PENGANTAR AKUNTANSI. Accounting in Action. Rina Y. Asmara SE, MM, Ak, CA. Modul ke: 01Fakultas Ekonomi dan Bisnis. Program Studi S1Manajemen

|

|

|

- Estella Waters

- 6 years ago

- Views:

Transcription

1 Modul ke: 01Fakultas Ekonomi dan Bisnis PENGANTAR AKUNTANSI Accounting in Action Rina Y. Asmara SE, MM, Ak, CA Program Studi S1Manajemen

2 1 Types of Businesses Service Business Delta Air Lines The Walt Disney Company Service Transportation services Entertainment services

3 1 Types of Businesses Merchandising Business Wal-Mart Amazon.com Product General merchandise Internet books, music, videos

4 1 Types of Businesses Manufacturing Business General Motors Corp. Dell Inc. Product Cars, trucks, vans Personal computers

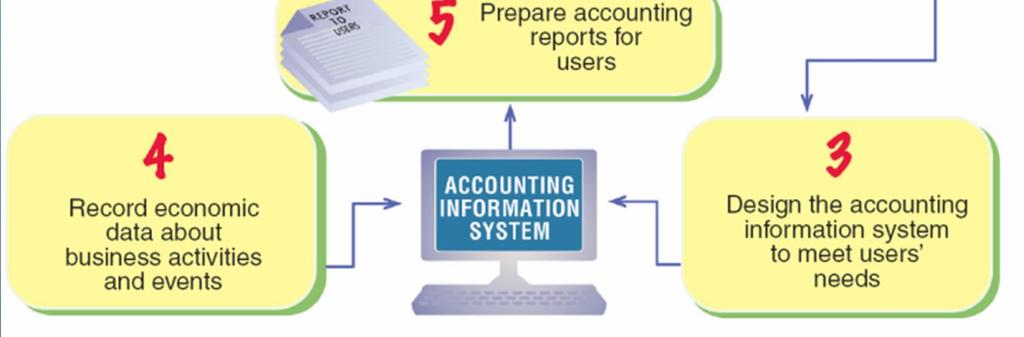

5 1 The Role of Accounting in Business Accounting can be defined as an information system that provides reports to users about the economic activities and condition of a business.

6 1 The process by which accounting provides information to users is as follows: Identify users. Assess users informational needs. Design the accounting information system to meet users needs. Record economic data about business activities and events. Prepare accounting reports for users.

7 1 Exhibit 1 Users of Accounting Information

8 1 Managerial Accounting The area of accounting that provides internal users with information is called managerial accounting. The objective of managerial accounting is to provide relevant and timely information for managers and employees decision-making needs.

9 1 Financial Accounting The area of accounting that provides external users with information is called financial accounting. The objective of financial accounting is to provide relevant and timely information for the decision-making needs of users outside of the business.

10 1 Role of Ethics in Accounting and Business Ethics are moral principles that guide the conduct of individuals.

11 1 The answer to What went wrong for these companies? (Exhibit 2) involves one or both of these factors. Failure of individual character Firm culture of greed and ethical indifference

12 1 Opportunities for Accountants Accountants employed by a business firm or a not-for-profit organization are said to be employed in private accounting. Accountants and their staff who provide services on a fee basis are said to be employed in public accounting.

13 3 The Accounting Equation Assets = Liabilities + Owner s Equity The resources owned by a business

14 3 The Accounting Equation Assets = Liabilities + Owner s Equity The rights of the creditors are the debts of the business.

15 3 The Accounting Equation Assets = Liabilities + Owner s Equity The rights of the owners

16 4 Business Transaction A business transaction is an economic event or condition that directly changes an entity s financial condition or its results of operations.

17 4 Transaction A On November 1, 2009, Chris Clark deposits $25,000 in a bank account in the name of NetSolutions in return for shares of stock in the corporation.

18 4 Transaction A (continued) Assets = CASH a. = 25,000 Stockholders Equity Share Capital-Ordinary 25,000

19 4 Transaction B On November 5, 2009, NetSolutions paid $20,000 for the purchase of land as a future building site.

20 4 Transaction B (continued) Assets = Stockholders Equity CASH + LAND Bal. 25,000 b. 20, ,000 = Share Capital-Ordinary 25,000 Bal. 5,000 20,000 25,000

21 4 Transaction C On November 10, 2009, NetSolutions purchased supplies for $1,350 and agreed to pay the supplier in the near future.

22 4 Transaction C (continued) Assets = Stockholders Liabilities + Equity ACCOUNTS CAPITAL CASH + SUPPLIES + LAND PAYABLE + STOCK = Bal. 5,000 20,000 25,000 c. +1,350 +1,350 Bal. 5,000 1,350 20,000 1,350 25,000

23 4 Beginning with Transaction D the asset section will be shown first, then the liabilities and stockholders equity will be shown in the following slide.

24 4 Transaction D On November 18, 2009, NetSolutions received cash of $7,500 for providing services to customers. A business earns money by selling goods or services to its customers. This amount is called Revenue.

25 4 Transaction D (continued) Assets CASH + SUPPLIES + LAND Bal. 5,000 1,350 20,000 d. +7,500 Bal. 12, ,000

26 4 Transaction D (continued) Liabilities + Stockholders Equity ACCOUNTS CAPITAL FEES PAYABLE + STOCK + EARNED Bal. 1,350 25,000 d. +7,500 Bal. 1,350 25,000 7,500

27 4 Expenses During the month, NetSolutions spent cash or used up other assets in earning revenue. Assets used in this process of earning revenue are called expenses.

