Mega-Trends Influencing the Workers Compensation Insurance Industry

|

|

|

- Phyllis Bond

- 5 years ago

- Views:

Transcription

494-5945 stevenw@iii.org")

1 Mega-Trends Influencing the Workers Compensation Insurance Industry 12 th Annual National Workers Compensation Insurance ExecuSummit Uncasville CT, February 3, 2015 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information Institute 110 William Street New York, NY Office: Cell: (917)

2 Presentation Outline: 6 Mega-Trends 1. A Growing Exposure Base, but with a Different Mix of Risks 2. Workplace Safety Improvement Continues, but Room for More 3. Inflation, WC-style 4. Low Investment Returns 5. The Aging Workforce 6. The Obesity Epidemic 2

3 WC Profitability 3

4 Workers Comp Return on Net Worth, % 10.1% 9.6% 10.0% Profits down during and after a severe recession: cause and effect? 9% 9.0% 6% 6.9% 5.1% 6.2% 5.9% 7.1% 4.2% 3.9% 3% 2.4% 0% Sources: NAIC; Insurance Information Institute 4

5 14.9% 14.5% 14.0% 13.4% 12.5% 12.0% 11.9% 11.8% 11.4% 11.1% 10.3% 10.3% 9.9% 9.8% 9.4% 9.4% 9.1% 9.1% 8.9% 8.8% 8.4% 8.1% 7.8% 7.8% 7.8% Workers Comp Return on Net Worth, by State, % Top 25 States 12 states posted doubledigit profit percentages in WC in % 12% 10% 8% 6% 4% 2% 0% WY NY WV OH MI MT SD VT AR KS AK NH NM NV TX TX AL FL MO UT ND TN NE WA SC 5

6 3.0% 2.5% 2.5% 5.3% 5.2% 5.2% 5.2% 5.1% 4.8% 4.5% 4.3% 4.1% 3.6% 7.7% 7.6% 7.6% 7.5% 7.5% 7.3% 7.2% 6.7% 6.6% 6.4% 6.2% 6.1% 5.9% Workers Comp Return on Net Worth, by State, % Bottom 25 States 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% MN NC OR IL KY VA US IN PA AZ MA RI GA ID CO CT OK IA MD NJ ME LA HI CA DE WI 6

7 Workers Compensation Combined Ratio: P Does the WC line get in trouble once each decade? P Workers Comp underwriting results were the worst they have been in a decade but lately are improving. Sources: A.M. Best; Insurance Information Institute. Data for P are from Exhibit 6, Best s Special Report, U.S. Workers Compensation Results Sustain Recent Improvement, November 10,

8 1. A Growing Exposure Base, but with a Different Mix of Risks Health Care, Education, Services Will Lead 8

9 Jan- Feb Mar Apr- May Jun- Jul-11 Aug Sep Oct- Nov Dec Jan- Feb Mar Apr- May Jun- Jul-12 Aug Sep Oct- Nov Dec Jan- Feb Mar Apr- May Jun- Jul-13 Aug Sep Oct- Nov Dec Jan- Feb Mar Apr- May Jun- Jul-14 Aug Sep Oct- Nov Monthly Change in Nonfarm Employment, Thousands Average Monthly Gain 2011: 173, : 186, : 194, *: 240, The pace of job growth varies considerably from month to month. *Seasonally adjusted. Oct 2014 and Nov 2014 are preliminary data. Monthly gain for 2014 is average for January-November Sources: US Bureau of Labor Statistics; Insurance Information Institute 9

10 Nonfarm Payroll (Wages and Salaries), Quarterly, :Q3 Billions $7,750 $7,500 $7,250 $7,000 $6,750 $6,500 $6,250 $6,000 $5,750 $5,500 Prior Peak was 2008:Q3 at $6.54 trillion Recent trough (2009:Q1) was $6.23 trillion, down 5.3% from prior peak Latest (2014:Q3) was $7.46 trillion, a new peak 05:Q1 05:Q2 05:Q3 05:Q4 06:Q1 06:Q2 06:Q3 06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2 09:Q3 09:Q4 10:Q1 10:Q2 10:Q3 10:Q4 11:Q1 11:Q2 11:Q3 11:Q4 12:Q1 12:Q2 12:Q3 12:Q4 13:Q1 13:Q2 13:Q3 13:Q4 14:Q1 14:Q2 14:Q3 Note: Recession indicated by gray shaded column. Data are seasonally adjusted annual rates. Sources: National Bureau of Economic Research (recession dates); Insurance Information Institute. 10

11 Workers Comp Net Written Premiums vs. Payroll, :Q3 Payroll Base* $Billions $8,000 $7,000 $6,000 $5,000 $4,000 $3,000 Wage & Salary Disbursements WC NPW 7/90-3/91 3/01-11/01 WC premium volume dropped two years before the recession began 12/07-6/09 WC NWP $Billions $50 $45 $40 $35 $30 $2, :3Q Continued Payroll Growth and Rate Increases Suggest WC NWP Will Grow Again in 2015 $25 *Private employment; Shaded areas indicate recessions. Sources: NBER (recessions); Federal Reserve Bank of St. Louis at ; NCCI; I.I.I. 11

12 1/31/2010 2/28/2010 3/31/2010 4/28/2010 5/31/2010 6/30/2010 7/31/2010 8/31/2010 9/30/ /30/ /30/ /30/2010 1/31/2011 2/28/2011 3/31/2011 4/28/2011 5/31/2011 6/30/2011 7/31/2011 8/31/2011 9/30/ /30/ /30/ /30/2011 1/30/2012 2/30/2012 3/30/2012 4/30/2012 5/30/2012 6/30/2012 7/30/2012 8/30/2012 9/30/ /30/ /30/ /30/2012 1/30/2013 Feb-13 3/30/2013 4/30/2013 5/30/2013 6/30/2013 7/30/2013 8/30/2013 9/30/ /30/ /30/ /31/2013 1/31/2014 2/28/2014 3/31/2014 4/30/2014 5/31/2014 6/30/2014 7/31/2014 8/31/2014 9/30/ /31/ /30/2014 5,587 5,508 5,536 5,555 5,524 5,512 5,502 5,525 5,503 5,507 5,504 5,462 5,432 5,464 5,475 5,496 5,520 5,524 5,551 5,553 5,590 5,584 5,585 5,606 5,627 5,622 5,627 5,630 5,613 5,620 5,635 5,647 5,648 5,666 5,687 5,720 5,743 5,789 5,813 5,811 5,816 5,829 5,830 5,836 5,849 5,864 5,896 5,876 5,927 5,951 5,964 6,000 6,009 6,017 6,047 6,064 6,082 6,089 6,109 Construction Employment, Jan November 2014* (Thousands) 6,200 6,100 6,000 5,900 5,800 5,700 5,600 5,500 Construction employment is +677,000 above Jan (+12.5%). 5,400 Construction and manufacturing employment constitute 1/3 of all workers comp payroll exposure. *Seasonally adjusted; Oct and Nov 2014 are preliminary Sources: US Bureau of Labor Statistics at Insurance Information Institute. 12

13 Manufacturing Employment, Monthly, January 2010 November 2014* 11,462 11,453 11,458 11,493 11,527 11,543 11,571 11,550 11,557 11,557 11,581 11,592 11,620 11,653 11,675 11,704 11,711 11,723 11,755 11,763 11,766 11,773 11,771 11,798 11,837 11,859 11,901 11,916 11,928 11,939 11,979 11,956 11,942 11,947 11,951 11,965 11,982 12,004 12,007 12,001 11,994 11,991 11,982 11,990 11,993 12,011 12,046 12,053 12,061 12,081 12,085 12,094 12,109 12,130 12,154 12,157 12,169 12,189 12,217 1/31/ 2/28/ 3/31/ 4/28/ 5/31/ 6/30/ 7/31/ 8/31/ 9/30/ 10/30 11/30 12/30 1/31/ 2/28/ 3/31/ 4/28/ 5/31/ 6/30/ 7/31/ 8/31/ 9/30/ 10/30 11/30 12/30 1/30/ 2/30/ 3/30/ 4/30/ 5/30/ 6/30/ 7/30/ 8/30/ 9/30/ 10/30 11/30 12/30 1/31/ 2/28/ 3/31/ 4/30/ 5/31/ 6/30/ 7/31/ 8/31/ 9/30/ 10/31 11/30 12/31 1/31/ 2/28/ 3/31/ 4/30/ 5/31/ 6/30/ 7/31/ 8/31/ 9/30/ 10/31 11/30 (Thousands) 12,500 Manufacturing employment is 750,000+ above Jan (+6.6%) and still growing. 12,250 12,000 11,750 11,500 11,250 11,000 Manufacturing employment is a surprising source of strength in the economy. Employment in the sector is at a multi-year high. *Seasonally adjusted; Oct and Nov 2014 are preliminary Sources: US Bureau of Labor Statistics at Insurance Information Institute. 13

