Monetary policy of the ECB, its concepts and tools

|

|

|

- Shanon Wilkinson

- 5 years ago

- Views:

Transcription

1 Monetary policy of the ECB, its concepts and tools Frankfurt am Main, 20 September 2011 Markus A. Schmidt Directorate Monetary Policy 1

2 Disclaimer The views expressed are those of the presenter and should therefore not necessarily be viewed and not be reported as representing the views of the European Central Bank. 2

3 Outline The ECB s monetary policy Principles of the ECB s monetary policy Economic Analysis Monetary Analysis The monetary transmission process ECB s response to the crisis 3

4 Outline The ECB s monetary policy Principles of the ECB s monetary policy Economic Analysis Monetary Analysis The monetary transmission process ECB s response to the crisis Anything else? 4

5 ECB s monetary policy objective Article 127 of the Treaty of the Functioning of the European Union: The primary objective of the ESCB [Eurosystem] shall be to maintain price stability Without prejudice of the objective of price stability, the ESCB [Eurosystem] shall support the general economic policies with a view to contributing to the achievement of the objectives of the Union as laid down in Article 3 of the Treaty on European Union. 5

6 ECB s quantitative definition of price stability The Governing Council [GovC] of the ECB in October 2008 defined price stability as a year-on-year increase of the Harmonised Index of Consumer Prices [HICP] for the euro area below 2%. Price Stability is to be maintained over the medium term. The GovC aims to maintain inflation rates at levels below, but close to, 2% over the medium term. 6

7 Why below, but close to, 2%? Below in order to fully reap the benefits of price stability. Close to to ensure an adequate margin that avoids risks of deflation, addresses implications of inflation differentials among euro area Member States and takes possible small measurement bias in HICP into account. 7

8 Why is price stability important Inflation is hampering the price mechanism (absolute-relative confusion, permanent-transitory confusion), is affecting the allocation of income (debtors vs. creditors, wagelag hypothesis) in case of non-anticipated inflation, causes a decrease in efficiency, even if inflation is anticipated, results in sub-optimal holdings of money, reducing households purchasing power. 8

9 Inflation s consequences for purchasing power Purchasing power of 100 Euro (2011) Purchasing power of 100 Euro (2011) Annual inflation rate of... 1% 2% 3% 4% 5% Source: ECB calculations.

10 Inflation and inflation expectations 5.0 Long-term inflation expectation (5y5y forward inflation swap rate) Medium-term inflation expectation (5y spot inflation swap rate) Short-term inflation expectations (1y spot inflation swap rate) HICP (annual growth rate, percentage points) Dec-04 Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Source: Bloomberg, ECB and ECB calculations. Latest observation: September 2011, end-of-month data (inflation swaps) and monthly data (HICP), percentage points. 10

11 Safeguards for sound monetary policy Institutional safeguards Clear mandate: Price stability as primary objective Independence from political influence Clear allocation of responsibilities Strategic safeguards Credible commitment towards mandate Consistent framework for analysis and decision-making Clear and transparent communication 11

12 The ECB s monetary policy strategy Primary objective of price stability Economic analysis Governing Council takes monetary policy decisions based on an overall assessment of the risks to price stability Monetary analysis Analysis of economic dynamics and shocks cross checking Analysis of monetary trends Full set of information 12

13 Key principles of the ECB s monetary policy strategy Forward-looking nature Medium-term orientation Broad-based analysis Cross-checking of analyses 13

14 Outline The ECB s monetary policy Principles of the ECB s monetary policy Economic Analysis Monetary Analysis The monetary transmission process ECB s response to the crisis Anything else? 14

15 Economic Analysis The Economic Analysis aims at identifying short- to medium-term risks to price stability. Forward-looking assessment of relevant information from a variety of indicators (e. g. business cycle, wages, exchange rate, asset prices, financial yields, fiscal policy, etc.). Quarterly macroeconomic projections for inflation and growth in the euro area, prepared by staff of the Eurosystem/ ECB 15

16 Economic Analysis The scope of the Economic Analysis are factors determining supply- and demand-conditions on goods markets, services markets, and factor markets [capital markets, labour markets]. It investigates shocks to the economy, the resulting dynamic processes as well as the perspectives stemming from that. 16

17 Economic Analysis Among the indicators relevant for Economic Analysis are price indicators, expenditure components, production indicators, sentiment indicators, labour market indicators and financial market indicators. 17

18 Outline The ECB s monetary policy Principles of the ECB s monetary policy Economic Analysis Monetary Analysis The monetary transmission process ECB s response to the crisis Anything else? 18

19 Monetary Analysis The Monetary Analysis aims at identifying medium- to longer-term risks to price stability. The basis of Monetary Analysis is the conviction that inflation is always a monetary phenomenon, at least in the long-run. Money has leading indicator properties for inflation in the euro area in the medium- to long-run. Regular monitoring of money and credit developments contributes to identifying emergence of unsustainable developments in asset prices. 19

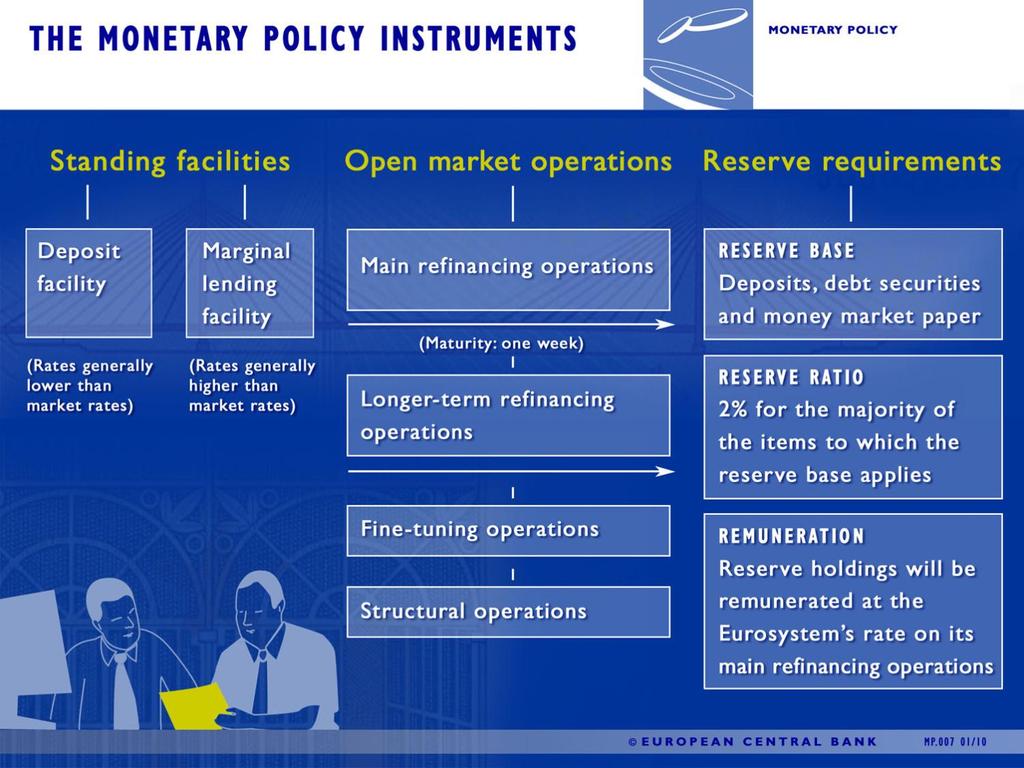

20 Monetary Analysis M P M* P* t t M M * P P * M * M* P * P* t t 20

21 Monetary Analysis Monetary Analysis is mainly based on balance sheet data of the money-issuing sector, i.e. so-called Monetary Financial Institutions [MFIs]. Assets Credit to general government Loans Securities Credit to private sector Loans Securities Net claims on non-euro area residents Securities Liabilities Currency in circulation Overnight deposits Other short term deposits Marketable instruments Holdings of central government Longer term liabilities 21

