Average per capita income evolution R$ at 2009

|

|

|

- Briana Lawrence

- 5 years ago

- Views:

Transcription

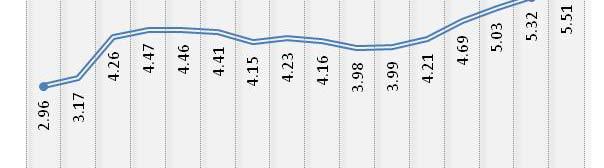

1 Average per capita income evolution R$ at * * , 40,5 7,95 506,70 514,75 518,96 527,24 483,99 506,53 507,72 477,89 492,45 524,75 572,69 585, ,65 630,25 1

2 2 Increase of Average househol Per Capita Income (all sources) 2001 to 2009Aumentodarendafamiliarpercapitaacumulada Menosde10%de10%a20%de20%a30%de20%a30%de30%a40%Maisde40% Average Income PNAD X GDP The magnitude of the resumption of growth in the period depends onthe database used: GDP period depends on the database used: GDP grows 3.78% in per capita per year, slower than the National Survey by Household Sampling (PNAD), 5.26 % per year, also discounting population growth and inflation. According to PNAD 2009 income i th GDP 15% f grows more once gain than GDP: 1.5% of per capita GDP against a positive growth of 2.04% in PNAD.

3 300,00 Welfare evolution R$ Sen s 1976 Measure = Average * (1 Gini) 280,00 260,00 240,00 220,00 200,00 180,00 160,00 203,00 204,93 207,36 210,84 196,67 204,79 208,87 199,29 211,21 226,57 250,68 260, ,81 286,92 140, , , ,41 100, * * Gini s index Evolution 0,62 0,61 0,60 0,59 0,58 0,57 0,56 0,55 0,54 0,53 0,52 0,5832 0,6068 0,5994 0,6019 0,6004 0,6001 0,5937 0,5957 0,5886 0,5830 0,5711 0,5682 0,5623 0,5550 0, , , * *

Richer 4")

4 Inequality Gini s Index Source: CPS/FGV based on microdata from PNAD and Census / IBGE Accumulated Variation of Average Income by Income Tenths - Brazil (2009/2001) Richer 4

")

Richer 5")

5 Variation of the Annual Per Capita of Average Income per Income Tenths - Brazil (2009/2008) Richer Variation of the Annual Per Capita of Average Income per Income Tenths - Brazil (2009/2003) Richer 5

6 Variation of the Annual Per Capita of Average Income per Income Tenths(2009/2001) Richer Total Income Participation in Brazil 41,8% 42,8% 15,4% Source: CPS / FGV based on microdata from PNAD / IBGE 6

7 Definition of Economic Classes Total Household Income from All Sources Earnings Brackets Inferior Superior Class E Class D Class C Class B Class A

8 Economic classes evolution Class AB/C Class D/E ,1 59,6 61, , ,9 30 Fonte: CPS/FGV a partir dos microdados da PNAD/IBGE Economic classes evolution Class AB Class C Class D/E , , , , , ,6 0 Fonte: CPS/FGV a partir dos microdados da PNAD/IBGE 8

9 Economic classes evolution Class E % -4.32% Class D % -3.00% Class C 34.32% 2.49% Class B 38.51% 3.49% Class A 40.99% 0.18% Fonte: CPS/FGV a partir dos microdados da PNAD/IBGE Population Difference by Economic Classes Class E -20,481,069-1,022,145 Class D -2,431, ,083 Class C 29,063,545 3,172,653 Class B 3,391, ,181 Class A 3,253, ,487 Fonte: CPS/FGV a partir dos microdados da PNAD/IBGE 9

10 The Population Pyramid divided in Economic Classes Class DE Class C Class AB Population by Economic Classes Total 175,398, ,758, ,001, ,218, ,384, ,440, ,194,383 Class E 49,319,851 45,147,533 41,047,646 35,196,724 33,659,359 29,860,927 28,838,782 Class D 46,884,477 48,286,025 48,713,422 48,006,542 46,298,711 45,399,117 44,453,034 Class C 65,871,283 70,620,183 75,266,800 81,889,806 86,476,548 91,762,175 94,934,828 Class B 6,977,329 7,100,301 7,583,287 8,549,859 9,271,379 9,925,842 10,369,023 Class A 6,345,080 6,604,018 7,390,555 8,575,570 8,678,295 9,492,229 9,598,716 10

11 The Key Role of the New Middle Class. Politics The 94.9 million Brazilians who are in the new middle class represent 50,5% of the population. This means that the new Brazilian middle class not only includes the median voter taken as the one who decides d the second round of an election, but that this class alone could decide an election campaign. The Key Role of the New Middle Class Economics The new middle class is also economically dominating, concentrating more 46.24% of the purchasing power of Brazilians in 2009 (it was 45.66% in 2008) surpassing those classes AB with 44.12% of total purchasing power. The other classes D and E now has 9.65% of the purchasing power (falling from 19.79% just before the release of the Real Plan. 11

12 Class A Evolution Class B Evolution 12

13 Class C Evolution Class D Evolution 13

14 Class E Evolution Economic Classes More Detailled Definition Total Household Income from All Sources Income Brackets limits Inferior Superior Class E Class E Class D Class D Class C Class C Class B Class B Class A Class A

15 14,31% 7,23% 7,28% ,81% 8,78% 8,05% Economic Classes Evolution More Detailed Classification 13,69% 11,28% 10,81% 13,04% 13,07% 12,81% 18,68% 22,69% 22,31%,53% 28,13% 18,88% 26, 2,01% 2,86% 2,94% 1,97% 2,46% 2,57% 1,83% 2,55% 2,50% 1,78% 2,54% 2,60% E2 E1 D2 D1 C2 C1 B2 B1 A2 A Income Mass by Economic Classes More Detailed Classification 29,2 2% 3 1,8% 32,9% 1,4% 0,5% 0,4% 3,1% 1,5% 1,4% 4,8% 3,1% 2,9% 6,6 6% 5,1% 4,9% 14,3% 13,8% 13,4% 5,8 8% 6,4 4% 6,4 4% 7, 6, 7,,1% 9%,0% 9,1% 9,7% 9,3% 18,6% 21,3% 21,4% E2 E1 D2 D1 C2 C1 B2 B1 A2 A1 15

16 16 Annual Rate of Poverty Reduction (Class E) 2003/2009TaxaAnualdeReduçãodaPobreza Até5%de5%a7,5%de7,5%a10%de10%a12,5%de12,5%a15%Maisde15%1993/1995TaxaAnualAté5%de5%a7,5%de7,5%a10%de10%a12,5%de12,5%a15%Maisde15%Source: CPS / FGV based on microdata from PNAD / IBGE Annual rate of growth in class ABC 2003/ /1995TaxaAnualdeCrescimentodasClassesABC Até5%de5%a7,5%de7,5%a10%de10%a12,5%de12,5%a15%Maisde15%Source: CPS / FGV based on microdata from PNAD / IBGE TaxaAnualAté5%de5%a7,5%de7,5%a10%de10%a12,5%de12,5%a15%Maisde15%

17 % Poverty In Minimun Wages Lines , , , , ,87 23,96 19,85 18,71 52,96 less than 1/4 1/4 to 1/2 more than de 1/2 17

18 Classic Indicators of Poverty 2003 % Poverty In Minimun Wages Lines ,0 32,50 30,58 Up to 1/2 Consumers and Producers 18

19 Simulador de Renda Is it Sustainable? The synthetic indicator of potential consumption power increasedby 22.6% between 2003 and 2008, while the index of the generation of income raised 31.2%. Difference of 38% in favor of the production side. During the crisis these indexes raised 2.49% and 3.05% respectively. 19

20 Net Generation of Formal Employment - BRAZIL Yearly (2000 to 2010 July*) * * up to august only Source: CPS/FGV based on microdata from CAGED / M T E. 20

