1.1 Generally Accepted Accounting Principles (GAAP) 1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation

|

|

|

- Jack Stevenson

- 6 years ago

- Views:

Transcription

1 1. General Topics

2 1.1 Generally Accepted Accounting Principles (GAAP) 1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation 1.3 The Accounting Cycle

3 1.4 Business Ethics 1.5 Purpose of, Presentation of, and Relationships Between Financial Statements 1.6 Forms of Business

4 1.1 Generally Accepted Accounting Principles (GAAP)

5

6

7 (GAAP) are a set of principles where they are a set of rules considered vital in the realm of Accounting

8 GAAP were created by the Financial Accounting Standards Board (FASB)

9

10 GAAP contain specific facts that must be adhered to, and they include:

11 1. Transactions get recorded twice

12 2. Financial statements report on the business entity only

13 3. Debts are paid within one year, or one business cycle, whichever is longer

14

15 GAAP contains Principles:

16 Conservative Principle:

17 Going-Concern Principle:

18 Historical Cost Principle:

19 Objectivity Principle:

20 Stable Monetary Unit Principle:

21

22 1.1.1 Generally Accepted Accounting Principles (GAAP): Summary

23 GAAP standards created by the Financial Accounting Standards Board (FASB) REMEMBER- FASB: Governing body Not gov t. entity

24 GAAP: Stresses essential characteristics of accounting, which initiate regulations the identification, measurement, and communication of financial information, about; economic business-oriented entities, to; interested parties.

25 GAAP s Primary Concern: Financial Statement Regulation Balance Sheet Income Statement Statement of Cash Flows Statement of Owners or Stockholders Equity Note Disclosures

26 What is the purpose of information presented in notes to the financial statements? To provide disclosure required by generally accepted accounting principles.

27 Summary of Financial Reporting: Information to help users with capital allocation decisions Who are the Users of info? Investors, creditors, and other users Capital Allocation The process of determining how and at what cost money is allocated among competing interests

28 GAAP Standard Setting: Summary WHO: Parties Involved in Standard Setting Four primary parties Securities and Exchange Commission (SEC) American Institute of Certified Public Accountants (AICPA) Financial Accounting Standards Board (FASB) Government Accounting Standards Board (GASB)

29 SEC (Profile) Accounting and reporting for public companies Enforcement Authority for the Government in this area Encouraged private standard-setting body SEC requires public companies to adhere to GAAP, and performs a lot of Oversight

30 Summary of Issues in Financial Reporting Standard Setting in a Political Environment SEC, IRS other Agencies ALL have a vested interest Expectation Gap What the public thinks accountants should do vs. what accountants think they can do. Sarbanes-Oxley Act (2002) (SOX): a system that auditors must test and evaluate

31 Ethics in the Environment of Financial Accounting frequently encounter ethical dilemmas; doing right thing is not always easy or obvious GAAP does not always provide an answer

32 Summary OF (3 Components of) : GAAP Principles 1. Transactions get recorded twice 2. Financial statements report on the business entity only 3. Debts are paid within one year, or one business cycle, whichever is longer; Business Cycles do not always last one year

33 GAAP s Primary Principles:

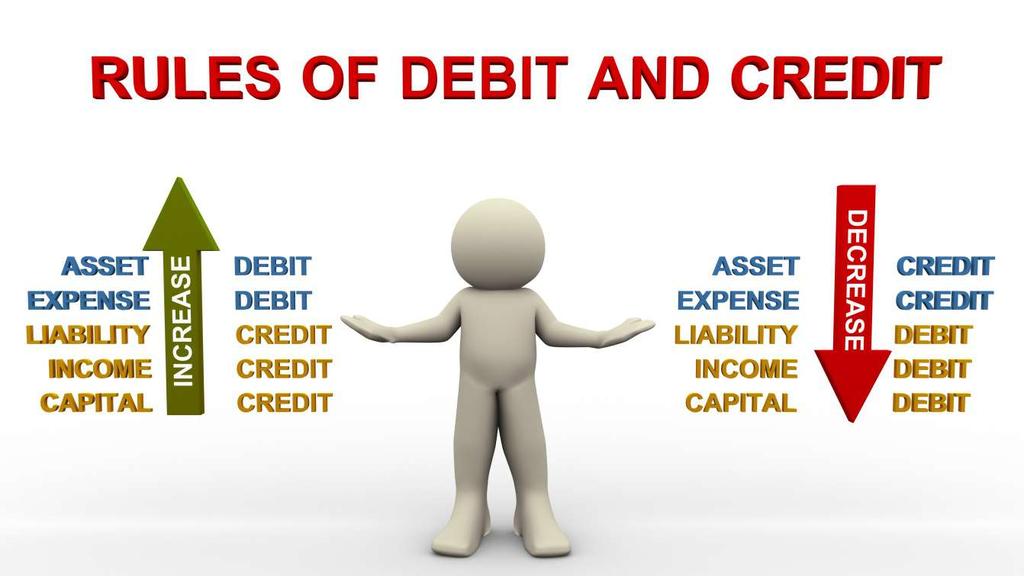

34 Conservative Principle: Resolving financial statement uncertainty in least favorable way Anticipates future losses, not gains Understates net assets/net income Allows companies to play it safe

35 Going-Concern Principle: financial statements are to assume that businesses will last indefinitely; THIS IS DONE in order to fulfill: Obligations Commitments Objectives

36 Objectivity Principle: Business Transactions are recorded using best objective evidence Organizational financial statements be based on solid evidence Prevent any accounting department of a business from documenting slanted information, based on bias

37 1.2 Rules of Double-Entry Accounting/Transaction Analysis Accounting Equation

38

39 1.2.1 Rules for Double- Entry Accounting Rules of Transaction Analysis Rules of the Accounting Equation

40 1.2.1 Rules for Double-Entry Accounting

41 Double-Entry accounting is a principle requiring that transactions gets recorded twice.

42 Therefore equal debits and credits are made in accounts for all transactions.

43

44 This principle of accounting includes factors which need to be monitored, such as:

45 Where the money comes from, and; Where the money is going, and why

46 Thus, the total debits will always equal the total credits in order for the accounting equation will always stay in balance.

