ACCOUNTING CONCEPTS AND PROCEDURES

|

|

|

- Willa Grant

- 5 years ago

- Views:

Transcription

1 ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1

2 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue, expenses, and withdrawals expand the basic accounting equation. 4. Preparing an income statement, a statement of owner s equity, and a balance sheet. 1-2

3 Learning Objective 1 Defining and listing the functions of accounting. 1-3 Copyright Pearson Education, Inc. Publishing as Prentice Hall.

4 Accounting Language of business Provides information to: Managers Owners Investors Governmental agencies 1-4 Others inside and outside the organization

5 Accounting System The accounting process: Analyzes - Looking at what happened Records - Putting information into system Classifies - Grouping similar activities Summarizes - Totaling the results Reports - Issuing the statements Interprets - Examining the statements Communicates Provides reports 1-5

6 Accounting Provides financial information for decision makers: Individuals Small businesses Large corporations Governmental agencies In a timely fashion 1-6

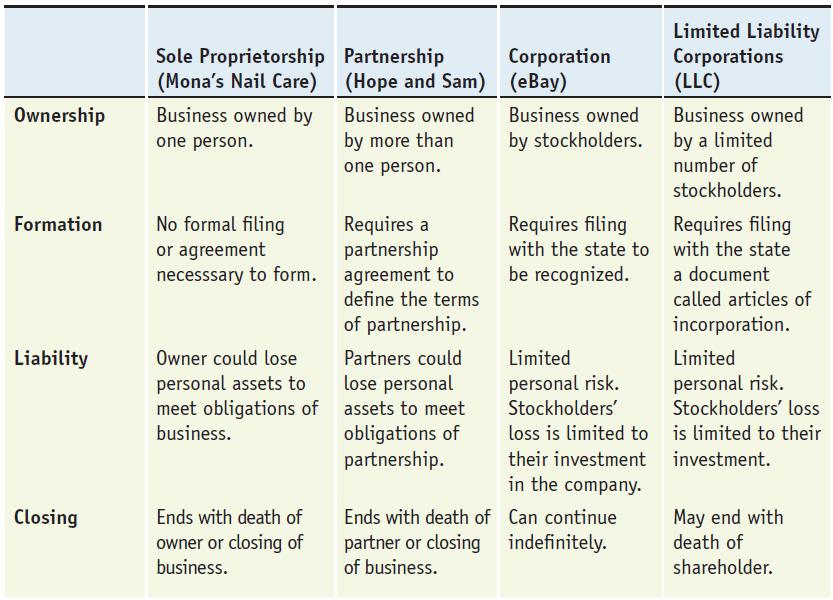

7 Business Organizations Sole proprietorship one owner The owner makes all the decisions for the business Partnership at least two owners Partners share the decision making and risks of the business Corporation owned by stockholders A business owned by stockholders 1-7

8 Business Organizations 1-8

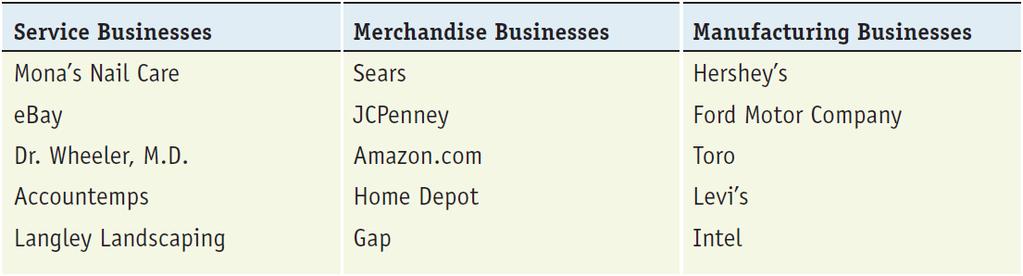

9 Business Classifications Service - actual services are provided for clients (e.g. consulting firms) Merchandising - make their own products or sell products made by another supplier (e.g. JCPenney) 1-9 Manufacturing - Companies that make their own products (e.g. Ford Motor Co.)

10 Business Classifications 1-10

11 GAAP Generally Accepted Accounting Principles Procedures and guidelines that must be followed during the accounting process Used to ensure everyone prepares and interprets financial reports the same way International Financial Reporting Standards (IFRS) Guidelines developed by the International Accounting Standards Board US is considering a change from GAAP to IFRS. 1-11

12 Difference between Bookkeeping and Accounting Bookkeeping Is the recording function of the accounting process Enters accounting information in the company s books Accounting Prepares the financial statements Involves many complex activities 1-12

13 The Accounting Equation A business is considered a separate business entity Finances are kept separate and distinct from personal finances All transactions use the accounting equation Assets = Liabilities + Owner s Equity 1-13

14 Assets = Liabilities + Owner s Equity Assets - properties of value owned by a business Cash, land, supplies, office equipment, buildings, and other properties of value Equities - rights of financial claim to the assets Assets = Equities (Total value owned by business) = (Total claims against the assets) 1-14

15 Liabilities Liabilities - Obligations that come due in the future. Result in increasing the financial rights or claims of creditors to assets. Examples include accounts payable Companies that are owed money are called creditors They have a claim to assets.