21 Occupation Occupied 1992 to years or more* 21

22 Occupation Occupied years or more* 67,33% 61,29% 49,24% 41,84% class AB class C class D class E Fonte: CPS/FGV a partir dos microdados da PNAD/IBGE Occupation Profile of Economic Classes 2009 Position on the Occupation Category CLASS AB CLASS C CLASS D CLASS E Unemployed 2.14% 3.86% 7.20% 10.11% Inactive 30.53% 34.84% 43.56% 48.05% Agricultural employee 0.29% 2.33% 4.49% 4.68% Domestic employee 0.57% 4.53% 5.95% 4.27% Formal Employee 21.11% 22.96% 11.77% 4.31% Informal Employee 4.85% 6.75% 6.68% 4.47% Self employed 11.89% 11.85% 11.00% 11.05% Employer 9.81% 2.14% 0.55% 0.55% Public Employee 16.84% 7.09% 3.19% 1.61% Unpaid 1.95% 3.65% 5.62% 10.90% 22

23 Pension Contribution Private and/or Public (Social Security) Contributes to Social Security Contributes Soc. Sec. Pub. & Priv Contributes Soc. Sec. Public Contributes Soc. Sec. Priv Unemployed Inactive Digital Assets Computer with internet at Home 1992 to

24 Digital Assets Cellular Phone (at lest one at Home) 1992 to 2009 Digital Assets At Home COMPUTER Have computer with Internet Have computer Doesn t have computer Unknown TELEPHONE Have fixed and Cellphone Have fixed Have Cellphone Doesn t have fixed and Cellphone

Average Years of Schooling Brazil - 1992-2008 Age 25 years or")

25 Digital Assets at Home 75,82% Computer with internet ,90% class AB class C 9,69% class D 6,73% class E 95,92% 86,23% Cellular Phone ,23% 62,81% class AB class C class D class E Education Evolution (years) Average Years of Schooling Brazil Age 25 years or more 25

2009 12 10 8 6 4 2 0 12,00 7,18 5,46 4,98 class AB class C class D class E Attends or attended Schools 2009 47,67% 10,47% 2,07% 2,44% class AB")

26 Education Evolution (%) of the population by Educational Level EDUCATION OF THE HEAD Without education or less than 1 year to to to or more EDUCATION OF THE SPOUSE Withouteducation or less than 1 year to to to or more Education Completed Years of Schooling (pop. with 25 years or more) ,00 7,18 5,46 4,98 class AB class C class D class E Attends or attended Schools ,67% 10,47% 2,07% 2,44% class AB class C class D class E 26

27 Public Services Sewage 1992 to 2009 Public Services Garbage collected directly 1992 to

28 Public Services 72,02% Sewage ,78% 40,45% 30,65% class AB class C class D class E Garbage collected directly ,85% 87,46% 76,97% 64,20% class AB class C class D class E Consumer Goods Washing machine 1992 to 2009 Washing machine ,72% 53,22% 24,96% 16,48% class AB class C class D class E 28

29 99,54% 97,62% 96,00% 7/10/2010 Consumer Goods Refrigerator 1992 to 2009 Refrigerator ,69% 97,49% 92,50% 79,82% class AB class C class D class E Consumer Goods Television 1992 to 2009 Television ,16% class AB class C class D class E 29

30 More than 3 bathrooms 1992 to 2009 More than 3 bathrooms ,24% 1,07% 0,23% 0,35% class AB class C class D class E Financed homeowners 1992 to ,74% Financed homeowners ,97% 2,98% 1,69% class AB class C class D class E 30

31 Evolution (%) Population by Housing Condition Own already paid Own still paying Rent below the median Rent above the median Given Other condition ORDER OF ENTRY IN THE MODEL 1 Number of per capita 2 Telephone 3 Spouses education 4 Type of family 5 chefe contribui para previdência head contributes to social security 6 Washing machine 7 # of bedrooms per capita 8 Head s education 9 position on the head s job 10 school attendance of child(7 to 14 years) 11 school attendance of child (0 a 6 anos) 12 position on the head s job 13 Computer 14 Refrigerator 15 school attendance of child (15 a 17 anos) 16 type of home (own, lease and financing) 17 Syndicalized Head 18 Freezer 19 # of bedrooms per capita 20 sewage 21 Radio 22 # of bathrooms 23 number of residents 24 Television 25 Garbage colected 26 age that the head started to work 27 number of rooms 28 share of labor income 29 # of bedrooms 31

32 Pre Crisis (Dec 2002 a 2009 x Crisis (Dec 2008 a 2009) Class ABC Class AB Class C Class D Class E Income Gini THEIL 0,4% 2,4% 8,2% 1,5% 0,4% 1,6% 4,2% 1,8% 0,1% 3,8% 4,2% 2,0% 3,7% 1,4% 3,8% 0,0% dec02 to dec08 dec08 to dec09 Source: CPS/FGV based on microdata from PME/IBGE Variation in Economic Classes in Post-Crisis Class ABC Class AB Class C Class D Class E 0,8% 1,0% 0,8% 5,3% 0,7% 1,2% 0,8% 3,0% 0,6% 6, 7% 2,3% 0,6% 2,7% 2,2% 0,2% 2,5% 2,5% 1,2% 4,1% 1,1% set08 to dec08 dec08 to jan09 jan09 to set09 out09 to dec09 Source: CPS/FGV based on microdata from PME/IBGE 32

33 Class ABC Class AB Class C Class D Class E 0,4% % 13,0% 2,4% 1,5% 3,8% 0,1% 3,9% 5,5% 4,2% 2,0% 7,8 3,7% 2,9% 3,4% 1,4% dec02 to dec08 dec08 to dec09 janjun09 to janjun10 jul09 to jul10 7,7 7% 12,4% 8,2 % 8,6% % 11,3% Source: CPS/FGV based on microdata from PME/IBGE 3,8% Class ABC Class AB Class C Class D Class E 12, 0,4% 2,4% 3,2% 3,4% 3,7% 4,8% 4,2% 4,4% 5,5% 4,2% 2,0% 5,5% 7,2 2% 5,3% 9,2% 10,3% 9,7% 13,0% 3,7% 4,6% 4,9% 8,4% 9,3% 8,8% 10,0%,4% 8,2% 0,1% 7,9% 8,7% 7,2% 10,0% 8,8% 9,0% 1,3% 1,4% 1,5% 2,5% 2,4% 3,3% 3,6% 2,5% 3,0% 3,4% 1 dec02 to dec08 dec08 to dec09 jan09 to jan10 feb09 to feb10 mar09 to mar10 apr09 to apr10 may09 to may10 jun09 to jun10 jul09 to jul10 Source: CPS/FGV based on microdata from PME/IBGE 33

34 income Gini THEIL 0,4% 1,6% 1,9% 1,4% 4,2% 1,8% 5,1% 2,7% 0,0% 3,8% 3,6% 7,7 7% dec02 to dec08 dec08 to dec09 janjun09 to janjun10 jul09 to jul10 Source: CPS/FGV based on microdata from PME/IBGE income Gini THEIL 0,4% 1,6% 1,8% 1,5% 1,5% 2,2% 1,9% 2,2% 1,4% 7,2% % 6,2 2% 5, 4,2% 1,8% 3,8%,8% 3,4% 4,3% 2,7% 0,9% 0,0% 3,8 8% 3,9 9% 3,6 6% 5,1% 4,6% 3,7 7% 7,7% dec02 to dec08 dec08 to dec09 jan09 to jan10 feb09 to feb10 mar09 to mar10 apr09 to apr10 Source: CPS/FGV based on microdata from PME/IBGE 34

35 Elections and Expantions" Variation in Median Income and Electoral Cycles* % % % % % % % % % % % % % % % % % % % % % % % Obs:In 1991, 1994 and 2000 PNAD did not go to the field 35

