Introduction to Accounting and Business

|

|

|

- Daniel Potter

- 5 years ago

- Views:

Transcription

1 Introduction to Accounting and Business Chapter 1 Prepared by: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine University

2 Learning Objectives 1. Describe the nature of a business, the role of accounting, and ethics in business. 2. Summarize the development of accounting principles and relate them to practice. 3. State the accounting equation and define each element of the equation. 4. Describe and illustrate how business transactions can be recorded in terms of the resulting change in the elements of the accounting equation. 5. Describe the financial statements of a corporation and explain how they interrelate. 6. Describe and illustrate the use of the ratio of liabilities to stockholders equity in evaluating a company s financial condition.

3 Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business.

4 LO 1 Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

5 LO 1 Nature of Business and Accounting The objective of most businesses is to earn a profit. Profit is the difference between the amounts received from customers for goods or services and the amounts paid for the inputs used to provide the goods or services.

6 LO 1 Types of Businesses Service Businesses Delta Air Lines The Walt Disney Company Merchandising Businesses Walmart Amazon.com Manufacturing Businesses Ford Motor Company Dell Service Transportation services Entertainment services Product General merchandise Internet books, music, videos Product Cars, trucks, vans Personal computers

7 LO 1 The Role of Accounting in Business Accounting can be defined as an information system that provides reports to users about the economic activities and condition of a business.

8 LO 1 The Role of Accounting in Business The process by which accounting provides information to users is as follows: Identify users. Assess users information needs. Design the accounting information system to meet users needs. Record economic data about business activities and events. Prepare accounting reports for users.

9 LO 1 The Role of Accounting in Business

10 LO 1 Managerial Accounting The area of accounting that provides internal users with information is called managerial accounting or management accounting. Managerial accountants employed by a business are employed in private accounting.

11 LO 1 Financial Accounting The area of accounting that provides external users with information is called financial accounting. The objective of financial accounting is to provide relevant and timely information for the decision-making needs of users outside of the business. General-purpose financial statements are one type of financial accounting report that is distributed to external users.

12 Role of Ethics in Accounting and Business The objective of accounting is to provide relevant, timely information for user decision making. Accountants must behave in an ethical manner so that the information they provide users will be trustworthy and, thus, useful for decision making. Ethics are moral principles that guide the conduct of individuals. LO 1

13 Role of Ethics in Accounting and Business LO 1 (continued)

14 Role of Ethics in Accounting and Business LO 1 (continued)

15 Role of Ethics in Accounting and Business LO 1 (concluded)

16 Role of Ethics in Accounting and Business LO 1 The answer to What went wrong for these companies? involves one or both of these factors. (Exhibit 2) Failure of individual character Firm culture of greed and ethical indifference

17 Role of Ethics in Accounting and Business LO 1

18 LO 1 Opportunities for Accountants Accountants and their staffs who provide services on a fee basis are said to be employed in public accounting. Accountants employed by a business firm or a not-for-profit organization are said to be employed in private accounting. Public accountants who have met a state s education, experience, and examination requirements may become Certified Public Accountants (CPAs).

19 LO 1 Opportunities for Accountants

20 Learning Objective 2 Summarize the development of accounting principles and relate them to practice.

21 Generally Accepted Accounting Principles Financial accountants follow generally accepted accounting principles (GAAP) in preparing reports. Within the U.S., the Financial Accounting Standards Board (FASB) has the primary responsibility for developing accounting principles. LO 2

22 Generally Accepted Accounting Principles The Securities and Exchange Commission (SEC), an agency of the U.S. government, has authority over the accounting and financial disclosures for companies whose shares of ownership (stock) are traded and sold to the public. Many countries outside the United States use generally accepted accounting principles adopted by the International Accounting Standards Board (IASB). LO 2

23 LO 2 Business Entity Concept Under the business entity concept, the activities of a business are recorded separately from the activities of its owners, creditors, or other businesses.

24 LO 2 Proprietorship A proprietorship is owned by one individual. 70% of business entities in the U.S. are proprietorships. They are easy and cheap to organize. Resources are limited to those of the owner. Used by small businesses.

25 LO 2 Partnership A partnership is similar to a proprietorship except that it is owned by two or more individuals. 10% of business organizations in the U.S. (combined with limited liability companies) are partnerships. Combines the skills and resources of more than one person.

26 LO 2 Corporation A corporation is organized under state or federal statutes as a separate legal taxable entity. Corporations generate 90% of business revenues. 20% of the business organizations in the U.S. are corporations. Ownership is divided into shares, called stock. (continued)

27 LO 2 Corporation A corporation is organized under state or federal statutes as a separate legal taxable entity. Can obtain large amounts of resources by issuing stocks. Used by large businesses.

28 LO 2 Limited Liability Company (LLC) A limited liability company (LLC) combines the attributes of a partnership and a corporation. 10% of business organizations in the U.S. (combined with partnerships). Often used as an alternative to a partnership. Has tax and legal liability advantages for owners.

