Chapter 16 Completing the Tests in the Sales and Collection Cycle:

|

|

|

- Hillary Manning

- 6 years ago

- Views:

Transcription

1 Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable

2 Describe the methodology for designing tests of details of balances using the audit risk model. Design and perform analytical procedures for accounts in the sales and collection cycle. Design and perform tests of details of balances for accounts receivable. 16-2

3 Obtain and evaluate accounts receivable confirmations. Design audit procedures for the audit of accounts receivable, using the evidence planning worksheet as a guide. 16-3

4 1 Describe the methodology for designing tests of details of balances using the audit risk model. 16-4

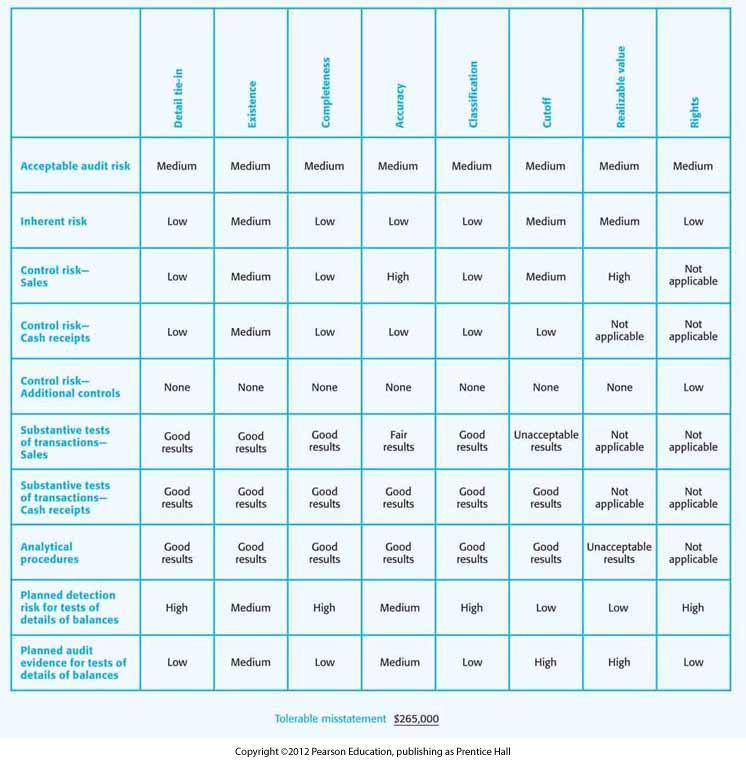

5 Detail tie-in Existence Rights Completeness A/R Audit Objectives Realizable value Accuracy Classification Cutoff 16-5

6 Phase I Identify client business risks affecting Accounts Receivable Set performance materiality and assess inherent risk for accounts receivable Assess control risk for sales and collection cycle 16-6

7 Phase II Design and perform tests of controls and substantive tests of transactions for the sales and collection cycle 16-7

8 Phase III Design and perform analytical procedures for accounts receivable Design tests of details of accounts receivable balance to satisfy balance-related objectives Audit procedures Sample size Items to select Timing 16-8

9 Detail tie-in Existence Completeness Accuracy Classification Cutoff Realizable value Rights ACCOUNTS RECEIVABLE BALANCE-RELATED AUDIT OBJECTIVES Translation-related audit objectives Sales Occurrence Completeness Accuracy Posting and summarization Classification Timing 16-9

10 Detail tie-in Existence Completeness Accuracy Classification Cutoff Realizable value Rights ACCOUNTS RECEIVABLE BALANCE-RELATED AUDIT OBJECTIVES Translation-related audit objectives Cash receipts Occurrence Completeness Accuracy Posting and summarization Classification Timing 16-10

11 2 Design and perform analytical procedures for accounts in the sales and collection cycle

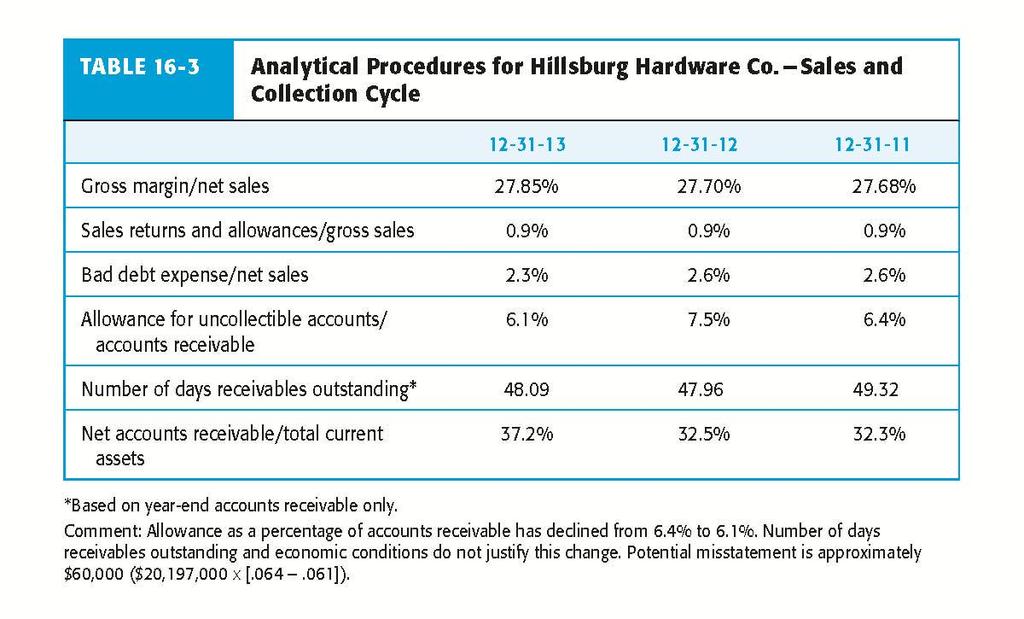

12 Compare by product line: Gross margin percentage with previous years Sales by month over time Sales returns and allowances as a percentage of gross sales with previous years 16-12

13 Compare with previous years: Individual customer balances over a stated amount Bad debt expense as a percentage of gross sales Days that accounts receivable are outstanding 16-13

14 Compare with previous years: Aging category as a percentage of receivables Allowance for uncollectible accounts as a percentage of accounts receivable Write-off of uncollectible accounts as a percentage of total accounts receivable 16-14