Measures of Polarization and Conceptualization of Middle Class

* Measures of Polarization and Conceptualization of Middle Class The EGR strategy generates brackets of income classes of the income distribution observed in practice. The brackets chosen were the ones

* Measures of Polarization and Conceptualization of Middle Class The EGR strategy generates brackets of income classes of the income distribution observed in practice. The brackets chosen were the ones

Rio Social Change : Is There a Pre-Olympic Legacy? Executive Summary

Rio Social Change 2009-2016: Is There a Pre-Olympic Legacy? www.fgv.br/fgvsocial/rio2016/en Executive Summary The project s prime objective is to measure the evolution of the Rio population s living conditions

Rio Social Change 2009-2016: Is There a Pre-Olympic Legacy? www.fgv.br/fgvsocial/rio2016/en Executive Summary The project s prime objective is to measure the evolution of the Rio population s living conditions

Goals. Access the project site

Goals The main goal of this project is to assess the change in the quality of life of the population in Rio after the olympic venue announcement. We analyzed several areas such as education, labor, housing,

Goals The main goal of this project is to assess the change in the quality of life of the population in Rio after the olympic venue announcement. We analyzed several areas such as education, labor, housing,

6/8/2017. Looking Through the X. Rio2016 announcement

**** About the Project The term Olympic legacy refers generally to the projection of the gains to be seized by the city after the realization of the event. But can we already assess significant inflections

**** About the Project The term Olympic legacy refers generally to the projection of the gains to be seized by the city after the realization of the event. But can we already assess significant inflections

Income Inequality and Labor Market Dynamics in Brazil

Income Inequality and Labor Market Dynamics in Brazil Fernando de Holanda Barbosa Filho IBRE FGV Brazilian Institute of Economics Getulio Vargas Foundation Facts Income inequality declined in Brazil over

Income Inequality and Labor Market Dynamics in Brazil Fernando de Holanda Barbosa Filho IBRE FGV Brazilian Institute of Economics Getulio Vargas Foundation Facts Income inequality declined in Brazil over

Reducing Inequality and The Brazilian Social Protection System. South-South Learning Forum 2014 Rio de Janeiro, March 17

Reducing Inequality and The Brazilian Social Protection System South-South Learning Forum 2014 Rio de Janeiro, March 17 REAL GDP PER CAPITA* AND GINI INDEX** (*) Values updated by the GDP deflator (2011).

Reducing Inequality and The Brazilian Social Protection System South-South Learning Forum 2014 Rio de Janeiro, March 17 REAL GDP PER CAPITA* AND GINI INDEX** (*) Values updated by the GDP deflator (2011).

Income inequality and mobility in Australia over the last decade

Income inequality and mobility in Australia over the last decade Roger Wilkins Meeting of National Economic Research Organisations, OECD Headquarters, 18 June 2012 1993-94 1994-95 1995-96 1996-97 1997-98

Income inequality and mobility in Australia over the last decade Roger Wilkins Meeting of National Economic Research Organisations, OECD Headquarters, 18 June 2012 1993-94 1994-95 1995-96 1996-97 1997-98

Ministry of Finance. Brazilian Economic OUTLOOK

of Finance Brazilian Economic OUTLOOK Special Edition Year of 2010 Summary Foreword: A balance of the 2000s Economic Activity Mass Consumer Market Inflation Interest Rates and Credit International Overview

of Finance Brazilian Economic OUTLOOK Special Edition Year of 2010 Summary Foreword: A balance of the 2000s Economic Activity Mass Consumer Market Inflation Interest Rates and Credit International Overview

Cost Estimation of a Manufacturing Company

Cost Estimation of a Manufacturing Company Name: Business: Date: Economics of One Unit: Manufacturing Company (Only complete if you are making a product, such as a bracelet or beauty product) Economics

Cost Estimation of a Manufacturing Company Name: Business: Date: Economics of One Unit: Manufacturing Company (Only complete if you are making a product, such as a bracelet or beauty product) Economics

Rate of Access to Insurance by Type Total Population (15 years old and above)

") Rate of Access to Insurance by Type Total Population (15 years old and above) 16,79 12,94 2,95 4,31 0,45 Seguros (total) Plano / Seguro- Saúde Seguro de Veículo Seguro de Vida Previdência Privada Aberta

Rate of Access to Insurance by Type Total Population (15 years old and above) 16,79 12,94 2,95 4,31 0,45 Seguros (total) Plano / Seguro- Saúde Seguro de Veículo Seguro de Vida Previdência Privada Aberta

BRAZILIAN ECONOMIC OUTLOOK

BRAZILIAN ECONOMIC OUTLOOK BRAZILIAN ECONOMIC OUTLOOK Henrique Meirelles Henrique Meirelles February 8th, 2016 February 08th, 2016 INTRODUCTION 80 s Hyper inflation and volatility. 1994 Monetary stabilization

BRAZILIAN ECONOMIC OUTLOOK BRAZILIAN ECONOMIC OUTLOOK Henrique Meirelles Henrique Meirelles February 8th, 2016 February 08th, 2016 INTRODUCTION 80 s Hyper inflation and volatility. 1994 Monetary stabilization

Banco do Brasil. 2Q10 Conference Call

Banco do Brasil 2Q10 Conference Call 1 Disclaimer This presentation may include references and statements, planned synergies, increasing estimates, projections of results and future strategy for Banco

Banco do Brasil 2Q10 Conference Call 1 Disclaimer This presentation may include references and statements, planned synergies, increasing estimates, projections of results and future strategy for Banco

Private Equity in Brazil

Round Table: Cimarron Partners Private Equity in Brazil Henrique Meirelles 28 de Fevereiro de 2013 1 Agenda Introduc7on Macroeconomic and Poli7cal Stability Brazil Private Equity: Challenges and Opportuni7es

Round Table: Cimarron Partners Private Equity in Brazil Henrique Meirelles 28 de Fevereiro de 2013 1 Agenda Introduc7on Macroeconomic and Poli7cal Stability Brazil Private Equity: Challenges and Opportuni7es

Poverty and Inequality Dynamics in Manaus: Legacy of a Free Trade Zone?

Poverty and Inequality Dynamics in : Legacy of a Free Trade Zone? Marta Menéndez (LEDa DIAL, Université Paris-Dauphine) Marta Reis Castilho (Universidade Federal do Rio de Janeiro, Brazil) Aude Sztulman

Poverty and Inequality Dynamics in : Legacy of a Free Trade Zone? Marta Menéndez (LEDa DIAL, Université Paris-Dauphine) Marta Reis Castilho (Universidade Federal do Rio de Janeiro, Brazil) Aude Sztulman

Capital Flows to Latin America: Policy Challenges and Responses

Capital Flows to Latin America: Policy Challenges and Responses Javier Guzmán Calafell Director General Center for Latin American Monetary Studies INTERNATIONAL CAPITAL MOVEMENTS: OLD AND NEW DEBATES Cusco,

Capital Flows to Latin America: Policy Challenges and Responses Javier Guzmán Calafell Director General Center for Latin American Monetary Studies INTERNATIONAL CAPITAL MOVEMENTS: OLD AND NEW DEBATES Cusco,

POVERTY AND THE NEW RURAL MIDDLE CLASS

66 67 article POVERTY AND THE NEW RURAL MIDDLE CLASS MARCELO NERI Marcelo Neri ECONOMIST - HEAD OF THE FGV SOCIAL POLICIES CENTER (CPS) AND PROFESSOR AT RIO DE JANEIRO SCHOOL OF ECONOMICS OF FGV FOUNDATION

66 67 article POVERTY AND THE NEW RURAL MIDDLE CLASS MARCELO NERI Marcelo Neri ECONOMIST - HEAD OF THE FGV SOCIAL POLICIES CENTER (CPS) AND PROFESSOR AT RIO DE JANEIRO SCHOOL OF ECONOMICS OF FGV FOUNDATION

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

INTERNATIONAL CRISIS AND POLICY RESPONSES IN BRAZIL. Secretariat of Economic Policy January 2010

INTERNATIONAL CRISIS AND POLICY RESPONSES IN BRAZIL January 2010 1 CONDITIONS TO FACE THE CRISIS 2 CONDITIONS TO FACE THE CRISIS International Reserves and Low External Vulnerability Fiscal Responsibility

INTERNATIONAL CRISIS AND POLICY RESPONSES IN BRAZIL January 2010 1 CONDITIONS TO FACE THE CRISIS 2 CONDITIONS TO FACE THE CRISIS International Reserves and Low External Vulnerability Fiscal Responsibility

QUESTION 2. QUESTION 3 Which one of the following is most indicative of a flexible short-term financial policy?