29 LO 2 Cost Concept Under the cost concept, amounts are initially recorded in the accounting records at their cost or purchase price.

30 LO 2 Cost Concept Aaron Publishers purchased a building on February 20, 2010, for $150,000. Other amounts related to this purchased are shown on the next slide.

31 LO 2 Cost Concept Price listed by seller on January 1, 2010 $160,000 Aaron Publishers initial offer to buy on January 31, ,000 Purchase price on February 20, ,000 Estimated selling price on December 31, ,000 Assessed value for property taxes, December 31, ,000

32 LO 2 Objectivity Concept The objectivity concept requires that the amounts recorded in the accounting records be based on objective evidence. Only the final agreed-upon amount is objective enough to be recorded in the accounting records.

33 LO 2 Unit of Measure Concept The unit of measure concept requires that economic data be recorded in dollars.

34 EE 1-1

35 Learning Objective 3 State the accounting equation and define each element of the equation.

36 LO 3 The Accounting Equation The resources owned by a business are its assets. The rights of creditors are the debts of the business and are called liabilities. The rights of the owners are called owner s equity. The equation Assets = Liabilities + Owner s Equity is called the accounting equation.

37 LO 3 The Accounting Equation Assets = Liabilities + Owner s Equity The resources owned by a business

38 LO 3 The Accounting Equation Assets = Liabilities + Owner s Equity The rights of creditors are the debts of the business

39 LO 3 The Accounting Equation Assets = Liabilities + Owner s Equity The rights of the owners

40 EE 1-2

41 Learning Objective 4 Describe and illustrate how business transactions can be recorded in terms of the resulting change in the elements of the accounting equation.

42 LO 4 Business Transaction A business transaction is an economic event or condition that directly changes an entity s financial condition or its results of operations.

43 LO 4 Transaction A On November 1, 2011, Chris Clark deposited $25,000 in a bank account in the name of NetSolutions in return for shares of stock in the corporation.

44 Transaction A Stock issued to owners (stockholders), such as Chris Clark, is referred to as capital stock. The owner s equity in a corporation is called stockholders equity.

45 LO 4 Transaction B On November 5, 2011, NetSolutions paid $20,000 for the purchase of land as a future building site. The new amounts are called balances.

46 LO 4 Transaction C On November 10, 2011, NetSolutions purchased supplies for $1,350 and agreed to pay the supplier in the near future.

47 LO 4 Transaction C The liability created by a purchase on account is called an account payable. Items such as supplies that will be used in the business in the future are called prepaid expenses, which are assets.

48 LO 4 Transaction D On November 18, 2011, NetSolutions received cash of $7,500 for providing services to customers. A business earns money by selling goods or services to its customers. This amount is called revenue.

49 LO 4 Transaction D Revenue from providing services is recorded as fees earned. Revenue from the sale of merchandise is record as sales. Other examples of revenue include rent, which is recorded as rent revenue, and interest, which is recorded as interest revenue. An account receivable is a claim against a customer, which is an asset.

50 LO 4 Transaction E During the month, NetSolutions spent cash or used up other assets in earning revenue. Assets used in this process of earning revenue are called expenses.

51 LO 4 Transaction E On November 30, 2011, NetSolutions paid the following expenses: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

52 LO 4 Transaction F On November 30, 2011, NetSolutions paid creditors on account, $950.

53 LO 4 Transaction G On November 30, 2011, Chris Clark determined that the cost of supplies on hand at the end of the period was $550; therefore, the amount of supplies used amounted to $800 ($1,350 $550 = $800).

54 LO 4 Transaction H On November 30, 2011, NetSolutions paid $2,000 to stockholders as dividends. Dividends are distributions of earnings to stockholders.

55 LO 4 Summary

56 LO 4 You Should Note the Following: The effect of every transactions is an increase or a decrease in one or more of the accounting equation elements. The two sides of the accounting equations are always equal. The stockholders equity (owner s equity) is increased by amounts invested by stockholders (capital stock). (continued)

57 LO 4 You Should Note the Following: The stockholders equity (owner s equity) is increased by revenue and decreased by expenses. The stockholders equity (owner s equity) is decreased by dividends paid to stockholders. Retained earnings is the stockholders equity created from business operations through revenue and expense transactions.

58 LO 4 Types of Transactions Affecting Stockholders Equity

59 EE 1-3

60 Learning Objective 5 Describe the financial statements of a corporation and explain how they interrelate.

61 LO 5 Financial Statements After transactions have been recorded and summarized, reports are prepared for users. The accounting reports providing this information are called financial statements.

62 LO 5 Financial Statements

63 LO 5 Income Statement The income statement reports the revenues and expenses for a period of time, based on the matching concept. The matching concept is applied by matching the expenses incurred during a period with the revenue that those expenses generated. The excess of the revenue over the expenses is called net income, net profit, or earnings. If expenses exceed revenue, the excess is a net loss.