14 U.S. Employment in Health Care & Social Services, Monthly, * 1/31/1990 9/30/1990 5/31/1991 1/31/1992 9/30/1992 5/31/1993 1/31/1994 9/30/1994 5/31/1995 1/31/1996 9/30/1996 5/31/1997 1/31/1998 9/30/1998 5/31/1999 1/31/2000 9/30/2000 5/31/2001 1/31/2002 9/30/2002 5/31/2003 1/31/2004 9/30/2004 5/31/2005 1/31/2006 9/30/2006 5/31/2007 1/31/2008 9/30/2008 5/31/2009 1/31/2010 9/30/2010 5/31/2011 1/31/2012 9/30/2012 5/31/2013 1/31/2014 9/30/2014 Millions Employment in the health care and social service sector grew in virtually every month for the last 24 years, unaffected by recessions, Cumulative growth over 25 years: 100.1% and this growth is expected to continue indefinitely 9 HC & SS employment *As of Nov 2014 (Nov 2014 and Oct 2014 are preliminary); Seasonally adjusted Note: Recessions indicated by gray shaded columns. Sources: US Bureau of Labor Statistics; National Bureau of Economic Research (recession dates); Insurance Information Institute. 14

15 2. Workplace Safety Improvement Continues, but Room for More The WC industry has certainly helped create/support the improvement 15

16 Fewer Occupational Deaths p Number of Fatal Injuries 7,000 6,500 6,000 5,500 6,217 6,331 6,632 6,275 6,202 6,238 6,055 6,054 5,920 5,915 5,534 5,575 5,764 5,734 5,840 5,657 5,214 5,000 4,500 4,551 4,690 4,693 4,628 4,405 4,000 3, p The death rate per 100,000 full-time-equivalent workers was 3.2 in 2013, down from 3.4 in 2012 and 3.5 in p = preliminary; final data will be released in late Spring 2015 Source: U.S. Bureau of Labor Statistics, National Census of Fatal Occupational Injuries in 2013 (Preliminary Results), released September 11,

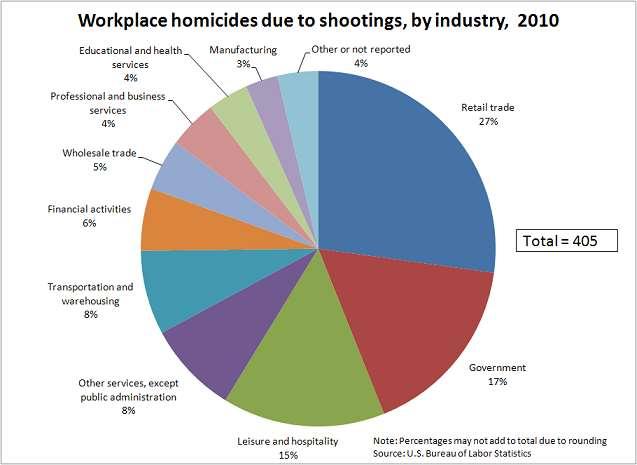

17 Number of Workplace Homicides,

18 18

19 407, , , , , , , , , , , , , , , , , , , , , ,560 Private Industry: Fewer Injuries & Illnesses with Days Away from Work Number 1,000, ,000 Goods-producing, 2013 vs. 2003: down 43.7% service-producing goods-producing Service-producing, 2013 vs. 2003: down 24.3% Slight increase because employment rose. 600, , , The total number of illnesses and injuries dropped from 2003 to 2007 despite growth in employment and the aging of the workforce. The drop continued through the Great Recession. Source: U.S. Bureau of Labor Statistics, National Occupational Injuries and Illnesses Requiring Days Away from Work, 2013, Table 1, released December 16, 2014: 19

20 Accidents per 10,000 Full-Time Private Workers, Healthcare Workers Are Injured by Violence at Almost Four Times the National Rate. Contact With Objects Much Less Common in Healthcare Fall on Same Level Violence Contact With Objects Lifting/Lowering Slip, No Fall Health Care and Social Assistance Service Producing Total Private 167,150 Lost-Time Injuries and Illnesses in the Healthcare Sector in 2013, 13% a Result of Violence. Source: U.S. Bureau of Labor Statistics, National Occupational Injuries and Illnesses Requiring Days Away from Work, 2013, Table 1, released December 16, 2014: 20

21 3. Inflation and Claim Severity The Low CPI Doesn t Reflect WC Cost Pressures 21

22 Workers Compensation Medical Severity Moderate Increase in 2011 Medical Claim Cost ($000s) Annual Change : +1.9% Annual Change : +8.9% Annual Change : +6.0% $8.1 Cumulative Change = 245% ( p) +6.8%+1.3%-2.1% +9.0%+5.1%+7.4% $8.2 $8.1 $8.8 $9.2 Average Medical Cost per Lost-Time Claim $ % +7.3% +10.1% +8.3% $10.9 $11.8 $13.1 $ % +5.4% +8.8% +13.5% $15.9 $17.3 Accident Year 2011p: Preliminary based on data valued as of 12/31/ : Based on data through 12/31/2010, developed to ultimate. Based on the states where NCCI provides ratemaking services; Excludes high 22 deductible policies. $18.7 $ % +5.9% +8.5% $21.3 $22.6 $ % +6.1% $25.5 $26.6 $ % +1.3% p $28.0

23 WC Medical Severity No Longer Rising Faster Than the Medical CPI Rate 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% 8.8% 4.7% 7.7% 5.4% 7.8% 5.8% 6.1% 4.0% 4.4% 4.2% 4.0% 4.4% Change in Medical CPI The average annual growth in WC medical severity from 2002 through 2009 was over 6% vs. the medical CPI (about 4%), which itself was higher than the overall CPI 6.8% 3.7% Change Med Cost per Lost Time Claim 4.0% 3.2% 3.4% 3.0% 1.2% but since 2010 growth in WC medical severity has closely tracked the medical CPI 2.6% 3.0% 3.0% 3.5% 2.5% 2.3% * *I.I.I. estimate based on data through October 2014 Sources: CPI and Med CPI from US Bureau of Labor Statistics, WC med severity from NCCI based on NCCI states.

24 Workers Comp Indemnity Claim Costs, p Indemnity Claim Cost ($ 000s) Average Indemnity Cost per Lost-Time Claim Average indemnity costs per claim have been at or below $22,500 since % +1.0% -3.1% -2.8% +4.9% +1.7% $9.2 $9.7 $9.8 $10.4 $11.2 $ % $ % $ % +3.6% +4.6% +3.1% +10.1% +10.1%+9.2% $16.2 $16.7 $17.5 $17.6 $18.3 $19.3 $ %+6.5% +0.6% p $22.3 $20.8 $21.9 $22.1 $22.2 $22.7 Accident Year 2010p: Preliminary based on data valued as of 12/31/ : Based on data through 12/31/2010, developed to ultimate Based on the states where NCCI provides ratemaking services Excludes high deductible policies

25 % 10% 8% 6% 4% 2% 0% WC Indemnity Severity No Longer Grows Faster than Wages, % 5.9% 7.7% 1.7% 2.3% 2.7% 9.0% 10.1% 10.1% 9.2% 5.0%4.9% 4.0% 3.5% Change in Median Usual Weekly Earnings Change in Indemnity Cost per Lost-Time Claim 4.6% 3.1% 3.1% 5.9% 6.5% 9.1% 2.9% 3.1% 3.6%3.9% 2.0% 2.4% 1.0% 1.1% 1.1% 2.0%2.0% 0.5% 2.0% 1.0% 1.2% 1.6% 1.0% -2% -4% -2.7% NCCI data on WC severity is based on the states where NCCI provides ratemaking services. Excludes the effects of deductible policies. Sources: NCCI, BLS, from Current Population Survey

26 4. Low Investment Returns 26

27 Jan-90 Jan-91 Jan-92 Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 9% 8% 7% U.S. Treasury 2- and 10-Year Note Yields*: Yields on 10-Year U.S. Treasury Notes have been essentially below 5% for over a dozen years. 6% 5% U.S. Treasury 10-year note yields spiked 4% 3% 2% 1% Recession 2-Yr Yield 10-Yr Yield 0% Since roughly 80% of P/C bond/cash investments are in 10-year or shorter durations, most P/C insurer portfolios will have low-yielding bonds for years to come. *Monthly, constant maturity, nominal rates, through December Sources: Federal Reserve Bank at National Bureau of Economic Research (recession dates); Insurance Information Institutes. 27

