Department Budgets and Finance

|

|

|

- Edward Melton

- 5 years ago

- Views:

Transcription

1 International Security Training, LLC Module 4 Page 1 of 18 Department Budgets and Finance Financial management is a crucial aspect of any thriving business. Profit maximization, or stockholder wealth maximization, are two real concerns for any organization and they depend on solid financial decisions. To make good decisions, management needs good information. And that information comes from the accounting system. From the accounting system come the financial statements. These statements contain important information about the organization's operating results. This information is important for effective management, and financial control. As a manager, or any other person with financial responsibility, you have to be able to interpret this information yourself. Financial statements contain important information about your company's operating results and financial position. The relationship between certain items of financial data can be used to identify areas where your firm excels and, more importantly, where there are opportunities for improvement. Using, understanding, and interpreting these statements will help you make much better business decisions. The Basic Financial Statements Businesses record their performance in standard formats called financial statements. The most common of these are: International Security Training, LLC Module 4 Page 1 of 18

2 International Security Training, LLC Module 4 Page 2 of Balance Sheet (also known as a Statement of Financial Position, or a Statement of Financial Condition) 2. Income Statement (Statement of Profit and Loss, Statement of Earnings, Statement of Operations) 3. Cash Flow Statement While these statements look at different aspects of the company, they are interrelated and dependent on each other, as information from one is needed to prepare the others. The key to understanding accounts is to have a good grasp of what the basic statements are there to do: how they are prepared, what they tell you, and what they don't. As a Director of Security, it s most probable that the Monthly Balance / Budget Sheet is the one you ll need to know inside and out. The annual budget will give a Director their max allowed spending, per line item. The monthly budget report will tell you where you re at, year to date. The Bookkeeping Process Every time your organization conducts a business transaction, the status of the accounts changes. In a retail company, for example, when a sale is made, the cash account increases, and the inventory decreases. The bookkeeping process keeps track of these changes in various ledgers and journals. The financial statements are then prepared using this information. Accounting is based on the fundamental accounting equation: Total Assets = Total Liabilities + Equity International Security Training, LLC Module 4 Page 2 of 18

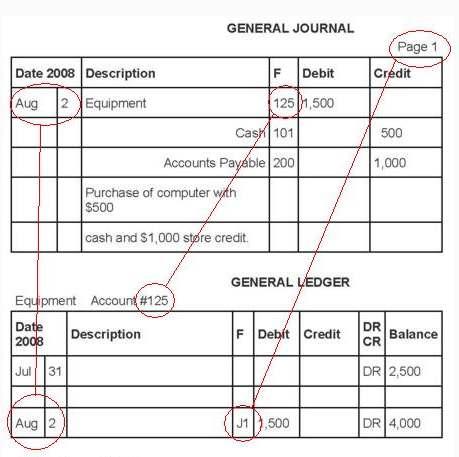

3 International Security Training, LLC Module 4 Page 3 of 18 This essentially means that the difference between what the business owns and what it owes represents the equity the company's owners have. To keep this equation in balance means that, with each transaction, at least two accounts and the balances in those accounts will change. Accounting is the process of keeping track of those changes, and recording and then reporting them. Transaction Example: On August 2, 2008, Tom's Plumbing purchased a computer for $1500 with $500 cash deposit, and the remainder on a store credit program. There are three accounts affected: The asset account 'Equipment.' The asset account 'Cash.' The liability account 'Accounts Payable.' These specific accounts can be found in what is called the Chart of Accounts. The titles Equipment, Cash, and Accounts Payable are not random; these are specific accounts that were identified as relevant to the company before it began operating as a business. The Chart of Accounts is a list of all the accounts used by a company to record financial transactions. The accounts are grouped according to type, and then numbered using the following conventions: International Security Training, LLC Module 4 Page 3 of 18

4 International Security Training, LLC Module 4 Page 4 of 18 Asset - line items Liability - line items Equity - line items Revenue - line items Expense - line items (some systems use 600s). Your monthly budget report may have different line item numbers. To keep track of transactions efficiently, a General Journal (Original Book of Entry) is used. The journal records what happened, the accounts affected, and the dollar amounts. Once you've identified the accounts that are involved, you need to apply the rules of what accountants call 'transaction analysis.' This involves the following: Asset and Expense accounts are increased by a debit, and decreased by a credit. Liabilities, Equity, and Revenue accounts are increased by a credit, and decreased by a debit. Example on next page International Security Training, LLC Module 4 Page 4 of 18