64 EE 1-4

65 LO 5 Retained Earnings Statement The retained earnings statement reports the changes in the retained earnings for a period of time. It is prepared after the income statement because the net income or net loss for the period must be reported in this statement.

66 LO 5 Retained Earnings Statement To illustrate, assume that NetSolutions earned net income of $4,155 and paid dividends of $2,000 during December. The following statement would be prepared.

67 EE 1-5

68 Income Statement LO 5 Net income is carried to the retained earnings statement (continued)

69 Retained Earnings Statement LO 5 From the income statement To the balance sheet

70 LO 5 Balance Sheet A balance sheet is a list of the assets, liabilities, and stockholders equity as of a specific date.

71 LO 5 Account Form The account form of a balance sheet lists the assets on the left and the liabilities and stockholders equity on the right. It resembles the basic format of the accounting equation.

72 LO 5 Balance Sheet This amount is compared to the net cash flow on the statement of cash flows. From the retained earnings statement

73 LO 5

74 LO 5 Statement of Cash Flows A statement of cash flows is a summary of the cash receipts and cash payments for a specific period of time. It consists of three sections: (1) operating activities (2) investing activities (3) financing activities

75 LO 5 Statement of Cash Flows This amount should match Cash on the balance sheet.

76 Cash Flows from Operating Activities The cash flows from operating activities section reports a summary of cash receipts and cash payments from operations. LO 5

77 Cash Flows from Investing Activities The cash flows from investing activities section reports the cash transactions for the acquisition and sale of relatively permanent assets. LO 5

78 Cash Flows from Financing Activities The cash flows from financing activities section reports the cash transactions related to cash investments by the owner, borrowings, and withdrawals by the owner. LO 5

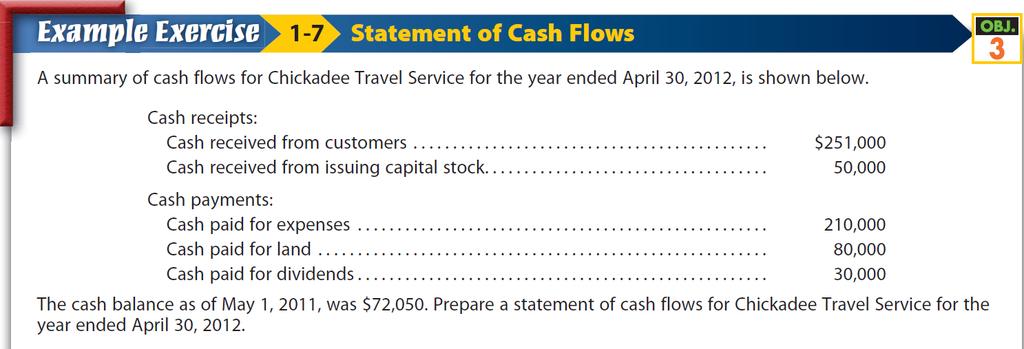

79 EE 1-7

80 EE 1-7

81 Interrelationships Among Financial Statements LO 5 Income Statement and Retained Earnings Statement Net income or net loss reported on the income statement is also reported on the retained earnings statement as either an addition (net income) to or deduction (net loss) from the beginning retained earnings.

82 Interrelationships Among Financial Statements LO 5 In Exhibit 6, NetSolutions net income of $3,050 for November is added to the beginning retained earnings on November 1, 2011, in the retained earnings statement.

83 Interrelationships Among Financial Statements LO 5 Retained Earnings Statement and and Balance Sheet Retained earnings at the end of the period reported on the retained earnings statement is also reported on the balance sheet as retained earnings.

84 Interrelationships Among Financial Statements LO 5 In Exhibit 6, NetSolutions retained earnings of $1,050 as of November 30, 2011, on the retained earnings statement also appears on the November 30, 20l1, balance sheet as retained earnings.

85 Interrelationships Among Financial Statements LO 5 Balance Sheet and Statement of Cash Flows The cash reported on the balance sheet is also reported as the end-of-period cash on the statement of cash flows.

86 Interrelationships Among Financial Statements LO 5 In Exhibit 6, cash of $5,900 reported on the balance sheet as of November 30, 2011, is also reported on the November statement of cash flows as the end-of-period cash.

87 Learning Objective 6 Describe and illustrate the use of the ratio of liabilities to stockholders equity in evaluating a company s financial condition.

