New developments in collateral and liquidity management in Europe: Quantitative Easing and monetary policy considerations

|

|

|

- Alan Wright

- 5 years ago

- Views:

Transcription

1 New developments in collateral and liquidity management in Europe: Quantitative Easing and monetary policy considerations 8th Conference on Payment and Securities Settlement Systems, Ohrid, May 2015 Nynke Doornbos

2 Outline Overview of the financial crisis and unconventional measures of the Eurosystem What is Quantitative Easing (QE)? Why Quantitative Easing (->inflationary developments) Monetary transmission and effects Implementation QE Market reaction on QE

3 Why does a central bank take unconventional measures? In times of immediate crisis, a central bank can act swiftly: Can expand balance sheet Operational, ready to act But: Within the mandate of the central bank? Legal/reputational/financial risks Effect on incentives / moral hazard

4 4 phases of the crisis: 1. Summer 2007 autumn 2008: liquidity crisis Banks hoarding liquidity Other pattern of liquidity provision (in time, maturity) 2. Autumn 2008 spring 2010: solvency crisis Interbank market dysfunctional Fixed rate full allotment, extension collateral list 3. Spring : sovereign debt crisis Distortions in government bond markets: SMP /OMT Risk disorderly deleveraging: VLTROs : low growth/inflation, credit supply subdued Monetary policy at (zero) lower bound: negative rates, QE Support credit supply: TLTRO, asset purchases

5 Liquidity measures Eurosystem Tensions from US sub-prime mortgage market spilled over to money markets inducing liquidity hoarding by banks. ECB reacted quickly by: Offering temporarily extra liquidity: Fine Tuning Operations, above-benchmark allotment in MRO s Still balanced liquidity conditions over maintenance period, but other pattern of liquidity provision during maintenance period More longer term refinancing operations: maturity profile changes MRO = Main Refinancing Operation

6 4 phases of the crisis: 1. Summer 2007 autumn 2008: liquidity crisis Banks hoarding liquidity Other pattern of liquidity provision (in time, maturity) 2. Autumn 2008 spring 2010: solvency crisis Interbank market dysfunctional Fixed rate full allotment, extension collateral list 3. Spring : sovereign debt crisis Distortions in government bond markets: SMP /OMT Risk disorderly deleveraging: VLTROs 4. Currently: low growth/inflation forward, guidance, negative rates TLTRO, asset purchases, QE

the ECB")

7 More liquidity! In reaction to a freeze of interbank market (Lehman) the ECB implemented: Interest rate cuts Fixed Rate Full Allotment, both in EUR and USD Narrowing interest rate corridor Temporary expansion list of eligible collateral No active absorption of excess liquidity.

8 Excess liquidity Balanced liquidity conditions

9 4 phases of the crisis: 1. Summer 2007 autumn 2008: liquidity crisis Banks hoarding liquidity Other pattern of liquidity provision (in time, maturity) 2. Autumn 2008 spring 2010: solvency crisis Interbank market dysfunctional Fixed rate full allotment, extension collateral list 3. Spring : sovereign debt crisis Distortions in government bond markets: SMP /OMT Risk disorderly deleveraging: VLTROs 4. Currently: low growth/inflation forward, guidance, negative rates TLTRO, asset purchases, QE

10 Sovereign debt crisis End of 2009/beginning 2010: Greek deficit turns out to be 12,7% (instead of 3,7%); April 2010 Greece in EU/IMF programme. November 2010: Ireland in EU/IMF programme (after real estate crash). Contagion to Portugal: requests EU/IMF programme in April Contagion to Spain and Italy (2011) July 2012: ESM-support granted for Spanish banking system. Cyprus in EU/IMF-programme since March ESM = European Stability Mechanism

11 Sovereign debt crisis

12 Securities Markets Programme (SMP) May 2010: SMP purchases of securities in market segments which are dysfunctional in order to ensure depth and liquidity Objective: address malfunctioning of markets and restore an appropriate monetary policy transmission Purchases of government bonds of in Greece, Ireland, Portugal, and later Spain and Italy; on secondary market only No Quantitative Easing: liquidity impact of interventions sterilized through weekly liquidity absorbing operations (Fixed Term Deposits)

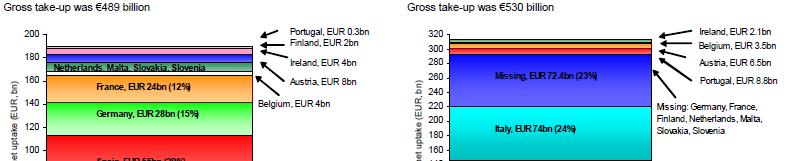

13 Further credit easing measures Ease funding conditions for banks Buy time: prevent disorderly deleveraging / credit crunch Covered Bond Purchase Programme (CBPP2) Very Long-Term Refinancing Operations (VLTROs) Two 3-year LTROs (gross 489 and 530 bln.) Temporary expansion collateral

14 The non-standard measures of the Eurosystem aim to ensure enhanced access of the banking sector to liquidity and facilitate the functioning of the euro area money market, thereby avoiding severe limitations to the real economy from a lack of financing possibilities. This also helps ensure that the official interest rates set by the ECB are transmitted in an appropriate way to the economy, and in that way help maintaining price stability in the medium term Mario Draghi, Hearing at the Committee on Economic and Monetary Affairs of the European Parliament, December 2011

15 Subscription to 3 years LTROs

16

17 Unconventional measures Can not solve the Eurosystem crisis Only buy time for structural adjustments Governments (fiscal, macro-economic, institutional) Banks (balance sheet adjustments, business models, recapitalization) Important that time is not wasted. Risks: Governments laying back when central bank steps in Postpone necessary bank restructuring. Keeping alive zombie banks Keep incentives in place!

18 2012: Draghi s whatever it takes. Speech Draghi 26/7/2012: Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough September 2012: Eurosystem may conduct Outright Monetary Transactions (OMT) to help address severe distortions in government bond markets which originate from, in particular, unfounded fears on the part of investors of the reversibility of the euro.

19 SMP (securities market programme) address malfunctioning of markets and restore an appropriate monetary policy transmission purchases of securities in market segments which are dysfunctional Not unlimited Market perception: seniority status Full sterilisation (fixed term deposits) OMT (outright monetary purchases) Provide, under appropriate conditions, fully effective backstop to avoid destructive scenarios transactions focused on shorter part of the yield curve (1-3 year) No ex ante quantitative limits Eurosystem accepts same (pari passu) treatment as other creditors Full sterilisation

20 4 phases of the crisis: 1. Summer 2007 autumn 2008: liquidity crisis Banks hoarding liquidity Other pattern of liquidity provision (in time, maturity) 2. Autumn 2008 spring 2010: solvency crisis Interbank market dysfunctional Fixed rate full allotment, extension collateral list 3. Spring : sovereign debt crisis Distortions in government bond markets: SMP /OMT Risk disorderly deleveraging: VLTROs 4. Currently: low growth/inflation forward, guidance, negative rates TLTRO, asset purchases, QE

21 Interest rate at all time low

22 Monetary policy at (zero) lower bound Forward guidance Negative rates Quantitative easing July 2013: The Governing Council has taken the unprecedented step of giving forward guidance in a rather more specific way than it ever has done in the past. The Governing Council expects the key ECB interest rates to remain at present or lower levels for an extended period of time. It is the first time that the Governing Council has said something like this.