QUESTION 1 Compute the cash cycle based on the following information: Average Collection Period = 47 Accounts Payable Period = 40 Average Age of Inventory = 55 QUESTION 2 Jan 41,700 July 39,182 Feb 18,921

QUESTION 1 Compute the cash cycle based on the following information: Average Collection Period = 47 Accounts Payable Period = 40 Average Age of Inventory = 55 QUESTION 2 Jan 41,700 July 39,182 Feb 18,921

Global Economic Prospects and the Developing Countries William Shaw December 1999

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Macro Research Economic outlook

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

ON MEASURING SOCIAL TENSIONS: with Applications to Brazil

ABSTRACT ON MEASURING SOCIAL TENSIONS: with Applications to Brazil Marcelo Neri Centro de Políticas Sociais (CPS/FGV) and EPGE/FGV-RJ Nanak Kakwani University of New South Wales, NSW, Sydney, Australia

ABSTRACT ON MEASURING SOCIAL TENSIONS: with Applications to Brazil Marcelo Neri Centro de Políticas Sociais (CPS/FGV) and EPGE/FGV-RJ Nanak Kakwani University of New South Wales, NSW, Sydney, Australia

P R O J E T A THE ECONOMIST

SCENARIOS OF THE BRAZILIAN ECONOMY Carlos Geraldo Langoni PricewaterhouseCoopers September / 2010 THE ECONOMIST STRUCTURAL CHANGES WORLD LEVEL: MULTIPOLARITY; DOMESTICALLY: MACRO CONSENSUS. MULTIPOLAR

SCENARIOS OF THE BRAZILIAN ECONOMY Carlos Geraldo Langoni PricewaterhouseCoopers September / 2010 THE ECONOMIST STRUCTURAL CHANGES WORLD LEVEL: MULTIPOLARITY; DOMESTICALLY: MACRO CONSENSUS. MULTIPOLAR

** Bolsa Família and the Economy (A Look on Final Goals)

") Accumulated variation of extreme poverty (p.p.) 12/05/2017 ** Bolsa Família and the Economy (A Look on Final Goals) Marcelo Neri Extreme Poverty Cumulative REDISTRIBUTION Effect Accumulated variation in

Accumulated variation of extreme poverty (p.p.) 12/05/2017 ** Bolsa Família and the Economy (A Look on Final Goals) Marcelo Neri Extreme Poverty Cumulative REDISTRIBUTION Effect Accumulated variation in

Overall Results - CCTs (Brazil)

") *Income Distribution, Distribution of Opportunities and Income Policies in Brazil: A Next Generation of CCTs? Marcelo Neri FGV Social/CPS *1 (Income Policies Block) Ref *2 A Next Generation of CCTs? Outline

*Income Distribution, Distribution of Opportunities and Income Policies in Brazil: A Next Generation of CCTs? Marcelo Neri FGV Social/CPS *1 (Income Policies Block) Ref *2 A Next Generation of CCTs? Outline

Nº 520 ISSN A new incidence analysis of Brazilian social policies using multiple data sources. Marcelo Neri

Nº 520 ISSN 0104-8910 A new incidence analysis of Brazilian social policies using multiple data sources Marcelo Neri Dezembro de 2003 A New Incidence Analysis of Brazilian Social Policies Using Multiple

Nº 520 ISSN 0104-8910 A new incidence analysis of Brazilian social policies using multiple data sources Marcelo Neri Dezembro de 2003 A New Incidence Analysis of Brazilian Social Policies Using Multiple

Ensaios Econômicos. Brazil s Middle Classes. Dezembro de Escola de. Pós-Graduação. em Economia. da Fundação. Getulio Vargas N 759 ISSN

Ensaios Econômicos Escola de Pós-Graduação em Economia da Fundação Getulio Vargas N 759 ISSN 0104-8910 Brazil s Middle Classes Marcelo Côrtes Neri Dezembro de 2014 URL: http://hdl.handle.net/10438/12988

Ensaios Econômicos Escola de Pós-Graduação em Economia da Fundação Getulio Vargas N 759 ISSN 0104-8910 Brazil s Middle Classes Marcelo Côrtes Neri Dezembro de 2014 URL: http://hdl.handle.net/10438/12988

INCOME, EXPENDITURE AND CONSUMPTION OF HOUSEHOLDS IN 2016

INCOME, EXPENDITURE AND CONSUMPTION OF HOUSEHOLDS IN 2016 Household income The annual total income average per capita is 5 167 BGN in 2016 and increases by 4.3 compared to 2015. The total income average

INCOME, EXPENDITURE AND CONSUMPTION OF HOUSEHOLDS IN 2016 Household income The annual total income average per capita is 5 167 BGN in 2016 and increases by 4.3 compared to 2015. The total income average

ASSETS, MARKETS AND POVERTY IN BRAZIL*

Red de Centros de Investigación de la Oficina del Economista Jefe Banco Interamericano de Desarrollo (BID) Documento de Trabajo R-357 ASSETS, MARKETS AND POVERTY IN BRAZIL* por Coordinator: Marcelo Côrtes

Red de Centros de Investigación de la Oficina del Economista Jefe Banco Interamericano de Desarrollo (BID) Documento de Trabajo R-357 ASSETS, MARKETS AND POVERTY IN BRAZIL* por Coordinator: Marcelo Côrtes

ECONOMY. Designing a new future THE BRAZILIAN

Argentina The rebuilding of Argentina Industry Change to survive Interview Marcelo Neri Director of the Social Policy Center of FGV THE BRAZILIAN ECONOMY A publication of the Getulio Vargas Foundation

Argentina The rebuilding of Argentina Industry Change to survive Interview Marcelo Neri Director of the Social Policy Center of FGV THE BRAZILIAN ECONOMY A publication of the Getulio Vargas Foundation

The Health of Jefferson County: 2010 Demographic Update

The Health of : 2010 Demographic Update BACKGROUND How people live the sociodemographic context of their lives influences their health. People who have lower incomes may not have the resources to meet

The Health of : 2010 Demographic Update BACKGROUND How people live the sociodemographic context of their lives influences their health. People who have lower incomes may not have the resources to meet

Development and investment prospects for Brazil. Brazilian American Chamber of Commerce Washington, October 10 th 2014

1 Development and investment prospects for Brazil Brazilian American Chamber of Commerce Washington, October 10 th 2014 2 Guide Growth prospects: sources of dynamism Investment forecast The role of BNDES

1 Development and investment prospects for Brazil Brazilian American Chamber of Commerce Washington, October 10 th 2014 2 Guide Growth prospects: sources of dynamism Investment forecast The role of BNDES

Interim results presentation 2017

Interim results presentation 2017 Contents Key indicators Operating environment What differentiates us Highlights Bank Save Credit Continued focus Key indicators Key indicators Earnings 4 000 3 500 3 000

Interim results presentation 2017 Contents Key indicators Operating environment What differentiates us Highlights Bank Save Credit Continued focus Key indicators Key indicators Earnings 4 000 3 500 3 000