88 Ratio of Liabilities to Stockholders Equity LO 6 Ratio of Liabilities to Stockholders Equity = Total Liabilities Total Stockholders Equity Ratio of Liabilities to Stockholders Equity = $400 $26,050 = 0.015

89 EE 1-8

90 Introduction to Accounting and Business The End Prepared by: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine University

o Chapter 1: INTRODUCTION TO ACCOUNTING

ACCOUNTING 2-MANAGERIAL ACCOUNTING o Chapter 1: INTRODUCTION TO ACCOUNTING AND BUSINESS Teacher Version Learning Objectives 1. Describe the nature of a business and the role of accounting and ethics in

ACCOUNTING 2-MANAGERIAL ACCOUNTING o Chapter 1: INTRODUCTION TO ACCOUNTING AND BUSINESS Teacher Version Learning Objectives 1. Describe the nature of a business and the role of accounting and ethics in

PENGANTAR AKUNTANSI. Accounting in Action. Rina Y. Asmara SE, MM, Ak, CA. Modul ke: 01Fakultas Ekonomi dan Bisnis. Program Studi S1Manajemen

Modul ke: 01Fakultas Ekonomi dan Bisnis PENGANTAR AKUNTANSI Accounting in Action Rina Y. Asmara SE, MM, Ak, CA Program Studi S1Manajemen 1 Types of Businesses Service Business Delta Air Lines The Walt

Modul ke: 01Fakultas Ekonomi dan Bisnis PENGANTAR AKUNTANSI Accounting in Action Rina Y. Asmara SE, MM, Ak, CA Program Studi S1Manajemen 1 Types of Businesses Service Business Delta Air Lines The Walt

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

CHAPTER 1. AP Photo/Paul Sakuma Introduction to Accounting and Business. Google W

CHAPTER 1 AP Photo/Paul Sakuma Introduction to Accounting and Business Google W hen two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer, and fireworks

CHAPTER 1 AP Photo/Paul Sakuma Introduction to Accounting and Business Google W hen two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer, and fireworks

Google. Introduction to Accounting and Business CHAPTER 1

CHAPTER 1 AP Photo/Paul Sakuma Google Introduction to Accounting and Business W hen two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer, and fireworks

CHAPTER 1 AP Photo/Paul Sakuma Google Introduction to Accounting and Business W hen two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer, and fireworks

When two teams pair up for a game of football, there

Chapter 01.qxd 2/15/08 12:03 AM Page 1 C H A P T E R 1 Introduction to Accounting and Business When two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer,

Chapter 01.qxd 2/15/08 12:03 AM Page 1 C H A P T E R 1 Introduction to Accounting and Business When two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer,

Presented by: Meredith Mostochuk, CBA

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Printed in USA Financial Accounting 13e. 2014, 2012 South-Western, Cengage Learning

This is an electronic version of the print textbook. Due to electronic rights restrictions, some third party content may be suppressed. Editorial review has deemed that any suppressed content does not

This is an electronic version of the print textbook. Due to electronic rights restrictions, some third party content may be suppressed. Editorial review has deemed that any suppressed content does not

Related Download: Solutions Manual Accounting 26th Edition Warren Reeve Duchac

Test Bank Accounting 26th Edition Warren Reeve Duchac. Completed download: https://testbankarea.com/download/accounting-26th-edition-warren-reeve-duchactest-bank/ Related Download: Solutions Manual Accounting

Test Bank Accounting 26th Edition Warren Reeve Duchac. Completed download: https://testbankarea.com/download/accounting-26th-edition-warren-reeve-duchactest-bank/ Related Download: Solutions Manual Accounting

Copyright 2009 The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12

The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12 Introduction Accounting Organizations and Basic Precepts For many students, Principles of Accounting is their first taste

The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12 Introduction Accounting Organizations and Basic Precepts For many students, Principles of Accounting is their first taste

Learning Objectives. LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose.

Learning Objectives LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose. Lesson 1-1 The Role of Accounting LO1 Data must be recorded and

Learning Objectives LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose. Lesson 1-1 The Role of Accounting LO1 Data must be recorded and

Accounting 1A Class Notes Chapter 1 Introduction to Accounting and Business

Types of Business Service Business - Lawyer, Consultant, Doctor Merchandiser Best Buy, Wal-Mart Manufacturer - Mattel, Coca Cola Purpose of Accounting Provide Financial Information for decision making

Types of Business Service Business - Lawyer, Consultant, Doctor Merchandiser Best Buy, Wal-Mart Manufacturer - Mattel, Coca Cola Purpose of Accounting Provide Financial Information for decision making

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Chapter 1 Accounting and the Business Environment

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Understanding Accounting & Financial Statements

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

Chapter 01 - Introducing Accounting in Business. Chapter Outline

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

ACCOUNTING CONCEPTS AND PROCEDURES

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

Accounting consists of three basic activities it

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Accounting Definition

Accounting Definition MINSK MINSK INNOVATION UNIVERSITY Oct, 2015 Learning Objectives After this lecture, you should be able to: 1. Define accounting. 2. Describe the primary forms of business organization.

Accounting Definition MINSK MINSK INNOVATION UNIVERSITY Oct, 2015 Learning Objectives After this lecture, you should be able to: 1. Define accounting. 2. Describe the primary forms of business organization.