23 Further monetary policy easing June 2014: Interest rate cut (15 bp): negative deposit rate (-10 bp) Continue FRFA, suspend SMP-related liquidity absorbing operations Targeted-LTRO (TLTRO): 4-year funding for MRO +10 bp increase credit supply to non-financial private sector Intensify preparations ABS purchases

24 Deterioration inflation outlook 22 Aug Mario Draghi: The 5 year/5 year swap rate declined by 15 basis points to just below 2% - this is the metric that we usually use for defining medium term inflation.

25 What is Quantitative Easing? = Buying bonds to stimulate the economy, primarily by boosting inflation

26 To QE or not to QE? Mario Draghi (Q&A september 2014): The aim is to increase the measures that produce credit easing for the banking industry and banking sector, which as you know represents more than 80% of total intermediation, credit intermediation, in the euro area. The second aim is to steer, significantly steer, the size of our balance sheet towards the dimensions it used to have at the beginning of QE was discussed. Some of our Governing Council members were in favour of doing more than I have just presented, and some were in favour of doing less. So our proposal strikes the middle of the road, but to answer your question, yes it was discussed. A broad asset purchase programme was discussed, and some Governors made clear that they would like to do more.

27

28 Measures taken in autumn 2014 Against background of: overall subdued outlook for inflation weakening in the euro area s growth momentum over the recent past continued subdued monetary and credit dynamics September 2014: Further rate cut: MRO rate 5 bp, deposit rate -20 bp (floor) ABS Purchase Programme and Covered Bond Purchase Programme (CBPP3)

29 ABS and covered bond purchases October 2014 Announcement operational details ABS and covered bond purchase programmes Size not published: hard to assess a figure, to give a figure on this programme as such, because there are several interactions between the ABS programme, the covered bond programme and the TLTRO programme. Less emphasis on balance sheet: I wouldn t want to emphasise the balance sheet size per se. That s very important, but it s only an instrument. The ultimate and the only mandate that we have to comply with is to bring inflation back to a level that is close to but below 2%.

30 Inflation Euro area HICP inflation and core inflation Annual percentage changes

31 Inflation expectations euro area fall in measures of inflation expectations over all horizons indicators stand at their historical lows. (Draghi, 22 Jan. 2015) our monetary policy decisions have stopped a decline in inflation expectations (Draghi, 5 March 2015)

32 Expectations Interest government bonds Exchange rate

33 Inflation projections Including effect T-LTRO s and QE Source: ECB

34 Announcement large scale purchases January 2015: Purchase programme extended with government bonds and EU institutions Intention to buy EUR 60 bln a month until at least September 2016 and in any case till inflation paths are in line with the inflation rate target (close to 2%)

35 ABSPP Asset-backed securities external managers EAPP Extended Asset Purchase Programme EUR 60 bln per month CBPP3 Covered bonds ECB + NCB's PSPP NCB's (80%) National governments and agencies (88%) ECB (8%) According to capital key European Institutions (12%) some NCB's

36 Setup PSPP Limited risk sharing PSPP: No loss sharing via central bank balance No reductions in incentives for fiscal reforms NCBs buy own domestic government bonds (pro rata according to capital key) Minimum credit quality

37 Setup PSPP Maturities: o Remaining maturities: 2-30 year o Buy bonds along the curve: preserve market functioning Bought securities available for securities lending Buy max 25% of each issue (issue limit) o Distribute purchases o No blocking minority in CACs

38 Setup PSPP Buy government bonds at secondary market o Prohibition of monetary financing: o No subscription to primary issuances o Embargo-period around auctions Outright purchases from own counterparties o Banks and brokers o Active buying: electronically and by phone

39 Risks (DNB) Limited risk sharing Interest risk: Buy bonds against low and even negative yields

40 Implementation QE-PSPP Decentralised execution: NCB s buy bonds ECB coordinates (+ own purchases) Benchmark Some flexibility (capital key, maturities) DNB buys NL government bonds

41 Implementation QE-PSPP (2) Purchases by DNB: Department Treasury and Monetary buys separated from the management of the own portfolio Experience with earlier purchase programmes (SMP, CBPP1/2/3) PSPP deviates through volume and length of earlier purchase programmes Settlement through the back office at the Payments and Securities department

42 Implementation QE-PSPP (3) When is the purchase programme successful? Purchases government bonds according to capital key Smooth implementation with limited market distortions

and already settled purchases CBPP3 runs 5 months: purchases ca.")

43 Recent purchases N.B. Market value on purchase date (liquidity effect) and already settled purchases CBPP3 runs 5 months: purchases ca. EUR 12 bln p/m ABSPP runs 4 months: purchases ca. EUR 1 bln p/m Start purchases PSPP as off 9 March 2015

44 The universe Source: research MS, numbers end of January 2015.

45 Who are selling bonds? Banks Liquidity- and capital regulation constraints Collateral need Insurers/pension funds Regulation constraints Experience UK: institutional investors switch partly to corporate bonds Asset managers Partly limited by mandates Not-Eurozone investors Least constraints

46 First experiences/reactions markets Willingness to sell Purchases so far have been done smoothly, market participants prepared a stock in advance No indications of large purchase movements Market reaction During 2014 QE was priced in stronger Strong effect on interest longer maturities at announcement And strong drop in interest longer maturities at purchase date

47 NL 30 year government bond interest rate after announcement and start QE N.B. Bond with maturity till January 2042 (longest maturity NL government bond within the programme)

48 NL interest curve

49 Effect QE on inflation expectations

50 Market reactions 1/1/ /1/ /3/2015 EURUSD yrs rentes DUI 10YR NL 10YR IT 10YR SWAP 10YR yrs rentes NL 30YR IT 30YR SWAP 30YR

51 Risks and potential costs of large scale asset purchases Medium term inflation risks Exit strategy and the possibility of losses incurred by the central bank Financial stability risks, stemming from search for yield and higher leverage Potential laxity of credit risk management by financial management institutions in a climate of low rates Wealth effects and increased inequality

52 DNB warns on risk of new asset price bubbles The present accommodative monetary policy is itself not without risks, not least because it exacerbates the risk of financial market bubbles. The ECB will constantly have to weigh this risk of new financial imbalances against the contribution made by monetary policy to economic recovery and stable prices. It is after all important that the remedy should not be worse than the disease. DNB, Overview of Financial Stability,

53 Do you have any question?

Challenges to the single monetary policy and the ECB s response. Benoît Cœuré Member of the Executive Board European Central Bank

