1

|

|

|

- Prosper Sims

- 5 years ago

- Views:

Transcription

1 1

2 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting 2

3 Definitions of Accounting Accounting is the language of the business AAA defines accounting as the process of identifying, measuring, and communicating economic information to permit informed judgment and decisions by the use of information AICPA defines Accounting is a services activity. Its function is to provide quantitative information primarily financial in nature, about economic entities that is intended to be useful in making economic decisions in making reasoned choices among alternative courses of action. 3

4 MCQs 1 Accounting can be defined as the process of identifying, measuring and communicating economic information about an entity to a variety of users? (a) True (b) False (a) True 4

5 MCQs 2 Which of the following does not describe accounting? (a) Language of business (b) Useful for decision making (c) Is an end rather than a mean to an end (d) Used by business, government, non-profit organizations and individuals (c) Is an end rather than a mean to an end? 5

6 MCQs 3 Why should a business keep accounts? (a) To discover how well the business is doing (b) To record assets and liabilities (c) To help run the business efficiently (d) All of the above (d) All of the above 6

7 Approaches and Objective of Accounting Approaches of Accounting American or Modern Approach British or Conventional or English Approach Objective/Aim/Purpose of Accounting The major objective of accounting is to provide useful information to economic decision maker 7

8 MCQs 4 What is the main aim of accounting? (a) To record every financial transaction individually (b) To maintain ledger accounts for every transaction (c) To prepare a trial balance (d) To provide financial information to users of such information (d) To provide financial information to users of such information 8

9 MCQs 5 Which of the following statements gives the best definition of the objective of accounting? (a) To provide useful information to users. (b) To record, categorise and summarise financial transactions. (c) To calculate the taxation due to the government. (d) To calculate the amount of dividend to pay to the shareholders. (a) To provide useful information to users. 9

10 Forms of Accounting Just as two types of economic decisions, there are two types of accounting information Financial Accounting and Management Accounting often are describing two types of accounting information that are widely used business decisions 10

11 Financial Accounting Financial accounting can be described as the recording, classification and summarizing of monetary transactions of an entity by means of various financial statements, during and at the end of an accounting period In accordance with established concepts, principles, accounting standards and legal requirements, and their presentation 11

12 Financial Accounting (Cont ) Financial accountants, however, are usually concerned with summarizing historical data, often from the same basic records as management accountants but in a different way Financial Accounting information is used for so many purposes that it often is called General-Purpose Accounting End results of financial accounting are Financial Statements 12

13 Management Accounting Management accounting information is used to assist the management in its operational and strategic planning Management accountants produce information which is forwardlooking, and used to prepare budgets and make decisions about the future activities of a business The most important role of Management accountants is to set targets in the form of budget or standards, measure the actual performance and then make variance It is specific purpose accounting 13

14 MCQs 6 Financial statements differ from management accounts in that they? (a) Are prepared monthly for internal control purposes (b) Contain details of costs incurred in manufacturing (c) Are summarized and prepared mainly for external users of accounting information (d) Provide information to enable the trial balance to be prepared (c) Are summarized and prepared mainly for external users of accounting information 14

15 MCQs 7 Which one of the following does not apply to the preparation of financial statements? (a) They are prepared annually (b) They provide a summary of the outcome of financial transactions (c) They are prepared mainly for external users of accounting information (d) They are prepared to show the detailed costs of manufacturing and trading (d) They are prepared to show the detailed costs of manufacturing and trading 15

16 MCQs 8 The main aim of financial accounting is to? (a) Record all transactions in the books of accounts (b) Provide management with detailed analyses of costs (c) Present the financial results of the organisation by means of recognised statements (d) Calculate profit (c) Present the financial results of the organisation by means of recognised statements 16

17 MCQs 9 Financial accounts differ from management accounts in that they (a) Are prepared monthly for internal control purposes (b) Contain details of costs incurred in manufacturing (c) Are summarised and prepared mainly for external users of accounting information (d) Provide information to enable the trial balance to be prepared (c) Are summarised and prepared mainly for external users of accounting information 17

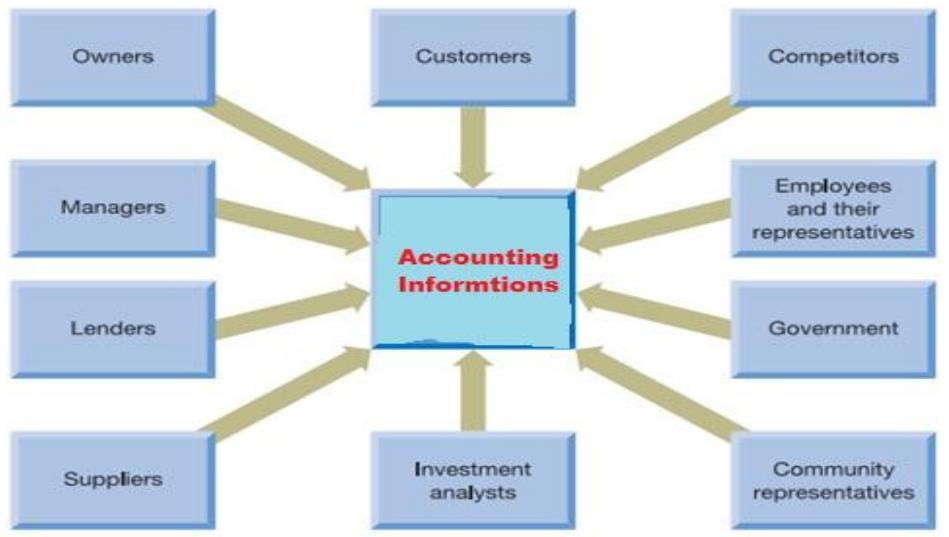

18 Users of Accounting Information Accounting information is needed by two sets of parties, which are internal and external Internal users are associated with management of the organization The external users consist of several explicit groups which are outside the organization and has interest (financial and nonfinancial) in an organization 18

19 19

20 Internal Users of Accounting Information o Internal users of accounting are parties who have directly connection with a company o Management accounting primarily use by internal parties or users o As well as financial accounting is also use for internal purpose 20

21 External Users of Accounting Information External users of accounting are potential investors, customers, banks, government agencies and other parties who are outside the business but need financial information about the business for a diverse number of reasons The Investor Group: They require information concerning the performance of the company measured in terms of its profitability (dividend). They are also interested in the corporate social responsibilities (CSR) of the company 21

22 External Users of Accounting Information (Cont ) The lender group: This group includes both existing and potential providers of secured or unsecured, long- or shortterm loan finance. They require information concerning the ability of the organization to repay the interest on such loans as they fall due; and the longer-term growth and stability of the organization to ensure that it is capable of repaying the principal amount at the agreed time. zaheerswati@ciit.net.pk 22

23 External Users of Accounting Information (Cont ) The employee group: They require information concerning the ability of the organization to pay wages and pensions today. In addition, they are interested in the future of the organization because this will affect their job security and future prospects within the organization 23