5 International Security Training, LLC Module 4 Page 5 of 18 Having a chronological record of the business' transactions is very useful, should you need to go back and review a particular transaction at a later date. The problem with keeping information in this format, though, is that there is no way to determine what the actual balance in each account is after each transaction. For example, you may need to know how much cash is actually in the cash account, and thus in the bank account, at any given time. To keep track of account balances, accountants use what is called a General Ledger. The General Ledger consists of ledger accounts, one for each account set up in the Chart of Accounts. Debits and credits to each account are posted to the ledger from the journal, and the balance is kept current. Posting is the process of transferring amounts from the general journal to specific general ledger accounts. Because entries are recorded in the ledger after the journal, the general ledger is often called the Book of Final Entry. Here's an example: International Security Training, LLC Module 4 Page 5 of 18

6 International Security Training, LLC Module 4 Page 6 of 18 International Security Training, LLC Module 4 Page 6 of 18

7 International Security Training, LLC Module 4 Page 7 of 18 Note the account balances from the previous month in the Cash and Bank Loan accounts. The 'Balance' column is used to keep a running total of the account balances. The journalizing and posting process are the first two steps of the entire accounting cycle. From there, the Financial Statements are prepared. As mentioned earlier, the financial statements are interrelated. To better understand the relationship between these statements, we'll look at Tom's Plumbing statements as they change from the start of an accounting period to the end. Balance Sheet A Balance Sheet indicates the financial position of a business at one point in time; it shows what the business owns and owes. The general journal captures day-to-day account balances. At the end of an accounting period, a Balance Sheet is prepared. The Balance Sheet has three sections: 1. Assets the things of value that the company owns. 2. Liabilities obligations to pay or provide goods or services at some later date. 3. Equity the amount of net assets (assets - liabilities) owing to the owners of the business. International Security Training, LLC Module 4 Page 7 of 18

8 International Security Training, LLC Module 4 Page 8 of 18 The Balance Sheet is named as such because the total of the assets must equal the total of the liabilities and equity. What a company owns equals what it owes to its creditors and owners. As at July 31, Tom's Plumbing has $19,500 in Assets, $6,000 in Liabilities, and $13,500 in Equity. International Security Training, LLC Module 4 Page 8 of 18

9 International Security Training, LLC Module 4 Page 9 of 18 The accounting staff at Tom's Plumbing dutifully record all the transactions that occur during the month of August, and they prepare an Income Statement to summarize the information. Income Statement At certain points during the year, each business wants to know how well it is doing. Is it earning a profit? Is it losing money? Just how well is it doing compared to other firms? Is it likely to be able to earn a profit in the future? To answer these questions, it uses an Income Statement. The Income Statement communicates the inflow of revenue, and the outflow of expenses, over a given period of time. Revenue is the inflow of assets (i.e. cash or accounts receivable) to a company in return for services performed, or goods sold. Expenses are the outflow or consumption of assets (i.e. cash, inventory, supplies), or obligations incurred (i.e. accounts payable, taxes payable) while generating revenue. The difference between these two is the Net Income. * An Income Statement therefore shows the operating profit (or loss) The Balance Sheet is named as such because the total of the assets must equal the total of the liabilities and equity. What a company owns equals what it owes to its creditors and owners. International Security Training, LLC Module 4 Page 9 of 18

10 International Security Training, LLC Module 4 Page 10 of 18 The Net Income amount is the amount by which a company's equity increases or decreases for the period. An equity account is used to record the change that results from business operations. In a proprietorship, this is International Security Training, LLC Module 4 Page 10 of 18

