What is Cyclical in Credit Cycles?

|

|

|

- Jane Beasley

- 5 years ago

- Views:

Transcription

1 What is Cyclical in Credit Cycles? Rui Cui May 31, 2014

2 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage constraints Credit cycles are also risk cycles Cyclicality in the distribution of new credit credit quality of the marginal borrowers Modeling production heterogeneity is essential Today: A general equilibrium model with a banking sector featuring the comovement in the quantity and quality of credit

3 Credit Cycles Facts Issuer Credit Quality (Expected Default Frequency) Credit Growth (in %) (Compustat) Credit cycles are not only growth cycles, they are also risk cycles.

4 Mechanism (0) Current banking sector balance sheet determines effective discount rates Bankers are the only marginal agent on the loan market by assumption

5 Mechanism (0) Current banking sector balance sheet determines effective discount rates Bankers are the only marginal agent on the loan market by assumption (1) Bankers evaluates potential projects by computing their risk-adjusted present values Risky borrowers are more sensitive to movements in discount rates

6 Mechanism (0) Current banking sector balance sheet determines effective discount rates Bankers are the only marginal agent on the loan market by assumption (1) Bankers evaluates potential projects by computing their risk-adjusted present values Risky borrowers are more sensitive to movements in discount rates (2) Capital producers respond to fluctuating asset prices in their production decisions Asset prices movements shift the production frontier of the aggregate economy

7 Mechanism (0) Current banking sector balance sheet determines effective discount rates Bankers are the only marginal agent on the loan market by assumption (1) Bankers evaluates potential projects by computing their risk-adjusted present values Risky borrowers are more sensitive to movements in discount rates (2) Capital producers respond to fluctuating asset prices in their production decisions Asset prices movements shift the production frontier of the aggregate economy (3) Once financed, these projects stay and accumulate on banks balance sheets Fully solved general equilibrium model to extract dynamic implications

8 Results Interaction between production heterogeneity and financial frictions generates fundamental economic forces that leads to endogeneous boom-bust cycles A risks buildup process A slow recovery process Negative correlation in financial volatility and growth in real volatility New perspective on volatility paradox that typically focuses on financial volatility

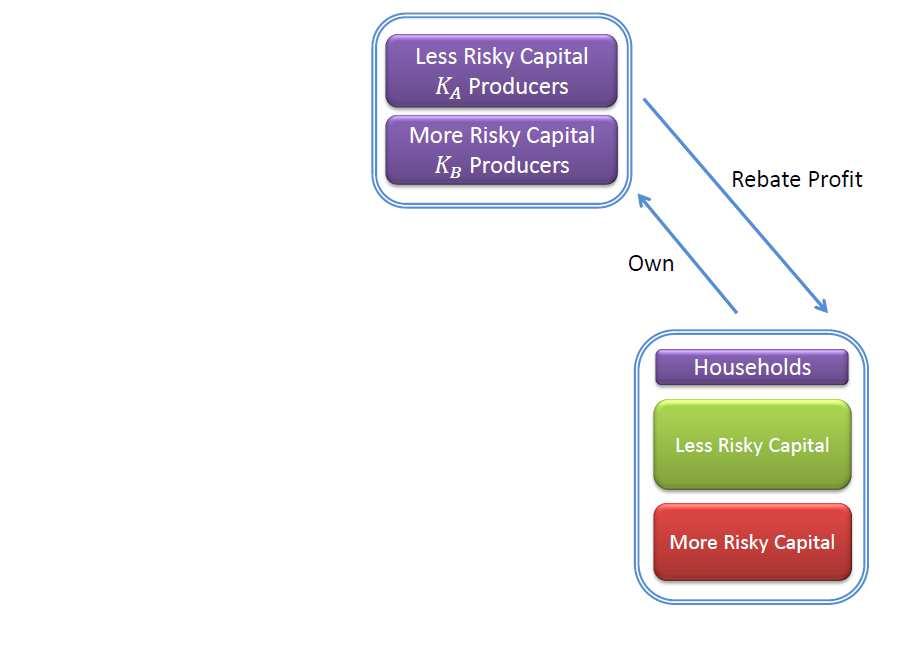

9 Set up Three types of agents: households, bankers and capital producers. Risk neutral households can consume and make deposits with bankers, they maximize [ ] E exp ( ρt) dct H 0 Bankers hold all risky capital. I impose that bankers consume λndt (N is bankers networth). They maximize E [ 0 exp ( λt) log (λn t) dt ] This is a continuous time adoption of Kiyotaki-Gertler model, but with fixed risk free rate ρ and simplified effective bankers pricing kernel θ t B = exp ( λt) λ N t.

10 Capital Producers Two types of capital producers producing K j {A,B}, both captial produces cash flow at rate AK j dt, they depreciate at rate δ. But they have differential exposure to the systematic shock, in aggregate dk j K j = (Φ j (i j ) δ) }{{} dt + σ j dz t net investment Quality is captured by σ A < σ B. Cash flow from type B projects are more sensitive to macroeconomic shocks than type A projects.

