Macroeconomics of Finance

|

|

|

- Briana Lucas

- 6 years ago

- Views:

Transcription

1 Macroeconomics of Finance Joanna Mackiewicz-Łyziak Lecture 12

2 Literature Borio C., 2012, The financial cycle and macroeconomics: What have we learnt?, BIS Working Papers No. 395.

3 Business cycles Business cycles are fluctuations in economic activity, defined in terms of expansion or recession. A recession is a period between a peak and a through, and an expansion is a period between a through and a peak. (NBER) During a recession, a significant decline in economic activity spreads across the economy and can last from a few months to more than a year. During an expansion, economic activity rises substantially, spreads across the economy, and usually lasts for several years. Measuring business cycles NBER examines and compares the behavior of various measures of broad activity: real GDP (the product and income sides), employment, and real income. NBER may consider real sales and industrial production.

4 Financial cycles key issues Macroeconomics without the financial cycle is like Hamlet without the Prince it is not possible to understand business fluctuations without understanding the financial cycle. The financial cycle is much longer than the traditional business cycle (medium term). To model the financial cycle correctly one has to take into account that the financial system does not just allocate, but also generates purchasing power (monetary view). Global economy is highly integrated and to understand its developments we need holistic perspective. This includes analysis of financial cycles which may proceed in sync or at different speed and in different phases across the world (global view).

5 Financial cycles core stylised features There is no consensus on the definition of the financial cycle. Borio: self-reinforcing interactions between perceptions of value and risk, attitudes towards risk and financing constraints, which translate into booms followed by busts. These interactions can amplify economic fluctuations and possibly lead to serious financial distress and economic dislocations. How best to approximate empirically the financial cycle? Feature 1: Most parsimonious description of FC: credit and property prices Closely related to each other, especially at low frequencies, The smallest set of variables needed to capture the interaction between financing constraint (credit) and perceptions of value and risks (property prices).

6 Financial cycles core stylised features Feature 2: The FC has a lower frequency than the traditional business cycle Business cycle: from 1 to 8 years, Financial cycle: around 16 years (in a sample of 7 industrialised countries since the 1960s). Feature 3: Peaks in the FC are closely associated with financial crises All the financial crises with domestic origin occur at, or close to, the peak of FC (in the sample examined). The financial crises that do not occur at peaks reflect losses on exposures to foreign such cycles. Recessions that coincide with the contraction phase of the financial cycle are especially severe.

7 Source: Borio (2014)

8 Source: Runstler G., Vlekke M. (2016), Business, housing and credit cycles, ECB Working Paper No.1915/June 2016

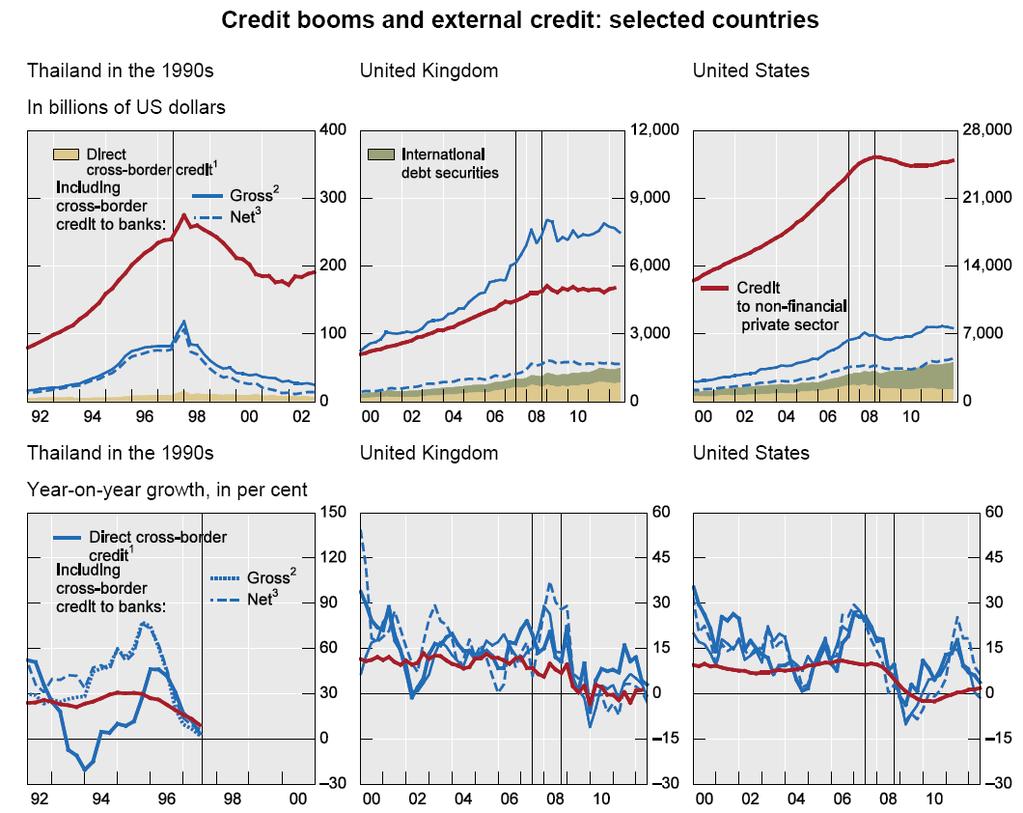

9 Financial cycles core stylised features Feature 4: FC helps detect financial distress risks with a good lead in real time Leading indicators of financial crises: simultaneous positive deviations (or gaps) of the ratio of (private sector) credit-to-gdp and asset prices (especially property prices) from historical norms. The cross-border credit tends to outgrow the domestic credit during financial booms.