22 Credit is the main source of monetary dynamics 14 Loans to the private sector (adjusted for securitisation) M Source: ECB. Latest observation: July 2011, monthly data, annual growth rates, percentage points Jan-00 Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

23 Outline The ECB s monetary policy Principles of the ECB s monetary policy Economic Analysis Monetary Analysis The monetary transmission process ECB s response to the crisis Anything else? 23

24 The monetary transmission process 24

25 25

26 Monetary transmission in normal times Overnight rate mirrors official key interest rate over maintenance period. ECB influences money market conditions by setting key interest rates and managing the liquidity situation in the banking sector by benchmark allotment. Banks with liquidity surplus lend to those with deficits over inter-bank money market. Government bonds play an important role as collateral and for the pricing of fixed income securities, hence availability is important. 26

27 Steering money market conditions Main refinancing operations Marginal lending facility Deposit facility Eonia (monhtly average) % 7 7 % Feb-00 Aug-00 Feb-01 Aug-01 Feb-02 Aug-02 Feb-03 Aug-03 Feb-04 Aug-04 Feb-05 Aug-05 Feb-06 Aug-06 Feb-07 Aug-07 Feb-08 Aug-08 Feb-09 Aug-09 Feb-10 Aug-10 Feb-11 Aug-11 Source: ECB. Latest observation: August 2011, monthly averages of daily observations

28 Steering money market conditions Long-term interest rate (10 y) Short-term interest rate (3 m) Eonia (monhtly average) % 6 6 % Feb-00 Aug-00 Feb-01 Aug-01 Feb-02 Aug-02 Feb-03 Aug-03 Feb-04 Aug-04 Feb-05 Aug-05 Feb-06 Aug-06 Feb-07 Aug-07 Feb-08 Aug-08 Feb-09 Aug-09 Feb-10 Aug-10 Feb-11 Aug Source: ECB. Latest observation: August 2011, monthly averages of daily observations

29 Outline The ECB s monetary policy Principles of the ECB s monetary policy Economic Analysis Monetary Analysis The monetary transmission process ECB s response to the crisis Anything else? 29

30 The financial turmoil and the money market Eurepo (3M) Euribor (3M) Depo-Repo-Spread (3M, RHS) % bp Jan-07 Mar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep Source: Bloomberg and ECB calculations. Last observation: 15 September 2011, daily observations

31 Impairment of the monetary transmission process 31

32 The ECB s response to the crisis Immediate response on 9 August 2007 Allowed banks to draw full amount of what they needed on overnight basis against collateral at the prevailing main refinancing rate (ca 95 bn) In the following months Supplementary refinancing operations with 3 and 6 months maturity Intra-maintenance period frontloading More frequent fine-tuning operations Provision of US dollar liquidity against euro-denominated collateral 32

33 Liquidity management measures Pre-crisis benchmark allotment Pre-Lehman frontloading [EUR billions] [EUR billions] /07/07 14/07/07 17/07/07 20/07/07 23/07/07 26/07/07 29/07/07 01/08/07 04/08/07 07/08/ /08/07 11/08/07 14/08/07 17/08/07 20/08/07 23/08/07 26/08/07 29/08/07 01/09/07 04/09/07 07/09/07 10/09/07 Daily current accounts Reserve requirements Daily current accounts Reserve requirements EUR [billions] Post-Lehman ample liquidity Reserve requirement Reserve holdings Recourse to deposit facility /12/08 14/12/08 18/12/08 22/12/08 26/12/08 30/12/08 03/01/09 07/01/09 11/01/09 15/01/09 19/01/09 Daily current accounts Deposit facility Reserve requirements EUR billions Source: ECB. 33

34 Decline in key interest rates by 325 bp in 7 months Main refinancing operations Marginal lending facility Deposit facility Eonia (monhtly average) % 6 6 % Aug-07 Oct-07 Dec-07 Feb-08 Apr-08 Jun-08 Aug-08 Oct-08 Dec-08 Feb-09 Apr-09 Jun-09 Aug-09 Oct-09 Dec-09 Feb-10 Apr-10 Jun-10 Aug-10 Oct-10 Dec-10 Feb-11 Apr-11 Jun-11 Aug Source: ECB. Last observation: August 2011, monthly averages of daily observations.

35 affected loans-rates, too! Short-term Long-term (floating rate and up to 1 year) (over 5 years) Small loans to NFCs Large loans to NFCs Loans for house pruchase Consumer credit Other lending Eonia (monhtly average) % % Small loans to NFCs 10 Large loans to NFCs Loans for house purchase (over 5 and up to 10 years) Loans for house purchase (over 10 years) Consumer credit Other lending % 10 Eonia (monhtly average) % Jan-07 Mar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Jan-07 M ar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-08 M ar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 M ar-09 May-09 Jul-09 Sep-09 Nov-09 Jan-10 M ar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 M ar-11 May-11 Jul-11 Source: ECB and ECB calculations. Last observation: July

36 Further responses enhanced credit support ECB s enhanced credit support consisted of mainly bank-based measures to support the flow of credit beyond standard interest rate channel Fixed-rate full allotment Expansion of collateral Longer-term liquidity provision Liquidity provision in foreign currencies Financial market support through purchases of covered bonds 36

37 Temporary improvements Against background of improved money market conditions ECB introduced exit strategy from non-standard measures, as they were temporary by nature Non-continuation of purchases of covered bonds Partly withdrawal of liquidity provision in foreign currency Non-continuation of long-term liquidity provision No pre-determined sequence between the exit from nonstandard measures and interest rate action Assessment of risks to price stability primary criterion 37

38 5-year sovereign CDS spreads DE FR IT ES IE PT GR bp bp Jan-07 Mar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep Source: Bloomberg. Last observation: 14 September 2011, daily observations.

39 ECB s response to the sovereign debt crisis ECB introduced the Securities Markets Programme [SMP] to safeguard the well-functioning of the transmission process by conducting interventions in euro area debt securities markets. Purchases ensure depth and liquidity in dysfunctional securities markets and are conducted on secondary markets only. 39

40 ECB s response to the sovereign debt crisis ECB re-introduced some non-standard measures that had been phased-out earlier. Fixed-rate full allotment in 3M refinancing operations Temporary 6M refinancing operations Fixed-rate full allotment in USD (new) 40

41 Literature Monthly Bulletin The ECB s monetary policy stance during the financial crisis (January 2010) The ECB s response to the financial crisis (October 2010) Asset price bubbles and monetary policy revisited (November 2010) 41

42 Literature The Monetary Policy of the ECB 42

43 Literature The European Central Bank, the Eurosystem, the European System of Central Banks 43

44 Literature Price Stability: Why is it important for you? 44

45 Monetary policy of the ECB, its concepts and tools Frankfurt am Main, 20 September 2011 Markus A. Schmidt Directorate Monetary Policy 45

Challenges to the single monetary policy and the ECB s response. Benoît Cœuré Member of the Executive Board European Central Bank

Challenges to the single monetary policy and the ECB s response Benoît Cœuré Member of the Executive Board European Central Bank Institut d études politiques, Paris 2 September 212 1 Prime conduit of monetary