11 International Security Training, LLC Module 4 Page 11 of 18 typically called Retained Earnings. In corporations, it is called Owner's Equity. When Tom's Plumbing goes to prepare its Balance Sheet as at August 31, 2008, it must include the $2950 of Net Income as an increase to the Retained Earnings Account. The Balance Sheet for the end of the month is also prepared: Many people are inclined to think that, because Tom's Plumbing had a net income of $2950, the cash account increased by $2950. As you can see, this is not the case: cash increased by only $550. The reason for this is because income can be accounted for in ways other than cash; and activities other than operations, like financing and investment, can affect cash. To get an accurate picture of the actual cash generated by a business in a period you must prepare a Cash Flow Statement (Statement of Changes in Financial Position). Cash Flow Statement The Cash Flow Statement records inflows and outflows of cash during a period of time, and is divided into cash flow from operations, financing, and International Security Training, LLC Module 4 Page 11 of 18

12 International Security Training, LLC Module 4 Page 12 of 18 investing activities. To prepare a statement of cash flow you must convert net income from accrual-based accounting to cash. You therefore have to add and subtract changes in non-cash accounts that have accrued during the period. For instance, you need to add back depreciation amounts, because although depreciation expense decreases net income, it has no bearing on actual cash. Likewise, you have to deduct any decreases in accounts payable because that is a use of cash that was not accounted for on the Income Statement. The following table outlines the major sources and uses of cash: By analyzing the differences between the balance sheets for the beginning of the period and the end of the period, and accounting for the net income for the period, you can prepare a Cash Flow Statement: International Security Training, LLC Module 4 Page 12 of 18

13 International Security Training, LLC Module 4 Page 13 of 18 The $550 dollar increase in cash has been explained by converting accrued amounts into actual cash value. Understanding the interrelatedness of the financial statements is very important when reading and interpreting them. Understanding where the numbers come from, and what they actually mean, is extremely important when evaluating your own performance, or comparing your performance to others. Financial Statement Interpretation Armed with some knowledge of accounts, it's important to understand what the statements actually tell you. What an Income Statement says: The Income Statement reports the main and any secondary sources of income. For example, Fees Earned would be the primary revenue in a dental International Security Training, LLC Module 4 Page 13 of 18

14 International Security Training, LLC Module 4 Page 14 of 18 office. If they had bonds, a secondary source of revenue would be Interest Earned from Bond Investment. The terms used to describe the revenue will provide a clue about the nature of the organization. For example, Fees Earned implies a service company; Commissions Earned implies a brokerage; while Sales Revenue implies a retail or wholesale firm. The items listed as expenses are expired, meaning they have no useful value left. The result of matching the revenues and expenses yields the Net Income or Net Earnings if the statement is called the Earnings Statement. The term 'net' implies that the revenues and expenses have been matched, and therefore there is not an over or under statement of the income (loss). What an Income Statement does not say: An Income Statement does not predict the future net income for any accounting period. Since the future is full of uncertainty, a reader of a historical Income Statement can't rely on the reported results of any single period for an indication of future results. An Income Statement, no matter how well prepared, does not provide an exact measurement of net income for the accounting period. No matter how hard you try, it is impossible to get an exact match. Consider, for example, an advertising expense. If management spent $1,000 in December on advertising, and achieved $5,000 sales revenue for December, that does not mean that the advertising brought in exactly $5,000 revenue. There may also be revenue generated in January that can be attributed to the December International Security Training, LLC Module 4 Page 14 of 18

15 International Security Training, LLC Module 4 Page 15 of 18 advertising. When it is difficult to measure, the expense is accounted for in the period it was incurred. An Income Statement does not report True Profit, which is the difference between total funds invested over the life of the company and funds realized from the sale of the company. To calculate this, you would have to calculate the difference between assets invested during the lifetime of the business, and the amount finally received from remaining assets after winding up the business. You would also have to deduct any personal withdrawals because these were actually paid out of the 'profits.' Net Income does not mean cash! Always keep in mind that net income is the excess revenue over related expenses for a specific accounting period. Cash has very little to do with determining net income. True, revenue refers to an inflow of cash and expense to an outflow, but often the inflow of cash is used for further investment. Additionally, revenues and expenses are recorded at the time of occurrence, not when cash changes hands. What about the case of depreciation expense which does not represent an outflow of cash at all? What a Balance Sheet says: A Balance Sheet gives readers a detailed summary of the assets and claims against those assets, as at a particular date. A Balance Sheet provides the reader with information about the financial position of the firm with regard to its ability to pay current debts. By comparing the current assets to the current liabilities, the reader can assess International Security Training, LLC Module 4 Page 15 of 18