15 12/31/13 ($000) Percent change /31/12 ($000) Percent change /31/11 ($000) Sales Gross margin Accounts receivable Bad debt expense Total current assets Total assets Net earnings Number of accounts receivable Number of accts. rec. with balances over $100, ,328 39,845 20,197 3,323 51,027 61,367 5, (2.1) 14.0 (7.0) ,421 36,350 18,827 3,394 44,779 66,021 4, ,737 33,961 16,505 3,162 41,989 61,147 3,

16 16-16

17 Planned detection risk for each objective is an auditor decision Combining the factors that determine planned detection risk is complex 16-17

18 3 Design and perform tests of details of balances for accounts receivable

19 Accounts receivable are correctly added and agree with the Master File and the General Ledger (aged trial balance). Recorded accounts receivable exist Existing accounts receivable are included 16-19

20 Accounts receivable are accurate Accounts receivable are properly classified Cutoff for accounts receivable is correct 16-20

21 Accounts receivable is stated at realizable value The client has rights to accounts receivable Accounts receivable presentation and disclosure 16-21

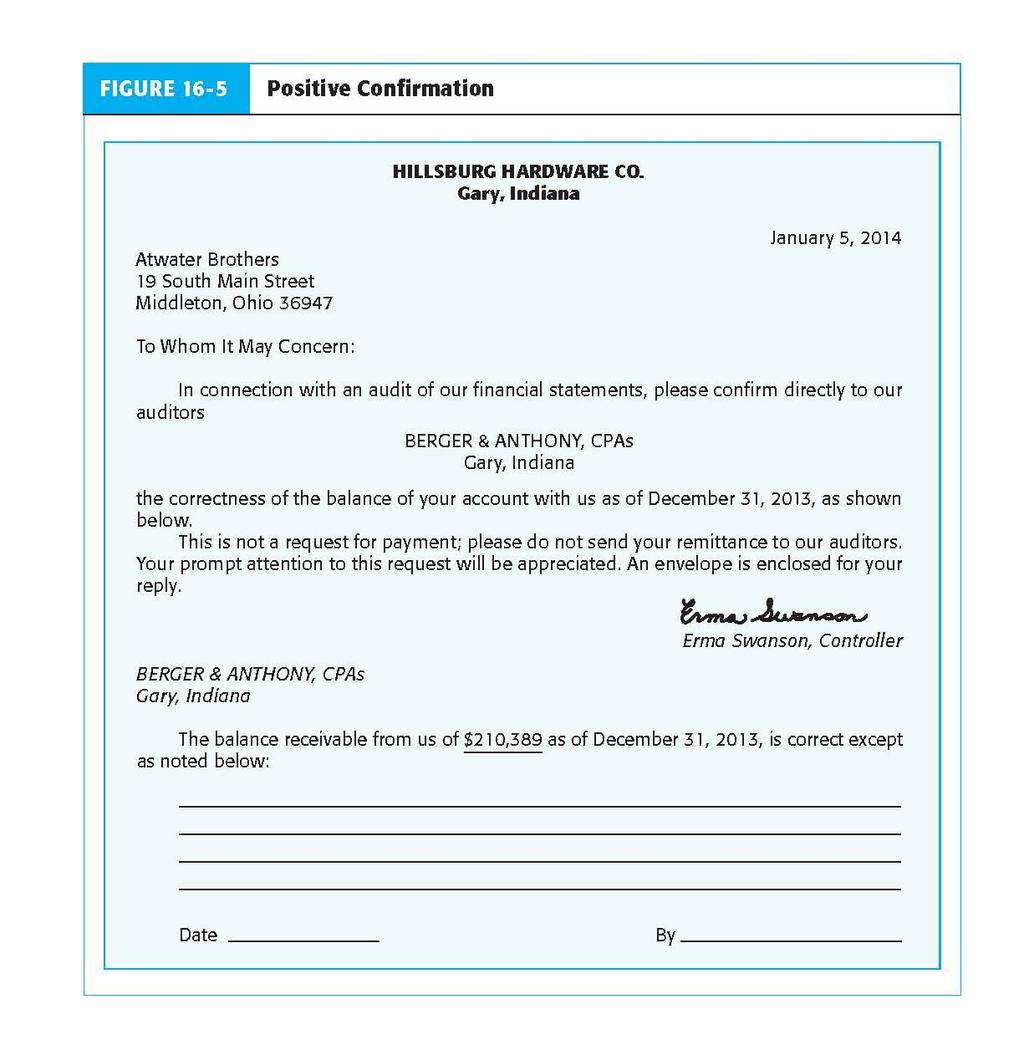

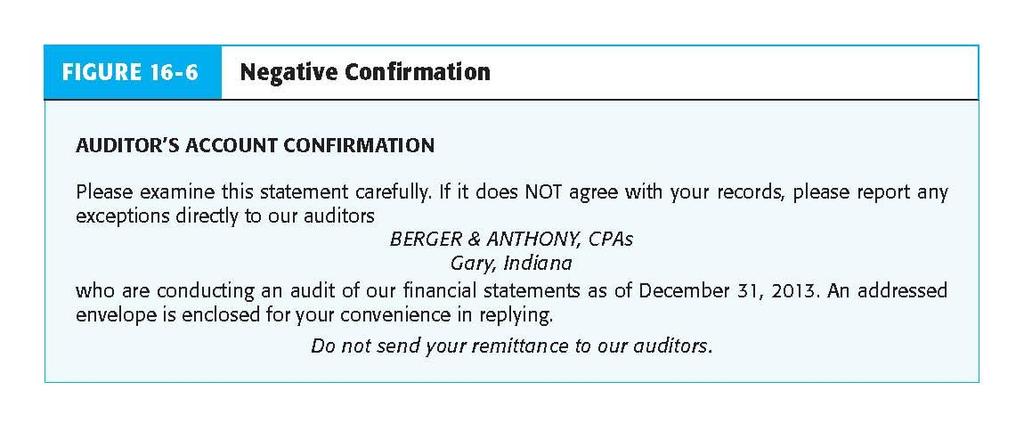

22 4 Obtain and evaluate accounts receivable confirmations

23 Auditing Standards United States International Required Except when: Confirmations not required Expected low response rate Low inherent & control risks Alternate Procedures 16-23

24 Positive confirmation Blank confirmation form Invoice confirmation Negative confirmation 16-24

25 16-25

26 Risk of material misstatement is low Large number of small account balances Expected low exception rate Expect adequate consideration from recipients 16-26

27 16-27

28 The most reliable evidence from confirmations is obtained when they are sent as close to the balance sheet date as possible

29 Performance materiality Inherent Risk Control Risk Sample Size factors Type of Confirmation Achieved Detection risk from other tests 16-29

