BUS512M Session 10. Leases, GRI, Fraud and Other Enduring Accounting Wonders

|

|

|

- Helena Gray

- 6 years ago

- Views:

Transcription

1 BUS512M Session 10 Leases, GRI, Fraud and Other Enduring Accounting Wonders

2 Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs Management has strong incentive to manage the balance sheet by using off-balance-sheet financing i.e., operating leases Have 3 years to bring on the books, management should be preparing.

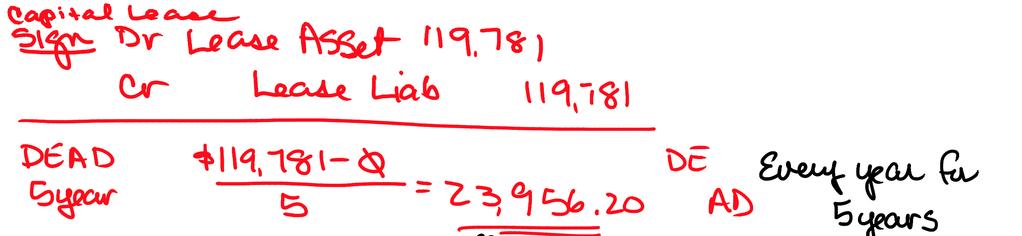

3 Leases: operating or capital FASB issued SFAS No. 13, which requires certain leases to be recorded as capital leases. Capital leases record the leased asset as a capital asset, and reflect the present value of the related payment contract as a liability. Requirements of SFAS No record as capital lease for the lessee if any one of the following is present in the lease: Title transfers at the end of the lease period, The lease contains a bargain purchase option, The lease life is at least 75% of the useful life of the asset, or The lessee pays for at least 90% of the fair market value of the lease.

4 Capital Lease

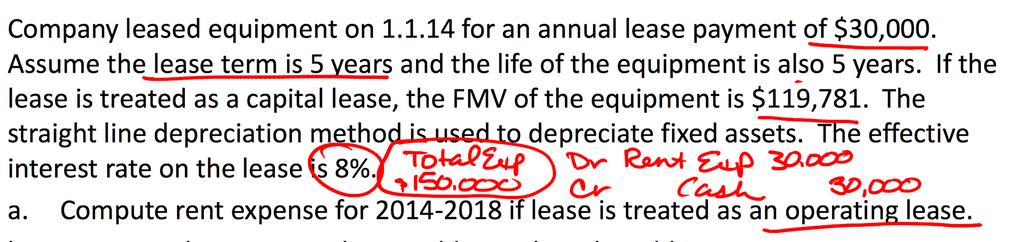

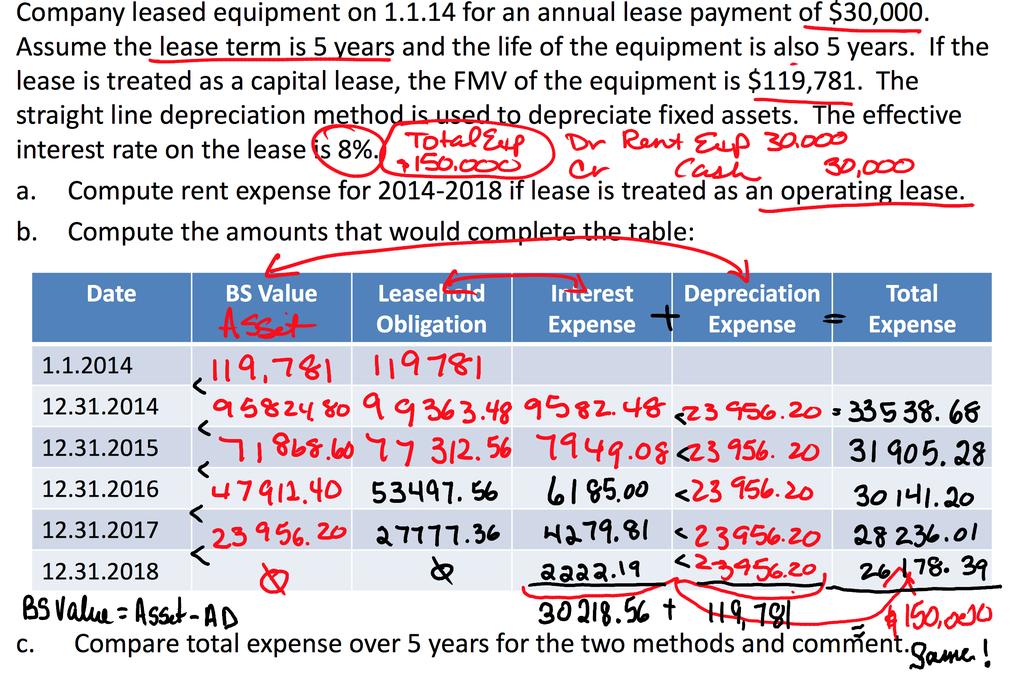

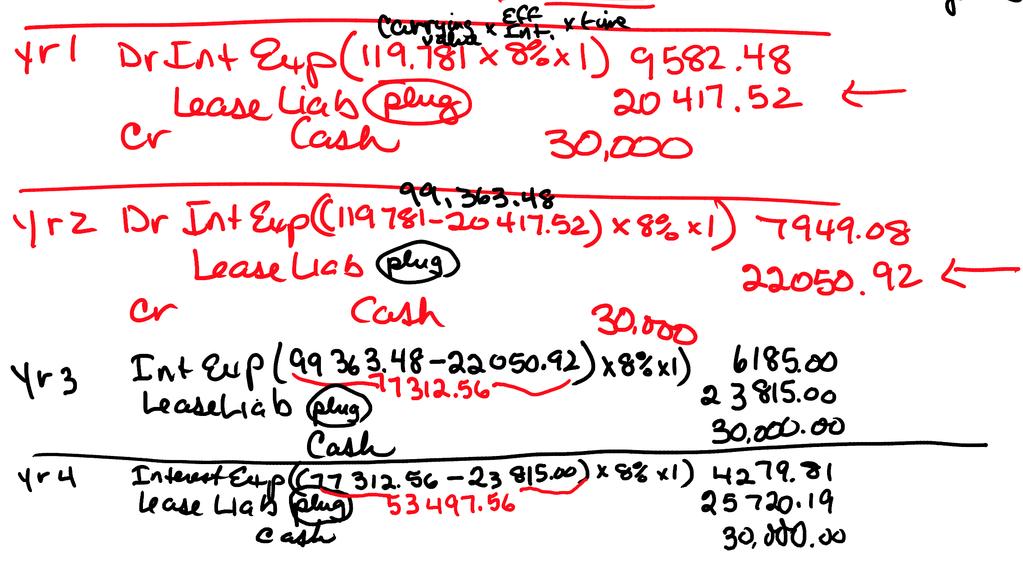

5 P11-14 Capital and Operating Leases Company leased equipment on for an annual lease payment of $30,000. Assume the lease term is 5 years and the life of the equipment is also 5 years. If the lease is treated as a capital lease, the FMV of the equipment is $119,781. The straight line depreciation method is used to depreciate fixed assets. The effective interest rate on the lease is 8%. a. Compute rent expense for if lease is treated as an operating lease. b. Compute the amounts that would complete the table: Date BS Value Leasehold Obligation Interest Expense Depreciation Expense Total Expense c. Compare total expense over 5 years for the two methods and comment.

6

7

8

9

10

11 The SEC mandated the use of XBRL for public company reporting and other reporting applications: Public Company Reporting all public companies must file in XBRL format; companies with worldwide public float greater than $5 billion to comply starting with period ending June 2009; all other large accelerated filers to comply starting with period ending June 2010; all other public companies comply with period ending June Risk Return Summary Portion of Mutual Fund Prospectus mutual funds must begin publishing the risk return summary portion of their prospectuses in XBRL format starting January 1, Credit Rating Agencies must report ratings actions (initial rating, upgrades, downgrades, etc.) in XBRL format. The SEC and XBRL US have resources available to help public company preparers get educated, identify tools and resources to tag their financials and create their own XBRLformatted financials.