16 International Security Training, LLC Module 4 Page 16 of 18 whether the company is in a position to meet to meet its short-term financial obligations. A Balance Sheet gives the reader a view of the firm's financial position to carry on its business operations. The fixed-asset section indicates how many resources the company has working for it to assist in revenue generation. Finally, a Balance Sheet reveals the strength of the owner's claim against the assets. Remember, however, that this claim is residual, or the remaining claim after the creditors'. What a Balance Sheet does not say: A Balance Sheet does not report the details of how the profits were made. That information comes from the Income Statement. A Balance Sheet does not show the claims of the creditors and the owner(s) against a specific asset. The claims are against the assets in general. The word 'Capital' under owner's equity must not be interpreted as cash. The investment can come in many forms cash being just one of them. The owner's original cash investment may have gone primarily to purchase fixed assets in order to assist revenue generation. Capital means investment not cash. International Security Training, LLC Module 4 Page 16 of 18

17 International Security Training, LLC Module 4 Page 17 of 18 A Balance Sheet does not report the market value, current value, or worth of a business. Many readers believe the total assets represent a bundle of future cash reserves. This is not true because fixed assets are reported at historical cost, and their purpose is to assist revenue generation. They are not intended for sale to enhance cash flow. Key Points Accounting is a language unto itself. To become perfectly fluent takes a great deal of training and experience. Thankfully, non-financial managers, and other employees with financial responsibility, can learn to be conversant with the key terminology. The bookkeeping process is how day-to-day transactions are recorded. Balances in the various accounts are tracked and summarized in the financial statements. The financial statements bring the cycle full circle as they reflect the changes that happened during the accounting period. By understanding this cycle, you have a much better appreciation for the numbers on the financial statements, and you can use them to make sound managerial decisions. As Director of Security, you ll need to ensure that YOU, your managers, and your supervisors know how to order / buy the things you need to run the department. Your accounting department will have procedure for things like: 1. Petty Cash / Reimbursements a. $50 or less. Gas, paper, pens, etc. 2. Purchase Orders a. $51 - $999. Toner, Software, Seminars, etc. International Security Training, LLC Module 4 Page 17 of 18

18 International Security Training, LLC Module 4 Page 18 of Capital Expenditure Requests a. $1,000 up. CCTV upgrade, Fire System Panels, Jersey Barriers, Bldg Rekey, etc. Your company / agency will have their own dollar limits and procedures. Don t complain just master the system you re working in. Always plan WAY ahead. A private company may be challenging but a public agency will be worse. Most of them have the same rules as a private company PLUS a Procurement department that has to follow government finance / budget rules. Again, learn the system plan ahead and master your departments money needs! - end - International Security Training, LLC Module 4 Page 18 of 18

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

Introduction to Financial Accounting

Introduction to Financial Accounting Introduction to Accounting Accounting is a process that identifies, records and communicates information to interested users. Who Uses Accounting Data? Internal Users

Introduction to Financial Accounting Introduction to Accounting Accounting is a process that identifies, records and communicates information to interested users. Who Uses Accounting Data? Internal Users

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

ACCOUNTING CONCEPTS AND PROCEDURES

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

FAQ: Financial Statements

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

DOWNLOAD PDF JOURNAL ENTRY EXAMPLES ACCOUNTING

Chapter 1 : Ledger Accounts Posting Transactions Example Analyzing transactions and recording them as journal entries is the first step in the accounting blog.quintoapp.com begins at the start of an accounting

Chapter 1 : Ledger Accounts Posting Transactions Example Analyzing transactions and recording them as journal entries is the first step in the accounting blog.quintoapp.com begins at the start of an accounting

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

Review of a Company s Accounting System

CHAPTER 3 O BJECTIVES After reading this chapter, you will be able to: 1 Understand the components of an accounting system. 2 Know the major steps in the accounting cycle. 3 Prepare journal entries in

CHAPTER 3 O BJECTIVES After reading this chapter, you will be able to: 1 Understand the components of an accounting system. 2 Know the major steps in the accounting cycle. 3 Prepare journal entries in

Chapter III The Language of Accounting

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Finance for Non Financial Professionals

Page 1 of 6 Introduction Finance for Non Financial Professionals The success of every company depends of each employee's understanding of the key business components. Employee training and development

Page 1 of 6 Introduction Finance for Non Financial Professionals The success of every company depends of each employee's understanding of the key business components. Employee training and development

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0).

