Financial Statements

|

|

|

- Charity Wilkerson

- 5 years ago

- Views:

Transcription

1 CH2404 Process Economics Unit IV Financial Statements Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam , Kanchipuram (Dist) Tamil Nadu, India msubbu.in[at]gmail.com 5-September-2011

2 Introduction Some basic knowledge of accounting and financial statements is necessary for a chemical professional to be able to analyze a firm s operations, discover whether the firm is making a profit and whether a company will continue to make a profit. Financial reports of a company are important sources of data used by management, owners, creditors, investment bankers, and financial analysts. Accounting systems have input business transactions in the form of receipts and invoices. These events are entered chronologically in a journal and are then classified and posted in an appropriate account in a ledger. Periodically, perhaps once a month but at least once a year, the accounts are closed and a summary is issued as an income statement and a balance sheet

3 Flow of Information through an Accounting System Business transaction takes place Business document is prepared Information is entered chronologically in a JOURNAL Debits and credits are posted to accounts in a LEDGER Financial statements are prepared and presented in INCOME STATEMENT and BALANCE SHEET Formal reports are issued to stockholders and government agencies

4 Debits and Credits Whenever economic events occur, the accounting equation changes and the events are recorded in books. The left side of the account book page has been arbitrarily designated the debit side, and the right side the credit side. This convention is true regardless of the type of account.

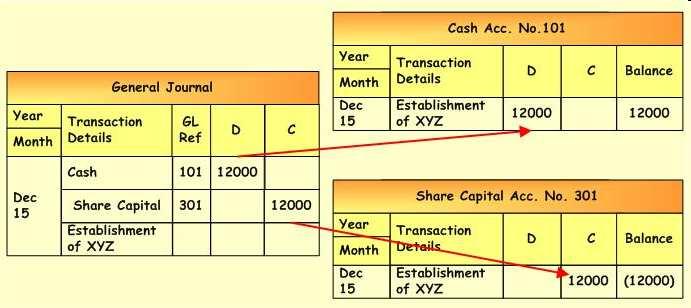

5 Journal and Ledger Entries Business transactions having an impact on the financial position of the business are first recorded in the general journal, which is one of the accounting prime entry books Then, entries from general journal are posted to the general ledger, i.e. to the corresponding account, which composes general ledger.

6

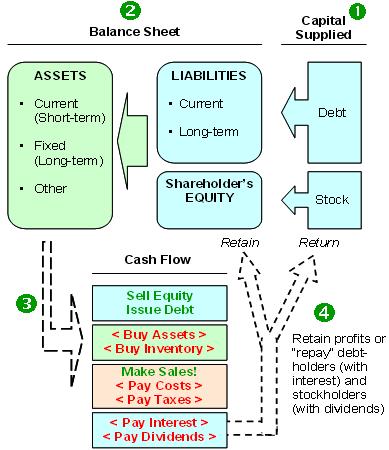

7 Accounting Equation Double-entry bookkeeping system, expressed as follows in simplest terms: Assets = Equities Assetsare the economic resources a company owns and which are expected to benefit future operations. Assets are items of value and may be tangible, such as equipment, buildings, furniture, or intangible, like franchises, patents, trademarks. Equitiesare claims against the firm and may be divided into liabilities and owners equity. The above equation then may be modified as follows: Assets = Liabilities + Owners equity

8 Liabilities are outside claims against the assets of a firm, e.g., accounts payable, borrowed funds, taxes owed. These obligations require settlement in the future. If liabilities are deducted from the assets, the difference is the amount belonging to the firm s owners, i.e., stockholders, and is called owners equity. Any transaction that takes place causes changes in the accounting equation. An increase in assets must be accompanied by one of the following: Increase in liabilities (e.g., money borrowed to purchase equipment) Increase in stockholders equity A change in one part of the equation due to an economic transaction must be accompanied by an equal change in another place hence the term double-entry bookkeeping.

9 Financial Report A financial report contains two significant documents the balance sheet and the income statement. Two ancillary documents are the accumulated retained earnings and the changes in working capital. In some annual reports, the accumulated retained earnings are included in the statement of consolidated stockholders equity.

