From Subprime Loans to Subprime Growth? Evidence for the Euro Area

|

|

|

- Maurice Lawson

- 5 years ago

- Views:

Transcription

1 9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 From Subprime Loans to Subprime Growth? Evidence for the Euro Area Martin Čihák International Monetary Fund and Petya Koeva International Monetary Fund Presented at the 9th Jacques Polak Annual Research Conference Hosted by the International Monetary Fund Washington, DC November 13-14, 2008 The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website does not imply that the IMF, its Executive Board, or its management endorses or shares the views expressed in the paper.

2 From Subprime Loans to Subprime Growth? Evidence for the Euro Area Martin Čihák and Petya Koeva IMF Ninth Jacques Polak Annual Research Conference on Macro Financial Linkages Washington, DC, November 13, 2008

3 Motivation Broad reassessment of risk in money and credit markets

4 Motivation Increased cost of financing from banks

5 Motivation Increased cost of financing

6 Motivation Equity market decline

7 Motivation

8 Motivation

9 Motivation

10 Motivation Too early to observe full impact of deterioration in financing conditions on euro area economy but still useful to examine linkages between the financial and real sectors in the Euro Area, using a combination of past and recent data. Likely channels: Higher lending rates Stricter lending standards Higher costs of corporate bond and equity financing Financial accelerator effects

11 Outline Empirical evidence Bank characteristics lending Bank loan supply output Corporate financing conditions and economic activity Risk transfers between banks and other sectors: contingent claims analysis Quantitative implications of results

12 Bank Characteristics and Lending Behavior Q: Is bank supply affected by deteriorating financing conditions? Analysis of the bank lending channel : banks unable to fully shield loan portfolios from changes in financing costs substantial group of borrowers unable to insulate spending from bank credit reduction. The financial turbulence/crisis of provides a natural experiment but we need to look at bank-by by-bank bank variation to isolate supply response from demand shock

13 Bank Characteristics and Lending Behavior Literature: mostly on U.S. data banks (esp. small) decrease loan supply in tighter financing conditions but little evidence of impact on real activity Literature for Europe: inconclusive bank lending channel effective in countries with many small banks, weak capitalization and liquidity, limited non-bank funding studies focus on impact of financing conditions on bank loans (less on impact on output)

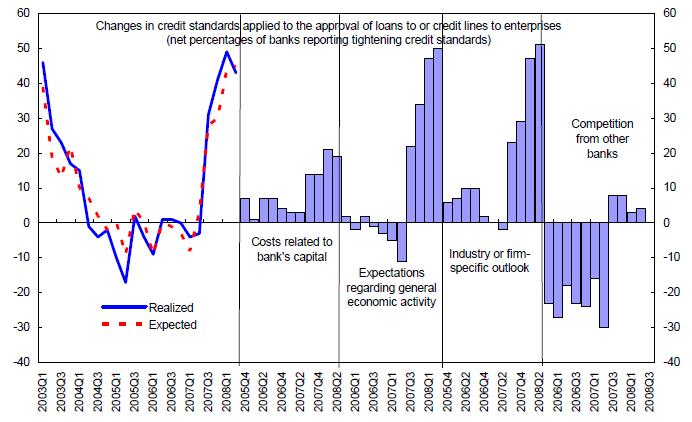

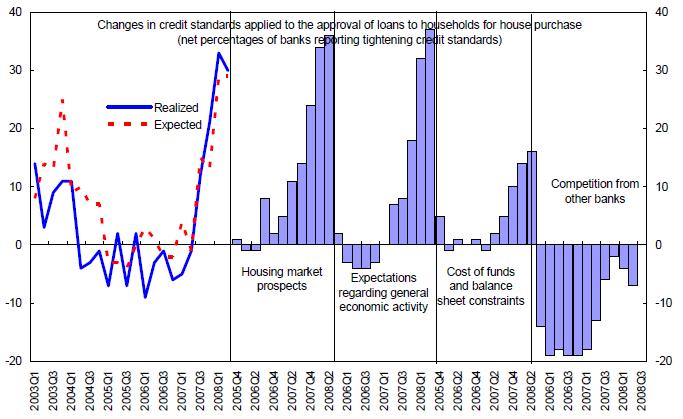

14 Bank Characteristics and Lending Behavior Correlation between the q/q growth of real GDP and the net percentages from the lending surveys: Loan demand Credit std s Households Enterprises Both loan demand and credit std s s are procyclical. Time series of lending surveys are too short for a more elaborate analysis.

15 Bank Characteristics and Lending Behavior -20 Euro Area: What Is Causing Banks to Tighten? Housing market prospects (lending to households) overall-expected General economic conditions (lending to corporates) overall-current assessment Mar-06 Sep-06 Mar-07 Sep-07 Mar-08 Sep-08 Mar-09

16 Bank Characteristics and Lending Behavior Econometric estimate: supply-demand disequilibrium model credit determined by the minimum of supply and demand (Pazarbasioglu( Pazarbasioglu,, 1997; Barajas, Steiner, 2002) this avoids the identification problem of equilibrium models, and allows for credit crunch. Estimated on individual bank data for 50 largest euro area banks in Specification: Demand side: see Bundesbank (2002). Supply side: see Pazarbasioglu (1997), but we add the distance to default among the supply-side side variables.

17 Bank Characteristics and Lending Behavior

18 Bank Characteristics and Lending Behavior Results: all key coefficients have expected signs and are significant. Explains year-on on-year real growth rates of customer loans as a function of a bank s s distance to default (+), real GDP growth rate as a proxy for overall economic activity (+), lending rate and net interest margin (-),( and bank size approximated by total value of loans (-).( The effect of bank soundness on loan supply is significant, but small. It implies that a 1 st.d.. drop in DD is associated with a y/y real growth of credit that is 1.5 percentage points lower than otherwise.

19 Bank Characteristics and Lending Behavior

20 Bank Characteristics and Lending Behavior 8 6 excess demand for credit demand minus supply % ofcredit supply st.dev st.dev. excess supply of credit

21 Loan Supply and Output

22 Loan Supply and Output Examine relationship btw bank loan supply and economic activity Econometric problem Identification solution Use shocks to country-specific money demand as an instrument for shocks to bank supply First proposed by Driscoll (2004) for the U.S. (using state-level data)

23 Loan Supply and Output Identification scheme: Regress output growth on growth rate of bank loans (and its lagged value), and its own lagged values. Recover shocks to money demand for each euro area country in the sample and regress growth rate of bank loans on its lagged values and the estimated money demand shocks. Re-estimate estimate effect of bank credit on output using the country-specific shocks to money demand as instruments.