(v. 1.0).") This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

Introduction Cengage Learning. All Rights Reserved.

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Presented by: Meredith Mostochuk, CBA

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

Guide to Bookkeeping Concepts

Guide to Bookkeeping Concepts Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Guide to Bookkeeping Concepts Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Chapter 2: Overview. Analyzing and Recording Business Transactions

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Accounting Terms Chap 1-8

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

16 Statement of Cash Flows

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

Bookkeeping (Explanation)

") Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

Introduction To The Income Statement

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

Financial Accounting. Course: prof. univ. dr. Adriana TIRON-TUDOR, ( room 222) Seminar: Vasile CARDOS ( room 258)

Seminar: Vasile CARDOS ( room 258)") Financial Accounting Course: prof. univ. dr. Adriana TIRON-TUDOR, ( room 222) Seminar: Vasile CARDOS ( room 258) Recap: accounting fundamentals Why study accounting? Accounting provides information for

Financial Accounting Course: prof. univ. dr. Adriana TIRON-TUDOR, ( room 222) Seminar: Vasile CARDOS ( room 258) Recap: accounting fundamentals Why study accounting? Accounting provides information for

GOVERNMENTAL ACCOUNTING

GOVERNMENTAL ACCOUNTING All those involved in the oversight or management of government operations, and those whose livelihood and interest rely on the finances of local governments, need to have a clear

GOVERNMENTAL ACCOUNTING All those involved in the oversight or management of government operations, and those whose livelihood and interest rely on the finances of local governments, need to have a clear

Understanding Financial Data

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Understanding Presented by Brenda M. Clarke, CPA/ABV/CFF, CVA FM25 5/24/2016 2:30 PM - 3:30 PM The handouts and presentations attached

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Understanding Presented by Brenda M. Clarke, CPA/ABV/CFF, CVA FM25 5/24/2016 2:30 PM - 3:30 PM The handouts and presentations attached

DOWNLOAD PDF GENERAL JOURNAL AND LEDGER

Chapter 1 : The General Journal and Ledger The general journal is a place to first record an entry before it gets posted to the appropriate accounts. Related Questions What is the difference between entries

Chapter 1 : The General Journal and Ledger The general journal is a place to first record an entry before it gets posted to the appropriate accounts. Related Questions What is the difference between entries

Statement of Cash Flows Revisited

21 Statement of Cash Flows Revisited Overview There is not much that is new in this chapter. Rather, this chapter draws on what was learned in Chapter 5 and subsequent chapters with respect to the statement

21 Statement of Cash Flows Revisited Overview There is not much that is new in this chapter. Rather, this chapter draws on what was learned in Chapter 5 and subsequent chapters with respect to the statement

Accounting Part 1 STUDY UNIT. Accounting Part 1 STUDY UNIT

Accounting Part 1 STUDY UNIT Accounting Part 1 STUDY UNIT 06100202 Study Unit Accounting, Part 1 By John R. Cerepak, Ph.D., C.P.A. Department Chairman and Professor of Accounting and Quantitative Analysis

Accounting Part 1 STUDY UNIT Accounting Part 1 STUDY UNIT 06100202 Study Unit Accounting, Part 1 By John R. Cerepak, Ph.D., C.P.A. Department Chairman and Professor of Accounting and Quantitative Analysis

Curriculum Document for Business Education

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

DOWNLOAD PDF LIST OF DEBIT AND CREDIT ITEMS IN ACCOUNTING

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

10. Describe an account and its use in recording transactions.

1MODULE learning objective Accounting in Business, Analyzing Transactions, and Preparing Journal 10. Describe an account and its use in recording transactions. 1. THE ACCOUNT AND ITS ANALYSIS An account

1MODULE learning objective Accounting in Business, Analyzing Transactions, and Preparing Journal 10. Describe an account and its use in recording transactions. 1. THE ACCOUNT AND ITS ANALYSIS An account