16 Assets = Liabilities + Owner s Equity Liability future obligation Total claims against the assets Equities Accountants divide equities into two parts The claims of creditors The claims of owners 1-16

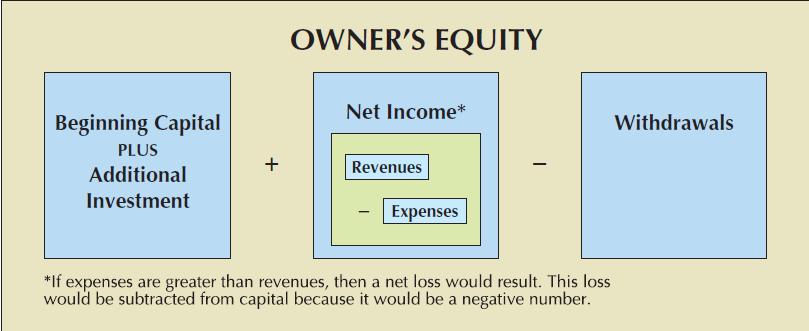

17 The Capital Account Capital - the owner s investment in a company Does not always mean cash Includes any assets the owner has put into the business 1-17

18 Learning Objective 2 Recording transactions in the basic accounting equation Copyright Pearson Education, Inc. Publishing as Prentice Hall.

19 Accounting Transactions Transaction A Aug. 28: Mia invests $6,000 in cash and $200 of office equipment into the business 1-19

20 Accounting Transactions Transaction B Aug. 29: Law practice buys office equipment for cash, $ Shift in assets - the makeup of the assets has changed, but the total remains the same

21 Accounting Transactions Transaction C Aug. 30: Buys additional office equipment on account, $300. Accounts payable - unwritten promise to pay the creditor 1-21

22 Balance Sheet Shows the history of a company Reports financial position as of a particular date Presents ending balances in assets, liabilities, and owner s equity Assets appear on the left side Liabilities and Equity appear on the right side 1-22

23 Balance Sheet 1-23

24 Preparing a Balance Sheet The heading of the balance sheet provides the following information: The company name The name of the statement The date for which the report is prepared Use of the Dollar Sign Placed to the left of each column s top figure and to the left of the column s total 1-24

25 Learning Objective 3 Seeing how revenue, expenses, and withdrawals expand the basic accounting equation Copyright Pearson Education, Inc. Publishing as Prentice Hall.

26 The Accounting Equation Expanded: Revenue, Expenses, and Withdrawals 1-26 Revenue Amount earned by performing services or selling goods to customers Increases owner s equity Recorded when earned Assets increase Cash if the client pays right away Accounts receivable - client promises to pay in the future

27 The Accounting Equation Expanded: Revenue, Expenses, and Withdrawals Expenses Cost incurred in its efforts to create revenue Decreases owner s equity Recorded when incurred Paid in cash or can be charged 1-27

28 Net Income/Net Loss Revenues Expenses = Net Income/Net Loss If revenues > expenses = net income Increases equity If expenses > revenues = net loss Decreases equity 1-28

29 Withdrawals Cash or other assets removed from the business to pay personal expenses Decreases owner s equity Not related to the business Not an expense 1-29

30 Withdrawals 1-30

31 Expanded Accounting Equation Transaction D Sept. 1 30: Provided legal services for cash, $2,

32 Expanded Accounting Equation Transaction E Sept. 1 30: Provided legal services on account, $3,

33 Expanded Accounting Equation Transaction F Sept. 1 30: Received $900 cash as partial payment from previous services performed on account. 1-33

34 Expanded Accounting Equation Transaction G Sept. 1 30: Paid salaries expense, $

35 Expanded Accounting Equation Transaction H Sept. 1 30: Paid rent expense, $

36 Expanded Accounting Equation Transaction I Sept. 1 30: Incurred advertising expenses of $200, to be paid next month. 1-36

37 Expanded Accounting Equation Transaction J Sept. 1 30: Mia withdrew $100 for personal use. 1-37

38 1-38

39 Learning Objective 4 Preparing an income statement, a statement of owner s equity, and a balance sheet Copyright Pearson Education, Inc. Publishing as Prentice Hall.