Chapter 1 Introduction to Accounting and Business Study Guide. Do You Know?

Chapter 1 Introduction to Accounting and Business Study Guide Do You Know? Learning Objective 1: Describe the nature of a business and the role of accounting and ethics in business. How to distinguish

Chapter 1 Introduction to Accounting and Business Study Guide Do You Know? Learning Objective 1: Describe the nature of a business and the role of accounting and ethics in business. How to distinguish

Accounting in Action

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

IN ACTION. Chapter 1 CHAPTER STUDY OBJECTIVES PREVIEW OF CHAPTER 1. The Navigator ACCOUNTING IN ACTION

Chapter 1 ACCOUNTING IN ACTION CHAPTER STUDY OBJECTIVES The Navigator Scan Study Objectives Read Preview Read Chapter Review Work Demonstration Problem Answer True-False Statements Answer Multiple-Choice

Chapter 1 ACCOUNTING IN ACTION CHAPTER STUDY OBJECTIVES The Navigator Scan Study Objectives Read Preview Read Chapter Review Work Demonstration Problem Answer True-False Statements Answer Multiple-Choice

Copyright 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-1 Accounting What the Numbers Mean CHAPTER 1: Accounting Present and Past Marshall, McManus, and Viele 11th Edition 1-2 Learning Objectives After studying this chapter you should understand and be able

1-1 Accounting What the Numbers Mean CHAPTER 1: Accounting Present and Past Marshall, McManus, and Viele 11th Edition 1-2 Learning Objectives After studying this chapter you should understand and be able

The Role of Accountants and Accounting Information

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Chapter 11. Corporations: Organization, Stock Transactions, and Dividends. Student Version

Corporations: Organization, Stock Transactions, and Dividends Chapter 11 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas

Corporations: Organization, Stock Transactions, and Dividends Chapter 11 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas

" Annual report: the main method that management uses to report the results of the company s activities during the year.

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment. Learning Objective 1-1

Chapter 1 Accounting and the Business Environment. Learning Objective 1-1") Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Module 1 Exhibits and Key terms

Exhibit 1... 2 Exhibit 2... 3 A. Income Statement... 3 C. Balance Sheet... 3 Transactions affecting only the balance sheet... 4 1a. Owners invested cash... 4 2a. Borrowed money... 4 3a. Purchased trucks

Exhibit 1... 2 Exhibit 2... 3 A. Income Statement... 3 C. Balance Sheet... 3 Transactions affecting only the balance sheet... 4 1a. Owners invested cash... 4 2a. Borrowed money... 4 3a. Purchased trucks

Fill-in-the-Blank Equations. Exercises

Chapter 1 Introduction to Accounting and Business Study Guide Solutions Fill-in-the-Blank Equations 1. Equity 2. Net income or net loss 3. Net income (or subtract if a net loss) 4. Cash flows from investing

Chapter 1 Introduction to Accounting and Business Study Guide Solutions Fill-in-the-Blank Equations 1. Equity 2. Net income or net loss 3. Net income (or subtract if a net loss) 4. Cash flows from investing

Reporting Financial Information

Learning Objectives LO1 Prepare an income statement for a service business. LO2 Calculate and analyze financial ratios using income statement amounts. Lesson 7-1 Reporting Financial Information LO1 The

Learning Objectives LO1 Prepare an income statement for a service business. LO2 Calculate and analyze financial ratios using income statement amounts. Lesson 7-1 Reporting Financial Information LO1 The

Chapter 1 Introduction to Accounting and Business Study Guide. Do You Know?

Chapter 1 Introduction to Accounting and Business Study Guide Do You Know? Learning Objective 1: Describe the nature of a business and the role of accounting and ethics in business. How to distinguish

Chapter 1 Introduction to Accounting and Business Study Guide Do You Know? Learning Objective 1: Describe the nature of a business and the role of accounting and ethics in business. How to distinguish

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

3) Managerial accounting focuses on information for external decision makers. Answer: FALSE

Managerial accounting focuses on information for external decision makers. Answer: FALSE") Horngren's Financial & Managerial Accounting, 4e (Nobles) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Horngren's Financial & Managerial Accounting, 4e (Nobles) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

CHAPTER 3 THE ADJUSTING PROCESS

1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and expenses are reported in the period in which cash is paid. b. Under accrual-basis accounting, revenues

1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and expenses are reported in the period in which cash is paid. b. Under accrual-basis accounting, revenues

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank Link download full: http://testbankcollection.com/download/financial-andmanagerialaccounting-information-for-decisions-4th-edition-by-wild-test-bank/

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank Link download full: http://testbankcollection.com/download/financial-andmanagerialaccounting-information-for-decisions-4th-edition-by-wild-test-bank/

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

Analyzing the Accounting Equation

Learning Objectives LO1 Show the relationship between the accounting equation and a T account. LO2 Identify the debit and credit side, the increase and decrease side, and the balance side of various accounts.