28 Long-Term Reduction in the Level of Investment Earnings: Outlook Fed actions will likely keep interest rates low for at least 2015 In a prolonged period of low interest rates, each year maturing higher-rate bonds are replaced with lower rates, building in a low portfolio yield that will last for the duration of the newer bonds Industry must be prepared to operate in an environment in which investment returns are a much smaller fraction of profits Drives rates higher? Regulators will not accept this Stiffens underwriting discipline? Yet to manifest itself Source: Insurance Information Institute. 28

29 5. The Aging Workforce 29

30 Labor Force Participation Rate, Ages 65-69, Quarterly, 1998:Q1-2014:Q4 Labor Force participation rate 34% 32% 30% 28% 26% 24% 22% 20% 22.1% 22.5% 22.3% 23.0% 22.8% 23.0% 22.9% 23.5% 24.4% 24.4% 24.3% 24.9% 24.4% 24.4% 24.8% The brown bars indicate recessions in 3 in this age group are working. Virtually none of them are baby boomers % 25.2% 26.3% 26.5% 26.2% 27.9% 27.2% % % 27.9% 27.3% 27.8% 27.6% 26.8% 27.6% 29.3% 29.5% 27.9% 28.5% 28.7% % 29.3% 30.1% 29.1% 30.3% 30.1% 30.9% 31.0% 30.7% 31.0% 31.4% 30.9% 31.2% 31.6% 31.3% 31.5% 31.4% 32.8% 32.3% 31.1% 32.2% 32.2% 32.5% 31.8% 31.8% 31.7% 32.9% 32.1% 31.8% 31.6% 31.9% 31.3% 31.5% The switch from DB pension plans (with early-retirement incentives) to DC plans (with, in effect, later-retirement incentives) might be partly responsible for raising this rate. Not seasonally adjusted. Sources: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute

31 Labor Force Participation Rate, Ages 70-74, Quarterly, 1998:Q1-2014:Q4 Labor Force participation rate 20% 18% 16% 14% 12% 12.5% 12.2% 12.4% 12.4% 12.9% 13.1% 13.6% Nearly 1 in 5 in this age group is working. 15 years ago it was 1 in % 13.3% 13.5% 13.6% 13.8% 14.4% 13.7% 14.2% 14.2% 13.8% 14.2% 14.0% 14.0% 14.4% 14.4% 14.6% 14.9% 14.9% 15.4% 15.6% 15.3% 16.4%17.0% 15.8% 16.2%16.7% 16.9% 17.2% 17.0% 16.7% 16.8% 18.0% 17.5% 17.3% 16.9% 18.6% 18.2% 17.7% 17.9% 18.9% 19.2% 18.0% 18.1% 17.4% 18.4% 18.0% 18.4% 19.3% 19.5% 19.2% 19.1% 19.9% 19.6% 18.8% 19.3% 19.7% 19.0% 19.0% 19.0% 18.9% 18.8% 10% The labor force participation rate for workers grew by about 50% since Growth in the participation rate has stalled at about 19% since Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute

32 Labor Force Participation Rate, Ages 70-74, Quarterly, 1998:Q1-2014:Q4 Labor Force participation rate 26% 24% 22% 20% 18% 16% 14% 12% 10% 8% Nearly 1 in 4 men and 1 in 7 women in this age group is working. The percent of women working has nearly doubled The labor force participation rate for workers grew by about 50% since Growth in the participation rate has stalled at about 19% since Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute

33 Labor Force Participation Rate, Quarterly Ages 75 and over, :Q4 Labor Force participation rate 9% 7% 5% 4.5% 4.6% 4.6% 5.0% 4.8% 5.1% 5.4% 5.2% 5.4% 5.3% 5.2% 5.3% 5.2% 5.2% 5.1% The labor force participation rate for workers 75 and over could hit 10% soon. This is close to what the rate was for the group a decade ago. 5.4% 5.1% 5.1% 5.2% 5.0% 5.5%5.9% 5.8% 5.8% 5.9% 6.0% 6.1% 6.5% 6.1% 6.6% 6.3% 6.7% 6.4% 6.6% 6.0% 6.5% 6.5% 7.1% 7.0% 6.9% 6.9% 7.2% 7.4% 7.6% 7.6% 7.0% 7.2% 7.3% 7.3% 6.9% 7.7% 7.5% 7.1% 7.5% 7.6% 7.7% 7.6% 7.6% 7.4% 7.8% 8.6% 7.9% 7.4% 7.7% 8.3% 8.0% 7.6% 8.0% 3% In the last 15 years, the labor force participation rate for workers 75 and over grew from 4.5% to 8.6% (in 2013:Q1), but has since fallen slightly. Sources: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

34 Labor Force Participation Rate, Quarterly Ages 75 and over, :Q4 Labor Force participation rate 14% 12% Nearly 1 in 8 men in this age group is working. 10% 8% 6% 4% 2% The percent of women in this age group that is working has doubled. 0% The labor force participation rate for workers 75 and over has doubled since 1998, but growth in the participation rate has slowed recently. Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute

35 Fatal Work Injury Rates Improved Slightly Since 2006 but Still Climb Sharply With Age Fatal Work Injury Rate per 100,000 full-time-equivalent workers The fatality rate for workers 65 and older was 4 times that of workers age The workplace of the future will have to be completely redesigned to accommodate the surge in older workers data are preliminary Source: U.S. Bureau of Labor Statistics, at 35

36 Median Days Away From Work Older Workers Lose More Days from Work Due to Injury or Illness Youngest baby boomer is age 51 (in 2015) Oldest baby boomer is age 69 (in 2015) Median lost time of workers age 65+ is 2-3X that of workers age These numbers are pretty stable they haven t changed much since Source: US Bureau of Labor Statistics, Nonfatal Occupational Injuries and Illnesses Requiring Days Away From Work, 2013 (Table 10), released December 16,

37 Percent of Days-Away-from-Work Cases, by Days Lost and Age Group, day 2 days 3-5 days 6-10 days days days 31 days or more Over one-third of days-lost cases of older workers involved a month or more away from work. And virtually 9 of 10 cases were for at least two days, compared to 8 of 10 for the youngest workers. Source: US Bureau of Labor Statistics, Nonfatal Occupational Injuries and Illnesses Requiring Days Away From Work, 2012 (Table 10), released November 26,

38 Percent of Days-Away-from-Work Cases, by Days Lost and Age Group, day 2 days 3-5 days 6-10 days days days 31 days or more Over one-third of days-lost cases of older workers involved a month or more away from work. And over 9 of 10 cases were for at least two days, compared to 8 of 10 for the youngest workers. Source: US Bureau of Labor Statistics, Nonfatal Occupational Injuries and Illnesses Requiring Days Away From Work, 2012 (Table 10), released November 26,

39 Older Workers Are Much More Likely to Break a Bone Incidence Rate* (2012) Fractures Multiple Traumatic Injuries *per 10,000 full-time-equivalent workers Source: US Bureau of Labor Statistics, US Department of Labor at Table 14 39

40 Older Workers Are Much More Likely to Break a Bone Incidence Rate* (2013) Fractures Multiple Traumatic Injuries *per 10,000 full-time-equivalent workers Source: US Bureau of Labor Statistics, US Department of Labor at Table 14 40

41 Older Workers Are More Likely Than Younger Workers to Slip/Fall, but Less Likely to Overexert Themselves Incidence Rate (2012) Source/Nature of Injury: Falls, slips, trips Overexertion Source: US Bureau of Labor Statistics, US Department of Labor at Table 14 41

42 Older Workers Are More Likely Than Younger Workers to Slip/Fall, but Less Likely to Overexert Themselves Incidence Rate (2013) Source/Nature of Injury: Falls, slips, trips Overexertion Source: US Bureau of Labor Statistics, US Department of Labor at Table 14 42

43 6. The Obesity Epidemic In 1994, in no state was the percent of adults who were obese as high as 20%. By 2010, all 50 states had adult obesity rates of 20% or more. In 18 states in 2013, 30% of the adults were obese. 43

44 Obesity Trends Among U.S. Adults BRFSS, 1994 Source: 44

45 Obesity Trends Among U.S. Adults BRFSS, 2013 Source:

46 Lost Workdays per 100 FTEs Claims per 100 FTEs The Most Obese Workers File Twice as Many WC Claims as Healthy-Weight Workers BMI <18.5 (Underweight) The most obese have twice as many claims and 13 times more lost workdays than healthy weight workers (Healthy Weight) (Overweight) (Obese (Obese Class I) Class II) (Obese Class III) Lost Workdays Claims Source: Ostbye, T., et al, Obesity and Workers Compensation, Archives of Internal Medicine, April 23,