24 External Users of Accounting Information (Cont ) The Business Contact or Trade Contact Group: This group includes customers and suppliers of the organization. Customers will be concerned to ensure that the organization has the ability to provide the goods/services requested and to continue to provide similar services in the future. Suppliers will wish to ensure that the organization will be capable of paying for the goods/services supplied when payment becomes due 24

25 External Users of Accounting Information (Cont ) The Government: This group includes taxation authorities, and other government agencies and departments. The taxation authorities will calculate the organization s taxation liability based upon the accounting reports it submits to them The Public: This group includes taxpayers, consumers and other community and special interest groups. They require information concerning the policies of the organization and how those policies affect the community. The public is increasingly interested in environmental issues 25

26 MCQs 10 External Users of Financial Accounting Information include all of the following except? (a) Investors (b) Labor Union (c) Line Manager (d) General Public (c) Line Manager 26

27 MCQs 11 Internal users of accounting information include which of the following? (a) Company officers (b) Investors (c) Financial institutions (d) Competitors (a) Company officers 27

28 MCQs 12 Which one of the following sentences does not explain the distinction between financial accounts and management accounts? (a) Financial accounts are primarily for external users and management accounts are primarily for internal users (b) Financial accounts are normally produced annually and management accounts are normally produced monthly (c) Financial accounts are audited by an external auditor and management accounts do not normally have an external audit (d) Financial accounts are more accurate than management accounts (d) Financial accounts are more accurate than management accounts 28

29 MCQs 13 Which of the following are not the information requirement of equity investors? (a) Profitability (b) Performance (c) Dividends (d) Ability to repay loans (d) Ability to repay loans 29

30 Financial Statements End results of financial accounts are financial statements 30

31 Financial Statements (Cont ) According to IAS 1 Presentation of financial statements; a complete set of financial statements comprises: 1. A statement of comprehensive income for the period 2. A statement of changes in equity for the period 3. A statement of financial position as at the end of the period 4. A statement of cash flows for the period 5. Notes, comprising a summary of significant accounting policies and other explanatory information 31

32 MCQs 14 Which of the following financial statements reports financial results as of a single date? (a) Balance Sheet (b) Income Statement (c) Statement of changes in equity (d) Statement of cash flows (a) Balance Sheet 32

33 MCQs 15 Which of the following financial statements answers the question How did the business perform? (a) Balance Sheet (b) Income Statement (c) Statement of Owners Equity (d) Statement of cash flows (b) Income Statement 33

34 MCQs 16 The information needed to determine whether a company is using accounting methods similar to those of its competitors would be found in the? (a) Auditor s report (b) Balance sheet (c) Management discussion and analysis section (d) Notes to the financial statements (d) Notes to the financial statements 34

35 MCQs 17 Which accounting document keeps track of the cash receipts and cash payments of a business during a specific period? (a) Balance sheet (b) Income statement (c) Financial report (d) Cash flow statement (d) Cash flow statement zaheerswati@ciit.net.pk 35

36 The Qualitative Characteristics of Financial Statements The IASB s Framework suggests that financial statements should have certain qualitative characteristics. The framework splits qualitative characteristics into two categories: 1. Fundamental Qualitative characteristics 2. Enhancing Qualitative characteristics 36

37 1. Fundamental Qualitative characteristics Relevance: Accounting information should be relevant to the information needs of its users Faithful representation or Reliability: Accounting information should be prepared in such a way that users could rely upon it. To ensure reliability, the information should reflect the underlying economic realities and should be capable of being verified independently. Completeness, neutrality and free of errors should considered 37

38 2. Enhancing Qualitative characteristics Comparability: Users must be able to compare financial statements over a period of time within organization and also be able to compare financial statements of different entities to be able to assess their relative financial position and performance Verifiability: Verification can be direct and in direct. Direct verification means verifying an amount or other representation through direct observation like counting cash in hand. Indirect verification means checking the inputs to a model, formula or other technique 38

39 2. Enhancing Qualitative characteristics Timeliness: Accounting information should be produced in time for it to be used effectively. The information should be made available when the need arise Understandability: Accounting information should be capable of being understood by the recipient without difficulty. To ensure a thorough understanding of information, the preparer should take note of avoiding the use of unexplained terminology and should good report statement layout 39

40 MCQs 18 Which one of the following is not a qualitative characteristic of useful accounting information? (a) Relevance (b) Reliability (c) Cash-basis accounting (d) Comparability (c) Cash-basis accounting 40

41 MCQs 19 Which of the following is not a useful characteristic of accounting information as per ASB Statement of Principles? (a) Relevance (b) Profitability (c) Comparable (d) Complete (b) Profitability 41

42 Business and its Classification The word business means the state of being busy A 'business' is also a very general term, but it does not extend as widely as the term 'enterprise' as it would not include none profit making organization. 1. Profit-making organizations 2. Non-profit-making organizations 42

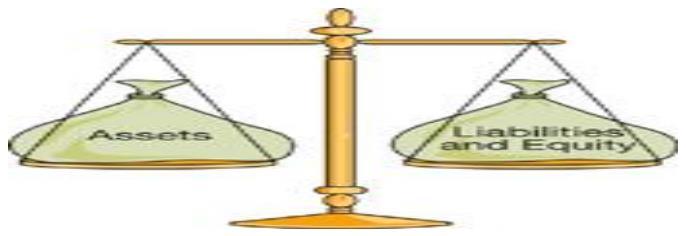

43 1. Profit-making organizations 43

44 2. Non-profit-making organizations Some organisations exist, not with the main intention of making profits in the long term, but with the objective of providing facilities to their members or others who may benefit from their activities. These organisations are often clubs and societies etc. 44

45 MCQs 20 Which one of the following is not a profit-making organisation? (a) Partnership (b) Local government (c) Sole trader (d) Limited company (b) Local government 45

46 MCQs 21 Which one of the following is not a non-profit-making organisation? (a) Public limited company (b) Charity (c) Clubs (d) Central government (a) Public limited company zaheerswati@ciit.net.pk 46

47 MCQs 22 All of the following are advantages for choosing a proprietorship for a business except? (a) A proprietorship is a simple form of business to set up (b) A proprietorship gives the owner control of the business (c) Transfer of ownership is easily achieved through stock sales (d) Proprietorship receives more favorable tax treatment (c) Transfer of ownership is easily achieved through stock sales 47

48 48

49 49

50 The separate entity convention According to the standard, every economic unit, regardless of its legal form of existence, is treated as a separate entity from parties having economic interest in it. A business entity is an economic unit which owns its assets and has its own obligations Financial statements always treat the business as a separate entity 50

51 The Accounting Equation Locus Pacioli 51

52 52

53 Note: Drawing/Dividend is also contra to Equity 53

54 54

55 Calculation of Capital 55

56 MCQs 23 The accounting equation at the start of the month was: Assets 14,000 less liabilities 6,250. During the month the following transactions took place: the business purchased a fixed asset for 3,000, paying by cheque, a profit of 3,500 was made and creditors of 2,750 were paid by cheque. Calculate the capital at the start of the month? (a) 7,750 (b) 11,500 (c) 5,500 (d) 8,250 (a) 7,750 56