28 4 Transaction E On November 30, 2009, NetSolutions paid the following expenses during the month: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

29 4 Transaction E (continued) Assets CASH + SUPPLIES + LAND Bal. 12,500 1,350 20,000 e. 3,650 Bal. 8, ,000

30 4 Transaction E (continued) Liabilities + Stockholders Equity ACCOUNTS CAPITAL FEES WAGES RENT UTIL. MISC. PAYABLE + STOCK + EARNED EXP. EXP. EXP. EXP. Bal. 1,350 25,000 7,500 e. 2, Bal. 1,350 25,000 7,500 2,

31 4 Transaction F On November 30, 2009, NetSolutions paid creditors on account, $950.

32 4 Transaction F (continued) Assets CASH + SUPPLIES + LAND Bal. 8,850 1,350 20,000 f. 950 Bal. 7, ,000

33 4 Transaction F (continued) Liabilities + Stockholders Equity ACCOUNTS CAPITAL FEES WAGES RENT UTIL. MISC. PAYABLE + STOCK + EARNED EXP. EXP. EXP. EXP. Bal. 1,350 25,000 7,500 f. 950 Bal ,000 7,500 2,

34 4 Transaction G On November 30, 2009, Chris Clark determined that the cost of supplies on hand at the end of the period was $550.

35 4 Transaction G (continued) Assets CASH + SUPPLIES + LAND Bal. 7,900 1,350 20,000 g. 800 Bal. 7, ,000

36 4 Transaction G (continued) Liabilities + Stockholders Equity ACCOUNTS CAPITAL FEES WAGES RENT SUP. UTIL. MISC. PAYABLE + STOCK + EARNED EXP. EXP. EXP. EXP. EXP. Bal ,000 7,500 2, g. 800 Bal ,000 7,500 2,

37 4 Transaction H On November 30, 2009, NetSolutions pays $2,000 to stockholders (Chris Clark) as dividends.

38 4 Transaction H (continued) Assets CASH + SUPPLIES + LAND Bal. 7, ,000 h. 2,000 Bal. 5, ,000

39 4 Transaction H (continued) Liabilities + Stockholders Equity ACCTS. CAPITAL, DIVI- FEES WAGES RENT SUP. UTIL. MISC. PAY. + STOCK DENDS + EARNED EXP. EXP. EXP. EXP. EXP. Bal ,000 7,500 2, h. 2,000 Bal ,000 2,000 7,500 2,

40 4 Summary

41 4 Exhibit 5 Effects of Transactions on Stockholders Equity

42 5 Financial Statements After transactions have been recorded and summarized, reports are prepared for users. The accounting reports providing this information are called financial statements.

43 5 statement of comprehensive income The statement of comprehensive income reports the revenues and expenses for a period of time, based on the matching concept.

44 5 Matching Concept The matching concept is applied by matching the expenses with the revenue generated during a period by those expenses.

45 5 The excess of revenue over the expenses is called net income or net profit. If the expenses exceed the revenue, the excess is a net loss.

46 5 Statement of Retained Earnings The statement of retained earnings reports the changes in the retained earnings for a specific period of time, such as a month or a year.

47 5 Statement of Financial Position A statement of financial position is a list of the assets, liabilities, and stockholders equity as of a specific date.

48 5 Account Form The account form of a statement of financial position lists the assets on the left and the liabilities and stockholders equity on the right similar to the design of an account.

49 5 Statement of Cash Flows A statement of cash flows is a summary of the cash receipts and payments for a specific period of time. It consists of three sections: (1) operating activities, (2) investing activities, and (3) financing activities.

50 5 Operating Activities The cash flows from operating activities section reports a summary of cash receipts and cash payments from operations.

51 5 Investing Activities The cash flows from investing activities section reports the cash transactions for the acquisition and sale of relatively permanent assets.

52 5 Financing Activities The cash flows from financing activities section reports the cash transactions related to cash investments by stockholders, borrowings, and cash dividends.

53 5 Interrelationships Among Financial Statements The statement of comprehensive income and the statement of retained earnings are interrelated. Net income or net loss appears on the statement of comprehensive income and is also reported on the statement of retained earnings as either an addition to or a deduction from the beginning retained earnings balance.

54 5 Interrelationships Among Financial Statements The statement of retained earnings and the statement of financial position are interrelated. Retained earnings at the end of the period reported on the statement of retained earnings is also reported on the statement of financial position as retained earnings.

55 5 Interrelationships Among Financial Statements The statement of financial position and the statement of cash flows are interrelated. The cash reported on the statement of financial position is also reported as the end-of-period cash on the statement of cash flows.