40 Income Statement Shows business results Revenues Expenses Net income/loss Covers a certain period of time A month, a quarter, a year 1-40

41 Income Statement Preparing Statements The company name The name of the statement The period of time the statement covers 1-41

42 Income Statement 1-42

43 Statement of Owner s Equity Increased by: Owner Investment Net Income (Revenue - Expenses) and Revenue Greater Than Expenses Decreased by: Owner Withdrawals Net Loss (Revenue - Expenses) and Expenses Greater Than Revenue 1-43

44 Statement of Owner s Equity 1-44

45 Balance Sheet 1-45

46 What Goes on Each Statement? 1-46

47 Main Elements of the Income Statement, the Statement of Owner s Equity, and the Balance Sheet The income statement is prepared first. Net income or loss is needed for the statement of owner s equity. The statement of owner s equity is prepared second. The net income or net loss comes from the income statement. The balance sheet is prepared last. The balance in Capital comes from the statement of owner s equity. 1-47

48 Summary of the chapter 1-48 Defining and listing the functions of accounting. The functions of accounting involve analyzing, recording, classifying, summarizing, reporting, and interpreting financial information. Forms of business organization: A sole proprietorship is a business owned by one person. A partnership is a business owned by two or more persons. A corporation is a business owned by stockholders. An LLC is owned by a limited number of stockholders. The Sarbanes-Oxley Act helps prevent fraud at trading companies. GAAP and IFRS are guidelines established by U.S. (GAAP) and international (IFRS) accounting standard boards.

49 Summary of the chapter Recording transactions in the basic accounting equation. Assets = Liabilities + Owner s Equity is the basic accounting equation. Liabilities represent amounts owed to creditors. Capital does not mean cash. In a shift of assets the composition of assets changes but the total of assets does not change. Seeing how revenue, expenses, and withdrawals expand the basic accounting equation. Revenue generates an inward flow of assets. Expenses generate an outward flow of assets or a potential outward flow. 1-49

50 Summary of the chapter When revenue totals more than expenses, net income is the result; when expenses total more than revenue, there is a net loss. Owner s equity can be subdivided into four elements: capital, withdrawals, revenue, and expenses. Withdrawals and expenses will decrease owner s equity. Preparing an income statement, a statement of owner s equity, and a balance sheet. The income statement is a statement written for a specific period of time that lists earned revenue and expenses incurred to produce the earned revenue. 1-50

51 Summary of the chapter The statement of owner s equity is a statement written for a specific period of time that reveals the causes of a change in capital. The ending figure for capital will be used on the balance sheet. The balance sheet is a statement written for a specific point of time that uses the ending balances of assets and liabilities from the accounting equation and the capital from the statement of owner s equity. The income statement should be prepared first because the information on it about net income or net loss is used to prepare the statement of owner s equity, which in turn provides information about capital for the balance sheet. 1-51

52 Questions 1-52

53 Copyright All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America. 1-53

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

Accounting Concepts and Procedures

1 Accounting Concepts and Procedures LEARNING OBJECTIVES DID YOU KNOW? By 2007 Best Buy employed 10,000 geek squad agents, 3,000 home theatre installers, and 3,000 vehicle installers. Revenues and net

1 Accounting Concepts and Procedures LEARNING OBJECTIVES DID YOU KNOW? By 2007 Best Buy employed 10,000 geek squad agents, 3,000 home theatre installers, and 3,000 vehicle installers. Revenues and net

Test Bank College Accounting A Practical Approach 13th Edition Jeffrey Slater

Test Bank College Accounting A Practical Approach 13th Edition Jeffrey Slater Instant download and all chapters TESK BANK College Accounting A Practical Approach 13th Edition Jeffrey Slater https://testbankdata.com/download/test-bank-college-accounting-practicalapproach-13th-edition-jeffrey-slater/

Test Bank College Accounting A Practical Approach 13th Edition Jeffrey Slater Instant download and all chapters TESK BANK College Accounting A Practical Approach 13th Edition Jeffrey Slater https://testbankdata.com/download/test-bank-college-accounting-practicalapproach-13th-edition-jeffrey-slater/

Accounting in Action

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Accounting Definition

Accounting Definition MINSK MINSK INNOVATION UNIVERSITY Oct, 2015 Learning Objectives After this lecture, you should be able to: 1. Define accounting. 2. Describe the primary forms of business organization.

Accounting Definition MINSK MINSK INNOVATION UNIVERSITY Oct, 2015 Learning Objectives After this lecture, you should be able to: 1. Define accounting. 2. Describe the primary forms of business organization.