11 Capital Producers Capital producers are owned by household, but can only sell their capital to bankers. The production function of type j capital is 2i j Φ j (i j ) = κ j Key assumption: κ A > κ B. Supply of high quality projects are limited. Key endogeneous variable is the risk adjusted present value of the cash flow (net of investment) produced by type j capital [ ] q j = PV j = E A K t j 0 K j θb t dt 0 where dk j t K j 0 = δdt + σ j dz t

12 Frictionless Benchmark

13 Model Schmetic

14 Capital Producers Problem Given q A, q B, capital producers solve a static problem max ij Φ j (i j ) K j q j i j K j Optimal investment follows Φ j ( i j ) = q j κ j

15 Bankers Problem Given their preference, bankers solves a portfolio problem that resembles standard mean-variance efficient investors max αa,α B E [ 0 exp ( λt) log (λn t) dt ] st. dn t N t = λdt + (α A π A + α B π B + (1 α A α B ) r f ) dt + (α A σ A + α B σ B ) dz t where α A, α B are portfolio shares, π A, π B are excess returns by investing in K A, K B ; σ A, σ B are return volatilities for K A, K B

16 Equilibrium Definition An equilibrium of this economy consists of prices processes (q A, q B, r f ), and decisions, (c H, α A, α B, i A, i B ), such that 1. Given prices, households, bankers and capital producers solve their optimization problems. 2. Given decisions, markets for risky capital (K A, K B ) and risk-free bond clears. This pins down bankers portfolio choices α A, α B 3. Market for goods clear A (K A + K B ) = i A K A + i B K B + C H

17 Solving the Model 1. Conjecture the model has two scaled state variables: size and quality of intermediaries balance sheet η = s = N q A K A + q B K B K B K A + K B 2. Write down a system of PDEs that q A and q B must satisfy as functions of η and s 3. Above equations solved on [η, s] [ɛ, 1 ɛ] [0, 1]. Boundary conditions 3.1 s = 0, 1 Single technology economy, solved in ODE 3.2 η = ɛ, impose q j η = η = 1 ɛ, reduce to a system of lower order equations 4. Numerically, I use projection method (5-7th order Chebshev polynomials) to minimize PDE error over a grid.

18 Parameters Model Parameters Interpretation Full Model Simple Model Justification ρ Household Time Discount Rate Risk Free Rate λ Bankers Time Discount Rate Unconditional Mome σ A Cash Flow Volatility of K A 0.02 σ B Cash Flow Volatility of K B Output Volatility κ A Adjustment Cost of K A κ B Adjustment Cost of K B Investment Volatilit A Productivity Investment-Capital R δ Depreciation Literature Full Model: Heterogeneous Production. Simple Model: Homogeneous Production.

19 Model Solution Figure: Solid blue line corresponds to the solution for median s. Shaded area plots the solution corresponding to 25% 75% distribution of s. Median output volatility= 0.046, top to bottom quartile of the distribution of output volatility is [0.025, 0.071].

20 Model Solution Figure: Solid blue line corresponds to the solution for median s. Shaded area plots the solution corresponding to 25% 75% distribution of s. Median output volatility= 0.046, top to bottom quartile of the distribution of output volatility is [0.025, 0.071].

21 Unconditional Moments Moment Interpretation Full Model Simple Model Data σ Y Median Output Volatility(%) σ A Return Volatility of K A(%) 5.11 σ B Return Volatility of K B (%) SR Sharpe Ratio µ c Consumption Growth(%) σ c Consumption Growth Volatility(%) σ Φ ( ia ) Investment Volatility of K A(%) 3.70 σ Φ ( ib ) Investment Volatility of K B (%) i A Investment / Captial Ratio for K A (%) 10.9 i B Investment / Capital Ratio for K B (%) Full Model: Heterogeneous production. Simple Model: Homogeneous production.

22 Conditional Implications Risks Buildup Without production heterogeneity, positive shocks always push the economy away from crisis state Therefore, well captialized banks (higher η) are associated with lower risks of entering a crisis In my framework, well capitalized banks have strong incentive to take on additional risks this will show up in the term structure of crisis probability

23 Conditional Implications Risks Buildup Without production heterogeneity, positive shocks always push the economy away from crisis state Therefore, well captialized banks (higher η) are associated with lower risks of entering a crisis In my framework, well capitalized banks have strong incentive to take on additional risks this will show up in the term structure of crisis probability Slow Recovery In the model, bank equity grows by earning this risk premium associated with its asset Risk premium is higher in crisis state, so return on equity is high recovery is fast When risk taking is endogeous, banks substitute risky, high-yield projects with safe, low-yield ones return on equity in crisis

24 Conditional Implications Risks Buildup Without production heterogeneity, positive shocks always push the economy away from crisis state Therefore, well captialized banks (higher η) are associated with lower risks of entering a crisis In my framework, well capitalized banks have strong incentive to take on additional risks this will show up in the term structure of crisis probability Slow Recovery In the model, bank equity grows by earning this risk premium associated with its asset Risk premium is higher in crisis state, so return on equity is high recovery is fast When risk taking is endogeous, banks substitute risky, high-yield projects with safe, low-yield ones return on equity in crisis

25 Risks Buildup Bottom s quartile Φ(i b )/Φ(i a ) 1 s Median s Top s quartile η η Figure: Left Panel: Investment Ratio as a function of η and s. Right Panel: Drifts of the state variable when starting from η = 0.6 and median s.

26 Risks Buildup Bottom s quartile Φ(i b )/Φ(i a ) 1 s Median s Top s quartile η η Figure: Left Panel: Investment Ratio as a function of η and s. Right Panel: Drifts of the state variable when starting from η = 0.6 and median s.