47 $7,109 $3,924 $7,503 $5,396 $13,338 $13,569 $19,661 $23,633 $23,373 $34,293 $51,091 $59,178 WC Medical Claims and Indemnity Costs are 5-10x Higher for the Most Obese Workers $70,000 $60,000 Indemnity costs are 11 times higher for the most obese workers than for healthy-weight workers. $50,000 $40,000 $30,000 $20,000 $10,000 $0 BMI <18.5 (Underweight) (Healthy Weight) (Overweight) (Obese Class I) (Obese Class II) 40+ (Obese Class III) Medical Claims Costs Indemnity Claims Costs Source: Ostbye, T., et al, Obesity and Workers Compensation, Archives of Internal Medicine, April 23,

48 Additional (to WC) Costs of Obese Workers Estimated Per Capita Costs $6,000 $5,000 $4,000 The most obese workers cost employers for greater medical care and by being less productive (by being absent more and being less productive when at work. $3,792 $3,000 $2,000 $1,010 $1,026 $1,000 $0 $657 $391 $277 $1,269 $85 $0 $824 $148 $ (Overweight) (Obese Class I) (Obese Class II) 40+ (Obese Class II) Medical Claims Costs Absenteeism Presenteeism Source: Finkelstein, E., et al, The Costs of Obesity in the Workplace, Journal of Occupational and Environmental Medicine, Volume 52, No. 10 (October 2010), pp

49 Insurance Information Institute Online: Thank you for your time and your attention!

P/C Insurance Industry Overview & Outlook

P/C Insurance Industry Overview & Outlook Alexander & Schmidt Loss Control Forum 2016 Portland, ME September 14, 2016 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information

P/C Insurance Industry Overview & Outlook Alexander & Schmidt Loss Control Forum 2016 Portland, ME September 14, 2016 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information

2016 Workers compensation premium index rates

2016 Workers compensation premium index rates NH WA OR NV CA AK ID AZ UT MT WY CO NM MI VT ND MN SD WI NY NE IA PA IL IN OH WV VA KS MO KY NC TN OK AR SC MS AL GA TX LA FL ME MA RI CT NJ DE MD DC = Under

2016 Workers compensation premium index rates NH WA OR NV CA AK ID AZ UT MT WY CO NM MI VT ND MN SD WI NY NE IA PA IL IN OH WV VA KS MO KY NC TN OK AR SC MS AL GA TX LA FL ME MA RI CT NJ DE MD DC = Under

Economic Trends, Challenges, and Opportunities Affecting the P/C and Surety LOB

Economic Trends, Challenges, and Opportunities Affecting the P/C and Surety LOB New Jersey Surety Association September 13, 2012 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist

Economic Trends, Challenges, and Opportunities Affecting the P/C and Surety LOB New Jersey Surety Association September 13, 2012 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist

Plunging Crude Prices: Impact on U.S. and State Economies

Plunging Crude Prices: Impact on U.S. and State Economies Mine Yücel Senior Vice President and Director of Research August 7, 215 Oil and gas prices plunge Nominal price, $, weekly 16 14 12 Oil Price 1

Plunging Crude Prices: Impact on U.S. and State Economies Mine Yücel Senior Vice President and Director of Research August 7, 215 Oil and gas prices plunge Nominal price, $, weekly 16 14 12 Oil Price 1

Florida 1/1/2016 Workers Compensation Rate Filing

Florida 1/1/2016 Workers Compensation Rate Filing Kirt Dooley, FCAS, MAAA October 21, 2015 1 $ Billions 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Florida s Workers Compensation Premium Volume 2.368 0.765 0.034

Florida 1/1/2016 Workers Compensation Rate Filing Kirt Dooley, FCAS, MAAA October 21, 2015 1 $ Billions 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Florida s Workers Compensation Premium Volume 2.368 0.765 0.034

Mega-Trends Influencing the Workers Compensation Insurance Industry

Mega-Trends Influencing the Workers Compensation Insurance Industry 5th Annual National Workers Compensation Insurance ExecuSummit New York, NY February 5, 2008 Steven N. Weisbart, Ph.D., CLU, Vice President

Mega-Trends Influencing the Workers Compensation Insurance Industry 5th Annual National Workers Compensation Insurance ExecuSummit New York, NY February 5, 2008 Steven N. Weisbart, Ph.D., CLU, Vice President

Today s Uncertain Economy: Implications for P/C Insurance

Today s Uncertain Economy: Implications for P/C Insurance CAMAR Spring Meeting Great Valley, PA May 24, 2018 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information

Today s Uncertain Economy: Implications for P/C Insurance CAMAR Spring Meeting Great Valley, PA May 24, 2018 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information

Texas Economic Outlook: Cruising in Third Gear

Texas Economic Outlook: Cruising in Third Gear Keith Phillips Assistant Vice President and Senior Economist 1/19/17 The views expressed in this presentation are strictly those of the presenter and do not

Texas Economic Outlook: Cruising in Third Gear Keith Phillips Assistant Vice President and Senior Economist 1/19/17 The views expressed in this presentation are strictly those of the presenter and do not

Texas Economic Outlook: Strong Growth Continues

Texas Economic Outlook: Strong Growth Continues Keith Phillips Assistant Vice President and Senior Economist 1/23/18 The views expressed in this presentation are strictly those of the presenter and do

Texas Economic Outlook: Strong Growth Continues Keith Phillips Assistant Vice President and Senior Economist 1/23/18 The views expressed in this presentation are strictly those of the presenter and do

Zions Bank Economic Overview

Zions Bank Economic Overview Jackson Hole Mountain Resort March 20, 2018 National Economic Conditions When Good News is Bad News Is Good News?? Dow Tops 26,000 Up 44% Since 2016 Election Source: Wall Street

Zions Bank Economic Overview Jackson Hole Mountain Resort March 20, 2018 National Economic Conditions When Good News is Bad News Is Good News?? Dow Tops 26,000 Up 44% Since 2016 Election Source: Wall Street

2018 Texas Economic Outlook: Firing on All Cylinders

218 Texas Economic Outlook: Firing on All Cylinders Keith Phillips Assistant Vice President and Senior Economist 4/5/218 The views expressed in this presentation are strictly those of the presenter and

218 Texas Economic Outlook: Firing on All Cylinders Keith Phillips Assistant Vice President and Senior Economist 4/5/218 The views expressed in this presentation are strictly those of the presenter and

Older consumers and student loan debt by state

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

Black Knight Mortgage Monitor

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of May, 2014 Month-end Black Knight First Look May 2014 Total U.S. loan delinquency rate (loans 30 or more days past due,

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of May, 2014 Month-end Black Knight First Look May 2014 Total U.S. loan delinquency rate (loans 30 or more days past due,

Zions Bank Economic Overview

Zions Bank Economic Overview Utah League of Cities and Towns June 18, 2018 Utah Economic Conditions CA 0.6% OR 1.4% WA 1.7% NV 2.0% Utah Population 3 rd Fastest Growing in U.S. ID 2.2% UT 1.9% AZ 1.6%

Zions Bank Economic Overview Utah League of Cities and Towns June 18, 2018 Utah Economic Conditions CA 0.6% OR 1.4% WA 1.7% NV 2.0% Utah Population 3 rd Fastest Growing in U.S. ID 2.2% UT 1.9% AZ 1.6%

ehealth, Inc Fall Cost Report for Individual and Family Policyholders

ehealth, Inc. 2010 Fall Cost Report for and Family Policyholders Table of Contents Page Methodology.................................................................. 2 ehealth, Inc. 2010 Fall Cost Report

ehealth, Inc. 2010 Fall Cost Report for and Family Policyholders Table of Contents Page Methodology.................................................................. 2 ehealth, Inc. 2010 Fall Cost Report

Texas Mid-Year Economic Outlook: Strong Growth Continues

Texas Mid-Year Economic Outlook: Strong Growth Continues Keith Phillips Assistant Vice President and Senior Economist 9/27/18 The views expressed in this presentation are strictly those of the presenter

Texas Mid-Year Economic Outlook: Strong Growth Continues Keith Phillips Assistant Vice President and Senior Economist 9/27/18 The views expressed in this presentation are strictly those of the presenter

Recap of 2017: The Best Year in a Decade

NOVEMBER 217 Recap of 217: The Best Year in a Decade Macroeconomic conditions remained favorable for housing and mortgage markets in 217. Despite challenges, the housing markets remain on track for their

NOVEMBER 217 Recap of 217: The Best Year in a Decade Macroeconomic conditions remained favorable for housing and mortgage markets in 217. Despite challenges, the housing markets remain on track for their

Refinance Report August 2012

This report contains data on refinance program activity of Fannie Mae and Freddie Mac (the Enterprises) through. Report Highlights Refinance volume continued to be strong in August as 30-year mortgage