Challenges to the single monetary policy and the ECB s response Benoît Cœuré Member of the Executive Board European Central Bank Institut d études politiques, Paris 2 September 212 1 Prime conduit of monetary

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

Recent developments in the euro money market. Money Market Contact Group Frankfurt, 18 September 2012

Recent developments in the euro money market Money Market Contact Group Frankfurt, 18 September 2012 ECB developments and announcements I 5 July 2012 The ECB reduced by 25 basis points the interest rate

Recent developments in the euro money market Money Market Contact Group Frankfurt, 18 September 2012 ECB developments and announcements I 5 July 2012 The ECB reduced by 25 basis points the interest rate

Monetary Policy Operations

Monetary Policy Operations Denis Blenck DG Market Operations Generation uro Students Award Teachers session 24 September 2012 Outline MONETARY POLICY IMPLEMENTATION IN NORMAL TIMES MONETARY POLICY IMPLEMENTATION

Monetary Policy Operations Denis Blenck DG Market Operations Generation uro Students Award Teachers session 24 September 2012 Outline MONETARY POLICY IMPLEMENTATION IN NORMAL TIMES MONETARY POLICY IMPLEMENTATION

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks. Franziska Schobert

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks Franziska Schobert Agenda 1. Overview on crisis-related developments in the euro area 2. Impact of crisis-related measures on central

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks Franziska Schobert Agenda 1. Overview on crisis-related developments in the euro area 2. Impact of crisis-related measures on central

ABI MONTHLY REPORT 1 March 2018 (Main evidence)

") ABI MONTHLY REPORT 1 March 2018 (Main evidence) LOANS AND DEPOSITS 1. In February 2018, loans to customers granted by banks operating in Italy, totalling 1,777.2 billion euro (cf. Table 1) was almost 70

ABI MONTHLY REPORT 1 March 2018 (Main evidence) LOANS AND DEPOSITS 1. In February 2018, loans to customers granted by banks operating in Italy, totalling 1,777.2 billion euro (cf. Table 1) was almost 70

ABI MONTHLY REPORT 1 January 2017 (Main evidence)

") ABI MONTHLY REPORT 1 January 2017 (Main evidence) LOANS AND DEPOSITS 1. At the end of 2016, loans to customers granted by banks operating in Italy, totalling 1,807.7 billion euro (cf. Table 1) was nearly

ABI MONTHLY REPORT 1 January 2017 (Main evidence) LOANS AND DEPOSITS 1. At the end of 2016, loans to customers granted by banks operating in Italy, totalling 1,807.7 billion euro (cf. Table 1) was nearly

The Eurosystem s asset purchase programme

Katja Hettler Lia Cruz Monika Znidar Euro Area Bond Markets Section DG-Market Operations The Eurosystem s asset purchase programme ECB Central Banking Seminar Frankfurt, 13 July 2018 Rubric The Eurosystem

Katja Hettler Lia Cruz Monika Znidar Euro Area Bond Markets Section DG-Market Operations The Eurosystem s asset purchase programme ECB Central Banking Seminar Frankfurt, 13 July 2018 Rubric The Eurosystem

ABI MONTHLY REPORT 1 July 2018 (Main evidence)

") ABI MONTHLY REPORT 1 July 2018 (Main evidence) LOANS AND DEPOSITS 1. In June 2018, loans to customers granted by banks operating in Italy, totalling 1,773.8 billion euro (cf. Table 1) was 37 billion higher

ABI MONTHLY REPORT 1 July 2018 (Main evidence) LOANS AND DEPOSITS 1. In June 2018, loans to customers granted by banks operating in Italy, totalling 1,773.8 billion euro (cf. Table 1) was 37 billion higher

LEGAL BASIS OBJECTIVES ACHIEVEMENTS

EUROPEAN MONETARY POLICY The European System of Central Banks (ESCB) comprises the ECB and the national central banks of all the EU Member States. The primary objective of the ESCB is to maintain price

EUROPEAN MONETARY POLICY The European System of Central Banks (ESCB) comprises the ECB and the national central banks of all the EU Member States. The primary objective of the ESCB is to maintain price

The crisis response in the euro area. Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 2013

The crisis response in the euro area Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 213 Outline A. How the crisis developed B. Monetary policy response C. Structural adjustment underway

The crisis response in the euro area Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 213 Outline A. How the crisis developed B. Monetary policy response C. Structural adjustment underway

Forecasting liquidity and conducting credit operations

Irene Katsalirou Money Market and Liquidity Division Directorate General Market Operations Forecasting liquidity and conducting credit operations ECB Central Banking Seminar Frankfurt am Main, 12 July

Irene Katsalirou Money Market and Liquidity Division Directorate General Market Operations Forecasting liquidity and conducting credit operations ECB Central Banking Seminar Frankfurt am Main, 12 July

1.1. Low yield environment

1. Key developments The overall macroeconomic environment remains very challenging for the European insurance and pension sector. The yields have been further compressed and are substantially below the

1. Key developments The overall macroeconomic environment remains very challenging for the European insurance and pension sector. The yields have been further compressed and are substantially below the

Independent Central Banking in times of crisis

Independent Central Banking in times of crisis The Eurosystem CEMLA: XI Meeting of Central Bank Legal Advisers Santiago, Chile Content A.The Eurosystem s response to the crisis B. The Eurosystem Framework

Independent Central Banking in times of crisis The Eurosystem CEMLA: XI Meeting of Central Bank Legal Advisers Santiago, Chile Content A.The Eurosystem s response to the crisis B. The Eurosystem Framework

Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017)

") Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017) Gillian Phelan Outline Monetary policy action Interest rate policy Non-standard measures Monetary policy

Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017) Gillian Phelan Outline Monetary policy action Interest rate policy Non-standard measures Monetary policy

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform Gilles Noblet Deputy Director General DG International and European Relations European Central Bank Presentation

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform Gilles Noblet Deputy Director General DG International and European Relations European Central Bank Presentation

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi Executive Board member of the European Central Bank Conference The ECB and

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi Executive Board member of the European Central Bank Conference The ECB and

The monetary policy of the ECB

Benoît Cœuré European Central Bank The monetary policy of the ECB Mexico City, 27 October 2015 Outline Rubric 1 The monetary policy strategy: key features 2 The ECB s monetary policy in times of crisis

Benoît Cœuré European Central Bank The monetary policy of the ECB Mexico City, 27 October 2015 Outline Rubric 1 The monetary policy strategy: key features 2 The ECB s monetary policy in times of crisis

FINANCIAL MARKETS IN EARLY AUGUST 2011 AND THE ECB S MONETARY POLICY MEASURES

Chart 28 Implied forward overnight interest rates (percentages per annum; daily data) 5. 4.5 4. 3.5 3. 2.5 2. 1.5 1..5 7 September 211 31 May 211.. 211 213 215 217 219 221 Sources:, EuroMTS (underlying

Chart 28 Implied forward overnight interest rates (percentages per annum; daily data) 5. 4.5 4. 3.5 3. 2.5 2. 1.5 1..5 7 September 211 31 May 211.. 211 213 215 217 219 221 Sources:, EuroMTS (underlying

05 April Government bond yields, curve slopes and spreads Swaps and Forwards Credit & money market spreads... 4

Strategy Euro Rates Update Nordea Research, April 1 US Treasury Yields Y Y 1Y 3Y.7 1.3 1.79.3 1D -. -. -1. -1. 1W -9. -. -11. -. German Benchmark Yields Y Y 1Y 3Y -. -.3.1.77 1D...1 -.1 1W.3 -. -7.1-1.