27 Risks Buildup Distress Probability Distress Probability Top s quartile Median s Bottom s quartile Horizon (yrs) Horizon (yrs) Figure: Left Panel: Homogeneous Production. Right Panel: Heterogeneous Production. I plot the conditional probability of hitting the top 25% of the Sharpe Ratio when starting from η = 0.6.

28 Risks Buildup Distress Probability Distress Probability Top s quartile Median s Bottom s quartile Horizon (yrs) Horizon (yrs) Figure: Left Panel: Homogeneous Production. Right Panel: Heterogeneous Production. I plot the conditional probability of hitting the top 25% of the Sharpe Ratio when starting from η = 0.6.

29 Recovery Dynamics Bottom s quartile 0.7 Φ(i b )/Φ(i a ) 1 Median s s Top s quartile η η Figure: Left Panel: Investment Ratio as a function of η and s. Right Panel: Drifts of the state variable when starting from η = 0.2 and median s.

30 Recovery Dynamics Φ(i b )/Φ(i a ) 1 Bottom s quartile Median s s Top s quartile η η Figure: Left Panel: Investment Ratio as a function of η and s. Right Panel: Drifts of the state variable when starting from η = 0.2 and median s.

31 Recovery Dynamics Bottom s quartile Distress Probability Distress Probability Median s Top s quartile Horizon (yrs) Horizon (yrs) Figure: Left Panel: Homogeneous Production. Right Panel: Heterogeneous Production. I plot the conditional probability of staying in the top 25% of the Sharpe Ratio when starting from η = 0.2.

32 Recovery Dynamics Bottom s quartile Distress Probability Distress Probability Median s Top s quartile Horizon (yrs) Horizon (yrs) Figure: Left Panel: Homogeneous Production. Right Panel: Heterogeneous Production. I plot the conditional probability of staying in the top 25% of the Sharpe Ratio when starting from η = 0.2.

33 Volatility Paradox No concensus has emerged to define volatility paradox generally refers to the observation that prolonged period of low volatility tends to precede a crisis Brunnermeier Sannikov (2013) : compare a series of models differing in their fundamental volatility, banks in low-volatility economies take on more leverage Adrian Boyarchenko (2013): banks run by VaR role, lower financial volatility corresponds to higher leverage Shorter distance to restructuring boundary

34 Volatility Paradox No concensus has emerged to define volatility paradox generally refers to the observation that prolonged period of low volatility tends to precede a crisis Brunnermeier Sannikov (2013) : compare a series of models differing in their fundamental volatility, banks in low-volatility economies take on more leverage Adrian Boyarchenko (2013): banks run by VaR role, lower financial volatility corresponds to higher leverage Shorter distance to restructuring boundary My model endogenize both fundamenal and financial volatilities Low financial volatility symptomatic of lower risk prices Riskier projects come into the money and get financed Negative correlation between financial volatility and growth in fundamental volatility Accumulation of riskier project tend to coincide with a period of low financial volatility and pushes economy closer to a crisis

35 Volatility Paradox Real Volatility Growth(in %) Real Volatility Growth (in %) Financial Volatility(in %) Financial Volatility (in %) Figure: Left Panel: Homogeneous Production. Right Panel: Heterogeneous Production. Simulated 200 years.

36 Conclusion Financial sector s optimal financing decision determined the production mix in the real economy Credit quality of the marginal borrowers vary systematically over the credit cycles. A model to keep track of both asset and liability side of the financial sector. Extract model s conditional implications from the term structure of distress probabilities.

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER May 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER May 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

A Macroeconomic Framework for Quantifying Systemic Risk. June 2012

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER March 215 He and Krishnamurthy (Chicago, Stanford) Systemic

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER March 215 He and Krishnamurthy (Chicago, Stanford) Systemic

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER November 2012 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER November 2012 He and Krishnamurthy (Chicago, Northwestern)

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

The Macroeconomics of Shadow Banking. January, 2016

The Macroeconomics of Shadow Banking Alan Moreira Yale SOM Alexi Savov NYU Stern & NBER January, 21 Shadow banking, what is it good for? Three views: 1. Regulatory arbitrage - avoid capital requirements,

The Macroeconomics of Shadow Banking Alan Moreira Yale SOM Alexi Savov NYU Stern & NBER January, 21 Shadow banking, what is it good for? Three views: 1. Regulatory arbitrage - avoid capital requirements,

Uncertainty, Liquidity and Financial Cycles

Uncertainty, Liquidity and Financial Cycles Ge Zhou Zhejiang University Jan 2019, ASSA Ge Zhou (Zhejiang University) Uncertainty, Liquidity and Financial Cycles Jan 2019 1 / 26 2500.00 Recession SP 500

Uncertainty, Liquidity and Financial Cycles Ge Zhou Zhejiang University Jan 2019, ASSA Ge Zhou (Zhejiang University) Uncertainty, Liquidity and Financial Cycles Jan 2019 1 / 26 2500.00 Recession SP 500

Online Appendix for The Macroeconomics of Shadow Banking

Online Appendix for The Macroeconomics of Shadow Banking Alan Moreira Alexi Savov April 29, 2 Abstract This document contains additional results for the paper The Macroeconomics of Shadow Banking. These

Online Appendix for The Macroeconomics of Shadow Banking Alan Moreira Alexi Savov April 29, 2 Abstract This document contains additional results for the paper The Macroeconomics of Shadow Banking. These

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 INCOMPLETE REFERENCES. REPORTED NUMBERS MAY CHANGE. Abstract Systemic risk arises when