Learning Objectives LO1 Show the relationship between the accounting equation and a T account. LO2 Identify the debit and credit side, the increase and decrease side, and the balance side of various accounts.

Accounting Principles

Accounting Principles The Accounting Process Identification Select Economic Events/Transactions Analyze and Interpret for Users Recording Communication Record, Classify, and Summarize Preparation of Accounting

Accounting Principles The Accounting Process Identification Select Economic Events/Transactions Analyze and Interpret for Users Recording Communication Record, Classify, and Summarize Preparation of Accounting

Four Basic Financial Statements. Income Statement Statement of Retained Earnings Balance Sheet Statement of Cash Flows. McGraw-Hill/Irwin Slide 1

Four Basic Financial Statements Income Statement Statement of Retained Earnings Balance Sheet Statement of Cash Flows McGraw-Hill/Irwin Slide 1 The Four Basic Financial Statements 1. On a company s INCOME

Four Basic Financial Statements Income Statement Statement of Retained Earnings Balance Sheet Statement of Cash Flows McGraw-Hill/Irwin Slide 1 The Four Basic Financial Statements 1. On a company s INCOME

CHAPTER1. Accounting in Action. PreviewofCHAPTER1. What is Accounting?

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

Chapter 10. Current Liabilities and Payroll. Student Version

Current Liabilities and Payroll Chapter 10 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas Cloud Professor Emeritus

Current Liabilities and Payroll Chapter 10 Student Version These slides should be viewed using the presentation mode (left click your mouse on the icon). Prepared by: C. Douglas Cloud Professor Emeritus

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File 1.0-1 By taking accounting classes, the student is learning the language of business. Answer: True LO: 1-0 EOC Ref: Vocabulary

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File 1.0-1 By taking accounting classes, the student is learning the language of business. Answer: True LO: 1-0 EOC Ref: Vocabulary

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Job Ready Assessment Blueprint

Blueprint Test Code: 2120 / Version: 01 Financial and Managerial Accounting (Written Only) Specific Competencies and Skills Tested in this Assessment: Journalizing Understand the theory of double entry

Blueprint Test Code: 2120 / Version: 01 Financial and Managerial Accounting (Written Only) Specific Competencies and Skills Tested in this Assessment: Journalizing Understand the theory of double entry

Aiden Jackson stared at the list the banker had

1 Accounting and the Business Environment Coffee, Anyone? Aiden Jackson stared at the list the banker had given him during their meeting. Business plan, cash flow projections, financial statements, tax

1 Accounting and the Business Environment Coffee, Anyone? Aiden Jackson stared at the list the banker had given him during their meeting. Business plan, cash flow projections, financial statements, tax

Financial Statements. M. En C. Eduardo Bustos Farías

Understanding 1 Financial Statements M. En C. Eduardo Bustos Farías 2 Objectives 1. Define the elements of financial statements. 3 Balance Sheet It It also is is called a statement of of financial position.

Understanding 1 Financial Statements M. En C. Eduardo Bustos Farías 2 Objectives 1. Define the elements of financial statements. 3 Balance Sheet It It also is is called a statement of of financial position.

Chapter Seventeen. Learning Objectives

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

1-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

Processing Accounting Information

2 Processing Accounting Information PAst Chapter 1 described the environment of financial accounting. It also introduced the financial statements and basic analysis of them. PResent This chapter explains

2 Processing Accounting Information PAst Chapter 1 described the environment of financial accounting. It also introduced the financial statements and basic analysis of them. PResent This chapter explains

16 Statement of Cash Flows

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

Fill-in-the-Blank Equations. Exercises

Chapter 1 Introduction to Accounting and Business Study Guide Solutions 1. Owner s Equity 2. Net Income or Net Loss 3. Net Income (or subtract if a Net Loss) 4. Cash Flows from Investing Activities 5.

Chapter 1 Introduction to Accounting and Business Study Guide Solutions 1. Owner s Equity 2. Net Income or Net Loss 3. Net Income (or subtract if a Net Loss) 4. Cash Flows from Investing Activities 5.

Chapter 1. Accounting in Business QUESTIONS

Chapter 1 Accounting in Business QUESTIONS 1. The purpose of accounting is to provide decision makers with relevant and reliable information to help them make better decisions. Examples include information

Chapter 1 Accounting in Business QUESTIONS 1. The purpose of accounting is to provide decision makers with relevant and reliable information to help them make better decisions. Examples include information

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for:

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for: A. Option a B. Option b C. Option c D. Option d 2. What is the primary purpose of financial

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for: A. Option a B. Option b C. Option c D. Option d 2. What is the primary purpose of financial

Introduction Cengage Learning. All Rights Reserved.

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Intuit Inc. Whether you realize it or not, you likely interact with. Accounting Systems CHAPTER 5

CHAPTER 5 Pixland/Jupiter Images Accounting Systems Intuit Inc. Whether you realize it or not, you likely interact with accounting systems. For example, your bank statement is a type of accounting system.