57 MCQs 24 A sole trader has opening capital of 20,000 and closing capital of 9,000. During the period, the owner introduced capital of 8,000 and withdrew 16,000 for her own use. Calculate her profit or loss during the period? (a) 21,000 loss (b) 3,000 profit (c) 3,000 loss (d) 21,000 profit (c) 3,000 loss zaheerswati@ciit.net.pk 57

58 MCQs 25 The profit of a business may be calculated by using which one of the following formula? (a) Opening capital - Drawings + Capital introduced - Closing capital (b) Opening capital + Drawings - Capital introduced - Opening capital (c) Closing capital + Drawings - Capital introduced - Opening capital (d) Closing capital - Drawings + Capital introduced - Opening capital (b) Opening capital + Drawings - Capital introduced - Opening capital 58

59 MCQs 26 The accounting equation can change as a result of certain transactions. Which one of the following transactions would not affect the accounting equation? (a) Selling goods more than their cost (b) Purchasing a fixed asset on credit (c) The owner withdrawing cash (d) Debtors paying their accounts in full, in cash (d) Debtors paying their accounts in full, in cash 59

60 MCQs 27 (c) $ 250,

61 Accounting Pillars 61

62 Assets All Economic Resources of business organization. Assets are defined in Statement of Financial Accounting Concept 6 (SFAC 6); as future economic benefits obtained or controlled by a particular entity as a result of past transactions or events (Para. 25) A resource having economic value that an individual, corporation or country owns or controls with the expectation that it will provide future benefit It has four types, Tangible Assets, Intangible Assets, Natural Resources and Financial Assets 62

63 Types of Assets 63

64 Balance Sheet Classification of Assets Assets in the statement of financial position are divided into two groups, current assets and non-current assets Current Assets are items owned by the business with the intention of turning them into cash within one year and Commonly current assets are showing in balance sheet by liquidity order 64

65 Balance Sheet Classification of Assets (Cont ) Non-current assets on the other hand, asset acquired for continuing use within the business, with a view to earning income or making profits from its use of more than one year Tangible non-current assets usually known as Property, plant and equipment (PP&E) Intangible non-current assets Investments (long term) 65

66 Liabilities All Economic Obligations of business organization Liabilities are defined by SFAC 6 as future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events (Para. 35) Liabilities are typically divided into two categories: short-term or current liabilities and long term liabilities 66

67 Balance Sheet Classification of Liabilities Current liabilities are debts of the business that must be paid within a fairly short period of time. By convention, a 'fairly short period of time' is taken as one year A non-current liability is a debt which is not payable within the 'short term' and so any liability which is not current must be longterm. By convention 'non-current' means more than one year 67

68 MCQs 28 A motor trader has a van for sale. How will this be shown in the accounts? (a) Non-current asset (b) Current asset (c) Non-current liability (d) Current liability (b) Current asset 68

69 MCQs 29 Which of the following is not the classification of current assets with respect to the company s act? (a) Cash in hand (b) Bank at bank (c) Marketable Securities (d) Premises (d) Premises 69

70 Classify the following items as Current assets, Non-current assets, Current liability or Non-current liability 70

71 Categorize the following as Current assets, Tangible non-current assets, Intangible non-current assets, Investments,, Current liabilities or Non-current liabilities 71

72 Equity/ Capital/ Shareholder s Equity/ Stockholder s Equity o Investment in the business by owner o According to SFAC 6 the residual interest in the net assets of an entity that remains after deducting its liabilities (Para. 49) 72

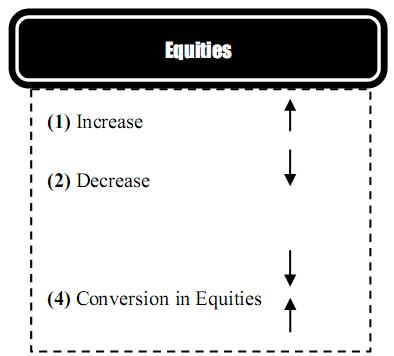

73 Drawings Deinvesment in the business by owner Drawing is defines as withdrawal by owner in the form of cash and other assets for their personal use. This will be deducted to owner personal account This is the case only sole proprietorship and partnership. There is no drawing account in case of corporation. Drawing decrease owner equity in the business 73

74 MCQs 30 Capital is? (a) The amount borrowed to set up a business (b) The amount owed by a business to its proprietor (s) (c) The value of the assets in a business (d) The total amount invested in a business by all the providers of capital (b) The amount owed by a business to its proprietor (s) zaheerswati@ciit.net.pk 74

75 State whether the following are Current assets, Non-current assets, Liabilities, Capital or Drawings 75

76 Expenses All Outflows of the business for earning According to SFAC 6 as outflows from delivering or producing goods, rendering services or carrying out other activities that constitute the entity s ongoing major operations (Para. 80). Expenses are economic costs that a business incurs through its operations to earn revenue 76

77 Revenue All inflows of the business Revenue = Cost + Profit or (Loss) According to SFAC 6 as inflow from delivering or producing goods, rendering services or other activities that constitute the entity s ongoing major or central operations (Para. 78) 77

78 MCQs 31 What is the definition of profit earned in a period? (a) Income less expenditure (b) Income less expenditure less drawings (c) The balance on the capital account (d) The total of assets less liabilities (a) Income less expenditure 78

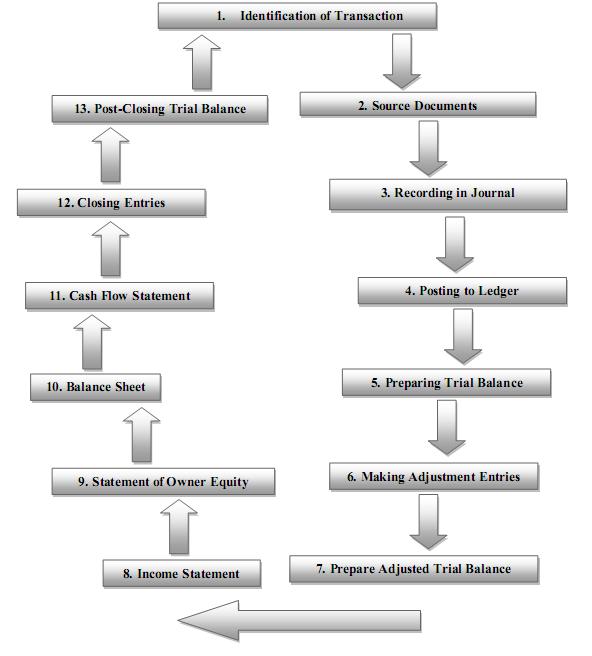

79 MCQs 32 Which of the following is correct? (a) Profit does not alter equity (b) Profit increases equity (c) Equity can only come from profit (d) Profit reduces equity (b) Profit increases equity 79

80 Four effects of Accounting 80

81 MCQs 33 (a) Rs. 26,000 (b) Rs. 36,000 (c) Rs. 46,000 (d) Rs. 50,000 (d) Rs. 50,000 81

82 For each of the following transactions indicate the effects on the Accounting Equation of the Company i.e. (Increase, Decrease, Conversion or No Effect)? 82