24 Loan Supply and Output Estimated on country-level data for 1999Q1 to 2008Q2 (robustness check: 2003Q1-2008Q2). 2008Q2). Sample includes 11 euro area countries. Key variables: real GDP, M3, deposit rates, and bank loans to non-financial corporations. All variables are constructed as deviations from their cross-sectional sectional mean values.

25 Loan Supply and Output

26 Loan Supply and Output

27 Loan Supply and Output

28 Loan Supply and Output The loan supply effect on output is positive (and statistically significant) but relatively small. An increase in the supply of bank loans by 1 percentage points is likely to lead to an increase in real GDP by about 0.1 percentage point. A cutback in bank loan supply is likely to have a negative impact on economic activity.

29 Corporate Financing and Economic Activity Analyze relationship between corporate bond spread and output in the Euro Area. Corporate bond risk premium is a good predictor of real activity. Can be treated as a proxy for financing conditions.

30 Corporate Financing and Economic Activity Define corporate bond spread = 7-year 7 BBB-rated corporate bond yield 7-year government bond yield (robustness check: different bonds) Monthly industrial production proxy for real activity. Run VARs for 1999M1:2008M1. Vars: : spread, (log) IP, 3M EURIBOR rate, (log) REER. Number of lags = 2 (robustness check: different lags)

31 Corporate Financing and Economic Activity Response of annual growth in industrial production to 1 st.d. innovation in corporate spread

32 Corporate Financing and Economic Activity A positive shock to the corporate bond spread leads to a negative response of real activity. One standard deviation shock (about 60 basis points) has an adverse effect on industrial production, which peaks at about ¼ percent in months. The effect is statistically significant. Results are fairly robust across alternative specifications.

33 Risk Transfers: Contingent Claims Analysis CCA: : an enhanced version of the balance sheet approach that takes into account market-based data. Basic idea: changes in observed variables used to infer changes in unobserved vars (econ. value of firm, sector). Basic tool: risk-adjusted balance sheet Sectors are viewed as interconnected portfolios of assets, liabilities, and guarantees. Can capture non-linearities First time CCA is used to identify vulnerabilities in the corporate, banking, and public sectors in the Euro Area.

34 Risk Transfers: Contingent Claims Analysis Source: Gray and Jones (2006).

35 Risk Transfers: Contingent Claims Analysis shows estimated PDs (next 4 quarters) in banks and corporates

36 Risk Transfers: Contingent Claims Analysis shows estimated PDs for sovereigns

37 Quantitative Implications First approach: Estimated losses in euro-area commercial banks: US$45 bn (sub-prime related losses in euro-area banks as of March 2008; reported in IMF s April 2008 GFSR) Latest estimates of the total exceptional losses in euro- area global banks (=sub-prime related losses plus exceptional part of losses on European assets) may be as large as 10 times that amount. These latest estimates would translate, other things being equal, into a decline in C/A from 5.6 to 4.8 %. To keep C/A unchanged (i.e. no change in leverage), assets would have to shrink by 14 percent. But banks are aiming to deleverage

38 Quantitative Implications

39 Quantitative Implications First approach (continued): If the banks aim to increase C/A to 5.9 % ( sample maximum), loans would go down by 19 %. If C/A goes up to 7 percent, loans go down 31 %. From the econometric estimate, a decline in the supply of bank loans by 10 percentage points is likely to lead to a decline in real GDP by about 1 percentage point. This means that the above declines in assets would translate to percentage points negative impact on real GDP. The impact can be mitigated by capital injections; exacerbated if massive deleveraging or strong confidence effects (breaking down the relationships).

40 Quantitative Implications Second approach: Average DD: 8.0 in July in October 2008 Using our estimates, this negative 19 % pt impact on real credit, which negative 1.9 % pt real GDP decline. All in all, the two approaches suggest an impact on output in the range of percentage points.

41 Conclusions Deterioration in banks health translates into lower bank loan supply. Cutback in bank loan supply likely to have a negative impact on economic activity. Higher costs of corporate bond financing lead to significant decline in industrial production. Risk indicators for the banking, corporate, and public sectors show an improvement in balance sheets since , 03, followed by a deterioration in , 2008, reflecting a combination of the increased market volatility and lower capitalization. Current estimates of bank losses would mean a negative 2-33 % pt impact on GDP.

From Subprime Loans to Subprime Growth? Evidence for the Euro Area

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 From Subprime Loans to Subprime Growth? Evidence for the Euro Area Martin Čihák and Petya Koeva Brooks International Monetary Fund Paper

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 From Subprime Loans to Subprime Growth? Evidence for the Euro Area Martin Čihák and Petya Koeva Brooks International Monetary Fund Paper

From Subprime Loans to Subprime Growth? Evidence for the Euro Area

WP/09/69 From Subprime Loans to Subprime Growth? Evidence for the Euro Area Martin Čihák and Petya Koeva Brooks 2009 International Monetary Fund WP/09/69 IMF Working Paper European Department From Subprime

WP/09/69 From Subprime Loans to Subprime Growth? Evidence for the Euro Area Martin Čihák and Petya Koeva Brooks 2009 International Monetary Fund WP/09/69 IMF Working Paper European Department From Subprime

A Micro Data Approach to the Identification of Credit Crunches

A Micro Data Approach to the Identification of Credit Crunches Horst Rottmann University of Amberg-Weiden and Ifo Institute Timo Wollmershäuser Ifo Institute, LMU München and CESifo 5 December 2011 in

A Micro Data Approach to the Identification of Credit Crunches Horst Rottmann University of Amberg-Weiden and Ifo Institute Timo Wollmershäuser Ifo Institute, LMU München and CESifo 5 December 2011 in

The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations Augustin Landier Toulouse School of Economics David Sraer Princeton

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 The Risk-Shifting Hypothesis: Evidence from Sub-Prime Originations Augustin Landier Toulouse School of Economics David Sraer Princeton

Designing Scenarios for Macro Stress Testing (Financial System Report, April 2016)

") Financial System Report Annex Series inancial ystem eport nnex A Designing Scenarios for Macro Stress Testing (Financial System Report, April 1) FINANCIAL SYSTEM AND BANK EXAMINATION DEPARTMENT BANK OF

Financial System Report Annex Series inancial ystem eport nnex A Designing Scenarios for Macro Stress Testing (Financial System Report, April 1) FINANCIAL SYSTEM AND BANK EXAMINATION DEPARTMENT BANK OF

Banking Globalization, Monetary Transmission, and the Lending Channel

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 Banking Globalization, Monetary Transmission, and the Lending Channel Nicola Cetorelli Federal Reserve Bank of New York and Linda Goldberg

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 Banking Globalization, Monetary Transmission, and the Lending Channel Nicola Cetorelli Federal Reserve Bank of New York and Linda Goldberg