30 The auditor should perform procedures to verify the addresses or addresses used for confirmation. Auditors must be responsible for mailing the confirmations and maintaining control of the confirmations until they are returned from the customer

31 When positive confirmations are used, Auditing standards require follow-up Procedures for confirmations not returned by the customer. Alternate Procedures Subsequent cash receipts Duplicate sales invoices Shipping documents

32 Payment-in-transit Shipment-in-transit The goods have been returned Errors and disputes 16-32

33 Reevaluate internal control Evaluate the qualitative nature of misstatements Determine whether sufficient evidence was obtained 16-33

34 5 Design audit procedures for the audit of accounts receivable, using an evidence planning worksheet as a guide

35 16-35

36 16-36

37 Copyright All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America

Chapter 23 Audit of Cash and Financial Instruments. Copyright 2014 Pearson Education

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Chapter 10. Auditing the Revenue Process. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 10 Auditing the Revenue Process McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Revenue Recognition Revenue is defined as inflows or other enhancements

Chapter 10 Auditing the Revenue Process McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Revenue Recognition Revenue is defined as inflows or other enhancements

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 07 Revenue and Collection Cycle What at first was plunder assumed the softer name of revenue. Thomas Paine

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 07 Revenue and Collection Cycle What at first was plunder assumed the softer name of revenue. Thomas Paine

Chapter 10. Auditing the Revenue Process

Chapter 10 Auditing the Revenue Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. LO# 1 Revenue

Chapter 10 Auditing the Revenue Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. LO# 1 Revenue

Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions

Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Chapter 14 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley 5-5 Learning Objective

Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Chapter 14 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley 5-5 Learning Objective

Chapter 22 Audit of the Capital Acquisition and Repayment Cycle. Copyright 2014 Pearson Education

Chapter 22 Audit of the Capital Acquisition and Repayment Cycle Identify the accounts and the unique characteristics of the capital acquisition and repayment cycle. Design and perform audit tests of notes

Chapter 22 Audit of the Capital Acquisition and Repayment Cycle Identify the accounts and the unique characteristics of the capital acquisition and repayment cycle. Design and perform audit tests of notes

Chapter 14. Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment

Chapter 14 Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights

Chapter 14 Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights

Chapter 10. Cash and Financial Investments. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Sources and Nature of Cash Sources General checking account Payroll checking

Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Sources and Nature of Cash Sources General checking account Payroll checking

Chapter 14. Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment

Chapter 14 Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or

Chapter 14 Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or

Chapter 15. Auditing the Financing/Investing Process: Long-Term Liabilities, Stockholders Equity, and Income Statement Accounts

Chapter 15 Auditing the Financing/Investing Process: Long-Term Liabilities, Stockholders Equity, and Income Statement Accounts Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction

Chapter 15 Auditing the Financing/Investing Process: Long-Term Liabilities, Stockholders Equity, and Income Statement Accounts Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction

Chapter 05. Audit Evidence and Documentation. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 05 Audit Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Audit Risk The possibility that the auditors may unknowingly fail to

Chapter 05 Audit Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Audit Risk The possibility that the auditors may unknowingly fail to

Auditing and Assurance Services, 15e

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Conceptual Framework of Assurance II: Types of Assertions

Conceptual Framework of Assurance II: Types of Assertions Joshua Onome Imoniana September 8, 2014 Student s Key takeaway from this lecture include: What is an assertion? Useful steps to verify an assertion.

Conceptual Framework of Assurance II: Types of Assertions Joshua Onome Imoniana September 8, 2014 Student s Key takeaway from this lecture include: What is an assertion? Useful steps to verify an assertion.

Chapter 13 Homework ACL Problem

Chapter 13 Homework 12-31 ACL Problem a. There are three transactions with missing dates. There are several negative balance transactions with no indication that they are purchase returns. b. Total purchases

Chapter 13 Homework 12-31 ACL Problem a. There are three transactions with missing dates. There are several negative balance transactions with no indication that they are purchase returns. b. Total purchases

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

Professional Bridging Examination. Paper III PBE Auditing and Information Systems

Professional Bridging Examination Pilot Examination Paper Paper III PBE Auditing and Information Systems Questions & Answers Booklet The suggested answers given in this booklet are purposely made to give

Professional Bridging Examination Pilot Examination Paper Paper III PBE Auditing and Information Systems Questions & Answers Booklet The suggested answers given in this booklet are purposely made to give

Piotr Pyziak, Consultant, CFRR

Piotr Pyziak, Consultant, CFRR 16 March 2017, Vienna Audit Training of Trainers Road to Europe: Program of Accounting Reform and Institutional Strengthening EU-REPARIS is funded by the European Union and

Piotr Pyziak, Consultant, CFRR 16 March 2017, Vienna Audit Training of Trainers Road to Europe: Program of Accounting Reform and Institutional Strengthening EU-REPARIS is funded by the European Union and

Audit and Assurance. Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

SUGGESTED SOLUTIONS 06204 - Audit and Assurance Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA All Rights Reserved (1) Answer No.

SUGGESTED SOLUTIONS 06204 - Audit and Assurance Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA All Rights Reserved (1) Answer No.

Script Reference. Complete the monthly REC1 Description & Objectives

Title Complete the monthly REC1 Description & Objectives Script Reference FMS REC1 Schools are required to complete the monthly REC1 to reconcile bank statements and FMS. Script Name Date Comments Created

Title Complete the monthly REC1 Description & Objectives Script Reference FMS REC1 Schools are required to complete the monthly REC1 to reconcile bank statements and FMS. Script Name Date Comments Created

Module 4. Instructions:

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

APPENDIX D Examples of Significant Deficiencies and Material Weaknesses

Page A 136 Standard APPENDIX D Examples of Significant Deficiencies and Material Weaknesses D1. Paragraph 8 of this standard defines a control deficiency. Paragraphs 9 and 10 go on to define a significant

Page A 136 Standard APPENDIX D Examples of Significant Deficiencies and Material Weaknesses D1. Paragraph 8 of this standard defines a control deficiency. Paragraphs 9 and 10 go on to define a significant

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting Transfer Encumbrances Outstanding Acct. Rec. Invoices Step-by-step Instructions 2012 Central Susquehanna Intermediate Unit, USA Table

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting Transfer Encumbrances Outstanding Acct. Rec. Invoices Step-by-step Instructions 2012 Central Susquehanna Intermediate Unit, USA Table