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 INCOMPLETE REFERENCES. REPORTED NUMBERS MAY CHANGE. Abstract Systemic risk arises when

Liquidity Policies and Systemic Risk Tobias Adrian and Nina Boyarchenko

Policies and Systemic Risk Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New York or of the Federal

Policies and Systemic Risk Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New York or of the Federal

Household Debt, Financial Intermediation, and Monetary Policy

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 This Draft: January 26, 2012 INCOMPLETE REFERENCES. REPORTED NUMBERS MAY CHANGE. Abstract

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 This Draft: January 26, 2012 INCOMPLETE REFERENCES. REPORTED NUMBERS MAY CHANGE. Abstract

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

Capital Flows, Financial Intermediation and Macroprudential Policies

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Arbitrageurs, bubbles and credit conditions

Arbitrageurs, bubbles and credit conditions Julien Hugonnier (SFI @ EPFL) and Rodolfo Prieto (BU) 8th Cowles Conference on General Equilibrium and its Applications April 28, 212 Motivation Loewenstein

Arbitrageurs, bubbles and credit conditions Julien Hugonnier (SFI @ EPFL) and Rodolfo Prieto (BU) 8th Cowles Conference on General Equilibrium and its Applications April 28, 212 Motivation Loewenstein

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 September 218 1 The views expressed in this paper are those of the

International Monetary Theory: Mundell Fleming Redux

International Monetary Theory: Mundell Fleming Redux by Markus K. Brunnermeier and Yuliy Sannikov Princeton and Stanford University Princeton Initiative Princeton, Sept. 9 th, 2017 Motivation Global currency

International Monetary Theory: Mundell Fleming Redux by Markus K. Brunnermeier and Yuliy Sannikov Princeton and Stanford University Princeton Initiative Princeton, Sept. 9 th, 2017 Motivation Global currency

Lecture notes on risk management, public policy, and the financial system Credit risk models

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: June 8, 2018 2 / 24 Outline 3/24 Credit risk metrics and models

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: June 8, 2018 2 / 24 Outline 3/24 Credit risk metrics and models

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk

Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk") Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

The Macroeconomics of Shadow Banking. February, 2016

The Macroeconomics of Shadow Banking Alan Moreira Yale SOM Alexi Savov NYU Stern & NBER February, 21 Shadow banking, what is it good for? Three views: 1. Regulatory arbitrage - avoid capital requirements,

The Macroeconomics of Shadow Banking Alan Moreira Yale SOM Alexi Savov NYU Stern & NBER February, 21 Shadow banking, what is it good for? Three views: 1. Regulatory arbitrage - avoid capital requirements,

Capital Requirements, Risk Choice, and Liquidity Provision in a Business Cycle Model

Capital Requirements, Risk Choice, and Liquidity Provision in a Business Cycle Model Juliane Begenau Harvard Business School July 11, 2015 1 Motivation How to regulate banks? Capital requirement: min equity/

Capital Requirements, Risk Choice, and Liquidity Provision in a Business Cycle Model Juliane Begenau Harvard Business School July 11, 2015 1 Motivation How to regulate banks? Capital requirement: min equity/

Taxing Firms Facing Financial Frictions

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Credit Booms, Financial Crises and Macroprudential Policy

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Delayed Capital Reallocation

Delayed Capital Reallocation Wei Cui University College London Introduction Motivation Less restructuring in recessions (1) Capital reallocation is sizeable (2) Capital stock reallocation across firms

Delayed Capital Reallocation Wei Cui University College London Introduction Motivation Less restructuring in recessions (1) Capital reallocation is sizeable (2) Capital stock reallocation across firms

ECON 815. A Basic New Keynesian Model II

ECON 815 A Basic New Keynesian Model II Winter 2015 Queen s University ECON 815 1 Unemployment vs. Inflation 12 10 Unemployment 8 6 4 2 0 1 1.5 2 2.5 3 3.5 4 4.5 5 Core Inflation 14 12 10 Unemployment

ECON 815 A Basic New Keynesian Model II Winter 2015 Queen s University ECON 815 1 Unemployment vs. Inflation 12 10 Unemployment 8 6 4 2 0 1 1.5 2 2.5 3 3.5 4 4.5 5 Core Inflation 14 12 10 Unemployment

How Costly is External Financing? Evidence from a Structural Estimation. Christopher Hennessy and Toni Whited March 2006

How Costly is External Financing? Evidence from a Structural Estimation Christopher Hennessy and Toni Whited March 2006 The Effects of Costly External Finance on Investment Still, after all of these years,

How Costly is External Financing? Evidence from a Structural Estimation Christopher Hennessy and Toni Whited March 2006 The Effects of Costly External Finance on Investment Still, after all of these years,

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory. November 7, 2014

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ali Shourideh Wharton Ariel Zetlin-Jones CMU - Tepper November 7, 2014 Introduction Question: How

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ali Shourideh Wharton Ariel Zetlin-Jones CMU - Tepper November 7, 2014 Introduction Question: How

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 This Draft: November 1, 2012 Abstract Systemic risk arises when shocks lead to states

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 This Draft: November 1, 2012 Abstract Systemic risk arises when shocks lead to states

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 This Draft: October 2, 2012 Abstract Systemic risk arises when shocks lead to states

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 This Draft: October 2, 2012 Abstract Systemic risk arises when shocks lead to states