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market Seung Jung Lee FRB Lucy Qian Liu IMF Viktors Stebunovs FRB BIS CCA Research Conference on "Low interest rates,

Risk Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market Seung Jung Lee FRB Lucy Qian Liu IMF Viktors Stebunovs FRB BIS CCA Research Conference on "Low interest rates,

Monetary and Macroprudential Policy in an Estimated DSGE Model of the Euro Area

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 Monetary and Macroprudential Policy in an Estimated DSGE Model of the Euro Area Jesper Lindé Federal Reserve Board Presentation presented

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 Monetary and Macroprudential Policy in an Estimated DSGE Model of the Euro Area Jesper Lindé Federal Reserve Board Presentation presented

Bank Lending Shocks and the Euro Area Business Cycle

Bank Lending Shocks and the Euro Area Business Cycle Gert Peersman Ghent University Motivation SVAR framework to examine macro consequences of disturbances specific to bank lending market in euro area

Bank Lending Shocks and the Euro Area Business Cycle Gert Peersman Ghent University Motivation SVAR framework to examine macro consequences of disturbances specific to bank lending market in euro area

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF)

and Erlend Nier (IMF)") What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF) What do we do? We document how ample liquidity ahead of the crisis encouraged increases in leverage sourced in wholesale

What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF) What do we do? We document how ample liquidity ahead of the crisis encouraged increases in leverage sourced in wholesale

Comments of The Hunt for Duration: Not Waving but Drowning?

16TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 5 6, 2015 Comments of The Hunt for Duration: Not Waving but Drowning? Sergio Schmukler World Bank Paper presented at the 16th Jacques Polak Annual

16TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 5 6, 2015 Comments of The Hunt for Duration: Not Waving but Drowning? Sergio Schmukler World Bank Paper presented at the 16th Jacques Polak Annual

The Labor Market Consequences of Adverse Financial Shocks

13TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 8 9, 2012 The Labor Market Consequences of Adverse Financial Shocks Tito Boeri Bocconi University and frdb Pietro Garibaldi University of Torino and

13TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 8 9, 2012 The Labor Market Consequences of Adverse Financial Shocks Tito Boeri Bocconi University and frdb Pietro Garibaldi University of Torino and

Does Macro-Pru Leak? Empirical Evidence from a UK Natural Experiment

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 Does Macro-Pru Leak? Empirical Evidence from a UK Natural Experiment Shekhar Aiyar International Monetary Fund Charles W. Calomiris Columbia

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 Does Macro-Pru Leak? Empirical Evidence from a UK Natural Experiment Shekhar Aiyar International Monetary Fund Charles W. Calomiris Columbia

Macroprudential Policies:Korea s Experiences

RETHINKING MACRO POLICY II: FIRST STEPS AND EARLY LESSONS APRIL 16 17, 2013 Macroprudential Policies:Korea s Experiences Choongsoo Kim Governor of the Bank of Korea Paper presented at the Rethinking Macro

RETHINKING MACRO POLICY II: FIRST STEPS AND EARLY LESSONS APRIL 16 17, 2013 Macroprudential Policies:Korea s Experiences Choongsoo Kim Governor of the Bank of Korea Paper presented at the Rethinking Macro

Insolvency risk in the Jamaican banking system. Locksley Todd Financial Stability Department Bank of Jamaica

Insolvency risk in the Jamaican banking system Locksley Todd Financial Stability Department Bank of Jamaica Outline Introduction Overview Literature Review Methodology Model refinement Data Results and

Insolvency risk in the Jamaican banking system Locksley Todd Financial Stability Department Bank of Jamaica Outline Introduction Overview Literature Review Methodology Model refinement Data Results and

Macroeconomic Impact of the Subprime Crisis

Franco German Council of Economic Advisors Paris, 5 February 2008 Dr. Stefan Kooths DIW Berlin, Macro Analysis and Forecasting Approach Assuming a strictly macroeconomic point of view - Thinking in aggregates

Franco German Council of Economic Advisors Paris, 5 February 2008 Dr. Stefan Kooths DIW Berlin, Macro Analysis and Forecasting Approach Assuming a strictly macroeconomic point of view - Thinking in aggregates

Comments on Assessing Policies to Revive Credit Markets

Comments on Assessing Policies to Revive Credit Markets Chapter 2 of Global Financial Stability Report, IMF, October, 2013 Rafael Doménech Madrid, October 18, 2013 Main results Chapter 2 of the GFSR offers

Comments on Assessing Policies to Revive Credit Markets Chapter 2 of Global Financial Stability Report, IMF, October, 2013 Rafael Doménech Madrid, October 18, 2013 Main results Chapter 2 of the GFSR offers

The Procyclical Effects of Basel II

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 The Procyclical Effects of Basel II Rafael Repullo CEMFI and CEPR, Madrid, Spain and Javier Suarez CEMFI and CEPR, Madrid, Spain Presented

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 The Procyclical Effects of Basel II Rafael Repullo CEMFI and CEPR, Madrid, Spain and Javier Suarez CEMFI and CEPR, Madrid, Spain Presented

The bank lending channel in monetary transmission in the euro area:

The bank lending channel in monetary transmission in the euro area: evidence from Bayesian VAR analysis Matteo Bondesan Graduate student University of Turin (M.Sc. in Economics) Collegio Carlo Alberto

The bank lending channel in monetary transmission in the euro area: evidence from Bayesian VAR analysis Matteo Bondesan Graduate student University of Turin (M.Sc. in Economics) Collegio Carlo Alberto

Macroeconomic Implications of Financial Frictions in the Euro Zone: Lessons from Canada

THE TWENTIETH DUBROVNIK ECONOMIC CONFERENCE Organized by the Croatian National Bank Pierre L. Siklos Macroeconomic Implications of Financial Frictions in the Euro Zone: Lessons from Canada Hotel "Grand

THE TWENTIETH DUBROVNIK ECONOMIC CONFERENCE Organized by the Croatian National Bank Pierre L. Siklos Macroeconomic Implications of Financial Frictions in the Euro Zone: Lessons from Canada Hotel "Grand

Credit Misallocation During the Financial Crisis

Credit Misallocation During the Financial Crisis Fabiano Schivardi 1 Enrico Sette 2 Guido Tabellini 3 1 LUISS and EIEF 2 Banca d Italia 3 Bocconi 4th Conference on Bank Performance, Financial Stability

Credit Misallocation During the Financial Crisis Fabiano Schivardi 1 Enrico Sette 2 Guido Tabellini 3 1 LUISS and EIEF 2 Banca d Italia 3 Bocconi 4th Conference on Bank Performance, Financial Stability