Challenges to the single monetary policy and the ECB s response Benoît Cœuré Member of the Executive Board European Central Bank Institut d études politiques, Paris 2 September 212 1 Prime conduit of monetary

Challenges to the single monetary policy and the ECB s response Benoît Cœuré Member of the Executive Board European Central Bank Institut d études politiques, Paris 2 September 212 1 Prime conduit of monetary

LEGAL BASIS OBJECTIVES ACHIEVEMENTS

EUROPEAN MONETARY POLICY The European System of Central Banks (ESCB) comprises the ECB and the national central banks of all the EU Member States. The primary objective of the ESCB is to maintain price

EUROPEAN MONETARY POLICY The European System of Central Banks (ESCB) comprises the ECB and the national central banks of all the EU Member States. The primary objective of the ESCB is to maintain price

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform Gilles Noblet Deputy Director General DG International and European Relations European Central Bank Presentation

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform Gilles Noblet Deputy Director General DG International and European Relations European Central Bank Presentation

Monetary Policy Operations

Monetary Policy Operations Denis Blenck DG Market Operations Generation uro Students Award Teachers session 24 September 2012 Outline MONETARY POLICY IMPLEMENTATION IN NORMAL TIMES MONETARY POLICY IMPLEMENTATION

Monetary Policy Operations Denis Blenck DG Market Operations Generation uro Students Award Teachers session 24 September 2012 Outline MONETARY POLICY IMPLEMENTATION IN NORMAL TIMES MONETARY POLICY IMPLEMENTATION

Euro area economic developments from monetary policy maker s perspective

Euro area economic developments from monetary policy maker s perspective Member of Executive Board Structure of the presentation: 1. Where do we come from? ECB s monetary policy set up and main reactions

Euro area economic developments from monetary policy maker s perspective Member of Executive Board Structure of the presentation: 1. Where do we come from? ECB s monetary policy set up and main reactions

Independent Central Banking in times of crisis

Independent Central Banking in times of crisis The Eurosystem CEMLA: XI Meeting of Central Bank Legal Advisers Santiago, Chile Content A.The Eurosystem s response to the crisis B. The Eurosystem Framework

Independent Central Banking in times of crisis The Eurosystem CEMLA: XI Meeting of Central Bank Legal Advisers Santiago, Chile Content A.The Eurosystem s response to the crisis B. The Eurosystem Framework

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

European Central Bank Monetary Policy Announcement

European Central Bank Monetary Policy Announcement 5 June 2014 Summary On June 5 th, the ECB announced a number of measures to provide additional monetary policy accommodation and to support lending in

European Central Bank Monetary Policy Announcement 5 June 2014 Summary On June 5 th, the ECB announced a number of measures to provide additional monetary policy accommodation and to support lending in

The Eurosystem s asset purchase programme

Katja Hettler Lia Cruz Monika Znidar Euro Area Bond Markets Section DG-Market Operations The Eurosystem s asset purchase programme ECB Central Banking Seminar Frankfurt, 13 July 2018 Rubric The Eurosystem

Katja Hettler Lia Cruz Monika Znidar Euro Area Bond Markets Section DG-Market Operations The Eurosystem s asset purchase programme ECB Central Banking Seminar Frankfurt, 13 July 2018 Rubric The Eurosystem

Forecasting liquidity and conducting credit operations

Irene Katsalirou Money Market and Liquidity Division Directorate General Market Operations Forecasting liquidity and conducting credit operations ECB Central Banking Seminar Frankfurt am Main, 12 July

Irene Katsalirou Money Market and Liquidity Division Directorate General Market Operations Forecasting liquidity and conducting credit operations ECB Central Banking Seminar Frankfurt am Main, 12 July

The ECB and the crisis

The ECB and the crisis Stefan Gerlach Chief Economist and Senior Vice President Hong Kong Institute for Monetary Research 29 February 2016 Outline 1. Introduction and background 2. The crisis 3. ECB s

The ECB and the crisis Stefan Gerlach Chief Economist and Senior Vice President Hong Kong Institute for Monetary Research 29 February 2016 Outline 1. Introduction and background 2. The crisis 3. ECB s

Recent developments in the euro money market. Money Market Contact Group Frankfurt, 18 September 2012

Recent developments in the euro money market Money Market Contact Group Frankfurt, 18 September 2012 ECB developments and announcements I 5 July 2012 The ECB reduced by 25 basis points the interest rate

Recent developments in the euro money market Money Market Contact Group Frankfurt, 18 September 2012 ECB developments and announcements I 5 July 2012 The ECB reduced by 25 basis points the interest rate

The ECB and The Fed. How Did They React to the Crisis? Executive Director Monetary and Statistics Department. 11 July 2012, Prague

The ECB and The Fed How Did They React to the Crisis? Tomáš Holub Executive Director Monetary and Statistics Department 11 July 2012, Prague Outline Interest rate response to the crisis Unconventional

The ECB and The Fed How Did They React to the Crisis? Tomáš Holub Executive Director Monetary and Statistics Department 11 July 2012, Prague Outline Interest rate response to the crisis Unconventional

The role of the ECB in the crisis

The role of the ECB in the crisis Boris K. Kisselevsky Deputy Head of Press and Information DirCom, Warsaw, 6 July 2012 Three-pronged response to the crisis: ECB response EU response National responses

The role of the ECB in the crisis Boris K. Kisselevsky Deputy Head of Press and Information DirCom, Warsaw, 6 July 2012 Three-pronged response to the crisis: ECB response EU response National responses

Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017)

") Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017) Gillian Phelan Outline Monetary policy action Interest rate policy Non-standard measures Monetary policy

Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017) Gillian Phelan Outline Monetary policy action Interest rate policy Non-standard measures Monetary policy

ARTICLES THE ECB S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS

ARTICLES THE S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS The s assessment of its monetary policy stance is essential for the preparation of its monetary policy decisions. That assessment aims

ARTICLES THE S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS The s assessment of its monetary policy stance is essential for the preparation of its monetary policy decisions. That assessment aims

ECB MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE DEVELOPMENTS

Box 7 MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE The has responded swiftly and decisively to the crisis and the subsequent deterioration in economic, monetary and conditions with the aim

Box 7 MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE The has responded swiftly and decisively to the crisis and the subsequent deterioration in economic, monetary and conditions with the aim

Monetary policy of the Eurosystem

Seppo Honkapohja Aalto University School of Business Monetary policy of the Eurosystem AMSE Policy Lecture, University of Marseille October 16, 2018 14.9.2018 1 0. Introduction Eurosystem is to the monetary

Seppo Honkapohja Aalto University School of Business Monetary policy of the Eurosystem AMSE Policy Lecture, University of Marseille October 16, 2018 14.9.2018 1 0. Introduction Eurosystem is to the monetary

Economic and Monetary Policy Perspectives for Europe and the Euro Area

Economic and Monetary Policy Perspectives for Europe and the Euro Area Peter Mooslechner Executive Director and Member of the Governing Board Oesterreichische Nationalbank Roundtable Discussion, Austrian