Macro, Money and Finance: A Continuous Time Approach

Macro, Money and Finance: A Continuous Time Approach Markus K. Brunnermeier & Yuliy Sannikov Princeton University International Credit Flows, Trinity of Stability Conference Princeton, Nov. 6 th, 2015

Macro, Money and Finance: A Continuous Time Approach Markus K. Brunnermeier & Yuliy Sannikov Princeton University International Credit Flows, Trinity of Stability Conference Princeton, Nov. 6 th, 2015

TopQuants. Integration of Credit Risk and Interest Rate Risk in the Banking Book

TopQuants Integration of Credit Risk and Interest Rate Risk in the Banking Book 1 Table of Contents 1. Introduction 2. Proposed Case 3. Quantifying Our Case 4. Aggregated Approach 5. Integrated Approach

TopQuants Integration of Credit Risk and Interest Rate Risk in the Banking Book 1 Table of Contents 1. Introduction 2. Proposed Case 3. Quantifying Our Case 4. Aggregated Approach 5. Integrated Approach

The I Theory of Money

The I Theory of Money Markus K. Brunnermeier & Yuliy Sannikov Princeton University CSEF-IGIER Symposium Capri, June 24 th, 2015 Motivation Framework to study monetary and financial stability Interaction

The I Theory of Money Markus K. Brunnermeier & Yuliy Sannikov Princeton University CSEF-IGIER Symposium Capri, June 24 th, 2015 Motivation Framework to study monetary and financial stability Interaction

Safe Assets. The I Theory of Money. with Valentin Haddad. - Money & Banking with Asset Pricing Tools - with Yuliy Sannikov. Princeton University

Safe ssets with Valentin Haddad The I Theory of Money - Money & Banking with sset Pricing Tools - with Yuliy Sannikov Princeton University World Finance Conference New York City, July 30 th, 2016 Definitions

Safe ssets with Valentin Haddad The I Theory of Money - Money & Banking with sset Pricing Tools - with Yuliy Sannikov Princeton University World Finance Conference New York City, July 30 th, 2016 Definitions

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 2, 211 This Draft: May 31, 212 Abstract Systemic risk arises when shocks lead to states where

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 2, 211 This Draft: May 31, 212 Abstract Systemic risk arises when shocks lead to states where

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Bank Capital, Agency Costs, and Monetary Policy. Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Macroprudential Policies in a Low Interest-Rate Environment

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

A Macroeconomic Model with Financially Constrained Producers and Intermediaries

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Simon Gilchrist Boston Univerity and NBER Federal Reserve Bank of San Francisco March 31st, 2017 Overview: Model that combines

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Simon Gilchrist Boston Univerity and NBER Federal Reserve Bank of San Francisco March 31st, 2017 Overview: Model that combines

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

A Model of Financial Intermediation

A Model of Financial Intermediation Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) A Model of Financial Intermediation December 25, 2012 1 / 43

A Model of Financial Intermediation Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) A Model of Financial Intermediation December 25, 2012 1 / 43

Financial Intermediation and Capital Reallocation

Financial Intermediation and Capital Reallocation Hengjie Ai, Kai Li, and Fang Yang November 16, 2014 Abstract We develop a general equilibrium framework to quantify the importance of intermediated capital

Financial Intermediation and Capital Reallocation Hengjie Ai, Kai Li, and Fang Yang November 16, 2014 Abstract We develop a general equilibrium framework to quantify the importance of intermediated capital

The Real Business Cycle Model

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

Financial Amplification, Regulation and Long-term Lending

Financial Amplification, Regulation and Long-term Lending Michael Reiter 1 Leopold Zessner 2 1 Instiute for Advances Studies, Vienna 2 Vienna Graduate School of Economics Barcelona GSE Summer Forum ADEMU,

Financial Amplification, Regulation and Long-term Lending Michael Reiter 1 Leopold Zessner 2 1 Instiute for Advances Studies, Vienna 2 Vienna Graduate School of Economics Barcelona GSE Summer Forum ADEMU,

Country Spreads as Credit Constraints in Emerging Economy Business Cycles

Conférence organisée par la Chaire des Amériques et le Centre d Economie de la Sorbonne, Université Paris I Country Spreads as Credit Constraints in Emerging Economy Business Cycles Sarquis J. B. Sarquis

Conférence organisée par la Chaire des Amériques et le Centre d Economie de la Sorbonne, Université Paris I Country Spreads as Credit Constraints in Emerging Economy Business Cycles Sarquis J. B. Sarquis

2.4 Industrial implementation: KMV model. Expected default frequency

2.4 Industrial implementation: KMV model Expected default frequency Expected default frequency (EDF) is a forward-looking measure of actual probability of default. EDF is firm specific. KMV model is based

2.4 Industrial implementation: KMV model Expected default frequency Expected default frequency (EDF) is a forward-looking measure of actual probability of default. EDF is firm specific. KMV model is based

Disagreement, Speculation, and Aggregate Investment

Disagreement, Speculation, and Aggregate Investment Steven D. Baker Burton Hollifield Emilio Osambela October 19, 213 We thank Elena N. Asparouhova, Tony Berrada, Jaroslav Borovička, Peter Bossaerts, David

Disagreement, Speculation, and Aggregate Investment Steven D. Baker Burton Hollifield Emilio Osambela October 19, 213 We thank Elena N. Asparouhova, Tony Berrada, Jaroslav Borovička, Peter Bossaerts, David