10 Balance Sheet Balance sheet indicates structure of the assets belonging to the company and financial means used to finance these assets at a particular point of time. The balance sheet consists of two parts: the assets, which are what the company owns, and the liabilities and stockholders equity, which are what the company owes. The total assets must equal the total liabilities plus the stockholders equity for both sides of the sheet to balance. A balance sheet contains some real figures (e.g., cash and marketable securities), some estimated numbers or allowances (e.g., inventories and accounts receivable), as well as some fictitious numbers (e.g., intangibles for which numbers are difficult to assess).

11 The Balance Sheet Format ASSETS LIABILITIES AND OWNERS EQUITY Current Assets (Cash, A/R, Inventory) Current Liabilities (Accounts Payable, Current debt) Noncurrent Assets Long-Term Liabilities Investments Owners Equity Fixed Assets (PP&E) Intangible assets Contributed capital Retained earnings

12

13

14 Non-current means long-term and current means short-term.

15 a. Amount in thousands of dollars

16 Contd..

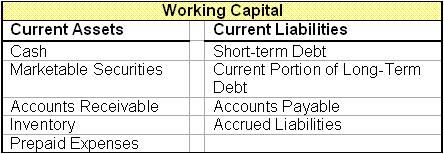

17 Assets The assets of a company are divided into three broad categories: current assets, fixed assets, and intangibles. Total Current Assets:the sum of cash, marketable securities, inventories, accounts receivable, and prepaid expenses is called total current asset. The current assets are those that may be converted to cash within a year from the date of the balance sheet. Fixed Assets: a company s fixed assets include land, buildings, manufacturing equipment, office equipment, automobiles, trucks, and so on that the company owns. These items are carried on the books at cost less the accumulated depreciation. Intangibles: they are assets that have substantial value to the company (patents, licenses, franchises, trademarks, goodwill, etc.).

18 Liabilities The liabilities are what a company owes, divided into current and long-term liabilities. Current Liabilities: these are debts that must be paid within a year from the date of the balance sheet. They are paid from the current assets. Current liabilities include accounts payable, notes payable, accrued expenses payable, and income taxes payable. Long-term liabilities are debts due more than a year from the date of the financial report. Long-term loans from insurance companies and investment houses are another form of long-term liability

19 Stockholders Equity This is the total interest that the stockholders have in the business. The stockholders equity is the net worth of the company, namely, total assets minus total liabilities. For convenience, stockholders equity is divided into three categories: capital stock, capital surplus, and accumulated retained earnings. Capital surplus is the amount of money stockholders paid for stock over and above the par value of the stock. The accumulated retained earnings are calculated by subtracting the dividends paid to stockholders from the net profit. If all the profits in one year are not distributed, they are retained by the firm and added to next year s earnings.

20

21

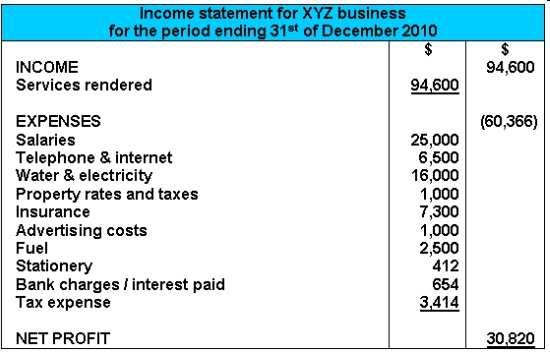

22 Income Statement Profits = Revenue - Expenses Income-sheet accounts of all income and expense items, such as sales, purchases, depreciation, wages, salaries, taxes, and insurance, are maintained, and these accounts are summarized periodically in income statements. A consolidated income statement is based on a given time period. It indicates surplus capital and shows the relationship among total income, costs, and profits over the time interval. It is also known as the profit and loss statement.