Economic and Monetary Policy Perspectives for Europe and the Euro Area Peter Mooslechner Executive Director and Member of the Governing Board Oesterreichische Nationalbank Roundtable Discussion, Austrian

Economic and Financial Affairs Committee. The EMU: challenges and the way forward

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN Óscar Arce Associate Director General Economics and Research 14 July 2017 XXVI International Financial Congress St. Petersburg ADG ECONOMICS AND

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN Óscar Arce Associate Director General Economics and Research 14 July 2017 XXVI International Financial Congress St. Petersburg ADG ECONOMICS AND

ECB policies involving government bond purchases: Impacts and channels

ECB policies involving government bond purchases: Impacts and channels Arvind Krishnamurthy, Northwestern University Stefan Nagel, University of Michigan Annette Vissing- Jorgensen, University of California

ECB policies involving government bond purchases: Impacts and channels Arvind Krishnamurthy, Northwestern University Stefan Nagel, University of Michigan Annette Vissing- Jorgensen, University of California

The ECB s perspective on covered bonds

Ulrich Bindseil Director General Market Operations ECB The ECB s perspective on covered bonds AFME/VDO covered bond conference Berlin, 2 December 2016 The Eurosystem and covered bonds Asset class as collateral

Ulrich Bindseil Director General Market Operations ECB The ECB s perspective on covered bonds AFME/VDO covered bond conference Berlin, 2 December 2016 The Eurosystem and covered bonds Asset class as collateral

Navigating Uncharted Waters: Analysis of Monetary Operations & Financial Market Developments

73 Navigating Uncharted Waters: Analysis of Monetary Operations & Financial Market Developments Eimear Curtin, Brian Gallagher and Fionnuala Ryan, Financial Markets Division 1 Abstract In 2014, monetary

73 Navigating Uncharted Waters: Analysis of Monetary Operations & Financial Market Developments Eimear Curtin, Brian Gallagher and Fionnuala Ryan, Financial Markets Division 1 Abstract In 2014, monetary

Monetary policy of the ECB, its concepts and tools

Monetary policy of the ECB, its concepts and tools Frankfurt am Main, 20 September 2011 Markus A. Schmidt Directorate Monetary Policy 1 Disclaimer The views expressed are those of the presenter and should

Monetary policy of the ECB, its concepts and tools Frankfurt am Main, 20 September 2011 Markus A. Schmidt Directorate Monetary Policy 1 Disclaimer The views expressed are those of the presenter and should

The crisis response in the euro area. Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 2013

The crisis response in the euro area Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 213 Outline A. How the crisis developed B. Monetary policy response C. Structural adjustment underway

The crisis response in the euro area Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 213 Outline A. How the crisis developed B. Monetary policy response C. Structural adjustment underway

The monetary policy of the ECB

Benoît Cœuré European Central Bank The monetary policy of the ECB Mexico City, 27 October 2015 Outline Rubric 1 The monetary policy strategy: key features 2 The ECB s monetary policy in times of crisis

Benoît Cœuré European Central Bank The monetary policy of the ECB Mexico City, 27 October 2015 Outline Rubric 1 The monetary policy strategy: key features 2 The ECB s monetary policy in times of crisis

The euro area economy: an update Eurochallenge November 2013

The euro area economy: an update Eurochallenge November 2013 Delegation of the European Union to the United States www.euro-challenge.org What this presentation will cover Update on the economic situation

The euro area economy: an update Eurochallenge November 2013 Delegation of the European Union to the United States www.euro-challenge.org What this presentation will cover Update on the economic situation

Quantitative easing in the Euro area

Quantitative easing in the Euro area Rationale, impact and some considerations for Malta 11 February 2015 Rationale for quantitative easing Quantitative easing (QE) refers to the purchase of government

Quantitative easing in the Euro area Rationale, impact and some considerations for Malta 11 February 2015 Rationale for quantitative easing Quantitative easing (QE) refers to the purchase of government

The role of ECB in relation to the modified EFSF and the future ESM. Prof. Dr. iur. Dr. rer. pol. Peter Sester

The role of ECB in relation to the modified EFSF and the future ESM Prof. Dr. iur. Dr. rer. pol. Peter Sester A monetary union with a stable euro can only survive if central bank independence is fully

The role of ECB in relation to the modified EFSF and the future ESM Prof. Dr. iur. Dr. rer. pol. Peter Sester A monetary union with a stable euro can only survive if central bank independence is fully

Central Bank Lending of Last Resort. Dr Christian Hofmann National University of Singapore

Central Bank Lending of Last Resort Dr Christian Hofmann National University of Singapore Terminology: liquidity How to define Lending of Last Resort? Central bank measures that lead to increases in liquid

Central Bank Lending of Last Resort Dr Christian Hofmann National University of Singapore Terminology: liquidity How to define Lending of Last Resort? Central bank measures that lead to increases in liquid

Investment Research General Market Conditions 3 December Dec HICP (flash est. 0.1%) LTRO1 matures

LTRO1 matures") Investment Research General Market Conditions 3 December 214 ECB preview ECB s timeline is tricky isn t it? The ECB has eased twice in 214, but liquidity conditions in the Euro system will still be balancing

Investment Research General Market Conditions 3 December 214 ECB preview ECB s timeline is tricky isn t it? The ECB has eased twice in 214, but liquidity conditions in the Euro system will still be balancing

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks. Franziska Schobert

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks Franziska Schobert Agenda 1. Overview on crisis-related developments in the euro area 2. Impact of crisis-related measures on central

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks Franziska Schobert Agenda 1. Overview on crisis-related developments in the euro area 2. Impact of crisis-related measures on central

MONETARY POLICY BEFORE AND AFTER THE CRISIS. Roberto Perotti December 2013

MONETARY POLICY BEFORE AND AFTER THE CRISIS Roberto Perotti December 2013 THE ECB Monetary base - currency (banknotes and coins) in circulation - the reserves (required and excess) held by counterparties

MONETARY POLICY BEFORE AND AFTER THE CRISIS Roberto Perotti December 2013 THE ECB Monetary base - currency (banknotes and coins) in circulation - the reserves (required and excess) held by counterparties

IN-DEPTH ANALYSIS. Requested by the ECON committee. constraints. Monetary Dialogue July 2018

IN-DEPTH ANALYSIS Requested by the ECON committee ECB non-standardpolicies and collateral constraints Monetary Dialogue July 2018 Policy Department for Economic, Scientific and Quality of Life Policies

IN-DEPTH ANALYSIS Requested by the ECON committee ECB non-standardpolicies and collateral constraints Monetary Dialogue July 2018 Policy Department for Economic, Scientific and Quality of Life Policies

MONETARY POLICY INSTRUMENTS OF THE ECB

Roberto Perotti November 17, 2016 Version 1.0 MONETARY POLICY INSTRUMENTS OF THE ECB For a mostly legal description of the ECB monetary policy operations, see here, here and in particular here. Like in