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

The Expanded Ledger: Revenue, Expense, and Drawings

Revenue, Expense, and Drawings Remember the following before proceeding to the next slide!! Up until now, we have been recording transactions to the Capital account in the Owner s Equity section. Here

Revenue, Expense, and Drawings Remember the following before proceeding to the next slide!! Up until now, we have been recording transactions to the Capital account in the Owner s Equity section. Here

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts

Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts") Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

BUSINESS FINANCIAL BASICS

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

MYOB Accounting 101. For Mac Users. Written by: Todd Salkovitz Macintosh Product Manager MYOB Ltd USA Edition

MYOB Accounting 101 For Mac Users Written by: Todd Salkovitz Macintosh Product Manager MYOB Ltd. 2009 USA Edition Like all small business owners, you went into business with a dream: to sell your unique

MYOB Accounting 101 For Mac Users Written by: Todd Salkovitz Macintosh Product Manager MYOB Ltd. 2009 USA Edition Like all small business owners, you went into business with a dream: to sell your unique

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1 The accounting cycle is accounting process that extends from the very start of an accounting period to the absolute

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1 The accounting cycle is accounting process that extends from the very start of an accounting period to the absolute

AGENDA: STATEMENT OF CASH FLOWS

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Topic 1! The Accounting Equation and The effect of Economic Transactions!

Topic 1 The Accounting Equation and The effect of Economic Transactions Accounting in Action : Knowing the Numbers : In business, accounting and financial statement are the means for communicating the

Topic 1 The Accounting Equation and The effect of Economic Transactions Accounting in Action : Knowing the Numbers : In business, accounting and financial statement are the means for communicating the

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions. Chapter Overview. Learning Objectives

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Chapter 2 Debits and Credits: Analyzing and Recording Business Transactions Chapter Overview This chapter transitions from analyzing transactions and listing each account in a potentially long accounting

Examination Booklet Version 1. Bookkeeping

Examination Booklet Version 1 Bookkeeping The Accounting Equation When you feel confident that you have mastered the material in The Accounting Equation, go to and submit your answers online EXAMINATION

Examination Booklet Version 1 Bookkeeping The Accounting Equation When you feel confident that you have mastered the material in The Accounting Equation, go to and submit your answers online EXAMINATION

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Scenic Video Transcript Dividends, Closing Entries, and Record-Keeping and Reporting Map Topics. Entries: o Dividends entries- Declaring and paying

Income Statements» What s Behind?» Statements of Changes in Owners Equity» Scenic Video www.navigatingaccounting.com/video/scenic-dividends-closing-entries-and-record-keeping-and-reporting-map Scenic Video

Income Statements» What s Behind?» Statements of Changes in Owners Equity» Scenic Video www.navigatingaccounting.com/video/scenic-dividends-closing-entries-and-record-keeping-and-reporting-map Scenic Video

BASIC FINANCIAL ACCOUNTING REVIEW

C H A P T E R 1 BASIC FINANCIAL ACCOUNTING REVIEW I N T R O D U C T I O N Every profit or nonprofit business entity requires a reliable internal system of accountability. A business accounting system provides

C H A P T E R 1 BASIC FINANCIAL ACCOUNTING REVIEW I N T R O D U C T I O N Every profit or nonprofit business entity requires a reliable internal system of accountability. A business accounting system provides

FBLA Accounting I Practice Test 2004

FBLA Accounting I Practice Test 2004 True/False Indicate whether the sentence or statement is true or false. 1. When a business uses a petty cash fund, the fund is debited each time it is replaced. 2.

FBLA Accounting I Practice Test 2004 True/False Indicate whether the sentence or statement is true or false. 1. When a business uses a petty cash fund, the fund is debited each time it is replaced. 2.

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

1

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

Working with Your Lender Thomas R. Stocksdale PNC Agricultural Banking

Working with Your Lender Thomas R. Stocksdale PNC Agricultural Banking Futuring the Dairy Farm Business: In, Out, Moving Ahead November 4, 2010 Dairy Practices Council Agenda Are you: IN, OUT, MOVING AHEAD?

Working with Your Lender Thomas R. Stocksdale PNC Agricultural Banking Futuring the Dairy Farm Business: In, Out, Moving Ahead November 4, 2010 Dairy Practices Council Agenda Are you: IN, OUT, MOVING AHEAD?