Chapter 20 Notes Uncollectible Accounts Expense

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

Chapter 20 Notes Uncollectible Accounts Expense Uncollectible Account- An account that has been defaulted on. Meaning that the person did not pay when it was due. Explanation of the Accounts Uncollectible

AUDIT OF TRADE RECEIVABLES

AUDIT OF TRADE RECEIVABLES Marius Nicolae MICULESCU Sergiu-Dorin GRUI Abstract:The present paper presents in the first part the trade receivables that arise from a company s relation with third parties

AUDIT OF TRADE RECEIVABLES Marius Nicolae MICULESCU Sergiu-Dorin GRUI Abstract:The present paper presents in the first part the trade receivables that arise from a company s relation with third parties

Financial Reporting Alert

Financial Reporting Alert ASPE DECEMBER 2017 2017 Annual Improvements to Accounting Standards for Private Enterprises In July 2017, the Accounting Standards Board (AcSB) released the 2017 annual improvements

Financial Reporting Alert ASPE DECEMBER 2017 2017 Annual Improvements to Accounting Standards for Private Enterprises In July 2017, the Accounting Standards Board (AcSB) released the 2017 annual improvements

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

DEBITS AND CREDITS: ANALYZING AND RECORDING BUSINESS TRANSACTIONS 2-1 Chapter 2 Learning Objectives 1. Setting up and organizing a chart of accounts. 2. Recording transactions in T accounts according to

Chapter 9. #17 is a bad question if it is changed as follows the answer is d

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Derivatives Analysis and Structured Products Ideas

Ucap Hong Kong Asset Management Limited Derivatives Analysis and Structured Products Ideas 28 th August 2018 10Y Rates - Global Market Parameters Volatility: Skew Overview Volatility: Global Overview Volatility

Ucap Hong Kong Asset Management Limited Derivatives Analysis and Structured Products Ideas 28 th August 2018 10Y Rates - Global Market Parameters Volatility: Skew Overview Volatility: Global Overview Volatility

Ucap Hong Kong Asset Management Limited. Weekly Equity Review. 25 th September 2018

Ucap Hong Kong Asset Management Limited Weekly Equity Review 25 th September 2018 Equity Highlights Investment Recommendations Global Leaders Global Leaders Current List Next-Gen Leaders Japanese Global

Ucap Hong Kong Asset Management Limited Weekly Equity Review 25 th September 2018 Equity Highlights Investment Recommendations Global Leaders Global Leaders Current List Next-Gen Leaders Japanese Global

Gleim CPA Review Updates to Auditing 2011 Edition, 1st Printing June 3, 2011

Page 1 of 7 Gleim CPA Review Updates to Auditing 2011 Edition, 1st Printing June 3, 2011 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown

Page 1 of 7 Gleim CPA Review Updates to Auditing 2011 Edition, 1st Printing June 3, 2011 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown

Cost Allocation Methodology

APPROVED COPYRIGHT TRANSEND NETWORKS PTY LTD ALL RIGHTS RESERVED This document is protected by copyright vested in Transend Networks Pty Ltd. No part of the document may be reproduced or transmitted in

APPROVED COPYRIGHT TRANSEND NETWORKS PTY LTD ALL RIGHTS RESERVED This document is protected by copyright vested in Transend Networks Pty Ltd. No part of the document may be reproduced or transmitted in

Khartoum Enterprises Inc. Audit Planning 15 October 2013

Procedure Objective Project Guidelines 1 Perform analytical procedures and follow up on significant changes from prior years. N/A Do not propose adjustments based on AP work; rather, identify areas of

Procedure Objective Project Guidelines 1 Perform analytical procedures and follow up on significant changes from prior years. N/A Do not propose adjustments based on AP work; rather, identify areas of

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES OUTLINE Application of specific substantive procedures to test the following categories of assertions: -Assertions relating to

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES OUTLINE Application of specific substantive procedures to test the following categories of assertions: -Assertions relating to

a) The elements required for establishing an auditor s liability for negligence to clients are:

The elements required for establishing an auditor s liability for negligence to clients are:") SOLUTION SET 1 ANSWERS 1 Part A a) The elements required for establishing an auditor s liability for negligence to clients are: 1. The duty to conform to a required standard duty of care 2. Failure to

SOLUTION SET 1 ANSWERS 1 Part A a) The elements required for establishing an auditor s liability for negligence to clients are: 1. The duty to conform to a required standard duty of care 2. Failure to

AMIT BACHHAWAT TRAINING FORUM VOUCHING EXTRA QUESTIONS

AMIT BACHHAWAT TRAINING FORUM VOUCHING EXTRA QUESTIONS Q. A trader is worried that in spite of substantial increase in sales compared to earlier year, there is considerable fall in Gross Profit after satisfying

AMIT BACHHAWAT TRAINING FORUM VOUCHING EXTRA QUESTIONS Q. A trader is worried that in spite of substantial increase in sales compared to earlier year, there is considerable fall in Gross Profit after satisfying

Guide for Auditors of Registered Electoral District Associations Appointed under the Canada Elections Act

Guide for Auditors of Registered Electoral District Associations Appointed under the Canada Elections Act Guide for Auditors of Registered Electoral District Associations Appointed under the Canada Elections

Guide for Auditors of Registered Electoral District Associations Appointed under the Canada Elections Act Guide for Auditors of Registered Electoral District Associations Appointed under the Canada Elections

ACCA F8. Provided by Academy of Professional Accounting (APA) Audit and Assurance (AA) 审计与鉴证业务第 7 讲 ACCA Lecturer: Andy Qu

Audit and Assurance (AA) 审计与鉴证业务第 7 讲 ACCA Lecturer: Andy Qu") Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F8 Audit and Assurance (AA) 审计与鉴证业务第 7 讲 ACCA Lecturer: Andy Qu ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F8 Audit and Assurance (AA) 审计与鉴证业务第 7 讲 ACCA Lecturer: Andy Qu ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

TAX CODE DIAGRAMS UltraTax/1041

TAX CODE DIAGRAMS UltraTax/1041 Introduction... 1 Automatic adjustments... 2 Multiple-unit input screens... 2 Form 1041, Page 2... 4 Form 1040NR, Page 1... 5 Form 1040NR, Charitable, Distribution, and

TAX CODE DIAGRAMS UltraTax/1041 Introduction... 1 Automatic adjustments... 2 Multiple-unit input screens... 2 Form 1041, Page 2... 4 Form 1040NR, Page 1... 5 Form 1040NR, Charitable, Distribution, and

General Ledger Audit Guide

General Ledger Audit Guide Last Updated: January 4, 2009 This General Ledger Audit Guide is for use by SedonaOffice customers only. This guide is to be used in conjunction with an approved training class