12 XBRL (extensible Business Reporting Language) is a freely available and global standard for exchanging business information. XBRL is a technology language for the electronic communication of business and financial data and is being implemented worldwide. XBRL-formatted documents enable greater efficiency, improved accuracy and reliability as well as cost savings to those involved in supplying and using financial and business information data. What XBRL can do: XBRL allows for the creation of interactive, intelligent data. Each piece of business information has detailed descriptive and contextual information wrapped around it, so that the data becomes machine-readable and can be automatically processed and analyzed. XBRL allows business reporting information to be reused and repurposed. A financial or business report created once can be used to create many documents in different formats--html, ASCII text, Microsoft Word or Excel with no loss of accuracy or integrity. XBRL adds value to every step of an organization s business information reporting. The entire reporting chain of business information -- from data collection through internal reporting and external reporting -- will be made more efficient and accurate and will contain more useful data. XBRL enhances the ability to compare information from one organization or entity to another, because XBRL lays out a common set of definitions by which all organizations tag their data. XBRL allows for unique reporting situations, because it can be extended by a single reporting entity by adding special elements that may be needed to best represent that company.

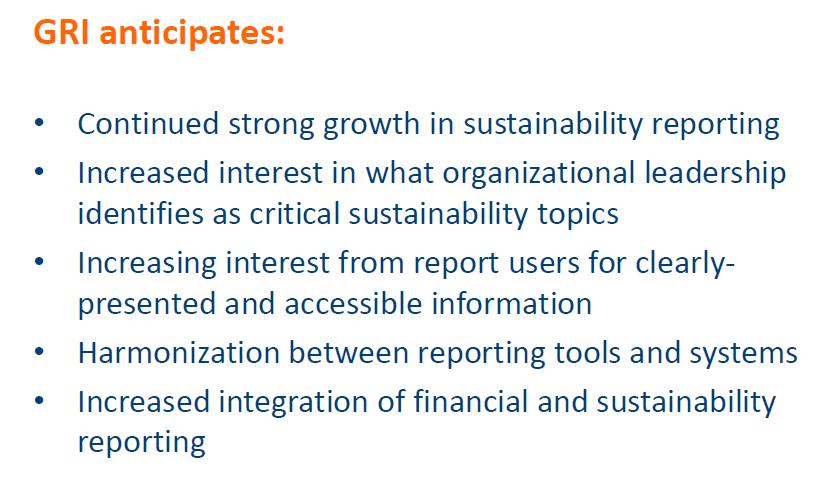

13 Sustainability Reporting The Global Reporting Initiative (GRI) is a nonprofit organization that promotes economic sustainability. It produces one of the world's most prevalent standards for sustainability reporting also known as ecological footprint reporting, environmental social governance (ESG) reporting, triple bottom line (TBL) reporting, and corporate social responsibility (CSR) reporting. GRI seeks to make sustainability reporting by all organizations as routine as, and comparable to, financial reporting. A sustainability report is an organizational report that gives information about economic, environmental, social and governance performance.

14

15

16

17

18

19

20

21

22 nsibility/environment/documents/sustainability Brochure_pages.pdf

23

24

25

26

27

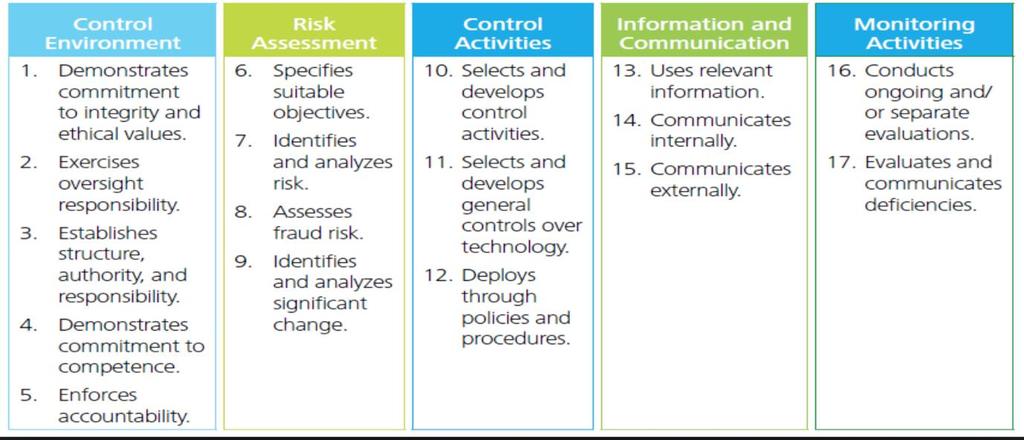

28 COSO Announces Internal Control Certificate Program NEW YORK, Dec. 16, The Committee of Sponsoring Organizations of the Treadway Commission (COSO) today announced an Internal Control Certificate Program that offers financial professionals, including internal auditors and CPAs, the opportunity to earn a professional certificate in the 2013 COSO Internal Control-Integrated Framework. The program is a combination of self-paced learning and a hands-on workshop, followed by an online examination. Upon successful completion of all three components, candidates will receive an official COSO certificate that demonstrates their ability to design and implement an effective system of internal control utilizing the COSO Internal Control-Integrated Framework. This unique course can be offered only through one of COSO s five sponsoring organizations: American Accounting Association (AAA), American Institute of CPAs (AICPA), Financial Executives International (FEI), IMA-The Association of Accountants and Financial Professionals in Business, and The Institute of Internal Auditors (IIA). The IIA and AICPA are offering the three-day workshops throughout 2016, AAA plans to train its staff on the Certificate, and the other sponsors are actively promoting the benefits of the offering to their members. An internal control system requires the use of judgment to monitor and assess its effectiveness, and it must provide insight on the application of controls. The new Certificate, through a blend of self-paced learning and live classroom training, offers a unique opportunity to develop expertise in designing, implementing, and conducting an internal control system, said Robert B. Hirth Jr., COSO Chair. The Certificate is much like a diploma, and can be earned through completion of training and an end-of-course examination. This program, which counts for 25.5 CPE credits, takes the user through the Framework from start to finish using realworld scenarios, allowing participants to: Understand the principles-based approach Identify and analyze risks Develop a confidence in the internal control system Learn from experts and share their experiences with peers "I believe the Certificate provides great value to risk and control professionals including chief audit executives (CAEs) looking to enhance their staffs qualifications, Hirth said. The goal of the online learning component is to introduce key Framework concepts to participants and to start them thinking about it in the context of their organizations. For a listing of live training events in 2016, please visit coso.org.

and interpreted")

29 Evolution of Accounting Telling the story of business by converting events into numbers Resources Unit of Measure Valuation Responsibilities Capital Cost-Benefits Exchange Transactions A=L+OE Rise of Corporations Going Concern & Business Entity Net Income, Contributed Capital, Retained Earnings, & Dividends Depreciation, Amortization, & Depletion Financial reporting & Auditing Product & Service Costing Accounting kept the books (locked the data up) and interpreted the data for others.

30 Financial Accounting Fundamentals Assumptions Economic Entity (identified and measured) Fiscal Period (periodicity) Going Concern (life indefinite) Stable Dollar (across time) Measurement Principles Objectivity (Verifiable and documented) Matching and Revenue Recognition (costs & benefits) Consistency (methods same across time) Two Exceptions Materiality little to no effect on user decisions Conservatism -understate assets, overstate liabilities, accelerate losses, and delay gains (due to legal liability) Valuation Input Market (purchase)-original, replacement Output Market (sell)-present, fair market Financial Statements: Original (Historic) Cost: Land, LT Invt Lower of Cost or Market: Inventory Net Realizable Value: net AR Net Book Value: PP&E, Intang. Face: Cash, Current liabilities Fair Market Value (sales price): ST Invt Present Value: LT NR & LTL IFRS v. US GAAP Principles based Rules based

31 Annual Report Treasure Hunt-The 6 Key Numbers Revenue Income (Loss) Cash Flow from (used by) Operating Activities Assets Liabilities Stockholders Equity Prove the Accounting Equation Can you tell the type of business? Service, Retail, Manufacturing

32

The publication of the magazine every month.")