56 5 Financial Analysis and Interpretation Ratio of Liabilities to Stockholders Equity = Total Liabilities Total Stockholders Equity For NetSolutions: Ratio of Liabilities to Stockholders Equity = $400 $26,050 = 0.015

57 Terima Kasih Rina Y. Asmara SE, MM, Ak., CA

Introduction to Accounting and Business

Introduction to Accounting and Business Chapter 1 Prepared by: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine University Learning Objectives 1. Describe the nature of a business, the role

Introduction to Accounting and Business Chapter 1 Prepared by: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine University Learning Objectives 1. Describe the nature of a business, the role

o Chapter 1: INTRODUCTION TO ACCOUNTING

ACCOUNTING 2-MANAGERIAL ACCOUNTING o Chapter 1: INTRODUCTION TO ACCOUNTING AND BUSINESS Teacher Version Learning Objectives 1. Describe the nature of a business and the role of accounting and ethics in

ACCOUNTING 2-MANAGERIAL ACCOUNTING o Chapter 1: INTRODUCTION TO ACCOUNTING AND BUSINESS Teacher Version Learning Objectives 1. Describe the nature of a business and the role of accounting and ethics in

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Modul ke: Pengantar Akuntansi. Accounting in Action. 1Fakultas Ekonomi dan Bisnis. Yullia Yustikasari, SE, M.Sc. Program Studi Akuntansi

Modul ke: 1Fakultas Ekonomi dan Bisnis Pengantar Akuntansi Accounting in Action Yullia Yustikasari, SE, M.Sc. Program Studi Akuntansi CHAPTER1 Accounting in Action PreviewofCHAPTER1 What is Accounting?

Modul ke: 1Fakultas Ekonomi dan Bisnis Pengantar Akuntansi Accounting in Action Yullia Yustikasari, SE, M.Sc. Program Studi Akuntansi CHAPTER1 Accounting in Action PreviewofCHAPTER1 What is Accounting?

CHAPTER 1. AP Photo/Paul Sakuma Introduction to Accounting and Business. Google W

CHAPTER 1 AP Photo/Paul Sakuma Introduction to Accounting and Business Google W hen two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer, and fireworks

CHAPTER 1 AP Photo/Paul Sakuma Introduction to Accounting and Business Google W hen two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer, and fireworks

Google. Introduction to Accounting and Business CHAPTER 1

CHAPTER 1 AP Photo/Paul Sakuma Google Introduction to Accounting and Business W hen two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer, and fireworks

CHAPTER 1 AP Photo/Paul Sakuma Google Introduction to Accounting and Business W hen two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer, and fireworks

When two teams pair up for a game of football, there

Chapter 01.qxd 2/15/08 12:03 AM Page 1 C H A P T E R 1 Introduction to Accounting and Business When two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer,

Chapter 01.qxd 2/15/08 12:03 AM Page 1 C H A P T E R 1 Introduction to Accounting and Business When two teams pair up for a game of football, there is often a lot of noise. The band plays, the fans cheer,

Printed in USA Financial Accounting 13e. 2014, 2012 South-Western, Cengage Learning

This is an electronic version of the print textbook. Due to electronic rights restrictions, some third party content may be suppressed. Editorial review has deemed that any suppressed content does not

This is an electronic version of the print textbook. Due to electronic rights restrictions, some third party content may be suppressed. Editorial review has deemed that any suppressed content does not

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Pengertian Laporan Keuangan, Pajak dan Arus Kas

Modul ke: Manajemen Keuangan Pengertian Laporan Keuangan, Pajak dan Arus Kas Fakultas EKONOMI & BISNIS Hidayat Wiweko,S.E.,M.Si. Program Studi Manajemen MODUL 2: Pengertian Laporan Keuangan, Pajak dan

Modul ke: Manajemen Keuangan Pengertian Laporan Keuangan, Pajak dan Arus Kas Fakultas EKONOMI & BISNIS Hidayat Wiweko,S.E.,M.Si. Program Studi Manajemen MODUL 2: Pengertian Laporan Keuangan, Pajak dan

Presented by: Meredith Mostochuk, CBA

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Accounting 1A Class Notes Chapter 1 Introduction to Accounting and Business

Types of Business Service Business - Lawyer, Consultant, Doctor Merchandiser Best Buy, Wal-Mart Manufacturer - Mattel, Coca Cola Purpose of Accounting Provide Financial Information for decision making

Types of Business Service Business - Lawyer, Consultant, Doctor Merchandiser Best Buy, Wal-Mart Manufacturer - Mattel, Coca Cola Purpose of Accounting Provide Financial Information for decision making

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 6 Accounting for Merchandising

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 6 Accounting for Merchandising

CHAPTER 3 ACCRUAL ACCOUNTING CONCEPTS

CHAPTER 3 ACCRUAL ACCOUNTING CONCEPTS CLASS DISCUSSION QUESTIONS 1. Google and Wal-Mart use the accrual basis of accounting. Generally accepted accounting principles (GAAP) require all but very small businesses

CHAPTER 3 ACCRUAL ACCOUNTING CONCEPTS CLASS DISCUSSION QUESTIONS 1. Google and Wal-Mart use the accrual basis of accounting. Generally accepted accounting principles (GAAP) require all but very small businesses

Evaluating a Firm s Financial Performance

Modul ke: Manajemen Keuangan Evaluating a Firm s Financial Performance Fakultas EKONOMI & BISNIS Hidayat Wiweko,S.E.,M.Si. Program Studi Manajemen MODUL 3 : Financial Statement Analysis Are our decisions

Modul ke: Manajemen Keuangan Evaluating a Firm s Financial Performance Fakultas EKONOMI & BISNIS Hidayat Wiweko,S.E.,M.Si. Program Studi Manajemen MODUL 3 : Financial Statement Analysis Are our decisions