Household Budget Survey

Central Bank of the Islamic Republic of Iran General Directorate of Economic Statistics Household Budget Survey In Urban Areas in Iran 1381 (March 21,2002 March 20,2003) Economic Statistics Bahman 1382

Central Bank of the Islamic Republic of Iran General Directorate of Economic Statistics Household Budget Survey In Urban Areas in Iran 1381 (March 21,2002 March 20,2003) Economic Statistics Bahman 1382

Trends and Transitory Shocks

EMBARGOED UNTIL WEDNESDAY, SEPTEMBER 27 AT 7:00 P.M.; OR UPON DELIVERY Trends and Transitory Shocks Eric S. Rosengren President & CEO Federal Reserve Bank of Boston September 27, 2017 The Money Marketeers

EMBARGOED UNTIL WEDNESDAY, SEPTEMBER 27 AT 7:00 P.M.; OR UPON DELIVERY Trends and Transitory Shocks Eric S. Rosengren President & CEO Federal Reserve Bank of Boston September 27, 2017 The Money Marketeers

Poverty Reduction in Brazil: Changes in the Profile and in the Determinants during the Early 2000s

Texto para Discussão 012 2017 Discussion Paper 012 2017 Poverty Reduction in Brazil: Changes in the Profile and in the Determinants during the Early 2000s Valéria Pero Associate Professor at the Economics

Texto para Discussão 012 2017 Discussion Paper 012 2017 Poverty Reduction in Brazil: Changes in the Profile and in the Determinants during the Early 2000s Valéria Pero Associate Professor at the Economics

INCOME, EXPENDITURE AND CONSUMPTION OF HOUSEHOLDS IN 2017

INCOME, EXPENDITURE AND CONSUMPTION OF HOUSEHOLDS IN 2017 Household income The annual total income average per capita is 5 586 BGN in 2017 and increases by 8.1 compared to 2016. The total income average

INCOME, EXPENDITURE AND CONSUMPTION OF HOUSEHOLDS IN 2017 Household income The annual total income average per capita is 5 586 BGN in 2017 and increases by 8.1 compared to 2016. The total income average

The Underground Economy. Fernando de Holanda Barbosa Filho IBRE FGV Brazilian Institute of Economics Getulio Vargas Foundation

The Underground Economy Fernando de Holanda Barbosa Filho IBRE FGV Brazilian Institute of Economics Getulio Vargas Foundation Underground Economy Refers to economic activities not reported to the authorities

The Underground Economy Fernando de Holanda Barbosa Filho IBRE FGV Brazilian Institute of Economics Getulio Vargas Foundation Underground Economy Refers to economic activities not reported to the authorities

Transparency in the U.S. Repo Market

Transparency in the U.S. Repo Market Antoine Martin Federal Reserve Bank of New York October 11, 2013 The views expressed in this presentation are my own and may not represent the views of the Federal

Transparency in the U.S. Repo Market Antoine Martin Federal Reserve Bank of New York October 11, 2013 The views expressed in this presentation are my own and may not represent the views of the Federal

INCOME DISTRIBUTION AND INEQUALITY MEASURES IN SINGAPORE

Conference on Chinese Population and Socioeconomic Studies: Utilizing the 2000/2001 round Census Data Hong Kong University of Science and Technology 19-21 June 2002, Hong Kong SAR INCOME DISTRIBUTION AND

Conference on Chinese Population and Socioeconomic Studies: Utilizing the 2000/2001 round Census Data Hong Kong University of Science and Technology 19-21 June 2002, Hong Kong SAR INCOME DISTRIBUTION AND

A Consistent Data Series to Evaluate Growth and Inequality in the National Accounts

A Consistent Data Series to Evaluate Growth and Inequality in the National Accounts David Johnson with D. Fixler, A. Craig, K. Furlong, Bureau of Economic Analysis Frontiers of Measuring Household Economic

A Consistent Data Series to Evaluate Growth and Inequality in the National Accounts David Johnson with D. Fixler, A. Craig, K. Furlong, Bureau of Economic Analysis Frontiers of Measuring Household Economic

The Future of Mexican Monetary Policy

The Future of Mexican Monetary Policy Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Mexico Summit Mexico City, 2 March 2017 */ The views expressed herein are strictly personal.

The Future of Mexican Monetary Policy Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Mexico Summit Mexico City, 2 March 2017 */ The views expressed herein are strictly personal.

Economic Conditions and Outlook and Consumer Credit Conditions

Economic Conditions and Outlook and Consumer Credit Conditions NACM-CFDD Kansas City Kansas City, MO Kelly D. Edmiston Senior Economist Disclaimer This presentation reflects the views of the speaker and

Economic Conditions and Outlook and Consumer Credit Conditions NACM-CFDD Kansas City Kansas City, MO Kelly D. Edmiston Senior Economist Disclaimer This presentation reflects the views of the speaker and

BNDES: The Financial Support for IT and Innovation Projects. December 2010

BNDES: The Financial Support for IT and Innovation Projects December 2010 Demand Drivers for IT in Brazil Domestic demandis supporting growth: increasing employment rates and salaries; reducing social

BNDES: The Financial Support for IT and Innovation Projects December 2010 Demand Drivers for IT in Brazil Domestic demandis supporting growth: increasing employment rates and salaries; reducing social

Financial results presentation Full year 2013

Financial results presentation Full year 2013 1 Contents Presentation of Speakers 2013 Operating Environment & Banking Industry CAL Bank Performance Highlights Income Statement Balance Sheet Share Price

Financial results presentation Full year 2013 1 Contents Presentation of Speakers 2013 Operating Environment & Banking Industry CAL Bank Performance Highlights Income Statement Balance Sheet Share Price

Gini coefficient

POVERTY AND SOCIAL INCLUSION INDICATORS (Preliminary results for 2010) 1 Poverty and social inclusion indicators are part of the general EU indicators for tracing the progress in the field of poverty and

POVERTY AND SOCIAL INCLUSION INDICATORS (Preliminary results for 2010) 1 Poverty and social inclusion indicators are part of the general EU indicators for tracing the progress in the field of poverty and

BRICs: actual growth and cooperation perspectives. International Advisory Council 3 rd Metting August 15, Luciano Coutinho President

BRICs: actual growth and cooperation perspectives International Advisory Council 3 rd Metting August 15, 2011 Luciano Coutinho President Emerging countries remain ahead in worldwide growth Annual Growth

BRICs: actual growth and cooperation perspectives International Advisory Council 3 rd Metting August 15, 2011 Luciano Coutinho President Emerging countries remain ahead in worldwide growth Annual Growth

Labour Market Challenges: Turkey

Labour Market Challenges: Turkey Conference Presentation «Boosting the social dimension in the Western Balkans and Turkey» Hakan Ercan Middle East Technical University, Ankara 31.01.2018 Belgrade 1 Growth

Labour Market Challenges: Turkey Conference Presentation «Boosting the social dimension in the Western Balkans and Turkey» Hakan Ercan Middle East Technical University, Ankara 31.01.2018 Belgrade 1 Growth

Poland s Economic Prospects

Poland s Economic Prospects Unicredit Conference Warsaw, June 8, 11 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe Recovery is driven by domestic demand Contributions to Real

Poland s Economic Prospects Unicredit Conference Warsaw, June 8, 11 Mark Allen Senior IMF Resident Representative for Central and Eastern Europe Recovery is driven by domestic demand Contributions to Real

ECONOMIC REPORT. Cost reduction and investment are key to resume economic growth. Brazilian economy in the third quarter of 2012

ECONOMIC REPORT Newsletter of the National Confederation of Industry Year 28 Number 03 July/September 2012 www.cni.org.br Cost reduction and investment are key to resume economic growth Brazilian economy

ECONOMIC REPORT Newsletter of the National Confederation of Industry Year 28 Number 03 July/September 2012 www.cni.org.br Cost reduction and investment are key to resume economic growth Brazilian economy

