Chapter 10. Cash and Financial Investments. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

|

|

|

- Miles Chandler

- 6 years ago

- Views:

Transcription

1 Chapter 10 Cash and Financial Investments McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

2 Sources and Nature of Cash Sources General checking account Payroll checking accounts Petty cash Savings accounts Cash equivalents Money market funds Certificates of deposit Savings certificates 10-2

3 Objectives for the Audit Cash 1. Use the understanding of the client and its environment to consider inherent risk, including fraud risks, related to cash 2. Obtain an understanding of internal control over cash. 3. Assess the risks of material misstatement of cash and design tests of controls and substantive procedures that: a. Substantiate the existence of recorded cash and occurrence of the related transactions b. Establish the completeness of recorded cash c. Verify the cutoff and accuracy of cash transactions d. Determine that the client has rights to recorded cash e. Determine that the presentation and disclosure of cash, including restricted funds, are appropriate 10-3

4 Audit time for cash Cash typically has a small account balance, but auditors devote a large proportion of total audit hours because: Liabilities, revenues, expenses and most other assets flow through cash Most liquid asset so greater temptation for misappropriation High risk account 10-4

5 Management Assurance Finance and accounting department work together to provide assurance that: All cash that should have been received was in fact received, recorded accurately and deposited promptly Cash disbursements have been made for authorized purposes only and have been properly recorded Cash balances are maintained at adequate, but not excessive, levels by forecasting 10-5

6 Guidelines for Internal Control (1 of 2) 1. Do not permit any one employee to handle a transaction from beginning to end. 2. Separate cash handling from recordkeeping. 3. Centralize receiving of cash to the extent practical. 4. Record cash receipts on a timely basis. 5. Encourage customers to obtain receipts and observe cash register totals. 10-6

7 Guidelines for Internal Control (2 of 2) 6. Deposit cash receipts daily. 7. Make all disbursements by check or electronic funds transfer, with the exception of small expenditures from petty cash. 8. Have monthly bank reconciliations prepared by employees not responsible for the issuance of checks or custody of cash. The completed reconciliation should be reviewed promptly by an appropriate official. 9. Monitor cash receipts and disbursements by comparing recorded amounts to forecasted amounts 10-7

8 Internal Control Over -- Cash Receipts Cash sales Involvement of two or more employees Cash Registers Electronic point of sales systems Collections of receivables Initial listing of cash receipts Custody and depositing of cash receipts Maintenance of customer account records Reconciliation of customers ledgers with control accounts Mailing monthly statements to customers Collection activity and past-due accounts Direct receipt of funds by financial institution 10-8

9 Cash Receipts Flowchart 10-9

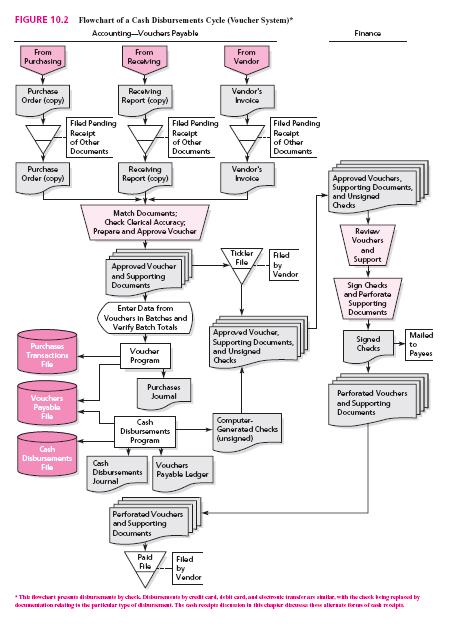

10 Internal Control--Cash Disbursements Segregation of duties Payment by check or electronic funds transfer Pre-numbered check Match of purchase order and receiving documents with vendor s invoice Review of supporting documents by authorized check signer Cancel of supporting documents Authorized check signer should mail checks Monthly bank reconciliation 10-10

11 10-11

12 Audit of Cash (1 of 3) A. Use the understanding of the client and its environment to consider inherent risks, including fraud risks, related to cash. B. Obtain an understanding of internal control over cash. C. Assess the risks of material misstatement and design further audit procedures

13 Audit of Cash (2 of 3) D. Perform further audit procedures tests of controls. 1. Examples of tests of controls: a. Test the accounting records and reconciliations by reperformance. b. Compare the details of a sample of cash receipts listings to the cash receipts journal, accounts receivable postings, and authenticated deposit slips. c. Compare the details of a sample of recorded disbursements in the cash payments journal to account payable postings, purchase orders, receiving reports, invoices, and paid checks. 2. If necessary, revise the risk of material misstatement based on the results of tests of controls

14 Audit of Cash (3 of 3) E. Perform further audit procedures substantive procedures for cash transactions and balances. 1. Obtain analyses of cash balances and reconcile them to the general ledger. 2. Confirm cash balances with financial institutions. 3. Obtain or prepare reconciliations of bank (financial institution) accounts as of the balance sheet date and consider the need to reconcile bank activity for additional months. 4. Obtain a cutoff bank statement containing transactions of at least seven business days subsequent to balance sheet date. 5. Count and list cash on hand. 6. Verify the client s cutoff of cash receipts and cash disbursements. 7. Analyze bank transfers for the last week of audit year and the first week of following year. 8. Investigate any checks representing large or unusual payments to related parties. 9. Evaluate proper financial statement presentation and disclosure of cash