Strategy Euro Rates Update Nordea Research, April 1 US Treasury Yields Y Y 1Y 3Y.7 1.3 1.79.3 1D -. -. -1. -1. 1W -9. -. -11. -. German Benchmark Yields Y Y 1Y 3Y -. -.3.1.77 1D...1 -.1 1W.3 -. -7.1-1.

Belgian Financial Forum

Peter Praet Member of the Executive Board of the ECB Belgian Financial Forum Colloquium on The low interest rate environment 4 May 217 Global PMI composite output (diffusion index; seasonally adjusted;

Peter Praet Member of the Executive Board of the ECB Belgian Financial Forum Colloquium on The low interest rate environment 4 May 217 Global PMI composite output (diffusion index; seasonally adjusted;

Economic developments in the euro area

Peter Praet Member of the Executive Board of the European Central Bank Economic developments in the euro area European Finance Forum Frankfurt am Main, 9 April 2018 Global PMI composite output and global

Peter Praet Member of the Executive Board of the European Central Bank Economic developments in the euro area European Finance Forum Frankfurt am Main, 9 April 2018 Global PMI composite output and global

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets Stefano Corradin (ECB) Maria Rodriguez (University of Navarra) Non-standard monetary policy measures, ECB workshop Frankfurt

Limits to Arbitrage: Empirical Evidence from Euro Area Sovereign Bond Markets Stefano Corradin (ECB) Maria Rodriguez (University of Navarra) Non-standard monetary policy measures, ECB workshop Frankfurt

Portuguese Banking System: latest developments. 2 nd quarter 2017

Portuguese Banking System: latest developments nd quarter 17 Lisbon, 17 www.bportugal.pt Prepared with data available up to th September of 17. Portuguese Banking System: latest developments Banco de Portugal

Portuguese Banking System: latest developments nd quarter 17 Lisbon, 17 www.bportugal.pt Prepared with data available up to th September of 17. Portuguese Banking System: latest developments Banco de Portugal

The new liquidity measurement model developed by the Hungarian Central Bank during the financial crisis

The new liquidity measurement model developed by the Júlia Király Deputy Governor 29 November 212 Content Liquidity and measurement prior to the crisis New measures and new data collection during the crisis

The new liquidity measurement model developed by the Júlia Király Deputy Governor 29 November 212 Content Liquidity and measurement prior to the crisis New measures and new data collection during the crisis

Portuguese Banking System: latest developments. 2 nd quarter 2018

Portuguese Banking System: latest developments 2 nd quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 26 th September of 218. Macroeconomic indicators and banking system data

Portuguese Banking System: latest developments 2 nd quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 26 th September of 218. Macroeconomic indicators and banking system data

The liquidity management of the ECB

The liquidity management of the ECB An explanatory note Anders Svendsen, Chief Analyst Alexander Wojt, Analyst March 214 Table of contents 1. Introduction ECB s monetary policy operations Liquidity supply

The liquidity management of the ECB An explanatory note Anders Svendsen, Chief Analyst Alexander Wojt, Analyst March 214 Table of contents 1. Introduction ECB s monetary policy operations Liquidity supply

30 ECB THE ECB S ADDITIONAL OPEN MARKET OPERATIONS IN THE PERIOD FROM 8 AUGUST TO 5 SEPTEMBER 2007

Box 3 THE ECB S ADDITIONAL OPEN MARKET OPERATIONS IN THE PERIOD FROM 8 AUGUST TO 5 SEPTEMBER 2007 In order to reduce the tensions observed in the money market in the period from 8 August to 5 September,

Box 3 THE ECB S ADDITIONAL OPEN MARKET OPERATIONS IN THE PERIOD FROM 8 AUGUST TO 5 SEPTEMBER 2007 In order to reduce the tensions observed in the money market in the period from 8 August to 5 September,

Recent developments and challenges for the Portuguese economy

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

The ECB s experience with unconventional measures. Vitor Constâncio. US Monetary Policy Forum, New York 25 February 2011.

The ECB s experience with unconventional measures Vitor Constâncio Vice President US Monetary Policy Forum, New York 25 February 2011 Summary 1. Nature and size of the measures taken by central banks Liquidity

The ECB s experience with unconventional measures Vitor Constâncio Vice President US Monetary Policy Forum, New York 25 February 2011 Summary 1. Nature and size of the measures taken by central banks Liquidity

The role of the ECB in the crisis

The role of the ECB in the crisis Boris K. Kisselevsky Deputy Head of Press and Information DirCom, Warsaw, 6 July 2012 Three-pronged response to the crisis: ECB response EU response National responses

The role of the ECB in the crisis Boris K. Kisselevsky Deputy Head of Press and Information DirCom, Warsaw, 6 July 2012 Three-pronged response to the crisis: ECB response EU response National responses

Benoît Cœuré Member of the Executive Board. The future of central bank money

Benoît Cœuré Member of the Executive Board The future of central bank money Geneva, 14 May 218 Card Rubric payments and cash demand have generally increased since 27 Card payments and cash demand (x-axis:

Benoît Cœuré Member of the Executive Board The future of central bank money Geneva, 14 May 218 Card Rubric payments and cash demand have generally increased since 27 Card payments and cash demand (x-axis:

Review of the latest money market developments since the last MMCG meeting

12 December 2016 Anne-Lise Nguyen Money Market and Liquidity Division Review of the latest money market developments since the last MMCG meeting ECB Money Market Contact Group meeting, Frankfurt Market

12 December 2016 Anne-Lise Nguyen Money Market and Liquidity Division Review of the latest money market developments since the last MMCG meeting ECB Money Market Contact Group meeting, Frankfurt Market

Economic situation and outlook

Peter Praet Member of the Executive Board Economic situation and outlook February 19 Rate cuts TLTROs Private asset purchases Public asset purchases Foreward guidance (FG) MRO:.15% MLF:.% DFR: -.1% MRO:.5%

Peter Praet Member of the Executive Board Economic situation and outlook February 19 Rate cuts TLTROs Private asset purchases Public asset purchases Foreward guidance (FG) MRO:.15% MLF:.% DFR: -.1% MRO:.5%

Globalisation and central bank policies

Globalisation and central bank policies Lucas Papademos European Central Bank Bridge Forum Dialogue 22 January 28, Luxembourg 1 Chart 1: Oil and other commodity prices Brent crude oil price (USD per barrel)

Globalisation and central bank policies Lucas Papademos European Central Bank Bridge Forum Dialogue 22 January 28, Luxembourg 1 Chart 1: Oil and other commodity prices Brent crude oil price (USD per barrel)

Negative interest rates: Lessons from the euro area

Jens Eisenschmidt and Frank Smets European Central Bank Negative interest rates: Lessons from the euro area The views expressed are our own and should not be attributed to those of the European Central

Jens Eisenschmidt and Frank Smets European Central Bank Negative interest rates: Lessons from the euro area The views expressed are our own and should not be attributed to those of the European Central

ECB monetary policy since June 2014

Frank Smets European Central Bank ECB monetary policy since June 2014 The views expressed are my own and not necessarily those of the ECB. Panel discussion Bank of Canada conference on Unconventional Monetary

Frank Smets European Central Bank ECB monetary policy since June 2014 The views expressed are my own and not necessarily those of the ECB. Panel discussion Bank of Canada conference on Unconventional Monetary

ARTICLES THE ECB S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS

ARTICLES THE S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS The s assessment of its monetary policy stance is essential for the preparation of its monetary policy decisions. That assessment aims