Chapter 01 - Introducing Accounting in Business. Chapter Outline

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

Accounting consists of three basic activities it

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

Weygandt, Kieso, Kimmel, Trenholm, Kinnear, Barlow, Atkins: Principles of Financial Accounting, Canadian Edition CHAPTER 1. Accounting in Action

CHAPTER 1 Accounting in Action ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A 1. Identify the use and users of accounting and the objective of financial

CHAPTER 1 Accounting in Action ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A 1. Identify the use and users of accounting and the objective of financial

Accounting in Action. Chapter 1. Learning Objectives. After studying this chapter, you should be able to:

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

CHAPTER1. Accounting in Action. PreviewofCHAPTER1. What is Accounting?

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

Accounting 1A Class Notes Chapter 1 Introduction to Accounting and Business

Types of Business Service Business - Lawyer, Consultant, Doctor Merchandiser Best Buy, Wal-Mart Manufacturer - Mattel, Coca Cola Purpose of Accounting Provide Financial Information for decision making

Types of Business Service Business - Lawyer, Consultant, Doctor Merchandiser Best Buy, Wal-Mart Manufacturer - Mattel, Coca Cola Purpose of Accounting Provide Financial Information for decision making

Introduction to Governmental and Not-for-Profit Accounting, 7e

Introduction to Governmental and Not-for-Profit Accounting, 7e Chapter 2: The Use of Funds in Governmental Accounting Part 2 Copyright 2013 Pearson Education, Inc. publishing as Prentice Hall 2-* Fund

Introduction to Governmental and Not-for-Profit Accounting, 7e Chapter 2: The Use of Funds in Governmental Accounting Part 2 Copyright 2013 Pearson Education, Inc. publishing as Prentice Hall 2-* Fund

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

Topic 1! The Accounting Equation and The effect of Economic Transactions!

Topic 1 The Accounting Equation and The effect of Economic Transactions Accounting in Action : Knowing the Numbers : In business, accounting and financial statement are the means for communicating the

Topic 1 The Accounting Equation and The effect of Economic Transactions Accounting in Action : Knowing the Numbers : In business, accounting and financial statement are the means for communicating the

Learning Objectives. LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose.

Learning Objectives LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose. Lesson 1-1 The Role of Accounting LO1 Data must be recorded and

Learning Objectives LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose. Lesson 1-1 The Role of Accounting LO1 Data must be recorded and

Copyright 2009 The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12

The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12 Introduction Accounting Organizations and Basic Precepts For many students, Principles of Accounting is their first taste

The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12 Introduction Accounting Organizations and Basic Precepts For many students, Principles of Accounting is their first taste

Understanding Accounting & Financial Statements

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File 1.0-1 By taking accounting classes, the student is learning the language of business. Answer: True LO: 1-0 EOC Ref: Vocabulary

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File 1.0-1 By taking accounting classes, the student is learning the language of business. Answer: True LO: 1-0 EOC Ref: Vocabulary

The Role of Accountants and Accounting Information

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Chapter 1 Accounting and the Business Environment

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

1-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

Accounting Part 1 STUDY UNIT. Accounting Part 1 STUDY UNIT

Accounting Part 1 STUDY UNIT Accounting Part 1 STUDY UNIT 06100202 Study Unit Accounting, Part 1 By John R. Cerepak, Ph.D., C.P.A. Department Chairman and Professor of Accounting and Quantitative Analysis

Accounting Part 1 STUDY UNIT Accounting Part 1 STUDY UNIT 06100202 Study Unit Accounting, Part 1 By John R. Cerepak, Ph.D., C.P.A. Department Chairman and Professor of Accounting and Quantitative Analysis

Chapter 1: Business Decisions and Financial Accounting

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

3) Managerial accounting focuses on information for external decision makers. Answer: FALSE

Managerial accounting focuses on information for external decision makers. Answer: FALSE") Horngren's Financial & Managerial Accounting, 4e (Nobles) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Horngren's Financial & Managerial Accounting, 4e (Nobles) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Chapter Seventeen. Learning Objectives

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Department Budgets and Finance

International Security Training, LLC Module 4 Page 1 of 18 Department Budgets and Finance Financial management is a crucial aspect of any thriving business. Profit maximization, or stockholder wealth maximization,

International Security Training, LLC Module 4 Page 1 of 18 Department Budgets and Finance Financial management is a crucial aspect of any thriving business. Profit maximization, or stockholder wealth maximization,

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Accounting I. Lesson Plan. Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Cash Payments Unit: 3 Chapter 11

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Understanding Accounting and Financial Information

Chapter Seventeen Understanding Accounting and Financial Information McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. SEAN PERICH Bakery Barn A lifelong weightlifter

Chapter Seventeen Understanding Accounting and Financial Information McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. SEAN PERICH Bakery Barn A lifelong weightlifter

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Accounting for Tourism and Hospitality I

2011 Accounting for Tourism and Hospitality I For Internal Use Only Complied by Cheng Tara CONTENTS TITLE PAGE CHAPTER 1 Accounting in Business 1 CHAPTER 2 Recording Process 17 CHAPTER 3 Adjusting the