LESSON Journalizing Purchases Using a Purchases Journal

LESSON 9-1 - Journalizing Purchases Using a Purchases Journal Service business vs. merchandising business Service business sells services for a fee nail salon, attorney Merchandising business purchases

LESSON 9-1 - Journalizing Purchases Using a Purchases Journal Service business vs. merchandising business Service business sells services for a fee nail salon, attorney Merchandising business purchases

Bookkeepers are the accountant s eyes and ears. Few accountants actually take the time

Chapter 1 Deciphering the Basics In This Chapter Cash vs. accrual Understanding assets, liabilities, and equity Putting it all on paper Managing transactions daily Introducing the financial statements

Chapter 1 Deciphering the Basics In This Chapter Cash vs. accrual Understanding assets, liabilities, and equity Putting it all on paper Managing transactions daily Introducing the financial statements

Chapter 1: Business Decisions and Financial Accounting

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Accounting Definition

Accounting Definition MINSK MINSK INNOVATION UNIVERSITY Oct, 2015 Learning Objectives After this lecture, you should be able to: 1. Define accounting. 2. Describe the primary forms of business organization.

Accounting Definition MINSK MINSK INNOVATION UNIVERSITY Oct, 2015 Learning Objectives After this lecture, you should be able to: 1. Define accounting. 2. Describe the primary forms of business organization.

Chapter 4. Posting to a General Ledger

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

Chapter 4 Posting to a General Ledger Introduction In the last chapter we journalized transactions. Now we have to post these entries to their own accounts so they can be analyzed if needed. 4-1 Terms

University of Denver Small Practice Management

University of Denver Small Practice Management Law Office Accounting Basics Bookkeeping, Record Keeping and Billing Brenda M. Clarke, CPA ABV CVA Seigneur Gustafson LLP April 11, 2013 2012 Brenda M. Clarke.

University of Denver Small Practice Management Law Office Accounting Basics Bookkeeping, Record Keeping and Billing Brenda M. Clarke, CPA ABV CVA Seigneur Gustafson LLP April 11, 2013 2012 Brenda M. Clarke.

Financial Statement Analysis-FIN621 ACCOUNTING & ACCOUNTING PRINCIPLES

ACCOUNTING & ACCOUNTING PRINCIPLES Lesson-1 Accounting Almost every organization and individual maintains accounts and deals with accounting. In simple terms, it can be described as a record of Income

ACCOUNTING & ACCOUNTING PRINCIPLES Lesson-1 Accounting Almost every organization and individual maintains accounts and deals with accounting. In simple terms, it can be described as a record of Income

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Chapter 2: The Balance Sheet

TRUE/FALSE 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. Answer: True Difficulty: 1 Easy LO: 02-01 Topic: Transactions and

TRUE/FALSE 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. Answer: True Difficulty: 1 Easy LO: 02-01 Topic: Transactions and

ACCOUNTING INTERVIEW QUESTIONS

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

Appendices - Introduction

Appendices - Introduction For more than one reason, we have posted a printable "pdf" copy of the appendices listed below, on our website @: http://www.full-chargebookkeeping.com/ > Resources & Links page.

Appendices - Introduction For more than one reason, we have posted a printable "pdf" copy of the appendices listed below, on our website @: http://www.full-chargebookkeeping.com/ > Resources & Links page.

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Not For Sale. Overview of Financial Statements FACMU14. Cengage Learning. All rights reserved. No distribution allowed without express authorization.

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE 1 CONTENTS A) Bookkeeping 1) About Single Entry System and its disadvantages 2) About Bookkeeping and Accounting Process 3) About Double

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE 1 CONTENTS A) Bookkeeping 1) About Single Entry System and its disadvantages 2) About Bookkeeping and Accounting Process 3) About Double

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Accounting I. Lesson Plan. Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Cash Payments Unit: 3 Chapter 11

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Exam 1 Sample Questions FINAN303 Principles of Finance McBrayer Spring 2018

Sample Multiple Choice Questions 1. The effect of a stock dividend (i.e., stock split) is that it a. Reduces owner s equity. b. Increases retained earnings. c. Reduces the liabilities of the firm. d. Increases