Global Economic Prospects: Navigating strong currents

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Financial stability is seen in the narrow sense of households being able to repay loans, and banks being exposed to the risk of non-performing loans,

FINANCE AND HOUSING IN CENTRAL AND EASTERN EUROPE: A DEMAND-SIDE APPROACH Liviu Voinea, Deputy Governor, National Bank of Romania Finance and Housing Panel, Bruegel Annual Meetings 217 In 215, ESRB published

FINANCE AND HOUSING IN CENTRAL AND EASTERN EUROPE: A DEMAND-SIDE APPROACH Liviu Voinea, Deputy Governor, National Bank of Romania Finance and Housing Panel, Bruegel Annual Meetings 217 In 215, ESRB published

THE BRAZILIAN ECONOMY AND THE AGENDA FOR REFORMS

THE BRAZILIAN ECONOMY AND THE AGENDA FOR REFORMS XX Joint of Japan Brazil Economic Cooperation Committee José Augusto Coelho Fernandes Policy and Strategy Director Curitiba, August 28th, 2017 FROM TOKYO

THE BRAZILIAN ECONOMY AND THE AGENDA FOR REFORMS XX Joint of Japan Brazil Economic Cooperation Committee José Augusto Coelho Fernandes Policy and Strategy Director Curitiba, August 28th, 2017 FROM TOKYO

Prices. Poverty Analysis. Poverty Datum Lines July Price $2.00. Enquiries: Tel /7. Date: 16 August 2016

Prices Poverty Analysis Main findings Price $2.00 Enquiries: Tel.706681/7 e-mail:prices@zimstat.co.zw Date: 16 August 2016 Poverty Datum Lines July 2016 The Food Poverty Line (FPL) for one person in July

Prices Poverty Analysis Main findings Price $2.00 Enquiries: Tel.706681/7 e-mail:prices@zimstat.co.zw Date: 16 August 2016 Poverty Datum Lines July 2016 The Food Poverty Line (FPL) for one person in July

A welfare union? Conference, BEI Luxembourg Kirchberg 10 December Tito Boeri, Università Bocconi. Tito Boeri Luxembourg Kirchberg Déc.

A welfare union? Conference, BEI Luxembourg Kirchberg 10 December Tito Boeri, Università Bocconi Tito Boeri Luxembourg Kirchberg Déc. The stress test Great Depression and Great Recession Fonte: Eichengreen

A welfare union? Conference, BEI Luxembourg Kirchberg 10 December Tito Boeri, Università Bocconi Tito Boeri Luxembourg Kirchberg Déc. The stress test Great Depression and Great Recession Fonte: Eichengreen

Evaluation of Latvia s Public Works Program (WWS)

") Capacity Building workshop on Impact Evaluation of Employment Programs Evaluation of Latvia s Public Works Program (WWS) Celine Ferre (Mehtabul Azam, Mohamed Ihsan Ajwad), Gdańsk, February 22, 2017 Background

Capacity Building workshop on Impact Evaluation of Employment Programs Evaluation of Latvia s Public Works Program (WWS) Celine Ferre (Mehtabul Azam, Mohamed Ihsan Ajwad), Gdańsk, February 22, 2017 Background

Annual General Meeting Fiscal Year 2013

Annual General Meeting Fiscal Year 2013 Oberhausen, April 16, 2014 Check against delivery. GEA Group Aktiengesellschaft Performance of GEA Group 2 Annual General Meeting Fiscal Year 2013 Highlights of

Annual General Meeting Fiscal Year 2013 Oberhausen, April 16, 2014 Check against delivery. GEA Group Aktiengesellschaft Performance of GEA Group 2 Annual General Meeting Fiscal Year 2013 Highlights of

Automated labor market diagnostics for low and middle income countries

Poverty Reduction Group Poverty Reduction and Economic Management (PREM) World Bank ADePT: Labor Version 1.0 Automated labor market diagnostics for low and middle income countries User s Guide: Definitions

Poverty Reduction Group Poverty Reduction and Economic Management (PREM) World Bank ADePT: Labor Version 1.0 Automated labor market diagnostics for low and middle income countries User s Guide: Definitions

Public Disclosure Copy

Public Disclosure Authorized LATIN AMERICA AND CARIBBEAN Brazil Social Protection & Labor Global Practice IBRD/IDA Investment Project Financing FY 2011 Seq No: 14 ARCHIVED on 21-Dec-2017 ISR30624 Implementing

Public Disclosure Authorized LATIN AMERICA AND CARIBBEAN Brazil Social Protection & Labor Global Practice IBRD/IDA Investment Project Financing FY 2011 Seq No: 14 ARCHIVED on 21-Dec-2017 ISR30624 Implementing

Too Big to Fail: Discussion of Quantifying Subsidies for SIFIs. Philip E. Strahan, Boston College & NBER. Minneapolis Fed.

Too Big to Fail: Discussion of Quantifying Subsidies for SIFIs Philip E. Strahan, Boston College & NBER Minneapolis Fed November 13 Distortions for TBTF borrowers Debt is too cheap for TBTF firms and not

Too Big to Fail: Discussion of Quantifying Subsidies for SIFIs Philip E. Strahan, Boston College & NBER Minneapolis Fed November 13 Distortions for TBTF borrowers Debt is too cheap for TBTF firms and not

Challenges to monetary policy in the EMEs

Challenges to monetary policy in the EMEs A view into the Brazilian Case Governor of the Banco Central do Brasil Ilan Goldfajn November 18th, 2017 Outline Benign international conditions and Emerging Markets

Challenges to monetary policy in the EMEs A view into the Brazilian Case Governor of the Banco Central do Brasil Ilan Goldfajn November 18th, 2017 Outline Benign international conditions and Emerging Markets

Current Economic Review April 16, 2014

Current Economic Review April 16, 2014 Brian Bonnenfant Project Manager Center for Regional Studies University of Nevada, Reno 784-1771 bonnen@unr.edu 230,000 225,000 **Peak = 228,100 Emp **Start of Great

Current Economic Review April 16, 2014 Brian Bonnenfant Project Manager Center for Regional Studies University of Nevada, Reno 784-1771 bonnen@unr.edu 230,000 225,000 **Peak = 228,100 Emp **Start of Great

Contents. HSBC Group in the world. HSBC in Brazil. New Economic Scenario / Macroeconomic Forecasts

HSBC GLOBAL & LOCAL STRATEGY IN A NEW ECONOMIC SCENARIO Conrado Engel CEO & President of HSBC Bank Brasil 26 March 2010 The British Chamber of Commerce and Industry in Brazil - São Paulo 0 Contents HSBC

HSBC GLOBAL & LOCAL STRATEGY IN A NEW ECONOMIC SCENARIO Conrado Engel CEO & President of HSBC Bank Brasil 26 March 2010 The British Chamber of Commerce and Industry in Brazil - São Paulo 0 Contents HSBC

Appendix E: The Economic Security Scorecard Sources and Definitions

Appendix E: The Economic Security Scorecard Sources and Definitions Economic Security Element Policy Area (Individual) Policy Data Definition Data Source Minimum Wage State Minimum Wage Minimum Wage State

Appendix E: The Economic Security Scorecard Sources and Definitions Economic Security Element Policy Area (Individual) Policy Data Definition Data Source Minimum Wage State Minimum Wage Minimum Wage State

Report to CenSus Joint Committee

Report to CenSus Joint Committee 9 th December 2016 By The Head of Revenues and Benefits (CenSus) INFORMATION REPORT CenSus Revenues and Benefits report. Executive Summary This report sets out the 16/17

Report to CenSus Joint Committee 9 th December 2016 By The Head of Revenues and Benefits (CenSus) INFORMATION REPORT CenSus Revenues and Benefits report. Executive Summary This report sets out the 16/17