15 Summary of Substantive Tests for Cash Balances 10-15

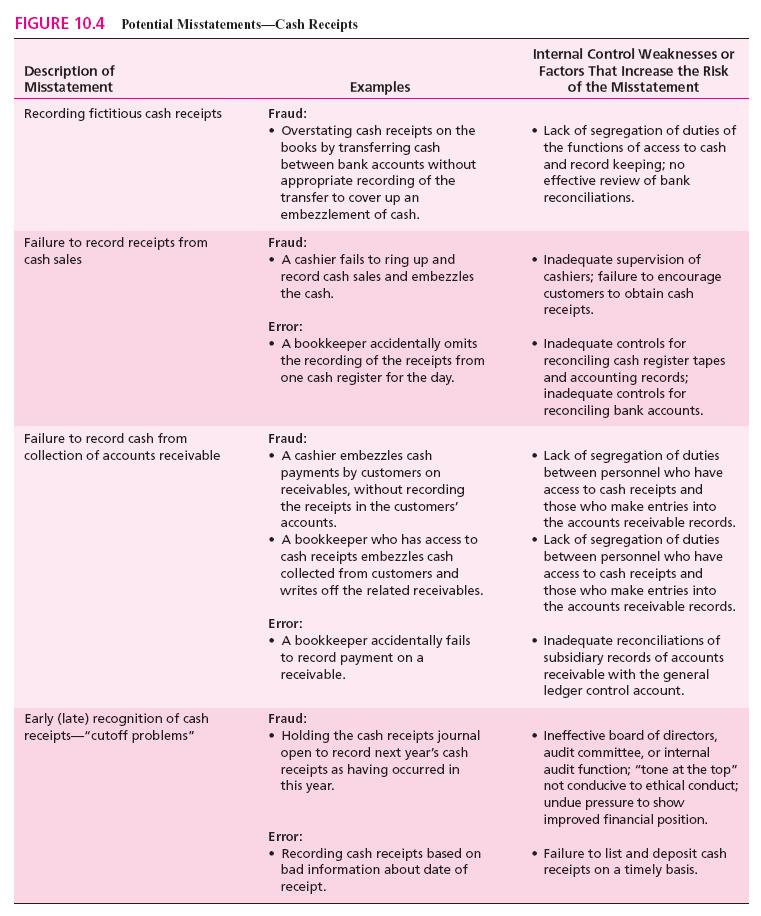

16 Examples of fraud with cash Do the client s records reflect all cash transactions that took place during the year? Were all cash payments properly authorized and for a legitimate business purpose? Fraud that may be disclosed Interception of cash receipts before any record is made Payment for materials not received Duplicate payments Overpayments to employees or payments to fictitious employees Payments for personal expenditures of officers or related parties 10-16

17 10-17

18 Potential Misstatements--Cash Disbursements Inaccurate recording of a purchase or disbursement Duplicate recording and payment of purchases Unrecorded disbursements 10-18

19 Standard Confirmation--General Information Confirmation of amounts on deposit by direct communication with financial institution officials Standard form agreed to by: AICPA American Bankers Association Bank Administration Institute Addresses only the client s deposit and loan balances The confirmation process may be performed electronically if properly controlled 10-19

20 Standard Confirmation 10-20

21 Proof of Cash General Information Reconciles the account balance and reconciles cash transactions during a specified period. Used to identify: Cash receipts and disbursements recorded in the accounting records, but not on the bank statement. Cash deposits and disbursements recorded on the bank statement, but not on the accounting records. Cash receipts and disbursements recorded at different amounts by the bank than in the accounting records

22 Proof of Cash 10-22

23 Check 21 Act Checks may be processed electronically Electronic processing creates a substitute check an electronic image of check Legal equivalent of original check for all purposes Audit implications Need to rely on substitute check for evidence of check Impossible for clients to kite checks (manipulate bank balances to conceal cash shortage) 10-23

.")

24 Kiting Manipulations that utilize temporarily overstated bank balances to conceal cash shortage or meet short-term cash needs Kiting schemes rely upon the existence of a float period in which transactions are not processed in real time; increased electronic processing has made kiting more difficult through reducing (or eliminating the float period). Auditors can detect kiting by preparing a schedule of bank transfers for a few days before and after balance sheet date Misstatements Date of recording per transfer per the books are from different financial statement periods Date the check was recorded by the bank is from financial statement period prior to books 10-24

25 Bank Transfer Schedule 10-25

26 Specialized Knowledge to Audit Financial Investments Identifying controls at service organizations that provide financial services and are part of the client s information system. Obtaining an understanding of information systems for securities and derivatives that are highly dependent on computer technology. Applying complex accounting principles to various types of financial investments. Understanding the methods used to determine the fair values of financial investments, especially those that must be valued using complex valuation models. Assessing inherent and control risk for assertions about derivatives used in hedging activities

27 Objectives for the Audit of Financial Investments 1. Use the understanding of the client and its environment to consider inherent risk, including fraud risks, related to financial instruments 2. Obtain an understanding of internal control over financial instruments. 3. Assess the risks of material misstatement of financial instruments and design tests of controls and substantive procedures that: a. Substantiate the existence of recorded financial investments and the occurrence of investment transactions. b. Establish the completeness of financial investments and investment transactions. c. Verify the cutoff of investment transactions. d. Determine that the client has rights to recorded investments

28 Controls Over Financial Investments Establishment of formal investment policies Review and approval of investment activities by the investment committee of the board of directors Separation of duties among employees 1. Authorizing purchases and sales 2. Having custody of the securities 3. Maintaining records Detailed records of all securities owned and the related revenue from interest and dividends Registration in the name of the company Periodic physical inspection of securities Determination of accounting for complex instruments by competent personnel 10-28

29 Audit of Financial Investments (1 of 4) A. Use the understanding of the client and its environment to consider inherent risks, including fraud risks related to financial investments. B. Obtain an understanding of internal control over financial investments C. Assess the risks of material misstatement and design further audit procedures

30 Audit of Financial Investments (2 of 4) D. Perform further audit procedures tests of controls. 1. Examples of tests of controls: a. Trace several transactions for purchases and sales of investments through the accounting system. b. Review and test reports of investment activity prepared for the investment committee. c. Inspect reports by internal auditors regarding their periodic inspection and review of securities and derivative instruments. d. Inspect monthly reports on securities owned, purchased, and sold and amounts of revenue earned and budgeted. 2. If necessary, revise the risk of material misstatement based on the results of tests of controls

31 Audit of Financial Investments (3 of 4) E. Perform further audit procedures substantive procedures for investment transactions and year-end balances. 1. Obtain or prepare analyses of the investment accounts and related revenue, gain, and loss accounts and reconcile them to the general ledger. 2. Inspect securities on hand and review agreements underlying derivatives. 3. Confirm securities and derivative instruments with holders and counterparties. 4. Vouch selected purchases and sales of financial investments during the year and verify the client s cutoff of investment transactions. 5. Review investment committee minutes and reports