ARTICLES THE S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS The s assessment of its monetary policy stance is essential for the preparation of its monetary policy decisions. That assessment aims

Euro GC Pooling. Continues Dynamic Growth. Frankfurt, February 29, 2008

Continues Dynamic Growth Frankfurt, February 29, 2008 Agenda Introduction Eurex Repo: Latest Development Euro GC Pooling: Overview and latest Development Outlook Page 2 Eurex Repo Development of Outstanding

Continues Dynamic Growth Frankfurt, February 29, 2008 Agenda Introduction Eurex Repo: Latest Development Euro GC Pooling: Overview and latest Development Outlook Page 2 Eurex Repo Development of Outstanding

Portuguese Banking System: latest developments. 1 st quarter 2018

Portuguese Banking System: latest developments 1 st quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 27 th June of 218. Macroeconomic indicators and banking system data are quarterly

Portuguese Banking System: latest developments 1 st quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 27 th June of 218. Macroeconomic indicators and banking system data are quarterly

Portuguese Banking System

Portuguese Banking System Recent Developments Updated: 1 st quarter 215 Prepared with data available up to 24 June 215 Outline Portuguese Banking System Main Highlights Macroeconomic and Financial Indicators

Portuguese Banking System Recent Developments Updated: 1 st quarter 215 Prepared with data available up to 24 June 215 Outline Portuguese Banking System Main Highlights Macroeconomic and Financial Indicators

Portuguese Banking System: latest developments. 1 st quarter 2017

Portuguese Banking System: latest developments 1 st quarter 17 Lisbon, 17 www.bportugal.pt Prepared with data available up to 7 th June of 17. Portuguese Banking System: latest developments Banco de Portugal

Portuguese Banking System: latest developments 1 st quarter 17 Lisbon, 17 www.bportugal.pt Prepared with data available up to 7 th June of 17. Portuguese Banking System: latest developments Banco de Portugal

An introduction to Invesco s Equity Long/Short Strategies

An introduction to Invesco s Equity Long/Short Strategies This marketing document is exclusively for use by Professional Clients and Financial Advisers in Germany. This document is not for consumer use,

An introduction to Invesco s Equity Long/Short Strategies This marketing document is exclusively for use by Professional Clients and Financial Advisers in Germany. This document is not for consumer use,

Development of Economy and Financial Markets of Kazakhstan

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

Development of Economy and Financial Markets of Kazakhstan National Bank of Kazakhstan Macroeconomic development GDP, real growth, % 116 112 18 14 1 113,5 11,7 216,7223,8226,5 19,8 19,8 19,3 19,619,7 199,

Quarterly selection of articles

Quarterly selection of articles BANQUE DE FRANCE BULLETIN STATISTICAL SUPPLEMENT December 21 Statistics Contents Economic developments 1 Industrial activity indicators Monthly Business Survey France S3

Quarterly selection of articles BANQUE DE FRANCE BULLETIN STATISTICAL SUPPLEMENT December 21 Statistics Contents Economic developments 1 Industrial activity indicators Monthly Business Survey France S3

Report on financial stability

Report on financial stability Márton Nagy MNB Club 26 April 212 Key risks Deteriorating lending capacity stemming particularly from liquidity side raises the risk of a credit crunch, mainly in the corporate

Report on financial stability Márton Nagy MNB Club 26 April 212 Key risks Deteriorating lending capacity stemming particularly from liquidity side raises the risk of a credit crunch, mainly in the corporate

Macroeconomic Impact of the Subprime Crisis

Franco German Council of Economic Advisors Paris, 5 February 2008 Dr. Stefan Kooths DIW Berlin, Macro Analysis and Forecasting Approach Assuming a strictly macroeconomic point of view - Thinking in aggregates

Franco German Council of Economic Advisors Paris, 5 February 2008 Dr. Stefan Kooths DIW Berlin, Macro Analysis and Forecasting Approach Assuming a strictly macroeconomic point of view - Thinking in aggregates

European Financial Stability and Integration Report Nadia CALVIÑO Deputy Director General DG Internal Market and Services

European Financial Stability and Integration Report 2011 Nadia CALVIÑO Deputy Director General DG Internal Market and Services EFSIR 2011 2011 critical year in the financial and economic crisis complex

European Financial Stability and Integration Report 2011 Nadia CALVIÑO Deputy Director General DG Internal Market and Services EFSIR 2011 2011 critical year in the financial and economic crisis complex

General debt-related data. page 3

18 19 1 3 4 5 6 7 8 9 3 31 3 33 34 35 36 37 38 39 4 41 4 43 44 45 46 47 MonthlyBulletin n 3 3 4 M a r c h 1 8 Publication manager: Anthony Requin Editor: Agence France Trésor Available in Arabic, Chinese,

18 19 1 3 4 5 6 7 8 9 3 31 3 33 34 35 36 37 38 39 4 41 4 43 44 45 46 47 MonthlyBulletin n 3 3 4 M a r c h 1 8 Publication manager: Anthony Requin Editor: Agence France Trésor Available in Arabic, Chinese,

Executive Board meeting. 14 December 2011

Executive Board meeting December EU measures ECB Key policy rate has been reduced to. percent Measures: Liquidity operation with a maturity of months Reserve requirements reduced from to per cent Reduced

Executive Board meeting December EU measures ECB Key policy rate has been reduced to. percent Measures: Liquidity operation with a maturity of months Reserve requirements reduced from to per cent Reduced

1.1. Low yield environment

1. Key developments Overall, the macroeconomic outlook has deteriorated since June 215. Although many European countries continue to recover, economic growth still remains fragile reflecting high public

1. Key developments Overall, the macroeconomic outlook has deteriorated since June 215. Although many European countries continue to recover, economic growth still remains fragile reflecting high public

Index of the articles in the Monthly Report

Index of the articles in the Monthly Report 2 Deutsche Bundesbank Wilhelm-Epstein-Strasse 14 60431 Frankfurt am Main Postfach 10 06 02 60006 Frankfurt am Main Germany Tel +49 69 9566 0 Fax +49 69 9566

Index of the articles in the Monthly Report 2 Deutsche Bundesbank Wilhelm-Epstein-Strasse 14 60431 Frankfurt am Main Postfach 10 06 02 60006 Frankfurt am Main Germany Tel +49 69 9566 0 Fax +49 69 9566

The Greek. Hans-Werner Sinn

CESifo, a Munich-based, globe-spanning economic research and policy advice institution Forum june 215 Special Issue - Update The Greek Tragedy Hans-Werner Sinn This document contains updated graphs and

CESifo, a Munich-based, globe-spanning economic research and policy advice institution Forum june 215 Special Issue - Update The Greek Tragedy Hans-Werner Sinn This document contains updated graphs and

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN Óscar Arce Associate Director General Economics and Research 14 July 2017 XXVI International Financial Congress St. Petersburg ADG ECONOMICS AND

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN Óscar Arce Associate Director General Economics and Research 14 July 2017 XXVI International Financial Congress St. Petersburg ADG ECONOMICS AND

DECISION OF THE EUROPEAN CENTRAL BANK of 29 July 2014 on measures relating to targeted longer-term refinancing operations (ECB/2014/34) (2014/541/EU)

(2014/541/EU)") 29.8.2014 L 258/11 DECISION OF THE EUROPEAN CTRAL BANK of 29 July 2014 on measures relating to targeted longer-term refinancing operations (ECB/2014/34) (2014/541/EU) THE GOVERNING COUNCIL OF THE EUROPEAN