General Ledger Audit Guide Last Updated: January 4, 2009 This General Ledger Audit Guide is for use by SedonaOffice customers only. This guide is to be used in conjunction with an approved training class

FASB Technical Bulletin No. 85-6

FASB Technical Bulletin No. 85-6 FTB 85-6 Status Page Accounting for a Purchase of Treasury Shares at a Price Significantly in Excess of the Current Market Price of the Shares and the Income Statement

FASB Technical Bulletin No. 85-6 FTB 85-6 Status Page Accounting for a Purchase of Treasury Shares at a Price Significantly in Excess of the Current Market Price of the Shares and the Income Statement

Clarity General Ledger Balancing Flow Charts

Clarity Balancing Flow Charts Release date: 2/16/2011 Version: Clarity (4.x) Summary: A flow chart for balancing accounts to the. Contents Balancing the Utility Management Cash Clearing Account... 2 Balancing

Clarity Balancing Flow Charts Release date: 2/16/2011 Version: Clarity (4.x) Summary: A flow chart for balancing accounts to the. Contents Balancing the Utility Management Cash Clearing Account... 2 Balancing

Corporate Reporting Briefing

Corporate Reporting Briefing WHAT SHOULD BE DISCLOSED ABOUT ESTIMATION UNCERTAINTY? APRIL 2016 Purpose of this Briefing Many accounting numbers involve estimates. Both International Financial Reporting

Corporate Reporting Briefing WHAT SHOULD BE DISCLOSED ABOUT ESTIMATION UNCERTAINTY? APRIL 2016 Purpose of this Briefing Many accounting numbers involve estimates. Both International Financial Reporting

Audit Evidence. What do mean by the Audit Evidence?

What do mean by the Audit Evidence? Audit Evidence Sri Lanka auditing Standard 500 provides the definition of the audit evidence as all the information used by auditors in arriving at the conclusions on

What do mean by the Audit Evidence? Audit Evidence Sri Lanka auditing Standard 500 provides the definition of the audit evidence as all the information used by auditors in arriving at the conclusions on

Audit Techniques, Audit Preparation and Audit Efficiencies for Small and

Audit Techniques, Audit Preparation and Audit Efficiencies for Small and M di Medium E Enterprises t i (SME (SMEs)) March 26 26, 2014 Although the presentation and related materials have been carefully

Audit Techniques, Audit Preparation and Audit Efficiencies for Small and M di Medium E Enterprises t i (SME (SMEs)) March 26 26, 2014 Although the presentation and related materials have been carefully

Sample Reports of Service Tax

Sample Reports of Service Tax The information contained in this document is current as of the date of publication and subject to change. Because Tally must respond to changing market conditions, it should

Sample Reports of Service Tax The information contained in this document is current as of the date of publication and subject to change. Because Tally must respond to changing market conditions, it should

Trading/Hedging Control Environment

Trading/Hedging Control Environment EEI/AGA Utility Internal Auditor s Training Glen Hecht Partner, Financial Accounting Advisory Services August 24, 2016 Agenda Trade Lifecycle Select Risks Select Controls

Trading/Hedging Control Environment EEI/AGA Utility Internal Auditor s Training Glen Hecht Partner, Financial Accounting Advisory Services August 24, 2016 Agenda Trade Lifecycle Select Risks Select Controls

FASB Technical Bulletin No. 81-4

FASB Technical Bulletin No. 81-4 Note: This Technical Bulletin has been completely superseded FTB 81-4 Status Page Classification as Monetary or Nonmonetary Items February 1981 Financial Accounting Standards

FASB Technical Bulletin No. 81-4 Note: This Technical Bulletin has been completely superseded FTB 81-4 Status Page Classification as Monetary or Nonmonetary Items February 1981 Financial Accounting Standards

Vudesk.com (chief)ismail shah SiLeNt Moon(Admin) ACC311- Fundamentals of Auditing (Session - 1)

ismail shah SiLeNt Moon(Admin) ACC311- Fundamentals of Auditing (Session - 1)") Vudesk.com (chief)ismail shah (admin@vudesk.com) SiLeNt Moon(Admin) ACC311- Fundamentals of Auditing (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one When the cash sales should be recorded

Vudesk.com (chief)ismail shah (admin@vudesk.com) SiLeNt Moon(Admin) ACC311- Fundamentals of Auditing (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one When the cash sales should be recorded

Trial Balance. Format of Trial Balance. The under mention points may be noted for preparing a trial balance.

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

NETWORK BUSINESS SYSTEMS SOFTWARE SYSTEM DOCUMENTATION GENERAL LEDGER

NETWORK BUSINESS SYSTEMS SOFTWARE SYSTEM DOCUMENTATION GENERAL LEDGER FEATURES Allows 99 divisions within 99 companies Separate General Ledger Data for Multiple Companies with Multiple Division and Multiple

NETWORK BUSINESS SYSTEMS SOFTWARE SYSTEM DOCUMENTATION GENERAL LEDGER FEATURES Allows 99 divisions within 99 companies Separate General Ledger Data for Multiple Companies with Multiple Division and Multiple

ACCOUNTING CONCEPTS AND PROCEDURES

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

ACCOUNTING CONCEPTS AND PROCEDURES 1-1 Chapter 1 Learning Objectives 1. Defining and listing the functions of accounting. 2. Recording transactions in the basic accounting equation. 3. Seeing how revenue,

Practical Illustration: Doing a Numerical and Discursive Question in Class. Adjunct Associate Professor Chee

Practical Illustration: Doing a Numerical and Discursive Question in Class Adjunct Associate Professor Chee Explaining Concept Some concepts may be abstract for students who do not have working experience,

Practical Illustration: Doing a Numerical and Discursive Question in Class Adjunct Associate Professor Chee Explaining Concept Some concepts may be abstract for students who do not have working experience,

GENERAL LEDGER TABLE OF CONTENTS

GENERAL LEDGER TABLE OF CONTENTS L.A.W.S. Documentation Manual General Ledger GENERAL LEDGER 298 General Ledger Menu 298 Overview Of The General Ledger Account Number Structure 299 Profit Center Processing

GENERAL LEDGER TABLE OF CONTENTS L.A.W.S. Documentation Manual General Ledger GENERAL LEDGER 298 General Ledger Menu 298 Overview Of The General Ledger Account Number Structure 299 Profit Center Processing