10 Source: Borio (2014)

11

12 Financial cycles core stylised features Feature 5: Length and amplitude of the FC depend on policy regimes Financial regime Financial liberalization weakens financing constraint Monetary policy regime Focused on near-term inflation => less resistance to financial booms Real-economy regime Positive supply side developments (eg. globalisation of the real side of the economy) raise growth potential (scope for credit and asset price booms) and lower inflation (less room for monetary policy tightening). Empirical evidence: the length and amplitude of the FC have increased since the mid-1980s.

13 Modelling of the financial cycle What features require modelling: The financial boom should not just precede the bust but cause it. The bust is a result of vulnerabilities that build up during the boom phase. Presence of debt and capital stock overhangs Current models usually do not include the presence of such disequilibrium stocks or assume them exogenous. Distinction between potential output as non-inflationary output and as sustainable output.

14

15 Modelling of the financial cycle How? Expectations are not rational and knowledge is not complete Attitudes towards risk vary with the state of the economy Monetary nature of economies Financial contracts are set in nominal, not in real, terms. The banking sector generates (nominal) purchasing power. Deposits are not endowments that precede loan formation, it is loans that create deposits.

16 The importance of a monetary economy: an example Excess saving view: global current account imbalances were at the origin of the financial crisis. How? CA surpluses (especially in Asia) and net capital outflows financed the credit boom in the deficit countries (especially USA). Excess of savings over investment put downward pressure on world real interest rates, which fuelled the credit boom and risk-taking. Objections to this view: financing vs. saving Financing is gross cash-flow concept Saving is income (output) not consumed Expenditures require financing, not saving Link between credit and saving is loose

17 The importance of a monetary economy: an example US credit boom was mostly finances domestically Foreign funding came largely from countries with a CA deficit (UK) or in balance (the euro area). Criticism concerning behavioral relationships: balance between savings and investment affects the natural, not market, interest rate. Market interest rates are determined by monetary factors: policy rates set by central banks, market expectations about future policy rates and risk premia. Natural rates are unobservable, equilibrium concepts determined by real factors. Empirically, little link between global saving and current accounts, and both short and long real interest rates. Application of real analysis to monetary economies is questionable

18

19 Policy challenges dealing with the boom Addressing financial booms may include several policies: Macroprudential policy appropriate design of tools (capital and liquidity standards, provisioning, collateral and margining practices) Monetary policy adopt strategies that allow central banks to tighten monetary conditions even if near-term inflation remains subdued (the lean option ) Extending policy horizon beyond 2-year one Fiscal policy extra prudence during economic expansions associated with financial booms. Unfinished recession phenomenon: policy responses that fail to take mediumterm financial cycles into account (too much focus on equity prices and standard business cycle measures) can contain recessions in the short run but at the cost of larger recessions later (continued build-up of the financial cycle).

20

21 Policy challenges dealing with the bust Not all recessions are born equal: the typical recession triggered by tightening of monetary policy (until the mid-1980s) vs. balance sheet recession (the most recent recession). Two phases: crisis management and crisis resolution Crisis management the priority is to prevent the implosion of the financial system (central banks lender of last resort function, sharp cuts in policy rates) Crisis resolution the priority is balance sheet repair. Essential is addressing the debt overhang. Fiscal policy may be less effective in balance sheet recessions than in normal ones. The possible solution would be to use the public sector balance sheet to repair and strengthen the private sector s balance sheet.

22 Policy challenges dealing with the bust Monetary policy is also likely to be less effective in stimulating aggregate demand in a balance sheet recession. Possible side-effects of extraordinarily accommodative monetary easing: It can mask balance sheet weakness and delay the recognition of losses. It can undermine the earnings capacity of financial intermediaries (very low interest rates). It can atrophy markets and mask market signals (central banks take over larger part of financial intermediation). It can make central banks vulnerable to losses (balance sheet policies), which can undermine their financial independence. The main problem: monetary policy typically operates by encouraging borrowing, boosting asset prices and risk-taking => but initial conditions already include to much debt, too high asset prices and too much risk-taking.

23

The financial cycle and macroeconomics: Rethinking the way forward

The financial cycle and macroeconomics: Rethinking the way forward Claudio Borio* Bank for International Settlements, Basel Keynote presentation at the conference in honour of Neils Thygesen Financing

The financial cycle and macroeconomics: Rethinking the way forward Claudio Borio* Bank for International Settlements, Basel Keynote presentation at the conference in honour of Neils Thygesen Financing

Capital Flows and the Interaction with Financial Cycles in Emerging Economies. Jinnipa Sarakitphan. A Thesis Submitted to

1 Capital Flows and the Interaction with Financial Cycles in Emerging Economies Jinnipa Sarakitphan A Thesis Submitted to The Graduate School of Public Policy, The University of Tokyo in partial fulfillment

1 Capital Flows and the Interaction with Financial Cycles in Emerging Economies Jinnipa Sarakitphan A Thesis Submitted to The Graduate School of Public Policy, The University of Tokyo in partial fulfillment

A Financial Cycle for Albania

A Financial Cycle for Albania Vasilika Kota and Arisa Goxhaj (Saqe) FInancial Stability Department Bank of Albania (First draft) The views expressed herein are of the authors and do not necessarily reflect

A Financial Cycle for Albania Vasilika Kota and Arisa Goxhaj (Saqe) FInancial Stability Department Bank of Albania (First draft) The views expressed herein are of the authors and do not necessarily reflect

Characterising the financial cycle: don t loose sight of the medium-term!