Portuguese Banking System: latest developments. 1 st quarter 2018

Portuguese Banking System: latest developments 1 st quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 27 th June of 218. Macroeconomic indicators and banking system data are quarterly

Portuguese Banking System: latest developments 1 st quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 27 th June of 218. Macroeconomic indicators and banking system data are quarterly

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

Effectiveness and Transmission of the ECB s Balance Sheet Policies

Effectiveness and Transmission of the ECB s Balance Sheet Policies Jef Boeckx NBB Maarten Dossche NBB Gert Peersman UGent Motivation There is a large literature that has used SVAR models to examine the

Effectiveness and Transmission of the ECB s Balance Sheet Policies Jef Boeckx NBB Maarten Dossche NBB Gert Peersman UGent Motivation There is a large literature that has used SVAR models to examine the

Monetary Policy Workshop on Strengthening

Monetary Policy Workshop on Strengthening Macroprudential Framework held by IMF Regional Office for Asia and Pacific (March 22~23, 2012, Tokyo) Macroprudential Policy Framework: The Case of Korea Tae Soo

Monetary Policy Workshop on Strengthening Macroprudential Framework held by IMF Regional Office for Asia and Pacific (March 22~23, 2012, Tokyo) Macroprudential Policy Framework: The Case of Korea Tae Soo

Bank Contagion in Europe

Bank Contagion in Europe Reint Gropp and Jukka Vesala Workshop on Banking, Financial Stability and the Business Cycle, Sveriges Riksbank, 26-28 August 2004 The views expressed in this paper are those of

Bank Contagion in Europe Reint Gropp and Jukka Vesala Workshop on Banking, Financial Stability and the Business Cycle, Sveriges Riksbank, 26-28 August 2004 The views expressed in this paper are those of

Credit Misallocation During the Financial Crisis

Credit Misallocation During the Financial Crisis Fabiano Schivardi 1 Enrico Sette 2 Guido Tabellini 3 1 Bocconi and EIEF 2 Banca d Italia 3 Bocconi ABFER Specialty Conference Financial Regulations: Intermediation,

Credit Misallocation During the Financial Crisis Fabiano Schivardi 1 Enrico Sette 2 Guido Tabellini 3 1 Bocconi and EIEF 2 Banca d Italia 3 Bocconi ABFER Specialty Conference Financial Regulations: Intermediation,

What s Driving Deleveraging? Evidence from the Survey of Consumer Finances

What s Driving Deleveraging? Evidence from the 2007-2009 Survey of Consumer Finances Karen Dynan Brookings Institution Wendy Edelberg Congressional Budget Office These slides were prepared for a presentation

What s Driving Deleveraging? Evidence from the 2007-2009 Survey of Consumer Finances Karen Dynan Brookings Institution Wendy Edelberg Congressional Budget Office These slides were prepared for a presentation

Systemic CCA A Model Approach to Systemic Risk

Conference on Beyond the Financial Crisis: Systemic Risk, Spillovers and Regulation Dresden, 28-29 October 2010 Andreas A Jobst International Monetary Fund Systemic CCA A Model Approach to Systemic Risk

Conference on Beyond the Financial Crisis: Systemic Risk, Spillovers and Regulation Dresden, 28-29 October 2010 Andreas A Jobst International Monetary Fund Systemic CCA A Model Approach to Systemic Risk

Macroeconomics of Finance

Macroeconomics of Finance Joanna Mackiewicz-Łyziak Lecture 12 Literature Borio C., 2012, The financial cycle and macroeconomics: What have we learnt?, BIS Working Papers No. 395. Business cycles Business

Macroeconomics of Finance Joanna Mackiewicz-Łyziak Lecture 12 Literature Borio C., 2012, The financial cycle and macroeconomics: What have we learnt?, BIS Working Papers No. 395. Business cycles Business

Financial Liberalization and Money Demand in Mauritius

Illinois State University ISU ReD: Research and edata Master's Theses - Economics Economics 5-8-2007 Financial Liberalization and Money Demand in Mauritius Rebecca Hodel Follow this and additional works

Illinois State University ISU ReD: Research and edata Master's Theses - Economics Economics 5-8-2007 Financial Liberalization and Money Demand in Mauritius Rebecca Hodel Follow this and additional works

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects Manju Puri (Duke) Jörg Rocholl (ESMT) Sascha Steffen (Mannheim) 3rd Unicredit Group Conference

Global Retail Lending in the Aftermath of the US Financial Crisis: Distinguishing between Supply and Demand Effects Manju Puri (Duke) Jörg Rocholl (ESMT) Sascha Steffen (Mannheim) 3rd Unicredit Group Conference

Banks Business Model and Credit in Chile: Mandates do Matter

Banks Business Model and Credit in Chile: Mandates do Matter Miguel Birón 1 Felipe Córdova 2 Antonio Lemus 3 Closing Conference of the BIS CCA CGDFS Working Group Mexico City, Mexico September 7, 2018

Banks Business Model and Credit in Chile: Mandates do Matter Miguel Birón 1 Felipe Córdova 2 Antonio Lemus 3 Closing Conference of the BIS CCA CGDFS Working Group Mexico City, Mexico September 7, 2018

If the Fed sneezes, who gets a cold?

If the Fed sneezes, who gets a cold? Luca Dedola Giulia Rivolta Livio Stracca (ECB) (Univ. of Brescia) (ECB) Spillovers of conventional and unconventional monetary policy: the role of real and financial

If the Fed sneezes, who gets a cold? Luca Dedola Giulia Rivolta Livio Stracca (ECB) (Univ. of Brescia) (ECB) Spillovers of conventional and unconventional monetary policy: the role of real and financial

Private and public risk-sharing in the euro area

Private and public risk-sharing in the euro area Jacopo Cimadomo (ECB) Oana Furtuna (ECB) Massimo Giuliodori (UvA) First Annual Workshop of ESCB Research Cluster 2 Medium- and long-run challenges for Europe

Private and public risk-sharing in the euro area Jacopo Cimadomo (ECB) Oana Furtuna (ECB) Massimo Giuliodori (UvA) First Annual Workshop of ESCB Research Cluster 2 Medium- and long-run challenges for Europe

Ninth UNCTAD Debt Management Conference

Ninth UNCTAD Debt Management Conference Geneva, 11-13 November 2013 Effective Debt Strategies in the Current Macroeconomic Environment by Mr. Phillip Anderson Senior Manager Government Debt and Risk Management

Ninth UNCTAD Debt Management Conference Geneva, 11-13 November 2013 Effective Debt Strategies in the Current Macroeconomic Environment by Mr. Phillip Anderson Senior Manager Government Debt and Risk Management