This report contains data on refinance program activity of Fannie Mae and Freddie Mac (the Enterprises) through. Report Highlights Refinance volume continued to be strong in August as 30-year mortgage

Plunging Oil Prices: Impact on the U.S. and State Economies

Plunging Oil Prices: Impact on the U.S. and State Economies Mine Yücel Senior Vice President and Director of Research November 17, 216 Nominal price, weekly 16 14 Oil and gas prices volatile 12 1 Oil price

Plunging Oil Prices: Impact on the U.S. and State Economies Mine Yücel Senior Vice President and Director of Research November 17, 216 Nominal price, weekly 16 14 Oil and gas prices volatile 12 1 Oil price

Maximizing Your State of the Line Experience

Maximizing Your State of the Line Experience P/C INDUSTRY NET WRITTEN PREMIUM SLIDE 4 The net written premium in this slide provides a measure of the size of each major line of business in the property/casualty

Maximizing Your State of the Line Experience P/C INDUSTRY NET WRITTEN PREMIUM SLIDE 4 The net written premium in this slide provides a measure of the size of each major line of business in the property/casualty

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

Utah Land Title Association Economic Overview February 1, 2016

Utah Land Title Association Economic Overview February 1, 2016 Utah is One of the Fastest Growing CA 0.9% States in the Country Percent Change in Population for States: 2012 to 2013 WA 1.1% OR 0.8% NV

Utah Land Title Association Economic Overview February 1, 2016 Utah is One of the Fastest Growing CA 0.9% States in the Country Percent Change in Population for States: 2012 to 2013 WA 1.1% OR 0.8% NV

STATE OF THE LINE REPORT

ANNUAL ISSUES SYMPOSIUM STATE OF THE LINE REPORT T H E SYSTEM @WORK KATHY ANTONELLO, FCAS, FSA, MAAA CHIEF ACTUARY NCCI Copyright NCCI Holdings, Inc. All Rights Reserved. ANNUAL ISSUES SYMPOSIUM PROPERTY/CASUALTY

ANNUAL ISSUES SYMPOSIUM STATE OF THE LINE REPORT T H E SYSTEM @WORK KATHY ANTONELLO, FCAS, FSA, MAAA CHIEF ACTUARY NCCI Copyright NCCI Holdings, Inc. All Rights Reserved. ANNUAL ISSUES SYMPOSIUM PROPERTY/CASUALTY

Tax Freedom Day 2019 is April 16th

Apr. 2019 Tax Freedom Day 2019 is April 16th Erica York Economist Madison Mauro Research Assistant Emma Wei Research Assistant Key Findings This year, Tax Freedom Day falls on April 16, or 105 days into

Apr. 2019 Tax Freedom Day 2019 is April 16th Erica York Economist Madison Mauro Research Assistant Emma Wei Research Assistant Key Findings This year, Tax Freedom Day falls on April 16, or 105 days into

Paying Out-of-Pocket

September 2017 Paying Out-of-Pocket The Healthcare Spending of 2 Million US Families Healthcare costs are rising for families. In 2015 the US spent 18 percent of Gross Domestic Product (GDP) on healthcare,

September 2017 Paying Out-of-Pocket The Healthcare Spending of 2 Million US Families Healthcare costs are rising for families. In 2015 the US spent 18 percent of Gross Domestic Product (GDP) on healthcare,

Uinta Basin Energy Summit Economic Overview September 10, 2015

Uinta Basin Energy Summit Economic Overview September 10, 2015 Overview National Economic Conditions Utah Economic Conditions Utah is One of the Fastest Growing CA States in the Country Percent Change

Uinta Basin Energy Summit Economic Overview September 10, 2015 Overview National Economic Conditions Utah Economic Conditions Utah is One of the Fastest Growing CA States in the Country Percent Change

Comparative Revenues and Revenue Forecasts Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

Who s Above the Social Security Payroll Tax Cap? BY NICOLE WOO, JANELLE JONES, AND JOHN SCHMITT*

Issue Brief September 2011 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Who s Above the Social Security

Issue Brief September 2011 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Who s Above the Social Security

Eye on the South Carolina Housing Market presented at 2008 HBA of South Carolina State Convention August 1, 2008

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

The Oil Market: From Boom to Gloom

The Oil Market: From Boom to Gloom Mine Yücel Senior Vice President and Director of Research February 12, 216 The views expressed are those of the speaker and should not be attributed to the or the Federal

The Oil Market: From Boom to Gloom Mine Yücel Senior Vice President and Director of Research February 12, 216 The views expressed are those of the speaker and should not be attributed to the or the Federal

Zions Bank Economic Overview

Zions Bank Economic Overview Utah Institute of Real Estate Management Economic Summit September 12, 2017 National Economic Conditions August Job Indicators Indicator Expectation Actual Total Nonfarm Payrolls

Zions Bank Economic Overview Utah Institute of Real Estate Management Economic Summit September 12, 2017 National Economic Conditions August Job Indicators Indicator Expectation Actual Total Nonfarm Payrolls

Unemployment Insurance Benefit Adequacy: How many? How much? How Long?

Unemployment Insurance Benefit Adequacy: How many? How much? How Long? Joel Sacks, Deputy Commissioner Washington State Employment Security Department March 1, 2012 1 Outline How many get unemployment

Unemployment Insurance Benefit Adequacy: How many? How much? How Long? Joel Sacks, Deputy Commissioner Washington State Employment Security Department March 1, 2012 1 Outline How many get unemployment

Workers Compensation Outlook Recap

Workers Compensation Outlook Recap Evolving Workplace Premium Growth in the Latest Year Underwriting Results Improved Again Frequency Continues to Decline Economic Recovery 2 Property/Casualty (P/C) Results

Workers Compensation Outlook Recap Evolving Workplace Premium Growth in the Latest Year Underwriting Results Improved Again Frequency Continues to Decline Economic Recovery 2 Property/Casualty (P/C) Results

Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average

Issue Brief March 6, 2012 Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average The money we pay in fees and taxes helps create jobs, build a strong economy, and preserve Oregon

Issue Brief March 6, 2012 Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average The money we pay in fees and taxes helps create jobs, build a strong economy, and preserve Oregon

TCJA and the States Responding to SALT Limits

TCJA and the States Responding to SALT Limits Kim S. Rueben Tuesday, January 29, 2019 1 What does this mean for Individuals under TCJA About two-thirds of taxpayers will receive a tax cut with the largest

TCJA and the States Responding to SALT Limits Kim S. Rueben Tuesday, January 29, 2019 1 What does this mean for Individuals under TCJA About two-thirds of taxpayers will receive a tax cut with the largest

Massachusetts Budget and Policy Center

Progressive Massachusetts 2013 Policy Conference March 24, 2013 Lasell College Newton, MA Presentation by Massachusetts Budget and Policy Center Our State Budget: Building a Better Future Together Massachusetts

Progressive Massachusetts 2013 Policy Conference March 24, 2013 Lasell College Newton, MA Presentation by Massachusetts Budget and Policy Center Our State Budget: Building a Better Future Together Massachusetts

Analyzing State-Level Construction Fatality Rates,

Analyzing State-Level Construction Fatality Rates, 1992-2016 John Mendeloff Professor of Public Affairs University of Pittsburgh jmen@pitt.edu Wayne B. Gray Professor of Economics Clark University wgray@clarku.edu

Analyzing State-Level Construction Fatality Rates, 1992-2016 John Mendeloff Professor of Public Affairs University of Pittsburgh jmen@pitt.edu Wayne B. Gray Professor of Economics Clark University wgray@clarku.edu

Nevada Labor Market Briefing: January Summary of Labor Market Economic Indicators

Nevada Labor Market Briefing: January 2019 Summary of Labor Market Economic Indicators Department of Employment, Training, & Rehabilitation Dr. Tiffany Tyler-Garner, Director Dennis Perea, Deputy Director

Nevada Labor Market Briefing: January 2019 Summary of Labor Market Economic Indicators Department of Employment, Training, & Rehabilitation Dr. Tiffany Tyler-Garner, Director Dennis Perea, Deputy Director

Marilyn Tavenner, CMS Administrator Don Moulds, Acting Assistant Secretary for Planning and Evaluation

TO: The Secretary Through: DS COS ES FROM: Marilyn Tavenner, CMS Administrator Don Moulds, Acting Assistant Secretary for Planning and Evaluation DATE: September 5, 2013 SUBJECT: Projected Monthly Targets

TO: The Secretary Through: DS COS ES FROM: Marilyn Tavenner, CMS Administrator Don Moulds, Acting Assistant Secretary for Planning and Evaluation DATE: September 5, 2013 SUBJECT: Projected Monthly Targets