Report on Inspection of Ernst & Young LLP (Headquartered in New York, New York) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 666 K Street NW Washington, DC 20006 Office: (202) 207-900 Fax: (202) 862-8430 www.pcaobus.org Report on 206 (Headquartered in New York, New York) Issued by the Public Company Accounting Oversight Board

666 K Street NW Washington, DC 20006 Office: (202) 207-900 Fax: (202) 862-8430 www.pcaobus.org Report on 206 (Headquartered in New York, New York) Issued by the Public Company Accounting Oversight Board

INTERNATIONAL STANDARD ON REVIEW ENGAGEMENTS 2400 ENGAGEMENTS TO REVIEW FINANCIAL STATEMENTS

INTERNATIONAL STANDARD ON REVIEW ENGAGEMENTS 2400 (Previously ISA 910) ENGAGEMENTS TO REVIEW FINANCIAL STATEMENTS (Effective for reviews of financial statements for periods beginning on or after December

INTERNATIONAL STANDARD ON REVIEW ENGAGEMENTS 2400 (Previously ISA 910) ENGAGEMENTS TO REVIEW FINANCIAL STATEMENTS (Effective for reviews of financial statements for periods beginning on or after December

2017 Annual Improvements to Accounting Standards for Private Enterprises

Basis for Conclusions 2017 Annual Improvements to Accounting Standards for Private Enterprises July 2017 CPA Canada Handbook Accounting, Part II Prepared by the staff of the Accounting Standards Board

Basis for Conclusions 2017 Annual Improvements to Accounting Standards for Private Enterprises July 2017 CPA Canada Handbook Accounting, Part II Prepared by the staff of the Accounting Standards Board

WCIRB Premium Audit Accuracy Program

Workers Compensation Insurance Rating Bureau of California WCIRB Premium Audit Accuracy Program Effective January 2018 Notice This WCIRB Premium Audit Accuracy Program was developed by the Workers Compensation

Workers Compensation Insurance Rating Bureau of California WCIRB Premium Audit Accuracy Program Effective January 2018 Notice This WCIRB Premium Audit Accuracy Program was developed by the Workers Compensation

Agency: Bus Area: Fiscal Year

Accounts Receivable 1 Are the agency's accounts receivable policies and procedures clearly stated through manuals, handbooks, or other media? 2 Are all receivable transactions properly and accurately recorded,

Accounts Receivable 1 Are the agency's accounts receivable policies and procedures clearly stated through manuals, handbooks, or other media? 2 Are all receivable transactions properly and accurately recorded,

INCREASE IN SMALL COMPANY AND AUDIT EXEMPTION THRESHOLDS

INCREASE IN SMALL COMPANY AND AUDIT EXEMPTION THRESHOLDS September 2012 Consultative Committee of Accountancy Bodies in Ireland 1 Disclaimer This document is for information purposes only and does not

INCREASE IN SMALL COMPANY AND AUDIT EXEMPTION THRESHOLDS September 2012 Consultative Committee of Accountancy Bodies in Ireland 1 Disclaimer This document is for information purposes only and does not

SERVICE FEES AND RATES REGARDING FOREIGN STOCK CERTIFICATES, ETC. (October 1, 2014 )

") APPENDIX SERVICE FEES AND RATES REGARDING FOREIGN STOCK CERTIFICATES, ETC. (October 1, 2014 ) This translation is prepared solely for reference purpose and shall not have any binding force. This is an

APPENDIX SERVICE FEES AND RATES REGARDING FOREIGN STOCK CERTIFICATES, ETC. (October 1, 2014 ) This translation is prepared solely for reference purpose and shall not have any binding force. This is an

ORIGINAL PRONOUNCEMENTS

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Statement of Financial Accounting Standards No. 37 Balance Sheet Classification of Deferred Income Taxes an amendment of APB Opinion

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Statement of Financial Accounting Standards No. 37 Balance Sheet Classification of Deferred Income Taxes an amendment of APB Opinion

Identifying Risk: Understanding the Entity and its Environment

CASE STUDY: PIZZA SHOP, INC. Identifying Risk: Understanding the Entity and its Environment Pizza Shop, Inc. (PSI or the Entity) owns and operates dine-in restaurants offering Italian cuisine. PSI was

CASE STUDY: PIZZA SHOP, INC. Identifying Risk: Understanding the Entity and its Environment Pizza Shop, Inc. (PSI or the Entity) owns and operates dine-in restaurants offering Italian cuisine. PSI was

TAX CODE DIAGRAMS UltraTax/1120 Puerto Rico

TAX CODE DIAGRAMS UltraTax/1120 Puerto Rico Introduction... 1 Automatic adjustments... 2 Retained earnings... 2 Balance sheet... 2 Multiple-unit input screens... 2 Form 480.2, Page 2... 3 Form 480.2, Page

TAX CODE DIAGRAMS UltraTax/1120 Puerto Rico Introduction... 1 Automatic adjustments... 2 Retained earnings... 2 Balance sheet... 2 Multiple-unit input screens... 2 Form 480.2, Page 2... 3 Form 480.2, Page

2018 GOVERNMENT ENTITIES OVERVIEW FOR KNOWLEDGE COACH USERS

2018 GOVERMET ETITIES OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements included in the current version.

2018 GOVERMET ETITIES OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements included in the current version.

VisionVPM General Ledger Module User Guide

VisionVPM General Ledger Module User Guide Version 1.0 VisionVPM user documentation is continually being developed. For the most up-to-date documentation please visit the VisionVPM website at www.visionvpm.com

VisionVPM General Ledger Module User Guide Version 1.0 VisionVPM user documentation is continually being developed. For the most up-to-date documentation please visit the VisionVPM website at www.visionvpm.com

ASSOCIATION OF ACCOUNTING TECHNICIANS

ASSOCIATION OF ACCOUNTING TECHNICIANS Prepare Final Accounts for Sole Traders and Partnerships Level 3 Published by: Home Learning College 1 Hammersmith Broadway London W6 9DL Home Learning College Ltd

ASSOCIATION OF ACCOUNTING TECHNICIANS Prepare Final Accounts for Sole Traders and Partnerships Level 3 Published by: Home Learning College 1 Hammersmith Broadway London W6 9DL Home Learning College Ltd

Chapter 9 Auditor s Response to Assessed Risk (ISA 330, ISA 500)

") Slide 9.1 Principles of Auditing: An Introduction to International Standards on Auditing Chapter 9 Auditor s Response to Assessed Risk (ISA 330, ISA 500) Rick Hayes, Hans Gortemaker and Philip Wallage