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

CHAPTER 2: CONSTRUCTING FINANCIAL STATEMENTS

M2-18. a. no effect e. increase b. decrease f. increase c. decrease g. increase d. no effect M2-19. a. Balance sheet e. Balance sheet i. Income statement b. Income statement f. Balance sheet j. Income

M2-18. a. no effect e. increase b. decrease f. increase c. decrease g. increase d. no effect M2-19. a. Balance sheet e. Balance sheet i. Income statement b. Income statement f. Balance sheet j. Income

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Fill-in-the-Blank Equations. Exercises

Chapter 1 Introduction to Accounting and Business Study Guide Solutions Fill-in-the-Blank Equations 1. Equity 2. Net income or net loss 3. Net income (or subtract if a net loss) 4. Cash flows from investing

Chapter 1 Introduction to Accounting and Business Study Guide Solutions Fill-in-the-Blank Equations 1. Equity 2. Net income or net loss 3. Net income (or subtract if a net loss) 4. Cash flows from investing

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

Module 1 Exhibits and Key terms

Exhibit 1... 2 Exhibit 2... 3 A. Income Statement... 3 C. Balance Sheet... 3 Transactions affecting only the balance sheet... 4 1a. Owners invested cash... 4 2a. Borrowed money... 4 3a. Purchased trucks

Exhibit 1... 2 Exhibit 2... 3 A. Income Statement... 3 C. Balance Sheet... 3 Transactions affecting only the balance sheet... 4 1a. Owners invested cash... 4 2a. Borrowed money... 4 3a. Purchased trucks

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

CHAPTER 2 ANALYZING TRANSACTIONS DISCUSSION QUESTIONS

Financial and Managerial Accounting 14th Edition Warren SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/financial-managerial-accounting-14thedition-warren-solutions-manual/

Financial and Managerial Accounting 14th Edition Warren SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/financial-managerial-accounting-14thedition-warren-solutions-manual/

Chapter 1 Introduction to Accounting and Business Study Guide. Do You Know?

Chapter 1 Introduction to Accounting and Business Study Guide Do You Know? Learning Objective 1: Describe the nature of a business and the role of accounting and ethics in business. How to distinguish

Chapter 1 Introduction to Accounting and Business Study Guide Do You Know? Learning Objective 1: Describe the nature of a business and the role of accounting and ethics in business. How to distinguish

Exercise 2-1. Exercise 2-2. Exercise 2-3. Name. = Liabilitiy Acounts + Debit Credit. Asset Acounts. Stockholders Equity Acounts Debit. Credit.

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

Exercise 2-1 Debit Asset Acounts Credit = Liabilitiy Acounts + Debit Credit Stockholders Equity Acounts Debit Credit Expense Accounts and Dividends Account Debit Credit Revenue Accounts Debit Credit Exercise

16 Statement of Cash Flows

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Related Download: Solutions Manual Accounting 26th Edition Warren Reeve Duchac

Test Bank Accounting 26th Edition Warren Reeve Duchac. Completed download: https://testbankarea.com/download/accounting-26th-edition-warren-reeve-duchactest-bank/ Related Download: Solutions Manual Accounting

Test Bank Accounting 26th Edition Warren Reeve Duchac. Completed download: https://testbankarea.com/download/accounting-26th-edition-warren-reeve-duchactest-bank/ Related Download: Solutions Manual Accounting

Chapter 1 Accounting and the Business Environment

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Learning Objectives. LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose.

Learning Objectives LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose. Lesson 1-1 The Role of Accounting LO1 Data must be recorded and

Learning Objectives LO1 Describe the different users of accounting information. LO2 Prepare a net worth statement and explain its purpose. Lesson 1-1 The Role of Accounting LO1 Data must be recorded and

CHAPTER 2 THE BASICS OF RECORD KEEPING AND FINANCIAL STATEMENT PREPARATION. Questions, Exercises, and Problems: Answers and Solutions

CHAPTER 2 THE BASICS OF RECORD KEEPING AND FINANCIAL STATEMENT PREPARATION Questions, Exercises, and Problems: Answers and Solutions 2.1 See the text or the glossary at the end of the book. 2.2 Accounting

CHAPTER 2 THE BASICS OF RECORD KEEPING AND FINANCIAL STATEMENT PREPARATION Questions, Exercises, and Problems: Answers and Solutions 2.1 See the text or the glossary at the end of the book. 2.2 Accounting

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Intuit Inc. Whether you realize it or not, you likely interact with. Accounting Systems CHAPTER 5

CHAPTER 5 Pixland/Jupiter Images Accounting Systems Intuit Inc. Whether you realize it or not, you likely interact with accounting systems. For example, your bank statement is a type of accounting system.

CHAPTER 5 Pixland/Jupiter Images Accounting Systems Intuit Inc. Whether you realize it or not, you likely interact with accounting systems. For example, your bank statement is a type of accounting system.

depends on the side of the equation where the item is located.