29.8.2014 L 258/11 DECISION OF THE EUROPEAN CTRAL BANK of 29 July 2014 on measures relating to targeted longer-term refinancing operations (ECB/2014/34) (2014/541/EU) THE GOVERNING COUNCIL OF THE EUROPEAN

CITI Bank Bangkok branch. Set B Capital Item1 Capital Structure Table 2 Capital of Foreign Banks Branchs Unit : THB. Item June 30, 2009

CITI Bank Bangkok branch Set B Capital Item1 Capital Structure Table 2 Capital of Foreign Banks Branchs Unit : THB Item June 30, 20 1 Assets required to be maintained under Section 32 17,753,449,882.45

CITI Bank Bangkok branch Set B Capital Item1 Capital Structure Table 2 Capital of Foreign Banks Branchs Unit : THB Item June 30, 20 1 Assets required to be maintained under Section 32 17,753,449,882.45

Capital Market Press Conference 2013 / Frankfurt, 5 December 2013

Capital Market Press Conference 2013 / 2014 Frankfurt, 5 December 2013 Key financial figures of KfW Group (IFRS) 2013: Solid business performance, decreasing profit, very sound capital basis 2011 2012

Capital Market Press Conference 2013 / 2014 Frankfurt, 5 December 2013 Key financial figures of KfW Group (IFRS) 2013: Solid business performance, decreasing profit, very sound capital basis 2011 2012

Impact of Reductions in Reserves in the euro area

Cornelia Holthausen European Central Bank Impact of Reductions in Reserves in the euro area Monetary Policy Implementation Workshop New York, 28 September 2018 The views expressed in this presentation

Cornelia Holthausen European Central Bank Impact of Reductions in Reserves in the euro area Monetary Policy Implementation Workshop New York, 28 September 2018 The views expressed in this presentation

PRESS RELEASE NOVEMBER 2009

PRESS RELEASE 13 January 21 EURO AREA SECURITIES ISSUES STATISTICS: NOVEMBER 29 The annual growth rate of the outstanding amount of debt securities issued by euro area residents decreased from 11.% in

PRESS RELEASE 13 January 21 EURO AREA SECURITIES ISSUES STATISTICS: NOVEMBER 29 The annual growth rate of the outstanding amount of debt securities issued by euro area residents decreased from 11.% in

Public Debt Strategy in Mexico

Public Debt Strategy in Mexico 3rd OECD-China Forum on Public Debt Management and Government Securities Markets September 2006, Beijing, China www.hacienda.gob.mx/ucp 2 Index 1. Debt Management Strategy

Public Debt Strategy in Mexico 3rd OECD-China Forum on Public Debt Management and Government Securities Markets September 2006, Beijing, China www.hacienda.gob.mx/ucp 2 Index 1. Debt Management Strategy

Portuguese Banking System: latest developments. 3 rd quarter 2017

Portuguese Banking System: latest developments 3 rd quarter 217 Lisbon, 218 www.bportugal.pt Prepared with data available up to 18 th December of 217 for macroeconomic and financial market indicators,

Portuguese Banking System: latest developments 3 rd quarter 217 Lisbon, 218 www.bportugal.pt Prepared with data available up to 18 th December of 217 for macroeconomic and financial market indicators,

Euro Rates Update. 26 January % 0.9% 0.8% 2.4% 0.7% 0.6% 2.2% 0.5% 0.4% 2.0% 0.3% 0.2% 1.8% 0.1% 0.0% 1.6% Jan-15 May-15 Aug-15 Nov-15 Feb-16

FI Strategy Nordea Research, January 1 US Treasury Yields Y Y 1Y 3Y.7 1... 1D -1.7 -. -. -. 1W.3.9 1. -1. German Benchmark Yields Y Y 1Y 3Y -. -.3. 1. 1D -. -.3-1.7-3. 1W -. -.7. -.1 German Curve Slopes

FI Strategy Nordea Research, January 1 US Treasury Yields Y Y 1Y 3Y.7 1... 1D -1.7 -. -. -. 1W.3.9 1. -1. German Benchmark Yields Y Y 1Y 3Y -. -.3. 1. 1D -. -.3-1.7-3. 1W -. -.7. -.1 German Curve Slopes

EUROZONE BANKS AND CAPITAL FLOW REVERSAL

EUROZONE BANKS AND CAPITAL FLOW REVERSAL Ashoka Mody Research Department International Monetary Fund European Crisis: Historical Parallels and Economic Lessons Julis-Rabinowitz Center for Public Policy

EUROZONE BANKS AND CAPITAL FLOW REVERSAL Ashoka Mody Research Department International Monetary Fund European Crisis: Historical Parallels and Economic Lessons Julis-Rabinowitz Center for Public Policy

Portuguese Banking System: latest developments. 4 th quarter 2017

Portuguese Banking System: latest developments 4 th quarter 217 Lisbon, 218 www.bportugal.pt Prepared with data available up to 2 th March of 218. Macroeconomic indicators and banking system data are

Portuguese Banking System: latest developments 4 th quarter 217 Lisbon, 218 www.bportugal.pt Prepared with data available up to 2 th March of 218. Macroeconomic indicators and banking system data are

REPORT MONETARY POLICY INSTRUMENTS OF THE NATIONAL BANK OF POLAND IN 2007 BANKING SECTOR LIQUIDITY

REPORT MONETARY POLICY INSTRUMENTS OF THE NATIONAL BANK OF POLAND IN 2007 BANKING SECTOR LIQUIDITY Warsaw 2008 2 Banking sector liquidity Executive summary Pursuant to Article 227 para. 1 of the Constitution

REPORT MONETARY POLICY INSTRUMENTS OF THE NATIONAL BANK OF POLAND IN 2007 BANKING SECTOR LIQUIDITY Warsaw 2008 2 Banking sector liquidity Executive summary Pursuant to Article 227 para. 1 of the Constitution

Bulletin BANQUE DE FRANCE STATISTICAL SUPPLEMENT

Bulletin BANQUE DE FRANCE STATISTICAL SUPPLEMENT March 217 Statistics Contents Economic developments 1 Industrial activity indicators Monthly Business Survey France S3 2 Industrial activity indicators

Bulletin BANQUE DE FRANCE STATISTICAL SUPPLEMENT March 217 Statistics Contents Economic developments 1 Industrial activity indicators Monthly Business Survey France S3 2 Industrial activity indicators

Euro Rates Update. 26 February % 0.9% 0.8% 2.4% 0.7% 0.6% 2.2% 0.5% 0.4% 2.0% 0.3% 0.2% 1.8% 0.1% 0.0%

FI Strategy Euro Rates Update Nordea Research, 6 February 6 US Treasury Yields Y Y Y Y.7.8.7.6 D....7 W -.6 -. -.7 -. German Benchmark Yields Y Y Y Y -. -...8 D -. -..7. W -. -.8 -.8 -. German Curve Slopes

FI Strategy Euro Rates Update Nordea Research, 6 February 6 US Treasury Yields Y Y Y Y.7.8.7.6 D....7 W -.6 -. -.7 -. German Benchmark Yields Y Y Y Y -. -...8 D -. -..7. W -. -.8 -.8 -. German Curve Slopes

2 The ECB s corporate sector purchase programme: its implementation and impact

2 The ECB s corporate sector purchase programme: its implementation and impact 8 June 217 marked the first anniversary of the start of the corporate sector purchase programme (CSPP) 9. The CSPP is part

2 The ECB s corporate sector purchase programme: its implementation and impact 8 June 217 marked the first anniversary of the start of the corporate sector purchase programme (CSPP) 9. The CSPP is part

14:45 16:00 - STREAM 1- Marly. Are Euro Debt Capital Markets a Sustainable Option to Fulfill Funding Requirements in the Current Financial Crisis?