Financial Regulation in a Quantitative Model of the Modern Banking System

Financial Regulation in a Quantitative Model of the Modern Banking System Juliane Begenau HBS Tim Landvoigt UT Austin CITE August 14, 2015 1 Flow of Funds: total nancial assets 22 20 18 16 $ Trillion 14

Financial Regulation in a Quantitative Model of the Modern Banking System Juliane Begenau HBS Tim Landvoigt UT Austin CITE August 14, 2015 1 Flow of Funds: total nancial assets 22 20 18 16 $ Trillion 14

Comparing Different Regulatory Measures to Control Stock Market Volatility: A General Equilibrium Analysis

Comparing Different Regulatory Measures to Control Stock Market Volatility: A General Equilibrium Analysis A. Buss B. Dumas R. Uppal G. Vilkov INSEAD INSEAD, CEPR, NBER Edhec, CEPR Goethe U. Frankfurt

Comparing Different Regulatory Measures to Control Stock Market Volatility: A General Equilibrium Analysis A. Buss B. Dumas R. Uppal G. Vilkov INSEAD INSEAD, CEPR, NBER Edhec, CEPR Goethe U. Frankfurt

1 Dynamic programming

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

Bernanke and Gertler [1989]

![Bernanke and Gertler [1989]](/thumbs/90/103712154.jpg "Bernanke and Gertler [1989]") Bernanke and Gertler [1989] Econ 235, Spring 2013 1 Background: Townsend [1979] An entrepreneur requires x to produce output y f with Ey > x but does not have money, so he needs a lender Once y is realized,

Bernanke and Gertler [1989] Econ 235, Spring 2013 1 Background: Townsend [1979] An entrepreneur requires x to produce output y f with Ey > x but does not have money, so he needs a lender Once y is realized,

Consumption and Portfolio Decisions When Expected Returns A

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Imperfect Information and Market Segmentation Walsh Chapter 5

Imperfect Information and Market Segmentation Walsh Chapter 5 1 Why Does Money Have Real Effects? Add market imperfections to eliminate short-run neutrality of money Imperfect information keeps price from

Imperfect Information and Market Segmentation Walsh Chapter 5 1 Why Does Money Have Real Effects? Add market imperfections to eliminate short-run neutrality of money Imperfect information keeps price from

Overborrowing, Financial Crises and Macro-prudential Policy. Macro Financial Modelling Meeting, Chicago May 2-3, 2013

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Lecture Notes. Petrosky-Nadeau, Zhang, and Kuehn (2015, Endogenous Disasters) Lu Zhang 1. BUSFIN 8210 The Ohio State University

Lu Zhang 1. BUSFIN 8210 The Ohio State University") Lecture Notes Petrosky-Nadeau, Zhang, and Kuehn (2015, Endogenous Disasters) Lu Zhang 1 1 The Ohio State University BUSFIN 8210 The Ohio State University Insight The textbook Diamond-Mortensen-Pissarides

Lecture Notes Petrosky-Nadeau, Zhang, and Kuehn (2015, Endogenous Disasters) Lu Zhang 1 1 The Ohio State University BUSFIN 8210 The Ohio State University Insight The textbook Diamond-Mortensen-Pissarides

Intermediary Asset Pricing

Intermediary Asset Pricing Z. He and A. Krishnamurthy - AER (2012) Presented by Omar Rachedi 18 September 2013 Introduction Motivation How to account for risk premia? Standard models assume households

Intermediary Asset Pricing Z. He and A. Krishnamurthy - AER (2012) Presented by Omar Rachedi 18 September 2013 Introduction Motivation How to account for risk premia? Standard models assume households

Lecture 23 The New Keynesian Model Labor Flows and Unemployment. Noah Williams

Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702 Basic New Keynesian Model of Transmission Can be derived from primitives:

Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702 Basic New Keynesian Model of Transmission Can be derived from primitives:

Introduction Model Results Conclusion Discussion. The Value Premium. Zhang, JF 2005 Presented by: Rustom Irani, NYU Stern.

, JF 2005 Presented by: Rustom Irani, NYU Stern November 13, 2009 Outline 1 Motivation Production-Based Asset Pricing Framework 2 Assumptions Firm s Problem Equilibrium 3 Main Findings Mechanism Testable

, JF 2005 Presented by: Rustom Irani, NYU Stern November 13, 2009 Outline 1 Motivation Production-Based Asset Pricing Framework 2 Assumptions Firm s Problem Equilibrium 3 Main Findings Mechanism Testable

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

Leverage Restrictions in a Business Cycle Model. March 13-14, 2015, Macro Financial Modeling, NYU Stern.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Comprehensive Exam. August 19, 2013

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Default Risk and Aggregate Fluctuations in an Economy with Production Heterogeneity

Default Risk and Aggregate Fluctuations in an Economy with Production Heterogeneity Aubhik Khan The Ohio State University Tatsuro Senga The Ohio State University and Bank of Japan Julia K. Thomas The Ohio

Default Risk and Aggregate Fluctuations in an Economy with Production Heterogeneity Aubhik Khan The Ohio State University Tatsuro Senga The Ohio State University and Bank of Japan Julia K. Thomas The Ohio

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Preliminary Examination: Macroeconomics Fall, 2009

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Fall, 2009 Instructions: Read the questions carefully and make sure to show your work. You

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Fall, 2009 Instructions: Read the questions carefully and make sure to show your work. You

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen June 15, 2012 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations June 15, 2012 1 / 59 Introduction We construct