47

48 1.2.2 Rules of Transaction Analysis

49

50 This concept is an examination of where transactions are identified, recorded, and summarized

51 The Transaction Analysis is conducted in order to prepare financial statements for the accounting data received, and maintained

52 For any business, an analysis of transactions must display two things:

53 Clear and concise: 1. increases, and; 2. decreases within the statement

54

55 Any increases or decreases from business transactions should display where the assets, liabilities, and owner s equity are balanced

56

57 1.2.3 Rules of the Accounting Equation

58

59 The Accounting Equation are balanced calculations, to include three components:

60 Assets

61

62 Liabilities

63

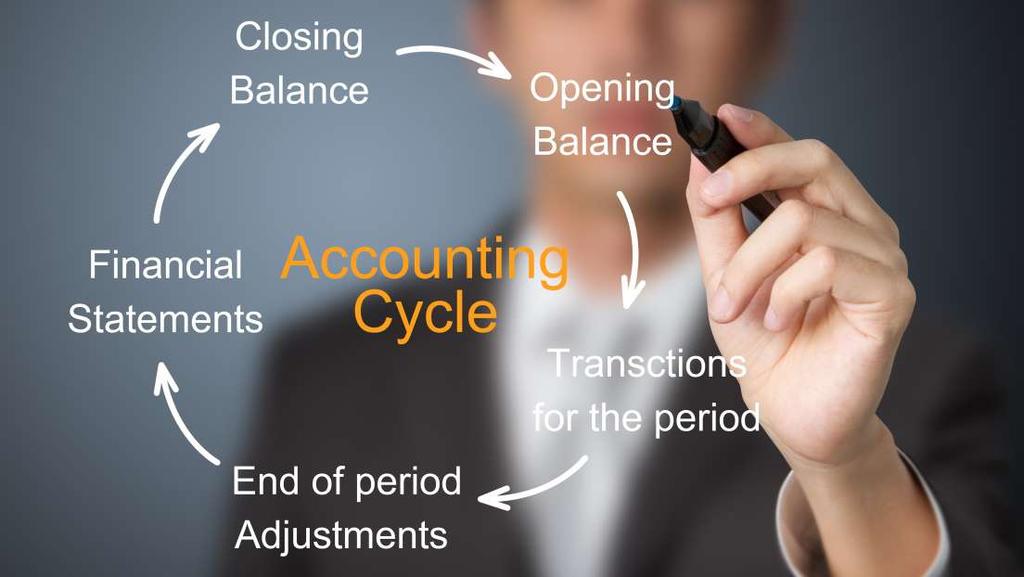

64 Owner s Equity

65

66 There are three (3) ways to demonstrate the accounting equation in realtime

67 Traditional examples of the equation are as follows:

68 Assets= Liabilities + Owner s Equity, or;

69 Owner s Equity= Assets Liabilities, or;

70 Liabilities= Asset Owner s Equity

71 1.3 The Accounting Cycle

72

73 The accounting cycle is the process of recording and processing the accounting events of a business.

74 It begins when transactions occur

75 The Accounting Cycle also begins with the recording of the transactions

76

77 The Accounting Cycle is continual throughout the Business Operating Cycle.

78 The natural period of time occurs before certain business activities tend to repeat

79 Transactions are recorded using entries, based on receipts, in recognition of a sale.

80

81 After businesses post entries to accounts, a balance sheet is prepared

82 Hence, the Balance Sheet ensures the total debits equals the total credits in the financial records.

83

84 Adjustments are often made, followed by creating financial statements.

85 Financial Statements allow for the following:

86 Revenues and expenses are closed at the end of the accounting period.

87

88 Net income transferred into earnings, as the business prepares to ensure debits and credits match

89

90 1.4 Business Ethics

91

92 Ethics are internalized standards considered to be the legality of any action performed

93 Ethics also initiate Internal Controls

94 Internal Controls are not only allow for monitoring, but also allow for an increase in profit.

95

96

97 Several primary internal controls for Accounting:

98 Sarbanes-Oxley Act (SOX): a system that auditors must test and evaluate

99

100 Code of ethics:

101 Law:

102 Full disclosure:

103 Conflicts of interest:

104

105 1.5 Purpose of, Presentation of, and Relationships Between Financial Statements

106

107 1.5.1 Purpose of Financial Statements Presentation of Financial Statements Relationships Between Financial Statements

108 1.5.1 Purpose of Financial Statements

109 The objective of financial statements:

110 Financial Statements also exhibit changes in financial position of an business

111

112 Financial Statements are useful for making economic decisions

113 Income statement:

114 Statement of owner s equity:

115

116 1.5.2 Presentation of Financial Statements

117

118 Financial Statements may be best demonstrated and displayed by:

119 The specific rules used to govern the creation of the statements themselves.

120 These rules include:

121 All financial statements have a three-line heading

122

123 The first line is the business name.

124 The second is the name of the report.

125 The third is the date, or period of time

126 Financial statements start all computations by placing numbers in the column farthest to the right

127

128 Next, to make a subcalculation, move one column to the left;

129 Draw a single line under the last number in a calculation;

130 Put a double underline under final numbers

131 Accountants place the results of a business calculation in one of three different places on the statement

132 Accountants should use the method that allows for the clearest communication.

133

134 1.5.3 Relationships Between Financial Statements

135

136 Financial statements, as there are various types, possess many common components

137 Regardless of the industry, these components are ever-present and observable in accounting.

138 Financial Statements for businesses show:

139 Inventory

140 Accounts, such as Income and Expenses

141

142 Costs of goods sold

143 Net Income

144

145 1.6 Forms of Business

146

147 Similar to the concept of existing types of financial statements, businesses themselves vary, as well.

148 Business variations are categorized based primarily on ownership.

149 Sole Proprietor:

150

151 Partnership:

152

153 Corporation:

154

155 Corporation management is very regulated and structured

156 Regulations and structure are good for handling up to thousands of individual stockholders.

157

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Chapter 1: Business Decisions and Financial Accounting

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Test Bank Fundamentals Of Financial Accounting 5th Edition by Fred Phillips, Robert Libby, Patricia Libby, completed download: https://testbankarea.com/download/fundamentals-financialaccounting-5th-edition-test-bank-fred-phillips-robert-libby-patricialibby/

Chapter 01 - Introducing Accounting in Business. Chapter Outline

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

Accounting: Decision Making by the Numbers BUSN

Accounting: Decision Making by the Numbers What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally accepted accounting principles?