The Aggregate and Distributional Effects of Financial Globalization: Evidence from Macro and Sectoral Data

The Aggregate and Distributional Effects of Financial Globalization: Evidence from Macro and Sectoral Data Davide Furceri, Prakash Loungani and Jonathan D. Ostry International Monetary Fund IMF Annual

The Aggregate and Distributional Effects of Financial Globalization: Evidence from Macro and Sectoral Data Davide Furceri, Prakash Loungani and Jonathan D. Ostry International Monetary Fund IMF Annual

Financial Crises and Asset Prices. Tyler Muir June 2017, MFM

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Private Leverage and Sovereign Default

Private Leverage and Sovereign Default Cristina Arellano Yan Bai Luigi Bocola FRB Minneapolis University of Rochester Northwestern University Economic Policy and Financial Frictions November 2015 1 / 37

Private Leverage and Sovereign Default Cristina Arellano Yan Bai Luigi Bocola FRB Minneapolis University of Rochester Northwestern University Economic Policy and Financial Frictions November 2015 1 / 37

by Sankar De and Manpreet Singh

Comments on: Credit Rationing in Informal Markets: The case of small firms in India by Sankar De and Manpreet Singh Discussant: Johanna Francis (Fordham University and UCSC) CAFIN Workshop 25-26 April

Comments on: Credit Rationing in Informal Markets: The case of small firms in India by Sankar De and Manpreet Singh Discussant: Johanna Francis (Fordham University and UCSC) CAFIN Workshop 25-26 April

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Discussion of The Effects of Fed Policy on EME Bond Markets by J. Burger, F. Warnock and V. Warnock

Discussion of The Effects of Fed Policy on EME Bond Markets by J. Burger, F. Warnock and V. Warnock Carlos Viana de Carvalho, Central Bank of Brazil Santiago, Chile, November 2016 Twentieth Annual Conference

Discussion of The Effects of Fed Policy on EME Bond Markets by J. Burger, F. Warnock and V. Warnock Carlos Viana de Carvalho, Central Bank of Brazil Santiago, Chile, November 2016 Twentieth Annual Conference

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan The US recession that began in late 2007 had significant spillover effects to the rest

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan The US recession that began in late 2007 had significant spillover effects to the rest

Determinants of intra-euro area government bond spreads during the financial crisis

Determinants of intra-euro area government bond spreads during the financial crisis by Salvador Barrios, Per Iversen, Magdalena Lewandowska, Ralph Setzer DG ECFIN, European Commission - This paper does

Determinants of intra-euro area government bond spreads during the financial crisis by Salvador Barrios, Per Iversen, Magdalena Lewandowska, Ralph Setzer DG ECFIN, European Commission - This paper does

3 The leverage cycle in Luxembourg s banking sector 1

3 The leverage cycle in Luxembourg s banking sector 1 1 Introduction By Gaston Giordana* Ingmar Schumacher* A variable that received quite some attention in the aftermath of the crisis was the leverage

3 The leverage cycle in Luxembourg s banking sector 1 1 Introduction By Gaston Giordana* Ingmar Schumacher* A variable that received quite some attention in the aftermath of the crisis was the leverage

Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017)

") Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017) Signe Krogstrup 1 1 Research Department, International Monetary Fund Annual Research Conference

Discussion of The dollar exchange rate as a global risk factor: evidence from investment by Avdjiev et al. (2017) Signe Krogstrup 1 1 Research Department, International Monetary Fund Annual Research Conference

Analyzing the Determinants of Project Success: A Probit Regression Approach

2016 Annual Evaluation Review, Linked Document D 1 Analyzing the Determinants of Project Success: A Probit Regression Approach 1. This regression analysis aims to ascertain the factors that determine development

2016 Annual Evaluation Review, Linked Document D 1 Analyzing the Determinants of Project Success: A Probit Regression Approach 1. This regression analysis aims to ascertain the factors that determine development

Discussion of Why Has Consumption Remained Moderate after the Great Recession?

Discussion of Why Has Consumption Remained Moderate after the Great Recession? Federal Reserve Bank of Boston 60 th Economic Conference Karen Dynan Assistant Secretary for Economic Policy U.S. Treasury

Discussion of Why Has Consumption Remained Moderate after the Great Recession? Federal Reserve Bank of Boston 60 th Economic Conference Karen Dynan Assistant Secretary for Economic Policy U.S. Treasury

The Run for Safety: Financial Fragility and Deposit Insurance

The Run for Safety: Financial Fragility and Deposit Insurance Rajkamal Iyer- Imperial College, CEPR Thais Jensen- Univ of Copenhagen Niels Johannesen- Univ of Copenhagen Adam Sheridan- Univ of Copenhagen

The Run for Safety: Financial Fragility and Deposit Insurance Rajkamal Iyer- Imperial College, CEPR Thais Jensen- Univ of Copenhagen Niels Johannesen- Univ of Copenhagen Adam Sheridan- Univ of Copenhagen

Economics Letters 108 (2010) Contents lists available at ScienceDirect. Economics Letters. journal homepage:

Contents lists available at ScienceDirect. Economics Letters. journal homepage:") Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Lecture 3: Forecasting interest rates

Lecture 3: Forecasting interest rates Prof. Massimo Guidolin Advanced Financial Econometrics III Winter/Spring 2017 Overview The key point One open puzzle Cointegration approaches to forecasting interest

Lecture 3: Forecasting interest rates Prof. Massimo Guidolin Advanced Financial Econometrics III Winter/Spring 2017 Overview The key point One open puzzle Cointegration approaches to forecasting interest

International Monetary Policy Transmission through Banks in Small Open Economies. S. Auer, C. Friedrich, M. Ganarin, T. Paligorova, P.