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen June 15, 2012 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations June 15, 2012 1 / 59 Introduction We construct

A Policy Model for Analyzing Macroprudential and Monetary Policies

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

Concerted Efforts? Monetary Policy and Macro-Prudential Tools

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Rokos Capital 20 th Central Bank Macroeconomic Modeling

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Rokos Capital 20 th Central Bank Macroeconomic Modeling

International Credit Flows, and Pecuniary Externalities. Princeton Initiative Princeton University. Brunnermeier & Sannikov

International Credit Flows and Pecuniary Externalities Markus K. Brunnermeier & Princeton University International Credit Flows, Yuliy Sannikov Princeton Initiative 2017 Princeton, NJ, Sept. 9 th, 2017

International Credit Flows and Pecuniary Externalities Markus K. Brunnermeier & Princeton University International Credit Flows, Yuliy Sannikov Princeton Initiative 2017 Princeton, NJ, Sept. 9 th, 2017

Earnings Dynamics, Mobility Costs and Transmission of Firm and Market Level Shocks

Earnings Dynamics, Mobility Costs and Transmission of Firm and Market Level Shocks Preliminary and Incomplete Thibaut Lamadon Magne Mogstad Bradley Setzler U Chicago U Chicago U Chicago Statistics Norway

Earnings Dynamics, Mobility Costs and Transmission of Firm and Market Level Shocks Preliminary and Incomplete Thibaut Lamadon Magne Mogstad Bradley Setzler U Chicago U Chicago U Chicago Statistics Norway

Bank Capital Requirements: A Quantitative Analysis

Bank Capital Requirements: A Quantitative Analysis Thiên T. Nguyễn Introduction Motivation Motivation Key regulatory reform: Bank capital requirements 1 Introduction Motivation Motivation Key regulatory

Bank Capital Requirements: A Quantitative Analysis Thiên T. Nguyễn Introduction Motivation Motivation Key regulatory reform: Bank capital requirements 1 Introduction Motivation Motivation Key regulatory

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 This Draft: June 2, 2014 Abstract Systemic risk arises when shocks lead to states where

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy First Draft: November 20, 2011 This Draft: June 2, 2014 Abstract Systemic risk arises when shocks lead to states where

GT CREST-LMA. Pricing-to-Market, Trade Costs, and International Relative Prices

: Pricing-to-Market, Trade Costs, and International Relative Prices (2008, AER) December 5 th, 2008 Empirical motivation US PPI-based RER is highly volatile Under PPP, this should induce a high volatility

: Pricing-to-Market, Trade Costs, and International Relative Prices (2008, AER) December 5 th, 2008 Empirical motivation US PPI-based RER is highly volatile Under PPP, this should induce a high volatility

Balance Sheet Recessions

Balance Sheet Recessions Zhen Huo and José-Víctor Ríos-Rull University of Minnesota Federal Reserve Bank of Minneapolis CAERP CEPR NBER Conference on Money Credit and Financial Frictions Huo & Ríos-Rull

Balance Sheet Recessions Zhen Huo and José-Víctor Ríos-Rull University of Minnesota Federal Reserve Bank of Minneapolis CAERP CEPR NBER Conference on Money Credit and Financial Frictions Huo & Ríos-Rull

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations?

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations? Bernard Dumas INSEAD, Wharton, CEPR, NBER Alexander Kurshev London Business School Raman Uppal London Business School,

What Can Rational Investors Do About Excessive Volatility and Sentiment Fluctuations? Bernard Dumas INSEAD, Wharton, CEPR, NBER Alexander Kurshev London Business School Raman Uppal London Business School,

Global Pricing of Risk and Stabilization Policies

Global Pricing of Risk and Stabilization Policies Tobias Adrian Daniel Stackman Erik Vogt Federal Reserve Bank of New York The views expressed here are the authors and are not necessarily representative

Global Pricing of Risk and Stabilization Policies Tobias Adrian Daniel Stackman Erik Vogt Federal Reserve Bank of New York The views expressed here are the authors and are not necessarily representative

2. Preceded (followed) by expansions (contractions) in domestic. 3. Capital, labor account for small fraction of output drop,

by expansions (contractions) in domestic. 3. Capital, labor account for small fraction of output drop,") Mendoza (AER) Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital,

Mendoza (AER) Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital,

Foreign Competition and Banking Industry Dynamics: An Application to Mexico

Foreign Competition and Banking Industry Dynamics: An Application to Mexico Dean Corbae Pablo D Erasmo 1 Univ. of Wisconsin FRB Philadelphia June 12, 2014 1 The views expressed here do not necessarily

Foreign Competition and Banking Industry Dynamics: An Application to Mexico Dean Corbae Pablo D Erasmo 1 Univ. of Wisconsin FRB Philadelphia June 12, 2014 1 The views expressed here do not necessarily

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

Microeconomic Foundations of Incomplete Price Adjustment

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Collateralized capital and news-driven cycles. Abstract

Collateralized capital and news-driven cycles Keiichiro Kobayashi Research Institute of Economy, Trade, and Industry Kengo Nutahara Graduate School of Economics, University of Tokyo, and the JSPS Research

Collateralized capital and news-driven cycles Keiichiro Kobayashi Research Institute of Economy, Trade, and Industry Kengo Nutahara Graduate School of Economics, University of Tokyo, and the JSPS Research