32 Audit of Financial Statements (4 of 4) E. further audit procedures cont. 6. Perform analytical procedures. 7. Make independent computations of revenue from securities. 8. Inspect documentation of management s intent to classify derivative transactions as hedging activities. 9. Evaluate the method of accounting for investments. 10. Test the valuation of financial investments. 11. Evaluate financial statement presentation and disclosure of financial investments

33 Test Valuation FASB requirements for derivative instruments and hedging activities: All derivative instruments valued at fair values Unrealized gains or losses depend on classification as hedges FASB requirements allow companies to choose to use fair value accounting in this area

34 Potential Misstatements--Financial Investments Misstatement of recorded value of investments Unauthorized investment transactions Incomplete recording of investments Inadequate disclosure of the nature of investment activities 10-34

35 Summary of Substantive Procedures for Financial Investments 10-35

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 10 Finance and Investment Cycle Learning Objectives 1. Describe the finance and investment cycle, including

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 10 Finance and Investment Cycle Learning Objectives 1. Describe the finance and investment cycle, including

Chapter 10. Auditing the Revenue Process. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 10 Auditing the Revenue Process McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Revenue Recognition Revenue is defined as inflows or other enhancements

Chapter 10 Auditing the Revenue Process McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO# 1 Revenue Recognition Revenue is defined as inflows or other enhancements

Chapter 10. Auditing the Revenue Process

Chapter 10 Auditing the Revenue Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. LO# 1 Revenue

Chapter 10 Auditing the Revenue Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. LO# 1 Revenue

Cash and Financial Investments

CHAPTER 10 Cash and Financial Investments Review Questions 10 1 The following circumstances might cause a client to understate assets: (1) Management of a privately held company may be motivated to understate

CHAPTER 10 Cash and Financial Investments Review Questions 10 1 The following circumstances might cause a client to understate assets: (1) Management of a privately held company may be motivated to understate

Chapter 23 Audit of Cash and Financial Instruments. Copyright 2014 Pearson Education

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Chapter 23 Audit of Cash and Financial Instruments Identify the major types of cash and financial instruments accounts maintained by business entities. Show the relationship of cash in the bank to the

Auditing and Assurance Services, 15e

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Auditing and Assurance Services, 15e (Arens) Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Learning Objective 14-1 1) Which of the following

Chapter 15. Auditing the Financing/Investing Process: Long-Term Liabilities, Stockholders Equity, and Income Statement Accounts

Chapter 15 Auditing the Financing/Investing Process: Long-Term Liabilities, Stockholders Equity, and Income Statement Accounts Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction

Chapter 15 Auditing the Financing/Investing Process: Long-Term Liabilities, Stockholders Equity, and Income Statement Accounts Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction

Chapter 14. Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment

Chapter 14 Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or

Chapter 14 Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or

Chapter 14. Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment

Chapter 14 Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights

Chapter 14 Auditing the Financing/Investing Process: Prepaid Expenses, Intangible Assets, and Property, Plant, and Equipment McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights

Chapter 05. Audit Evidence and Documentation. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 05 Audit Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Audit Risk The possibility that the auditors may unknowingly fail to

Chapter 05 Audit Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Audit Risk The possibility that the auditors may unknowingly fail to

Chapter 16 Completing the Tests in the Sales and Collection Cycle:

Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Describe the methodology for designing tests of details of balances using the audit risk model. Design and perform

Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Describe the methodology for designing tests of details of balances using the audit risk model. Design and perform

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 07 Revenue and Collection Cycle What at first was plunder assumed the softer name of revenue. Thomas Paine

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 07 Revenue and Collection Cycle What at first was plunder assumed the softer name of revenue. Thomas Paine

Identifying Risk: Understanding the Entity and its Environment

CASE STUDY: PIZZA SHOP, INC. Identifying Risk: Understanding the Entity and its Environment Pizza Shop, Inc. (PSI or the Entity) owns and operates dine-in restaurants offering Italian cuisine. PSI was

CASE STUDY: PIZZA SHOP, INC. Identifying Risk: Understanding the Entity and its Environment Pizza Shop, Inc. (PSI or the Entity) owns and operates dine-in restaurants offering Italian cuisine. PSI was

Solutions. I. Auditing Cash and Cash Equivalents. A. Learning Question Answers

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

Piotr Pyziak, Consultant, CFRR

Piotr Pyziak, Consultant, CFRR 16 March 2017, Vienna Audit Training of Trainers Road to Europe: Program of Accounting Reform and Institutional Strengthening EU-REPARIS is funded by the European Union and

Piotr Pyziak, Consultant, CFRR 16 March 2017, Vienna Audit Training of Trainers Road to Europe: Program of Accounting Reform and Institutional Strengthening EU-REPARIS is funded by the European Union and

5/03/15. Module 8: Revenue and collection cycle, and acquisition and expenditure cycle

Instructor Michael Brownlee B.Comm(Hons),CGA Module 8: Revenue and collection cycle, and acquisition and expenditure cycle 8.1 The balance sheet approach 8.2 Revenue and collection cycle The basics 8.3

Instructor Michael Brownlee B.Comm(Hons),CGA Module 8: Revenue and collection cycle, and acquisition and expenditure cycle 8.1 The balance sheet approach 8.2 Revenue and collection cycle The basics 8.3

Chapter 9. #17 is a bad question if it is changed as follows the answer is d

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Corridor District of the North Carolina Conference The United Methodist Church

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

ACCOUNTING POLICIES AND PROCEDURES MANUAL

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

Audit Program for Cash

Form AP 10 Index Reference Audit Program for Cash Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

Form AP 10 Index Reference Audit Program for Cash Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES OUTLINE Application of specific substantive procedures to test the following categories of assertions: -Assertions relating to

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES OUTLINE Application of specific substantive procedures to test the following categories of assertions: -Assertions relating to

If no board of directors exists, identify the equivalent body with oversight responsibility.

October 26, 2017 These illustrative reports conform to the requirements of AT-C section 315 and are applicable when a practitioner expresses an opinion on management s assertion about compliance with Rule

October 26, 2017 These illustrative reports conform to the requirements of AT-C section 315 and are applicable when a practitioner expresses an opinion on management s assertion about compliance with Rule

Audit Evidence. What do mean by the Audit Evidence?