33 Crucial event(s) in Revenue Recognition 1. The company has completed a significant portion of the production and sales efforts. 2. The amount of revenue can be objectively measured. 3. The company has incurred the majority of costs, and remaining costs can be reasonably estimated, and 4. Cash collection is reasonably assured. Discuss the propriety of timing the recognition of revenue from customers and advertising in the company s accounts with: a) The cash sale of the magazine subscription. b) The publication of the magazine every month. c) Both events, by recognizing a portion of the revenue with the cash sale of the magazine subscription and a portion of the revenue with the publication of the magazine every month.

34 Today and Tomorrow Transformative Technologies Now data unlocked with 24/7 access to anyone via Internet & Cloud. Massive quantities of financial and nonfinancial data. Making sense of business to an audience-what info important? Point of view of who s telling the story- single entity or helicopter? Accountants still can be the storytellers by bringing meaning to data through the process of: Understanding the Concepts first Then applying the best Accounting Tools To analyze and make Business Decisions Resources-Events-Agents

35 Resources-Events-Agents

36

37

38

39 Case Your class will be divided into teams. The task of each team is to determine if any fraud was committed in this company between April and July and to prepare a report of your findings. To investigate any suspected frauds, follow the requirements below using the materials in the Student Handouts and any additional information you think you might need to investigate the frauds. To successfully complete this assignment, each team must determine what additional information is needed for the various frauds. REQUIREMENTS You believe that a good forensic investigation is built on instinct and experience, and you like to remember to look up from the numbers and consider the people who created those numbers. You have previously developed the following methodology that your team will follow. Your Firm s Methodology for Forensic Accounting Investigations Step 1: Obtain an understanding of the company Step 2: Brainstorm and Hypothesize 1. List up to 3 hunch areas you want to investigate 2. Best hunch at perpetrator(s) Step 3: Plan the investigation Step 4: Execute the plan Step 5: Discuss findings and investigate further Step 6: Prepare the main points of a Final Report

40 Case Debrief Step 6: Prepare the main points of a Final Report At the conclusion of your investigation you will begin to prepare a final report. This report will include: 1. A brief statement of your conclusion (fraud or no fraud at TBC) 2. If a fraud or frauds have occurred, you will present the following for each fraud: a. Identification of the perpetrator; b. Description of the fraud; c. Evidence of the pressure or motive the perpetrator had to commit the fraud; d. Evidence the perpetrator had the opportunity and knowledge to commit the fraud; e. Evidence of the perpetrator s intent. That is, you must show that the perpetrator s actions were not simply a mistake or ignorance that resulted in the fraud, but a deliberate action; f. Evidence of how the perpetrator benefited from the crime.

41

42 And we ll all live happily ever after!

BUS512M Session 10. Leases, and Enduring Accounting Wonders

BUS512M Session 10 Leases, and Enduring Accounting Wonders Homework see handout Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs Management

BUS512M Session 10 Leases, and Enduring Accounting Wonders Homework see handout Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs Management

Draw an Accountant. Who/What Information needs for business/financial decisions

Draw an Accountant. Who/What Information needs for business/financial decisions BUS210 Session 1 Handouts: To Do List Syllabus Teaching Perspectives Inventory (TPI) Class Handout Attendance: Sign roster!!!

Draw an Accountant. Who/What Information needs for business/financial decisions BUS210 Session 1 Handouts: To Do List Syllabus Teaching Perspectives Inventory (TPI) Class Handout Attendance: Sign roster!!!

SEC Proposes New Rules Mandating XBRL-Format Filings. by Joseph D. Kline, Elaine Wolff and William L. Tolbert, Jr.

Corporate SEC Client Alert May 22, 2008 SEC Proposes New Rules Mandating XBRL-Format Filings by Joseph D. Kline, Elaine Wolff and William L. Tolbert, Jr. On May 14, 2008, the Securities and Exchange Commission

Corporate SEC Client Alert May 22, 2008 SEC Proposes New Rules Mandating XBRL-Format Filings by Joseph D. Kline, Elaine Wolff and William L. Tolbert, Jr. On May 14, 2008, the Securities and Exchange Commission

Measurement Fundamentals BUS 210. Chapter 3

Measurement Fundamentals BUS 210 Chapter 3 What do you know? Financial Accounting Fundamentals Valuation Input Market (purchase)-original, replacement Output Market (sell)-present, fair market Financial

Measurement Fundamentals BUS 210 Chapter 3 What do you know? Financial Accounting Fundamentals Valuation Input Market (purchase)-original, replacement Output Market (sell)-present, fair market Financial

Accounting Concepts, Time Value of Money, and Financial Analysis & Reporting BUS512M. November 23, 2013 Session 3 7:00-10:30 Susan Crosson

Accounting Concepts, Time Value of Money, and Financial Analysis & Reporting BUS512M November 23, 2013 Session 3 7:00-10:30 Susan Crosson Homework See Handout Today s Learning Outcomes Time Value of Money

Accounting Concepts, Time Value of Money, and Financial Analysis & Reporting BUS512M November 23, 2013 Session 3 7:00-10:30 Susan Crosson Homework See Handout Today s Learning Outcomes Time Value of Money

4 Criteria for Recognizing Revenue

What do you know? E4-7 Preparing financial statements Taken from the 2008 annual report of Bristol-Myers Squibb, a world-leading drug company (dollars in millions), reconstruct the financials. Cost of

What do you know? E4-7 Preparing financial statements Taken from the 2008 annual report of Bristol-Myers Squibb, a world-leading drug company (dollars in millions), reconstruct the financials. Cost of

Financial Statements Additional Information

ILLUSTRATION 1-1 THE ESSENTIAL CHARACTERISTICS OF ACCOUNTING AND FINANCIAL REPORTING Economic Entity Financial Information Accounting Identifies Measures Communicates Financial Reporting Financial Statements

ILLUSTRATION 1-1 THE ESSENTIAL CHARACTERISTICS OF ACCOUNTING AND FINANCIAL REPORTING Economic Entity Financial Information Accounting Identifies Measures Communicates Financial Reporting Financial Statements

Accounting, financial reporting, and regulatory developments for public companies

Accounting, financial reporting, and regulatory developments for public companies SECOND QUARTER 2018 In this update, we highlight some of the more important 2018 second-quarter accounting, financial reporting,

Accounting, financial reporting, and regulatory developments for public companies SECOND QUARTER 2018 In this update, we highlight some of the more important 2018 second-quarter accounting, financial reporting,

Accounting and Financial Reporting Developments for Public Companies

Accounting and Financial Reporting Developments for Public Companies SECOND QUARTER UPDATE 2018 The Quarterly Newsletter is a quarterly publication from EKS&H s Technical Accounting and Auditing Group.

Accounting and Financial Reporting Developments for Public Companies SECOND QUARTER UPDATE 2018 The Quarterly Newsletter is a quarterly publication from EKS&H s Technical Accounting and Auditing Group.

July 30, Secretary Securities and Exchange Commission 100F Street, NE Washington, D.C

July 30, 2008 Secretary Securities and Exchange Commission 100F Street, NE Washington, D.C. 20549-1090 RE: File No. S7-11-08, Interactive Data to Improve Financial Reporting Dear Sir or Madame: On behalf

July 30, 2008 Secretary Securities and Exchange Commission 100F Street, NE Washington, D.C. 20549-1090 RE: File No. S7-11-08, Interactive Data to Improve Financial Reporting Dear Sir or Madame: On behalf

SEC Proposes Amendments Requiring Companies to use extensible Business Reporting Language, or XBRL

July 22, 2008 SEC Proposes Amendments Requiring Companies to use extensible Business Reporting Language, or XBRL On May 30, 2008, the SEC published for public comment proposed amendments under the U.S.