Sample Multiple Choice Questions 1. The effect of a stock dividend (i.e., stock split) is that it a. Reduces owner s equity. b. Increases retained earnings. c. Reduces the liabilities of the firm. d. Increases

Accounting Vocabulary

Accounting Vocabulary A. Accounting: planning, recording, analyzing and interpreting financial information. Accounting Equation: an equation showing the relationship among assets, liabilities, and owner

Accounting Vocabulary A. Accounting: planning, recording, analyzing and interpreting financial information. Accounting Equation: an equation showing the relationship among assets, liabilities, and owner

Chapter 4: Posting from a General Journal to a General Ledger

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 3: Double-Entry Bookkeeping

Chapter 3: Double-Entry Bookkeeping Double-entry bookkeeping underpins accounting A way of systematically recording the financial transactions of a company so that each transaction is recorded twice. Basic

Chapter 3: Double-Entry Bookkeeping Double-entry bookkeeping underpins accounting A way of systematically recording the financial transactions of a company so that each transaction is recorded twice. Basic

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1 Published by ICB Direct Ltd ICB Direct Ltd 2013 All rights reserved. No part of this publication may be reproduced, sorted in a retrieval system,

ICB Level II Certificate in Book-keeping TRAINING MANUAL 1 Published by ICB Direct Ltd ICB Direct Ltd 2013 All rights reserved. No part of this publication may be reproduced, sorted in a retrieval system,

Accounting Basics. (Flashcards: Double-sided)

") Accounting Basics (Flashcards: Double-sided) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or

Accounting Basics (Flashcards: Double-sided) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or

> > > > > > > > Chapter 16. Understanding Accounting and Financial Statements

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

A Simple Start to Managing Your Business Finances

A Simple Start to Managing Your Business Finances A Guide to the Essentials QB_10/2004_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

A Simple Start to Managing Your Business Finances A Guide to the Essentials QB_10/2004_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

LESSON Posting to an Accounts Payable Ledger. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

Job Ready Assessment Blueprint

Blueprint Test Code: 2120 / Version: 01 Financial and Managerial Accounting (Written Only) Specific Competencies and Skills Tested in this Assessment: Journalizing Understand the theory of double entry

Blueprint Test Code: 2120 / Version: 01 Financial and Managerial Accounting (Written Only) Specific Competencies and Skills Tested in this Assessment: Journalizing Understand the theory of double entry

100 Accounting Interview Questions and Answers

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

Seminar on Bookkeeping Basics

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Evaluating the Financial Viability of the Business

Evaluating the Financial Viability of the Business Just as it is important to construct a new building on a strong foundation, it is important to build the economic future of your business on a sound financial

Evaluating the Financial Viability of the Business Just as it is important to construct a new building on a strong foundation, it is important to build the economic future of your business on a sound financial

Accounting I Class Schedule

Accounting I Class Schedule Accounting I Instructor: Dr. Ben Mahdavian Time: Tuesday 1:00 3:30 PM Thurs. 1:00 3:30 PM Room: BJ 106 02/09/2016 through 06/02/2016 Office Hours: Thursday 12:30-1:00 P.M in

Accounting I Class Schedule Accounting I Instructor: Dr. Ben Mahdavian Time: Tuesday 1:00 3:30 PM Thurs. 1:00 3:30 PM Room: BJ 106 02/09/2016 through 06/02/2016 Office Hours: Thursday 12:30-1:00 P.M in

Financial Statements

CH2404 Process Economics Unit IV Financial Statements Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

CH2404 Process Economics Unit IV Financial Statements Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

Chapter 1 Accounting and the Business Environment

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Extra Practice for Block 1

Extra Practice for Block 1 Source: Harrison, Walter T., Jr., and Charles T. Horngren. Financial Accounting. 3rd ed. Boston: Pearson, 2008. Print. Custom Edition. Chapter 1 p.26-27 1. Which of the following

Extra Practice for Block 1 Source: Harrison, Walter T., Jr., and Charles T. Horngren. Financial Accounting. 3rd ed. Boston: Pearson, 2008. Print. Custom Edition. Chapter 1 p.26-27 1. Which of the following

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

Debits and Credits CHAPTER

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of