2011 Accounting for Tourism and Hospitality I For Internal Use Only Complied by Cheng Tara CONTENTS TITLE PAGE CHAPTER 1 Accounting in Business 1 CHAPTER 2 Recording Process 17 CHAPTER 3 Adjusting the

1

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

o Chapter 1: INTRODUCTION TO ACCOUNTING

ACCOUNTING 2-MANAGERIAL ACCOUNTING o Chapter 1: INTRODUCTION TO ACCOUNTING AND BUSINESS Teacher Version Learning Objectives 1. Describe the nature of a business and the role of accounting and ethics in

ACCOUNTING 2-MANAGERIAL ACCOUNTING o Chapter 1: INTRODUCTION TO ACCOUNTING AND BUSINESS Teacher Version Learning Objectives 1. Describe the nature of a business and the role of accounting and ethics in

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1 Published by ICB Direct Ltd ICB Direct Ltd 2013 All rights reserved. No part of this publication may be reproduced, sorted in a retrieval system,

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1 Published by ICB Direct Ltd ICB Direct Ltd 2013 All rights reserved. No part of this publication may be reproduced, sorted in a retrieval system,

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

Introduction to Accounting and Business

Introduction to Accounting and Business Chapter 1 Prepared by: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine University Learning Objectives 1. Describe the nature of a business, the role

Introduction to Accounting and Business Chapter 1 Prepared by: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine University Learning Objectives 1. Describe the nature of a business, the role

1 Accounting Concepts and Procedures

1 Accounting Concepts and Procedures ANSWERS TO DISCUSSION QUESTIONS AND CRITICAL THINKING/ETHICAL CASE 1. The functions of accounting are to analyze, record, classify, summarize, report, and interpret

1 Accounting Concepts and Procedures ANSWERS TO DISCUSSION QUESTIONS AND CRITICAL THINKING/ETHICAL CASE 1. The functions of accounting are to analyze, record, classify, summarize, report, and interpret

Chapter 1 MULTIPLE CHOICE

Chapter 1 Objectives: 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue, expenses, and withdrawals expand the basic

Chapter 1 Objectives: 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue, expenses, and withdrawals expand the basic

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Chapter 2 Analyzing Business Transactions

College Accounting Chapters 1 30 15th Edition Price Solutions Manual Full Download: http://testbanklive.com/download/college-accounting-chapters-1-30-15th-edition-price-solutions-manual/ Price, Haddock,

College Accounting Chapters 1 30 15th Edition Price Solutions Manual Full Download: http://testbanklive.com/download/college-accounting-chapters-1-30-15th-edition-price-solutions-manual/ Price, Haddock,

Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment. Learning Objective 1-1

Chapter 1 Accounting and the Business Environment. Learning Objective 1-1") Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting 1. Lesson Plan. Name: Terry Wilhelmi Day/Date:

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

IN ACTION. Chapter 1 CHAPTER STUDY OBJECTIVES PREVIEW OF CHAPTER 1. The Navigator ACCOUNTING IN ACTION

Chapter 1 ACCOUNTING IN ACTION CHAPTER STUDY OBJECTIVES The Navigator Scan Study Objectives Read Preview Read Chapter Review Work Demonstration Problem Answer True-False Statements Answer Multiple-Choice

Chapter 1 ACCOUNTING IN ACTION CHAPTER STUDY OBJECTIVES The Navigator Scan Study Objectives Read Preview Read Chapter Review Work Demonstration Problem Answer True-False Statements Answer Multiple-Choice

Analyzing and Recording Transactions QUESTIONS

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Module 4. Instructions:

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

> > > > > > > > Chapter 16. Understanding Accounting and Financial Statements

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

Analyzing and Recording Transactions QUESTIONS

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Chapter 2 Analyzing and Recording Transactions QUESTIONS 1. a. Common asset accounts: cash, accounts receivable, notes receivable, prepaid expenses (rent, insurance, etc.), office supplies, store supplies,

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Introduction to Governmental and Not-for-Profit Accounting, 7e

Introduction to Governmental and Not-for-Profit Accounting, 7e Chapter 10: Government-Wide Financial Statements Chapter 10 Topics Format of Government-Wide Financial Statements Preparing Government-Wide

Introduction to Governmental and Not-for-Profit Accounting, 7e Chapter 10: Government-Wide Financial Statements Chapter 10 Topics Format of Government-Wide Financial Statements Preparing Government-Wide

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank Link download full: http://testbankcollection.com/download/financial-andmanagerialaccounting-information-for-decisions-4th-edition-by-wild-test-bank/