July 22, 2008 SEC Proposes Amendments Requiring Companies to use extensible Business Reporting Language, or XBRL On May 30, 2008, the SEC published for public comment proposed amendments under the U.S.

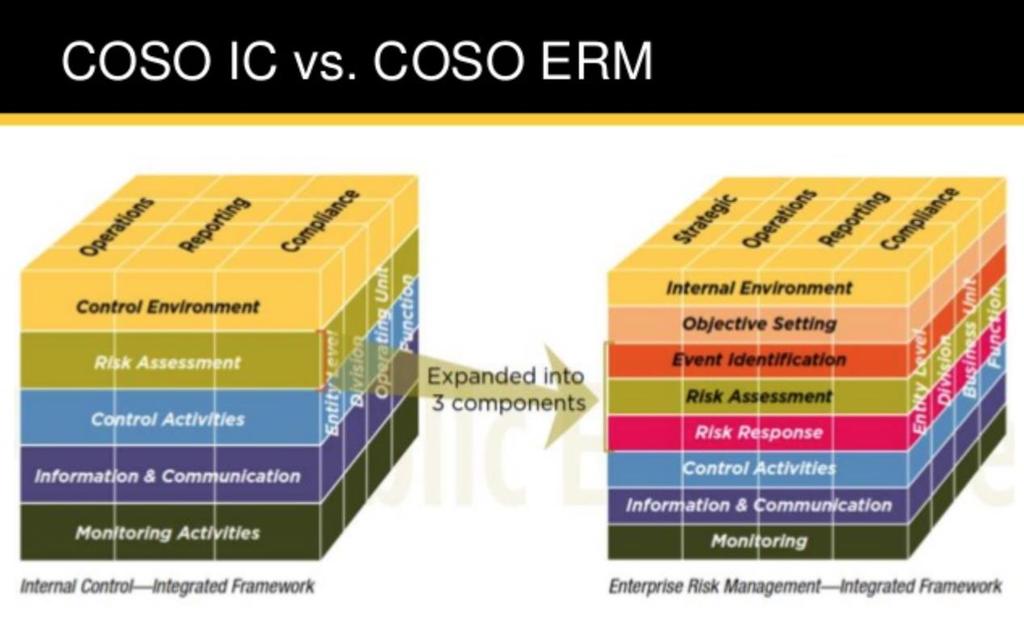

Applying COSO s Enterprise Risk Management Integrated Framework

Applying COSO s Enterprise Risk Management Integrated Framework COSO COSO stands for the Committee Of Sponsoring Organizations of the Treadway Commission. The sponsoring organizations are: Institute of

Applying COSO s Enterprise Risk Management Integrated Framework COSO COSO stands for the Committee Of Sponsoring Organizations of the Treadway Commission. The sponsoring organizations are: Institute of

Accounting Standards Update. Mike Renzelman Shareholder, Accounting, Assurance and Advisory Services

Accounting Standards Update Mike Renzelman Shareholder, Accounting, Assurance and Advisory Services 1 Agenda FASB Private Company Council AICPA SEC PCAOB On the Horizon 2 FASB International Convergence

Accounting Standards Update Mike Renzelman Shareholder, Accounting, Assurance and Advisory Services 1 Agenda FASB Private Company Council AICPA SEC PCAOB On the Horizon 2 FASB International Convergence

Accounting updates. Kaustav Ghose

Accounting updates Kaustav Ghose New guidance of Financial Accounting Standards Board (FASB) on the definition of a business The FASB has changed its definition of a business in an effort to assist entities

Accounting updates Kaustav Ghose New guidance of Financial Accounting Standards Board (FASB) on the definition of a business The FASB has changed its definition of a business in an effort to assist entities

Chapter 01 - Introducing Accounting in Business. Chapter Outline

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

1.1 Generally Accepted Accounting Principles (GAAP) 1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation

1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation") 1. General Topics 1.1 Generally Accepted Accounting Principles (GAAP) 1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation 1.3 The Accounting Cycle 1.4 Business Ethics 1.5 Purpose

1. General Topics 1.1 Generally Accepted Accounting Principles (GAAP) 1.2 Rules of Double- Entry Accounting/ Transaction Analysis/ Accounting Equation 1.3 The Accounting Cycle 1.4 Business Ethics 1.5 Purpose

International Financial Reporting Standards (IFRS) and 2019 Updates

and 2019 Updates") International Financial Reporting Standards (IFRS) and 2019 Updates Page 1 of 11 Why Attend Our 'International Financial Reporting Standards (IFRS) and 2019 Updates' course will help build the knowledge

International Financial Reporting Standards (IFRS) and 2019 Updates Page 1 of 11 Why Attend Our 'International Financial Reporting Standards (IFRS) and 2019 Updates' course will help build the knowledge

Course 1600: International Oil and Gas Accounting and Financial Management Immersion Workshop (8 days)

") Course 1600: International Oil and Gas Accounting and Financial Management Immersion Workshop (8 days) Course level: Location: CPE / CPD: Overview Dubai 64 hours Start date: 24 Nov 2019 Finish date: 3

Course 1600: International Oil and Gas Accounting and Financial Management Immersion Workshop (8 days) Course level: Location: CPE / CPD: Overview Dubai 64 hours Start date: 24 Nov 2019 Finish date: 3

CPAs. The preferred choice for assurance on sustainability information

CPAs. The preferred choice for assurance on sustainability information i A fiercely competitive economic climate. Escalating policy developments and environmental regulations. The impact of climate disruption

CPAs. The preferred choice for assurance on sustainability information i A fiercely competitive economic climate. Escalating policy developments and environmental regulations. The impact of climate disruption

Accounting What the Numbers Mean. Cash. What are Current Assets? Cash Equivalents. Cash Management Goals 5-1

5-1 Accounting What the Numbers Mean CHAPTER 5: Accounting for and Presentation of Current Assets Marshall, McManus, and Viele 11th Edition 5-1 5-2 What are Current Assets? Current assets include cash

5-1 Accounting What the Numbers Mean CHAPTER 5: Accounting for and Presentation of Current Assets Marshall, McManus, and Viele 11th Edition 5-1 5-2 What are Current Assets? Current assets include cash

FASB Update Private Company Focus

FASB Update Private Company Focus RKL Accounting & Auditing Conference Michael Cheng, PCC Coordinator The views expressed in this presentation are those of the presenters. Official positions of the FASB

FASB Update Private Company Focus RKL Accounting & Auditing Conference Michael Cheng, PCC Coordinator The views expressed in this presentation are those of the presenters. Official positions of the FASB

IFRS: 2018 Updates. Why Attend. Course Methodology. Course Objectives. Target Audience. Target Competencies. Associations

IFRS: Updates Why Attend Our International Financial Reporting Standards (IFRS): updates training course will help build the knowledge you need in IFRS for success in today's global business world. Like

IFRS: Updates Why Attend Our International Financial Reporting Standards (IFRS): updates training course will help build the knowledge you need in IFRS for success in today's global business world. Like

Audit Committee Evolving Trends

1 Audit Committee Evolving Trends Arthur Bill and Mark Plichta, Foley & Lardner LLP Richard Herlin, Deloitte & Touche LLP Isaac Kaufman, Advanced Medical Management Cheryl Mayberry McKissack, Nia Enterprises,

1 Audit Committee Evolving Trends Arthur Bill and Mark Plichta, Foley & Lardner LLP Richard Herlin, Deloitte & Touche LLP Isaac Kaufman, Advanced Medical Management Cheryl Mayberry McKissack, Nia Enterprises,

Analysis of Financial Statements and Statement of Cash Flows BUS512M. December 16, 2016 Session 2 8:00-noon Susan Crosson