Roberto Perotti November 17, 2016 Version 1.0 MONETARY POLICY INSTRUMENTS OF THE ECB For a mostly legal description of the ECB monetary policy operations, see here, here and in particular here. Like in

Europe s Response to the Sovereign Debt Crisis. Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

Europe s Response to the Sovereign Debt Crisis Klaus Regling, CEO of EFSF 40 th Economics Conference OeNB Vienna, 10 May 2012 Eight reasons for sovereign debt crisis Member States did not fully accept

ECB research Implications of the ECB easing measures

Investment Research General Market Conditions 5 June ECB research Implications of the ECB easing measures The ECB surprised the markets by boosting liquidity through a new 4Y targeted LTRO (TLTRO) while

Investment Research General Market Conditions 5 June ECB research Implications of the ECB easing measures The ECB surprised the markets by boosting liquidity through a new 4Y targeted LTRO (TLTRO) while

Effectiveness and Transmission of the ECB s Balance Sheet Policies

Effectiveness and Transmission of the ECB s Balance Sheet Policies Jef Boeckx NBB Maarten Dossche NBB Gert Peersman UGent Motivation There is a large literature that has used SVAR models to examine the

Effectiveness and Transmission of the ECB s Balance Sheet Policies Jef Boeckx NBB Maarten Dossche NBB Gert Peersman UGent Motivation There is a large literature that has used SVAR models to examine the

Strategic Stimulus: Analysis of Eurosystem Monetary Operations

52 Strategic Stimulus: Analysis of Eurosystem by John Graham, Anthony Nolan, and Paul Kane, Financial Markets Division 1 Abstract Throughout 2016 and during the first half of 2017, the Eurosystem continued

52 Strategic Stimulus: Analysis of Eurosystem by John Graham, Anthony Nolan, and Paul Kane, Financial Markets Division 1 Abstract Throughout 2016 and during the first half of 2017, the Eurosystem continued

Transcript of interview with ESM Managing Director Klaus Regling. The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016

Transcript of interview with ESM Managing Director Klaus Regling Published in Yomiuri Shimbun (Japan), 1 February 2016 The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016 Yomiuri

Transcript of interview with ESM Managing Director Klaus Regling Published in Yomiuri Shimbun (Japan), 1 February 2016 The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016 Yomiuri

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

FINANCIAL MARKETS IN EARLY AUGUST 2011 AND THE ECB S MONETARY POLICY MEASURES

Chart 28 Implied forward overnight interest rates (percentages per annum; daily data) 5. 4.5 4. 3.5 3. 2.5 2. 1.5 1..5 7 September 211 31 May 211.. 211 213 215 217 219 221 Sources:, EuroMTS (underlying

Chart 28 Implied forward overnight interest rates (percentages per annum; daily data) 5. 4.5 4. 3.5 3. 2.5 2. 1.5 1..5 7 September 211 31 May 211.. 211 213 215 217 219 221 Sources:, EuroMTS (underlying

Do Central Bank Interventions Limit the Market Discipline from Short-Term Debt?

Do Central Bank Interventions Limit the Market Discipline from Short-Term Debt? Viral Acharya NYU Stern School of Business Diane Pierret HEC Lausanne Sascha Steffen European School of Management and Technology

Do Central Bank Interventions Limit the Market Discipline from Short-Term Debt? Viral Acharya NYU Stern School of Business Diane Pierret HEC Lausanne Sascha Steffen European School of Management and Technology

How Europe is Overcoming the Euro Crisis?

How Europe is Overcoming the Euro Crisis? Klaus Regling, Managing Director, ESM University of Latvia, Riga 3 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did not fully accept

How Europe is Overcoming the Euro Crisis? Klaus Regling, Managing Director, ESM University of Latvia, Riga 3 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did not fully accept

Recent developments and challenges for the Portuguese economy

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Monetary Policy on the Way out of the Crisis

Monetary Policy on the Way out of the Crisis Professor Juergen von Hagen - Bruegel and University of Bonn 1. THE END OF THE CRISIS IS AT HANDS More than two years after the beginning, in August 2007, of

Monetary Policy on the Way out of the Crisis Professor Juergen von Hagen - Bruegel and University of Bonn 1. THE END OF THE CRISIS IS AT HANDS More than two years after the beginning, in August 2007, of

Mario Draghi: Introductory remarks at the French Assemblée Nationale

Mario Draghi: Introductory remarks at the French Assemblée Nationale Speech by Mr Mario Draghi, President of the European Central Bank, at the French Assemblée Nationale, Paris, 26 June 2013. Presidents,

Mario Draghi: Introductory remarks at the French Assemblée Nationale Speech by Mr Mario Draghi, President of the European Central Bank, at the French Assemblée Nationale, Paris, 26 June 2013. Presidents,

Market Operations in Fiscal 2016

July 2017 Market Operations in Fiscal 2016 Financial Markets Department Bank of Japan Please contact below in advance to request permission when reproducing or copying the content of this report for commercial

July 2017 Market Operations in Fiscal 2016 Financial Markets Department Bank of Japan Please contact below in advance to request permission when reproducing or copying the content of this report for commercial

Vítor Constâncio: Assessing the new phase of unconventional monetary policy at the European Central Bank

Vítor Constâncio: Assessing the new phase of unconventional monetary policy at the European Central Bank Panel remarks by Mr Vítor Constâncio, Vice-President of the European Central Bank, at the Annual

Vítor Constâncio: Assessing the new phase of unconventional monetary policy at the European Central Bank Panel remarks by Mr Vítor Constâncio, Vice-President of the European Central Bank, at the Annual

Erkki Liikanen: Reforming the structure of the EU banking sector

Erkki Liikanen: Reforming the structure of the EU banking sector Speech by Mr Erkki Liikanen, Governor of the Bank of Finland and Chairman of the Highlevel Expert Group on reforming the structure of the

Erkki Liikanen: Reforming the structure of the EU banking sector Speech by Mr Erkki Liikanen, Governor of the Bank of Finland and Chairman of the Highlevel Expert Group on reforming the structure of the

In response to the financial crisis, the Eurosystem has introduced

Understanding Central Bank Balance Sheets B Y J O A C H I M N A G E L The new monetary tool. THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY 220 I Street, N.E., Suite 200 Washington, D.C. 20002 Phone: 202-861-0791

Understanding Central Bank Balance Sheets B Y J O A C H I M N A G E L The new monetary tool. THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY 220 I Street, N.E., Suite 200 Washington, D.C. 20002 Phone: 202-861-0791

The ECB s Expanded Asset Purchase Programme

The ECB s Expanded Asset Purchase Programme Presentation at the ICMA CBIC Conference 7 May 2015 Ulrich Bindseil Director General Market Operations European Central Bank The views expressed do not necessarily

The ECB s Expanded Asset Purchase Programme Presentation at the ICMA CBIC Conference 7 May 2015 Ulrich Bindseil Director General Market Operations European Central Bank The views expressed do not necessarily

International Money and Banking: 8. How Central Banks Set Interest Rates

International Money and Banking: 8. How Central Banks Set Interest Rates Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Central Banks and Interest Rates Spring 2018 1 / 32 Monetary