Characterising the financial cycle: don t loose sight of the medium-term! Mathias Drehmann Claudio Borio Kostas Tsatsaronis Bank for International Settlements 14 th Annual International Banking Conference

Characterising the financial cycle: don t loose sight of the medium-term! Mathias Drehmann Claudio Borio Kostas Tsatsaronis Bank for International Settlements 14 th Annual International Banking Conference

Persistent unusually low interest rates. Why? What consequences?

Persistent unusually low interest rates. Why? What consequences? Claudio Borio Head of the Monetary and Economic Department 85th Annual General Meeting Themes and takeaways One Annual Report (AR) theme

Persistent unusually low interest rates. Why? What consequences? Claudio Borio Head of the Monetary and Economic Department 85th Annual General Meeting Themes and takeaways One Annual Report (AR) theme

An Introduction to Macroeconomics

An Introduction to Macroeconomics Economics 4353 - Intermediate Macroeconomics Aaron Hedlund University of Missouri Fall 2015 Econ 4353 (University of Missouri) Introduction Fall 2015 1 / 19 What is Macroeconomics?

An Introduction to Macroeconomics Economics 4353 - Intermediate Macroeconomics Aaron Hedlund University of Missouri Fall 2015 Econ 4353 (University of Missouri) Introduction Fall 2015 1 / 19 What is Macroeconomics?

Presentation. The Boom in Capital Flows and Financial Vulnerability in Asia

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

Bank Indonesia s Experience on Policy Mix

Bank Indonesia s Experience on Policy Mix Sahminan Department of Economic and Monetary Policy Bank Indonesia Central Bank Policy Mix: Issues, Challenges and Policy Responses Jakarta, 9-13 April 2018 Outline

Bank Indonesia s Experience on Policy Mix Sahminan Department of Economic and Monetary Policy Bank Indonesia Central Bank Policy Mix: Issues, Challenges and Policy Responses Jakarta, 9-13 April 2018 Outline

Overview: Financial Stability and Systemic Risk

Overview: Financial Stability and Systemic Risk Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views

Overview: Financial Stability and Systemic Risk Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY C. Detken, K. Masuch and F. Smets 1 On 11-12 December 2003, the Directorate Monetary Policy of the Directorate General Economics in

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY C. Detken, K. Masuch and F. Smets 1 On 11-12 December 2003, the Directorate Monetary Policy of the Directorate General Economics in

Monetary policy and financial stability: the end of benign neglect?

Monetary policy and financial stability: the end of benign neglect? Claudio Borio* Bank for International Settlements, Basel Financial stability and the role of central banks Deutsche Bundesbank Symposium

Monetary policy and financial stability: the end of benign neglect? Claudio Borio* Bank for International Settlements, Basel Financial stability and the role of central banks Deutsche Bundesbank Symposium

INDICATORS OF FINANCIAL DISTRESS IN MATURE ECONOMIES

B INDICATORS OF FINANCIAL DISTRESS IN MATURE ECONOMIES This special feature analyses the indicator properties of macroeconomic variables and aggregated financial statements from the banking sector in providing

B INDICATORS OF FINANCIAL DISTRESS IN MATURE ECONOMIES This special feature analyses the indicator properties of macroeconomic variables and aggregated financial statements from the banking sector in providing

CCBS Chief Economists Workshop May How Distinct are Financial Cycles from Business Cycles in Asia?

CCBS Chief Economists Workshop 18-19 May 2017 How Distinct are Financial Cycles from Business Cycles in Asia? Dr. Hans Genberg Executive Director The SEACEN Centre 1 Motivation 1 The literature has established

CCBS Chief Economists Workshop 18-19 May 2017 How Distinct are Financial Cycles from Business Cycles in Asia? Dr. Hans Genberg Executive Director The SEACEN Centre 1 Motivation 1 The literature has established

The financial cycle and macroeconomics: What have we learnt?

The financial cycle and macroeconomics: What have we learnt? Claudio Borio* Bank for International Settlements, Basel Conference on European Economic Integration Financial Cycles and the Real Economy:

The financial cycle and macroeconomics: What have we learnt? Claudio Borio* Bank for International Settlements, Basel Conference on European Economic Integration Financial Cycles and the Real Economy:

Financial cycle in Iceland

Seðlabanki Íslands Financial cycle in Iceland Characteristics, spillovers, and cross-border channels Nordic Summer Symposium in Macroeconomics Ebeltoft, 1 August 16 T. Tjörvi Ólafsson (co-authored work

Seðlabanki Íslands Financial cycle in Iceland Characteristics, spillovers, and cross-border channels Nordic Summer Symposium in Macroeconomics Ebeltoft, 1 August 16 T. Tjörvi Ólafsson (co-authored work

Notes on the monetary transmission mechanism in the Czech economy

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Deepak Mohanty: Perspectives on inflation in India