S1 Learning Goal 21 Discussion Questions and Brief Exercises for Learning Goals 20 21 1. An account is a detailed historical record that shows all the increases, decreases, and balance of a specific item

S1 Learning Goal 21 Discussion Questions and Brief Exercises for Learning Goals 20 21 1. An account is a detailed historical record that shows all the increases, decreases, and balance of a specific item

Chapter 01 - Introducing Accounting in Business. Chapter Outline

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

CHAPTER 2 Solutions MEASUREMENT CONCEPTS: RECORDING BUSINESS TRANSACTIONS

CHAPTER 2 Solutions MEASUREMENT CONCEPTS: RECORDING BUSINESS TRANSACTIONS Discussion Questions DQ1. DQ2. DQ3. DQ4. DQ5. DQ6. DQ7. DQ8. All equipment needs normal repairs. These are considered an ongoing

CHAPTER 2 Solutions MEASUREMENT CONCEPTS: RECORDING BUSINESS TRANSACTIONS Discussion Questions DQ1. DQ2. DQ3. DQ4. DQ5. DQ6. DQ7. DQ8. All equipment needs normal repairs. These are considered an ongoing

Accounting Principles

Accounting Principles The Accounting Process Identification Select Economic Events/Transactions Analyze and Interpret for Users Recording Communication Record, Classify, and Summarize Preparation of Accounting

Accounting Principles The Accounting Process Identification Select Economic Events/Transactions Analyze and Interpret for Users Recording Communication Record, Classify, and Summarize Preparation of Accounting

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

After studying this chapter, you should be able to:

5 Accounting Systems 1 After studying this chapter, you should be able to: 1. Define an accounting system and describe its implementation. 2. Journalize and post transactions in a manual accounting system

5 Accounting Systems 1 After studying this chapter, you should be able to: 1. Define an accounting system and describe its implementation. 2. Journalize and post transactions in a manual accounting system

Chapter 1 Introduction to Accounting and Business Study Guide. Do You Know?

Chapter 1 Introduction to Accounting and Business Study Guide Do You Know? Learning Objective 1: Describe the nature of a business and the role of accounting and ethics in business. How to distinguish

Chapter 1 Introduction to Accounting and Business Study Guide Do You Know? Learning Objective 1: Describe the nature of a business and the role of accounting and ethics in business. How to distinguish

The Role of Accountants and Accounting Information

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Copyright 2009 The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12

The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12 Introduction Accounting Organizations and Basic Precepts For many students, Principles of Accounting is their first taste

The Learning House, Inc. Accounting Organizations & Basic Precepts Page 1 of 12 Introduction Accounting Organizations and Basic Precepts For many students, Principles of Accounting is their first taste

Chapter 1 Question Review 1

Chapter 1 Question Review 1 Chapter 1 Questions Multiple Choice 1. A business organized as a separate legal entity is a a. corporation. b. proprietor. c. government unit. d. partnership. 2. Which of the

Chapter 1 Question Review 1 Chapter 1 Questions Multiple Choice 1. A business organized as a separate legal entity is a a. corporation. b. proprietor. c. government unit. d. partnership. 2. Which of the

Chapter 1 QUESTIONS. Solutions Manual, Chapter 1

Chapter 1 Accounting in Business Download full Solution Manual for Financial and Managerial Accounting 6th Edition by Wild at: https://getbooksolutions.com/download/solutio n-manual-for-financial-and-managerialaccounting-6th-edition

Chapter 1 Accounting in Business Download full Solution Manual for Financial and Managerial Accounting 6th Edition by Wild at: https://getbooksolutions.com/download/solutio n-manual-for-financial-and-managerialaccounting-6th-edition

Do you subscribe to any magazines? Most of us subscribe

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

CHAPTER 1 INTRODUCTION TO ACCOUNTING AND BUSINESS

CHAPTER 1 INTRODUCTION TO ACCOUNTING AND BUSINESS PROBLEMS Prob. 1 1B Owner s Assets = Liabilities + Equity Accounts Accounts Pamela Larsen, Cash + Receivable + Supplies = Payable + Capital a. +15,000

CHAPTER 1 INTRODUCTION TO ACCOUNTING AND BUSINESS PROBLEMS Prob. 1 1B Owner s Assets = Liabilities + Equity Accounts Accounts Pamela Larsen, Cash + Receivable + Supplies = Payable + Capital a. +15,000

CHAPTER 1. Accounting Principles Weygandt, Kieso, Trenholm 1-1 CHAPTER 1 ACCOUNTING IN ACTION ACCOUNTING IN ACTION

CHAPTER 1 ACCOUNTING IN ACTION Accounting Principles Weygandt, Kieso, Trenholm Prepared by Barbara Trenholm University of New Brunswick CHAPTER 1 ACCOUNTING IN ACTION After studying this chapter, you should

CHAPTER 1 ACCOUNTING IN ACTION Accounting Principles Weygandt, Kieso, Trenholm Prepared by Barbara Trenholm University of New Brunswick CHAPTER 1 ACCOUNTING IN ACTION After studying this chapter, you should

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File 1.0-1 By taking accounting classes, the student is learning the language of business. Answer: True LO: 1-0 EOC Ref: Vocabulary

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File 1.0-1 By taking accounting classes, the student is learning the language of business. Answer: True LO: 1-0 EOC Ref: Vocabulary

Statement of Cash Flows

JWCL162_c13_582-643.qxd 8/13/09 1:09 PM Page 582 chapter 13 Statement of Cash Flows the navigator Scan Study Objectives Read Feature Story Read Preview Read Text and answer Do it! p. 588 p. 595 p. 599

JWCL162_c13_582-643.qxd 8/13/09 1:09 PM Page 582 chapter 13 Statement of Cash Flows the navigator Scan Study Objectives Read Feature Story Read Preview Read Text and answer Do it! p. 588 p. 595 p. 599