Analysis of Financial Statements and Statement of Cash Flows BUS512M December 16, 2016 Session 2 8:00-noon Susan Crosson P4-20 Reverse T-account analysis You are a credit analyst for a bank. Badger Business

Analysis of Financial Statements and Statement of Cash Flows BUS512M December 16, 2016 Session 2 8:00-noon Susan Crosson P4-20 Reverse T-account analysis You are a credit analyst for a bank. Badger Business

Governmental Finance Online Courses

Governmental Finance Online Courses Center for Continuing Education Carl Vinson Institute of Government Introductory Governmental Accounting Part I & Part II Intermediate Governmental Accounting These

Governmental Finance Online Courses Center for Continuing Education Carl Vinson Institute of Government Introductory Governmental Accounting Part I & Part II Intermediate Governmental Accounting These

MAKING SENSE OF BALANCE SHEETS. Ronald Sereika, CCE, CEW

MAKING SENSE OF BALANCE SHEETS Ronald Sereika, CCE, CEW How to start analysis process The user of a firm s annual report can expect to encounter a great quantity of information that encompasses the required

MAKING SENSE OF BALANCE SHEETS Ronald Sereika, CCE, CEW How to start analysis process The user of a firm s annual report can expect to encounter a great quantity of information that encompasses the required

Twin Valley School District. What is the purpose and importance of accounting? Who are the users of accounting information?

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

XBRL and Accounting Update. Presented by Avi Alpert

XBRL and Accounting Update Presented by Avi Alpert Toolbox for Finance: An Online Knowledge Sharing Community Mission Toolbox for Finance helps finance professionals do their jobs better by enabling them

XBRL and Accounting Update Presented by Avi Alpert Toolbox for Finance: An Online Knowledge Sharing Community Mission Toolbox for Finance helps finance professionals do their jobs better by enabling them

ANSWER SHEET EXAMINATION #1 29) Problem 1 30) 31) 32) 33) 34) 35) 36) 37) 10) 38) 11) 12) Problem 2 Problem 3 Problem 4 13) 14) 15) 16) 17) 18) 19)

Problem 1 30) 31) 32) 33) 34) 35) 36) 37) 10) 38) 11) 12) Problem 2 Problem 3 Problem 4 13) 14) 15) 16) 17) 18) 19)") ANSWER SHEET EXAMINATION #1 1) B 29) A Problem 1 2) B 30) D B 01 3) D 31) B A 02 4) D 32) B D 03 5) C 33) A A 04 6) C 34) C B 05 7) B 35) B A 06 8) B 36) B B 07 9) D 37) D C 08 10) B 38) D C 09 11) D D

ANSWER SHEET EXAMINATION #1 1) B 29) A Problem 1 2) B 30) D B 01 3) D 31) B A 02 4) D 32) B D 03 5) C 33) A A 04 6) C 34) C B 05 7) B 35) B A 06 8) B 36) B B 07 9) D 37) D C 08 10) B 38) D C 09 11) D D

Financial Accounting. 1. Introduction. Agenda. Financial Accounting prof. univ. dr. TIRON TUDOR Adriana

Financial Accounting prof. Adriana Tiron Tudor- course lect. Vasile Cardos- practice Accounting Crossword Puzzle Word Scramble Agenda 2. Organizational matters 4. Must to know test your knowledges Objectives

Financial Accounting prof. Adriana Tiron Tudor- course lect. Vasile Cardos- practice Accounting Crossword Puzzle Word Scramble Agenda 2. Organizational matters 4. Must to know test your knowledges Objectives

SU 3.1 Property, Plant, and Equipment

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

Year-End Update From the SEC, PCAOB and FASB. January 19, 2016

Year-End Update From the SEC, PCAOB and FASB January 19, 2016 Agenda for Today Topics to Discuss: Update from AICPA Conference on Current SEC & PCAOB Developments ASU FASB Updates for 2015 and 2014 Leases

Year-End Update From the SEC, PCAOB and FASB January 19, 2016 Agenda for Today Topics to Discuss: Update from AICPA Conference on Current SEC & PCAOB Developments ASU FASB Updates for 2015 and 2014 Leases

1. Reference for Financial Report Conceptual Model Domain Semantics

1. Reference for Financial Report Conceptual Model Domain Semantics Financial report semantics are identified and articulated within the Financial Report Semantics and Dynamics Theory 1. This section covers

1. Reference for Financial Report Conceptual Model Domain Semantics Financial report semantics are identified and articulated within the Financial Report Semantics and Dynamics Theory 1. This section covers

Accounting and financial reporting activities for private companies

Accounting and financial reporting activities for private companies SECOND-QUARTER 2018 In this update, we highlight some of the more important 2018 second-quarter accounting and financial reporting activities

Accounting and financial reporting activities for private companies SECOND-QUARTER 2018 In this update, we highlight some of the more important 2018 second-quarter accounting and financial reporting activities

Certificate in Professional Accounting. Contents are subject to change. For the latest updates visit

Certificate in Professional Accounting Page 1 of 9 Why Attend This course is essential for accounting and finance employees in every company as it covers the rules and regulations under International Financial

Certificate in Professional Accounting Page 1 of 9 Why Attend This course is essential for accounting and finance employees in every company as it covers the rules and regulations under International Financial

Michael Ohata Managing Director - KPMG. Landon Westerlund Audit Partner - Financial Services -KPMG

Preparers Track Integrating XBRL into your reporting process Michael Ohata Managing Director - KPMG Landon Westerlund Audit Partner - Financial Services -KPMG Michael Schlanger VP, Development & Strategy

Preparers Track Integrating XBRL into your reporting process Michael Ohata Managing Director - KPMG Landon Westerlund Audit Partner - Financial Services -KPMG Michael Schlanger VP, Development & Strategy

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C FORM 10-Q

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [x] QUARTERLY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For Quarterly Period Ended December

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [x] QUARTERLY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For Quarterly Period Ended December

Not-for-Profit Year-End Accounting Update A road map to upcoming changes. December 5, 2017

Not-for-Profit Year-End Accounting Update A road map to upcoming changes December 5, 2017 2017 Crowe 2017 Crowe Horwath Horwath LLP LLP Housekeeping All phones will be automatically muted upon entering

Not-for-Profit Year-End Accounting Update A road map to upcoming changes December 5, 2017 2017 Crowe 2017 Crowe Horwath Horwath LLP LLP Housekeeping All phones will be automatically muted upon entering

Analysis of Financial Statements and Statement of Cash Flows BUS512M. November 21, 2014 Session 2 8:00-11:30 Susan Crosson

Analysis of Financial Statements and Statement of Cash Flows BUS512M November 21, 2014 Session 2 8:00-11:30 Susan Crosson Homework See Handout Today s Learning Outcomes Analyzing Financial Statementscommon

Analysis of Financial Statements and Statement of Cash Flows BUS512M November 21, 2014 Session 2 8:00-11:30 Susan Crosson Homework See Handout Today s Learning Outcomes Analyzing Financial Statementscommon

Accounting for Consolidations What You Need to Know about Cost, Equity and Acquisition Methods, Part 1

Accounting U.S. GAAP Accounting for Consolidations What You Need to Know about Cost, Equity and Acquisition Methods, Part 1 Accounting for Consolidations What You Need to Know about Cost, Equity and Acquisition

Accounting U.S. GAAP Accounting for Consolidations What You Need to Know about Cost, Equity and Acquisition Methods, Part 1 Accounting for Consolidations What You Need to Know about Cost, Equity and Acquisition

Understanding Accounting & Financial Statements

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

Chapter 2 Asset and Liability Valuation and Income Measurement

Chapter 2 Asset and Liability Valuation and Measurement MULTIPLE CHOICE 1. Which of the following assets appears on the balance sheet at Historical cost? a. Equipment b. Notes Payable c. Investments in

Chapter 2 Asset and Liability Valuation and Measurement MULTIPLE CHOICE 1. Which of the following assets appears on the balance sheet at Historical cost? a. Equipment b. Notes Payable c. Investments in