International Money and Banking: 8. How Central Banks Set Interest Rates Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Central Banks and Interest Rates Spring 2018 1 / 32 Monetary

The near-term global economic outlook

Overview The near-term global economic outlook Paul van den Noord Counsellor to the Chief Economist OECD 1 Overview World growth has slowed, including in EMEs. Trade has weakened. Unemployment is high

Overview The near-term global economic outlook Paul van den Noord Counsellor to the Chief Economist OECD 1 Overview World growth has slowed, including in EMEs. Trade has weakened. Unemployment is high

EUROPEAN ECONOMY. An event-study analysis of ECB balance sheet policies since October Lucian Briciu, Giulio Lisi ECONOMIC BRIEF 001 JULY 2015

ISSN 2443-8030 (online) An event-study analysis of ECB balance sheet policies since October 2008 Lucian Briciu, Giulio Lisi ECONOMIC BRIEF 001 JULY 2015 EUROPEAN ECONOMY UROPEAN Economic and Financial

ISSN 2443-8030 (online) An event-study analysis of ECB balance sheet policies since October 2008 Lucian Briciu, Giulio Lisi ECONOMIC BRIEF 001 JULY 2015 EUROPEAN ECONOMY UROPEAN Economic and Financial

Benoît Cœuré: SME financing a euro area perspective

Benoît Cœuré: SME financing a euro area perspective Speech by Mr Benoît Cœuré, Member of the Executive Board of the European Central Bank, at the Conference on Small Business Financing, jointly organised

Benoît Cœuré: SME financing a euro area perspective Speech by Mr Benoît Cœuré, Member of the Executive Board of the European Central Bank, at the Conference on Small Business Financing, jointly organised

The Future of EMU: How Could the New Normal of Monetary Policy Look Like?

The Future of EMU: How Could the New Normal of Monetary Policy Look Like? Peter Mooslechner Executive Director and Member of the Governing Board Oesterreichische Nationalbank ELEC Monetary Commission Conference:

The Future of EMU: How Could the New Normal of Monetary Policy Look Like? Peter Mooslechner Executive Director and Member of the Governing Board Oesterreichische Nationalbank ELEC Monetary Commission Conference:

The ECB and its Watchers XIII. Klaus Regling CEO of EFSF Frankfurt, 10 June 2011

The ECB and its Watchers XIII Klaus Regling CEO of EFSF Frankfurt, 10 June 2011 Is the real economy disconnected from financial market developments? 3 Real GDP per capita growth (changes in percent) 2

The ECB and its Watchers XIII Klaus Regling CEO of EFSF Frankfurt, 10 June 2011 Is the real economy disconnected from financial market developments? 3 Real GDP per capita growth (changes in percent) 2

QE Main Channels and its Impact (incl. impact exercise for a small-open economy Slovakia) Jan Toth Deputy Governor National Bank of Slovakia

Jan Toth Deputy Governor National Bank of Slovakia") QE Main Channels and its Impact (incl. impact exercise for a small-open economy Slovakia) Jan Toth Deputy Governor National Bank of Slovakia Non-standard measures Academic consensus? Negative interest

QE Main Channels and its Impact (incl. impact exercise for a small-open economy Slovakia) Jan Toth Deputy Governor National Bank of Slovakia Non-standard measures Academic consensus? Negative interest

1 The ECB s asset purchase programme and TARGET balances: monetary policy implementation and beyond

Boxes 1 The ECB s asset purchase programme and TARGET balances: monetary policy implementation and beyond This box analyses the increase in TARGET balances since the start of the asset purchase programme

Boxes 1 The ECB s asset purchase programme and TARGET balances: monetary policy implementation and beyond This box analyses the increase in TARGET balances since the start of the asset purchase programme

ECB easing will it work? #2

Investment Research General Market Conditions 26 August 214 ECB easing will it work? #2 Liquidity and money market rates We expect the TLTROs will boost liquidity. However, the amount of borrowing limits

Investment Research General Market Conditions 26 August 214 ECB easing will it work? #2 Liquidity and money market rates We expect the TLTROs will boost liquidity. However, the amount of borrowing limits

ECB s easing package and markets zig-zag

ECB s easing package and markets zig-zag Pernille Bomholdt Henneberg Jens Peter Sørensen Christin Tuxen Senior Analyst, Euro Macro Research Chief Analyst, Fixed Income Research Senior Analyst, FX Research

ECB s easing package and markets zig-zag Pernille Bomholdt Henneberg Jens Peter Sørensen Christin Tuxen Senior Analyst, Euro Macro Research Chief Analyst, Fixed Income Research Senior Analyst, FX Research

The ECB s experience with unconventional measures. Vitor Constâncio. US Monetary Policy Forum, New York 25 February 2011.

The ECB s experience with unconventional measures Vitor Constâncio Vice President US Monetary Policy Forum, New York 25 February 2011 Summary 1. Nature and size of the measures taken by central banks Liquidity

The ECB s experience with unconventional measures Vitor Constâncio Vice President US Monetary Policy Forum, New York 25 February 2011 Summary 1. Nature and size of the measures taken by central banks Liquidity

Central banks new challenges. Intervention of José Luis Malo de Molina at the policy conference on Central Bank (R)evolutions.

evolutions.") Central banks new challenges. Intervention of José Luis Malo de Molina at the policy conference on Central Bank (R)evolutions. Madrid. Banco de España. 17 th June 2013 1 Introduction I would like to start

Central banks new challenges. Intervention of José Luis Malo de Molina at the policy conference on Central Bank (R)evolutions. Madrid. Banco de España. 17 th June 2013 1 Introduction I would like to start

30 ECB THE ECB S ADDITIONAL OPEN MARKET OPERATIONS IN THE PERIOD FROM 8 AUGUST TO 5 SEPTEMBER 2007

Box 3 THE ECB S ADDITIONAL OPEN MARKET OPERATIONS IN THE PERIOD FROM 8 AUGUST TO 5 SEPTEMBER 2007 In order to reduce the tensions observed in the money market in the period from 8 August to 5 September,

Box 3 THE ECB S ADDITIONAL OPEN MARKET OPERATIONS IN THE PERIOD FROM 8 AUGUST TO 5 SEPTEMBER 2007 In order to reduce the tensions observed in the money market in the period from 8 August to 5 September,

Jean-Claude Trichet: The monetary policy of the ECB during the financial crisis

Jean-Claude Trichet: The monetary policy of the ECB during the financial crisis Speech by Mr Jean-Claude Trichet, President of the European Central Bank, at the University of Montreal, Montreal, 6 June

Jean-Claude Trichet: The monetary policy of the ECB during the financial crisis Speech by Mr Jean-Claude Trichet, President of the European Central Bank, at the University of Montreal, Montreal, 6 June

The liquidity management of the ECB

The liquidity management of the ECB An explanatory note Anders Svendsen, Chief Analyst Alexander Wojt, Analyst March 214 Table of contents 1. Introduction ECB s monetary policy operations Liquidity supply