83 From the list of accounts below, determine which assets are and which equities are. List the assets under the Asset Column and the equities under the equities Column. Then add each column and complete the Fundamental Accounting Equation? 83

84 84

85 85

86 Accounting Cycle 86

87 Identification of Transactions In accounting, only business transaction or economic activities are recorded. A transaction is a particular type of event, which can be expressed in terms of money and brings changes in the financial position of a business unit. 87

88 Source Documents Cash Memo Invoice or Bill Receipt When a trader sells goods for cash, he gives a cash memo and when a trader purchases goods for cash, he receives a cash memo When a trader sells goods on credit, he prepares a sale invoice When a trader receives cash from a credit customer, he issues a receipt 88

89 Source Documents (Cont ) Debit Note Credit Note Pay-in-slip A debit note is prepared by the buyer and it contains the date of the goods returned, name of the supplier, details of the goods returned and reasons for returning the goods A credit note is prepared by the seller and it contains the date on which goods are returned, name of the customer, details of the goods received back, amount of such goods and reasons for returning the goods Pay-in-slip is a form available in banks and is used to deposit money into a bank account 89

90 Bookkeeping Vs. Accounting Bookkeeping is a small part of the field of accounting. Bookkeeping is recording phase of accounting system. Accounting is broad subject. Greater understanding of recording obtained from bookkeeping and an ability to analyze and interpret the information provided by bookkeeping records. 90

91")

91 MCQs 34 (b) 91

92")

92 MCQs 35 (b) 92

93 Systems or Basis of Accounting Cash Basis Events are recorded when actual cash / check is received or paid. Accrual Basis Income is recorded when it is earned and expense is recorded when they incurred 93

94 MCQs 36 The accounting system, in which accounting entries are made on the basis of amount having become due for payment or receipt, is known as? (a) Cash system of accounting (b) Current accounting period (c) Accrual system of accounting (d) None of the given options (c) 94

95 Methods of Recording That means, only one aspect of transaction i.e. either cash receipt or the fact that money is receivable from someone is recorded. The accounting system that records both the aspects of transaction in books of accounts Single Entry Double Entry 95

96 MCQs 37 Which one of the following system of recording transaction has a dual aspect concept of accounting? (a) Cash system of accounting (b) Single entry system (c) Double entry system (d) Accrual system of accounting (c) 96

")

are denoted by Dr and Cr respectively.")

97 Double Entry Book-Keeping Locus Pacioli, an Italian wrote a first book on double entry system in 1494 The concept of double entry is based on the fact that every transaction has two aspects i.e. receiving a benefit and giving a benefit Each transaction is recorded in terms of accounting alphabetic i.e. debit (Dr) and credit (Cr) Debit (derived from Latin word Debere which means to owe) and Credit (derived from Latin word Credere which means that which one believes in, including persons, like creditor) are denoted by Dr and Cr respectively. The ultimate result of the system is that for every Debit (Dr) there is an equal Credit (Cr) 97

98 MCQs 38 Commercial Accounting is done through? (a) Single entry book-keeping (b) Double entry book-keeping (c) Both Single entry and Double entry book-keeping (d) None of given option (b) 98

99 Entry Single record of the business transaction is called entry. Following are three parts of entry Part of Entry Debit Credit Narration 99

100 MCQs 39 Which of the following presents key aspects of the process of accounting in the correct chronological order? (a) Communicating, recording, and identifying (b) Recording, identifying, and communicating (c) Recording, totaling, and identifying (d) Identifying, recording, and communicating (d) 100

101 Types of Entry Types of Entry Simple Compound 101

102 MCQs 40 A Journal entry which requires more than two accounts is called? (a) Double entry (b) Compound entry (c) Combined entry (d) None (b) 102

103 Golden Rules 103

104 104

105 Application of Golden Rules Assets Increase in asset will be recorded Dr and decrease will be recorded Cr Continued 105

106 Application of Golden Rules Drawing It is essential to remember that Drawing always Debited and the asset which is taken by owner will Credited Continued 106

107")

107 MCQs 41 (d) 107

108 MCQs 42 (a) 108

109 Application of Golden Rules Expanses It is important to understand that all Expanses must be Debited to their name. Continued 109

110 Application of Golden Rules Liabilities Decrease will be recorded Debited and increase will be Credited. Continued 110

111 MCQs 43 The correct entries needed to record the return of office equipment that had been bought on credit from Ali, and not yet paid for, are Debit (a) Office equipment (b) Office equipment (c) Ali (d) Cash Credit Sales Ali Office equipment Office equipment (c) Ali Office equipment 111

112 MCQs 44 Of the following account types, which would be increased by a debit? (a) Liabilities and expenses (b) Assets and equity (c) Assets and expenses (d) Equity and revenues (c) Assets and expenses 112

113 Application of Golden Rules Owner Equity When Owner increases his Equity it is recorded as Credit, and when owner reduced his equity it will be Debit with specified term Drawing Continued 113

114 Application of Golden Rules Revenue It is important to note that all Revenues items must be credited with its names 114

115 MCQs 45 X receives goods from Y on credit and X subsequently pays by cheque. A then discovers that the goods are faulty and cancels the cheque before it is cashed by Y. How should X record the cancellation of the cheque in his books? Debit (a) Creditors (b) Creditors (c) Bank (d) Returns outwards Credit Returns outwards Bank Creditors Creditors (c) 115

116 MCQs 46 According to the rules of debit and credit for balance sheet accounts? (a) Increase in assets, liabilities and owner equity recorded by debit (b) Decrease in asset and liability are recorded by credit (c) Increase in asset and owner s equity are recorded by debit (d) Decrease in liability and owner s equity are recorded by debit (d) Decrease in liability and owner s equity are recorded by debit 116

117 MCQs 47 Which of the following account/s will be affected under the rule of accrual accounting, when furniture is purchased on cash? (a) Only cash account (b) Only furniture account (c) Cash & furniture account (d) Only purchases account (c) Cash & furniture account 117

118 MCQs 48 Which of the following is the correct entry to record the purchase on credit of stocks intended for resale? Debit Credit (a) Stock Debtor (b) Stock Creditor (c) Purchases Creditor (d) Creditor Purchases (c) Purchases Creditor 118

119 Contra Accounts 119

120 General Journal Book of Original Entry Book of Prime Entry 120

121 121

122 122

123 For More Resources 123

Executive Level. Financial Accounting & Reporting Fundamentals. (3) Section 1(a): 10 multiple choice questions (MCQs) all questions are compulsory.