What do mean by the Audit Evidence? Audit Evidence Sri Lanka auditing Standard 500 provides the definition of the audit evidence as all the information used by auditors in arriving at the conclusions on

What do mean by the Audit Evidence? Audit Evidence Sri Lanka auditing Standard 500 provides the definition of the audit evidence as all the information used by auditors in arriving at the conclusions on

Introduction to Fraud in Cash Collections and Disbursements

Introduction to Fraud in Cash Collections and Disbursements #6180C COURSE MATERIAL TABLE OF CONTENTS Chapter 1: Cash Collections and Receivables 1 Revenue and Collection Cycle: Typical Activities 1 Audit

Introduction to Fraud in Cash Collections and Disbursements #6180C COURSE MATERIAL TABLE OF CONTENTS Chapter 1: Cash Collections and Receivables 1 Revenue and Collection Cycle: Typical Activities 1 Audit

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Vudesk.com (chief)ismail shah SiLeNt Moon(Admin) ACC311- Fundamentals of Auditing (Session - 1)

ismail shah SiLeNt Moon(Admin) ACC311- Fundamentals of Auditing (Session - 1)") Vudesk.com (chief)ismail shah (admin@vudesk.com) SiLeNt Moon(Admin) ACC311- Fundamentals of Auditing (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one When the cash sales should be recorded

Vudesk.com (chief)ismail shah (admin@vudesk.com) SiLeNt Moon(Admin) ACC311- Fundamentals of Auditing (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one When the cash sales should be recorded

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS The principal shall be responsible to the county board of education for financial management of his school. He shall authorize

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS The principal shall be responsible to the county board of education for financial management of his school. He shall authorize

City of Albertville Wright County, Minnesota Reports on Compliance with Government Auditing Standards and Minnesota Legal Compliance

Wright County, Minnesota Reports on Compliance with Government Auditing Standards and Minnesota Legal Compliance December 31, 2015 Table of Contents Report on Internal Control over Financial Reporting

Wright County, Minnesota Reports on Compliance with Government Auditing Standards and Minnesota Legal Compliance December 31, 2015 Table of Contents Report on Internal Control over Financial Reporting

TownofGibsland Gibsland, Louisiana. Agreed Upon Procedures For the Period July 1,2006 to December 31,2006

2-2 5" / RECEIVED ATE AUOITjR 2007 MAR -7 PMI2= 12 TownofGibsland Gibsland, Louisiana Agreed Upon Procedures For the Period July 1,2006 to December 31,2006 Under provisions of state law, this report is

2-2 5" / RECEIVED ATE AUOITjR 2007 MAR -7 PMI2= 12 TownofGibsland Gibsland, Louisiana Agreed Upon Procedures For the Period July 1,2006 to December 31,2006 Under provisions of state law, this report is

a) The elements required for establishing an auditor s liability for negligence to clients are:

The elements required for establishing an auditor s liability for negligence to clients are:") SOLUTION SET 1 ANSWERS 1 Part A a) The elements required for establishing an auditor s liability for negligence to clients are: 1. The duty to conform to a required standard duty of care 2. Failure to

SOLUTION SET 1 ANSWERS 1 Part A a) The elements required for establishing an auditor s liability for negligence to clients are: 1. The duty to conform to a required standard duty of care 2. Failure to

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings. September 30, 2001 and 2000

Schedule of Findings. September 30, 2001 and 2000") GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

Campus Financial Sub-Certification - Explanation

Campus Financial Sub-Certification - Explanation 1. Within the areas for which I am responsible, all transactions, agreements and amounts have been properly reflected in the University s accounting records.

Campus Financial Sub-Certification - Explanation 1. Within the areas for which I am responsible, all transactions, agreements and amounts have been properly reflected in the University s accounting records.

Syracuse City School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Syracuse City School District Internal Controls Over Selected Financial Operations Report of Examination Period

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Syracuse City School District Internal Controls Over Selected Financial Operations Report of Examination Period

Floyd County, Georgia Report Of Independent Certified Public Accountants In Accordance With Government Auditing Standards

Floyd County, Georgia Report Of Independent Certified Public Accountants In Accordance With Government Auditing Standards For the Year Ended December 31, 2017 TABLE OF CONTENTS Page INDEPENDENT AUDITOR

Floyd County, Georgia Report Of Independent Certified Public Accountants In Accordance With Government Auditing Standards For the Year Ended December 31, 2017 TABLE OF CONTENTS Page INDEPENDENT AUDITOR

October 19, Board of School Directors North Hero School District c/o Grand Isle Supervisory Union 5038 US Route 2 North Hero, Vermont 05474

October 19, 2018 Board of School Directors North Hero School District c/o Grand Isle Supervisory Union 5038 US Route 2 North Hero, Vermont 05474 We have audited the financial statements of the North Hero

October 19, 2018 Board of School Directors North Hero School District c/o Grand Isle Supervisory Union 5038 US Route 2 North Hero, Vermont 05474 We have audited the financial statements of the North Hero

STATE OF MINNESOTA Office of the State Auditor

STATE OF MINNESOTA Office of the State Auditor Patricia Anderson State Auditor MANAGEMENT AND COMPLIANCE REPORT PREPARED AS A RESULT OF THE AUDIT OF THE FINANCIAL AFFAIRS OF THE CITY OF GREENFIELD GREENFIELD,

STATE OF MINNESOTA Office of the State Auditor Patricia Anderson State Auditor MANAGEMENT AND COMPLIANCE REPORT PREPARED AS A RESULT OF THE AUDIT OF THE FINANCIAL AFFAIRS OF THE CITY OF GREENFIELD GREENFIELD,

OFFICE OF THE STATE AUDITOR

OFFICE OF THE STATE AUDITOR Timothy M Keller Hanover Mutual Domestic Water Consumers Association Independent Accountant s Report on Applying Agreed-Upon For the Year Ended December 31, 2014 Hanover Mutual

OFFICE OF THE STATE AUDITOR Timothy M Keller Hanover Mutual Domestic Water Consumers Association Independent Accountant s Report on Applying Agreed-Upon For the Year Ended December 31, 2014 Hanover Mutual

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS 99 100 101 102 CITY OF GEORGETOWN, SOUTH CAROLINA Schedule of Findings and Questioned Costs For the Year Ended June 30, 2008 A. Summary

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS 99 100 101 102 CITY OF GEORGETOWN, SOUTH CAROLINA Schedule of Findings and Questioned Costs For the Year Ended June 30, 2008 A. Summary

Chapter 06 - Cash and Internal Controls. Chapter Outline

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

I. Internal Control A. Purpose of Internal Control A properly designed internal control system is a key part of system design, analysis, and performance. Internal controls do not provide guarantees, but

Conceptual Framework of Assurance II: Types of Assertions

Conceptual Framework of Assurance II: Types of Assertions Joshua Onome Imoniana September 8, 2014 Student s Key takeaway from this lecture include: What is an assertion? Useful steps to verify an assertion.