14:45 16:00 - STREAM 1- Marly 1 Are Euro Debt Capital Markets a Sustainable Option to Fulfill Funding Requirements in the Current Financial Crisis? 2 Are Euro Debt Capital Markets a Sustainable Option

14:45 16:00 - STREAM 1- Marly 1 Are Euro Debt Capital Markets a Sustainable Option to Fulfill Funding Requirements in the Current Financial Crisis? 2 Are Euro Debt Capital Markets a Sustainable Option

Maintaining Price Stability with Unconventional Monetary Policy

Peter Praet Member of the Executive Board of the European Central Bank Maintaining Price Stability with Unconventional Monetary Policy Council of the European Union Brussels, 29 January 218 Global PMI

Peter Praet Member of the Executive Board of the European Central Bank Maintaining Price Stability with Unconventional Monetary Policy Council of the European Union Brussels, 29 January 218 Global PMI

New developments in collateral and liquidity management in Europe: Quantitative Easing and monetary policy considerations

New developments in collateral and liquidity management in Europe: Quantitative Easing and monetary policy considerations 8th Conference on Payment and Securities Settlement Systems, Ohrid, 11-13 May 2015

New developments in collateral and liquidity management in Europe: Quantitative Easing and monetary policy considerations 8th Conference on Payment and Securities Settlement Systems, Ohrid, 11-13 May 2015

Index of the articles in the Monthly Report

Index of the articles in the Monthly Report 2 Deutsche Bundesbank Wilhelm-Epstein-Strasse 14 60431 Frankfurt am Main Postfach 10 06 02 60006 Frankfurt am Main Germany In the form of catchwords, this index

Index of the articles in the Monthly Report 2 Deutsche Bundesbank Wilhelm-Epstein-Strasse 14 60431 Frankfurt am Main Postfach 10 06 02 60006 Frankfurt am Main Germany In the form of catchwords, this index

Foreign exchange intervention in Argentina: motives, techniques and implications

Foreign exchange intervention in Argentina: motives, techniques and implications Claudio Irigoyen 1. Introduction Finding the optimal degree of exchange rate flexibility is difficult. To a great extent

Foreign exchange intervention in Argentina: motives, techniques and implications Claudio Irigoyen 1. Introduction Finding the optimal degree of exchange rate flexibility is difficult. To a great extent

1Q14 Results Analyst s Appendix. Madrid, April 30 th 2014

1Q14 Results Analyst s Appendix Madrid, April 30 th 2014 Disclaimer This presentation has been prepared by Banco Popular Español solely for purposes of information. It may contain estimates and forecasts

1Q14 Results Analyst s Appendix Madrid, April 30 th 2014 Disclaimer This presentation has been prepared by Banco Popular Español solely for purposes of information. It may contain estimates and forecasts

Supplements to the Statistical Bulletin

Supplements to the Statistical Bulletin Monetary and Financial Indicators New series Volume XII Number 29-3 June 2002 CONTENTS Notice to readers General information Table Table Table Table Table Table

Supplements to the Statistical Bulletin Monetary and Financial Indicators New series Volume XII Number 29-3 June 2002 CONTENTS Notice to readers General information Table Table Table Table Table Table

The Fall of Bagehot: An Inductive Approach to Understanding Monetary Policy Implementation

The Fall of Bagehot: An Inductive Approach to Understanding Monetary Policy Implementation Adjunct professor Jesper Berg, Managing Director, Nykredit Bank Friday the 28 th of August, 2015 Please note that

The Fall of Bagehot: An Inductive Approach to Understanding Monetary Policy Implementation Adjunct professor Jesper Berg, Managing Director, Nykredit Bank Friday the 28 th of August, 2015 Please note that

Determinants of intra-euro area government bond spreads during the financial crisis

Determinants of intra-euro area government bond spreads during the financial crisis by Salvador Barrios, Per Iversen, Magdalena Lewandowska, Ralph Setzer DG ECFIN, European Commission - This paper does

Determinants of intra-euro area government bond spreads during the financial crisis by Salvador Barrios, Per Iversen, Magdalena Lewandowska, Ralph Setzer DG ECFIN, European Commission - This paper does

Euro Area Securities Issues Statistics: February 2017

PRESS RELEASE 1 April 17 Euro Area Securities Issues Statistics: February 17 The annual growth rate of the outstanding amount of debt securities issued by euro area residents increased from.7% in January

PRESS RELEASE 1 April 17 Euro Area Securities Issues Statistics: February 17 The annual growth rate of the outstanding amount of debt securities issued by euro area residents increased from.7% in January

Vítor Constâncio ECB Vice-President. Fragmentation and Rebalancing in the euro area

Vítor Constâncio ECB Vice-President Fragmentation and Rebalancing in the euro area Joint EC-ECB Conference on Financial Integration Brussels, 25 April 2013 Introduction Rubric In the first half of 2012,

Vítor Constâncio ECB Vice-President Fragmentation and Rebalancing in the euro area Joint EC-ECB Conference on Financial Integration Brussels, 25 April 2013 Introduction Rubric In the first half of 2012,

ECB Money Market Workshop Discussion Strains on money market makers and money market tensions by Fecht, Reitz and Weber

Dr. Directorate General Market Operations Money Market & Liquidity *Disclaimer: Any views expressed are only those of the author and do not necessarily represent the views of the ECB or the Eurosystem.

Dr. Directorate General Market Operations Money Market & Liquidity *Disclaimer: Any views expressed are only those of the author and do not necessarily represent the views of the ECB or the Eurosystem.

Implementing Monetary Policy: Transition Tools

Implementing Monetary Policy: Transition Tools Julie Remache Central Banking Seminar Oct 6, 2015 The views expressed in this presentation reflect the author s and do not necessarily reflect that of the

Implementing Monetary Policy: Transition Tools Julie Remache Central Banking Seminar Oct 6, 2015 The views expressed in this presentation reflect the author s and do not necessarily reflect that of the

Evolution of Unconventional Monetary Policy: Japan s Experiences

Evolution of Unconventional Monetary Policy: Japan s Experiences CIGS Conference on Macroeconomic Theory and Policy May 29, 2017 Institute for Monetary and Economic Studies Bank of Japan Shigenori SHIRATSUKA

Evolution of Unconventional Monetary Policy: Japan s Experiences CIGS Conference on Macroeconomic Theory and Policy May 29, 2017 Institute for Monetary and Economic Studies Bank of Japan Shigenori SHIRATSUKA

The ECB s Expanded Asset Purchase Programme

The ECB s Expanded Asset Purchase Programme Presentation at the ICMA CBIC Conference 7 May 2015 Ulrich Bindseil Director General Market Operations European Central Bank The views expressed do not necessarily

The ECB s Expanded Asset Purchase Programme Presentation at the ICMA CBIC Conference 7 May 2015 Ulrich Bindseil Director General Market Operations European Central Bank The views expressed do not necessarily

The repo market, the public debt management and the implementation of the ECB monetary policy

The repo market, the public debt management and the implementation of the ECB monetary policy Denis Blenck Head of Operations Analysis Division 13th OECD Global Forum 27 November 2003 0 Contents I II Eurosystem

The repo market, the public debt management and the implementation of the ECB monetary policy Denis Blenck Head of Operations Analysis Division 13th OECD Global Forum 27 November 2003 0 Contents I II Eurosystem