Deepak Mohanty: Perspectives on inflation in India Speech by Mr Deepak Mohanty, Executive Director of the Reserve Bank of India, at the Bankers Club, Chennai, 28 September 2010. * * * The assistance provided

Deepak Mohanty: Perspectives on inflation in India Speech by Mr Deepak Mohanty, Executive Director of the Reserve Bank of India, at the Bankers Club, Chennai, 28 September 2010. * * * The assistance provided

What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF)

and Erlend Nier (IMF)") What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF) What do we do? We document how ample liquidity ahead of the crisis encouraged increases in leverage sourced in wholesale

What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF) What do we do? We document how ample liquidity ahead of the crisis encouraged increases in leverage sourced in wholesale

Monetary Policy and Asset Price Volatility Ben Bernanke and Mark Gertler

Monetary Policy and Asset Price Volatility Ben Bernanke and Mark Gertler 1 Introduction Fom early 1980s, the inflation rates in most developed and emerging economies have been largely stable, while volatilities

Monetary Policy and Asset Price Volatility Ben Bernanke and Mark Gertler 1 Introduction Fom early 1980s, the inflation rates in most developed and emerging economies have been largely stable, while volatilities

II. Underlying domestic macroeconomic imbalances fuelled current account deficits

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

causing the crisis and what lessons can be drawn for its future conduct?

Did monetary policy play a role in causing the crisis and what lessons can be drawn for its future conduct? Remarks prepared by Charles (Chuck) Freedman for the panel discussion at the conference on Economic

Did monetary policy play a role in causing the crisis and what lessons can be drawn for its future conduct? Remarks prepared by Charles (Chuck) Freedman for the panel discussion at the conference on Economic

Commentary: Housing is the Business Cycle

Commentary: Housing is the Business Cycle Frank Smets Prof. Leamer s paper is witty, provocative and very timely. It is also written with a certain passion. Now, passion and central banking do not necessarily

Commentary: Housing is the Business Cycle Frank Smets Prof. Leamer s paper is witty, provocative and very timely. It is also written with a certain passion. Now, passion and central banking do not necessarily

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

Household Balance Sheets and Debt an International Country Study

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

ASSET PRICES IN ECONOMIC THEORY 1

26 1 Ing. Silvia Gantnerová, National Bank of Slovakia Asset prices, though not a goal or instrument of monetary policy, are nonetheless important for its realization, since they are a component of its

26 1 Ing. Silvia Gantnerová, National Bank of Slovakia Asset prices, though not a goal or instrument of monetary policy, are nonetheless important for its realization, since they are a component of its

An interim assessment

What is the economic outlook for OECD countries? An interim assessment Paris, 8 September 2011 11h00 Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General Activity has come close

What is the economic outlook for OECD countries? An interim assessment Paris, 8 September 2011 11h00 Paris time Pier Carlo Padoan OECD Chief Economist and Deputy Secretary-General Activity has come close

ECO 403 L0301 Developmental Macroeconomics. Lecture 8 Balance-of-Payment Crises

ECO 403 L0301 Developmental Macroeconomics Lecture 8 Balance-of-Payment Crises Gustavo Indart Slide 1 The Capitalist Economic System Capitalism is basically an unstable economic system Disequilibrium is

ECO 403 L0301 Developmental Macroeconomics Lecture 8 Balance-of-Payment Crises Gustavo Indart Slide 1 The Capitalist Economic System Capitalism is basically an unstable economic system Disequilibrium is

Financial System and Monetary Policy Transmission Mechanism: How to Address the Increasing Risk Perception

Financial System and Monetary Policy Transmission Mechanism: How to Address the Increasing Risk Perception Miranda S. Goeltom Acting Governor, Bank Indonesia Bank Indonesia s 7th International Seminar

Financial System and Monetary Policy Transmission Mechanism: How to Address the Increasing Risk Perception Miranda S. Goeltom Acting Governor, Bank Indonesia Bank Indonesia s 7th International Seminar

Empirical research, considers 20 countries with fixed exchange rate, crawling peg or floating within a band.

Connection between Banking and Currency Crises Literature: Kaminsky & Reinhart (1999) Empirical research, considers 20 countries with fixed exchange rate, crawling peg or floating within a band. Monthly

Connection between Banking and Currency Crises Literature: Kaminsky & Reinhart (1999) Empirical research, considers 20 countries with fixed exchange rate, crawling peg or floating within a band. Monthly

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

Macroeconomics for Finance

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 1 Contact E-mail: jmackiewicz@wne.uw.edu.pl Office hours: Wednesdays, 5:00-6:00 p.m., room 409. Webpage: http://coin.wne.uw.edu.pl/jmackiewicz/

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 1 Contact E-mail: jmackiewicz@wne.uw.edu.pl Office hours: Wednesdays, 5:00-6:00 p.m., room 409. Webpage: http://coin.wne.uw.edu.pl/jmackiewicz/

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 2014 Monetary Policy Statement (MPS) examines recent price developments and reviews key financial

MID-TERM REVIEW OF THE 2014 MONETARY POLICY STATEMENT 1. INTRODUCTION 1.1 The Mid-Term Review (MTR) of the 2014 Monetary Policy Statement (MPS) examines recent price developments and reviews key financial

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Economic state of the union, EuroMemo Engelbert Stockhammer Kingston University

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Monetary Policy on the Way out of the Crisis