Conceptual Framework of Assurance II: Types of Assertions Joshua Onome Imoniana September 8, 2014 Student s Key takeaway from this lecture include: What is an assertion? Useful steps to verify an assertion.

UNIVERSITY OF TOLEDO INTERNAL AUDIT DEPARTMENT HANDLE WARRANTIES AND CLAIMS

The following control objectives provide a basis for strengthening your control environment for the process of handling warranties and claims. When you select an objective, you will access a list of the

The following control objectives provide a basis for strengthening your control environment for the process of handling warranties and claims. When you select an objective, you will access a list of the

MORTON SALT Employee Handbook. Internal Control Procedures

MORTON SALT Employee Handbook Internal Control Procedures 1. Bank Accounts the opening of any new account at any bank or financial institution. All such accounts must be listed in the name of the appropriate

MORTON SALT Employee Handbook Internal Control Procedures 1. Bank Accounts the opening of any new account at any bank or financial institution. All such accounts must be listed in the name of the appropriate

Illustrate by way of some example how Fraudulent Financial Reporting and Misappropriation of Asset can be done?

SA240(R) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL What is a Fraud? Intentional mistakes to get unjust advantage are commonly known as fraud. Fraud as defined by SA 240

SA240(R) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL What is a Fraud? Intentional mistakes to get unjust advantage are commonly known as fraud. Fraud as defined by SA 240

ACCA F8. Provided by Academy of Professional Accounting (APA) Audit and Assurance (AA) 审计与鉴证业务第 7 讲 ACCA Lecturer: Andy Qu

Audit and Assurance (AA) 审计与鉴证业务第 7 讲 ACCA Lecturer: Andy Qu") Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F8 Audit and Assurance (AA) 审计与鉴证业务第 7 讲 ACCA Lecturer: Andy Qu ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F8 Audit and Assurance (AA) 审计与鉴证业务第 7 讲 ACCA Lecturer: Andy Qu ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM. Test Code CIN 5020

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM SUBJECT- AUDIT Test Code CIN 5020 (Date :09.09.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM SUBJECT- AUDIT Test Code CIN 5020 (Date :09.09.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P

Professional Bridging Examination. Paper III PBE Auditing and Information Systems

Professional Bridging Examination Pilot Examination Paper Paper III PBE Auditing and Information Systems Questions & Answers Booklet The suggested answers given in this booklet are purposely made to give

Professional Bridging Examination Pilot Examination Paper Paper III PBE Auditing and Information Systems Questions & Answers Booklet The suggested answers given in this booklet are purposely made to give

UNIVERSITY OF TOLEDO INTERNAL AUDIT DEPARTMENT MANAGE CASH FLOW

The following control objectives provide a basis for strengthening your control environment for the process of managing cash flow. When you select an objective, you will access a list of the associated

The following control objectives provide a basis for strengthening your control environment for the process of managing cash flow. When you select an objective, you will access a list of the associated

Guidelines for Church Financial Review

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Special Considerations in Auditing Complex Financial Instruments Draft International Auditing Practice Statement 1000

Special Considerations in Auditing Complex Financial Instruments Draft International Auditing Practice Statement CONTENTS [REVISED FROM JUNE 2010 VERSION] Paragraph Scope of this IAPS... 1 3 Section I

Special Considerations in Auditing Complex Financial Instruments Draft International Auditing Practice Statement CONTENTS [REVISED FROM JUNE 2010 VERSION] Paragraph Scope of this IAPS... 1 3 Section I

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 8 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF RECEIVABLES PROBLEM NO. 1 In the audit of Beatles Company, the auditor had an appreciation of the following schedule and noted

Page 1 of 8 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF RECEIVABLES PROBLEM NO. 1 In the audit of Beatles Company, the auditor had an appreciation of the following schedule and noted

TOWN OF WEST BROOKFIELD, MASSACHUSETTS MANAGEMENT LETTER FOR THE YEAR ENDED JUNE 30, 2007

TOWN OF WEST BROOKFIELD, MASSACHUSETTS MANAGEMENT LETTER FOR THE YEAR ENDED JUNE 30, 2007 To the Board of Selectmen Town of West Brookfield West Brookfield, Massachusetts Dear Members of the Board: In

TOWN OF WEST BROOKFIELD, MASSACHUSETTS MANAGEMENT LETTER FOR THE YEAR ENDED JUNE 30, 2007 To the Board of Selectmen Town of West Brookfield West Brookfield, Massachusetts Dear Members of the Board: In

2013 NOT-FOR-PROFIT ENTITIES OVERVIEW FOR KNOWLEDGE COACH USERS

2013 OT-FOR-PROFIT ETITIES OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose communicating, to users the toolset, updates and enhancements included in the current version.

2013 OT-FOR-PROFIT ETITIES OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose communicating, to users the toolset, updates and enhancements included in the current version.