LOAN MARKET DATA AND ANALYTICS BY THOMSON REUTERS LPC

LOAN MARKET DATA AND ANALYTICS BY THOMSON REUTERS LPC GLOBAL LOAN MARKET DATA AND ANALYTICS BY THOMSON REUTERS LPC Secondary Market Bid Levels: Europe Slide 2 European CLO New Issue Volume Monthly Slide

LOAN MARKET DATA AND ANALYTICS BY THOMSON REUTERS LPC GLOBAL LOAN MARKET DATA AND ANALYTICS BY THOMSON REUTERS LPC Secondary Market Bid Levels: Europe Slide 2 European CLO New Issue Volume Monthly Slide

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices Francesco Paolo Mongelli (ECB & Goethe Univ.) ASSOCIATION FOR COMPARATIVE ECONOMIC STUDIES Poster Session,

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices Francesco Paolo Mongelli (ECB & Goethe Univ.) ASSOCIATION FOR COMPARATIVE ECONOMIC STUDIES Poster Session,

Recent developments in Money Markets Johan Evenepoel

Recent developments in Money Markets Johan Evenepoel November 6th, 2017 1 Main drivers of Money Markets today (1/3) Monetary policy developments (1/2) Global reflation trade making a comeback in the main

Recent developments in Money Markets Johan Evenepoel November 6th, 2017 1 Main drivers of Money Markets today (1/3) Monetary policy developments (1/2) Global reflation trade making a comeback in the main

Monetary policy operating procedures: the Peruvian case

Monetary policy operating procedures: the Peruvian case Marylin Choy Chong 1. Background (i) Reforms At the end of 1990 Peru initiated a financial reform process as part of a broad set of structural reforms

Monetary policy operating procedures: the Peruvian case Marylin Choy Chong 1. Background (i) Reforms At the end of 1990 Peru initiated a financial reform process as part of a broad set of structural reforms

Inflation projection of Narodowy Bank Polski based on the NECMOD model

Economic Institute Inflation projection of Narodowy Bank Polski based on the NECMOD model Warsaw / 9 March Inflation projection of the NBP based on the NECMOD model Outline: Introduction Changes between

Economic Institute Inflation projection of Narodowy Bank Polski based on the NECMOD model Warsaw / 9 March Inflation projection of the NBP based on the NECMOD model Outline: Introduction Changes between

Bulletin BANQUE DE FRANCE STATISTICAL SUPPLEMENT

Bulletin BANQUE DE FRANCE STATISTICAL SUPPLEMENT April 217 Statistics Contents Economic developments 1 Industrial activity indicators Monthly Business Survey France S3 2 Industrial activity indicators

Bulletin BANQUE DE FRANCE STATISTICAL SUPPLEMENT April 217 Statistics Contents Economic developments 1 Industrial activity indicators Monthly Business Survey France S3 2 Industrial activity indicators

Statistics. Pocket Book

Statistics Pocket Book January March 2010 2008 Statistics Pocket Book The Statistics Pocket Book is updated monthly. As a general rule, the cut-off date for the statistics included in the Pocket Book is

Statistics Pocket Book January March 2010 2008 Statistics Pocket Book The Statistics Pocket Book is updated monthly. As a general rule, the cut-off date for the statistics included in the Pocket Book is

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya August 6, 2015 Outline 1. The Information basis for the MPC meeting 2.

Presentation to Chief Executive Officers of Commercial and Microfinance Banks Dr. Patrick Njoroge Governor, Central Bank of Kenya August 6, 2015 Outline 1. The Information basis for the MPC meeting 2.

Investment Research General Market Conditions 3 December Dec HICP (flash est. 0.1%) LTRO1 matures

LTRO1 matures") Investment Research General Market Conditions 3 December 214 ECB preview ECB s timeline is tricky isn t it? The ECB has eased twice in 214, but liquidity conditions in the Euro system will still be balancing

Investment Research General Market Conditions 3 December 214 ECB preview ECB s timeline is tricky isn t it? The ECB has eased twice in 214, but liquidity conditions in the Euro system will still be balancing

Verso l Unione Bancaria Europea

Verso l Unione Bancaria Europea Ignazio Angeloni Conferenza in onore di Marco Onado Modena, 15 gennaio 2014 1 My idea of a bank before knowing Marco Onado 2 Twenty years later Narrow monetary union: one

Verso l Unione Bancaria Europea Ignazio Angeloni Conferenza in onore di Marco Onado Modena, 15 gennaio 2014 1 My idea of a bank before knowing Marco Onado 2 Twenty years later Narrow monetary union: one

Quarterly selection of articles

Quarterly selection of articles BANQUE DE FRANCE BULLETIN STATISTICAL SUPPLEMENT JUNE 212 Contents Economic developments 1 Industrial activity indicators Monthly Business Survey France S3 2 Industrial

Quarterly selection of articles BANQUE DE FRANCE BULLETIN STATISTICAL SUPPLEMENT JUNE 212 Contents Economic developments 1 Industrial activity indicators Monthly Business Survey France S3 2 Industrial

3rd Bi-Monthly Monetary Policy Review, Kotak Mutual Fund Update as on 9 th August

3rd Bi-Monthly Monetary Policy Review, 2016-17 Kotak Mutual Fund Update as on 9 th August 2016 1 Monetary Measures: Key Rates Measures CRR Unchanged at 4.00% Reverse Repo rate Unchanged at 6.00% (affixed

3rd Bi-Monthly Monetary Policy Review, 2016-17 Kotak Mutual Fund Update as on 9 th August 2016 1 Monetary Measures: Key Rates Measures CRR Unchanged at 4.00% Reverse Repo rate Unchanged at 6.00% (affixed

UNCTAD s Seventh Debt Management Conference. Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective

UNCTAD s Seventh Debt Management Conference 9-11 November 2009 Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective by Mr. Udaibir S. Das Monetary and Capital

UNCTAD s Seventh Debt Management Conference 9-11 November 2009 Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective by Mr. Udaibir S. Das Monetary and Capital

Zenith Monthly Economic Report December 2011

Zenith Monthly Economic Report December 211 ECONOMIC STATISTICS SUMMARY Cash Rate Inflation Rate (%) Unemployment Rate (%) GDP Annual Growth (%) Country Latest Last Change Latest Change Latest Change Past

Zenith Monthly Economic Report December 211 ECONOMIC STATISTICS SUMMARY Cash Rate Inflation Rate (%) Unemployment Rate (%) GDP Annual Growth (%) Country Latest Last Change Latest Change Latest Change Past

On some Shortcomings of the Transmission of Monetary Policy

1 On some Shortcomings of the Transmission of Monetary Policy in the euro area 1. Introduction - 2. Monetary Base and the Supply of Money 3. Transmission through the Credit Channel - 4. Transmission through

1 On some Shortcomings of the Transmission of Monetary Policy in the euro area 1. Introduction - 2. Monetary Base and the Supply of Money 3. Transmission through the Credit Channel - 4. Transmission through

EUROPEAN CENTRAL BANK ECB EZB EKT BCE EKP. MONTHLY BULLETIN November November 2001

MONTHLY BULLETIN November 2001 EUROPEAN CENTRAL BANK EN ECB EZB EKT BCE EKP M O N T H L Y B U L L E T I N November 2001 M O N T H L Y B U L L E T I N November 2001 European Central Bank, 2001 Address Kaiserstrasse

MONTHLY BULLETIN November 2001 EUROPEAN CENTRAL BANK EN ECB EZB EKT BCE EKP M O N T H L Y B U L L E T I N November 2001 M O N T H L Y B U L L E T I N November 2001 European Central Bank, 2001 Address Kaiserstrasse