Alaska Transportation Finance Study Alaska Municipal League

Alaska Transportation Finance Study Alaska Municipal League presented to Alaska House Transportation Committee presented by Christopher Wornum Cambridge Systematics, Inc. February 12, 2009 Transportation

Alaska Transportation Finance Study Alaska Municipal League presented to Alaska House Transportation Committee presented by Christopher Wornum Cambridge Systematics, Inc. February 12, 2009 Transportation

Workers Compensation and the Economy

Workers Compensation and the Economy Trends, Challenges and Opportunities Workers Compensation Education Conference Orlando, FL August 20, 2013 Robert P. Hartwig, Ph.D., CPCU, President & Economist Insurance

Workers Compensation and the Economy Trends, Challenges and Opportunities Workers Compensation Education Conference Orlando, FL August 20, 2013 Robert P. Hartwig, Ph.D., CPCU, President & Economist Insurance

Mississippi s Business Monitoring The State s Economy

Mississippi s Business January 2012 Monitoring The State s Economy ECONOMY AT A GLANCE Volume 70 - Number 1 A Publication of the University Research Center, Mississippi Institutions of Higher Learning

Mississippi s Business January 2012 Monitoring The State s Economy ECONOMY AT A GLANCE Volume 70 - Number 1 A Publication of the University Research Center, Mississippi Institutions of Higher Learning

Property Tax Relief in New England

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

A Perspective from the Federal Reserve Institute of Internal Auditors San Antonio Chapter August 19, 2015 Blake Hastings Senior Vice President

A Perspective from the Federal Reserve Institute of Internal Auditors San Antonio Chapter August 19, 215 Blake Hastings Senior Vice President The views expressed in this presentation are strictly those

A Perspective from the Federal Reserve Institute of Internal Auditors San Antonio Chapter August 19, 215 Blake Hastings Senior Vice President The views expressed in this presentation are strictly those

Maryland. September 7,

Maryland September 7, 2018 David_Benedict@ncci.com 804-380-3005 Dawn_Ingham@ncci.com 561-893-3165 Robert_Moss@ncci.com 561-893-3794 Maryland State Advisory Forum The Future@Work (Video) Countrywide Workers

Maryland September 7, 2018 David_Benedict@ncci.com 804-380-3005 Dawn_Ingham@ncci.com 561-893-3165 Robert_Moss@ncci.com 561-893-3794 Maryland State Advisory Forum The Future@Work (Video) Countrywide Workers

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q4 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q4 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Tax Freedom Day 2018 is April 19th

Apr. 2018 Tax Freedom Day 2018 is April 19th Erica York Analyst Key Findings Tax Freedom Day is a significant date for taxpayers and lawmakers because it represents how long Americans as a whole have to

Apr. 2018 Tax Freedom Day 2018 is April 19th Erica York Analyst Key Findings Tax Freedom Day is a significant date for taxpayers and lawmakers because it represents how long Americans as a whole have to

2018 National Electric Rate Study

2018 National Electric Rate Study Ranking of Typical Residential, Commercial and Industrial Electric Bills LES Administrative Board June 15, 2018 Emily N. Koenig Director of Finance & Rates 1 Why is the

2018 National Electric Rate Study Ranking of Typical Residential, Commercial and Industrial Electric Bills LES Administrative Board June 15, 2018 Emily N. Koenig Director of Finance & Rates 1 Why is the

Construction, Manufacturing and Oil & Gas Industries and the P/C Insurance Industry:

Construction, Manufacturing and Oil & Gas Industries and the P/C Insurance Industry: Trends, Challenges & Opportunities Insurance Information Institute June 12, 2013 Download at www.iii.org/presentations

Construction, Manufacturing and Oil & Gas Industries and the P/C Insurance Industry: Trends, Challenges & Opportunities Insurance Information Institute June 12, 2013 Download at www.iii.org/presentations

Mega-Trends Affecting the Workers Compensation Insurance Industry

Mega-Trends Affecting the Workers Compensation Insurance Industry Challenges Amid the Economic Crisis 6 th Annual National Workers Compensation ExecuSummit Uncasville, CT February 2, 2009 Robert P. Hartwig,

Mega-Trends Affecting the Workers Compensation Insurance Industry Challenges Amid the Economic Crisis 6 th Annual National Workers Compensation ExecuSummit Uncasville, CT February 2, 2009 Robert P. Hartwig,

Western Treasure Valley Economic Breakfast Economic Overview March 17, 2016

Western Treasure Valley Economic Breakfast Economic Overview March 17, 2016 Utah is One of the Fastest Growing CA 0.9% States in the Country Percent Change in Population for States: 2012 to 2013 WA 1.1%

Western Treasure Valley Economic Breakfast Economic Overview March 17, 2016 Utah is One of the Fastest Growing CA 0.9% States in the Country Percent Change in Population for States: 2012 to 2013 WA 1.1%

NCCI Research Investigating the Drivers of the 2015 Workers Compensation Medical Severity Decline

NCCI Research Investigating the Drivers of the 2015 Workers Compensation Medical Severity Decline By David Colón, ACAS, MAAA Associate Actuary, NCCI Introduction NCCI reported at its 2016 Annual Issues

NCCI Research Investigating the Drivers of the 2015 Workers Compensation Medical Severity Decline By David Colón, ACAS, MAAA Associate Actuary, NCCI Introduction NCCI reported at its 2016 Annual Issues

The Acquisition of Regions Insurance Group. April 6, 2018

The Acquisition of Regions Insurance Group April 6, 2018 Forward-Looking Statements This presentation contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform

The Acquisition of Regions Insurance Group April 6, 2018 Forward-Looking Statements This presentation contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform

Texas Economic Outlook: Tapping on the Brakes

National Economy Picking Up After Q1 Pause Texas Economic Outlook: Tapping on the Brakes Keith Phillips Assistant Vice President and Senior Economist Consumer spending picked up in 1 as housing prices

National Economy Picking Up After Q1 Pause Texas Economic Outlook: Tapping on the Brakes Keith Phillips Assistant Vice President and Senior Economist Consumer spending picked up in 1 as housing prices

Texas Mid-Year Economic Outlook: The Skies are Beginning to Clear Keith Phillips Assistant Vice President and Senior Economist

Texas Mid-Year Economic Outlook: The Skies are Beginning to Clear Keith Phillips Assistant Vice President and Senior Economist The views expressed in this presentation are strictly those of the presenter

Texas Mid-Year Economic Outlook: The Skies are Beginning to Clear Keith Phillips Assistant Vice President and Senior Economist The views expressed in this presentation are strictly those of the presenter

State of the Line AIS AIS th Anniversary th Anniversary. Copyright 2018 NCCI Holdings, Inc. All Rights Reserved.

State of the Line Copyright NCCI Holdings, Inc. All Rights Reserved. PROPERTY/CASUALTY (P/C) RESULTS Copyright NCCI Holdings, Inc. All Rights Reserved. P/C Industry Net Written Premium Growth Private Carriers

State of the Line Copyright NCCI Holdings, Inc. All Rights Reserved. PROPERTY/CASUALTY (P/C) RESULTS Copyright NCCI Holdings, Inc. All Rights Reserved. P/C Industry Net Written Premium Growth Private Carriers

The Lincoln National Life Insurance Company Term Portfolio

The Lincoln National Life Insurance Company Term Portfolio State Availability as of 7/16/2018 PRODUCTS AL AK AZ AR CA CO CT DE DC FL GA GU HI ID IL IN IA KS KY LA ME MP MD MA MI MN MS MO MT NE NV NH NJ

The Lincoln National Life Insurance Company Term Portfolio State Availability as of 7/16/2018 PRODUCTS AL AK AZ AR CA CO CT DE DC FL GA GU HI ID IL IN IA KS KY LA ME MP MD MA MI MN MS MO MT NE NV NH NJ

The Changing Revenue Landscape

The Changing Revenue Landscape NCSL Legislative Summit, 2018 July 30, 2018 Lucy Dadayan July 30, 2018 Lucy Dadayan State Revenue Trends and Volatility TCJA, South Dakota vs. Wayfair, Sports Betting Overview

The Changing Revenue Landscape NCSL Legislative Summit, 2018 July 30, 2018 Lucy Dadayan July 30, 2018 Lucy Dadayan State Revenue Trends and Volatility TCJA, South Dakota vs. Wayfair, Sports Betting Overview

2016 Texas Economic Outlook: Riding the Energy Roller Coaster Keith Phillips Assistant Vice President and Senior Economist

216 Texas Economic Outlook: Riding the Energy Roller Coaster Keith Phillips Assistant Vice President and Senior Economist The views expressed in this presentation are strictly those of the presenter and