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank Link download full: http://testbankcollection.com/download/financial-andmanagerialaccounting-information-for-decisions-4th-edition-by-wild-test-bank/

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 3 1 Analyzing Business Transactions Using T Accounts Section 1: Transactions That Affect Assets, Liabilities, and Owner s

Financial Statement Analysis-FIN621 ACCOUNTING & ACCOUNTING PRINCIPLES

ACCOUNTING & ACCOUNTING PRINCIPLES Lesson-1 Accounting Almost every organization and individual maintains accounts and deals with accounting. In simple terms, it can be described as a record of Income

ACCOUNTING & ACCOUNTING PRINCIPLES Lesson-1 Accounting Almost every organization and individual maintains accounts and deals with accounting. In simple terms, it can be described as a record of Income

Name Date Class. Concept Assessment. Business Transactions and the Accounting Equation

Concept Assessment PART A Accounting Vocabulary (15 points) Directions: Using terms from the following list, complete the sentences below. Write the letter of the term you have chosen in the space provided.

Concept Assessment PART A Accounting Vocabulary (15 points) Directions: Using terms from the following list, complete the sentences below. Write the letter of the term you have chosen in the space provided.

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

CHAPTER 1. Accounting in Action 12, 13, 14 1, 2, 3, 4, 5, 8, 9 18, 20, 21 22

CHAPTER 1 Accounting in Action ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Explain what accounting is. 2. Identify the users

CHAPTER 1 Accounting in Action ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Explain what accounting is. 2. Identify the users

Module 1 Exhibits and Key terms

Exhibit 1... 2 Exhibit 2... 3 A. Income Statement... 3 C. Balance Sheet... 3 Transactions affecting only the balance sheet... 4 1a. Owners invested cash... 4 2a. Borrowed money... 4 3a. Purchased trucks

Exhibit 1... 2 Exhibit 2... 3 A. Income Statement... 3 C. Balance Sheet... 3 Transactions affecting only the balance sheet... 4 1a. Owners invested cash... 4 2a. Borrowed money... 4 3a. Purchased trucks

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Financial Services Insurance (Topic 944)

") No. 2010-15 April 2010 Financial Services Insurance (Topic 944) How Investments Held through Separate Accounts Affect an Insurer s Consolidation Analysis of Those Investments a consensus of the FASB Emerging

No. 2010-15 April 2010 Financial Services Insurance (Topic 944) How Investments Held through Separate Accounts Affect an Insurer s Consolidation Analysis of Those Investments a consensus of the FASB Emerging

Chapter 16 Completing the Tests in the Sales and Collection Cycle:

Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Describe the methodology for designing tests of details of balances using the audit risk model. Design and perform

Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Describe the methodology for designing tests of details of balances using the audit risk model. Design and perform

QUICKBOOKS ONLINE PLUS: A COMPLETE COURSE Chapter 5: General Accounting and End-of- Period Procedures

QUICKBOOKS ONLINE PLUS: A COMPLETE COURSE 2016 Chapter 5: General Accounting and End-of- Period Procedures Lecture Focus 2 Complete end-of-period procedures Record adjusting entries Record Owner s Equity

QUICKBOOKS ONLINE PLUS: A COMPLETE COURSE 2016 Chapter 5: General Accounting and End-of- Period Procedures Lecture Focus 2 Complete end-of-period procedures Record adjusting entries Record Owner s Equity

Introduction to Governmental and Not-for-Profit Accounting, 7e

Introduction to Governmental and Not-for-Profit Accounting, 7e Chapter 12: Accounting For Not-For-Profit Organizations Chapter 12 Topics Characteristics of Not-for-Profits Financial Reporting Contributions

Introduction to Governmental and Not-for-Profit Accounting, 7e Chapter 12: Accounting For Not-For-Profit Organizations Chapter 12 Topics Characteristics of Not-for-Profits Financial Reporting Contributions

Financial Accounting Chapter 1 Review

Financial Accounting Chapter 1 Review Fall 2011 1. What are the Forms of Business Organization? Chapter 1: An Introduction to Accounting Sole Proprietorship a business owned by a individual; Advantages:

Financial Accounting Chapter 1 Review Fall 2011 1. What are the Forms of Business Organization? Chapter 1: An Introduction to Accounting Sole Proprietorship a business owned by a individual; Advantages:

Watch the Bottom Line

Thinkstock images/comstock/thinkstock Objective Watch the Bottom Line istockphoto/thinkstock Last winter, Tucker and Ian started a lawn-mowing and snow-shoveling service. Although they did well initially,

Thinkstock images/comstock/thinkstock Objective Watch the Bottom Line istockphoto/thinkstock Last winter, Tucker and Ian started a lawn-mowing and snow-shoveling service. Although they did well initially,