Chapter 9 Auditor s Response to Assessed Risk (ISA 330, ISA 500)

") Slide 9.1 Principles of Auditing: An Introduction to International Standards on Auditing Chapter 9 Auditor s Response to Assessed Risk (ISA 330, ISA 500) Rick Hayes, Hans Gortemaker and Philip Wallage

Slide 9.1 Principles of Auditing: An Introduction to International Standards on Auditing Chapter 9 Auditor s Response to Assessed Risk (ISA 330, ISA 500) Rick Hayes, Hans Gortemaker and Philip Wallage

Asset Misappropriation. Peter N. Munachewa, CICA, CFIP, CFE

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

Asset Misappropriation Peter N. Munachewa, CICA, CFIP, CFE CORPORATE FRAUD AND ABUSE CLASSIFICATION SYSTEM Corruption Asset Misappropriation Fraudulent Statements Conflicts of Interest Purchasing Schemes

APPENDIX D Examples of Significant Deficiencies and Material Weaknesses

Page A 136 Standard APPENDIX D Examples of Significant Deficiencies and Material Weaknesses D1. Paragraph 8 of this standard defines a control deficiency. Paragraphs 9 and 10 go on to define a significant

Page A 136 Standard APPENDIX D Examples of Significant Deficiencies and Material Weaknesses D1. Paragraph 8 of this standard defines a control deficiency. Paragraphs 9 and 10 go on to define a significant

Financial Statement Fraud

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

DRAFT 11/07/2018. Cowboy Joe Club. Independent Accountant s Report on the Application of Agreed-upon Procedures. Year Ended June 30, 2018

Independent Accountant s Report on the Application of Agreed-upon Procedures June 30, 2018 Contents Independent Accountant s Report on the Application of Agreed-upon Procedures... 1 Additional Information...

Independent Accountant s Report on the Application of Agreed-upon Procedures June 30, 2018 Contents Independent Accountant s Report on the Application of Agreed-upon Procedures... 1 Additional Information...

VILLAGE OF ROME ADAMS COUNTY TABLE OF CONTENTS. Independent Auditor s Report... 1

VILLAGE OF ROME ADAMS COUNTY TABLE OF CONTENTS TITLE PAGE Independent Auditor s Report... 1 Combined Statement of Receipts, Disbursements, and Changes in Fund Balances (Cash Basis) - All Governmental Fund

VILLAGE OF ROME ADAMS COUNTY TABLE OF CONTENTS TITLE PAGE Independent Auditor s Report... 1 Combined Statement of Receipts, Disbursements, and Changes in Fund Balances (Cash Basis) - All Governmental Fund

BASIC POLICY STATEMENT

SAMPLE A Well Known FINANCIAL Philosophy POLICIES For & High PROCEDURES Standards HANDBOOK BASIC POLICY STATEMENT The BEST NONPROFIT, INCORPORATED (BIN) is committed to responsible financial management.

SAMPLE A Well Known FINANCIAL Philosophy POLICIES For & High PROCEDURES Standards HANDBOOK BASIC POLICY STATEMENT The BEST NONPROFIT, INCORPORATED (BIN) is committed to responsible financial management.

26 PTA Audit. Overview. The Purpose of an Audit. Compiled Financial Statements

PTA Audit Overview Auditing involves examining financial records and transactions to ensure that receipts have been properly accounted for and expenditures have been properly authorized and recorded in

PTA Audit Overview Auditing involves examining financial records and transactions to ensure that receipts have been properly accounted for and expenditures have been properly authorized and recorded in

CORRECTIVE ACTION METHOD OF IMPLEMENTATION. Request Risk Management to increase Treasurer s surety bond to the amount required under NJ 6A:23-2.

I. Administrative Practices and Procedures 1. Surety bond coverage for the Treasurer of School Monies be increased to ensure compliance with the minimum requirement set forth in NJAC 6A:23-2.5 Increase

I. Administrative Practices and Procedures 1. Surety bond coverage for the Treasurer of School Monies be increased to ensure compliance with the minimum requirement set forth in NJAC 6A:23-2.5 Increase

Audit and Assurance. Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

SUGGESTED SOLUTIONS 06204 - Audit and Assurance Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA All Rights Reserved (1) Answer No.

SUGGESTED SOLUTIONS 06204 - Audit and Assurance Certificate in Accounting and Business II Examination September 2012 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA All Rights Reserved (1) Answer No.

Advances (Including Petty Cash and Accounts Receivable)

") CORNELL UNIVERSITY POLICY LIBRARY Advances (Including Petty Cash and Accounts Receivable) Chapter: 21, Advances Revised: POLICY STATEMENT Cornell University provides advances of cash or other resources

CORNELL UNIVERSITY POLICY LIBRARY Advances (Including Petty Cash and Accounts Receivable) Chapter: 21, Advances Revised: POLICY STATEMENT Cornell University provides advances of cash or other resources

Report on Inspection of Ernst & Young LLP (Headquartered in New York, New York) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 666 K Street NW Washington, DC 20006 Office: (202) 207-900 Fax: (202) 862-8430 www.pcaobus.org Report on 206 (Headquartered in New York, New York) Issued by the Public Company Accounting Oversight Board

666 K Street NW Washington, DC 20006 Office: (202) 207-900 Fax: (202) 862-8430 www.pcaobus.org Report on 206 (Headquartered in New York, New York) Issued by the Public Company Accounting Oversight Board

SHARED SERVICES Office of Financial Services

SHARED SERVICES Services Procedure Title: Procedure Number: Petty Cash DHS OHA-040-017-01 Version: 1.0 Effective Date: 03/28/2014 Jim Scherzinger, DHS Chief Operating Officer Suzanne Hoffman, OHA Chief

SHARED SERVICES Services Procedure Title: Procedure Number: Petty Cash DHS OHA-040-017-01 Version: 1.0 Effective Date: 03/28/2014 Jim Scherzinger, DHS Chief Operating Officer Suzanne Hoffman, OHA Chief

CITY OF BLOOMINGTON, ILLINOIS MANAGEMENT LETTER. April 30, 2010

CITY OF BLOOMINGTON, ILLINOIS MANAGEMENT LETTER April 30, 2010 October 6, 2010 Honorable Mayor and Members of the City Council 109 East Olive St. Bloomington, Illinois 61702 In planning and performing

CITY OF BLOOMINGTON, ILLINOIS MANAGEMENT LETTER April 30, 2010 October 6, 2010 Honorable Mayor and Members of the City Council 109 East Olive St. Bloomington, Illinois 61702 In planning and performing

October 10, Report of Independent Registered Public Accounting Firm. To the Board of Directors of XYZ Custodian, Inc. fn 1.