Section 1(a): 10 multiple choice questions (MCQs) all questions are compulsory.") Copyright Reserved No. of pages: 14 Executive Level Financial Accounting & Reporting Fundamentals Instructions to candidates (1) Time allowed: Reading and planning 15 minutes Writing 3 hours (2) Total:

Copyright Reserved No. of pages: 14 Executive Level Financial Accounting & Reporting Fundamentals Instructions to candidates (1) Time allowed: Reading and planning 15 minutes Writing 3 hours (2) Total:

MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50

Time: 60 min Marks: 50") MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50 Question No: 1 ( Marks: 1 ) - Please choose one An accounting system is used by a business to: Analyze transactions

MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50 Question No: 1 ( Marks: 1 ) - Please choose one An accounting system is used by a business to: Analyze transactions

Chapter 3: The Ledger and Double-Entry Accounting System. 3. How to record in Assets, Liabilities & Owner s Equity account:

1 Chapter 3: The Ledger and Double-Entry Accounting System Topic Outline: 1. Ledger 2. Ledger Account the T-account 3. How to record in Assets, Liabilities & Owner s Equity account: - the increases - the

1 Chapter 3: The Ledger and Double-Entry Accounting System Topic Outline: 1. Ledger 2. Ledger Account the T-account 3. How to record in Assets, Liabilities & Owner s Equity account: - the increases - the

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Types of Accounts and Rules of Debit & Credit

Types of s and Rules of Debit & Credit : A summarized record of transactions in a classified manner is known as. For example,, Machinery etc. In all transactions relating to cash are to be posted whereas

Types of s and Rules of Debit & Credit : A summarized record of transactions in a classified manner is known as. For example,, Machinery etc. In all transactions relating to cash are to be posted whereas

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

BSc (Hons) Tourism and Hospitality Management. Cohort: BTHM/12B/FT Year 1. Examinations for 2012/2013 Semester I. & 2012 Semester II

Tourism and Hospitality Management. Cohort: BTHM/12B/FT Year 1. Examinations for 2012/2013 Semester I. & 2012 Semester II") BSc (Hons) Tourism and Hospitality Management Cohort: BTHM/12B/FT Year 1 Examinations for 2012/2013 Semester I & 2012 Semester II MODULE: FINANCIAL ACCOUNTING MODULE CODE: ACCF 1102A Duration: 2 Hours

BSc (Hons) Tourism and Hospitality Management Cohort: BTHM/12B/FT Year 1 Examinations for 2012/2013 Semester I & 2012 Semester II MODULE: FINANCIAL ACCOUNTING MODULE CODE: ACCF 1102A Duration: 2 Hours

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 FINANCIAL ACCOUNTING Introduction to financial accounting Recording non-current assets and depreciation

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 FINANCIAL ACCOUNTING Introduction to financial accounting Recording non-current assets and depreciation Compiling financial statement Compiling financial statement

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 FINANCIAL ACCOUNTING Introduction to financial accounting Recording non-current assets and depreciation Compiling financial statement Compiling financial statement

MGT101 All Solved Past Papers of Mid Term Exam in one file By

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

MGT101- Financial Accounting

MIDTERM EXAMINATION MGT101- Financial Accounting Question No: 1 ( Marks: 1 ) - Please choose one Depreciation arises because of: Fall in the market value of an asset Fall in the value of money Physical

MIDTERM EXAMINATION MGT101- Financial Accounting Question No: 1 ( Marks: 1 ) - Please choose one Depreciation arises because of: Fall in the market value of an asset Fall in the value of money Physical

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2)

") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS GCE ORDINARY LEVEL (SYLLABUS 7092) INTRODUCTION The syllabus aims to develop an understanding of the principles and concepts of accounting and their applications in a variety of

PRINCIPLES OF ACCOUNTS GCE ORDINARY LEVEL (SYLLABUS 7092) INTRODUCTION The syllabus aims to develop an understanding of the principles and concepts of accounting and their applications in a variety of

Financial Statement Analysis-FIN621 ACCOUNTING & ACCOUNTING PRINCIPLES

ACCOUNTING & ACCOUNTING PRINCIPLES Lesson-1 Accounting Almost every organization and individual maintains accounts and deals with accounting. In simple terms, it can be described as a record of Income

ACCOUNTING & ACCOUNTING PRINCIPLES Lesson-1 Accounting Almost every organization and individual maintains accounts and deals with accounting. In simple terms, it can be described as a record of Income

INTRODUCTION TO THE ACCOUNTING STATEMENTS

INTRODUCTION TO THE ACCOUNTING STATEMENTS The purpose of this course is to introduce you to basic bookkeeping and accounting and thus to eplain the basis upon which financial information is recorded, aggregated

INTRODUCTION TO THE ACCOUNTING STATEMENTS The purpose of this course is to introduce you to basic bookkeeping and accounting and thus to eplain the basis upon which financial information is recorded, aggregated

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

Fin621 Online Quizzes & Papers GURU

1.If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an: A.. understatement of net income for the year by $7,500 B.. understatement of cost of merchandise sold

1.If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an: A.. understatement of net income for the year by $7,500 B.. understatement of cost of merchandise sold

CBA Model Question Paper CO2. The difference between an income statement and an income and expenditure account is that

CBA Model Question Paper CO2 Question 1 The difference between an income statement and an income and expenditure account is that A an income and expenditure account is an international term for a Income

CBA Model Question Paper CO2 Question 1 The difference between an income statement and an income and expenditure account is that A an income and expenditure account is an international term for a Income

ACCOUNTANCY 2 BOOK- KEEPING

1 ACCOUNTANCY 1. Introduction to Accounting Business - whether large or small - main aim is to earn profit The details of business transactions viz., purchase of goods, sale of goods, salary, rent, interest

1 ACCOUNTANCY 1. Introduction to Accounting Business - whether large or small - main aim is to earn profit The details of business transactions viz., purchase of goods, sale of goods, salary, rent, interest

Paper N0:15. Solved by Chanda Rehman, Nomi chakwal ABr FINALTERM EXAMINATION. Fall MGT101- Financial Accounting (Session - 4)

") Paper N0:15 Solved by Chanda Rehman, Nomi chakwal ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 4) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one

Paper N0:15 Solved by Chanda Rehman, Nomi chakwal ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 4) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Debits and Credits CHAPTER

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

FINANCIAL ACCOUNTING CLASS - 11 TH

OBJECTIVE QUESTIONS FINANCIAL ACCOUNTING CLASS - 11 TH Accounting : Meaning and Objects I. Multiple Choice Questions 1. Qualitative characteristics of Accounting Informations are : (a) Reliability (b)

OBJECTIVE QUESTIONS FINANCIAL ACCOUNTING CLASS - 11 TH Accounting : Meaning and Objects I. Multiple Choice Questions 1. Qualitative characteristics of Accounting Informations are : (a) Reliability (b)

Section A: Multiple-Choice Questions (2 marks each; Total 30 marks)

") Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS Accounting : The systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS Accounting : The systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers

1 Theoretical Framework

1 Theoretical Framework This Chapter Includes : Meaning and Scope of Accounting, Accounting Concepts, Accounting Principles, Conventions and Standards - Concepts, Objectives, Benefits, Accounting Policies,

1 Theoretical Framework This Chapter Includes : Meaning and Scope of Accounting, Accounting Concepts, Accounting Principles, Conventions and Standards - Concepts, Objectives, Benefits, Accounting Policies,

Talking Accounting Definitions

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

Chapter 2: The Balance Sheet

TRUE/FALSE 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. Answer: True Difficulty: 1 Easy LO: 02-01 Topic: Transactions and

TRUE/FALSE 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. Answer: True Difficulty: 1 Easy LO: 02-01 Topic: Transactions and

Introduction to Financial Accounting

Introduction to Financial Accounting Introduction to Accounting Accounting is a process that identifies, records and communicates information to interested users. Who Uses Accounting Data? Internal Users

Introduction to Financial Accounting Introduction to Accounting Accounting is a process that identifies, records and communicates information to interested users. Who Uses Accounting Data? Internal Users

" Annual report: the main method that management uses to report the results of the company s activities during the year.

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Please spread the word about OpenTuition, so that all ACCA students can benefit.

ACCA COURSE NOTES June 2014 Examinations ACCA F3 FIA FFA Financial Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY with your support can the site exist

ACCA COURSE NOTES June 2014 Examinations ACCA F3 FIA FFA Financial Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY with your support can the site exist

CERTIFICATE LEVEL. SUBJECT BA3 Fundamentals of Financial Accounting CIMA OFFICIAL REVISION CARDS

CERTIFICATE LEVEL SUBJECT BA3 Fundamentals of Financial Accounting CIMA OFFICIAL REVISION CARDS FUNDAMENTALS OF FINANCIAL ACCOUNTING British library cataloguing-in-publication data A catalogue record for

CERTIFICATE LEVEL SUBJECT BA3 Fundamentals of Financial Accounting CIMA OFFICIAL REVISION CARDS FUNDAMENTALS OF FINANCIAL ACCOUNTING British library cataloguing-in-publication data A catalogue record for

NCERT Solutions for Class 11 Accountancy. Financial Accounting Part-1 Chapter 1

NCERT Solutions for Class 11 Accountancy Financial Accounting Part-1 Chapter 1 Short answers Q1 : Define accounting. Accounting is a process of identifying the events of financial nature, recording them

NCERT Solutions for Class 11 Accountancy Financial Accounting Part-1 Chapter 1 Short answers Q1 : Define accounting. Accounting is a process of identifying the events of financial nature, recording them

Institute of Certified Bookkeepers

Making you count Institute of Certified Bookkeepers Level II Certificate in Bookkeeping Syllabus from April 2014 1 Level II Certificate in Bookkeeping from April 2014 Course Code L2C Introduction Level

Making you count Institute of Certified Bookkeepers Level II Certificate in Bookkeeping Syllabus from April 2014 1 Level II Certificate in Bookkeeping from April 2014 Course Code L2C Introduction Level

Objective Accountancy

Objective Accountancy CLASS XI Multiple Choice Questions with Answers SBPD Model Paper for BSEB ( with OMR Sheet) Dr. S. K. Singh M. Com., Ph. D. Recipient of Rashtriya Gaurav Award, Asian Admirable Achiever,

Objective Accountancy CLASS XI Multiple Choice Questions with Answers SBPD Model Paper for BSEB ( with OMR Sheet) Dr. S. K. Singh M. Com., Ph. D. Recipient of Rashtriya Gaurav Award, Asian Admirable Achiever,

DOWNLOAD PDF LIST OF DEBIT AND CREDIT ITEMS IN ACCOUNTING

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

(50) BASIC ACCOUNTING

BASIC ACCOUNTING") All Rights Reserved Time: 03 hours THE ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Instructions to candidates FOUNDATION EXAMINATION - JANUARY 2015 (50) BASIC ACCOUNTING (1) This paper consists

All Rights Reserved Time: 03 hours THE ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Instructions to candidates FOUNDATION EXAMINATION - JANUARY 2015 (50) BASIC ACCOUNTING (1) This paper consists

Contents. 1 - Finance Financial Statements 4. 3 Accounting Concept & Conventions 5. 4 Capital & Revenue Expenditure 8

Contents 1 - Finance 3 2 - Financial Statements 4 3 Accounting Concept & Conventions 5 4 Capital & Revenue Expenditure 8 5 - Financial Statements Analysis 15 6 - Management Accounting 21 7 - Working Capital

Contents 1 - Finance 3 2 - Financial Statements 4 3 Accounting Concept & Conventions 5 4 Capital & Revenue Expenditure 8 5 - Financial Statements Analysis 15 6 - Management Accounting 21 7 - Working Capital

Advanced Financial Accounting (Fin611)

") Table of Content Advanced Financial Accounting (Fin611) Lesson No. Title / Topic 1 Accounting For Incomplete Records (Single Entry). 1 2 Practicing Accounting For Incomplete Records... 7 3 Conversion of

Table of Content Advanced Financial Accounting (Fin611) Lesson No. Title / Topic 1 Accounting For Incomplete Records (Single Entry). 1 2 Practicing Accounting For Incomplete Records... 7 3 Conversion of

Investing and Financing Decisions and the Accounting System

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE 1 CONTENTS A) Bookkeeping 1) About Single Entry System and its disadvantages 2) About Bookkeeping and Accounting Process 3) About Double

ACCOUNTING MANUAL ON DOUBLE ENTRY SYSTEM OF ACCOUNTING FOR ICFRE 1 CONTENTS A) Bookkeeping 1) About Single Entry System and its disadvantages 2) About Bookkeeping and Accounting Process 3) About Double

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS EXTERNAL TRANSACTIONS INTERNAL TRANSACTIONS NON-TRANSACTIONAL EVENTS Involves an

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS EXTERNAL TRANSACTIONS INTERNAL TRANSACTIONS NON-TRANSACTIONAL EVENTS Involves an

MGT101 - FINANCIAL ACCOUNTING I

MGT101 - FINANCIAL ACCOUNTING I Lesson No. TOPICS Page No. 1 Basic Concepts of Accounting... 1 2 Record Keeping and Some Basic Concepts 4 3 Systems of Accounting and Some Basic Terminologies. 7 4 Single

MGT101 - FINANCIAL ACCOUNTING I Lesson No. TOPICS Page No. 1 Basic Concepts of Accounting... 1 2 Record Keeping and Some Basic Concepts 4 3 Systems of Accounting and Some Basic Terminologies. 7 4 Single

Paper No:34 Solved by Chanda Rehman & ABr

Paper No:34 Solved by Chanda Rehman & ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one We can say that

Paper No:34 Solved by Chanda Rehman & ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one We can say that

True / False Questions

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

where the value of the transaction is

CHAPTER- INTRODUCTION TO ACCOUNTING Two marks Questions and Answers.. What is Book keeping? Book keeping is the art of recording business transactions in a systematic manner.. Give the meaning of Accounting?

CHAPTER- INTRODUCTION TO ACCOUNTING Two marks Questions and Answers.. What is Book keeping? Book keeping is the art of recording business transactions in a systematic manner.. Give the meaning of Accounting?

Unit 1 Theoretical Framework.