THE BOTTOM LINE, INC. FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2017 AND 2016 (WITH INDEPENDENT AUDITORS REPORT THEREON)

") FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2017 AND 2016 (WITH INDEPENDENT AUDITORS REPORT THEREON) FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2017 AND 2016 TABLE OF CONTENTS INDEPENDENT

FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2017 AND 2016 (WITH INDEPENDENT AUDITORS REPORT THEREON) FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2017 AND 2016 TABLE OF CONTENTS INDEPENDENT

PROFESSIONAL DISC GOLF ASSOCIATION, INC. FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016

FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016 TABLE OF CONTENTS Independent Auditor's Report 1-2 Financial Statements: Statements of Financial Position...... 3 Statements of Activities 4 Statements of

FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016 TABLE OF CONTENTS Independent Auditor's Report 1-2 Financial Statements: Statements of Financial Position...... 3 Statements of Activities 4 Statements of

Accounting Matters and Disclosure and Internal Control

Accounting Matters and Disclosure and Internal Control Critical Accounting Estimates The most significant assets and liabilities for which we must make estimates include: allowance for credit losses; financial

Accounting Matters and Disclosure and Internal Control Critical Accounting Estimates The most significant assets and liabilities for which we must make estimates include: allowance for credit losses; financial

Accounting Self Study Guide for Staff of Micro Finance Institutions DEFINITION OF ACCOUNTING

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 1 DEFINITION OF ACCOUNTING Objectives: The purpose of this lesson is to introduce the concepts of accounting, what it is used

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 1 DEFINITION OF ACCOUNTING Objectives: The purpose of this lesson is to introduce the concepts of accounting, what it is used

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

THE ULTIMATE SOFTWARE GROUP, INC. (Exact name of Registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Fraud in Financial Statements

Fraud in Financial Statements Course Instructions and Final Examination Fraud in Financial Statements Gerard M. Zack CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 The CPE Store

Fraud in Financial Statements Course Instructions and Final Examination Fraud in Financial Statements Gerard M. Zack CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 The CPE Store

ixbrl 7 September 2017 Paul Braden - KPMG

ixbrl 7 September 2017 Paul Braden - KPMG Overview What is ixbrl? Why do Revenue want ixbrl financials? When is an ixbrl filing required for Revenue? What does a Revenue ixbrl filing consist of? What needs

ixbrl 7 September 2017 Paul Braden - KPMG Overview What is ixbrl? Why do Revenue want ixbrl financials? When is an ixbrl filing required for Revenue? What does a Revenue ixbrl filing consist of? What needs

International Financial Reporting Standards (IFRS) and 2018 Updates

and 2018 Updates") International Financial Reporting Standards (IFRS) and 2018 Updates Why Attend Our 'International Financial Reporting Standards (IFRS) and 2018 Updates' course will help build the knowledge you need in

International Financial Reporting Standards (IFRS) and 2018 Updates Why Attend Our 'International Financial Reporting Standards (IFRS) and 2018 Updates' course will help build the knowledge you need in

Module Behind the scenes Case studies International spotlights

International and US comparative curriculum master user guide: behind the scenes, case studies and international spotlights The document provides an overview of the behind the scenes, case studies and

International and US comparative curriculum master user guide: behind the scenes, case studies and international spotlights The document provides an overview of the behind the scenes, case studies and

SAMPLE EXAM - CHAPTER 1

SAMPLE EXAM - CHAPTER 1 Name: Date: 1. General-purpose financial statements are the product of A) financial accounting. B) managerial accounting. C) both financial and managerial accounting. D) neither

SAMPLE EXAM - CHAPTER 1 Name: Date: 1. General-purpose financial statements are the product of A) financial accounting. B) managerial accounting. C) both financial and managerial accounting. D) neither

Not-for-Profit Conference A&A Update for NFPs

Not-for-Profit Conference A&A Update for NFPs James Schmutte July 24, 2014 This session focuses on recent and developing activities of the four standard setters (FASB, AICPA, OMB and GAO) that impact nonprofit

Not-for-Profit Conference A&A Update for NFPs James Schmutte July 24, 2014 This session focuses on recent and developing activities of the four standard setters (FASB, AICPA, OMB and GAO) that impact nonprofit

Profit or loss recorded to Retained Earnings

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Kush Bottles, Inc. A Nevada corporation (the Company )

") Kush Bottles, Inc. A Nevada corporation (the Company ) Audit Committee Charter The Audit Committee (the Committee ) is created by the Board of Directors of the Company (the Board ) to: assist the Board

Kush Bottles, Inc. A Nevada corporation (the Company ) Audit Committee Charter The Audit Committee (the Committee ) is created by the Board of Directors of the Company (the Board ) to: assist the Board

Financial Accounting. prof. Adriana Tiron Tudor- course lect. Vasile Cardos- practice

Financial Accounting prof. Adriana Tiron Tudor- course lect. Vasile Cardos- practice Accounting Crossword Puzzle Word Scramble Agenda 1. Introduction 2. Organizational matters 4. Must to know test your

Financial Accounting prof. Adriana Tiron Tudor- course lect. Vasile Cardos- practice Accounting Crossword Puzzle Word Scramble Agenda 1. Introduction 2. Organizational matters 4. Must to know test your

FINANCE & ACCOUNTING FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION NON-TECHNICAL & CERTIFIED TRAINING COURSE

FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION FINANCE & ACCOUNTING NON-TECHNICAL & CERTIFIED TRAINING COURSE The Course Uses A Mix Of Interactive Techniques, Such As Brief Presentations By

FEASIBILITY STUDIES: PREPARATION, ANALYSIS AND EVALUATION FINANCE & ACCOUNTING NON-TECHNICAL & CERTIFIED TRAINING COURSE The Course Uses A Mix Of Interactive Techniques, Such As Brief Presentations By

Financial Reporting Framework for Small- and Medium-Sized Entities FRF for SMEs Accounting Framework

Financial Reporting Framework for Small- and Medium-Sized Entities FRF for SMEs Accounting Framework December 11, 2013 Presented by: Jackie H. White, CPA www.pbmares.com An Introduction to the New Financial

Financial Reporting Framework for Small- and Medium-Sized Entities FRF for SMEs Accounting Framework December 11, 2013 Presented by: Jackie H. White, CPA www.pbmares.com An Introduction to the New Financial

Non-GAAP Measures What Do They Say About Fraud Risk? Wednesday, July 18, 2018

Non-GAAP Measures What Do They Say About Fraud Risk? Wednesday, July 18, 2018 The views expressed by the presenters do not necessarily represent the views, positions, or opinions of the Center for Audit

Non-GAAP Measures What Do They Say About Fraud Risk? Wednesday, July 18, 2018 The views expressed by the presenters do not necessarily represent the views, positions, or opinions of the Center for Audit

Financial reporting briefs

December 2014 In this issue: Top story... 2 Accounting update... 3 Regulatory developments... 6 Other considerations... 8 Effective date highlights... 9 Reference library... 11 Financial reporting briefs

December 2014 In this issue: Top story... 2 Accounting update... 3 Regulatory developments... 6 Other considerations... 8 Effective date highlights... 9 Reference library... 11 Financial reporting briefs

ANSWER SHEET EXAMINATION #1

ANSWER SHEET EXAMINATION #1 NAME: DATE: 1) 29) Multiple-choice (38) 2) 30) Matching (46) 3) 31) Problems (16) 4) 32) Total (100) / Grade 5) 33) 6) 34) 7) 35) 8) 36) 9) 37) 10) 38) 11) 12) 13) 14) 15) 16)

ANSWER SHEET EXAMINATION #1 NAME: DATE: 1) 29) Multiple-choice (38) 2) 30) Matching (46) 3) 31) Problems (16) 4) 32) Total (100) / Grade 5) 33) 6) 34) 7) 35) 8) 36) 9) 37) 10) 38) 11) 12) 13) 14) 15) 16)

Fixed Asset Accounting

Fixed Asset Accounting 4 th Edition Steven M. Bragg Chapter 1 Introduction to Fixed Assets... 1 Learning Objectives... 1 Introduction... 1 What are Fixed Assets?... 1 The Fixed Asset Designation... 2 Fixed

Fixed Asset Accounting 4 th Edition Steven M. Bragg Chapter 1 Introduction to Fixed Assets... 1 Learning Objectives... 1 Introduction... 1 What are Fixed Assets?... 1 The Fixed Asset Designation... 2 Fixed

ENGINEERS WITHOUT BORDERS - USA, INC. (A COLORADO NOT-FOR-PROFIT CORPORATION)

") ENGINEERS WITHOUT BORDERS - USA, INC. (A COLORADO NOT-FOR-PROFIT CORPORATION) Financial Statements For the year ended December 31, 2012 With summarized financial information for the year ended December

ENGINEERS WITHOUT BORDERS - USA, INC. (A COLORADO NOT-FOR-PROFIT CORPORATION) Financial Statements For the year ended December 31, 2012 With summarized financial information for the year ended December

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C FORM 10-Q

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [x] QUARTERLY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For Quarterly Period Ended March

UNITED STATES SECURITIES & EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q [x] QUARTERLY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For Quarterly Period Ended March

Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011

1 November 2010 Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011 Online filing requirement Online filing to HMRC will be mandatory for all UK companies from 1 April 2011.

1 November 2010 Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011 Online filing requirement Online filing to HMRC will be mandatory for all UK companies from 1 April 2011.

Business Introducing Financial Statements. Professor Sergio Janczak, Ph.D KC 1

Business 1220 Introducing Financial Statements Professor Sergio Janczak, Ph.D. 2008-9 KC 1 Introducing Financial Statements Types of Financial Statements 1. Balance Sheet 2. The Statement of Earnings or

Business 1220 Introducing Financial Statements Professor Sergio Janczak, Ph.D. 2008-9 KC 1 Introducing Financial Statements Types of Financial Statements 1. Balance Sheet 2. The Statement of Earnings or

CSP Inc. (Exact name of Registrant as specified in its charter)

") United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

United States SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

DO SOMETHING, INC. FINANCIAL STATEMENTS DECEMBER 31, 2016 (WITH DECEMBER 31, 2015 SUMMARIZED COMPARATIVE TOTALS)

") FINANCIAL STATEMENTS (WITH DECEMBER 31, 2015 SUMMARIZED COMPARATIVE TOTALS) CONTENTS Page Independent Auditors' Report 1-2 Financial Statements Statement of Financial Position at December 31, 2016 (With

FINANCIAL STATEMENTS (WITH DECEMBER 31, 2015 SUMMARIZED COMPARATIVE TOTALS) CONTENTS Page Independent Auditors' Report 1-2 Financial Statements Statement of Financial Position at December 31, 2016 (With

Impact on Actuarially Determined Items SEAC Fall Meeting - Atlanta, GA November 19, 2003

Sarbanes-Oxley Act of 2002 Preparing Your Organization for Section 404 Internal Control over Financial Reporting Impact on Actuarially Determined Items SEAC Fall Meeting - Atlanta, GA November 19, 2003

Sarbanes-Oxley Act of 2002 Preparing Your Organization for Section 404 Internal Control over Financial Reporting Impact on Actuarially Determined Items SEAC Fall Meeting - Atlanta, GA November 19, 2003

Speech by SEC Staff: OCA Current Projects: Remarks Before the 2006 AICPA Conference on Current SEC & PCAOB Developments

Home Previous Page Speech by SEC Staff: OCA Current Projects: Remarks Before the 2006 AICPA Conference on Current SEC & PCAOB Developments by John W. Albert Senior Associate Chief Accountant, Office of

Home Previous Page Speech by SEC Staff: OCA Current Projects: Remarks Before the 2006 AICPA Conference on Current SEC & PCAOB Developments by John W. Albert Senior Associate Chief Accountant, Office of

WILLIAM I. ESKIN, CPA. Presentation to : Southeastern Accounting Show FINANCIAL STATEMENT ANALYSIS/FRAUD. August 18, 2011.

WILLIAM I. ESKIN, CPA Presentation to : Southeastern Accounting Show FINANCIAL STATEMENT ANALYSIS/FRAUD August 18, 2011 Introduction What is Fraud? SAS No. 99 defines fraud as: an intentional act that

WILLIAM I. ESKIN, CPA Presentation to : Southeastern Accounting Show FINANCIAL STATEMENT ANALYSIS/FRAUD August 18, 2011 Introduction What is Fraud? SAS No. 99 defines fraud as: an intentional act that

FINANCE FOR THE NONFINANCIAL PROFESSIONAL INSTRUCTOR GUIDE 2-DAY COURSE

FINANCE FOR THE NONFINANCIAL PROFESSIONAL INSTRUCTOR GUIDE 2-DAY COURSE FINANCE FOR THE NONFINANCIAL PROFESSIONAL Finance for the Nonfinancial Professional Copyright 2008 TreeLine 2008 Published by HRDQ

FINANCE FOR THE NONFINANCIAL PROFESSIONAL INSTRUCTOR GUIDE 2-DAY COURSE FINANCE FOR THE NONFINANCIAL PROFESSIONAL Finance for the Nonfinancial Professional Copyright 2008 TreeLine 2008 Published by HRDQ

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA. Course Title ACCOUNTING II

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA Course Title ACCOUNTING II Month: September ESSENTIAL QUESTIONS THAT THE COURSE CONTENT ANSWERS: Why is it essential for businesses to follow the accounting

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA Course Title ACCOUNTING II Month: September ESSENTIAL QUESTIONS THAT THE COURSE CONTENT ANSWERS: Why is it essential for businesses to follow the accounting

The 9th International Anti-Corruption Conference The Papers

The 9th International Anti-Corruption Conference The Papers COSO STUDY ON FRAUD IN FINANCIAL REPORTING Carlo di Florio Introduction TI-Home Lima Declaration Durban Commitment I have been asked to address

The 9th International Anti-Corruption Conference The Papers COSO STUDY ON FRAUD IN FINANCIAL REPORTING Carlo di Florio Introduction TI-Home Lima Declaration Durban Commitment I have been asked to address

FASB Update: A View from the Top - The Latest Developments in Financial Accounting Standards

FASB Update: A View from the Top - The Latest Developments in Financial Accounting Standards Jenifer Wyss Project Manager, FASB MACPA 2014 CPA Innovation Summit June 16, 2014 The views expressed in this

FASB Update: A View from the Top - The Latest Developments in Financial Accounting Standards Jenifer Wyss Project Manager, FASB MACPA 2014 CPA Innovation Summit June 16, 2014 The views expressed in this

FASB Update: A View from the Top - The Latest Developments in Financial Accounting Standards

FASB Update: A View from the Top - The Latest Developments in Financial Accounting Standards Jenifer Wyss Project Manager, FASB MACPA 2014 CPA Innovation Summit June 16, 2014 The views expressed in this

FASB Update: A View from the Top - The Latest Developments in Financial Accounting Standards Jenifer Wyss Project Manager, FASB MACPA 2014 CPA Innovation Summit June 16, 2014 The views expressed in this

Course 2615: US GAAP for Upstream (E&P) Oil and Gas (3 days)

Oil and Gas (3 days)") Course introduction The complexities of accounting for oil and gas companies require an ability to properly interpret and comply with the accounting requirements that are applicable to this industry's

Course introduction The complexities of accounting for oil and gas companies require an ability to properly interpret and comply with the accounting requirements that are applicable to this industry's

IMPLEMENTATION PROBLEMS

1 RESEARCHING IFRS IMPLEMENTATION PROBLEMS Overview 1 The IFRS Hierarchy 1 Researching IFRS 4 Researching Accounting Controls 5 Researching Accounting Forms and Reports 6 Researching Accounting Footnotes

1 RESEARCHING IFRS IMPLEMENTATION PROBLEMS Overview 1 The IFRS Hierarchy 1 Researching IFRS 4 Researching Accounting Controls 5 Researching Accounting Forms and Reports 6 Researching Accounting Footnotes

Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information

Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information") Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded companies can

Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded companies can

STARWOOD REAL ESTATE INCOME TRUST, INC. (Exact name of Registrant as specified in Governing Instruments)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE QUARTERLY PERIOD

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE QUARTERLY PERIOD

Key Learning: Students will review basic accounting concepts learned in the first level course.

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

JOURNAL ENTRIES APPENDIX

The Ultimate Accountants Reference: Including GAAP, IRS and SEC Regulations, Leases, and More, 3rd Edition Steven M. Bragg Copyright 2010 by John Wiley & Sons, Inc. APPENDIX B JOURNAL ENTRIES B.1 ACQUISITIONS

The Ultimate Accountants Reference: Including GAAP, IRS and SEC Regulations, Leases, and More, 3rd Edition Steven M. Bragg Copyright 2010 by John Wiley & Sons, Inc. APPENDIX B JOURNAL ENTRIES B.1 ACQUISITIONS

Financial Statements. For the Years Ended December 31, 2014 and and Report Thereon

Financial Statements and Report Thereon INDEPENDENT AUDITOR S REPORT To the Board of Directors of GOOD360 Report on the Financial Statements We have audited the accompanying financial statements of GOOD360,

Financial Statements and Report Thereon INDEPENDENT AUDITOR S REPORT To the Board of Directors of GOOD360 Report on the Financial Statements We have audited the accompanying financial statements of GOOD360,

Financial Accounting

Financial Accounting Roger H. Hermanson, Ph.D., CPA Regents' Professor of Accounting Ernst & Whinney Professor School of Accountancy Georgia State University James Don Edwards^ Ph.D., CPA J. M. Tull Professor

Financial Accounting Roger H. Hermanson, Ph.D., CPA Regents' Professor of Accounting Ernst & Whinney Professor School of Accountancy Georgia State University James Don Edwards^ Ph.D., CPA J. M. Tull Professor

Financial Statement Analysis for the Boardroom. An Attorney s Guide September 13, 2017

Financial Statement Analysis for the Boardroom An Attorney s Guide September 13, 2017 Contact information For more information, please contact one of the following members of the engagement team: Marc

Financial Statement Analysis for the Boardroom An Attorney s Guide September 13, 2017 Contact information For more information, please contact one of the following members of the engagement team: Marc

THE CHANDA PLAN FOUNDATION (A Colorado Non-Profit Corporation) Financial Statements December 31, 2017 and 2016

Financial Statements December 31, 2017 and 2016") Financial Statements December 31, 2017 and 2016 C O N T E N T S Independent Auditors Report 1 Financial Statements Statements of Financial Position 2-3 Statements of Activities 4 Statements of Cash Flows

Financial Statements December 31, 2017 and 2016 C O N T E N T S Independent Auditors Report 1 Financial Statements Statements of Financial Position 2-3 Statements of Activities 4 Statements of Cash Flows

Re: File Number S

April 9, 2009 Ms. Florence Harmon Acting Secretary U.S. Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-1090 Dear Ms. Harmon: Re: File Number S7-27-08 The American Institute

April 9, 2009 Ms. Florence Harmon Acting Secretary U.S. Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-1090 Dear Ms. Harmon: Re: File Number S7-27-08 The American Institute

Nottingham City Homes

ITEM 7 AUDIT COMMITTEE 27 MARCH 2014 Nottingham City Homes Audit Strategy and Planning Memorandum Year ending 31 March 2014 February 2014 Contents The contacts at KPMG in connection with this report are:

ITEM 7 AUDIT COMMITTEE 27 MARCH 2014 Nottingham City Homes Audit Strategy and Planning Memorandum Year ending 31 March 2014 February 2014 Contents The contacts at KPMG in connection with this report are:

THE BOTTOM LINE, INC. FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015 (Restated) (WITH INDEPENDENT AUDITORS REPORT THEREON)

(WITH INDEPENDENT AUDITORS REPORT THEREON)") FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015 (Restated) (WITH INDEPENDENT AUDITORS REPORT THEREON) FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015 (Restated) TABLE OF

FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015 (Restated) (WITH INDEPENDENT AUDITORS REPORT THEREON) FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015 (Restated) TABLE OF

XTEND, INC. FINANCIAL STATEMENTS September 30, 2018 and 2017

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

All the darkness in the world cannot extinguish the light from a single candle. St. Francis of Assisi

All the darkness in the world cannot extinguish the light from a single candle. St. Francis of Assisi Supplementary Study Guide to Accompany the Quarterly CPE Exam on Topics Addressed in the Journal of

All the darkness in the world cannot extinguish the light from a single candle. St. Francis of Assisi Supplementary Study Guide to Accompany the Quarterly CPE Exam on Topics Addressed in the Journal of

AMERICAN SOFTWARE, INC.

ˆ200G4i3f7shhq7zLyŠ 200G4i3f7shhq7zLy GA0113AM022800 12.8.8.0 ADG davir0at 06-Dec-2018 11:38 EST 645446 TX 1 4* Page 1 of 2 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM

ˆ200G4i3f7shhq7zLyŠ 200G4i3f7shhq7zLy GA0113AM022800 12.8.8.0 ADG davir0at 06-Dec-2018 11:38 EST 645446 TX 1 4* Page 1 of 2 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM

6 key areas of change for accountants and auditors

6 key areas of change for accountants and auditors Professionals face challenges as they implement numerous new rules. By Ken Tysiac IMAGES BY CHOMBOSAN/ISTOCK Sponsored by Sage Workiva Thomson Reuters

6 key areas of change for accountants and auditors Professionals face challenges as they implement numerous new rules. By Ken Tysiac IMAGES BY CHOMBOSAN/ISTOCK Sponsored by Sage Workiva Thomson Reuters

079 - Internal Audit GENERAL GOVERNMENT SERVICES Internal Audit. At a Glance:

GENERAL GOVERNMENT SERVICES 079 - INTERNAL AUDIT Operational Summary Mission: The mission of the Internal Audit Department (IAD) is to provide reliable, independent, objective evaluations and business

GENERAL GOVERNMENT SERVICES 079 - INTERNAL AUDIT Operational Summary Mission: The mission of the Internal Audit Department (IAD) is to provide reliable, independent, objective evaluations and business

WAYNESBORO AREA SCHOOL DISTRICT ADVANCED ACCOUNTING

COURSE NAME: Advanced UNIT: Departmentalized (4 Chapters plus a simulation project) NO. OF DAYS: 60 KEY LEARNING(S): Recording Departmental Purchases, Cash Payments, Sales, and Cash Receipts; Calculating

COURSE NAME: Advanced UNIT: Departmentalized (4 Chapters plus a simulation project) NO. OF DAYS: 60 KEY LEARNING(S): Recording Departmental Purchases, Cash Payments, Sales, and Cash Receipts; Calculating

TEXAS TRIBUNE, INC. Financial Statements as of and for the Years Ended December 31, 2014 and 2013 and Independent Auditors Report

TEXAS TRIBUNE, INC. Financial Statements as of and for the Years Ended December 31, 2014 and 2013 and Independent Auditors Report TEXAS TRIBUNE, INC. TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 Page

TEXAS TRIBUNE, INC. Financial Statements as of and for the Years Ended December 31, 2014 and 2013 and Independent Auditors Report TEXAS TRIBUNE, INC. TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 Page

It's more than just numbers

What are the goals of a business? It's more than just numbers Make a profit Remain in a healthy financial position Make good use of cash flow FINANCIAL STATEMENTS AND THE DETAILS What is a Financial Statement?

What are the goals of a business? It's more than just numbers Make a profit Remain in a healthy financial position Make good use of cash flow FINANCIAL STATEMENTS AND THE DETAILS What is a Financial Statement?