Accounting: Decision Making by the Numbers What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally accepted accounting principles?

Understanding Accounting & Financial Statements

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

CHAPTER 8: Accounting

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

Copyright 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-1 Accounting What the Numbers Mean CHAPTER 1: Accounting Present and Past Marshall, McManus, and Viele 11th Edition 1-2 Learning Objectives After studying this chapter you should understand and be able

1-1 Accounting What the Numbers Mean CHAPTER 1: Accounting Present and Past Marshall, McManus, and Viele 11th Edition 1-2 Learning Objectives After studying this chapter you should understand and be able

> > > > > > > > Chapter 16. Understanding Accounting and Financial Statements

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

Statement of Cash Flows

CHAPTER 14 Statement of Cash Flows LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Prepare the operating activities section of a statement of cash flows

CHAPTER 14 Statement of Cash Flows LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Prepare the operating activities section of a statement of cash flows

Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession. Learning Objective 2-1

Chapter 2 The CPA Profession. Learning Objective 2-1") Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of: A) each state. B) the Financial

Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of: A) each state. B) the Financial

Twin Valley School District. What is the purpose and importance of accounting? Who are the users of accounting information?

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

The Role of Accountants and Accounting Information

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Slide 1 BA-101 Introduction to Business The Role of Accountants and Accounting Information Chapter Fourteen 1-1 Slide 2 What Is Accounting, and Who Uses Accounting Information? Accounting comprehensive

Accounting and Finance for Lawyers

ACADEMY OF AMERICAN AND INTERNATIONAL LAW Accounting and Finance for Lawyers Stanley Siegel New York University Law School 2015, Stanley Siegel Financial Accounting Part I: Overview and Basic Principles

ACADEMY OF AMERICAN AND INTERNATIONAL LAW Accounting and Finance for Lawyers Stanley Siegel New York University Law School 2015, Stanley Siegel Financial Accounting Part I: Overview and Basic Principles

Financial Statements Additional Information

ILLUSTRATION 1-1 THE ESSENTIAL CHARACTERISTICS OF ACCOUNTING AND FINANCIAL REPORTING Economic Entity Financial Information Accounting Identifies Measures Communicates Financial Reporting Financial Statements

ILLUSTRATION 1-1 THE ESSENTIAL CHARACTERISTICS OF ACCOUNTING AND FINANCIAL REPORTING Economic Entity Financial Information Accounting Identifies Measures Communicates Financial Reporting Financial Statements

Chapter 01. The Role of the Public Accountant in the American Economy. McGraw-Hill/Irwin

Chapter 01 The Role of the Public Accountant in the American Economy McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Assurance services The broad range of information

Chapter 01 The Role of the Public Accountant in the American Economy McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Assurance services The broad range of information

SEC Proposes New Rules To Implement Provisions of the Sarbanes-Oxley Act Regarding Service of Financial Experts on Audit Committees, Codes of Ethics

SEC Proposes New Rules To Implement Provisions of the Sarbanes-Oxley Act Regarding Service of Financial Experts on Audit Committees, Codes of Ethics and Internal Controls October 30, 2002 SEC Proposes

SEC Proposes New Rules To Implement Provisions of the Sarbanes-Oxley Act Regarding Service of Financial Experts on Audit Committees, Codes of Ethics and Internal Controls October 30, 2002 SEC Proposes

SAMPLE EXAM - CHAPTER 1

SAMPLE EXAM - CHAPTER 1 Name: Date: 1. General-purpose financial statements are the product of A) financial accounting. B) managerial accounting. C) both financial and managerial accounting. D) neither

SAMPLE EXAM - CHAPTER 1 Name: Date: 1. General-purpose financial statements are the product of A) financial accounting. B) managerial accounting. C) both financial and managerial accounting. D) neither

Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment. Learning Objective 1-1

Chapter 1 Accounting and the Business Environment. Learning Objective 1-1") Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Horngren's Financial & Managerial Accounting, 5e (Miller) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

CHAPTER 2. Financial Reporting: Its Conceptual Framework CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS NUMBER Q2-1 Conceptual Framework Q2-2 Conceptual Framework Q2-3 Conceptual Framework Q2-4 Conceptual Framework Q2-5 Objective of Financial Reporting Q2-6

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS NUMBER Q2-1 Conceptual Framework Q2-2 Conceptual Framework Q2-3 Conceptual Framework Q2-4 Conceptual Framework Q2-5 Objective of Financial Reporting Q2-6

CHAPTER 2. Financial Reporting: Its Conceptual Framework CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 2 Financial Reporting: Its Conceptual Framework NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 2-1 Conceptual Framework 2-2 Conceptual Framework 2-3

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 2 Financial Reporting: Its Conceptual Framework NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 2-1 Conceptual Framework 2-2 Conceptual Framework 2-3

AUDIT COMMITTEE CHARTER

Page 1 of 7 A. GENERAL 1. PURPOSE The purpose of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of Teck Resources Limited ( the Corporation ) is to provide an open avenue of

Page 1 of 7 A. GENERAL 1. PURPOSE The purpose of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of Teck Resources Limited ( the Corporation ) is to provide an open avenue of