23

24

25 Multi-Step Format Net Sales Cost of Sales Single-Step Format Net Sales Materials and Production Gross Income* Selling, General and Administrative Expenses (SG&A) Operating Income* Marketing and Administrative Research and Development Expenses (R&D) Other Income & Expenses Other Income & Expenses Pretax Income Pretax Income* Taxes Taxes Net Income Net Income (after tax)* -- Read more:

26 Income Statement Formats Two basic formats for the income statement are used in financial reporting presentations - the multi-step and the single-step In the multi-step income statement, four measures of profitability (*) are revealed at four critical junctions in a company's operations -gross, operating, pretax and after tax. In the single-step presentation, the gross and operating income figures are not stated; nevertheless, they can be calculated from the data provided. Read more: B5ZlV

27 Income Statement Example

28 Terminologies in Income Statement Net Sales: the net sales is the amount of money received for the goods sold less the amount of returned goods and allowances for reduction in prices (e.g., allowing for freight on goods shipped). Cost of Goods Sold and Operating Expenses: this item includes all the expenses in converting raw materials into finished products, including depreciation, as well as sales, administration, research, and engineering expenses. Operating Profit (Operating Income): this entry is the difference between net sales and all operating expenses.

29

30

31 Connections between income statement and balance sheet accounts

32 Connections between income statement and balance sheet accounts. Here s a quick summary explaining the lines of connection in the figure, starting from the top and working down to the bottom: Making sales (and incurring expenses for making sales) requires a business to maintain a working cash balance. Making sales on credit generates accounts receivable. Selling products requires the business to carry an inventory (stock) of products. Acquiring products involves purchases on credit that generate accounts payable. Depreciation expense is recorded for the use of fixed assets (long-term operating resources). Depreciation is recorded in the accumulated depreciation contra account (instead decreasing the fixed asset account). Amortization expense is recorded for limited-life intangible assets. -contd..

33 Operating expenses is a broad category of costs encompassing selling, administrative, and general expenses: Some of these operating costs are prepaid before the expense is recorded, and until the expense is recorded, the cost stays in the prepaid expenses asset account. Some of these operating costs involve purchases on credit that generate accounts payable. Some of these operating costs are from recording unpaid expenses in the accrued expenses payable liability. Borrowing money on notes payable causes interest expense. A portion (usually relatively small) of income tax expense for the year is unpaid at year-end, which is recorded in the accrued expenses payable liability. Earning net income increases retained earnings.

34

35 400 (300) 500 2,000

36

37

38 (contd.)

39

40

41 (contd.)

42 Example Financial Statements Based on Annual Report of POWER GRID Corporation of India Ltd

43 POWER GRID Corporation of India Ltd

44 Assets Distribution - Example Source: POWER GRID Corporation of India Ltd., Annual Report

45 Liabilities Distribution - Example Source: POWER GRID Corporation of India Ltd., Annual Report

46

47

48 Income Contributions - Example Source: POWER GRID Corporation of India Ltd., Annual Report

49 Expenses Distribution - Example Source: POWER GRID Corporation of India Ltd., Annual Report

Sensitivity Analysis

CH2404 Process Economics Unit III Sensitivity Analysis Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

CH2404 Process Economics Unit III Sensitivity Analysis Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

CH2404 Process Economics Unit V Economic Balance. Dr. M. Subramanian

CH2404 Process Economics Unit V www.msubbu.in Economic Balance www.msubbu.in Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam

CH2404 Process Economics Unit V www.msubbu.in Economic Balance www.msubbu.in Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Profitability Estimates

CH2404 Process Economics Unit III Profitability Estimates Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110,

CH2404 Process Economics Unit III Profitability Estimates Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110,

Chapter 6 The annual report and accounts. The closure of the accounting cycle and Accounting information disclosed to the public

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

FORENSIC ACCOUNTING VERSION

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Digging Into The Balance Sheet and Income Statement. The Balance Sheet

Digging Into The Balance Sheet and Income Statement Jim Menard, CCE email: jsmenard62@gmail.com The Balance Sheet Also called the statement of condition or statement of financial position Financial Condition

Digging Into The Balance Sheet and Income Statement Jim Menard, CCE email: jsmenard62@gmail.com The Balance Sheet Also called the statement of condition or statement of financial position Financial Condition

AccountingCoach.com Financial Ratios

AccountingCoach.com Financial Ratios All underlined words are defined in the attached Glossary (Pages 13 20). Introduction to Financial Ratios When analyzing computing financial ratios and when doing other

AccountingCoach.com Financial Ratios All underlined words are defined in the attached Glossary (Pages 13 20). Introduction to Financial Ratios When analyzing computing financial ratios and when doing other