Monetary Policy on the Way out of the Crisis Professor Juergen von Hagen - Bruegel and University of Bonn 1. THE END OF THE CRISIS IS AT HANDS More than two years after the beginning, in August 2007, of

Monetary Policy on the Way out of the Crisis Professor Juergen von Hagen - Bruegel and University of Bonn 1. THE END OF THE CRISIS IS AT HANDS More than two years after the beginning, in August 2007, of

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Ángel Estrada and Francesca Viani (*) 14 th EMERGING MARKET WORKSHOP Madrid (*) The views expressed here do not necessarily coincide with those of Banco de España

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Ángel Estrada and Francesca Viani (*) 14 th EMERGING MARKET WORKSHOP Madrid (*) The views expressed here do not necessarily coincide with those of Banco de España

China s Economy and Monetary Policy

China s Economy and Monetary Policy Asia Economic Policy Conference, Fed San Frencisco 17 th November, 2017 Sun Guofeng Director General of Research Institute The People s Bank of China 1 Main Contents

China s Economy and Monetary Policy Asia Economic Policy Conference, Fed San Frencisco 17 th November, 2017 Sun Guofeng Director General of Research Institute The People s Bank of China 1 Main Contents

Economics: Canada in the Global Environment, 7e (Parkin) Chapter 29 Fiscal Policy Government Budgets

Chapter 29 Fiscal Policy Government Budgets") Economics: Canada in the Global Environment, 7e (Parkin) Chapter 29 Fiscal Policy 29.1 Government Budgets 1) If revenues exceed outlays, the government's budget balance is, and the government has a budget.

Economics: Canada in the Global Environment, 7e (Parkin) Chapter 29 Fiscal Policy 29.1 Government Budgets 1) If revenues exceed outlays, the government's budget balance is, and the government has a budget.

Outlook for Economic Activity and Prices (April 2010)

") April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

Challenges for Monetary Policy in Latin America and the Caribbean

Challenges for Monetary Policy in Latin America and the Caribbean XCVII Meeting of Central Bank Governors of the Center for Latin American Monetary Studies Brian Wynter Governor Bank of Jamaica 29 April

Challenges for Monetary Policy in Latin America and the Caribbean XCVII Meeting of Central Bank Governors of the Center for Latin American Monetary Studies Brian Wynter Governor Bank of Jamaica 29 April

Credit and Financial Cycles as Predictors of Business Cycles: Example of EAEU Countries

Credit and Financial Cycles as Predictors of Business Cycles: Example of EAEU Countries Yulia Vymyatnina, professor Daria Antonova, associate researcher Mariia Artemova, junior researcher European University

Credit and Financial Cycles as Predictors of Business Cycles: Example of EAEU Countries Yulia Vymyatnina, professor Daria Antonova, associate researcher Mariia Artemova, junior researcher European University

ECB MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE DEVELOPMENTS

Box 7 MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE The has responded swiftly and decisively to the crisis and the subsequent deterioration in economic, monetary and conditions with the aim

Box 7 MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE The has responded swiftly and decisively to the crisis and the subsequent deterioration in economic, monetary and conditions with the aim

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Trends in financial intermediation: Implications for central bank policy

Trends in financial intermediation: Implications for central bank policy Monetary Authority of Singapore Abstract Accommodative global liquidity conditions post-crisis have translated into low domestic

Trends in financial intermediation: Implications for central bank policy Monetary Authority of Singapore Abstract Accommodative global liquidity conditions post-crisis have translated into low domestic

No 02. Chapter 1. Chapter Outline. What Macroeconomics Is About. Introduction to Macroeconomics

No 02. Chapter 1 Introduction to Macroeconomics Chapter Outline What Macroeconomists Do Why Macroeconomists Disagree Macroeconomics: the study of structure and performance of national economies and government

No 02. Chapter 1 Introduction to Macroeconomics Chapter Outline What Macroeconomists Do Why Macroeconomists Disagree Macroeconomics: the study of structure and performance of national economies and government

Note on Countercyclical Capital Buffer Methodology

Note on Countercyclical Capital Buffer Methodology Prepared by Financial Stability Department December 2018 1 1. Background and Legal Basis Following the recent financial crisis, the Basel Committee on

Note on Countercyclical Capital Buffer Methodology Prepared by Financial Stability Department December 2018 1 1. Background and Legal Basis Following the recent financial crisis, the Basel Committee on

The Financial Crisis, Global Imbalances, and the

The Financial Crisis, Global Imbalances, and the International Monetary System David Vines Oxford University, Australian National University, and CEPR ICRIER-CEPII-BRUEGEL Conference on International Cooperation

The Financial Crisis, Global Imbalances, and the International Monetary System David Vines Oxford University, Australian National University, and CEPR ICRIER-CEPII-BRUEGEL Conference on International Cooperation

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES. Javier Guzmán Calafell 1

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES Javier Guzmán Calafell 1 1. Introduction Capital flows to Latin America and other emerging market regions fell sharply after the collapse

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES Javier Guzmán Calafell 1 1. Introduction Capital flows to Latin America and other emerging market regions fell sharply after the collapse

IB Economics The Level of Overall Economic Activity 2.4: The Business Cycle Activity

IB Economics: www.ibdeconomics.com 2.4 THE BUSINESS CYCLE: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: Business cycle Contraction Economic growth

IB Economics: www.ibdeconomics.com 2.4 THE BUSINESS CYCLE: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: Business cycle Contraction Economic growth

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

What Governance for the Eurozone? Paul De Grauwe London School of Economics

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

Iceland s crisis and recovery: are there lessons for the eurozone and its member countries?

Central Bank of Iceland Iceland s crisis and recovery: are there lessons for the eurozone and its member countries? Már Guðmundsson Governor, Central Bank of Iceland Levy Institute conference, Athens,

Central Bank of Iceland Iceland s crisis and recovery: are there lessons for the eurozone and its member countries? Már Guðmundsson Governor, Central Bank of Iceland Levy Institute conference, Athens,

Macroeconomics for Finance

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 3 From tools to goals Tools of the Central Bank Open market operations Discount policy Reserve requirements Interest on reserves Large-scale

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 3 From tools to goals Tools of the Central Bank Open market operations Discount policy Reserve requirements Interest on reserves Large-scale

Challenges for the global economy: A diagnosis

Challenges for the global economy: A diagnosis Claudio Borio* Bank for International Settlements Breakfast seminar, Frankfurt Main Finance, Frankfurt, 1 December 2015 * Head of the Monetary and Economic

Challenges for the global economy: A diagnosis Claudio Borio* Bank for International Settlements Breakfast seminar, Frankfurt Main Finance, Frankfurt, 1 December 2015 * Head of the Monetary and Economic

Managing the Fragility of the Eurozone. Paul De Grauwe London School of Economics

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Research Iceland: Recovery in uncertain times

Investment Research General Market Conditions 12 April 2011 Research Iceland: Recovery in uncertain times The Icelandic economy is now recovering after the collapse of the Icelandic banking sector in October

Investment Research General Market Conditions 12 April 2011 Research Iceland: Recovery in uncertain times The Icelandic economy is now recovering after the collapse of the Icelandic banking sector in October

Provision of FX hedge by the public sector: the Brazilian experience

Provision of FX hedge by the public sector: the Brazilian experience Afonso Bevilaqua 1 and Rodrigo Azevedo 2 Introduction A singular experience with forex intervention in Brazil over the past ten years

Provision of FX hedge by the public sector: the Brazilian experience Afonso Bevilaqua 1 and Rodrigo Azevedo 2 Introduction A singular experience with forex intervention in Brazil over the past ten years

Economic policy-making in a small and open economy the case of Suriname

Is small beautiful? Economic policy-making in a small and open economy the case of Suriname Gillmore Hoefdraad November 2012 Highlights World Economic Outlook 2 Summary Global growth has decelerated. Growth

Is small beautiful? Economic policy-making in a small and open economy the case of Suriname Gillmore Hoefdraad November 2012 Highlights World Economic Outlook 2 Summary Global growth has decelerated. Growth

Macroeconomic perspectives

12 July 2018 Macroeconomic perspectives Csaba Bálint OTP Bank Romania Global context: Ultra-loose monetary policy seemingly came to an end; precaution is warranted (1) SUMMARY: In the beginning of 2018,

12 July 2018 Macroeconomic perspectives Csaba Bálint OTP Bank Romania Global context: Ultra-loose monetary policy seemingly came to an end; precaution is warranted (1) SUMMARY: In the beginning of 2018,

Ms Hessius comments on the inflation target and the state of the economy in Sweden

Ms Hessius comments on the inflation target and the state of the economy in Sweden Speech given by Ms Kerstin Hessius, Deputy Governor of the Sveriges Riksbank, before the Swedish Economic Association,

Ms Hessius comments on the inflation target and the state of the economy in Sweden Speech given by Ms Kerstin Hessius, Deputy Governor of the Sveriges Riksbank, before the Swedish Economic Association,

Eurozone Ernst & Young Eurozone Forecast June 2013

Eurozone Ernst & Young Eurozone Forecast June 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Ernst & Young

Eurozone Ernst & Young Eurozone Forecast June 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Ernst & Young

Automatic Fiscal Stabilizers

118 Finance Challenges of the Future Automatic Fiscal Stabilizers Narcis Eduard Mitu 1 1 Faculty of Economy and Business Administration, University of Craiova mitunarcis@yahoo.com Abstract: Policies or

118 Finance Challenges of the Future Automatic Fiscal Stabilizers Narcis Eduard Mitu 1 1 Faculty of Economy and Business Administration, University of Craiova mitunarcis@yahoo.com Abstract: Policies or

Andersons Professor of International Trade Department of Agricultural, Environmental & Development Economics Ohio State University

Macroeconomic Outlook Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Global economic

Macroeconomic Outlook Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Global economic

Macro-prudential policy: expanding the central bank s countercyclical arsenal. Andrzej Sławiński, National Bank of Poland

Macro-prudential policy: expanding the central bank s countercyclical arsenal Andrzej Sławiński, National Bank of Poland Should macroprudential policy be ambitious in setting its goals? There are hardly

Macro-prudential policy: expanding the central bank s countercyclical arsenal Andrzej Sławiński, National Bank of Poland Should macroprudential policy be ambitious in setting its goals? There are hardly

MANAGING CAPITAL FLOWS

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

September 21, 2016 Bank of Japan

September 21, 2016 Bank of Japan Comprehensive Assessment: Developments in Economic Activity and Prices as well as Policy Effects since the Introduction of Quantitative and Qualitative Monetary Easing