Unit 1 Theoretical Framework. A. Answer the Following (1 Mark) 1. What is Accounting equation? 2. Find out the value of assets if: Liabilities=Rs. 5000 and Capital=Rs.1000. 3. Give the classification of

Unit 1 Theoretical Framework. A. Answer the Following (1 Mark) 1. What is Accounting equation? 2. Find out the value of assets if: Liabilities=Rs. 5000 and Capital=Rs.1000. 3. Give the classification of

1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

HI-Aims College of Commerce & Management Sargodha Virtual University Campus PSGD03

1. Introduction to Accounting and its terminology 2. The Double entry system - Debit and Credit 3. Book of original entries - General journal 4. Preparing Ledger Account 5. Book of original entries - Specialized

1. Introduction to Accounting and its terminology 2. The Double entry system - Debit and Credit 3. Book of original entries - General journal 4. Preparing Ledger Account 5. Book of original entries - Specialized

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an):

- Please choose one Wages outstanding given in the trial balance will be treated as a (an):") Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

FFA. Financial Accounting. OpenTuition.com ACCA FIA exams. Free resources for accountancy students

September/December 2015 exams OpenTuition.com Free resources for accountancy students ACCA FIA F3 FFA Financial Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit.

September/December 2015 exams OpenTuition.com Free resources for accountancy students ACCA FIA F3 FFA Financial Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit.

Rate = 1 n RV / C Where: RV = Residual Value C = Cost n = Life of Asset Calculate the rate if: Cost = 100,000

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

resources controlled - as a result of past events - future economic benefits expected to flow

Discussion class notes : FAC1503 Financial accounting the provision of financial information to mainly external parties recording of transactions and the preparation of financial statements Management

Discussion class notes : FAC1503 Financial accounting the provision of financial information to mainly external parties recording of transactions and the preparation of financial statements Management

Unit 2. Theory Base of Accounting. Accounting Concepts

Generally Accepted Accounting Principles (GAAP) Unit 2 Theory Base of Accounting Generally accepted accounting principles (GAAP) refer to the standard framework of guidelines for financial accounting used

Generally Accepted Accounting Principles (GAAP) Unit 2 Theory Base of Accounting Generally accepted accounting principles (GAAP) refer to the standard framework of guidelines for financial accounting used

CS101 Introduction of computing

FINAL TERM EXAMINATION MGT101- Financial Accounting (PAPER 1). Question No: 1 (Marks: 1 ) basic accounting principle/concept according to which Business is independent from its owner(s) is known as: Separate

FINAL TERM EXAMINATION MGT101- Financial Accounting (PAPER 1). Question No: 1 (Marks: 1 ) basic accounting principle/concept according to which Business is independent from its owner(s) is known as: Separate

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME

GENERAL / SPECIAL DEGREE PROGRAMME") All Rights Reserved No. of Pages - 12 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER I (INTAKE VI GROUP B) END SEMESTER

All Rights Reserved No. of Pages - 12 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER I (INTAKE VI GROUP B) END SEMESTER

1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders'

Chapter 02 The Balance Sheet True / False Questions 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. True False 2. A debit may

Chapter 02 The Balance Sheet True / False Questions 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. True False 2. A debit may

CIMA F1. Financial Operations Student Notes

CIMA F1 Financial Operations Student Notes Contents CIMA F1...1 Topic 6 The Regulatory Environment...2 International Financial Reporting Standards (IFRSs)...5 Topic 7: The Conceptual Framework...7 Topic

CIMA F1 Financial Operations Student Notes Contents CIMA F1...1 Topic 6 The Regulatory Environment...2 International Financial Reporting Standards (IFRSs)...5 Topic 7: The Conceptual Framework...7 Topic

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

Module 1: The role and importance of financial reporting

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

ACCT2542 Week 1 Notes

ACCT2542 Week 1 Notes Chapter 1: History, Current Regulatory Structures and Processes Australian Standard-Setting Arrangements: There are five main bodies which formulate and/or enforce accounting regulations

ACCT2542 Week 1 Notes Chapter 1: History, Current Regulatory Structures and Processes Australian Standard-Setting Arrangements: There are five main bodies which formulate and/or enforce accounting regulations

ACCOUNTING. Written examination 1

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 10 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 10 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

BUSS 1030 ACCOUNTING, BUSINESS AND SOCIETY NOTES

WEEK 1 BUSS 1030 ACCOUNTING, BUSINESS AND SOCIETY NOTES Accounting information system measuring business activity, processes data into reports and communicates results to decision makers (ethics important

WEEK 1 BUSS 1030 ACCOUNTING, BUSINESS AND SOCIETY NOTES Accounting information system measuring business activity, processes data into reports and communicates results to decision makers (ethics important

ACCOUNTING INTERVIEW QUESTIONS

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

1 Theoretical Framework

1 Theoretical Framework This Chapter Includes: Meaning and Scope of Accounting, Accounting Concepts, Accounting Principles, Conventions and Standards - Concepts, Objectives, Benefits, Accounting Policies,

1 Theoretical Framework This Chapter Includes: Meaning and Scope of Accounting, Accounting Concepts, Accounting Principles, Conventions and Standards - Concepts, Objectives, Benefits, Accounting Policies,

UNIT ONE : INTRODUCTION TO ACCOUNTING

Slide 1.1 UNIT ONE : INTRODUCTION TO ACCOUNTING Learning Outcome Unit 1 Describe the purpose and aims of financial and management accounting. Describe the different users of financial information. Describe

Slide 1.1 UNIT ONE : INTRODUCTION TO ACCOUNTING Learning Outcome Unit 1 Describe the purpose and aims of financial and management accounting. Describe the different users of financial information. Describe

Chapter 2 MULTIPLE CHOICE

Objectives: 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to the rules of debit and credit. 3. Preparing a trial balance. 4. Preparing financial statements

Objectives: 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to the rules of debit and credit. 3. Preparing a trial balance. 4. Preparing financial statements

Full file at

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

COMPOSED BY SADIA ALI SADI (MBA)

") Mega File MGT101 Fall 2011 Question No: 7 ( Marks: 1 ) - Please choose one Which of the following business publishes the Financial Statements? Sole-Proprietorship Partnership Trust Public Limited Company

Mega File MGT101 Fall 2011 Question No: 7 ( Marks: 1 ) - Please choose one Which of the following business publishes the Financial Statements? Sole-Proprietorship Partnership Trust Public Limited Company

Not For Sale. Overview of Financial Statements FACMU14. Cengage Learning. All rights reserved. No distribution allowed without express authorization.