The liquidity management of the ECB An explanatory note Anders Svendsen, Chief Analyst Alexander Wojt, Analyst March 214 Table of contents 1. Introduction ECB s monetary policy operations Liquidity supply

Bank of Finland Annual Report 2013

Bank of Finland Annual Report 2013 Bank of Finland Annual Report 2013 Front cover Ville Tietäväinen s work Finland s building. Bank of Finland Established 1811 Street address Snellmaninaukio, Helsinki

Bank of Finland Annual Report 2013 Bank of Finland Annual Report 2013 Front cover Ville Tietäväinen s work Finland s building. Bank of Finland Established 1811 Street address Snellmaninaukio, Helsinki

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi Executive Board member of the European Central Bank Conference The ECB and

Solvency, systemic risk and moral hazard: Where does the central bank s role begin and where does it end? Lorenzo Bini Smaghi Executive Board member of the European Central Bank Conference The ECB and

Eurozone Focus The Ongoing Saga Of Sovereign Debt

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

International Money and Banking: 7. The Fed and the ECB

International Money and Banking: 7. The Fed and the ECB Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Fed and the ECB Spring 2018 1 / 17 A Closer Look at the Fed and ECB Before

International Money and Banking: 7. The Fed and the ECB Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Fed and the ECB Spring 2018 1 / 17 A Closer Look at the Fed and ECB Before

Europe s Response to the Sovereign Debt Crisis. Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

The Boundaries of Central Banks

The Boundaries of Central Banks Ignazio Angeloni (**) XX International Tor Vergata Conference on Money, Banking and Finance 7 December 2011 (**) Tentative thoughts for discussion All views are personal

The Boundaries of Central Banks Ignazio Angeloni (**) XX International Tor Vergata Conference on Money, Banking and Finance 7 December 2011 (**) Tentative thoughts for discussion All views are personal

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL ON BORROWING AND LENDING ACTIVITIES OF THE EUROPEAN UNION IN 2014

EUROPEAN COMMISSION Brussels, 10.7.2015 COM(2015) 327 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL ON BORROWING AND LENDING ACTIVITIES OF THE EUROPEAN UNION IN 2014 EN EN

EUROPEAN COMMISSION Brussels, 10.7.2015 COM(2015) 327 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL ON BORROWING AND LENDING ACTIVITIES OF THE EUROPEAN UNION IN 2014 EN EN

The switch to variable rate tenders in the main refinancing operations

The switch to variable rate tenders in the main refinancing operations At its meeting on 8 June 2 the Governing Council of the ECB decided that, starting from the operation to be settled on 28 June 2,

The switch to variable rate tenders in the main refinancing operations At its meeting on 8 June 2 the Governing Council of the ECB decided that, starting from the operation to be settled on 28 June 2,

International Money and Banking: 17. Exchange Rate Regimes and the Euro Crisis

International Money and Banking: 17. Exchange Rate Regimes and the Euro Crisis Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Exchange Rate Regimes and the Euro Spring 2018 1 / 31 Part

International Money and Banking: 17. Exchange Rate Regimes and the Euro Crisis Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Exchange Rate Regimes and the Euro Spring 2018 1 / 31 Part

MONETARY POLICY ON THE WAY OUT OF THE CRISIS

ISSUE 29/15 DECEMBER 29 MONETARY ON THE WAY OUT OF THE CRISIS JÜRGEN VON HAGEN Highlights Telephone +32 2 227 421 info@bruegel.org www.bruegel.org The European economy and the economy of the euro area

ISSUE 29/15 DECEMBER 29 MONETARY ON THE WAY OUT OF THE CRISIS JÜRGEN VON HAGEN Highlights Telephone +32 2 227 421 info@bruegel.org www.bruegel.org The European economy and the economy of the euro area

The Greek. Hans-Werner Sinn

CESifo, a Munich-based, globe-spanning economic research and policy advice institution Forum june 215 Special Issue - Update The Greek Tragedy Hans-Werner Sinn This document contains updated graphs and

CESifo, a Munich-based, globe-spanning economic research and policy advice institution Forum june 215 Special Issue - Update The Greek Tragedy Hans-Werner Sinn This document contains updated graphs and

FINANCIAL STABILITY SOVEREIGN DEBT ECONOMIC GROWTH

The European sovereign debt crisis and the future of the euro Peter Bekx European Commission i Tokyo, 30 November 2012 1 A Vicious circle FINANCIAL STABILITY SOVEREIGN DEBT ECONOMIC GROWTH 2 Breaking the

The European sovereign debt crisis and the future of the euro Peter Bekx European Commission i Tokyo, 30 November 2012 1 A Vicious circle FINANCIAL STABILITY SOVEREIGN DEBT ECONOMIC GROWTH 2 Breaking the

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks September 26, 2013 by Andrew Balls of PIMCO In the following interview, Andrew Balls, managing director and head of European portfolio

PIMCO Cyclical Outlook for Europe: Near-Term Recovery, Long-Term Risks September 26, 2013 by Andrew Balls of PIMCO In the following interview, Andrew Balls, managing director and head of European portfolio

NON-CONVENTIONAL MONETARY POLICY OF THE EUROPEAN CENTRAL BANK DURING THE FINANCIAL CRISIS

ICADE Business School NON-CONVENTIONAL MONETARY POLICY OF THE EUROPEAN CENTRAL BANK DURING THE FINANCIAL CRISIS Autor: Francisco Javier Buendia Murcia Director: Juan Rodríguez Calvo NON-CONVENTIONAL MONETARY

ICADE Business School NON-CONVENTIONAL MONETARY POLICY OF THE EUROPEAN CENTRAL BANK DURING THE FINANCIAL CRISIS Autor: Francisco Javier Buendia Murcia Director: Juan Rodríguez Calvo NON-CONVENTIONAL MONETARY

EUROZONE BANKS AND CAPITAL FLOW REVERSAL

EUROZONE BANKS AND CAPITAL FLOW REVERSAL Ashoka Mody Research Department International Monetary Fund European Crisis: Historical Parallels and Economic Lessons Julis-Rabinowitz Center for Public Policy

EUROZONE BANKS AND CAPITAL FLOW REVERSAL Ashoka Mody Research Department International Monetary Fund European Crisis: Historical Parallels and Economic Lessons Julis-Rabinowitz Center for Public Policy

Member of

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Management Report. Banco Espírito Santo do Oriente, S.A.