Chapter Outline Notes. Business Transactions and the Accounting Equation

Chapter Outline Notes Section 1: Property and Financial Claims A. Property property anything of value that a person or business owns and therefore controls When you own an item of property, you have a

Chapter Outline Notes Section 1: Property and Financial Claims A. Property property anything of value that a person or business owns and therefore controls When you own an item of property, you have a

Chapter 3: The Ledger and Double-Entry Accounting System. 3. How to record in Assets, Liabilities & Owner s Equity account:

1 Chapter 3: The Ledger and Double-Entry Accounting System Topic Outline: 1. Ledger 2. Ledger Account the T-account 3. How to record in Assets, Liabilities & Owner s Equity account: - the increases - the

1 Chapter 3: The Ledger and Double-Entry Accounting System Topic Outline: 1. Ledger 2. Ledger Account the T-account 3. How to record in Assets, Liabilities & Owner s Equity account: - the increases - the

ACCT 151A WEEK 2, CHAP 2. Instructor: Michael Booth Cabrillo College

ACCT 151A WEEK 2, CHAP 2 Instructor: Michael Booth Cabrillo College ANALYZING BUSINESS TRANSACTIONS Property and Financial Objectives Interest 1. Record in equation form the financial effects of a business

ACCT 151A WEEK 2, CHAP 2 Instructor: Michael Booth Cabrillo College ANALYZING BUSINESS TRANSACTIONS Property and Financial Objectives Interest 1. Record in equation form the financial effects of a business

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

ACCOUNTING AND THE FINANCIAL STATEMENTS

1 ACCOUNTING AND THE FINANCIAL STATEMENTS DISCUSSION QUESTIONS 1. Accounting is a system for identifying, measuring, recording, and communicating financial information about an organization s activities

1 ACCOUNTING AND THE FINANCIAL STATEMENTS DISCUSSION QUESTIONS 1. Accounting is a system for identifying, measuring, recording, and communicating financial information about an organization s activities

Price, Haddock, Farina College Accounting, 15e

Price, Haddock, Farina College Accounting, 15e College Accounting Chapters 1 30 15th Edition Price SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/college-accounting-chapters-1-30-15th-edi

Price, Haddock, Farina College Accounting, 15e College Accounting Chapters 1 30 15th Edition Price SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/college-accounting-chapters-1-30-15th-edi

Chapter 22 Audit of the Capital Acquisition and Repayment Cycle. Copyright 2014 Pearson Education

Chapter 22 Audit of the Capital Acquisition and Repayment Cycle Identify the accounts and the unique characteristics of the capital acquisition and repayment cycle. Design and perform audit tests of notes

Chapter 22 Audit of the Capital Acquisition and Repayment Cycle Identify the accounts and the unique characteristics of the capital acquisition and repayment cycle. Design and perform audit tests of notes

DSST Principles of Financial Accounting

DSST Principles of Financial Accounting Time 120 Minutes 76 Questions For each question below, choose the best answer from the choices given. 1. Which of the following are periodic reports created to convey

DSST Principles of Financial Accounting Time 120 Minutes 76 Questions For each question below, choose the best answer from the choices given. 1. Which of the following are periodic reports created to convey

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Introduction to Financial Accounting (2nd Edition) by A.J. Cataldo II, PhD CPA CMA CGMA. Order the complete book from the publisher Booklocker.

by A.J. Cataldo II, PhD CPA CMA CGMA. Order the complete book from the publisher Booklocker.") Introduction to Financial Accounting covers all material covered and tested in an undergraduate degree level course required for all business majors. This text should have a shelf-life of 20-years, if

Introduction to Financial Accounting covers all material covered and tested in an undergraduate degree level course required for all business majors. This text should have a shelf-life of 20-years, if

Statement of Cash Flows

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

Show Me the Money. Watch the Bottom Line. Objectives. Nature of Accounting. For discussion only. Fig 1. Student Guide

Student Guide Product/Service Management Financial Analysis LAP LAP 1 85 Performance Indicator: PM:013 FI:085 Nature of Accounting Last winter, Tucker and Ian started a lawnmowing and snow-shoveling service.

Student Guide Product/Service Management Financial Analysis LAP LAP 1 85 Performance Indicator: PM:013 FI:085 Nature of Accounting Last winter, Tucker and Ian started a lawnmowing and snow-shoveling service.

Not For Sale. Overview of Financial Statements FACMU14. Cengage Learning. All rights reserved. No distribution allowed without express authorization.