Capital Structure with Endogenous Liquidation Values

1/22 Capital Structure with Endogenous Liquidation Values Antonio Bernardo and Ivo Welch UCLA Anderson School of Management September 2014 Introduction 2/22 Liquidation values are an important determinant

1/22 Capital Structure with Endogenous Liquidation Values Antonio Bernardo and Ivo Welch UCLA Anderson School of Management September 2014 Introduction 2/22 Liquidation values are an important determinant

TFP Persistence and Monetary Policy. NBS, April 27, / 44

TFP Persistence and Monetary Policy Roberto Pancrazi Toulouse School of Economics Marija Vukotić Banque de France NBS, April 27, 2012 NBS, April 27, 2012 1 / 44 Motivation 1 Well Known Facts about the

TFP Persistence and Monetary Policy Roberto Pancrazi Toulouse School of Economics Marija Vukotić Banque de France NBS, April 27, 2012 NBS, April 27, 2012 1 / 44 Motivation 1 Well Known Facts about the

A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite)

") A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite) Edward Kung UCLA March 1, 2013 OBJECTIVES The goal of this paper is to assess the potential impact of introducing alternative

A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite) Edward Kung UCLA March 1, 2013 OBJECTIVES The goal of this paper is to assess the potential impact of introducing alternative

Monetary Economics. Financial Markets and the Business Cycle: The Bernanke and Gertler Model. Nicola Viegi. September 2010

Monetary Economics Financial Markets and the Business Cycle: The Bernanke and Gertler Model Nicola Viegi September 2010 Monetary Economics () Lecture 7 September 2010 1 / 35 Introduction Conventional Model

Monetary Economics Financial Markets and the Business Cycle: The Bernanke and Gertler Model Nicola Viegi September 2010 Monetary Economics () Lecture 7 September 2010 1 / 35 Introduction Conventional Model

Comment on: Capital Controls and Monetary Policy Autonomy in a Small Open Economy by J. Scott Davis and Ignacio Presno

Comment on: Capital Controls and Monetary Policy Autonomy in a Small Open Economy by J. Scott Davis and Ignacio Presno Fabrizio Perri Federal Reserve Bank of Minneapolis and CEPR fperri@umn.edu December

Comment on: Capital Controls and Monetary Policy Autonomy in a Small Open Economy by J. Scott Davis and Ignacio Presno Fabrizio Perri Federal Reserve Bank of Minneapolis and CEPR fperri@umn.edu December

The Role of the Net Worth of Banks in the Propagation of Shocks

The Role of the Net Worth of Banks in the Propagation of Shocks Preliminary Césaire Meh Department of Monetary and Financial Analysis Bank of Canada Kevin Moran Université Laval The Role of the Net Worth

The Role of the Net Worth of Banks in the Propagation of Shocks Preliminary Césaire Meh Department of Monetary and Financial Analysis Bank of Canada Kevin Moran Université Laval The Role of the Net Worth

The Extensive Margin of Trade and Monetary Policy

The Extensive Margin of Trade and Monetary Policy Yuko Imura Bank of Canada Malik Shukayev University of Alberta June 2, 216 The views expressed in this presentation are our own, and do not represent those

The Extensive Margin of Trade and Monetary Policy Yuko Imura Bank of Canada Malik Shukayev University of Alberta June 2, 216 The views expressed in this presentation are our own, and do not represent those

Chapter 9 Dynamic Models of Investment

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

Volatility Risk Pass-Through

Volatility Risk Pass-Through Ric Colacito Max Croce Yang Liu Ivan Shaliastovich 1 / 18 Main Question Uncertainty in a one-country setting: Sizeable impact of volatility risks on growth and asset prices

Volatility Risk Pass-Through Ric Colacito Max Croce Yang Liu Ivan Shaliastovich 1 / 18 Main Question Uncertainty in a one-country setting: Sizeable impact of volatility risks on growth and asset prices

Technology shocks and Monetary Policy: Assessing the Fed s performance

Technology shocks and Monetary Policy: Assessing the Fed s performance (J.Gali et al., JME 2003) Miguel Angel Alcobendas, Laura Desplans, Dong Hee Joe March 5, 2010 M.A.Alcobendas, L. Desplans, D.H.Joe

Technology shocks and Monetary Policy: Assessing the Fed s performance (J.Gali et al., JME 2003) Miguel Angel Alcobendas, Laura Desplans, Dong Hee Joe March 5, 2010 M.A.Alcobendas, L. Desplans, D.H.Joe

Credit Frictions and Optimal Monetary Policy

Credit Frictions and Optimal Monetary Policy Vasco Cúrdia FRB New York Michael Woodford Columbia University Conference on Monetary Policy and Financial Frictions Cúrdia and Woodford () Credit Frictions

Credit Frictions and Optimal Monetary Policy Vasco Cúrdia FRB New York Michael Woodford Columbia University Conference on Monetary Policy and Financial Frictions Cúrdia and Woodford () Credit Frictions

Inflation Dynamics During the Financial Crisis

Inflation Dynamics During the Financial Crisis S. Gilchrist 1 1 Boston University and NBER MFM Summer Camp June 12, 2016 DISCLAIMER: The views expressed are solely the responsibility of the authors and

Inflation Dynamics During the Financial Crisis S. Gilchrist 1 1 Boston University and NBER MFM Summer Camp June 12, 2016 DISCLAIMER: The views expressed are solely the responsibility of the authors and

ECON 4325 Monetary Policy and Business Fluctuations

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research