Slide 9.1 Principles of Auditing: An Introduction to International Standards on Auditing Chapter 9 Auditor s Response to Assessed Risk (ISA 330, ISA 500) Rick Hayes, Hans Gortemaker and Philip Wallage

Comments to be received by 1 August 2008

16 June 2008 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IFAC S INTERNATIONAL ETHICS STANDARDS BOARD FOR ACCOUNTANTS (IESBA) RE EXPOSURE DRAFT ON

16 June 2008 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IFAC S INTERNATIONAL ETHICS STANDARDS BOARD FOR ACCOUNTANTS (IESBA) RE EXPOSURE DRAFT ON

REVIEW OF AMG s QUARTERLY FINANCAL STATEMENTS: A SHORT CASE ABOUT AUDITOR RESPONSIBILITIES AND REQUIREMENTS

REVIEW OF AMG s QUARTERLY FINANCAL STATEMENTS: A SHORT CASE ABOUT AUDITOR RESPONSIBILITIES AND REQUIREMENTS Kathleen A Simione, Quinnipiac University Aamer Sheikh, Quinnipiac University INSTRUCTORS NOTES

REVIEW OF AMG s QUARTERLY FINANCAL STATEMENTS: A SHORT CASE ABOUT AUDITOR RESPONSIBILITIES AND REQUIREMENTS Kathleen A Simione, Quinnipiac University Aamer Sheikh, Quinnipiac University INSTRUCTORS NOTES

Utility Debt Securitization Authority

Utility Debt Securitization Authority Audit results Financial statements for the year ended December 31, 2017 March 26, 2018 This presentation to the Finance and Audit Committee is intended solely for

Utility Debt Securitization Authority Audit results Financial statements for the year ended December 31, 2017 March 26, 2018 This presentation to the Finance and Audit Committee is intended solely for

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS 99 100 101 102 CITY OF GEORGETOWN, SOUTH CAROLINA Schedule of Findings and Questioned Costs For the Year Ended June 30, 2008 A. Summary

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS 99 100 101 102 CITY OF GEORGETOWN, SOUTH CAROLINA Schedule of Findings and Questioned Costs For the Year Ended June 30, 2008 A. Summary

ACCOUNTING I. 1. The cash account is used to summarize information about the amount of money the business has available.

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

ACCOUNTING I True/False Indicate whether the sentence or statement is true or false. 1. The cash account is used to summarize information about the amount of money the business has available. 2. The source

Features for Singapore

Features for Singapore Microsoft Corporation Published: November 2006 Microsoft Dynamics is a line of integrated, adaptable business management solutions that enables you and your people to make business

Features for Singapore Microsoft Corporation Published: November 2006 Microsoft Dynamics is a line of integrated, adaptable business management solutions that enables you and your people to make business

Verification of Debtor Balances Confirmation by Direct Communication

AUDIT GUIDANCE STATEMENT AGS 2 Verification of Debtor Balances Confirmation by Direct Communication This Statement of Auditing Practice was approved by the Council of the Institute of Singapore Chartered

AUDIT GUIDANCE STATEMENT AGS 2 Verification of Debtor Balances Confirmation by Direct Communication This Statement of Auditing Practice was approved by the Council of the Institute of Singapore Chartered

FUNDAMENTAL ACCOUNTING (01)

") 13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2006 Multiple Choice (30 @ 3 points each) Account Identification (15 @ 3 points each) Production Portion Problem 1: Financial Transactions

13 Pages Contestant Number Time Rank FUNDAMENTAL ACCOUNTING (01) Regional 2006 Multiple Choice (30 @ 3 points each) Account Identification (15 @ 3 points each) Production Portion Problem 1: Financial Transactions

Tally.ERP 9 Series A Release 1.5 Stat.900 Version 90. Release Notes

Tally.ERP 9 Series A Release 1.5 Stat.900 Version 90 Release Notes August 28, 2009 The information contained in this document is current as of the date of publication and subject to change. Because Tally

Tally.ERP 9 Series A Release 1.5 Stat.900 Version 90 Release Notes August 28, 2009 The information contained in this document is current as of the date of publication and subject to change. Because Tally

National State Auditors Association

National State Auditors Association GASB Update Assessing Risks The views expressed in this presentation are those of Chairman Vaudt and Mr. Bean. Official positions of the GASB are reached only after

National State Auditors Association GASB Update Assessing Risks The views expressed in this presentation are those of Chairman Vaudt and Mr. Bean. Official positions of the GASB are reached only after

Statement of Financial Accounting Standards No. 37

Statement of Financial Accounting Standards No. 37 FAS37 Status Page FAS37 Summary Balance Sheet Classification of Deferred Income Taxes (an amendment of APB Opinion No. 11) July 1980 Financial Accounting

Statement of Financial Accounting Standards No. 37 FAS37 Status Page FAS37 Summary Balance Sheet Classification of Deferred Income Taxes (an amendment of APB Opinion No. 11) July 1980 Financial Accounting

Glossary of Terms. (From 2001 IFAC Handbook of Auditing and Ethics Pronouncements)

") Appendix 1 Glossary of Terms (From 2001 IFAC Handbook of Auditing and Ethics Pronouncements) Accounting estimate An accounting estimate is an approximation of the amount of an item in the absence of a

Appendix 1 Glossary of Terms (From 2001 IFAC Handbook of Auditing and Ethics Pronouncements) Accounting estimate An accounting estimate is an approximation of the amount of an item in the absence of a

New VAT Return for Orissa Form 201

New VAT Return for Orissa Form 201 The information contained in this document represents the current view of Tally Solutions Pvt. Ltd., ( Tally in short) on the topics discussed as of the date of publication.

New VAT Return for Orissa Form 201 The information contained in this document represents the current view of Tally Solutions Pvt. Ltd., ( Tally in short) on the topics discussed as of the date of publication.

Name: Date: Period: Standard 2: Students will list and identify characteristics of the three basic accounting equation elements.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Name: Date: Period: Accounting I State Test Review Standard 2: Students will list and identify characteristics of the three basic accounting equation elements. (Chapter 1) 1. Write the accounting equation.