October 10, 2017 This publication, which consists of an illustrative report, assertion, and description of controls and control objectives, has been prepared by the AICPA Investment Companies Expert Panel

October 10, 2017 This publication, which consists of an illustrative report, assertion, and description of controls and control objectives, has been prepared by the AICPA Investment Companies Expert Panel

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November Uphold public interest

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Types of Fraud, Detection and Mitigation Presentation by: Isaac Mutembei Murugu CIA, CISA 23 rd November 2017 Uphold public interest Contents Types of fraud, their modes of detection and mitigation Contract

Friends of the Library Financial Policies

Note: This may seem to be overkill for such a small organization. The Executive Committee is proposing these policies to ensure that the 501(c)3 status which the IRS has given to the Friends will not be

Note: This may seem to be overkill for such a small organization. The Executive Committee is proposing these policies to ensure that the 501(c)3 status which the IRS has given to the Friends will not be

State of New Mexico Cottonwood Rural Water Association. Office of the State Auditor Tier 6 Agreed Upon Procedures for the Year Ended December 31, 2014

L State of New Mexico Office of the State Auditor Tier 6 Agreed Upon Procedures for the Year Ended December 31, 2014 Alamogordo Albuquerque Carlsbad Clovis Hobbs Roswell Lubbock, TX El Paso, TX This page

L State of New Mexico Office of the State Auditor Tier 6 Agreed Upon Procedures for the Year Ended December 31, 2014 Alamogordo Albuquerque Carlsbad Clovis Hobbs Roswell Lubbock, TX El Paso, TX This page

Applied Skills, AA. Section B

Answers Applied Skills, AA Audit and Assurance (AA) September/December 2018 Sample Answers Section B 16 (a) Analytical procedures Analytical procedures can be used at all stages of an audit, however, ISA

Answers Applied Skills, AA Audit and Assurance (AA) September/December 2018 Sample Answers Section B 16 (a) Analytical procedures Analytical procedures can be used at all stages of an audit, however, ISA

REVIEW OF AMG s QUARTERLY FINANCAL STATEMENTS: A SHORT CASE ABOUT AUDITOR RESPONSIBILITIES AND REQUIREMENTS

REVIEW OF AMG s QUARTERLY FINANCAL STATEMENTS: A SHORT CASE ABOUT AUDITOR RESPONSIBILITIES AND REQUIREMENTS Kathleen A Simione, Quinnipiac University Aamer Sheikh, Quinnipiac University INSTRUCTORS NOTES

REVIEW OF AMG s QUARTERLY FINANCAL STATEMENTS: A SHORT CASE ABOUT AUDITOR RESPONSIBILITIES AND REQUIREMENTS Kathleen A Simione, Quinnipiac University Aamer Sheikh, Quinnipiac University INSTRUCTORS NOTES

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

ANNUAL REPORT ON THE INTERIM INSPECTION PROGRAM RELATED TO AUDITS OF BROKERS AND DEALERS (PCAOB Release No August 20, 2018)

") ANNUAL REPORT ON THE INTERIM INSPECTION PROGRAM RELATED TO AUDITS OF BROKERS AND DEALERS (PCAOB Release No. 2018-003 August 20, 2018) Table of Contents Background 1 Inspections of Firms During 2017 1 Independence

ANNUAL REPORT ON THE INTERIM INSPECTION PROGRAM RELATED TO AUDITS OF BROKERS AND DEALERS (PCAOB Release No. 2018-003 August 20, 2018) Table of Contents Background 1 Inspections of Firms During 2017 1 Independence

Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions

Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Chapter 14 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley 5-5 Learning Objective

Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Chapter 14 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley 5-5 Learning Objective

STANDARD FOR AUDITS OF SMALL ENTITIES

STANDARD FOR AUDITS OF SMALL ENTITIES DRAFT JUNE 4 TH 2015 Contents Preface... 1 1 General Principles and Responsibilities... 2 1.1 Overall Objectives...2 1.2 Supervision and quality control...2 1.3 Performing

STANDARD FOR AUDITS OF SMALL ENTITIES DRAFT JUNE 4 TH 2015 Contents Preface... 1 1 General Principles and Responsibilities... 2 1.1 Overall Objectives...2 1.2 Supervision and quality control...2 1.3 Performing

Tax Action Memo TAM-1358

Tax Action Memo TAM-1358 Establish Reasonable Record Retention Policies Date: June 23, 2009 Background Businesses maintain tax records primarily to document amounts reported on their tax returns in the

Tax Action Memo TAM-1358 Establish Reasonable Record Retention Policies Date: June 23, 2009 Background Businesses maintain tax records primarily to document amounts reported on their tax returns in the

AMIT BACHHAWAT TRAINING FORUM VOUCHING EXTRA QUESTIONS

AMIT BACHHAWAT TRAINING FORUM VOUCHING EXTRA QUESTIONS Q. A trader is worried that in spite of substantial increase in sales compared to earlier year, there is considerable fall in Gross Profit after satisfying

AMIT BACHHAWAT TRAINING FORUM VOUCHING EXTRA QUESTIONS Q. A trader is worried that in spite of substantial increase in sales compared to earlier year, there is considerable fall in Gross Profit after satisfying

The Trust Account s 2017 financial statements are reliable.

Northern Municipal Trust Account 1.0 MAIN POINTS Other than the following, the Ministry of Government Relations had effective rules and procedures to safeguard the Northern Municipal Trust Account s public

Northern Municipal Trust Account 1.0 MAIN POINTS Other than the following, the Ministry of Government Relations had effective rules and procedures to safeguard the Northern Municipal Trust Account s public

SANCTIONED GROUPS: POLICY REQUIREMENT

Updated April 19, 2018 P.O. Box 1009 753 Fort Sill Boulevard Lawton Oklahoma 73502-1009 Phone: (580) 357-6900 SANCTIONED GROUPS: Parent groups such as booster clubs and PTAs must be sanctioned EACH YEAR.

Updated April 19, 2018 P.O. Box 1009 753 Fort Sill Boulevard Lawton Oklahoma 73502-1009 Phone: (580) 357-6900 SANCTIONED GROUPS: Parent groups such as booster clubs and PTAs must be sanctioned EACH YEAR.