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

CHAPTER 1. Accounting in Action ASSIGNMENT CLASSIFICATION TABLE. Brief Exercises Do It! Exercises. A Problems. B Problems

CHAPTER 1 Accounting in Action ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Explain what accounting is. 2. Identify the users

CHAPTER 1 Accounting in Action ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Explain what accounting is. 2. Identify the users

Presented by: Meredith Mostochuk, CBA

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Chapter Outline Notes. Transactions That Affect Revenue, Expenses, and Withdrawals

Chapter Outline Notes Transactions That Affect Revenue, Expenses, and Withdrawals Section 1: Relationship of Revenue, Expenses, and Withdrawals to Owner s Equity The revenue, expense, and owner s withdrawals

Chapter Outline Notes Transactions That Affect Revenue, Expenses, and Withdrawals Section 1: Relationship of Revenue, Expenses, and Withdrawals to Owner s Equity The revenue, expense, and owner s withdrawals

Chapter 1. The Role of Managerial Finance. Copyright 2012 Pearson Prentice Hall. All rights reserved.

Chapter 1 The Role of Managerial Finance Copyright 2012 Pearson Prentice Hall. All rights reserved. COURSE DESCRIPTION Business Finance is an examination of the principles, theory and techniques of modern

Chapter 1 The Role of Managerial Finance Copyright 2012 Pearson Prentice Hall. All rights reserved. COURSE DESCRIPTION Business Finance is an examination of the principles, theory and techniques of modern

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions. Chapter Overview. Learning Objectives

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Chapter 16. Financial Statements for a Partnership. South-Western Educational Publishing

Chapter 16 Financial Statements for a Partnership Reporting Financial Information Adequate Disclosure Concept Applied when financial statements contain all information necessary to understand a business

Chapter 16 Financial Statements for a Partnership Reporting Financial Information Adequate Disclosure Concept Applied when financial statements contain all information necessary to understand a business

Debits and Credits CHAPTER

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

ADVANCED ACCOUNTING (110) Secondary

Secondary") Page 1 of 10 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2017 Multiple Choice (20 @ 2 points each) Short Answers (18 @ 3 points each) Problems: Job 1 Classifying Accounts

Page 1 of 10 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2017 Multiple Choice (20 @ 2 points each) Short Answers (18 @ 3 points each) Problems: Job 1 Classifying Accounts

Related Download: Solutions Manual Accounting 26th Edition Warren Reeve Duchac

Test Bank Accounting 26th Edition Warren Reeve Duchac. Completed download: https://testbankarea.com/download/accounting-26th-edition-warren-reeve-duchactest-bank/ Related Download: Solutions Manual Accounting

Test Bank Accounting 26th Edition Warren Reeve Duchac. Completed download: https://testbankarea.com/download/accounting-26th-edition-warren-reeve-duchactest-bank/ Related Download: Solutions Manual Accounting

Bookkeeping (Explanation)

") Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

1. A business entity's accounting system creates financial accounting reports which are provided to

Chapter 01 Financial Statements and Business Decisions True / False Questions 1. A business entity's accounting system creates financial accounting reports which are provided to external decision makers.

Chapter 01 Financial Statements and Business Decisions True / False Questions 1. A business entity's accounting system creates financial accounting reports which are provided to external decision makers.

Analyzing the Accounting Equation

Learning Objectives LO1 Show the relationship between the accounting equation and a T account. LO2 Identify the debit and credit side, the increase and decrease side, and the balance side of various accounts.

Learning Objectives LO1 Show the relationship between the accounting equation and a T account. LO2 Identify the debit and credit side, the increase and decrease side, and the balance side of various accounts.

BROOKLYN COMMUNITY PRIDE CENTER, INC. FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2017

BROOKLYN COMMUNITY PRIDE CENTER, INC. FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2017 Table of Contents Year Ended June 30, 2017 Page Independent Auditor s Report... 1 Financial Statements: Statement of

BROOKLYN COMMUNITY PRIDE CENTER, INC. FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2017 Table of Contents Year Ended June 30, 2017 Page Independent Auditor s Report... 1 Financial Statements: Statement of

Accounting for. Sole Proprietorship. 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

INTRODUCTION TO ACCOUNTING SEMINAR (1)

") INTRODUCTION TO ACCOUNTING SEMINAR (1) TRUE/FALSE (NOTE: Show any required calculations in your answers) 1. A corporation is a business that is legally separate and distinct from its owners. 2. Primary

INTRODUCTION TO ACCOUNTING SEMINAR (1) TRUE/FALSE (NOTE: Show any required calculations in your answers) 1. A corporation is a business that is legally separate and distinct from its owners. 2. Primary

Accounting - the recording, measurement, and interpretation of financial information essential in making business decisions.

Introduction to Business Administration Lesson 8 8. Accounting Accounting is the language of business. Accounting - the recording, measurement, and interpretation of financial information essential in

Introduction to Business Administration Lesson 8 8. Accounting Accounting is the language of business. Accounting - the recording, measurement, and interpretation of financial information essential in