216 Texas Economic Outlook: Riding the Energy Roller Coaster Keith Phillips Assistant Vice President and Senior Economist The views expressed in this presentation are strictly those of the presenter and

SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008

U.S. DEPARTMENT OF LABOR EMPLOYMENT AND TRAINING ADMINISTRATION Office Workforce Security SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008 AL AK AZ AR CA CO CT DE DC FL GA HI /

U.S. DEPARTMENT OF LABOR EMPLOYMENT AND TRAINING ADMINISTRATION Office Workforce Security SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008 AL AK AZ AR CA CO CT DE DC FL GA HI /

Black Knight Mortgage Monitor

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of April, 2014 Month-end Black Knight First Look April 2014 2 Focus Points Prepayment activity and originations ARM loans

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of April, 2014 Month-end Black Knight First Look April 2014 2 Focus Points Prepayment activity and originations ARM loans

CONNECTICUT. October 5,

CONNECTICUT October 5, 2016 Laura_Backus_Hall@ncci.com 802-454-1800 Jim_Davis@ncci.com 561-893-3097 Opening Remarks Economic Outlook: Countrywide and Connecticut Workers Compensation System Overview: Countrywide

CONNECTICUT October 5, 2016 Laura_Backus_Hall@ncci.com 802-454-1800 Jim_Davis@ncci.com 561-893-3097 Opening Remarks Economic Outlook: Countrywide and Connecticut Workers Compensation System Overview: Countrywide

Utah Association of Special Districts Economic Overview November 5, 2015

Utah Association of Special Districts Economic Overview November 5, 2015 Utah is One of the Fastest Growing CA 0.9% States in the Country Percent Change in Population for States: 2012 to 2013 WA 1.1% OR

Utah Association of Special Districts Economic Overview November 5, 2015 Utah is One of the Fastest Growing CA 0.9% States in the Country Percent Change in Population for States: 2012 to 2013 WA 1.1% OR

Local Anesthesia Administration by Dental Hygienists State Chart

Education or AK 1981 General Both Specific Yes WREB 16 hrs didactic; 6 hrs ; 8 hrs lab AZ 1976 General Both Accredited Yes WREB 36 hrs; 9 types of AR 1995 Direct Both Accredited/ Board Approved No 16 hrs

Education or AK 1981 General Both Specific Yes WREB 16 hrs didactic; 6 hrs ; 8 hrs lab AZ 1976 General Both Accredited Yes WREB 36 hrs; 9 types of AR 1995 Direct Both Accredited/ Board Approved No 16 hrs

Tax Breaks for Elderly Taxpayers in the States in 2016

AL Payments from defined benefit private plans are exempt; most public systems are exempt; military and US Civil service are exempt Special Homestead ion for 65+ +25.2% +2.4% AK No PIT Homestead ion for

AL Payments from defined benefit private plans are exempt; most public systems are exempt; military and US Civil service are exempt Special Homestead ion for 65+ +25.2% +2.4% AK No PIT Homestead ion for

Indexed Universal Life Caps

Indexed Universal Life Caps Effective March 15, 2013, the caps on FG Life-Elite II will be changing as follows: Cap Illustrative Rate 100% Participation Annual Point-to-Point 14.75% 8.32% 140% Participation

Indexed Universal Life Caps Effective March 15, 2013, the caps on FG Life-Elite II will be changing as follows: Cap Illustrative Rate 100% Participation Annual Point-to-Point 14.75% 8.32% 140% Participation

NCCI Research Workers Compensation and Prescription Drugs 2016 Update

NCCI Research Workers Compensation and Prescription Drugs 2016 Update By Barry Lipton, FCAS, MAAA, Practice Leader and Senior Actuary, NCCI David Colón, ACAS, MAAA, Associate Actuary, NCCI Introduction

NCCI Research Workers Compensation and Prescription Drugs 2016 Update By Barry Lipton, FCAS, MAAA, Practice Leader and Senior Actuary, NCCI David Colón, ACAS, MAAA, Associate Actuary, NCCI Introduction

One Year Later: Update on Claim Payouts to Alabama Policyholders

One Year Later: Update on Claim Payouts to Alabama Policyholders Insurance and Economic Recovery in the Wake of the April 211 Tornadoes Insurance Information Institute April 19, 212 Download at www.iii.org/presentations

One Year Later: Update on Claim Payouts to Alabama Policyholders Insurance and Economic Recovery in the Wake of the April 211 Tornadoes Insurance Information Institute April 19, 212 Download at www.iii.org/presentations

KENTUCKY. August 18, 2016

KENTUCKY August 18, 2016 Cathy_Booth@ncci.com 202-655-2699 Sean_Cooper@ncci.com 561-893-3072 Mona_Carter@ncci.com 561-893-3045 Ed O Daniel, Esq. 859-336-9611 Kentucky Workers Compensation State Advisory

KENTUCKY August 18, 2016 Cathy_Booth@ncci.com 202-655-2699 Sean_Cooper@ncci.com 561-893-3072 Mona_Carter@ncci.com 561-893-3045 Ed O Daniel, Esq. 859-336-9611 Kentucky Workers Compensation State Advisory

Regional Economic Update

Regional Economic Update Roberto Coronado Assistant Vice President in Charge and Sr. Economist July 23, 2015 The views expressed in this presentation are strictly those of the authors and do not necessarily

Regional Economic Update Roberto Coronado Assistant Vice President in Charge and Sr. Economist July 23, 2015 The views expressed in this presentation are strictly those of the authors and do not necessarily

State Trust Fund Solvency

Unemployment Insurance State Trust Fund Solvency National Employment Law Project Conference - Washington DC December 7, 2009 Robert Pavosevich pavosevich.robert@dol.gov Unemployment Insurance Program

Unemployment Insurance State Trust Fund Solvency National Employment Law Project Conference - Washington DC December 7, 2009 Robert Pavosevich pavosevich.robert@dol.gov Unemployment Insurance Program

Obamacare in Pictures

Obamacare in Pictures VISUALIZING THE EFFECTS OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Spring 2014 If you like your health care plan, can you really keep it? At least 4.7 million health care plans

Obamacare in Pictures VISUALIZING THE EFFECTS OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Spring 2014 If you like your health care plan, can you really keep it? At least 4.7 million health care plans

Alternative Paths to Medicaid Expansion

Alternative Paths to Medicaid Expansion Robin Rudowitz Kaiser Commission on Medicaid and the Uninsured Kaiser Family Foundation National Health Policy Forum March 28, 2014 Figure 1 The goal of the ACA

Alternative Paths to Medicaid Expansion Robin Rudowitz Kaiser Commission on Medicaid and the Uninsured Kaiser Family Foundation National Health Policy Forum March 28, 2014 Figure 1 The goal of the ACA

RESEARCH REPORT VARIABLE RATE DEMAND OBLIGATIONS 2010 UPDATE OCTOBER New York n Washington. Volume V No.

RESEARCH REPORT OCTOBER 21 VARIABLE RATE DEMAND OBLIGATIONS 21 UPDATE Volume V No. 16 New York n Washington Variable Rate Demand Obligations Q2 29-21 VARIABLE RATE DEMAND OBLIGATIONS Variable rate demand

RESEARCH REPORT OCTOBER 21 VARIABLE RATE DEMAND OBLIGATIONS 21 UPDATE Volume V No. 16 New York n Washington Variable Rate Demand Obligations Q2 29-21 VARIABLE RATE DEMAND OBLIGATIONS Variable rate demand

Fourth Quarter 2014 Financial Results Supplement

Fourth Quarter 20 Financial Results Supplement February 19, 2015 Table of contents Financial Results Segment Business Information 2 - Annual Financial Results 12 - Single-Family New Funding Volume 3 -

Fourth Quarter 20 Financial Results Supplement February 19, 2015 Table of contents Financial Results Segment Business Information 2 - Annual Financial Results 12 - Single-Family New Funding Volume 3 -

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015 Norton Francis State and Local Finance Initiative Urban-Brookings

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015 Norton Francis State and Local Finance Initiative Urban-Brookings

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA Phone: Fax:

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA 30329 Phone: 404-315-9515 Fax: 404-315-6558 AGENCY/BROKER PROFILE Please type your answers. Use a separate

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA 30329 Phone: 404-315-9515 Fax: 404-315-6558 AGENCY/BROKER PROFILE Please type your answers. Use a separate

Premium Savings Program Broker Training

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Premium Savings Program Broker Training April 2013 We are responding to ACA changes Pricing volatility Rate shock

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Premium Savings Program Broker Training April 2013 We are responding to ACA changes Pricing volatility Rate shock