Interest Calculation Add-on Supernova Add-on for SAP Business One

User Manual Supernova Add-on for SAP Business One Date: October 2013 Copyright 2013 Supernova Consulting Ltd. All rights reserved. This content may not be reproduced or transmitted in any form or by any

User Manual Supernova Add-on for SAP Business One Date: October 2013 Copyright 2013 Supernova Consulting Ltd. All rights reserved. This content may not be reproduced or transmitted in any form or by any

VIETNAMESE STANDARDS ON AUDITING

VIETNAMESE STANDARDS ON AUDITING -------------------------------------------------------------------------------------------------------- STANDARD 910 ENGAGEMENTS TO REVIEW FINANCIAL STATEMENTS (Issued

VIETNAMESE STANDARDS ON AUDITING -------------------------------------------------------------------------------------------------------- STANDARD 910 ENGAGEMENTS TO REVIEW FINANCIAL STATEMENTS (Issued

Operational Procedures for Loaning Funds to Others

Note: The original version of this regulation is published in Chinese. In case of discrepancy between the Chinese and English versions the Chinese version shall prevail. This document is copyrighted by

Note: The original version of this regulation is published in Chinese. In case of discrepancy between the Chinese and English versions the Chinese version shall prevail. This document is copyrighted by

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 8 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF RECEIVABLES PROBLEM NO. 1 In the audit of Beatles Company, the auditor had an appreciation of the following schedule and noted

Page 1 of 8 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF RECEIVABLES PROBLEM NO. 1 In the audit of Beatles Company, the auditor had an appreciation of the following schedule and noted

XCEDE PROFESSIONAL ACCOUNTING. Master Sheets and Templates Release Notes

XCEDE PROFESSIONAL ACCOUNTING Master Sheets and Templates Release Notes August 2016 Author Created and Published by Reckon Limited Level 12, 65 Berry Street North Sydney NSW 2060 Australia ACN 003 348

XCEDE PROFESSIONAL ACCOUNTING Master Sheets and Templates Release Notes August 2016 Author Created and Published by Reckon Limited Level 12, 65 Berry Street North Sydney NSW 2060 Australia ACN 003 348

Best Execution Retail Client Orders Summary Disclosure Statement HSBC Bank plc Global Markets

Jan 2018 Best Execution Retail Client Orders Summary Disclosure Statement HSBC Bank plc Global Markets Dated 3 January 2018 PUBLIC Jan 2018 Copyright. HSBC Bank plc 2018 ALL RIGHTS RESERVED. No part of

Jan 2018 Best Execution Retail Client Orders Summary Disclosure Statement HSBC Bank plc Global Markets Dated 3 January 2018 PUBLIC Jan 2018 Copyright. HSBC Bank plc 2018 ALL RIGHTS RESERVED. No part of

2017 Audit Timeline/Critical Dates List

2017 Audit Timeline/Critical Dates List Item Due Date Status Planning Meeting with AUDITORS and SJCERA Management Wednesday, December 06, 2017 Completed RETIRED Populations provided to AUDITOR Friday,

2017 Audit Timeline/Critical Dates List Item Due Date Status Planning Meeting with AUDITORS and SJCERA Management Wednesday, December 06, 2017 Completed RETIRED Populations provided to AUDITOR Friday,

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Little Britain Township Tax Collector Audit Report

Audit Report For the period of January 1, 2016 through January 15, 2017 covering the 2016 tax year Brian K. Hurter, CPA Lancaster County Controller Audit For the period of January 1, 2016 through January

Audit Report For the period of January 1, 2016 through January 15, 2017 covering the 2016 tax year Brian K. Hurter, CPA Lancaster County Controller Audit For the period of January 1, 2016 through January

SAMPLE AUDIT REPORT. Sample Credit Union. Report on Operations. As of Audit Date

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

Principal Audit Procedures

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF INFOSYS LIMITED Report on the Audit of the Interim Consolidated Financial Statements Opinion We have audited the accompanying interim consolidated

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF INFOSYS LIMITED Report on the Audit of the Interim Consolidated Financial Statements Opinion We have audited the accompanying interim consolidated

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF INFOSYS LIMITED. Report on the Audit of Interim Consolidated Financial Statements.

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF INFOSYS LIMITED Report on the Audit of Interim Consolidated Financial Statements Opinion We have audited the accompanying interim consolidated

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF INFOSYS LIMITED Report on the Audit of Interim Consolidated Financial Statements Opinion We have audited the accompanying interim consolidated

Tally.ERP 9 Series A Release 1.51 Stat.900 Version 91. Release Notes

Tally.ERP 9 Series A Release 1.51 Stat.900 Version 91 Release Notes September 25, 2009 The information contained in this document is current as of the date of publication and subject to change. Because

Tally.ERP 9 Series A Release 1.51 Stat.900 Version 91 Release Notes September 25, 2009 The information contained in this document is current as of the date of publication and subject to change. Because

Oracle Communications Billing and Revenue Management

Oracle Communications Billing and Revenue Management Managing Accounts Receivable Release 7.4 E25079-01 March 2013 Oracle Communications Billing and Revenue Management Managing Accounts Receivable, Release

Oracle Communications Billing and Revenue Management Managing Accounts Receivable Release 7.4 E25079-01 March 2013 Oracle Communications Billing and Revenue Management Managing Accounts Receivable, Release

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

5/03/15. Module 8: Revenue and collection cycle, and acquisition and expenditure cycle

Instructor Michael Brownlee B.Comm(Hons),CGA Module 8: Revenue and collection cycle, and acquisition and expenditure cycle 8.1 The balance sheet approach 8.2 Revenue and collection cycle The basics 8.3

Instructor Michael Brownlee B.Comm(Hons),CGA Module 8: Revenue and collection cycle, and acquisition and expenditure cycle 8.1 The balance sheet approach 8.2 Revenue and collection cycle The basics 8.3

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF INFOSYS LIMITED. Report on the Audit of the Interim Consolidated Financial Statements

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF INFOSYS LIMITED Report on the Audit of the Interim Statements Opinion We have audited the accompanying interim consolidated financial statements

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF INFOSYS LIMITED Report on the Audit of the Interim Statements Opinion We have audited the accompanying interim consolidated financial statements

Campus Financial Sub-Certification - Explanation

Campus Financial Sub-Certification - Explanation 1. Within the areas for which I am responsible, all transactions, agreements and amounts have been properly reflected in the University s accounting records.

Campus Financial Sub-Certification - Explanation 1. Within the areas for which I am responsible, all transactions, agreements and amounts have been properly reflected in the University s accounting records.

The District Municipality of Muskoka

The District Municipality of Muskoka For the year ended December 31, 2017 Report to Council Audit strategy February 22, 2018 Mike Bunn CPA, CA Principal T 705 797 3012 E Mike.Bunn@ca.gt.com Thomas Turnbull

The District Municipality of Muskoka For the year ended December 31, 2017 Report to Council Audit strategy February 22, 2018 Mike Bunn CPA, CA Principal T 705 797 3012 E Mike.Bunn@ca.gt.com Thomas Turnbull