3) Managerial accounting focuses on information for external decision makers. Answer: FALSE

Managerial accounting focuses on information for external decision makers. Answer: FALSE") Horngren's Financial & Managerial Accounting, 4e (Nobles) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

Horngren's Financial & Managerial Accounting, 4e (Nobles) Chapter 1 Accounting and the Business Environment Learning Objective 1-1 1) Accounting is the information system that measures business activities,

CHAPTER 1 INTRODUCTION TO FINANCIAL STATEMENTS

CHAPTER 1 INTRODUCTION TO FINANCIAL STATEMENTS SUMMARY OF QUESTIONS BY LEARNING OBJECTIVE AND BLOOM S TAXONOMY Item LO BT Item LO BT Item LO BT Item LO BT Item LO BT True-False Statements 1. 1 K 9. 2 K

CHAPTER 1 INTRODUCTION TO FINANCIAL STATEMENTS SUMMARY OF QUESTIONS BY LEARNING OBJECTIVE AND BLOOM S TAXONOMY Item LO BT Item LO BT Item LO BT Item LO BT Item LO BT True-False Statements 1. 1 K 9. 2 K

A Review of the Accounting Cycle

CHAPTER 2 A Review of the Accounting Cycle LEARNING OBJECTIVES 1. Identify and explain the basic steps in the accounting process (accounting cycle). Analyze business documents, Journalize transactions,

CHAPTER 2 A Review of the Accounting Cycle LEARNING OBJECTIVES 1. Identify and explain the basic steps in the accounting process (accounting cycle). Analyze business documents, Journalize transactions,

Applying COSO s Enterprise Risk Management Integrated Framework

Applying COSO s Enterprise Risk Management Integrated Framework COSO COSO stands for the Committee Of Sponsoring Organizations of the Treadway Commission. The sponsoring organizations are: Institute of

Applying COSO s Enterprise Risk Management Integrated Framework COSO COSO stands for the Committee Of Sponsoring Organizations of the Treadway Commission. The sponsoring organizations are: Institute of

CHAPTER 1 FINANCIAL ACCOUNTING AND ACCOUNTING STANDARDS. IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual

CHAPTER 1 FINANCIAL ACCOUNTING AND ACCOUNTING STANDARDS IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual Answer No. Description F 1. Definition of financial accounting. T

CHAPTER 1 FINANCIAL ACCOUNTING AND ACCOUNTING STANDARDS IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual Answer No. Description F 1. Definition of financial accounting. T

Revenue from Contracts with Customers: The Final Standard

Revenue from Contracts with Customers: The Final Standard 1 TABLE OF CONTENTS Overview and effective date.... 3 Key provisions of the standard.... 3 Transition.... 12 Planning.... 13 How Experis Finance

Revenue from Contracts with Customers: The Final Standard 1 TABLE OF CONTENTS Overview and effective date.... 3 Key provisions of the standard.... 3 Transition.... 12 Planning.... 13 How Experis Finance

Accounting for Management: Concepts and Tools

Accounting for Management: Concepts and Tools Accounting for Management: Concepts and Tools Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by

Accounting for Management: Concepts and Tools Accounting for Management: Concepts and Tools Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by

Kush Bottles, Inc. A Nevada corporation (the Company )

") Kush Bottles, Inc. A Nevada corporation (the Company ) Audit Committee Charter The Audit Committee (the Committee ) is created by the Board of Directors of the Company (the Board ) to: assist the Board

Kush Bottles, Inc. A Nevada corporation (the Company ) Audit Committee Charter The Audit Committee (the Committee ) is created by the Board of Directors of the Company (the Board ) to: assist the Board

Introduction to Financial Accounting

READING MATERIAL FOR WEEK 1 Introduction to Financial Accounting 1.1 Introduction All organizations, irrespective of the legal status proprietorship, partnership, incorporated company, statutory corporation

READING MATERIAL FOR WEEK 1 Introduction to Financial Accounting 1.1 Introduction All organizations, irrespective of the legal status proprietorship, partnership, incorporated company, statutory corporation

Asset Management Workshop. Midwest Transportation Consortium November 14, 2000

Asset Management Workshop Midwest Transportation Consortium November 14, 2000 Accounting Fundamentals Lincoln University Sherrie Koechling-Andrae Assistant Professor of Accounting Governments Are Unique

Asset Management Workshop Midwest Transportation Consortium November 14, 2000 Accounting Fundamentals Lincoln University Sherrie Koechling-Andrae Assistant Professor of Accounting Governments Are Unique

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018 8:54 PM Financial Accounting Environment Primary Focus of financial accounting is on the information needs

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018 8:54 PM Financial Accounting Environment Primary Focus of financial accounting is on the information needs

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for:

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for: A. Option a B. Option b C. Option c D. Option d 2. What is the primary purpose of financial

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for: A. Option a B. Option b C. Option c D. Option d 2. What is the primary purpose of financial

THE ACCOUNTING INFORMATION SYSTEM

2 THE ACCOUNTING INFORMATION SYSTEM DISCUSSION QUESTIONS 1. The conceptual framework of accounting is the collection of general concepts that logically flow from the objective of financial reporting to

2 THE ACCOUNTING INFORMATION SYSTEM DISCUSSION QUESTIONS 1. The conceptual framework of accounting is the collection of general concepts that logically flow from the objective of financial reporting to

Name Chapter 1--The Environment of Financial Reporting Description Instructions

Name Chapter 1--The Environment of Financial Reporting Description Instructions Modify Question 1 Multiple Choice 0 points Modify Remove Question Exchanges of capital stock and bonds that occur between

Name Chapter 1--The Environment of Financial Reporting Description Instructions Modify Question 1 Multiple Choice 0 points Modify Remove Question Exchanges of capital stock and bonds that occur between

Public Company Advisory Recent developments governing public companies and their officers, directors and investors

January 29, 2003 Public Company Advisory Recent developments governing public companies and their officers, directors and investors SEC Adopts Disclosure Rules on Audit Committee Financial Experts and

January 29, 2003 Public Company Advisory Recent developments governing public companies and their officers, directors and investors SEC Adopts Disclosure Rules on Audit Committee Financial Experts and

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank Link download full: http://testbankcollection.com/download/financial-andmanagerialaccounting-information-for-decisions-4th-edition-by-wild-test-bank/

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank Link download full: http://testbankcollection.com/download/financial-andmanagerialaccounting-information-for-decisions-4th-edition-by-wild-test-bank/

NPO-CX-13: Nonprofit Organization Disclosure Checklist Updated through January 31, 2015

SPD 1 Index 340.10 : Nonprofit Organization Disclosure Checklist Updated through January 31, 2015 Organization: Society of Insurance Research Statement of Financial Position Date: 12/31/2015 Prepared by:

SPD 1 Index 340.10 : Nonprofit Organization Disclosure Checklist Updated through January 31, 2015 Organization: Society of Insurance Research Statement of Financial Position Date: 12/31/2015 Prepared by:

POST-IMPLEMENTATION REVIEW REPORT

JANUARY 2012 POST-IMPLEMENTATION REVIEW REPORT on FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes (Codified in Accounting Standards Codification Topic 740, Income Taxes) FINANCIAL

JANUARY 2012 POST-IMPLEMENTATION REVIEW REPORT on FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes (Codified in Accounting Standards Codification Topic 740, Income Taxes) FINANCIAL

FANNIE MAE CORPORATE GOVERNANCE GUIDELINES

FANNIE MAE CORPORATE GOVERNANCE GUIDELINES 1. The Roles and Responsibilities of the Board and Management On September 6, 2008, the Director of the Federal Housing Finance Authority, or FHFA, our safety

FANNIE MAE CORPORATE GOVERNANCE GUIDELINES 1. The Roles and Responsibilities of the Board and Management On September 6, 2008, the Director of the Federal Housing Finance Authority, or FHFA, our safety

1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders'

Chapter 02 The Balance Sheet True / False Questions 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. True False 2. A debit may

Chapter 02 The Balance Sheet True / False Questions 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. True False 2. A debit may

CHAPTER 1. Accounting and the Business Environment. Chapter Overview

CHAPTER 1 Accounting and the Business Environment Chapter Overview The chapter begins with an introduction to accounting. The text discusses how accounting information is needed by various users individuals,

CHAPTER 1 Accounting and the Business Environment Chapter Overview The chapter begins with an introduction to accounting. The text discusses how accounting information is needed by various users individuals,

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File 6.0-1 Some accounting professionals believe that GAAP may have contributed to the accounting scandals as early as the

Financial Accounting, 1e Chapter 6: Ethics, Internal Control, and IFRS Test Item File 6.0-1 Some accounting professionals believe that GAAP may have contributed to the accounting scandals as early as the

CHAPTER 1 Introduction to financial statements

CHAPTER 1 Introduction to financial statements CHAPTER OVERVIEW Chapter 1 introduces you to a variety of financial accounting topics. You will learn about the main forms of business organisation, and the

CHAPTER 1 Introduction to financial statements CHAPTER OVERVIEW Chapter 1 introduces you to a variety of financial accounting topics. You will learn about the main forms of business organisation, and the

CHARTER of the AUDIT COMMITTEE of the BOARD of DIRECTORS of TYSON FOODS, INC.

I. PURPOSE CHARTER of the AUDIT COMMITTEE of the BOARD of DIRECTORS of TYSON FOODS, INC. The primary function of the Audit Committee (the "Committee") is to assist the Board of Directors of Tyson Foods,

I. PURPOSE CHARTER of the AUDIT COMMITTEE of the BOARD of DIRECTORS of TYSON FOODS, INC. The primary function of the Audit Committee (the "Committee") is to assist the Board of Directors of Tyson Foods,

Chapter 15 Accounting & Financial Analysis

Chapter 15 Accounting & Financial Analysis Professor Muriel Anderson, CPA MGG 150: Introduction to Business November 12, 2013 Chapter Outline How Firms Use Accounting Responsible Financial Reporting Interpreting

Chapter 15 Accounting & Financial Analysis Professor Muriel Anderson, CPA MGG 150: Introduction to Business November 12, 2013 Chapter Outline How Firms Use Accounting Responsible Financial Reporting Interpreting

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Key Learning: Students will review basic accounting concepts learned in the first level course.

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) )") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202 207-9100 Facsimile: (202 862-0757 www.pcaobus.org INSTITUTING DISCIPLINARY PROCEEDINGS, MAKING FINDINGS, AND IMPOSING SANCTIONS In the Matter of

1666 K Street, N.W. Washington, DC 20006 Telephone: (202 207-9100 Facsimile: (202 862-0757 www.pcaobus.org INSTITUTING DISCIPLINARY PROCEEDINGS, MAKING FINDINGS, AND IMPOSING SANCTIONS In the Matter of

Full file at

Chapter 3 Financial Statements, Cash Flows, and Taxes Learning Objectives 1. Discuss generally accepted accounting principles (GAAP) and their importance to the economy. 2. Know the balance sheet identity,

Chapter 3 Financial Statements, Cash Flows, and Taxes Learning Objectives 1. Discuss generally accepted accounting principles (GAAP) and their importance to the economy. 2. Know the balance sheet identity,

September audit deficiencies continue to be significant. description of a deficiency. audit deficiency trends. concluding thoughts

September 2017 home executive summary audit deficiencies continue to be significant pcaob inspections 2017 inspection cycle description of a deficiency audit deficiency trends fvm deficiencies impairment

September 2017 home executive summary audit deficiencies continue to be significant pcaob inspections 2017 inspection cycle description of a deficiency audit deficiency trends fvm deficiencies impairment

Chapter 02. Financial Statements and Accounting Concepts/Principles. Multiple Choice Questions

Chapter 02 Financial Statements and Accounting Concepts/Principles Multiple Choice Questions 1. Which of the following is not a transaction to be recorded in the accounting records of an entity? A. Investment

Chapter 02 Financial Statements and Accounting Concepts/Principles Multiple Choice Questions 1. Which of the following is not a transaction to be recorded in the accounting records of an entity? A. Investment

CHAPTER1. Accounting in Action. PreviewofCHAPTER1. What is Accounting?