CHAPTER 5 Pixland/Jupiter Images Accounting Systems Intuit Inc. Whether you realize it or not, you likely interact with accounting systems. For example, your bank statement is a type of accounting system.

Chapter 1: Business Decisions and Financial Accounting

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Accounting in Action. Chapter 1. Learning Objectives. After studying this chapter, you should be able to:

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

SAMPLE EXAM - CHAPTER 1

SAMPLE EXAM - CHAPTER 1 Name: Date: 1. General-purpose financial statements are the product of A) financial accounting. B) managerial accounting. C) both financial and managerial accounting. D) neither

SAMPLE EXAM - CHAPTER 1 Name: Date: 1. General-purpose financial statements are the product of A) financial accounting. B) managerial accounting. C) both financial and managerial accounting. D) neither

Chapter 1: Accounting and the Business Environment

Chapter 1: Accounting and the Business Environment 1.1-1 Accounting is the information system that measures business activity, processes the data into reports, and communicates the results to decisions

Chapter 1: Accounting and the Business Environment 1.1-1 Accounting is the information system that measures business activity, processes the data into reports, and communicates the results to decisions

CHAPTER 2 ANALYZING TRANSACTIONS DISCUSSION QUESTIONS

Financial and Managerial Accounting 14th Edition Warren SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/financial-managerial-accounting-14thedition-warren-solutions-manual/

Financial and Managerial Accounting 14th Edition Warren SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/financial-managerial-accounting-14thedition-warren-solutions-manual/

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

A Review of the Accounting Cycle

CHAPTER 2 A Review of the Accounting Cycle LEARNING OBJECTIVES 1. Identify and explain the basic steps in the accounting process (accounting cycle). Analyze business documents, Journalize transactions,

CHAPTER 2 A Review of the Accounting Cycle LEARNING OBJECTIVES 1. Identify and explain the basic steps in the accounting process (accounting cycle). Analyze business documents, Journalize transactions,

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Introduction to Financial Accounting

READING MATERIAL FOR WEEK 1 Introduction to Financial Accounting 1.1 Introduction All organizations, irrespective of the legal status proprietorship, partnership, incorporated company, statutory corporation

READING MATERIAL FOR WEEK 1 Introduction to Financial Accounting 1.1 Introduction All organizations, irrespective of the legal status proprietorship, partnership, incorporated company, statutory corporation

STATEMENT OF CASH FLOWS

Chapter Seventeen STATEMENT OF CASH FLOWS LEARNING OBJECTIVES After reading this chapter, you should be able to Explain why investors and others are interested in cash flows. State the three types of activities

Chapter Seventeen STATEMENT OF CASH FLOWS LEARNING OBJECTIVES After reading this chapter, you should be able to Explain why investors and others are interested in cash flows. State the three types of activities

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Test Bank College Accounting A Practical Approach 13th Edition Jeffrey Slater

Test Bank College Accounting A Practical Approach 13th Edition Jeffrey Slater Instant download and all chapters TESK BANK College Accounting A Practical Approach 13th Edition Jeffrey Slater https://testbankdata.com/download/test-bank-college-accounting-practicalapproach-13th-edition-jeffrey-slater/

Test Bank College Accounting A Practical Approach 13th Edition Jeffrey Slater Instant download and all chapters TESK BANK College Accounting A Practical Approach 13th Edition Jeffrey Slater https://testbankdata.com/download/test-bank-college-accounting-practicalapproach-13th-edition-jeffrey-slater/

Chapter 2: Overview. Analyzing and Recording Business Transactions

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

1. A business entity's accounting system creates financial accounting reports which are provided to

Chapter 01 Financial Statements and Business Decisions True / False Questions 1. A business entity's accounting system creates financial accounting reports which are provided to external decision makers.

Chapter 01 Financial Statements and Business Decisions True / False Questions 1. A business entity's accounting system creates financial accounting reports which are provided to external decision makers.

HORNGREN'S ACCOUNTING - Eleventh Edition

1. What is accounting? 2. Briefly describe the two major fields of accounting. 3. Describe the various types of individuals who use accounting information and how they use that information to make important

1. What is accounting? 2. Briefly describe the two major fields of accounting. 3. Describe the various types of individuals who use accounting information and how they use that information to make important

Financial Accounting

Financial Accounting Roger H. Hermanson, Ph.D., CPA Regents' Professor of Accounting Ernst & Whinney Professor School of Accountancy Georgia State University James Don Edwards^ Ph.D., CPA J. M. Tull Professor

Financial Accounting Roger H. Hermanson, Ph.D., CPA Regents' Professor of Accounting Ernst & Whinney Professor School of Accountancy Georgia State University James Don Edwards^ Ph.D., CPA J. M. Tull Professor

Accounting: Decision Making by the Numbers BUSN

Accounting: Decision Making by the Numbers What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally accepted accounting principles?