Introduction to Financial Accounting

Solutions Manual to Accompany Introduction to Financial Accounting Third Edition (v. 3.1) Based on International Financial Reporting Standards David Annand Copyright 2018 David Annand Published by David

Solutions Manual to Accompany Introduction to Financial Accounting Third Edition (v. 3.1) Based on International Financial Reporting Standards David Annand Copyright 2018 David Annand Published by David

Study. Part One Identifying Accounting Terms. Column II. Answers. Column I

Study 1 Name Identifying Accounting Terms Identifying Accounting Concepts and Practices Analyzing How Transactions Change an Accounting Equation Analyzing How Transactions Change Owner's Equity in an Accounting

Study 1 Name Identifying Accounting Terms Identifying Accounting Concepts and Practices Analyzing How Transactions Change an Accounting Equation Analyzing How Transactions Change Owner's Equity in an Accounting

Holiday Assignment for POA Sec 3 students

Holiday Assignment for POA Sec 3 students Marker s Comment Instructions Answer ALL questions on this paper. Omission of essential working will result in loss of marks, Use ledger paper as per necessary.

Holiday Assignment for POA Sec 3 students Marker s Comment Instructions Answer ALL questions on this paper. Omission of essential working will result in loss of marks, Use ledger paper as per necessary.

Recording Business Transactions

2-1 Recording Business Transactions Atanas Atanasov Assist.prof., University of Economics - Varna 2-2 Tools of The Recording Process Debits and Credits Journal Entries Ledger Accounts First, however, let

2-1 Recording Business Transactions Atanas Atanasov Assist.prof., University of Economics - Varna 2-2 Tools of The Recording Process Debits and Credits Journal Entries Ledger Accounts First, however, let

Module 3 Exhibits and Key Terms. Table of Contents. 1 Principles of Accounting Adjustments for Financial Reporting

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Q Financial Results Conference Call Slides

Q1 2008 Financial Results Conference Call Slides Amazon.com This presentation may contain forward-looking statements which are inherently difficult to predict. Actual results could differ materially for

Q1 2008 Financial Results Conference Call Slides Amazon.com This presentation may contain forward-looking statements which are inherently difficult to predict. Actual results could differ materially for

Accounting Concepts and Procedures

1 Accounting Concepts and Procedures LEARNING OBJECTIVES DID YOU KNOW? By 2007 Best Buy employed 10,000 geek squad agents, 3,000 home theatre installers, and 3,000 vehicle installers. Revenues and net

1 Accounting Concepts and Procedures LEARNING OBJECTIVES DID YOU KNOW? By 2007 Best Buy employed 10,000 geek squad agents, 3,000 home theatre installers, and 3,000 vehicle installers. Revenues and net

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

Understanding Accounting & Financial Statements

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

Study Guide 1. Part One Identifying Accounting Terms. Answers

Study Guide 1 Name Identifying Accounting Terms Identifying Accounting Concepts and Practices Analyzing How Transactions Change an Accounting Equation Analyzing How Transactions Change Owner s Equity in

Study Guide 1 Name Identifying Accounting Terms Identifying Accounting Concepts and Practices Analyzing How Transactions Change an Accounting Equation Analyzing How Transactions Change Owner s Equity in

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

Fill-in-the-Blank Equations. Exercises

Chapter 1 Introduction to Accounting and Business Study Guide Solutions 1. Owner s Equity 2. Net Income or Net Loss 3. Net Income (or subtract if a Net Loss) 4. Cash Flows from Investing Activities 5.

Chapter 1 Introduction to Accounting and Business Study Guide Solutions 1. Owner s Equity 2. Net Income or Net Loss 3. Net Income (or subtract if a Net Loss) 4. Cash Flows from Investing Activities 5.

CHAPTER 10 PREPARING THE STATEMENT OF CASH FLOWS

CHAPTER 10 PREPARING THE STATEMENT OF CASH FLOWS Accrual Accounting Versus Cash T-accounts may be used to determine the amount of cash collected or paid for various items. Following the example in the

CHAPTER 10 PREPARING THE STATEMENT OF CASH FLOWS Accrual Accounting Versus Cash T-accounts may be used to determine the amount of cash collected or paid for various items. Following the example in the

ACCOUNTING CONCEPTS AND PROCEDURES

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

Processing Accounting Information

2 Processing Accounting Information PAst Chapter 1 described the environment of financial accounting. It also introduced the financial statements and basic analysis of them. PResent This chapter explains

2 Processing Accounting Information PAst Chapter 1 described the environment of financial accounting. It also introduced the financial statements and basic analysis of them. PResent This chapter explains

Chapter Seventeen. Learning Objectives

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Chapter Seventeen Using Accounting Information Learning Objectives 1. Explain why accounting information and audited financial statements are important. 2. Identify the people who use accounting information

Supplies Bal. 5 Bal. 4 Bal. 2 a 20 b 18 d 14 g 8 i 10 l 8 c 5 e 28 d 56 f 3 g 8 h 11 j 3 k 10 Bal. 27 Bal. 10 Bal. 4