Report on Inspection of RSM US LLP (Headquartered in Chicago, Illinois) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Chicago, Illinois) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Chicago, Illinois) Issued by the Public Company Accounting

CREIA ACCOUNTING POLICIES AND PROCEDURES

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR AUTHORITY AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A AS

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR AUTHORITY AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A AS

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

Cash Management Policy Knox County Housing Authority 216 W. Simmons St. Galesburg, IL (309)

") Article I. Purpose / Scope of the Policy Cash Management Policy 216 W. Simmons St. Galesburg, IL 61401 (309) 342-8129 Section 1.01 The follows the best practices when it comes to cash management. These

Article I. Purpose / Scope of the Policy Cash Management Policy 216 W. Simmons St. Galesburg, IL 61401 (309) 342-8129 Section 1.01 The follows the best practices when it comes to cash management. These

SOLUTIONS. Learning Goal 25

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

File No: PERMANENT AUDIT FILE INDEX Annual update confirmation. Business details 1. Background to client

Client: Year/Period End: PERMANENT AUDIT FILE INDEX Annual update confirmation Business details 1. Background to client 2. Financial History 3. Register of laws and regulations 4. Related parties 5. Group

Client: Year/Period End: PERMANENT AUDIT FILE INDEX Annual update confirmation Business details 1. Background to client 2. Financial History 3. Register of laws and regulations 4. Related parties 5. Group

COWBOY JOE CLUB FINANCIAL REPORT JUNE 30, 2017

COWBOY JOE CLUB Report on the Application of Agreed-Upon Procedures to the Records of the University of Wyoming Cowboy Joe Club and to its System of Internal Accounting Control FINANCIAL REPORT JUNE 30,

COWBOY JOE CLUB Report on the Application of Agreed-Upon Procedures to the Records of the University of Wyoming Cowboy Joe Club and to its System of Internal Accounting Control FINANCIAL REPORT JUNE 30,

UNIVERSITY OF SOUTH FLORIDA Cash Collections Action Plan February 10, 2006

VIII UNIVERSITY OF SOUTH FLORIDA Cash Collections Action Plan February 10, 2006 1. Eliminate Cash Collection Sites (see Attachment A) [FC] 2. Consolidate Cash Collection Sites (see Attachment A) a minimum

VIII UNIVERSITY OF SOUTH FLORIDA Cash Collections Action Plan February 10, 2006 1. Eliminate Cash Collection Sites (see Attachment A) [FC] 2. Consolidate Cash Collection Sites (see Attachment A) a minimum

Episcopal Diocese of Western Massachusetts MODEL AUDIT PROGRAM - AUDIT YEAR 2017

Episcopal Diocese of Western Massachusetts MODEL AUDIT PROGRAM - AUDIT YEAR 2017 GUIDELINES FOR AUDITORS: The following worksheets are provided for use by your audit committee. This model program can be

Episcopal Diocese of Western Massachusetts MODEL AUDIT PROGRAM - AUDIT YEAR 2017 GUIDELINES FOR AUDITORS: The following worksheets are provided for use by your audit committee. This model program can be

AUSTIN INDEPENDENT SCHOOL DISTRICT

PURCHASING CARD GENERAL: The purchasing card ("p-card") program was implemented several years ago to establish a more efficient, cost-effective method of purchasing and paying for small dollar transactions

PURCHASING CARD GENERAL: The purchasing card ("p-card") program was implemented several years ago to establish a more efficient, cost-effective method of purchasing and paying for small dollar transactions

DuPage County, Illinois

DuPage County, Illinois Report on Internal Controls November 30, 2014 DUPAGE COUNTY, ILLINOIS TABLE OF CONTENTS Auditor s Letter 1-2 County Board Comments Material Weakness Finance Department Accounting

DuPage County, Illinois Report on Internal Controls November 30, 2014 DUPAGE COUNTY, ILLINOIS TABLE OF CONTENTS Auditor s Letter 1-2 County Board Comments Material Weakness Finance Department Accounting

Risk Assessment Proces Case study Slovenian Construction Company

Assessment Proces Case study Slovenian Construction Company Sabina Softic, Audit Director Deloitte Bosnia and Herzegovina Vienna, 6 February 2013 Assessment Procedures ISA 315: auditor should obtain an

Assessment Proces Case study Slovenian Construction Company Sabina Softic, Audit Director Deloitte Bosnia and Herzegovina Vienna, 6 February 2013 Assessment Procedures ISA 315: auditor should obtain an

SAMPLE AUDIT REPORT. Sample Credit Union. Report on Operations. As of Audit Date

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

ACCA F8. Provided by Academy of Professional Accounting (APA) Liability, Capital and Directors Emoluments ACCA Lecturer: Tom Liu

Liability, Capital and Directors Emoluments ACCA Lecturer: Tom Liu") Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F8 Liability, Capital and Directors Emoluments ACCA Lecturer: Tom Liu ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright

Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F8 Liability, Capital and Directors Emoluments ACCA Lecturer: Tom Liu ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

Internal Audit Policy

Internal Audit Policy This policy was adopted by the Board of Directors of Armagh Credit Union Limited. Signed:- Position Position Date: Internal Audit Plan 1. Introduction The internal audit function

Internal Audit Policy This policy was adopted by the Board of Directors of Armagh Credit Union Limited. Signed:- Position Position Date: Internal Audit Plan 1. Introduction The internal audit function

CENTRAL VIRGINIA COMMUNITY SERVICES BOARD COMMENTS ON INTERNAL CONTROL AND OTHER SUGGESTIONS FOR YOUR CONSIDERATION. June 30, 2011

CENTRAL VIRGINIA COMMUNITY SERVICES BOARD COMMENTS ON INTERNAL CONTROL AND OTHER SUGGESTIONS FOR YOUR CONSIDERATION CONTENTS INDEPENDENT AUDITOR S REPORT ON COMMENTS AND SUGGESTIONS...3 COMMENTS AND SUGGESTIONS

CENTRAL VIRGINIA COMMUNITY SERVICES BOARD COMMENTS ON INTERNAL CONTROL AND OTHER SUGGESTIONS FOR YOUR CONSIDERATION CONTENTS INDEPENDENT AUDITOR S REPORT ON COMMENTS AND SUGGESTIONS...3 COMMENTS AND SUGGESTIONS