International Monetary Policy Transmission through Banks in Small Open Economies S. Auer, C. Friedrich, M. Ganarin, T. Paligorova, P. Towbin Disclaimer The views expressed in this paper are our own and

International Monetary Policy Transmission through Banks in Small Open Economies S. Auer, C. Friedrich, M. Ganarin, T. Paligorova, P. Towbin Disclaimer The views expressed in this paper are our own and

Demographics and the behavior of interest rates

Demographics and the behavior of interest rates (C. Favero, A. Gozluklu and H. Yang) Discussion by Michele Lenza European Central Bank and ECARES-ULB Firenze 18-19 June 2015 Rubric Persistence in interest

Demographics and the behavior of interest rates (C. Favero, A. Gozluklu and H. Yang) Discussion by Michele Lenza European Central Bank and ECARES-ULB Firenze 18-19 June 2015 Rubric Persistence in interest

On Neutral Interest Rates in Latin America By Nicolas E. Magud and Evridiki Tsounta

On Neutral Interest Rates in Latin America By Nicolas E. Magud and Evridiki Tsounta Introduction An increasing number of Latin American countries have been strengthening their monetary policy frameworks

On Neutral Interest Rates in Latin America By Nicolas E. Magud and Evridiki Tsounta Introduction An increasing number of Latin American countries have been strengthening their monetary policy frameworks

The relationship amongst public debt and economic growth in developing country case of Tunisia

The relationship amongst public debt and economic growth in developing country case of Tunisia FERHI Sabrine Department of economic, FSEGT Faculty of Economics and Management Tunis Campus EL MANAR 1 sabrineferhi@yahoo.fr

The relationship amongst public debt and economic growth in developing country case of Tunisia FERHI Sabrine Department of economic, FSEGT Faculty of Economics and Management Tunis Campus EL MANAR 1 sabrineferhi@yahoo.fr

EUR Rates & FX QE perspectives on what s priced in. Martin Enlund, Chief Analyst FX Alexander Wojt, Analyst Fixed Income

EUR Rates & FX QE perspectives on what s priced in Martin Enlund, Chief Analyst FX Alexander Wojt, Analyst Fixed Income Summary: surprisingly little QE priced in Most analysts have over the past months

EUR Rates & FX QE perspectives on what s priced in Martin Enlund, Chief Analyst FX Alexander Wojt, Analyst Fixed Income Summary: surprisingly little QE priced in Most analysts have over the past months

Credit Spreads and the Macroeconomy

Credit Spreads and the Macroeconomy Simon Gilchrist Boston University and NBER Joint BIS-ECB Workshop on Monetary Policy & Financial Stability Bank for International Settlements Basel, Switzerland September

Credit Spreads and the Macroeconomy Simon Gilchrist Boston University and NBER Joint BIS-ECB Workshop on Monetary Policy & Financial Stability Bank for International Settlements Basel, Switzerland September

The Term Structure of Growth-at-Risk

The Term Structure of Growth-at-Risk Tobias Adrian (IMF), Federico Grinberg (IMF), Nellie Liang (Brookings), and Sherheryar Malik (IMF) BIS Research meeting on Pushing the Frontier of Central Bank s Macro

The Term Structure of Growth-at-Risk Tobias Adrian (IMF), Federico Grinberg (IMF), Nellie Liang (Brookings), and Sherheryar Malik (IMF) BIS Research meeting on Pushing the Frontier of Central Bank s Macro

Liquidity Matters: Money Non-Redundancy in the Euro Area Business Cycle

Liquidity Matters: Money Non-Redundancy in the Euro Area Business Cycle Antonio Conti January 21, 2010 Abstract While New Keynesian models label money redundant in shaping business cycle, monetary aggregates

Liquidity Matters: Money Non-Redundancy in the Euro Area Business Cycle Antonio Conti January 21, 2010 Abstract While New Keynesian models label money redundant in shaping business cycle, monetary aggregates

The Short and Long-Run Implications of Budget Deficit on Economic Growth in Nigeria ( )

") Canadian Social Science Vol. 10, No. 5, 2014, pp. 201-205 DOI:10.3968/4517 ISSN 1712-8056[Print] ISSN 1923-6697[Online] www.cscanada.net www.cscanada.org The Short and Long-Run Implications of Budget Deficit

Canadian Social Science Vol. 10, No. 5, 2014, pp. 201-205 DOI:10.3968/4517 ISSN 1712-8056[Print] ISSN 1923-6697[Online] www.cscanada.net www.cscanada.org The Short and Long-Run Implications of Budget Deficit

Portuguese Banking System: latest developments. 4 th quarter 2017

Portuguese Banking System: latest developments 4 th quarter 217 Lisbon, 218 www.bportugal.pt Prepared with data available up to 2 th March of 218. Macroeconomic indicators and banking system data are

Portuguese Banking System: latest developments 4 th quarter 217 Lisbon, 218 www.bportugal.pt Prepared with data available up to 2 th March of 218. Macroeconomic indicators and banking system data are

António Afonso, Jorge Silva Debt crisis and 10-year sovereign yields in Ireland and in Portugal

Department of Economics António Afonso, Jorge Silva Debt crisis and 1-year sovereign yields in Ireland and in Portugal WP6/17/DE/UECE WORKING PAPERS ISSN 183-181 Debt crisis and 1-year sovereign yields

Department of Economics António Afonso, Jorge Silva Debt crisis and 1-year sovereign yields in Ireland and in Portugal WP6/17/DE/UECE WORKING PAPERS ISSN 183-181 Debt crisis and 1-year sovereign yields

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

Using R for Regulatory Stress Testing Modeling

Using R for Regulatory Stress Testing Modeling Thomas Zakrzewski (Tom Z.,) Head of Architecture and Digital Design S&P Global Market Intelligence Risk Services May 19 th, 2017 requires the prior written

Using R for Regulatory Stress Testing Modeling Thomas Zakrzewski (Tom Z.,) Head of Architecture and Digital Design S&P Global Market Intelligence Risk Services May 19 th, 2017 requires the prior written

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

GDP, Share Prices, and Share Returns: Australian and New Zealand Evidence

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 Ninth BIS CCA Research Conference Rio de Janeiro June 2018 1 Previously presented as Cross-Section Skewness, Business Cycle Fluctuations

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 Ninth BIS CCA Research Conference Rio de Janeiro June 2018 1 Previously presented as Cross-Section Skewness, Business Cycle Fluctuations

Macro-prudential Policy: Israel

RETHINKING MACRO POLICY II: FIRST STEPS AND EARLY LESSONS APRIL 16 17, 2013 Macro-prudential Policy: Israel Stanley Fischer Governor, Bank of Israel Paper presented at the 13th Jacques Polak Annual Research

RETHINKING MACRO POLICY II: FIRST STEPS AND EARLY LESSONS APRIL 16 17, 2013 Macro-prudential Policy: Israel Stanley Fischer Governor, Bank of Israel Paper presented at the 13th Jacques Polak Annual Research

Stress Testing: Financial Sector Assessment Program (FSAP) Experience

Experience") Stress Testing: Financial Sector Assessment Program (FSAP) Experience Tomás Baliño Deputy Director Monetary and Financial Systems Department Paper presented at the Expert Forum on Advanced Techniques on

Stress Testing: Financial Sector Assessment Program (FSAP) Experience Tomás Baliño Deputy Director Monetary and Financial Systems Department Paper presented at the Expert Forum on Advanced Techniques on

New Evidence on the Lending Channel

New Evidence on the Lending Channel Adam B. Ashcraft 20 November, 2003 Abstract Affiliation with a multi-bank holding company gives a subsidiary bank better access to external funds than otherwise similar