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

Accounting and Financial Management 1A

Accounting and Financial Management 1A LECTURE 1 NOTES Accounting definition: Way in which organisations provide measure of financial position/performance. Conveys economic info. to decision makers > economic

Accounting and Financial Management 1A LECTURE 1 NOTES Accounting definition: Way in which organisations provide measure of financial position/performance. Conveys economic info. to decision makers > economic

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Model Paper Principals of Accounting Objective

Model Paper Principals of Accounting Objective Intermediate Part I (11 th Class) Examination Session 2012-2013 and onward Total marks: 15 Paper Code Time Allowed: 20 minutes Note:- You have four choices

Model Paper Principals of Accounting Objective Intermediate Part I (11 th Class) Examination Session 2012-2013 and onward Total marks: 15 Paper Code Time Allowed: 20 minutes Note:- You have four choices

CHAPTER 2 QUESTIONS. revenue, and expense accounts of the

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

ACCOUNTING CONCEPTS AND PROCEDURES

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

MINISTRY OF EDUCATION

REPUBLIC OF NAMIBIA MINISTRY OF EDUCATION NAMIBIA SENIOR SECONDARY CERTIFICATE ACCOUNTING SPECIMEN PAPERS 1 2 AND MARK SCHEMES HIGHER LEVEL GRADES 11 12 THESE PAPERS AND MARK SCHEMES SERVE TO EXEMPLIFY

REPUBLIC OF NAMIBIA MINISTRY OF EDUCATION NAMIBIA SENIOR SECONDARY CERTIFICATE ACCOUNTING SPECIMEN PAPERS 1 2 AND MARK SCHEMES HIGHER LEVEL GRADES 11 12 THESE PAPERS AND MARK SCHEMES SERVE TO EXEMPLIFY

Prof. S P Bansal Vice Chancellor Maharaja Agrasen University, Baddi

Paper: 02, Accounting & Financial Analysis Module: 10, Cash Book: Meaning, Features, Advantages, Types and Petty Cash book Principal Investigator Co-Principal Investigator Paper Coordinator Content Writer

Paper: 02, Accounting & Financial Analysis Module: 10, Cash Book: Meaning, Features, Advantages, Types and Petty Cash book Principal Investigator Co-Principal Investigator Paper Coordinator Content Writer

Index. Cambridge University Press Short Introduction to Accounting Richard Barker Index More information

accountants, roles, 4 5 accounting applications, 11 12 approaches, 8 9 building blocks, 64 coverage, 9 divisiveness of, 3 foundations of, 11, 65 83 importance of, 1 3 incompleteness, 7 knowledge of, 1

accountants, roles, 4 5 accounting applications, 11 12 approaches, 8 9 building blocks, 64 coverage, 9 divisiveness of, 3 foundations of, 11, 65 83 importance of, 1 3 incompleteness, 7 knowledge of, 1

BOOKS OF ORIGINAL ENTRIES

BOOKS OF ORIGINAL ENTRIES These are the books of first entry. The transactions are first recorded in these books before being entered in the ledger books. These books are also called as books of Prime

BOOKS OF ORIGINAL ENTRIES These are the books of first entry. The transactions are first recorded in these books before being entered in the ledger books. These books are also called as books of Prime

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

Cambridge IGCSE Accounting (0452)

") www.xtremepapers.com Cambridge IGCSE Accounting (0452) International Accounting Standards (IAS) Guidance for Teachers Contents Introduction... 2 Use of this document... 2 Users of financial statements...

www.xtremepapers.com Cambridge IGCSE Accounting (0452) International Accounting Standards (IAS) Guidance for Teachers Contents Introduction... 2 Use of this document... 2 Users of financial statements...

HIGHER SECONDARY I ST YEAR ACCOUNTANCY. TIME : 2 ½ Hours MARKS : 90 MODEL QUESTION PAPER PART - I

HIGHER SECONDARY I ST YEAR ACCOUNTANCY TIME : 2 ½ Hours MARKS : 90 MODEL QUESTION PAPER PART - I Answer all the questions. Choose the correct answer. 20 X 1 = 20 1. The Debts owing to others by business

HIGHER SECONDARY I ST YEAR ACCOUNTANCY TIME : 2 ½ Hours MARKS : 90 MODEL QUESTION PAPER PART - I Answer all the questions. Choose the correct answer. 20 X 1 = 20 1. The Debts owing to others by business

Chapter III The Language of Accounting

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

COMSATS INSTITUTE OF INFORMATION TECHNOLOGY, ABBOTTABAD

COMSATS INSTITUTE OF INFORMATION TECHNOLOGY, ABBOTTABAD Registration # Signature Quiz # 2 and 3 Financial MBA 1(3.5) Instructions: 1. Borrowing of Calculator, Ruler etc. is not allowed 2. Switch off Mobile

COMSATS INSTITUTE OF INFORMATION TECHNOLOGY, ABBOTTABAD Registration # Signature Quiz # 2 and 3 Financial MBA 1(3.5) Instructions: 1. Borrowing of Calculator, Ruler etc. is not allowed 2. Switch off Mobile

100 Accounting Interview Questions and Answers

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

2010 Accounting GA 1: Written examination 1

Accounting GA 1: Written examination 1 GENERAL COMMENTS The June examination comprised of two 45-mark questions, with multiple parts to each question. Each question presented a business scenario which

Accounting GA 1: Written examination 1 GENERAL COMMENTS The June examination comprised of two 45-mark questions, with multiple parts to each question. Each question presented a business scenario which

Institute of Certified Bookkeepers

Making you count Institute of Certified Bookkeepers Level II Certificate in Bookkeeping Syllabus from April 2014 1 Level II Certificate in Bookkeeping Level II Certificate in Bookkeeping (Skills and Underpinning

Making you count Institute of Certified Bookkeepers Level II Certificate in Bookkeeping Syllabus from April 2014 1 Level II Certificate in Bookkeeping Level II Certificate in Bookkeeping (Skills and Underpinning

DOWNLOAD PDF JOURNAL ENTRY EXAMPLES ACCOUNTING

Chapter 1 : Ledger Accounts Posting Transactions Example Analyzing transactions and recording them as journal entries is the first step in the accounting blog.quintoapp.com begins at the start of an accounting

Chapter 1 : Ledger Accounts Posting Transactions Example Analyzing transactions and recording them as journal entries is the first step in the accounting blog.quintoapp.com begins at the start of an accounting

FUNDAMENTALS OF ACCOUNTING STUDY NOTES FOUNDATION FOUNDATION : PAPER - 2 SYLLABUS The Institute of Cost Accountants of India

FOUNDATION : PAPER - 2 SYLLABUS - 2016 FUNDAMENTALS OF ACCOUNTING FOUNDATION STUDY NOTES The Institute of Cost Accountants of India CMA Bhawan, 12, Sudder Street, Kolkata - 700 016 First Edition : August

FOUNDATION : PAPER - 2 SYLLABUS - 2016 FUNDAMENTALS OF ACCOUNTING FOUNDATION STUDY NOTES The Institute of Cost Accountants of India CMA Bhawan, 12, Sudder Street, Kolkata - 700 016 First Edition : August

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

[Time: Hours] 2. The cash book is used for recording the credit transaction of the business

![[Time: Hours] 2. The cash book is used for recording the credit transaction of the business](/thumbs/92/110038863.jpg "[Time: Hours] 2. The cash book is used for recording the credit transaction of the business") Q.1) A) N.B: [Time: 2 1 2 Hours] Please check whether you have got the right question paper. 1. All Questions are compulsory carrying 15 marks each. 2. Working notes should form part of your answers wherever

Q.1) A) N.B: [Time: 2 1 2 Hours] Please check whether you have got the right question paper. 1. All Questions are compulsory carrying 15 marks each. 2. Working notes should form part of your answers wherever