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

Chapter 2: The Basics of Record Keeping and Financial Statement Preparation: Balance Sheet

Chapter 2: The Basics of Record Keeping and Financial Statement Preparation: Balance Sheet Student: 1. The T-account looks like the letter T, with a horizontal line bisected by a vertical line. Increases

Chapter 2: The Basics of Record Keeping and Financial Statement Preparation: Balance Sheet Student: 1. The T-account looks like the letter T, with a horizontal line bisected by a vertical line. Increases

Profit or loss recorded to Retained Earnings

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Investing and Financing Decisions and the Accounting System

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

Bookkeeping (Explanation)

") Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30 Wages paid to laborers working in the manufacturing department is treated as an expense of: Cost of goods sold Administrative expense Selling expense

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30 Wages paid to laborers working in the manufacturing department is treated as an expense of: Cost of goods sold Administrative expense Selling expense

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

Financial Statement Overview. Introduction

Financial Statement Overview Bankers Insight Group, LLC Jeffery W. Johnson Introduction Financial Statement Analysis is the Cornerstone of a Bank s credit decision making process They report on an economic

Financial Statement Overview Bankers Insight Group, LLC Jeffery W. Johnson Introduction Financial Statement Analysis is the Cornerstone of a Bank s credit decision making process They report on an economic

Financial statements present the results of operations and the financial position of the company.

Accounting Fundamentals Lesson 1 1. The Financial Statements Financial statements present the results of operations and the financial position of the company. Publicly traded companies commonly prepare

Accounting Fundamentals Lesson 1 1. The Financial Statements Financial statements present the results of operations and the financial position of the company. Publicly traded companies commonly prepare

Learning Objectives. Chapter 5. Balance Sheet. Learning Objective 1, 2, 3. Liquidity. Chapter Overview. Balance Sheet and Statement of Cash Flows

Chapter 5 Balance Sheet and Statement of Cash Flows Campbell, Coca-Cola, American Airlines, Borders Learning Objectives 1. Explain uses, limitations of a balance sheet 2. Identify major classifications

Chapter 5 Balance Sheet and Statement of Cash Flows Campbell, Coca-Cola, American Airlines, Borders Learning Objectives 1. Explain uses, limitations of a balance sheet 2. Identify major classifications

UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS. Chapter 3

1 UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS Chapter 3 2 Learning Objectives (1 of 2) 1. Describe the content of the four basic financial statements and discuss the importance of financial

1 UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS Chapter 3 2 Learning Objectives (1 of 2) 1. Describe the content of the four basic financial statements and discuss the importance of financial

Not For Sale. Overview of Financial Statements FACMU14. Cengage Learning. All rights reserved. No distribution allowed without express authorization.

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Functions. The various financial statements are- Income Statement Balance Sheet

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018 Administrative Items Re-do Seating Chart for Sections 14 and 15 Reminder of correct usage of Self-Assessments Reminder of

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018 Administrative Items Re-do Seating Chart for Sections 14 and 15 Reminder of correct usage of Self-Assessments Reminder of

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Fin621 Online Quizzes & Papers GURU

1.If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an: A.. understatement of net income for the year by $7,500 B.. understatement of cost of merchandise sold

1.If the inventory shrinkage at the end of the year is overstated by $7,500, the error will cause an: A.. understatement of net income for the year by $7,500 B.. understatement of cost of merchandise sold

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Vocabulary

Accounting Vocabulary A. Accounting: planning, recording, analyzing and interpreting financial information. Accounting Equation: an equation showing the relationship among assets, liabilities, and owner

Accounting Vocabulary A. Accounting: planning, recording, analyzing and interpreting financial information. Accounting Equation: an equation showing the relationship among assets, liabilities, and owner

2000 Accounting II Page 1

2000 Accounting II Page 1 1. In accounting, the two types of equity are liabilities and owner's equity. 2. When journalizing, you are advised to go from left to right. 3. Transportation charges need to

2000 Accounting II Page 1 1. In accounting, the two types of equity are liabilities and owner's equity. 2. When journalizing, you are advised to go from left to right. 3. Transportation charges need to

