RIETI Discussion Paper Series 09-E-05 Quantitative Significance of Collateral Constraints as an Amplification Mechanism INABA Masaru The Canon Institute for Global Studies KOBAYASHI Keiichiro RIETI The

Discussion of The Cost of Macroprudential Policy by Bjorn Richter, Moritz Schularick, Ilhyock Shim

Discussion of The Cost of Macroprudential Policy by Bjorn Richter, Moritz Schularick, Ilhyock Shim Ozge Akinci Federal Reserve Bank of New York International Symposium on Macroeconomics The views expressed

Discussion of The Cost of Macroprudential Policy by Bjorn Richter, Moritz Schularick, Ilhyock Shim Ozge Akinci Federal Reserve Bank of New York International Symposium on Macroeconomics The views expressed

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan The US recession that began in late 2007 had significant spillover effects to the rest

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan The US recession that began in late 2007 had significant spillover effects to the rest

Macroeconomics IV (14.454)

") Macroeconomics IV (14.454) Ricardo J. Caballero Spring 2018 1 Introduction 1.1 Secondary 1. Luttrell, D., T. Atkinson, and H. Rosenblum. Assessing the Costs and Consequences of the 2007-09 Financial crisis

Macroeconomics IV (14.454) Ricardo J. Caballero Spring 2018 1 Introduction 1.1 Secondary 1. Luttrell, D., T. Atkinson, and H. Rosenblum. Assessing the Costs and Consequences of the 2007-09 Financial crisis

What s Driving Deleveraging? Evidence from the Survey of Consumer Finances

What s Driving Deleveraging? Evidence from the 2007-2009 Survey of Consumer Finances Karen Dynan Brookings Institution Wendy Edelberg Congressional Budget Office These slides were prepared for a presentation

What s Driving Deleveraging? Evidence from the 2007-2009 Survey of Consumer Finances Karen Dynan Brookings Institution Wendy Edelberg Congressional Budget Office These slides were prepared for a presentation

Optimal Credit Market Policy. CEF 2018, Milan

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

A Macroeconomic Model with Financially Constrained Producers and Intermediaries

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Simon Gilchrist Boston Univerity and NBER Federal Reserve Bank of San Francisco March 31st, 2017 Overview: Model that combines

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Simon Gilchrist Boston Univerity and NBER Federal Reserve Bank of San Francisco March 31st, 2017 Overview: Model that combines

MONETARY ECONOMICS Objective: Overview of Theoretical, Empirical and Policy Issues in Modern Monetary Economics

MONETARY ECONOMICS Objective: Overview of Theoretical, Empirical and Policy Issues in Modern Monetary Economics Questions Why Did Inflation Take Off in Many Countries in the 1970s? What Should be Done

MONETARY ECONOMICS Objective: Overview of Theoretical, Empirical and Policy Issues in Modern Monetary Economics Questions Why Did Inflation Take Off in Many Countries in the 1970s? What Should be Done

The Socially Optimal Level of Capital Requirements: AViewfromTwoPapers. Javier Suarez* CEMFI. Federal Reserve Bank of Chicago, November 2012

The Socially Optimal Level of Capital Requirements: AViewfromTwoPapers Javier Suarez* CEMFI Federal Reserve Bank of Chicago, 15 16 November 2012 *Based on joint work with David Martinez-Miera (Carlos III)

The Socially Optimal Level of Capital Requirements: AViewfromTwoPapers Javier Suarez* CEMFI Federal Reserve Bank of Chicago, 15 16 November 2012 *Based on joint work with David Martinez-Miera (Carlos III)

The International Transmission of Credit Bubbles: Theory and Policy

The International Transmission of Credit Bubbles: Theory and Policy Alberto Martin and Jaume Ventura CREI, UPF and Barcelona GSE March 14, 2015 Martin and Ventura (CREI, UPF and Barcelona GSE) BIS Research

The International Transmission of Credit Bubbles: Theory and Policy Alberto Martin and Jaume Ventura CREI, UPF and Barcelona GSE March 14, 2015 Martin and Ventura (CREI, UPF and Barcelona GSE) BIS Research

Financial Ampli cation of Foreign Exchange Risk Premia 1

Financial Ampli cation of Foreign Exchange Risk Premia 1 Tobias Adrian, Erkko Etula, Jan Groen Federal Reserve Bank of New York Brussels, July 23-24, 2010 Conference on Advances in International Macroeconomics

Financial Ampli cation of Foreign Exchange Risk Premia 1 Tobias Adrian, Erkko Etula, Jan Groen Federal Reserve Bank of New York Brussels, July 23-24, 2010 Conference on Advances in International Macroeconomics

Macroeconomics of Finance

Macroeconomics of Finance Joanna Mackiewicz-Łyziak Lecture 12 Literature Borio C., 2012, The financial cycle and macroeconomics: What have we learnt?, BIS Working Papers No. 395. Business cycles Business

Macroeconomics of Finance Joanna Mackiewicz-Łyziak Lecture 12 Literature Borio C., 2012, The financial cycle and macroeconomics: What have we learnt?, BIS Working Papers No. 395. Business cycles Business

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER May 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER May 2013 He and Krishnamurthy (Chicago, Northwestern)

Discussion of Exits from Recessions by Bordo and Landon-Lane

Discussion of Exits from Recessions by Bordo and Landon-Lane Robert J. Gordon Northwestern University, NBER, and CEPR SNB Conference on Monetary Policy after the Financial Crisis, Zurich, 24 September

Discussion of Exits from Recessions by Bordo and Landon-Lane Robert J. Gordon Northwestern University, NBER, and CEPR SNB Conference on Monetary Policy after the Financial Crisis, Zurich, 24 September

Private Leverage and Sovereign Default

Private Leverage and Sovereign Default Cristina Arellano Yan Bai Luigi Bocola FRB Minneapolis University of Rochester Northwestern University Economic Policy and Financial Frictions November 2015 1 / 37

Private Leverage and Sovereign Default Cristina Arellano Yan Bai Luigi Bocola FRB Minneapolis University of Rochester Northwestern University Economic Policy and Financial Frictions November 2015 1 / 37

Operationalizing the Selection and Application of Macroprudential Instruments

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Leverage Restrictions in a Business Cycle Model. Lawrence J. Christiano Daisuke Ikeda

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Discussion of Gerali, Neri, Sessa, Signoretti. Credit and Banking in a DSGE Model

Discussion of Gerali, Neri, Sessa and Signoretti Credit and Banking in a DSGE Model Jesper Lindé Federal Reserve Board ty ECB, Frankfurt December 15, 2008 Summary of paper This interesting paper... Extends

Discussion of Gerali, Neri, Sessa and Signoretti Credit and Banking in a DSGE Model Jesper Lindé Federal Reserve Board ty ECB, Frankfurt December 15, 2008 Summary of paper This interesting paper... Extends

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Bank Debt Securities, etc. Bank Equity Balance Sheet,

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Bank Debt Securities, etc. Bank Equity Balance Sheet,