Management Report Banco Espírito Santo do Oriente, S.A. Summary of Management Report International Economic Framework The year under review was marked by a slowdown in global economic activity and GDP

Management Report Banco Espírito Santo do Oriente, S.A. Summary of Management Report International Economic Framework The year under review was marked by a slowdown in global economic activity and GDP

Since 2014 the macroeconomic situation in the. Rue de la Banque No. 32 October 2016

Monetary policy measures in the euro area and their effects since 21 Magali Marx Benoît Nguyen Jean-Guillaume Sahuc Monetary and Financial Analysis Directorate This letter presents the findings of research

Monetary policy measures in the euro area and their effects since 21 Magali Marx Benoît Nguyen Jean-Guillaume Sahuc Monetary and Financial Analysis Directorate This letter presents the findings of research

OPENING STATEMENT BY MARIO DRAGHI CANDIDATE FOR PRESIDENT OF THE ECB TO THE ECONOMIC AND MONETARY AFFAIRS COMMITTEE OF THE EUROPEAN PARLIAMENT

OPENING STATEMENT BY MARIO DRAGHI CANDIDATE FOR PRESIDENT OF THE ECB TO THE ECONOMIC AND MONETARY AFFAIRS COMMITTEE OF THE EUROPEAN PARLIAMENT Brussels, 14 June 2011 I am honoured to appear before your

OPENING STATEMENT BY MARIO DRAGHI CANDIDATE FOR PRESIDENT OF THE ECB TO THE ECONOMIC AND MONETARY AFFAIRS COMMITTEE OF THE EUROPEAN PARLIAMENT Brussels, 14 June 2011 I am honoured to appear before your

The ECB s sovereign quantitative easing will be supportive to the euro area economy but it is not panacea

ISSN: 79- February, 0 Vasilis Zarkos Economic Analyst vzarkos@eurobank.gr The ECB s sovereign quantitative easing will be supportive to the euro area economy but it is not panacea Quantitative easing (QE)

ISSN: 79- February, 0 Vasilis Zarkos Economic Analyst vzarkos@eurobank.gr The ECB s sovereign quantitative easing will be supportive to the euro area economy but it is not panacea Quantitative easing (QE)

Effectiveness of the ECB programme of asset purchases: Where do we stand?

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY Effectiveness of the ECB programme of asset purchases: Where do we stand? Monetary Dialogue 21 June 2016 COMPILATION

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY Effectiveness of the ECB programme of asset purchases: Where do we stand? Monetary Dialogue 21 June 2016 COMPILATION

Financial Assistance in the Euro Area: An Early Evaluation

Financial Assistance in the Euro Area: An Early Evaluation Presentation at Peterson Institute Jean Pisani-Ferry, André Sapir, Guntram B. Wolff April 2013 This study Two innovations in major financial assistance

Financial Assistance in the Euro Area: An Early Evaluation Presentation at Peterson Institute Jean Pisani-Ferry, André Sapir, Guntram B. Wolff April 2013 This study Two innovations in major financial assistance

EUROPEAN SOVEREIGN DEBT MARKETS

EUROPEAN COMMISSION DIRECTORATE GENERAL ECONOMIC AND FINANCIAL AFFAIRS Brussels, 14 January 2011 ECFIN/E/E1 EUROPEAN SOVEREIGN DEBT MARKETS - RECENT DEVELOPMENTS AND POLICY OPTIONS - Note for the attention

EUROPEAN COMMISSION DIRECTORATE GENERAL ECONOMIC AND FINANCIAL AFFAIRS Brussels, 14 January 2011 ECFIN/E/E1 EUROPEAN SOVEREIGN DEBT MARKETS - RECENT DEVELOPMENTS AND POLICY OPTIONS - Note for the attention

Banking Union in Europe Glass Half Full or Glass Half Empty. Thorsten Beck

Banking Union in Europe Glass Half Full or Glass Half Empty Thorsten Beck ` Bank resolution a critical part of the regulatory reform agenda Many regulatory reforms over past five years: Basel 3: capital

Banking Union in Europe Glass Half Full or Glass Half Empty Thorsten Beck ` Bank resolution a critical part of the regulatory reform agenda Many regulatory reforms over past five years: Basel 3: capital

12. The European Balance of Payments Crisis. Recall: Macro Background: Interest rates, ten-year government bonds. Greece.

12. The European Balance of Payments Crisis Recall: Macro Background: 35 30 % Interest rates, ten-year government bonds Irrevocably fixed conversion rates Introduction of virtual euro Greece 25 20 Introduction

12. The European Balance of Payments Crisis Recall: Macro Background: 35 30 % Interest rates, ten-year government bonds Irrevocably fixed conversion rates Introduction of virtual euro Greece 25 20 Introduction

How to monitor the exit from the Eurosystem s unconventional monetary policy: Is EONIA dead and gone?

No. 504 / March 2016 How to monitor the exit from the Eurosystem s unconventional monetary policy: Is EONIA dead and gone? Ronald Heijmans, Richard Heuver and Zion Gorgi How to monitor the exit from the

No. 504 / March 2016 How to monitor the exit from the Eurosystem s unconventional monetary policy: Is EONIA dead and gone? Ronald Heijmans, Richard Heuver and Zion Gorgi How to monitor the exit from the

What is the global economic outlook?

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

The outlook What is the global economic outlook? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent United States.... Euro area. -. -.. Japan -.... Total OECD....

Summary of the June 2010 Financial Stability RevieW

Summary of the June 21 Financial Stability RevieW The primary objective of the s Financial Stability Review (FSR) is to identify the main sources of risk to the stability of the euro area financial system

Summary of the June 21 Financial Stability RevieW The primary objective of the s Financial Stability Review (FSR) is to identify the main sources of risk to the stability of the euro area financial system

Transmission channels of unconventional monetary policy in the euro area: where do we stand?

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY Transmission channels of unconventional monetary policy in the euro area: where do we stand? Monetary Dialogue

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY Transmission channels of unconventional monetary policy in the euro area: where do we stand? Monetary Dialogue

ECB Watch: The ECB delivers a down size of the APP

ECB Watch: The ECB delivers a down size of the APP Sonsoles Castillo / María Martínez 26 October 2017 The ECB has opted for an alternative way to taper QE, downsizing monthly purchases to 30 bn euros The

ECB Watch: The ECB delivers a down size of the APP Sonsoles Castillo / María Martínez 26 October 2017 The ECB has opted for an alternative way to taper QE, downsizing monthly purchases to 30 bn euros The

FINANCIAL STATEMENTS

FINANCIAL STATEMENTS 2016 http://www.oenb.at/en/about-us/financial-statements-and-key-figures.html Stability and Security. 2016 Balance sheet as at December 31, 2016 Assets December 31, 2016 December 31,

FINANCIAL STATEMENTS 2016 http://www.oenb.at/en/about-us/financial-statements-and-key-figures.html Stability and Security. 2016 Balance sheet as at December 31, 2016 Assets December 31, 2016 December 31,

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL ON BORROWING AND LENDING ACTIVITIES OF THE EUROPEAN UNION IN 2013

EUROPEAN COMMISSION Brussels, 21.8.2014 COM(2014) 529 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL ON BORROWING AND LENDING ACTIVITIES OF THE EUROPEAN UNION IN 2013 EN EN

EUROPEAN COMMISSION Brussels, 21.8.2014 COM(2014) 529 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL ON BORROWING AND LENDING ACTIVITIES OF THE EUROPEAN UNION IN 2013 EN EN