Beyond market incorporation: challenges ahead

INOVANDO NO SETOR PÚBLICO BRASILEIRO Desafios Ins*tucionais e Polí*cas Públicas INNOVATION FOR INCLUSIVE GROWTH Columbia University NYC 2015 Beyond market incorporation: challenges ahead Lena LAVINAS Ins$tute

INOVANDO NO SETOR PÚBLICO BRASILEIRO Desafios Ins*tucionais e Polí*cas Públicas INNOVATION FOR INCLUSIVE GROWTH Columbia University NYC 2015 Beyond market incorporation: challenges ahead Lena LAVINAS Ins$tute

Development of Economy and Financial Markets of Kazakhstan

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

Introduction to the UK Economy

Introduction to the UK Economy What are the key objectives of macroeconomic policy? Price Stability (CPI Inflation of 2%) Growth of Real GDP (National Output) Falling Unemployment / Raising Employment

Introduction to the UK Economy What are the key objectives of macroeconomic policy? Price Stability (CPI Inflation of 2%) Growth of Real GDP (National Output) Falling Unemployment / Raising Employment

Brazil. Results 1H13. July 30 th, 2013

Brazil Results 1H13 July 30 th, 2013 Important information Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements within the meaning of the US Private Securities

Brazil Results 1H13 July 30 th, 2013 Important information Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements within the meaning of the US Private Securities

National Economic Conditions. Cheyenne AIA Meeting February 25th, 2011 Rob Godby

National Economic Conditions Cheyenne AIA Meeting February 25th, 2011 Rob Godby Percent Change Recovery is Technically Underway 8 Quarter-Quarter Growth in Real GDP 6 4 2 0-2 -4-6 -8 I II III IV I II III

National Economic Conditions Cheyenne AIA Meeting February 25th, 2011 Rob Godby Percent Change Recovery is Technically Underway 8 Quarter-Quarter Growth in Real GDP 6 4 2 0-2 -4-6 -8 I II III IV I II III

Economic Outlook. Macroeconomic Research Itaú Unibanco

Economic Outlook Macroeconomic Research Itaú Unibanco March 2015 Overview International Global growth on the rise. U.S. interest rates will soon follow U.S. economic fundamentals remain solid. Rates are

Economic Outlook Macroeconomic Research Itaú Unibanco March 2015 Overview International Global growth on the rise. U.S. interest rates will soon follow U.S. economic fundamentals remain solid. Rates are

Quarterly Statistical Digest

Quarterly Statistical Digest August Volume 27, No. 3 The Statistical Digest is a quarterly publication of the Central Bank of The Bahamas, prepared by the Research Department for issue in February, May,

Quarterly Statistical Digest August Volume 27, No. 3 The Statistical Digest is a quarterly publication of the Central Bank of The Bahamas, prepared by the Research Department for issue in February, May,

Macroeconomic Impact of the Subprime Crisis

Franco German Council of Economic Advisors Paris, 5 February 2008 Dr. Stefan Kooths DIW Berlin, Macro Analysis and Forecasting Approach Assuming a strictly macroeconomic point of view - Thinking in aggregates

Franco German Council of Economic Advisors Paris, 5 February 2008 Dr. Stefan Kooths DIW Berlin, Macro Analysis and Forecasting Approach Assuming a strictly macroeconomic point of view - Thinking in aggregates

Gallons per Capita - v2.05

Gallons per Capita - v2.5 This spreadsheet-based GPCD calculator is designed to help quantify and track water uses associated with water distribution systems. The spreadsheet contains several separate

Gallons per Capita - v2.5 This spreadsheet-based GPCD calculator is designed to help quantify and track water uses associated with water distribution systems. The spreadsheet contains several separate

Brazil. Results January 30 th, 2014

Brazil Results 2013 January 30 th, 2014 Important information Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements within the meaning of the US Private

Brazil Results 2013 January 30 th, 2014 Important information Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements within the meaning of the US Private

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16 FISCAL POLICY IN THE GREAT RECESSION MARCH 19, 2018 I. OVERVIEW II. ECONOMIC STIMULUS ACT

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 16 FISCAL POLICY IN THE GREAT RECESSION MARCH 19, 2018 I. OVERVIEW II. ECONOMIC STIMULUS ACT

Case No. FINANCIAL AFFIDAVIT

IN THE DISTRICT COURT OF COUNTY STATE OF OKLAHOMA Plaintiff, Case No. v. Defendant, FINANCIAL AFFIDAVIT This document is filed by father/mother (Circle one) FATHER: ADDRESS: CITY, STATE, ZIP SOC SEC NO:

IN THE DISTRICT COURT OF COUNTY STATE OF OKLAHOMA Plaintiff, Case No. v. Defendant, FINANCIAL AFFIDAVIT This document is filed by father/mother (Circle one) FATHER: ADDRESS: CITY, STATE, ZIP SOC SEC NO:

London Borough of Barnet Pension Fund. Communication Strategy (2018)

") London Borough of Barnet Pension Fund Communication Strategy (2018) Background This document sets out the communication strategy for the London Borough of Barnet Pension Fund. The London Borough of Barnet

London Borough of Barnet Pension Fund Communication Strategy (2018) Background This document sets out the communication strategy for the London Borough of Barnet Pension Fund. The London Borough of Barnet

THE BRAZILIAN ECONOMY AND THE AGENDA FOR REFORMS

THE BRAZILIAN ECONOMY AND THE AGENDA FOR REFORMS VIII CNI DIPLOMATIC BRIEFING José Augusto Coelho Fernandes Policy and Strategy Director Brasilia, November 21st, 2017 FROM JUNE TO NOVEMBER WHAT CHANGED

THE BRAZILIAN ECONOMY AND THE AGENDA FOR REFORMS VIII CNI DIPLOMATIC BRIEFING José Augusto Coelho Fernandes Policy and Strategy Director Brasilia, November 21st, 2017 FROM JUNE TO NOVEMBER WHAT CHANGED

EMPLOYMENT AND EARNINGS

L2- EMPLOYMENT AND EARNINGS U.S. Department of Labor Bureau of Labor Statistics October 997 In this issue: Third quarter 997 averages for household survey data Monthly Household Data Historical A-. Employment

L2- EMPLOYMENT AND EARNINGS U.S. Department of Labor Bureau of Labor Statistics October 997 In this issue: Third quarter 997 averages for household survey data Monthly Household Data Historical A-. Employment

Structural Reforms in the Argentine Economy: Achievements and Pending Reforms

Structural Reforms in the Argentine Economy: Achievements and Pending Reforms Achievements Elimination of Capital Flows Controls ( cepo ) Agreement with holdouts and resolution of conflicts with other

Structural Reforms in the Argentine Economy: Achievements and Pending Reforms Achievements Elimination of Capital Flows Controls ( cepo ) Agreement with holdouts and resolution of conflicts with other

Employment from the BLS household and payroll surveys: summary of recent trends

Employment from the BLS household and payroll surveys: summary of recent trends Overview The Bureau of Labor Statistics (BLS) has two monthly surveys that measure employment levels and trends: the Current

Employment from the BLS household and payroll surveys: summary of recent trends Overview The Bureau of Labor Statistics (BLS) has two monthly surveys that measure employment levels and trends: the Current

Spheria Australian Smaller Companies Fund

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

International Monetary Fund Washington, D.C.

2004 International Monetary Fund May 2004 IMF Country Report No. 04/140 January 29, 2001 January 29, 2001 January 29, 2001 January 29, 2001 January 29, 2001 Republic of Belarus: Statistical Appendix This

2004 International Monetary Fund May 2004 IMF Country Report No. 04/140 January 29, 2001 January 29, 2001 January 29, 2001 January 29, 2001 January 29, 2001 Republic of Belarus: Statistical Appendix This

Economic Overview York County, South Carolina. February 14, 2018

Economic Overview York County, February 14, 2018 DEMOGRAPHIC PROFILE... 3 EMPLOYMENT TRENDS... 5 UNEMPLOYMENT RATE... 5 WAGE TRENDS... 6 COST OF LIVING INDEX... 6 INDUSTRY SNAPSHOT... 7 OCCUPATION SNAPSHOT...