COMP4-2. Req. 1, 2, 3, and 5 T-accounts (in thousands) Accounts Receivable Cash Supplies Bal. 5 Bal. 4 Bal. 2 a 20 b 18 d 14 g 8 i 10 l 8 c 5 e 28 d 56 f 3 g 8 h 11 j 3 k 10 Bal. 27 Bal. 10 Bal. 4 Small

COMP4-2. Req. 1, 2, 3, and 5 T-accounts (in thousands) Accounts Receivable Cash Supplies Bal. 5 Bal. 4 Bal. 2 a 20 b 18 d 14 g 8 i 10 l 8 c 5 e 28 d 56 f 3 g 8 h 11 j 3 k 10 Bal. 27 Bal. 10 Bal. 4 Small

Statistics and Risk Management

Statistics and Risk Management Money Flow Video URL: jukebox.esc13.net/untdeveloper/videos/money%20flow.mov Vocabulary List: Measure of Central Tendencies: The measurement of a relationship between two

Statistics and Risk Management Money Flow Video URL: jukebox.esc13.net/untdeveloper/videos/money%20flow.mov Vocabulary List: Measure of Central Tendencies: The measurement of a relationship between two

Four Basic Financial Statements. Income Statement Statement of Retained Earnings Balance Sheet Statement of Cash Flows. McGraw-Hill/Irwin Slide 1

Four Basic Financial Statements Income Statement Statement of Retained Earnings Balance Sheet Statement of Cash Flows McGraw-Hill/Irwin Slide 1 The Four Basic Financial Statements 1. On a company s INCOME

Four Basic Financial Statements Income Statement Statement of Retained Earnings Balance Sheet Statement of Cash Flows McGraw-Hill/Irwin Slide 1 The Four Basic Financial Statements 1. On a company s INCOME

IN ACTION. Chapter 1 CHAPTER STUDY OBJECTIVES PREVIEW OF CHAPTER 1. The Navigator ACCOUNTING IN ACTION

Chapter 1 ACCOUNTING IN ACTION CHAPTER STUDY OBJECTIVES The Navigator Scan Study Objectives Read Preview Read Chapter Review Work Demonstration Problem Answer True-False Statements Answer Multiple-Choice

Chapter 1 ACCOUNTING IN ACTION CHAPTER STUDY OBJECTIVES The Navigator Scan Study Objectives Read Preview Read Chapter Review Work Demonstration Problem Answer True-False Statements Answer Multiple-Choice

Chapter 1 Financial Accounting and Business Decisions 41

Chapter 1 Financial Accounting and Business Decisions 41 E19B. Determining and Net Income The following infmation appears in the recds of the Jones Cpation at yearend: receivable............... $ 40,000

Chapter 1 Financial Accounting and Business Decisions 41 E19B. Determining and Net Income The following infmation appears in the recds of the Jones Cpation at yearend: receivable............... $ 40,000

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

" Annual report: the main method that management uses to report the results of the company s activities during the year.

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

EXERCISES. 6. manufacturing 7. service 8. manufacturing 9. manufacturing 10. service

EXERCISES Ex. 1 1 a. 1. service 2. service 3. merchandise 4. manufacturing 5. service 6. manufacturing 7. service 8. manufacturing 9. manufacturing 10. service 11. merchandise 12. service 13. merchandise

EXERCISES Ex. 1 1 a. 1. service 2. service 3. merchandise 4. manufacturing 5. service 6. manufacturing 7. service 8. manufacturing 9. manufacturing 10. service 11. merchandise 12. service 13. merchandise

CHAPTER 2 ANALYZING TRANSACTIONS

CHAPTER 2 ANALYZING TRANSACTIONS EYE OPENERS 1. An account is a form designed to record changes in a particular asset, liability, owner s equity, revenue, or expense. A ledger is a group of related accounts.

CHAPTER 2 ANALYZING TRANSACTIONS EYE OPENERS 1. An account is a form designed to record changes in a particular asset, liability, owner s equity, revenue, or expense. A ledger is a group of related accounts.

Accounting Definition

Accounting Definition MINSK MINSK INNOVATION UNIVERSITY Oct, 2015 Learning Objectives After this lecture, you should be able to: 1. Define accounting. 2. Describe the primary forms of business organization.

Accounting Definition MINSK MINSK INNOVATION UNIVERSITY Oct, 2015 Learning Objectives After this lecture, you should be able to: 1. Define accounting. 2. Describe the primary forms of business organization.

Financial & Managerial Accounting 13th Edition Solutions Manual Warren

Financial & Managerial Accounting 13th Edition Solutions Manual Warren Completed downloadable package SOLUTIONS MANUAL for Financial & Managerial Accounting 13th Edition by Carl S Warren, James M Reeve,

Financial & Managerial Accounting 13th Edition Solutions Manual Warren Completed downloadable package SOLUTIONS MANUAL for Financial & Managerial Accounting 13th Edition by Carl S Warren, James M Reeve,

FINANCIAL STATEMENTS, TAXES, AND CASH FLOW

FINANCIAL STATEMENTS, TAXES, AND CASH FLOW Chapter 2 Reem Alnuaim The Balance Sheet Financial statement showing a firm s accounting value on a particular date. Is a snapshot of the firm. It is a convenient

FINANCIAL STATEMENTS, TAXES, AND CASH FLOW Chapter 2 Reem Alnuaim The Balance Sheet Financial statement showing a firm s accounting value on a particular date. Is a snapshot of the firm. It is a convenient

Leasing Companies. Balance Sheet. December 31 Q

Amounts in thousands of $ Balance Sheet Leasing Companies December 31 Q2-2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 Assets Cash in hand and Banks Loans and Lease financing

Amounts in thousands of $ Balance Sheet Leasing Companies December 31 Q2-2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 Assets Cash in hand and Banks Loans and Lease financing

Accounting consists of three basic activities it

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

CHAPTER 3 THE ADJUSTING PROCESS

1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and expenses are reported in the period in which cash is paid. b. Under accrual-basis accounting, revenues

1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and expenses are reported in the period in which cash is paid. b. Under accrual-basis accounting, revenues

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

What are your three most important financial goals? What are your three most important personal goals? GOALS

GOALS What are your three most important financial goals? Client: Spouse: A. A. B. B. C. C. What are your three most important personal goals? Client: Spouse: A. A. B. B. C. C. What would you like for

GOALS What are your three most important financial goals? Client: Spouse: A. A. B. B. C. C. What are your three most important personal goals? Client: Spouse: A. A. B. B. C. C. What would you like for

THE WALT DISNEY COMPANY REPORTS FIRST QUARTER EARNINGS

FOR IMMEDIATE RELEASE February 5, 2008 THE WALT DISNEY COMPANY REPORTS FIRST QUARTER EARNINGS BURBANK, Calif. The Walt Disney Company today reported earnings for its first fiscal quarter ended December

FOR IMMEDIATE RELEASE February 5, 2008 THE WALT DISNEY COMPANY REPORTS FIRST QUARTER EARNINGS BURBANK, Calif. The Walt Disney Company today reported earnings for its first fiscal quarter ended December

Chapter 1 MULTIPLE CHOICE

Chapter 1 Objectives: 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue, expenses, and withdrawals expand the basic

Chapter 1 Objectives: 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue, expenses, and withdrawals expand the basic

Accounting Title 2015/12/ /12/31 Balance Sheet

Financial Statement Balance Sheet Provided by: MECHEMA CHEMICALS INT CORP. Finacial year: Yearly Accounting Title 2015/12/31 2014/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total

Financial Statement Balance Sheet Provided by: MECHEMA CHEMICALS INT CORP. Finacial year: Yearly Accounting Title 2015/12/31 2014/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total

Full file at Chapter 02 - Solutions to Exercises - Series A

SOLUTIONS TO EXERCISES - SERIES A - CHAPTER 2 EXERCISE 2-1A Horizontal Statements Model Stock. Equity Type of Com. Ret. Net Cash Even t Event Asset s = Liab. + Stock + Earn. Rev. Exp. = Inc. Flows a. AS

SOLUTIONS TO EXERCISES - SERIES A - CHAPTER 2 EXERCISE 2-1A Horizontal Statements Model Stock. Equity Type of Com. Ret. Net Cash Even t Event Asset s = Liab. + Stock + Earn. Rev. Exp. = Inc. Flows a. AS

Ch02 Solutions Manual pdf Ch02 Show.pdf

Ch02 Solutions Manual 2015-10-07.pdf Ch02 Show.pdf Chapter 2 Financial Statements, Cash Flow, and Taxes ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. The annual report is a report issued annually by a corporation

Ch02 Solutions Manual 2015-10-07.pdf Ch02 Show.pdf Chapter 2 Financial Statements, Cash Flow, and Taxes ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. The annual report is a report issued annually by a corporation

THE ACCOUNTING EQUATION

Where are we headed? After completing this chapter, you should be able to: define identify explain calculate explain define identify prepare apply analyse CHAPTER 2 THE ACCOUNTING EQUATION KEY TERMS After

Where are we headed? After completing this chapter, you should be able to: define identify explain calculate explain define identify prepare apply analyse CHAPTER 2 THE ACCOUNTING EQUATION KEY TERMS After

Chapter 3 The Accrual Basis of Accounting

Chapter 3 The Accrual Basis of Accounting T HE L AW OF S OLID G ROUND Trust is the foundation of leadership. The 21 Irrefutable Laws of Leadership Dr. John C. Maxwell Learning Goals 1 2 3 4 94 Describe

Chapter 3 The Accrual Basis of Accounting T HE L AW OF S OLID G ROUND Trust is the foundation of leadership. The 21 Irrefutable Laws of Leadership Dr. John C. Maxwell Learning Goals 1 2 3 4 94 Describe

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Reporting and Analyzing Cash Flows

A Look Back Chapter 11 focused on capital budgeting. It explained and illustrated several methods that help identify projects with the higher return on investment. A Look at This Chapter This chapter focuses

A Look Back Chapter 11 focused on capital budgeting. It explained and illustrated several methods that help identify projects with the higher return on investment. A Look at This Chapter This chapter focuses

The Accounting Cycle

C H A P T E R 3 The Accounting Cycle Learning Objectives AFTER STUDYING THIS CHAPTER, YOU SHOULD BE ABLE TO: Capturing Economic Events LO1 Identify the steps in the accounting cycle and discuss the role

C H A P T E R 3 The Accounting Cycle Learning Objectives AFTER STUDYING THIS CHAPTER, YOU SHOULD BE ABLE TO: Capturing Economic Events LO1 Identify the steps in the accounting cycle and discuss the role

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Accounting in Action

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

4. If cash is collected in advance for services, the revenue is recognized when the services are rendered.

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is