How to Read Financial Statements 2015

CORPORATE LAW AND PRACTICE Course Handbook Series Number B-2157 How to Read Financial Statements 2015 Chair Chad Rucker To order this book, call (800) 260-4PLI or fax us at (800) 321-0093. Ask our Customer

CORPORATE LAW AND PRACTICE Course Handbook Series Number B-2157 How to Read Financial Statements 2015 Chair Chad Rucker To order this book, call (800) 260-4PLI or fax us at (800) 321-0093. Ask our Customer

Financial Statements, Forecasts, and Planning Chapter 6

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

Financial Statement Analysis

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

A Simple Model. Introduction to Financial Statements

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Welspun USA, Inc. Financial Report (000s omitted) March 31, 2018

March 31, 2018") Financial Report March 31, 2018 Contents Independent Auditor's Report 1 Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Stockholders' Equity 4 Statement of Cash Flows 5 Notes

Financial Report March 31, 2018 Contents Independent Auditor's Report 1 Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Stockholders' Equity 4 Statement of Cash Flows 5 Notes

1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

Accounting Cheat Sheet

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

MGT101- Financial Accounting

MIDTERM EXAMINATION MGT101- Financial Accounting Question No: 1 ( Marks: 1 ) - Please choose one Depreciation arises because of: Fall in the market value of an asset Fall in the value of money Physical

MIDTERM EXAMINATION MGT101- Financial Accounting Question No: 1 ( Marks: 1 ) - Please choose one Depreciation arises because of: Fall in the market value of an asset Fall in the value of money Physical

MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Question No: 1 ( Marks: 1 ) - Please choose one According to the double entry system of accounting, an account that obtains benefit is: Debit

MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Question No: 1 ( Marks: 1 ) - Please choose one According to the double entry system of accounting, an account that obtains benefit is: Debit

Practice Multiple Choice Questions

FINAL EXAM REVIEW The comprehensive final exam consists of 50 questions, approximately 2/3 of which are from chapters 10 through 12. The remaining questions are from chapters 1 through 9. The questions

FINAL EXAM REVIEW The comprehensive final exam consists of 50 questions, approximately 2/3 of which are from chapters 10 through 12. The remaining questions are from chapters 1 through 9. The questions

CHAPTER 2: FINANCIAL STATEMENTS AND THE ANNUAL REPORT

Using Financial Accounting Information The Alternative to Debits and Credits 9th Edition Porter Test Bank Full Download: http://testbanklive.com/download/using-financial-accounting-information-the-alternative-to-debits-and-credits-9th-

Using Financial Accounting Information The Alternative to Debits and Credits 9th Edition Porter Test Bank Full Download: http://testbanklive.com/download/using-financial-accounting-information-the-alternative-to-debits-and-credits-9th-

Shared By: Hira Ali. If u like me than raise your hand with me If not than raise ur standard That s about me! Time: 60 min Marks: 50

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Asslam O Alikum FIN621- Financial Statement Analysis mid term paper shared n rechecked by Hira Ali Remember Us In Your Prayers

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Asslam O Alikum FIN621- Financial Statement Analysis mid term paper shared n rechecked by Hira Ali Remember Us In Your Prayers

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Glossary of Terms NEL G-1

Glossary of Terms This glossary provides definitions for many terms in financial accounting 1 and refers readers back to those chapter sections in which the terms are discussed. If a good definition or

Glossary of Terms This glossary provides definitions for many terms in financial accounting 1 and refers readers back to those chapter sections in which the terms are discussed. If a good definition or

Talking Accounting Definitions

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2)

") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

CS101 Introduction of computing

FINAL TERM EXAMINATION MGT101- Financial Accounting (PAPER 1). Question No: 1 (Marks: 1 ) basic accounting principle/concept according to which Business is independent from its owner(s) is known as: Separate

FINAL TERM EXAMINATION MGT101- Financial Accounting (PAPER 1). Question No: 1 (Marks: 1 ) basic accounting principle/concept according to which Business is independent from its owner(s) is known as: Separate

FEAR out. Taking the FEAR of Financial Statement Analysis. Toni Drake, CCE TRM Financial Services, Inc.