Economic Overview York County, February 14, 2018 DEMOGRAPHIC PROFILE... 3 EMPLOYMENT TRENDS... 5 UNEMPLOYMENT RATE... 5 WAGE TRENDS... 6 COST OF LIVING INDEX... 6 INDUSTRY SNAPSHOT... 7 OCCUPATION SNAPSHOT...

Investor Presentation JUNE 2018

Investor Presentation JUNE 2018 Forward Looking Statements & Other Disclosure Matters Forward-Looking Statements - This presentation contains forward-looking statements within the meaning of the federal

Investor Presentation JUNE 2018 Forward Looking Statements & Other Disclosure Matters Forward-Looking Statements - This presentation contains forward-looking statements within the meaning of the federal

Common stock prices 1. New York Stock Exchange indexes (Dec. 31,1965=50)2. Transportation. Utility 3. Finance

2. Transportation. Utility 3. Finance") Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Forecasting long-term electricity demand in the residential sector

Available online at www.sciencedirect.com ScienceDirect Procedia Computer Science 55 (2015 ) 529 538 Information Technology and Quantitative Management (ITQM 2015) Forecasting long-term electricity demand

Available online at www.sciencedirect.com ScienceDirect Procedia Computer Science 55 (2015 ) 529 538 Information Technology and Quantitative Management (ITQM 2015) Forecasting long-term electricity demand

Regional overview Gisborne

Regional overview Purchasing intentions - additional income-related rent subsidy (IRRS) places Area District 1 2 3 4+ TOTAL 3 35 5 7 total 3 35 5 7 7 8 9 1 11 Purchasing intentions - change within the

Regional overview Purchasing intentions - additional income-related rent subsidy (IRRS) places Area District 1 2 3 4+ TOTAL 3 35 5 7 total 3 35 5 7 7 8 9 1 11 Purchasing intentions - change within the

Section 6621 of the Internal Revenue Code establishes the interest rates on

Part 1 Section 6621.--Determination of Rate of Interest 26 CFR 301.6621-1: Interest rate. Rev. Rul. -32 Section 6621 of the Internal Revenue Code establishes the interest rates on overpayments and underpayments

Part 1 Section 6621.--Determination of Rate of Interest 26 CFR 301.6621-1: Interest rate. Rev. Rul. -32 Section 6621 of the Internal Revenue Code establishes the interest rates on overpayments and underpayments

Exotic Tea Prices. Year

Price, cents per pound UNDERSTANDING HOW TO READ GRAPHS Information is often presented in the form of a graph, a diagram that shows numerical data in a visual form. Graphs enable us to see relationships

Price, cents per pound UNDERSTANDING HOW TO READ GRAPHS Information is often presented in the form of a graph, a diagram that shows numerical data in a visual form. Graphs enable us to see relationships

Nonfarm Payroll Employment

PRESIDENT'S REPORT TO THE BOARD OF DIRECTORS, FEDERAL RESERVE BANK OF BOSTON Current Economic Developments - June 10, 2004 Data released since your last Directors' meeting show the economy continues to

PRESIDENT'S REPORT TO THE BOARD OF DIRECTORS, FEDERAL RESERVE BANK OF BOSTON Current Economic Developments - June 10, 2004 Data released since your last Directors' meeting show the economy continues to

Lower GDP growth due to new drop in industry

Change in investment% Newsletter of the National Confederation of Industry ISSN 1983-621X Year 29 Number 02 April/June 2014 www.cni.org.br Lower GDP growth due to new drop in industry Brazilian economy

Change in investment% Newsletter of the National Confederation of Industry ISSN 1983-621X Year 29 Number 02 April/June 2014 www.cni.org.br Lower GDP growth due to new drop in industry Brazilian economy

Section 6621(c) provides that for purposes of interest payable under 6601 on any large corporate underpayment, the underpayment

provides that for purposes of interest payable under 6601 on any large corporate underpayment, the underpayment") Section 6621. Determination of Interest Rate 26 CFR 301.6621 1: Interest rate. Interest rates; underpayments and overpayments. The rate of interest determined under section 6621 of the Code for the calendar

Section 6621. Determination of Interest Rate 26 CFR 301.6621 1: Interest rate. Interest rates; underpayments and overpayments. The rate of interest determined under section 6621 of the Code for the calendar

Regional overview Hawke's Bay

Regional overview Purchasing intentions - additional income-related rent subsidy (IRRS) places Area Hastings Central 1 2 3 4+ TOTAL 5 5 25 125 3 3 1 7 total 8 8 35 195 7 8 9 1 11 Purchasing intentions

Regional overview Purchasing intentions - additional income-related rent subsidy (IRRS) places Area Hastings Central 1 2 3 4+ TOTAL 5 5 25 125 3 3 1 7 total 8 8 35 195 7 8 9 1 11 Purchasing intentions

SOVEREIGN ISSUES PLURINATIONAL STATE OF BOLIVIA

SOVEREIGN ISSUES PLURINATIONAL STATE OF BOLIVIA Presented by Roger Edwin Rojas Ulo Vice Minister of the Treasury and Public Credit Ministry of Economy and Public Finance Brussels, 4 April 2014 Bolivia

SOVEREIGN ISSUES PLURINATIONAL STATE OF BOLIVIA Presented by Roger Edwin Rojas Ulo Vice Minister of the Treasury and Public Credit Ministry of Economy and Public Finance Brussels, 4 April 2014 Bolivia

New Jersey Employer Certification

New Jersey Employer Certification Oxford Health Insurance, Inc. or Oxford Health Plans (NJ), Inc. ( Oxford ) Mailing Address: Oxford Group Enrollment, P.O. Box 29142, Hot Springs, AR 71903-9142 800-385-9088

New Jersey Employer Certification Oxford Health Insurance, Inc. or Oxford Health Plans (NJ), Inc. ( Oxford ) Mailing Address: Oxford Group Enrollment, P.O. Box 29142, Hot Springs, AR 71903-9142 800-385-9088

1Q of FY ending December 31, (0.2) (1.9) 11.3 (0.2) (0.2) (0.2) (0.2) (1.2) (89.2) 0.1

(1.9) 11.3 (0.2) (0.2) (0.2) (0.2) (1.2) (89.2) 0.1") August 6, ISEKI & CO., LTD. Supplementary Information to Consolidated Financial Results (April 1, June 30, ) I. Consolidated business results for the three months ended June 30, (Billions of yen, %) Year-on

August 6, ISEKI & CO., LTD. Supplementary Information to Consolidated Financial Results (April 1, June 30, ) I. Consolidated business results for the three months ended June 30, (Billions of yen, %) Year-on

Asia Key Economic and Financial Indicators 20-Oct-16

Asia Key Economic and Financial Indicators -Oct- ASEAN Brunei (BN) Cambodia (KH) Indonesia () Laos (LA) Malaysia () Myanmar (MM) Philippines () Singapore () Thailand () Vietnam () East Asia China (CN)

Asia Key Economic and Financial Indicators -Oct- ASEAN Brunei (BN) Cambodia (KH) Indonesia () Laos (LA) Malaysia () Myanmar (MM) Philippines () Singapore () Thailand () Vietnam () East Asia China (CN)

The effects of changes to housing benefit in the private rented sector

The effects of changes to housing benefit in the private rented sector Robert Joyce, Institute for Fiscal Studies Presentation at ESRI, Dublin 5 th March 2015 From joint work with Mike Brewer, James Browne,

The effects of changes to housing benefit in the private rented sector Robert Joyce, Institute for Fiscal Studies Presentation at ESRI, Dublin 5 th March 2015 From joint work with Mike Brewer, James Browne,