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

Chapter 01 Environment and Theoretical Structure of Financial. Accounting Answer Key

Chapter 01 Environment and Theoretical Structure of Financial Accounting Answer Key True / False Questions 1. The primary function of financial accounting is to provide relevant financial information to

Chapter 01 Environment and Theoretical Structure of Financial Accounting Answer Key True / False Questions 1. The primary function of financial accounting is to provide relevant financial information to

Chapter 02 Financial Statements and Cash Flow

Chapter 02 Financial Statements and Cash Flow Multiple Choice Questions 1. The financial statement showing a firm's accounting value on a particular date is the: A. income statement. B. balance sheet.

Chapter 02 Financial Statements and Cash Flow Multiple Choice Questions 1. The financial statement showing a firm's accounting value on a particular date is the: A. income statement. B. balance sheet.

Chapter 1 Accounting and the Business Environment

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Use accounting vocabulary: Chapter 1 Accounting and the Business Environment Business, as a general system, has a number of systems (purchasing, production, marketing, human resource, accounting, and so

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises.

Page 1 of 38 1 Student: 1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises. True False 2. Accrual accounting attempts

Page 1 of 38 1 Student: 1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises. True False 2. Accrual accounting attempts

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q [ ] Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q [ ] Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the quarterly period ended

Appendix 3A. The Cost Method

Appendix 3A The Cost Method 1 2 APPENDIX 3A THE COST METHOD When the parent uses the cost method of accounting, a third consolidation entry (in addition to the basic elimination entry and the intercompany

Appendix 3A The Cost Method 1 2 APPENDIX 3A THE COST METHOD When the parent uses the cost method of accounting, a third consolidation entry (in addition to the basic elimination entry and the intercompany

Test Bank for Corporate Finance 10th Edition by Ross

Test Bank for Corporate Finance 10th Edition by Ross Chapter 02 Financial Statements and Cash Flow Multiple Choice Questions 1. The financial statement showing a firm's accounting value on a particular

Test Bank for Corporate Finance 10th Edition by Ross Chapter 02 Financial Statements and Cash Flow Multiple Choice Questions 1. The financial statement showing a firm's accounting value on a particular

Full file at

Chapter 2 Preparing Financial Statements and Analyzing Business Transactions Multiple-Choice Questions 1. The primary objective of financial reporting is to provide a. external users with financial statements

Chapter 2 Preparing Financial Statements and Analyzing Business Transactions Multiple-Choice Questions 1. The primary objective of financial reporting is to provide a. external users with financial statements

WATERMILL INSTITUTIONAL TRADING LLC (A Limited Liability Company) STATEMENT OF FINANCIAL CONDITION DECEMBER 31, 2017

STATEMENT OF FINANCIAL CONDITION DECEMBER 31, 2017") STATEMENT OF FINANCIAL CONDITION UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ANNUAL AUDITED REPORT FORM X-17A-5 PART Ill OMB APPROVAL OMBNumber: Expires: August 31, 2020 Estimated

STATEMENT OF FINANCIAL CONDITION UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ANNUAL AUDITED REPORT FORM X-17A-5 PART Ill OMB APPROVAL OMBNumber: Expires: August 31, 2020 Estimated

Basic Understanding of the Accounting Industry: Basic Understanding of the Accounting Industry:

Texas University Interscholastic League Contest Event: Accounting The contest focuses on the elementary principles and practices of accounting for sole proprietorship, partnerships and corporations, and

Texas University Interscholastic League Contest Event: Accounting The contest focuses on the elementary principles and practices of accounting for sole proprietorship, partnerships and corporations, and

Chapter 2: Overview. Analyzing and Recording Business Transactions

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Topic: Accounting for Management Fees Based on a Formula. The SEC staff has been asked to provide its views on revenue recognition under

Topic No. D-96 Topic: Accounting for Management Fees Based on a Formula Date Discussed: April 18 19, 2001 The SEC staff has been asked to provide its views on revenue recognition under arrangements (other

Topic No. D-96 Topic: Accounting for Management Fees Based on a Formula Date Discussed: April 18 19, 2001 The SEC staff has been asked to provide its views on revenue recognition under arrangements (other

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C FORM 10-Q

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [x] QUARTERLY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For Quarterly Period Ended March

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [x] QUARTERLY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For Quarterly Period Ended March

Statement of Financial Condition

PRIME DEALER SERVICES CORP. Statement of Financial Condition May 31, 2007 (Unaudited) Investments and services are offered through Prime Dealer Services Corp. Statement of Financial Condition (Unaudited)

PRIME DEALER SERVICES CORP. Statement of Financial Condition May 31, 2007 (Unaudited) Investments and services are offered through Prime Dealer Services Corp. Statement of Financial Condition (Unaudited)

Chapter 6 in your text discusses consolidation working papers when the parent

C H A P T E R 6 ELECTRONIC SUPPLEMENT TO CHAPTER 6 Chapter 6 in your text discusses consolidation working papers when the parent company uses the equity method of accounting. This supplement repeats those

C H A P T E R 6 ELECTRONIC SUPPLEMENT TO CHAPTER 6 Chapter 6 in your text discusses consolidation working papers when the parent company uses the equity method of accounting. This supplement repeats those

CHAPTER 8 Financial Reporting

CHAPTER 8 Financial Reporting Table of Contents Page OVERVIEW... 1 BUDGETS... 3 Comparing Actual Financial Results With the Legally Adopted Budget... 3 Form F-195 Official Budget Document... 3 Form F-198

CHAPTER 8 Financial Reporting Table of Contents Page OVERVIEW... 1 BUDGETS... 3 Comparing Actual Financial Results With the Legally Adopted Budget... 3 Form F-195 Official Budget Document... 3 Form F-198

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C FORM 10-Q

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [x] QUARTERLY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For Quarterly Period Ended December

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [x] QUARTERLY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For Quarterly Period Ended December

International Accounting Standards : Where Do We Go From Here?

International Accounting Standards -- 1973 2003: Where Do We Go From Here? Background Almost 1,200 foreign companies list their stocks on exchanges in the United States (US). Worldwide, there are more

International Accounting Standards -- 1973 2003: Where Do We Go From Here? Background Almost 1,200 foreign companies list their stocks on exchanges in the United States (US). Worldwide, there are more

LIMITED EDITION. Conceptual Framework, Standards, Standard Setting, and Presentation of Financial Statements

LIMITED EDITION Conceptual Framework, Standards, Standard Setting, and Presentation of Financial Statements Contents Learning Outcomes 1 1.1 U.S. Securities and Exchange Commission 2 SEC Rulemaking Process

LIMITED EDITION Conceptual Framework, Standards, Standard Setting, and Presentation of Financial Statements Contents Learning Outcomes 1 1.1 U.S. Securities and Exchange Commission 2 SEC Rulemaking Process

LIFETIME BRANDS, INC. AUDIT COMMITTEE CHARTER

LIFETIME BRANDS, INC. AUDIT COMMITTEE CHARTER ORGANIZATION The Board of Directors (the Board ) of Lifetime Brands, Inc. (the Company ) shall appoint an Audit Committee (the Committee ) of at least three

LIFETIME BRANDS, INC. AUDIT COMMITTEE CHARTER ORGANIZATION The Board of Directors (the Board ) of Lifetime Brands, Inc. (the Company ) shall appoint an Audit Committee (the Committee ) of at least three

ENER-CORE, INC. DISCLOSURE CONTROLS AND PROCEDURES. Adopted September 24, analyzed to determine whether disclosure is appropriate; and

ENER-CORE, INC. DISCLOSURE CONTROLS AND PROCEDURES I. Policy Regarding Public Disclosures Adopted September 24, 2013 Ener-Core, Inc., a Nevada corporation (the Company ), including all subsidiaries, branches

ENER-CORE, INC. DISCLOSURE CONTROLS AND PROCEDURES I. Policy Regarding Public Disclosures Adopted September 24, 2013 Ener-Core, Inc., a Nevada corporation (the Company ), including all subsidiaries, branches

RATIO ANALYSIS. The preceding chapters concentrated on developing a general but solid understanding

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

Proposed Statement on Auditing Standards (SAS) Forming an Opinion and Reporting on Financial Statements

Forming an Opinion and Reporting on Financial Statements") Proposed Statement on Auditing Standards (SAS) Forming an Opinion and Reporting on Financial Statements Matrix Comparison of ISA 700, (Revised and Redrafted) Forming an Opinion and Reporting on Financial

Proposed Statement on Auditing Standards (SAS) Forming an Opinion and Reporting on Financial Statements Matrix Comparison of ISA 700, (Revised and Redrafted) Forming an Opinion and Reporting on Financial

CSP Inc. (Exact name of Registrant as specified in its Charter)

") United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q x o QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q x o QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

Accounting in Action

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File 1.0-1 By taking accounting classes, the student is learning the language of business. Answer: True LO: 1-0 EOC Ref: Vocabulary

Financial Accounting, 1e Chapter 1: Business, Accounting, and You Test Item File 1.0-1 By taking accounting classes, the student is learning the language of business. Answer: True LO: 1-0 EOC Ref: Vocabulary

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS PURPOSE The primary purpose of the Audit Committee (the Committee ) is to assist the Board of Directors (the Board ) in fulfilling

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS PURPOSE The primary purpose of the Audit Committee (the Committee ) is to assist the Board of Directors (the Board ) in fulfilling

Fried, Frank, Harris, Shriver & Jacobson August 26, 2003

August 26, 2003 Timeline Effective Dates for Implementing The Sarbanes-Oxley Act of 2002 ("SOX") and New and Proposed SEC, NYSE & Nasdaq Rules for Non-U.S. Issuers Disclosure 1. CEO/CFO certification A.

August 26, 2003 Timeline Effective Dates for Implementing The Sarbanes-Oxley Act of 2002 ("SOX") and New and Proposed SEC, NYSE & Nasdaq Rules for Non-U.S. Issuers Disclosure 1. CEO/CFO certification A.

Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international financial statements.

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

EVINE LIVE INC. AUDIT COMMITTEE CHARTER

EVINE LIVE INC. AUDIT COMMITTEE CHARTER I. PURPOSE, DUTIES, and RESPONSIBILITIES The audit committee (the Committee ) is established by the board of directors (the board ) of EVINE Live Inc. (the company

EVINE LIVE INC. AUDIT COMMITTEE CHARTER I. PURPOSE, DUTIES, and RESPONSIBILITIES The audit committee (the Committee ) is established by the board of directors (the board ) of EVINE Live Inc. (the company

Learning Objectives. Chapter 2 The Accounting Cycle: During the Period INSTRUCTOR S MANUAL

Financial Accounting 4th Edition SOLUTIONS MANUAL Spiceland Thomas Herrmann Full download at: https://testbankreal.com/download/financial-accounting-4th-editionsolutions-manual-spiceland-thomas-herrmann/

Financial Accounting 4th Edition SOLUTIONS MANUAL Spiceland Thomas Herrmann Full download at: https://testbankreal.com/download/financial-accounting-4th-editionsolutions-manual-spiceland-thomas-herrmann/

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Information about 2017 Inspections

Vol. 2017/3 August 2017 Staff Inspection Brief The staff of the ( PCAOB or Board ) prepares Inspection Briefs to assist auditors, audit committees, investors, and preparers in understanding the PCAOB inspection

Vol. 2017/3 August 2017 Staff Inspection Brief The staff of the ( PCAOB or Board ) prepares Inspection Briefs to assist auditors, audit committees, investors, and preparers in understanding the PCAOB inspection

FINANCIAL TABLE OF CONTENTS. 1. Presentation order of the major components of an income and retained earnings Statement

Becker CPA Review Financial FINANCIAL TABLE OF CONTENTS TOPIC 1: REVENUE RECOGNITION and ACCOUNTING CHANGE 1. Presentation order of the major components of an income and retained earnings Statement......

Becker CPA Review Financial FINANCIAL TABLE OF CONTENTS TOPIC 1: REVENUE RECOGNITION and ACCOUNTING CHANGE 1. Presentation order of the major components of an income and retained earnings Statement......

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

Chapter 4 Income Statement 4-1

Chapter 4 Income Statement 1. The concept of income 2. Why income measure is important 3. How income is measured 4. The format of an income statement 5. The components of an income statement 6. The comprehensive

Chapter 4 Income Statement 1. The concept of income 2. Why income measure is important 3. How income is measured 4. The format of an income statement 5. The components of an income statement 6. The comprehensive

BLOOM ENERGY CORPORATION CORPORATE GOVERNANCE GUIDELINES. (As adopted on May 10, 2018)

") BLOOM ENERGY CORPORATION CORPORATE GOVERNANCE GUIDELINES (As adopted on May 10, 2018) The following Corporate Governance Guidelines have been adopted by the Board of Directors (the Board ) of Bloom Energy

BLOOM ENERGY CORPORATION CORPORATE GOVERNANCE GUIDELINES (As adopted on May 10, 2018) The following Corporate Governance Guidelines have been adopted by the Board of Directors (the Board ) of Bloom Energy

BUS512M Session 10. Leases, GRI, Fraud and Other Enduring Accounting Wonders

BUS512M Session 10 Leases, GRI, Fraud and Other Enduring Accounting Wonders Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs Management

BUS512M Session 10 Leases, GRI, Fraud and Other Enduring Accounting Wonders Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs Management

Chapter One Partnerships

Chapter One Partnerships DEFINED...1-1 AGREEMENTS...1-1 DIVISION OF PROFITS...1-1 ADMISSION OF A PARTNER...1-1 PURCHASE OF AN INTEREST...1-1 Payment to an Existing Partner Payment to More Than One Partner

Chapter One Partnerships DEFINED...1-1 AGREEMENTS...1-1 DIVISION OF PROFITS...1-1 ADMISSION OF A PARTNER...1-1 PURCHASE OF AN INTEREST...1-1 Payment to an Existing Partner Payment to More Than One Partner

FORM 10-Q. ADVANCED OXYGEN TECHNOLOGIES, INC. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

Chapter = c01 Date: Jan 28, 2011 Time: 4:57 pm PART ONE. The Basics of Bookkeeping COPYRIGHTED MATERIAL

PART ONE The Basics of Bookkeeping COPYRIGHTED MATERIAL CHAPTER 1 Bookkeeping Basics What Is Bookkeeping? Bookkeeping is how you record and report on the financial transactions of a business. The bookkeeper

PART ONE The Basics of Bookkeeping COPYRIGHTED MATERIAL CHAPTER 1 Bookkeeping Basics What Is Bookkeeping? Bookkeeping is how you record and report on the financial transactions of a business. The bookkeeper

Related Download: Solutions Manual Accounting 26th Edition Warren Reeve Duchac

Test Bank Accounting 26th Edition Warren Reeve Duchac. Completed download: https://testbankarea.com/download/accounting-26th-edition-warren-reeve-duchactest-bank/ Related Download: Solutions Manual Accounting

Test Bank Accounting 26th Edition Warren Reeve Duchac. Completed download: https://testbankarea.com/download/accounting-26th-edition-warren-reeve-duchactest-bank/ Related Download: Solutions Manual Accounting

Requirements for Public Company Boards

Public Company Advisory Group Requirements for Public Company Boards Including IPO Transition Rules November 2016 Introduction. 1 The Role and Authority of Independent Directors. 2 The Definition of Independent

Public Company Advisory Group Requirements for Public Company Boards Including IPO Transition Rules November 2016 Introduction. 1 The Role and Authority of Independent Directors. 2 The Definition of Independent

Sarbanes-Oxley Update: Impact on Public Companies, Management, and Audit Committees. W. Lynn Loden Deloitte & Touche LLP

Sarbanes-Oxley Update: Impact on Public Companies, Management, and Audit Committees W. Lynn Loden Deloitte & Touche LLP Dynamic and Defining Times The Sarbanes-Oxley Act of 2002 (the Act ) Unprecedented

Sarbanes-Oxley Update: Impact on Public Companies, Management, and Audit Committees W. Lynn Loden Deloitte & Touche LLP Dynamic and Defining Times The Sarbanes-Oxley Act of 2002 (the Act ) Unprecedented

Chapter 01 Introduction To Corporate Finance

Fundamentals of Corporate Finance 11th Edition Ross Westerfield Jordan Test Bank Complete download Test Bank for Fundamentals of Corporate Finance 11th Edition Ross Westerfield Jordan: Complete download

Fundamentals of Corporate Finance 11th Edition Ross Westerfield Jordan Test Bank Complete download Test Bank for Fundamentals of Corporate Finance 11th Edition Ross Westerfield Jordan: Complete download

NASBA 103 rd Annual Meeting

NASBA 103 rd Annual Meeting James L. Kroeker Chief Accountant U.S. Securities and Exchange Commission October 2010 1 2 t What We ve Been Working On " IFRS Work Plan Overview and Update " Major Convergence

NASBA 103 rd Annual Meeting James L. Kroeker Chief Accountant U.S. Securities and Exchange Commission October 2010 1 2 t What We ve Been Working On " IFRS Work Plan Overview and Update " Major Convergence