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

Chapter III The Language of Accounting

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Rate = 1 n RV / C Where: RV = Residual Value C = Cost n = Life of Asset Calculate the rate if: Cost = 100,000

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

$100,000 Eag5. Eagle plans to purchase non-interest bearing investment securities once during the first year (e.g., common stock of other companies)

") Input Data For Eagle's Pro-Forma First-Year Accounting Entries Pro-forma Model: This Excel model provides pro-forma first-year financial statements, meaning statements that are estimated for planning purposes

Input Data For Eagle's Pro-Forma First-Year Accounting Entries Pro-forma Model: This Excel model provides pro-forma first-year financial statements, meaning statements that are estimated for planning purposes

CHAPTER 2 SOLUTIONS TO END OF CHAPTER MATERIAL QUESTIONS

CHAPTER 2 SOLUTIONS TO END OF CHAPTER MATERIAL QUESTIONS 1. The principal focus of financial accounting is to serve the needs of external decisionmakers. External decision makers need financial data about

CHAPTER 2 SOLUTIONS TO END OF CHAPTER MATERIAL QUESTIONS 1. The principal focus of financial accounting is to serve the needs of external decisionmakers. External decision makers need financial data about

Accounting Cycle. Ahmad Tariq Bhatti. The Fundamentals of Accounting. FCMA, FPA, MA (Economics), BSc Dubai, United Arab Emirates

, BSc Dubai, United Arab Emirates") Accounting Cycle The Fundamentals of Accounting Ahmad Tariq Bhatti FCMA, FPA, MA (Economics), BSc Dubai, United Arab Emirates Contents UNIT 1: ACCOUNTING CYCLE 7 1.1 Assumptions of financial accounting

Accounting Cycle The Fundamentals of Accounting Ahmad Tariq Bhatti FCMA, FPA, MA (Economics), BSc Dubai, United Arab Emirates Contents UNIT 1: ACCOUNTING CYCLE 7 1.1 Assumptions of financial accounting

Agribusiness Procedures

Agribusiness Procedures Financial Statements are Scorecards! Balance sheet A measure of the value of the business at one moment in time Should be prepared periodically Usually at end of fiscal monthly,

Agribusiness Procedures Financial Statements are Scorecards! Balance sheet A measure of the value of the business at one moment in time Should be prepared periodically Usually at end of fiscal monthly,

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations. Exercises

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Balance Sheet Terms. HAME513: Understanding Financial Statements Cornell School of Hotel Administration

Balance Sheet Terms This is a printer- friendly version of the content included in the "Balance Sheet Line by Line" activities. You may want to print this page for future reference. Assets Assets are used

Balance Sheet Terms This is a printer- friendly version of the content included in the "Balance Sheet Line by Line" activities. You may want to print this page for future reference. Assets Assets are used

AGENDA: STATEMENT OF CASH FLOWS

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

ASSETS Amount % Amount % LIABILITIES AND STOCKHOLDERS EQUITY Amount % Amount %

BALANCE SHEETS JUNE 30, 2010 AND 2009 (In Thousands of New Taiwan Dollars, Except Par Value) ASSETS Amount % Amount % LIABILITIES AND STOCKHOLDERS EQUITY Amount % Amount % CURRENT ASSETS CURRENT LIABILITIES

BALANCE SHEETS JUNE 30, 2010 AND 2009 (In Thousands of New Taiwan Dollars, Except Par Value) ASSETS Amount % Amount % LIABILITIES AND STOCKHOLDERS EQUITY Amount % Amount % CURRENT ASSETS CURRENT LIABILITIES

True / False Questions

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

1

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

Paper No:34 Solved by Chanda Rehman & ABr

Paper No:34 Solved by Chanda Rehman & ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one We can say that

Paper No:34 Solved by Chanda Rehman & ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one We can say that

A U D I T I N G P R O B L E M S

2011 NATIONAL CPA MOCK BOARD EXAMINATION In partnership with the Professional Review & Training Center, Inc. and Isla Lipana & Co. A U D I T I N G P R O B L E M S INSTRUCTIONS: Select the best answer for

2011 NATIONAL CPA MOCK BOARD EXAMINATION In partnership with the Professional Review & Training Center, Inc. and Isla Lipana & Co. A U D I T I N G P R O B L E M S INSTRUCTIONS: Select the best answer for