Accounting: Decision Making by the Numbers What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally accepted accounting principles?

ACCOUNTING AND THE FINANCIAL STATEMENTS

1 ACCOUNTING AND THE FINANCIAL STATEMENTS DISCUSSION QUESTIONS 1. Accounting is a system for identifying, measuring, recording, and communicating financial information about an organization s activities

1 ACCOUNTING AND THE FINANCIAL STATEMENTS DISCUSSION QUESTIONS 1. Accounting is a system for identifying, measuring, recording, and communicating financial information about an organization s activities

Topic 1! The Accounting Equation and The effect of Economic Transactions!

Topic 1 The Accounting Equation and The effect of Economic Transactions Accounting in Action : Knowing the Numbers : In business, accounting and financial statement are the means for communicating the

Topic 1 The Accounting Equation and The effect of Economic Transactions Accounting in Action : Knowing the Numbers : In business, accounting and financial statement are the means for communicating the

CHAPTER 1. Accounting and the Business Environment. Chapter Overview

CHAPTER 1 Accounting and the Business Environment Chapter Overview The chapter begins with an introduction to accounting. The text discusses how accounting information is needed by various users individuals,

CHAPTER 1 Accounting and the Business Environment Chapter Overview The chapter begins with an introduction to accounting. The text discusses how accounting information is needed by various users individuals,

Introductory Financial Accounting

West Chester University Digital Commons @ West Chester University Accounting Text Books Accounting 2-20-2015 Introductory Financial Accounting Anthony J. Cataldo II West Chester University of Pennsylvania,

West Chester University Digital Commons @ West Chester University Accounting Text Books Accounting 2-20-2015 Introductory Financial Accounting Anthony J. Cataldo II West Chester University of Pennsylvania,

Do you subscribe to any magazines? Most of us subscribe

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Understanding Financial Data

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Understanding Presented by Brenda M. Clarke, CPA/ABV/CFF, CVA FM25 5/24/2016 2:30 PM - 3:30 PM The handouts and presentations attached

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Understanding Presented by Brenda M. Clarke, CPA/ABV/CFF, CVA FM25 5/24/2016 2:30 PM - 3:30 PM The handouts and presentations attached

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Chapter 1 MULTIPLE CHOICE

Chapter 1 Objectives: 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue, expenses, and withdrawals expand the basic

Chapter 1 Objectives: 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue, expenses, and withdrawals expand the basic

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018 8:54 PM Financial Accounting Environment Primary Focus of financial accounting is on the information needs

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018 8:54 PM Financial Accounting Environment Primary Focus of financial accounting is on the information needs

Key Learning: Students will review basic accounting concepts learned in the first level course.

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

After completing Chapter 2, your students should be able to answer these questions:

Solution Manual for Financial Accounting A Business Process Approach 3rd Edition by Reimers Link full download solution manual: http://testbankcollection.com/download/solution-manual-for-financial-accountinga-business-process-approach-3rd-edition-by-reimers/

Solution Manual for Financial Accounting A Business Process Approach 3rd Edition by Reimers Link full download solution manual: http://testbankcollection.com/download/solution-manual-for-financial-accountinga-business-process-approach-3rd-edition-by-reimers/

CITY ARTS CENTER, INC. June 30, 2010

June 30, 2010 June 30, 2010 Audited Financial Statements Independent Auditors Report... 1 Statement of Financial Position--Modified Cash Basis... 2 Statement of Activities--Modified Cash Basis... 3 Statement

June 30, 2010 June 30, 2010 Audited Financial Statements Independent Auditors Report... 1 Statement of Financial Position--Modified Cash Basis... 2 Statement of Activities--Modified Cash Basis... 3 Statement

1.1 Generally Accepted Accounting Principles (GAAP) 1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation

1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation") 1. General Topics 1.1 Generally Accepted Accounting Principles (GAAP) 1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation 1.3 The Accounting Cycle 1.4 Business Ethics 1.5 Purpose

1. General Topics 1.1 Generally Accepted Accounting Principles (GAAP) 1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation 1.3 The Accounting Cycle 1.4 Business Ethics 1.5 Purpose

Accounting Concepts and Procedures

1 Accounting Concepts and Procedures LEARNING OBJECTIVES DID YOU KNOW? By 2007 Best Buy employed 10,000 geek squad agents, 3,000 home theatre installers, and 3,000 vehicle installers. Revenues and net

1 Accounting Concepts and Procedures LEARNING OBJECTIVES DID YOU KNOW? By 2007 Best Buy employed 10,000 geek squad agents, 3,000 home theatre installers, and 3,000 vehicle installers. Revenues and net

CHAPTER 8: Accounting

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

TH E ACCO U NTI NG LEARNING OBJECTIVES. Needed: A Reliable Information System. After studying this chapter, you should be able to:

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting