Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

|

|

|

- Everett Harvey

- 6 years ago

- Views:

Transcription

1 Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation.

2 Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a balance sheet similar to those used by a proprietorship. A corporation also prepares a statement of stockholders equity. SLIDE 2

3 Preparing an Income Statement from a Trial Balance Lesson 16-1 LO1 SLIDE 3

4 Operating Revenue Section of an Income Statement for a Merchandising Business Lesson 16-1 LO1 The revenue earned by a business from its normal business operations is called operating revenue. The amount of sales, less sales discounts and sales returns and allowances, is called net sales. SLIDE 4

5 Operating Revenue Section of an Income Statement for a Merchandising Business Operating Revenue Section 2 5 Less Contra Accounts 1 Heading 4 Lesson 16-1 LO1 Sales Amount 3 Title of Revenue Account 8 Net Sales Contra 6 Contra 7 Net Sales Account Amounts Account Total Amount 9 SLIDE 5

6 Lesson 16-1 Cost of Merchandise Sold Section of an Income Statement for a Merchandising Business The original price of all merchandise sold during a fiscal period is called the cost of merchandise sold. Cost of merchandise sold is also known as cost of goods sold or cost of sales. The operating revenue remaining after cost of merchandise sold has been deducted is called gross profit. Gross profit is often referred to as gross profit on sales. LO1 SLIDE 6

7 Lesson 16-1 Cost of Merchandise Sold Section of an Income Statement for a Merchandising Business Cost of Merchandise Sold Section 1 2 Beginning Inventory Vertical Analysis Percentages 8 LO1 Purchases Section 3 Ending 5 Inventory Gross Profit 7 6 Cost of 4 Total Cost of Merchandise Merchandise Sold Available for Sale SLIDE 7

8 Lesson 16-1 Cost of Merchandise Sold Section of an Income Statement for a Merchandising Business LO1 Total of adjacent column SLIDE 8

9 Completing an Income Statement for a Merchandising Business The expenses incurred by a business in its normal operations are called operating expenses. The operating revenue remaining after the cost of merchandise sold and operating expenses have been deducted is called income from operations. Income from operations is also referred to as operating income. Lesson 16-1 LO1 SLIDE 9

10 Completing an Income Statement for a Merchandising Business Operating Expenses Section 1 8 Lesson 16-1 LO1 Vertical Analysis Percentages Income from Operations 2 Other 3 Revenue Section 7 Double Rules Less Federal 5 Income Tax Expense 6 Net Income after 4 Net Income before Federal Income Tax Federal Income Tax SLIDE 10

11 Lesson 16-1 Lesson 16-1 Audit Your Understanding 1. What is the major difference between the income statements for merchandising businesses and service businesses? ANSWER The Cost of Merchandise Sold section SLIDE 11

12 Lesson 16-1 Lesson 16-1 Audit Your Understanding 2. How is the cost of merchandise sold calculated? ANSWER Beginning merchandise inventory, plus purchases, equals total cost of merchandise available for sale, less ending merchandise inventory, equals cost of merchandise sold. SLIDE 12

13 Lesson 16-1 Lesson 16-1 Audit Your Understanding 3. Why is interest income presented in a section other than Operating Revenue? ANSWER The interest earned on notes receivable is not a normal operating activity. SLIDE 13

14 Learning Objective LO2 Prepare a statement of stockholders equity for a business organized as a corporation.

15 Lesson 16-2 Stockholders Equity Information A financial statement that shows changes in a corporation s ownership for a fiscal period is called a statement of stockholders equity. LO2 SLIDE 15

16 Lesson 16-2 Stockholders Equity Information LO2 SLIDE 16

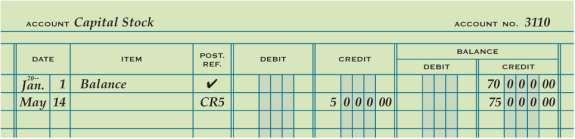

17 Capital Stock Section of the Statement of Stockholders Equity Lesson 16-2 LO2 A value assigned to a share of stock and printed on the stock certificate is called par value. When issuing shares of stock, a corporation can assign any par value allowed by laws in the state in which it incorporates. SLIDE 17

18 Capital Stock Section of the Statement of Stockholders Equity Lesson 16-2 LO2 2 Capital Stock Section 1 Heading Stock Issued During the Year 4 3 Stock at Beginning of Year 5 Total Stock Issued SLIDE 18

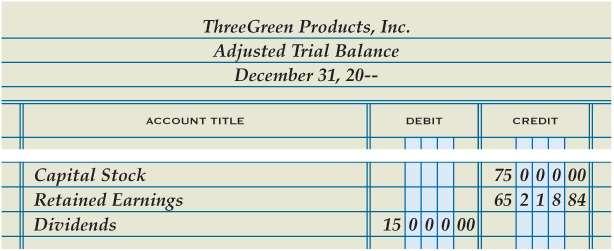

19 Retained Earnings Section of the Statement of Stockholders Equity 1 Retained Earnings Section 3 Net Income after Federal Income Tax Lesson 16-2 LO2 2 5 Beginning Balance Increase in Retained Earnings Dividends Declared 4 6 Ending Balance 7 Total Stockholders Equity SLIDE 19

20 Lesson 16-2 Lesson 16-2 Audit Your Understanding 1. What financial information does a statement of stockholders equity report? ANSWER The changes in a corporation s ownership for a fiscal period SLIDE 20

21 Lesson 16-2 Lesson 16-2 Audit Your Understanding 2. What are the two major sections of a statement of stockholders equity? ANSWER Capital Stock and Retained Earnings SLIDE 21

22 Lesson 16-2 Lesson 16-2 Audit Your Understanding 3. Where is the information found to prepare the Capital Stock section of a statement of stockholders equity? ANSWER In the Capital Stock general ledger account SLIDE 22

23 Lesson 16-2 Lesson 16-2 Audit Your Understanding 4. Where is the beginning balance of retained earnings found? ANSWER The Retained Earnings amount on the unadjusted trial balance SLIDE 23

24 Lesson 16-2 Lesson 16-2 Audit Your Understanding 5. When issuing shares of stock, what par value can a corporation assign to each share? ANSWER A corporation can assign any par value allowed by laws in the state in which it incorporates. SLIDE 24

25 Lesson 16-2 Lesson 16-2 Audit Your Understanding 6. Where is net income after federal income taxes found? ANSWER The income statement SLIDE 25

26 Learning Objective LO3 Prepare a balance sheet for a business organized as a corporation.

27 Lesson 16-3 Balance Sheet Information on a Trial Balance LO3 SLIDE 27

28 Lesson 16-3 Current Assets Section of a Balance Sheet 2 Current Assets Section 1 Heading Book Value of Accounts Receivable 3 LO3 4 Remaining Current 5 Total Current Asset Accounts Assets SLIDE 28

29 Lesson 16-3 Plant Assets Section of a Balance Sheet 1 Plant Assets Section 2 Book Value of Office Equipment LO3 Book Value of 3 Store Equipment 4 Total Plant Assets 5 Total Assets SLIDE 29

30 Lesson 16-3 Liabilities Section of a Balance Sheet LO3 Liabilities are classified according to the length of time until they are due. Liabilities due within a short time, usually within a year, are called current liabilities. Liabilities owed for more than a year are called long-term liabilities. SLIDE 30

31 Lesson 16-3 Liabilities Section of a Balance Sheet LO3 1 Liabilities Section 2 Account Title and Amount of Each Current Liability 3 Total Liabilities SLIDE 31

32 Stockholders Equity Section of a Balance Sheet Stockholders Retained Equity Section 1 3 Earnings 2 Capital Stock Lesson 16-3 LO3 6 Double Rule Total Stockholders Equity 4 5 Total Liabilities and Stockholders Equity SLIDE 32

33 Completed Balance Sheet Lesson 16-3 LO3 SLIDE 33

34 Lesson 16-3 Supporting Schedules for a Balance Sheet LO3 A report prepared to give details about an item on a principal financial statement is called a supporting schedule. A supporting schedule is sometimes referred to as a supplementary report or an exhibit. SLIDE 34

35 Lesson 16-3 Lesson 16-3 Audit Your Understanding 1. How does ThreeGreen classify its assets? ANSWER Current assets and plant assets SLIDE 35

36 Lesson 16-3 Lesson 16-3 Audit Your Understanding 2. What three items are listed on the balance sheet for an account having a related contra asset account? ANSWER 1. The balance of the asset account 2. The balance of the contra asset account 3. The book value SLIDE 36

37 Lesson 16-3 Lesson 16-3 Audit Your Understanding 3. What is an example of a long-term liability? ANSWER Mortgage payable SLIDE 37

38 Lesson 16-3 Lesson 16-3 Audit Your Understanding 4. Where are the amounts obtained for the Stockholders Equity section of the balance sheet? ANSWER From the statement of stockholders equity SLIDE 38

39 Lesson 16-3 Lesson 16-3 Audit Your Understanding 5. What are two supporting schedules that might accompany a balance sheet? ANSWER Schedule of accounts payable and schedule of accounts receivable SLIDE 39

40 Learning Objective LO4 Prepare closing entries.

41 Lesson 16-4 Closing Entries LO4 A corporation records four closing entries: 1. A closing entry for income statement accounts with credit balances (revenue and contra-cost accounts). 2. A closing entry for income statement accounts with debit balances (cost, contra revenue, and expense accounts). 3. A closing entry to record net income or net loss in the Retained Earnings account and close the Income Summary account. 4. A closing entry for the Dividends account. SLIDE 41

42 Lesson 16-4 The Income Summary Account LO4 Income Summary Debit Expenses Credit Revenue (greater than expenses) (Credit balance is the net income) SLIDE 42

43 Closing Entry for Accounts with Credit Balances Lesson 16-4 LO4 Closing 632, Sales Bal. 632, (New Bal. 0.00) Adj. (mdse inv.) 5, Interest Expense Closing 635, (credit accounts) SLIDE 43

44 Closing Entry for Accounts with Credit Balances Lesson 16-4 LO4 Debit to Close Date 1 Heading Credit to 4 Income Summary SLIDE 44

45 Closing Entry for Income Statement Accounts with Debit Balances Lesson 16-4 LO4 Credit to Close 3 3 Date 1 2 Income summary 4 Debit to Income Summary SLIDE 45

Closing 254,851.26 Income Summary Adj. (mdse. Inv.) 5,643.44 Closing (debit accounts) 549,800.89 Closing (credit accounts) 635,345.90 (New Bal.")

46 Summary of Closing Entry for Income Statement Accounts with Debit Balances Lesson 16-4 LO4 Purchases Bal. 254, (New Bal. 0.00) Closing 254, Income Summary Adj. (mdse. Inv.) 5, Closing (debit accounts) 549, Closing (credit accounts) 635, (New Bal. 79,896.57) SLIDE 46

LO4 Retained Earnings Date Closing (credit accounts) 65,218.84 Closing (Retained Earnings) 79,896.57 (New Bal. 145,115.41) Debit Income Summary Credit Retained Earnings SLIDE 47")

47 Lesson 16-4 Closing Entry to Record Net Income Adj. (mdse. inv.) 5, Closing (debit accounts) 549, Closing (Retained Earnings) 79, Income Summary Closing (credit accounts) 635, (New Bal. 0.00) LO4 Retained Earnings Date Closing (credit accounts) 65, Closing (Retained Earnings) 79, (New Bal. 145,115.41) Debit Income Summary Credit Retained Earnings SLIDE 47

LO4 Dividends Bal. 15,000.00 (New Bal. 0.00) Closing (Retained Earnings) 15,000.")

48 Lesson 16-4 Closing Entry for Dividends Retained Earnings Closing (Dividends) 15, Bal. 65, Closing (Income Summary) 79, (New Bal. 130,115.41) LO4 Dividends Bal. 15, (New Bal. 0.00) Closing (Retained Earnings) 15, Date Debit Retained Earnings Credit Dividends SLIDE 48

49 Completed Closing Entries for a Corporation Recorded in a Journal Lesson 16-4 LO4 SLIDE 49

50 Lesson 16-4 Lesson 16-4 Audit Your Understanding 1. Where is the information obtained to journalize closing entries for revenue, cost, and expenses? ANSWER From the adjusted trial balance SLIDE 50

51 Lesson 16-4 Lesson 16-4 Audit Your Understanding 2. What is the name of the temporary account used to summarize the closing entries for revenue, cost, and expenses? ANSWER Income Summary SLIDE 51

52 Learning Objective LO5 Prepare a post-closing trial balance.

53 General Ledger After Closing Entries Are Posted Lesson 16-5 LO5 SLIDE 53

54 Lesson 16-5 Post-Closing Trial Balance 1 Heading LO5 Accounts with Balances 2 3 Account Balances Totals 4 Column Totals 5 6 Double Rule SLIDE 54

55 Accounting Cycle for a Merchandising Business Organized as a Corporation Lesson 16-5 LO Source documents are checked for accuracy, and transactions are analyzed. 2. Transactions are recorded in journals. 3. Journal entries are posted to the accounts payable ledger, the accounts receivable ledger, and the general ledger. 4. Schedules of accounts payable and accounts receivable are prepared from the subsidiary ledgers. 5. An unadjusted trial balance is prepared from the general ledger. 6. Adjusting entries are journalized Adjusting entries are posted to the general ledger. 8. An adjusted trial balance is prepared from the general ledger. 9. Financial statements are prepared from the adjusted trial balance Closing entries are journalized. 11. Closing entries are posted to the general ledger. 12. A post-closing trial balance is prepared from the general ledger. SLIDE 55

56 Lesson 16-5 Lesson 16-5 Audit Your Understanding 1. Which accounts and balances are listed on a post-closing trial balance? In what order are they listed? ANSWER General ledger accounts that have balances. Accounts are listed in the same order as they appear in the general ledger. SLIDE 56

57 Lesson 16-5 Lesson 16-5 Audit Your Understanding 2. What is the purpose of preparing a postclosing trial balance? ANSWER To prove the equality of debits and credits in the general ledger SLIDE 57

58 Lesson 16-5 Lesson 16-5 Audit Your Understanding 3. What two steps in the accounting cycle occur after adjusting entries are posted to the general ledger? ANSWER 1. An adjusted trial balance is prepared from the general ledger. 2. Financial statements are prepared from the adjusted trial balance. SLIDE 58

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

LESSON Preparing an Income Statement. CENTURY 21 ACCOUNTING Thomson/South-Western

Preparing an Income Statement 2 Uses of Financial Statements Financial statements provide the source of information needed by owners and managers to make decisions on the future activity of a business

Preparing an Income Statement 2 Uses of Financial Statements Financial statements provide the source of information needed by owners and managers to make decisions on the future activity of a business

Reporting Financial Information

Learning Objectives LO1 Prepare an income statement for a service business. LO2 Calculate and analyze financial ratios using income statement amounts. Lesson 7-1 Reporting Financial Information LO1 The

Learning Objectives LO1 Prepare an income statement for a service business. LO2 Calculate and analyze financial ratios using income statement amounts. Lesson 7-1 Reporting Financial Information LO1 The

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

Accounting 1. Lesson Plan. Name: Terry Wilhelmi Day/Date:

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Accounting 1. Lesson Plan. Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

LESSON Posting to an Accounts Payable Ledger. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON 8-1. Recording Adjusting Entries. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

Curriculum Document for Business Education

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Completing the Accounting Cycle

4 Completing the Accounting Cycle 4-1 Closing the Books At the end of the accounting period, the company gets the accounts ready for the next period. Very similar to what happens at AHS at the end of a

4 Completing the Accounting Cycle 4-1 Closing the Books At the end of the accounting period, the company gets the accounts ready for the next period. Very similar to what happens at AHS at the end of a

Allowance Method of Recording Losses from Uncollectible Accounts

Learning Objectives LO1 Explain the purpose of the allowance method for recording losses from uncollectible accounts. LO2 Estimate uncollectible accounts expense using an aging of accounts receivable.

Learning Objectives LO1 Explain the purpose of the allowance method for recording losses from uncollectible accounts. LO2 Estimate uncollectible accounts expense using an aging of accounts receivable.

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Chapter 4: Posting from a General Journal to a General Ledger

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Chapter 6: Worksheets for a Service Business

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

LESSON Journalizing Purchases Using a Purchases Journal

LESSON 9-1 - Journalizing Purchases Using a Purchases Journal Service business vs. merchandising business Service business sells services for a fee nail salon, attorney Merchandising business purchases

LESSON 9-1 - Journalizing Purchases Using a Purchases Journal Service business vs. merchandising business Service business sells services for a fee nail salon, attorney Merchandising business purchases

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Week 5, Chap 4 Part 2

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Key Learning: Students will review basic accounting concepts learned in the first level course.

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Answer: b Rationale: Journalizing means to record a transaction in a general journal.

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

Chapter 16: Financial Statements and Closing Entries for a Corporation: Chapter Overview

Chapter 16: Financial Statements and Closing Entries for a Corporation: Chapter Overview Financial Statements and Closing Entries for a Corporation: Chapter Objectives Financial Statements and Closing

Chapter 16: Financial Statements and Closing Entries for a Corporation: Chapter Overview Financial Statements and Closing Entries for a Corporation: Chapter Objectives Financial Statements and Closing

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

4/9/2012. Recording Transactions. Learning Objectives (LO) LO 1 Double-Entry System. LO 1 Double-Entry System. LO 1 Double-Entry System

LO 1 Double-Entry System. LO 1 Double-Entry System. LO 1 Double-Entry System") 4/9/212 Recording Transactions CHAPTER 3 Learning Objectives (LO) After studying this chapter, you should be able to 1. Use double-entry accounting 2. Describe the five steps in the recording process 3.

4/9/212 Recording Transactions CHAPTER 3 Learning Objectives (LO) After studying this chapter, you should be able to 1. Use double-entry accounting 2. Describe the five steps in the recording process 3.

LESSON 2-1. Departmental Sales on Account and Sales Returns and Allowances. CENTURY 21 ACCOUNTING 2009 South-Western, Cengage Learning

LESSON 2-1 Departmental Sales on Account and Sales Returns and Allowances 2 Departmental Sales on Account Sales on account are recorded by department in order to help management make decisions Sales on

LESSON 2-1 Departmental Sales on Account and Sales Returns and Allowances 2 Departmental Sales on Account Sales on account are recorded by department in order to help management make decisions Sales on

SENECA HIGH SCHOOL CURRICULUM MAP BUSINESS/COMPUTER EDUCATION ACCOUNTING II

UNIT 1 Accounting for Sales and Cash Receipts How do merchandising businesses keep track of what is sold and how much money is collected? How does this benefit the consumer? Accounting for a Merchandising

UNIT 1 Accounting for Sales and Cash Receipts How do merchandising businesses keep track of what is sold and how much money is collected? How does this benefit the consumer? Accounting for a Merchandising

Accounting for. Sole Proprietorship. 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS. Assign Students to Read Ch. 9 and complete the terms p. 234

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS Assign Students to Read Ch. 9 and complete the terms p. 234 (Students may hand-write them on handout or do on word processor) Discuss Section

Accounting I Chapter 9 JOURNALIZING PURCHASES AND CASH PAYMENTS Assign Students to Read Ch. 9 and complete the terms p. 234 (Students may hand-write them on handout or do on word processor) Discuss Section

Enter account titles and their unadjusted balances in the Trial Balance columns Total the amounts

Process by which companies produce their financial statements Chapter 4 Copyright 2009 Prentice Hall. All rights reserved 2 Journalize Transaction Post to Accounts Adjust Accounts Prepare an accounting

Process by which companies produce their financial statements Chapter 4 Copyright 2009 Prentice Hall. All rights reserved 2 Journalize Transaction Post to Accounts Adjust Accounts Prepare an accounting

Introduction Cengage Learning. All Rights Reserved.

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

Introduction How would you obtain a balance for any account recorded in the journal? How do you keep track of cash received and spent? Name different ways you can pay with cash. What types of accounts

LESSON Recording A Payroll. CENTURY 21 ACCOUNTING Thomson/South-Western

Recording A Payroll 2 Different Forms of Payroll Information Payroll information for each pay period is recorded in a payroll register Each pay period the payroll information for each employee is also

Recording A Payroll 2 Different Forms of Payroll Information Payroll information for each pay period is recorded in a payroll register Each pay period the payroll information for each employee is also

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Accounting Vocabulary

Accounting Vocabulary A. Accounting: planning, recording, analyzing and interpreting financial information. Accounting Equation: an equation showing the relationship among assets, liabilities, and owner

Accounting Vocabulary A. Accounting: planning, recording, analyzing and interpreting financial information. Accounting Equation: an equation showing the relationship among assets, liabilities, and owner

ACCOUNTING I. 1. The cash account is used to summarize information about the amount of money the business has available.

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I Chapter 10 Reading Guide. 1. What are the two major activities of merchandising businesses?

Due: Name: Hour: ACCOUNTING I Chapter 10 Reading Guide Answer the following questions as you read Chapter 10, pages 268-288. 10-1 JOURNALIZING SALES ON ACCOUNT; USING A SALES JOURNAL 1. What are the two

Due: Name: Hour: ACCOUNTING I Chapter 10 Reading Guide Answer the following questions as you read Chapter 10, pages 268-288. 10-1 JOURNALIZING SALES ON ACCOUNT; USING A SALES JOURNAL 1. What are the two

Chapter 16. Financial Statements for a Partnership. South-Western Educational Publishing

Chapter 16 Financial Statements for a Partnership Reporting Financial Information Adequate Disclosure Concept Applied when financial statements contain all information necessary to understand a business

Chapter 16 Financial Statements for a Partnership Reporting Financial Information Adequate Disclosure Concept Applied when financial statements contain all information necessary to understand a business

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts

Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts") Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

Investing and Financing Decisions and the Accounting System

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

Learning Objective. LO1 Analyze an income statement using vertical analysis Cengage Learning. All Rights Reserved.

Learning Objective LO1 Analyze an income statement using vertical analysis. Lesson 17-1 Vertical Analysis Ratios LO1 Vertical analysis ratios measure the relationship between one financial statement item

Learning Objective LO1 Analyze an income statement using vertical analysis. Lesson 17-1 Vertical Analysis Ratios LO1 Vertical analysis ratios measure the relationship between one financial statement item

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 4/5, Chap 4. The General Journal and the General Ledger. Instructor: Michael Booth

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

1 of 8 8/11/2014 11:20 AM Units: Teacher: Accounting, CORE Course: Accounting Year: 2012-13 Accounting Activities for a Service Business owned by a Sole Proprietor Other standards 2.4.G 2.5.G Content Skills

1 of 8 8/11/2014 11:20 AM Units: Teacher: Accounting, CORE Course: Accounting Year: 2012-13 Accounting Activities for a Service Business owned by a Sole Proprietor Other standards 2.4.G 2.5.G Content Skills

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

HS Accounting I 2013 Business and Technology

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Accounting I. Lesson Plan. Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Cash Payments Unit: 3 Chapter 11

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Accounting I Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Journalizing Purchases and Payments Unit: 3 Chapter 11 I. Objective(s): By the end of today s lesson, the student will be able to: define

Total Test Questions: 57 Levels: Grades Units of Credit:.50

DESCRIPTION Students will develop advanced skills that build upon those acquired in Accounting I. Students continue applying concepts of double-entry accounting systems related to merchandising businesses.

DESCRIPTION Students will develop advanced skills that build upon those acquired in Accounting I. Students continue applying concepts of double-entry accounting systems related to merchandising businesses.

Review of a Company s Accounting System

CHAPTER 3 O BJECTIVES After reading this chapter, you will be able to: 1 Understand the components of an accounting system. 2 Know the major steps in the accounting cycle. 3 Prepare journal entries in

CHAPTER 3 O BJECTIVES After reading this chapter, you will be able to: 1 Understand the components of an accounting system. 2 Know the major steps in the accounting cycle. 3 Prepare journal entries in

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

FBLA Accounting I Practice Test 2004

FBLA Accounting I Practice Test 2004 True/False Indicate whether the sentence or statement is true or false. 1. When a business uses a petty cash fund, the fund is debited each time it is replaced. 2.

FBLA Accounting I Practice Test 2004 True/False Indicate whether the sentence or statement is true or false. 1. When a business uses a petty cash fund, the fund is debited each time it is replaced. 2.

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

District > Intermediate > Business Education > Accounting II ( ) (District) > Juett, David

(District) > Juett, David") Granite School District Accounting II (52.0322) (District) District > Intermediate > Business Education > Accounting II (52.0322) (District) > Juett, David Unit Essential Questions Content Skills Vocabulary

Granite School District Accounting II (52.0322) (District) District > Intermediate > Business Education > Accounting II (52.0322) (District) > Juett, David Unit Essential Questions Content Skills Vocabulary

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Accounting 3 4. Course Outline. Board Approved: October 10, I. Course Information. A. Course Title: Accounting 3-4. B. Course Code Number: BU143

Accounting 3 4 Course Outline Board Approved: October 10, 1995 I. Course Information A. Course Title: Accounting 3-4 B. Course Code Number: BU143 C. Course Length: One Year D. Grade Level: 12 E. Units

Accounting 3 4 Course Outline Board Approved: October 10, 1995 I. Course Information A. Course Title: Accounting 3-4 B. Course Code Number: BU143 C. Course Length: One Year D. Grade Level: 12 E. Units

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Recording Business Transactions

2-1 Recording Business Transactions Atanas Atanasov Assist.prof., University of Economics - Varna 2-2 Tools of The Recording Process Debits and Credits Journal Entries Ledger Accounts First, however, let

2-1 Recording Business Transactions Atanas Atanasov Assist.prof., University of Economics - Varna 2-2 Tools of The Recording Process Debits and Credits Journal Entries Ledger Accounts First, however, let

Accounting 1A Class Notes Chapter 3 The Adjusting Process

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Accounting for Merchandising Businesses

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

CURRICULUM MAPPING FORM

Course Accounting 1 Teacher Mr. Garritano Aug. I. Starting a Proprietorship - 2 weeks A. The Accounting Equation B. How Business Activities Change the Accounting Equation C. Reporting Financial Information

Course Accounting 1 Teacher Mr. Garritano Aug. I. Starting a Proprietorship - 2 weeks A. The Accounting Equation B. How Business Activities Change the Accounting Equation C. Reporting Financial Information

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 3 The Adjusting Process 2 After studying

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 3 The Adjusting Process 2 After studying

Week 5, Chap 4 Part 1

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

DOWNLOAD PDF LIST OF DEBIT AND CREDIT ITEMS IN ACCOUNTING

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

Ch.8 Accounting for a Merchandising Business: Sales and Cash Receipts

Ch.8 Accounting for a Merchandising Business: Sales and Cash Receipts Procedures and forms used in selling merchandise Credit sales Sales Journal Sales returns and allowances Sales discounts Posting procedure

Ch.8 Accounting for a Merchandising Business: Sales and Cash Receipts Procedures and forms used in selling merchandise Credit sales Sales Journal Sales returns and allowances Sales discounts Posting procedure

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

EL DORADO UNION HIGH SCHOOL DISTRICT Educational Services. Course of Study Information Page

Course of Study Information Page (Course #482) Course Description: This course is designed to familiarize students with the principles of accounting theory and the application through practice. The students

Course of Study Information Page (Course #482) Course Description: This course is designed to familiarize students with the principles of accounting theory and the application through practice. The students

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow:

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow: Additional data: 1. Rockford paid a cash dividend in 2012. 2. The $4 million

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow: Additional data: 1. Rockford paid a cash dividend in 2012. 2. The $4 million

BUSINESS and FINANCE TECHNOLOGY CURRICULUM. For ACCOUNTING II. (Elective Course)

") BUSINESS and FINANCE TECHNOLOGY CURRICULUM For ACCOUNTING II (Elective Course) Supports Academic Learning Objective # 3 - Students and graduates of Ledyard High School will employ problem-solving skills

BUSINESS and FINANCE TECHNOLOGY CURRICULUM For ACCOUNTING II (Elective Course) Supports Academic Learning Objective # 3 - Students and graduates of Ledyard High School will employ problem-solving skills

Full file at

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

Presented by: Meredith Mostochuk, CBA

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Debit and Credit Rules Module 2 part I. T- Accounts Assets = Liabilities + OE. T- Accounts: Basic Patterns A = L + OE

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

a) Post-closing trial balance c) Income statement d) Statement of retained earnings

Post-closing trial balance c) Income statement d) Statement of retained earnings") Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

CHAPTER 2 QUESTIONS. revenue, and expense accounts of the

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

REINFORCEMENT ACTIVITY 3, Part B, p. 715

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.