Chapter 3: Accounting and Finance

FIN 301 Class Notes Chapter 3: Accounting and Finance INTRODUCTION Accounting Function: Gathering, processing, and reporting data. End result is a set of four financial statements 1- Balance sheet 2-Income

FIN 301 Class Notes Chapter 3: Accounting and Finance INTRODUCTION Accounting Function: Gathering, processing, and reporting data. End result is a set of four financial statements 1- Balance sheet 2-Income

Mock Test 4 For DECEMBER 2016 The Institute of Chartered Accountants of India ABHIMANYYU AGARRWAL

Mock Test 4 For DECEMBER 2016 The Institute of Chartered Accountants of India ABHIMANYYU AGARRWAL CA - CPT Marks 60 Time 1 hrs. Every correct answer carries +1 mark each and 0.25 mark will be deducted

Mock Test 4 For DECEMBER 2016 The Institute of Chartered Accountants of India ABHIMANYYU AGARRWAL CA - CPT Marks 60 Time 1 hrs. Every correct answer carries +1 mark each and 0.25 mark will be deducted

Disclaimer. Accounting Illustrated Dictionary is not legal or tax advice. Information is to be used for educational purposes only.

Copyright and Legal 2015 John Gillingham, All Rights Reserved. AccountingPlay and Accounting Play are trademarks. Please go to AccountingPlay.com for more information. Disclaimer Accounting Illustrated

Copyright and Legal 2015 John Gillingham, All Rights Reserved. AccountingPlay and Accounting Play are trademarks. Please go to AccountingPlay.com for more information. Disclaimer Accounting Illustrated

Chapter Seventeen. Learning Objectives

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Corporate Finance. Prof. Dr. Frank Andreas Schittenhelm. Introduction to Financial Accounting. Prof. Dr. Frank Andreas Schittenhelm

Corporate Finance Introduction to Financial Accounting Corporate Finance slide 1 Literature Basic Literature Anthony/Hawkins/Merchant: Accounting, 11 th ed., McGraw-Hill Additional Literature Dyckman/Dukes/Davis:

Corporate Finance Introduction to Financial Accounting Corporate Finance slide 1 Literature Basic Literature Anthony/Hawkins/Merchant: Accounting, 11 th ed., McGraw-Hill Additional Literature Dyckman/Dukes/Davis:

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

Welspun USA, Inc. Financial Report March 31, 2017

Financial Report March 31, 2017 Contents Independent Auditor's Report 1 Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Stockholders' Equity 4 Statement of Cash Flows 5 Notes

Financial Report March 31, 2017 Contents Independent Auditor's Report 1 Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Stockholders' Equity 4 Statement of Cash Flows 5 Notes

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

Chapter 2: Financial Statements and the Annual Report

True / False 1. Financial statements are intended to tell the reader the value of a company. False LEARNING OBJECTIVES: FACC.PONO.13.02-01 - LO: 03-01 2. Accountants are the main reason financial statements

True / False 1. Financial statements are intended to tell the reader the value of a company. False LEARNING OBJECTIVES: FACC.PONO.13.02-01 - LO: 03-01 2. Accountants are the main reason financial statements

Statement of Cash Flows

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

CHAPTER 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Page 1 of 10 Ehab Abdou ( )

") Statement of Financial Position, also referred to as the balance sheet: 1. Reports assets, liabilities, and equity at a specific date. 2. Provides information about resources, obligations to creditors,

Statement of Financial Position, also referred to as the balance sheet: 1. Reports assets, liabilities, and equity at a specific date. 2. Provides information about resources, obligations to creditors,

Lesson 9: Breaking Down the Balance Sheet

Lesson 9: Breaking Down the Balance Sheet As we touched upon in previous lessons, a balance sheet is divided into three categories: Assets, Liabilities, and Owner s Equity. This lesson will go over each

Lesson 9: Breaking Down the Balance Sheet As we touched upon in previous lessons, a balance sheet is divided into three categories: Assets, Liabilities, and Owner s Equity. This lesson will go over each

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts

Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts") Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

Chart of Accounts ASSETS

This exam supplement includes a chart of accounts for all exam entries, BSE matrix for a fictitious company, financial statements from Dillards fiscal 2012 annual report, and Analysis Considerations Map