September 21, 2016 Bank of Japan Comprehensive Assessment: Developments in Economic Activity and Prices as well as Policy Effects since the Introduction of Quantitative and Qualitative Monetary Easing

Macroprudential policy frameworks, instruments and indicators: a review 1

IFC workshop on Combining micro and macro statistical data for financial stability analysis. Experiences, opportunities and challenges Warsaw, Poland, 14-15 December 2015 Macroprudential policy frameworks,

IFC workshop on Combining micro and macro statistical data for financial stability analysis. Experiences, opportunities and challenges Warsaw, Poland, 14-15 December 2015 Macroprudential policy frameworks,

2 Macroeconomic Scenario

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

CIE Economics A-level

CIE Economics A-level Topic 4: The Macroeconomy f) Money supply (theory) Notes Quantity theory of money (MV = PT) The Quantity Theory of Money states that there is inflation if the money supply increases

CIE Economics A-level Topic 4: The Macroeconomy f) Money supply (theory) Notes Quantity theory of money (MV = PT) The Quantity Theory of Money states that there is inflation if the money supply increases

Evaluating the Impact of Macroprudential Policies in Colombia

Esteban Gómez - Angélica Lizarazo - Juan Carlos Mendoza - Andrés Murcia June 2016 Disclaimer: The opinions contained herein are the sole responsibility of the authors and do not reflect those of Banco

Esteban Gómez - Angélica Lizarazo - Juan Carlos Mendoza - Andrés Murcia June 2016 Disclaimer: The opinions contained herein are the sole responsibility of the authors and do not reflect those of Banco

ETUC Position Paper: A European Treasury for Public Investment

ETUC Position Paper: A European Treasury for Public Investment Adopted at the ETUC Executive Committee on 15-16 March 2017 For many years now, the ETUC has been calling for public investment in Europe

ETUC Position Paper: A European Treasury for Public Investment Adopted at the ETUC Executive Committee on 15-16 March 2017 For many years now, the ETUC has been calling for public investment in Europe

The macroeconomics of macroprudential policies

The macroeconomics of macroprudential policies Philip Turner Bank for International Settlements Presentation at the Conference on Effective Macroprudential Instruments The University of Nottingham Centre

The macroeconomics of macroprudential policies Philip Turner Bank for International Settlements Presentation at the Conference on Effective Macroprudential Instruments The University of Nottingham Centre

Discussion of Michael Klein s Capital Controls: Gates and Walls Brookings Papers on Economic Activity, September 2012

Discussion of Michael Klein s Capital Controls: Gates and Walls Brookings Papers on Economic Activity, September 2012 Kristin Forbes 1, MIT-Sloan School of Management The desirability of capital controls

Discussion of Michael Klein s Capital Controls: Gates and Walls Brookings Papers on Economic Activity, September 2012 Kristin Forbes 1, MIT-Sloan School of Management The desirability of capital controls

MCCI ECONOMIC OUTLOOK. Novembre 2017

MCCI ECONOMIC OUTLOOK 2018 Novembre 2017 I. THE INTERNATIONAL CONTEXT The global economy is strengthening According to the IMF, the cyclical turnaround in the global economy observed in 2017 is expected

MCCI ECONOMIC OUTLOOK 2018 Novembre 2017 I. THE INTERNATIONAL CONTEXT The global economy is strengthening According to the IMF, the cyclical turnaround in the global economy observed in 2017 is expected

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Phases of the Business Cycle. Business Cycle. Business Cycle

Phases of the Business Cycle Business Cycle Definition: alternating increases and decreases in the level of business activity of varying amplitude and length How do we measure increases and decreases in

Phases of the Business Cycle Business Cycle Definition: alternating increases and decreases in the level of business activity of varying amplitude and length How do we measure increases and decreases in

Operationalizing the Selection and Application of Macroprudential Instruments

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Econ 102 Exam 2 Name ID Section Number

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

Statistics used by the BIS in monitoring and research of the economic and financial crises

Statistics used by the BIS in monitoring and research of the economic and financial crises A note presented by Gert Schnabel 1 at the International Seminar on Timeliness, Methodology and Comparability

Statistics used by the BIS in monitoring and research of the economic and financial crises A note presented by Gert Schnabel 1 at the International Seminar on Timeliness, Methodology and Comparability

From Subprime Loans to Subprime Growth? Evidence for the Euro Area

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 From Subprime Loans to Subprime Growth? Evidence for the Euro Area Martin Čihák International Monetary Fund and Petya Koeva International

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 From Subprime Loans to Subprime Growth? Evidence for the Euro Area Martin Čihák International Monetary Fund and Petya Koeva International

C K F C K F. Center for Economic Forecasting of Mexico MEXICO ECONOMIC OUTLOOK

C K F Center for Economic Forecasting of Mexico MEXICO ECONOMIC OUTLOOK 2017 2019 Prepared for the Fall Meeting of Project LINK, to be hosted by UNCTAD, Palais des Nations. Geneva, Switzerland. October

C K F Center for Economic Forecasting of Mexico MEXICO ECONOMIC OUTLOOK 2017 2019 Prepared for the Fall Meeting of Project LINK, to be hosted by UNCTAD, Palais des Nations. Geneva, Switzerland. October