Understanding the New Trump Economy Economic Overview. November 15, 2016

Understanding the New Trump Economy Economic Overview November 15, 2016 Uncertainty at the Na@onal and Interna@onal Level Source: Bureau of Labor Statistics The Trump Bump Why? National Job Growth 500

Understanding the New Trump Economy Economic Overview November 15, 2016 Uncertainty at the Na@onal and Interna@onal Level Source: Bureau of Labor Statistics The Trump Bump Why? National Job Growth 500

Old Dominion University 2013 National Economic Outlook

Old Dominion University 2013 National Economic Outlook January 30, 2013 Professor Vinod Agarwal Professor Mohammad Najand Professor Gary A. Wagner www.odu.edu/forecasting 1 Presentation Outline 2012 Scorecard

Old Dominion University 2013 National Economic Outlook January 30, 2013 Professor Vinod Agarwal Professor Mohammad Najand Professor Gary A. Wagner www.odu.edu/forecasting 1 Presentation Outline 2012 Scorecard

Zions Bank Economic Overview Alta High School. March 24, 2017

Zions Bank Economic Overview Alta High School March 24, 2017 Economic Fundamentals Scarcity Based on limited resources Scarce resources must be allocated using a method of distribution Example: Food Clean

Zions Bank Economic Overview Alta High School March 24, 2017 Economic Fundamentals Scarcity Based on limited resources Scarce resources must be allocated using a method of distribution Example: Food Clean

Latinas Access to Health Insurance

FACT SHEET Latinas Access to Health Insurance APRIL 2018 Data released by the U.S. Census Bureau show that, despite significant health insurance gains since the Affordable Care Act (ACA) was implemented,

FACT SHEET Latinas Access to Health Insurance APRIL 2018 Data released by the U.S. Census Bureau show that, despite significant health insurance gains since the Affordable Care Act (ACA) was implemented,

Workers Compensation Temporary Total Disability Indemnity Benefit Duration 2011 Update

April 2012 by Barry Lipton, John Robertson, and Katy Porter Workers Compensation Temporary Total Disability Indemnity Benefit Duration 2011 Update KEY FINDINGS This brief updates our previous paper 1 published

April 2012 by Barry Lipton, John Robertson, and Katy Porter Workers Compensation Temporary Total Disability Indemnity Benefit Duration 2011 Update KEY FINDINGS This brief updates our previous paper 1 published

ALASKA. October 19,

ALASKA October 19, 2016 Maggie_Karpuk@ncci.com 818-707-8374 John_Deacon@ncci.com 818-707-8376 Alaska Workers Compensation State Advisory Forum State of the Industry Economic Overview Alaska Workers Compensation

ALASKA October 19, 2016 Maggie_Karpuk@ncci.com 818-707-8374 John_Deacon@ncci.com 818-707-8376 Alaska Workers Compensation State Advisory Forum State of the Industry Economic Overview Alaska Workers Compensation

Percent of Employees Waiving Coverage 27.0% 30.6% 29.1% 23.4% 24.9%

Number of Health Plans Reported 18,186 3,561 681 2,803 3,088 Offer HRA or HSA 34.0% 42.7% 47.0% 39.7% 35.0% Annual Employer Contribution $1,353 $1,415 $1,037 $1,272 $1,403 Percent of Employees Waiving

Number of Health Plans Reported 18,186 3,561 681 2,803 3,088 Offer HRA or HSA 34.0% 42.7% 47.0% 39.7% 35.0% Annual Employer Contribution $1,353 $1,415 $1,037 $1,272 $1,403 Percent of Employees Waiving

SCHIP: Let the Discussions Begin

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

Medicare Alert: Temporary Member Access

Medicare Alert: Temporary Member Access Plan Sponsor: Coventry/Aetna Medicare Part D Effective Date: Jan. 12, 2015 Geographic Area: National If your pharmacy is a Non Participating provider in the Aetna/Coventry

Medicare Alert: Temporary Member Access Plan Sponsor: Coventry/Aetna Medicare Part D Effective Date: Jan. 12, 2015 Geographic Area: National If your pharmacy is a Non Participating provider in the Aetna/Coventry

Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston

The Growing Instability of Revenues over the Business Cycle: Putting the New England States in Perspective Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston Lincoln Institute

The Growing Instability of Revenues over the Business Cycle: Putting the New England States in Perspective Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston Lincoln Institute

MEMORANDUM. SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08

MEMORANDUM TO: FROM: HR Investment Center Members Matt Cinque, Managing Director DATE: March 12, 2009 SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08 Please find enclosed the

MEMORANDUM TO: FROM: HR Investment Center Members Matt Cinque, Managing Director DATE: March 12, 2009 SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08 Please find enclosed the

While one in five Californians overall is uninsured, the rate among those who work is even higher: one in four.

: By the Numbers December 2013 Introduction California had the greatest number of uninsured residents of any state, 7 million, and the seventh largest percentage of uninsured residents under 65 in the

: By the Numbers December 2013 Introduction California had the greatest number of uninsured residents of any state, 7 million, and the seventh largest percentage of uninsured residents under 65 in the

Obamacare in Pictures. Visualizing the Effects of the Patient Protection and Affordable Care Act

Visualizing the Effects of the Patient Protection and Affordable Care Act Fall 2012 expands dependence on government health care dumps millions into Medicaid and creates new federal subsidies for government-approved

Visualizing the Effects of the Patient Protection and Affordable Care Act Fall 2012 expands dependence on government health care dumps millions into Medicaid and creates new federal subsidies for government-approved

Report to Congressional Defense Committees

Report to Congressional Defense Committees The Department of Defense Comprehensive Autism Care Demonstration December 2016 Quarterly Report to Congress In Response to: Senate Report 114-255, page 205,

Report to Congressional Defense Committees The Department of Defense Comprehensive Autism Care Demonstration December 2016 Quarterly Report to Congress In Response to: Senate Report 114-255, page 205,

Increase Profitability by Controlling Insurance Premiums

Increase Profitability by Controlling Insurance Premiums Increase Profitability by Controlling Insurance Premiums Jeff Mount Senior Vice President Federated Insurance This session is eligible for 1.5 Continuing

Increase Profitability by Controlling Insurance Premiums Increase Profitability by Controlling Insurance Premiums Jeff Mount Senior Vice President Federated Insurance This session is eligible for 1.5 Continuing

Zions Bank Salt Lake Northeast Region Officers Mee8ng Economic Overview. July 28, 2016

Zions Bank Salt Lake Northeast Region Officers Mee8ng Economic Overview July 28, 2016 National Economic Conditions Readings on the U.S. economy since the turn of the year have been somewhat mixed. - Janet

Zions Bank Salt Lake Northeast Region Officers Mee8ng Economic Overview July 28, 2016 National Economic Conditions Readings on the U.S. economy since the turn of the year have been somewhat mixed. - Janet

IMPROVING COLLEGE ACCESS

IMPROVING COLLEGE ACCESS Grants and Resources for Education Leaders West Virginia Leaders of Education Conference December 3, 2018 THE EDUCATION ALLIANCE Statewide non-profit organization W E brings B

IMPROVING COLLEGE ACCESS Grants and Resources for Education Leaders West Virginia Leaders of Education Conference December 3, 2018 THE EDUCATION ALLIANCE Statewide non-profit organization W E brings B

2018 ADDENDUM INSTRUCTIONS

2018 ADDENDUM INSTRUCTIONS FEBRUARY 22, 2019 UPDATE: 2018 MUNICIPAL REFERENCE BOOK 1. DELAWARE funds are listed on page 15. You may note on page 15 to see the addendum for additional Delaware funds. The

2018 ADDENDUM INSTRUCTIONS FEBRUARY 22, 2019 UPDATE: 2018 MUNICIPAL REFERENCE BOOK 1. DELAWARE funds are listed on page 15. You may note on page 15 to see the addendum for additional Delaware funds. The

Changes in Monday Claims

September 2018 By Chun Shyong, Barry Lipton, and John Robertson Changes in Monday Claims INTRODUCTION Sometimes, workers compensation (WC) pays claims for injuries that are reported as work related but

September 2018 By Chun Shyong, Barry Lipton, and John Robertson Changes in Monday Claims INTRODUCTION Sometimes, workers compensation (WC) pays claims for injuries that are reported as work related but

Mega Trends in Workers Compensation

Mega Trends in Workers Compensation Past, Present and Future 16 th Annual AMCOMP Conference Las Vegas, NV March 27, 2014 Download at www.iii.org/presentations Robert P. Hartwig, Ph.D., CPCU, President

Mega Trends in Workers Compensation Past, Present and Future 16 th Annual AMCOMP Conference Las Vegas, NV March 27, 2014 Download at www.iii.org/presentations Robert P. Hartwig, Ph.D., CPCU, President