New Evidence on the Lending Channel Adam B. Ashcraft 20 November, 2003 Abstract Affiliation with a multi-bank holding company gives a subsidiary bank better access to external funds than otherwise similar

Shocks to Bank Lending, Risk-Taking and Securitization, and their role for U.S. Business Cycle Fluctuations

Shocks to Bank Lending, Risk-Taking and Securitization, and their role for U.S. Business Cycle Fluctuations Gert Peersman Ghent University Wolf Wagner Tilburg University Motivation Better understanding

Shocks to Bank Lending, Risk-Taking and Securitization, and their role for U.S. Business Cycle Fluctuations Gert Peersman Ghent University Wolf Wagner Tilburg University Motivation Better understanding

Assessing Potential Inflation Consequences of QE after Financial Crises

Assessing Potential Inflation Consequences of QE after Financial Crises Samuel Reynard Economic Advisor International dimensions of conventional and unconventional monetary policy ECB-IMF Conference, Frankfurt,

Assessing Potential Inflation Consequences of QE after Financial Crises Samuel Reynard Economic Advisor International dimensions of conventional and unconventional monetary policy ECB-IMF Conference, Frankfurt,

Macro-Financial Linkages: Issues and Challenges

Macro-Financial Linkages: Issues and Challenges Presentation by: Dr. Yuba Raj Khatiwada Governor Nepal Rastra Bank at SEACEN s 30 th Anniversary Conference Kuala Lumpur, 20 October 2013 Background (1)

Macro-Financial Linkages: Issues and Challenges Presentation by: Dr. Yuba Raj Khatiwada Governor Nepal Rastra Bank at SEACEN s 30 th Anniversary Conference Kuala Lumpur, 20 October 2013 Background (1)

Using Balance Sheets for Fiscal Analysis and Policymaking Amanda Sayegh Fiscal Affairs Department International Monetary Fund

Using Balance Sheets for Fiscal Analysis and Policymaking Amanda Sayegh Fiscal Affairs Department International Monetary Fund Meeting of the IMF GFS Advisory Committee Washington, D.C. March 14, 2017 Overview

Using Balance Sheets for Fiscal Analysis and Policymaking Amanda Sayegh Fiscal Affairs Department International Monetary Fund Meeting of the IMF GFS Advisory Committee Washington, D.C. March 14, 2017 Overview

Impact of the Capital Requirements Regulation (CRR) on the access to finance for business and long-term investments Executive Summary

on the access to finance for business and long-term investments Executive Summary") Impact of the Capital Requirements Regulation (CRR) on the access to finance for business and long-term investments Executive Summary Prepared by The information and views set out in this study are those

Impact of the Capital Requirements Regulation (CRR) on the access to finance for business and long-term investments Executive Summary Prepared by The information and views set out in this study are those

Describing the Macro- Prudential Surveillance Approach

Describing the Macro- Prudential Surveillance Approach JANUARY 2017 FINANCIAL STABILITY DEPARTMENT 1 Preface This aim of this document is to provide a summary of the Bank s approach to Macro-Prudential

Describing the Macro- Prudential Surveillance Approach JANUARY 2017 FINANCIAL STABILITY DEPARTMENT 1 Preface This aim of this document is to provide a summary of the Bank s approach to Macro-Prudential

Cross-border spillovers of monetary policy: what changes during a banking crisis?

Cross-border spillovers of monetary policy: what changes during a banking crisis? Luciana Barbosa, Diana Bonfim, Sónia Costa (Banco de Portugal) Mary Everett (Central Bank of Ireland) (presenter) Disclaimer:

Cross-border spillovers of monetary policy: what changes during a banking crisis? Luciana Barbosa, Diana Bonfim, Sónia Costa (Banco de Portugal) Mary Everett (Central Bank of Ireland) (presenter) Disclaimer:

What Explains Growth and Inflation Dispersions in EMU?

JEL classification: C3, C33, E31, F15, F2 Keywords: common and country-specific shocks, output and inflation dispersions, convergence What Explains Growth and Inflation Dispersions in EMU? Emil STAVREV

JEL classification: C3, C33, E31, F15, F2 Keywords: common and country-specific shocks, output and inflation dispersions, convergence What Explains Growth and Inflation Dispersions in EMU? Emil STAVREV

Cross-border banking, parents bank performance and subsidiaries credit extensions: evidence from the CESEE region

Cross-border banking, parents bank performance and subsidiaries credit extensions: evidence from the CESEE region L U C A G A T T I N I A N D A N G E L I K I Z A G O R I S I O U S T A R E B E I F I N A

Cross-border banking, parents bank performance and subsidiaries credit extensions: evidence from the CESEE region L U C A G A T T I N I A N D A N G E L I K I Z A G O R I S I O U S T A R E B E I F I N A

Economic policies, financial stability and economic performance

This project has received funding from the European Union s Seventh Framework Programme for research, technological development and demonstration under grant agreement no 266800 Economic policies, financial

This project has received funding from the European Union s Seventh Framework Programme for research, technological development and demonstration under grant agreement no 266800 Economic policies, financial

Financial Regulation, Banking Integration, and Business Cycle Synchronization

Financial Regulation, Banking Integration, and Business Cycle Synchronization Elias Papaioannou (London Business School, CEPR, and NBER) European Investment Bank Luxembourg February 2014 1 Introduction

Financial Regulation, Banking Integration, and Business Cycle Synchronization Elias Papaioannou (London Business School, CEPR, and NBER) European Investment Bank Luxembourg February 2014 1 Introduction

Ministerial Conference on the Financial Crisis

UNECA Ministerial Conference on the Financial Crisis BRIEFING NOTE 1: The Current Financial Crisis: Impact on African Economies Ramada Plaza Hotel, Tunis, Tunisia November 12, 2008 1. Introduction The

UNECA Ministerial Conference on the Financial Crisis BRIEFING NOTE 1: The Current Financial Crisis: Impact on African Economies Ramada Plaza Hotel, Tunis, Tunisia November 12, 2008 1. Introduction The

An EM-Algorithm for Maximum-Likelihood Estimation of Mixed Frequency VARs

An EM-Algorithm for Maximum-Likelihood Estimation of Mixed Frequency VARs Jürgen Antony, Pforzheim Business School and Torben Klarl, Augsburg University EEA 2016, Geneva Introduction frequent problem in

An EM-Algorithm for Maximum-Likelihood Estimation of Mixed Frequency VARs Jürgen Antony, Pforzheim Business School and Torben Klarl, Augsburg University EEA 2016, Geneva Introduction frequent problem in

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1 Valentina Bruno, Ilhyock Shim and Hyun Song Shin 2 Abstract We assess the effectiveness of macroprudential policies

Effectiveness of macroprudential and capital flow measures in Asia and the Pacific 1 Valentina Bruno, Ilhyock Shim and Hyun Song Shin 2 Abstract We assess the effectiveness of macroprudential policies

Financial Intermediaries and Monetary Economics

Financial Intermediaries and Monetary Economics By T. Adrian and H. Shin Based on a series of papers by Adrian, Shin, and coauthors and forthcoming in Handbook of Monetary Economics Motivation This paper

Financial Intermediaries and Monetary Economics By T. Adrian and H. Shin Based on a series of papers by Adrian, Shin, and coauthors and forthcoming in Handbook of Monetary Economics Motivation This paper

Assessing the Systemic Risk Contributions of Large and Complex Financial Institutions

Assessing the Systemic Risk Contributions of Large and Complex Financial Institutions Xin Huang, Hao Zhou and Haibin Zhu IMF Conference on Operationalizing Systemic Risk Monitoring May 27, 2010, Washington

Assessing the Systemic Risk Contributions of Large and Complex Financial Institutions Xin Huang, Hao Zhou and Haibin Zhu IMF Conference on Operationalizing Systemic Risk Monitoring May 27, 2010, Washington

Macroeconomic Interdependence and the International Role of the Dollar

8TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 15-16, 2007 Macroeconomic Interdependence and the International Role of the Dollar Linda Goldberg Federal Reserve Bank of New York and NBER Cedric

8TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 15-16, 2007 Macroeconomic Interdependence and the International Role of the Dollar Linda Goldberg Federal Reserve Bank of New York and NBER Cedric

ESCB Sovereign Debt Sustainability Analysis: a methodological framework

ECB-UNRESTRICTED ESCB Sovereign Debt Sustainability Analysis: a methodological framework Cristina Checherita-Westphal ECB, Fiscal Policies Division ESM workshop on Debt sustainability: current practice

ECB-UNRESTRICTED ESCB Sovereign Debt Sustainability Analysis: a methodological framework Cristina Checherita-Westphal ECB, Fiscal Policies Division ESM workshop on Debt sustainability: current practice

Corporate Governance, Regulation, and Bank Risk Taking. Luc Laeven, IMF, CEPR, and ECGI Ross Levine, Brown University and NBER

Corporate Governance, Regulation, and Bank Risk Taking Luc Laeven, IMF, CEPR, and ECGI Ross Levine, Brown University and NBER Introduction Recent turmoil in financial markets following the announcement

Corporate Governance, Regulation, and Bank Risk Taking Luc Laeven, IMF, CEPR, and ECGI Ross Levine, Brown University and NBER Introduction Recent turmoil in financial markets following the announcement

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Effects of the U.S. Quantitative Easing on a Small Open Economy

Effects of the U.S. Quantitative Easing on a Small Open Economy César Carrera Fernando Pérez Nelson Ramírez-Rondán Central Bank of Peru November 5, 2014 Ramirez-Rondan (BCRP) US QE and Peru November 5,

Effects of the U.S. Quantitative Easing on a Small Open Economy César Carrera Fernando Pérez Nelson Ramírez-Rondán Central Bank of Peru November 5, 2014 Ramirez-Rondan (BCRP) US QE and Peru November 5,

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Liquidity & Treasury Management Conference. Reporting to the Board Writing a Winning Treasury Report

Liquidity & Treasury Management Conference Reporting to the Board Writing a Winning Treasury Report Martin Watts Head of Treasury, L&Q email: mwatts@lqgroup.org.uk Introduction Post TSA abolishment, the

Liquidity & Treasury Management Conference Reporting to the Board Writing a Winning Treasury Report Martin Watts Head of Treasury, L&Q email: mwatts@lqgroup.org.uk Introduction Post TSA abolishment, the

Financial Frictions and Risk Premiums

Financial Frictions and Swap Market Risk Premiums Kenneth J. Singleton and NBER Joint Research with Scott Joslin September 20, 2009 Introduction The global impact of the subprime crisis provides a challenging

Financial Frictions and Swap Market Risk Premiums Kenneth J. Singleton and NBER Joint Research with Scott Joslin September 20, 2009 Introduction The global impact of the subprime crisis provides a challenging

Online Appendix: Asymmetric Effects of Exogenous Tax Changes

Online Appendix: Asymmetric Effects of Exogenous Tax Changes Syed M. Hussain Samreen Malik May 9,. Online Appendix.. Anticipated versus Unanticipated Tax changes Comparing our estimates with the estimates

Online Appendix: Asymmetric Effects of Exogenous Tax Changes Syed M. Hussain Samreen Malik May 9,. Online Appendix.. Anticipated versus Unanticipated Tax changes Comparing our estimates with the estimates

The effect of macroprudential policies on credit developments in Europe

Katarzyna Budnik Martina Jasova European Central Bank The effect of macroprudential policies on credit developments in Europe 1995-2017 Joint European Central Bank and Central Bank of Ireland research

Katarzyna Budnik Martina Jasova European Central Bank The effect of macroprudential policies on credit developments in Europe 1995-2017 Joint European Central Bank and Central Bank of Ireland research

Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation

ECONOMIC BULLETIN 3/218 ANALYTICAL ARTICLES Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation Ángel Estrada and Francesca Viani 6 September 218 Following

ECONOMIC BULLETIN 3/218 ANALYTICAL ARTICLES Creditor countries and debtor countries: some asymmetries in the dynamics of external wealth accumulation Ángel Estrada and Francesca Viani 6 September 218 Following

2018 Dodd-Frank Act Annual Stress Test (DFAST) Filed with Board of Governors of the Federal Reserve System on April 5th, 2018 Including UBS Bank USA

Filed with Board of Governors of the Federal Reserve System on April 5th, 2018 Including UBS Bank USA") (DFAST) Filed with Board of Governors of the Federal Reserve System on April 5th, 2018 Including UBS Bank USA June, 2018 Cautionary statement This 2018 Dodd Frank Act Stress Test Disclosure presents stress

(DFAST) Filed with Board of Governors of the Federal Reserve System on April 5th, 2018 Including UBS Bank USA June, 2018 Cautionary statement This 2018 Dodd Frank Act Stress Test Disclosure presents stress

Clearing, Counterparty Risk and Aggregate Risk

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 Clearing, Counterparty Risk and Aggregate Risk Bruno Biais Toulouse School of Economics Florian Heider European Central Bank Marie Hoerova

12TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 10 11, 2011 Clearing, Counterparty Risk and Aggregate Risk Bruno Biais Toulouse School of Economics Florian Heider European Central Bank Marie Hoerova