This exam supplement includes a chart of accounts for all exam entries, BSE matrix for a fictitious company, financial statements from Dillards fiscal 2012 annual report, and Analysis Considerations Map

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

AccountingCoach.com Cash Flow Statement

AccountingCoach.com Cash Flow Statement All underlined words are defined in the attached Glossary (Pages 40 46). Introduction to the Cash Flow Statement The official name for the cash flow statement is

AccountingCoach.com Cash Flow Statement All underlined words are defined in the attached Glossary (Pages 40 46). Introduction to the Cash Flow Statement The official name for the cash flow statement is

Accountings Summary OUTLINE

Accountings Summary OUTLINE 1. Accounting and Business Environment 2. Recording Business Transaction 3. The Adjusting Process 4. Completing the Accounting Cycle 5. Merchandising Operations 6. Accounting

Accountings Summary OUTLINE 1. Accounting and Business Environment 2. Recording Business Transaction 3. The Adjusting Process 4. Completing the Accounting Cycle 5. Merchandising Operations 6. Accounting

Statement of Cash Flows (SCF)

") Statement of Cash Flows (SCF) The statement of cash flows (SCF) or cash flow statement reports a corporation's significant cash inflows and outflows that occurred during an accounting period. This financial

Statement of Cash Flows (SCF) The statement of cash flows (SCF) or cash flow statement reports a corporation's significant cash inflows and outflows that occurred during an accounting period. This financial

MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50

Time: 60 min Marks: 50") MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50 Question No: 1 ( Marks: 1 ) - Please choose one An accounting system is used by a business to: Analyze transactions

MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50 Question No: 1 ( Marks: 1 ) - Please choose one An accounting system is used by a business to: Analyze transactions

EL PASO NATURAL GAS COMPANY, L.L.C. CONSOLIDATED FINANCIAL STATEMENTS For the Three and Six Months Ended June 30, 2013 and 2012 Unaudited

CONSOLIDATED FINANCIAL STATEMENTS For the Three and Six Months Ended June 30, 2013 and Unaudited TABLE OF CONTENTS Page Number Consolidated Financial Statements Consolidated Statements of Income and Comprehensive

CONSOLIDATED FINANCIAL STATEMENTS For the Three and Six Months Ended June 30, 2013 and Unaudited TABLE OF CONTENTS Page Number Consolidated Financial Statements Consolidated Statements of Income and Comprehensive

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

Ch.4 The Accounting Cycle for a Service Business (cont )

") Ch.4 The Accounting Cycle for a Service Business (cont ) Adjusting entries using T-accounts Work with a Worksheet for a service business Prepare Financial Statements Journalizing and posting adjusting

Ch.4 The Accounting Cycle for a Service Business (cont ) Adjusting entries using T-accounts Work with a Worksheet for a service business Prepare Financial Statements Journalizing and posting adjusting

Yasheng Group 2010 Financial Results

Yasheng Group 2010 Financial Results CONSOLIDATED BALANCE SHEETS 2010 2009 2008 ASSETS 849,454,265 739,630,043 736,213,299 Current assets: Cash and cash equivalents 10,116,750 8,010,017 7,880,338 Accounts

Yasheng Group 2010 Financial Results CONSOLIDATED BALANCE SHEETS 2010 2009 2008 ASSETS 849,454,265 739,630,043 736,213,299 Current assets: Cash and cash equivalents 10,116,750 8,010,017 7,880,338 Accounts

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

TRADITIONAL CLASSIFICATION OF ACCOUNTS. Abhimanyyu Agarrwal

TRADITIONAL CLASSIFICATION OF ACCOUNTS Abhimanyyu Agarrwal The classification of accounts according to the Traditional Approach is given below: Types of accounts Meaning Examples a. Personal Accounts These

TRADITIONAL CLASSIFICATION OF ACCOUNTS Abhimanyyu Agarrwal The classification of accounts according to the Traditional Approach is given below: Types of accounts Meaning Examples a. Personal Accounts These

BUSINESS FINANCE. Financial Statement Analysis. 1. Introduction to Financial Analysis. Copyright 2004 by Larry C. Holland

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And