Monetary policy normalization in the euro area

Monetary policy normalization in the euro area Stefano Siviero Bank of Italy, Economic Outlook and Monetary Policy Directorate Policy Research Meeting on Financial Markets and Institutions Rome, 4 October

Monetary policy normalization in the euro area Stefano Siviero Bank of Italy, Economic Outlook and Monetary Policy Directorate Policy Research Meeting on Financial Markets and Institutions Rome, 4 October

An Introduction to Basic Macroeconomic Markets

An Introduction to Basic Macroeconomic Markets Full Length Text Part: Macro Only Text Part: 3 Chapter: 9 3 Chapter: 9 To Accompany Economics: Private and Public Choice 13th ed. James Gwartney, Richard

An Introduction to Basic Macroeconomic Markets Full Length Text Part: Macro Only Text Part: 3 Chapter: 9 3 Chapter: 9 To Accompany Economics: Private and Public Choice 13th ed. James Gwartney, Richard

Financial Crises and Asset Prices. Tyler Muir June 2017, MFM

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Discussant remarks: monetary policy and exchange rate issues in Asia and the Pacific

Discussant remarks: monetary policy and exchange rate issues in Asia and the Pacific Kyungsoo Kim 1 First of all, let me thank the People s Bank of China and the Bank for International Settlements for

Discussant remarks: monetary policy and exchange rate issues in Asia and the Pacific Kyungsoo Kim 1 First of all, let me thank the People s Bank of China and the Bank for International Settlements for

Macroprudential Policy in Korea - An Introduction to BOK Framework -

II Meeting on Financial Stability Bogotá, Colombia (October 25, 2012) Macroprudential Policy in Korea - An Introduction to BOK Framework - Hyeonjin Cha Bank of Korea DISCLAIMER: This presentation represents

II Meeting on Financial Stability Bogotá, Colombia (October 25, 2012) Macroprudential Policy in Korea - An Introduction to BOK Framework - Hyeonjin Cha Bank of Korea DISCLAIMER: This presentation represents

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Resilience in Emerging Market and Developing Economies: Will It Last?

International Monetary Fund World Economic Outlook October 212 Resilience in Emerging Market and Developing Economies: Will It Last? Abdul Abiad, John Bluedorn, Jaime Guajardo, and Petia Topalova with

International Monetary Fund World Economic Outlook October 212 Resilience in Emerging Market and Developing Economies: Will It Last? Abdul Abiad, John Bluedorn, Jaime Guajardo, and Petia Topalova with

A Regional Early Warning System Prototype for East Asia

A Regional Early Warning System Prototype for East Asia Regional Economic Monitoring Unit Asian Development Bank 1 A Regional Early Warning System Prototype for East Asia Regional Economic Monitoring Unit

A Regional Early Warning System Prototype for East Asia Regional Economic Monitoring Unit Asian Development Bank 1 A Regional Early Warning System Prototype for East Asia Regional Economic Monitoring Unit

Chapter 18. The International Financial System

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

What do new forms of finance mean for EM central banks?

What do new forms of finance mean for EM central banks? An overview M S Mohanty 1 The size and the structure of financial intermediation influence the cost of credit, the risk exposure of financial institutions

What do new forms of finance mean for EM central banks? An overview M S Mohanty 1 The size and the structure of financial intermediation influence the cost of credit, the risk exposure of financial institutions

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies Giancarlo Corsetti (Cambridge & CEPR) Gernot Müller (Bonn & CEPR) Stockholm June 8, 2016 Swedish Fiscal Policy Council 1. Introduction

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies Giancarlo Corsetti (Cambridge & CEPR) Gernot Müller (Bonn & CEPR) Stockholm June 8, 2016 Swedish Fiscal Policy Council 1. Introduction

Monetary Theory and Policy

October 16, 2015 1 Basics Problems of Macroeconomics Analysis of Policy Effects 2 Conduct of 3 Explaning Analyzing Definitions Outline Basics Problems of Macroeconomics Analysis of Policy Effects Economics

October 16, 2015 1 Basics Problems of Macroeconomics Analysis of Policy Effects 2 Conduct of 3 Explaning Analyzing Definitions Outline Basics Problems of Macroeconomics Analysis of Policy Effects Economics

Crises and Growth: A Re-Evaluation

Crises and Growth: A Re-Evaluation Romain Rancière Aaron Tornell Frank Westermann Dubrovnik, July 2005 "The regular development of wealth does not occur without pain and resistance. In crises everything

Crises and Growth: A Re-Evaluation Romain Rancière Aaron Tornell Frank Westermann Dubrovnik, July 2005 "The regular development of wealth does not occur without pain and resistance. In crises everything

EUROPEAN ECONOMY. Fiscal Policy Stabilisation and the Financial Cycle in the Euro Area. Cinzia Alcidi DISCUSSION PAPER 052 JULY 2017

ISSN 2443-8022 (online) Fiscal Policy Stabilisation and the Financial Cycle in the Euro Area Cinzia Alcidi FELLOWSHIP INITIATIVE Challenges to Integrated Markets DISCUSSION PAPER 052 JULY 2017 EUROPEAN

ISSN 2443-8022 (online) Fiscal Policy Stabilisation and the Financial Cycle in the Euro Area Cinzia Alcidi FELLOWSHIP INITIATIVE Challenges to Integrated Markets DISCUSSION PAPER 052 JULY 2017 EUROPEAN